UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08360

GUINNESS ATKINSON FUNDS

(Exact name of registrant as specified in charter)

251 South Lake Avenue, Suite 800

Pasadena, CA 91101

(Address of principal executive offices) (Zip code)

(Name and address of agent for service)

James J. Atkinson, Jr.

251 South Lake Avenue, Suite 800

Pasadena, CA 91101

Registrant’s telephone number, including area code: (800-915-6566)

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Item 1. Reports to Stockholders.

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Guinness Atkinson™ Funds

Annual Report

December 31, 2021

TABLE OF CONTENTS

| 3 | | Letter to Shareholders |

| 6 | | Expense Examples |

| 8 | | Alternative Energy Fund |

| 20 | | Asia Focus Fund |

| 22 | | China & Hong Kong Fund |

| 40 | | Global Energy Fund |

| 51 | | Global Innovators Fund |

| 60 | | Renminbi Yuan & Bond Fund |

| 66 | | Statements of Assets and Liabilities |

| 68 | | Statements of Operations |

| 70 | | Statements of Changes in Net Assets |

| 75 | | Financial Highlights |

| 82 | | Notes to Financial Statements |

| 93 | | Report of Independent Registered Public Accounting Firm |

| 96 | | Liquidity Risk Management Program |

| 97 | | Trustee and Officer Information |

| 99 | | Privacy Notice |

| 100 | | Guinness Atkinson Funds Information |

Dear Guinness Atkinson Funds Shareholders,

Like everyone else, we’re waiting for things to return to normal. Whatever that is. It’s difficult to argue that the world has changed dramatically in the last few years, but in fact, it’s been experiencing dramatic change for the last several decades. Although we won’t argue the point that it has really seen dramatic change in the last 24 plus months. Despite the upheaval, the markets delivered solid returns.

The year was another good one for most of the Guinness Atkinson Funds. Of the six GA Funds, four produced positive returns for the year with the Global Energy Fund leading the way with a 45.98% total return for the 12 months ending December 31, 2021.

The Global Innovators Fund enjoyed another good year with the Investor Class return of 21.52% and the Institutional Class returning 21.86% for the year.

The Alternative Energy Fund returned 8.40% for the year while the Renminbi Yuan & Bond Fund provided a total return of 3.00%.

The two GA Funds that experienced negative returns for the year are the Asia Focus Fund, down 6.32% and the China & Hong Kong Fund which was down 6.70%.

Two of the Guinness Atkinson Funds converted to exchange traded funds (ETFs) during the year. The Dividend Builder Fund is now the SmartETFs Dividend Builder ETF (DIVS) and the Asia Pacific Dividend Builder Fund is now the SmartETFs Asia Pacific Dividend Builder ETF (ADIV). These two Funds are still part of the Guinness Atkinson Funds Trust and are still managed by Guinness Atkinson.

We encourage you to check out SmartETFs. In addition to DIVS and ADIV, SmartETFs includes the SmartETFs Smart Transportation & Technology ETF (MOTO), SmartETFs Sustainable Energy II ETF (SOLR, a twin of the Alternative Energy Fund) and SmartETFs Advertising & Marketing Technology ETF (MRAD). For more information, please visit www.smartetfs.com.

Consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For a prospectus or summary prospectus with this and other information, please call (866) 307-5990 or visit our website at www.SmartETFs.com. Read the prospectus or summary prospectus carefully before investing.

Investing involves risk including the loss of principal.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

Shares of the SmartETFs Funds are distributed by Foreside Fund Services, LLC.

Throughout this report are detailed commentaries on each of the Guinness Atkinson Funds prepared by our portfolio managers.

As usual, we appreciate the confidence you have placed in us and our management team and look ahead to what we hope is a great 2022.

We encourage you to visit gafunds.com for the latest news and announcements on the Guinness Atkinson Funds.

Sincerely,

| Timothy Guinness | James Atkinson |

The table below provides total return data for each of the Funds over the one, three, five, ten-year and since inception periods through December 31, 2021. Also included in the table is the expense ratio data from the most recent prospectus dated May 1, 2021.

| Fund (inception date) | 1-year | 3-year | 5-year | 10-year | Since Inception | Expense Ratio |

Alternative Energy Fund (March 31, 2006) | 8.40% | 38.06% | 21.83% | 8.75% | -3.03% | 2.46% gross; 1.98% net |

Asia Focus Fund (April 29, 1996) | -6.32% | 15.08% | 12.27% | 6.19% | 4.03% | 2.21% gross; 1.98% net |

China & Hong Kong Fund (June 30, 1994) | -6.70% | 11.58% | 10.53% | 6.48% | 7.06% | 1.60% |

Global Energy Fund (June 30, 2004) | 45.98% | 1.97% | -3.19% | -2.00% | 4.32% | 2.56% gross; 1.46% net |

Global Innovators Fund Investor Class (December 15, 1998) | 21.52% | 31.36% | 20.51% | 18.13% | 9.74% | 1.24% gross; 1.24% net |

Global Innovators Fund Institutional Class (December 31, 2015) | 21.86% | 31.69% | 20.81% | 18.31% | 9.81% | 1.07% gross; 0.99% net |

Renminbi Yuan & Bond Fund (June 30, 2011) | 3.00% | 5.16% | 4.56% | 2.28% | 2.19% | 5.26% gross; 0.91% net |

Periods of greater than one year are average annualized returns; one year and shorter period returns are actual returns. All returns are for the periods ending December 31, 2021.

Performance data shown for the Global Innovators, Institutional Class (GINNX), prior to its launch date on December 31, 2015, uses performance data from the Global Innovators, Investor Class (IWIRX).

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Each of the Asia Focus Fund, t, the China & Hong Kong Fund, and the Renminbi Yuan & Bond Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect this fee. If it had, total return would be lower.

Expense ratios are from the most recent prospectus (dated May 1, 2021) and are from the most recent audited financials (period ending December 31, 2020) at the time that prospectus was completed.

The Adviser has contractually agreed to reduce its fees and/or pay Fund expenses in order to limit the Fund’s Total Annual Operating Expenses to through June 30,2025. Total returns reflect a fee waiver in effect & in the absence of this waiver, the total returns would be lower.

Morningstar Ratings Through December 31, 2021

| Fund | Category | Overall | 3-Year | 5-Year | 10-Year |

| Alternative Energy | Foreign Small/Mid Value | 3 ««« (139 funds) | 5 «««««

(139 funds) | 4 «««« (105 funds) | 1 « (70 funds) |

| Asia Focus | Pacific/Asia ex-Japan | 2 «« (52 funds) | 3 ««« (52 funds) | 3 ««« (45 funds) | 1 « (32 funds) |

| China & Hong Kong | China Region | 3 ««« (95 funds) | 3 ««« (95 funds) | 3 ««« (72 funds) | 3 ««« (53 funds) |

| Global Energy | Energy Equity | 4 «««« (69 funds) | 4 «««« (66 funds) | 4 «««« (68 funds) | 3 ««« (51 funds) |

| Global Innovators Investor Class | Large Growth | 3 ««« (1,116 funds) | 3 ««« (1,116 funds) | 2 «« (1,012 funds) | 3 ««« (768 funds) |

| Global Innovators Institutional Class | Large Growth | 3 ««« (1,116 funds) | 3 ««« (1,116 funds) | 2 «« (1,012 funds) | 3 ««« (768 funds) |

| Renminbi Yuan & Bond | Emerging Markets Local Currency Bond | 5 ««««« (73 funds) | 5 ««««« (73 funds) | 5 ««««« (69 funds) | 5 ««««« (52 funds) |

Morningstar Ratings Disclosure

Global Innovators Fund ratings shown were given for the Investor Share Class.

For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in distribution percentages.)

