UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08360

Guinness Atkinson Funds

(Exact name of registrant as specified in charter)

251 South Lake Avenue, Suite 800,

Pasadena, California 91101

(Address of principal executive offices) (Zip code)

(Name and address of agent for service)

James J. Atkinson, Jr.

251 South Lake Avenue, Suite 800,

Pasadena, CA 91101

Registrant’s telephone number, including area code: (866-307-5990)

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Item 1. Reports to Stockholders.

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

SmartETFs

Annual Report

December 31, 2021

TABLE OF CONTENTS

| Letter to Shareholders (Unaudited) | 3 |

| Management’s Discussion of Fund Performance (Unaudited) and Schedules of Investments | |

| Smart Transportation & Technology ETF (MOTO) | 7 |

| Advertising & Marketing Technology ETF (MRAD) | 17 |

| Sustainable Energy II ETF (SOLR) | 26 |

| Asia Pacific Dividend Builder ETF (ADIV) | 38 |

| Dividend Builder ETF (DVIS) | 46 |

| Statements of Assets and Liabilities | 57 |

| Statements of Operations | 59 |

| Statements of Changes in Net Assets | 61 |

| Financial Highlights | 64 |

| Notes to Financial Statements | 69 |

| Report of Independent Registered Public Accounting Firm | 79 |

| Other Information (Unaudited) | 81 |

Dear SmartETF Shareholders,

Welcome to the many new members of the SmartETFs family and thank you for joining us. The last year saw the number of SmartETFs grow from three to five. And we’re just getting started. As we mentioned last year, we’re working to enlarge the SmartETFs offerings and have plans for 2022. Stay tuned.

We’re delighted to report that all of the SmartETFs produced positive returns for 2021. In fact, you may notice that all of the SmartETFs have positive returns for all of the standard time periods ending December 31, 2021. That’s not to say that there were not any bumps along the way; the last few weeks of 2021 brought a bit of turbulence.

The top performing SmartETF was DIVS, the SmartETFs Dividend Builder ETF, which produced a total return of 23.60% for the year. Not bad for a boring dividend fund. Along with the Asia Pacific Dividend Builder ETF, the Dividend Builder was one of two Funds converted from traditional, open-end mutual funds in March of 2021.

The SmartETFs Asia Pacific Dividend Builder ETF (ADIV) provided a total return of 11.27% for the year.

MOTO, the SmartETFs Smart Transportation & Technology ETF, delivered a total return of 17.12% over the calendar year.

SOLR, the SmartETFs Sustainable Energy II ETF, also had a good year, producing a total return of 12.07%.

MRAD, the SmartETFs Advertising and Marketing Technology ETF, had a decent year, turning in a total return of 6.69%. This despite the fact that the MarTech stocks were buffeted as the year closed.

You’ll see in the performance table that two of the SmartETFs have Morningstar ratings. (The other three SmartETFs are too new to be rated.) The Dividend Builder sports a Five-Star overall rating while the Asia Pacific Dividend Builder has earned a Four-Star overall rating.

The concept that underpins the SmartETFs family is a series of mega themes. Our world view is one of change and opportunity. We believe that Asia, innovation, demographics, and increasing social responsibility are four mega themes that will lead to profound changes over the balance of this century.

Our objective with SmartETFs is not just to provide investors with excellent investment opportunities but to also inform and engage. If you haven’t already done so we encourage you to sign up to follow us on Twitter (“SmartETFs”) and/or sign up for our email service. You can do both of these from the SmartETFs website at www.SmartETFs.com. Or, if you prefer, simply visit the website occasionally to see the latest news and views from our portfolio managers.

We appreciate the confidence you’ve placed in us and look forward to serving you.

Regards,

President

SmartETFs

The total expense ratio for MOTO ETF is 0.68% net and 1.51% gross. For SOLR ETF, the expense ratio is 0.79% net and 1.91% gross. For MRAD ETF, the expense ratio is 0.68% net and 0.71% gross. All returns are for the periods ending December 31, 2021. For ADIV ETF, the expense ratio is 0.78% net and 4.97% gross. All returns are for the periods ending December 31, 2021. For DIVS ETF, the expense ratio is 0.65% net and 1.42% gross. All returns are for the periods ending December 31, 2021. The Adviser has contractually agreed to reduce its fees and/or pay ETF expenses in order to limit the Fund's total annual operating expenses through June 30, 2022 for MOTO and through June 30, 2025 for SOLR, MRAD, ADIV, and DIVS. Performance would have been lower without fee waivers in effect.

[SmartETFs Annual Report Letter Dec 2021]

Fund

Symbol

Inception date | 1-year | 3-year | 5-year | 10-year | From

Inception | Expense

Ratio |

Advertising & Marketing Technology ETF

MRAD

December 31, 2020 | 6.69% | | | | | 0.68% net;

0.71% gross |

Asia Pacific Dividend Builder

ADIV

March 31, 2006 | 11.27% | 15.10% | 11.74% | 9.08% | | 0.78% net;

4.97% gross |

Dividend Builder ETF DIVS

March 30, 2012 | 23.60% | 20.70% | 15.38% | | 11.96% | 0.65% net;

1.42% gross |

Smart Transportation & Technology ETF

MOTO

November 14, 2019 | 17.12% | | | | 37.32% | 0.68% net;

1.51% gross |

Sustainable Energy II ETF

SOLR

November 11, 2020 | 12.11% | | | | 28.22% | 0.79% net;

1.91% gross |

Periods of greater than one year are average annualized returns; one year and shorter period returns are actual returns. All returns are for the periods ending December 31, 2021.

The Asia Pacific Dividend Builder ETF and the Dividend Builder ETF converted from traditional open-end mutual funds to exchange traded funds on March 29, 2021. Performance data shown for these two ETFs includes their performance history as traditional open-end mutual funds.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.SmartETFs.com.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

Investing involves risk including the loss of principal.

Shares of the SmartETFs Funds are distributed by Foreside Fund Services, LLC.

Morningstar Ratings Through December 31, 2021

| Fund | Category | Overall | 3-Year | 5-Year | 10-Year |

Asia Pacific Dividend Builder

ADIV | Pacific/Asia ex-Japan Stock | 4 «««« (139 funds) | 4 ««««

(139 funds) | 4 «««« (105 funds) | 4 «««« (70 funds) |

Dividend Builder

DIVS | World Large-Stock Blend | 5 «««««

(283 funds) | 4 «««« (283 funds) | 5 «««««

(236 funds) | |

Morningstar Ratings Disclosure

For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in distribution percentages.)

© 2022 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar (2) may not be copied or distributed and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

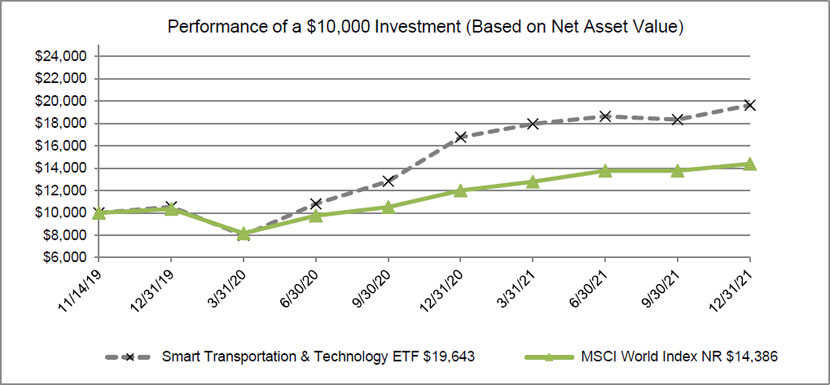

SmartETFs Smart Transportation & Technology ETF

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

1. Performance

Average annualized Total returns | 1 Year | Since Inception 11/14/2019 |

| Smart Transportation & Technology ETF (Net Asset Value) | 17.12% | 37.32% |

| Smart Transportation & Technology ETF (Market Price) | 17.24% | 37.07% |

| | | |

| Benchmark Indices: | | |

| MSCI World Index (Net Return) | 21.82% | 46.10% |

The Fund’s total expense ratio is 1.51% and the net expense ratio is 0.68%. The Adviser has contractually agreed to reduce its fees and/or pay ETF expenses in order to limit the Fund's total annual operating expenses to 0.68% through June 30, 2022. For the Fund’s current one-year expense ratios, please refer to the Financial Highlights section of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.smartetfs.com, or calling (866) 307-5990.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns. SmartETFs NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times.

