Eldorado Gold Corporation

Annual information form

for the year ended December 31, 2013

March 28, 2014

ELD (TSX) EGO (NYSE)

About this annual information form

Throughout this annual information form (AIF), we, us, our, Eldorado Gold, corporation and the Company mean Eldorado Gold Corporation and its subsidiaries. This year means 2013.

All dollar amounts are in United States dollars unless stated otherwise.

Except as otherwise noted, the information in this AIF is as of December 31, 2013. We prepare the financial statements referred to in the AIF in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board, and file the AIF with appropriate regulatory authorities in Canada and the United States. Information on our website is not part of this AIF, or incorporated by reference. Filings on SEDAR are also not part of this AIF or incorporated by reference, except as specifically stated.

You can find more information about Eldorado Gold Corporation, including information about executive and director compensation and loans outstanding, principal holders of our securities, and securities authorized for issue under equity compensation plans (our incentive stock option plan, for example), in our most recent management proxy circular. For additional information you should also read our audited consolidated financial statements and management’s discussion and analysis (MD&A) for the year ended December 31, 2013. These are filed under our name on SEDAR (www.sedar.com), or you can ask us for a copy by writing to:

Eldorado Gold Corporation

Executive VP, Administration and Corporate Secretary

1188 – 550 Burrard Street

Vancouver, BC V6C 2B5

| What’s inside | ||

| About Eldorado Gold..................................................... | 5 | |

| Key milestones in our recent history ............................. | 8 | |

| About our business........................................................ | 10 | |

| Environmental policy..................................................... | 18 | |

| Material Properties | ||

| Kisladag...................................................................... | 20 | |

| Efemcukuru................................................................. | 26 | |

| Jinfeng ........................................................................ | 32 | |

| Olympias ..................................................................... | 36 | |

| Skouries ...................................................................... | 43 | |

| Other Operating Mines and Development Projects | ||

| Tanjianshan ................................................................. | 49 | |

| White Mountain ............................................................ | 52 | |

| Eastern Dragon ............................................................ | 54 | |

| Vila Nova ..................................................................... | 56 | |

| Tocantinzinho .............................................................. | 58 | |

| Stratoni ....................................................................... | 60 | |

| Perama Hill .................................................................. | 62 | |

| Certej .......................................................................... | 65 | |

| Sappes ....................................................................... | 68 | |

| Mineral reserves and resources.................................... | 70 | |

| Risk factors in our business ........................................... | 81 | |

| Investor information ...................................................... | 103 | |

| Governance .................................................................. | 108 | |

| Schedule A – Audit committee terms of reference ........................................................ | 119 |

| 1 |

Forward-looking information and risks

This document includes statements and information about what we expect to happen in the future. When we discuss our strategy; plans; outlook; future financial and operating performance; price of gold and other commodities; cash flow; cash costs; targets; production and expenditures; our mineral reserve and resource estimates; our proposed mine development; exploration and acquisitions; our expectation as to future performance at our mines; or other events and developments that have not yet happened, we are making statements considered to beforward-looking information orforward-looking statements under Canadian and United States securities laws. We refer to them in this AIF asforward-looking information.

Key things to understand about the forward-looking information in this AIF:

| · | It typically includes words and phrases about the future, such as plan, expect, forecast, intend, anticipate, believe, estimate, budget, scheduled, may, could, would, might, will, as well as the negative of these words and phrases. |

| · | It is provided to help you understand our current views and can change significantly; it may not be appropriate for other purposes. |

| · | It is based on a number of assumptions, estimates and opinions that may prove to be incorrect,including things like the future price of gold and other commodities, currency exchange ratios, anticipated costs and spending, production, mineral resources and reserves and metallurgical recoveries, impact of acquisitions on our business, the political and economic environment in which we operate, and our ability to achieve our goals. |

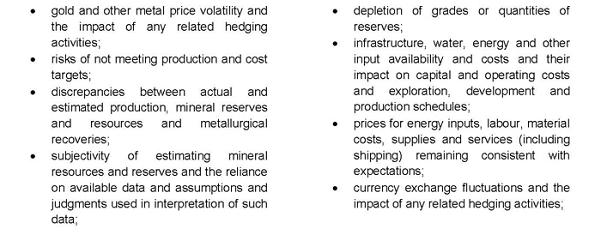

| · | It is inherently subject to known and unknown risks, uncertainties and other factors. Actual results and events may be significantly different from what we currently expect due to the risks detailed on page 81 of this AIF, which includes a discussion of material and other risks that could cause actual results to differ significantly from our current expectations and risks associated with our business, including the risks listed below: |

| 2 |

| 3 |

Although we have attempted to identify important factors that could cause actual results to differ materially from those contained in the forward-looking information, there may be other factors that cause actual results to differ materially from those which are anticipated, estimated or intended.

Forward-looking information is not a guarantee of future performance and actual results and future events could materially differ from those anticipated in such statements and information.

We will not necessarily update this information unless we are required to do so by applicable securities laws.

All forward-looking information in this AIF is qualified by these cautionary statements.

Reporting reserves and resources

There are material differences between the standards and terms used for reporting reserves and resources in Canada and the US. While the termsmineral resource,measured mineralresource,indicated mineral resource andinferred mineral resource are defined by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), and the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by the CIM Council, and must be disclosed according to Canadian securities regulations, the US Securities and Exchange Commission (SEC) does not recognize them under SEC Industry Guide 7 and they are not normally permitted to be used in reports and registration statements filed with the SEC.

Investors should not assume that:

| · | any or all of ameasured, indicated or inferred resourcewill ever be upgraded to a higher category or to mineral reserves; or |

| · | any or all of anindicatedorinferred mineral resourceexists or is economically feasible to mine. |

Under Canadian securities regulations, estimates of inferred mineral resources cannot be used as the basis of feasibility or prefeasibility studies.

Other information about our mineral deposits may not be comparable to similar information made public by US domestic mining companies, including information prepared according to Industry Guide 7.

| 4 |

About Eldorado Gold

Based in Vancouver, Canada, Eldorado Gold owns and operates mines around the world, primarily gold mines but also an iron ore and a silver-lead-zinc mine. Its activities involve all facets of the mining industry, including exploration, discovery, development, production and reclamation. Our business is currently focused on Brazil, China, Greece, Turkey and Romania. Eldorado Gold is governed by the Canada Business Corporations Act.

Each operation has its own general manager and operates as a decentralized business unit within the Company. We manage exploration properties, merger and acquisition strategies, corporate financing, global tax planning, regulatory compliance, metal and currency risk management programs, investor relations, engineering capital projects and general corporate matters centrally, at our head office in Vancouver. Our risk management program is developed by senior management and monitored by the board of directors.

Properties as of March 28, 2014

| Operating gold mines | Other Operating Mines and Development projects |

· Kisladag, in Turkey (100%) · Efemcukuru, in Turkey (100%) · Jinfeng, in China (82%) · White Mountain, in China (95%) · Tanjianshan, in China (90%) · Olympias, in Greece (95%)

| · Vila Nova, in Brazil (100%), Iron Ore mine · Stratoni, in Greece (95%), Silver, Lead, Zinc mine · Skouries, in Greece (95%) development project · Perama Hill, in Greece (100%) development project · Eastern Dragon, in China (75%) development project · Certej, in Romania (80.5%) development project · Tocantinzinho, in Brazil (100%) development project · Sappes, in Greece (100%) development project

|

Kisladag, Efemcukuru, Jinfeng, Olympias, and Skouries, are material properties for the purposes of NI 43-101.

