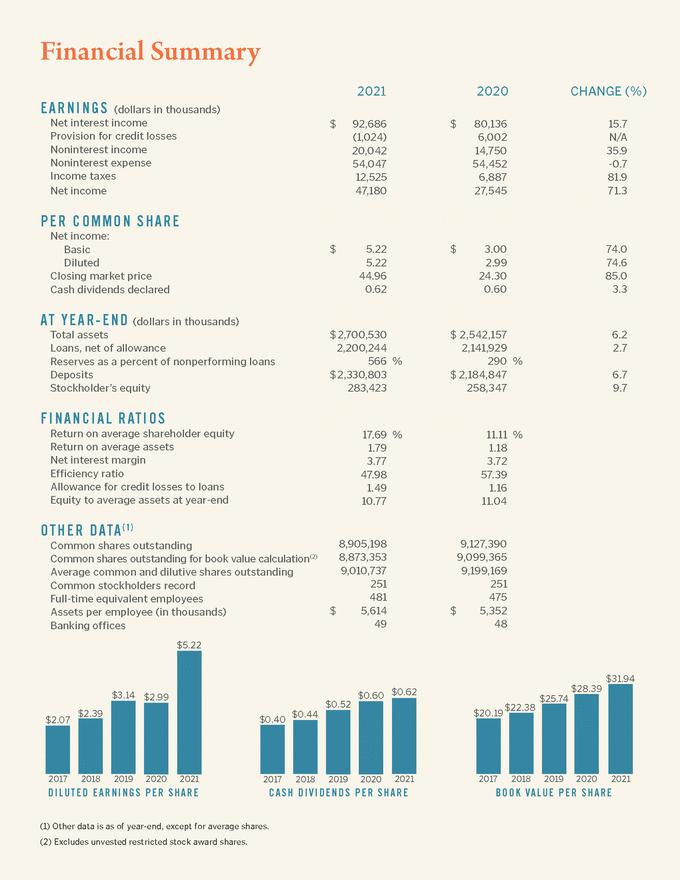

| Loan growth slowed somewhat in fiscal 2021, but actually held up a little better than we anticipated a year ago. Gross loans increased $66.4 million, net of PPP reductions of $69.3 million. Growth consisted primarily of residential real estate loans and drawn balances on construction loans, partially offset by declines in commercial loans and consumer loans. The Company adopted ASU 2016-13, also known as the “CECL” standard, which increased our allowance for credit losses through a one-time adjustment to retained earnings. Deposits again had a strong year, as economic impact payments, deferrals of payroll and other taxes due from businesses, and proceeds from additional PPP lending continued to impact account balances. Total deposit growth of $146.0 million, or 6.7%, reflected an increase in transaction accounts, savings accounts, and money market deposit accounts, partially offset by a decline in time deposits. Total public unit deposits increased $21.2 million, while brokered funding declined by $18.3 million. (Dollars in millions) net of allowance for loan losses (Dollars in millions) $2,200 $2,701 $2,142 $2,185 $1,456 $1,398 $1,708 Book value per common share at June 30, 2021, was $31.94, an increase of 12.5% from June 30, 2020. Tangible book value per common share, a non-GAAP measure, improved 13.7%, to $29.55 at June 30, 2021. Our closing stock price at the end of the 2021 fiscal year rebounded notably from a year earlier, to $44.96, as compared to $24.30 at June 30, 2020, an increase of 85.0%, as banking industry multiples improved with reduced economic uncertainty. Over that same period, the S&P Broad Market Index (BMI) for US Banks reported an increase of 65.7%, while the S&P 500 increased 38.6%. Our total shareholder return over the five years ended June 30, 2021, assuming dividends had been reinvested, has been 107.3%. Over that same time period the S&P BMI for US Banks has returned 113.6%, and the S&P 500 has returned 125.4%. During the fiscal year, the Company restarted and completed its previously-announced repurchase plan. In May 2021, the Company announced a new repurchase plan providing for the repurchase of up to 5% of outstanding shares. During fiscal 2021, under both plans, the Company utilized capital of $8.3 million to repurchase approximately 238,000 shares. Under the current repurchase plan, 439,000 shares remain available for repurchase. Dividends paid during fiscal 2021 represented a 1.4% return on our closing stock price on the final day of the fiscal year, and a 1.9% return on our average closing stock price for fiscal 2021. In July 2021, the board approved an increase in our quarterly dividends per share to $0.20. During fiscal 2021, the Company’s capital base grew somewhat faster than our assets, despite our repurchase activity, driven by strong earnings and moderate asset growth. We ended fiscal 2021 with a ratio of tangible common equity LONG-TERM GROWTH IN LOANS, DEPOSITS, AND TOT AL ASSETS Loan growth held up reasonably well, net of PPP repayments, in fiscal 2021; Nonmaturity deposit growth remained strong, while CDs continued to trend lower. Total AssetsTotal Loans,Total Deposits (Dollars in millions) $2,331 $2,214 $2,542 $1,846$1,894 $1,886$1,563$1,580 2017201820192020 20212017201820192020 20212017201820192020 2021 |