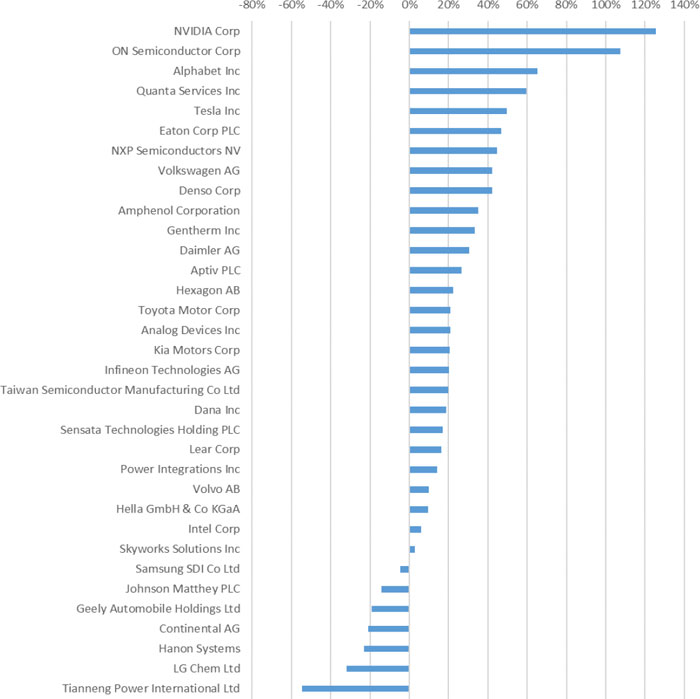

2021 was positive for global equities, although Smart Transportation equities underperformed. The Smart Transportation ETF (MOTO ETF) rose by 17.12%, underperforming the MSCI World Net Total Return Index (+21.82%) by 4.70%.

In terms of individual stock performance, the three best performers were:

| ● | NVIDIA shares rallied consistently through the year as a result of strong AV (autonomous vehicle) and EV (electric vehicle) related product demand complimented by near-term continued tightness in the semiconductor market. |

| ● | ON Semiconductor shares reacted positively to a hopeful capital markets day that was held early in the third quarter that coincided with an improving trend of quarterly results. The company rebranded itself to ‘onsemi’ and plans to prune both its revenue base and manufacturing footprint to invest in high-value, high-growth applications served by its power and sensing-biased semiconductor portfolio. |

| ● | Alphabet shares were a consistently strong performer over the year. Its autonomous driving subsidiary, Waymo, continues to grow and expand and commenced a fully autonomous ride-hailing service in Phoenix Arizona called Waymo One. |

The three weakest individual performers were:

| ● | Tianneng Power is a Hong Kong listed manufacturer of predominantly lead acid batteries for the Chinese market. The shares receded early in 2021 due to profit taking after standout performance in 2020 and then they suffered later in the year as raw material cost inflation impacted manufacturing margins. |

| ● | LG Chem shares were weaker following a $1.9bn product recall with GM regarding battery faults on the Chevrolet Bolt. |

| ● | Hanon Systems is a Korean-listed supplier of innovative thermal and energy management solutions for car OEMs. The shares were weaker as a result of semiconductor supply shortages and cost inflation during the year despite the majority owner, Hahn & Co, running a sale process for the company. |

Individual Stock Performance over the period

Source: Bloomberg, Guinness Atkinson

2. Activity

In the second half of the year, Continental spun-off of its powertrain division into a separate company, Vitesco, while Daimler AG spun off its trucks business into a separate listed company, Daimler Trucks. Both stocks are still held in the MOTO ETF.

Offsetting this in the second half of the year, we sold our position in Autohome, the largest online automotive platform for auto advertising, sales, financing and content in China. The company faces increasing competition and margin compression, compounded by unexpected management changes.

3. Portfolio Position

The sector and geographic weightings of the MOTO ETF at December 31st, 2021 were as follows:

| Sector breakdown | Dec. 31, 2021 |

| EV Manufacturers | |

| EV Transition | 15.8% |

| EV Dominated | 5.3% |

| Components | |

| Autonomous | 16.3% |

| Car Components | 21.9% |

| Batteries | 8.1% |

| Semiconductors | |

| Power | 7.1% |

| General | 8.6% |

| Connectivity | 8.5% |

| Services | |

| TAAS | 3.4% |

| Other | 3.2% |

| Cash | 1.7% |

| Geographic breakdown | Dec. 31, 2021 |

| United States | 49.0% |

| Germany | 12.9% |

| South Korea | 10.1% |

| Japan | 6.1% |

| Sweden | 5.6% |

| China | 3.2% |

| Netherlands | 3.2% |

| Taiwan | 3.0% |

| Ireland | 2.9% |

| UK | 2.1% |

| Cash | 1.7% |

4. Outlook

2021 was another year of growth and improving outlook for companies associated with the entire value chain of electrification of transportation. We consider here the recent activity and subsequently the outlook for both the lithium battery markets and the electric vehicle markets.

The catalyst for greater lithium-ion battery use has been sharp falls in the cost of manufacturing. According to BloombergNEF (BNEF), battery pack costs are down 89% over the period 2010 to 2021 (an implied ‘learning rate’ of around 18%) with the average cost being $132/kWh in 2021 (split $101/kWh for the cell itself and an additional $31/kWh for the pack).

The $132/kWh survey outcome for 2021 is an average calculated across a wide range of uses and regions. China was typically the lowest cost manufacturer with some individual passenger EV battery packs at below $100/kWh (and e-bus and commercial vehicle packs at $101/kWh on average) while BNEF calculated that Tesla’s estimated average pack price in 2021 was around $112/kWh. The survey also includes stationary storage solutions which saw a fall in cost of around 16% in 2021, to $152/kWh, as manufacturers turned to simple and cheaper battery chemistries, such as lithium-ion phosphate, to offset raw material inflation.

Raw materials make up around 50% of the cost of a lithium-ion battery pack, with cathode materials alone representing around 20% of the total cost. The key catalyst material is lithium carbonate, whose price in China rose by 270% in 2021. While battery manufacturers have long-term contracts and approaches in place to mitigate such inflation, they ultimately have little choice but to pass on the costs to consumers. In Q4 2021, BYD increased its battery prices by 20%.

Raw material cost inflation will continue to have an impact in 2022 and we see the likelihood that the cost of manufacturing may exceed levels seen in 2020. Rapidly increasing manufacturing capacity, (bringing further efficiencies of scale) together with reduced supply chain disruptions should help to alleviate the cost pressures in subsequent years and allow the average cost of producing a lithium-ion battery for an EV is likely to fall towards $100/kWh in the mid-2020s, maybe a year or so later than we previously expected.

While the $100/kWh cost level is a key target, we note that in 2021 the battery and EV industry started focusing on manufacturing costs well below $100/kWh. EV manufacturers started to vertically integrate with battery manufacturers and form battery manufacturing JVs such as BlueOvalSK (Ford/SK) and Ultium Cells (GM/LG Energy Solutions) in efforts to improve manufacturing efficiencies with $60/kWh targets discussed for the end of the decade. The US Department of Energy also set $60/kWh as its ‘stretch’ goal, a level would be achieved by 2030 if the current 18% learning rate is maintained.

Strong momentum in electric vehicle sales growth continued through 2021. On our estimates, nearly 6.1m new EVs were sold in the twelve months to November 2021, a growth of around 116% versus sales in the same period twelve months earlier (affected by COVID) and 178% higher than the same period in 2019. This growth compares very favourably to overall global light vehicle sales growth of 6.8%% and -9.4% for the same periods in 2021 and 2020 respectively. Accordingly, the market share for EVs has increased to around 7.6% for 2021 versus 3.4% and 2.4% in 2020 and 2019 respectively.

Regionally, China has regained its position as the largest EV market with total sales of new EVs of 2.9m in the twelve months to November 2021, up 150% on 2020. Europe, which overtook China to be the largest EV market at the end of 2020, saw total new EV sales of 2.27m units, up 94%. The US still lags Europe and China with new EV sales of 0.6m, up 95% on the same period twelve months earlier.

