Exhibit 3

December 7, 2022

Bogotá D.C.

Republic of Colombia

Ministry of Finance and Public Credit

Carrera 8, No. 6C-38, Piso 1

Bogotá D.C., Colombia

Ladies and Gentlemen:

In my capacity as Head of the Legal Affairs Group of the General Directorate of Public Credit and National Treasury of the Ministry of Finance and Public Credit of the Republic of Colombia (the “Republic”), and in connection with the Republic’s offering, pursuant to its registration statement under Schedule B of the United States Securities Act of 1933, as amended (the “Securities Act”), filed by the Republic with the United States Securities and Exchange Commission (the “Commission”) under Registration No. 333-253587, (the “Registration Statement”), of U.S.$ 1,624,241,000 aggregate principal amount of its 8.000% Global Bonds due 2033 (the “Securities”), I have reviewed the following documents:

(i) the Registration Statement and the related Prospectus dated April 15, 2021 included in the Registration Statement most recently filed with the Commission, as supplemented by the Prospectus Supplement dated November 28, 2022 relating to the Securities, as filed with the Commission pursuant to Rule 424(b)(5) under the Securities Act;

(ii) an executed copy of the Indenture, dated January 28, 2015, between the Republic and The Bank of New York Mellon, as amended and supplemented by the Supplemental Indenture thereto, dated as of September 8, 2015, and as further amended and supplemented from time to time (as amended and supplemented, the “Indenture”);

(iii) the global Securities dated December 7, 2022 in the aggregate principal amount of $1,624,241,000 executed by the Republic;

(iv) an executed copy of the Authorization Certificate dated December 7, 2022 pursuant to which the terms of the Securities were established;

1

(v) all relevant provisions of the Constitution of the Republic and the following acts, laws and decrees of the Republic, under which the issuance of the Securities has been authorized:

| (a) | The relevant portions of Law 80 of October 28, 1993 (a translation of which has been filed as part of Exhibit F to the Republic’s Registration Statement No. 333-13172 and incorporated herein by reference); |

| (b) | Article 16 of Law 185 of January 27, 1995 (a translation of which has been filed as part of Exhibit F to the Republic’s Registration Statement No. 333-13172 and incorporated herein by reference); |

| (c) | Article 13 of Law 533 of November 11, 1999 (a translation of which has been filed as part of Exhibit F to the Republic’s Registration Statement No. 333-13172 and incorporated herein by reference); |

| (d) | Law 781 of December 20, 2002 (a translation of which has been filed as part of Exhibit F to the Republic’s Registration Statement No. 333-109215 and incorporated herein by reference); |

| (e) | Law 1366 of December 21, 2009 (a translation of which has been filed as part of Exhibit 3 to Amendment No. 2 to the Republic’s Annual Report on Form 18-K for the fiscal year ended December 31, 2008 and incorporated herein by reference); |

| (f) | Law 1624 of April 29, 2013 (a translation of which has been filed as part of Exhibit 3 to Amendment No. 1 to the Republic’s Annual Report on Form 18-K for the fiscal year ended December 31, 2012 and incorporated herein by reference); |

| (g) | Decree No 1068 of May 26, 2015 (a summary of the material portion of which has been filed as part of Exhibit 3 of Amendment No. 1 to the Republic’s Annual Report on Form 18-K for the fiscal year ended December 31, 2014 and incorporated herein by reference); |

2

| (h) | Law 1771 of December 30, 2015, (a translation of which has been filed as Exhibit A to Exhibit 3 to Amendment No. 2 to the Republic’s Annual Report From 18-K for the fiscal year ended December 31, 2014); and |

| (i) | Law 2073 of December 31, 2020 (a translation of which has been filed as part of Exhibit 4 to Amendment No. 1 to the Republic’s Report on Form 18-K for the fiscal year ended December 31, 2019 and incorporated herein by reference). |

(vi) the following additional actions under which the issuance of the Securities has been authorized:

| (a) | CONPES Document No. 4043 DNP, MINHACIENDA, dated August 9, 2021 (a translation of which is attached as Exhibit A hereto); |

| (b) | Authorization by Act of the Interparliamentary Commission of Public Credit (Comisión Interparlamentaria de Crédito Público) adopted in its meetings held on December 9, 2021 (a translation of which is attached as Exhibit B hereto); and |

| (c) | Resolution No. 3184 of November 28, 2022 of the Ministry of Finance and Public Credit (a translation of which is attached as Exhibit C hereto). |

It is my opinion that under and with respect to the present laws of the Republic, the Securities have been duly authorized, executed and delivered by the Republic and, assuming due authentication thereof pursuant to the Indenture, constitute valid and legally binding obligations of the Republic.

I hereby consent to the filing of this opinion as an exhibit to the Republic’s Amendment No. 1 to its Annual Report on Form 18-K for its fiscal year ended December 31, 2021 and to the use of the name of the Head of the Legal Affairs Group of the General Directorate of Public Credit and National Treasury of the Ministry of Finance and Public Credit of the Republic under the caption “Validity of the Securities” in the Prospectuses and under the heading “General Information—Validity of the Bonds” in the Prospectus Supplements referred to above. In giving the foregoing consent, I do not thereby admit that I am in the category of persons whose consent is required under Section 7 of the Act or the rules and regulations of the Commission thereunder.

3

No opinion is expressed as to any law of any jurisdiction other than Colombia. With respect to the opinion set forth above, my opinion is limited to the laws of Colombia. In particular, to the extent that New York State or United States Federal law is relevant to the opinions expressed above, I have relied, without making any independent investigation, on the opinion of Arnold & Porter Kaye Scholer LLP, filed as an exhibit to Amendment No. 1 to the Republic’s Annual Report on Form 18-K for its fiscal year ended December 31, 2021. This opinion is specific as to the transactions and the documents referred to herein and is based upon the law as of the date hereof. My opinion is limited to that expressly set forth herein, and I express no opinions by implication.

| Very truly yours |

| /s/ Claudia Marcela Gomez Vásquez |

| Claudia Marcela Gomez Vásquez |

| Head of the Legal Affairs Group of the General Directorate of Public Credit and National Treasury of the |

| Ministry of Finance and Public Credit of the Republic of Colombia |

4

Exhibit A

|  |

National Council of Social and Political Economy

Republic of Colombia

Favorable Opinion to the Nation for the execution of transactions related to External Public Credit

to the refinancing and/or financing budget appropriations of the 2021 and 2022 terms up to U.S.

$5,500 million, or its equivalent amount in other currencies

Department of National Planning

Ministry of Finance and Public Credit

Approved version

Bogotá, D.C., August 9th, 2021

NATIONAL COUNCIL OF SOCIAL AND POLITICAL ECONOMY

CONPES

Iván Duque Márquez

President of the Republic

Marta Lucía Ramírez Blanco

Vice President of the Republic

| Daniel Palacios Martínez | Marta Lucía Ramírez Blanco | |

| Minister of Interior | Minister of Foreign Relations | |

| José Manuel Restrepo Abondano | Wilson Ruiz Orejuela | |

| Minister of Finance and Public Credit | Minister of Justice and Law | |

| Diego Andrés Molano Aponte | Rodolfo Enrique Zea Navarro | |

| Minister of National Defense | Minister of Farming and Rural Development | |

| Fernando Ruíz Gómez | Ángel Custodio Cabrera Báez | |

| Minister of Health and Social Protection | Minister of Labor | |

| Diego Mesa Puyo | María Ximena Lombaba Villalba | |

| Minister of Mines and Energy | Minister of Commerce, Industry and Tourism | |

| María Victoria Angulo González | Carlos Eduardo Correa Escaf | |

| Minister of National Education | Minister of Environment and Sustainable Development | |

| Jonathan Tybal Malagón González | Jaren Cecilia Abudinen Abuchaibe | |

| Minister of Housing, Cities and Territory | Minister of Information Technologies and communications | |

| Angela María Orozco Gómez | Angélica María Mayolo Obregón | |

| Minister of Transportation | Minister of Culture | |

| Guillermo Antonio Herrera Castaño | Tito José Crissien Borrero | |

| Minister of Sports | Minister of Science, Technology and Innovation | |

Alejandra Carolina Botero Barco

General Director of the National Planning Department

| Daniel Gómez Gaviria | Amparo García Montaña | |

| Sector Deputy General Director | Territorial Deputy General Director | |

Executive Summary

Pursuant the set forth in paragraph 2 of article 41, Law 80 of 19931 and articles 2.2.1.3.1, 2.2.1.3.2 and 2.2.1.6, Decree 1068 of 20152, through the present document submits for the consideration of the National Council of Social and Economic Policy (CONPES), the favorable opinion for the nation to contract transactions related to external public credit for the re-financing and/or financing of budget appropriations for the terms 2021 and 2022 up to the amount of U.S. $ 5,500 million, or its equivalent in other currencies.

The above mentioned is aimed to grant flexibility and room for maneuver for (i) the pre-financing and/or financing of the necessities of the terms 2021 and 2022; (ii) to obtain timely access to international capital markets; (iii) to obtain funding in favorable terms and conditions; (iv) to diversify the investor base; (v) to achieve the strategic objective of the building of liquid and efficient curves.

Having this flexibility is important for the nation to have the necessary resources to finance budget appropriations and comply with interests and amortizations payments for 2021 and 2022, in a changing international context with potential risks.

Classification: H63.

