UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08228

The Timothy Plan

(Exact name of registrant as specified in charter)

1055 Maitland Center Commons, Maitland, FL 32751

(Address of principal executive offices) (Zip code)

Art Ally, The Timothy Plan

1055 Maitland Center Commons, Maitland, FL 32751

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-846-7526

Date of fiscal year end: 9/30

Date of reporting period: 9/30/18

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Registrant’s audited annual financial reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 are as follows:

September 30, 2018

Dear Shareholder,

As you review the details on the following pages, you will see that most of our funds experienced excellent performance over the past fiscal year (10-1-17 thru 9-30-18). Our fixed-income oriented funds were slightly down for the past 12 months due to weakness in the bond markets. Our only fund that was down fairly significantly was Emerging Markets (down nearly 10%) but that was due to the cyclical nature of that market. All of that simply underscores the wisdom of asset allocation since different market segments perform differently over differing periods.

The positive returns we experienced are, we believe, in large part the result of our country’s leadership changes in Washington, DC, and the positive pro-business agenda they are pursuing. These changes gave us a positive long-term view of our economy and, therefore the equity markets. Even though we experienced periodic short-term volatility, we fully expect the market trend to continue. Nevertheless, Timothy Partners, Ltd, (the “Advisor”) continued (and will continue) to take a conservative approach to the markets as we believe our shareholders prefer a preservation of principal course to that of chasing returns. I do need to reiterate, however, that, in the capital markets in general and our funds in particular, returns can never be guaranteed.

For more complete information about the individual Funds, please read each of the sub-advisors’ annual review letters in the pages that follow. They more fully detail the various factors that impacted this fiscal year’s performance along with their economic outlook for the coming year.

Although we cannot guarantee any actual outcome, I remain confident that all our sub-advisors are, in our opinion, among the best in the industry and they each continue to honor our overall policy to manage their respective funds both in accordance with our screening restrictions and with a continued conservative bias.

Finally, I would once again like to thank you for your moral convictions that led you to becoming part of the Timothy Plan Family.

Yours in Christ,

Arthur D. Ally

President

1

| | |

| |

Timothy Plan Aggressive Growth Fund Letter from the Manager – September 30, 2018 | |

|

| | | |

The growth rate of the U.S. economy accelerated over the past year, with the Commerce Department reporting that GDP grew 3.05 percent over the past twelve months, compared to 2.35 percent growth over the twelve-month period ending September 2017. Unemployment is now at a 50-year low at 3.83 percent, compared to 4.3 percent unemployment as of September 2017. Consumer Confidence, as measured by the University of Michigan Consumer Sentiment Survey, is nearing record high readings not seen since 1999. Not surprisingly, this high economic activity is leading to higher inflation across several indices: CPI less Food & Energy is now at 2.2 pct, compared to 1.7 pct a year ago; PPI less Food & Energy is at 2.7 pct, compared to 1.7 pct a year ago. Federal government spending, following the adoption in mid-March of a $1.3 trillion spending plan for the fiscal year ending September 30, 2018, also added to aggregate U.S. growth. The federal budget is estimated to have led to half of the increased growth over the past year. Given that we are entering the ninth year of economic expansion, paired with sharply rising inflationary pressures, investors are closely watching the Federal Reserve. The next round of tariffs scheduled to be implemented at year end will only add to inflationary pressures. That will keep the Federal Reserve in the hot seat as it tries to manage inflation expectations while at the same time allowing this economic expansion to continue as long as possible. The above-trend growth in the second and third quarters is likely unsustainable and we would expect some softening as rising prices and rising interest rates start to have an impact.

The Fund enjoyed strong returns in 2018, gaining 6.69 percent in the September 2018 quarter, 11.23 percent year to date, and 14.62 percent for Class I over the last 12 months. This compares to the Russell Midcap Growth Index that returned 7.57 percent in the past quarter, 13.38 percent year to date, and 21.1 percent over the last 12 months.

The underperformance over the past 12 months was driven by weak stock selection in the consumer discretionary and the industrial sectors. Our largest stock underperformer in the consumer discretionary sector was Lumber Liquidators [LL], which suffered from tougher competition in the flooring markets from big box retailers. They also disappointed investors by not improving their margin structure. Within the industrial sector, our investment in Oshkosh [OSK] proved to be disappointing. While Oshkosh never reported subpar earnings, its valuation contracted significantly as investors moved away from nearly all industrial stocks; investors worried that higher raw material costs driven by tariffs, and higher freight costs would negatively impact the operating margins for those companies.

The largest outperformers over the past 12 months were primarily investments in the healthcare sector, specifically biotech companies. Sarepta [SRPT] had significant gains after they reported incredibly strong clinical data in their first gene therapy program to treat Duchennes Muscular Dystrophy. Also, the company made a strong strategic move in partnering with Myonexus, another biotechnology company with a compelling gene therapy program for the treatment of Limb-Girdle muscular dystrophies. Another top performer was Ignyta [RXDX]. Ignyta agreed to be acquired at a 74% premium by Roche Holding, in a $1.7 billion transaction. Ignyta has an exciting late stage oncology program that targets ROS1 and TRK mutations across several different cancers. Initial clinical results are very promising, leading to interest from Roche in acquiring the company.

Looking forward, we continue to emphasize the healthcare and technology sectors within the portfolio, as they do not face many of the headwinds seen in other sectors of the economy. Specifically, we believe that many companies in the industrial sectors will find it difficult to fully pass on higher costs to their end customers. Also, the likelihood of higher interest rates will continue to depress several industries, specifically the homebuilding and auto industries. Conversely, there are many attractive midcap healthcare and technology companies that largely are focused on the US market, and are relatively sheltered from cost pressures seen in other sectors. We thank you for your continuing support and investment.

Chartwell Investment Partners, LLC

2

Letter from The Manager

The Timothy Plan International Fund

September 30, 2018

International equities continued to perform well as strong corporate earnings supported equities up until volatility came back to the markets in early 2018. The markets were spooked earlier this year when U.S. wage growth accelerated, and inflation pressures entered the conversation. Despite increased global concerns, The Timothy Plan International Fund rose in absolute terms slightly outperforming the MSCI EAFE index for the twelve-month period. Good stock selection in the Financials, Consumer Staples and Industrials sectors more than offset negative selection in Consumer Discretionary, Materials, and Utilities sectors. An overweight to the Technology sector helped performance but stock selection there was challenged. Country allocation was tough as any allocation to emerging market countries was negative while stock selection was positive. Selection in Norway and Spain was good while that in Japan and France and emerging markets was less favorable. Strong returns from individual stocks included Equinor ASA (Norway-Energy), Amadeus IT (Spain-Technology), and DBS Group (Financials-Singapore). The Fund was hurt from poor performance in auto parts including Valeo (France-Consumer Discretionary) and Continental (Germany-Consumer Discretionary), and from technology exposure in China.

While this twelve-month period started on a solid footing of global economic acceleration, it ended on a wall of worries related to central bank policies, Brexit, Italian election outcomes, China growth slowdown, trade wars, and emerging market contagions. This affected stock prices over the second half of the period as volatility increased. President Trump stepped up his trade battles which rattled equity markets on concerns of effect on global growth and rising input prices. The U.S. dollar bounced back, supported by rising rates and strong growth in the U.S., all placing more pressures on emerging market currencies. The IMF came to the rescue in Argentina while contagion gripped Brazil, South Africa, Turkey and others. Oil prices rose as the U.S. backed away from the Iran nuclear pact while tariffs were placed on Chinese goods. The European Central bank is scheduled to end its bond buying program at the end of 2018 while uncertainty remains on Brexit negotiation outcomes. U.S. economic growth remains strong while European and Japanese economic growth has decelerated but remains well above trend.

Relative and absolute valuations have improved for international equities over the last twelve months. Equity price volatility is likely to remain in the near term as the market climbs a wall of worries which may provide good buying opportunities for long term investors. We remain committed to a consistent investment approach dedicated to finding long-term investments for the Fund. We thank you for your continued investment in the Fund.