Head office

Eldorado Gold Corporation

Suite 1188 – 550 Burrard Street

Vancouver, British Columbia, V6C 2B5

Telephone: 604.687.4018

Facsimile: 604.687.4026

Website: www.eldoradogold.com

Registered office

Suite 2900 – 550 Burrard Street

Vancouver, British Columbia V6C 0A3

| 5 |

Other offices

| Turkey | China | Brazil | Greece | Romania | Barbados | Netherlands |

· Ankara · Usak · Izmir · Canakkale | · Beijing, · Xining, Qinghai Province · Qianxinan Prefecture, Guizhou Province · Baishan, Jilin Province · Heihe, Heilongjiang Province | · Belo Horizonte · Macapa

| · Athens · Alexandropoulos · Stratoni · Sappes | · Deva

| · Bridgetown | · Amsterdam |

| 6 |

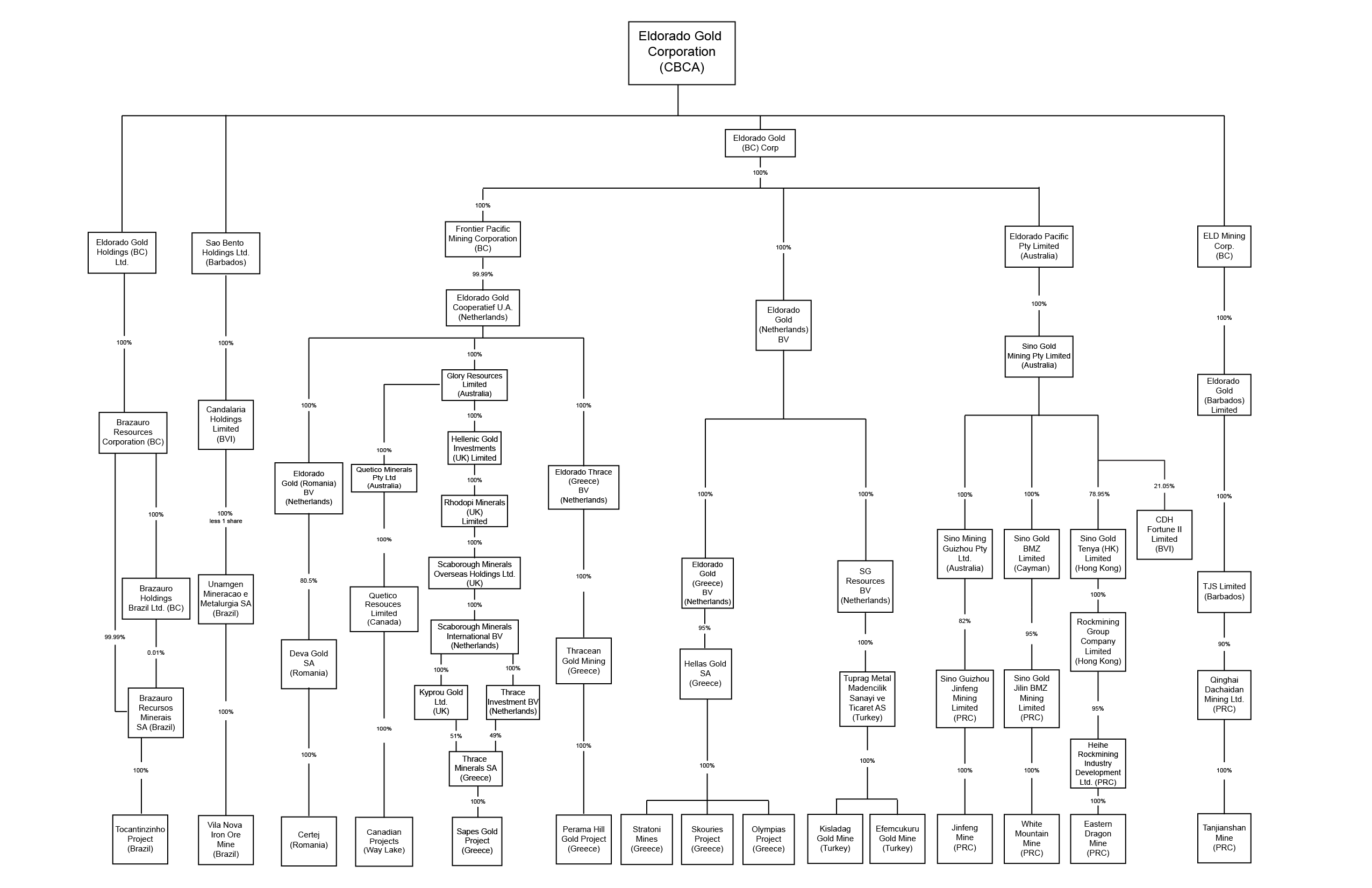

Subsidiaries

As of the date of this AIF, we own our assets through 43 subsidiaries. The total assets of any subsidiary which does not exceed 10% of our consolidated assets has been excluded from the chart below.

| 7 |

| 8 |

| 9 |

About our business

Eldorado Gold is one of the world’s lowest cost gold producers, with new mines, robust margins and a strong balance sheet. Our international expertise in mining, finance and project development places us in a strong position to grow in value and deliver strong returns for our shareholders as we create and pursue new opportunities in gold and other resources.

We are focused on building a successful and profitable, intermediate gold company. Our strategy is to actively pursue growth opportunities by discovering deposits through grassroots exploration and acquiring advanced exploration, development or low-cost production assets with a focus on the regions where we already have a presence.

Industry factors that affect our results

Gold market and price

Gold is used mainly for product fabrication and investment. It is traded on international markets. The London AM price fixing for gold on December 31, 2013 was $1,202 per ounce.

Foreign currency exposure

All of our revenues from gold sales are denominated in US dollars, while the majority of our operating costs are denominated in the local currencies of the countries we operate in. We monitor the economic environment, including foreign exchange rates, in these countries on an ongoing basis.

The table below shows the foreign exchange (gains)/losses recorded in the last three financial years:

| As at December 31 | |

| 2013 | $6,799,000 |

| 2012 | ($2,780,000) |

| 2011 | $5,367,000 |

Gold hedging

We monitor and consider the use of a variety of hedging techniques to mitigate the impact of downturns in the gold market.

As of the date of this AIF, we do not have any long term gold or currency hedges. Our future hedging activities will depend on an ongoing assessment of the gold market, our hedging strategy, financing restrictions and other factors.

| 10 |

An overview of our business

Exploration

| Our exploration programs include mine site drilling, advanced stage projects and grassroots programs. Our exploration programs are focused in the countries in which we operate, China, Turkey, Greece, Brazil and Romania, and are conducted through our regional exploration offices. Our exploration and business development teams actively pursue new early-stage project opportunities both within our focus jurisdictions and new regions. |

Mining and milling

| Ore and waste are removed from deposits by underground and open pit mining methods. The ore is then treated to extract metals. The waste is placed on an engineered dump for subsequent rehabilitation and reclamation or placed back underground as engineered backfill. The ore is treated using different methods depending on its metallurgy and grade. This may include heap leaching, crushing, milling, flotation, roasting, bacterial leaching and carbon-in-leach (CIL) methods for gold extraction. Flotation concentrates are also produced for sale. |

Refining and sales

| The gold doré produced at Kisladag is refined to market delivery standards at gold refineries in Turkey and sold at the spot price on the Istanbul Gold Exchange. Gold doré from our Chinese operations is sold to a variety of local refineries. Iron ore is sold on the spot market to Chinese or European interests through various agents. Contracts are also in place for the sale of concentrates in Greece and Turkey. These include gold concentrates from Efemcukuru and Olympias as well as lead / silver and zinc concentrates from Stratoni in Greece. These concentrates are sold under contract and are paid for at prevailing spot prices for the contained metals. |

Except as otherwise noted, Norman Pitcher, P. Geo., our President, is the Qualified Person under NI 43-101 responsible for preparing or supervising the preparation of, or approving the scientific or technical information contained in this AIF for all the properties described here and for verifying the technical data disclosed in this document relating to Kisladag, Efemcukuru, Jinfeng, Olympias and Skouries.

| 11 |

Production and costs1

| 2013 | |||||||

| 2013 | 2012 | change | First quarter | Second quarter | Third quarter | Fourth quarter | |

| Total | |||||||

| Gold ounces produced (including pre-commercial production) | 721,201 | 656,324 | 64,877 | 163,768 | 183,971 | 204,620 | 168,842 |

| Cash operating costs ($ per ounce) | 494 | 483 | 11 | 505 | 478 | 472 | 526 |

| Total cash cost ($ per ounce) | 551 | 554 | (3) | 567 | 536 | 528 | 577 |

| Realized price ($ per ounce sold) | 1,407 | 1,674 | (267) | 1,622 | 1,382 | 1,338 | 1,264 |

| Kisladag | |||||||

| Gold ounces produced | 306,182 | 289,294 | 16,888 | 65,707 | 61,575 | 84,016 | 77,996 |

| Tonnes to pad | 13,296,621 | 12,606,575 | 690,046 | 2,915,508 | 3,301,333 | 3,336,465 | 3,743,315 |

| Grade (grams per tonne) | 1.12 | 1.20 | (0.08) | 1.29 | 1.26 | 1.28 | 0.71 |

| Cash operating costs ($ per ounce)3 | 338 | 332 | 6 | 334 | 327 | 324 | 370 |

| Total cash cost ($ per ounce)2,3 | 358 | 361 | (3) | 359 | 348 | 343 | 384 |

| Efemcukuru | |||||||

| Gold ounces produced | 90,818 | 66,870 | 23,948 | 19,856 | 26,289 | 23,438 | 21,235 |

