EXHIBIT 13

SONESTA INTERNATIONAL HOTELS CORPORATION

ANNUAL REPORT 2008

TO OUR SHAREHOLDERS:

For Sonesta, 2008 was a year comprised of two distinct periods: January through August, and September through December. Through the first eight months we were on track for a strong year: cumulative revenues from our hotel operations in Boston and New Orleans exceeded what we realized during the same period in 2007 by $4,100,000. In addition our management and franchise income increased substantially from 2007 to 2008. In the last four months of the year, however, revenues and profits from hotel operations, and from management and franchise fee income, trailed what we reported for those months in 2007. By the end of 2008, the increase in total revenues over 2007 was $3,614,000, and operating income increased by $4,443,000.

During 2008, we collected $5,002,000 in connection with the termination of our management contract to operate Trump International Sonesta Beach Resort, in Sunny Isles, Florida, and $3,397,000 of loan repayments regarding Sonesta Bayfront Hotel in Coconut Grove, Florida. During the year we also distributed a total of $4,438,000 in dividends, including a special dividend of $1.00 per share paid in February.

Through October, Royal Sonesta Boston was 9% ahead of the same period in 2007 in revenues. The Hotel relies heavily on group business, however, and cancellations in November and December – the result of corporate cost-cutting – and seasonal drop-off in group business significantly affected year-end results. Even so, the Hotel surpassed 2007’s results by $1,401,000 in revenues, and $538,000 in operating income. The hotel remains in outstanding condition, and we completed the renovation of the Hotel’s East Tower meeting space and public restrooms in the first quarter of this year.

For Royal Sonesta New Orleans, the pivotal month was September, when the back-to-back threats from Hurricanes Gustav and Ike adversely affected the Hotel’s business. Although Gustav caused no physical damage to the Hotel, many people evacuated the City and the Hotel was closed for several days. Gustav, alone, resulted in an estimated $500,000 in lost revenues. Due to a strong first eight months, the Hotel finished 2008 $907,000 ahead of 2007 in revenues. Operating income before rent expense increased by $414,000. The Hotel continues to be the upper upscale market leader in New Orleans. In March 2009, the Hotel will transform its lobby lounge into a new jazz club: Irvin Mayfield’s Jazz Playhouse.

While it, too, fell victim to the economy in the later part of 2008, Sonesta Bayfront Hotel Coconut Grove had a good year in a challenging market. Revenues decreased slightly compared to 2007, but profits increased over 2007, as did the Company’s fee income. In October, the Hotel’s owner refinanced the Hotel and repaid the balance of the Company’s original $5 Million loan.

We terminated our relationship with Trump International Sonesta Beach Resort, in Sunny Isles, Florida, effective April 1, 2008. We then engaged in an arbitration process with the Hotel’s owner, seeking reimbursement of some $7 Million in deferred fees and advances, as provided in our contract. During that process, the parties agreed to a settlement of all claims, and the Company received approximately $5 million in cash.

Redevelopment of the Sonesta Key Biscayne site stalled during 2008 due to the severe economic conditions and their impact on the condominium market in South Florida. We and our partner in the project, Fortune International, continue to explore a number of possible scenarios regarding the property.

All of our hotels, resorts and cruise ships in Egypt realized more revenues and profits in 2008 than they had in 2007. Additionally, our Cairo and Luxor properties are being expanded by 171 and 119 guestrooms, respectively, and both are adding function and meeting space. At the end of March 2009, our operation of Sonesta Port Said, a 92-room hotel, will end.

Relationships with our licensed hotels in Peru, Brazil and St. Maarten continue to be strong. These hotels provide us with important brand exposure in South America and the Caribbean. We anticipate additional licensed hotels in South America with our Colombian associates at GHL Hotels.

Last spring, we determined to grow the Company through expansion of the Sonesta brand, particularly in the United States. One way to accomplish this is through franchising. In September, Philip Silberstein joined us as Executive Vice President of Development. Phil has 30 plus years of industry development experience, including franchising, and he is leading our expansion efforts. We are excited to have him on board.

The first phase of Sonesta Jaco Resort, in Costa Rica, is scheduled to open this summer. At least half of the condo-hotel’s 190 luxurious suites should be available this summer, together with a restaurant, lazy-river, and other wonderful features and amenities. Sonesta San Carlos, on Mexico’s Sea of Cortez, remains in development, and we anticipate that the developer will break ground soon. Both the aforementioned hotels will be operated under management agreements. In January of this year, we announced the signing of a management contract to operate a 252-room hotel as part of a mixed-use development in downtown Miami. Sonesta Mikado Hotel will open in 2011. Development of Sonesta Orlando Resort, on the other hand, is stalled. In January 2009, we formally severed ties with the project.

We are sad to report that Roger P. Sonnabend, Sonesta’s Executive Chairman of the Board, passed away in early December 2008 after a brief illness. Roger guided the Company for 44 years and was universally admired and respected. Our memories of him will inspire us for many years to come.

If you would like additional information about Sonesta hotels, resorts, or cruises, please visit our website at www.sonesta.com.

We appreciate the continued interest and support of you, our shareholders, and of our hotel owners, guests, partners and employees.

| /s/ Peter J. Sonnabend | |

| Peter J. Sonnabend | |

| Executive Chairman of the Board | |

| /s/ Stephanie Sonnabend | |

| Stephanie Sonnabend | |

| Chief Executive Officer and President | |

March 19, 2009

1

SONESTA INTERNATIONAL HOTELS CORPORATION

5-YEAR SELECTED FINANCIAL DATA

(In thousands except for per share data)

| 2008 | 2007 | 2006 | 2005 | 2004 | ||||||||||||||||

| Revenues | $ | 71,552 | $ | 67,938 | $ | 77,595 | $ | 88,125 | $ | 89,907 | ||||||||||

| Other revenues from managed and affiliated properties | 8,965 | 18,747 | 21,237 | 14,543 | 12,727 | |||||||||||||||

| Total revenues | 80,517 | 86,685 | 98,832 | 102,668 | 102,634 | |||||||||||||||

| Operating income (loss) | 6,671 | 2,228 | (3,829 | ) | (1,905 | ) | 1,502 | |||||||||||||

| Net interest expense | (1,788 | ) | (1,292 | ) | (1,441 | ) | (2,836 | ) | (5,860 | ) | ||||||||||

| Other income | 574 | 250 | 49 | 4,054 | 182 | |||||||||||||||

| Income (loss) before income taxes | 5,457 | 1,186 | (5,221 | ) | (687 | ) | (4,176 | ) | ||||||||||||

| Income tax provision (benefit) | 1,377 | (151 | ) | (1,698 | ) | (5,355 | ) | 426 | ||||||||||||

| Net income (loss) | $ | 4,080 | $ | 1,337 | $ | (3,523 | ) | $ | 4,668 | $ | (4,602 | ) | ||||||||

| Basic and diluted net income (loss) per share of common stock | $ | 1.10 | $ | 0.36 | $ | (0.95 | ) | $ | 1.26 | $ | (1.24 | ) | ||||||||

| Cash dividends declared | $ | 1.35 | $ | 0.20 | $ | 0.20 | $ | 1.10 | $ | -- | ||||||||||

| Net property and equipment | $ | 35,031 | $ | 37,303 | $ | 38,400 | $ | 72,799 | $ | 76,638 | ||||||||||

| Total assets | 127,040 | 129,591 | 126,428 | 130,619 | 109,537 | |||||||||||||||

| Long-term debt including currently payable portion | 33,002 | 34,061 | 34,061 | 34,061 | 69,816 | |||||||||||||||

| Common stockholders' equity | 4,126 | 8,547 | 7,371 | 11,865 | 11,264 | |||||||||||||||

| Common stockholders' equity per share | 1.12 | 2.31 | 1.99 | 3.21 | 3.05 | |||||||||||||||

| Common shares outstanding at end of year | 3,698 | 3,698 | 3,698 | 3,698 | 3,698 | |||||||||||||||

Market price data for the Company’s common stock showing high and low prices by quarter for each of the last two years is as follows:

| NASDAQ Quotations | ||||||||||||||||

| 2008 | 2007 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| First | $ | 35.99 | $ | 18.93 | $ | 29.97 | $ | 20.00 | ||||||||

| Second | 30.61 | 22.92 | 32.40 | 22.02 | ||||||||||||

| Third | 27.97 | 18.78 | 59.00 | 31.50 | ||||||||||||

| Fourth | 20.79 | 7.85 | 47.99 | 28.05 | ||||||||||||

The Company’s common stock trades on the NASDAQ Stock Market under the symbol SNSTA. As of February 11, 2009 there were 322 holders of record of the Company’s common stock.