Lower EV prices, greater brand choice and growing consumer appetite continue to be the key drivers of improved EV sales. The strength in Europe has been helped by new generous EV incentives offered by Germany and France (amongst other countries) for passenger vehicles and increasing compliance with stricter emissions standards that came into effect at the start of the 2020. While passenger EVs are benefitting, EU data indicates that trucks are still witness the electrification trend; only 6 electric trucks were registered in Europe in the 12 months to the end of July 2020, versus 167,000 new diesel/petrol powered trucks. In China, after stagnating in 2019 as a result of the removal of EV subsidies, EV sales activity rebounded as a result of a broader range of EV models, including a number at lower price points.

Government support for EVs will reduce in 2022. Europe will continue rolling back its EV “super-credits”, and China plans to reduce EV subsidies further. Despite this, we expect global EV sales to exceed 9 million in 2022, representing around 10% of total passenger vehicle sales, taking the global EV stock from 16m vehicles to 25m vehicles.

US EV sales are expected to lag again. As part of the currently stalled Build Back Better plan, the Biden administration is attempting to increase the tax credit for EVs to US$12,500, but this will be applicable only to a small number of vehicles as the limits for individual manufacturers have not been lifted. In December, the Environmental protection Agency (EPA) announced tougher emissions standards for US passenger cars and light trucks, requiring the 2026 model year vehicles to deliver average fuel economy of around 55 miles per gallon, around 23% greater than existing legislation.

On a global basis, we expect EVs will represent around 20% of new vehicle sales in 2025 (concurrent with the cost of EV lithium-ion batteries falling to around $100/kWh), 50% of new vehicle sales in 2030 and nearly all new vehicle sales by 2040. At that point, it implies an overall EV population of around 1bn vehicles, over sixty-five times greater than current global population of around 15m EVs. With EVs using roughly one third of the energy of a typical internal combustion engine vehicle, this transition alone will have substantial impact on global energy efficiency and global decarbonisation.

Despite these rapid EV growth assumptions, we calculate that oil demand from passenger vehicles will not peak until around 2024/25 and that, even by 2030, passenger vehicle oil demand will be similar to 2021 levels. With transportation generating just over 7bn tonnes of carbon emissions in 2020, accelerating the transition and reducing associated oil demand is critical to achieving a net zero 2050 scenario.

The MOTO ETF is positioned to benefit from these long-term trends, providing exposure to a basket of smart transportation companies with cash returns and growth that are on average greater than the MSCI World Index but that trade at a 2022 P/E multiple discount of around 14%.

Will Riley & Jonathan Waghorn

January 2022

P/E Ratio is the price-to-earnings ratio and is a ratio for valuing a company that measures its current share price relative to its earnings per share.

International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

The companies in which the Fund invests may be subject to rapid changes in technology, intense competition, rapid obsolescence of products and services, loss of intellectual property protections, evolving industry standards and frequent new product productions and changes in business cycles and government regulations.

These risks could adversely affect the value of companies in which the Fund invests. Limitations on applications for autonomous or electric vehicles could adversely affect the value of companies in which the Fund invests.

MSCI World Index A free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. One cannot invest directly in an index.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

Smart Transportation & Technology ETF

FUND PERFORMANCE AND SUMMARY

As of December 31, 2021 (Unaudited)

Average Annual Returns

December 31, 2021 | One Year | Since Inception

(11/14/2019) |

| Smart Transportation & Technology ETF - NAV | | 17.12% | 37.32% |

| Smart Transportation & Technology ETF - Market | | 17.24% | 37.07% |

| MSCI World Index NR | | 21.82% | 46.10% |

The performance data quoted represents past performance and past performance is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of theFund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.smartetfs.com.

Total returns reflect the reinvestment of distributions made by the Fund, if any. The deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares is not reflected in the total returns.

The Fund's shares are listed on an exchange. The price of the Fund's shares is based on market price, and because the exchange-traded fund shares trade at market prices rather and net asset value, shares may trade at a price greater than net asset value (premium) or less than net asset value (discount).

The MSCI World Index (Net Return) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. Net Return reflects deduction for withholding tax but reflects no duduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay.

SmartETFs Smart Transportation & Technology ETF

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 96.0% | | Value ($) | |

| | | | | Auto/Trucks Parts & Equipment: 5.9% | | | | |

| | 6,776 | | | Gentherm Inc.* | | $ | 588,834 | |

| | 5,772 | | | Hella GmbH & Co KGaA | | | 391,399 | |

| | | | | | | | 980,233 | |

| | | | | Commerical Services: 3.2% | | | | |

| | 4,662 | | | Quanta Services Inc. | | | 534,545 | |

| | | | | | | | | |

| | | | | Rubber-Tires: 1.6% | | | | |

| | 2,506 | | | Continental AG | | | 265,475 | |

| | | | | | | | | |

| | | | | Smart Transportation: 30.9% | | | | |

| | 2,954 | | | Aptiv PLC | | | 487,262 | |

| | 5,250 | | | Daimler AG | | | 403,728 | |

| | 2,373 | | | Daimler Truck AG | | | 87,179 | |

| | 7,000 | | | Denso Corp. | | | 579,547 | |

| | 154,000 | | | Geely Automobile Holdings Ltd. | | | 420,727 | |

| | 12,642 | | | Johnson Matthey PLC | | | 349,909 | |

| | 6,286 | | | KiaCorp | | | 434,629 | |

| | 7,560 | | | Sensata Technologies Holding* | | | 466,376 | |

| | 840 | | | Tesla Inc.* | | | 887,695 | |

| | 112,000 | | | Tianneng Power International | | | 118,515 | |

| | 23,800 | | | Toyota Motor Corp. | | | 435,387 | |

| | 500 | | | Vitesco Technologies Group AG* | | | 24,575 | |

| | 18,592 | | | Volvo AB Class B | | | 430,929 | |

| | | | | | | | 5,126,458 | |

| | | | | | | | | |

| | | | | Technology: 3.0% | | | | |

| | 4,214 | | | Taiwan Semiconductor Manufacturing Co Ltd. - ADR | | | 506,986 | |

| | | | | | | | | |

| | | | | Technology & Transportation: 51.4% | | | | |

| | 196 | | | Alphabet Inc. Class C* | | | 567,144 | |

| | 5,852 | | | Amphenol Corp. Class A | | | 511,816 | |

| | 2,730 | | | Analog Devices Inc. | | | 479,852 | |

| | 18,578 | | | Dana Inc. | | | 423,950 | |

| | 3,220 | | | Eaton Corp. PLC | | | 556,480 | |

| | 32,942 | | | Hanon Systems | | | 372,688 | |

| | 31,850 | | | Hexagon AB Class B | | | 505,824 | |

| | 12,250 | | | Infineon Technologies AG - ADR | | | 568,090 | |

| | 8,092 | | | Intel Corp. | | | 416,738 | |

| | 2,450 | | | Lear Corp. | | | 448,228 | |

| | 742 | | | LG Chem Ltd. | | | 383,842 | |

| | 2,268 | | | NVIDIA Corp. | | | 667,041 | |

| | 2,310 | | | NXP Semiconductors NV | | | 526,172 | |

| | 10,080 | | | ON Semiconductor Corp.* | | | 684,634 | |

| | 5,320 | | | Power Integrations Inc. | | | 494,175 | |

| | 896 | | | Samsung SDI Co., Ltd. | | | 493,654 | |

| | 2,772 | | | Skyworks Solutions Inc. | | | 430,048 | |

| | | | | | | | 8,530,376 | |

| | | | | | | | | |

| | | | | Total Common Stocks (Cost $12,757,457) | | | 15,944,073 | |

The accompanying notes are an integral part of these financial statements.

SmartETFs Smart Transportation & Technology ETF

Schedule of Investments

at December 31, 2021

| Shares | | | | | Value ($) | |

| | | | | Preferred Stocks | | | | |

| | | | | Smart Transportation: 2.5% | | | | |

| | 2,030 | | | Volkswagen AG | | $ | 409,914 | |

| | | | | Total Preferred Stocks (Cost $392,904) | | | 409,914 | |

| | | | | | | | | |

| | | | | Total Investments (Cost $13,150,361): 98.5% | | | 16,353,987 | |

| | | | | Other Assets in Excess of Liabilities - 1.5% | | | 254,420 | |

| | | | | Total Net Assets - 100.0% | | $ | 16,608,407 | |

| * | Non-income producing security. |

ADR - American Depository Receipt

PLC - Public Limited Company

The accompanying notes are an integral part of these financial statements.

