United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the

Securities Exchange Act of 1934

For the month of

September 2021

Vale S.A.

Praia de Botafogo nº 186, 18º andar, Botafogo

22250-145 Rio de Janeiro, RJ, Brazil

(Address of principal executive office)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.)

(Check One) Form 20-F x Form 40-F ¨

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1))

(Check One) Yes ¨ No x

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7))

(Check One) Yes ¨ No x

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

(Check One) Yes ¨ No x

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b). 82- .)

| September 9th, 2021 21st Analyst & Investor Tour Iron ore briquettes stockpile |

| Agenda Disclaimer “This presentation may include statements that present Vale's expectations about future events or results .. All statements, when based upon expectations about the future involve various risks and uncertainties .. Vale cannot guarantee that such statements will prove correct .. These risks and uncertainties include factors related to the following : (a) the countries where we operate, especially Brazil and Canada ; (b) the global economy ; (c) the capital markets ; (d) the mining and metals prices and their dependence on global industrial production, which is cyclical by nature ; (e) global competition in the markets in which Vale operates ; and (f) the estimation of mineral resources and reserves, the exploration of mineral reserves and resources and the development of mining facilities, our ability to obtain or renew licenses, the depletion and exhaustion of mines and mineral reserves and resources .. To obtain further information on factors that may lead to results different from those forecast by Vale, please consult the reports Vale files with the U .. S .. Securities and Exchange Commission (SEC), the Brazilian Comissão de Valores Mobiliários (CVM) and in particular the factors discussed under “Forward - Looking Statements” and “Risk Factors” in Vale’s annual report on Form 20 - F .. ” “Cautionary Note to U .. S .. Investors – Vale currently complies with SEC Industry Guide 7 in its reporting of mineral reserves in SEC filings .. SEC Industry Guide 7 permits mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce .. We present certain information in this presentation that are not be permitted in an SEC filing .. These materials are not proven or probable reserves, as defined by the SEC, and we cannot assure you that these materials will be converted into proven or probable reserves, as defined by the SEC .. Starting in its next annual report on Form 20 - F, Vale will comply with Subpart 1300 of Regulation S - K, which will replace SEC Industry Guide 7 .. Subpart 1300 of Regulation S - K permits mining companies, in their filings with the SEC, to disclose “mineral reserves”, “mineral resources” and “exploration targets” that are based upon and accurately reflects information and supporting documentation of a qualified person .. We present certain information in this presentation that are not based upon information or documentation of a qualified person, and that will not be permitted in an SEC filing under Subpart 1300 of Regulation S - K .. These materials are not mineral reserves, mineral resources or exploration targets, as defined by the SEC, and we cannot assure you that these materials will be converted into mineral reserves, mineral resources or exploration targets, as defined by the SEC .. U .. S .. Investors should consider closely the disclosure in our Annual Report on Form 20 - K, which may be obtained from us, from our website or at http : //http : //us .. sec .. gov/edgar .. shtml .. ” |

| September 9th, 2021 21st Analyst & Investor Tour Marcello Spinelli |

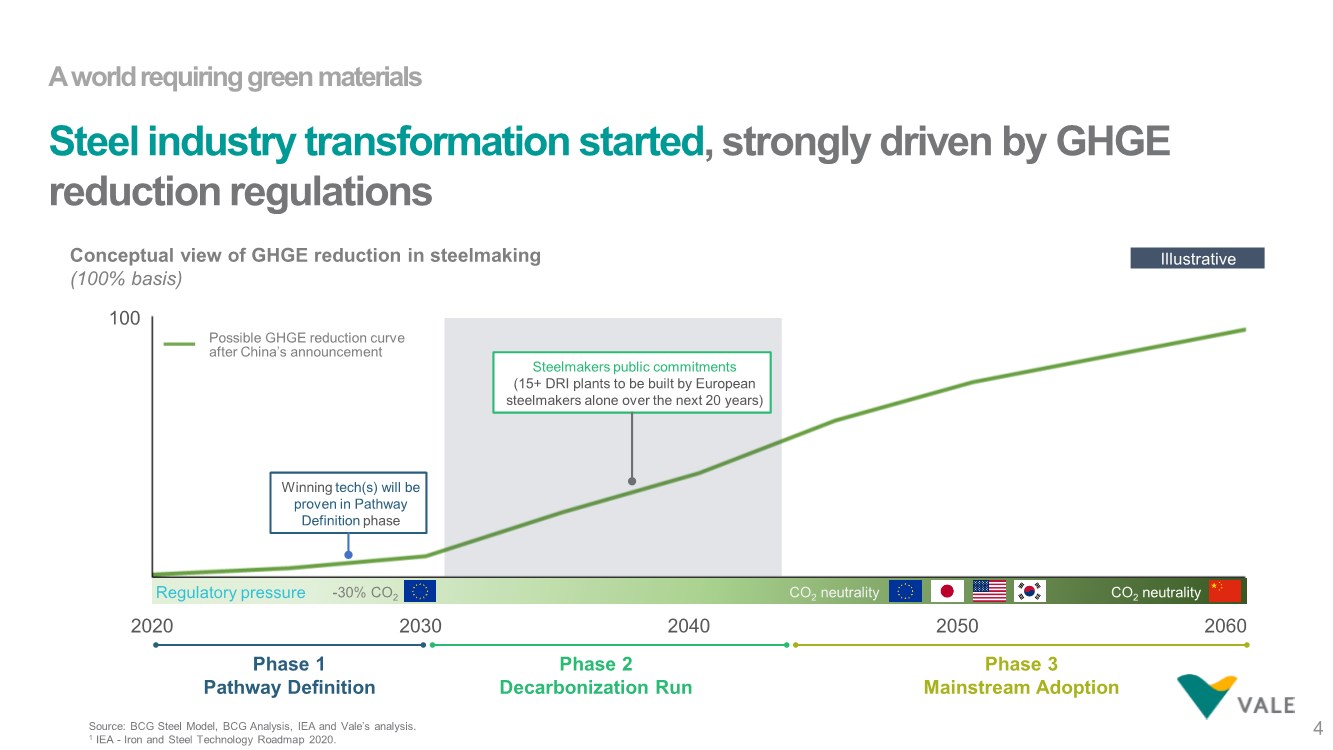

| A world requiring green materials Steel industry transformation started, strongly driven by GHGE reduction regulations 4 Phase 2 Decarbonization Run Phase 1 Pathway Definition Phase 3 Mainstream Adoption 2020 2030 2040 2050 2060 CO2 neutrality -30% CO2 Regulatory pressure CO2 neutrality Steelmakers public commitments (15+ DRI plants to be built by European steelmakers alone over the next 20 years) Winning tech(s) will be proven in Pathway Definition phase Illustrative Conceptual view of GHGE reduction in steelmaking (100% basis) 100 Possible GHGE reduction curve after China’s announcement Source: BCG Steel Model, BCG Analysis, IEA and Vale’s analysis. 1 IEA - Iron and Steel Technology Roadmap 2020. |

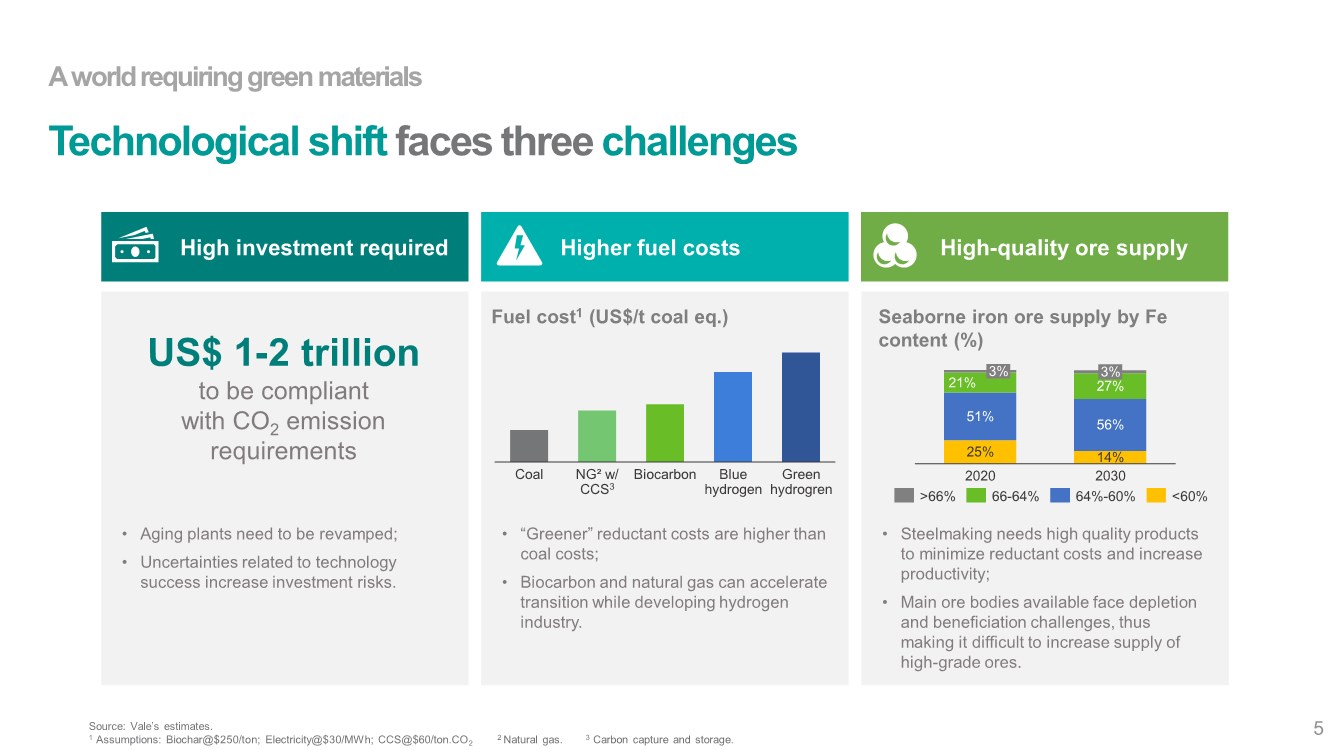

| A world requiring green materials Technological shift faces three challenges 5 High investment required Higher fuel costs High-quality ore supply Fuel cost1 (US$/t coal eq.) NG² w/ CCS3 Coal Blue hydrogen Biocarbon Green hydrogren Source: Vale’s estimates. 1 Assumptions: Biochar@$250/ton; Electricity@$30/MWh; CCS@$60/ton.CO2 2 Natural gas. 3 Carbon capture and storage. Seaborne iron ore supply by Fe content (%) 25% 14% 51% 56% 21% 27% 3% 3% 2020 2030 64%-60% >66% <60% 66-64% • Steelmaking needs high quality products to minimize reductant costs and increase productivity; • Main ore bodies available face depletion and beneficiation challenges, thus making it difficult to increase supply of high-grade ores. •“Greener” reductant costs are higher than coal costs; • Biocarbon and natural gas can accelerate transition while developing hydrogen industry. • Aging plants need to be revamped; • Uncertainties related to technology success increase investment risks. US$ 1-2 trillion to be compliant with CO2 emission requirements |

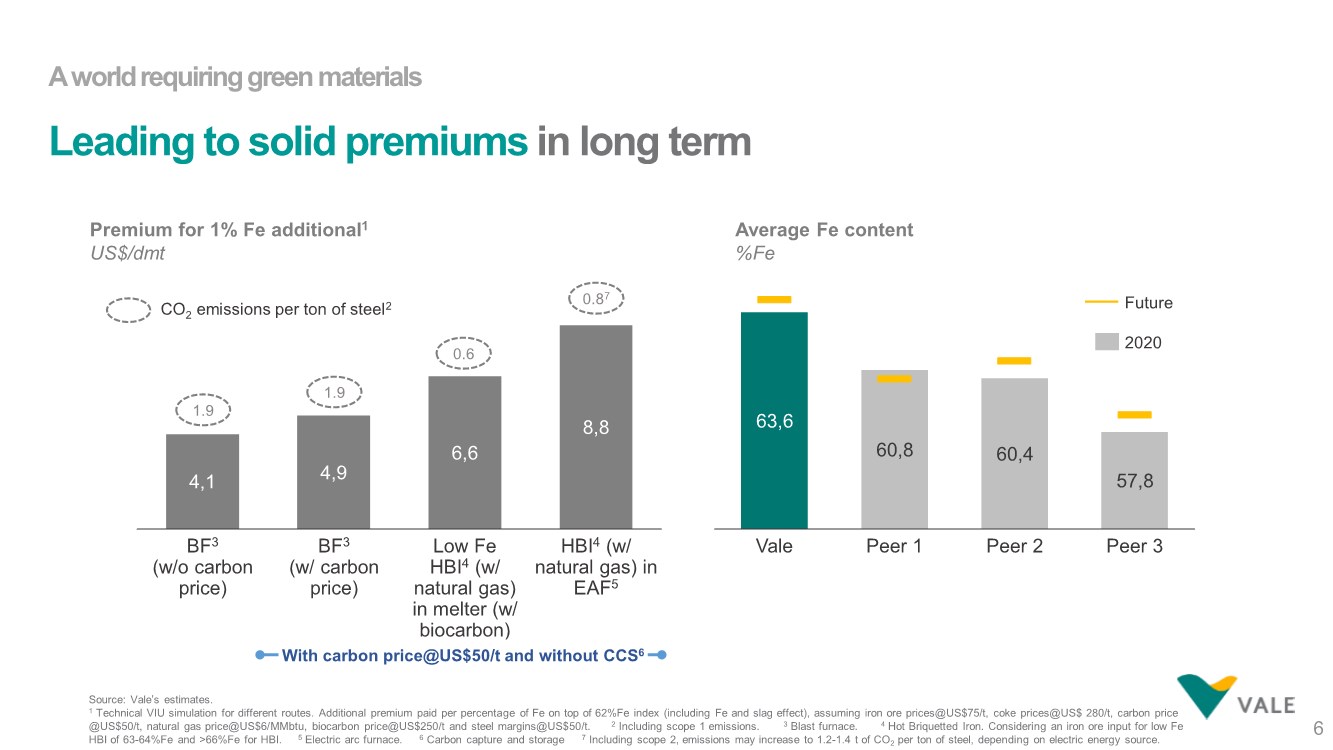

| A world requiring green materials Leading to solid premiums in long term 6 4,1 4,9 6,6 8,8 BF3 (w/o carbon price) BF3 (w/ carbon price) Low Fe HBI4 (w/ natural gas) in melter (w/ biocarbon) HBI4 (w/ natural gas) in EAF5 63,6 60,8 60,4 57,8 Peer 2 Vale Peer 1 Peer 3 Premium for 1% Fe additional1 US$/dmt Average Fe content %Fe Future 2020 Source: Vale’s estimates. 1 Technical VIU simulation for different routes. Additional premium paid per percentage of Fe on top of 62%Fe index (including Fe and slag effect), assuming iron ore prices@US$75/t, coke prices@US$ 280/t, carbon price @US$50/t, natural gas price@US$6/MMbtu, biocarbon price@US$250/t and steel margins@US$50/t. 2 Including scope 1 emissions. 3 Blast furnace. 4 Hot Briquetted Iron. Considering an iron ore input for low Fe HBI of 63-64%Fe and >66%Fe for HBI. 5 Electric arc furnace. 6 Carbon capture and storage 7 Including scope 2, emissions may increase to 1.2-1.4 t of CO2 per ton of steel, depending on electric energy source. 1.9 1.9 0.6 0.87 CO2 emissions per ton of steel2 With carbon price@US$50/t and without CCS6 |

