UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08282

Loomis Sayles Funds I

(Exact name of Registrant as specified in charter)

399 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Coleen Downs Dinneen, Esq.

NGAM Distribution, L.P.

399 Boylston Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2810

Date of fiscal year end: September 30

Date of reporting period: September 30, 2013

| Item 1. | Reports to Stockholders. |

The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Loomis Sayles Small Cap Growth Fund

Loomis Sayles Small Cap Value Fund

Annual Report

September 30, 2013

LOOMIS SAYLES SMALL CAP GROWTH FUND

| | | | |

| Managers | | Symbols | | |

| Mark F. Burns, CFA | | Institutional Class | | LSSIX |

| John J. Slavik, CFA | | Retail Class | | LCGRX |

| | Class N | | LSSNX |

Objective

Long-term capital growth from investments in common stocks or other equity securities

Strategy

The fund normally will invest at least 80% of its net assets in equity securities of companies with market capitalizations that fall within the capitalization range of the Russell 2000® Index or is $3 billion or less at the time of investment. Unlike the Index, the fund may invest in companies of any size.

The fund may invest any portion of its assets in Canadian securities and up to 20% of assets in other foreign securities, including emerging markets securities.

Market Conditions

Despite rising interest rate concerns, conflict in Syria and disappointing economic growth, equity markets were strong during the 12-month period. Small-cap companies posted particularly robust results, generally outperforming their mid- and large-cap counterparts. As a result of the strong returns in the small cap universe, stock valuations have trended much higher.

Performance Results

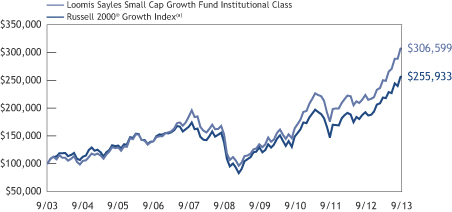

For the 12 months ended September 30, 2013, Institutional Class shares of Loomis Sayles Small Cap Growth Fund returned 37.45%. The fund outperformed its benchmark, the Russell 2000® Growth Index, which returned 33.07%.

Explanation of Fund Performance

Almost all of the fund’s outperformance was due to stock selection, particularly in the financials, energy and healthcare sectors. The consumer staples and information technology sectors detracted slightly from performance.

A position in Financial Engines, a provider of investment advice to 401(k) plan participants using a quantitative model developed by Nobel Laureate Bill Sharpe, was the top contributor to fund performance. The company reported steadily increasing adoption rates during the year. In addition, Aegerion Pharmaceuticals, a biotech company focused on therapies for cardiovascular and metabolic diseases, was a top-performing stock. The company launched its cholesterol drug during the period, and patient usage continued to accelerate with low discontinuation rates. The drug’s price also increased, eliminating

1 |

tiered pricing. Another top contributor to performance was Wageworks, a leading on-demand provider of tax-advantaged programs for consumer-directed health, commuter and other employee spending account benefits in the United States. The company reported strong results, raised its organic growth target for the year and continued to execute strategic acquisitions that further augment growth. The Affordable Care Act, which has increased the role of consumer- and employee-driven benefits, also helped the stock’s performance.

An out-of-index position in Allot Communications, which designs and develops broadband service optimization solutions to help carriers track and bill usage, was the largest individual detractor from relative performance, lagging on near-term business trend concerns. Specifically, carriers have been hesitant to spend in the face of macroeconomic uncertainty. Given the customer concentration that comes with doing business in this industry, these spending hesitations quickly and significantly affected orders. This triggered our stop loss, and we sold the position. In addition, NuVasive, maker of a minimally invasive spine surgery device, detracted from performance. Due to weak procedure growth and pricing pressure, the company reported disappointing earnings and poor forward guidance. The market’s negative reaction triggered our stop loss, and we sold the position. A position in Nektar Therapeutics, a drug delivery technology company, also detracted from results. Mixed phase-three trial results for an important pipeline drug caused a selloff in the stock, which triggered our stop loss. We exited the position.

Outlook

We continue to estimate earnings growth in the mid single-digit range this year and next. While margin expansion from recessionary lows has largely played out, the evidence tends to support our view that margins should remain healthy in an environment of moderate but steady gross domestic product (GDP) growth. Dividends are expected to grow at a double-digit rate in 2013 and likely in 2014 as well. The potential for dividend growth and moderately higher equity prices could provide equity investors with two opportunities over time. While the Fed has refrained from tapering its monthly bond-buying purchases, known as quantitative easing (QE) for now, investors should prepare for an eventual return to a more normal interest rate environment with a federal funds rate above the zero lower bound. If yields normalize gradually, on the basis of improved economic growth with contained inflation, equity investors should be able to adjust to the changing environment and use periodic average corrections as opportunities to add to favored positions.

| 2

LOOMIS SAYLES SMALL CAP GROWTH FUND

Cumulative Performance — September 30, 2003 through September 30, 2013(b)(c)

Average Annual Total Returns — September 30, 2013(b)

| | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | 1 year | | | 5 years | | | 10 years | | | Since Class N

Inception | |

| | | | | | |

| Institutional Class (Inception 12/31/96) | | | | | 37.45 | % | | | 15.05 | % | | | 11.86 | % | | | — | % |

| Retail Class (Inception 12/31/96) | | | | | 37.05 | | | | 14.73 | | | | 11.56 | | | | — | |

| Class N (Inception 2/1/13) | | | | | — | | | | — | | | | — | | | | 30.37 | |

| Comparative Performance | | | | | | | | | | | | | |

| Russell 2000® Growth Index(a) | | | | | 33.07 | | | | 13.17 | | | | 9.85 | | | | 23.08 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| (a) | | See page 7 for a description of the index. |

| (b) | | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| (c) | | The mountain chart is based on the initial minimum of $100,000 for the Institutional Class. |

3 |

LOOMIS SAYLES SMALL CAP VALUE FUND

| | | | |

| Managers | | Symbols | | |

| Joseph R. Gatz, CFA | | Institutional Class | | LSSCX |

| Jeffrey Schwartz, CFA | | Retail Class | | LSCRX |

| | Admin Class | | LSVAX |

| | Class N | | LSCNX |

Objective

Long-term capital growth from investments in common stocks or other equity securities

Strategy

The fund normally will invest at least 80% of its net assets in equity securities of companies with market capitalizations that fall within the capitalization range of the Russell 2000® Index or is $3 billion or less at the time of investment. Unlike the Index, the fund may invest in companies of any size.

The fund may invest up to 20% of its assets in securities of foreign issuers, including emerging market securities.

Market Conditions

Large- and small-cap U.S. equities in the growth and value styles delivered strong returns for the 12-month period. Overall, small-cap stocks outpaced large-cap stocks, and growth styles measurably exceeded value. Economically sensitive sectors, including consumer discretionary, industrials and information technology, were the performance leaders in the small-cap universe. Slower-growing, high-dividend-yielding sectors and industries, including utilities and real estate investment trusts, generally lagged. Higher valuations and a return of equity fund inflows helped drive market returns higher. In addition, monetary policy remained accommodative, which encouraged investors to hold stocks and other riskier assets, as yields on U.S. Treasuries and other fixed-income securities remained low.

Performance Results

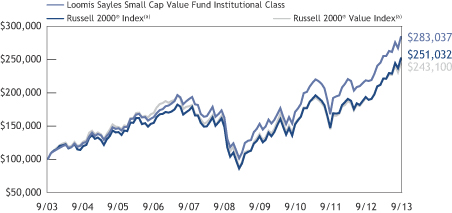

For the 12 months ended September 30, 2013, Institutional Class shares of Loomis Sayles Small Cap Value Fund returned 29.82%. The fund outperformed its benchmark, the Russell 2000® Value Index, which returned 27.04%.

Explanation of Fund Performance

Both sector allocation and stock selection were important drivers of performance. Sector allocation was positive, primarily due to an overweight position in the industrials sector, which was the benchmark’s second-best performing sector for the period. The fund also had underweight positions in financials and utilities, two of the weakest performing sectors in the index. Stock selection was also positive, with significant outperformance in the energy, utilities and financials sectors offsetting weaker results in consumer discretionary. The utilities sector posted a strong showing due to favorable stock selection in the gas and electric utilities industries and lack of exposure to the poor-performing independent power producers industry.

Within the industrials sector, which was the fund’s top-contributing sector, an emphasis on energy infrastructure-related investments contributed to results. Specifically, positions in Primoris, a provider of engineering and pipeline construction services; H&E Equipment

| 4

LOOMIS SAYLES SMALL CAP VALUE FUND

Services, a distributor of heavy construction and industrial equipment in the Gulf Coast region and DXP Enterprises, a distributor of industrial equipment and parts and service in the Gulf Coast region, aided performance. In addition, a position in Euronet Worldwide, a provider of electronic transaction processing solutions to financial institutions and mobile telephone operators, was the fund’s top contributor for the period. The company reported strong earnings growth throughout the 12 months, primarily due to solid growth in ATMs from European banks seeking outsourcing solutions, improved money transfer volumes and new electronic payment applications outside the core mobile telephone offering.