© 2022 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar (2) may not be copied or distributed and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

GUINNESS ATKINSON FUNDS

Expense Examples (Unaudited)

As a shareholder of the Funds, you incur two types of costs: (1) redemption fees (applicable to the Asia Focus Fund, the Asia Pacific Dividend Builder Fund, the China & Hong Kong Fund, and the Renminbi Yuan & Bond Fund); and (2) ongoing costs, including advisory fees and other Fund expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period shown and held for the entire period from July 1, 2021 to December 31, 2021.

Actual Expenses

For each Fund, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid during Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each Fund, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any redemption fees. Therefore, the second line for each Fund of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these redemption fees were included, your costs would have been higher.

| | | Beginning Account Value (07/01/21) | | | Ending Account Value (12/31/21) | | | Expenses Paid During Period* (07/01/21 to 12/31/21) | | | Expense Ratios During Period* (07/01/21 to 12/31/21) | |

| Guinness Atkinson Alternative Energy Fund Actual | | $ | 1,000.00 | | | $ | 1,024.40 | | | $ | 10.10 | | | | 1.98 | %† |

| Guinness Atkinson Alternative Energy Fund Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.22 | | | $ | 10.06 | | | | 1.98 | %† |

| Guinness Atkinson Asia Focus Fund Actual | | $ | 1,000.00 | | | $ | 909.90 | | | $ | 9.53 | | | | 1.98 | %† |

| Guinness Atkinson Asia Focus Fund Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.22 | | | $ | 10.06 | | | | 1.98 | %† |

| Guinness Atkinson China & Hong Kong Fund Actual | | $ | 1,000.00 | | | $ | 893.70 | | | $ | 7.16 | | | | 1.49 | % |

| Guinness Atkinson China & Hong Kong Fund Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.64 | | | $ | 7.63 | | | | 1.49 | % |

| Guinness Atkinson Global Energy Fund Actual | | $ | 1,000.00 | | | $ | 1,077.80 | | | $ | 7.65 | | | | 1.46 | %† |

| Guinness Atkinson Global Energy Fund Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.85 | | | $ | 7.43 | | | | 1.45 | %† |

| Guinness Atkinson Global Innovators Fund – Investor Class Actual | | $ | 1,000.00 | | | $ | 1,062.20 | | | $ | 6.45 | | | | 1.24 | %† |

| Guinness Atkinson Global Innovators Fund – Investor Class Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,018.95 | | | $ | 6.31 | | | | 1.24 | %† |

| Guinness Atkinson Global Innovators Fund – Institutional Class Actual | | $ | 1,000.00 | | | $ | 1,063.80 | | | $ | 5.15 | | | | 0.99 | %† |

| Guinness Atkinson Global Innovators Fund – Institutional Class Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.21 | | | $ | 5.04 | | | | 0.99 | %† |

| Guinness Atkinson Renminbi Yuan & Bond Fund Actual | | $ | 1,000.00 | | | $ | 1,012.10 | | | $ | 4.56 | | | | 0.90 | %† |

| Guinness Atkinson Renminbi Yuan & Bond Fund Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.67 | | | $ | 4.58 | | | | 0.90 | %† |

GUINNESS ATKINSON FUNDS

Expense Examples (Unaudited)

| * | Expenses are equal to the Funds’ annualized expense ratio as indicated, multiplied by the average account value over the period, multiplied by the number of days in most recent fiscal half-year period (184), then divided by the number of days in the fiscal year (365) (to reflect the one-half year period). |

| † | Net of fee waivers and expenses absorbed/recaptured. If those fee waivers and expenses absorbed/recaptured had not been in effect, the Fund’s actual expenses would have been higher/lower. |

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

| Average annualized Total returns | 1 Year | 3 Years | 5 Years | 10 Years |

| Fund | 8.40% | 38.06% | 21.83% | 8.75% |

| Benchmark Index: | | | | |

| MSCI World Index (Net Return) | 21.82% | 21.68% | 15.01% | 12.68% |

Gross 2.46% & Net 1.98%. The Adviser has contractually agreed to reduce its fees and/or pay Fund expenses in order to limit the Fund’s Total Annual Operating Expenses to 1.98% through June 30, 2025.

For the Fund’s current one-year expense ratios, please refer to the Financial Highlights section of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 915-6565.

The Guinness Atkinson Alternative Energy Fund is positioned to benefit from the many opportunities associated with the sustainable energy transition that we have discussed. As part of our investment process, we have identified a universe of around 250 companies (market capitalisation of over USD$500m) that are most directly exposed to the theme, and classify them into the following four sub-sectors:

| · | Displacement includes companies involved in the displacement or more efficient usage of existing hydrocarbon-based energy |

| · | Electrification includes companies involved specifically in the switching of hydrocarbon-based fuel demand towards electricity, especially for electric vehicles |

| · | Generation includes companies involved in the generation of sustainable energy, either pureplay companies or those transitioning from hydrocarbon-based fuels |

| · | Installation (Equipment) includes companies involved in the manufacturing of equipment for the generation and consumption of sustainable energy |

Sustainable Energy equities delivered a positive return in 2021 with the Guinness Atkinson Alternative Energy fund delivering 8.40% return in USD terms while the MSCI World Net Return index delivered 21.82%.

The largest positive contributors to the fund in 2021 were our two Chinese generation companies (independent power producers) China Longyuan and China Suntien. At the start of the year, China Longyuan announced a corporate transaction with its parent company CNH Energy and its sister company Pingzhuang Energy that provided China Longyuan with a China A share listing while China Suntien’s share price increase reflected strong profit growth resulting from the start-up of new wind projects. Their strong performance was sustained through the third quarter of 2021 as the Chinese economy rebounded strongly and warm weather increased air conditioning demand, driving higher electricity prices and better margins for both.

Within electrification, Onsemi enjoyed numerous earnings upgrades through the year, as demand and pricing for its semiconductor products both rose. The company announced plans to prune both its revenue base and manufacturing footprint to invest in high-value, high-growth applications served by its power and sensing-biased semiconductor portfolio. Growth will be sacrificed in the 2022/2023 period while it focuses on higher margin businesses. Also within electrification, Gentherm delivered strong results and good new contract awards, including a first production vehicle award for its new “ClimateSense” product which combines several individual product lines (such as thermal products, electronics and software) into a system solution.

With displacement, Nibe Industrier was the greatest contributor, with the shares reacting to strong demand for heat pumps, solid underlying business performance and a share split that increased accessibility of its shares. Of particular note was the company’s North American Climate Solutions business returning to growth and signs that Nibe’s decentralised business model was providing good insulation against raw material cost inflation. Ameresco and Hubbell also delivered strong contribution over the year.

The equipment (installation) sector was the weakest contributor with only three companies delivering a positive contribution over the year. Of note was Schneider Electric, whose shares reacted positively to consistent improvements in business performance, and polysilicon manufacturer Daqo New Energy which delivered a significant contribution to the fund during the first quarter of the year (prior to its sale from the portfolio) as a result of strong polysilicon demand and rising polysilicon prices.

While the strongest performers came from all four sub sectors, the weaker performers came predominantly from the equipment (installation) sector. Siemens Gamesa, TPI Composites and Vestas Wind Systems suffered from slowing momentum within the near-term wind macro environment (compounded by supply chain pressures and raw material inflationary concerns) that trumped longer-term positive wind industry developments.

Other weak contributors included LG Chem whose shares were weak following a $1.9 billion product recall with GM regarding battery faults on the Chevrolet Bolt, and two generation companies, Albioma and Iberdrola, which de-rated as a result of general market concerns around rising interest rates and the risk of greater regulation to compensate for higher fossil fuel prices.