Key words: external bonds, financing, Nation, international, issuance, sovereign debt, debt service.

| 1 | Through which the General Statute for Public Administration Purchases was enacted. |

| 2 | Through which the Single Regulatory Decree for Finance and Public Credit Sector was enacted and that revoked Decrees 1497 of 2002 and 3160 of 2011. |

Table of Contents

1. INTRODUCTION | 1 | |||||

2. BACKGROUND | 2 | |||||

2.1. Issuances Global Bond 2032 and Global Bond 2042 | 2 | |||||

3. JUSTIFICATION: FUNDING NEEDS | 3 | |||||

4. MARKET CONTEXT | 6 | |||||

4.1. Global Macroeconomic Performance | 6 | |||||

4.2. United States of America | 12 | |||||

4.2.1. Macroeconomic Evolution | 12 | |||||

4.2.2. Monetary Policy and Interest Rates | 13 | |||||

4.2.3. Tax Policy | 18 | |||||

4.3. Euro Zone | 19 | |||||

4.3.1. Macroeconomic Evolution | 19 | |||||

4.3.2. Monetary Policy and Interest Rates | 21 | |||||

4.3.3. Tax Policy | 22 | |||||

4.4. Japan | 23 | |||||

4.4.1. Macroeconomic Evolution | 23 | |||||

4.4.2. Monetary Policy and Interest Rates | 24 | |||||

4.4.3. Tax Policy | 25 | |||||

4.5. Emerging Markets | 25 | |||||

4.5.1. Macroeconomic Evolution | 25 | |||||

4.5.2. Investments flow to emerging markets and market performance | 27 | |||||

4.6. Colombia | 29 | |||||

4.6.1. Macroeconomic Evolution | 29 | |||||

4.6.2. COVID-19 measures | 30 | |||||

4.6.3. Recent performance of Colombia in international markets | 34 | |||||

4.6.4. Issuance strategy | 38 | |||||

4.6.5. Thematic bonds | 43 | |||||

5. Objectives | 44 | |||||

6. Recommendations | 45 | |||||

| Bibliography | 46 | |||||

Graphic Index

Graphic 1. Changes in world growth expectations IMF

Graphic 2. Oil price yield

Graphic 3. Inflation and unemployment in the USA data

Graphic 4. FED’s intervention rate

Graphic 5. Forecast for FED’s reference rate by FED members

Graphic 6. Implicit probability of the FED’s reference rate

Graphic 7. 10-year US Treasury securities

Graphic 8. Forecast for the 10-year US Treasury securities

Graphic 9. Forecast for the 30-year US Treasury securities

Graphic 10. Euribor 6M and Germany’s reference 10-year bond yield

Graphic 11. Emerging Markets’ cash flow—International Bonds

Graphic 12. Colombia’s Cash Flow—Global bonds

Graphic 13. Emerging Market’s Bonds Index

Graphic 14. Colombia’s historical credit rating

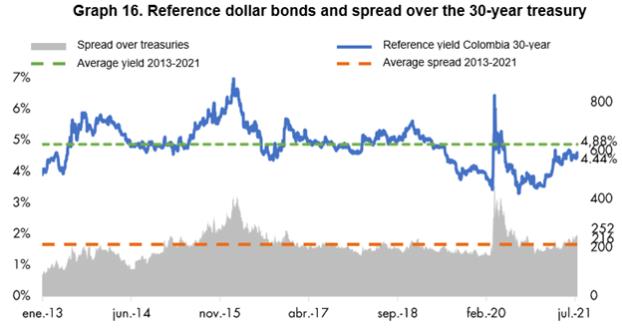

Graphic 15. Reference bonds in U.S. dollars and differential over 10-year Treasury

Graphic 16. Refence bons in U.S. dollars and differential over 30-year Treasury.

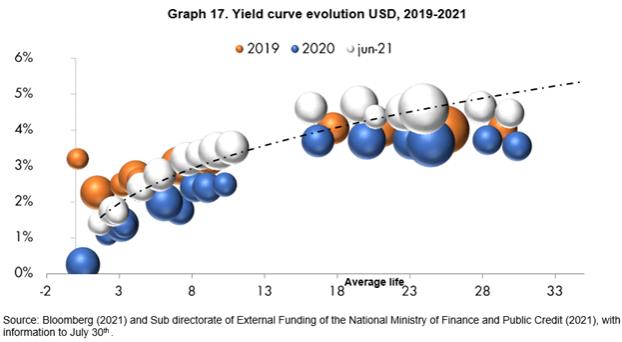

Graphic 17. U.S. dollar Yield Curve Evolution, 2019-2021.

Graphic 18. U.S. dollars LATAM 10-12 years issuances yield

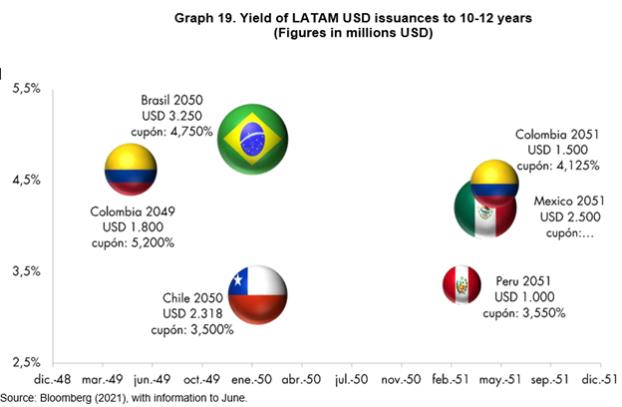

Graphic 19. U.S. dollars LATAM 30 years issuances yield

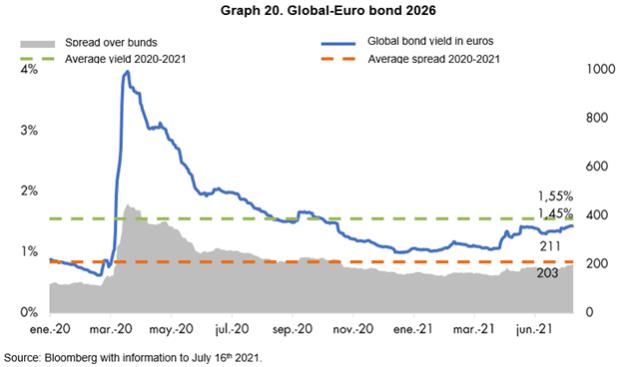

Graphic 20. Euro 2026—Global Bond

Graphic 21. 10 years Yen vs. Swap (LIBOR 6M) reference

Table Index

Table 1. Uses and Sources of the National Government 2021

Table 2. Uses and Sources of the National Government 2022

Table 3. Colombia Sovereign Ratings

| Acronyms and abbreviations | ||

| ECB | European Central Bank | |

| CONPES | National Council of Social and Economic Policy | |

| COVID-19 | Coronavirus 2019 disease | |

| DANE | National Statistic Administrative Department | |

| EGDMP | National Medium Term Debt management strategy | |

| EMBI | Emerging markets bond index | |

| EPFR | Emerging Portfolio Fund Research, Inc. | |

| EURIBOR | Euro Interbank Offered Rate | |

| FED | Federal Reserve | |

| IMF | International Monetary Fund | |

| FOMC | Federal Open Market Committee | |

| FOME | Fund for Emergencies Mitigation | |

| LIBOR | London Interbank Offered Rate | |

| OPEP | Organization of Petroleum Exporting Countries | |

| OPEP+ | Organization of Petroleum Exporting Countries and their allies | |

| PEPP | Pandemic Emergency Purchase Program—European Central Bank | |

| PIB | Gross Domestic Product | |

| S&P | Standard and Poor’s Global Ratings | |

| USD | U.S. Dollar | |

| WIT | West Texas Intermediate. | |

1. INTRODUCTION

The present document submits for the consideration of the National Council of Social and Economic Policy (CONPES), the favorable opinion for the nation to contract transactions related to external public credit for the prefinancing and/or financing of budget appropriations for the terms 2021 and 2022 up to the amount of U.S. $ 5,500 million, or its equivalent in other currencies. The aforementioned, pursuant paragraph 2, article 41, Law 80 of 19933 and articles 2.2.1.3.1, 2.2.1.3.2 and 2.2.1.6, Decree 1068 of 20154. In this way, having the required authorizations to access to different sources of funding, the Nation will be entitled to: (i) the prefinancing and/or financing of the necessities of the terms 2021 and 2022; (ii) to obtain timely access to international capital markets; (iii) to obtain funding in favorable terms and conditions; (iv) to diversify the investor base; (v) to achieve the strategic objective of the building of liquid and efficient curves. The present document is divided in principal sections, including this introduction. The second section presents the background, specifically, background related to issuances made by the Nation. Third section justify the need of prefinancing and/or financing for the 2021 and 2022 terms. Forth section presents the market context, particularly the behavior of the U.S., Eurozone, Japanese and emerging markets economies as well as the performance of Colombian economy. Fifth section presents the objectives to be achieved with the document and Sixth section presents recommendations to the CONPES.

| 3 | Through which the General Statute for Public Administration Purchases was enacted. |

Paragraph 2 of article 41 sets forth:

Public Credit Transactions. Notwithstanding the provisions of special laws, for the purposes of this law, it will be considered as “public credit transactions” to those whose purpose is to provide to an entity with resources with a term for its payment, among which are the contracting of loans, the issuance, subscription and placement of bonds and securities, supplier credits and the granting of guarantees for credit obligations in charge of governmental entities.

| (...) | For the management and execution of all external credit transactions and transactions similar to these of Governmental entities and for internal public credit transactions and transactions assimilated to these by part of the Nation and its decentralized entities, as well as for the granting of the guarantee of Nation, the authorization of the Ministry of Finance and Public Credit will be required, with prior favorable concepts from CONPES and the National Planning Department. |

| (...) | In any case, the external public credit transactions of the Nation and those guaranteed by it, with term of more than one year, required a prior favorable concept from the Inter-Parliamentary Commission of Public Credit. |

| (...) | The transactions referred to in this article and that are held to be executed abroad are submitted to the jurisdiction agreed in the contracts". |

| 4 | Through which the Single Regulatory Decree for Finance and Public Credit Sector was enacted and that revoked Decrees 1497 of 2002 and 3160 of 2011. |

Article 2.2.1.3.1. sets forth:

Public debt Securities. Public debt securities include bonds and other debt securities and with a term for its redemption, issued by governmental entities. Public debt securities do not include securities issued by credit institutions, insurance companies and other financial entities of public nature character, in the ordinary course of its business. The placement of public debt securities will be subject to the general financial terms and conditions set forth by the Board of Directors of Banco de la República.