A position in EPL Oil & Gas, an independent oil and gas exploration and production company, also contributed to results. Recent acquisitions that led to higher oil production and expanded inventory reserves allowed the company to experience strong cash flow and earnings growth. The fund also benefited from owning shares of MarketAxess Holdings, a provider of electronic trading platforms for U.S. and international corporate bonds, which outperformed due to higher trading volumes associated with rising long-term interest rates. In addition, the company’s strategic alliance with BlackRock, an acquisition in Europe and opportunities in the high-yield, emerging markets and credit default swap businesses all improved the outlook and supported a higher valuation.

Consumer discretionary was the benchmark’s top-performing sector, but our stock selection did not keep pace with the benchmark’s strong sector return for the year. Laggards included several retailers, such as Genesco, which was an overweight relative to the index, and an out-of-index position in Sally Beauty, where sales trends moderated due to diminished consumer spending patterns. Outside the consumer discretionary sector, a position in Impax Labs, a developer of branded and generic pharmaceuticals, detracted from performance. Shares declined following an adverse FDA inspection of a manufacturing facility, and we eliminated the position. In addition, DFC Global, a provider of consumer loans and check cashing services in North America and Europe, weighed on results. Mounting regulatory pressures in the company’s U.K. payday lending business led to declining earnings and reduced forecasts. However, our experience with management’s ability to navigate through similar regulatory issues in the past led us to believe that DFC will recover and gain significant market share, as we expect the number of competitors to diminish materially. A position in Titan Machinery, an operator of agriculture and construction equipment dealerships and stores, detracted from results. The company reported disappointing earnings and below consensus guidance for the April and July fiscal quarters. With underlying trends in the agriculture equipment market deteriorating, we eliminated the position.

Outlook

We continue to estimate earnings growth in the mid single-digit range this year and next. While margin expansion from recessionary lows has largely played out, the evidence tends to support our view that margins should remain healthy in an environment of moderate but steady gross domestic product growth. Dividends are expected to grow at a double-digit rate in 2013 and likely in 2014 as well. The potential for dividend growth and moderately higher equity prices could provide equity investors with two opportunities over time. While the Fed has refrained from tapering its monthly bond-buying purchases, known as quantitative easing (QE) for now, investors should prepare for an eventual return to a more normal interest rate environment with a federal funds rate above the zero lower bound. If yields normalize gradually, on the basis of improved economic growth with contained inflation, equity investors should be able to adjust to the changing environment and use periodic average corrections as opportunities to add to favored positions.

5 |

Cumulative Performance — September 30, 2003 through September 30, 2013(b)(c)

Average Annual Total Returns — September 30, 2013(b)

| | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | 1 year | | | 5 years | | | 10 years | | | Since Class N

Inception | |

| | | | | | |

| Institutional Class (Inception 5/13/91) | | | | | 29.82 | % | | | 11.87 | % | | | 10.97 | % | | | — | % |

| Retail Class (Inception 12/31/96) | | | | | 29.48 | | | | 11.59 | | | | 10.69 | | | | — | |

| Admin Class (Inception 1/2/98) | | | | | 29.17 | | | | 11.31 | | | | 10.41 | | | | — | |

| Class N (Inception 2/1/13) | | | | | — | | | | — | | | | — | | | | 16.71 | |

| | | | |

| Comparative Performance | | | | | | | | | | | | | |

| Russell 2000® Value Index(a) | | | | | 27.04 | | | | 9.13 | | | | 9.29 | | | | 14.96 | |

| Russell 2000® Index(a) | | | | | 30.06 | | | | 11.15 | | | | 9.64 | | | | 18.96 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| (a) | | See page 7 for a description of the index. |

| (b) | | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| (c) | | The mountain chart is based on the initial minimum of $100,000 for the Institutional Class. |

| 6

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the fund is actively managed, there is no assurance that it will continue to invest in the securities or industries mentioned.

Index Definitions

Indices are unmanaged and do not have expenses that affect results, unlike mutual funds. Index returns are adjusted for the reinvestment of capital gain distributions and income dividends. It is not possible to invest directly in an index.

Russell 2000® Index is an unmanaged index that measures the performance of the small-cap segment of the U.S. equity universe.

Russell 2000® Growth Index is an unmanaged index that measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Value Index is an unmanaged index that measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

Additional Index Information

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Global Asset Management or any of its related or affiliated companies (collectively “NGAM”) and does not sponsor, endorse or participate in the provision of any NGAM services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

Proxy Voting Information

A description of the funds’ proxy voting policies and procedures is available without charge, upon request, (i) by calling Loomis Sayles at 800-633-3330; (ii) on the funds’ website, www.loomissayles.com, and (iii) on the SEC’s website, www.sec.gov. Information about how the funds voted proxies relating to portfolio securities during the 12 months ended June 30, 2013 is available on (i) the funds’ website and (ii) the SEC’s website.

Quarterly Portfolio Schedules

The funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The funds’ Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

7 |

UNDERSTANDING YOUR FUND’S EXPENSES

As a mutual fund shareholder you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. These costs are described in more detail in the funds’ prospectus. The following examples are intended to help you understand the ongoing costs of investing in the funds and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table of each fund shows the actual amount of fund expenses you would have paid on a $1,000 investment in the fund from April 1, 2013 through September 30, 2013. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.6) and multiply the result by the number in the Expenses Paid During Period column as shown below for your class.

The second line in the table of each fund provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the funds to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs. Therefore, the second line in the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

| 8

Loomis Sayles Small Cap Growth Fund

| | | | | | | | | | | | |

Institutional Class | | Beginning

Account Value

4/1/2013 | | | Ending

Account Value

9/30/2013 | | | Expenses Paid

During Period*

4/1/2013 – 9/30/2013 | |

Actual | | | $1,000.00 | | | | $1,226.70 | | | | $5.14 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,020.46 | | | | $4.66 | |

| | | |

Retail Class | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,224.80 | | | | $6.97 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,018.80 | | | | $6.33 | |

| | | |

Class N | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,227.20 | | | | $4.63 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,020.91 | | | | $4.20 | |

* Expenses are equal to the Fund’s annualized expense ratio: 0.92%, 1.25% and 0.83% for Institutional Class, Retail Class and Class N, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). | |

Loomis Sayles Small Cap Value Fund

| | | | | | | | | | | | |

Institutional Class | | Beginning

Account Value

4/1/2013 | | | Ending

Account Value

9/30/2013 | | | Expenses Paid

During Period*

4/1/2013 – 9/30/2013 | |

Actual | | | $1,000.00 | | | | $1,112.00 | | | | $4.77 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,020.56 | | | | $4.56 | |

| | | |

Retail Class | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,110.70 | | | | $6.08 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,019.30 | | | | $5.82 | |

| | | |

Admin Class | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,109.30 | | | | $7.40 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,018.05 | | | | $7.08 | |

| | | |

Class N | | | | | | | | | |

Actual | | | $1,000.00 | | | | $1,112.30 | | | | $4.50 | |

Hypothetical

(5% return before expenses) | | | $1,000.00 | | | | $1,020.81 | | | | $4.31 | |

* Expenses are equal to the Fund’s annualized expense ratio (after waiver/reimbursement): 0.90%, 1.15%, 1.40% and 0.85% for Institutional Class, Retail Class, Admin Class and Class N, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). | |

9 |

BOARD APPROVAL OF THE EXISTING ADVISORY AGREEMENTS

The Board of Trustees of the Trusts (the “Board”), including the Independent Trustees, considers matters bearing on each Fund’s advisory agreement (collectively, the “Agreements”) at most of its meetings throughout the year. Each year, usually in the spring, the Contract Review and Governance Committee of the Board meets to review the Agreements to determine whether to recommend that the full Board approve the continuation of the Agreements, typically for an additional one-year period. After the Committee has made its recommendation, the full Board, including the Independent Trustees, determines whether to approve the continuation of the Agreements.