2021 individual stock contribution, in USD

source: Bloomberg, Guinness Atkinson Asset Management estimates

In terms of attribution relative to the Guinness sustainable energy universe, the fund delivered positive sector allocation and stock selection within efficiency (due to a small sector overweight and advantaged stock selection as described above); electric vehicles (due to a bias towards power semiconductors and electronics and avoidance of recently listed US Special Purpose Acquisition Companies (SPACs)); within independent power producers (IPPs) (due to exposure to Chinese wind-dominated IPPs and the avoidance of US residential solar and pure-play high-growth solar IPPs that were weaker as a result of rising interest rate concerns); and within other equipment (due to avoidance of weak hydrogen fuel cell and electrolyser companies as well as newly listed energy storage stocks).

The fund delivered negative sector allocation and stock selection within batteries (due to lack of exposure to battery raw material companies as well as pure-play cathode and anode manufacturers); and within solar and wind equipment (where we held overweight positions to sectors and manufacturing companies that suffered from raw material cost inflation and supply chain issues).

Early in the year, we sold Daqo New Energy and replaced the holding with a position in Infineon Technologies. We also added Eaton towards the end of the year.

| · | Daqo is a fast growing, low cost, China based manufacturer of polysilicon, whose shares increased by more than eight times since the start of 2019. While underlying profitability has increased at Daqo, we are concerned that the share price now fully reflects a very optimistic outlook for long term polysilicon pricing and company growth. |

| · | Infineon Technologies designs, manufactures, and markets semiconductors with a focus on the automotive, industrial power control, power management and digital security markets. Having recently acquired Cypress Semi, we believe that Infineon is very well placed to benefit from the industry’s need for greater semiconductor (especially power semiconductor) content in electric vehicles. |

| · | Eaton is a US listed, $65 billionn market capitalisation specialized producer of highly engineered products and services. These offerings are designed to solve customer pain points in vital portions of the world’s infrastructure. We believe Eaton has mostly positioned its portfolio in profitable niches that should benefit from secular trends like energy transition and electrification, to propel long-term growth. |

The sector and geographic weightings of the portfolio at December 31, 2021 were as follows:

| Sector breakdown | Dec. 31, 2021 |

| Displacement | |

| Efficiency | 11.9% |

| Electrification | |

| Battery | 8.7% |

| Electric vehicles | 24.6% |

| Generation | |

| IPP | 16.0% |

| Utility | 8.4% |

| Installation | |

| Equipment | 27.5% |

| Cash | 2.9% |

| Total | 100% |

| Geographic breakdown | Dec 31, 2021 |

| USA | 39.0% |

| China | 9.9% |

| Germany | 7.9% |

| France | 6.6% |

| Spain | 6.6% |

| South Korea | 6.0% |

| Canada | 6.0% |

| Sweden | 4.1% |

| Ireland | 4.1% |

| Denmark | 2.7% |

| UK | 2.4% |

| Israel | 1.8% |

| Cash | 2.9% |

The year of 2021 saw continued positive momentum for the energy transition. Policy commitments and investments were made to accelerate the decarbonisation of the global energy sector. Offsetting this, we saw raw material cost inflation, supply chain issues and some political tensions which have slowed the pace of growth and profitability in certain subsectors. Against this backdrop, our portfolio has seen improved cash return expectations versus twelve months ago. It continues to offer broad exposure to companies that are well placed to benefit from an energy transition that will gather pace through the remainder of this decade.

After very strong policy support in 2020, we witnessed further policy commitment in 2021. The most significant policy milestones last year included:

| · | President Biden returning the US to the Paris Agreement, and announcing significantly increased 2030 GHG reduction targets; |

| · | the influential 2021 Intergovernmental Panel on Climate Change (IPCC) climate report, which highlighted the importance and urgency of pursuing a 1.5° warming or net zero 2050 scenario; |

| · | the Conference of the Parties(COP)15 Biological Diversity Conference, at which President Xi gave more clarity on how China would meet its climate targets over the coming years, including a major expansion in solar; and |

| · | and the Conference of the Parties(COP)26 climate conference, which introduced new net zero targets, additional country pledges and some “alliances of the willing” to reduce coal usage and methane emissions. |

In addition to enhanced policy commitment, 2021 saw major steps forward for various aspects of the transition. We saw around 290 gigawatts (GW) of new renewable generation capacity installed, 10 GW higher than the record installations seen in 2020 and nearly 100 GW higher than the 194 GW installed in 2019. Solar represented nearly two-thirds of the new capacity additions, followed by wind then hydro. Renewable electricity generation increased by around 6% to over 7,900 TWh, outpacing global electricity demand growth (4.5% in 2021). Electric vehicle sales surged, reaching around 7% of global light auto sales, up from just over 3% in 2020. Sales were particularly strong in China and Europe. And investment into energy efficiency also accelerated, with building infrastructure remaining a key focus for spending.

2021 was also a year in which the complexities of a shift to a lower carbon economy become more evident.

In Europe, record natural gas prices became a major political headache, forcing governments to seek protection for consumers from the extreme price spike. On the one hand, observers could point to extraordinarily high post-pandemic power demand, plus the tactics of President Putin to withhold gas exports into Europe, as reasons for the extreme prices. But on the other hand, the spike has been driven by an attempt to shift away from carbon intensive coal usage in China, and the impact of a rapidly rising carbon price in Europe, which is affecting the behaviour of utilities.

In the US, Democratic Senator Joe Manchin has blocked the path of the “Build Back Better” (BBB) bill, a cornerstone spending plan of the current administration which includes various clean energy related provisions designed to accelerate the transition. Manchin represents West Virginia, a major coal producing state, and claims the bill will “risk the reliability of our electric grid and increase our dependence on foreign supply chains”.

After many years of consistent cost reductions, 2021 also saw the emergence of inflationary conditions and supply chain pressures across the breadth of the sustainable energy sector. Energy transition technologies and equipment are typically raw material intensive (leaving them exposed to raw material inflation) and are dominated by Chinese manufacturing (50% of all wind turbines and 70% of all solar panels are manufactured in China), leaving importers exposed to supply chain inefficiencies and higher freight costs.

Natural gas prices will moderate; there will be a resolution to Manchin’s opposition to BBB, and most areas of raw material inflation will settle down and be trumped by scale and technological improvements. But the world is waking up to the fact that although the energy transition will result in economic and environmental gains, policy decisions have the potential in the short-term to cause economic and political friction.

Against this backdrop, the Guinness Atkinson Alternative Energy Fund has seen improved cash return expectations and delivered a total return (USD) of +8.4% vs the MSCI World Index (net return) of +21.8%. Within the portfolio, outperforming sectors included Chinese wind generation, EV component suppliers, poly-silicon (for solar) and efficiency. Underperforming sectors included European green utilities, solar component manufacturers and wind developers.