Article 2.2.1.3.2. establishes:

National Public Debt Securities. The issuance and placement of public debt securities in the name of the Nation will require authorization, issued by resolution of the Ministry of Finance and Public Credit, which may be granted once the following have been previously obtained: a) Favorable opinion of the National Council of Social and Economic Policy, CONPES; and, b) Concept of the Public Credit Commission in the case of external public debt securities with a term of more than one year.

Article 2.2.1 .6. sets forth:

Issuance of authorizations and concepts. To issue the corresponding concepts and authorizations, the CONPES, the National Planning Department and the Ministry of Finance and Public Credit will take into account, among others, the adequacy of the respective transactions to the Government's policy in matters of public credit and its conformity with the Macroeconomic Program and Financial Plan approved by the CONPES, and the Superior Council of Tax Policy, CONFIS. The concepts of CONPES and the National Planning Department Board, when there is room for them, will be issued over the technical, economic and social justification of the project, the execution capacity and the financial situation of the respective entity, its financing plan by sources of resources and its schedule of annual expenses.

1

2. Background

Through the document CONPES 4022, approved on February 3rd, 2021, the Nation received favorable opinion for the contracting of transactions related to external public credit to prefinance and/or finance budget appropriations for the terms 2021 and 2022 up to USD 4,000 million, or its equivalent in other currencies. Over this amount, the Nation executed an operation in the international capital markets to finance budget needs for the term 2021 for a total amount of USD 3,000 million, as detailed in Section 2.1, remaining an authorized and non-used amount of USD 1,000 million, or its equivalent in other currencies.

2.1. Global Bond 2032 and Global Bond 2042 Issuances

On April 19, 2021, the Nation issued a Global Bond due in April 2032 for an amount of USD 2,000 million, at a rate of 3,356% and with a coupon of 3,250%. Additionally, it issued the Global Bond due in February 2042, for an amount of USD 1,000 million, at a rate of 4,235% and with a coupon of 4,125%. These financing transactions, for a total amount of USD 3,000 million, is the biggest executed by the Nation through Global Bonds. Similarly, the issuance of the Bond due on 2042 represented the issuance of the first 20 years term Global Bond, strengthening the building of the USD Yield Curve and improving the maturity profile of the external public debt. Once finished the operation, remained an amount of USD 1,000 million, or its equivalent in other currencies, from the total amount approved on the Document CONPES 4022.

2

3. Funding Needs

The Nation has maintained a proactive management in order to ensure the necessary resources to meet the external debt service, looking the proper market windows and avoiding to access to international capital markets in contexts of high volatility, as the experienced from the third week of February and through March 2022 because of: (i) the uncertainty created by the dissemination of COVID-19 and its effects on the world economy; (ii) the international fall of oil prices in approximately 30%, after Saudi Arabia announced a raise in its production after the failure of negotiations for a cutout agreement among Russia and the OPEP to stabilize the oil crude market; and, (iii) the Pandemic Declaration of COVID-19 by the World Health Organization on March 11, 2020.

So far in 2021, the international advances in vaccination programs and the economic reactivation, have resulted in higher projections for economic growth, especially in the United States. The above, together with a reduction in the unemployment rate and an increase in inflation, have generated expectations about the withdrawal of monetary policy stimulus programs and, in consequence, in volatility in the rates of fixed income securities issued the United States (Treasuries).

Therefore, to maintain a proactive management for the obtaining of financial resources, is more important in the current market context, due to the expectations of changes in the monetary policy of the United States that affect the rates of financing for emerging economies, possible outbreaks of COVID-19 and its variants and the approximation of electoral periods in Latin America, which can generate uncertainty.

It is also important to mention that, in recent years, funding through external bonds has represented at least half of the financing needs of the Nation for which, in the current context, to have the proper authorizations of timely manner, provides the Nation with greater flexibility in its sources of financing and its margin of maneuver.

Considering the above, following we present tables of uses and sources for the 2021 and 2022, included both in the 2021 Medium-Term Fiscal Framework (Ministry of Finance and Public Credit, 2021 b). In this regard, it is important to mention that the Nation has made progress in achieving external debt disbursements for 2021 and that, in the case of external bonds, the remaining amount authorized on Document CONPES 4022 would reach to cover the disbursements projected for this source in the current fiscal period, in line with the table of uses and sources 2021. However, given the uncertainty regarding the evolution of the pandemic and its effects on the main economic and financial variables, the amount requested in this CONPES includes the term 2021 with the objective of having greater flexibility in the sources of financing. On the other hand, the requested amount seeks to meet the projected financing needs for the term 2022 through external bonds, as presented below.

3

In 2021, total external debt amortizations are estimated at USD 2,981 million, which are concentrated in the first six months of 2021, while external interests are projected at approximately USD 2,577 million, for a total external debt service of USD 5,558 million. Considering this together with the deficit to be financed for 95.7 49 billion pesos (8.6% of GDP), including optimization of assets as income, external financial annual needs were estimated at USD 10,110 million (Table 1).

National Government debt management during 2021 together with financing transactions destined to meet the needs of the uses and sources 2021, has allowed the Nation to improve its external debt profile and advance in the financing of the present fiscal term under favorable conditions.

4

Table 1. Sources and uses of the Central National Government 2021

(Figures In millions of USD and billions of pesos)

Sources | Column in millions of USD | Colombian Pesos 134,068 | Uses |

| Column in millions of USD | Colombian Pesos 134,068 | ||||||||||||||||

Disbursements | 91,634 | Deficit to be financed | 95,749 | |||||||||||||||||||

External | 10,110 | 36,302 | Of which | |||||||||||||||||||

Internal | 55,332 | Internal interests | 27,058 | |||||||||||||||||||

| External interests | 2,577 | 9,712 | ||||||||||||||||||||

|

|

|

| |||||||||||||||||||

Other resources | 9,773 | Amortizations | 18,928 | |||||||||||||||||||

|

| |||||||||||||||||||||

| External | 2,981 | 10,937 | ||||||||||||||||||||

| Internal | 7,991 | |||||||||||||||||||||

Sources | Column in millions of USD | Colombian Pesos 134,068 | Uses | Column in millions of USD | Colombian Pesos 134,068 | |||||||||||||

Payment of obligations (judgement, health, others) | 8,590 | |||||||||||||||||

|

|

|

| |||||||||||||||

Initial availability | 32,661 | Final availability | 10,800 | |||||||||||||||

Source: Medium-Term Fiscal Framework (2021).

Notes: Projected figures.

By 2022, total external debt amortizations amount to approximately to USD 1,009 million, which are distributed throughout the year with the amortization of multilateral loans, while external interests are projected in approximately USD 2,996 million, concentrated in the first seven months of the year, for a total external debt service for 2022 of USD 4,005 million.

Considering the above, and the projected deficit for the year 2022 that amounts to 83.57 4 billion pesos (7% of GDP), the annual external financing needs are projected at USD l0,500 million, as shown in Table 2, referred to uses and sources for the National Government in 2022 of the Medium-Term Fiscal Framework 2021, which will be reviewed and updated in the first months of 2022.

5

Table 2. Sources and uses of the Central National Government

2022

(figures in millions of USD and billions of pesos)

Source | Columns in millions of USD | Colombian Pesos 127,757 | Uses | Column in millions of USD | Colombian Pesos 127,757 | |||||||||||||

Disbursements | 102,195 | Deficit to be financed | 33.574 | 83,574 | ||||||||||||||

External | 10,500 | 39,312 | Of which | |||||||||||||||

Internos | 62,883 | Internal interests | 29,654 | |||||||||||||||

| �� | External interests |

| 2,996 |

|

| 11,635 |

| |||||||||||

Other resources | 14,763 | Amortizations | 27,773 | |||||||||||||||

|

|

|

|

|

| |||||||||||||

| External | 1,009 | 3,936 | ||||||||||||||||

| Internal | 23,837 | |||||||||||||||||

Payment of obligations (judgment, health, other) | 6,382 | |||||||||||||||||

|

|

|

| |||||||||||||||

Initial availability | 10,800 | Fin al availability | 10,028 | |||||||||||||||

|

|

|

| |||||||||||||||

Source: Medium-Term Fiscal Framework (2021).

Notes: Projected figures.

Thus, considering the importance of having flexibility in the sources of financing in the current period and to finance the needs for the period 2022 in a timely manner, it is important that the Nation have room to maneuver under the current international context for (i) the prefinancing and/or financing of the necessities of the terms 2021 and 2022; (ii) to obtain timely access to international capital markets; (iii) to obtain funding in favorable terms and conditions; (iv) to diversify the investor base; (v) to achieve the strategic objective of the building of liquid and efficient curves.