A copy of the Company’s Form 10-K Report, which is filed annually with the Securities and Exchange Commission, is available to stockholders. Requests should be sent to the Office of the Secretary at the Company’s Executive Office.

2

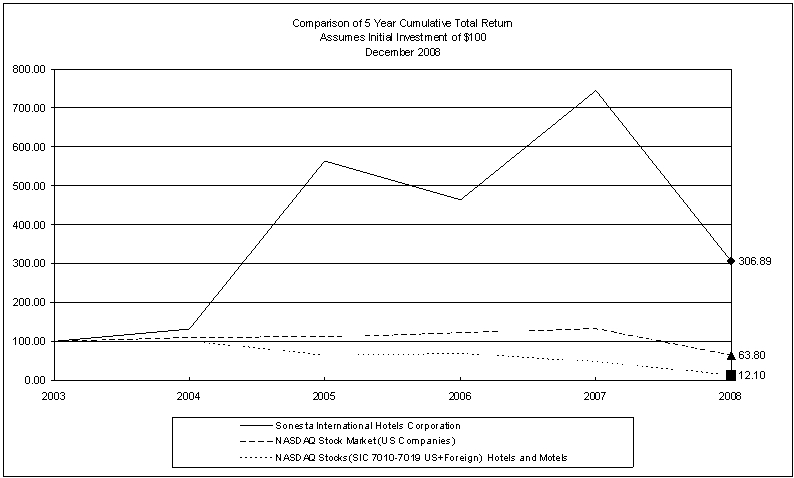

Performance Graph

The following graph compares the annual percentage change in the cumulative total stockholder return on the Company’s Common Stock against the cumulative total return of the NASDAQ Stock Market (US Companies) and the NASDAQ Hotels and Motels Stocks (SIC 7010-7019) for the five-year period commencing December 31, 2003 and ending December 31, 2008.

3

MANAGEMENT'S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL CONDITION

The Company's consolidated financial statements include the revenues, expenses, assets and liabilities of Royal Sonesta Hotel Boston, Royal Sonesta Hotel New Orleans and the Company’s investment in a partnership which owns the site of the former Sonesta Beach Resort Key Biscayne. The Boston property is owned by the Company, and the New Orleans hotel is operated under a long-term lease. The financial statements also include the Company’s revenues and expenses from the management of properties in the United States and Egypt, and license fee income from properties in New Orleans, Louisiana (until October 2008); St. Maarten, Brazil and Peru.

Results of Operations

During 2008, the Company recorded net income of $4,080,000, or $1.10 per share, compared to net income of $1,337,000, or $0.36 per share, during 2007. A reconciliation of the $2,743,000 increase in earnings follows (in thousands):

| Increase in operating income Royal Sonesta Boston | $ | 538 | ||

| Decrease in operating income Royal Sonesta New Orleans | (741 | ) | ||

| Income from Management Agreement settlement | 3,279 | |||

| Decrease in loss from management activities | 1,367 | |||

| Decrease in interest income | (537 | ) | ||

| Other changes | 365 | |||

| Increase in tax expense, partially due to improved earnings | (1,528 | ) | ||

| Increase in earnings 2008 compared to 2007 | $ | 2,743 |

| · | Royal Sonesta Hotel Boston had a good year, increasing revenues by 5% compared to 2007. Business was strong through October 2008, but declined substantially during the months of November and December, as a result of the decline in economic activity. |

| · | Royal Sonesta Hotel New Orleans recorded a modest 3% increase in revenues compared to 2007. Operating income decreased primarily as a result of increased rent expense. Through August 2008, revenues increased by 10% compared to the same period in 2007. September 2008 revenues were impacted by Hurricane Gustav, and 2008 fourth quarter revenues declined due to the worsening economic conditions. |

| · | The loss from management activities decreased primarily as a result of higher income from the Company’s managed properties in Egypt. |

| · | During the 2008 third quarter, the Company recorded pre-tax income of $3,279,000 related to the settlement of a dispute with the owner of Trump International Sonesta Beach Resort (see Note 2). The Company terminated the Management Agreement for this property effective April 1, 2008. |

A detailed analysis of the revenues and expenses by location follows.

Revenues

The Company records costs incurred on behalf of owners of managed and affiliated properties, and expenses reimbursed from managed and affiliated properties, on a gross basis. The revenues included and discussed in this Management’s Discussion and Analysis exclude the “other revenues and expenses from managed and affiliated properties”.

| TOTAL REVENUES | ||||||||||||||||

| (in thousands) | ||||||||||||||||

NO. OF ROOMS | 2008 | 2007 | 2006 | |||||||||||||

| Sonesta Beach Resort Key Biscayne | 300 | $ | -- | $ | -- | $ | 19,341 | |||||||||

| Royal Sonesta Hotel Boston | 400 | 30,778 | 29,377 | 26,408 | ||||||||||||

| Royal Sonesta Hotel New Orleans | 500 | 32,795 | 31,888 | 27,894 | ||||||||||||

| Management and service fees | 7,979 | 6,673 | 3,952 | |||||||||||||

| Total revenues, excluding other revenues from managed and affiliated properties | $ | 71,552 | $ | 67,938 | $ | 77,595 | ||||||||||

2008 versus 2007: Total revenues, excluding other revenues from managed and affiliated properties, were $71,552,000 in 2008 compared to $67,938,000 in 2007, an increase of $3,614,000. Revenues at Royal Sonesta Hotel Boston increased by $1,401,000 in 2008 compared to 2007, representing a 5% increase. Demand in the Boston hotel market was strong in 2008 through the month of October. Revenues declined during the last two months of 2008. Revenues at Royal Sonesta Hotel New Orleans in 2008 increased by a modest 3%. Business during the first eight months of the year was strong, but September 2008 revenues were impacted by Hurricane Gustav. Revenues during the fourth quarter decreased compared to 2007, due to worsening economic conditions. Revenues from management activities increased from $6,673,000 during 2007 to $7,979,000 during 2008, primarily due to an increase in management income from the Company’s collection of hotels and cruise ships in Egypt. A more detailed analysis of the revenues by hotel, and of our management income, follows.

Royal Sonesta Hotel Boston recorded revenues of $30,778,000 during 2008 compared to $29,377,000 in 2007, representing an increase of $1,401,000, or 5%. This increase was mainly due to an increase of $1,160,000 in room revenues. Room revenues per available room (“REVPAR”) increased by 6% in 2008 compared to 2007, mainly due to an increase in occupancy levels. Demand in Boston was strong through October 2008, which benefitted the Hotel. The increase in occupancy was entirely from increased transient rooms business. The increase in non-rooms revenue of $241,000 was mainly due to increased food and beverage revenues, which included higher revenues from the hotel’s newly renovated ArtBar.

Revenues at Royal Sonesta Hotel New Orleans during 2008 totaled $32,795,000 compared to $31,888,000 during 2007, representing an increase of $907,000, or 3%. In general, hotel business in New Orleans continued to improve during the first eight months of 2008 from the downturn in business following Hurricane Katrina in 2005. September revenues, however, were impacted by Hurricanes Gustav and Ike, and fourth quarter 2008 revenues were affected by decreased business volumes resulting from worsened economic conditions. Room revenues increased by $771,000 in 2008 due to a 4% REVPAR increase which was entirely due to higher average room rates achieved. Revenues other than rooms increased by $215,000 due to increased banquet revenues. Revenues from the hotel’s laundry, which also services third party hotels, decreased by $79,000 in 2008 compared to 2007 due to the loss of revenues from Chateau Sonesta Hotel New Orleans, which was operated by the Company under a management agreement until October, 2007.

4

Revenues from management activities increased from $6,673,000 during 2007 to $7,979,000 during 2008, representing an increase of $1,306,000. Of this increase, $1,146,000 resulted from improved fee income from the Company’s collection of hotels and Nile River cruise ships in Egypt. Business in Egypt in 2008 continued to improve, and management income also included fee income from Sonesta Pharaoh Beach Resort Hurghada, which was added under management effective January 1, 2008. The remaining increase resulted from higher income from hotels to which the Company licenses the use of its name in St. Maarten and South America, partially offset by decreased fee income from Chateau Sonesta Hotel New Orleans, which the Company stopped operating in October, 2007, and decreased income from Trump International Sonesta Beach Resort following the termination by the Company of the management agreement for this hotel effective April 1, 2008 (see Note 2).