| Tonnes milled | 413,513 | 352,156 | 61,357 | 86,879 | 109,349 | 105,641 | 111,644 |

| Grade (grams per tonne) | 8.87 | 9.26 | (0.39) | 8.47 | 9.28 | 8.50 | 9.13 |

| Cash operating costs ($ per ounce)3 | 580 | 583 | (3) | 582 | 519 | 551 | 696 |

| Total cash cost ($ per ounce)2,3 | 604 | 613 | (9) | 619 | 537 | 568 | 700 |

| Tanjianshan | |||||||

| Gold ounces produced | 101,451 | 110,611 | (9,160) | 26,207 | 27,938 | 28,179 | 19,127 |

| Tonnes milled | 1,064,058 | 1,056,847 | 7,211 | 247,061 | 273,065 | 285,406 | 258,526 |

| Grade (grams per tonne) | 3.47 | 3.67 | (0.20) | 3.74 | 3.50 | 3.40 | 3.25 |

| Cash operating costs ($ per ounce)3 | 415 | 415 | 0 | 442 | 398 | 377 | 458 |

| Total cash cost ($ per ounce)2,3 | 601 | 612 | (11) | 636 | 577 | 557 | 655 |

| Jinfeng | |||||||

| Gold ounces produced | 123,246 | 107,854 | 15,392 | 21,742 | 28,889 | 40,212 | 32,403 |

| Tonnes milled | 1,412,548 | 1,422,794 | (10,246) | 351,901 | 336,707 | 363,798 | 360,142 |

| Grade (grams per tonne) | 3.24 | 2.65 | 0.59 | 2.43 | 3.33 | 3.66 | 3.51 |

| Cash operating costs ($ per ounce)3 | 736 | 817 | (81) | 832 | 757 | 684 | 719 |

| Total cash cost ($ per ounce)2,3 | 823 | 901 | (78) | 930 | 845 | 767 | 801 |

| White Mountain | |||||||

| Gold ounces produced | 73,060 | 80,869 | (7,809) | 20,915 | 17,462 | 19,287 | 15,396 |

| Tonnes milled | 810,389 | 754,673 | 55,716 | 198,934 | 203,033 | 209,581 | 198,841 |

| Grade (grams per tonne) | 3.39 | 3.85 | (0.46) | 3.80 | 3.25 | 3.28 | 3.23 |

| Cash operating costs ($ per ounce)3 | 705 | 625 | 80 | 634 | 742 | 713 | 748 |

| Total cash cost ($ per ounce)2,3 | 745 | 671 | 74 | 679 | 781 | 751 | 786 |

| 12 |

| 2013 | |||||||

| 2013 | 2012 | change | First quarter | Second quarter | Third quarter | Fourth quarter | |

| Olympias | |||||||

| Gold ounces produced (including pre-commercial production) | 26,444 | 826 | 25,618 | 4,827 | 6,658 | 8,742 | 6,217 |

| Tonnes milled | 552,557 | 28,331 | 524,226 | 89,112 | 116,972 | 185,012 | 161,461 |

| Grade (grams per tonne) | 3.32 | 5.07 | (1.75) | 3.97 | 3.80 | 3.19 | 2.78 |

| Cash operating costs ($ per ounce)3 | - | - | - | - | - | - | |

| Total cash cost ($ per ounce)2,3 | - | - | - | - | - | - | |

| Stratoni | |||||||

| Lead/zinc concentrate tonnes sold | 59,534 | 52,934 | 6,600 | 13,968 | 16,783 | 12,096 | 16,687 |

| Cash operating costs ($ per tonne) | 757 | 729 | 28 | 829 | 829 | 547 | 776 |

| Vila Nova | |||||||

| Iron ore tonnes sold | 470,140 | 603,668 | (133,528) | 129,548 | 81,874 | 126,835 | 131,883 |

| Cash operating costs ($ per tonne sold)3 | 63 | 60 | 3 | 66 | 74 | 58 | 59 |

1 We calculate cash operating costs according to the Gold Institute Standard.

2 Total cash cost is cash operating costs plus royalties, production taxes and off-site administration costs.

3 Cash operating costs and total cash cost are non-IFRS measures. See page 11 of the MD&A for more information.

| 13 |

How we measure our costs

Costs are calculated using the standard developed by The Gold Institute, a worldwide association of suppliers of gold and gold products of leading North American gold producers.

The Gold Institute stopped operating in 2002, but its standard is still widely used in North America to report cash costs of production. Adoption of the standard is voluntary, so you may not be able to compare the costs reported here to those reported by other companies.

Cash operating costs

Cash operating costs include the costs of operating the site, including mining, processing and administration. They do not include royalties and production taxes, amortization, reclamation costs, financing costs or capital development (initial and sustaining) and exploration costs.

Cash operating costs are divided by ounces sold to arrive at cash operating cost per ounce of production.

Total cash cost

Total cash cost is cash operating costs, plus royalties and production taxes and off-site administration costs.

Cash flow from operations before changes in non-cash working capital

We use cash flow from operations (or operating activities) before changes in non-cash working capital to supplement our consolidated financial statements, and calculate it by not including the period to period movement of non-cash working capital items, like accounts receivable, advances and deposits, inventory, accounts payable and accrued liabilities.

This is a non-IFRS measure, which we believe provides a better indication of our cash flow from operations and may be meaningful in evaluating our past performance or future prospects. It is not meant to be a substitute for cash flow from operations (or operating activities), which we calculate according to IFRS.

Since there is no standard method for calculating non-IFRS measures, they are not a reliable way to compare us against other companies. Non-IFRS measures should be used with other performance measures prepared in accordance with IFRS.

Production outlook, guidance and estimates are forward-looking information

We made several assumptions when they were developed and actual results and events may be significantly different from what we currently expect due to the risks associated with our business.

Assumptions:

| · | future events; |

| · | economic, competitive and regulatory conditions; |

| · | financial market conditions; and |

| · | future business decisions, including, without limitation, a continuation of existing business operations as they currently exist. |

Risks;

| · | global and local economic conditions; |

| · | pricing and cost factors; |

| · | unanticipated events or changes in current development plans, execution of development plans, future operating results, financial conditions or other aspects of our business; and |

| · | unfavorable regulatory developments that could cause actual events and results to vary significantly from what we expect. |

Please see Forward-looking information and risks on page 3 and Risk factors in our business on page 81.

| 14 |

Corporate Responsibility

For us, being a responsible corporate citizen means protecting the environment, providing a safe workplace for our employees and contractors, and investing in infrastructure, economic development and health and education in the communities where we operate so that we can enhance the lives of those who work and live there beyond the life of the mine.

Over the past two decades, we have operated mines in Mexico, Brazil, Turkey, Greece and China. We continue to grow our operations in Turkey, China, Brazil, Greece and Romania. We are proud of our record of implementing industry best practices that minimize environmental impacts while maximizing social and economic benefits.

Employees

We employ 7,261 employees directly and through contractors worldwide, with the majority of employees residing in local communities near our operations. We invest in education programs and we partner with local communities to create new opportunities for economic development.

We have hourly workers, contractors and permanent employees in eight countries. We also engage a number of contractors to work on specific projects. The table shows the approximate number of personnel working at our operations by country at December 31, 2013.

| Turkey | 1,754 |

| China | 3,144 |

| Brazil | 438 |

| Greece | 1,696 |

| Canada | 46 |

| Romania | 179 |

| Barbados | 1 |

| Netherlands | 3 |

| Total | 7,261 |

Most of our employees are unionized. The labour agreement at Kisladag and Efemcukuru is valid for a three-year term and was renewed on March 15, 2013. Union membership at Tanjianshan is voluntary, most hourly workers are using individual Bargaining Agreements. Collective Bargaining agreements are in force for all our operations. We consider employee relations to be good at all of our operations.

Operational Responsibility

Exploration

During exploration, while we conduct geological surveys and sampling to determine the existence and location of an ore deposit, we engage directly with local community members to identify their main social and environmental concerns and to better understand their needs.

Development

During the development stage, we complete feasibility studies that outline the economics, optimal mining methods and mineral recovery processes for the project, including environmental and closure considerations. We conduct extensive environmental testing and studies to establish baseline data and characteristics for air, water, soil and biodiversity. All this information becomes part of the Environmental Impact Assessment (EIA) that we file with the appropriate authorities.These are also available to the public. The environmental permitting process usually provides ample opportunity for consultation with the community to enable community reviews, input and commentary.