4. Market Context

4.1. Global Macroeconomic Performance

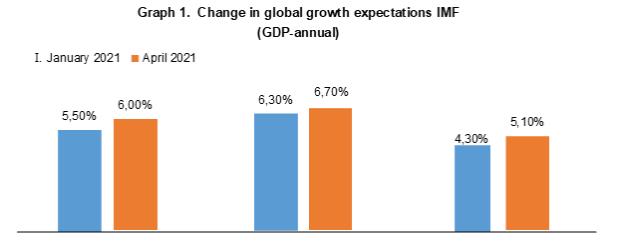

The IMF growth report from April 2021 projected an acceleration of 6.0% for the world economy in 2021, 6.7% for emerging economies and 5.1% for developed economies. The updating of the projections estimated in April by the IMF were 0.5 percentage points (p.p.) higher for the world economy, 0.4 p.p. for emerging economies and 0.8 p.p. for developed economies compared to the forecast made in January 2021, as evidenced in Graphic 1.

6

The upward revisions in global economic growth projections compared to the estimations made in January 2021 are due to fiscal support implemented in some economies and the expected recovery in the second half of the year thanks to global vaccination processes. However, the strength of the global economic recovery is subject to the trajectory of the health crisis, including the new variants of Covid-19, the effectiveness of measures taken to contain economic damage, the evolution of financial conditions and commodities prices, and the adjustability of each economy.

In developed economies, economic recovery projections vary between countries according to the evolution of the pandemic, the flexibility and adaptability of each economy to the reduction of mobility and structural trends and rigidities existing before the pandemic. On the other hand, the economic growth trajectory of emerging economies varies between regions depending on the severity of the pandemic, the economic structure of each country, exposure to specific shocks and the effectiveness of response policies aimed at combating the aftermath of the pandemic (International Monetary Fund, 2021).

As for the commodities market, in 2021 there has been a generalized increase led by energy raw materials following the development of COVID-19 vaccines and in an environment of global economic growth despite the resumption of lockdowns because of new COVID -19 outbreaks and variants in some countries. The IMF’s Primary Commodities Prices Index increased by 29% between August 2020 and February 2021 highlighting oil prices, coal prices -these stimulated by a strong demand from the steel and cement industry-, as well as base metal prices such as copper and iron driven by demand from the manufacturing and construction sectors of some developed economies (International Monetary Fund l, 2021).

7

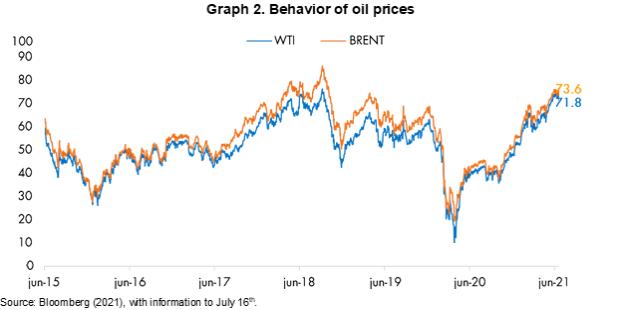

Specifically in the energy context, during 2020, COVID-19 affected oil prices, causing a historic suspension of economic activity, undermining demand through the mitigation and containment measures adopted to fight the pandemic (World Bank, 2020). As such, the disagreements around the supply of oil between Russia and OPEP and the announcement of Saudi Arabia to increase crude production at the beginning of March 2020 caused uncertainty in the markets before a possible oversupply of crude oil amid depressed global demand because of the pandemic (Reuters, 2020). This caused WTI and Brent to reach historical lows with some reference indices trading on negative levels such as WTI that reached prices of USD/b -37.6 in April 2020.

In the second half of 2020, OPEP began the dismantling of the restrictions on oil production agreed in the second half of the year by reducing the cuts from 9.6 daily million barrels (dmb) in July to 7.7 (dmb) in August as the demand recovered with the lifting of closures around the world (Reuters, 2020). However, COVID-19 outbreaks and weak global economic growth caused OPEP+ to extend restrictions on oil production until December 2020 (Organization of Petroleum Exporting Countries, 2020). During that year, WTI and Brent traded on average at $39.5/barrel and $43.0/barrel respectively.

On January 5, 2021, in the framework of the XIII ministerial meeting of OPEP and non-OPEP, the countries that are part of the Declaration of Cooperation (DoC) ratified the decision to voluntarily increase oil production from January 2021 by 0.5 (dmb) adjusting production cuts from 7.7 (dmb) to 7.2 (dmb) and recognized the need to gradually return 2 (dmb) to the market, at a pace determined by market conditions that does not exceed increases of the order of 0.5 (dmb) monthly (Organization of Petroleum Exporting Countries, 2021). In that sense, and after several months of discussions among OPEP+ members, on July 18, 2021 within the framework of the XIX OPEC and non-OPEC Ministerial Meeting, it was decided to increase oil production from August 2021 by 0.4 (dmb) to reach 2 (dmb) in December 2021, jointly, it was decided to extend the agreement until December 2022 and adjust, as of May of the same year, the basis for calculating production adjustments ( Organization of Oil Exporting Countries, 2021).

8

So far in 2021, WTI and Brent have traded on average at 62.2 USD/barrel and 65.3 USD/barrel respectively with an upward trend from January to mid-July of 50.8% and 44.0 %, respectively, reaching pre-pandemic levels (Graphic 2). However, there is uncertainty associated with: (i) the emergence of new variants of COVID-19 in the world and the impact they may have on growth world economic and global oil demand, and (ii) the possible rupture of OPEP agreements to increase production gradually, in a context of economic recovery and excess demand.

Under this scenario, Colombia must have the capacity to finance itself in the international capital markets, having the required authorizations, getting ahead of oil price drops that could occur before setbacks in the recovery of the global demand as consequence of new COVID-19 outbreaks, a high level of existences, or because of a progressive and accelerated dismantling of the production restrictions in the oil market.

COVID-19 Pandemic and its impact on the global economic activity and in the growth has had as consequence that central banks around the world play an important role in the current crisis through the implementation of new conventional and non-conventional instruments of monetary policy as part of a counter cyclic strategy called to the preservation of liquidity and promotion of credit. As example, the FED has implemented monetary policy tools aimed to keep the economy floating, composed by liquidity injection programs, the purchase of securities and the reduction of the FED interest rate (Federal Fund Rate) in 2020. The FED has decided to keep a monetary policy on an accommodative stance keeping unaltered the 0,25% rate, even after the strengthening of the economic activity indicators, of the employment and of the progress of the vaccination process in the USA (FED, 2021).

9

On other hand, the Bank of England (BoE) cut its rate through 2020, from 0.75% to 0,10% where is currently maintained and is assessing the possibility to implement negative rates after August 2021 if the prospects for inflation and production justify it. Similarly, the BoE continues its UK Government Bonds Purchase Program with a total stock purchase target equivalent to £875 billion; and the purchase of non-financial corporate bonds in pounds with investment grade, with a stock purchase target equivalent to £20 billion (Bank of England, 2021).

The European Central Bank (ECB), for its part, stated in the policy statement of June 2021 that it will continue with the implementation of measures that contribute to preserving favorable financing conditions for all sectors of the economy and that are necessary to achieve a sustained recovery of the economy and the safeguarding of price stability, given the uncertainty that persists in the short term associated with the evolution of the pandemic. In this way, it announced that it will continue with the program of asset purchase at a monthly rate of 20 billion euros and with the Pandemic Emergency Purchase Program of the European Central Bank (PEPP) amounting to €85 trillion, which will be maintained at least until the end of March 2022. In December, the ECB kept the euro zone’s bank deposit rate at 0.50% and the main refinancing rate at O%, in line with expectations of the market (European Central Bank, 2021).

Finally, in Asia, the Bank of Japan maintained, in its July 2021 meeting, its negative short-term interest rate at -0.0% and extended its asset and loan purchase programs until March 2022, with the aim of continuing to support financing, mainly from companies which have had economic pressures as a result of the pandemic and the new variants of COVID-19 (Bank of Japan, 2021).

In line with the monetary policy measures adopted to address the crisis, governments have implemented unprecedented fiscal stimulus measures to counter deteriorating macroeconomic conditions and mitigate the impact of COVID-19 on global economic activity. Fiscal support varies between economies depending on the impact of the pandemic, access to sources of financing under favorable conditions, and pre-crisis fiscal conditions. According to the IMF, fiscal support measures in response to the pandemic amounted to USD 16 trillion worldwide as of March 17, 2021, increasing the global fiscal deficit levels and public debt at unprecedented levels. World public debt ascended to 97.3% of GDP in 2020, while the average fiscal deficit as a percentage of GDP stood by 11.7% for developed economies, 9.8% for emerging economies and 5.5% for low-income developing countries (International Monetary Fund, 2021).

10

In 2020, the U.S. Congress passed four fiscal stimulus bills worth $2.9 trillion to strengthen the health care system, support small businesses through loans, subsidies and forgivable guarantees and to support the unemployed and vulnerable population of the country, among other measures (International Monetary Fund, 2021). Additionally, former President Donald Trump, signed into law a $900 billion aid and spending package to counter the effects of the pandemic, restoring unemployment benefits and avoiding a federal government shutdown. (Library of Congress Law, 2020). For its part, in March 2021, President Joe Biden signed into law the US Rescue Plan for USD l, 9 trillion aimed at households that have been financially impacted by the pandemic, funding testing, vaccine tracking and distribution, and allocating resources to state governments (Library of Congress).

For its part, to address the economic and social damage caused by COVID-19, the European Union approved in April 2020 a package of measures for 540,000 million of euros aimed at helping member states of the union, workers and companies. As such, the European Commission designed a recovery plan for Europe that includes 750,000 million euros, which represents a total of exceptional fiscal measures to address the crisis equivalent to 1.29 trillion euros (European Commission, 2020). According to the IMF, as of June 30, 2021, 24 member states of the union have submitted plans to access funds under the Recovery and Resilience Facility, of which 9 have been recommended for approval by part of the European Council (International Monetary Fund, 2021).