| September 9th, 2021 21st Analyst & Investor Tour Rogerio Nogueira |

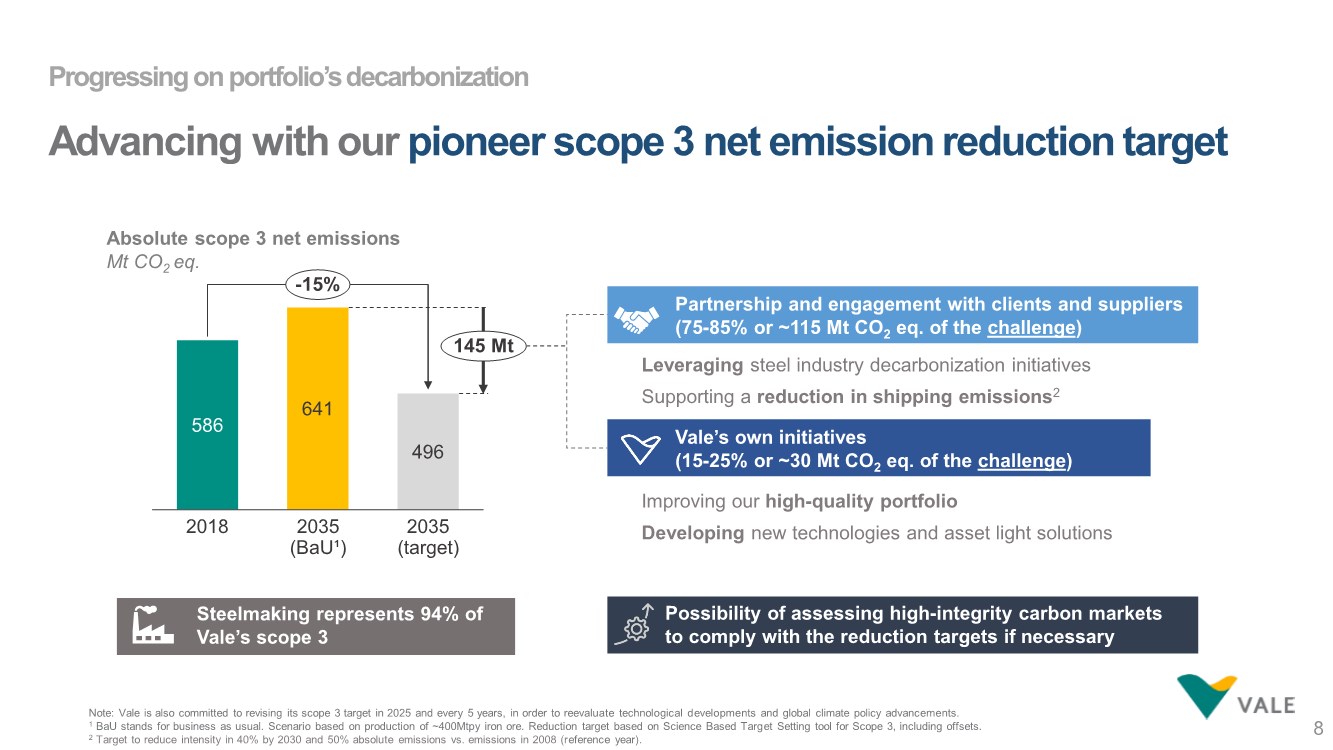

| Progressing on portfolio’s decarbonization Advancing with our pioneer scope 3 net emission reduction target 8 Note: Vale is also committed to revising its scope 3 target in 2025 and every 5 years, in order to reevaluate technological developments and global climate policy advancements. 1 BaU stands for business as usual. Scenario based on production of ~400Mtpy iron ore. Reduction target based on Science Based Target Setting tool for Scope 3, including offsets. 2 Target to reduce intensity in 40% by 2030 and 50% absolute emissions vs. emissions in 2008 (reference year). Steelmaking represents 94% of Vale’s scope 3 Leveraging steel industry decarbonization initiatives Supporting a reduction in shipping emissions2 586 641 496 2018 2035 (BaU¹) 2035 (target) 145 Mt -15% Partnership and engagement with clients and suppliers (75-85% or ~115 Mt CO2 eq. of the challenge) Improving our high-quality portfolio Developing new technologies and asset light solutions Vale’s own initiatives (15-25% or ~30 Mt CO2 eq. of the challenge) Absolute scope 3 net emissions Mt CO2 eq. Possibility of assessing high-integrity carbon markets to comply with the reduction targets if necessary |

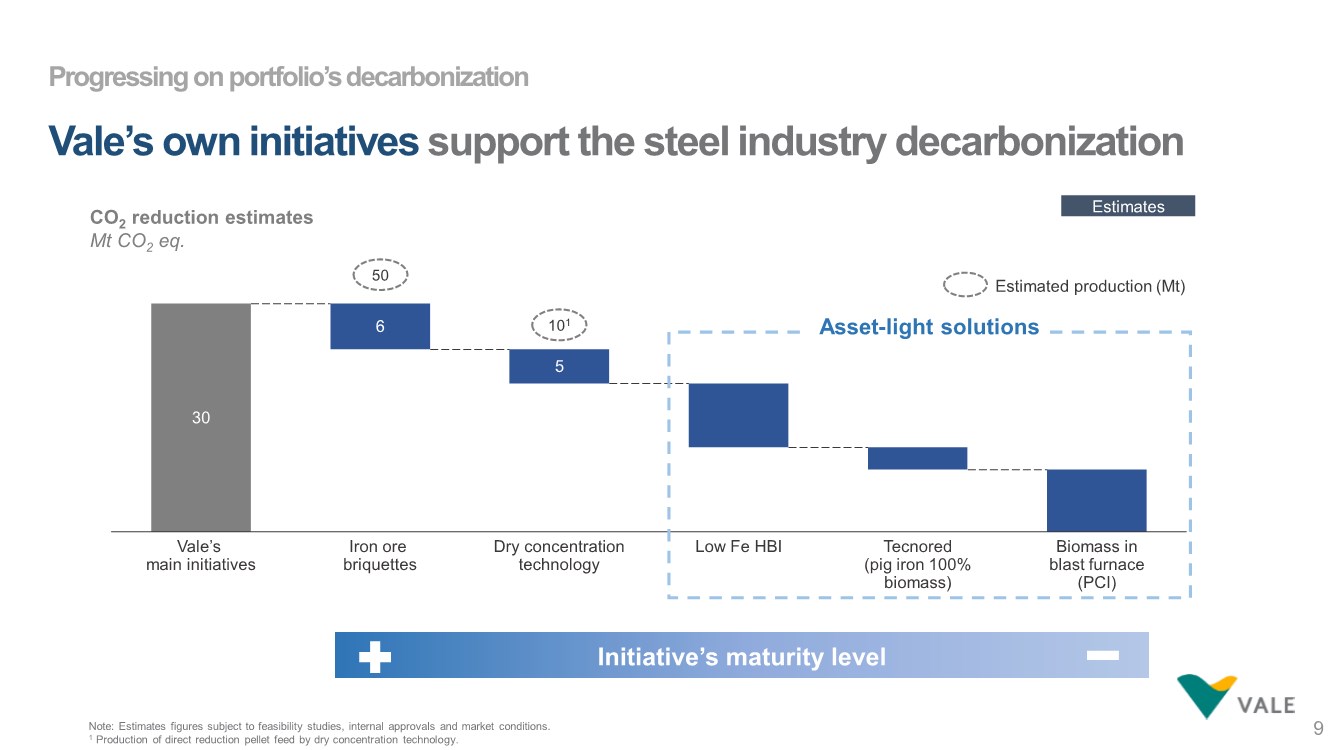

| Progressing on portfolio’s decarbonization Vale’s own initiatives support the steel industry decarbonization 9 30 6 5 Dry concentration technology Vale’s main initiatives Iron ore briquettes Low Fe HBI Tecnored (pig iron 100% biomass) Biomass in blast furnace (PCI) Asset-light solutions Initiative’s maturity level 50 101 Estimated production (Mt) Estimates CO2 reduction estimates Mt CO2 eq. Note: Estimates figures subject to feasibility studies, internal approvals and market conditions. 1 Production of direct reduction pellet feed by dry concentration technology. |

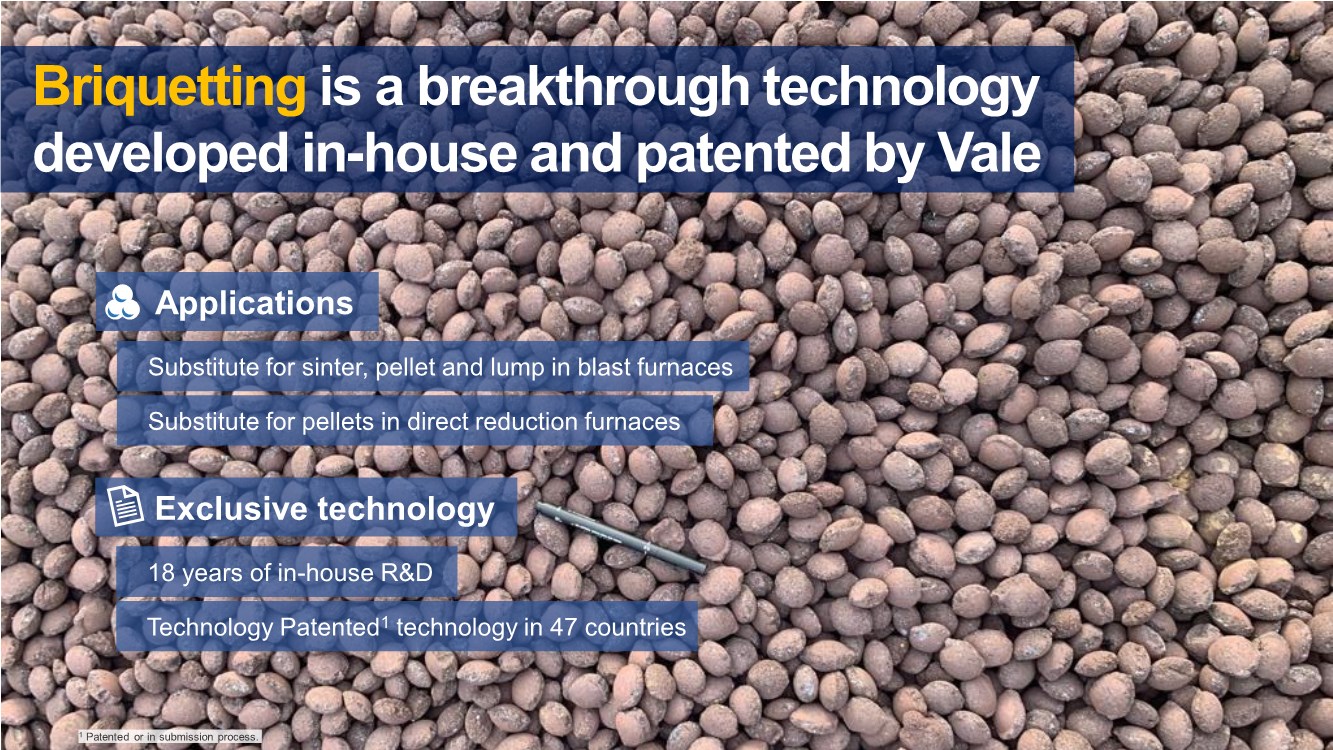

| Briquetting is a breakthrough technology developed in-house and patented by Vale 1 Patented or in submission process. Applications Substitute for sinter, pellet and lump in blast furnaces Substitute for pellets in direct reduction furnaces Exclusive technology 18 years of in-house R&D Technology Patented1 technology in 47 countries |