Looking ahead to 2022 and beyond, we expect further acceleration of the transition:

| · | On the supply side of the energy transition, the International Energy Agency (IEA) is forecasting that renewable power additions over the coming five years will be just over 1,800 GW; a near 50% increase on its previous five-year forecast published twelve months earlier. The increase is driven by a further reduction in the levelized cost of electricity for renewables. |

| · | The IEA has described solar power as “the cheapest electricity in history” and, despite near term headwinds and cyclical cost inflationary factors, large-scale solar remains at the bottom end of the cost curve. Globally, we expect solar installations to grow in 2022 by over 20%, led by China, India, Middle East and other parts of Asia. It is likely that poly-silicon prices have peaked, bringing cost relief for cell and module manufacturers. The outlook for solar in the US this year is less certain due to various issues (stimulus spending, net metering and Chinese import issues). |

| · | Global wind installations are expected to be around flat in 2022, as changes in tax incentives, COVID-related logistics issues and raw material cost inflation are worked through. Onshore installations should pick up meaningfully in the middle of the decade, and there is clear momentum in offshore wind, albeit with a 3-4 year lead time. President Biden has recently called for the US to have 30 GW of offshore wind by 2030 (current installed base = <1 GW), which would represent a step change for the industry. |

| · | Energy efficiency will continue to receive a good proportion of post-COVID stimulus spending, with a continued focus on buildings. We expect an acceleration in the penetration of LED lighting, insulation and heat pumps, as well as a focus on grid and transmission upgrades. The IEA estimates that to meet current government policies, energy efficiency spending needs to increase from a recent average level of around $250bn per annum to around $375bn this decade and nearly $550bn in the 2030s. |

| · | EV sales should exceed 9 million in 2022, representing around 10% of total passenger vehicle sales, taking the global EV stock from 16 million vehicles to 25 million vehicles. Lower EV prices, greater brand choice and growing consumer appetite continue to be the key drivers of improved EV sales. |

| · | Battery demand for use in EVs and energy storage will accelerate in 2022. We expect new battery capacity of nearly 300 GWh to be sold this year, up by around 25% versus 2021. Raw material cost inflation will continue to have an impact in 2022, but rapidly increasingly manufacturing capacity, coupled with technological improvements, will continue to push average battery pack costs towards $100/kWh, the level at which mass market EVs become affordable. |

The outlook we summarise here is broadly consistent with current government activity and observable investment plans. To be clear, however, the growth described falls well short of the energy transition activity needed to achieve a net zero / 1.5 degree scenario in 2050, as targeted by the IPCC and at COP26. In a net zero scenario, the deployment of renewable generation capacity, penetration of EVs and battery storage, use of alternative fuels and implementation of energy efficiency measures will need to accelerate markedly.

At December 31, 2021, the Guinness Atkinson Alternative Energy Fund traded on a 2022 Price Earnings (P/E) ratio of 24.5x and 2022 Enterprise Value to Earning Before Interest, Taxes, Depreciation, and Amortization (EV/EBITDA) multiple of 13.2x. The fund trades at about a 20% premium to the MSCI World Index, which we see as justified given the attractive growth rates available to invest in across the sector. As a sense check, consensus EPS growth (2021-2023E) of the portfolio (at 21.3%pa) is well ahead of the MSCI World (at 13.5%pa). Looking over the next five years, we believe that the portfolio is likely to deliver average earnings growth.

Portfolio managers

Jonathan Waghorn and Will Riley

January 2022

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. These risks are greater for emerging markets. The Fund’s focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund’s assets were diversified among various sectors. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. Net Return reflects deduction for withholding tax but reflects no deduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay. This index is unmanaged, not available for investment and does not incur expenses.

P/E – Price to Earnings ratio is calculated by dividing current price of the stock by the company's trailing twelve months' earnings per share.

EV/EBITDA - The enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio is calculated by dividing EV by EBITDA or earnings before interest, taxes, depreciation, and amortization.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

Alternative Energy Fund

Growth of $10,000 (Unaudited)

Average Annual Total Return

Periods Ended December 31, 2021

| One Year | | Five Years | | Ten Years |

| 8.40% | | 21.83% | | 8.75% |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. Net Return reflects deduction for withholding tax but reflects no deduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay.

FUND HIGHLIGHTS at December 31, 2021

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

| # of Holdings in Portfolio: | | | 31 | |

| Portfolio Turnover: | | | 29.0 | % |

| % of Stocks in Top 10: | | | 42.4 | % |

| Fund Managers: |

| Will Riley |

| Jonathan Waghorn |

| Top 10 Holdings (% of net assets) | | | |

| Nextera Energy Inc. | | | 4.5 | % |

| Schneider Electric SE | | | 4.4 | % |

| Nibe Industrier AB - B Shares | | | 4.4 | % |

| Infineon Technologies AG | | | 4.3 | % |

| ON Semiconductor Corp | | | 4.3 | % |

| Sensata Technologies Holding | | | 4.1 | % |

| China Longyuan Power Group Corp, - H Shares | | | 4.1 | % |

| Gentherm Inc. | | | 4.1 | % |

| Iberdrola SA | | | 4.1 | % |

| APTIV PLC | | | 4.1 | % |

| Geographic Breakdown (% of net assets) |

| United States | | | 38.7 | % |

| China | | | 10.4 | % |

| Spain | | | 9.8 | % |

| Germany | | | 8.4 | % |

| France | | | 7.0 | % |

| Canada | | | 6.1 | % |

| Sweden | | | 4.4 | % |

| Ireland | | | 4.1 | % |

| South Korea | | | 3.5 | % |

| Denmark | | | 2.9 | % |

| United Kingdom | | | 2.6 | % |

| Israel | | | 1.7 | % |

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 99.6% | | Value | |

| | | | | | | |

| | | | | Electrification: 41.1% | | | | |

| | 7,930 | | | APTIV PLC | | $ | 1,308,054 | |

| | 15,150 | | | Gentherm Inc.* | | | 1,316,535 | |

| | 19,210 | | | Hella GmbH & Co. KGaA | | | 1,302,628 | |

| | 30,220 | | | Infineon Technologies AG | | | 1,401,443 | |

| | 11,950 | | | Itron Inc.* | | | 818,814 | |

| | 29,720 | | | Johnson Matthey PLC | | | 822,599 | |

| | 1,760 | | | LG Chem Ltd. | | | 910,460 | |

| | 20,370 | | | ON Semiconductor Corp.* | | | 1,383,530 | |

| | 2,070 | | | Samsung SDI Co., Ltd. | | | 1,140,472 | |

| | 7,180 | | | Schneider Electric SE | | | 1,408,834 | |

| | 21,360 | | | Sensata Technologies Holding* | | | 1,317,698 | |

| | 80,000 | | | Tianneng Power International | | | 84,653 | |

| | | | | | | | 13,215,720 | |

| | | | | | | | | |

| | | | | Energy Efficiency: 12.1% | | | | |

| | 15,460 | | | Ameresco PLC* | | | 1,259,062 | |

| | 5,900 | | | Hubbell Inc. | | | 1,228,793 | |

| | 93,140 | | | Nibe Industrier AB - B Shares | | | 1,408,146 | |

| | | | | | | | 3,896,001 | |

| | | | | | | | | |

| | | | | Renewable Energy Generation: 28.0% | | | | |

| | 21,790 | | | Albioma SA | | | 849,855 | |

| | 564,000 | | | China Longyuan Power Group Corp. - H Shares | | | 1,316,591 | |

| | 1,362,000 | | | China Suntien Green Energy Corp. Ltd. - H Shares | | | 1,062,138 | |

| | 110,450 | | | Iberdrola SA | | | 1,308,167 | |

| | 15,480 | | | Nextera Energy Inc. | | | 1,445,213 | |

| | 11,369 | | | Ormat Technologies Inc. | | | 901,562 | |

| | 38,640 | | | Siemens Gamesa Renewable Energy SA | | | 926,293 | |

| | 78,900 | | | TransAlta Renewables Inc. | | | 1,169,883 | |

| | | | | | | | 8,979,702 | |

| | | | | Renewal Equipment Manufacturing: 18.4% | | | | |

| | 25,150 | | | Canadian Solar Inc.* | | | 786,944 | |

| | 4,700 | | | Eaton Corp PLC | | | 812,254 | |

| | 3,350 | | | Enphase Energy Inc.* | | | 612,849 | |

| | 12,910 | | | First Solar Inc.* | | | 1,125,236 | |

| | 2,000 | | | Solaredge Technologies Inc.* | | | 561,140 | |

| | 14,510 | | | TPI Composites Inc.* | | | 217,070 | |

| | 30,165 | | | Vestas Wind Systems A/S | | | 922,886 | |

| | 530,200 | | | Xinyi Solar Holdings Ltd. | | | 899,024 | |

| | | | | | | | 5,937,403 | |

The accompanying notes are an integral part of these financial statements.