2007 versus 2006: Total revenues, excluding other revenues from managed and affiliated properties, were $67,938,000 in 2007 compared to $77,595,000 in 2006, a decrease of $9,657,000. Revenues from Sonesta Beach Resort Key Biscayne, which closed for operations on August 31, 2006 were $19,341,000 in 2006. The Company contributed the land and improvements to a development partnership, in which it is a 50% owner, with the intent to redevelop the site. Revenues at Royal Sonesta Hotel Boston increased from $26,408,000 in 2006 to $29,377,000 in 2007, an increase of $2,969,000, and Royal Sonesta Hotel New Orleans increased revenues from $27,894,000 in 2006 to $31,888,000 in 2007, an increase of $3,994,000. Demand in Boston was strong in 2007 compared to 2006, and Royal Sonesta Hotel New Orleans continued to recover from the after-effects of Hurricane Katrina. Revenues from management activities increased from $3,952,000 in 2006 to $6,673,000 in 2007, an increase of $2,721,000. This increase was primarily due to higher fee income from the Company’s managed hotels in Coconut Grove and Sunny Isles, Florida, and from the Company’s managed operations in Egypt. A more detailed analysis of the revenues by hotel, and of our management income, follows.

Revenues at Sonesta Beach Resort Key Biscayne, which closed for operations on August 31, 2006, were $19,341,000 during the 2006 period. In April 2005, the Company contributed the land and improvements of the Key Biscayne Resort to a development partnership in which it is a 50% limited partner, with the objective to redevelop the hotel’s site. Additional information regarding this transaction is provided in Note 3 – Investment in Development Partnership.

Royal Sonesta Hotel Boston reported revenues during 2007 of $29,377,000 compared to $26,408,000 in 2006, representing an increase of $2,969,000, or 11%. This increase was primarily due to an increase in room revenues of $2,573,000. Room revenues per available room (“REVPAR”) increased by 15% in 2007 compared to 2006, due to both an increase in occupancy levels as well as average room rates achieved. Increases in room revenue were primarily from the transient market segment, resulting from continued strong demand in the Boston hotel market. The hotel’s room nights sold to groups and conventions business declined slightly in 2007, which accounts for the modest increase in revenues from other sources, including food and beverage.

Revenues at Royal Sonesta Hotel New Orleans during 2007 were $31,888,000 compared to $27,894,000 in 2006, which represented an increase of $3,994,000, or 14%. Of the increase in revenues, approximately $1,724,000 was due to increased room revenues, resulting from a 9% increase in REVPAR. Occupancies in 2007 improved, but increases in average room rates achieved were modest, as many hotels competed for limited business in the post-Katrina era. The remaining increase in revenues of $2,270,000 was primarily from additional food and beverage revenues. During 2006, especially in the first half, the Hotel received very little group and convention business in the aftermath of Hurricane Katrina, which struck New Orleans in August 2005. In 2007, the Hotel was able to capture much more group business which provided the Hotel with much higher food and beverage revenues, including banqueting business.

Revenues from management activities increased from $3,952,000 in 2006 to $6,673,000 in 2007, an increase of $2,721,000. Management income in 2007 from Sonesta Bayfront Hotel Coconut Grove increased by $797,000 and income from Trump International Sonesta Beach Resort Sunny Isles increased by $974,000 compared to last year. Net operating income of both the Coconut Grove and Sunny Isles hotels improved substantially in 2007 compared to 2006. The Company’s fees from these properties depend on profits achieved. Income from the Company’s managed operations in Egypt increased by $641,000 in 2007 compared to 2006, which represented a 38% increase. Business in Egypt improved substantially in 2007, both in the resort and city hotels.

Operating Income

| OPERATING INCOME/(LOSS) | ||||||||||||

| (in thousands) | ||||||||||||

| 2008 | 2007 | 2006 | ||||||||||

| Sonesta Beach Resort Key Biscayne | $ | -- | $ | -- | $ | (1,073 | ) | |||||

| Royal Sonesta Hotel Boston | 5,464 | 4,926 | 2,416 | |||||||||

| Royal Sonesta Hotel New Orleans | 144 | 885 | 450 | |||||||||

| Operating income from hotels after management and service fees | 5,608 | 5,811 | 1,793 | |||||||||

| Management activities and other income | (2,216 | ) | (3,583 | ) | (5,622 | ) | ||||||

| Subtotal | 3,392 | 2,228 | (3,829 | ) | ||||||||

| Income from Management Agreement settlement, net | 3,279 | -- | -- | |||||||||

| Operating income (loss) | $ | 6,671 | $ | 2,228 | $ | (3,829 | ) | |||||

2008 versus 2007: The Company recorded operating income in 2008 of $6,671,000, compared to operating income of $2,228,000 in 2007, an increase of $4,443,000. In the 2008 third quarter, the Company recorded pre-tax income of $3,279,000 related to the settlement of a dispute with the owner of Trump International Sonesta Beach Resort. The Company terminated the management agreement for this property effective April 1, 2008 (see Note 2). Operating income at Royal Sonesta Hotel Boston increased by $538,000 compared to 2007 due to a 5% increase in revenues at this property. Operating income at Royal Sonesta Hotel New Orleans decreased by $741,000, mainly due to higher rent expense incurred under the lease under which the Company operates the hotel. Operating losses from management activities decreased by $1,367,000 to $2,216,000 in 2008, primarily due to higher income achieved from the Company’s managed hotels and cruise ships in Egypt. A more detailed discussion of the changes in operating income by location follows.

Royal Sonesta Hotel Boston increased operating income during 2008 by $538,000 to $5,464,000. Revenues during 2008 increased by $1,401,000, but were partially offset by a 4% increase in expenses, totaling $863,000. The expense increase was almost entirely due to a 5% increase in cost and operating expenses, totaling $624,000. The hotel operated at a higher occupancy level in 2008 compared to 2007, resulting in increased payroll expenses. In addition, the hotel incurred

5

higher commissions and reservations costs, increases in linens and guest supplies expense, as well as increased employee benefit costs. In December 2008, the hotel incurred severance expenses related to layoffs following the decline in business in late 2008.

Operating income from Royal Sonesta Hotel New Orleans decreased from $885,000 in 2007 to $144,000 in 2008. Increases in revenues of $907,000 were more than offset by increased expenses of $1,648,000. The hotel expensed $303,000 in 2008 for costs incurred during 2006, 2007 and 2008 related to the potential addition of a spa in the hotel, following its decision to postpone this project because of the high cost. Rent expense increased by $1,185,000 in 2008 compared to 2007. The Company operates the hotel under a lease, and rent is equal to 75% of net cash flow. The rent increase was due in part to higher operating profits achieved in 2008 compared to 2007. In addition, the hotel spent less on capital additions in 2008 compared to previous year. Under the lease, capital expenditures are deducted from cash flow for rent purposes. Excluding the rent increase and development cost write off, the hotel’s total expenses were virtually the same in 2008 as in 2007. Costs and operating expenses, as well as advertising and repairs and maintenance costs, increased slightly, but this increase was offset by decreased real estate tax expense in 2008 due to a favorable abatement received from the City of New Orleans. Operating profits from the hotel’s laundry, which also services third party hotels, decreased by $266,000 in 2008 compared to 2007. This was in part due to the loss of revenues from Chateau Sonesta Hotel New Orleans, which was operated by the Company under a management agreement until October, 2007, as well as increased costs and operating expenses of the laundry, including utility costs.

The Company’s loss from management activities, which is computed after giving effect to management fees from owned and leased hotels, decreased by $1,367,000 to $2,216,000 in 2008. Revenues increased by $1,306,000, primarily from increased fee income from the Company’s managed operations in Egypt. Expenses related to these activities decreased by $61,000. Corporate expenses in 2008 included $720,000 related to an employment agreement with Roger Sonnabend, the Company’s former Executive Chairman of the Board who passed away in December 2008. The 2008 expenses also included approximately $250,000 in costs related to a hotel project in Miami. The Company started to work on this project during the summer of 2008, but decided in February 2009 not to further pursue this opportunity. The Company also incurred higher legal costs related to the negotiation of management agreements for additional hotels, including the aforementioned project. Expenses in 2007 included $691,000 based on an employment agreement following the retirement of a long term Company executive, Mr. Paul Sonnabend. In addition, the Company spent approximately $265,000 in 2007 on legal and other costs in connection with a review of the Company’s strategic options to enhance shareholder value.

2007 versus 2006: The Company recorded operating income in 2007 of $2,228,000, compared to an operating loss of $3,829,000 in 2006, representing an improvement of $6,057,000. Sonesta Beach Resort Key Biscayne, which closed for operations on August 31, 2006, reported an operating loss of $1,073,000 in the eight-month period it operated in 2006. Royal Sonesta Hotel Boston improved its operating income from $2,416,000 in 2006 to $4,926,000 in 2007 as a result of strong revenue growth and tight expense controls. Operating losses from management activities decreased by $2,039,000 to $3,583,000 in 2007. A more detailed discussion of the changes in operating income by location follows.