Eagle Global Advisors, LLC

3

| | |

Timothy Plan Large/Mid Cap Growth Fund Letter from the Manager – September 30, 2018 | | |

The growth rate of the U.S. economy accelerated over the past year, with the Commerce Department reporting that GDP grew 3.05 percent over the past twelve months, compared to 2.35 percent growth over the twelve-month period ending September 2017. Unemployment is now at a 50-year low at 3.83 percent, compared to 4.3 percent unemployment as of September 2017. Consumer Confidence, as measured by the University of Michigan Consumer Sentiment Survey, is nearing record high readings not seen since 1999. Not surprisingly, this high economic activity is leading to higher inflation across several indices: CPI less Food & Energy is now at 2.2 pct, compared to 1.7 pct a year ago; PPI less Food & Energy is at 2.7 pct, compared to 1.7 pct a year ago. Federal government spending, following the adoption in mid-March of a $1.3 trillion spending plan for the fiscal year ending September 30, 2018, also added to aggregate U.S. growth. The federal budget is estimated to have led to half of the increased growth over the past year. Given that we are entering the ninth year of economic expansion, paired with sharply rising inflationary pressures, investors are closely watching the Federal Reserve. The next round of tariffs scheduled to be implemented at year end will only add to inflationary pressures. That will keep the Federal Reserve in the hot seat as it tries to manage inflation expectations while at the same time allowing this economic expansion to continue as long as possible. The above-trend growth in the second and third quarters is likely unsustainable and we would expect some softening as rising prices and rising interest rates start to have an impact.

The bull market in growth stocks continued unabated over the last twelve months, in fact, it was even more pronounced than last year: the Russell 1000 Growth Index was up 26.3%, vs. +22% the prior year. As we wrote in last year’s letter, while this is a good environment for the absolute return of the fund, it provides a significant headwind for our returns relative to the benchmark – due to the restrictions on what we can own (the Fund was up 11.69% for Class I). Not being able to hold the “bellwether” growth/tech stocks that have been the market leaders leaves us with a portfolio – on average – of much smaller market capitalization companies and with a lower growth profile compared to the benchmark. In the past year, that positioning was a liability, given that large growth was the place to be. One way to quantify this is that the portion of the R1G Index that is not restricted was up about 20%, or 6.3 percentage points short of the full index. Another reference point is to look at the returns for the period of some of the large R1G stocks that are restricted: Amazon was up 108%; Microsoft +56%; and Apple +48% (not owning just those 3 stocks in their index weights was a “cost” of 4.8 percentage points). Finally, the Tech sector as a whole – which we were underweight by 8 percentage points on average - was up 41%, and it was one of only two sectors that meaningfully outperformed the benchmark (Consumer Discretionary being the other).

Turning to stock selection, we had two great performers in Health Care – Neurocrine Biosciences (+101%), which had an exceptional commercial launch for its drug Ingrezza, and Sarepta Therapeutics (+71%), which presented promising gene therapy data for the treatment of Duchenne Muscular Dystrophy. Home-improvement retailer Lowe’s was also a big winner (+46%), and energy company ConocoPhillips vastly outperformed its sector’s return with a gain of 58%. Negative selection was most pronounced in the Tech sector, where some of the stocks that we owned as substitutes for the restricted stocks fared poorly: Western Digital fell 31%; Mercury Systems dropped 28%; and IPG Photonics was down 16%. A partial offset, however, came from semiconductor company, NVIDIA, a multi-year strong performer for us, which came through again with a 58% gain. Its solid results in data-center and growing potential in leading-edge technologies like artificial intelligence have continued to propel the stock. In Health Care, biotech company Celgene lowered near-term growth expectations, and the market punished it with a 39% drop. In Financials, asset-manager Invesco was a drag on our performance, falling 25%, and in the Materials sector, chemical-company Albemarle (one of last year’s big winners) sold off by 26%.

For the portfolio, there has been no change to our time-tested, bottom up fundamental approach to managing large and mid-cap growth investments. As an overview, the portfolio remains well diversified by issuers and

4

sectors, as all areas of the economy are impacted by broad macroeconomic trends. We continue to find attractive investments at reasonable valuations. However, with the recent above-trend earnings resulting from tax reform, comparisons for earnings growth will become more difficult in 2019. This, along with input-cost pressures and tariff-related challenges will create a more uneven playing field. We will be vigilant in orienting the portfolio toward industries and companies that are best-positioned for this environment. Healthcare is a sector that we currently favor, and Industrials and Materials are “under review” as we move through the current earnings season. We thank you for your continuing support and investment.

Chartwell Investment Partners, LLC

5

LETTER FROM THE MANAGER

September 30, 2018

TIMOTHY PLAN SMALL CAP VALUE FUND

We are pleased to provide you with our report for the Timothy Plan Small Cap Value Fund for the twelve months ending September 30, 2018 and would like to thank you for entrusting your assets with us.

Looking back, equity markets have marched higher with only a small blip from a short-lived spike in volatility. While headline noise remains deafening, the normalization of post-crisis monetary policy and the pick up in economic growth remain key drivers for markets going forward. The Federal Reserve again hiked rates, with the fed funds rate now sitting at 2.00-2.25 percent, and the reductions of the balance sheet continuing as expected. Supporting their actions, the most recent GDP figure showed an acceleration to 4.2 percent growth in the second quarter of 2018. This tailwind has driven strong topline growth and, in conjunction with the reduction in tax rates, produced very strong earnings growth to underpin the move higher by the equity markets. Stronger cash balances have been a driver for incremental spending on capital expenditures as well as returning additional cash to shareholders. Margins for many companies have held up well despite input cost pressures, whether labor or raw material, as pricing power has returned after being absent for a number of years. In contrast to the strength in the U.S., the rest of the world has been more mixed with varying impacts from the stronger dollar and trade policies. There remains a high degree of concern regarding the potential for further disruptions and impacts in the future.

For the twelve months ending September 30, 2018, the Timothy Plan Small Cap Value Fund produced a net return of

10.37% for Class I, while the Russell 2000 Index produced a return of 15.24%. Positive stock selection was offset by unfavorable allocation, as the more growth-oriented areas of the market produced strong absolute returns. Strong selection was seen in Industrials and Materials while less favorable selection in Consumer Discretionary and an overweight in Financials were headwinds to relative performance.

Sonic Corp. moved up after agreeing to be acquired at a significant premium by Inspire Brands. Our domestically-focused cyclicals, including Novanta, rallied strongly on better economic data points that translated into sales and earnings growth, even as the rest of world was more mixed in terms of underlying growth trends. Comfort Systems, an installer of heating and air conditioning systems saw a strong rise in their backlog on continued strength in the commercial construction market. Additionally, KapStone Paper and Packaging, a containerboard company, was taken out at a significant premium by a competitor as the industry consolidation theme marched forward. Oxford Industries rallied as their lifestyle brands of Tommy Bahama and Lilly Pulitzer continue to resonate well with the consumer and their sales exceeded expectations.

Concerns over the housing cycle and rising input pressures weighed heavily on Installed Building Products. Wet weather caused volumes and pricing realizations to fall short of expectations for Summit Materials. The recent rise in rates has captured the headlines and coincided with a seasonally slower time of the year which has raised concerns regarding both the residential and non-residential cycles. Lithia Motors saw topline trends remain strong, underpinned by low unemployment and rising wages, but faced cost pressures from the rising wages and incremental marketing expenses that weighed on shares. Consumers looking for higher interest rates on their deposits compressed net interest margins, which caused a decline in the shares of Hanmi Financial. OSI Systems moved lower on investor concerns regarding the profitability of their turn key business in two areas, Albania and Mexico.

The Small Cap Value team is focused on seeking well-run companies with growth prospects that are underappreciated by the marketplace. We look for companies with above average growth and strong balance sheets that generate positive cash flows. As economic growth continues, we feel our companies are well positioned to achieve higher earnings and have the potential to provide superior relative returns.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corporation

6

LETTER FROM THE MANAGER

September 30, 2018

TIMOTHY PLAN LARGE/MID CAP VALUE FUND

We are pleased to provide you with our report for the Timothy Plan Large/Mid Cap Value Fund for the twelve months ending September 30, 2018 and would like to thank you for entrusting your assets with us.