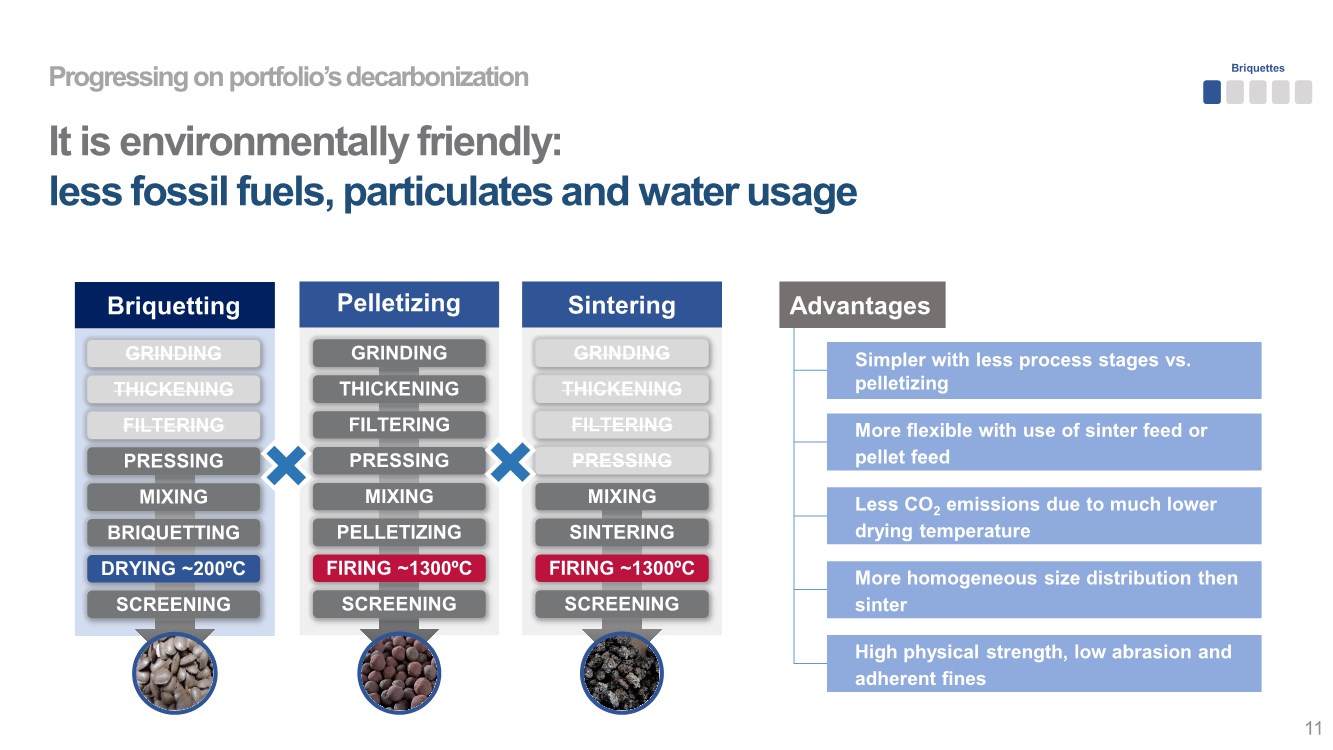

| Progressing on portfolio’s decarbonization It is environmentally friendly: less fossil fuels, particulates and water usage GRINDING THICKENING FILTERING PRESSING MIXING BRIQUETTING DRYING ~200ºC SCREENING Briquetting GRINDING THICKENING FILTERING PRESSING MIXING PELLETIZING FIRING ~1300ºC SCREENING Pelletizing GRINDING THICKENING FILTERING PRESSING MIXING SINTERING FIRING ~1300ºC SCREENING Sintering Briquettes 11 Simpler with less process stages vs. pelletizing More flexible with use of sinter feed or pellet feed Less CO2 emissions due to much lower drying temperature More homogeneous size distribution then sinter High physical strength, low abrasion and adherent fines Advantages |

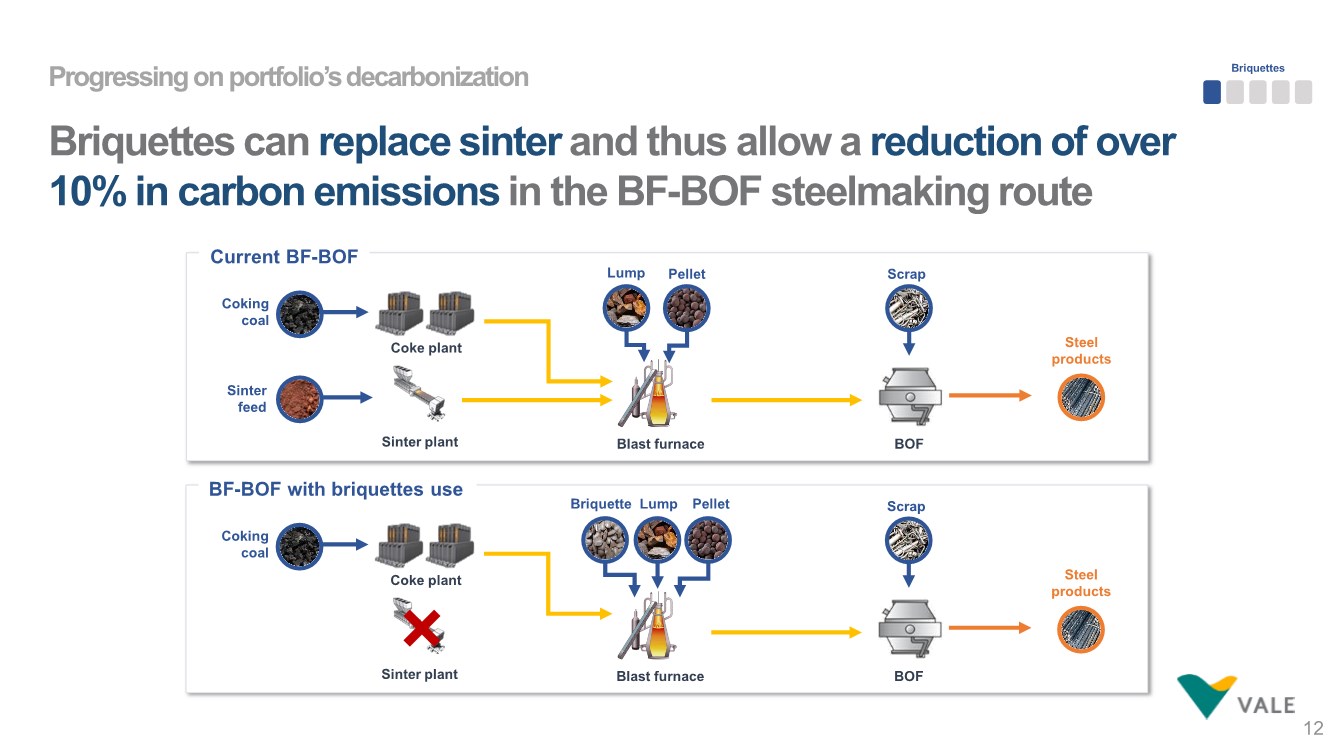

| Progressing on portfolio’s decarbonization Briquettes can replace sinter and thus allow a reduction of over 10% in carbon emissions in the BF-BOF steelmaking route 12 Briquettes Current BF-BOF BOF Scrap Coke plant Pellet Lump Sinter feed Coking coal Sinter plant Blast furnace Steel products BF-BOF with briquettes use BOF Scrap Coke plant Pellet Lump Coking coal Sinter plant Blast furnace Steel products Briquette |

| Vargem Grande Tubarão 1 & 2 Projects under development Progressing on portfolio’s decarbonization Three briquetting plants are already under construction 13 • 0.75 Mtpy capacity (expandable option to 1.5 Mtpy) • US$ 50 million investment • Start-up by 2023 • Synergies with adjacent dry concentration plant • Conversion of two idle pellet plants • 6 Mtpy capacity • US$ 135 million investment • Start-up by 2023 • Lower capex intensity than potential revamp of pellet plants • 5 other plants currently under analysis • Oman plant to produce direct reduction briquettes • MoU signed with Ternium Brasil to build a co-located plant • Other partnerships under analysis |

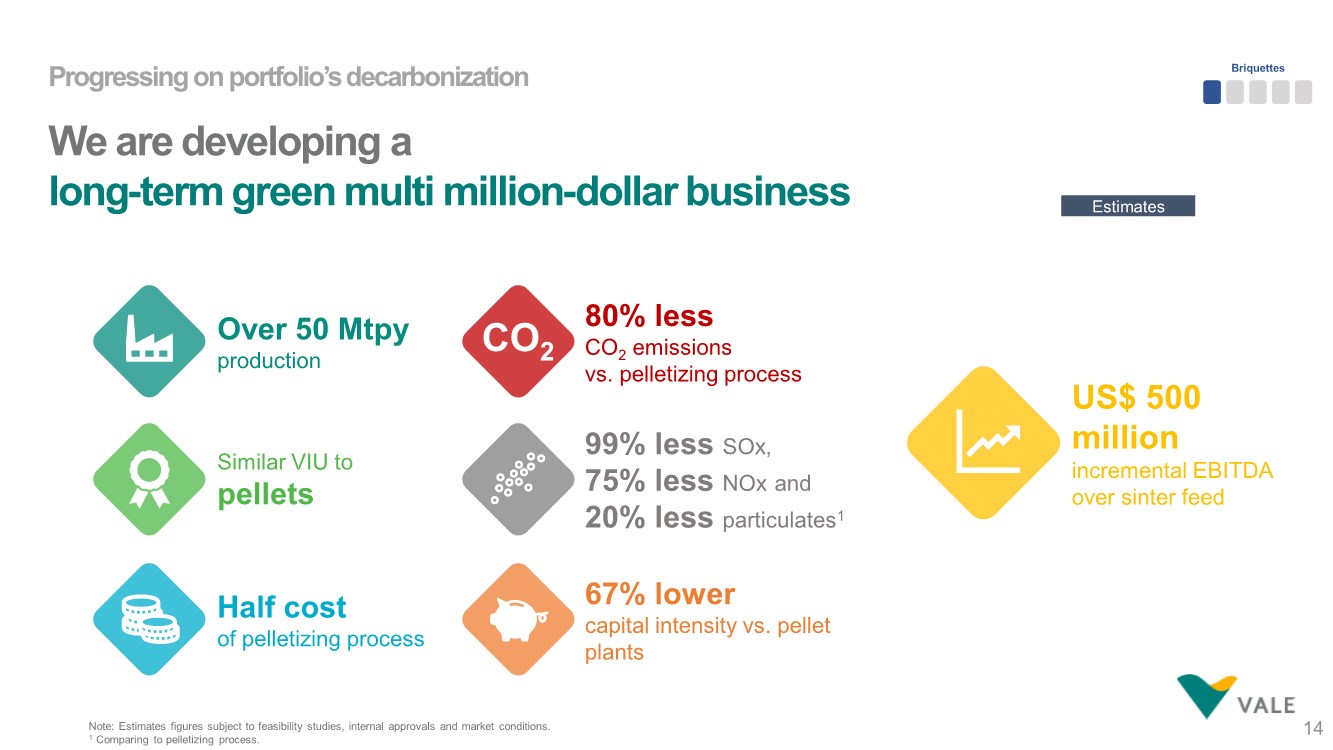

| Progressing on portfolio’s decarbonization We are developing a long-term green multi million-dollar business 14 Half cost of pelletizing process Similar VIU to pellets Over 50 Mtpy production US$ 500 million incremental EBITDA over sinter feed Briquettes 80% less CO2 emissions vs. pelletizing process 67% lower capital intensity vs. pellet plants CO2 Estimates Note: Estimates figures subject to feasibility studies, internal approvals and market conditions. 1 Comparing to pelletizing process. 99% less SOx, 75% less NOx and 20% less particulates1 |

| 15 No use of water = no tailings dam Final products with up to 68% Fe Dry concentration is a sustainable solution to produce high grade products Potentially integrated with other process routes Modular design |

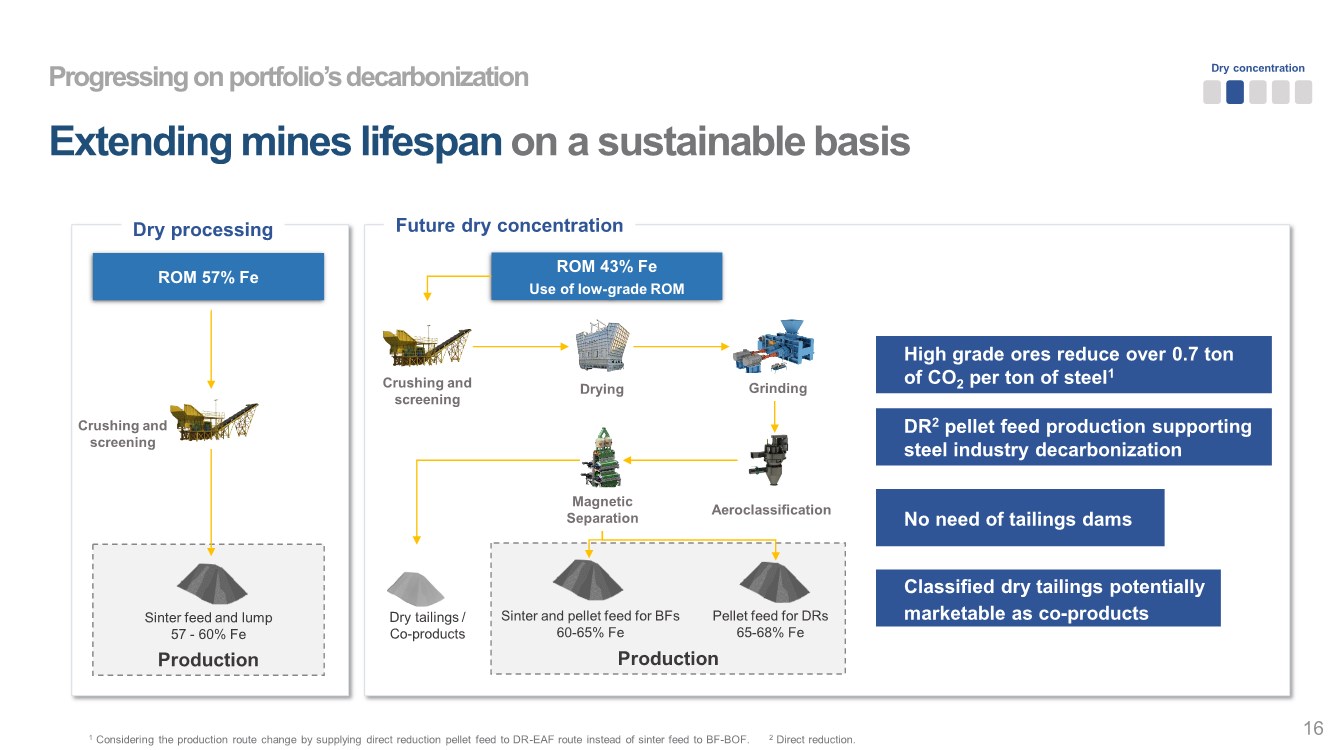

| Dry concentration Progressing on portfolio’s decarbonization Extending mines lifespan on a sustainable basis Production Dry processing Crushing and screening ROM 57% Fe Sinter feed and lump 57 - 60% Fe Future dry concentration ROM 43% Fe Use of low-grade ROM Crushing and screening Production Sinter and pellet feed for BFs 60-65% Fe Pellet feed for DRs 65-68% Fe Drying Aeroclassification Dry tailings / Co-products Grinding Magnetic Separation 16 DR2 pellet feed production supporting steel industry decarbonization No need of tailings dams Classified dry tailings potentially marketable as co-products 1 Considering the production route change by supplying direct reduction pellet feed to DR-EAF route instead of sinter feed to BF-BOF. 2 Direct reduction. High grade ores reduce over 0.7 ton of CO2 per ton of steel1 |

| Progressing on portfolio’s decarbonization First industrial plant under construction and more to come 17 Three new plants to be approved 6 Mtpy 2 Mtpy Vargem Grande plant under construction Fazendão (approval by 2023) Fábrica (approval by 2023) Start-up by 2023 with 1.5 Mtpy capacity US$ 125-150 million investment Concentration of 45% Fe ROM Dry concentration 8.5 Mtpy Oman (approval by 2022) |