Finally, in Asia, Japan has approved three unprecedented fiscal stimulus packages, the first two for 117,1 trillion yen each and a third package worth 73.6 trillion yen. Fiscal protection measures include deliveries of money to people and enterprises affected by the pandemic, deferral of tax payments, loans on favorable terms by public and private financial institutions, labor subsidies and subsidies to affected enterprises (International Monetary Fund, 2021).

This global panorama shows the importance of having the authorizations to issue external debt securities, since there is no guarantee that the currently favorable conditions in terms of low financing rates will be maintained indefinitely and there is a high degree of uncertainty regarding: i) changes in monetary policy of developed economies, especially the beginning and the pace of the dismantling of the stimulus programs that caused an increase in reference rates (ii) the evolution of the pandemic in the coming months in the face of the development of new variants and possible scenarios of new outbreaks that may impact economic activity during 2021 and subsequent years, generating a widening of spreads; (iii) supply of and demand for commodities that may affect commodities prices and spreads in emerging countries; (iv) the expansion of the stimulus programs in the developed economies that could allow an accelerated economic recovery and therefore an increase in reference rates. Such scenarios may negatively affect conditions in fixed income financial markets, generating an increase in the cost of financing for emerging countries such as Colombia.

11

4.2. United States

4.2.1. Macroeconomic Evolution

During 2020, the U.S. economy grew at a negative rate of 3.5%, compared to 2.2% growth in 2019, which represents the largest contraction since the Great Depression in 1920. Although growth was affected globally by the COVID-19 pandemic, the impacts were heterogeneous in developed economies and developing economies according to the time of the isolation measures, which generated a strong shock on consumption, global demand and production (Bank of the Republic, 2021).

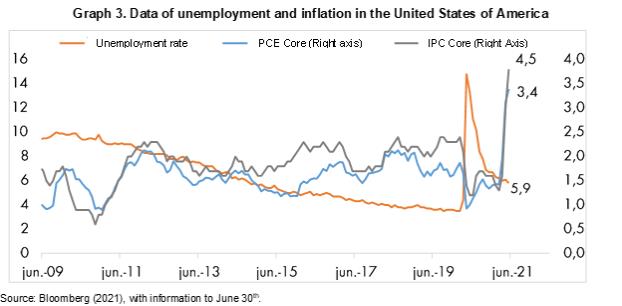

In this context, the IMF established, in its economic growth perspectives published in January 2021, a projected growth for the United States of 5.1 % for 2021 and 3.0% for 2022. This projected growth reflects additional fiscal support from the government and the speed of vaccination that will allow for rapid recovery. However, in its report published in April, the IMF again adjusted its projections, estimating a growth of 6.4% for 2021 and 3.5% for 2022, as a result of accelerated growth in the first quarter of 2021 and a new perspective on the full recovery of all sectors of the economy (IMF, 2021). Graphic 3 shows the behavior of the labor market and inflation in the United States of America.

12

4.2.2. Monetary Policy and Interest Rates

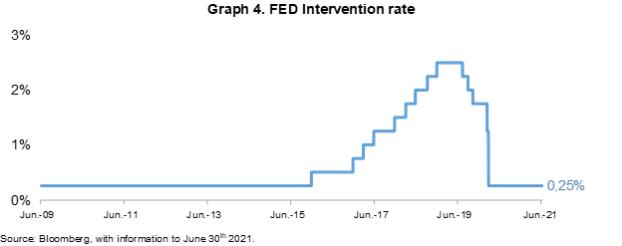

In March, 2020, once the pandemic had been declared, the FED, as emergency measure to support the credit flow to homes and business and, as consequence, to promote its maximum objectives in employment and price stability, adopted the following decisions: (i) cut the effective interest rate to levels close to zero (0,25%); (ii) announced a purchase program for another USD 700,000 million to be allocated in treasury bonds (USD 500,000 million) and mortgage related securities (USD 200,000 million); and, (iii) reached to an agreement with other five foreign central banks (Bank of Canada, Bank of England, Bank of Japan, ECB and Switzerland National Bank) to improve liquidity supply through USD swaps liquidity lines (FED, 2020). Finally, the FOMC declared at its meeting December 2020, that the coronavirus pandemic still presents considerable risks in the medium term for the country economic perspectives and therefore it will keep the reference rate close to zero (0,25%), as reflected in Graphic 4, and that it will increase its treasury securities holdings in USD 80,000 million per month and in agency mortgage backed securities in USD 40,000 million per month, until the economy does not reflect a sustained growth, full employment objective is achieved and a 2% long term price stability exists5 (FED, 2020).

In June 2020, the FED Committee pointed to strengthened economic activity and employment indicators as consequence of the implement policies and the progress in the vaccination process that has reduced the propagation of the COVID-19 in the United States. Additionally, it remarked that the economic sector more affected by the pandemic are still weak but have presented recovery and that the inflation has increased reflecting principally temporary effects.

Additionally, the Committee stated that its objective is to reach the maximum employment and an inflation rate of 2% in the long term. Having had inflation persistently below this target, the Committee will try to keep inflation moderately higher than to the 2% for some time, for inflation to average 2% in the long term and to keep anchored the expectations. It keeps the following policies: (i) target interest rate to levels of 0% - 0,25%; (ii) it will continue raising its holdings in treasury securities for at least USD 80,000 million per month; and (iii) it will continue with the purchasing of agency mortgage-backed securities for at least USD 40,000 million per month (FED, 2021).

| 5 | The FOMC after its meeting August 2020 adopted a new approach in regard of the inflation goal, which is expected to be in a medium level of 2% long term but will allow periods in which that limit is exceeded for some time, in an attempt to ensure a stable growth and an employment not far from its maximum levels. |

13

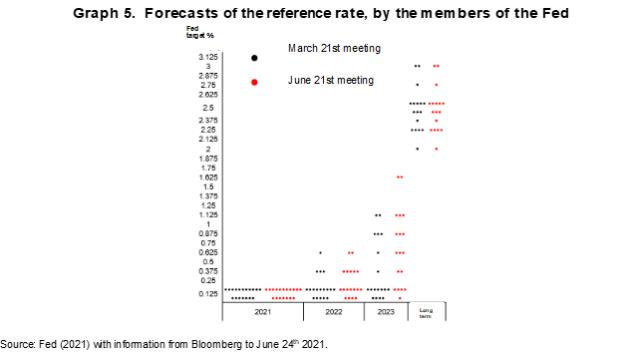

In June 2021, the FED also published its summary of economic projections. In it, it highlights that 13 FOMC members consider that the FED will raise its rates in 2023 and that a majority believes that at least two increases in rates will occur this year. Differently from the report published in March, in which just 7 of the committee members expected rates increase in 2023. Similarly, the number of members that expect an increase in 2022, increased, from 4 in March to 7 in June, as presented in Graphic 5.

14

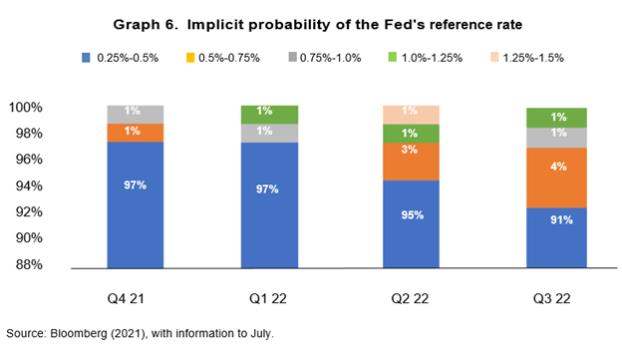

The implied probability of the behavior of the futures market supports the FED’s announcement, since it is expected with a probability of 97% that the reference rate will remain unchanged during the fourth quarter of 2021 and with a probability of 91%, in the third quarter of 2022, aimed of contribute to the economic stability of the country (Graphic 6). However, it is important to bear in mind that, if the US economy shows a faster-than-expected recovery reflected in employment and inflation indicators, there may be an increase in treasury rates, such as those experienced in the first half of the year.

15

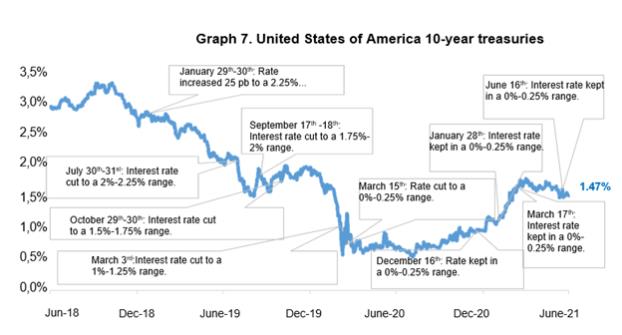

During the last semester (January 2021—June 2021), the rates of the US 10- yeas US treasuries have presented an increase of approximately 50 basis points, as evidenced in Graphic 7. This is mainly explained by market expectations about the beginning of the dismantling of the securities purchase program by the FED, after the acceleration of inflation, the reduction in the rate of unemployment and the recovery observed in the first months of the year in the United States.

In the minutes of the meeting of June 15 and 16, 2021, the members of the FED discussed the possibility of adjusting, ahead of schedule, the pace and composition of the securities purchase programs, for which they agreed to establish a prudential and timely planning that allows them to announce to the market sufficiently in advance the adjustments to these programs (FED, 2021). According to Bill Dudley, former vice president of the FOMC, the liquidation of asset purchase programs should be gradual, accompanied by an increase in short-term interest rates and have a defined roadmap to avoid volatility in the markets as occurred in 2013. In this regard, Dudley assures that now the members of the Fed have the experience of 2013 and although the liquidation of the programs may require adjustments along the way, the market will be clear about the process and the roadmap of the dismantling of the stimulus programs (Bloomberg, 2021).