Sonesta Beach Resort Key Biscayne, which closed on August 31, 2006 (see Note 3 – Investment in Development Partnership), recorded an operating loss of $1,073,000 during 2006. The 2006 operating loss was primarily from additional depreciation charges totaling $2.5 million in 2006, from the revision of useful lives of certain furniture and equipment, which became obsolete following the closure of the hotel in August 2006. During the period the hotel was operating in 2006, it reported a substantial operating cash flow. The operating loss of $1,073,000 was primarily a result of depreciation expense of $4,038,000, and, in addition, the hotel had minimal capital expenditures due to the anticipated closing. Since the hotel’s debt was repaid in April 2005 no interest expense was incurred during 2006.

Royal Sonesta Hotel Boston increased operating income from $2,416,000 in 2006 to $4,926,000 in 2007, an increase of $2,510,000. Revenues increased by $2,969,000 due to strong demand in the Boston hotel market, and overall expenses only increased by $459,000, representing a 2% increase, due to strict expense controls. Increased costs and operating expenses and depreciation expense were partially offset by lower maintenance costs, and a decrease in human resources expense, since the 2006 expenses included the cost of recruiting and relocating a new General Manager for the Hotel. In addition, employee benefit costs decreased following the freeze of the Company’s pension plan effective December 31, 2006.

Royal Sonesta Hotel New Orleans reported an increase in operating income of $435,000, improving operating income to $885,000 in 2007 compared to 2006. Revenues in 2007 increased by $3,994,000, and expenses increased by $3,559,000. The increase in expenses was primarily due to increased costs and operating expenses, including payroll expense. The 2007 revenue growth was primarily from increased food and beverage revenues, which have a much lower profit margin compared to rooms income. In addition, the Hotel’s staffing levels during 2006, especially during the first quarter, were much lower than in 2007, since many of its employees were unable to return to New Orleans in the aftermath of Hurricane Katrina. The Hotel also experienced increased payroll costs in 2007 due to the continuing labor shortages in New Orleans. Lower employee benefit costs due to the freeze of the Company’s Pension Plan partially offset the increase in payroll costs. The Hotel increased its sales and marketing expenditures in 2007 compared to 2006 in an effort to generate additional business.

The Company’s loss from management activities decreased from $5,622,000 in 2006 to $3,583,000 in 2007. The Company’s loss from management activities is computed after giving effect to management and marketing fees from owned and leased hotels. Revenues from management increased by $2,722,000 compared to last year, primarily due to increased management income from Sonesta Bayfront Hotel Coconut Grove and Trump International Sonesta Beach Resort Sunny Isles, and additional income from the Company’s managed operations in Egypt. Expenses related to these activities increased by $683,000 in 2007 compared to 2006. Decreases in corporate sales and marketing expenditures, due to a restructuring of the Company’s regional sales offices, and lower employee benefit costs due to the freeze of the Company’s Pension Plan, were offset by increased administrative and general expenses and depreciation expense. Administrative and general expenses included costs related to the retirement of a long-term company executive. This expense of $691,000 was based on an employment agreement. In addition, administrative and general expenses included $265,000 in legal and other costs incurred in connection with a review of the Company’s strategic options to enhance shareholder value. The Company completed the review in December 2007, and decided to continue operating as an independent entity. Depreciation expense included an additional expense of $567,000 related to accelerated depreciation of an investment the Company made in Trump International Sonesta Beach Resort. The Company invested $2,268,000 in the Hotel in 2003, which it was amortizing over the initial ten-year term of the management contract. Since the Company decided to exercise an early termination option (see Note 2

6

– Operations) the Company relinquished management of this property effective April 1, 2008, and as a result accelerated the depreciation of the remaining investment in the Hotel.

Other Income and Deductions

Interest expense, which consists entirely of interest paid on the Company’s mortgage loan secured by Royal Sonesta Hotel Boston, decreased by $42,000 in 2008 compared to 2007, due to the principal payments made on the loan during 2008. No principal payments were made in 2007.

Interest income increased from $1,584,000 in 2006 to $1,720,000 in 2007, but decreased to $1,182,000 in 2008. The decrease in 2008 was the result of lower income earned on the Company’s short-term cash investments, due to lower rates of return. In addition, the 2008 period included lower interest earned on a loan to the owner of Sonesta Bayfront Hotel Coconut Grove. This loan was repaid during 2008. The decrease in interest income was partially offset by interest earned on a new loan made to the owners of Sonesta Beach Resort and Sonesta Club, in Sharm El Sheikh, and from income received related to the settlement of a dispute with the owner of Trump International Sonesta Beach Resort, in Sunny Isles, Florida, which the Company managed until April 1, 2008 (see Note 2). The increase in interest income in 2007 compared to 2006 was primarily due to an increase in short-term investment income on the Company’s cash balances.

The $576,000 gain on sale of assets in 2008 resulted primarily from a $422,000 gain on the sale of a co-op unit the Company owned in New York City to the Company’s Executive Chairman. The sale price was $700,000. The Company’s Board of Directors approved this transaction. In addition, the Company realized a gain on the sale of art in 2008. The gain on the sale of assets of $214,000 during the 2007 period was almost entirely from the sale of art.

Federal, State and Foreign Income Taxes

In 2008, the Company recorded a net tax provision of $1,377,000 on its pre-tax income of $5,457,000. The Company is able to take substantial credits for foreign taxes paid in 2008, and for foreign taxes paid in prior years which had been carrying forward. In addition, the Company benefited from current and prior year’s general business credits, including work opportunity tax credits related to Hurricane Katrina. The Company also recorded a state income tax benefit of $216,000 for Massachusetts taxes resulting from changes enacted in tax laws during 2008. These changes include conforming to federal entity classification rules and adopting a unitary method of taxation.

In 2007, the Company recorded a net tax benefit of $151,000, even though pre-tax income equaled $1,186,000. The Company was able to take substantial credits for foreign taxes paid in 2007, and foreign taxes paid in previous years, which it had been carrying forward. In addition, the Company benefited from general business credits, including work opportunity tax credits related to Hurricane Katrina.

Liquidity and Capital Resources

The Company had cash and cash equivalents of approximately $37.5 million at December 31, 2008. As of that date, the majority of these funds were held in money market mutual funds which participate in the U.S. Treasury Department Temporary Guarantee Program for Money Market Funds, and in money market funds which invest solely in U.S. government obligations.

In February 2008 the Company paid a special dividend of $1 per share ($3,698,000). In October 2008, the Company declared an additional special dividend of $0.15 per share ($555,000), which was paid in January, 2009. These were in addition to dividends of $0.20 per share paid during each of the years 2006, 2007 and 2008. Total dividends declared in 2008 equaled $4,993,000.

The Company contributed $1,280,000 and $1,722,000 to its Pension Plan in 2008 and 2007, respectively.

From April 2003 through March 2008, the Company operated Trump International Sonesta Beach Resort Sunny Isles, in Florida, under a management agreement. The Company had a one-time right to cancel the management agreement, effective five years after the opening date, upon 6 months notice, and receive repayment of advances it was obligated to make for net operating losses and certain minimum returns due to the hotel’s owner. The amount due upon termination, $7,031,000, was disputed by the hotel’s owner. An arbitration procedure to resolve the dispute commenced in April 2008 and was settled in October 2008. The Company received a total of $5,002,000, which included the amount of the settlement of $4,929,000, and its share of the interest earned on an escrow account in the amount of $73,000. Of the settlement amount, $1,135,000 repaid the Company’s outstanding receivable (see Note 4). After deducting $515,000 for legal and other costs in connection with the arbitration, the remaining amount of $3,279,000 was recorded as income in the 2008 third quarter. This amount relates to fees due to the Company which were not previously recorded since the hotel’s profits were insufficient to pay them, and the collectability was uncertain.

In January 2008, the Company agreed to convert approximately $1.6 million of receivables for fees and expenses from two hotels it manages in Sharm El Sheikh, Egypt into a five-year loan. This was part of a transaction which also included the extension until 2024 of the management agreement for Sonesta Club Sharm El Sheikh, which otherwise would have expired at the end of 2009. In return, the Company agreed to pay $500,000, which payment was made by reducing outstanding receivables from Sonesta Club.

Under the terms of the partnership agreement for a development project in which the Company is a 50% limited partner, the Company received monthly payments of $125,000 since August 2006. These payments reduced the carrying value of the Company’s investment. The partnership’s general partner suspended these payments as of February 2008, in order to conserve cash for development expenditures. Previously, the partnership deferred payments of a monthly development fee to the general partner. During the 2009 first quarter, the Company advanced $842,000 to the partnership (see also Note 3).