Looking back, equity markets have marched higher with only a small blip from a short-lived spike in volatility. While headline noise remains deafening, the normalization of post-crisis monetary policy and the pick up in economic growth remain key drivers for markets going forward. The Federal Reserve again hiked rates, with the fed funds rate now sitting at 2.00-2.25 percent, and the reductions of the balance sheet continuing as expected. Supporting their actions, the most recent GDP figure showed an acceleration to 4.2 percent growth in the second quarter of 2018. This tailwind has driven strong topline growth and, in conjunction with the reduction in tax rates, produced very strong earnings growth to underpin the move higher by the equity markets. Stronger cash balances have been a driver for incremental spending on capital expenditures as well as returning additional cash to shareholders. Margins for many companies have held up well despite input cost pressures, whether labor or raw material, as pricing power has returned after being absent for a number of years. In contrast to the strength in the U.S., the rest of the world has been more mixed with varying impacts from the stronger dollar and trade policies. There remains a high degree of concern regarding the potential for further disruptions and impacts in the future.

For the twelve months ending September 30, 2018, the Timothy Plan Large/Mid Cap Value Fund produced a net return of 13.83% for Class I, while the S&P 500 Index produced a return of 17.91%. While absolute returns remained strong, the relative performance faced headwinds. Notable positives included better stock selection within Consumer Staples and Industrials while our underweight to more growth-oriented parts of the market, namely Information Technology, Consumer Discretionary, and Health Care, weighed on relative performance.

Several areas saw strong stock selection, particularly in Consumer Staples which benefitted from the acquisition of a carbonated beverage company at a significant premium. This created a powerhouse in the beverage category combing single-serve coffee with a variety of carbonated and non-carbonated drinks. Strong economic growth boosted several industrials with broad exposures, notably Union Pacific where better pricing and solid volumes contributed to strong earnings growth. Management at Union Pacific also announced a recent long-term plan to further expand margins as they focus on precision railroading. FLIR Systems benefitted as well from incremental defense spending and a refocused management team under the helm of a new CEO on expanding their gross margins. SVB Financial saw both strong asset growth and better sensitivity to rising rates which pushed earnings up materially higher than expected and shares followed. Their exposure to technology lending has allowed them to avoid some of the headwinds such as commercial real estate that have weighed on other banks. PerkinElmer gained as they continued to see management’s strategy to shift towards higher growth markets pay off as topline growth accelerated to double-digits in both their segments. Continued strength in the housing market and housing turnover pushed shares of Sherwin-Williams higher as they delivered on their synergies from their recent acquisition of Valspar.

The Fund’s under-exposure to high growth areas of the market were a notable headwind, though offset somewhat by more favorable stock selection elsewhere. DENTSPLY closed on their acquisition of Sirona, however, dental consumable volume trends have been disappointing and weighed on shares and recent softness in equipment has been met with lowering of prices to stimulate demand. Patterson Companies shared many of the same headwinds as DENTSPLY, including the loss of their exclusive arrangement with Sirona. Eagle Materials suffered from higher than usual rainfall, limiting cement volumes, and leading to less pricing realizations than anticipated. The consolidation thesis for the industry remains intact and should lead to better pricing in the future. Mohawk Industries faced a number of expense headwinds in their flooring businesses and management had a rare earnings miss as a result. Price increases are being enacted to restore margins, though their impact will come over time as they flow through their various products. Lam

7

Research declined as a lull in spending in the semiconductor industry pressured their sales and earnings. While management expects a rebound, the market remains uncertain despite secular growth trends in several end-markets for chips.

The Westwood team remains focused on seeking high-quality companies trading at a discount to intrinsic value. While market returns have most recently been bolstered by unprecedented monetary stimulus rather than fundamentals, the continued rise in interest rates has begun shifting the focus back to company-specific drivers. These normalizations are occurring across a number of areas including monetary policy, where the Federal Reserve continues to hike rates and reduce their balance sheet. Fiscal policies, particularly the tax cuts, serve as a replacement to the stimulus and should continue to have a positive impact despite the potential trade headwinds into the following year. These benefits, as well as other fiscal changes, will benefit companies in disproportionate ways and is expected to further create dispersion in returns. In total, the overall impact to the investing landscape should provide additional opportunities to active managers as dispersion of returns increases and correlations between stocks decrease. We continue to leverage our intensive research-driven process to identify securities with company-specific opportunities and visible earnings growth. As has always been our practice, we look to invest in companies with conservative balance sheets, robust free cash flow generation, and high returns as we believe those characteristics among others help provide attractive risk-adjusted returns for the portfolio. Given the above-average market returns over the past few years, we are mindful of the potential for downside risk and are focusing on opportunities which we feel have measurable and limited potential for loss should volatility rise.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corporation

8

Letter from the Manager

September 30, 2018

Timothy Plan Fixed Income Fund

The fiscal year ended September 30, 2018 saw an increase in interest rates as the Federal Reserve (Fed) maintained its rate normalization policy and economic growth continued to surprise to the upside. The Timothy Plan Fixed Income Fund invests in the broad U.S. investment grade bond market benchmarked to the Bloomberg Barclays Aggregate index which began the last 12 months with a 2.55% yield and ended at 3.46%.

The U.S. Treasury (UST) 10-year rate rose after starting the fiscal period at 2.33%, peaking at 3.11% in May, and ending at 3.06%. By comparison, the 2-year rate rose even higher starting at 1.48% and ending the last 12 months at 2.82% or 1.34% higher. This rise resulted in the UST yield curve flattening to levels not seen since September of 2007. Low volatility in UST rates was also a bellwether event in late 2017 and early 2018. The markets shrugged off global geopolitical events, natural disasters, and the North Korean nuclear threat to register the lowest volatility in 25 years. The U.S. economy continued to evidence low unemployment and solid job creation and in May 2018 the Fed’s 2.0% Core Personal Consumption Expenditure target was attained for the first time since April 2012. Consequently, the Fed continues to telegraph and maintain its hawkish quantitative tightening actions.

Corporate bond spreads started the last 12 months at 96 basis points (bps), widened to a high of 116 and finished at 100bps. The widening was a result of supply/demand dynamics that included new issue supply to fund accelerated M&A activity, diminished foreign buying, and repatriation of foreign cash holdings of U.S. corporations. The Mortgage Backed Securities (MBS) sector struggled during the period as the Fed announced its balance sheet reduction plan. For the first time in nearly a decade, the Fed will no longer be the primary buyer of MBS.

The Timothy Fixed Income Fund A shares returned -2.31% (Class A shares) over the 12 months ended September 30, 2018 which was below the Bloomberg Barclays Aggregate index at -1.22%. The overweight to Industrials added value as the sector performed better than the overall index. Security selection in Energy, Capital Goods and Technology also added to results. Detracting from results was our underweight to Financials, as the sector posted the second-best return for the period. The portfolio’s MBS holdings generated returns below their counterparts in the index which also hurt performance. The portfolio is positioned with modestly less interest rate risk than the market, an over-weight in corporate bonds and GNMA MBS for yield. We remain focused on generating income consistent with a prudent level of risk.

BARROW, HANLEY, MEWHINNEY & STRAUSS

9

Letter from the Manager

September 30, 2018

Timothy Plan High Yield Fund

The fiscal year ended September 30, 2018 saw an increase in High Yield rates as investor demand for yield remained modestly healthy. The Timothy Plan High Yield Fund invests primarily in BB and B rated High Yield (HY) bonds with a benchmark of the Bloomberg Barclays BA/B HY index which began the last 12 months yielding 4.68% and ended at 5.78%. Over the period, the HY market posted a return of 2.18% and generated an excess return of 3.29%, the highest of any major bond market sector. Performance was led by lower rated credits and continued recovery in the Energy and Basic Industry (including Metals & Mining) sectors.

The primary influence on performance has been favorable technicals, particularly a lack of supply, and improvement of credit fundamentals. During the first nine-months of 2018, net new issuance totaled $11.5B which was significantly lower than the $55.4B issued in 2017. Favorable economic growth and improving earnings will support HY companies and help to contain defaults. On a trailing 1-year basis, the HY default rate was 2.57% (latest available data as of 8/31/18).