We also begin infrastructure development initiatives that include improving roads, building sewage systems and drilling water wells, according to the needs of the communities.

| 15 |

Construction and training

We make it a priority to hire local residents, training and instructing all employees and contractors in the best environmental, health and safety practices, procedures and controls. Based on our dialogue with the local community, we identify gaps in skills, provide on-the-job training and work with local technical schools and universities as required to enhance their mining-specific programs to help local residents increase their prospects of employment and provide a pool of trained workers for the Company.

Mining and processing

All our mining operations are expected to comply with the more stringent of local or international environmental standards. We implement the practices described in our EIA to mitigate any potential environmental impact throughout the entire mine life cycle.

Consultation with local communities continues throughout the mining and processing cycle. As part of our commitment to protecting the environment, we maintain extensive environmental monitoring programs, the results of which are shared with relevant government agencies. Independent government and academic groups also regularly audit our operations to ensure each site is within environmental limits. We continually monitor the quality of air, water (surface and ground) and soil. Noise, blast vibration and dust levels are also continually monitored both on the mine site and in any surrounding villages that may be impacted.We are sensitive to our potential effects on the local communities and have robust programs to mitigate any such effects. We also implement programs to preserve biodiversity at and near our operations. All types of waste, including hazardous wastes, are stored and disposed of with consideration for their potential environmental impacts. For example, at Efemcukuru where waste rock has acid rock drainage potential, storage areas are lined and seepage is collected and treated before disposal. Where waste rock does not pose any toxicity risk, such as at White Mountain, it is partially recycled for mine backfill.

Water quality is strictly controlled across all of our sites. We recycle as much water as is possible. Process tailings are discharged into lined facilities, and water from tailings is recycled through the process or, if being discharged, treated and tested to meet regulated limits before release. Measures are also in place to safeguard our tailings storage areas in the case of heavier than usual rainfall.

Remediation is done parallel to operation. Topsoil from mining and construction areas is stored for later reclamation use. We also investigate different plant, shrub and tree species suitable for local propagation in studies that are typically done in onsite greenhouses. Plots that are released from the mining areas are then re-vegetated concurrently to operations in other locations.

To provide a healthy and safe work environment, our employees are trained on an ongoing basis. These training programs are designed to minimize accidents and occupational illnesses.

We employ 7,261 employees and contractors worldwide, the majority of whom are from the local communities near our operations. Less than 1% of our employees at the operation and project level are expatriates. We pay locally competitive salaries and benefits to our employees and contractors.

Since the life of any mine is limited, we encourage and work with local communities to create new opportunities for economic development in sustainable areas. For example, we have supported the creation of local companies such as a vineyard at Efemcukuru, an organic agricultural company at White Mountain, and brick factories at White Mountain and Jinfeng. This ultimately benefits local communities and helps to provide opportunity for all local people, including those not directly associated with mining operations, beyond the life of the mine.

Reclamation and closure

Prior to and throughout a mine's operation, we conduct research to establish best reclamation practices. These reclamation activities are concurrent with mine operations to the extent possible. Financial provision is made for closure costs.

Once a mine is no longer profitable to operate, we close the mine site and conduct further reclamation activities as required in our environmental impact assessment so that the environment can successfully

| 16 |

transition to a productive ecosystem. For example, at Kisladag, cover system designs for capping the leach pad and rock dumps have been studied and are implemented as work is completed on those areas.

We have an excellent record on mining closure and reclamation. In October 2000, we were the first company to receive a final full regulatory environmental release from the Mexican government for reclamation activities at our La Trinidad mine near Rosario, Mexico. The former mine became a lake capable of supporting aquatic animals including fish.

Health and Safety Policy

In 2011, Eldorado Gold implemented a health and safety policy. The health and safety of our employees and local stakeholders is the number one priority of Eldorado Gold. We are committed to providing our employees with both a safe working environment and the skills necessary to perform their tasks in a safe manner.

To achieve these goals, Eldorado Gold will:

- promote safety as a core value within all levels of the organization;

- provide appropriate safety and job training to all employees so that the risks associated with any task are understood and mitigated;

- comply with all applicable health and safety regulations and international best practices;

- set up effective safety management systems at all mine sites so that health and safety goals can be set and results measured and evaluated; and

- promote a health and safety culture where all employees and contractors understand and take responsibility for their own safety and that of their fellow workers.

This policy is placed on notice boards at all of our operations as well as available on Eldorado Gold’s website. Eldorado Gold also has a sustainability committee comprising selected members of the board of directors. Their task is to oversee and monitor the environmental, health, safety, community relations and other sustainability practices, programs and performance of the Company.

LTI Performance

We work to maintain a good safety record by investing in environmental, health and safety training at our operations, and measure our results by tracking the numbers of lost-time incidents (LTI), and their frequency per million man hours (LTIFR). This year we continued to assimilate our Greek operations and continued programs to improve safety across all of our operations. Our LTI rates at our Greek operations were higher than our average. This is partly a function of early stage construction work at two of the projects and a high proportion of local contract workers. We continue to train our workers and stress the importance of safety at our operations as one of our primary values, in order to minimize or eliminate all LTI’s.

The table below shows our LTI performance for 2013.

Total hours worked | Lost-time incidents (LTI) | Lost-time incident frequency rate (LTIFR) | ||

| Turkey | Kisladag | 2,532,123 | 2 | 0.79 |

| Efemcukuru | 1,186,747 | 3 | 2.53 | |

| China | Tanjianshan | 1,813,232 | 2 | 1.10 |

| Jinfeng | 4,376,214 | 9 | 2.06 | |

| White Mountain | 2,671,097 | 2 | 0.75 | |

| Eastern Dragon | 82,906 | 0 | 0.00 | |

| Brazil | Vila Nova | 948,861 | 1 | 1.05 |

| Tocantinzinho | 213,400 | 1 | 4.69 | |

| Greece | Stratoni | 1,146,578 | 4 | 3.49 |

| 17 |

| Olympias | 871,035 | 4 | 4.59 | |

| Skouries | 535,241 | 3 | 5.60 | |

| Perama Hill | 47,262 | 0 | 0.00 | |

| Romania | Certej | 299,633 | 0 | 0.00 |

| Total | 16,724,329 | 31 | 1.85 |

We had an overall LTIFR of 1.85this year, which compares favourably with industry benchmarks in Canada and Australia. Unfortunately, we had three fatalities at our operations in 2013. In Turkey, an employee died while driving home in a company vehicle and two employees in China died while working on the job. Eastern Dragon, Tocantinzinho, Perama Hill and Certej employees all completed a full year without any lost-time incidents (one incident at Tocantinzinho was attributed to a contractor).

As part of our commitment to a safe workplace, we align our safety management systems with best practice frameworks. OHSAS 18001 is a best quality standard for occupational health and safety management systems. Hellas Gold’s Occupational Health & Safety Management system was recertified in November 2012. Efemçukuru achieved OHSAS 18001 certification in July 2013.

For further information on our safety initiatives please visit the “Responsibility” section of our website.

Environmental Policy

All of our mining and operations are expected to comply with local and international environmental standards. We implement best practices described in our environmental impact assessment and feasibility studies to maintain compliance.

In 2011 Eldorado Gold implemented an environmental policy which states that the Company and its subsidiaries are committed to protecting all aspects of the natural environment of the areas in which we work. This is a core value of Eldorado Gold and applies to all elements of the mining cycle including exploration, development, operation and closure.

To address this protection, Eldorado Gold will:

- comply with all applicable environmental regulations and international best practices;

- share environmental performance with local communities, government agencies and stakeholders;

- provide the necessary training, equipment and systems to our employees and contractors to address the protection of the environment and the most efficient use of non-renewable resources;

- design and operate facilities that are based on the efficient and economic use of energy and materials and the protection of the environment; and

- identify, evaluate, manage and audit scientifically the potential impact of our projects from inception through to closure.

This policy is placed on notice boards at all of our operations and on our website at www.eldoradogold.com. Eldorado Gold’s properties are routinely inspected by regulatory staff along with local community members to determine that the properties are in compliance with applicable laws and regulations as well as the company’s Environmental Policy and standards. Eldorado Gold also has closure plans for all of its operations. This allows us to properly estimate for the costs associated with implementing the required closure provisions.

ISO 14001 is an international standard for best practice in environmental management systems. Kisladag was certified on October 23, 2012. Efemcukuru was certified in July 2013. Our Greek operations under our subsidiary, Hellas Gold, intend to apply for ISO 14001 certification in 2014. The target is to include all activities (exploration, construction, mining, beneficiation and waste management) at these sites.