In connection with these meetings, the Trustees receive materials that the Funds’ investment adviser (the “Adviser”) believes to be reasonably necessary for the Trustees to evaluate the Agreements. These materials generally include, among other items, (i) information on the investment performance of the Funds and the performance of peer groups and categories of funds and the Funds’ performance benchmarks, (ii) information on the Funds’ advisory fees and other expenses, including information comparing the Funds’ expenses to the fees charged to institutional accounts with similar strategies managed by the Adviser, if any, and to those of peer groups of funds and information about applicable expense caps and fee “breakpoints,” (iii) sales and redemption data in respect of the Funds, (iv) information about the profitability of the Agreements to the Adviser and (v) information obtained through the completion by the Adviser of a questionnaire distributed on behalf of the Trustees. The Board, including the Independent Trustees, also consider other matters such as (i) the Adviser’s financial results and/or financial condition, (ii) each Fund’s investment objective and strategies and the size, education and experience of the Adviser’s investment staff and its use of technology, external research and trading cost measurement tools, (iii) arrangements in respect of the distribution of the Funds’ shares and the related costs, (iv) the procedures employed to determine the value of the Funds’ assets, (v) the allocation of the Funds’ brokerage, if any, including, if applicable, allocations to brokers affiliated with the Adviser and the use of “soft” commission dollars to pay Fund expenses and to pay for research and other similar services, (vi) the resources devoted to, and the record of compliance with, the Funds’ investment policies and restrictions, policies on personal securities transactions and other compliance policies, (vii) information about amounts invested by the Funds’ portfolio managers in the Funds or in similar accounts that they manage and (viii) the general economic outlook with particular emphasis on the mutual fund industry. Throughout the process, the Trustees are afforded the opportunity to ask questions of and request additional materials from the Adviser.

In addition to the materials requested by the Trustees in connection with their annual consideration of the continuation of the Agreements, the Trustees receive materials in advance of each regular quarterly meeting of the Board that provide detailed information about the Funds’ investment performance and the fees charged to the Funds for advisory and other services. This information generally includes, among other things, an internal performance rating for each Fund based on agreed-upon criteria, graphs showing each Fund’s performance and fee differentials against each Fund’s peer group/category,

| 10

performance ratings provided by a third-party, total return information for various periods, and third-party performance rankings for various periods comparing a Fund against similarly categorized funds. The portfolio management team for each Fund or other representatives of the Adviser make periodic presentations to the Contract Review and Governance Committee and/or the full Board, and Funds identified as presenting possible performance concerns may be subject to more frequent board presentations and reviews. In addition, each quarter the Trustees are provided with detailed statistical information about each Fund’s portfolio. The Trustees also receive periodic updates between meetings.

The Board most recently approved the continuation of the Agreements at their meeting held in June 2013. The Agreements were continued for a one-year period for the Funds. In considering whether to approve the continuation of the Agreements, the Board, including the Independent Trustees, did not identify any single factor as determinative. Individual Trustees may have evaluated the information presented differently from one another, giving different weights to various factors. Matters considered by the Trustees, including the Independent Trustees, in connection with their approval of the Agreements included, but were not limited to, the factors listed below.

The nature, extent and quality of the services provided to the Funds under the Agreements. The Trustees considered the nature, extent and quality of the services provided by the Adviser and its affiliates to the Funds and the resources dedicated to the Funds by the Adviser and its affiliates.

The Trustees considered not only the advisory services provided by the Adviser to the Funds, but also the administrative services provided by NGAM Advisors, L.P. (“NGAM Advisors”) and its affiliates to the Funds. For each Fund, the Trustees also considered the benefits to shareholders of investing in a mutual fund that is part of a family of funds that offers shareholders the right to exchange shares of one type of fund for shares of another type of fund, and provides a variety of fund and shareholder services.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the nature, extent and quality of services provided supported the renewal of the Agreements.

Investment performance of the Funds and the Adviser. As noted above, the Trustees received information about the performance of the Funds over various time periods, including information that compared the performance of the Funds to the performance of peer groups and categories of funds and the Funds’ respective performance benchmarks. In addition, the Trustees also reviewed data prepared by an independent third party that analyzed the performance of the Funds using a variety of performance metrics, including metrics that also measured the performance of the Funds on a risk adjusted basis. With respect to each Fund, the Board concluded that the Fund’s performance or other relevant factors supported the renewal of the Agreement relating to that Fund. In the case of the Loomis Sayles Small Cap Growth Fund, the performance of which lagged that of a relevant peer group median and/or category median of funds for certain (although not necessarily all) periods, the Board concluded that other factors relevant to performance supported renewal of the relevant Agreement, including (1) that the underperformance

11 |

was attributable, to a significant extent, to investment decisions (such as security selection or sector allocation) by the Adviser that were reasonable and consistent with the Fund’s investment objective and policies; (2) that the Fund’s performance was stronger over the long term; and (3) that the Fund’s more recent performance, although lagging in certain periods, had recently shown improvement relative to its category and benchmark.

The Trustees also considered the Adviser’s performance and reputation generally, the performance of the fund family generally, and the historical responsiveness of the Adviser to Trustee concerns about performance and the willingness of the Adviser to take steps intended to improve performance.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the performance of the Funds and the Adviser supported the renewal of the Agreements.

The costs of the services to be provided and profits to be realized by the Adviser and its affiliates from their respective relationships with the Funds. The Trustees considered the fees charged to the Funds for advisory services as well as the total expense levels of the Funds. This information included comparisons (provided both by management and also by an independent third party) of the Funds’ advisory fees and total expense levels to those of their peer groups and information about the advisory fees charged by the Adviser to comparable accounts (such as institutional separate accounts), as well as information about differences in such fees and the reasons for any such differences. In considering the fees charged to comparable accounts, the Trustees considered, among other things, management’s representations about the differences between managing mutual funds as compared to other types of accounts, including the additional resources required to effectively manage and the greater regulatory costs associated with the management of mutual fund assets. In evaluating each Fund’s advisory fee, the Trustees also took into account the demands, complexity and quality of the investment management of such Fund and the need for the Adviser to offer competitive compensation. The Trustees considered that over the past several years, management had made recommendations regarding reductions in advisory fee rates, implementation of advisory fee breakpoints and the institution of advisory fee waivers and expense caps for various funds in the fund family. They noted that both of the Funds in this report have expense caps in place, and they considered the amounts waived or reimbursed by the Adviser for the Loomis Sayles Small Cap Value Fund. The Loomis Sayles Small Cap Growth Fund’s current expenses are below the cap.

The Trustees also considered the compensation directly or indirectly received by the Adviser and its affiliates from their relationships with the Funds. The Trustees reviewed information provided by management as to the profitability of the Adviser and its affiliates’ relationships with the Funds, and information about the allocation of expenses used to calculate profitability. They also reviewed information provided by management about the effect of distribution costs and changes in asset levels on Adviser profitability, including information regarding resources spent on distribution activities. When reviewing profitability, the Trustees also considered information about court cases in which adviser compensation or profitability were issues, the performance of the relevant Funds, the

| 12

expense levels of the Funds, and whether the Adviser had implemented breakpoints and/or expense caps with respect to such Funds.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the advisory fee charged to each of the Funds was fair and reasonable, and that the costs of these services generally and the related profitability of the Adviser and its affiliates in respect of their relationships with the Funds supported the renewal of the Agreements.

Economies of Scale. The Trustees considered the existence of any economies of scale in the provision of services by the Adviser and whether those economies are shared with the Funds through breakpoints in their investment advisory fees or other means, such as expense waivers or caps. The Trustees also discussed with management the factors considered with respect to the implementation of breakpoints in investment advisory fees or expense waivers or caps for certain funds. Management explained that a number of factors are taken into account in considering the implementation of breakpoints or an expense cap for a fund, including, among other things, factors such as a fund’s assets, the projected growth of a fund, projected profitability and a fund’s fees and performance. With respect to economies of scale, the Trustees noted that although neither Fund’s management fee was subject to breakpoints, each Fund’s management fee and each Fund’s overall net expense ratio was at or below the median for a peer group of funds and that each Fund was subject to an expense cap. In considering these issues, the Trustees also took note of the costs of the services provided (both on an absolute and a relative basis) and the profitability to the Adviser and its affiliates of their relationships with the Funds, as discussed above.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the extent to which economies of scale were shared with the Funds supported the renewal of the Agreements.