The Timothy High Yield Fund A shares generated a total return of -0.17% (Class A shares) over the 12 months ended September 30, 2018 while the Barclays Capital U.S. Corporate High Yield Bond index returned 3.05% and the Bloomberg Barclays Ba/B index returned 0.37%. The portfolio’s overweight in Energy benefitted results. We continue to hold Energy names especially MLP issues that we believe are less correlated with the price of oil. Holdings in Technology and REITS were also additive to returns. Detracting from performance was our underweight to Financials which posted the second highest return in the index. The portfolio remains focused on generating a higher level of carry income consistent with a reasonable level of risk.

BARROW, HANLEY, MEWHINNEY & STRAUSS

10

September 30, 2018

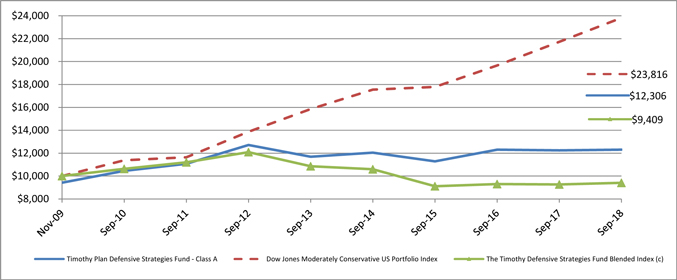

Dear Shareholder,

The Defensive Strategies Fund was designed and is managed to do what its name implies, hedge against a possible scenario of hyper-inflation which could result from our Congress’s proven unwillingness to address our core problems of too much spending and too much debt. The Fund was also designed with built-in flexibility that allows it to be adjusted to address a possible risk of extreme deflation, with the ability to convert the inflation sensitive assets to cash and fixed income securities during a deflationary environment, and to be adjusted to a more normal, traditional investment strategy.

The Fund’s portfolio is comprised of four inflation sensitive investment sleeves: commodities (commodity company stocks and ETF’s), real estate (in the form of REITs), precious metals (primarily gold and silver bullion), and TIPs (Treasury Inflation Protected Bonds), with the balance in cash. Timothy Partners, Ltd. (the “Advisor”) is responsible for setting the percentages of the Fund that will be allocated to each investment sleeve. Different sub-advisors manage the holdings in each sleeve. As a result of continued low inflation and the general weakness in the commodities market over the past year, the Fund experienced a fairly weak 0.75% total return for Class A for the fiscal year ended September 30, 2018. For a more complete description of the elements that impacted Fund performance and the outlook for the future, please read the sub-advisors’ reports in the pages that follow.

I would like to point out that, since there does not exist an appropriate benchmark index with which to compare our performance, we have created a blended index comprised of roughly 1/3 each of U.S. Government TIPs, FTSE NAREIT Equity Index and Dow Jones UBS Commodity Index. We believe the blend offers a fairly accurate reflection and comparison of the composition of the Fund. For the fiscal year ended September 30, 2018, the blended index had a total return of 1.34%. The primary reason the index slightly beat our fund’s performance has a lot to do with the weakness of the gold and silver markets over the past year (initially 10% of the portfolio but with fairly significant appreciation now comprise 17.5% of the portfolio).

While no one can predict future events, I remain confident that our sub-advisors (i.e. money management firms that manage the various sleeves of this Fund) are, in our opinion, among the best in the industry, and they each continue to honor our overall policy that they manage their respective Fund sleeve both in accordance with our screening restrictions and with a conservative bias. As I stated in last year’s report, although we will do our very best to be successful, we cannot guarantee results in any of these scenarios.

Finally, I would once again like to thank you for your moral convictions that led you to become part of the Timothy Plan Family.

Yours in Christ,

Arthur D. Ally

Fund Advisor

11

| | |

| |  |

| |

Annual Letter from the Manager | | September 30, 2018 |

We are pleased to provide you with our annual report for the Timothy Plan Defensive Strategies Fund Commodity Sleeve (the Portfolio) for the twelve months ending September 30, 2018. The CoreCommodity sleeve of the Timothy Defensive Fund rose 7.35% on a net basis. Commodities broadly rose over these twelve months with the Bloomberg Commodity Total Return Index rising 2.6%. The Portfolio had positive contributions to performance from all sectors (energy, industrial metals, and agriculture) except for precious metals over the period.

Metals & Mining

Industrial metal commodity futures were modestly down for the period with the Bloomberg Industrial Metals Total Return Subindex falling (2.4%). The best performing base metal was Nickel, rising more than 20% over the period. Zinc fell nearly (17%) and was the worst performing base metal over the period, giving back most of its strong performance in the year prior. The Portfolio’s industrial metal holdings performed substantially better than the commodity futures, returning over 11% for the period. While most industries in the base metals sleeve of the portfolio performed positively, steel companies (up over 13%) and iron mining companies (up roughly 25%, the primary input to the steel-making process) combined constituted over half of the base metals outperformance. It’s important to note that the portfolio benefitted from exposure to these globally important commodities for which no highly liquid futures contracts exist. The Portfolio’s largest industrial metal holdings as of September 30th were Rio Tinto (RIO US), Vale (VALE US), and Freeport-McMoran (FCX US).

Precious metal futures struggled again this year with the Bloomberg Precious Metals Total Return Subindex falling nearly (9%). The Portfolio’s precious metals miners also struggled, falling nearly (27%). Holding a smaller allocation to precious metals miners than other sectors helped curb the underperformance from this sector for the period. The Portfolio’s largest precious metal holdings as of September 30th were Newmont Mining (NEM US), Franco-Nevada Corp (FNV US), and Agnico Eagle Mines (AEM US).

Energy

Energy was the best performing sector for the prior year, with the Bloomberg Energy Total Return Subindex rising over 28%. The Portfolio’s energy holdings were also the best performing sector, returning over 16% for the period. The Portfolio’s higher allocation to energy (averaging 42% over the period) significantly helped performance. While the Portfolio’s Oil & Gas Exploration and Production holdings did not keep pace with the futures (only rising about 12%) the Integrated Oil & Gas companies significantly outperformed (rising over 37%) which helped offset some of the difference. The Portfolio’s largest energy holdings as of September 30th were Lukoil (LKOD LI), EOG Resources (EOG US), and Concho Resources (CXO US).

Agriculture

Over the past year agricultural commodities, as proxied by the Bloomberg Commodity Agriculture and Livestock Total Return Subindex, fell nearly (11%). Over the same period the Portfolio’s agricultural holdings rallied roughly 2.5%, providing additional outperformance. The Portfolio had strong performance from the Fertilizer industry, which was (on average) the largest agriculture industry, as well as from Fisheries and Forestry companies. The decision to hold less weight in the animal producers than in the past year helped performance, as those industries generated significant losses this year after strong returns in the prior year. The Portfolio’s largest agriculture holdings as of September 30th were CF Industries (CF US), The Mosaic Company (MOS US), and Deere & Company (DE US).

Market Outlook

12

The Timothy Plan Defensive Strategy Fund Commodity Sleeve currently utilizes a diversified portfolio of natural resource equities that is intended to capture commodity price movements. To the extent commodities rally in the coming year we would expect the Portfolio to perform positively. We believe commodities may rally if global economic growth remains healthy. If industry demand falls off then commodities may not continue to rally, in which case we would not expect the Portfolio to perform positively.

13

Letter from the Manager

September 30, 2018

Timothy Plan Defensive Fund – TIPS

Over the past 12 months ended September 30th, the U.S. experienced moderately stronger economic growth and slightly higher inflation. The Timothy Defensive Fund has an allocation of U.S. Treasury Inflation Protected Securities (TIPS) designed to help protect assets from higher rates of inflation.

Investors’ future inflation expectations reached a low in late 2017 but subsequently climbed during the 12 month period. We measure investors’ inflation expectations as the difference between the U.S. Treasury 10 year and the U.S. TIPS 10 year. This “breakeven rate” of inflation is what would be required to make these two securities have the same yield. The “breakeven rate” of inflation fell to a low of 1.83% in October 2017, climbed to a high of 2.20% by May 2018, and eventually settled at 2.14% by September 30th. As a result, TIPS securities generated a return of 0.37%, as reported by Bloomberg Barclays, for the 12 months ended September 30th.