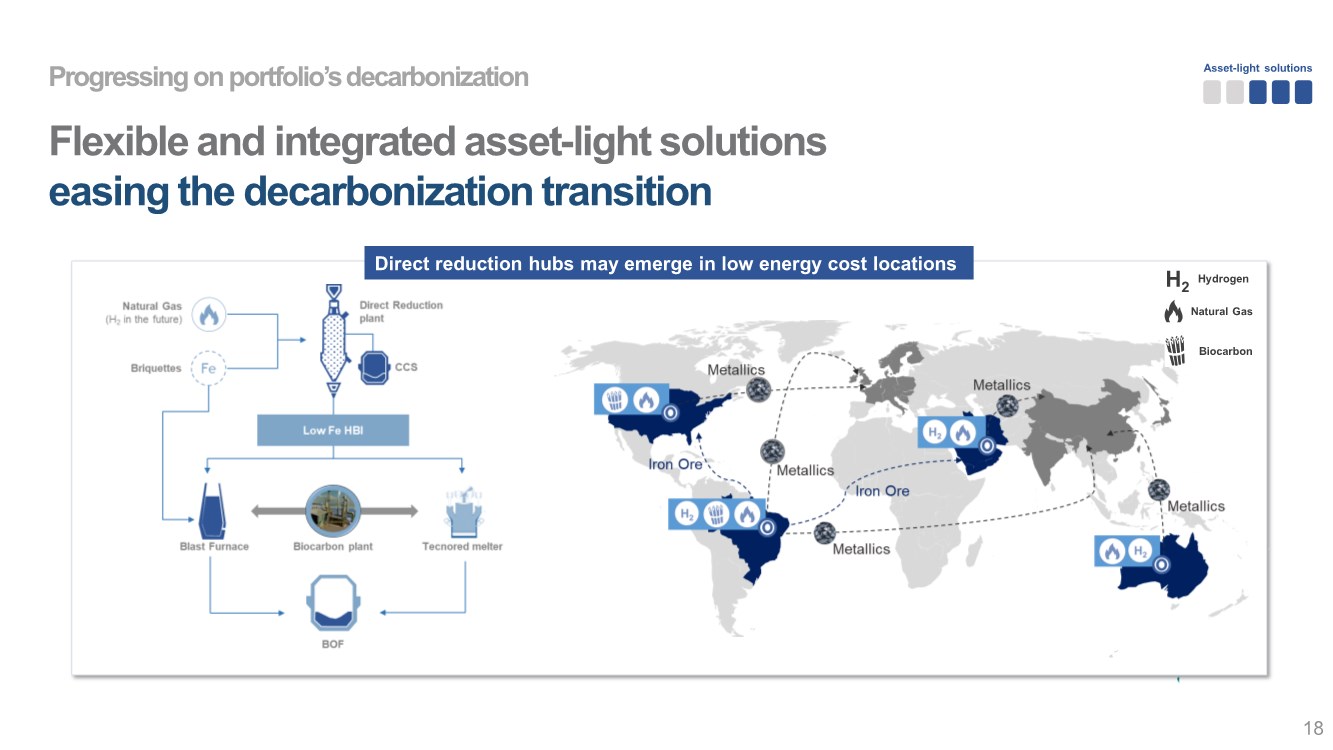

| Asset-light solutions Progressing on portfolio’s decarbonization Flexible and integrated asset-light solutions easing the decarbonization transition 18 Direct reduction hubs may emerge in low energy cost locations Hydrogen Natural Gas H2 Biocarbon |

| 19 Tecnored is a ready-to-use technology Technological uses “Green” low-cost pig iron production by potentially using biocarbon instead of coal Energy efficient and flexible carbon solution for melting scrap or low Fe HBI Plants underway Industrial scale plant in São Paulo Project in Pará under analysis Low-cost residue recycling |

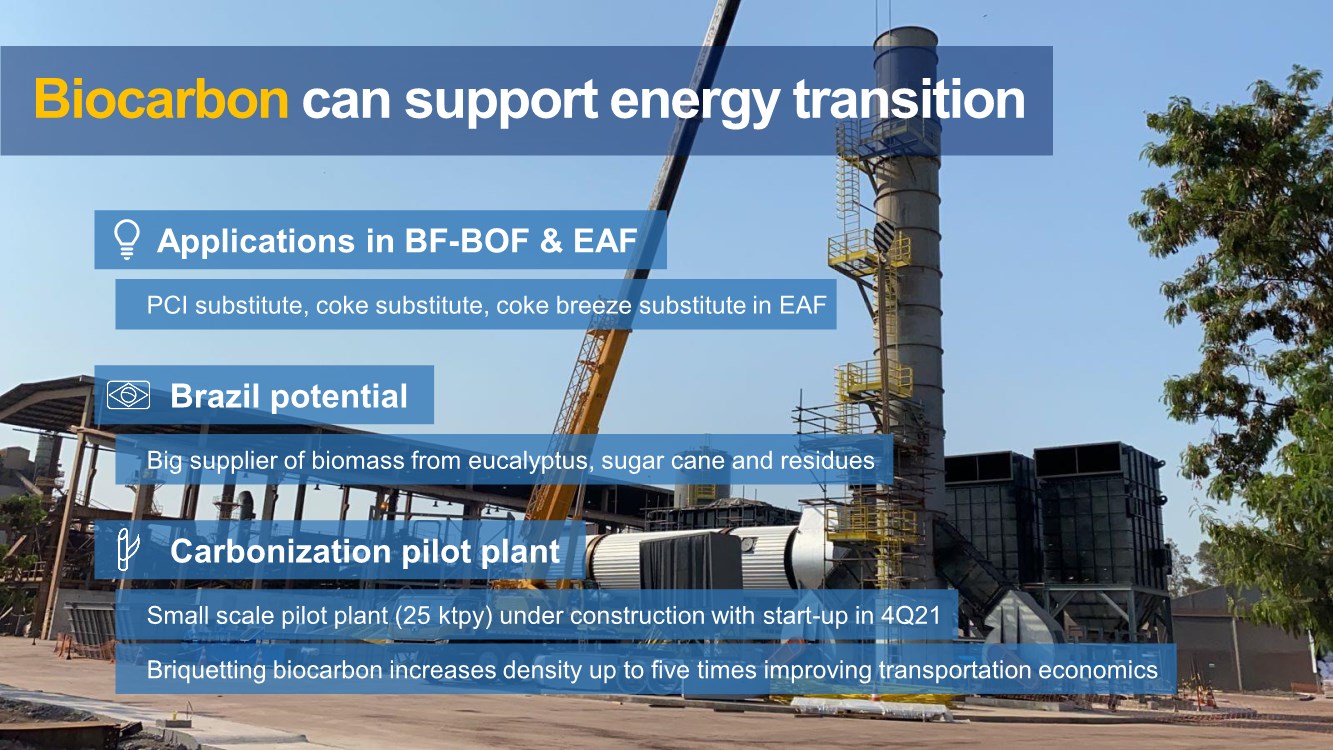

| Tecnored is a flex technology 20 Biocarbon can support energy transition Big supplier of biomass from eucalyptus, sugar cane and residues PCI substitute, coke substitute, coke breeze substitute in EAF Small scale pilot plant (25 ktpy) under construction with start-up in 4Q21 Briquetting biocarbon increases density up to five times improving transportation economics Brazil potential Carbonization pilot plant Applications in BF-BOF & EAF |

| Progressing on portfolio’s decarbonization Promoting technological advance in steel industry 21 Investment of US$ 6 million in Boston Metal Company to promote the development of Oxide Electrolysis (MOE) technology Fostering new technologies 13 years of R&D developing solutions for industry and customers Vale’s Ferrous Technology Center Capable to simulate steelmaking condition in laboratory |

| 22 We are also fostering innovative shipping solutions Valemaxes: largest vessels in industry Rotor sails: wind-assisted propulsion systems Air lubrication: reducing water resistance Click here to watch a video Click here to watch a video |

| September 9th, 2021 21st Analyst & Investor Tour Vagner Loyola |

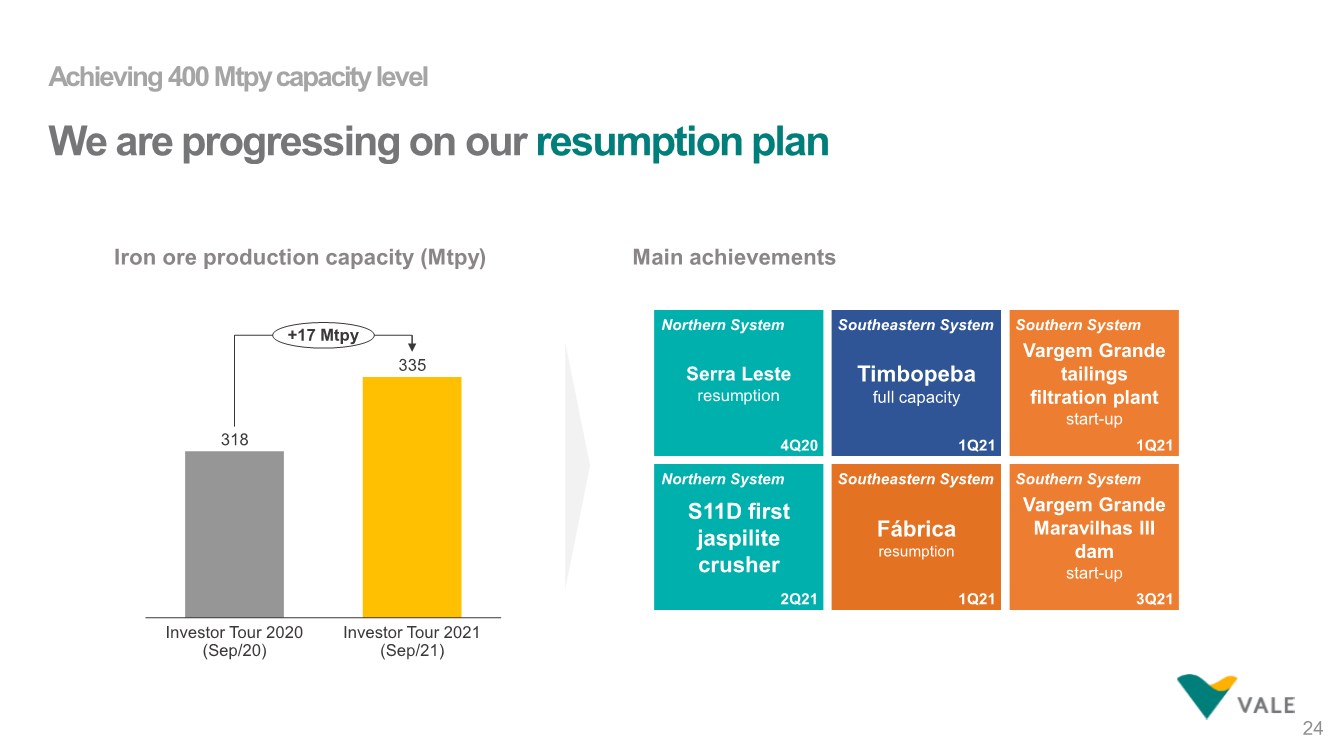

| Achieving 400 Mtpycapacity level We are progressing on our resumption plan 24 318 335 Investor Tour 2021 (Sep/21) Investor Tour 2020 (Sep/20) +17 Mtpy Iron ore production capacity (Mtpy) Main achievements Serra Leste resumption Northern System Timbopeba full capacity S11D first jaspilite crusher Fábrica resumption Vargem Grande tailings filtration plant start-up Vargem Grande Maravilhas III dam start-up 4Q20 Southern System Southern System Southeastern System Southeastern System Northern System 1Q21 1Q21 3Q21 2Q21 1Q21 |

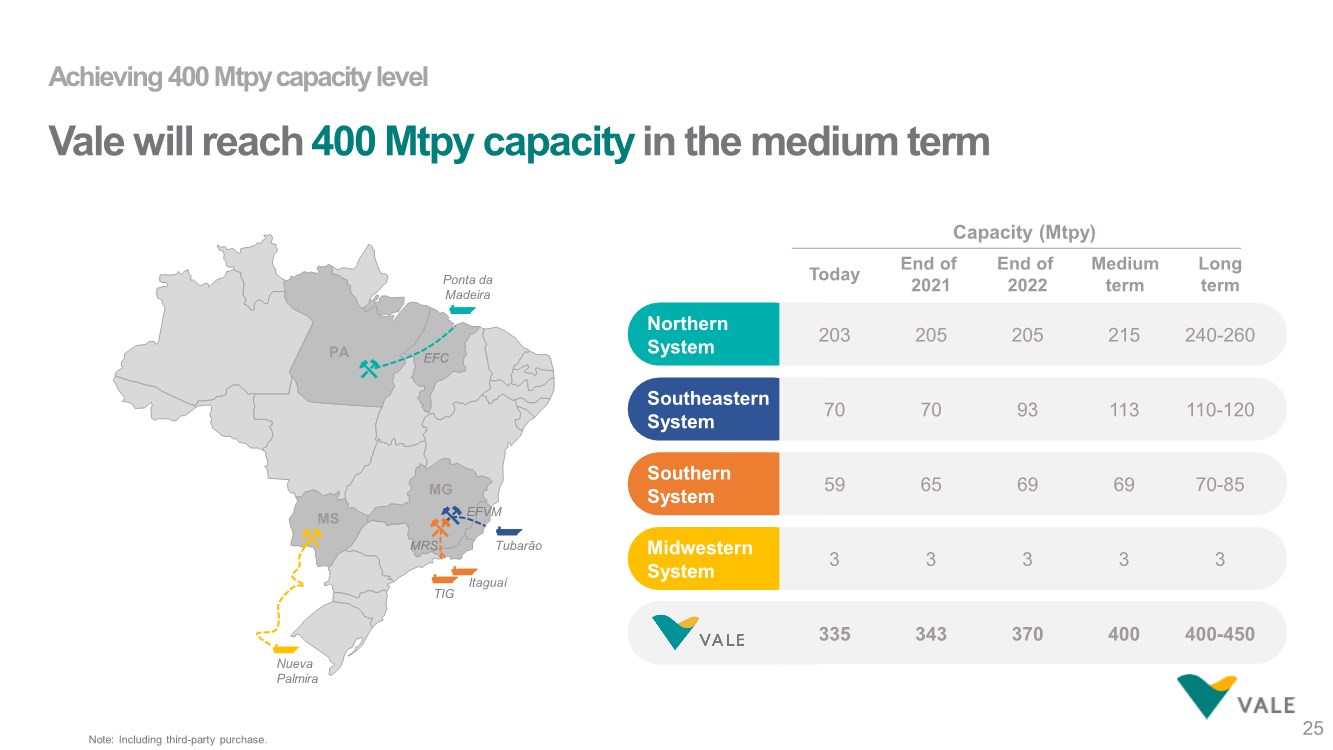

| Achieving 400 Mtpycapacity level Vale will reach 400 Mtpy capacity in the medium term 25 Capacity (Mtpy) Northern System Southeastern System Southern System Midwestern System 240-260 110-120 70-85 3 Long term 205 70 65 3 End of 2021 343 400-450 Medium term 215 113 69 3 400 Today 203 70 59 3 335 PA MG MS TIG Itaguaí Tubarão Ponta da Madeira EFC EFVM MRS Nueva Palmira 205 93 69 3 End of 2022 370 Note: Including third-party purchase. |