The Trustees also considered other factors, which included but were not limited to the following:

| • | | the effect of recent market and economic events on the performance, asset levels and expense ratios of each Fund. |

| • | | whether each Fund has operated in accordance with its investment objective and the Fund’s record of compliance with its investment restrictions, and the compliance programs of the Funds and the Adviser. They also considered the compliance-related resources the Adviser and its affiliates were providing to the Funds. |

| • | | the nature, quality, cost and extent of administrative and shareholder services performed by the Adviser and its affiliates, both under the Agreements and under separate agreements covering administrative services. |

| • | | so-called “fallout benefits” to the Adviser, such as the engagement of affiliates of the Adviser to provide distribution, administrative and brokerage services to the Funds, and the benefits of research made available to the Adviser by reason of brokerage commissions (if any) generated by the Funds’ securities transactions. The Trustees also |

13 |

| | considered the fact that NGAM Advisors’ parent company benefits from the retention of an affiliated Adviser. The Trustees considered the possible conflicts of interest associated with these fallout and other benefits, and the reporting, disclosure and other processes in place to disclose and monitor such possible conflicts of interest. |

| • | | the Trustees’ review and discussion of the Funds’ advisory arrangements in prior years, and management’s record of responding to Trustee concerns raised during the year and in prior years. |

Based on their evaluation of all factors that they deemed to be material, including those factors described above, and assisted by the advice of independent counsel, the Trustees, including the Independent Trustees, concluded that each of the existing Agreements should be continued through June 30, 2014.

| 14

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – 95.6% of Net Assets | |

| | |

| | | | Aerospace & Defense – 2.1% | | | | |

| | 354,359 | | | Hexcel Corp.(b) | | $ | 13,749,129 | |

| | 140,813 | | | Triumph Group, Inc. | | | 9,887,889 | |

| | | | | | | | |

| | | | | | | 23,637,018 | |

| | | | | | | | |

| | | | Air Freight & Logistics – 1.0% | | | | |

| | 501,780 | | | XPO Logistics, Inc.(b) | | | 10,873,573 | |

| | | | | | | | |

| | | | Airlines – 1.0% | | | | |

| | 319,735 | | | Spirit Airlines, Inc.(b) | | | 10,957,318 | |

| | | | | | | | |

| | | | Auto Components – 1.0% | | | | |

| | 211,184 | | | Dorman Products, Inc. | | | 10,464,167 | |

| | 25,904 | | | Drew Industries, Inc. | | | 1,179,668 | |

| | | | | | | | |

| | | | | | | 11,643,835 | |

| | | | | | | | |

| | | | Biotechnology – 6.2% | | | | |

| | 72,079 | | | Aegerion Pharmaceuticals, Inc.(b) | | | 6,177,891 | |

| | 428,159 | | | Alkermes PLC(b) | | | 14,394,705 | |

| | 83,597 | | | Clovis Oncology, Inc.(b) | | | 5,081,026 | |

| | 196,970 | | | Cubist Pharmaceuticals, Inc.(b) | | | 12,517,443 | |

| | 426,434 | | | Emergent Biosolutions, Inc.(b) | | | 8,123,568 | |

| | 662,304 | | | Exact Sciences Corp.(b) | | | 7,821,810 | |

| | 269,988 | | | Myriad Genetics, Inc.(b) | | | 6,344,718 | |

| | 316,181 | | | NPS Pharmaceuticals, Inc.(b) | | | 10,057,718 | |

| | | | | | | | |

| | | | | | | 70,518,879 | |

| | | | | | | | |

| | | | Capital Markets – 2.0% | | | | |

| | 194,719 | | | Artisan Partners Asset Management, Inc. | | | 10,195,487 | |

| | 211,389 | | | Financial Engines, Inc. | | | 12,564,962 | |

| | | | | | | | |

| | | | | | | 22,760,449 | |

| | | | | | | | |

| | | | Chemicals – 1.2% | | | | |

| | 584,264 | | | Flotek Industries, Inc.(b) | | | 13,438,072 | |

| | | | | | | | |

| | | | Commercial Banks – 3.5% | | | | |

| | 232,351 | | | Bank of the Ozarks, Inc. | | | 11,150,524 | |

| | 691,641 | | | Boston Private Financial Holdings, Inc. | | | 7,677,215 | |

| | 113,909 | | | Signature Bank(b) | | | 10,424,952 | |

| | 114,994 | | | SVB Financial Group(b) | | | 9,932,032 | |

| | | | | | | | |

| | | | | | | 39,184,723 | |

| | | | | | | | |

| | | | Communications Equipment – 1.1% | | | | |

| | 511,876 | | | Ciena Corp.(b) | | | 12,786,663 | |

| | | | | | | | |

| | | | Construction & Engineering – 0.8% | | | | |

| | 297,345 | | | MasTec, Inc.(b) | | | 9,009,554 | |

| | | | | | | | |

| | | | Consumer Finance – 1.0% | | | | |

| | 246,412 | | | Encore Capital Group, Inc.(b) | | | 11,300,454 | |

| | | | | | | | |

See accompanying notes to financial statements.

15 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Distributors – 0.8% | | | | |

| | 167,986 | | | Pool Corp. | | $ | 9,429,054 | |

| | | | | | | | |

| | | | Diversified Consumer Services – 3.6% | | | | |

| | 253,682 | | | Bright Horizons Family Solutions, Inc.(b) | | | 9,089,426 | |

| | 482,944 | | | Grand Canyon Education, Inc.(b) | | | 19,452,984 | |

| | 794,188 | | | LifeLock, Inc.(b) | | | 11,777,808 | |

| | | | | | | | |

| | | | | | | 40,320,218 | |

| | | | | | | | |

| | | | Diversified Financial Services – 1.1% | | | | |

| | 206,738 | | | MarketAxess Holdings, Inc. | | | 12,412,550 | |

| | | | | | | | |

| | | | Electrical Equipment – 1.6% | | | | |

| | 234,262 | | | Polypore International, Inc.(b) | | | 9,597,714 | |

| | 348,032 | | | Thermon Group Holdings, Inc.(b) | | | 8,043,020 | |

| | | | | | | | |

| | | | | | | 17,640,734 | |

| | | | | | | | |

| | | | Electronic Equipment, Instruments & Components – 2.8% | | | | |

| | 137,284 | | | FEI Co. | | | 12,053,535 | |

| | 146,825 | | | IPG Photonics Corp. | | | 8,267,716 | |

| | 211,443 | | | Measurement Specialties, Inc.(b) | | | 11,468,668 | |

| | | | | | | | |

| | | | | | | 31,789,919 | |

| | | | | | | | |

| | | | Energy Equipment & Services – 2.9% | | | | |

| | 104,823 | | | Dril-Quip, Inc.(b) | | | 12,028,439 | |

| | 348,155 | | | Forum Energy Technologies, Inc.(b) | | | 9,403,667 | |

| | 461,624 | | | Helix Energy Solutions Group, Inc.(b) | | | 11,711,401 | |

| | | | | | | | |

| | | | | | | 33,143,507 | |

| | | | | | | | |

| | | | Food & Staples Retailing – 1.0% | | | | |

| | 206,335 | | | Susser Holdings Corp.(b) | | | 10,966,705 | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies – 6.6% | | | | |

| | 216,984 | | | Abaxis, Inc. | | | 9,135,026 | |

| | 108,148 | | | Analogic Corp. | | | 8,937,351 | |

| | 532,804 | | | Endologix, Inc.(b) | | | 8,594,129 | |

| | 299,992 | | | Insulet Corp.(b) | | | 10,871,710 | |

| | 208,728 | | | MAKO Surgical Corp.(b) | | | 6,159,563 | |

| | 450,018 | | | Novadaq Technologies, Inc.(b) | | | 7,461,298 | |

| | 310,496 | | | Quidel Corp.(b) | | | 8,818,086 | |

| | 557,988 | | | Spectranetics Corp.(b) | | | 9,363,039 | |

| | 284,387 | | | Tornier NV(b) | | | 5,497,201 | |

| | | | | | | | |

| | | | | | | 74,837,403 | |

| | | | | | | | |

| | | | Health Care Providers & Services – 1.9% | | | | |

| | 285,641 | | | Acadia Healthcare Co., Inc.(b) | | | 11,262,825 | |

| | 258,831 | | | Team Health Holdings, Inc.(b) | | | 9,820,048 | |

| | | | | | | | |

| | | | | | | 21,082,873 | |

| | | | | | | | |

See accompanying notes to financial statements.

| 16

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Health Care Technology – 2.1% | | | | |

| | 569,483 | | | MedAssets, Inc.(b) | | $ | 14,476,258 | |

| | 91,462 | | | Medidata Solutions, Inc.(b) | | | 9,048,336 | |

| | | | | | | | |

| | | | | | | 23,524,594 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure – 2.8% | | | | |