The Company operates the Sonesta Bayfront Hotel Coconut Grove, in Miami, which is a condominium hotel that opened in April 2002. Under its agreements, the Company is committed to fund net operating losses, and to provide the hotel’s owner with a minimum annual return ($442,000 during 2008), adjusted annually by increases in the Consumer Price Index. The management agreement can be terminated by the hotel’s owner if the Company fails to cure shortfalls against a minimum target return ($1,001,000 during 2008), adjusted annually by increases in the CPI. The hotel’s 2008 and 2007 net operating profits were sufficient to cover the owner’s target returns and to earn fees from the hotel of $1,039,000 and $947,000 in 2008 and 2007, respectively. In October 2008, the Company received $2,627,000 in connection with the repayment of a loan made to the owner of the hotel for initial furniture, fixtures and equipment and pre-opening expenses.

In October 2007, the Company agreed to terminate its management agreement for Chateau Sonesta Hotel New Orleans. In connection with the termination, the Company received $1,500,000, which included the repayment of advances the Company made to the Hotel’s owner following Hurricane Katrina and interest thereon. The Company also received a note for $1.6 million, which accrues interest at 8%. The note,

7

which is unsecured, represents a settlement for amounts owed for deferred management fees and a bonus incentive fee which were not previously recorded, as collectability was uncertain, as well as interest on the aforementioned fees and unpaid interest on the advances. Since payments on the note prior to maturity, in September 2010, are dependent on future cash flows of the hotel, the Company has fully reserved this note receivable. The Company will recognize loan payments as income when cash payments are received. The Company entered into a license agreement for the use of its name with the owner of the hotel, which agreement was terminated in October 2008.

Brewster Wholesale Corporation, a wholly owned subsidiary of the Company, provides purchasing services to the Company’s hotels and third party clients. In 2007 and 2008, Brewster contracted to provide purchasing services for two major refurbishment projects for a third-party client. Deposits received against orders placed on behalf of this client of approximately $174,000 and $1,700,000 are included in Restricted Cash and Advance Deposits on the Company’s balance sheet at December 31, 2008 and 2007, respectively.

Company management believes that its present cash balances will be more than adequate to meet its cash requirements for 2009 and for the foreseeable future.

As of December 31, 2008, the Company’s fixed contractual obligations were as follows (in thousands):

| YEAR | ||||||||||||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | Thereafter | Total | ||||||||||||||||||||||

| Long-Term Debt Obligations | $ | 1,163 | $ | 31,839 | $ | -- | $ | -- | $ | -- | $ | -- | $ | 33,002 | ||||||||||||||

| Operating Leases | 744 | 702 | 636 | 296 | 104 | -- | 2,482 | |||||||||||||||||||||

| Total | $ | 1,907 | $ | 32,541 | $ | 636 | $ | 296 | $ | 104 | $ | -- | $ | 35,484 | ||||||||||||||

The Company’s hotels also have certain purchase obligations, primarily for maintenance and service contracts. These are not included in the contractual obligations since the amounts committed are not material, and because the majority of these contracts may be terminated on relatively short notice.

8

Economic Outlook

The economic recession affected the Company’s business in the 2008 fourth quarter, and this has continued during the first quarter of 2009. Hotel business depends heavily on economic activity, and the Company’s U.S. hotels will be impacted in 2009 both from lower consumer demand as well as diminished corporate spending. Both of the Company’s Boston and New Orleans hotels depend heavily on corporate groups and conventions. Cost saving initiatives have been implemented, including layoffs at the Boston hotel and salary freezes at the Company’s Corporate office and for hotel management. In addition, the Company will temporarily halt matching contributions to its 401(k) Plan, effective April 1, 2009.

It is impossible to predict the extent of the impact of the poor economic environment on the Company’s 2009 results. The Company does have adequate cash resources to continue operations, and meet its foreseeable needs.

Review of Strategic Options

In June 2007, the Company’s Board of Directors retained Goldman, Sachs & Company to explore, under the direction of a special committee comprised of independent directors, strategic options available to the Company to increase shareholder value. After considerable efforts evaluating alternatives with Goldman, Sachs & Company, and in light of the conditions affecting the real estate and financing markets, the Company completed the review in December 2007, and decided to continue to operate and license hotels in the United States and abroad as an independent entity. Sonesta’s Board of Directors will continue to monitor both the real estate and financial markets to determine appropriate strategy in order to maximize shareholder value.

Critical Accounting Policies and Estimates

The consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States, which require the Company to make estimates and assumptions. The Company believes that of its significant accounting policies, the following may involve a higher degree of judgment and complexity.

| · | Revenue recognition – a substantial portion of our revenues result from the operations of our owned and leased hotels. These revenues are recognized at the time that lodging and other hotel services are provided to our guests. Certain revenues, principally those relating to groups using lodging and banquet facilities, are billed directly to the customers. These revenues are subject to credit risk, which the Company manages by establishing allowances for uncollectible accounts. If management establishes allowances for uncollectible accounts that are insufficient, it will overstate income, and this will result in increases in allowances for uncollectible accounts in future periods. |

Management, license and service fees represents fee income from hotels operated under management agreements, and license fees from hotels to which the Company has licensed the use of the “Sonesta” name. Management fees include base fees and marketing fees, which are generally based on a percentage of gross revenues, and incentive fees, which are generally based on the hotels’ profitability. These fees are typically based on revenues and income achieved during each calendar year. Incentive fees, and management fees of which the receipt is based on annual profits achieved, are recognized throughout the year on a quarterly basis based on profits achieved during the interim periods when our agreements provide for quarterly payments during the calendar years they are earned, and when such fees would be due if the management agreements were terminated. As a result, during quarterly periods, fee income may not be indicative of eventual income recognized at the end of each calendar year due to changes in business conditions and profitability. License fees are earned based on a percentage of room revenues of the hotels.

The Company records the reimbursement of certain expenses incurred on behalf of managed and affiliated properties, and the costs incurred on behalf of owners of managed properties on a “gross” basis in revenues and costs. These costs relate primarily to payroll and benefit costs of managed properties in which the Company is the employer.

| · | Impairment of long lived assets – the Company monitors the carrying value of its owned properties and its investment in development property from the perspective of accounting rules relating to impairment. A requirement to assess impairment would be triggered by so called “impairment indicators”. For us, these might include low rates of occupancy, operating costs in excess of revenues, or maturing mortgages for which there were no suitable refinancing options. Impairment also needs to be considered with respect to costs incurred for new hotel investments or development opportunities that are under study. The Company monitors these costs on a quarterly basis and if a pending project is no longer considered to be viable, the cost is charged against income. If the Company estimates incorrectly or misjudges the impairment indicators, it may result in the Company failing to record an impairment charge, or recording a charge which may be inaccurate. |

| · | Pension Benefits – the Company maintains a defined benefit plan for eligible employees, which was frozen effective December 31, 2006. Costs and liabilities are developed from actuarial valuations. In these valuations are assumptions relating to discount rates, expected return on assets and employee turnover. Differences between assumed amounts and actual performance will impact reported amounts for the Company’s pension expense, as well as the liability for future pension benefits. |

| · | Sonesta Bayfront Hotel Coconut Grove – the Company operates a condominium hotel under a management agreement, under which it is committed to fund net operating losses, and provide the owner with minimum annual returns ($442,000 during 2008), adjusted annually by increases in the Consumer Price Index, beginning as of January 1, 2004. In addition, starting in 2005, the management agreement may be subject to termination if the Company elects not to cure shortfalls against a minimum target return ($1,001,000 during 2008), adjusted annually by increases in the Consumer Price Index. Under its agreements, the Company is entitled to management and marketing fees based on revenues, and incentive fees based on profits. In case the aforementioned annual minimum returns and minimum target returns are not met, the Company’s policy is to eliminate management and marketing fees from its revenues. If the amount of the shortfall exceeds the fee income, the Company will book the additional amount as an administrative and general expense. |

| · | Trump International Sonesta Beach Resort - until April 2008, the Company operated a condominium hotel in Sunny Isles Beach, Florida. The hotel opened in April 2003. Under the management agreement, the Company was entitled to management and marketing fees based on the hotel’s revenues, and incentive fees based on the hotel’s net operating income. The Company was obligated to advance funds for operating losses and to provide |

9

a minimum annual return of $800,000 to the hotel’s owner, starting as of November 1, 2004. From the opening in April 2003 until November 1, 2004, the Company was obligated to advance 50% of any net operating losses. Amounts advanced under these obligations were subject to repayment, without interest, out of future profits in excess of the aforementioned minimum return. During the years the minimum returns were not earned, the Company eliminated the fee income earned from the property from its revenues. If the amounts of the shortfalls exceeded the total fee income, the Company reflected such excess amounts either as long-term receivables and advances on its balance sheet, or recorded an expense equal to the amount advanced. The Company exercised its right to terminate the management agreement effective April 1, 2008, and receive back advances it made under the agreement totaling $7,031,000. In October 2008, following the settlement of a dispute, the Company received $5,002,000 in connection with the termination of the management agreement, which included the repayment of advances and the payment of fees which were not previously recorded. The Company had invested in the furniture, fixtures and equipment of the non-guestroom areas of the hotel, an amount of $2,268,000. This was included in other long-term assets, and was being amortized over the 10-year initial term of the management agreement. As a result of the decision to terminate the agreement, the Company accelerated the depreciation of the long-term asset during the 2007 fourth quarter.