SmartETFs Smart Transportation & Technology ETF

Schedule of Investments

at December 31, 2021

Country Breakdown | Percent of Total

Net Assets |

| Common Stocks | |

| United States | 49.1% |

| Germany | 10.5% |

| South Korea | 10.0% |

| Japan | 6.1% |

| Sweden | 5.6% |

| Netherlands | 3.2% |

| Taiwan | 3.0% |

| Ireland | 2.9% |

| Hong Kong | 2.5% |

| United Kingdom | 2.1% |

| China | 1.0% |

| Total Common Stocks | 96.0% |

| Preferred Stocks | |

| Germany | 2.5% |

| Total Preferred Stocks | 2.5% |

| Total Investments | 98.5% |

| Other Assets in Excess of Liabilities | 1.5% |

| Total Net Assets | 100.0% |

The accompanying notes are an integral part of these financial statements.

SMARTETFS ADVERTISING & MARKETING TECHNOLOGY ETF

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

Performance

| Average annualized Total returns | 1 year | SINCE

INCEPTION

12/31/2020 |

| Advertising & Marketing Tech ETF (Net Asset Value) | 6.69% | 6.69% |

| Advertising & Marketing Tech ETF (Market Price) | 6.38% | 6.38% |

| Benchmark Index: |

| MSCI World Index (Net Return) | 21.82% | 21.82% |

The Fund’s total expense ratio is 0.71% and the net expense ratio is 0.68%. The Adviser has contractually agreed to reduce its fees and/or pay ETF expenses in order to limit the Fund’s total annual operating expense to 0.68% through June 30, 2025. For the Fund’s current one-year expense ratios, please refer to the Financial Highlights section of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.SmartETFs.com, or calling (866) 307-5990.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns. SmartETFs NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times

Review

In 2021, the SmartETFs Advertising & Marketing Technology ETF produced a total return of 6.69% (NAV, in USD), versus the MSCI World Index (net return) of 21.82% (in USD). The Fund therefore underperformed by 15.1%.

At quarter end, the Fund’s assets under management was $2.69mn.

In the first quarter of 2021, the Fund returned 3.60% (in USD) vs the MSCI World Index return of 4.92% (underperformance of 1.32%).

Global equities advanced in the first quarter in 2021, supported by (1) the roll-out of Covid-19 vaccines, (2) news of further US fiscal stimulus, and (3) a pledge by the Federal Reserve System’s (the Fed) Chairman, Jerome Powell, to keep interest rates lower-for-longer to help support the economic recovery. One year on from when equity markets bottomed, the MSCI World Index has rallied 79% (in USD) and is 18% above its pre-Covid highs.

Over Q1, the MSCI World Index rose 5% (in USD) and all regions registered gains, though markets were choppy and repeatedly tested as optimism drove bond yields higher. Despite the Fed’s reassurances that interest rates will remain low, the sharp rise in yields sparked sell-offs in global equity markets due to fears that rates may not remain supportively lower-for-longer if there is a material spike in inflation. This particularly dragged on the outlook for growth stocks which are expected to see earnings growth further out into the future and so are more vulnerable to higher discount rates. In contrast, value stocks performed relatively better as the “stay-at-home” trade gave way to the “re-opening” trade.

Equity markets’ advance was fueled by value stocks and cyclical sectors, i.e. those which are most sensitive to the economic cycle. Energy, Financials, and Industrials performed best over the quarter, and this dragged on the Fund’s performance.

In the second quarter of 2021, the Fund returned 10.28% (in USD) vs the MSCI World Index return of 7.74% (outperformance of 2.54%).

Global equity markets rallied strongly in the second quarter, building on first quarter gains, and closing out one of the best first half starts in history. Over Q2, the MSCI World Index rose 7.74% (in USD) and all regions registered gains. The US market delivered the best return, thanks to the rebound of growth stocks, strong first-quarter earnings growth (47% year-on-year), and the prospect of more fiscal stimulus as Joe Biden reached a bipartisan deal to boost infrastructure spending by $600 billion. Q2 marked the S&P 500 Index’s fifth consecutive quarter of gains, and best first-half performance since 1998. Overall, the economic picture remained rosy too. The US economy accelerated in Q2 2021, recording an annualized GDP increase of 6.4%.

Growth equities led in the quarter, supported by strong earnings releases from mega-cap technology companies, reversing some of the year-to-date underperformance versus value. Large cap companies generally outperformed their small-cap counterparts during the quarter, also breaking from recent trends. IT and Communication Services were the best performing sectors in Q2 and this benefitted the Fund’s performance.

Nonetheless the largest positive contributor to the Fund was news released by Google announcing that it is extending its deadline to remove third-party cookies from Chrome, from its original date of January 2022 until late 2023. Google also said it will conclude its initial trial of Federated Learning of Cohorts or FLoC, its most well-known and criticized Privacy Sandbox ad method, on July 13th. Share prices of a number of demand-side and sell-side advertising platform companies increased for 2 reasons: (1) significantly more time to plan for the removal of cookies and, (2) increased likelihood that cookies could not be removed at all.

In the third quarter of 2021, the Fund returned -3.28% (in USD) vs the MSCI World Index return of -0.01% (underperformance of 3.27%).

After a strong start to the quarter in July and August (+4.32% in USD), the MSCI World Index fell 4.15% in September as several risks surfaced, and volatility spiked towards the end of the quarter. This was due to numerous factors including increasing Delta-variant Covid cases, ongoing debt ceiling negotiations, fiscal and monetary policy uncertainty, global supply chain bottlenecks, slowing economic and earnings growth projections, ongoing inflation fears, and regulatory uncertainty in China.

The MSCI World Index ended flat for the quarter, whilst the Asia-Pac ex Japan and Emerging Market markets were markedly the worst performing after negative news from China weighed heavily on performance. Greater regulation on the education and tech sectors, and the potential default of Evergrande – a large indebted Chinese property developer – all contributed to spooking investors.

In the US, equities notched up a small positive return in Q3: strong earnings had lifted US stocks in the run up to August, when the Fed seemed to strike a dovish tone, confirming its hesitance to tighten policy too fast. However, growth and inflation concerns late in the quarter meant US equities retraced their steps in September. This was exacerbated late in the month after the Fed stated that tapering of quantitative easing (i.e. a slowdown in the pace of asset purchases) will be announced in November, as expected, and will finish by mid-2022.

The above resulted in a sharp style rotation at the end of the quarter, away from growth stocks and towards value. Value’s outperformance coincided with rate-sensitive stocks leading the gains, as the Financials and Energy sectors fared best over the quarter. This proved a drag on the Fund’s performance.

In the fourth quarter of 2021, the Fund returned -3.25% (in USD) vs the MSCI World Index return of 7.77% (underperformance of 11.01%).

Stocks remained subdued in early October, with increasingly disrupted supply chains, hawkish Fed rhetoric, and higher persistent inflation. However, markets soon regained momentum following the onset of a strong Q3 earnings season, with over 80% of S&P 500 companies beating earnings expectations in the month.

Further evidence of an economic rebound and sustained strong earnings releases continued to drive equities higher during November. However, the World Health Organization labelled the new Omicron strain as a “variant of concern” in the final week of the month, spooking the market to one of the largest sell-offs of the year. Equities were dealt another blow as Fed chair Jerome Powell also offered a more hawkish tone.

Volatility continued into December though fears over Omicron eventually waned as investors were encouraged by data indicating a lower risk of hospitalisation. Investors showed a preference for more defensive stocks as coronavirus infections surged past previous peaks across the US and Europe.

Over the quarter, Central Banks become more hawkish. In late November, Jay Powell told congress that the Fed was retiring the word “transitory”. Powell’s change of tact represented a significant turning point in Central Bank thinking – that inflation now takes top priority and the need to stimulate the economy had “clearly diminished”. The market is now expecting three rate hikes of 0.25% over 2022 and an earlier timeline to the tapering of assets. The European Central Bank (ECB) also scaled back their asset purchasing programming, and the UK went a step further – raising rates to 0.25% from 0.10%.

Whilst growth outperformed by 0.8% during Q4, December saw a strong rotation into value. This followed what was perceived as a hawkish ‘pivot’ by the Fed, reversing much of the strength seen by growth in the prior two months. The sharp style rotation at the end of the quarter proved a drag on the Fund’s performance given it holds high growth adtech and martech names. Higher rates used to discount future growth, reduces the valuation of such fast-growing companies. Further, the Fund is predominantly exposed to the Communications sector, which was the only sector with negative returns in the quarter.