| | 249,776 | | | AFC Enterprises, Inc.(b) | | | 10,887,736 | |

| | 393,067 | | | Texas Roadhouse, Inc. | | | 10,329,801 | |

| | 153,465 | | | Vail Resorts, Inc. | | | 10,647,401 | |

| | | | | | | | |

| | | | | | | 31,864,938 | |

| | | | | | | | |

| | | | Insurance – 1.1% | | | | |

| | 304,536 | | | Amtrust Financial Services, Inc. | | | 11,895,176 | |

| | | | | | | | |

| | | | Internet & Catalog Retail – 1.0% | | | | |

| | 385,897 | | | HomeAway, Inc.(b) | | | 10,805,116 | |

| | | | | | | | |

| | | | Internet Software & Services – 6.8% | | | | |

| | 293,762 | | | Angie’s List, Inc.(b) | | | 6,609,645 | |

| | 49,225 | | | Benefitfocus, Inc.(b) | | | 2,419,901 | |

| | 183,189 | | | Cornerstone OnDemand, Inc.(b) | | | 9,423,242 | |

| | 79,066 | | | CoStar Group, Inc.(b) | | | 13,275,181 | |

| | 416,913 | | | Dealertrack Technologies, Inc.(b) | | | 17,860,553 | |

| | 235,972 | | | Envestnet, Inc.(b) | | | 7,315,132 | |

| | 140,478 | | | OpenTable, Inc.(b) | | | 9,830,651 | |

| | 37,722 | | | Shutterstock, Inc.(b) | | | 2,743,144 | |

| | 169,802 | | | Trulia, Inc.(b) | | | 7,985,788 | |

| | | | | | | | |

| | | | | | | 77,463,237 | |

| | | | | | | | |

| | | | IT Services – 1.6% | | | | |

| | 239,141 | | | EPAM Systems, Inc.(b) | | | 8,250,365 | |

| | 449,052 | | | InterXion Holding NV(b) | | | 9,986,916 | |

| | | | | | | | |

| | | | | | | 18,237,281 | |

| | | | | | | | |

| | | | Life Sciences Tools & Services – 0.9% | | | | |

| | 203,908 | | | PAREXEL International Corp.(b) | | | 10,242,299 | |

| | | | | | | | |

| | | | Machinery – 5.1% | | | | |

| | 117,964 | | | Chart Industries, Inc.(b) | | | 14,514,290 | |

| | 510,126 | | | Manitowoc Co., Inc. (The) | | | 9,988,267 | |

| | 51,354 | | | Middleby Corp. (The)(b) | | | 10,728,364 | |

| | 146,399 | | | Proto Labs, Inc.(b) | | | 11,183,420 | |

| | 177,685 | | | RBC Bearings, Inc.(b) | | | 11,707,665 | |

| | | | | | | | |

| | | | | | | 58,122,006 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels – 3.9% | | | | |

| | 191,103 | | | Diamondback Energy, Inc.(b) | | | 8,148,632 | |

| | 195,546 | | | Gulfport Energy Corp.(b) | | | 12,581,430 | |

| | 260,889 | | | Oasis Petroleum, Inc.(b) | | | 12,817,477 | |

See accompanying notes to financial statements.

17 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Oil, Gas & Consumable Fuels – continued | | | | |

| | 201,014 | | | Rosetta Resources, Inc.(b) | | $ | 10,947,222 | |

| | | | | | | | |

| | | | | | | 44,494,761 | |

| | | | | | | | |

| | | | Pharmaceuticals – 0.8% | | | | |

| | 198,304 | | | Pacira Pharmaceuticals, Inc.(b) | | | 9,536,439 | |

| | | | | | | | |

| | | | Professional Services – 6.3% | | | | |

| | 272,576 | | | Advisory Board Co. (The)(b) | | | 16,212,821 | |

| | 224,374 | | | Corporate Executive Board Co. (The) | | | 16,294,040 | |

| | 211,986 | | | Huron Consulting Group, Inc.(b) | | | 11,152,583 | |

| | 330,052 | | | On Assignment, Inc.(b) | | | 10,891,716 | |

| | 332,889 | | | WageWorks, Inc.(b) | | | 16,794,250 | |

| | | | | | | | |

| | | | | | | 71,345,410 | |

| | | | | | | | |

| | | | Road & Rail – 1.2% | | | | |

| | 151,826 | | | Genesee & Wyoming, Inc., Class A(b) | | | 14,115,263 | |

| | | | | | | | |

| | | | Semiconductors & Semiconductor Equipment – 3.9% | | | | |

| | 235,983 | | | Cavium, Inc.(b) | | | 9,722,500 | |

| | 183,700 | | | Hittite Microwave Corp.(b) | | | 12,004,795 | |

| | 286,362 | | | Semtech Corp.(b) | | | 8,587,996 | |

| | 229,711 | | | Silicon Laboratories, Inc.(b) | | | 9,810,957 | |

| | 149,294 | | | Ultratech, Inc.(b) | | | 4,523,608 | |

| | | | | | | | |

| | | | | | | 44,649,856 | |

| | | | | | | | |

| | | | Software – 7.4% | | | | |

| | 373,411 | | | Aspen Technology, Inc.(b) | | | 12,901,350 | |

| | 131,939 | | | CommVault Systems, Inc.(b) | | | 11,588,203 | |

| | 203,305 | | | FleetMatics Group PLC(b) | | | 7,634,103 | |

| | 322,274 | | | Guidewire Software, Inc.(b) | | | 15,182,328 | |

| | 234,301 | | | Imperva, Inc.(b) | | | 9,845,328 | |

| | 350,671 | | | QLIK Technologies, Inc.(b) | | | 12,006,975 | |

| | 102,568 | | | Ultimate Software Group, Inc. (The)(b) | | | 15,118,523 | |

| | | | | | | | |

| | | | | | | 84,276,810 | |

| | | | | | | | |

| | | | Specialty Retail – 5.2% | | | | |

| | 208,633 | | | Asbury Automotive Group, Inc.(b) | | | 11,099,276 | |

| | 136,601 | | | Cabela’s, Inc.(b) | | | 8,609,961 | |

| | 465,065 | | | Chico’s FAS, Inc. | | | 7,747,983 | |

| | 183,768 | | | Hibbett Sports, Inc.(b) | | | 10,318,573 | |

| | 76,302 | | | Lumber Liquidators Holdings, Inc.(b) | | | 8,137,608 | |

| | 442,140 | | | Tile Shop Holdings, Inc.(b) | | | 13,038,709 | |

| | | | | | | | |

| | | | | | | 58,952,110 | |

| | | | | | | | |

| | | | Textiles, Apparel & Luxury Goods – 2.3% | | | | |

| | 88,363 | | | Deckers Outdoor Corp.(b) | | | 5,824,889 | |

| | 175,007 | | | Oxford Industries, Inc. | | | 11,896,976 | |

See accompanying notes to financial statements.

| 18

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Textiles, Apparel & Luxury Goods – continued | | | | |

| | 432,171 | | | Tumi Holdings, Inc.(b) | | $ | 8,708,245 | |

| | | | | | | | |

| | | | | | | 26,430,110 | |

| | | | | | | | |

| | | | Total Common Stocks

(Identified Cost $763,703,479) | | | 1,083,688,907 | |

| | | | | | | | |

| | |

| Principal

Amount |

| | | | | | |

|

| | Short-Term Investments – 5.3% | |

| $ | 59,677,799 | | | Tri-Party Repurchase Agreement with Fixed Income Clearing Corporation, dated 9/30/2013 at 0.000% to be repurchased at $59,677,799 on 10/01/2013 collateralized by $59,390,000 U.S. Treasury Note, 2.625% due 7/31/2014 valued at $60,874,750 including accrued interest (Note 2 of Notes to Financial Statements) (Identified Cost $59,677,799) | | | 59,677,799 | |

| | | | | | | | |

| | | | Total Investments – 100.9%

(Identified Cost $823,381,278)(a) | | | 1,143,366,706 | |

| | | | Other Assets Less Liabilities—(0.9)% | | | (10,062,941 | ) |

| | | | | | | | |

| | | | Net Assets – 100.0% | | $ | 1,133,303,765 | |

| | | | | | | | |

| | (†) | | | See Note 2 of Notes to Financial Statements. | | | | |

| | (a) | | | Federal Tax Information: | | | | |

| | | | At September 30, 2013, the net unrealized appreciation on investments based on a cost of $823,526,294 for federal income tax purposes was as follows: | |

| | | | Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | | $ | 324,898,686 | |

| | | | Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | | | (5,058,274 | ) |

| | | | | | | | |

| | | | Net unrealized appreciation | | $ | 319,840,412 | |

| | | | | | | | |

| | (b) | | | Non-income producing security. | | | | |

See accompanying notes to financial statements.