International Cyanide Management Code (Cyanide Code)

The Cyanide Code is an industry voluntary program for gold mining companies. It focuses exclusively on the safe management of cyanide including cyanide present in mill tailings and leach solutions. Companies that adopt the Cyanide Code must have their mining operations that use cyanide to recover gold audited by an independent third party to determine the status of Cyanide Code implementation.

| 18 |

Those operations that meet the Cyanide Code requirements can be certified. A unique trademark symbol can then be utilized by the certified operation. Audit results are made public to inform stakeholders of the status of cyanide management practices at the certified operation.

The objective of the Cyanide Code is to improve the management of cyanide used in gold mining and assist in the protection of human health and the reduction of environmental impacts. Eldorado Gold became a signatory to the Cyanide Code in 2012 and has nominated all of its operations that use cyanide for the extraction of gold. While there are issues in certain jurisdictions with regard to the legal requirements involved in purchasing and using cyanide, Eldorado Gold will require that as a minimum, all of its operations are working to best practices with regard to cyanide and will encourage our suppliers and transporters to join us in becoming signatories also.

Kisladag received Cyanide Code certification in December 2013. Our remaining operations that use cyanide have three years from Eldorado Gold becoming a signatory to become compliant by completing a third-party audit.

CDP

The CDP (formerly Carbon Disclosure Project) is an independent not-for-profit organization aiming to create a lasting relationship between shareholders and corporations regarding the implications for shareholder value and commercial operations presented by climate change. Eldorado Gold submitted its first report in 2012. Eldorado continues to report on an annual basis. The data initially presented will form a baseline for future reports.

Sustainability Report

As part of our continued move to enhance corporate responsibility disclosure and transparency, Eldorado Gold began publishing Sustainability Reports in 2012, and intends to continue to publish this report on an annual basis. This report follows the Global Reporting Initiative (GRI) framework. The GRI is a generally accepted framework for reporting on an organization’s economic, environmental and social performance. The GRI Reporting Framework contains general and sector-specific content for reporting an organization’s sustainability performance.

| 19 |

MATERIAL PROPERTIES

Kisladag

Material property under NI 43-101

| location | Usak Province, Turkey |

| ownership | 100% through TupragMetal Madencilik Sanayi ve Ticaret SA (Tuprag), |

| type of mine | open pit |

| metal | gold |

| in situ gold as of December 31, 2013* | proven and probable reserves: 9.55 million ounces measured and indicated resources: 11.05 million ounces grade: 0.63 g/t inferred resources: 4.91 million ounces grade: 0.40 g/t |

| average annual production | 240,000 ounces average over remaining life of mine (LOM) |

| expected mine life | 22 years, based on mining of 12.5 million tonnes per annum (Mtpa) ore crushed and approximately 7 Mtpa run of mine ore (ROM) |

| employees | 1040 (including 324 contractors) |

*Mineral reserves are included in the total of mineral resources.

History

| 1997 | Identified ore body and began in-depth exploration |

| 2003 | Completed the feasibility study in March Environmental impact assessment study (Kisladag EIA) submitted Received environmental positive certificate Increased the reserves and resources in March and September |

| 2004 | Received approvals for construction and the zoning plan in April Updated the feasibility study in May Received the construction permit in September and began site activities |

| 2005 | Began construction |

| 2006 | Poured the first doré in May Began commercial production in July |

| 2007 | Completed Phase II plant construction Commercial production interrupted in August |

| 2008 | Resumed commercial production in March |

| 2009 | Completed expansion of Phase II level pad and installed large carbon columns in ADR plant |

| 20 |

| 2011 | Received approval of supplementary EIA for the expansion of mining to 12.5 Mtpa and completed Phase III expansion Announced the intention to expand the process circuit to handle 25 Mtpa of crushed ore plus an additional capacity averaging about 8 Mtpa ROM ore |

| 2013 | Applied for a supplemental EIA to increase yearly ore extraction to 35Mtpa of ore. Announced the deferral of the plans to upgrade the treatment capacity from 12.5 Mtpa to 25 Mtpa crushed and 8 Mtpa ROM ore |

Licenses, permits and royalties

We currently have the required licenses and permits to support our mining operations.

| Surface rights | Operating license, IR 7302, covers 15,717 hectares, expires May 10, 2032. License can be extended if production is still ongoing at the end of the license period. Under Turkish law, we have the right to explore and develop mineral resources in the license area as long as we continue to pay fees and taxes. |

| Permits | All permits have been received. Please see the technical report for more information. |

| Royalties | An annual royalty is paid to the Government of Turkey, calculated as 2% of the sale price of the gold produced during the year, less the associated cost of mineral processing, refining, transportation and depreciation. |

About the property

Kisladag is in a rural area in west-central Turkey, between the city of Izmir (180 km to the west on the Aegean coast) and Ankara (the capital city, 350 km to the northeast). The site is 35 km southwest of the city of Usak (population 173,000) near the village of Gumuskol. Kisladag sits approximately 1,000 metres above sea level in gently rolling hills. Other economic activity in the area is a mixture of subsistence farming and grazing. A 5.3 km access road connects the site to the highway between Ulubey and Esme. Employees are mostly from the region. Supplies and services are accessed from the city of Usak. The site is serviced by a water well field consisting of 5 water wells with a 13 km water pipeline, and a 25 km power transmission line.

Climate

The area has a temperate climate. The average annual rainfall of 493 mm, occurs mostly during the winter months.

Operations

As of the date of this AIF, Kisladag has been operating for nearly eight years. Commercial production began in July 2006 but was temporarily interrupted from August 2007 to March 2008. Seelitigation, below, for more information.

Kisladag is a large tonnage, low grade operation. The ore is amenable to heap leach and, while recoveries are lower than they would be if conventional CIL was used, this is the most efficient method for treatment of the ore.

The open pit is mined using a standard drill and blast, truck and shovel mining process. The mine and the crusher operate 24 hours a day, seven days a week. A Turkish mining contractor provides ancillary services such as hauling crushed and ROM ore to the leach pad as required.

Ore is processed in a standard heap leach facility using the following process:

| · | crushing and screening in a three-stage plant; |

| · | transporting the crushed ore on overland conveyors, and placing it on the heap leach pad using a radial stacker. The heap leach pad has a two-part liner system consisting of a layer of compacted |

| 21 |

| low permeability clay soil or geosynthetic membrane, and a 2 mm thick both sides textured (for stability toe areas) and non textured (for regular areas) low density polyethylene synthetic liner. High density polyethylene (HDPE) liner is also used where the membrane will be subjected to sunlight for an extended period. The current designed stack height is 60 metres, placed in 10 metre high lifts; and | ||

| · | leaching the crushed ore using a diluted cyanide solution applied by drip emitters recovering the gold in a carbon adsorption facility (ADR plant) that uses a standard Zadra process including pressure stripping, electro winning and smelting. |

The final product is a gold doré bar which can be processed to 99.999% purity in domestic or offshore refineries.

The crushing and screening plant was upgraded in 2011 when additional crushing and screening equipment was installed to allow an increase of nominal throughput to 12.5 Mtpa of ore . The Phase III expanded plant was commissioned in the first quarter of 2011 and has performed above expectation.

During 2011, we announced the results of the Kisladag Expansion Study. This Phase IV study envisions the expansion of the crushing and screening plant with the installation of a parallel process circuit to handle a nominal 12.5 Mtpa of increased ore capacity. The primary crusher would be replaced with a single larger unit, capable of handling in excess of 25 Mtpa of ore. This new plant would also include three stages of crushing and screening and scalping of fines from the ore using a similar design incorporated in the Phase III expansion.Low grade ROM ore would be trucked directly from the mine to a dedicated leach pad. Metallurgical recoveries of 66% for crushed ore and 40% for ROM ore have been used in the study and reflect operating results and metallurgical test work to date.

The current truck and shovel fleet will continue to be utilized through the fleet’s expected operating life. In addition, a fleet of larger trucks and loading equipmenthas been introduced to deal with increasing tonnage mined and haul distances as the pit gets deeper. This larger haulage equipment is equipped for electric operation to reduce operating costs.

In 2013, we announced the deferral of the Phase IV expansion as described above. We will continue to upgrade the truck and shovel fleet to take advantage of the operating cost difference between diesel and electric motive power.

In 2013, 13.2 million tonnes of ore were placed on the pad at a grade of 1.12 g/t. Gold production in 2013 totaled 306,000 ounces at a cash cost of $338 per ounce.

LOM and cost estimates

| · | gold production: 240,000 ounces per year for the remaining LOM; and |

| · | cash operating cost: LOM cash costs are expected to average $570 per ounce. |

Forecast gold production for 2014 is expected to be between 300,000 – 335,000 ounces at a cash cost of $470 to $485 per ounce. Sustaining capital costs for 2014 are expected to be $70 million, most of which is to be used for mining equipment and assorted infrastructure projects.

