QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on October 10, 2003

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ADVANSTAR COMMUNICATIONS INC.

(Exact Name of Registrant as Specified in Its Charter)

| New York (State or Other Jurisdiction of Incorporation or Organization) | 7389 (Primary Standard Industrial Classification Code Number) | 59-2757389 (I.R.S. Employer Identification Number) | ||

545 Boylston Street, 9th Floor Boston, MA 02116 (617) 267-6500 SEE TABLE OF ADDITIONAL REGISTRANTS (Address, Including Zip Code, and Telephone Number Including Area Code, of Registrant's Principal Executive Offices) | ||||

David W. Montgomery Vice President-Finance, Chief Financial Officer & Secretary Advanstar Communications Inc. 131 West First Street Duluth, MN 55802 (218) 723-9200 (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service) | ||||

Copies to:

Michael Kaplan, Esq.

Davis Polk & Wardwell

450 Lexington Avenue

New York, New York 10017

(212) 450-4000

Approximate date of commencement of proposed sale to the public:From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

CALCULATION OF REGISTRATION FEE

| Title Of Each Class Of Securities To Be Registered | Amount To Be Registered | Proposed Maximum Offering Price Per Unit(1) | Proposed Maximum Aggregate Offering Price(1) | Amount Of Registration Fee | ||||

|---|---|---|---|---|---|---|---|---|

| Second Priority Senior Secured Floating Rate Exchange Notes | $130,000,000 | 100% | $130,000,000 | $10,517 | ||||

| 103/4% Second Priority Senior Secured Exchange Notes | $300,000,000 | 100% | $300,000,000 | $24,270 | ||||

| Guarantees | $— | —% | $— | $—(2) | ||||

- (1)

- Estimated solely for the purpose of calculating the amount of the registration fee. Pursuant to Rule 457(g) an indeterminate number of such securities is being registered for marketing purposes.

- (2)

- Pursuant to Rule 457(n), no registration fee is payable with respect to the guarantees.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

| REGISTRANT | STATE OR OTHER JURISDICTION OF INCORPORATION OR ORGANIZATION | PRIMARY STANDARD INDUSTRIAL CLASSIFICATION NUMBER | I.R.S. EMPLOYER IDENTIFICATION NUMBER | |||

|---|---|---|---|---|---|---|

| Men's Apparel Guild in California, Inc. | California | 7389 | 95-1588605 | |||

| Applied Business teleCommunications | California | 7389 | 94-2896012 |

This Registration Statement covers the registration of an aggregate principal amount of $130,000,000 of Second Priority Senior Secured Floating Rate Notes due 2008 and $300,000,000 of 103/4% Second Priority Senior Secured Notes due 2010 of Advanstar Communications Inc. that may be exchanged for equal principal amounts of Advanstar's outstanding $130,000,000 of Second Priority Senior Secured Floating Rate Notes due 2008 and $300,000,000 of 103/4% Second Priority Senior Secured Notes due 2010, respectively. This Registration Statement also covers the registration of the new notes for resale by Credit Suisse First Boston LLC, which is an affiliate of Advanstar Communications Inc., in market-making transactions. The complete prospectus relating to the exchange offer follows immediately after this Explanatory Note. Following the prospectus are certain pages of the prospectus relating solely to market-making transactions, including an alternate front cover page, Table of Contents, a section entitled "Risk Factors—Risks Relating to the Notes—There is no existing trading market for the notes, which could make it difficult for you to sell your notes at an acceptable price or at all" to be used in lieu of the section entitled "Risk Factors—Risks Relating to the Notes—No public trading market for the notes exists which could result in an illiquid trading market and/or lower sales price for your notes," an alternate "Use of Proceeds" section and an alternate "Plan of Distribution" section. In addition, the market-making prospectus will not include the following captions (or the information set forth under those captions) in the exchange offer prospectus: "Summary—The Exchange Offer" and "Material United States Tax Consequences of the Exchange Offer" or the section entitled "Risk Factors—The exchange offer will result in reduced liquidity of the unexchanged old notes, so you may face lower prices for your old notes if you do not exchange them for new notes." All other sections of the exchange offer prospectus will be included in the market-making prospectus.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (SUBJECT TO COMPLETION DATED OCTOBER 10, 2003)

Offer to Exchange

Second Priority Senior Secured Floating Rate Notes due 2008

for

Second Priority Senior Secured Floating Rate Exchange Notes due 2008

and

103/4% Second Priority Senior Secured Notes due 2010

for

103/4% Second Priority Senior Secured Exchange Notes due 2010

We are offering to exchange

- •

- up to $130,000,000 of our new Second Priority Senior Secured Floating Rate Exchange Notes due 2008 for up to $130,000,000.00 of our existing, or old, Second Priority Senior Secured Floating Rate Notes due 2008 and

- •

- up to $300,000,000 of our new 103/4% Second Priority Senior Secured Exchange Notes due 2010 for up to $300,000,000 of our existing, or old, 103/4% Second Priority Senior Secured Notes due 2010.

The terms of the new notes are generally identical in all material respects to the terms of the old notes, except that the new notes have been registered under the Securities Act and the transfer restrictions and registration rights relating to the old notes do not apply to the new notes.

To exchange your old notes for new notes:

- •

- you are required to make the representations described on page 136 to us

- •

- you must complete and send the letter of transmittal that accompanies this prospectus to the exchange agent, Wells Fargo Bank Minnesota, N.A., by 5:00 p.m., New York time, on , 200

- •

- you should read the section called "The Exchange Offer" for further information on how to exchange your old notes for new notes

See "Risk Factors" beginning on page 13 for a discussion of risk factors that should be considered by you prior to tendering your old notes in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the exchange offer or passed upon the adequacy or accuracy of this Prospectus. Any representation to the contrary is a criminal offense.

, 2003

| | Page | |

|---|---|---|

| Summary | 1 | |

| Risk Factors | 13 | |

| The Acquisition | 25 | |

| Use of Proceeds | 27 | |

| Capitalization | 28 | |

| Industry and Market Data | 29 | |

| Selected Historical Consolidated Financial Data | 30 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 32 | |

| Business | 51 | |

| Management | 66 | |

| Executive Compensation | 68 | |

| Security Ownership of Certain Beneficial Owners and Management | 74 | |

| Certain Relationships and Related Party Transactions | 76 | |

| Description of Certain Indebtedness | 78 | |

| Description of Notes | 82 | |

| The Exchange Offer | 130 | |

| Material United States Tax Consequences of the Exchange | 137 | |

| Plan of Distribution | 137 | |

| Legal Matters | 137 | |

| Experts | 138 | |

| Where You Can Find More Information | 138 | |

| Index to Financial Statements | F-1 | |

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

The names of events, publications and services used in this prospectus are trademarks, trade names and service marks of Advanstar Communications Inc., its subsidiaries or its joint ventures. Names of companies and associations used in this prospectus are trademarks or trade names of the respective organizations.