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 99.6% | | Value | |

| | | | | Total Common Stocks | | $ | 32,028,826 | |

| | | | | (cost $26,882,246) | | | | |

| | | | | | | | | |

| | | | | Total Investments in Securities | | | 32,028,826 | |

| | | | | (cost $26,882,246): 99.6% | | | | |

| | | | | | | | | |

| | | | | Other Assets less Liabilities: 0.4% | | | 145,116 | |

| | | | | | | | | |

| | | | | Net Assets: 100.0% | | $ | 32,173,942 | |

| * | Non-income producing security. |

PLC - Public Limited Company

The accompanying notes are an integral part of these financial statements.

GUINNESS ATKINSON ASIA FOCUS FUND

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

| Average annualized Total returns | 1 Year | 3 Years | 5 Years | 10 Years |

| Fund | -6.32% | 15.08% | 12.27% | 6.19% |

| Benchmark Index: | | | | |

| MSCI AC Far East Free ex japan index (net return) | -8.42% | 11.29% | 10.71% | 7.63% |

(All performance data given in USD terms)

Gross 2.21% & Net 1.98%; The Adviser has contractually agreed to reduce its fees and/or pay Fund expenses in order to limit the Fund’s Total Annual Operating Expenses to 1.98% through June 30, 2025.

For the Fund’s current one-year expense ratio, please refer to the Financial Highlights section of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 915-6565.

The Fund fell -6.32% in 2021 compared to the benchmark which fell -8.42%.

Macro challenges for all markets, Asian and Developed, have intensified in 2021. Consumer price inflation in the US has continued to climb and the market now expects that the Federal Reserve will need to raise interest rates by more than anticipated. The effect of this has been most keenly felt by growth stocks for whom rising interest rates reduce the value of future earnings in today’s money bringing stock valuations down along with it. The second set of challenges emerged during the third quarter in China with the imposition of tighter polices on the operations of the e-commerce giants and restrictions on debt accumulation by the privately-owned real estate developers. This has had a destabilising effect on investor sentiment and has sent a chill through the housing market as companies seek to raise cash to meet near-term debt obligations; however, in our view it probably contributes on balance, to the long-term stability of China’s economic growth.

The Fund, held up better than the market despite its heavy exposure to China and the consumer discretionary sector which, at the index level, were significant underperformers during the period. However, with its bias toward higher growth stocks the Fund has been affected by a rotation toward value stocks. Relative performance was undoubtedly helped by its more modest exposure (than index and peers) to Chinse e-commerce and technology names like Alibaba and Tencent. Our equal-weighting approach, in more volatile times works more in our favour. But more positively we saw positive outperformance from Chinese names like NetEase and Ping An Insurance and there strong contributions from Mainland-listed companies including Nari Technology (electricity transmission equipment), Inner Mongolia Yili (dairy), Wuxi Lead Intelligent (capital equipment for EV battery makers) and Venustech (cyber security software).

At the forefront of performance were technology manufacturers and chip designers listed in either Taiwan or the US. Broadcom designs chips and provides software services whilst Applied Materials makes and services capital equipment used by the semiconductor manufacturers. Novatek Microelectronics reported a tripling of earnings as its chip designs for screen controllers have application in handheld devices, cars, appliances and televisions. Elite Material is another success story with is specialised laminates being used not only in smartphones but now also in infrastructure equipment such as Intel’s new servers and for switches being used in data centres.

At the other end, Autohome was the weakest performer over the year. Slower car sales have reduced both advertising and commission revenues, but we have also seen competition emerge from other search engine companies like Baidu. There have been management changes to try and address the challenges and we shall look for evidence of their effectiveness in the course of 2022. Sany Heavy is a mainland China listed maker of construction equipment whose share price fell along with slowdown in construction activity in the second half of the year. We believe earnings are forecast by the consensus to grow over the next two years with the scope for upgrades to forecasts if, as we believe, activity stabilises and then picks up again.

We sold four stocks: New Oriental Education, Beijing Oriental Yuhong Waterproof Co., KT&G and Catcher Technology. We sold New Oriental Education after changes in the regulatory environment meant its prospects for growth fell significantly. We sold Yuhong, which is a manufacturer of waterproofing materials used in the construction industry. We believe its share price did not fully reflect the company’s exposure to Evergrande, and therefore took profit on the stock. We still like the company and it remains on our watchlist as Yuhong’s balance sheet is strong enough to weather a weaker year. KT&G and Catcher were sold as these companies are now considered as low growth companies.

We bought Applied Materials, Broadcom, LG Household & Health, and China Medical System. Applied Materials and Broadcom derive more than 50% of their revenue from Asia and so are eligible for the Fund. LG Household Healthcare is a Korean company with exposure to cosmetics, drinks and personal products. China Medical System sells generic drugs on behalf of other companies and is moving into drug development itself.

At a country level the Fund is overweight China and underweight Hong Kong resulting in a modest overweight to the two combined. The Fund also has off-benchmark exposures to Australia and to the US, where the Fund has holdings in Applied Materials and Broadcom, both of which derive over half their revenues from the region. The biggest country under-weights are to Korea and Taiwan. At a sector level, the Fund has the highest relative exposure to Information Technology, Healthcare and Industrials while its lowest relative exposures are to Financials. The Fund has no exposure to Materials, Real estate or to Utilities.

We see valuations in Asia as attractive, being one of the few regions trading at a discount to its historic average. China is clearly a big influence on outcomes. We expect to see the Federal Reserve switch back to its main job this year in trying to deliver price stability and the provision of liquidity when the system needs it. We think it is trying to shake off its role, begun in 1994, as a stock market prop. We expect therefore, that low unemployment and high inflation means higher interest rates and we think it is unlikely that the Federal reserve will be inclined to act on stock market weakness unless there is serious disruption. In short, monetary policy looks set to tighten.

The opposite, we think, is true in China. Interest rates have eased a little and as economic growth decelerates following the moves to force deleveraging in the real estate sector, we shall see more moves to provide support. China never spent anything like as much as the US did during COVID (China spent 4.7% of Gross Domestic Product (GDP), the US spent upward of 25% of GDP) leaving them room to loosen. We therefore expect to China to be easing at a time when the developed world is tightening, and with Chinese stock price valuations so low, we think there are opportunities.

Edmund Harriss

January 2022

The Fund invests in foreign securities, which involves political, economic and currency risks, greater volatility, and differences in accounting methods. These risks are greater for emerging markets. Investments focused in a single geographic region may be exposed to greater risk and more volatility than investments diversified among various geographies. The Fund invests in smaller companies, which involves additional risks such as limited liquidity and greater volatility.

The MSCI AC (All Country) Far East ex Japan Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance of the Far East, excluding Japan. Net Return reflects deduction for withholding tax but reflects no deduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay. This index is unmanaged and is not available for investment, and does not incur expenses.

PER or P/E – Price to Earnings ratio is calculated by dividing current price of the stock by the company's trailing twelve months' earnings per share.

GDP – Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country's borders in a specific time period.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

Asia Focus Fund

Growth of $10,000 (Unaudited)

Average Annual Total Return

Periods Ended December 31, 2021

| One Year | | Five Years | | Ten Years |

| -6.32% | | 12.27% | | 6.19% |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East Free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance of the Far East region excluding Japan. The index referenced in this chart is not available for investment and does not incur expenses. Net Return reflects deduction for withholding tax but reflects no deduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay.

