1 Tender Offer Employee Meeting November 7, 2007 Exhibit 99(a)(1)(h) |

2 Tender Offer-Meeting objectives Explain the tax law impact on certain stock options. Both exercised and unexercised. Explain what the Company is doing to remedy the affected options. Your choices and deadline. |

3 General Comments Issues The Company restated financial results for FY2006 and prior years. The accounting findings cause discounted options. These unintended discounted options have adverse tax consequences. |

4 What is a discounted option and how does it get created? A discounted option is a stock option where the price of the option is less than the closing price of the stock on the date of the grant. For today’s discussion, let’s say – a discounted option really means your strike price is less than the accounting option price. |

5 Consequences 1. Discounted options cause ISO’s to become NQO’s (“Busted ISO’s”). Result is a personal tax rate problem. 2. Certain discounted options are subject to IRC 409A. Result is an additional 20% personal tax penalty and withholdings before you exercise. General Comments |

6 What the Company will offer The Company will fix the previously exercised “Busted ISO” problem by paying tax on your behalf. The Company will “make you whole” on 409A issues. This will be accomplished through the tender offer and other cash payments. |

7 Tender Offer IRC 409A Background Certain Stock Options that are granted at a discount are subject to IRC 409A. We will show which grants later in this presentation. Originally 409A was a deferred compensation regulation. Subsequently Stock Option restatement impacts have been included. 409A says that “income” created from “discounted options” is considered wages for individual tax purposes. Therefore, withholdings (FIT, SIT, FICA) need to be paid on the deferred “income”. Further, there is additional tax of 20% on the notional gain. |

8 General Comments The Company would like to make you whole for both past and future exercise problems caused by discounted options. |

9 For those exercised – Busted ISO’s SCSC will pay the tax difference from the L-T tax rate and the mandatory W/H. This will cover all options exercised in years 2004 through May 1, 2007. We estimate this cost to be over $1.67 million. SCSC will have paid the IRS directly. We will work with the IRS so individual employees will not be required to amend your tax return nor pay the additional tax on “busted ISOs”. We will need approval of the IRS but are advised that they will likely approve. |

10 • The Company will compensate you for the 409A 20% penalty on past exercises. This covers affected options exercised in calendar 2006 through November 6, 2007. • The Company will work directly with the IRS so that individual employees will not be required to amend their 2006 tax return nor will they need to include any 409A income on their 2007 tax return. We will need approval of the IRS but are advised that they will likely approve. |

11 Tender Offer For those not exercised-IRC 409A As long as the discounted stock options remain unexercised, the 409A issues continue; (i.e. the withholdings continue and the 20% penalty can increase). This continues for the remainder of the 10 year stock option award term unless the options are exercised. Slide 13 will indicate which grants are impacted. The Company is allowed to “cure” the discounted options through repricing. Tendered options which are repriced are NOT subject to adverse personal income tax consequences. |

12 Tender Offer IRC 409A Background Certain Stock Options that are granted at a discount are subject to IRC 409A. (see chart on next page) 409A says that income created from “discounted options” is considered wages for individual tax purposes. Therefore, withholdings (FIT, SIT, FICA) need to be paid on the deferred income. |

13 Tender Offer IRC 409A 409A Exposure - by year Grant Year 2004 2005 2006 2007 2008 2009 2003 NO YES YES 2004 YES YES YES 2005 YES YES YES 2006 YES YES YES 2007 December 31, 2006 409A tax issue December 31, 2007 409A tax issue December 31, 2008 409A tax issue December 31, 2009 409A tax issue N/A Vesting Year |

14 Discounted Option continued Using a specific example from 2005, we intended for a grant to be done on January 5, 2005 when the stock price was $29.70. The final approvals from the compensation committee were not received until February 8, 2005 when the stock price was $33.92. Therefore the 2005 option above was issued at a $4.22 discount. |

15 Discounted Options What’s wrong with discounted options? Primarily unfavorable tax issues 409A Lose Incentive Stock Option treatment – the options become non-qualified options 409A is a section of the Internal Revenue Code that treats discounted stock options that vest in 2005, 2006, 2007, and later years with a 20% penalty. |

16 Can we fix discounted options? Yes, with a tender offer. Fixes unexercised options subject to 409A for “rank and file” only. The tender offer takes the option and ‘re-prices’ it to the correct accounting price-only for (2/3) of 2003 and 2004 through 2006 grant years. Vesting and maturity remain as it was. This cures the 409A problem, but the option is still a non-qualified option. |

17 Specific Example Remember the example before of a discount of $4.22, we would re-price the 2005 stock option from $29.70 to $33.92. |