In this prospectus, "Advanstar," the "Company," "we," "us" or "our" refer to Advanstar Communications Inc. and its subsidiaries, except where the context makes clear that the reference is only to Advanstar Communications Inc. itself and is not inclusive of its subsidiaries.

i

This summary highlights the more detailed information in this prospectus and you should read the entire prospectus carefully.

| Securities Offered | We are offering up to $130,000,000 aggregate principal amount of Second Priority Senior Secured Floating Rate Exchange Notes due 2008 and up to $300,000,000 aggregate principal amount of 103/4% Second Priority Senior Secured Exchange Notes due 2010, which have been registered under the Securities Act. | |

The Exchange Offer | We are offering to issue the new notes in exchange for a like principal amount of your old notes which were issued in two transactions in August and September 2003. See "—Recent Developments." We are offering to issue the new notes to satisfy our obligations contained in the registration rights agreements entered into when the old notes were sold in transactions permitted by Rule 144A and Regulation S under the Securities Act and therefore not registered with the SEC. For procedures for tendering, see "The Exchange Offer." | |

Tenders, Expiration Date, Withdrawal | The exchange offer will expire at 5:00 p.m. New York City time on , 200 unless it is extended. If you decide to exchange your old notes for new notes, you must acknowledge that you are not engaging in, and do not intend to engage in, a distribution of the new notes. If you decide to tender your old notes in the exchange offer, you may withdraw them at any time prior to , 200 . If we decide for any reason not to accept any old notes for exchange, your old notes will be returned to you without expense to you promptly after the exchange offer expires. | |

Federal Income Tax Consequences | Your exchange of old notes for new notes in the exchange offer will not result in any income, gain or loss to you for Federal income tax purposes. See "Material United States Federal Income Tax Consequences of the Exchange Offer." | |

Use of Proceeds | We will not receive any proceeds from the issuance of the new notes in the exchange offer. | |

Exchange Agent | Wells Fargo Bank Minnesota, N.A. is the exchange agent for the exchange offer. | |

Failure to Tender Your Old Notes | If you fail to tender your old notes in the exchange offer, you will not have any further rights under the applicable registration rights agreement, including any right to require us to register your old notes or to pay you additional interest. |

1

You will be able to resell the new notes without registering them with the SEC if you meet the requirements described below.

Based on interpretations by the SEC's staff in no-action letters issued to third parties, we believe that new notes issued in exchange for old notes in the exchange offer may be offered for resale, resold or otherwise transferred by you without registering the new notes under the Securities Act or delivering a prospectus, unless you are a broker-dealer receiving securities for your own account, so long as:

- •

- you are not one of our "affiliates", which is defined in Rule 405 of the Securities Act;

- •

- you acquire the new notes in the ordinary course of your business;

- •

- you do not have any arrangement or understanding with any person to participate in the distribution of the new notes; and

- •

- you are not engaged in, and do not intend to engage in, a distribution of the new notes.

If you are an affiliate of Advanstar, or you are engaged in, intend to engage in or have any arrangement or understanding with respect to, the distribution of new notes acquired in the exchange offer, you (1) should not rely on our interpretations of the position of the SEC's staff and (2) must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction.

If you are a broker-dealer and receive new notes for your own account in the exchange offer:

- •

- you must represent that you do not have any arrangement with us or any of our affiliates to distribute the new notes;

- •

- you must acknowledge that you will deliver a prospectus in connection with any resale of the new notes you receive from us in the exchange offer; the letter of transmittal states that by so acknowledging and by delivering a prospectus, you will not be deemed to admit that you are an "underwriter" within the meaning of the Securities Act; and

- •

- you may use this prospectus, as it may be amended or supplemented from time to time, in connection with the resale of new notes received in exchange for old notes acquired by you as a result of market-making or other trading activities.

For a period of 90 days after the expiration of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any resale described above.

2

Summary Description of the Notes

All of the new notes will be issued under the indenture under which the old notes issued in August 2003 were issued. The terms of the new notes and the old notes are identical in all material respects, except that the new notes will be registered under the Securities Act and the transfer restrictions and registration rights relating to the old notes will not apply to the new notes. The following summary contains basic information about the new notes. It does not contain all of the information that is important to you. For a more complete understanding of this offering, see "Description of Notes."

Issuer | Advanstar Communications Inc. | |||

Notes Offered | $130 million of second priority senior secured floating rate notes due 2008. | |||

$300 million of 10.75% second priority senior secured notes due 2010. | ||||

Principal and Maturity | Floating rate notes: Principal on the floating rate notes will be payable in quarterly installments on each interest payment date, beginning November 15, 2003 through May 15, 2008, with each installment equal to 0.25% of the original principal amount of the floating rate notes, and the balance payable at maturity on August 15, 2008. | |||

Fixed rate notes: The fixed rate notes will mature on August 15, 2010. | ||||

Interest | Floating rate notes: Initially 8.64% per annum for the quarterly period ending November 15, 2003 and reset quarterly on each February 15, May 15, August 15 and November 15 at three-month LIBOR plus 7.50%. Interest will be payable quarterly on each February 15, May 15, August 15 and November 15, beginning November 15, 2003. | |||

Fixed rate notes: 10.75% per annum, payable every May 15 and November 15, beginning November 15, 2003, and at maturity. Interest will accrue from August 18, 2003. | ||||

Collateral | The notes will be secured by second-priority liens, subject to certain exceptions and permitted liens, on the collateral securing our credit facility, other than the capital stock of certain of our subsidiaries and assets of our parent companies (which we refer to collectively as the "collateral"). Our credit facility is secured by a first-priority lien on the collateral. The indenture and the security documents relating to the notes permit us to incur a significant amount of debt including obligations secured (including on a first-priority basis) by the collateral, subject to compliance with certain conditions. No appraisals of any collateral have been prepared by us or on our behalf in connection with this exchange offer or in connection with the original offerings of the notes. The value of the collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. | |||

3

Advanstar and the administrative agent under the security documents governing the first-priority liens may release the first-priority liens on the collateral, whereupon the second-priority lien that secures the notes on such released collateral shall automatically be released without the consent of the holders of the notes. In addition, the lenders under the credit facility will have the sole ability to control remedies (including any sale or liquidation after acceleration of the debt under the senior secured credit facility) with respect to the collateral. See "Risk Factors—Risks Related to the Notes—The security for your benefit can be released without your consent, and the lenders under our credit facility will have control over all decisions with respect to enforcement of the security interests, including decisions regarding whether and when to foreclose upon assets." | ||||

You should read "Description of the Notes—Collateral" for a more complete description of the security granted to the holders of the notes. | ||||

Ranking | The notes and the guarantees will rank: | |||

• | equally with all of our and the guarantors' existing and future senior indebtedness; | |||

• | effectively junior to indebtedness under our credit facility, which is secured by a first-priority lien on the collateral, to the extent of the value of such collateral; | |||

• | senior to our and the guarantors' subordinated indebtedness, including our senior subordinated notes; and | |||

• | effectively junior to all of the liabilities of our subsidiaries that have not guaranteed the notes. | |||

4

At June 30, 2003, as adjusted to give effect to the offerings of the old notes and the application of proceeds therefrom as described in "Recent Developments" the notes and the guarantees would have effectively been junior to: | ||||

• | $32.5 million of borrowings, hedging obligations and reimbursement obligations in respect of letters of credit issued under our credit facility; and | |||

• | $9.7 million of liabilities, including trade payables but excluding intercompany obligations, of our non-guarantor subsidiaries. | |||

Optional Redemption | Floating rate notes: We may redeem any of the floating rate notes at any time on or after February 15, 2006, in whole or in part, in cash at the redemption prices described in this prospectus, plus accrued and unpaid interest to the date of redemption. | |||

Fixed rate notes: We may redeem any of the fixed rate notes at any time on or after February 15, 2008, in whole or in part, in cash at the redemption prices described in this prospectus, plus accrued and unpaid interest to the date of redemption. | ||||