19 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Growth Fund – continued

Industry Summary at September 30, 2013 (Unaudited)

| | | | |

Software | | | 7.4 | % |

Internet Software & Services | | | 6.8 | |

Health Care Equipment & Supplies | | | 6.6 | |

Professional Services | | | 6.3 | |

Biotechnology | | | 6.2 | |

Specialty Retail | | | 5.2 | |

Machinery | | | 5.1 | |

Semiconductors & Semiconductor Equipment | | | 3.9 | |

Oil, Gas & Consumable Fuels | | | 3.9 | |

Diversified Consumer Services | | | 3.6 | |

Commercial Banks | | | 3.5 | |

Energy Equipment & Services | | | 2.9 | |

Hotels, Restaurants & Leisure | | | 2.8 | |

Electronic Equipment, Instruments & Components | | | 2.8 | |

Textiles, Apparel & Luxury Goods | | | 2.3 | |

Aerospace & Defense | | | 2.1 | |

Health Care Technology | | | 2.1 | |

Capital Markets | | | 2.0 | |

Other Investments, less than 2% each | | | 20.1 | |

Short-Term Investments | | | 5.3 | |

| | | | |

Total Investments | | | 100.9 | |

Other assets less liabilities | | | (0.9 | ) |

| | | | |

Net Assets | | | 100.0 | % |

| | | | |

See accompanying notes to financial statements.

| 20

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – 95.6% of Net Assets | |

| | |

| | | | Auto Components – 1.7% | | | | |

| | 472,300 | | | Dana Holding Corp. | | $ | 10,787,332 | |

| | 204,378 | | | Remy International, Inc. | | | 4,136,611 | |

| | 123,821 | | | Tenneco, Inc.(b) | | | 6,252,960 | |

| | | | | | | | |

| | | | | | | 21,176,903 | |

| | | | | | | | |

| | | | Building Products – 0.7% | | | | |

| | 146,078 | | | Armstrong World Industries, Inc.(b) | | | 8,028,447 | |

| | | | | | | | |

| | | | Capital Markets – 1.2% | | | | |

| | 313,442 | | | Safeguard Scientifics, Inc.(b) | | | 4,917,905 | |

| | 238,176 | | | Stifel Financial Corp.(b) | | | 9,817,615 | |

| | | | | | | | |

| | | | | | | 14,735,520 | |

| | | | | | | | |

| | | | Chemicals – 3.1% | | | | |

| | 235,502 | | | Cabot Corp. | | | 10,058,290 | |

| | 113,012 | | | Minerals Technologies, Inc. | | | 5,579,402 | |

| | 256,669 | | | Olin Corp. | | | 5,921,354 | |

| | 331,159 | | | Tronox Ltd., Class A | | | 8,103,461 | |

| | 56,578 | | | WR Grace & Co.(b) | | | 4,944,917 | |

| | 182,083 | | | Zep, Inc. | | | 2,960,670 | |

| | | | | | | | |

| | | | | | | 37,568,094 | |

| | | | | | | | |

| | | | Commercial Banks – 11.3% | | | | |

| | 587,102 | | | BancorpSouth, Inc. | | | 11,706,814 | |

| | 618,248 | | | Cathay General Bancorp | | | 14,448,456 | |

| | 159,134 | | | City National Corp. | | | 10,607,872 | |

| | 495,700 | | | CVB Financial Corp. | | | 6,701,864 | |

| | 482,130 | | | First Financial Bancorp | | | 7,313,912 | |

| | 138,673 | | | First Financial Bankshares, Inc. | | | 8,156,746 | |

| | 160,056 | | | IBERIABANK Corp. | | | 8,302,105 | |

| | 268,620 | | | PacWest Bancorp | | | 9,229,783 | |

| | 249,560 | | | Pinnacle Financial Partners, Inc.(b) | | | 7,439,384 | |

| | 226,020 | | | Popular, Inc.(b) | | | 5,928,505 | |

| | 183,036 | | | Prosperity Bancshares, Inc. | | | 11,318,946 | |

| | 133,352 | | | Signature Bank(b) | | | 12,204,375 | |

| | 163,937 | | | Texas Capital Bancshares, Inc.(b) | | | 7,536,184 | |

| | 426,402 | | | Tristate Capital Holdings, Inc.(b) | | | 5,496,322 | |

| | 264,608 | | | Wintrust Financial Corp. | | | 10,867,450 | |

| | | | | | | | |

| | | | | | | 137,258,718 | |

| | | | | | | | |

| | | | Commercial Services & Supplies – 4.3% | | | | |

| | 683,448 | | | ACCO Brands Corp.(b) | | | 4,538,095 | |

| | 452,349 | | | KAR Auction Services, Inc. | | | 12,760,765 | |

| | 144,766 | | | McGrath Rentcorp | | | 5,168,146 | |

| | 241,139 | | | Performant Financial Corp.(b) | | | 2,633,238 | |

| | 292,380 | | | Rollins, Inc. | | | 7,750,994 | |

| | 174,790 | | | Viad Corp. | | | 4,361,010 | |

See accompanying notes to financial statements.

21 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Commercial Services & Supplies – continued | | | | |

| | 182,077 | | | Waste Connections, Inc. | | $ | 8,268,117 | |

| | 309,847 | | | West Corp. | | | 6,869,308 | |

| | | | | | | | |

| | | | | | | 52,349,673 | |

| | | | | | | | |

| | | | Communications Equipment – 0.8% | | | | |

| | 496,640 | | | Harmonic, Inc.(b) | | | 3,819,162 | |

| | 181,462 | | | NETGEAR, Inc.(b) | | | 5,599,917 | |

| | | | | | | | |

| | | | | | | 9,419,079 | |

| | | | | | | | |

| | | | Computers & Peripherals – 0.5% | | | | |

| | 526,686 | | | QLogic Corp.(b) | | | 5,761,945 | |

| | | | | | | | |

| | | | Construction & Engineering – 1.3% | | | | |

| | 318,096 | | | MYR Group, Inc.(b) | | | 7,729,733 | |

| | 327,074 | | | Primoris Services Corp. | | | 8,330,574 | |

| | | | | | | | |

| | | | | | | 16,060,307 | |

| | | | | | | | |

| | | | Consumer Finance – 0.9% | | | | |

| | 45,299 | | | Credit Acceptance Corp.(b) | | | 5,019,582 | |

| | 503,699 | | | DFC Global Corp.(b) | | | 5,535,652 | |

| | | | | | | | |

| | | | | | | 10,555,234 | |

| | | | | | | | |

| | | | Distributors – 0.5% | | | | |

| | 89,097 | | | Core-Mark Holding Co., Inc. | | | 5,919,605 | |

| | | | | | | | |

| | | | Diversified Financial Services – 1.1% | | | | |

| | 222,094 | | | MarketAxess Holdings, Inc. | | | 13,334,524 | |

| | | | | | | | |

| | | | Electric Utilities – 2.4% | | | | |

| | 273,388 | | | ALLETE, Inc. | | | 13,204,640 | |

| | 60,113 | | | ITC Holdings Corp. | | | 5,642,206 | |

| | 261,847 | | | UIL Holdings Corp. | | | 9,735,472 | |

| | | | | | | | |

| | | | | | | 28,582,318 | |

| | | | | | | | |

| | | | Electrical Equipment – 2.5% | | | | |

| | 250,413 | | | AZZ, Inc. | | | 10,482,288 | |

| | 146,460 | | | EnerSys | | | 8,879,870 | |

| | 258,156 | | | General Cable Corp. | | | 8,196,453 | |

| | 148,139 | | | Global Power Equipment Group, Inc. | | | 2,979,075 | |

| | | | | | | | |

| | | | | | | 30,537,686 | |

| | | | | | | | |

| | | | Electronic Equipment, Instruments & Components – 4.6% | | | | |

| | 181,646 | | | Belden, Inc. | | | 11,634,426 | |

| | 125,677 | | | Checkpoint Systems, Inc.(b) | | | 2,098,806 | |

| | 129,858 | | | Cognex Corp. | | | 4,072,347 | |

| | 153,412 | | | Littelfuse, Inc. | | | 11,999,887 | |

| | 262,595 | | | Methode Electronics, Inc. | | | 7,352,660 | |

| | 166,474 | | | Rogers Corp.(b) | | | 9,901,873 | |

See accompanying notes to financial statements.

| 22

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Electronic Equipment, Instruments & Components – continued | | | | |

| | 696,707 | | | Vishay Intertechnology, Inc.(b) | | $ | 8,980,553 | |

| | | | | | | | |

| | | | | | | 56,040,552 | |

| | | | | | | | |

| | | | Energy Equipment & Services – 2.5% | | | | |

| | 147,478 | | | Bristow Group, Inc. | | | 10,730,499 | |

| | 469,230 | | | Helix Energy Solutions Group, Inc.(b) | | | 11,904,365 | |

| | 1,447,550 | | | Parker Drilling Co.(b) | | | 8,251,035 | |

| | | | | | | | |

| | | | | | | 30,885,899 | |

| | | | | | | | |

| | | | Food & Staples Retailing – 1.1% | | | | |

| | 93,950 | | | Casey’s General Stores, Inc. | | | 6,905,325 | |

| | 312,584 | | | Spartan Stores, Inc. | | | 6,895,603 | |

| | | | | | | | |

| | | | | | | 13,800,928 | |

| | | | | | | | |

| | | | Food Products – 1.2% | | | | |

| | 260,206 | | | Darling International, Inc.(b) | | | 5,505,959 | |

| | 75,683 | | | Ingredion, Inc. | | | 5,007,944 | |

| | 52,080 | | | J & J Snack Foods Corp. | | | 4,203,898 | |

| | | | | | | | |

| | | | | | | 14,717,801 | |

| | | | | | | | |

| | | | Gas Utilities – 0.5% | | | | |

| | 71,432 | | | New Jersey Resources Corp. | | | 3,146,580 | |

| | 73,877 | | | UGI Corp. | | | 2,890,807 | |

| | | | | | | | |

| | | | | | | 6,037,387 | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies – 1.0% | | | | |