Activity

We made five changes to the portfolio in 2021.

BOUGHT: AcuityAds, Digital Turbine, Perion Network, PubMatic, Tremor International

SOLD: Accenture, Hakuhodo, Medallia, New York Times, SAP

Portfolio Positioning (as of December 31, 2021)

Source: Bloomberg

Outlook

The table below shows the Fund’s 1-year forward earnings and sales growth (analyst consensus estimates) versus the MSCI World Index.1

| As of 12/31/2021 | 1-yr forward earnings growth | 1-yr forward sales growth |

| Fund | 15.0% | 16.0% |

| MSCI World Net TR | 6.7% | 6.1% |

Source: Bloomberg; SmartETFs

The Fund at year end has higher expected sales and earnings growth vs the broad market and this is characteristic of the secular growth that the advertising tech/marketing tech industries are expected to experience.

Whilst there may be volatility in equity markets and for advertising tech companies, there is good reason to be optimistic as we continue into 2022. A build-up of cash for both the average consumer and corporation, and government continuing to push through large stimulus packages should translate into robust near-term gross domestic product (GDP) growth. In particular, we continue to see an acceleration in technological transformations post-COVID that will have a lasting effect on how consumers and businesses operate. As such, we believe the Fund and its holdings are well positioned to benefit from such transformations, which include the move from traditional to digital advertising.

Sagar Thanki

January 2022

International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

Growth stocks typically are more volatile than value stocks; however, value stocks have a lower expected growth rate in earnings and sales.

The companies in which the Fund invests may be subject to rapid changes in technology, intense competition, rapid obsolescence of products and services, loss of intellectual property protections, evolving industry standards and frequent new product productions and changes in business cycles and government regulations.

These risks could adversely affect the value of companies in which the Fund invests. Limitations on applications for autonomous or electric vehicles could adversely affect the value of companies in which the Fund invests.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

The S&P 500 Index is a stock market index tracking the performance of 500 large companies listed on stock exchanges in the United States.

One cannot invest directly in an index.

| 1 | Earnings growth is not a measure of the Fund’s future performance. |

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings, and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

| SmartETFs Advertising & Marketing Technology ETF |

| FUND PERFORMANCE AND SUMMARY |

| As of December 31, 2021 (Unaudited) |

Average Annual Returns

December 31, 2021 | One Year | Since Inception

(12/31/2020) |

| SmartETFs Advertising & Marketing Technology ETF - NAV | 6.69% | 6.67% |

| SmartETFs Advertising & Marketing Technology ETF - Market | 6.38% | 6.36% |

| MSCI World Index NR | 21.82% | 21.82% |

The performance data quoted represents past performance and past performance is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.smartetfs.com.

Total returns reflect the reinvestment of distributions made by the Fund, if any. The deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares is not reflected in the total returns.

The Fund's shares are listed on an exchange. The price of the Fund's shares is based on market price, and because the exchange-traded fund shares trade at market prices rather and net asset value, shares may trade at a price greater than net asset value (premium) or less than net asset value (discount).

The MSCI World Index (Net Return) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. Net Return reflects deduction for withholding tax but reflects no duduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay.

SmartETFs Advertising & Marketing Technology ETF

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 99.5% | | Value ($) | |

| | | | | Advertising: 55.1% | | | | |

| | 2,325 | | | AcuityAds Holdings Inc.* | | $ | 8,742 | |

| | 50 | | | Alphabet Inc.* | | | 144,852 | |

| | 380 | | | Baidu Inc.* | | | 56,540 | |

| | 4,000 | | | CyberAgent Inc.* | | | 66,519 | |

| | 1,400 | | | Digital Turbine Inc.* | | | 85,386 | |

| | 3,500 | | | Future PLC | | | 181,343 | |

| | 2,230 | | | Magnite Inc.* | | | 39,025 | |

| | 310 | | | Meta Platforms Inc. - Class A* | | | 104,269 | |

| | 5,300 | | | Perion Network Ltd. | | | 127,465 | |

| | 2,550 | | | PubMatic Inc.* | | | 86,828 | |

| | 260 | | | Roku Inc.* | | | 59,332 | |

| | 1,440 | | | TechTarget Inc.* | | | 137,750 | |

| | 1,000 | | | Trade Desk Inc/The* | | | 91,640 | |

| | 3,832 | | | Tremor International Ltd.* | | | 58,055 | |

| | 2,000 | | | ValueCommerce Co., Ltd. | | | 77,675 | |

| | 1,280 | | | Yandex NV* | | | 77,440 | |

| | 14,000 | | | Z Holdings Corp. | | | 81,182 | |

| | | | | | | | 1,484,042 | |

| | | | | Enterprise Software/Services: 5.2% | | | | |

| | 370 | | | Atlassian Corp PLC* | | | 141,077 | |

| | | | | | | | | |

| | | | | Internet Content: 2.2% | | | | |

| | 1,000 | | | Tencent Holdings Ltd. | | | 58,590 | |

| | | | | | | | | |

| | | | | Marketing Technology: 37.0% | | | | |

| | 170 | | | Adobe Inc.* | | | 96,400 | |

| | 4,020 | | | Criteo SA* | | | 156,257 | |

| | 220 | | | HubSpot Inc.* | | | 145,013 | |

| | 8,040 | | | iClick Interactive Asia Group Ltd.* | | | 37,064 | |

| | 1,180 | | | LiveRamp Holdings Inc.* | | | 56,581 | |

| | 660 | | | Pegasystems Inc. | | | 73,801 | |

| | 3,870 | | | QuinStreet Inc.* | | | 70,395 | |

| | 12,280 | | | S4 Capital PLC* | | | 105,323 | |

| | 380 | | | salesforce.com Inc.* | | | 96,569 | |

| | 40,000 | | | Weimob Inc.* | | | 40,480 | |

| | 1,850 | | | ZoomInfo Technologies Inc.* | | | 118,770 | |

| | | | | | | | 996,654 | |

| | | | | | | | | |

| | | | | Total Common Stocks (Cost $2,558,350) | | | 2,680,364 | |

| | | | | | | | | |

| | | | | Total Investments (Cost $2,558,350) - 99.5% | | | 2,680,364 | |

| | | | | Other Assets in Excess of Liabilities - 0.5% | | | 13,266 | |

| | | | | Total Net Assets - 100.0% | | $ | 2,693,630 | |

| * | Non-income producing security. |

ADR - American Depository Receipt

PLC - Public Limited Company

The accompanying notes are an integral part of these financial statements.

SmartETFs Advertising & Marketing Technology ETF

Schedule of Investments

at December 31, 2021

| Country Breakdown | Percent of Total

Net Assets |

| Common Stocks | |

| Unites States | 52.2% |

| United Kingdom | 10.6% |

| Japan | 8.4% |

| Israel | 6.9% |

| France | 5.8% |

| China | 5.8% |

| Australia | 5.2% |

| Russia | 2.9% |

| Hong Kong | 1.4% |

| Canada | 0.3% |

| Total Investments | 99.5% |

| Other Assets in Excess of Liabilities | 0.5% |

| Total Net Assets | 100.0% |

The accompanying notes are an integral part of these financial statements.

GUINNESS ATKINSON SMARTETFS SUSTAINABLE ENERGY II ETF

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

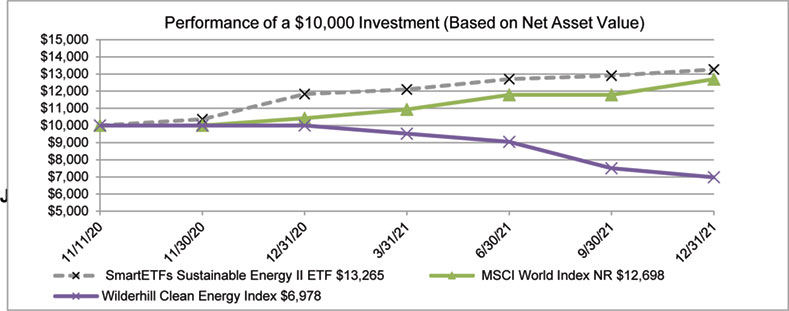

| Average annualized Total returns | 1

Year | Since Inception

11/11/2020 |

| Sustainable Energy II ETF (Net Asset Value) | 12.11% | 28.22% |

| Sustainable Energy II ETF (Market Price) | 11.54% | 30.17% |

| | | |

| Benchmark Indices: | | |

| MSCI World Index (Net Return) | 21.82% | 30.80% |

The Fund’s total expense ratio is 1.91% and the net expense ratio is 0.79%. The Adviser has contractually agreed to reduce its fees and/or pay ETF expenses in order to limit the Fund's total annual operating expenses to 0.68% through June 30, 2025. For the Fund’s current one-year expense ratios, please refer to the Financial Highlights section of this report.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.smartetfs.com, or calling (866) 307-5990.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns. SmartETFs NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times.