| · | Accounting for 2005 Asset Transfer – in April 2005, the Company completed the transfer of the land and improvements of Sonesta Beach Key Biscayne to a development partnership, of which the Company is a 50% partner. At that time, the Company received non-refundable proceeds of approximately $60 million, and is entitled to a priority return of an additional $60 million from the sale proceeds of residential condominium units to be constructed on the site. Since the Company has a continuing involvement in the ownership of the development, the initial gain is being deferred. A comprehensive description of this transaction is included in Note 3 – Investment in Development Partnership. |

10

Quantitative and Qualitative Disclosure of Market Risk

The Company is exposed to market risk from changes in interest rates. The Company uses fixed rate debt to finance the ownership of Royal Sonesta Boston. The table that follows summarizes the Company’s fixed rate debt obligations outstanding at December 31, 2008, and presents the fair value of the debt based on current prevailing interest rates for similar financing. This information should be read in conjunction with Note 5 — Borrowing Arrangements.

Short and Long Term Debt (in thousands) maturing in:

| YEAR | ||||||||||||||||||||

| 2009 | 2010 | Thereafter | Total | Fair Value | ||||||||||||||||

| Fixed rate | $ | 1,163 | $ | 31,839 | $ | -- | $ | 33,002 | $ | 33,944 | ||||||||||

| Average interest rate | 8.6 | % | 8.6 | % | ||||||||||||||||

Selected Quarterly Financial Data

Following are selected quarterly financial information for the years ended December 31, 2008 and 2007.

| (in thousands except for per share data) | ||||||||||||||||

| 2008 | ||||||||||||||||

1st | 2nd | 3rd | 4th | |||||||||||||

| Revenues | $ | 17,798 | $ | 20,422 | $ | 16,398 | $ | 16,934 | ||||||||

| Other revenues from managed and affiliated properties | 5,117 | 1,346 | 1,286 | 1,216 | ||||||||||||

| Total revenues | 22,915 | 21,768 | 17,684 | 18,150 | ||||||||||||

| Operating income (loss) | 80 | 2,730 | 4,411 | (550 | ) | |||||||||||

| Net income (loss) | 90 | 1,506 | 2,792 | (308 | ) | |||||||||||

| Net income (loss) per share | $ | 0.02 | $ | 0.41 | $ | 0.76 | $ | (0.09 | ) | |||||||

| 2007 | ||||||||||||||||

1st | 2nd | 3rd | 4th | |||||||||||||

| Revenues | $ | 15,383 | $ | 18,118 | $ | 15,599 | $ | 18,839 | ||||||||

| Other revenues from managed and affiliated properties | 4,900 | 4,678 | 4,537 | 4,631 | ||||||||||||

| Total revenues | 20,283 | 22,796 | 20,136 | 23,470 | ||||||||||||

| Operating income (loss) | (737 | ) | 1,636 | 809 | 520 | |||||||||||

| Net income (loss) | (821 | ) | 762 | 442 | 954 | |||||||||||

| Net income (loss) per share | $ | (0.22 | ) | $ | 0.21 | $ | 0.12 | $ | 0.25 | |||||||

11

Fourth Quarter Results

Revenues

| TOTAL REVENUES | ||||||||||||

| (in thousands) | ||||||||||||

NO. OF ROOMS | 2008 | 2007 | ||||||||||

| Royal Sonesta Hotel Boston | 400 | $ | 7,344 | $ | 8,128 | |||||||

| Royal Sonesta Hotel New Orleans | 500 | 7,884 | 8,496 | |||||||||

| Management and service fees | 1,706 | 2,215 | ||||||||||

| Total revenues, excluding other revenues from managed and affiliated properties | $ | 16,934 | $ | 18,839 | ||||||||

Total revenues, excluding other revenues from managed and affiliated properties, during the fourth quarter of 2008 were $16,934,000 compared to $18,839,000 during the fourth quarter of 2007, a decrease of $1,904,000. Revenues at both the Company’s Boston and New Orleans hotels were affected by the economic downturn during the 2008 fourth quarter.

Royal Sonesta Hotel Boston reported fourth quarter 2008 revenues of $7,344,000 compared to $8,128,000 during the fourth quarter of 2007, representing a $784,000, or 10%, decrease. Room revenues decreased by $442,000 in the 2008 fourth quarter compared to last year, due to an 8.5% decrease in room revenues per available room (“REVPAR”). Occupancies were virtually the same in the fourth quarter of 2008 compared to 2007, but the hotel’s average daily room rate declined substantially. Group and convention business in particular decreased during the 2008 quarter. The hotel made up the deficiency in occupancy with increased transient sales, albeit at lower rates. Revenues from other sources declined by $342,000 in the 2008 quarter compared to last year due to a decrease in banqueting revenues, resulting from the aforementioned decrease in group and convention business.

Royal Sonesta Hotel New Orleans recorded 2008 fourth quarter revenues of $7,884,000 compared to $8,496,000 during the 2007 fourth quarter, a decrease of $612,000, or 7%. Room revenues declined by $478,000 due to a 9% REVPAR decrease. Both lower occupancies as well as average room rates achieved contributed to the REVPAR decrease. The loss in occupancy was primarily from group and convention business, which also affected the hotel’s banqueting revenues.

Revenues from management activities decreased by $509,000 to $1,706,000 during the 2008 fourth quarter. This was primarily due to decreased fee income from Trump International Sonesta Beach Resort, Sunny Isles, which was only partially offset by an increase in fee income from the Company’s managed hotels in Egypt. The Company terminated its management agreement for the Sunny Isles hotel, effective April 1, 2008 (see Note 2).

Operating Income

| OPERATING INCOME (LOSS) | ||||||||

| (in thousands) | ||||||||

| 2008 | 2007 | |||||||

| Royal Sonesta Hotel Boston | $ | 1,257 | $ | 1,766 | ||||

| Royal Sonesta Hotel New Orleans | (373 | ) | 71 | |||||

| Operating income from hotels after management and service fees | 884 | 1,837 | ||||||

| Management activities and other income | (1,434 | ) | (1,317 | ) | ||||

| Operating income (loss) | $ | (550 | ) | $ | 520 | |||

The Company reported an operating loss of $550,000 during the fourth quarter of 2008, compared to operating income of $520,000 in the fourth quarter of 2007.

Royal Sonesta Hotel Boston reported operating income of $1,257,000 in the 2008 fourth quarter compared to $1,766,000 during the 2007 fourth quarter, a decrease of $509,000. Decreases in revenues of $784,000 were partially offset by decreased expenses of $275,000. The decrease in expenses was primarily from lower costs and operating expenses of $283,000 (an 8% decrease). Management reduced payroll and other expenses in response to the decline in business levels.

Royal Sonesta Hotel New Orleans reported an operating loss of $373,000 during the 2008 fourth quarter compared to operating income of $71,000 during the 2007 fourth quarter, a decrease of $444,000. Revenues decreased by $612,000, and were partially offset by a $168,000 decrease in expenses. The decrease was primarily from lower costs and operating expenses and lower rent expense due to the lower operating profits.

Operating loss from management activities was $1,434,000 in the 2008 fourth quarter, a $117,000 increase compared to the 2007 fourth quarter loss of $1,317,000. Revenue decreases of $509,000 were partially offset by lower expenses related to these activities of $392,000. The decrease was primarily from lower depreciation expense. The 2007 quarter included an additional depreciation charge of $567,000 related to accelerated depreciation of an investment the Company made in Trump International Sonesta Beach Resort Sunny Isles, following its decision to terminate the management agreement for this hotel (see also Note 2 – Operations). Administrative and general expenses increased during the 2008 fourth quarter due to legal fees associated with the negotiation of management agreements, as well as a $250,000 charge for costs incurred related to a hotel project in Miami. The Company started to work on this project during the summer of 2008, but decided in February 2009 not to further pursue this opportunity.