16

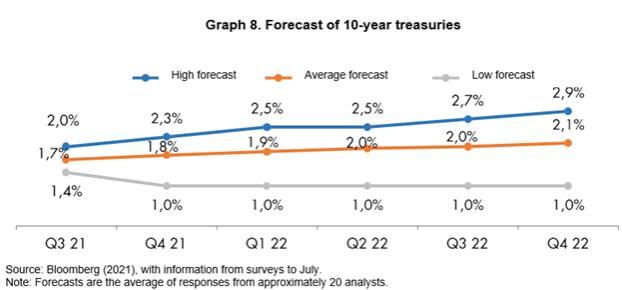

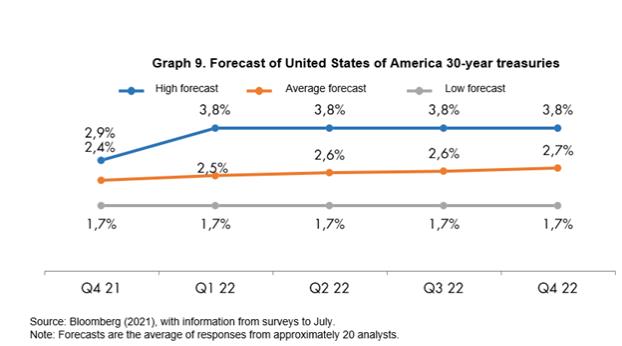

On the other hand, it is important to mention that the results in the pool about the performance of the rates of 10- and 30-years treasury securities carried out by Bloomberg to analysts in July 2021, estimate average levels of 1,7% and 2,4% in Q4 2021, for 10- and 30-years securities, respectively; and of 1,8% and 2,5% in Q1 2022, respectively. (Graphic 8 and Graphic 9).

17

Under this scenario in which the FED keeps its rate policy unaltered and its securities purchase programs, Colombia would have the possibility to finance and/or prefinance that needs of the Government, anticipating the dismantling of the stimulus programs as the United States economic recovery progresses. However, it is important to bear in mind that, in the case of a more accelerated recovery of the United States economy in 2021 or 2022, la treasury curve could continue showing upward pressures that will cause raises in the financing cost of all agents, principally for sovereign and corporative issuers of emerging economies.

4.2.3. Tax Policy

The Congressional Budget Office projects a federal budget deficit of USD 3 billion in 2021 (13,4% of the GDP), almost 130,000 million less than in 2020 and the second highest deficit since 1945. This high deficit is the result of the economic shock caused by the pandemic, which meant lower income and higher expenses in the years 2020 and 2021. In 2022, a USD 789,000 million budget deficit is projected, representing 4,7% of the GDP.

Pursuant the last report of the Congressional Budget Office, federal expenses for 2021 are projected in USD 6,8 trillion, that represents 30,6% of the GDP, and for the term 2022, federal expenses are estimated in USD 5,5 trillion, equivalent to 22,8% of the GDP. On the other hand, tax income is estimated in USD 3,8 trillion by 2021, representing 17.2% of GDP; for the year 2022, revenues of USD 4.3 trillion are projected, corresponding to 18.2% of GDP.

18

Additionally, as a result of the increase in the deficit, the federal debt increased to l00% of GDP in 2020, compared to 79 % at the end of 2019. By 2021, debt is estimated to be close to USD 23 trillion, which will represent 103% of GDP, then debt is expected to fall slightly below 100% between 2023 and 2025 and is expected to reach 106 % in 2031, a level like that recorded in 1946 and which constitutes the highest level of indebtedness in the history of the United States (Office of Congressional Budget, 2021).

With the inauguration of President Joe Biden’s administration on January 20, 2021, new fiscal stimulus packages were introduced. On March 11, the US Rescue Plan was signed for a value of USD 1,9 billion, aimed at the population most affected by the pandemic and to promote the economic reactivation of the country. This plan included direct payments of up to USD 1.400 to a significant part of the population according to income level, an increase in unemployment insurance of USD 300 per week until September 6, the extension of child tax deductions for one year, USD 20,000 million for COVID-19 vaccines, $25 billion in leasing and utility assistance, and $350 billion in state, local and federal aid (Bloomberg, 2021).

4.3. Euro Zone

4.3.1. Macroeconomic Evolution

Economic growth in the euro zone has deteriorated as a result of the region’s geopolitical and economic instability, reaching historically low levels of growth, pressured by the coronavirus pandemic and the impact it has had on global economic activity.

According to the ECB’s Economic Bulletin 2020, after economic growth in the euro zone moderated in 2019, real GDP in the euro zone contracted by 6.6% in 2020 as result of the unusual impact of COVID-19 on the region’s economy. Even though the economy rebounded with great force in the third quarter of the year, the escalation in the number of infected people forced the restoration of confinements and virus containment measures that slowed down the dynamism of the economy affecting domestic demand in an environment of global uncertainty.

As for Brexit, after the ratification of the Withdrawal Agreement between the United Kingdom and the European Union and after months of negotiations, on April 29, 2021 the European Union ratified the Trade and Cooperation Agreement and the Security of Information Agreement, which established preferential rules on trade, intellectual property, fisheries and police cooperation, among others, and agreed on the exchange of classified information as a tool for cooperation against common threats, respectively.

19

Both agreements entered into force on May 2021, however, despite the trade and cooperation agreement between the United Kingdom and the European Union, post-Brexit relations have deteriorated around the so-called sausage war caused by the lack of agreements on trade controls that must be implemented for the imports of frozen meat from the United Kingdom to Northern Ireland in the context of the Brexit agreements, a situation that is particularly complex because of the social division in Northern Ireland on this issue, deepening the geopolitical instability of the region.

However, regarding the resources to address the impact of Brexit on the euro zone, the Council and the European Parliament have reached a preliminary agreement on the disbursement of 5,000 million euros from the Brexit Adaptation Reserve, a financial instrument to mitigate the economic and social effects caused by Brexit. These resources will be intended for the most affected regions and sectors and will be used with the objective, among other things, of compensating companies, encouraging employment and implementing customs controls, once the agreements is endorsed.

On the other hand, with respect to COVID-19, the speed of spread of the virus worldwide led to, according to the World Health Organization (WHO), in mid-March 2020, Europe becoming the epicenter of the pandemic, reporting 40% of infection cases worldwide. In terms of mortality, in April 2020, Europe accounted for 63% deaths due to COVID-19 worldwide, which most strongly affected the adult population of the region (World Health Organization, 2020).

According to the ECB’s Economic Bulletin, the GDP of the euro zone increased in the third quarter of 2020 by 12.4% after experiencing setbacks of 3.7% and 11.7% in the first and second half of the year, in a context of strict lockdown measures that undermined employment and affected the productive capacity and domestic demand of the euro zone (European Central Bank, 2020). However, the rebound observed in the third quarter, the increase in COVID-19 infections and the restrictions and containment measures adopted by the different countries slowed the growth of the euro zone in the fourth quarter of 2020 in which real GDP fell by 0.6% (European Central Bank, 2021).

In the first quarter of 2021, real GDP contracted by an additional 5.1 % as a result of the epidemiological situation in the euro zone and the world. European vaccination strategy, through which the European Commission mobilized part of the available budget to guarantee the supply of vaccines through the advance acquisition of doses from Moderna, AstraZeneca, Johnson & Johnson and BioNTech Pfizer, has allowed gradual reopening of economies that allow to foresee an economic reactivation of the euro area in the second half of 2021 (European Commission, 2021). However, the European Council warns that caution should be exercised and closely monitor the development of new variants of COVID-19.

20

Although the economic perspective in the short term remains anchored to the evolution of the pandemic in an environment of uncertainty, IMF estimates foresee an acceleration of GDP for the euro area in 2021 of 4.4% (0.2 p.p. above what was projected in January) and 3.8% in 2022. In the estimates disaggregated by country, the IMF calculates a growth by developed economies: Germany, 3.6% in 2021 and 3.4% in 2022; France, 5.8% in 2021 and 4.2% in 2022; Italy, 4.2% in 2021 and 3.6% in 2022 and Spain 6.4% in 2021 and 4.7% in 2022.

4.3.2. Monetary policy and interest rates

In 2020, the ECB maintained its expansionary monetary policy as a stimulus to try to reactivate the economy after the slowdown in economic activity marked by the pandemic and persistent low inflation. In 2020, the Governing Council of the ECB kept unchanged the interest rates of the main financing transactions, the rates on the marginal lending facility and the deposit facility at 0,00 %, 0,25 % and -0.50 %, respectively. Additionally, it launched the temporary asset purchase program called Pandemic Emergency Purchase Program (PEPP) with a total allocation of 1.85 billion euros in force until March 2022. Similarly, the ECB continues with the Asset Purchase Program (APP) for 20,000 million euros per month and financing transactions (TLTRO-111) extending its term until June 2022 (European Central Bank, 2020).

At the monetary policy meeting on December 10, 2020, the Governing Council of the ECB decided to offer four additional longer-term emergency refinancing transactions (PELTROs) on a quarterly basis during 2021 under accommodative interest rate terms 25 basis points below the Euro system’s main refinancing transactions, as a liquidity backing (European Central Bank, 2020).

In the monetary policy meeting on June 10, 2021, the ECB kept the interest rates in 0,00%, 0,25%, and -0,50% in line with the accommodative monetary policy that aims to grant favorable conditions for financing, to be a backup for the economic activity, to safeguard the price stability in the midterm and to tend for a solid convergency on inflation to levels close to 2% in the medium term (European Central Bank).