The SmartETFs Sustainable Energy II ETF is positioned to benefit from the many opportunities associated with the sustainable energy transition that we have discussed. As part of our investment process, we have identified a universe of around 250 companies (market capitalisation of over USD$500m) that are most directly exposed to the theme, and classify them into the following four sub-sectors:

| ● | Displacement includes companies involved in the displacement or more efficient usage of existing hydrocarbon-based energy |

| ● | Electrification includes companies involved specifically in the switching of hydrocarbon-based fuel demand towards electricity, especially for electric vehicles |

| ● | Generation includes companies involved in the generation of sustainable energy, either pureplay companies or those transitioning from hydrocarbon-based fuels |

| ● | Installation (Equipment) includes companies involved in the manufacturing of equipment for the generation and consumption of sustainable energy |

Sustainable Energy equities delivered a positive return in 2021 with the SmartETFs Sustainable Energy II ETF delivering 12.11% return (net asset value) in USD terms while the MSCI World Index Net Return index delivered 21.82%.

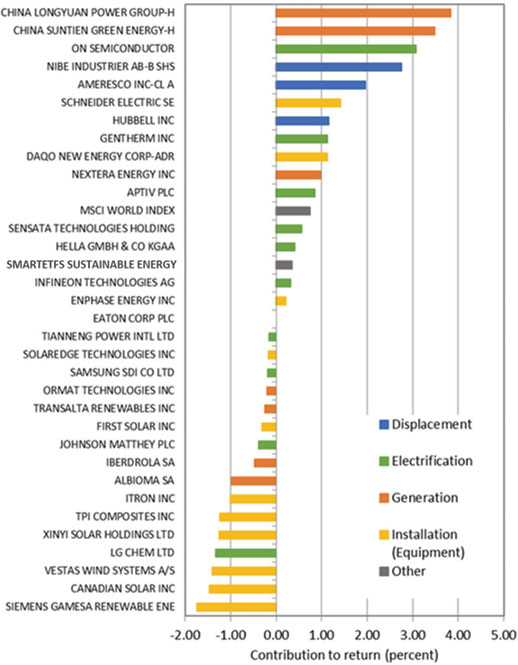

The largest positive contributors to the Fund in 2021 were our two Chinese generation companies (independent power producers) China Longyuan and China Suntien. At the start of the year, China Longyuan announced a corporate transaction with its parent company CNH Energy and its sister company Pingzhuang Energy that provided China Longyuan with a China A share listing while China Suntien’s share price increase reflected strong profit growth resulting from the start-up of new wind projects. Their strong performance was sustained through the third quarter of 2021 as the Chinese economy rebounded strongly and warm weather increased air conditioning demand, driving higher electricity prices and better margins for both.

Within electrification, Onsemi enjoyed numerous earnings upgrades through the year, as demand and pricing for its semiconductor products both rose. The company announced plans to prune both its revenue base and manufacturing footprint to invest in high-value, high-growth applications served by its power and sensing-biased semiconductor portfolio. Growth will be sacrificed in the 2022/2023 period while it focuses on higher margin businesses. Also, within electrification, Gentherm delivered strong results and good new contract awards, including a first production vehicle award for its new “ClimateSense” product which combines several individual product lines (such as thermal products, electronics and software) into a system solution.

With displacement, Nibe Industrier was the greatest contributor, with the shares reacting to strong demand for heat pumps, solid underlying business performance and a share split that increased accessibility of its shares. Of particular note was the company’s North American Climate Solutions business returning to growth and signs that Nibe’s decentralised business model was providing good insulation against raw material cost inflation. Ameresco and Hubbell also delivered strong contribution over the year.

The equipment (installation) sector was the weakest contributor with only three companies delivering a positive contribution over the year. Of note was Schneider Electric, whose shares reacted positively to consistent improvements in business performance, and polysilicon manufacturer Daqo New Energy which delivered a significant contribution to the Fund during the first quarter of the year (prior to its sale from the portfolio) as a result of strong polysilicon demand and rising polysilicon prices.

While the strongest performers came from all four sub sectors, the weaker performers came predominantly from the equipment (installation) sector. Siemens Gamesa, TPI Composites and Vestas Wind Systems suffered from slowing momentum within the near-term wind macro environment (compounded by supply chain pressures and raw material inflationary concerns) that trumped longer-term positive wind industry developments.

Other weak contributors included LG Chem whose shares were weak following a $1.9bn product recall with GM regarding battery faults on the Chevrolet Bolt, and two generation companies, Albioma and Iberdrola, which de-rated as a result of general market concerns around rising interest rates and the risk of greater regulation to compensate for higher fossil fuel prices.

2021 individual stock contribution, in USD

source: Bloomberg, Guinness Atkinson Asset Management estimates

In terms of attribution relative to the Guinness sustainable energy universe, the Fund delivered positive sector allocation and stock selection within efficiency (due to a small sector overweight and advantaged stock selection as described above); electric vehicles (due to a bias towards power semiconductors and electronics and avoidance of recently listed US special purpose acquisition companies (SPACs)); within independent power producers (IPPs) (due to exposure to Chinese wind-dominated IPPs and the avoidance of US residential solar and pure-play high-growth solar IPPs that were weaker as a result of rising interest rate concerns); and within other equipment (due to avoidance of weak hydrogen fuel cell and electrolyser companies as well as newly listed energy storage stocks).

The Fund delivered negative sector allocation and stock selection within batteries (due to lack of exposure to battery raw material companies as well as pure-play cathode and anode manufacturers); and within solar and wind equipment (where we held overweight positions to sectors and manufacturing companies that suffered from raw material cost inflation and supply chain issues).

Early in the year, we sold Daqo New Energy and replaced the holding with a position in Infineon Technologies. We also added Eaton towards the end of the year.

| ● | Daqo is a fast growing, low cost, China based manufacturer of polysilicon, whose shares increased by more than eight times since the start of 2019. While underlying profitability has increased at Daqo, we are concerned that the share price now fully reflects a very optimistic outlook for long term polysilicon pricing and company growth. |

| ● | Infineon Technologies designs, manufactures, and markets semiconductors with a focus on the automotive, industrial power control, power management and digital security markets. Having recently acquired Cypress Semi, we believe that Infineon is very well placed to benefit from the industry’s need for greater semiconductor (especially power semiconductor) content in electric vehicles. |

| ● | Eaton is a US listed, US$65bn market capitalisation specialized producer of highly engineered products and services. These offerings are designed to solve customer pain points in vital portions of the world’s infrastructure. We believe Eaton has mostly positioned its portfolio in profitable niches that should benefit from secular trends like energy transition and electrification, to propel long-term growth. |

The sector and geographic weightings of the portfolio at December 31, 2021 were as follows:

| Sector breakdown | Dec. 31, 2021 |

| Displacement | |

| Efficiency | 11.8% |

| Electrification | |

| Battery | 8.1% |

| Electric vehicles | 23.7% |

| Generation | |

| IPP | 15.0% |

| Utility | 8.1% |

| Installation | |

| Equipment | 28.5% |

| Cash | 4.8% |

| Total | 100% |

| Geographic breakdown | Dec 31, 2021 |

| USA | 38.7% |

| China | 9.8% |

| Germany | 7.3% |

| France | 6.5% |

| Spain | 6.4% |

| Canada | 6.1% |

| South Korea | 5.6% |

| Sweden | 4.1% |

| Ireland | 3.9% |

| Denmark | 2.5% |

| UK | 2.5% |

| Israel | 1.8% |

| Cash | 4.8% |

The year of 2021 saw continued positive momentum for the energy transition. Policy commitments and investments were made to accelerate the decarbonisation of the global energy sector. Offsetting this, we saw raw material cost inflation, supply chain issues and some political tensions which have slowed the pace of growth and profitability in certain subsectors. Against this backdrop, our portfolio has seen improved cash return expectations versus twelve months ago. It continues to offer broad exposure to companies that are well placed to benefit from an energy transition that will gather pace through the remainder of this decade.