| | 111,089 | | | SurModics, Inc.(b) | | | 2,641,697 | |

| | 112,062 | | | Teleflex, Inc. | | | 9,220,461 | |

| | | | | | | | |

| | | | | | | 11,862,158 | |

| | | | | | | | |

| | | | Health Care Providers & Services – 2.5% | | | | |

| | 303,234 | | | Bio-Reference Labs, Inc.(b) | | | 9,060,632 | |

| | 157,482 | | | Hanger Orthopedic Group, Inc.(b) | | | 5,316,592 | |

| | 69,094 | | | MEDNAX, Inc.(b) | | | 6,937,038 | |

| | 136,766 | | | WellCare Health Plans, Inc.(b) | | | 9,538,061 | |

| | | | | | | | |

| | | | | | | 30,852,323 | |

| | | | | | | | |

| | | | Health Care Technology – 0.8% | | | | |

| | 379,203 | | | MedAssets, Inc.(b) | | | 9,639,340 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure – 3.7% | | | | |

| | 139,446 | | | Churchill Downs, Inc. | | | 12,064,868 | |

| | 58,331 | | | Cracker Barrel Old Country Store, Inc. | | | 6,022,093 | |

| | 482,098 | | | Diamond Resorts International, Inc.(b) | | | 9,068,263 | |

| | 233,793 | | | Marriott Vacations Worldwide Corp.(b) | | | 10,286,892 | |

| | 233,047 | | | Six Flags Entertainment Corp. | | | 7,874,658 | |

| | | | | | | | |

| | | | | | | 45,316,774 | |

| | | | | | | | |

See accompanying notes to financial statements.

23 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Household Durables – 1.3% | | | | |

| | 249,633 | | | Jarden Corp.(b) | | $ | 12,082,237 | |

| | 160,487 | | | La-Z-Boy, Inc. | | | 3,644,660 | |

| | | | | | | | |

| | | | | | | 15,726,897 | |

| | | | | | | | |

| | | | Industrial Conglomerates – 0.8% | | | | |

| | 314,611 | | | Raven Industries, Inc. | | | 10,290,926 | |

| | | | | | | | |

| | | | Insurance – 3.8% | | | | |

| | 446,540 | | | Employers Holdings, Inc. | | | 13,280,100 | |

| | 326,467 | | | HCC Insurance Holdings, Inc. | | | 14,305,784 | |

| | 216,618 | | | ProAssurance Corp. | | | 9,760,807 | |

| | 133,959 | | | Reinsurance Group of America, Inc., Class A | | | 8,973,913 | |

| | | | | | | | |

| | | | | | | 46,320,604 | |

| | | | | | | | |

| | | | Internet & Catalog Retail – 1.3% | | | | |

| | 153,101 | | | HSN, Inc. | | | 8,209,276 | |

| | 87,030 | | | Liberty Ventures, Series A(b) | | | 7,673,435 | |

| | | | | | | | |

| | | | | | | 15,882,711 | |

| | | | | | | | |

| | | | Internet Software & Services – 0.9% | | | | |

| | 341,227 | | | Perficient, Inc.(b) | | | 6,264,927 | |

| | 515,461 | | | United Online, Inc. | | | 4,113,379 | |

| | | | | | | | |

| | | | | | | 10,378,306 | |

| | | | | | | | |

| | | | IT Services – 2.9% | | | | |

| | 459,809 | | | Convergys Corp. | | | 8,621,419 | |

| | 354,406 | | | Euronet Worldwide, Inc.(b) | | | 14,105,359 | |

| | 142,959 | | | WEX, Inc.(b) | | | 12,544,652 | |

| | | | | | | | |

| | | | | | | 35,271,430 | |

| | | | | | | | |

| | | | Machinery – 5.6% | | | | |

| | 156,182 | | | Actuant Corp., Class A | | | 6,066,109 | |

| | 79,516 | | | Alamo Group, Inc. | | | 3,889,128 | |

| | 225,097 | | | Albany International Corp., Class A | | | 8,074,229 | |

| | 369,810 | | | Altra Holdings, Inc. | | | 9,951,587 | |

| | 254,862 | | | John Bean Technologies Corp. | | | 6,340,967 | |

| | 179,900 | | | RBC Bearings, Inc.(b) | | | 11,853,611 | |

| | 214,905 | | | TriMas Corp.(b) | | | 8,015,956 | |

| | 214,071 | | | Wabtec Corp. | | | 13,458,644 | |

| | | | | | | | |

| | | | | | | 67,650,231 | |

| | | | | | | | |

| | | | Marine – 0.9% | | | | |

| | 121,016 | | | Kirby Corp.(b) | | | 10,473,935 | |

| | | | | | | | |

| | | | Media – 2.8% | | | | |

| | 345,302 | | | Carmike Cinemas, Inc.(b) | | | 7,624,268 | |

| | 267,658 | | | E.W. Scripps Co. (The), Class A(b) | | | 4,911,524 | |

See accompanying notes to financial statements.

| 24

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | Media – continued | | | | |

| | 186,322 | | | John Wiley & Sons, Inc., Class A | | $ | 8,885,696 | |

| | 360,616 | | | Live Nation Entertainment, Inc.(b) | | | 6,689,427 | |

| | 333,537 | | | National CineMedia, Inc. | | | 6,290,508 | |

| | | | | | | | |

| | | | | | | 34,401,423 | |

| | | | | | | | |

| | | | Metals & Mining – 2.2% | | | | |

| | 199,275 | | | Globe Specialty Metals, Inc. | | | 3,070,828 | |

| | 149,911 | | | Haynes International, Inc. | | | 6,795,465 | |

| | 459,624 | | | Horsehead Holding Corp.(b) | | | 5,726,915 | |

| | 40,984 | | | Reliance Steel & Aluminum Co. | | | 3,002,898 | |

| | 440,342 | | | SunCoke Energy, Inc.(b) | | | 7,485,814 | |

| | | | | | | | |

| | | | | | | 26,081,920 | |

| | | | | | | | |

| | | | Multi Utilities – 0.7% | | | | |

| | 184,776 | | | NorthWestern Corp. | | | 8,300,138 | |

| | | | | | | | |

| | | | Multiline Retail – 0.4% | | | | |

| | 293,168 | | | Fred’s, Inc. Class A | | | 4,588,079 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels – 1.2% | | | | |

| | 389,935 | | | EPL Oil & Gas, Inc.(b) | | | 14,470,488 | |

| | | | | | | | |

| | | | Pharmaceuticals – 0.4% | | | | |

| | 122,062 | | | Mallinckrodt PLC(b) | | | 5,381,713 | |

| | | | | | | | |

| | | | REITs – Apartments – 1.9% | | | | |

| | 213,247 | | | American Campus Communities, Inc. | | | 7,282,385 | |

| | 124,279 | | | Home Properties, Inc. | | | 7,177,112 | |

| | 133,984 | | | Mid-America Apartment Communities, Inc. | | | 8,374,000 | |

| | | | | | | | |

| | | | | | | 22,833,497 | |

| | | | | | | | |

| | | | REITs – Diversified – 1.0% | | | | |

| | 224,639 | | | DuPont Fabros Technology, Inc. | | | 5,788,947 | |

| | 157,581 | | | Potlatch Corp. | | | 6,252,814 | |

| | | | | | | | |

| | | | | | | 12,041,761 | |

| | | | | | | | |

| | | | REITs – Healthcare – 0.8% | | | | |

| | 324,457 | | | Omega Healthcare Investors, Inc. | | | 9,691,531 | |

| | | | | | | | |

| | | | REITs – Hotels – 0.8% | | | | |

| | 1,629,443 | | | Hersha Hospitality Trust | | | 9,108,586 | |

| | | | | | | | |

| | | | REITs – Office Property – 0.8% | | | | |

| | 532,268 | | | BioMed Realty Trust, Inc. | | | 9,894,862 | |

| | | | | | | | |

| | | | REITs – Single Tenant – 0.5% | | | | |

| | 195,910 | | | National Retail Properties, Inc. | | | 6,233,856 | |

| | | | | | | | |

See accompanying notes to financial statements.