12

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

For the years ended December 31, 2008 and 2007

(in thousands, except for per share data)

| 2008 | 2007 | |||||||

| Revenues: | ||||||||

| Rooms | $ | 41,052 | $ | 39,121 | ||||

| Food and beverage | 17,519 | 17,113 | ||||||

| Management, license and service fees | 7,956 | 6,635 | ||||||

| Parking, telephone and other | 5,025 | 5,069 | ||||||

| 71,552 | 67,938 | |||||||

| Other revenues from managed and affiliated properties | 8,965 | 18,747 | ||||||

| Total revenues | 80,517 | 86,685 | ||||||

| Costs and expenses: | ||||||||

| Costs and operating expenses | 30,819 | 29,878 | ||||||

| Advertising and promotion | 5,608 | 5,427 | ||||||

| Administrative and general | 14,405 | 13,823 | ||||||

| Human resources | 1,191 | 1,122 | ||||||

| Maintenance | 3,549 | 3,573 | ||||||

| Rentals | 5,392 | 4,168 | ||||||

| Property taxes | 1,358 | 1,672 | ||||||

| Depreciation and amortization | 5,838 | 6,047 | ||||||

| 68,160 | 65,710 | |||||||

| Other expenses from managed and affiliated properties | 8,965 | 18,747 | ||||||

| Total costs and expenses | 77,125 | 84,457 | ||||||

| Income from Management Agreement settlement, net | 3,279 | -- | ||||||

| Operating income | 6,671 | 2,228 | ||||||

| Other income (deductions): | ||||||||

| Interest expense | (2,970 | ) | (3,012 | ) | ||||

| Interest income | 1,182 | 1,720 | ||||||

| Foreign exchange profit (loss) | (2 | ) | 36 | |||||

| Gain on sales of assets | 576 | 214 | ||||||

| (1,214 | ) | (1,042 | ) | |||||

| Income before income taxes | 5,457 | 1,186 | ||||||

| Income tax expense (benefit) | 1,377 | (151 | ) | |||||

| Net income | $ | 4,080 | $ | 1,337 | ||||

| Basic and diluted income per share | $ | 1.10 | $ | 0.36 | ||||

| Dividends per share | $ | 1.35 | $ | 0.20 | ||||

| Weighted average number of shares outstanding | 3,698 | 3,698 | ||||||

See accompanying notes to consolidated financial statements.

13

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED BALANCE SHEETS

December 31, 2008 and 2007

(in thousands, except for per share data)

| 2008 | 2007 | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 37,463 | $ | 32,620 | ||||

| Restricted cash | 175 | 1,700 | ||||||

| Accounts and notes receivable: | ||||||||

| Trade, less allowance of $59 ($66 in 2007) for doubtful accounts | 5,407 | 7,676 | ||||||

| Other, including current portion of long-term receivables and advances | 1,001 | 1,151 | ||||||

| Total accounts and notes receivable | 6,408 | 8,827 | ||||||

| Inventories | 628 | 607 | ||||||

| Current deferred tax assets | 462 | 578 | ||||||

| Prepaid expenses and other current assets | 2,163 | 1,915 | ||||||

| Total current assets | 47,299 | 46,247 | ||||||

| Long-term receivables and advances | 992 | 3,776 | ||||||

| Deferred tax assets | 9,049 | 7,242 | ||||||

| Investment in development partnership (see Note 3) | 33,666 | 33,791 | ||||||

| Property and equipment, at cost: | ||||||||

| Land and land improvements | 2,102 | 2,102 | ||||||

| Buildings | 25,610 | 26,190 | ||||||

| Furniture and equipment | 30,150 | 31,413 | ||||||

| Leasehold improvements | 8,785 | 8,450 | ||||||

| Projects in progress | 472 | 246 | ||||||

| 67,119 | 68,401 | |||||||

| Less accumulated depreciation and amortization | 32,088 | 31,098 | ||||||

| Net property and equipment | 35,031 | 37,303 | ||||||

| Other long-term assets | 1,003 | 1,232 | ||||||

| $ | 127,040 | $ | 129,591 | |||||

See accompanying notes to consolidated financial statements.

14

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED BALANCE SHEETS

| 2008 | 2007 | |||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Current portion of long-term debt | $ | 1,163 | $ | 1,059 | ||||

| Accounts payable | 3,747 | 4,494 | ||||||

| Advance deposits | 1,281 | 2,936 | ||||||

| Accrued income taxes | 402 | 306 | ||||||

| Accrued liabilities: | ||||||||

| Salaries and wages | 1,772 | 2,000 | ||||||

| Rentals | 4,787 | 3,575 | ||||||

| Interest | 244 | 252 | ||||||

| Pension and other employee benefits | 1,612 | 2,341 | ||||||

| Other | 862 | 839 | ||||||

| 9,277 | 9,007 | |||||||

| Total current liabilities | 15,870 | 17,802 | ||||||

| Long-term debt | 31,839 | 33,002 | ||||||

| Deferred gain (see Note 3) | 64,481 | 64,481 | ||||||

| Pension liability, non-current | 9,338 | 4,553 | ||||||

| Other non-current liabilities | 1,386 | 1,206 | ||||||

| Commitments and contingencies (see Note 7) | ||||||||

| Stockholders’ equity: | ||||||||

| Common stock: | ||||||||

| Class A, $.80 par value | ||||||||

| Authorized--10,000 shares | ||||||||

| Issued – 6,102 shares at stated value | 4,882 | 4,882 | ||||||

| Retained earnings | 14,155 | 15,068 | ||||||

| Treasury shares – 2,404, at cost | (12,053 | ) | (12,053 | ) | ||||

| Accumulated other comprehensive income (loss) | (2,858 | ) | 650 | |||||

| Total stockholders’ equity | 4,126 | 8,547 | ||||||

| $ | 127,040 | $ | 129,591 | |||||

15

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

For the years ended December 31, 2008 and 2007

(in thousands, except for per share data)

| Common Shares Outstanding | Class A Common Stock | Treasury Shares at Cost | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Total Stockholders’ Equity | |||||||||||||||||

| 3,698 | Balance January 1, 2007 | $ | 4,882 | $ | (12,053 | ) | $ | 14,773 | $ | (231 | ) | $ | 7,371 | |||||||||

| -- | Cash dividends declared on common stock ($0.20 per share) | -- | -- | (740 | ) | -- | (740 | ) | ||||||||||||||

| -- | Net income | -- | -- | 1,337 | -- | 1,337 | ||||||||||||||||

| -- | Cumulative effect of change in accounting for sabbatical leaves | -- | -- | (302 | ) | -- | (302 | ) | ||||||||||||||

| -- | Pension Plan, actuarial gain recognized | -- | -- | -- | 881 | 881 | ||||||||||||||||

| 3,698 | Balance December 31, 2007 | 4,882 | (12,053 | ) | 15,068 | 650 | 8,547 | |||||||||||||||

| -- | Cash dividends declared on common stock ($1.35 per share) | -- | -- | (4,993 | ) | -- | (4,993 | ) | ||||||||||||||

| -- | Net income | -- | -- | 4,080 | -- | 4,080 | ||||||||||||||||

| -- | Pension plan, actuarial loss recognized | -- | -- | -- | (3,508 | ) | (3,508 | ) | ||||||||||||||

| 3,698 | Balance December 31, 2008 | $ | 4,882 | $ | (12,053 | ) | $ | 14,155 | $ | (2,858 | ) | $ | 4,126 | |||||||||

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

For the years ended December 31, 2008 and 2007

(in thousands)

| 2008 | 2007 | |||||||

| Net income | $ | 4,080 | $ | 1,337 | ||||

| Other comprehensive income (loss), net of tax: | ||||||||

| Pension Plan, actuarial income (loss) recognized | (3,508 | ) | 881 | |||||

| Comprehensive income | $ | 572 | $ | 2,218 | ||||

See accompanying notes to consolidated financial statements.

16

SONESTA INTERNATIONAL HOTELS CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

For the years ended December 31, 2008 and 2007

(in thousands)

| 2008 | 2007 | |||||||

| Cash provided by operating activities | ||||||||

| Net income | $ | 4,080 | $ | 1,337 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities | ||||||||

| Depreciation and amortization of property and equipment | 5,838 | 6,047 | ||||||

| Other amortization and non-cash expenses | 262 | 41 | ||||||

| Deferred federal and state income tax provision | 353 | 109 | ||||||

| Gain on sales of assets | (576 | ) | (214 | ) | ||||

| Changes in assets and liabilities | ||||||||

| Restricted cash | 1,526 | (1,700 | ) | |||||

| Accounts and notes receivable | (39 | ) | (412 | ) | ||||

| Inventories | (21 | ) | (75 | ) | ||||

| Prepaid expenses and other | 71 | 51 | ||||||

| Accounts payable | (1,301 | ) | 712 | |||||

| Advance deposits | (1,655 | ) | 2,107 | |||||

| Income taxes | (223 | ) | (446 | ) | ||||

| Accrued liabilities | (319 | ) | (112 | ) | ||||

| Cash provided by operating activities | 7,996 | 7,445 | ||||||

| Cash provided by investing activities | ||||||||

| Proceeds from sales of assets | 1,058 | 324 | ||||||

| Payments received from development partnership | 125 | 1,500 | ||||||

| Expenditures for property and equipment | (3,494 | ) | (4,267 | ) | ||||

| New loans and advances | (135 | ) | -- | |||||

| Payments received on long-term receivables and advances | 4,789 | 3,470 | ||||||

| Cash provided by investing activities | 2,343 | 1,027 | ||||||

| Cash used in financing activities | ||||||||

| Repayments of long-term debt | (1,058 | ) | -- | |||||

| Cash dividends paid | (4,438 | ) | (740 | ) | ||||

| Cash used in financing activities | (5,496 | ) | (740 | ) | ||||

| Net increase in cash and cash equivalents | 4,843 | 7,732 | ||||||

| Cash and cash equivalents at beginning of year | 32,620 | 24,888 | ||||||

| Cash and cash equivalents at end of year | $ | 37,463 | $ | 32,620 | ||||

See accompanying notes to consolidated financial statements.