In addition, on or before February 15, 2006, in the case of the floating rate notes, and August 15, 2006, in the case of the fixed rate notes, we may redeem up to 35% of the aggregate principal amount of notes of each series originally issued at a redemption price of 100% plus the then applicable interest rate (in the case of the floating rate notes) or 110.75% (in the case of the fixed rate notes) with the proceeds of equity offerings within 90 days of the closing of an equity offering. We may make that redemption only if, after the redemption, at least 65% of the aggregate principal amount of notes originally issued remain outstanding. | ||||

Change of Control | Upon a change of control, as defined in "Description of Notes," we will have the option, at any time prior to February 15, 2006, in the case of the floating rate notes, or February 15, 2008, in the case of the fixed rate notes, to redeem all of the notes of each series at a redemption price equal to 100% of their principal amount plus an applicable premium as described in "Description of Notes," together with accrued and unpaid interest. If a change of control occurs and we do not exercise our option to redeem the notes, we will be required to make an offer to purchase the notes of each series. The purchase price will equal 101% of the principal amount of the notes on the date of purchase, plus accrued and unpaid interest to the date of repurchase. | |||

Subsidiary Guarantees | The notes will be jointly and severally guaranteed on a senior secured basis by all of our existing domestic restricted subsidiaries. In addition, all future wholly-owned domestic restricted subsidiaries, and any future domestic restricted subsidiaries that guarantee our senior subordinated notes, will be required to guarantee the notes. | |||

5

Certain Covenants | The terms of the notes will restrict our ability and the ability of our restricted subsidiaries to: | |||

• | incur additional indebtedness; | |||

• | create liens; | |||

• | engage in sale-leaseback transactions; | |||

• | pay dividends or make other equity distributions; | |||

• | purchase or redeem capital stock; | |||

• | make investments; | |||

• | sell assets; | |||

• | engage in transactions with affiliates; or | |||

• | effect a consolidation or merger. | |||

However, these limitations will be subject to a number of important qualifications and exceptions. In particular, many of our joint ventures are not "subsidiaries" under the existing indenture, although they are consolidated subsidiaries for accounting purposes. | ||||

Use of Proceeds | We will not receive any proceeds from the issuance of the new notes in the exchange offer. | |||

See "Risk Factors" immediately following this summary for a discussion of certain risks relating to an investment in the notes.

6

Overview

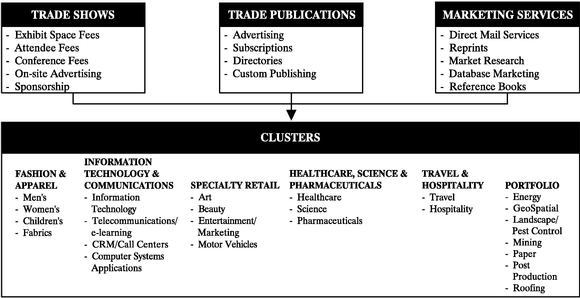

We are a leading worldwide provider of integrated B-to-B marketing communications products and services for targeted industry sectors, principally through trade shows and conferences and through controlled circulation trade, business and professional magazines. We also provide a broad range of other marketing services products, including classified advertising, direct mail services, reprints, database marketing, directories, guides and reference books. We are one of the largest trade show operators in the United States based on total square footage and number of shows in 2002 and one of the largest B-to-B trade publishers in the United States as measured by advertising pages in 2002.

Products and Services

We offer our customers a comprehensive array of B-to-B communications products and services to reach their existing and prospective buyers on a cost-effective basis.

Trade Shows

As of June 30, 2003, we owned and managed 68 trade shows and nine stand-alone conferences for business, professional and consumer audiences worldwide, most of which were among the leading events in their respective markets based on square footage. Our trade show revenue is derived primarily from the sale of trade show floor space to exhibitors, show-specific advertising, sponsorships and conferences. Trade show revenue accounted for approximately 53%, 54% and 52% of our revenue in 2000, 2001 and 2002, respectively, and 57% in each of the six months ended June 30, 2002 and June 30, 2003. See "The Acquisition."

Trade Publications

As of June 30, 2003, we published 68 specialized business magazines and professional journals and 32 directories and other publications. Of our 60 magazines and journals for which competitive data is available, 70% ranked either #1 or #2 in their respective markets, based on the number of advertising pages in the twelve months ended May 31, 2003. Our publications are generally distributed free-of-charge to qualified professional recipients and generate revenues predominantly from advertising. Trade publications revenue accounted for approximately 42%, 41% and 43% of our total revenue in 2000, 2001 and 2002 and 38% and 39% of our revenue in the six months ended June 30, 2002 and June 30, 2003, respectively.

Marketing Services

Within each industry cluster, we provide a comprehensive set of marketing communications products, services and support geared to the particular industry's marketing and customer needs. These services include direct mail and database marketing programs, reprint services, reference books and other services to facilitate our clients' B-to-B marketing and communications programs. Marketing services revenue accounted for approximately 5% of our revenue in 2000 and 5% of our revenue in each of 2001 and 2002 and 5% and 4% of our revenue in the six months ended June 30, 2002 and June 30, 2003, respectively.

Internet

In addition, we work with Advanstar.com, a subsidiary of our parent but not an obligor of the notes, to use Internet based products and services to complement our delivery of trade show, publishing and marketing services products to our customers. We also use the Internet as a cost-effective method of developing qualifying magazine circulation and to register trade show and conference attendees. We

7

intend to integrate Advanstar.com into our core operations, at which point it would become part of Advanstar Communications. Such integration is not expected to have a material effect on our future results of operations or financial condition. See "Certain Relationships and Related Party Transactions—Relationship with Advanstar.com."

Industry Clusters

We also operate our business by targeting a number of industry sectors in North America, Latin America, Europe and Asia through certain niche markets grouped together in five core clusters. In addition to our five core clusters, we have grouped the industry sectors in which we provide products and services but do not have a significant industry presence into a "Portfolio" cluster. We believe that by focusing on industries, we better identify the broad array of our customers' B-to-B marketing communications needs which our products and services can meet. In addition, we believe our industry focus allows us to cross-sell our products and services effectively and to capture a larger share of our customers' marketing budgets. In each of our niche markets, many of the same customers advertise in our publications, exhibit at our trade shows and use our marketing services to reach their buyers. We have expanded our trade show, conference and publication offerings within each cluster through new product introductions and strategic acquisitions, which we believe maximizes our existing marketing and customer service infrastructure and industry expertise. We believe that our total cluster participants, including readers, attendees, conferees, exhibitors, advertisers, and other customers, number approximately 3.0 million.

Industry Overview

B-to-B communications companies provide marketing solutions through trade shows and conferences, trade publications, ancillary marketing services and through Internet applications. According to the July 2002 Veronis Suhler StevensonCommunications Industry Forecast, the communications industry was the third fastest growing sector of the U.S. economy from 1996 to 2001, expanding at a compound annual growth rate, or CAGR, of 6.5%. Total spending on B-to-B communications increased from $17.6 billion to $21.0 billion from 1996 to 2001, which represents a CAGR of 3.6% during that period. According to the Veronis Suhler Stevenson report, total spending on U.S. trade shows and conferences amounted to $8.1 billion in 2001, a decline of 3.2% from 2000 and a CAGR of 3.7% over the period from 1996 to 2001. The U.S. B-to-B publishing industry generated revenue of $13.0 billion in 2001 according to Veronis Suhler Stevenson, and grew at a CAGR of 3.5% from 1996 to 2001.