After very strong policy support in 2020, we witnessed further policy commitment in 2021. The most significant policy milestones last year included:

| ● | President Biden returning the US to the Paris Agreement, and announcing significantly increased 2030 Greenhouse Gas (GHG) reduction targets; |

| ● | the influential 2021 Intergovernmental Panel on Climate Change (IPCC) climate report, which highlighted the importance and urgency of pursuing a 1.5° warming or net zero 2050 scenario; |

| ● | the Conference of the Parties (COP)-15 Biological Diversity Conference, at which President Xi gave more clarity on how China would meet its climate targets over the coming years, including a major expansion in solar; and |

| ● | and the COP26 climate conference, which introduced new net zero targets, additional country pledges and some “alliances of the willing” to reduce coal usage and methane emissions. |

In addition to enhanced policy commitment, 2021 saw major steps forward for various aspects of the transition. We saw around 290 GW of new renewable generation capacity installed, 10 GW (gigawatt) higher than the record installations seen in 2020 and nearly 100 GW higher than the 194 GW installed in 2019. Solar represented nearly two-thirds of the new capacity additions, followed by wind then hydro. Renewable electricity generation increased by around 6% to over 7,900 TWh (terawatt-hour), outpacing global electricity demand growth (4.5% in 2021). Electric vehicle sales surged, reaching around 7% of global light auto sales, up from just over 3% in 2020. Sales were particularly strong in China and Europe. And investment into energy efficiency also accelerated, with building infrastructure remaining a key focus for spending.

2021 was also a year in which the complexities of a shift to a lower carbon economy become more evident.

In Europe, record natural gas prices became a major political headache, forcing governments to seek protection for consumers from the extreme price spike. On the one hand, observers could point to extraordinarily high post-pandemic power demand, plus the tactics of President Putin to withhold gas exports into Europe, as reasons for the extreme prices. But on the other hand, the spike has been driven by an attempt to shift away from carbon intensive coal usage in China, and the impact of a rapidly rising carbon price in Europe, which is affecting the behaviour of utilities.

In the US, Democratic Senator Joe Manchin has blocked the path of the “Build Back Better” (BBB) bill, a cornerstone spending plan of the current administration which includes various clean energy related provisions designed to accelerate the transition. Manchin represents West Virginia, a major coal producing state, and claims the bill will “risk the reliability of our electric grid and increase our dependence on foreign supply chains”.

After many years of consistent cost reductions, 2021 also saw the emergence of inflationary conditions and supply chain pressures across the breadth of the sustainable energy sector. Energy transition technologies and equipment are typically raw material intensive (leaving them exposed to raw material inflation) and are dominated by Chinese manufacturing (50% of all wind turbines and 70% of all solar panels are manufactured in China), leaving importers exposed to supply chain inefficiencies and higher freight costs.

Natural gas prices will moderate; there will be a resolution to Manchin’s opposition to BBB, and most areas of raw material inflation will settle down and be trumped by scale and technological improvements. But the world is waking up to the fact that although the energy transition will result in economic and environmental gains, policy decisions have the potential in the short-term to cause economic and political friction.

Against this backdrop, the SmartETFs Sustainable Energy II ETF has seen improved cash return expectations and delivered a total return (USD) (net asset value) of +12.07% vs the MSCI World Index (net return) of +21.82%. Within the portfolio, outperforming sectors included Chinese wind generation, electric vehicle (EV) component suppliers, polysilicon (for solar) and efficiency. Underperforming sectors included European green utilities, solar component manufacturers and wind developers.

Looking ahead to 2022 and beyond, we expect further acceleration of the transition:

| ● | On the supply side of the energy transition, the International Energy Agency (IEA) is forecasting that renewable power additions over the coming five years will be just over 1,800 GW; a near 50% increase on its previous five-year forecast published twelve months earlier. The increase is driven by a further reduction in the levelized cost of electricity for renewables. |

| ● | The IEA has described solar power as “the cheapest electricity in history” and, despite near term headwinds and cyclical cost inflationary factors, large-scale solar remains at the bottom end of the cost curve. Globally, we expect solar installations to grow in 2022 by over 20%, led by China, India, Middle East and other parts of Asia. It is likely that poly-silicon prices have peaked, bringing cost relief for cell and module manufacturers. The outlook for solar in the US this year is less certain due to various issues (stimulus spending, net metering and Chinese import issues). |

| ● | Global wind installations are expected to be around flat in 2022, as changes in tax incentives, COVID-related logistics issues and raw material cost inflation are worked through. Onshore installations should pick up meaningfully in the middle of the decade, and there is clear momentum in offshore wind, albeit with a 3-4 year lead time. President Biden has recently called for the US to have 30 GW of offshore wind by 2030 (current installed base = <1 GW), which would represent a step change for the industry. |

| ● | Energy efficiency will continue to receive a good proportion of post-COVID stimulus spending, with a continued focus on buildings. We expect an acceleration in the penetration of LED lighting, insulation and heat pumps, as well as a focus on grid and transmission upgrades. The IEA estimates that to meet current government policies, energy efficiency spending needs to increase from a recent average level of around $250bn per annum (pa) to around $375bn this decade and nearly $550bn in the 2030s. |

| ● | EV sales should exceed 9 million in 2022, representing around 10% of total passenger vehicle sales, taking the global EV stock from 16 million vehicles to 25 million vehicles. Lower EV prices, greater brand choice and growing consumer appetite continue to be the key drivers of improved EV sales. |

| ● | Battery demand for use in EVs and energy storage will accelerate in 2022. We expect new battery capacity of nearly 300 GWh to be sold this year, up by around 25% versus 2021. Raw material cost inflation will continue to have an impact in 2022, but rapidly increasingly manufacturing capacity, coupled with technological improvements, will continue to push average battery pack costs towards $100/kWh, the level at which mass market EVs become affordable. |

The outlook we summarise here is broadly consistent with current government activity and observable investment plans. To be clear, however, the growth described falls well short of the energy transition activity needed to achieve a net zero / 1.5 degree scenario in 2050, as targeted by the IPCC and at COP26. In a net zero scenario, the deployment of renewable generation capacity, penetration of EVs and battery storage, use of alternative fuels and implementation of energy efficiency measures will need to accelerate markedly.

At December 31, 2021, the SmartETFs Sustainable Energy II ETF traded on a 2022 P/E ratio of 24.5x and 2022 EV/EBITDA multiple of 13.2x. The Fund trades at about a 20% premium to the MSCI World Index, which we see as justified given the attractive growth rates available to invest in across the sector. As a sense check, consensus EPS growth (2021-2023E) of the portfolio (at 21.3% pa) is well ahead of the MSCI World (at 13.5% pa). Looking over the next five years, we believe that the portfolio is in a position to deliver average earnings growth.

Jonathan Waghorn and Will Riley

January 2022

Definitions

P/E Ratio is the price-to-earnings ratio and is a ratio for valuing a company that measures its current share price relative to its earnings per share.

EV/EBITDA is the enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA). This ratio is used by investment managers to measure a company’s return on investment.

International investments involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume.

The companies in which the Fund invests may be subject to rapid changes in technology, intense competition, rapid obsolescence of products and services, loss of intellectual property protections, evolving industry standards and frequent new product productions and changes in business cycles and government regulations.

These risks could adversely affect the value of companies in which the Fund invests. Limitations on applications for autonomous or electric vehicles could adversely affect the value of companies in which the Fund invests.

MSCI World Index A free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. One cannot invest directly in an index.

Please refer to the Schedule of Investments for details on Fund holdings. Current and future portfolio holdings are subject to risk.

The information provided herein represents the opinion of Guinness Atkinson Asset Management, Inc. for the period stated and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions, Fund holdings and sector allocations are subject to change at any time, and are not recommendations to buy or sell any security.

Sustainable Energy II ETF

FUND PERFORMANCE AND SUMMARY

As of December 31, 2021 (Unaudited)

Average Annual Returns

December 31, 2021 | One Year | Since Inception

(11/11/2020) |

| Sustainable Energy II ETF - NAV | 12.11% | 28.22% |

| Sustainable Energy II ETF - Market | 11.54% | 30.17% |

| MSCI World Index NR | 21.82% | 30.80% |

The performance data quoted represents past performance and past performance is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of theFund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.smartetfs.com.

