Exhibit 99.1

Exhibit 99.1

(in United States dollars, tabular amounts in millions, except where noted)

MANAGEMENT’S DISCUSSION AND ANALYSIS FOR THE YEAR ENDED DECEMBER 31, 2016

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with the consolidated financial statements of Goldcorp Inc. (“Goldcorp” or “the Company”) for the year ended December 31, 2016 and related notes thereto which have been prepared in accordance with International Financial Reporting Standards (“GAAP” or “IFRS”) as issued by the International Accounting Standards Board (“IASB”). All figures are in United States (“US”) dollars unless otherwise noted. References to C$ are to Canadian dollars. This MD&A has been prepared as of February 15, 2017.

TABLE OF CONTENTS

|

| | |

| | | Page Number |

| Cautionary Statements | |

| 2016 Highlights | |

| Business Overview and Strategy | |

| 2016 Achievements | |

| Market Overview | |

| Annual Results | |

| Fourth Quarter Results | |

| Liquidity and Capital Resources | |

| Guidance | |

| Operational and Projects Review | |

| 2016 Reserves and Resources | |

| Non-GAAP Performance Measures | |

| Risks and Uncertainties | |

| Accounting Matters | |

| Controls and Procedures | |

| Reserves and Resources | |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This MD&A contains “forward-looking statements” within the meaning of Section 27A of the United States Securities Act of 1933, as amended, Section 21E of the United States Exchange Act of 1934, as amended, the United States Private Securities Litigation Reform Act of 1995, or in releases made by the United States Securities and Exchange Commission, all as may be amended from time to time, and "forward-looking information" under the provisions of applicable Canadian securities legislation, concerning the business, operations and financial performance and condition of Goldcorp. Forward-looking statements include, but are not limited to, statements with respect to the future price of gold, silver, copper, lead and zinc, the estimation of Mineral Reserves (as defined below) and Mineral Resources (as defined below), the realization of Mineral Reserve estimates, the timing and amount of estimated future production, costs of production, targeted cost reductions, capital expenditures, free cash flow, costs and timing of the development of new deposits, success of exploration activities, permitting time lines, hedging practices, currency exchange rate fluctuations, requirements for additional capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, timing and possible outcome of pending litigation, title disputes or claims and limitations on insurance coverage. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” , “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes”, or variations or comparable language of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, "should", “might” or “will be taken”, “occur” or “be achieved” or the negative connotation thereof.

Forward-looking statements are necessarily based upon a number of factors and assumptions that, if untrue, could cause the actual results, performances or achievements of Goldcorp to be materially different from future results, performances or achievements expressed or implied by such statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which Goldcorp will operate in the future, including the price of gold, anticipated costs and ability to achieve goals. Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, among others, gold price volatility, discrepancies between actual and estimated production, Mineral Reserves and Mineral Resources and metallurgical recoveries, mining operational and development risks, litigation risks, regulatory restrictions (including environmental regulatory restrictions and liability), changes in national and local government legislation, taxation, controls or regulations and/or change in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company does or may carry on business in the future, delays, suspension and technical challenges associated with capital projects, higher prices for fuel, steel, power, labour and other consumables, currency fluctuations, the speculative nature of gold exploration, the global economic climate, dilution, share price volatility, competition, loss of key employees, additional funding requirements and defective title to mineral claims or property. Although Goldcorp believes its expectations are based upon reasonable assumptions and has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, level of activity, performance or achievements of Goldcorp to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to international operations, including economic and political instability in foreign jurisdictions in which Goldcorp operates; risks related to current global financial conditions; risks related to joint venture operations; actual results of current exploration activities; actual results of current reclamation activities; environmental risks; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; future prices of gold, silver, copper, lead and zinc; possible variations in ore reserves, grade or recovery rates; failure of plant, equipment or processes to operate as anticipated; mine development and operating risks; accidents, labour disputes and other risks of the mining industry; risks associated with restructuring and cost-efficiency initiatives; delays in obtaining governmental approvals or financing or in the completion of development or construction activities; risks related to the integration of acquisitions; risks related to indebtedness and the service of such indebtedness, as well as those factors discussed in the section entitled "Description of the Business – Risk Factors” in Goldcorp’s most recent annual information form available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. Although Goldcorp has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Forward-looking statements are made as of the date hereof and, accordingly, are subject to change after such date. Except as otherwise indicated by Goldcorp, these statements do not reflect the potential impact of any non-recurring or other special items or of any disposition, monetization, merger, acquisition, other business combination or other transaction that may be announced or that may occur after the date hereof. Forward-looking statements are provided for the purpose of providing information about management’s current expectations and plans and allowing investors and others to get a better understanding of Goldcorp's operating environment. Goldcorp does not intend or undertake to publicly update any forward-looking statements that are included in this document, whether as a result of new information, future events or otherwise, except in accordance with applicable securities laws.