In 2001, the B-to-B marketing and advertising market experienced its most significant downturn since 1990-1991 according to Veronis Suhler Stevenson. This downturn continued into 2002. Media advertising spending declined significantly as companies reduced their marketing expenditures in response to the economic slowdown. Industry-wide advertising pages, as measured by the Business Information Network, declined 19.7% in 2001 from 2000 levels and 15.0% in 2002 from 2001 levels. Trade show exhibition space and attendance were less severely impacted by the downturn in the B-to-B marketing and advertising market in the first half of 2001. After the events of September 11, 2001, however, trade show exhibition space and attendance suffered dramatically. As measured byTradeshow Week, fourth quarter 2001 trade show attendance and number of exhibitors declined approximately 20.4% and 6.8%, respectively, from the fourth quarter of 2000. The decline continued in 2002, with 2002 net square footage dropping 5.3% from 2001 figures. Attendance was down 2.2% over the same period.

Our results during 2002 and year-to-date in 2003 reflect the general economic slowdown in the United States as a result of decreased marketing and advertising expenditure by our customers. However, we believe that our balanced portfolio between trade shows and publications and our

8

diversification across many industry sectors has mitigated the overall impact from continued weakness in general economic conditions and reduces our exposure to the potential volatility of any one sector.

Competitive Strengths

We believe that the following factors contribute to our strong competitive position:

- •

- Market Leadership

- •

- Industry-Focused Integrated Marketing

- •

- Diverse Customer Base

- •

- Experienced and Motivated Management Team

See "Business—Competitive Strengths" for additional detail on these strengths.

Business Strategy

Our objective is to increase profitability by solidifying our position as a leading provider of comprehensive one stop B-to-B marketing communications products and services. In order to achieve this objective, we operate our business based on the following strategies:

- •

- Operate Leading Trade Shows and Publish Leading Magazines in Attractive Niche Markets

- •

- Utilize Industry Cluster Strategy to Drive Growth

- •

- Maximize Share of Customers' Total Marketing Expenditures

- •

- Launch New Products and Services Within Existing Clusters

- •

- Identify and Consummate Strategic Acquisitions

For additional detail on our Business Strategy see "Business—Business Strategy."

On August 18, 2003, we issued $130 million aggregate principal amount of second priority senior secured floating rate notes due 2008 and $230 million aggregate principal amount of 103/4% second priority senior secured notes due 2010 for net proceeds of approximately $350 million. We refer to this offering as the "August offering." These old notes were issued under an indenture dated August 18, 2003, which we refer to as the "indenture" or the "August indenture", among Advanstar, the guarantors party thereto and Wells Fargo Bank Minnesota, N.A., as trustee. Our net proceeds were approximately $350 million, after deduction of the initial purchasers' discounts and commissions and fees and expenses. We used these net proceeds to repay all outstanding Term A loans and all but $25 million of Term B loans under our credit facility, to repay a portion of our revolving credit borrowings and to pay related fees and expenses. In connection with this issuance of old notes we amended our credit facility to permit the offering and the use of the proceeds thereof, eliminate the leverage ratio covenant and amend certain other covenants contained in the credit facility and reduce the revolving loan commitments thereunder from $80 million to $60 million. We recorded an expense of $11.3 million in the third quarter of 2003 to reflect the write-off of deferred financing costs related to the term loans that were repaid and the reduction in revolving loan commitments.

On September 25, 2003, we issued $70 million aggregate principal amount of 103/4% second priority senior secured notes due 2010 for net proceeds of approximately $68 million, after deducting the initial purchaser's fee and other fees and expenses. We refer to this offering as the "September offering." The old notes issued in the September offering were issued under an indenture, which we refer to as the "September indenture," dated September 25, 2003 among Advanstar, the guarantors

9

party thereto and Wells Fargo Bank Minnesota, N.A., as trustee. The terms of the old 103/4% notes issued in the September offering are identical to the terms of the old 103/4% notes issued in the August offering except that the notes issued in the September offering contained a special redemption provision that would have required Advanstar to redeem these old notes if the Thomson acquisition (as described below) was not consummated prior to December 31, 2003. In addition, for purposes of all votes under the September indenture, other than votes requiring the consent of all holders, the 103/4% notes issued in the September offering are deemed to vote together as a class with the 103/4% notes issued in the August offering. New notes issued in the exchange offer will all be issued under the August indenture.

On October 1, 2003, we purchased a portfolio of healthcare industry-specific magazines and related custom project services from the Thomson Corporation and its subsidiaries, which we refer to as "Thomson," for $135 million in cash. We used a portion of the approximately $68 million in net proceeds of the September offering, $7 million of cash generated by operations, revolver borrowings of $13 million and proceeds of $60 million of equity contributions from Advanstar, Inc. ($50 million of which was received on the closing date of the September offering and $10 million of which was received on the closing date of the Thomson acquisition), which represent the proceeds from the sale by its parent company of equity to the DLJ Merchant Banking funds, to fund the acquisition and related fees and expenses. See "The Acquisition."

In this prospectus, we disclose certain financial information "as adjusted to give effect to the offerings of the old notes and the application of proceeds therefrom". Unless otherwise noted, this financial information has been adjusted to give effect to

(a) the August offering and the application of the net proceeds thereof,

(b) the September offering and the concurrent equity contribution of $50 million and the use of proceeds thereof, but

(c) has not been adjusted to give effect to the application of $136.0 million in cash to purchase Thomson's portfolio of healthcare industry-specific magazines and related custom project services and pay related fees and expenses.

10

The following table presents summary historical and other consolidated financial data for Advanstar and its predecessor for each of the periods indicated. The summary historical financial data for Advanstar's predecessor for the period January 1, 2000 through October 11, 2000 have been derived from the audited consolidated financial statements and the notes thereto of our predecessor for that period included herein. The summary historical financial data for Advanstar for the period October 12, 2000 through December 31, 2000 and for the years ended December 31, 2001 and 2002 have been derived from Advanstar's audited financial statements and the notes thereto included herein. The summary combined financial data for the combined year ended December 31, 2000 have been derived from the audited consolidated financial statements of the predecessor and Advanstar and the notes thereto but have not been audited and do not comply with generally accepted accounting principles. The summary historical financial data for Advanstar for the six months ended June 30, 2002 and 2003 have been derived from Advanstar's unaudited financial statements and the notes thereto included herein. The summary historical financial data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the consolidated financial statements and notes thereto included elsewhere in this prospectus.

| | Predecessor | Advanstar | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | For the period from January 1, 2000 through October 11, 2000 | For the period from October 12, 2000 through December 31, 2000 | | | | | | |||||||||||||||

| | | For the Year Ended December 31, | For the Six Months Ended June 30, | |||||||||||||||||||

| | Combined 2000 | |||||||||||||||||||||

| | 2001 | 2002 | 2002 | 2003 | ||||||||||||||||||

| | (dollars in thousands) | | (unaudited) | | | (unaudited) | ||||||||||||||||

| | | (dollars in thousands) | ||||||||||||||||||||

| Income Statement Data: | ||||||||||||||||||||||

| Net revenue | $ | 314,045 | $ | 63,434 | $ | 377,479 | $ | 346,997 | $ | 307,183 | $ | 172,720 | $ | 172,790 | ||||||||

| Cost of production and selling | 191,638 | 49,339 | 240,977 | 219,992 | 187,683 | 101,257 | 100,825 | |||||||||||||||

| General and administrative expenses | 32,981 | 7,740 | 40,721 | 35,697 | 35,027 | 19,243 | 17,813 | |||||||||||||||

| Stock option compensation expense (benefit) (1) | (2,485 | ) | — | (2,485 | ) | — | — | — | — | |||||||||||||

| Funding of Advanstar.com operations | — | — | — | — | 39,587 | 38,716 | 635 | |||||||||||||||