FUND HIGHLIGHTS at December 31, 2021

GUINNESS ATKINSON ASIA FOCUS FUND

| # of Holdings in Portfolio: | | | 32 | |

| Portfolio Turnover: | | | 29.1 | % |

| % of Stocks in Top 10: | | | 44.1 | % |

| Fund Manager: |

| Edmund Harriss |

| Sharukh Malik |

| Mark Hammonds |

| Top 10 Holdings (% of net assets) | | | |

| NARI Technology Co., Ltd. | | | 5.5 | % |

| DBS Group Holdings | | | 4.8 | % |

| Broadcom Inc. | | | 4.5 | % |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | | 4.5 | % |

| Elite Material Co., Ltd. | | | 4.5 | % |

| Wuxi Lead Intelligent Equipment Co., Ltd. | | | 4.3 | % |

| Samsung Electronics Co., Ltd. | | | 4.0 | % |

| Inner Mongolia Yili - A Shares | | | 4.0 | % |

| Corporate Travel Management Ltd. | | | 4.0 | % |

| Sonic Healthcare Ltd. | | | 4.0 | % |

| Industry Breakdown (% of net assets) |

| Electronic Components - Semiconductor | | | 12.0 | % |

| Semiconductor Components - Integrated Circuits | | | 8.3 | % |

| Commercial Banks | | | 7.9 | % |

| E-Commerce/Services | | | 5.7 | % |

| Machinery - General Industries | | | 5.5 | % |

| Electronic Component Miscellaneous | | | 4.5 | % |

| Batteries/Battery Systems | | | 4.3 | % |

| Food - Dairy Products | | | 4.0 | % |

| Travel Services | | | 4.0 | % |

| MRI/Medical Diagnostic Imaging | | | 4.0 | % |

| Entertainment Software | | | 3.5 | % |

| Auto - Cars/Light Trucks | | | 3.4 | % |

| Textile - Apparel | | | 3.3 | % |

| Medical Products | | | 3.0 | % |

| Computer Data Security | | | 3.0 | % |

| Internet Application Software | | | 2.9 | % |

| Pharmaceuticals | | | 2.8 | % |

| Building & Construction Products - Miscellaneous | | | 2.8 | % |

| Auto/Truck Parts & Equipment | | | 2.7 | % |

| Photo Equipment & Supplies | | | 2.6 | % |

| Machinery - Construction & Mining | | | 2.5 | % |

| Cosmetics & Toiletries | | | 2.4 | % |

| Insurance | | | 2.2 | % |

| E-Commerce/Products | | | 2.0 | % |

| Building Products - Cement/Aggregates | | | 1.0 | % |

| Metal Processors & Fabricators | | | 0.0 | % |

GUINNESS ATKINSON ASIA FOCUS FUND

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 100.3% | | Value | |

| | | | | | | |

| | | | | Australia: 8.0% | | | | |

| | 40,819 | | | Corporate Travel Management Ltd. | | $ | 653,066 | |

| | 19,149 | | | Sonic Healthcare Ltd. | | | 649,062 | |

| | | | | | | | 1,302,128 | |

| | | | | | | | | |

| | | | | China: 55.1% | | | | |

| | 8,900 | | | Alibaba Group Holding Ltd. | | | 135,729 | |

| | 1,700 | | | Alibaba Group Holding Ltd. - ADR | | | 201,943 | |

| | 5,800 | | | Autohome Inc. - ADR | | | 170,984 | |

| | 2,900 | | | Baidu Inc.* -ADR | | | 431,491 | |

| | 321,000 | | | China Lesso Group Holdings Ltd. | | | 461,130 | |

| | 293,000 | | | China Medical System Holdings Ltd. | | | 489,304 | |

| | 66,500 | | | China Merchants Bank Co., Ltd. - H Shares | | | 516,459 | |

| | 205,000 | | | Geely Automobile Holdings Ltd. | | | 560,059 | |

| | 100,700 | | | Inner Mongolia Yili Industrial Group Co., Ltd. - A Shares | | | 655,929 | |

| | 7,200 | | | JD.com Inc. - ADR | | | 504,504 | |

| | 143,340 | | | NARI Technology Co., Ltd. - A Shares | | | 901,470 | |

| | 5,700 | | | NetEase Inc. - ADR | | | 580,146 | |

| | 49,000 | | | Ping An Insurance Group Company of China Ltd. - H Shares | | | 352,896 | |

| | 114,600 | | | Sany Heavy Industry Co., Ltd. - A Shares | | | 410,504 | |

| | 27,800 | | | Shenzhou International | | | 534,499 | |

| | 659,000 | | | Sino Biopharmaceutical Ltd. | | | 461,507 | |

| | 8,000 | | | Tencent Holdings Ltd. | | | 468,723 | |

| | 108,400 | | | Venustech Group Inc. - A Shares | | | 485,880 | |

| | 60,160 | | | Wuxi Lead Intelligent Equipment Co., Ltd. - A Shares | | | 702,917 | |

| | | | | | | | 9,026,074 | |

| | | | | | | | | |

| | | | | Singapore: 4.8% | | | | |

| | 32,362 | | | DBS Group Holdings Ltd. | | | 783,966 | |

| | | | | | | | | |

| | | | | South Korea: 9.1% | | | | |

| | 38,530 | | | Hanon Systems | | | 435,907 | |

| | 430 | | | LG Household & Health Care Ltd. | | | 396,778 | |

| | 10,050 | | | Samsung Electronics Co., Ltd. | | | 661,913 | |

| | | | | | | | 1,494,598 | |

The accompanying notes are an integral part of these financial statements.

GUINNESS ATKINSON ASIA FOCUS FUND

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 100.3% | | Value | |

| | | | Taiwan: 15.4% | | | |

| | 73,000 | | | Elite Material Co., Ltd. | | $ | 732,239 | |

| | 4,800 | | | Largan Precision Co., Ltd. | | | 426,917 | |

| | 32,000 | | | Novatek Microelectronics Corp. | | | 622,335 | |

| | 2 | | | Shin Zu Shing Co., Ltd. | | | 7 | |

| | 33,000 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 732,275 | |

| | | | | | | | 2,513,773 | |

| | | | | United States: 7.9% | | | | |

| | 3,508 | | | Applied Materials Inc. | | | 552,019 | |

| | 1,120 | | | Broadcom Inc. | | | 745,259 | |

| | | | | | | | 1,297,278 | |

| | | | | Total Common Stocks | | $ | 16,417,817 | |

| | | | | (cost $9,837,897) | | | | |

| | | | | Total Investments in Securities | | | 16,417,817 | |

| | | | | (cost $9,837,897): 100.3% | | | | |

| | | | | Liabilities in Excess of Other Assets: (0.3%) | | | (50,441 | ) |

| | | | | | | | | |

| | | | | Net Assets: 100.0% | | $ | 16,367,376 | |

| * | Non-income producing security. |

ADR - American Depository Receipt

The accompanying notes are an integral part of these financial statements.

GUINNESS ATKINSON CHINA & HONG KONG FUND

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

| Average annualized Total returns | 1 Year | 3 Years | 5 Years | 10 Years |

| Fund | -6.70% | 11.58% | 10.53% | 6.48% |

| Benchmark Index: | | | | |

| Hang Seng Composite Index | -13.89% | 4.80% | 6.99% | 6.96% |

Expense Ratio 1.60%.

For the Fund’s current one-year expense ratio, please refer to the Financial Highlights sect of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.gafunds.com, or calling (800) 915-6565.

In 2021, the Fund fell 6.70% and the Hang Seng Composite Index fell 13.89% and the MSCI China Net Total Return Index fell 21.72%. Therefore the Fund outperformed the Hang Seng Index by 7.19% and the MSCI China Index by 15.02%.