The TIPS allocation we manage held 5 to 10% in investment grade corporate bonds for their higher nominal yield. Although inflation has ticked up it remains relatively subdued. Going forward the potential of higher inflation exists as global central banks have engaged in massive monetary stimulus and the unemployment rate remains low which could potentially trigger higher wages. The primary goal of the TIPS allocation continues to be protection from rising inflation rates.

BARROW, HANLEY, MEWHINNEY & STRAUSS

14

| | |

| | 2005 Market St. |

| | Philadelphia, PA 19103-7094 |

The Timothy Plan Defensive Strategies Fund

Real Estate Sleeve (the “Portfolio”)

Annual Manager Letter: 12 months ended September 30, 2018

The strong market returns of the S&P 500 continued over the past year providing investors with a 17.91% return. Solid earnings and a still accommodative credit backdrop drove the markets higher. However, as good as earnings have been, the P/E multiple has compressed by 3 points as the Federal Reserve’s rate increases are beginning to signal a slowdown is potentially ahead. The US continues to be the strongest market globally, but investors can already see the effects of a more hawkish Federal Reserve. Emerging markets, China, Europe, Asia and US housing have been in negative territory over much of 2018. Generally, when the Federal Reserve begins to tighten, bad things tend to occur and as we write this letter, US equities are beginning to play catch up with global markets.

REITs underperformed but were able to provide a positive 3.47% return during a rising rate environment. We have always contended that REITs can still provide positive returns even in a rising rate period if the economy is improving. Initially, investors will sell yield but if GDP is rising that is generally good for all sectors, including real estate. Obviously, growth and cyclical areas of the economy benefit more than REITs however, it proves that REITS should always be apart of any portfolio. Again, since quarter end, the growth, tech and cyclical areas of the market have vastly underperformed the REITs. Interestingly, REITs have outperformed FANG’s since the end of February 2018.

For the twelve months ended September 30, 2018, the Timothy Plan Defensive Fund Real Estate Sleeve generated a gross return of 4.59% versus the FTSE NAREIT Equity REITs Index return of 3.47%. Strong stock selection drove performance while sector allocation was moderately negative. Diversified, Freestanding, Industrial and Healthcare drove positive performance while Lodging, Self-Storage and Mixed sectors detracted from performance. At times, avoiding stocks is more beneficial than owning them and thus within the Diversified sector, Colony Capital dropped 50% during this period and we did not own the stock. A merger gone bad was mostly the cause for their decline. As ironic as it seems, Freestanding stocks performed well and are leading the way in 2018 even with long leases in a rising rate environment. Logic says that short duration with growth should work better than long duration but, in this case, cap rates in triple net properties have proven resilient given their lack of credit issues and higher going in yield. Industrial stocks performed well as the expanding economy and e-commerce are driving higher rents and based on most recent quarter, this momentum should continue. The demand for e-commerce is changing the supply chain and new technologically efficient buildings are needed for the future of on-line economy. Healthcare REITs were strong performers for the portfolio as skilled nursing company Sabra Health Care had improved returns as occupancies stabilized. On the negative side, Lodging was the largest underperformer as we lost 56 basis points. Our underweight and stock selection hurt performance. As the economy improves, business and transient travel benefits hotels. Self-storage stocks were a detractor to performance as we maintained an underweight given slowing

15

cash flow growth from excessive supply. Although fundamentally we were right, the hurricanes in late 2017 temporarily increased demand in Houston and Florida.

Lastly, real estate stocks continue to deliver on their merits of higher than average yield and good dividend growth. Importantly, some sectors should see trough fundamentals in 2019 which will set up for a stronger 2020. We believe retail should see less bankruptcies and thus FFO growth should improve as the year progresses. Senior housing has been through a difficult period but with construction starts moving lower and deliveries also peaking, this sector should also begin to attract investor attention in the 2nd to 3rd quarter of 2019. We continue to position for a turn in senior housing with our Brookdale Senior Living investment while waiting for a better entry in the retail sectors.

For Institutional Client Use Only

(675219)

16

Important Information:

Investing involves risk, including possible loss of principal.

The FTSE NAREIT Equity REITs Index measures the performance of all publicly traded equity real estate investment trusts (REITs) traded on U.S. exchanges, excluding timber and infrastructure REITs.

All third-party trademarks are the property of their respective owners.

Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

The views expressed represent the Investment Manager’s assessment of the account and market environment as of September 30, 2018 and should not be considered a recommendation to buy, hold, or sell any security, and should not be relied on as research or investment advice. Holdings are as of September 30, 2018 and subject to change.

Past performance is no guarantee of future results.

Unless otherwise noted, the source of statistical information used in this document was FactSet.

Because this Strategy expects to hold a concentrated fund of a limited number of securities, the fund’s risk is increased because each investment has a greater effect on the Strategy’s overall performance.

REIT investments are subject to many of the risks associated with direct real estate ownership, including changes in economic conditions, credit risk, and interest rate fluctuations.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Additional information regarding the firm’s policies and procedures for calculating and reporting performance results is available upon request. A complete list and description of composites managed is available upon request. The above information is not intended and should not be construed as a presentation of information regarding any mutual fund.

Macquarie Investment Management (MIM) is the marketing name for the following registered investment advisers: Macquarie Investment Management Business Trust, Macquarie Funds Management Hong Kong Limited, Macquarie Investment Management Austria Kapitalanlage AG, Macquarie Investment Management Global Limited, Macquarie Investment Management Europe Limited, and Macquarie Capital Investment Management LLC.

Other than Macquarie Bank Limited (MBL), none of the entities noted are authorised deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise

© 2018 Macquarie Group Limited

For Institutional Client Use Only

(675219)

17

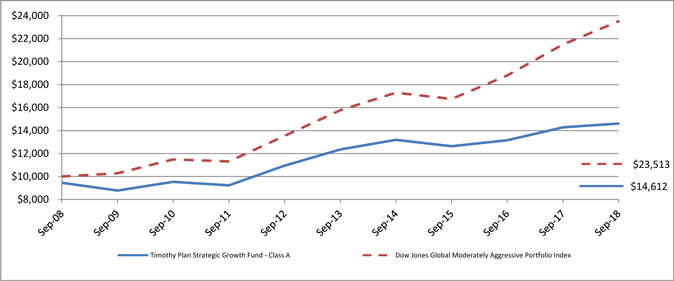

September 30, 2018

Dear Strategic Growth Fund Shareholder:

The Timothy Plan Strategic Growth Fund is an asset allocation fund that invests in ten of Timothy Plan’s underlying funds. The allocation percentages vary from time to time due to Timothy Partners, Ltd.’s (the “Advisor”) observations and perceptions of changing economic conditions. As of September 30, 2018, the allocation was as follows:

| | | | | | | | | | | | |

| • | | Large/Mid-Cap Growth Fund | | 10.00% | | | | * | | Small-Cap Value Fund | | 6.00% |

| | | | | | |

| • | | Large/Mid-Cap Value Fund | | 11.00% | | | | * | | Aggressive Growth Fund | | 5.50% |

| | | | | | |

| • | | International Fund | | 19.50% | | | | * | | High-Yield Bond Fund | | 6.50% |

| | | | | | |

| • | | Defensive Strategies Fund | | 12.00% | | | | * | | Israel Common Values | | 5.00% |

| | | | | | |

| • | | Emerging Markets Fund | | 7.00% | | | | * | | Growth & Income | | 9.50% |

| | | | | | |

| • | | Fixed Income | | 5.00% | | | | * | | Cash | | 3.00% |

At fiscal year end, the Fund’s overall allocation resulted in approximately 64.0% invested in Timothy Plan’s underlying domestic and international equity funds, 23.5% in Timothy Plan’s underlying bond and Defensive Strategies funds, 9.5% in Growth & Income, which also incorporates a relatively significant bond portfolio, and 3.0% in cash. The Strategic Growth Fund’s performance was a positive 2.32% for Class A for the fiscal year ending 9-30-18 even with the weakness in international equities and commodities (which comprise a significant portion of our Defensive Strategies Fund). Detailed descriptions of events that contributed to this past year’s performance of the underlying Funds is contained in each sub-advisor’s letter, found within the pages of this Annual Report.