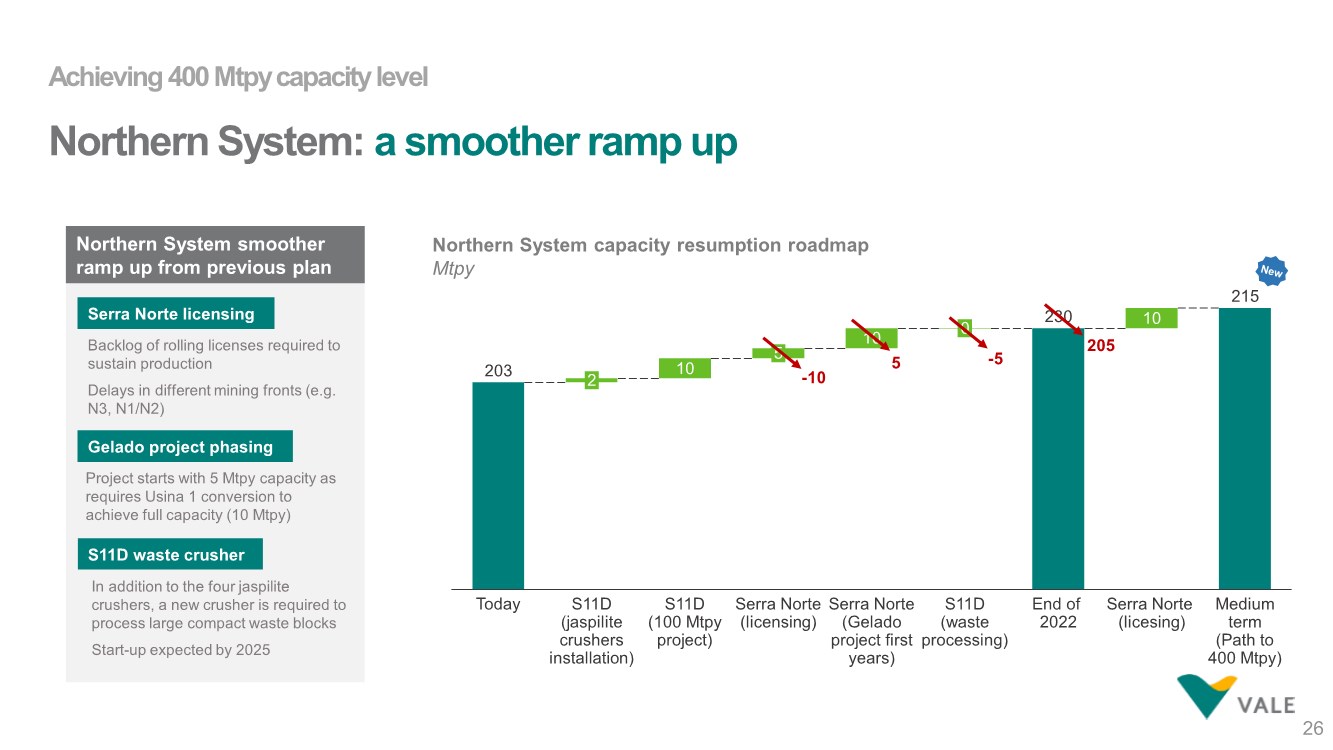

| Achieving 400 Mtpycapacity level Northern System: a smoother ramp up 26 Northern System capacity resumption roadmap Mtpy Serra Norte licensing Backlog of rolling licenses required to sustain production Delays in different mining fronts (e.g. N3, N1/N2) Gelado project phasing Project starts with 5 Mtpy capacity as requires Usina 1 conversion to achieve full capacity (10 Mtpy) S11D waste crusher In addition to the four jaspilite crushers, a new crusher is required to process large compact waste blocks Start-up expected by 2025 Northern System smoother ramp up from previous plan 203 230 10 10 S11D (jaspilite crushers installation) 2 Today S11D (100 Mtpy project) 5 Serra Norte (Gelado project first years) 10 Serra Norte (licensing) 0 S11D (waste processing) 215 End of 2022 Serra Norte (licesing) Medium term (Path to 400 Mtpy) -10 5 205 -5 |

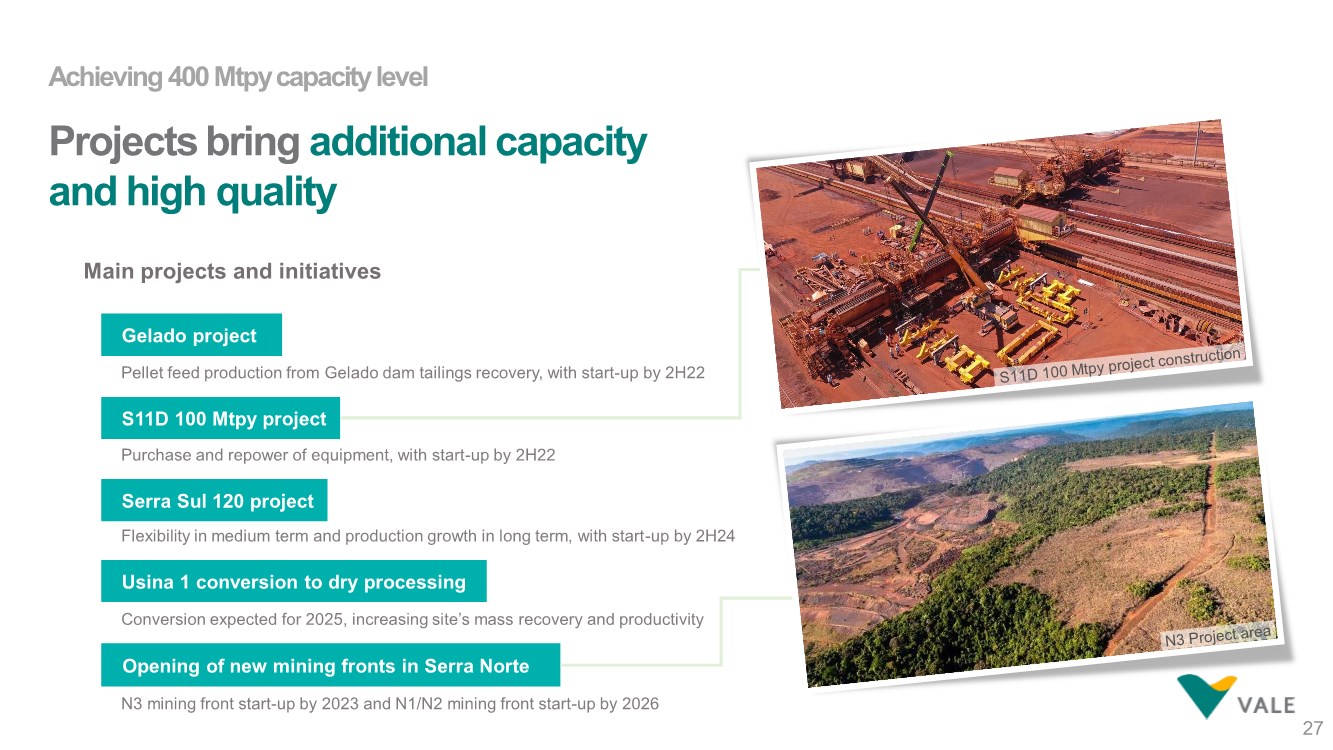

| Achieving 400 Mtpycapacity level Projects bring additional capacity and high quality 27 Main projects and initiatives Conversion expected for 2025, increasing site’s mass recovery and productivity Usina 1 conversion to dry processing Opening of new mining fronts in Serra Norte N3 mining front start-up by 2023 and N1/N2 mining front start-up by 2026 Serra Sul 120 project Flexibility in medium term and production growth in long term, with start-up by 2H24 Gelado project Pellet feed production from Gelado dam tailings recovery, with start-up by 2H22 S11D 100 Mtpy project Purchase and repower of equipment, with start-up by 2H22 |

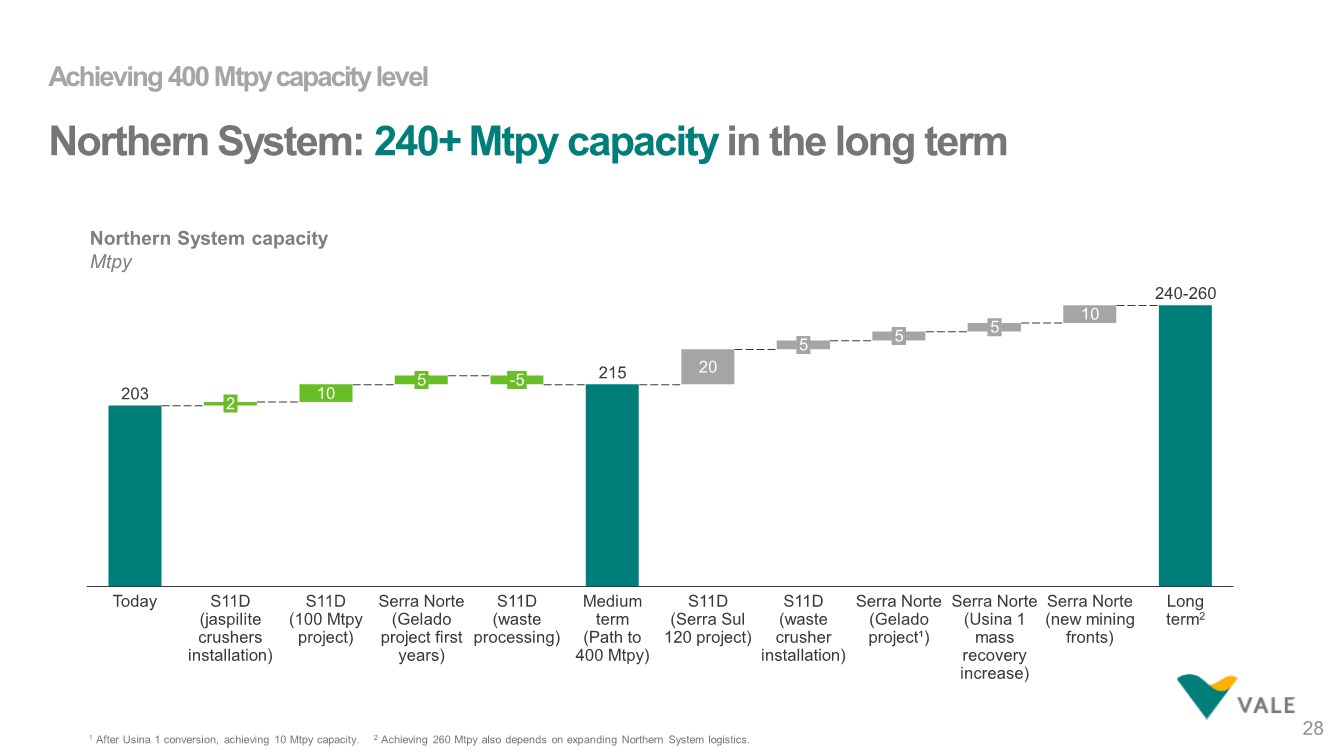

| 203 215 10 20 10 Today S11D (waste processing) S11D (100 Mtpy project) 5 2 S11D (jaspilite crushers installation) Serra Norte (Gelado project first years) -5 Medium term (Path to 400 Mtpy) S11D (Serra Sul 120 project) 5 S11D (waste crusher installation) 5 Serra Norte (Gelado project¹) 5 Serra Norte (Usina 1 mass recovery increase) Serra Norte (new mining fronts) Long term2 240-260 Achieving 400 Mtpycapacity level Northern System: 240+ Mtpy capacityin the long term 28 Northern System capacity Mtpy 1 After Usina 1 conversion, achieving 10 Mtpy capacity. 2 Achieving 260 Mtpy also depends on expanding Northern System logistics. |

| Achieving 400 Mtpycapacity level In Southeastern System, new assets are solving tailings disposal restrictions in Brucutu… 29 Main projects and initiatives Start-up by 2H22 Works to increase safety factor started in August Tailings filtration plant construction Torto dam start-up 76% of physical progress Start-up by end of 2021 Tailings piles areas Licensing and preparation of areas to receive dry tailings from filtration plants Atualizar foto |