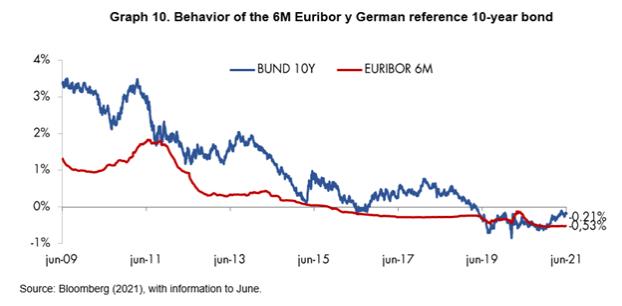

Conventional and unconventional measures of expansionist monetary policy of the ECB, the persistent low inflation and the uncertainty with respect to political and economic factors, caused the Euribor rate and the interest rates of sovereign bonds of some countries of the euro zone to be in historically low levels or in a negative zone through 2020 and so far in 2021, as is the case of Germany’s treasury bonds. However, the yields of sovereign debt of the euro zone registered a moderate increase between March and June 2021, due to the progress of the vaccination process, the subsequent improvement in the perspectives on economic growth and the increase in inflation (1,9% in June 2021).

21

Considering the implied probability of the futures market behavior to July 9, 2021, an BCE’s unaltered rate is expected for the fourth quarter of 2021 and through the first three quarters of 2022 with a probability of 100%.

The continuation of an expansionary monetary policy by the ECB and low interest rates could generate a financing alternative in euros for emerging countries with competitive rates.

4.3.3. Fiscal policy

The European Union (EU) implemented fiscal policies with the aim of mitigate the socio-economic impact of the pandemic in the region, strengthening health systems and promoting the economic recovery of the EU. Following this, on April 23, 2020, the European Council approved a support package for employment and workers, companies and Member States worth 540,000 million euros distributed in three lines of work: (i) Instrument of Temporary Support to Mitigate Unemployment Risks in an Emergency, which consists of providing financial assistance in the form of EU loans to Member States under favorable conditions for a total of €100 billion to protect jobs and workers affected by the pandemic; (ii) Pan-European Guarantee Fund of the European Investment Bank Group providing loans of up to €200 billion in particular to small and medium-sized enterprises throughout the Union, and (iii) a credit line established by the European Stability Mechanism providing loans to Member States totaling €240 billion (European Council, 2020).

22

Additionally, to contribute to the repair of the economic and social damage caused by the pandemic, on May 27, 2020, the European Commission presented a proposal for economic recovery aimed at exploiting budget potential consisting of: (i) European Recovery Structure (Next Generation EU) worth €750 billion to boost the EU budget through financial market resources aimed at reviving the economy and promoting economic growth; and (ii) Multiannual Financial Framework for 2021-2027 through which it is intended to create and strengthen existing programs through the resources of the EU Next Generation to channel resources quickly, strengthen the internal market, promote cooperation in the field of health, promote transitions ecological and digital and promote a fair and resilient economy (European Commission, 2020).

The exceptional fiscal measures adopted to deal with the crisis and put the European Union’s economy back on track amount to €1.29 trillion. The energetic fiscal response of the countries of the euro zone resulted in an increase in the fiscal deficit of its public administrations that stood at 7.3% in 2020 compared to 0.6% in 2019 (European Central Bank, 2020). However, in the ECB’s view:

“An ambitious and coordinated fiscal stance remains crucial, as an early withdrawal of fiscal support could weaken the recovery and aggravate the long-term aftermath. Therefore, national tax policies must continue to provide substantive and timely support to the companies and households most exposed to the pandemic and the associated containment measures”

The ECB also states that as vaccination continues its progress, temporary emergency and anticyclical measures should be replaced by structured economic recovery policies with an emphasis on public investment to support euro zone growth in the medium term.

4.4. Japan

4.4.1. Macroeconomic Evolution

Japan’s real GDP contracted by 4.8% in 2020 as a result of the impact of the COVID-19 pandemic on the economy, mainly in the first half of 2020. The IMF’s economic growth forecast for Japan in 2021 is 3.3%, 0.2% higher than the IMF’s January 2021 projections. This growth is supported by greater domestic and external demand and the expected impact of the pandemic on that country. For 2022, the IMF estimates a growth in economic activity of 2.5%. Likewise, the Bank of Japan (BoJ) revised upwards the inflation perspective for 2021 of 0.1% to 0.6% driven by an increase in energy prices. However, the bank estimates that inflation will remain close to 0% as a result of the impact of the new wave of COVID-19 affecting the country and which is expected to weaken domestic demand (Bank of Japan, 2021).

23

4.4.2. Monetary policy and interest rates

During 2020, the Bank of Japan continues with its massive asset purchase program with the aim of reaching the inflation target of 2%. During the first half of 2020, the BoJ further relaxed its monetary policy through (i) an increase in purchases of short-term debt and corporate bonds; (ii) strengthening special funding transactions to facilitate financing in response to COVID-19; (iii) active purchases of exchange-traded funds (ETFs) and real estate investment trusts in Japan, and (iv) eliminating the upper limit on active purchases of Japanese government bonds and treasury discount bills (Bank of Japan, 2020).

At the BoJ meeting on 16 June 2021, the committee decided to maintain its monetary policy rate at -0.10% and announced that it expects interest rates to remain at their current levels or lower in the short and long term. Regarding monetary policy structures, it decided to maintain qualitative and quantitative monetary easing until target inflation and stabilization of financial markets were achieved. In this regard, the BoJ will continue to support financing to companies and promote the stability of the financial market through the (i) Special Program to Support Financing in Response to COVID-19; (ii) the provision of yen and funds in foreign currency through the purchase of Japanese government bonds (JGB) without top limit thus the 10-year JGB yields remain around 0%, and (iii) the purchase of ETF and J-REIT actives as needed with higher limits of approximately 12 trillion yen and 1.80 billion yen, respectively; programs that the BoJ decided to extend until March 2022. The BoJ itself announced that a new provision of funds was unanimously approved to support various efforts of private financial institutions with respect to the climate change (Bank of Japan, 2021).

In the latest BoJ’s Perspectives for Economic Activity report, the Japanese economy is expected to grow by 3.8% for 2021, or 0.2 p.p. less than the projections estimated in the previous report, because of the impact of the fourth wave of COVID-19 on the country. However, the bank raised the economic growth perspective for 2022 from 2.4% to 2.7% (Bank of Japan, 2021).

24

4.4.1. Tax Policy

To keep businesses and households in Japan floating, the Japan government has approved three unprecedented fiscal stimulus packages, the first two worth 1.17 trillion yen each one and a third package worth 73.6 trillion yen. The fiscal stimulus packages have focused on (i) preventing the spread of the virus and strengthening the health system, (ii) protecting jobs and businesses, (iii) recovering economic activity after the lockdown, (iv) move towards a resilient economic structure, (v) support local governments with transfers, (vi) raise the ceiling of the COVID-19 reserve fund, (vii) promote positive economic cycles for the post-COVID 19 era and (viii) ensure safety and assistance with respect to disaster management.

4.5. Emerging markets

4.5.1. Macroeconomic evolution

In its January 2021 report for the years 2021 and 2022, the IMF predicted a growth for emerging and developing markets economies of 6.3% and 5.0%, respectively, an accelerated growth as a result of progress in the vaccination process, the recovery of international trade and other sectors, and the increase in oil demand as consequence of the fiscal stimulus implemented by countries such as the United States and China. For the economies of Latin America and the Caribbean, the projections in January were 4,1% and 2.9% for 2021 and 2022 respectively.

However, the projections were adjusted in the report published in April 2021 considering continued fiscal support, the speed of vaccines and the positive results in the growth of some countries. For emerging and developing economies, in general, the IMF projects growth of 6.7% for 2021 and 5.0% for 2022. Growth of 8.6 % is projected for 2021 and 6.0% for 2022 for emerging economies in Asia, while for emerging economies in Europe, which contracted by 2.0% in 2020, growth of 4.4% is expected for 2021 and 3.9 % in 2022. Finally, for the economies of Latin America and the Caribbean, the IMF in its report reported a contraction of 7.0% in 2020 and estimates a recovery of 4.6% in 2021 and 3.1% in 2022 (Monetary Fund international, 2021).

While China was the country where the spread of COVID-19 began, restrictions on economic and social life were gradually lifted in the first half of 2020. The Chinese authorities, since the beginning of the outbreak, have continuously intensified economic policy measures to cushion the economic and social impacts. This allowed an accelerated recovery of the Chinese economy that grew 2.3% in 2020, driven mainly by the commercial sector and private consumption.

For its part, China’s central bank has secured ample liquidity to bolster market confidence and ease banks’ short-term liquidity constraints. Since February 2020, the bank has reduced short and long-term policy interest rates by 30 basis points, causing interbank market rates and bond yields to fall by between 20 and 50 basis points. Reserve requirements were also reduced, generating significant liquidity of approximately 1.7 trillion yuan. However, unlike other major central banks, China’s central bank has refrained from implementing quantitative easing and asset purchases. According to IMF estimates (2021), the Chinese economy is expected to grow at an accelerated rate of 8.5% in 2021 and 5.6% in 2022.

25

On the other hand, the slowdown in Latin America was the most pronounced of the entire group of emerging economies, which is explained by the prolonged quarantines, the different outbreaks of COVID-19, the speed of vaccination and the negative growth trend that was already affecting in the region.

In 2020, Brazil’s economy contracted 4,1% and, according to the IMF report of April, it has an estimated growth of 3.7% for 2021 and 2.6% for the 2022. At the start of the pandemic, the authorities responded by announcing a series of fiscal measures amounting to 12% of GDP, the direct impact of which on the 2020 primary deficit was of 7.2% of GDP. Tax measures include temporary revenue support for vulnerable households, employment support, lower taxes and taxes on the importation of medical supplies, new transfers from the federal government to state governments, among others (International Monetary Fund, 2021).