25 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

|

| | Common Stocks – continued | |

| | |

| | | | REITs – Storage – 2.2% | | | | |

| | 701,228 | | | CubeSmart | | $ | 12,509,907 | |

| | 180,366 | | | Sovran Self Storage, Inc. | | | 13,650,099 | |

| | | | | | | | |

| | | | | | | 26,160,006 | |

| | | | | | | | |

| | | | Road & Rail – 2.2% | | | | |

| | 267,431 | | | Avis Budget Group, Inc.(b) | | | 7,710,036 | |

| | 62,675 | | | Genesee & Wyoming, Inc., Class A(b) | | | 5,826,895 | |

| | 293,871 | | | Old Dominion Freight Line, Inc.(b) | | | 13,515,127 | |

| | | | | | | | |

| | | | | | | 27,052,058 | |

| | | | | | | | |

| | | | Semiconductors & Semiconductor Equipment – 2.3% | | | | |

| | 352,473 | | | Magnachip Semiconductor Corp.(b) | | | 7,588,744 | |

| | 315,850 | | | Semtech Corp.(b) | | | 9,472,341 | |

| | 637,778 | | | Teradyne, Inc.(b) | | | 10,536,093 | |

| | | | | | | | |

| | | | | | | 27,597,178 | |

| | | | | | | | |

| | | | Software – 1.9% | | | | |

| | 234,935 | | | Monotype Imaging Holdings, Inc. | | | 6,733,237 | |

| | 234,725 | | | SS&C Technologies Holdings, Inc.(b) | | | 8,943,022 | |

| | 201,746 | | | Synchronoss Technologies, Inc.(b) | | | 7,678,453 | |

| | | | | | | | |

| | | | | | | 23,354,712 | |

| | | | | | | | |

| | | | Specialty Retail – 2.7% | | | | |

| | 282,867 | | | Barnes & Noble, Inc.(b) | | | 3,660,299 | |

| | 170,258 | | | Genesco, Inc.(b) | | | 11,165,520 | |

| | 49,036 | | | Jos. A. Bank Clothiers, Inc.(b) | | | 2,155,622 | |

| | 175,920 | | | Rent-A-Center, Inc. | | | 6,702,552 | |

| | 363,798 | | | Sally Beauty Holdings, Inc.(b) | | | 9,516,956 | |

| | | | | | | | |

| | | | | | | 33,200,949 | |

| | | | | | | | |

| | | | Thrifts & Mortgage Finance – 0.5% | | | | |

| | 485,003 | | | Capitol Federal Financial, Inc. | | | 6,028,587 | |

| | | | | | | | |

| | | | Trading Companies & Distributors – 1.6% | | | | |

| | 98,104 | | | DXP Enterprises, Inc.(b) | | | 7,747,273 | |

| | 156,263 | | | H&E Equipment Services, Inc.(b) | | | 4,150,345 | |

| | 267,058 | | | Rush Enterprises, Inc., Class A(b) | | | 7,079,708 | |

| | | | | | | | |

| | | | | | | 18,977,326 | |

| | | | | | | | |

| | | | Transportation Infrastructure – 0.7% | | | | |

| | 147,211 | | | Macquarie Infrastructure Co. LLC | | | 7,881,677 | |

| | | | | | | | |

| | | | Water Utilities – 0.3% | | | | |

| | 150,135 | | | Middlesex Water Co. | | | 3,211,388 | |

| | | | | | | | |

| | | | Total Common Stocks

(Identified Cost $756,315,294) | | | 1,158,927,990 | |

| | | | | | | | |

See accompanying notes to financial statements.

| 26

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

| |

| | Closed End Investment Companies – 2.1% | | | | |

| | 468,764 | | | Ares Capital Corp. | | $ | 8,104,929 | |

| | 899,272 | | | Fifth Street Finance Corp. | | | 9,253,509 | |

| | 475,547 | | | Hercules Technology Growth Capital, Inc. | | | 7,252,092 | |

| | | | | | | | |

| | | | Total Closed End Investment Companies

(Identified Cost $22,036,891) | | | 24,610,530 | |

| | | | | | | | |

| |

| | Warrants – 0.0% | | | | |

| | 67,892 | | | Magnum Hunter Resources Corp., Expiration on 10/14/2013 at $10.50(b)(c)(d)

(Identified Cost $0) | | | — | |

| | | | | | | | |

| | |

| Principal

Amount |

| | | | | | |

|

| | Short-Term Investments – 2.2% | |

| $ | 26,590,292 | | | Tri-Party Repurchase Agreement with Fixed Income Clearing Corporation, dated 9/30/2013 at 0.000% to be repurchased at $26,590,292 on 10/01/2013 collateralized by $27,540,000 U.S. Treasury Note, 0.625% due 8/31/2017 valued at $27,126,900 including accrued interest (Note 2 of Notes to Financial Statements) (Identified Cost $26,590,292) | | | 26,590,292 | |

| | | | | | | | |

| | | | Total Investments – 99.9%

(Identified Cost $804,942,477)(a) | | | 1,210,128,812 | |

| | | | Other assets less liabilities – 0.1% | | | 1,752,314 | |

| | | | | | | | |

| | | | Net Assets – 100.0% | | $ | 1,211,881,126 | |

| | | | | | | | |

| | (†) | | | See Note 2 of Notes to Financial Statements. | |

| | (a) | | | Federal Tax Information: | |

| | | | At September 30, 2013, the net unrealized appreciation on investments based on a cost of $804,927,604 for federal income tax purposes was as follows: | |

| | | | Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | | $ | 416,234,871 | |

| | | | Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | | | (11,033,663 | ) |

| | | | | | | | |

| | | | Net unrealized appreciation | | $ | 405,201,208 | |

| | | | | | | | |

| | (b) | | | Non-income producing security. | |

| | (c) | | | Fair valued by the Fund’s investment adviser. | |

| | (d) | | | Illiquid security. | |

| | | | | |

| | REITs | | | Real Estate Investment Trusts | |

See accompanying notes to financial statements.

27 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Small Cap Value Fund – continued

Industry Summary at September 30, 2013 (Unaudited)

| | | | |

Commercial Banks | | | 11.3 | % |

Machinery | | | 5.6 | |

Electronic Equipment, Instruments & Components | | | 4.6 | |

Commercial Services & Supplies | | | 4.3 | |

Insurance | | | 3.8 | |

Hotels, Restaurants & Leisure | | | 3.7 | |

Chemicals | | | 3.1 | |

IT Services | | | 2.9 | |

Media | | | 2.8 | |

Specialty Retail | | | 2.7 | |

Energy Equipment & Services | | | 2.5 | |

Health Care Providers & Services | | | 2.5 | |

Electrical Equipment | | | 2.5 | |

Electric Utilities | | | 2.4 | |

Semiconductors & Semiconductor Equipment | | | 2.3 | |

Road & Rail | | | 2.2 | |

REITs – Storage | | | 2.2 | |

Metals & Mining | | | 2.2 | |

Closed End Investment Companies | | | 2.1 | |

Other Investments, less than 2% each | | | 32.0 | |

Short-Term Investments | | | 2.2 | |

| | | | |

Total Investments | | | 99.9 | |

Other assets less liabilities | | | 0.1 | |

| | | | |

Net Assets | | | 100.0 | % |

| | | | |

See accompanying notes to financial statements.

| 28

Statements of Assets and Liabilities

September 30, 2013

| | | | | | | | |

| | | Small Cap

Growth Fund | | | Small Cap Value Fund | |

ASSETS | | | | | | | | |

Investments at cost | | $ | 823,381,278 | | | $ | 804,942,477 | |

Net unrealized appreciation | | | 319,985,428 | | | | 405,186,335 | |

| | | | | | | | |

Investments at value | | | 1,143,366,706 | | | | 1,210,128,812 | |

Cash | | | — | | | | 264,281 | |

Receivable for Fund shares sold | | | 5,248,378 | | | | 731,263 | |

Receivable for securities sold | | | 1,301,626 | | | | 3,399,342 | |

Dividends receivable | | | 66,572 | | | | 1,298,165 | |

| | | | | | | | |

TOTAL ASSETS | | | 1,149,983,282 | | | | 1,215,821,863 | |

| | | | | | | | |

LIABILITIES | | | | | | | | |

Payable for securities purchased | | | 14,269,972 | | | | 1,841,328 | |

Payable for Fund shares redeemed | | | 1,486,433 | | | | 1,086,230 | |

Management fees payable (Note 5) | | | 698,032 | | | | 701,507 | |

Deferred Trustees’ fees (Note 5) | | | 98,499 | | | | 173,171 | |

Administrative fees payable (Note 5) | | | 40,229 | | | | 43,393 | |

Payable to distributor (Note 5d) | | | 14,086 | | | | 15,202 | |

Other accounts payable and accrued expenses | | | 72,266 | | | | 79,906 | |

| | | | | | | | |

TOTAL LIABILITIES | | | 16,679,517 | | | | 3,940,737 | |

| | | | | | | | |

NET ASSETS | | $ | 1,133,303,765 | | | $ | 1,211,881,126 | |

| | | | | | | | |

NET ASSETS CONSIST OF: | | | | | | | | |

Paid-in capital | | $ | 747,231,982 | | | $ | 711,714,328 | |

Accumulated net investment (loss)/Undistributed net investment income | | | (6,100,899 | ) | | | 192,931 | |