The corporate income tax rate applicable to profits of Kisladag is currently 20%. Production taxes in Turkey are assessed at 2% of gold revenues net of processing and selling costs.

Unit costs are expected to increase as the pit deepens. We expect the cost for processing and mine support to remain constant for the rest of the mine life, except in response to changes in costs that affect the entire gold mining industry, such as the cost of fuel and reagents, the cost of labor, currency exchange rates and inflation.

Environment

The Kisladag EIA was submitted to the Ministry of Environment and Urbanization in January 2003, and the environmental positive certificate was issued in June of that year. A supplementary Kisladag EIA to increase mine ore production to 12.5 Mtpa was subsequently approved in June, 2011.

The Kisladag EIA identified several socio-economic effects of mine development, and identified measures that can be used to avoid or minimize potential environmental impacts.

| 22 |

A new addendum to the Kisladag EIA was prepared and submitted in 2013. This Kisladag EIA covers the Phase IV expansion allowing maximum total mine ore production of 35 Mtpa. This EIA is expected to be approved by mid-2014.

Exploration

Tuprag discovered the Kisladag deposit in the late 1980’s during a regional grassroots exploration program focusing on Late Cretaceous to Tertiary volcanic centres in western Turkey. It selected the prospect area on the basis of Landsat-5 images that had been processed to enhance areas of clay and iron alteration, followed by regional stream sediment and soil sampling programs. Preliminary soil sampling programs identified a broad 50 ppb gold anomaly within a poorly exposed area now known to directly overlie the porphyry deposit.

Early exploration of the deposit area included excavation of trenches to better characterize the soil anomaly, and ground geophysical surveys including IP-resistivity (IP), magnetics, and radiometrics.

To date, there have been over 155,000 metres of diamond core and reverse circulation drilling at Kisladag. Most of this has focused on resource definition drilling of the known deposit and exploration drilling in nearby areas. We have completed detailed geological mapping of the deposit and surrounding region, and definition and modeling of alteration zonation in the deposit area.

In 2011, our exploration program included over 10,000 metres of diamond drilling focused on condemnation work in areas of planned additional leach pad and waste rock dump sites. We also executed IP programs and soil geochemical surveys northeast and west of the Kisladag deposit.

Our 2012 exploration program included an additional 13 holes totaling 10,500 metres of drilling to test geochemical and geophysical targets peripheral to the Kisladag deposit. This drilling program was testing for possible mineralized satellite intrusions not exposed at the surface. None of these holes identified any satellite intrusions.

2013 exploration work was limited to participation in a regional airborne geophysical survey that included the Kisladag property as part of the survey grid.

Geology and mineralization

Geological setting

Kişladağ is a porphyry gold deposit that formed beneath a coeval Miocene volcanic complex in Western Anatolia, Turkey. At least four latite intrusive phases are recognised in the deposit but these are extensively altered. Alteration consists of a potassic core with K-feldspar, biotite, quartz and locally magnetite, outwardly overprinted by illite, kaolinite, quartz, and tourmaline. Remnants of a quartz-alunite lithocap are found near surface. The mineralized intrusions at Kisladag are enclosed within volcanic and volcaniclastic strata that overlie basement schist and gneiss of the Menderes Massif Core Complex. These strata dip outward from the deposit core, and display rapid facies changes from massive lavas and coarse poorly stratified units proximal to the porphyry centre, to finer well-stratified volcaniclastic strata that inter-finger with lacustrine sedimentary rocks in surrounding sedimentary basins.

There has been relatively little structural modification to the deposit and surrounding Tertiary rocks. Lithologic contacts are primarily intrusive or depositional, with no documented major fault offsets. The deposit and adjacent rocks do, however, contain a high density of joints and low-displacement brittle fractures. Most of these are only a few metres to a few tens of metres in length, and have negligible displacement.

Mineralization

Gold mineralization at Kisladag occurs within zones of sulphide and quartz stockworks, and disseminated to fracture controlled sulphides. Pyrite is the dominant sulphide mineral, averaging around 3% in the primary mineralized zone, with trace amounts of molybdenum, zinc, lead, and copper. Highest gold grades occur, in multiphase quartz sulphide stockworks and zones of mottled to pervasive silicification.

Oxidation extends to a depth of 30 to 80 metres on the southern side of the deposit, and 20 to 50 metres on the northern side of the deposit. Limonite and geothite are the most abundant oxide minerals. There is no supergene enrichment within the oxidized zone.

| 23 |

Drilling

Exploration drilling was undertaken at Kisladag in several drilling campaigns between 1998 and 2012. Approximately 125,000 metres of diamond drilling, and 30,000 metres of reverse circulation drilling have been completed. All diamond drilling was done with wire line core rigs of mostly HQ size (63.5mm core diameter). Drillers placed drill core into wooden core boxes, each holding about 4 metres of core.

Project geologists systematically collected geological and geotechnical data from the core, and photographed all core (wet) before sampling. Specific gravity measurements were obtained approximately every five metres. The entire length of each core was cut in half with a diamond saw. One half was submitted for assay and one half retained for reference on site. Core recovery in the mineralized units was excellent, usually between 95% and 100%.

Sampling and analysis

Core samples are prepared at our preparation facility in Çanakkale in north-western Turkey by inserting a Standard Reference Material (SRM), a duplicate and a blank sample into the sample stream at every eighth sample.

The samples are then shipped to ALS Chemex Analytical Laboratory in North Vancouver. The samples are assayed for gold by 30 g fire assay with an atomic absorption finish, and for other elements using fusion digestion and ICP analysis.

Data verification

A review of the entire drill hole database since production started in 2006 has been done, and checked against the original assay certificates and survey data. Any discrepancies have been corrected and incorporated into our resource database. The mined portions of the resource model have been reconciled to production and agreement was excellent.

In our opinion, the Kisladagdeposit assay database is accurate and precise enough to estimate resources.

Technical report

The information about Kisladag in this AIF is partly derived from the scientific and technical data in the Kisladag technical report:Technical Report for Kisladag Gold Mine, Turkey.

Qualified persons: Stephen Juras, Ph.D., P.Geo., Richard Miller, P.Eng., and Paul Skayman, MAusIMM, all of Eldorado Gold.

The report is dated March 15, 2010, and effective January 2010. It’s available on SEDAR (www.sedar.com) and EDGAR (www.sec.gov).

Litigation

Original EIA Litigation

Litigation by certain third parties was brought against the Turkish Ministry of the Environment and Urban Planning (former Ministry of Environment and Forests) in April 2004 in the Manisa Administrative Court. The parties were seeking to cancel the positive environmental certificate for Kisladagon the basis of alleged threats to the environment and deficiencies in the environmental impact assessment. Tuprag was accepted as a co-defendant in the cases alongside the defendant ministry.

In 2007, a lower administrative court ruled in our favour. The plaintiff appealed that decision and on July 19, 2007, the Sixth Department of Council of State ordered the mine to be shut down pending a decision on the case. We shut the mining operations down on August 18, 2007, except for activities approved by the Turkish authorities related to sound environmental practices. The mine remained closed for the rest of that year.

On February 6, 2008, the Sixth Department of the High Administrative Court in Ankara, decided that the expert reports prepared for the Lower Administrative Court were not sufficient to make either a positive or negative decision on the merits of the case, and referred the matter for rehearing before the Lower Administrative Court. The matter was then referred to the Lower Administrative Court, which named an expert panel to review the environmental impact assessment and prepare a report.

| 24 |

The temporary injunction automatically expired with this decision and Tuprag obtained the necessary permits from the Turkish government authorities and on March 6, 2008, the KisladagMine reopened and resumed production.

On October 13, 2010, the Lower Administrative Court issued a decision in the case that was unanimously in favour of the project. The plaintiff appealed the decision to the High Administrative Court in Ankara, where the file was reviewed. On December 7, 2011, the High Administrative Court issued its decision in favour of the project. The plaintiff has appealed to the court to reconsider its decision. On November 13, 2013, the High Administrative Court rejected the final appeal of the plaintiffs. The file was returned to the Manisa Administrative court and the case was closed.

Revised EIA Litigation (for increasing production from 10 Mtpa to 12.5 Mtpa)

On September 12, 2011 certain third parties filed litigation against the revised Environmental Positive Certificate issued by the Ministry of Environment and Urban Planning. The case is being heard by the Manisa Administrative Court. A request for an immediate injunction has been rejected by the court and appeal of this decision was rejected by the District Appeals Court. Tuprag has been accepted as a co-defendant next to the Ministry of Environment and Urban Planning. The court is currently in the process of selecting an expert committee to evaluate the file.