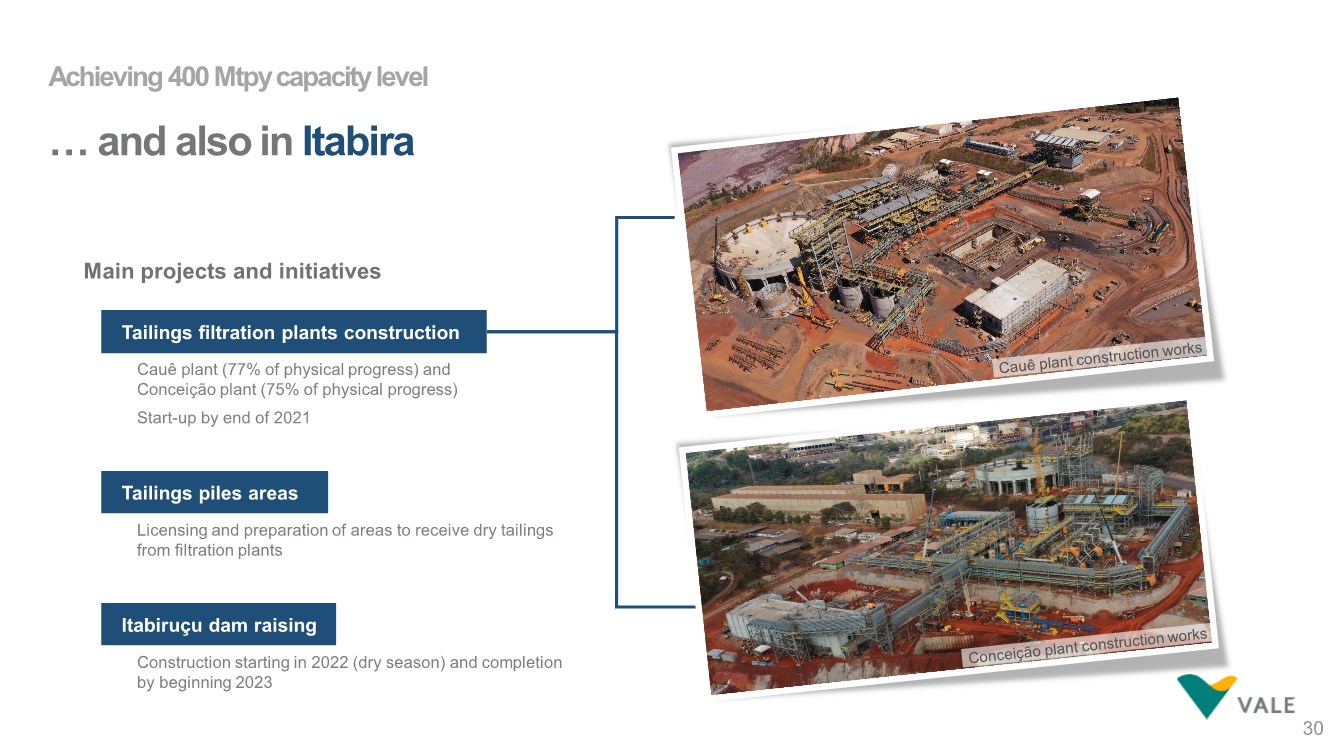

| Main projects and initiatives Achieving 400 Mtpycapacity level … and also in Itabira 30 Construction starting in 2022 (dry season) and completion by beginning 2023 Tailings filtration plants construction Itabiruçu dam raising Cauê plant (77% of physical progress) and Conceição plant (75% of physical progress) Start-up by end of 2021 Tailings piles areas Licensing and preparation of areas to receive dry tailings from filtration plants |

| Achieving 400 Mtpycapacity level Capanema project increases Mariana complex capacity and optimize Timbopeba’s operations 31 Use of Timbopeba assets reducing investments 18 Mtpy capacity1 by natural moisture (without tailings generation) Start-up in 2H23 Production of sinter feed for BRBF 1 Net addition capacity of 14 Mtpy in the first years. |

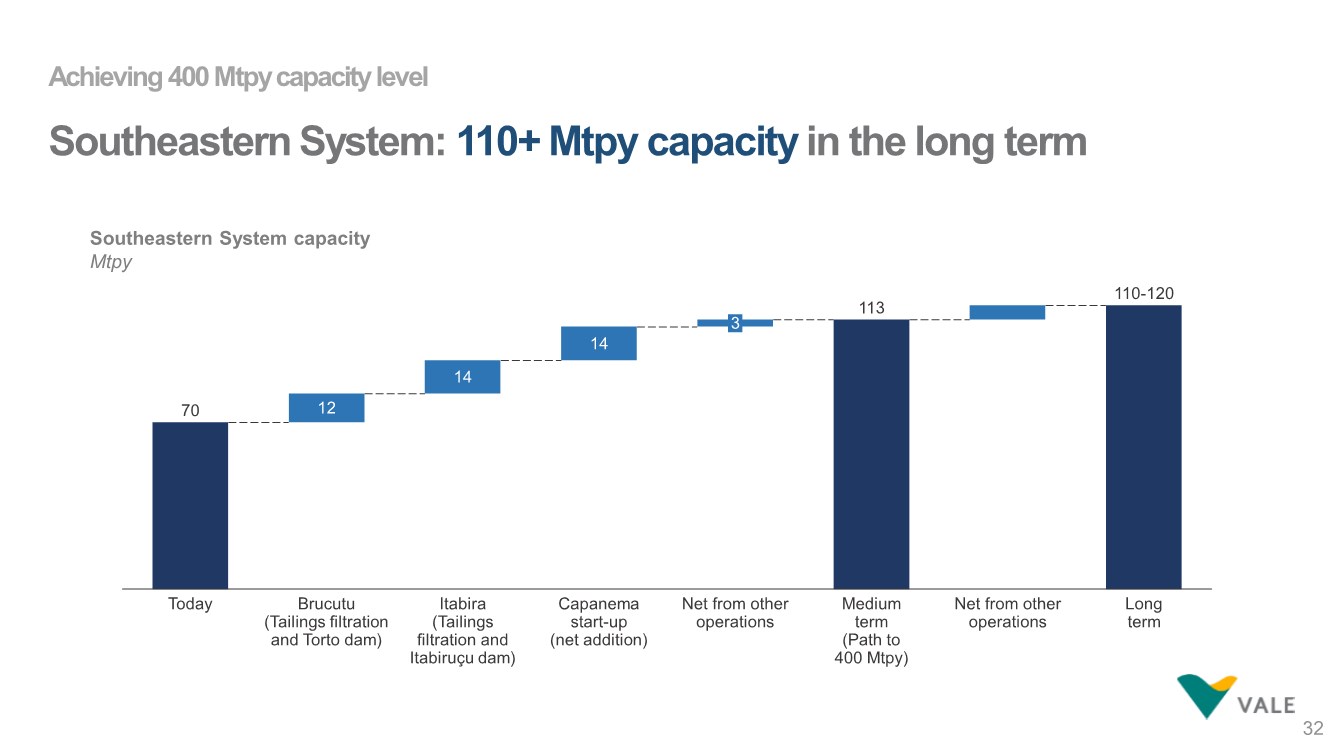

| 70 113 12 14 14 Today Medium term (Path to 400 Mtpy) Brucutu (Tailings filtration and Torto dam) Itabira (Tailings filtration and Itabiruçu dam) Capanema start-up (net addition) 3 Net from other operations Net from other operations Long term 110-120 Achieving 400 Mtpycapacity level Southeastern System: 110+ Mtpy capacity in the long term 32 Southeastern System capacity Mtpy |

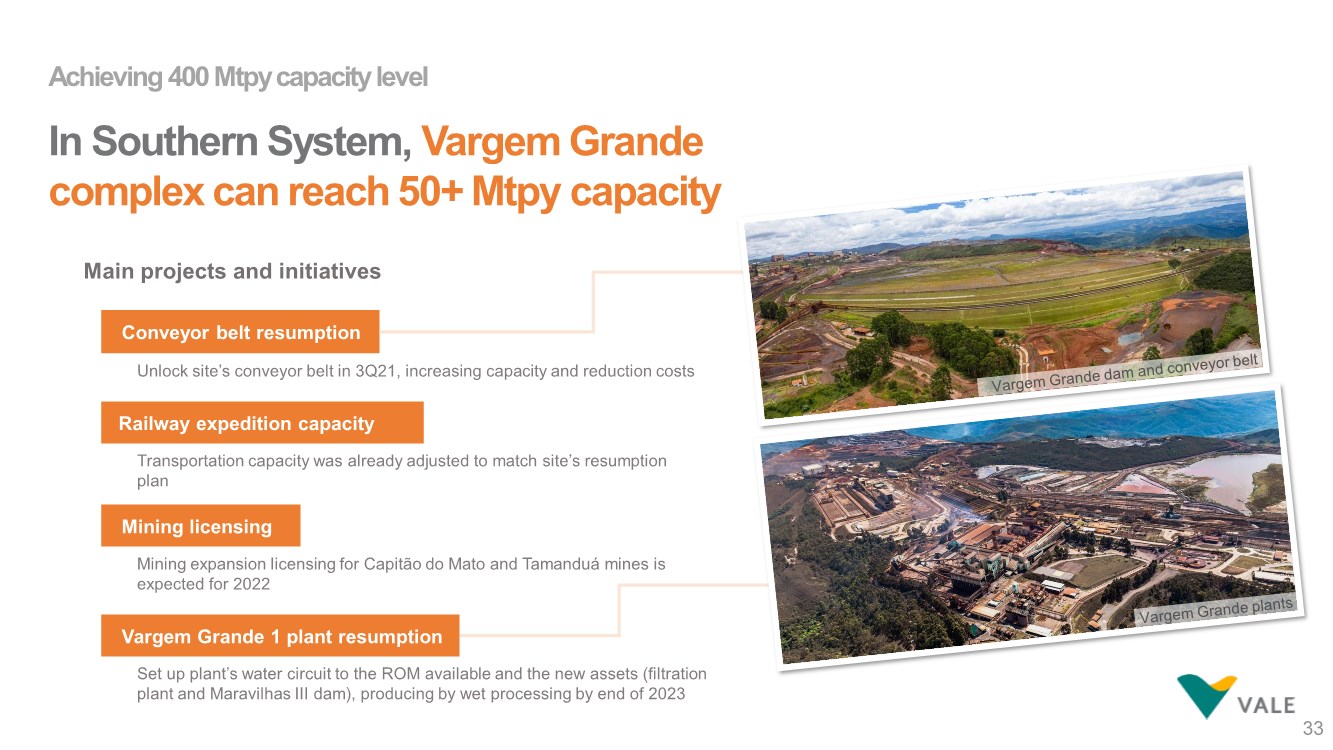

| Achieving 400 Mtpycapacity level In Southern System, Vargem Grande complex can reach 50+ Mtpy capacity 33 Main projects and initiatives Conveyor belt resumption Mining licensing Unlock site’s conveyor belt in 3Q21, increasing capacity and reduction costs Mining expansion licensing for Capitão do Mato and Tamanduá mines is expected for 2022 Vargem Grande 1 plant resumption Set up plant’s water circuit to the ROM available and the new assets (filtration plant and Maravilhas III dam), producing by wet processing by end of 2023 Railway expedition capacity Transportation capacity was already adjusted to match site’s resumption plan |

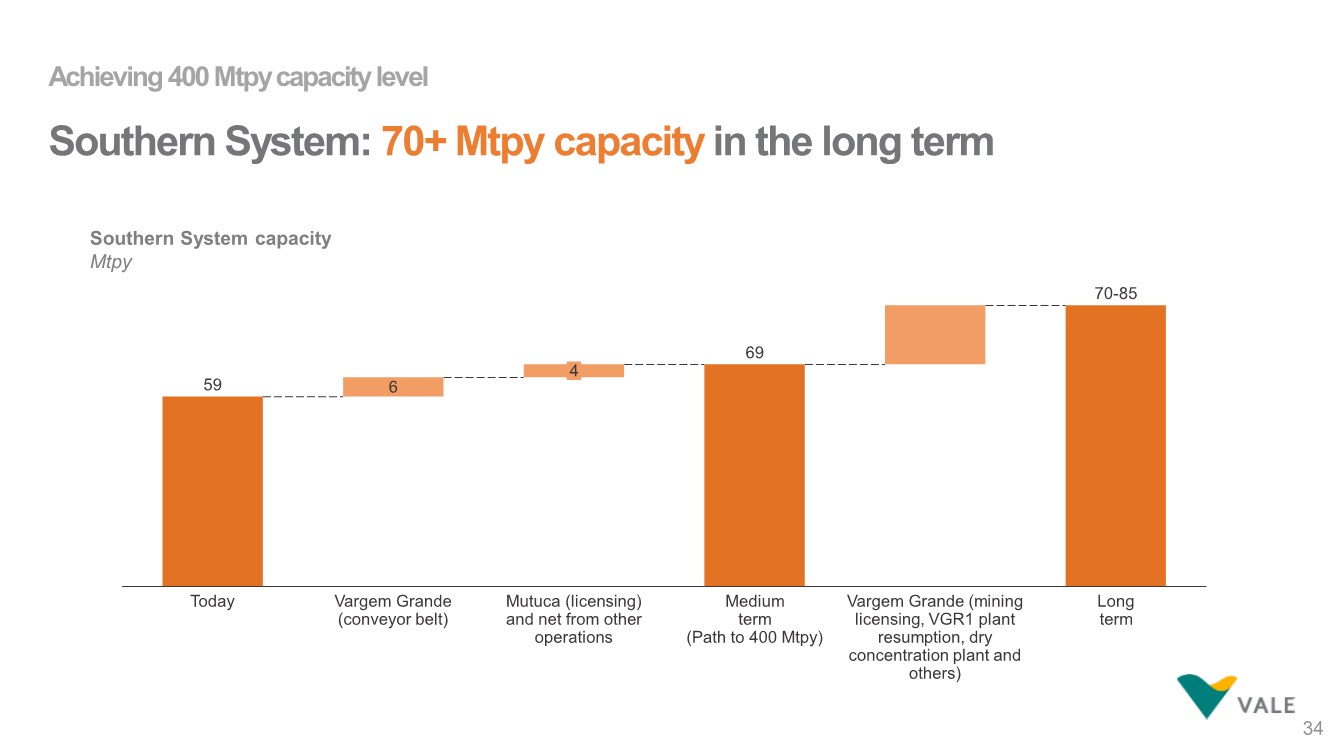

| 59 69 6 Vargem Grande (mining licensing, VGR1 plant resumption, dry concentration plant and others) 4 Today Mutuca (licensing) and net from other operations Vargem Grande (conveyor belt) Medium term (Path to 400 Mtpy) Long term 70-85 Achieving 400 Mtpycapacity level Southern System: 70+ Mtpy capacity in the long term 34 Southern System capacity Mtpy |

| 35 Leading industry decarbonizing transformation Delivering resumption plan Improving safety and reducing risks We are strengthening iron ore business sustainability |