Fund Philosophy

The Fund invests in quality, profitable companies which give exposure to the structural growth themes in China. These seven themes are:

| · | Rise of the Middle Class1 |

| · | Cloud Computing & Artificial Intelligence |

Once we have identified companies which give exposure to these themes, we also apply a set of quantitative filters to identify quality, profitable companies with strong balance sheets. Quality is defined as a return on capital above the cost of capital while a strong balance sheet is defined as debt/equity less than 150%. These filters reduce the universe from an initial ~1,600 companies to ~800 companies, of which we generally pick 30-40 to form an equally weighted portfolio.

| 1 | The Rise of the Middle Class refers to the opportunity set as China’s middle class continues to grow in size and wealth. A company falls within this theme if it gives exposure to Food, Home Improvements, Beverages, Urbanization, Leisure or Education. |

| 2 | Sustainability refers to China’s efforts to reduce it carbon output and to reduce its impact to the environment. A company falls within this theme if it gives exposure to the ongoing energy transition, electric vehicles or waste reduction. |

| 3 | Next Gen Consumer refers to new ways of consumption. A company falls within this theme if it gives exposure to E-Commerce or Online Entertainment. |

Overall, we are looking for companies with the following characteristics:

| · | High return on capital companies. |

| · | Companies with growing operating cashflow, which we expect to continue to grow. |

| · | The ability to deploy this cash at a high rate of return. |

| · | Sensibly structured balance sheets with no excessive debt. |

| · | Management we trust to grow the business. |

| · | Companies that are judged to not harm society’s wider interests. |

| · | Market is undervaluing the growth opportunities. |

The Fund has a valuation discipline to ensure that we do not overpay for future growth. When assessing the valuation of companies on a discounted cash flow basis, we adjust the discount rate where necessary to reflect the potential for higher global interest rates.

The Fund is run on an equally weighted basis, meaning it has high conviction in 30-40 stocks.

Fund and Market Review

The Rally

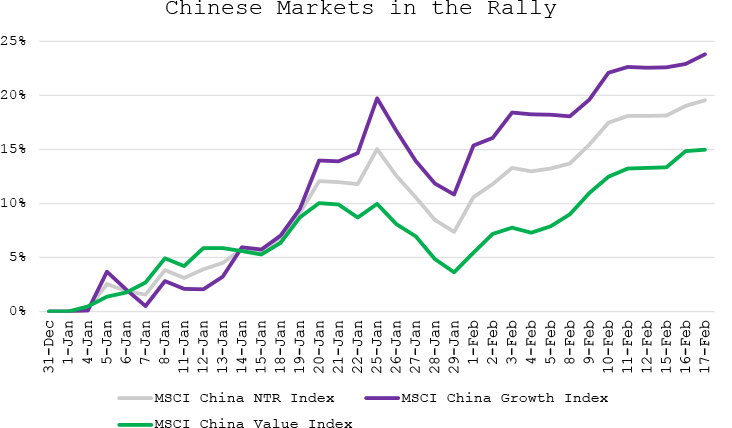

The year started off strongly for China, with the large cap tech stocks driving a rally which lasted until mid-February. A bullish mood partly explained this rally, with newly launched funds braking fundraising records. At the time we did note that certain parts of the market were looking expensive and there was a risk of a derating if expectations were not met. In particular, discount rates in Hong Kong reached their lowest level in 10 years and so we made a point of using higher discount rates when valuing companies, to reflect the risk of rising global interest rates.

(Data from 12/31/20 to 02/17/21, returns in USD)

Chinese markets peaked in February, and in this rally, the MSCI China NTR Index rose 19.6%. We think it is also meaningful to split China’s performance into Growth and Value. The MSCI China Growth Index rose 23.8% while the MSCI China Value Index rose by 15.0%.

The Sell-Off

But following the peak, Chinese markets were weak for the rest of the year due to multiple reasons. In February concerns over the potential for higher global interest rates, in response to higher inflation, led to a global sell-off. High growth stocks, whose valuations were boosted by 12 months of very low discount rates, were particularly weak. Additionally in China the central bank indicated monetary policy was unlikely to be loosened further, compounding the initial effect. In March, the MSCI China NTR Index fell 6.3%.

Over the spring and summer, we saw increased government regulation affecting various industries. We think the government introduced new rules for several reasons, with the aims of:

| · | Improving poor corporate behaviour in industries where there had previously been relatively less regulation. |

| · | Reducing social inequality, which links in with the government’s focus on common prosperity. |

| · | Protecting data security, which is linked to the structure that Chinese companies use to list overseas. |

(Data from 02/17/21 to 12/31/21, returns in USD)

Chinese markets were most affected by regulations in July, with the MSCI China Net Total Return Index falling 13.8%. Towards the end of the summer, new headwinds appeared, including:

| · | Evergrande was unable to borrow more to pay off its liabilities, meaning it could not repay a bond due in September. This led to concerns over potential contagion in the property market, as well as in the wider economy. |

| · | Unexpected power cuts led to weaker economic activity in September. We think these cuts were due to inefficiencies in Chinese power markets, meaning power plants were reluctant to produce in light of higher cost prices. |

| · | Economic growth was slowing down, as the government wound down monetary stimulus. |

Chinese markets were broadly flat between August and October, but fell in November, driven by further weakness in the large cap tech stocks. Tencent was asked by regulators to temporarily pause releasing new apps and to stop updating existing apps. This was because the company was found to violate data protection rules on four occasions in the past. Alibaba reported weaker results than expected, which reflected the headwinds the business was facing. Though revenues grew 29% year-on-year in the third quarter, the core business, the customer management segment, only grew sales by 3%. The company is investing to generate growth in other parts of the business, but margins are likely to suffer.

Stock Performance

Leaders

Nari Technology benefited from a rerating during the year. The company makes software and hardware for the electricity grid, focusing on dispatching and distribution solutions. Nari is an indirect beneficiary of China’s buildout of renewable energy, which requires investment in the state grid network to link the sources of renewable energy to where electricity is demanded. Part of this effort also involves the construction of Ultra High Voltage (UHV) lines to transport electricity at long distances with minimal energy loss, where Nari also has exposure to.

China Medical System was by far the strongest stock in the portfolio in the first half of the year, rising 139%. The stock then gave back much of its gains, but still ended the year as one of the strongest performing stocks in the portfolio. The company was historically a contract sales organisation that sold drugs on behalf of foreign companies in China. Its focus was on generics, an area in which the government has initiated significant price cuts to lower overall healthcare costs. As a business dealing exclusively in generics, CMS’s share price sold off sharply in 2019 and was weak in 2020. We felt the share price during this period was implying the worst-case scenario so continued to add to the position as part of the Fund’s rebalancing process. Over time, CMS has delivered. Price cuts for its generic products have been well below average due to the relatively lower level of competition. The business has signed deals to build its innovative pipeline, where pricing power is much higher compared to generics. In the first half of 2021, revenue grew 24% and net income grew 27%.

Lead Intelligent makes equipment used to manufacture batteries for electric vehicles. It is well known for its winding equipment, which packs cells together, but also has a good offering in the early stage of the battery manufacturing process where electrodes are made. CATL, one of the largest battery manufacturers in the world, is now Lead’s second largest shareholder. CATL has guaranteed the company at least 50% share in its main battery cell equipment orders between 2021 and 2023, so Lead Intelligent should derive good earnings growth from this deal. The business also has exposure to other customers, such as Northvolt in Europe. We think the demand for electric vehicles is very likely to continue to grow, which requires battery plants to be built, leading to rapid growth in Lead Intelligent’s business.

China Merchants Bank is, in our opinion, the best run bank in China. One of the company’s advantages is its good customer service, which allows the company to obtain cheaper sources of funding from its retail base, rather than rely on wholesale markets. The business earns its income through income on loans, as well as on fee income from its credit card, wealth management and custodian businesses. The wealth management business sells funds, insurance products and wealth management products, which allows the bank to take advantage of China’s growing middle class. In 2021, China Merchants Bank grew operating income by 14% and grew net profit by 23%.