| Depreciation and amortization (2) | 39,653 | 15,747 | 55,400 | 94,261 | 69,132 | 33,477 | 26,527 | |||||||||||||||

| Operating income (loss) | 52,258 | (9,392 | ) | 42,866 | (2,953 | ) | (24,246 | ) | (19,973 | ) | 26,990 | |||||||||||

| Other income (expense): | ||||||||||||||||||||||

| Interest expense | (38,161 | ) | (13,765 | ) | (51,926 | ) | (55,499 | ) | (51,211 | ) | (25,926 | ) | (24,635 | ) | ||||||||

| Other income (expense), net | (2,394 | ) | 215 | (2,179 | ) | 788 | 2,931 | 2,258 | 308 | |||||||||||||

| Income (loss) before income taxes and minority interests | 11,703 | (22,942 | ) | (11,239 | ) | (57,664 | ) | (72,526 | ) | (43,641 | ) | 2,663 | ||||||||||

| Provision (benefit) for income taxes | 11,190 | (4,772 | ) | 6,418 | (11,166 | ) | (15,478 | ) | (8,072 | ) | 725 | |||||||||||

| Minority interests | (1,003 | ) | 125 | (878 | ) | (156 | ) | (474 | ) | (680 | ) | (542 | ) | |||||||||

| Income (loss) before extraordinary item and cumulative effect of accounting change. | $ | (490 | ) | $ | (18,045 | ) | $ | (18,535 | ) | $ | (46,654 | ) | $ | (57,522 | ) | $ | (36,249 | ) | $ | 1,396 | ||

Other Data: | ||||||||||||||||||||||

| Capital expenditures | $ | 11,882 | $ | 7,935 | $ | 7,216 | $ | 3,190 | $ | 3,001 | ||||||||||||

| Cash Flow from operating activities | $ | 39,948 | $ | (3,675 | ) | 36,273 | 41,813 | 24,275 | (178 | ) | 12,397 | |||||||||||

| Cash Flow from investing activities | (29,550 | ) | (22,395 | ) | (51,945 | ) | (41,733 | ) | (31,155 | ) | (16,458 | ) | (3,205 | ) | ||||||||

| Cash Flow from financing activities | (17,978 | ) | — | (17,978 | ) | 24,774 | (15,388 | ) | (14,988 | ) | (10,796 | ) | ||||||||||

| Ratio of earnings to fixed charges (3) | 1.3 | x | — | — | — | — | — | 1.1 | x | |||||||||||||

11

| | As of June 30, 2003 | ||||||

|---|---|---|---|---|---|---|---|

| | Historical | As Adjusted(4) | |||||

| | (unaudited) (in thousands) | ||||||

| Balance Sheet Data: | |||||||

| Cash and cash equivalents | $ | 17,986 | $ | 123,636 | |||

| Working capital (5) | (51,771 | ) | (51,771 | ) | |||

| Total assets | 848,218 | 955,149 | |||||

| Total senior secured debt | 387,400 | 455,000 | |||||

| Total debt | 550,800 | 618,400 | |||||

| Total stockholder's equity | 193,551 | 231,832 | |||||

- (1)

- We account for stock-based compensation using the intrinsic value method. As a result, for options that do not have fixed terms, we measure compensation cost as the difference between the exercise price of the options and the fair value of the shares underlying the options at the end of the period. Our results for the period January 1, 2000 through October 11, 2000 were favorably impacted by compensation benefits due to a decrease in the fair value of the shares underlying the options. Because we no longer maintain the variable plan that resulted in compensation cost (benefit) and we intend to issue options with fixed terms, we no longer expect to recognize compensation expense or benefit in future periods, unless changes in GAAP require otherwise.

- (2)

- Upon adoption of Statement of Financial Accounting Standards No. 142, "Goodwill and Other Intangible Assets," we discontinued the amortization of goodwill beginning on January 1, 2002. The following table represents a reconciliation of loss from continuing operations adjusted for the exclusion of goodwill amortization, net of tax:

| | Predecessor | Advanstar | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | For the period from January 1, 2000 through October 11, 2000 | For the period from October 12, 2000 through December 31, 2000 | | | | | | ||||||||||||||

| | | For the Year Ended December 31, | For the Six Months Ended June 30, | ||||||||||||||||||

| | Combined 2000 | ||||||||||||||||||||

| | 2001 | 2002 | 2002 | 2003 | |||||||||||||||||

| | (dollars in thousands) | | (unaudited) | | | (unaudited) | |||||||||||||||

| | | (dollars in thousands) | |||||||||||||||||||

| Reported loss from continuing operations | $ | (490 | ) | $ | (18,045 | ) | $ | (18,535 | ) | $ | (46,654 | ) | $ | (57,522 | ) | $ | (36,249 | ) | $ | 1,396 | |

| Add: goodwill amortization, net of tax | $ | 15,450 | $ | 7,308 | $ | 22,758 | $ | 22,738 | — | — | — | ||||||||||

| Adjusted income (loss) from continuing operations | $ | 14,960 | $ | (10,737 | ) | $ | 4,223 | $ | (23,916 | ) | $ | (57,522 | ) | $ | (36,249 | ) | $ | 1,396 | |||

- (3)

- For purposes of determining the ratio of earnings to fixed charges, earnings are defined as pretax income from continuing operations plus fixed charges, and fixed charges consist of interest expense and one-third of rental expense, which is considered representative of the interest component of rental expense. Earnings were insufficient to cover fixed charges in the years ended December 31, 1998, 1999, 2000, 2001, 2002 and the six months ended June 30, 2002 by $27.2 million, $12.0 million, $12.1 million, $57.8 million, $73.0 million and $44.3 million, respectively.

- (4)

- Adjusted to give effect to the offerings of the old notes and the application of the proceeds therefrom as described in "—Recent Developments."

- (5)

- Working capital is defined as current assets, excluding cash of $18.0 million less current liabilities, excluding the current portion of long-term debt of approximately $18.5 million.

12

In addition to the other matters described in this prospectus, you should carefully consider the following risk factors before making an investment in the notes.

We have a significant amount of debt, which could limit our ability to remain competitive or grow our business

As of June 30, 2003, as adjusted to give effect to the offerings of the old notes and the application of the proceeds therefrom, we would have had (a) total indebtedness of approximately $618.4 million and (b) approximately $57.9 million of borrowings available under our credit facility, subject to customary borrowing conditions. On October 1, 2003, we used $13 million of additional revolving credit borrowings to finance the Thomson acquisition and related fees and expenses. In addition, subject to the restrictions in our credit facility, the indenture and our other debt instruments, we may incur significant additional indebtedness from time to time. The level of our indebtedness may have important consequences, including:

- •

- limiting cash flow available for general corporate purposes, including capital expenditures and acquisitions, because a substantial portion of our cash flow from operations must be dedicated to servicing our debt;

- •

- limiting our ability to obtain additional debt financing in the future for working capital, capital expenditures or acquisitions;

- •

- limiting our flexibility in reacting to competitive and other changes in our industry and economic conditions generally; and

- •

- exposing us to risks inherent in interest rate fluctuations because some of our borrowings will be at variable rates of interest, which could result in higher interest expense in the event of increases in interest rates.