We are confident in both the methodology of the Kisladag EIA and Tuprag’s compliance with all procedural steps taken to obtain the environmental positive certificate. We believe that we will successfully defend this litigation. If we do not succeed, our ability to operate Kisladag at a production rate of greater than 10 million tons of ore per year may be affected, which may adversely affect our production and revenue.

In addition to the litigation brought against Tuprag described above, Tuprag is, from time to time, involved in various claims, legal proceedings and complaints, including pertaining to our operating licenses and permits, arising in the normal course of business. The Company and Tuprag cannot reasonably predict the likelihood or outcome of these actions.

| 25 |

Efemcukuru

Material property under NI 43-101

| location | Izmir Province, Turkey |

| ownership | 100% through Tuprag |

| type of mine | underground |

| metal | gold |

| in situ gold as of December 31, 2013* | proven and probable reserves: 1.19 million ounces measured and indicated resources: 1.53 million ounces inferred resources: 0.88 million ounces |

| average annual production | 103,000 ounces |

| expected mine life | 10 years,based on 2013 proven and probable reserves |

| employees | 645 (including 212 contractors) |

* Mineral reserves are included in the total of mineral resources.

History

| 1992 | Discovered the deposit while carrying out reconnaissance work in western Turkey |

| 1997 | Completed drilling program along the north, middle and south ore shoots, delineating the resource and hydrogeologically testing the vein structure and the hanging wall and foot wall rocks |

| 2004 | Completed environmental impact assessment study |

| 2005 | Received positive environmental impact assessment certificate |

| 2007 | Released a positive feasibility study in August based on underground mining, milling the ore on site and treating the gold concentrate at Kisladag prepared by Wardrop Engineering Inc. (Wardrop) |

| 2008 | Wardrop completed positive feasibility study update in August Construction of the mine commenced |

| 2009 | Construction continued throughout 2009 |

| 2011 | In June the mining and processing operations started In December commercial production started and treatment of the Efemcukuru concentrate commenced at the Kisladag concentrate treatment plant |

| 2012 | In September 2012, the Kisladag concentrate treatment plant was taken out of operation pending modifications to the circuit Commercial sales of concentrate to third parties started in November 2012 |

| 26 |

| 2013 | Completed addendum to EIA increasing production capacity to a maximum of 600,000 metric tons per year |

Licenses, permits and royalties

| Surface rights | Operating license, IR 5419, covers 2,262 hectares. Under Turkish law, we have the right to explore and develop mineral resources in the license area as long as we continue to pay fees and taxes. |

| Permits | We currently have the required licenses and permits to support our mining operations. |

| Royalties | An annual royalty is paid to the Government of Turkey, calculated as 2% of the sale price of the gold produced during the year, less the associated cost of mineral processing, refining, transportation and depreciation. |

About the property

Efemcukuru is in Izmir Province near the coast of western Turkey, about 30 km from Izmir, the provincial capital. The site is 2 km north of the village of Efemcukuru (population approximately 500). It sits approximately 580 to 720 metres above sea level in hilly terrain. Vegetation is mainly mature pine trees with sparse undergrowth covering the hillsides.

Economic activity in the area is a mixture of subsistence farming and grazing. We mainly access supplies and services from the city of Izmir. Several paved and unpaved roads connect the village with other local population centres.

Employees are mostly drawn from the local region.

Power has been provided by a dedicated transmission line from the Urla substation approximately 23 km away. Mine infrastructure includes administration buildings, a concentrator, a filtration plant; tailings and waste rock impound areas. Initial plans called for concentrate to be treated at Kisladag through a dedicated treatment plant. All concentrate is now being sold to third parties.

Climate

The area has hot and dry summers and warm and rainy winters with limited snowfall. Temperatures range between 30ºC in summer and 0ºC in winter with an annual average of approximately 17ºC. Average annual precipitation is 720 mm.

Operations

Efemcukuru is a high grade underground deposit with the gold occurring as free gold closely associated with sulphides. The ore is mined using conventional mechanized cut and fill along with some opportunity for longhole mining methods.

The ore is processed through milling and gravity circuits followed by flotation to produce a flotation concentrate and a gravity concentrate. The gravity concentrate is refined to doré on site. As part of our operating agreement, we were transporting the flotation concentrate to a treatment plant (KCTP) located at Kisladag, where it was being treated in a dedicated cyanide leach plant. In late 2012 and 2013, the flotation concentrate was being sold under contract to the spot market while the KCTP was under review to improve gold recoveries. A decision was taken late in 2013 to decommission the KCTP and continue to sell the product under contract to third parties.

The flotation tailings are filtered and either placed back underground as paste fill or placed in a lined dry stack tailings facility.

Key milestones

2010

| · | installed the power supply and finished the primary surface facilities |

| · | concentrator plant: completed the majority of the mechanical installations, installed the SAG and ball mills, and completed plant buildings; |

| 27 |

| · | concentrate treatment plant: completed engineering and procurement, and prepared for construction; |

| · | tailings filtration and backfill plants: 80% completed; |

| · | rock dump and tailings dump: ready to be commissioned; and |

| · | selected a Turkish contractor to carry out mine preproduction, including underground development to prepare for mine operations. |

2011

| · | The plant commenced operations in Q2 2011. |

During 2013, Efemcukuru mined 399,000 tonnes of ore at 8.85 g/t gold and treated 414,000 tonnes of ore and recovered 109,000 ounces of gold in concentrate and gravity doré.

Processing of Efemcukuru concentrate was halted at the KCTP in the third quarter of 2012. During 2013, we completed testwork to determine the most efficient metallurgical process to maximize recovery of gold from the Efemcukuru concentrate. At the end of the testwork, we concluded that, based on the results, the payability we could achieve from modifying the KCTP was not sufficiently higher than that received by selling concentrates under contract to justify additional capital expenditures. Therefore, we have decided to sell concentrates to third parties long term from Efemcukuru and decommissioned the KCTP.

In 2013, 121,000 ounces of gold from concentrate and the gravity circuit combined were sold. Cash costs for 2013 were $580per ounce.

LOM production and cost estimates

The latest LOM production schedule is based upon increasing production from 400,000 tonnes per year in 2013 to 500,000 tonnes per year in 2016 by way of a plant expansion and additional underground equipment. Long term parameters are:

- 11 year mine plan from 2014 – 2025;

- Gold doré or concentrate – averaging 103,000 ounces of gold per year.; and

- LOM cash operating costs in the range of 590 - $650 per ounce.

Forecast production for 2014 is approximately 90,000 to 100,000 ounces of gold at $575 - $590 per ounce. Capital spending for 2014 is estimated at $20 million.

The corporate income tax rate applicable to profits of Efemcukuru is currently 20%. Production taxes in Turkey are assessed at 2% of gold revenues net of processing and selling costs.

Environment

The environmental impact assessment study (Efemcukuru EIA) was submitted to the Ministry of Environment and Urbanization in 2005, and the environmental positive certificate was issued in September of that year.

The Efemcukuru EIA identified several socio-economic effects of mine development, and identified measures that can be used to avoid or minimize potential environmental impacts.

Subsequent to completion of the Efemcukuru EIA, a revision was approved in December 2012, allowing for a larger disturbance footprint and an increased mining production rate of 600,000 tonnes per annum.

Exploration

Shallow pits and underground workings along the auriferous veins, now overgrown by mature stands of forest, indicate that mining activity at Efemcukuru dates back at least several centuries.

Modern exploration began in 1992, when Tupragrecognized the exploration potential of the area while conducting reconnaissance work in western Turkey. Between 1992 and 1996, Tupragconducted ground magnetic surveys, rock chip and soil sampling, geological mapping and a 6,000 metre diamond drilling program focusing primarily on the Kestane Beleni vein. This work identified high-grade gold mineralization in three separate zones: the south ore shoot, the middle ore shoot and the north ore shoot.

Infill drilling in 1997 and 1998 provided an initial resource estimate for the south and middle ore shoots, and a prefeasibility study was completed in 1999. Additional drilling programs from 2006 to 2010 with stepouts to deeper levels and along strike significantly increased the resource estimate and provided a resource estimate for the north ore shoot.

| 28 |

Drilling in 2011 and 2012 focused on a new zone along strike from the north ore shoot, referred to as the Northwest Extension, on down-dip extension to the south ore shoot and on the nearby Kokarpinar vein.

The Kokarpinar vein is parallel to and east of the Kestane Beleni vein. We have drilled widely spaced exploration holes and obtained potentially economic grades from both surface samples and drill hole intercepts.