| September 9th, 2021 21st Analyst & Investor Tour Luciano Siani Pires |

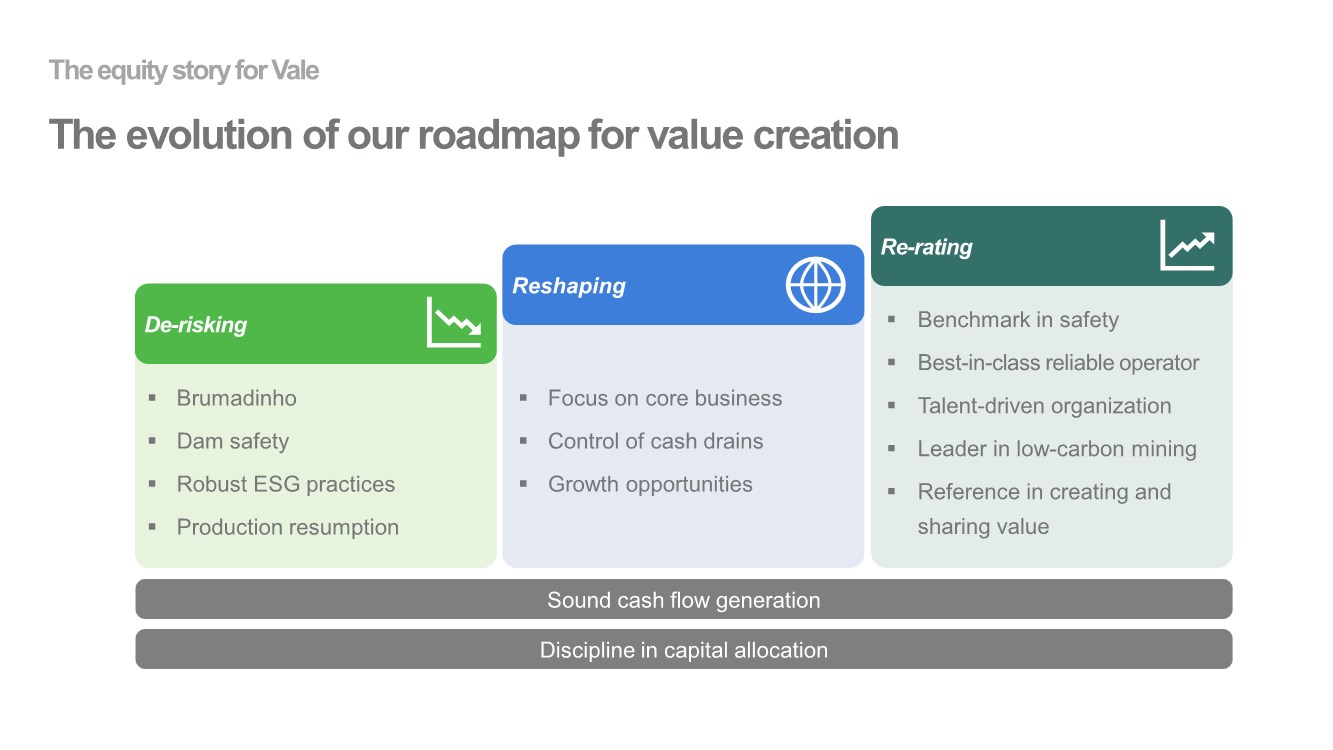

| Re-rating ▪ Benchmark in safety ▪ Best-in-class reliable operator ▪ Talent-driven organization ▪ Leader in low-carbon mining ▪ Reference in creating and sharing value De-risking ▪ Brumadinho ▪ Dam safety ▪ Robust ESG practices ▪ Production resumption Reshaping ▪ Focus on core business ▪ Control of cash drains ▪ Growth opportunities Sound cash flow generation Discipline in capital allocation The equity story for Vale The evolution of our roadmap for value creation |

| Commitment to fully revegetate the entire affected area 2025 The equity story for Vale We have made solid progress in repairing Brumadinho + R$ 2.8 billion in signed agreements for individual indemnification¹ A robust legal framework ¹ Related to agreements entered into as of August 31st, 2021, approximate figures and including amounts already disbursed. Hydraulic barrier that prevents sediment flow at Brumadinho (MG) Projects for Brumadinho and other municipalities Recover the environment Projects demanded by affected communities Ensure water supply Resources to Urban Mobility Program and Public Service Strengthening Program Income transfer program |

| Ground Zero project for environmental recovery Ferro Carvão water stream, Brumadinho (MG) Picture from January/21 |

| Commissioning of the new water supply system Paraopeba River (MG) Picture from July/21 |

| New basic healthcare unit Parque da Cachoeira, Brumadinho (MG) Picture from February/21 |

| Decharacterization of 8B dam Nova Lima, MG, Brazil The equity story for Vale We have advanced in dam management Picture from January/20 |

| Decharacterization of Dique Rio do Peixe Itabira, MG, Brazil The equity story for Vale We have advanced in dam management Picture from July/21 |

| Decharacterization of Fernadinho dam Vargem Grande Complex, MG, Brazil The equity story for Vale We have advanced in dam management Picture from July/21 |

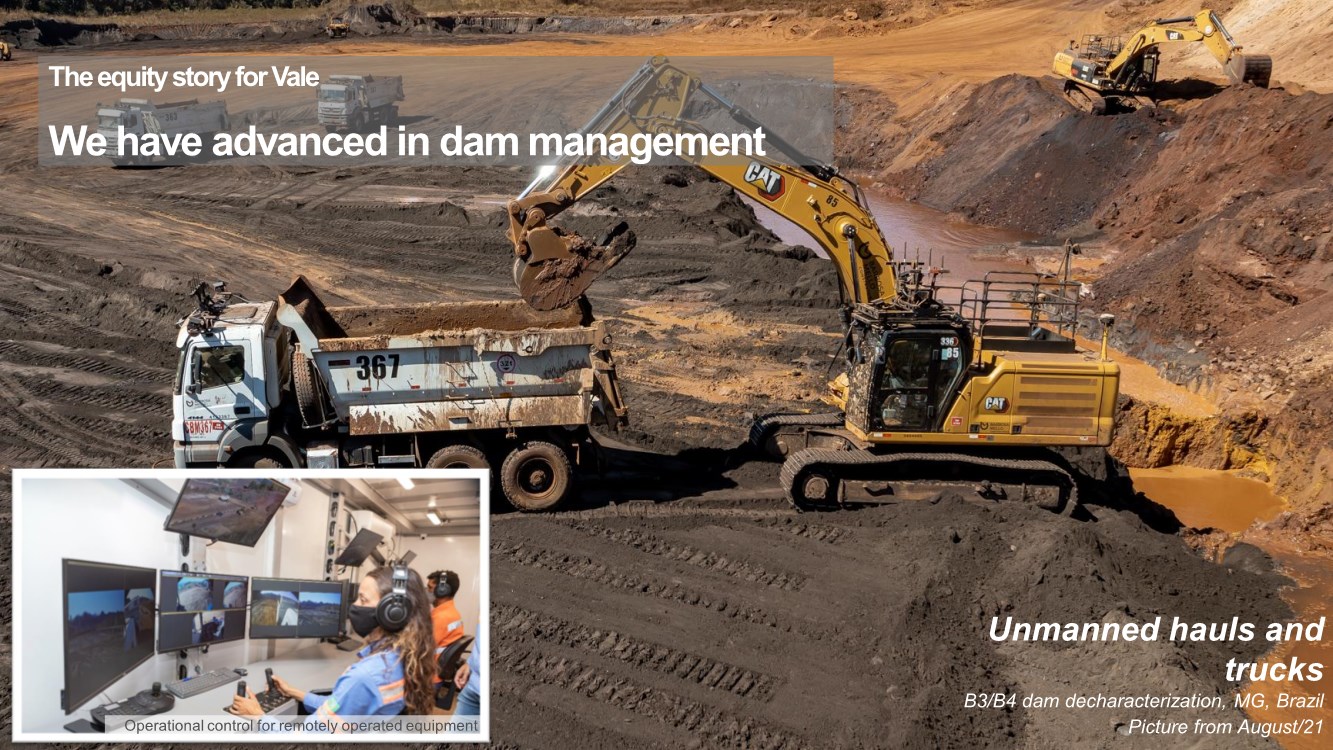

| Unmanned hauls and trucks B3/B4 dam decharacterization, MG, Brazil Operational control for remotely operated equipment The equity story for Vale We have advanced in dam management Picture from August/21 |

| B3/B4 back-up dam Nova Lima, MG, Brazil The equity story for Vale We have advanced in dam management Picture from March/21 |

| Sul Superior back-up dam Barão de Cocais, MG, Brazil The equity story for Vale We have advanced in dam management Picture from December/20 |

| Forquilhas and Grupo back-up dam Ouro Preto and Itabirito, MG, Brazil The equity story for Vale We have advanced in dam management Picture from July/21 |

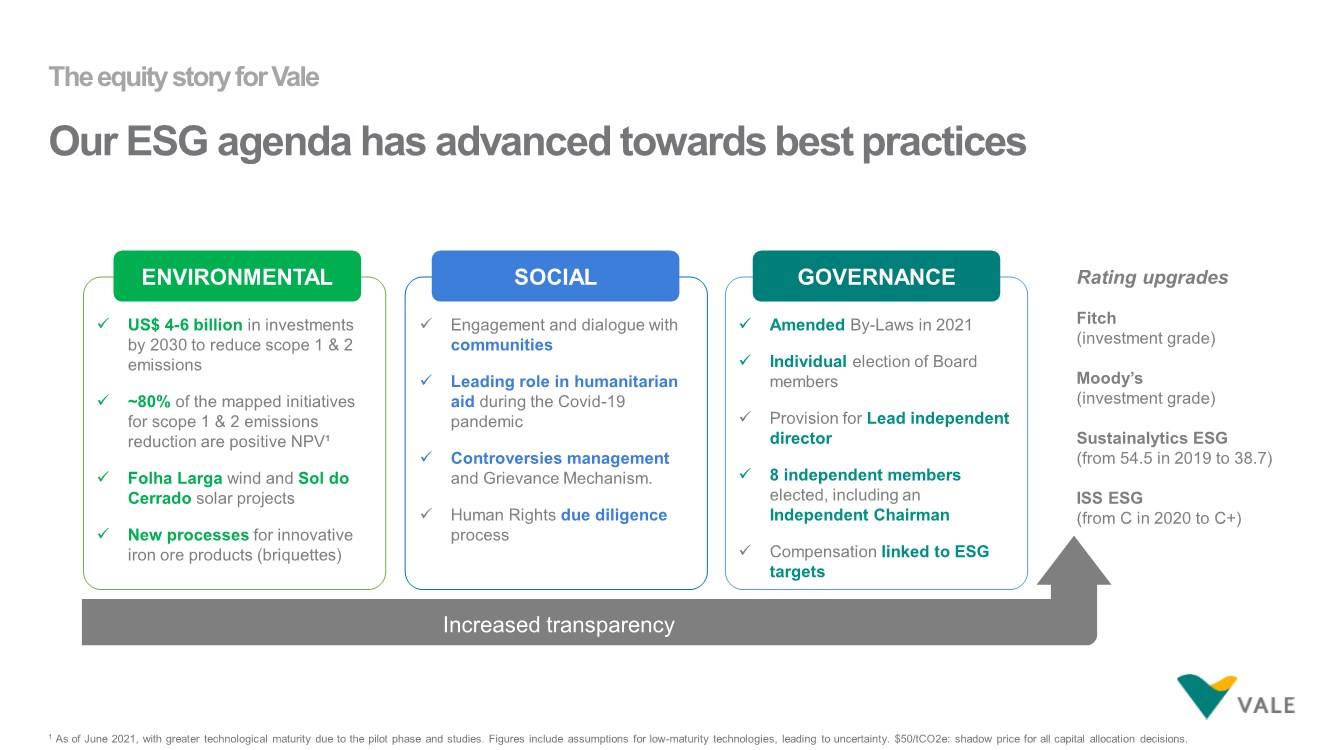

| The equity story for Vale Our ESG agenda has advanced towards best practices SOCIAL ENVIRONMENTAL Fitch (investment grade) Moody’s (investment grade) Sustainalytics ESG (from 54.5 in 2019 to 38.7) ISS ESG (from C in 2020 to C+) GOVERNANCE ✓ US$ 4-6 billion in investments by 2030 to reduce scope 1 & 2 emissions ✓ ~80% of the mapped initiatives for scope 1 & 2 emissions reduction are positive NPV¹ ✓ Folha Larga wind and Sol do Cerrado solar projects ✓ New processes for innovative iron ore products (briquettes) ✓ Engagement and dialogue with communities ✓ Leading role in humanitarian aid during the Covid-19 pandemic ✓ Controversies management and Grievance Mechanism. ✓ Human Rights due diligence process ✓ Amended By-Laws in 2021 ✓ Individual election of Board members ✓ Provision for Lead independent director ✓ 8 independent members elected, including an Independent Chairman ✓ Compensation linked to ESG targets Increased transparency Rating upgrades 1 As of June 2021, with greater technological maturity due to the pilot phase and studies. Figures include assumptions for low-maturity technologies, leading to uncertainty. $50/tCO2e: shadow price for all capital allocation decisions. |

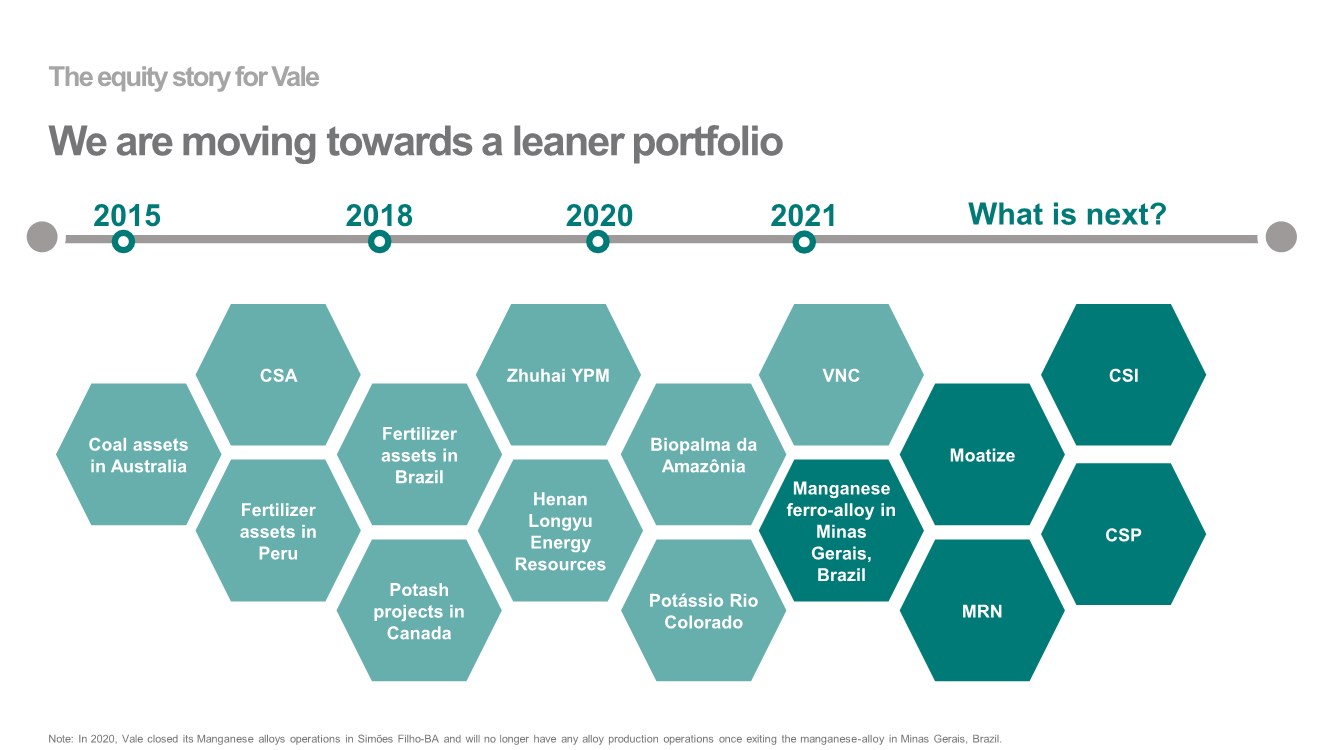

| CSA Fertilizer assets in Brazil Potash projects in Canada Coal assets in Australia Zhuhai YPM Moatize CSP MRN Manganese ferro-alloy in Minas Gerais, Brazil Henan Longyu Energy Resources VNC Biopalma da Amazônia Fertilizer assets in Peru Potássio Rio Colorado 2015 2021 2018 2020 The equity story for Vale We are moving towards a leaner portfolio CSI What is next? Note: In 2020, Vale closed its Manganese alloys operations in Simões Filho-BA and will no longer have any alloy production operations once exiting the manganese-alloy in Minas Gerais, Brazil. |