We realize the volatility and uncertainty of the markets over the past couple of years may have been unsettling for many investors; however, as mentioned above, we believe the outlook for the capital markets for the remainder of 2018 and beyond should be fairly bright long-term; nevertheless, we are committed to manage our funds with a definite conservative bias.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Sincerely,

Arthur D. Ally

Fund Advisor

18

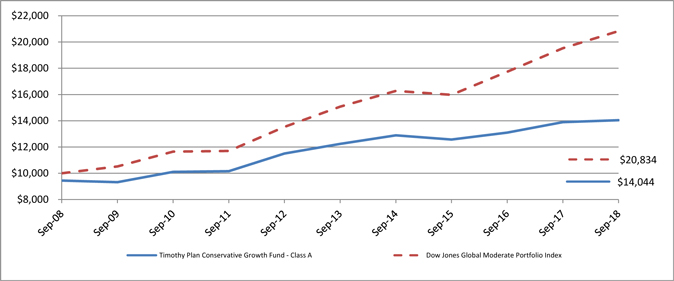

September 30, 2018

Dear Conservative Growth Fund Shareholder:

The Timothy Plan Conservative Growth Fund is an asset allocation fund that invests in Timothy Plan underlying funds. The allocation percentages vary from time to time due to Timothy Partners Ltd.‘s (the “Advisor”) observations and perceptions of changing economic conditions; the allocation on September 30, 2018 was as follows:

| | | | | | | | | | | | |

| • | | Large/Mid-Cap Growth Fund | | 7.50% | | | | * | | Small-Cap Value Fund | | 5.00% |

| | | | | | |

| • | | Large/Mid-Cap Value Fund | | 8.50% | | | | * | | Aggressive Growth Fund | | 4.00% |

| | | | | | |

| • | | International Fund | | 10.50% | | | | * | | High-Yield Bond Fund | | 6.50% |

| | | | | | |

| • | | Defensive Strategies Fund | | 11.00% | | | | * | | Israel Common Values | | 3.50% |

| | | | | | |

| • | | Emerging Markets Fund | | 4.50% | | | | * | | Growth & Income | | 9.50% |

| | | | | | |

| • | | Fixed Income | | 24.50% | | | | * | | Cash | | 5.00% |

At fiscal year end, the Fund’s overall allocation resulted in approximately 43.5% invested in Timothy Plan’s underlying domestic and international equity funds, 42.0% in Timothy Plan’s underlying bond and Defensive Strategies funds, 9.5% in Growth & Income, which also incorporates a relatively significant bond portfolio, and 5.0% in cash. The Conservative Growth Fund’s performance was a positive 1.06% for Class A for the fiscal year ending 9-30-18 even with the weakness in international equities and commodities (which comprise a significant portion of our Defensive Strategies Fund). Detailed descriptions of events that contributed to this past year’s performance of the underlying Funds is contained in each sub-advisor’s letter, found within the pages of this Annual Report.

We realize the volatility and uncertainty of the markets over the past couple of years may have been unsettling for many investors; however, as mentioned above, we believe the outlook for the capital markets for the remainder of 2018 and beyond should be fairly bright long-term; nevertheless, we are committed to manage our funds with a definite conservative bias.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is that every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment with which you can feel comfortable.

Yours in Christ,

Arthur D. Ally

Fund Advisor

19

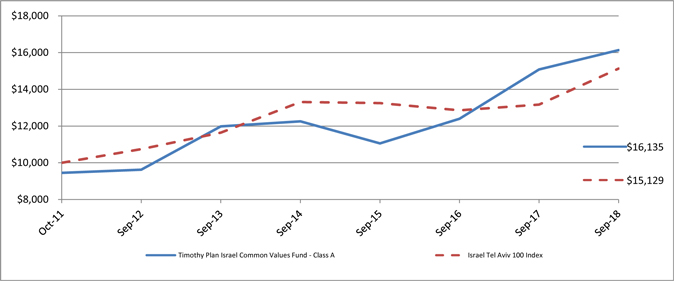

Letter from The Manager

The Timothy Plan Israel Common Values Fund

September 30, 2018

The Timothy Plan Israel Common Values Fund performed well on an absolute basis but trailed the TA-125 index over the twelve-month period. Strong absolute performance in the Technology, Financials, and Materials sectors led the way. Sector allocation was positive for the last twelve months while stock selection proved negative. The main culprit in the negative selection was detrimental stock selection in the Consumer Discretionary and Health Care sectors. The negative relative performance was more a story of what the Fund did not own rather than what it did own. Not owning some of the pharmaceutical names that came back strong in the year as well as Consumer Discretionary company Sodastream, which was acquired by Pepsi, were detrimental to relative performance versus the index. On the positive front, the Fund’s exposure to cyber security companies, where Israel is a world leader in innovation, was helpful to the Fund with names such as CyberArk Software performing well. In addition, Fund holding Orbotech was acquired by a U.S. company following on the trend of global companies acquiring innovative Israeli firms. The Fund’s overweight to the Technology sector provided good opportunities to the leading-edge technologies in cloud computing, data centers, and cyber security.

The Israeli economy remains strong and most economists forecast GDP growth to remain above 3% for the foreseeable future. Household spending remains robust on the back of strong wage growth and a historically low unemployment rate and historically high labor participation rate. The Bank of Israel (BoI) remained on the sidelines during this period and most analysts do not expect the BoI to raise interest rates until later in 2019. Inflation has bounced back a bit given the strong wage growth but remains at the low end of the central bank’s desired range. The energy sector continues to invest in infrastructure as new natural gas export deals are struck with Israel’s neighbors. Export growth improved over this period as global growth rebounded while some depreciation of the strong Israeli shekel helped the export economy as well.

The Fund continues to invest alongside the innovate spirit of Israeli companies providing ample attractive investment opportunities. Strong domestic consumption should continue to support corporate earnings into next year. We remain committed to a consistent investment approach dedicated to finding long-term investments for the Fund. We thank you for your continued investment in the Fund.

Eagle Global Advisors, LLC

20

Brandes Investment Partners, L.P.

Emerging Markets Fund

Equity Strategy Notes

Third Quarter 2018 (July 1 – September 30, 2018)

The Brandes Emerging Markets Equity Strategy slightly outperformed its benchmark, the MSCI Emerging Markets Index, which fell 1.1%.

Positive Contributors

Highlighting how volatility is often part and parcel of emerging markets investing, two of this period’s major positive contributors were detractors to returns in the second quarter. Brazilian Petrobras and Argentinian YPF rebounded sharply as short-term concerns that weighed on their shares last quarter abated. As with our other oil & gas holdings, both companies continued to benefit from improved earnings and cash flows in a higher oil-price environment.

Holdings in Mexico also aided returns, led by real estate investment trusts (REITs) PLA Administradora Industrial (Terrafina) and Macquarie Mexico Real Estate Management. Investors seemed to welcome the prospect of the new trade deal between the United States and Mexico, which lifted some uncertainty regarding future relations between the two countries.

Additionally, our underweight to China helped relative performance.

Performance Detractors

The strategy’s exposure to Turkey, most notably our commercial bank holdings, hurt performance amid the country’s currency crisis. President Erdogan’s interference in monetary policy and the appointment of his son-in-law as treasury and finance minister shook investor confidence. Furthermore, weakened diplomatic relations with western partners added fuel to the lira’s tumbling. While fears of contagion momentarily spread throughout emerging markets, they have since dissipated.

As the risks of investing in the country intensified, we exited our position in bank Vakif Bankasi, especially given the company’s direct government control. We continuously monitor the situation in Turkey and maintain measured positions in Akbank, Garanti Bankasi and REIT Emlak Konut.

Holdings in Brazil also declined as the country’s upcoming election led to increased volatility. Notable detractors included food producer Marfrig Global Foods, regional jet manufacturer Embraer, health insurer Hapvida Participacoes and payment processor Cielo.