Haier Smart Home gives exposure to rising demand for household appliances such as air conditioners, washing machines and fridges. Management are confident the business can grow profits by 15% a year in the medium to long-term, given the wide range of products the business offers. The company’s premium Casarte continues to grow quickly at higher margins than the rest of the business. The Leader brand, on the other hand, is a mass market brand targeted at younger consumers, offering more value-for-money products. The combined contribution from the two brands is now 20% of total revenue.

Laggards

New Oriental Education was sold in June after it became much likelier that the government would ban weekend and holiday tuition. This fear became a reality as after we sold the stock, the government banned for-profit firms from operating in the after-school tuition industry. Though we did sell well below the stock’s peak, we still made a ~50% return on the stock over the total holding period. Furthermore, we avoided making a loss on the investment, as after the government announced its restrictions in the month after we sold the stock, New Oriental’s share price fell a further 70% in two days.

We sold Autohome due to its lack of earnings growth. The company operates China’s largest online platform for buying and selling cars. However, the ongoing chip shortage has affected car sales which is out of the company’s control. Increasing competition from well-funded businesses is another headwind that Autohome is facing. The market is not expecting earnings to reach 2020’s level until 2024 and we do not have a strong view as to why the market is wrong.

Alibaba had a tough year, with increased government restrictions and a slowing core business. In November 2020, Alibaba’s founder, Jack Ma, gave a speech criticising various aspects of China’s financial system. While criticism is allowed in China, one has to be very careful about the way in which it is done. Jack Ma’s method was public and direct, which was not well received by the government. Soon after, Ant Group, which is owned by Alibaba, saw its public listing suspended. This marked the beginning of the government’s antitrust efforts targeting the tech sector. Additionally, the core e-commerce business is slowing down and Alibaba is investing to try to generate new growth drivers, which will depress margins in the short-term. The business was trading at high valuations at the beginning of the year, implying growth rates which the business has not been able to achieve, explaining the sharp derating in 2021. As previously discussed, the Fund’s equally weighted nature means Alibaba has a neutral weight of ~3.3% in the Fund. In Feb-21, Alibaba was the second largest stock in the MSCI China Index with a 14.1% weight. Therefore given the sell-off in the stock, the Fund has benefited significantly from its underweight in the stock. We continue to hold the stock because Alibaba gives good, return on capital exposure to e-commerce which we expect to continue to grow over time. We limit the stock specific risk to the company through the equally weighted nature of the portfolio, which helped in 2021.

Chinese insurers have had a tough year, and Ping An is no exception. Consumer demand has been sluggish in a weaker macro environment and so demand for more expensive insurance protection products has been weak. Customers have instead shifted towards savings products but these are lower margin for Ping An. In response to the weak market, insurers have been letting go of part-time agents and are replacing them with fewer, but more qualified and productive full-time agents. Additionally, the market has been worried about Ping An’s exposure to property. Ping An invested in the property developer China Fortune Land Development, which defaulted on its debt in March, and so Ping An took an impairment of RMB 36bn. We think the share price probably reflects the issues we have outlined and that the business is trying to increase productivity in the current environment.

Galaxy Entertainment operates casinos and hotels in Macau. Given China’s zero-COVID policy, only domestic Chinese customers can enter Macau. But with COVID outbreaks over the year, it has been difficult for some domestic Chinese to move around the country. Therefore it has been another weak year for the business.

Sells

Conch Cement was sold as it was difficult to argue, with confidence, that earnings will meaningfully increase in the medium term. The long-term growth driver for the cement industry is ultimately driven by real estate and infrastructure and at least in the case of infrastructure, there are better names available. Conch Cement is a consolidator but is ultimately a price taker in the cement industry, and so has limited pricing power.

We sold Shenzhen Expressway as it was also difficult to identify the long-term structural growth drivers for the business. The company runs toll roads with revenue concentrated in Shenzhen and the broader Guangdong province. Though margins are relatively high, the business is very capital intensive and so asset turnover is low, resulting in a low overall return on capital.

We sold Yuhong, a manufacturer of waterproofing materials used in the construction industry. We believe the share price did not fully reflect the company’s exposure to Evergrande, and therefore took profit on the stock. We still like the company and it remains on our watchlist as Yuhong’s balance sheet is strong enough to weather a weaker year. At the time of the sale, there were more attractive ideas on the watchlist.

New Oriental Education and Autohome were also sold – please see the previous section for details.

Buys

We bought Xinyi Solar, which is the world’s largest manufacturer of solar glass and so through its economies of scale, has benefited as the low-cost producer in the industry. However its competitive advantage is not solely a function of its scale. The quality of Xinyi’s glass is high relative to its peers so the company is well trusted by its clients. This is very important given the rising popularity of bifacial panels which need thinner and so more durable glass. Tighter emissions standards also raise the cost of production, as well as the barriers to entry, protecting incumbents such as Xinyi. Policymakers in all major regions around the world are aiming to significantly increase investment into renewable energy sources which should bode well for Xinyi.

Fuling Zhacai is a condiment company focused on the production of zhacai and paocai. Zhacai is made using mustard roots and is commonly eaten with rice and buns. Fuling Zhacai has a long history of manufacturing zhacai and has a market share of 36%. 28% of sales are from the South where the company is based but there is a fairly even split between the other major regions of China. Fuling Zhacai has been able to pass on cost increases to its customers which is a strong indicator of its pricing power, allowing the company to earn a high return on capital over time.

AIA gives the Fund exposure to the rising demand for premium life and health insurance. It is headquartered in Hong Kong and derives more than 50% of its revenue from the China region. AIA also has exposure to Southeast Asia, namely Thailand, Malaysia and Singapore. However, much of the future earnings growth is likely to come from mainland China. AIA is targeting the rising middle class in the country and we believe there is a lot of room for the company to grow from a relatively low base. AIA targets the premium end of the market, using its highly trained workforce which is viewed as giving some of the best service in the industry. This is backed up by AIA’s very low turnover rate amongst its staff, relative to its competitors.

Shengyi Technology makes copper clad laminates (CCLs), which are the main base material for printed circuit boards (PCBs). It has benefited from multiple trends which point to greater demand for CCLs and PCBs: growing popularity of 5G compatible devices, growing demand for servers and cloud services as well as localisation towards Chinese suppliers in the Chinese market. Shengyi is quickly moving up the value chain, supporting a gradual rise in margins over time.

We bought H&T Intelligent which makes controllers used in applications such as household appliances and power tools. H&T’s controllers are used in well-known brands such as Whirlpool, Siemens and Bosch. The company is well placed to take advantage of growing demand for the Internet of Things (IoT), which naturally complements the existing business. H&T is also aiming to expand into the automobile market where electronic control units, which are not too dissimilar from controllers, are becoming increasingly used.

3. OUTLOOK

Valuations for China have fallen significantly from their peak and are now at more reasonable levels. But to justify an investment in China, we argue lower valuations are not enough. Earnings growth is required to justify long-term returns and this is the component of shareholder return that we can attempt to control in the Fund.

The Fund is invested in quality, profitable companies which give exposure to the structural growth opportunities present in China. Our companies have in aggregate grown net income by 13% a year over the past 10 years i.e. they have shown they can translate the structural growth opportunities into consistent earnings growth. Our companies have done this while maintaining a high return on equity of 22%. To be clear, we are not interested in loss making, low return businesses which happen to be in boom areas.

Though our companies have, over the past 10 years, grown earning by 13% a year, the market is expecting higher growth over the next two years. Based on consensus earning estimates, the market is expecting earnings for the Fund’s holdings, in aggregate, to grow by 17% a year between 2020 and 2022, as China and the global economy recover from COVID.