We may not be able to service our debt without the need for additional financing, which we may not be able to obtain on satisfactory terms, if at all

Our ability to pay or to refinance our indebtedness, including the notes, will depend upon our future operating performance, which will be affected by general economic, financial, competitive, legislative, regulatory, business and other factors beyond our control. We cannot assure you that our business will generate sufficient cash flow from operations, that currently anticipated revenue growth and operating improvements will be realized or that future borrowings will be available to us in amounts sufficient to enable us to pay our indebtedness, including the notes, or to fund our other liquidity needs. If we are unable to meet our debt service obligations or fund our other liquidity needs, we could attempt to restructure or refinance our indebtedness or seek additional equity capital. We cannot assure you that we will be able to accomplish those actions on satisfactory terms, if at all.

Our parent company will likely need to rely upon distributions from us to service its debt and we may not be able to make distributions in amounts sufficient to satisfy such debt service

In addition to our debt service needs, our parent company, Advanstar, Inc., will likely need to rely upon distributions from us to service its 15% Senior Discount Notes due 2011, which we refer to as "parent company notes", including for the payment of interest which must be paid in cash beginning April 15, 2006. Our ability to generate sufficient cash from operations to make distributions to Advanstar, Inc. will depend upon our future operating performance, which will be affected by general economic, financial, competitive, legislative, regulatory, business and other factors beyond our control.

13

In addition, our ability to make distributions to Advanstar, Inc. is subject to restrictions in our various debt instruments. For example, the notes and our senior subordinated notes limit the amount of "restricted payments," including dividends, that we can make. Generally, we can make dividends only if our leverage ratio (as defined) is 6.0 to 1 or better and only from the amount by which our cumulative EBITDA (as defined) since January 1, 2001 exceeds 150% of our cumulative interest expense in that same period. As described above, our ability to generate EBITDA will depend upon various factors that may be beyond our control. Our interest expense will increase as a result of this offering and, because a portion of our debt bears variable rates of interest, our interest expense could increase further in the future. We may not generate sufficient cash flow from operations or be permitted by the terms of our debt instruments to pay dividends or distributions to Advanstar, Inc. in amounts sufficient to allow it to pay cash interest on the parent company notes. If Advanstar, Inc. is unable to meet its debt service obligations, it could attempt to restructure or refinance its indebtedness or seek additional equity capital. We cannot assure you that Advanstar, Inc. will be able to accomplish these actions on satisfactory terms or at all. A default under the parent company notes could result in an acceleration of all outstanding loans under our credit facility which, in turn, would trigger a cross-default under both the notes and our senior subordinated notes. See "Description of Certain Indebtedness."

Restrictive covenants in our debt instruments may limit our ability to engage in a variety of transactions and could trigger defaults that would accelerate all of our debt

The indentures governing the notes contain various covenants that limit our ability to engage in a variety of transactions. In addition, our senior subordinated notes, the parent company notes and our credit facility contain other and more restrictive covenants. Our credit facility requires us to maintain a fixed charge coverage ratio (as defined). Our ability to meet such financial covenant can be affected by events beyond our control, and we cannot assure you that we will meet those tests. We have required amendments in the past to relax financial covenants contained in our credit facility. If not for the completion of the old notes offering in August 2003, management expects that Advanstar would have needed additional covenant or other relief in the future. We are substantially leveraged and our business remains subject to the same risks that created our historical liquidity and covenant concerns. A breach of any of these covenants or other provisions in the agreement governing the credit facility, our senior subordinated notes, the parent company notes and/or the notes could result in a default under our credit facility, our senior subordinated notes, the parent company notes, and/or the notes. Upon the occurrence of an event of default under our credit facility, the lenders could elect to declare all amounts outstanding under our credit facility to be immediately due and payable and terminate all commitments to extend further credit. If we were unable to repay those amounts, the lenders could proceed against the collateral granted to them to secure that indebtedness. We have pledged substantially all of our assets, other than assets of our foreign subsidiaries, as security under our credit facility on a first-priority basis. If the lenders under our credit facility accelerate the repayment of borrowings, we cannot assure you that we will have sufficient assets to repay our credit facility and our other indebtedness, including the notes.

Risks Relating to Our Business

Trade show exhibit space and ad pages declined significantly in 2001, 2002 and the first half of 2003 as a result of the economic slowdown in the United States and the September 11, 2001 terrorist attacks, and this trend may continue

Our customers typically reduce their marketing and advertising budgets during a general economic downturn or a recession in the United States or in any other market where we conduct a significant amount of business. The longer a recession or economic downturn continues, the more likely it becomes that our customers may significantly reduce their marketing and advertising budgets. Any material decrease in marketing budgets could reduce the demand for exhibition space and also reduce

14

attendance at our trade shows and conferences. In addition, any material decrease in advertising budgets could reduce the demand for advertising space in our publications. As a result, our revenue and our cash flow from operations could decrease significantly. In addition, our integrated marketing strategy could be materially adversely affected if advertising revenue cannot support one or more of our important publications or if declines in our customers' marketing and advertising budgets require us to discontinue one or more of our important trade shows or conferences.

Our business and results of operations in 2001, 2002 and the first half of 2003 were significantly impacted by the downturn in the U.S. economy, particularly in our Information Technology & Communications cluster and Travel & Hospitality cluster, which together accounted for approximately 23.7% of our revenue in 2002 and 16.3% of our contribution margin. Our future results will continue to be affected if the economic slowdown continues. We expect any improvement in the performance of our trade shows and conferences to lag behind any general economic recovery, just as it lagged behind the downturn in the economy going into the recession beginning in late 2000. The events of September 11, 2001 also significantly impacted our results in those periods, including cancellations in ad pages, particularly in our travel industry publications, and cancellations of exhibitor participation in several of our events in the quarters following September 11, 2001.

It is unclear what the continuing impact of the September 11, 2001 terrorist attacks will have on our future results of operations and financial condition, in relationship to the impact arising from the current economic slowdown. However, further terrorist attacks and continued geopolitical concern (including conflict in the Middle East) may significantly affect our future results of operations or financial condition, whether as a result of (1) reduced attendance at, or curtailment or cancellation of, trade shows due to travel fears, (2) further reduction in economic activity and a related reduction in marketing expenditures on publications or trade shows, or (3) other circumstances that could result from these or subsequent attacks.

We depend on securing desirable dates and locations for our trade shows and conferences, which we may not be able to secure

The date and location of a trade show or a conference can impact its profitability and prospects. The market for desirable dates and locations is highly competitive. If we cannot secure desirable dates and locations for our trade shows and conferences, their profitability and future prospects would suffer, and our financial condition and results of operations would be materially adversely affected. In general, we maintain multi-year reservations for our trade shows and conferences. Consistent with industry practice, we do not pay for these reservations, and these reservations are not binding on the facility owners until we execute a contract with the owner. We typically sign contracts that guarantee the right to venues or dates for only one year. Therefore, our multi-year reservations may not lead to binding contracts with facility owners. In addition, because trade shows and conferences are held on pre-scheduled dates at specific locations, the success of a particular trade show or conference depends upon events outside of our control, such as natural catastrophes, labor strikes and transportation shutdowns.

A significant portion of our revenue and contribution before general and administrative expenses is generated from our MAGIC trade shows, so any decline in the performance of these shows would reduce our revenues and operating income

For the year ended December 31, 2002 and the six months ended June 30, 2003, our MAGIC trade shows represented approximately 20% and 18.2% of our total revenue, respectively, and approximately 34% and 29.0% of contribution margin (defined as net revenue less cost of production and selling, editorial and circulation costs), respectively. We expect that the MAGIC trade shows will continue to represent a significant portion of our overall revenue and contribution margin in the future. Therefore, a significant decline in the performance of one or both of the MAGIC trade shows, typically

15

held in the first and third quarters, could have a material adverse effect on our financial condition and results of operations. For example, MAGIC trade shows' performance in 2002 was adversely affected by a difficult apparel market (which has also affected our other apparel and fashion shows) and the effects of the September 11 events, particularly on our February 2002 show.