In early July, Boeing and Embraer released a non-binding agreement to establish a new joint venture (JV) for commercial aircraft. The deal values Embraer’s commercial aircraft business unit, which will be fully transferred to the new JV, at $4.75bn. Based on the proposed terms, Boeing will own an 80% stake in the JV, while Embraer will hold the remaining 20%. Embraer will also retain control of its defense and business jet operations. The deal is expected to close by the end of 2019, subject to regulatory clearance.

Embraer’s shares fell as many investors appeared unsatisfied with the offered price. However, in our opinion, the price was adequate, especially considering the other terms outlined in the agreement. Through its 20% stake, Embraer will be able to participate in the potential synergies that may materialize within the JV. Additionally, as the commercial aviation segment has faced increased competition, particularly from Chinese, Russian and Japanese newcomers, we believe the deal actually “neutralizes” a major long-term business threat for Embraer.

In August, Marfrig announced that it would sell about 90% of its stake in Keystone, a fully owned subsidiary, to Tyson Foods. Keystone supplies protein to fast food chains mostly in the United States and Asia. The deal is expected to close by year-end at an enterprise value of $2.4bn, which was below the market’s initial expectations. Nevertheless, we believe Marfrig remains undervalued. We are encouraged by the company’s continued balance sheet improvements and its efforts to streamline its business model.

Select Activity in the Third Quarter

The investment committee added X5 Retail Group to the strategy.

X5 is Russia’s largest food retailer by revenue, with an approximately 9% market share in food retailing and a strong footprint in big cities such as Moscow and St. Petersburg. The company operates in three retail formats, namely proximity/convenience stores (78% of 2017 sales), supermarkets (15% of sales) and hypermarkets (7% of sales). The company has a vertically integrated supply chain and delivers over 90% of the items sold in its stores from internal distribution centers.

A number of factors have weighed on X5’s shares, including an increasing pressure on margins (an industry-wide challenge), a recent move of management personnel to a main competitor and the potential impact of further sanctions against Russia. We believe these concerns have been more than reflected in the current share price. Despite the pressure on margins, the food retailing industry in Russia is still underpenetrated relative to developed countries, with fewer grocery stores per 1,000 inhabitants.

Trading at less than 10x forward earnings and offering a dividend yield of 5.5% as of September 30, X5 represents an appealing investment opportunity to us.

Year-to-Date 2018 Briefing

The Brandes Emerging Markets Equity Strategy underperformed the MSCI Emerging Markets Index, which fell 7.7% for the nine months ended September 30, 2018.

Similar to what happened in the quarter, holdings in Turkey and Brazil detracted from year-to-date returns. Turkish Akbank, Vakif Bankasi and Emlak Konut performed poorly, as did Brazil’s Marfrig Global Foods and Embraer.

Other detractors included Indian electric utility Reliance Infrastructure and Argentinian oil & gas firm YPF.

We saw positive contributions from our oil & gas holdings, specifically Lukoil, Surgutneftegas and Petrobras. Retailers with exposure to China—namely Lifestyle International, Bosideng and Luk Fook Holdings—also helped performance. Additionally, Indian technology company Infosys aided returns.

Current Positioning

We have increasingly found investment opportunities in China amid the country’s trade war with the United States, coupled with increased market volatility.

The strategy’s exposures have been relatively unchanged, as Brazil, Russia and Mexico continue to represent overweight positions. We also maintained higher allocations to consumer discretionary and telecommunication services companies than the benchmark.

China remained one of our largest underweights at quarter end, along with Taiwan. From a sector perspective, we held material underweight allocations to information technology and financials.

We remain convinced that the current positioning of the Brandes Emerging Markets Equity Strategy, which results from our careful bottom-up stock selection, bodes well for the long term.

Thank you for your continued trust.

Cash Flow: The amount of cash generated minus the amount of cash used by a company in a given period.

Dividend Yield: Dividends per share divided by price per share.

Enterprise value: Market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Forward Earnings: Sell-side analysts’ consensus earnings estimates for the next fiscal year.

Forward Price/ Earnings: Price per share divided by earnings estimates for the next fiscal year.

The declaration and payment of shareholder dividends are solely at the discretion of the issuer and are subject to change at any time.

The MSCI Emerging Markets Index with net dividends captures large and mid cap representation of emerging market countries. Data prior to 2001 is gross dividend and linked to the net dividend returns.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The foregoing Quarterly Commentary reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice. The information provided in the commentary should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings or sectors discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. International and emerging markets investi ng is subject to certain risks such as currency fluctuation and social and political changes; such risks may result in greater share price volatility. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that the securities sold have not been repurchased. The actual characteristics with respect to any particular account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Unlike bonds issued or guaranteed by the U.S. government or its agencies, stocks and other bonds are not backed by the full faith and credit of the United States. Stock and bond prices will experience market fluctuations. Please note that the value of government securities and bonds in general have an inverse relationship to interest rates. Bonds carry the risk of default, or the risk that an issuer will be unable to make income or principal payment. There is no assurance that private guarantors or insurers will meet their obligations. The credit quality of the investments in the portfolio is not a guarantee of the safety or stability of the portfolio. Investments in Asset Backed and Mortgage Backed Securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Securities of small companies generally experience more volatility than mid and large sized companies. Although the statements of fact and data in this report have been obtained from, and are based upon, sources that are believed to be reliable, we cannot guarantee their accuracy, and any such information may be incomplete or condensed. Strategies discussed are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. The Brandes investment approach tends to result in portfolios that are materially different than their benchmarks with regard to characteristics such as risk, volatility, diversification, and concentration. Please note that all indices are unmanaged and are not available for direct investment. Past performance is not a guarantee of future results. No investment strategy can assure a profit or protect against loss. Market conditions may impact performance. The performance results presented were achieved in particular market conditions which may not be repeated. Moreover, the current market volatility and uncertain regulatory environment may have a negative impact on future performance. The margin of safety for any security is defined as the discount of its market price to what the firm believes is the intrinsic value of that security. The declaration and payment of shareholder dividends are solely at the discretion of the issuer and are subject to change at any time.

United States: Issued by Brandes Investment Partners, L.P., 11988 El Camino Real, Suite 600, San Diego, CA 92130.

LETTER FROM THE MANAGER

September 30, 2018

Timothy Plan Growth and Income Fund

We are pleased to provide you our annual report for the Timothy Plan Growth and Income Fund for the period ending September 30, 2018. Like you, our company continues to hold corporate and retirement assets in the fund and some officers have additional personal assets in the fund. We certainly thank you for entrusting your assets with us.

For the period starting 1 October 2017 through 30 September 2018, the fund returned -1.22% for Class A shares. The Energy and Industrial sectors contributed the most to performance. Two top stock contributors were Sodastream International Ltd and Cleveland-Cliffs Inc.

We continue to see divergences in the indices and underlying stock returns. Stocks with earnings have underperformed stocks without earnings so far in 2018. Bargain stocks, those with inexpensive valuation ratios, positive and growing earnings, and relative price strength, underperformed stocks with the opposite characteristics. This is not normal and we expect this to reverse as it has in the past.

Bonds helped reduce volatility during the past year. This is one reason why we continue to advocate a balanced portfolio approach. We continue to favor high quality bonds over lower quality bonds. They tend to hold up better in times of uncertainty and the extra compensation earned on lower quality bonds is near the lowest levels of this credit cycle.

We think the best returns in bonds are probably behind us. However, when stocks suffer another setback, having bonds in the portfolio should help. We think volatility will continue but if our research works well, this actually could give us opportunities to take advantage of these moves.

This fund has two main objectives, growth and income but also preserving capital in declining markets. We have been managing similar assets for over 40 years. We will adjust equity and fixed income levels according to our risk analysis. We do this on a weekly basis. We continue to see opportunities for small capitalization value stocks going forward as they typically have less exposure to international economies and more opportunities for growth.

We thank you for your trust in the James Investment Research Inc., we are grateful for the opportunity to serve you.

James Investment Research, Inc.