Additionally, the Central Bank of Brazil lowered the monetary policy interest rate (SELIC) by 225 basis points from mid-February 2020 to August 2020, at the historical minimum of 2% and implemented measures to increase liquidity in the financial system, including opening a facility to grant loans to financial institutions backed by private corporate bonds. In the first half of 2021, due to the acceleration of inflation, the Central Bank of Brazil increased the policy rate (SELIC) by 225 basis points to 4.25% at its last meeting in June (International Monetary Fund, 2021).

In the case of Mexico, the economic situation was aggravated by the decline in oil prices and the weakening of business confidence since before the pandemic, as consequence the economic contraction for the 2020 was 8.2%. According to its report of April, the IMF projects a recovery of 5.0 % of GDP in 2021 and 3.0% in 2022. In fiscal terms, during 2020 the measures taken by the Government of Mexico represented near the 9% of GDP and were focused on the following: (i) ensuring that the Ministry of Health had sufficient financial resources; (ii) support households and businesses; (iii) boost credit, strengthen liquidity and ensure the proper functioning of financial resources, and (iv) accelerate public expenditure bidding processes to ensure budget execution (International Monetary Fund, 2021).

26

The Central Bank of Mexico cut the reference rate 300 basis points to 4.0% between March 2020 and February 2021 and introduced measures to support the operation of the financial system by up to 800 billion pesos. The Central Bank recorded its first policy rate hike of 25 basis points on June 24, 2021, in response to inflation risks (International Monetary Fund, 2021).

4.5.1. Investments flow to emerging markets and market performance

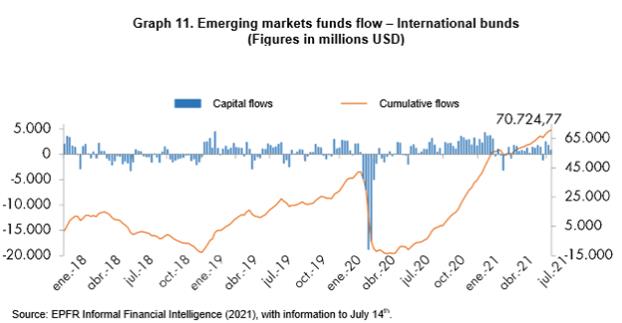

After the strong outflow of investment flows that affected international fixed income securities issued by emerging markets in the first half of 2020, in the second half of 2020 and at the beginning of 2021 there was a recovery, which made that the accumulate amount to July 14, 2021, was above USD 70,000 million, while in September of the previous year, the accumulate amount was below USD 6,000 million, as evidenced in graphic 11.

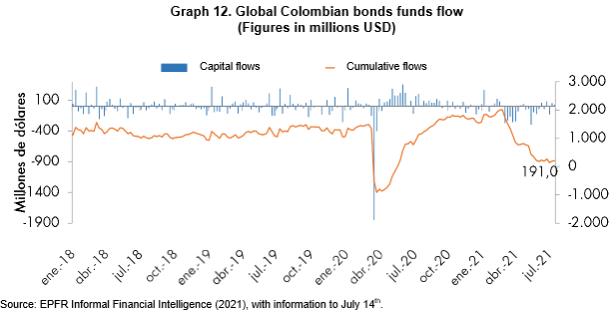

As for Colombia, the behavior of the flow of funds directed to Colombian Global Bonds has had a variable behavior in the last year; however, it is still positive and accumulates USD 191 million as of April 17, 2021, as evidenced in graphic 12.

27

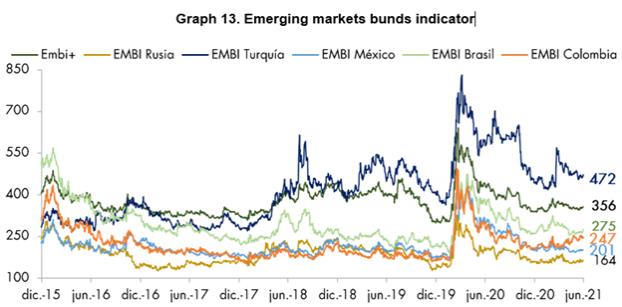

On the other hand, through the first half of 2020, the credit risk perception represented by the index of emerging markets bonds (EMBI+)6 showed stability in the first quarter. Nonetheless, once the pandemic was declared, credit risk perception had a considerable increase up to historical levels in all the emerging countries, with a variation of approximately 300 basis points (graphic 13). In the second half of 2020 and the first half of 2021, credit risk perception has diminished but remains in levels above those reached before the pandemic.

The index for Colombia, like the one of emerging countries, was affected by the sanitary crisis, especially in the first half of 2020; however, in the second half of 2020 and the first months of 2021, it presented a favorable behavior, that took it below the EMBI+ general index, after the correction presented in April 2020. Since the end of April 2021, due to the order public situation that affected the country, the withdraw of the tax reform and the subsequent reduction in Colombia’s credit rating, which is described below, an increase in risk perception was showed and therefore an extension of Colombia’s EMBI in approximately 45 basis points, as represented in graphic 13. Nonetheless, Colombia’s risk perception remains below the 2020 average (267 basis points), and near the levels observed in 2016.

| 6 | The index represents the difference between the interest rates of a bond in US dollars issued by emerging markets and a bond basket issued by the treasury of the United States of America with similar characteristics. |

28

4.6. Colombia

4.6.1. Macroeconomic Performance

According to information from the National Administrative Department of Statistics (DANE), during 2020, GDP registered an economic contraction of 6.8% as a result of the economic shock due to the COVID-19 pandemic, particularly due to social isolation measures, both voluntary and those implemented by national and local authorities. In particular, the sectors that contributed most to the dynamics of aggregated value are: (i) wholesale and retail trade, transport and storage, accommodation and food services, that decreased 15.1%; (ii) construction sector which decreased 27,7% and (iii) mining and quarrying that fell 15.7% (National Administrative Department of Statistics, 2021).

In the first quarter of 2021 the economy showed a recovery of 1.1% compared to the same quarter of 2020, the economic activities that contributed the most to this growth were the following: (i) manufacturing industries that grew 7.0%; (ii) public administration and defense, education; human health care and social services activities that grew by 3.5% and (iii) agriculture, livestock, hunting, forestry and fishing that grew 3.3% (National Administrative Department of Statistics, 2021).

At the domestic level, inflation stood at 1.6% in 2020, this behavior, like the falls in all basic inflation indicators, is partly the reflection of weak aggregate demand and excess productive capacity. The dynamics of inflation will also be explained by the effect of the temporary reduction of some indirect taxes, the re-composition of household spending and the freezing of some prices. So far in 2021, as of June, inflation is 3.13% (National Administrative Department of Statistics, 2021).

29

The strong decline in economic activity, associated with the health emergency, generated a generalized and unprecedented deterioration of the Colombian labor market, reaching an unemployment rate of 21.4% in May 2020. So far in 2021, a recovery has been evidenced in this regard, reaching 15.6% in May 2021; the economic sectors that contributed the most to this recovery were: (i) trade and repair of vehicles; (ii) construction; and (iii) manufacturing industry with 4,1; 2,6 and 2,3 percentage points, respectively (National Administrative Department of Statistics, 2021).

In 2021, a recovery of the Colombian economy is expected; the Ministry of Finance and Public Credit projects a growth of 6% in 2021, based on the progress of the vaccination process, the counter cyclical policy measures implemented by the Government and the recovery of the world economy. For the second quarter, a slowdown in growth is projected, influenced both by social mobilizations that have interrupted the normal functioning of the economy, and by some confinement measures in response to the third peak of the pandemic. However, growth is expected to accelerate again towards the second half of the year. (Ministry of Finance and Public Credit, 2021).

As happened in 2020, for 2021 there is a high uncertainty regarding the growth rate figure. However, most of the forecasters estimate an acceleration of the Colombian economy. For example, the International Monetary Fund projects growth of 5.0%, the Bank of the Republic, 6.5% and the Organization for Cooperation and Economic Development (OECD) of 7.3% by 2021.

4.6.2. COVID-19 measures

The country faced two strong economic shocks at the beginning of 2020: the effects of the COVID-19 pandemic and the decline in oil prices. In this scenario, the Government declared on March 17 through Decree 417 of 20207, the State of Economic, Social and Ecological Emergency throughout the National Territory, pursuant the provisions set forth in article 215 of the Political Constitution of Colombia. Despite the measures taken to address the adverse effects, new circumstances arose that made it necessary to maintain mandatory preventive isolation, therefor, on May 6, a new State of Economic, Social and Ecological Emergency is declared in the country for a term of 30 days through Decree 637 of 20208.

| 7 | By which a State of Economic, Social and Ecological Emergency is declared throughout the national territory. |

| 8 | By which a State of Economic, Social and Ecological Emergency is declared throughout the national territory. |

30

Monetary policy

In this context, the Bank of the Republic resorted to various tools to inject liquidity into the economy, and contribute to ensuring that companies, households and the financial system are affected as little as possible:

| (i) | Monetary policy measures: the Board of Directors of Bank of the Republic, since the pandemic began, has lowered the interest rate seven times, by a total of 250 basis points. The first reduction was on 27 March from 4.25% to 3.75%, to support the future recovery of domestic demand once the functioning of markets normalizes. The last reduction was made on September 28, 2020, by a quarter of a percentage point from 2.0% to 1.75%. |

| (ii) | Changes in the balance sheet of the Bank of the Republic: Solidarity Bonds were included as eligible securities in transitory and definitive expansion transactions, and temporary liquidity support. At the end of June 2021, the Bank’s TES portfolio (expressed in nominal values) consists of TES denominated in pesos (8,351.5 billion) and TES denominated in UVR (UVR 5.3 billion). |