As a result of the Thomson acquisition, we will derive significant revenue from our healthcare cluster, which is dependent upon pharmaceutical marketing budgets

As a result of the Thomson acquisition we expect to have an increase in the percentage of revenues from our healthcare cluster which accounted for 7% of our revenues in 2002. A substantial portion of the advertising in the healthcare cluster is by pharmaceutical companies. As a result, any material reduction in marketing activities by pharmaceutical companies, which could occur due to general economic conditions or factors specific to the industry, including a continued reduction in new drug introductions, a shift in marketing expenditures by pharmaceutical companies to sources other than publications (which shift has occurred to some extent in the last several years) and any future governmental regulation such as price controls or types of advertising restrictions, could have a material adverse effect on our results.

Any significant increase in paper or postage costs would cause our expenses to increase significantly

Because of our print products, direct mail solicitations and product distributions, we incur substantial costs for paper and postage. We do not use forward contracts to purchase paper, and therefore are not protected against fluctuations in paper prices. In general, we use the U.S. Postal Service to distribute our print products and mailings. U.S. Postal Service rates increase periodically. If we cannot pass increased paper and postage costs through to our customers, our financial condition and results of operations could be materially adversely affected.

The market for our products and services is intensely competitive

The market for our products and services is intensely competitive. The competition is highly fragmented by product offering and by geography. On a global level, larger international firms operate in many geographic markets and have broad product offerings in trade shows, conferences, publications and marketing services. In several industries, such as information technology and healthcare, we compete with large firms with a single-industry focus. Many of these large international and single-industry firms are better capitalized than we are and have substantially greater financial and other resources than we do.

Within each particular industry sector, we also compete with a large number of small to medium-sized firms. While most small to medium-sized firms operate in a single geographic market, in some cases, our competitors operate in several geographic markets. Our trade shows and conferences compete with trade associations and, in several international markets, with exposition hall owners and operators. Our publications typically have between two and five direct competitors that target the same industry sector, and we also have many indirect competitors that define niche markets differently than we do and thus may provide alternatives for readers and/or advertisers.

We depend in part on new product introductions, and the process of researching, developing, launching and establishing profitability for a new event or publication is inherently risky and costly

Our success depends in part upon our ability to monitor rapidly changing market trends and to adapt our events and publications to meet the evolving needs of existing and emerging target audiences. Our future success will depend in part on our ability to continue to adapt our existing events and publications and to offer new events and publications by addressing the needs of specific audience groups within our target markets. The process of researching, developing, launching and establishing

16

profitability for a new event or publication is inherently risky and costly. We generally incur initial operating losses when we introduce new events and publications. Our efforts to introduce new events or publications may not ultimately be successful or profitable. In addition, costs related to the development of new events and publications are accounted for as expenses, so our year-to-year results may be materially adversely affected by the number and timing of new product launches.

Our growth strategy of identifying and consummating acquisitions entails integration and financing risk

We intend to continue to grow in part through strategic acquisitions and joint ventures. This growth strategy entails risks inherent in identifying desirable acquisition candidates, in integrating the operations of acquired businesses into our existing operations and risks relating to potential unknown liabilities associated with acquired businesses. In addition, we may not be able to finance the acquisition of a desirable candidate or to pay as much as our competitors because of our leveraged financial condition or general economic conditions. Difficulties that we may encounter in integrating the operations of acquired businesses, including the asset portfolio we purchased from Thomson, could have a material adverse effect on our results of operations and financial condition. Moreover, we may not realize any of the anticipated benefits of an acquisition, and integration costs may exceed anticipated amounts. For example, we expect synergies in connection with the Thomson acquisition but we may not be able to achieve them. In addition, while we believe that we will be able to stop the recent decline in operating results of the assets acquired from Thomson, we may not be able to do so, which could substantially reduce the benefits of the Thomson acquisition and have a material adverse effect on our expected results of operations and financial condition.

We depend on our senior management team, and we do not have employment contracts for many of our senior managers

We benefit substantially from the leadership and experience of members of our senior management team and depend on their continued services to successfully implement our business strategy. The loss of any member of our senior management team or other key employee could materially adversely affect our financial condition and results of operations. Although we have entered into employment agreements with Mr. Krakoff, Mr. Alic and Mr. Loggia, we do not have employment contracts with most other members of our senior management team or other key employees. We have entered into a new contract with Mr. Krakoff that expires in December 2005. Mr. Krakoff's new contract provides that he will continue as Chairman and Chief Executive Officer until December 31, 2003, following which time, he will continue as executive chairman of the board until December 31, 2005. We are currently under discussions with Mr. Loggia with respect to a new employment contract pursuant to which Mr. Loggia would succeed to the position of chief executive officer. We cannot assure you that we will be able to complete Mr. Loggia's contract renewal on terms satisfactory to the company and Mr. Loggia, or at all. We cannot be certain that we will continue to retain the executives' services, or the services of other key personnel, in the future. Moreover, we may not be able to attract and retain other qualified personnel in the future. We do not currently maintain key-man life insurance policies on any member of our senior management team or other key employees.

Our international operations and expansion strategy exposes us to various risks associated with international operations

Our growth strategy includes expanding our product and service offerings internationally. We currently maintain offices in Brazil, the United Kingdom, Germany and Hong Kong and also hold an important show in France. International operations accounted for approximately 10% of our total revenue in 2002. International operations and expansion involve numerous risks, such as:

- •

- the uncertainty of product acceptance by different cultures;

17

- •

- divergent business expectations or cultural incompatibility in establishing joint ventures with foreign partners;

- •

- difficulties in staffing and managing multinational operations;

- •

- currency fluctuations;

- •

- state-imposed restrictions on the repatriation of funds; and

- •

- potentially adverse tax consequences.

The impact of any of these risks could materially adversely affect our future international operations and our financial condition and results of operations.

Current geopolitical conditions and the continuing threat of domestic and international terrorist attacks may adversely impact our results

International geopolitical conditions, exacerbated by the war in Iraq and the escalating tensions elsewhere have contributed to an uncertain political and economic climate, both in the United States and globally, which may affect our ability to generate revenue on a predictable basis. In particular, our travel publications and trade shows remain sensitive to cutbacks in destination and vacation travel trade advertising in response to concerns over terrorism and possible further conflicts in the Middle East and in other regions of the world. In addition, terrorist attacks internationally and the threat of future terrorist attacks both domestically and internationally have negatively impacted an already weakened worldwide economy. Customers are deferring and may continue to defer or reconsider purchasing our products and services as a result of these factors. Accordingly, adverse impacts on our business due to these factors could continue or worsen for an unknown period of time.

We have some exposure to fluctuations in the exchange rates of international currencies

Our consolidated financial statements are prepared in U.S. dollars. However, a portion of our revenues, expenses, assets and liabilities is denominated in currencies other than the U.S. dollar, including the British Pound Sterling, the euro and the Brazilian Real. Consequently, fluctuations in exchange rates could result in exchange losses. In 2000, 2001, 2002 and the first half of 2003, there was no material effect on our net income due to currency fluctuations, but the impact of future exchange rate fluctuations on our results of operations cannot be accurately predicted. Moreover, because we intend to continue our international expansion, the effect of exchange rate fluctuations could be greater in the future. We have previously undertaken, and in the future may undertake, transactions to hedge the risks associated with fluctuations in exchange rates of other currencies to the dollar. We do not know if any hedging techniques that we may implement will be successful or will mitigate the effect, if any, of exchange rate fluctuations on our financial condition and results of operations.