Soil and rock chip geochemical survey programs have been carried out as well as detailed geological mapping.The soil geochemistry surveys have identified several zones with multi-element anomalies. These anomalies are especially strong over the Kestane Beleni vein and the central part of the Kokarpinar vein.

Geology and mineralization

Geological setting

Efemçukuru is an intermediate sulfidation epithermal gold deposit hosted within Upper Cretaceous phyllite and schist at the western end of the Izmir-Ankara Suture Zone in SW Turkey. The host rocks are locally silicified to hornfels and are cut by moderately N- to NE-dipping faults that are exploited by rhyolite dykes and epithermal veins.

Mineralization

Two major veins host mineralization, Kestanebeleni and Kokarpinar, with the former containing the bulk of the ore. Vein mineralogy is variable but primarily consists of quartz, rhodonite (commonly replaced by rhodochrosite), adularia, and sulfide assemblages including pyrite, galena, chalcopyrite, and sphalerite. Spectacular, high grade banded crustiform-colloform textures characterize the veins in addition to multi-stage breccias that were likely the result of shallow-level boiling. Most of the gold is very fine (2.5 to 50 microns), occurring as free grains in quartz and carbonate, and as inclusions in sulphide minerals. Lower grade mineralized stockworks occur peripheral to the ore shoots, and are most strongly developed in hangingwall rocks. Most of the current resources are in the Kestane Beleni vein. Both veins strike northwesterly (320°-340°), dip 60°E to 70°E, and can be traced on surface for strike lengths of over a kilometre. The veins commonly have faults with post-mineral movement along either hangingwall or footwall contacts, or within the veins themselves.

The Kestane Beleni vein’s three ore shoots (south, middle and north) differ slightly in strike and dip orientation, but the vein and the fault zone is continuous between them.

Drilling

Drilling campaigns were conducted between 1992 and 1997, and from 2006 to 2012. To date, 414 core holes have been drilled totaling 89,600 metres, and 59 reverse-circulation holes totaling 5,000 metres. All diamond drilling was done with wire line core rigs of mostly HQ size (63.5mm). Drillers placed the core into wooden core boxes. Each box held about 4 metres of core.

Geological and geotechnical data was collected from the core, and photographed (wet) before sampling. Core recovery in the mineralized units was very good. The core library is kept in storage facilities near the site.

Sampling and analysis

A five foot or ten foot single tube core barrel is used to collect samples. Sample intervals from 0.1 metres to 1.6 metres were selected by the geologist and marked in the core boxes. Individual samples were then cut using a diamond rock saw. After initial crushing, each sample was split to approximately one kilogram, and then pulverized and split again into two 200 g pulps. One of these was shipped to the analytical laboratory and the other, with the approximately one kilogram of pulp reject, was put into storage.

The core samples were prepared at our preparation facility in Çanakkale in northwestern Turkey by inserting a SRM, a duplicate and a blank sample into the sample stream at every eighth sample. Samples were shipped to ALS Chemex Analytical Laboratory in North Vancouver. These were assayed for gold by 30 g fire assay with an atomic absorption finish (with a gravimetric finish re-assay for samples returning initial values greater than 8 g/t), and for other elements using fusion digestion and ICP analysis.

| 29 |

Data verification

The database used to estimate the 2009 mineral resource was checked against the original source data. Survey and assay data were checked for discrepancies and corrected before entering them into the resource database. Newer data entered directly into the database was also periodically compared to original electronic certificates (assays), down hole measurements and collar survey data. In our opinion, the Efemcukuru deposit assay database is accurate and precise enough to estimate resources.

Technical report

The information about Efemcukuru in this AIF is partly based on the scientific and technical data in the Efemcukuru technical report:Technical Report on the Efemcukuru Project.

Qualified persons: Scott Cowie, BE (Mining), LLB, MAusIMM, Tetra Tech Australia Pty. Ltd. and Stephen Juras, Ph.D., P. Geo.

The report is dated September 17, 2007, effective August 1, 2007, and is available on SEDAR (www.sedar.com) and EDGAR (www.sec.gov).

Litigation

Mineral license litigation

On December 3, 2004, certain third parties filed litigation against the Ministry of Energy and Natural Resources. The parties were seeking to cancel the mineral license for Efemcukuru on the basis of an alleged threat to the water quality in the local catchment area. Tuprag was accepted as a co-defendant in the cases alongside the defendant ministry.

Turkey's Lower Administrative Court issued a negative decision, delaying the start of mining activities at Efemcukuru in December 2004. The High Administrative Court overturned the decision in December 2005, referred the case back to the Lower Administrative Court, and our mining license was re-issued.

The Lower Administrative Court formed a new expert committee to review the case. The majority of experts were in favour of the project and on June 15, 2007, the court ruled unanimously in favour of the project.

The decision was appealed to the High Administrative Court, and the decision was overturned on March 31, 2008. Tuprag appealed this decision. On March 10, 2009, the appeal was refused, and the case referred back to the Lower Administrative Court. The lower court formed a new expert committee to review the case and on June 2, 2011, the Court unanimously ruled in favour of the project. On September 6, 2012, the 8th department High Administrative Court confirmed the ruling of the Lower Administrative Court. The plaintiffs have exercised their right to appeal to the 8th Department of the High Administrative Court to reconsider its decision.

Environmental Positive Certificate litigation

On January 26, 2009, the High Administrative Court delivered a positive decision in Tuprag’s favour in a case brought by certain third parties seeking to cancel the Environmental Positive Certificate for Efemcukuru issued by the Ministry of Environment and Urban Planning (former Ministry of Environment and Forests). The unsuccessful litigants have appealed this decision to the High Administrative Court requesting that its decision be reconsidered, which decision is pending.

We believe that chances of a reversal are low. We are confident in both the methodology of the environmental assessment report and Tuprag's compliance with all procedural steps taken to obtain the Environmental Positive Certificate.

On April 24, 2013, certain parties filed litigation against the Revised Environmental Certificate for Efemçukuru issued in December 2012 by the Ministry of Environment and Urban Planning. The case is being heard by the 1st Administrative Court in Izmir. A request for an immediate injunction has been rejected by the court and appeal of this decision was rejected by the Izmir District Appeals Court. Tuprag has been accepted as a co-defendant next to the Ministry of Environment and Urban Planning. The court is currently considering petitions by other parties to join the case.

| 30 |

We believe that we will successfully defend this litigation. If we do not succeed, our ability to operate Efemçukuru at a production rate of more than 250,000 tons of ore per year may be affected, which may adversely affect our production and revenue.

Operation Permit litigation

On September 7, 2012, certain parties filed litigation against the Izmir Province Special Administration, seeking to cancel the Operation Permit for Efemcukuru on the basis that the Efemcukuru Mining License and the Environmental Positive Opinion are unlawful. Tuprag has become a co-defendant in this case. On September 20, 2013 the 3rd Administrative Court of Izmir rejected the claims of the defendants and ruled in favor of the validity of the Operation Permit. The plaintiffs have exercised their right to appeal this decision. The case is now under review at the 8th Department of the High Administrative Court in Ankara. We believe that we will successfully defend this litigation. If we do not succeed, our ability to operate Efemcukuru may be adversely affected, which may adversely affect our production and revenue.

Environmental License Litigation

On September 12, 2012, certain third parties filed litigation against the Environmental License issued by the Ministry of Environment and Urban Planning. The case is being heard by the 4th Administrative Court of Izmir. A request for an immediate injunction has been rejected by the court and appeal of this decision was rejected by the Izmir District Appeals Court. Tuprag has been accepted as a co-defendant next to the Ministry of Environment and Urban Planning. The court is in the process of selecting an expert committee to review the file.

We believe that we will successfully defend this litigation. If we do not succeed, our ability to operate Efemçukuru may be adversely affected, which may adversely affect our production and revenue.

In addition to the litigation brought against Tuprag described above, Tuprag is, from time to time, involved in various claims, legal proceedings and complaints, including pertaining to our operating and environmental licenses and permits, arising in the normal course of business. The Company and Tuprag cannot reasonably predict the likelihood or outcome of these actions.

| 31 |

Jinfeng

Material property under NI 43-101

| location | Guizhou Province, China |

| ownership | 82% through Sino Guizhou Jinfeng Mining Limited, |

| type of mine | open pit, underground |

| metal | gold |

| in situ gold as of December 31, 2013* | proven and probable reserves: 1.98 million ounces measured and indicated resources: 2.97 million ounces inferred resources: 1.00 million ounces grade: 2.98 g/t |

| average annual production | 120,000 to 165,000 ounces |