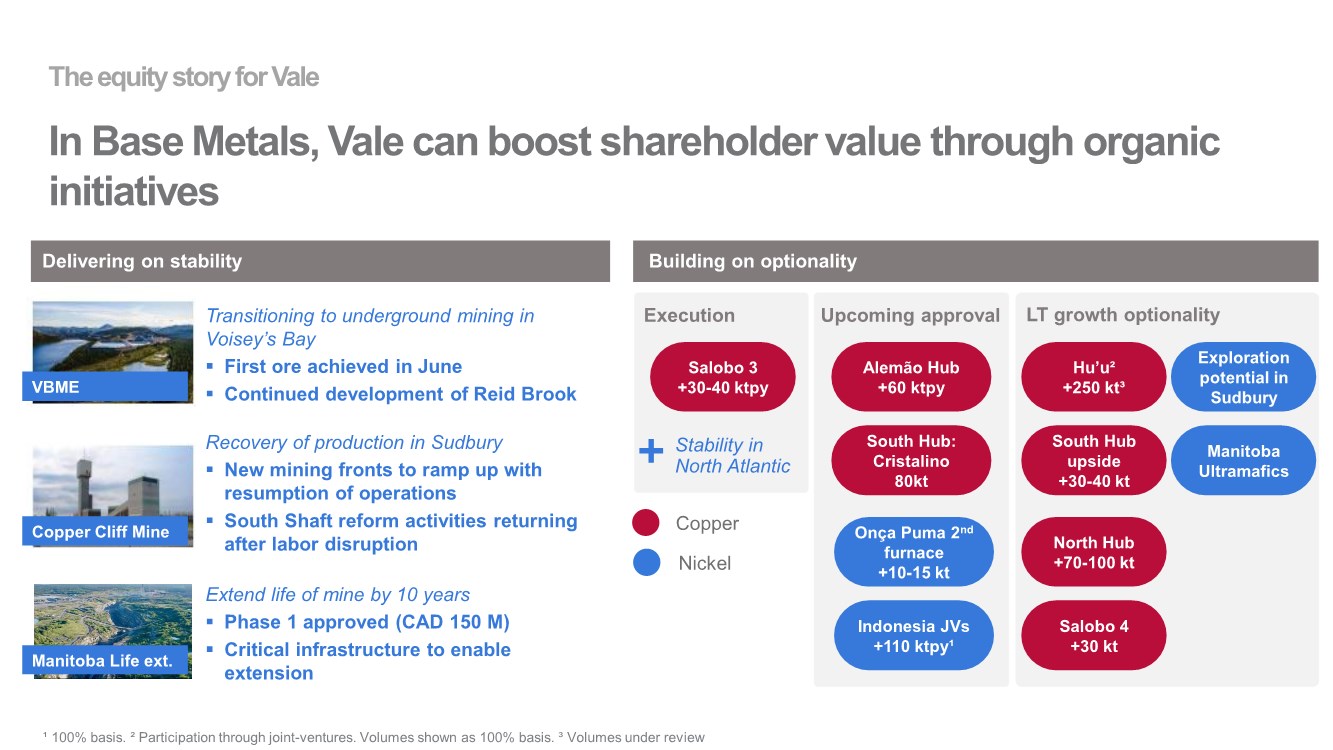

| The equity story for Vale In Base Metals, Vale can boost shareholder value through organic initiatives Upcoming approval LT growth optionality Copper Nickel Hu’u² +250 kt³ Alemão Hub +60 ktpy South Hub: Cristalino 80kt Onça Puma 2nd furnace +10-15 kt Manitoba Ultramafics South Hub upside +30-40 kt Exploration potential in Sudbury North Hub +70-100 kt Salobo 4 +30 kt Indonesia JVs +110 ktpy¹ Building on optionality Delivering on stability Transitioning to underground mining in Voisey’s Bay ▪ First ore achieved in June ▪ Continued development of Reid Brook Recovery of production in Sudbury ▪ New mining fronts to ramp up with resumption of operations ▪ South Shaft reform activities returning after labor disruption Execution Salobo 3 +30-40 ktpy Extend life of mine by 10 years ▪ Phase 1 approved (CAD 150 M) ▪ Critical infrastructure to enable extension Stability in North Atlantic Manitoba Life ext. Copper Cliff Mine VBME ¹ 100% basis. ² Participation through joint-ventures. Volumes shown as 100% basis. ³ Volumes under review |

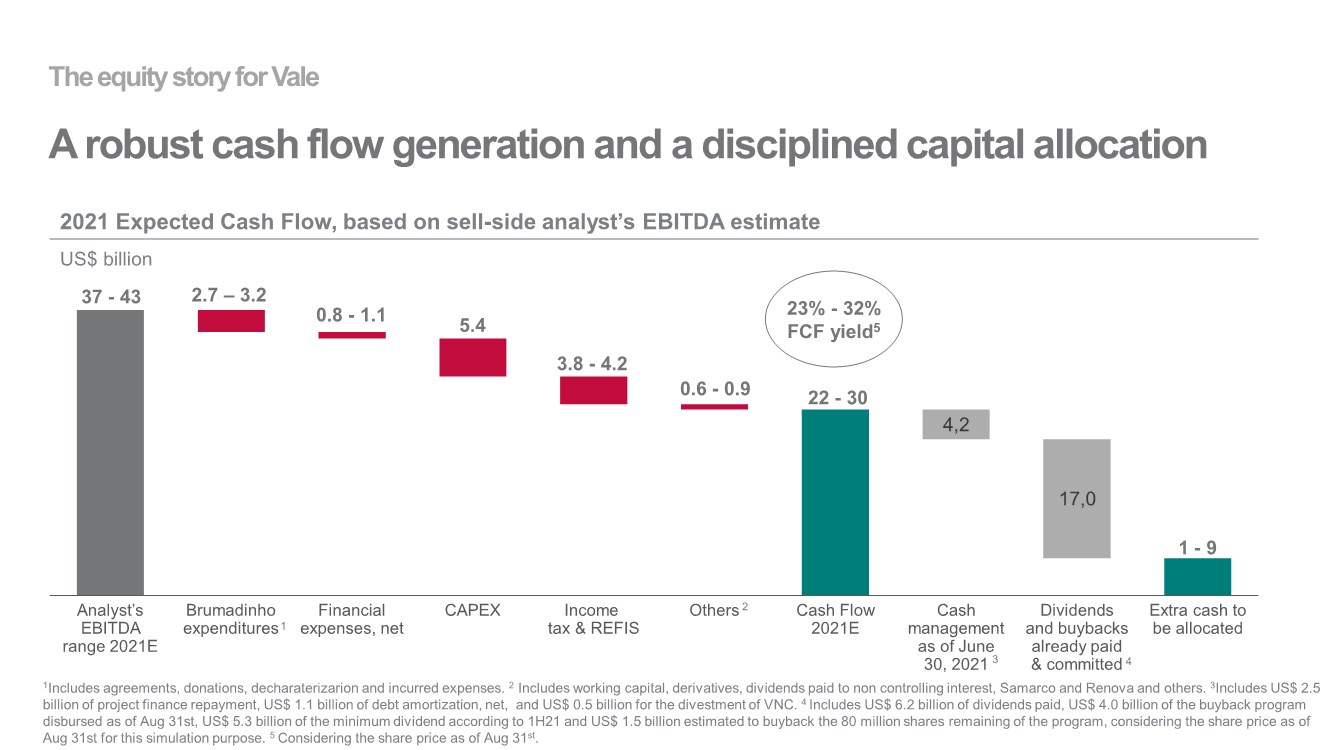

| 4,2 17,0 CAPEX Cash management as of June 30, 2021 Income tax & REFIS Analyst’s EBITDA range 2021E Financial expenses, net Brumadinho expenditures Others Cash Flow 2021E Dividends and buybacks already paid & committed Extra cash to be allocated 2021 Expected Cash Flow, based on sell-side analyst’s EBITDA estimate US$ billion The equity story for Vale A robust cash flow generation and a disciplined capital allocation 1Includes agreements, donations, decharaterizarion and incurred expenses. 2 Includes working capital, derivatives, dividends paid to non controlling interest, Samarco and Renova and others. 3Includes US$ 2.5 billion of project finance repayment, US$ 1.1 billion of debt amortization, net, and US$ 0.5 billion for the divestment of VNC. 4 Includes US$ 6.2 billion of dividends paid, US$ 4.0 billion of the buyback program disbursed as of Aug 31st, US$ 5.3 billion of the minimum dividend according to 1H21 and US$ 1.5 billion estimated to buyback the 80 million shares remaining of the program, considering the share price as of Aug 31st for this simulation purpose. 5 Considering the share price as of Aug 31st. 23% - 32% FCF yield5 0.8 - 1.1 5.4 3.8 - 4.2 0.6 - 0.9 22 - 30 1 - 9 37 - 43 2.7 – 3.2 1 2 3 4 |

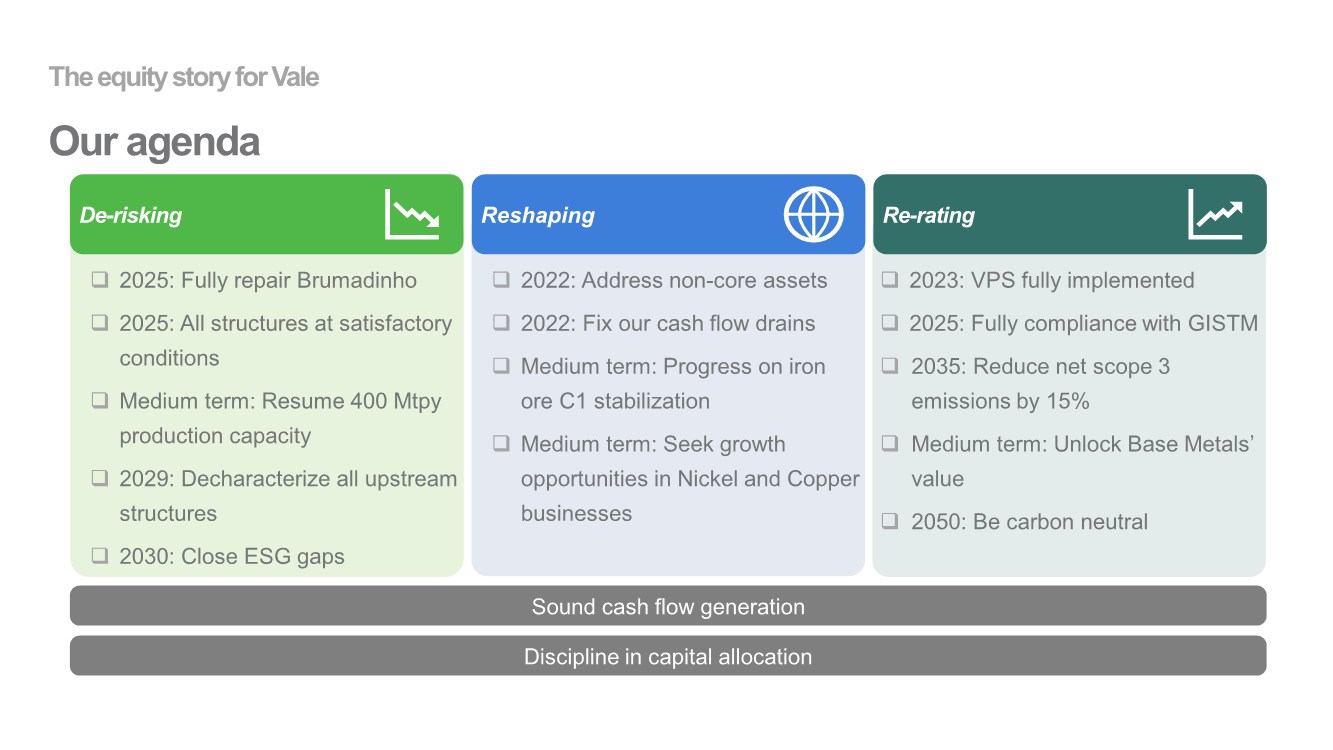

| Re-rating De-risking Reshaping Sound cash flow generation Discipline in capital allocation The equity story for Vale Our agenda ❑ 2023: VPS fully implemented ❑ 2025: Fully compliance with GISTM ❑ 2035: Reduce net scope 3 emissions by 15% ❑ Medium term: Unlock Base Metals’ value ❑ 2050: Be carbon neutral ❑ 2025: Fully repair Brumadinho ❑ 2025: All structures at satisfactory conditions ❑ Medium term: Resume 400 Mtpy production capacity ❑ 2029: Decharacterize all upstream structures ❑ 2030: Close ESG gaps ❑ 2022: Address non-core assets ❑ 2022: Fix our cash flow drains ❑ Medium term: Progress on iron ore C1 stabilization ❑ Medium term: Seek growth opportunities in Nickel and Copper businesses |

|

Signatures

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Vale S.A. | ||

| (Registrant) | ||

| By: | /s/ Ivan Fadel | |

| Date: September 9th, 2021 | Head of Investor Relations | |