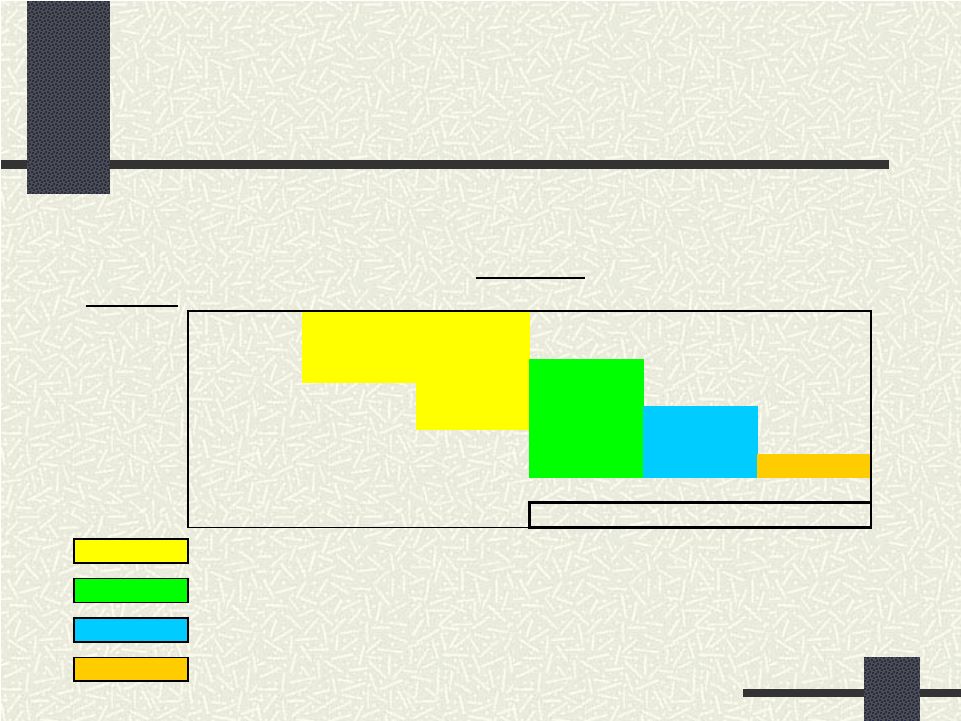

18 So can you put this in simple terms? We’ll try. Tender Offer Grant Strike Price Strike Price Difference Grant Date January 5, 2005 29.70 $ New Date February 8, 2005 33.92 $ 4.22 $ |

19 Tender Offer Re-price the option from $29.70 to $33.92 which decreases the income that you receive when you exercise. So, we’ll give you the difference of $4.22 in early 2008 to compensate you for the loss of income. We will also gross up for Medicare but not FIT and SIT. All options will be NQO’s. Covers options issued 2003, 2004, 2005 and 2006. |

20 Tender Offer What happens if I don’t accept the re-pricing? Your unexercised options will be subject to IRS rules which impose a 20% penalty. The penalty is in addition to any “normal” capital gain income tax . The penalty is not tax deductible. The next slide is an example of what could happen. If you participate, it is important that your acceptance is received by December 6, 2007. This is a one time offer. |

21 409A Ramifications Assume 1,000 options granted in 2005 with new data of February 8. 2006 vested, unexercised as of 12/31/2006 @ $ 30.625 409A penalty 61.79 2007 vesting est 409A penalty @ $ 34.00 11/2/2007 511.83 2008 vesting est 409A penalty @ $40 1,486.38 409A Penalty for 2005 Grant 2,060.00 |

22 409A Ramifications Repriced vs. Not Repriced Assume exercise in December 2008 at $40 If not repriced: Proceeds - 1000 shares x ($40-29.70) 10,300.00 assume taxes - use 30% 3,100.00 Net gain before 409A penalties 7,200.00 409A penalties - payable 2009 2,060.00 Net gain after 409A penalties 5,140.00 $ If repriced: 2008 bonus 1000 x $4.22 - paid in Jan 2008 4,220.00 taxes @ 30% 1,266.00 2008 Exercise 1000 x ($40-33.92) - exercise Dec 2008 6,080.00 assumed taxes @ 30% 1,834.00 Net gain after considering 409A 7,200.00 $ |

23 409A From the previous slide you can see that the IRS penalty is punitive. As the stock price climbs, the penalty climbs as well. Even if you do not exercise the options, you may owe the 409A penalty. |

24 Tender Offer So you have two possibilities with options that are subject to 409A Accept the tender offer and the bonus which makes you roughly even as before OR Accept the options as they are today and likely be subject to the penalty. |

25 Tender Offer Timing Tender offer launched November 7, 2007. Employees respond by 11:59PM on December 6, 2007. Tender offer expires December 6, 2007. Employees who tendered options receive cash bonus for “discount” in January 2008. |

26 Tender Offer Questions |