Our business is seasonal due largely to higher trade show revenue in the first and third quarters

Our business is seasonal, with revenue typically reaching its highest levels during the first and third quarters of each calendar year, largely due to the timing of the MAGIC trade shows and our other large trade shows and conferences. In 2002, approximately 36% of our revenue was generated during the first quarter and approximately 27% during the third quarter. The second quarter accounted for approximately 20% of revenue in 2002 and the fourth quarter accounted for approximately 17% of revenue in 2002. Because event revenue is recognized when a particular event is held, we may also experience fluctuations in quarterly revenue based on the movement of annual trade show dates from one quarter to another.

18

Risks Related to Our Stockholders

We are controlled by principal stockholders whose interests may differ from your interests

Circumstances may occur in which the interests of our principal stockholders could be in conflict with your interests. In addition, these stockholders may have an interest in pursuing transactions that, in their judgment, enhance the value of their equity investment in our company, even though those transactions may involve risks to you as a holder of the notes.

Substantially all of the outstanding shares of common stock of our ultimate parent company are held by the DLJ Merchant Banking funds. As a result of their stock ownership, the DLJ Merchant Banking funds control us and have the power to elect a majority of our directors, appoint new management and approve any action requiring the approval of the holders of common stock, including adopting amendments to our certificate of incorporation and approving acquisitions or sales of all or substantially all of our assets. The directors elected by the DLJ Merchant Banking funds have the ability to control decisions affecting our capital structure, including the issuance of additional capital stock, the implementation of stock repurchase programs and the declaration of dividends.

The general partners of each of the DLJ Merchant Banking funds are affiliates or employees of Credit Suisse First Boston LLC, which is also an affiliate of (1) Credit Suisse First Boston, the arranger, syndication agent and a lender under our credit facility, to which we have obtained amendments in the past to avoid future potential covenant defaults, and (2) the general partners of each of the DLJ Investment Partners funds, which own a substantial portion of the parent Company notes.

The security for your benefit can be released without your consent, and the lenders under our credit facility will have control over all decisions with respect to enforcement of the security interests, including decisions regarding whether and when to foreclose upon assets

The liens for the benefit of the notes may be released without your vote or consent:

- •

- The security documents generally provide for an automatic release of all liens on any asset that is disposed of in compliance with the provisions of the credit facility.

- •

- Any lien can be released if approved by the requisite number of lenders under our credit facility.

- •

- Except in limited circumstances, the administrative agent and Advanstar may amend the provisions of the security documents with the consent of the requisite number of lenders under our credit facility and without the consent of the holders of the notes, even if the amendment adversely affects the holders of the notes.

- •

- The notes will automatically cease to be secured by the liens if and when the liens no longer secure our credit facility.

As a result, we cannot assure you that the notes will continue to be secured by a substantial portion of our assets. You will have no recourse if the lenders under our credit facility approve the release of any or all the collateral, even if that release adversely affects the value or trading prices of the notes.

In addition, the lenders under our credit facility will have the sole ability to control remedies (including upon sale or liquidation of the collateral after acceleration of the notes or the debt under the credit facility) with respect to the collateral. These lenders may have different interests than the holders of the notes.

19

If there is a default, proceeds from sales of the collateral will be applied first to satisfy amounts owed under the credit facility, and the value of the collateral may not be sufficient to repay the holders of the notes

Advanstar and each guarantor will secure their obligations under the notes and the notes guaranteed by a second-priority lien on certain assets that are also pledged on a first-priority basis to the lenders under our credit facility. As a result, upon any foreclosure on the collateral, proceeds will be applied first to repay amounts owed under our credit facility, and only then to satisfy amounts owed to holders of the notes. The value of the collateral in the event of liquidation will depend on market and economic conditions, the availability of buyers and other factors. The proceeds from the sale or sales of all of such collateral may not be sufficient to satisfy the amounts due on the notes in the event of a default. If such proceeds were not sufficient to repay amounts due on the notes, then holders of the notes (to the extent not repaid from the proceeds of the sale of the collateral) would only have an unsecured claim against our remaining assets. The collateral has not been appraised in connection with this offering. As of June 30, 2003, the book value of the collateral was approximately $800 million, approximately $700 million of which consists of intangible assets, including $600 million of goodwill. Depending upon market and economic conditions and the availability of buyers, the sale value of the collateral may be substantially different from its book value.

Bankruptcy laws may limit your ability to realize value from the collateral

The right of the collateral agent to repossess and dispose of the pledged assets upon the occurrence of an event of default under the indenture is likely to be significantly impaired by applicable bankruptcy law if a bankruptcy case were to be commenced by or against us before the collateral agent repossessed and disposed of the collateral. Under U.S. bankruptcy laws, a secured creditor is prohibited from repossessing its collateral from a debtor in a bankruptcy case, or from disposing of collateral repossessed from such debtor, without bankruptcy court approval. Moreover, the bankruptcy code permits the debtor to continue to retain and to use collateral even though the debtor is in default under the applicable debt instruments, provided that the secured creditor is given "adequate protection." The meaning of the term "adequate protection" may vary according to circumstances, but it is intended in general to protect the value of the secured creditor's interest in the collateral and may include cash payments or the granting of additional security, if and at such times as the court in its discretion determines, for any diminution in the value of the collateral as a result of the stay of repossession or disposition or any use of the collateral by the debtor during the pendency of the bankruptcy case. Generally, adequate protection payments, in the form of interest or otherwise, are not required to be paid by a debtor to a secured creditor unless the bankruptcy court determines that the value of the secured creditor's interest in the collateral is declining during the pendency of the bankruptcy case. In view of the lack of a precise definition of the term "adequate protection" and the broad discretionary powers of a bankruptcy court, it is impossible to predict (1) how long payments under the notes could be delayed following commencement of a bankruptcy case, (2) whether or when the collateral agent could repossess or dispose of the pledged assets or (3) whether or to what extent holders of the notes would be compensated for any delay in payment or loss of value of the pledged assets through the requirement of "adequate protection." Under the intercreditor agreement executed in connection with the issuance of the old notes, the trustee and the holders of the notes (except in certain specified circumstances) waived their right to request or require "adequate protection" in connection with the provision by the lenders under our credit facility of any debtor in possession financing in any bankruptcy case in which we are a debtor.

20

The notes and the guarantees will effectively rank junior or pari passu to a substantial amount of obligations

The notes and the guarantees will effectively rank junior to debt under our credit facility with respect to the collateral

The notes effectively rank junior to all amounts owed under our credit facility to the extent of the value of the collateral, as the credit facility is secured by a first-priority lien on the collateral pledged for the benefit of the notes. In addition, the credit facility is secured by liens on certain other collateral not pledged for the benefit of the holders, including a pledge by our parent company of its assets (including our capital stock owned by it) and a pledge by us and each guarantor of the capital stock of certain of our respective subsidiaries. As a result, the lenders under the credit facility will be paid in full from the proceeds of the collateral pledged to them before you are paid from such proceeds. In addition, subject to the restrictions contained in the indenture, we may incur additional debt that is secured by first-priority liens on the collateral or by liens on assets that are not pledged to the holders of notes, all of which would effectively rank senior to the notes to the extent of the value of the assets securing such debt. At June 30, 2003, as adjusted to give effect to the offerings of the old notes and the application of the proceeds therefrom, the notes and guarantees would have ranked junior to $32.5 million of indebtedness, hedging obligations and reimbursement obligations in respect of letters of credit issued under our credit facility.