Total returns reflect the reinvestment of distributions made by the Fund, if any. The deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares is not reflected in the total returns.

The Fund's shares are listed on an exchange. The price of the Fund's shares is based on market price, and because the exchange-traded fund shares trade at market prices rather and net asset value, shares may trade at a price greater than net asset value (premium) or less than net asset value (discount).

The MSCI World Index (Net Return) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. Net Return reflects deduction for withholding tax but reflects no duduction for fees and expenses. Net Return is net of local withholding taxes that any investor would pay.

SmartETFs Sustainable Energy II ETF

Schedule of Investments

at December 31, 2021

| Shares | | | Common Stocks: 96.2% | | Value ($) | |

| | | | | Electrification: 39.0% | | | | |

| | 1,422 | | | Aptiv PLC* | | $ | 234,559 | |

| | 2,898 | | | Gentherm Inc.* | | | 251,836 | |

| | 2,896 | | | Hella GmbH & Co. KGaA | | | 196,378 | |

| | 5,202 | | | Infineon Technologies AG | | | 241,241 | |

| | 2,214 | | | Itron Inc.* | | | 151,703 | |

| | 5,346 | | | Johnson Matthey PLC | | | 147,968 | |

| | 288 | | | LG Chem Ltd. | | | 148,984 | |

| | 3,744 | | | ON Semiconductor Corporation* | | | 254,293 | |

| | 342 | | | Samsung SDI Co., Ltd. | | | 188,426 | |

| | 1,296 | | | Schneider Electric SE | | | 254,296 | |

| | 3,906 | | | Sensata Technologies Holding* | | | 240,961 | |

| | | | | | | | 2,310,645 | |

| | | | | Energy Efficiency: 11.9% | | | | |

| | 2,898 | | | Ameresco Inc.* | | | 236,013 | |

| | 1,080 | | | Hubbell Inc. | | | 224,932 | |

| | 16,272 | | | Nibe Industrier AB - B Shares | | | 246,010 | |

| | | | | | | | 706,955 | |

| | | | | | | | | |

| | | | | Renewable Energy Generation: 28.0% | | | | |

| | 3,438 | | | Albioma SA | | | 134,089 | |

| | 95,994 | | | China Longyuan Power Group Corp Ltd. | | | 224,087 | |

| | 228,000 | | | China Suntien Green Energy Corp Ltd. | | | 177,803 | |

| | 612 | | | Enphase Energy Inc.* | | | 111,959 | |

| | 18,324 | | | Iberdrola SA | | | 217,029 | |

| | 2,862 | | | Nextera Energy Inc. | | | 267,196 | |

| | 1,764 | | | Ormat Technologies Inc. | | | 139,885 | |

| | 6,984 | | | Siemens Gamesa Renewable Energy SA | | | 167,423 | |

| | 14,850 | | | TransAlta Renewables Inc. | | | 220,187 | |

| | | | | | | | 1,659,658 | |

| | | | | | | | | |

| | | | | Renewable Equipment Manufacturing: 17.3% | | | | |

| | 4,662 | | | Canadian Solar Inc.* | | | 145,874 | |

| | 1,170 | | | Eaton Corp. PLC | | | 202,199 | |

| | 2,340 | | | First Solar Inc.* | | | 203,954 | |

| | 378 | | | Solaredge Technologies Inc.* | | | 106,056 | |

| | 2,088 | | | TPI Composites Inc.* | | | 31,237 | |

| | 4,914 | | | Vestas Wind Systems A/S | | | 150,342 | |

| | 108,000 | | | Xinyi Solar Holdings Ltd. | | | 183,128 | |

| | | | | | | | 1,022,790 | |

| | | | | | | | | |

| | | | | Total Common Stocks (Cost $5,538,510) | | | 5,700,048 | |

| | | | | | | | | |

| | | | | Total Investments (Cost $5,538,510) - 96.2% | | | 5,700,048 | |

| | | | | Other Assets in Excess of Liabilities - 3.8% | | | 226,469 | |

| | | | | Total Net Assets - 100.0% | | $ | 5,926,517 | |

| * | Non-income producing security. |

ADR - American Depository Receipt

PLC - Public Limited Company

The accompanying notes are an integral part of these financial statements.

| SmartETFs Sustainable Energy II ETF |

| Schedule of Investments |

| at December 31, 2021 |

| Country Breakdown | Percent of Total

Net Assets |

| Common Stocks | |

| United States | 38.6% |

| China | 9.8% |

| Germany | 7.4% |

| Spain | 7.0% |

| France | 6.6% |

| Canada | 6.2% |

| South Korea | 5.7% |

| Sweden | 4.1% |

| Ireland | 4.0% |

| Denmark | 2.5% |

| United Kingdom | 2.5% |

| Israel | 1.8% |

| Total Investments | 96.2% |

| Other Assets in Excess of Liabilities | 3.8% |

| Total Net Assets | 100.0% |

The accompanying notes are an integral part of these financial statements.

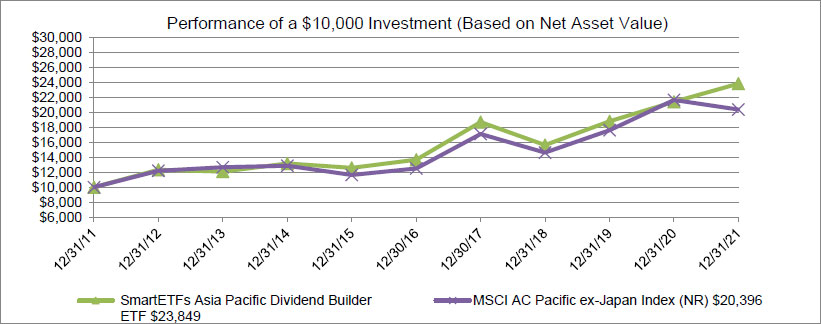

SmartETFs Asia Pacific Dividend Builder ETF

ANNUAL REPORT FOR THE PERIOD ENDED

DECEMBER 31, 2021

1. Performance

| Average annualized Total returns | 1

Year | 3

Years | 5

Years | 10

Years |

| Asia Pacific Dividend Builder ETF (Net Asset Value) | 11.27% | 15.10% | 11.74% | 9.08% |

| Asia Pacific Dividend Builder ETF (Market Price) | 11.72% | 15.26% | 11.83% | 9.12% |

| Benchmark Index: | | | | |

| MSCI AC Pacific Ex Japan Index (net return) | -5.85% | 11.69% | 10.28% | 7.38% |

The Fund’s total expense ratio is 4.97% and the net expense ratio is 0.78%. The Adviser has contractually agreed to reduce its fees and/or pay ETF expenses in order to limit the Fund's total annual operating expenses to 0.68% through June 30, 2025. For the Fund’s current one-year expense ratios, please refer to the Financial Highlights section of this report.

The SmartETFs Asia Pacific Dividend Builder ETF acquired the assets and liabilities of the predecessor mutual fund, the Guinness Atkinson Asia Pacific Dividend Builder Fund, on March 26, 2021. As a result of the transaction, the Fund adopted the accounting and performance history of its predecessor mutual fund Performance results shown prior to March 26, 2021, reflect the performance of the predecessor mutual fund. The Market Price returns shown prior to March 26, 2021 reflects the predecessor mutual fund's NAV.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by visiting www.smartetfs.com, or calling (866) 307-5990.

Total returns for certain periods reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and the performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distribution or the redemption of Fund shares.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns. SmartETFs NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times.

The Fund rose 11.27% in 2021 compared to the MSCI AC Pacific ex Japan Net Return Index which fell -5.85%.

Most of the absolute gains made by the Fund came in the first half of the year while the relative performance, from holding onto them, came in the second half of the year. Stock selection made an important contribution this year notably with our China exposure outperforming the MSCI China Index. The main contributors to performance in 2021 were our holdings in financials, Health care, and Technology but we also saw contributions coming from holdings in the communication services, consumer discretionary and real estate sectors.

Over the whole COVID period, taking the under-performance in 2020 and its outperformance in 2021, the Fund was up 26.77% and outperformed the index which rose 15.85% by 10.92%