17

SONESTA INTERNATIONAL HOTELS CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

| 1. | Basis of Presentation and Significant Accounting Policies |

Basis of Presentation:

Sonesta International Hotels Corporation (the Company) is engaged in the operation of hotels in Boston, Massachusetts; New Orleans, Louisiana; and Key Biscayne, Florida (until August 2006). The Company also operates, under management agreements, hotels in Coconut Grove, Florida, New Orleans, Louisiana (until October 2007) and Sunny Isles, Florida (until March 2008); and in Cairo, Sharm El Sheikh, Luxor, Taba, Hurghada and Port Said, Egypt. The Company also manages five Nile River cruise ships in Egypt. Sonesta has granted licenses, for which it receives fees, for the use of its name for hotels in St. Maarten, Peru and Brazil.

In April 2005, the Company transferred the land and improvements of Sonesta Beach Resort Key Biscayne to a development partnership, in which the Company is a 50% owner (see Note 3 – Investment in Development Partnership). The new partnership intends to redevelop the hotel’s site. The hotel closed for operations on August 31, 2006. Since the Company has a continuing interest in the development partnership, the historical results of Sonesta Beach Resort Key Biscayne are not accounted for as a discontinued operation.

Principles of Consolidation:

The consolidated financial statements include the results of operations of wholly-owned and leased properties, and fee income and certain revenues and costs from reimbursable expenses incurred at managed and affiliated properties. All significant intercompany balances and transactions have been eliminated. The Company has identified certain of its management agreements as variable interest entities in accordance with Financial Accounting Standards Board Interpretation No. 46(R), “Consolidation of Variable Interest Entities”. However, the Company does not believe it bears the majority of the risk of loss from the variable interest entity’s activities, nor is it entitled to receive the majority of the variable interest entity’s residual returns. As a result, these entities are not consolidated in the Company’s financial statements.

Foreign Currency Transactions:

Assets and liabilities denominated in foreign currency are converted at end of year rates, and income and expense items are converted at weighted average rates during the period. The net result of such conversions is charged or credited to the statement of operations.

Inventories:

Inventories consist of merchandise and supplies, and are stated at the lower of cost (first-in/first-out method) or market.

Revenue Recognition:

The Company’s revenues are primarily derived from (1) owned and leased hotels and (2) management, license and service fees.

| · | Owned and leased hotels – The majority of the Company’s income is derived from its owned and leased hotels from the rental of rooms, food and beverage sales as well as charges for parking, telephone and other incidental charges. These revenues are recognized when rooms are occupied and services have been rendered. |

| · | Management, license and service fees – Represents fee income from hotels operated under management agreements, and license fees from hotels to which the Company has licensed the use of the “Sonesta” name. Management fees include base fees and marketing fees, which are generally based on a percentage of gross revenues, and incentive fees, which are generally based on the hotels’ profitability. These fees are typically based on revenues and income achieved during each calendar year. Incentive fees, and management and marketing fees of which the receipt is based on annual profits achieved, are recognized throughout the year on a quarterly basis based on profits achieved during the interim periods when our agreements provide for quarterly payments during the calendar years they are earned, and when such fees would be due if the management agreements were terminated. As a result, during quarterly periods, fee income may not be indicative of eventual income recognized at the end of each calendar year due to changes in business conditions and profitability. License fees are earned based on a percentage of room revenues of the hotels. Revenues and expenses of hotels operated under management agreements are excluded from the Company’s consolidated statements of operations, except for certain costs described below. |

In accordance with the Emerging Issues Task Force, Issue no. 01-14, “Income Statement Characterization of Reimbursements received for ‘Out of Pocket’ expenses Incurred”, the reimbursements of certain expenses incurred on behalf of managed and affiliated properties, and the costs incurred on behalf of owners of managed properties are recorded on a “gross” basis in revenues and costs. These costs relate primarily to payroll and related costs of managed properties in which the Company is the employer. The revenue for these costs is included in Other revenue from managed and affiliated properties and the offsetting expense is included in Other expenses from managed and affiliated properties.

Advertising:

The cost of advertising is generally expensed as incurred.

Property and Equipment:

Property and equipment are stated at cost. Depreciation and amortization of items of property and equipment are computed on the straight-line method based on the following estimated useful lives:

| Buildings and building improvements: | |

| Owned properties | 10 to 40 years |

| Furniture and Equipment: | |

| Located in owned properties | 5 to 10 years |

| Located in leased properties | 5 to 10 years or remaining lease terms |

| Leasehold improvements: | Remaining lease terms |

Impairment of Long-Lived Assets and Long-Lived Assets to be Disposed of:

The carrying values of long-lived assets, which include property and equipment, an investment in a development partnership and intangibles, are evaluated periodically for impairment when impairment indicators are present. Future undiscounted cash flows of the underlying assets are compared to the assets’ carrying values. Adjustments to fair value are made if the sum of expected future undiscounted cash flows are less than book value. To date, no adjustments for impairment have been made.

Income Taxes:

We provide for income taxes in accordance with SFAS No. 109, “Accounting for Income Taxes”. The Company and its United States subsidiaries file a consolidated federal income tax return. Federal and foreign income taxes are provided on earnings of foreign subsidiaries.

18

Fair Value of Financial Instruments:

The Company's financial instruments consist of cash and cash equivalents, accounts and notes receivable, accounts payable and long-term debt. With the exception of its long-term debt, the Company believes that the carrying value of its financial instruments approximates their fair values. The majority of the Company’s cash and cash equivalents at December 31, 2008 were held in money market mutual funds which participate in the U.S. Treasury Department Temporary Guarantee Program for Money Market Funds, and in money market funds which invest solely in U.S. Government obligations. The book balance at December 31, 2008 of the Company’s long-term debt, which carries an interest rate of 8.6%, is $33,002,000. The Company estimates the fair value of this debt at approximately $33,944,000, based on current prevailing interest rates for similar mortgage debt.

Impact of Recently Issued Accounting Standards:

In December 2007, the FSAB issued SFAS No. 160, “Noncontrolling Interest in Consolidated Financial Statements” (SFAS No. 160). SFAS No. 160 addresses consolidation rules for noncontrolling interests. The objective is to improve the relevance, comparability, and transparency of the financial information that a reporting entity provides in its consolidated financial statements by establishing accounting and reporting standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary. It applies to all entities that prepare consolidated financial statements, except for not-for-profit organization, but will affect only those entities that have an outstanding noncontrolling interest in one or more subsidiaries or that deconsolidate a subsidiary. This Statement is effective for fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2008. Early adoption is prohibited. Management is currently evaluating SFAS No. 160 to determine if it will have a material impact on the Company’s future financial statements.

In December 2007, the FASB issued SFAS No.141R, “Business Combinations” (SFAS no. 141R). SFAS No. 141R addresses financial accounting and reporting for business combinations, and supersedes APB Opinion No. 16, Business Combinations and FASB Statement No. 38, Accounting for Preacquisition Contingencies of Purchased Enterprises. The objective is to provide consistency to the accounting and financial reporting of business combinations by using only one method, the purchase method. This Statement is effective for fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2008. Early adoption is prohibited. Management is currently evaluating SFAS No. 141R. It could have a material impact on the Company’s future financial statements if an acquisition is completed.

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities” (SFAS No. 161). SFAS No. 161 enhances the disclosure requirements for derivative instruments and hedging activities. Entities are required to provide enhanced disclosures about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for under SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities, and its related interpretations, and (c) how derivative instruments and related hedged items affect an entity’s financial position, financial performance and cash flows. This Statement is effective for fiscal years, and interim periods within those fiscal years, beginning after November 15, 2008. This Statement encourages, but does not require, comparative disclosures for earlier periods at initial adoption. Early adoption is encouraged. Management is currently evaluating SFAS No. 161 to determine if it will have a material impact on the Company’s future financial statements.