24

Fund Performance - (Unaudited)

September 30, 2018

Aggressive Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | |

Timothy Aggressive Growth Fund - Class A (With Sales Charge) | | 8.04% | | 6.09% | | | 8.78% | |

Russell Mid-Cap Growth Index | | 21.10% | | 13.00% | | | 13.46% | |

Timothy Aggressive Growth Fund - Class C * | | 12.67% | | 6.52% | | | 8.61% | |

Russell Mid-Cap Growth Index | | 21.10% | | 13.00% | | | 13.46% | |

Timothy Aggressive Growth Fund - Class I | | 14.62% | | 7.55% | | | 7.62% (a) | |

Russell Mid-Cap Growth Index | | 21.10% | | 13.00% | | | 12.79% (a) | |

| | (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2018. |

| | * | With Maximum Deferred Sales Charge |

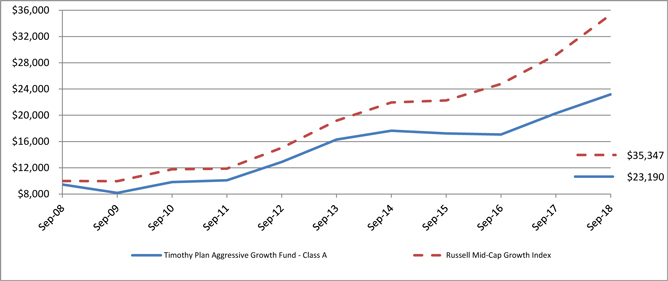

Timothy Plan Aggressive Growth Fund vs. Russell Mid-Cap Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell Mid-Cap Growth Index on September 30, 2008 and held through September 30, 2018. The Russell Mid-Cap Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

25

Fund Performance - (Unaudited)

September 30, 2018

International Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | |

Timothy International Fund - Class A (With Sales Charge) | | (4.69)% | | 2.52% | | | 2.87% | |

MSCI EAFE Index | | (0.01)% | | 1.65% | | | 2.42% | |

Timothy International Fund - Class C * | | (0.87)% | | 2.91% | | | 2.69% | |

MSCI EAFE Index | | (0.01)% | | 1.65% | | | 2.42% | |

Timothy International Fund - Class I | | 1.04% | | 3.91% | | | 4.23% (a) | |

MSCI EAFE Index | | (0.01)% | | 1.65% | | | 2.45% (a) | |

| | (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2018. |

| | * | With Maximum Deferred Sales Charge |

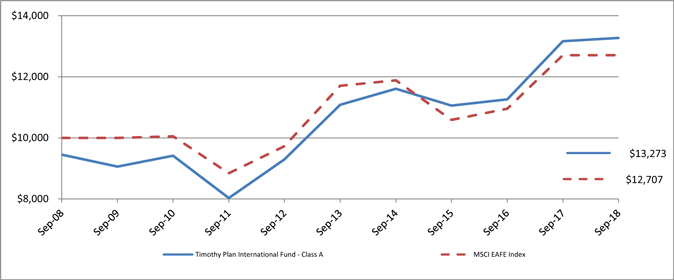

Timothy Plan International Fund vs. MSCI EAFE Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the MSCI EAFE Index on September 30, 2008 and held through September 30, 2018. The MSCI EAFE Index is a widely recognized unmanaged index of equity prices and is representative of equity market performance of developed countries, excluding the U.S. and Canada. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

26

Fund Performance - (Unaudited)

September 30, 2018

Large/Mid Cap Growth Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | |

Timothy Large/Mid Cap Growth Fund - Class A (With Sales Charge) | | 5.36% | | 8.34% | | | 9.57% | |

Russell 1000 Growth Index | | 26.30% | | 16.58% | | | 14.31% | |

Timothy Large/Mid Cap Growth Fund - Class C * | | 9.63% | | 8.75% | | | 9.35% | |

Russell 1000 Growth Index | | 26.30% | | 16.58% | | | 14.31% | |

Timothy Large/Mid Cap Growth Fund - Class I | | 11.69% | | 9.84% | | | 9.66% (a) | |

Russell 1000 Growth Index | | 26.30% | | 16.58% | | | 16.29% (a) | |

| | (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2018. |

| | * | With Maximum Deferred Sales Charge |

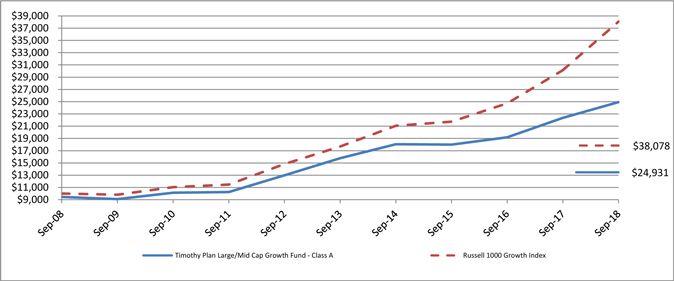

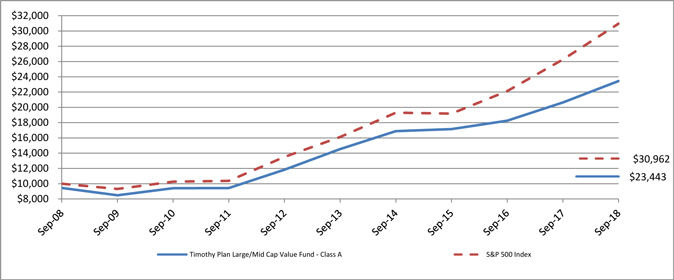

Timothy Plan Large/Mid Cap Growth Fund vs. Russell 1000 Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 1000 Growth Index on September 30, 2008 and held through September 30, 2018. The Russell 1000 Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

27

Fund Performance - (Unaudited)

September 30, 2018

Small Cap Value Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | |

Timothy Small Cap Value Fund - Class A (With Sales Charge) | | 4.07% | | 8.91% | | | 9.86% | |

Russell 2000 Index | | 15.24% | | 11.07% | | | 11.11% | |

Timothy Small Cap Value Fund - Class C * | | 8.27% | | 9.33% | | | 9.66% | |

Russell 2000 Index | | 15.24% | | 11.07% | | | 11.11% | |

Timothy Small Cap Value Fund - Class I | | 10.37% | | 10.42% | | | 10.73% (a) | |

Russell 2000 Index | | 15.24% | | 11.07% | | | 11.04% (a) | |

| | (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2018. |

| | * | With Maximum Deferred Sales Charge |

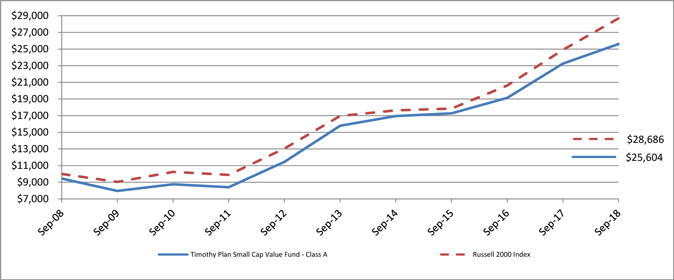

Timothy Plan Small Cap Value Fund vs. Russell 2000 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 2000 Index on September 30, 2008 and held through September 30, 2018. The Russell 2000 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

28

Fund Performance - (Unaudited)

September 30, 2018

Large/Mid Cap Value Fund

| | | | | | | | |

| Fund/Index | | 1 Year Total Return | | 5 Year Average Annual Return | | 10 Year Average Annual Return | |

Timothy Large/Mid Cap Value Fund - Class A (With Sales Charge) | | 7.31% | | 8.79% | | | 8.89% | |

S&P 500 Index | | 17.91% | | 13.95% | | | 11.97% | |

Timothy Large/Mid Cap Value Fund - Class C * | | 11.75% | | 9.22% | | | 8.69% | |

S&P 500 Index | | 17.91% | | 13.95% | | | 11.97% | |

Timothy Large/Mid Cap Value Fund - Class I | | 13.83% | | 10.30% | | | 9.89% (a) | |

S&P 500 Index | | 17.91% | | 13.95% | | | 13.23% (a) | |

| | (a) | For the period August 1, 2013 (commencement of investment in accordance with objective) to September 30, 2018. |

| | * | With Maximum Deferred Sales Charge |

Timothy Plan Large/Mid Cap Value Fund vs. S&P 500 Index