CAUTIONARY STATEMENT REGARDING CERTAIN MEASURES OF PERFORMANCE

This MD&A presents certain measures, including "total cash costs: by-product", "total cash costs: co-product", ‘‘all-in sustaining costs" and ‘‘adjusted operating cash flow’’, that are not recognized measures under IFRS. This data may not be comparable to data presented by other gold producers. For a reconciliation of these measures to the most directly comparable financial information presented in the consolidated financial statements prepared in accordance with IFRS, see Non-GAAP Financial Performance Measures in this MD&A. The Company believes that these generally accepted industry measures are realistic indicators of operating performance and are useful in performing year over year comparisons. However, these non-GAAP measures should be considered together with other data prepared in accordance with IFRS, and these measures, taken by themselves, are not

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

necessarily indicative of operating costs or cash flow measures prepared in accordance with IFRS. This MD&A also contains information as to estimated future all-in sustaining costs. The estimates of future all-in sustaining costs are not based on total production cash costs calculated in accordance with IFRS, which forms the basis of the Company’s cash costs: by-product. The estimates of future all-in sustaining costs are anticipated to be adjusted to include sustaining capital expenditures, corporate administrative expense, exploration and evaluation costs and reclamation cost accretion and amortization, and exclude the effects of expansionary capital, tax payments, dividends and financing costs. Projected IFRS total production cash costs for the full year would require inclusion of the projected impact of future included and excluded items, including items that are not currently determinable, but may be significant, such as sustaining capital expenditures, reclamation cost accretion and amortization and tax payments. Due to the uncertainty of the likelihood, amount and timing of any such items, the Company does not have information available to provide a quantitative reconciliation of projected all-in sustaining costs to a total production cash costs projection.

CAUTIONARY NOTE REGARDING RESERVES AND RESOURCES

Scientific and technical information contained in this MD&A relating to Mineral Reserves and Mineral Resources was reviewed and approved by Gil Lawson, P.Eng., Vice President, Geology and Mine Planning for Goldcorp, and a “qualified person” as defined by Canadian Securities Administrators' National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”). Scientific and technical information in this MD&A relating to exploration results was reviewed and approved by Sally Goodman, PhD, PGeo, Director, Generative Geology for Goldcorp, and a "qualified person" as defined by NI 43-101. All Mineral Reserves and Mineral Resources have been calculated in accordance with the standards of the Canadian Institute of Mining, Metallurgy and Petroleum ("CIM") and NI 43-101, or the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves equivalent. All Mineral Resources are reported exclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Information on data verification performed on the mineral properties mentioned in this MD&A that are considered to be material mineral properties to the Company are contained in Goldcorp’s most recent annual information form and the current technical report for each of those properties, all available on SEDAR at www.sedar.com.

Cautionary Note to United States investors concerning estimates of measured, indicated and inferred resources: The Mineral Resource and Mineral Reserve estimates contained in this MD&A have been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws and uses terms that are not recognized by the United States Securities and Exchange Commission (“SEC”). Canadian reporting requirements for disclosure of mineral properties are governed by NI 43-101. The definitions used in NI 43-101 are incorporated by reference from the CIM Definition Standards adopted by CIM Council on May 10, 2014 (the “CIM Definition Standards”) . U.S. reporting requirements are governed by the SEC Industry Guide 7 (“Industry Guide 7”) under the United States Securities Act of 1933, as amended. These reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but embody difference approaches and definitions. For example, the terms “Mineral Reserve”, “Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms as defined in in NI 43-101, and these definitions differ from the definitions in Industry Guide 7. Under Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. Further, under Industry Guide 7, mineralization may not be classified as "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

While the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and required to be disclosed by NI 43-101, these terms are not defined terms under Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. United States readers are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves. In addition, “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. A significant amount of exploration must be completed in order to determine whether an Inferred Mineral Resource may be upgraded to a higher category. Under Canadian regulations, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. United States readers are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations if such disclosure includes the grade or quality and the quantity for each category of Mineral Resource and Mineral Reserve; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this MD&A containing descriptions of the Goldcorp’s mineral deposits may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

FULL YEAR FINANCIAL AND OPERATIONAL HIGHLIGHTS

Net earnings of $162 million, or $0.19 per share, compared to a net loss of $4.2 billion, or loss of $5.03 per share, in 2015. Net earnings were negatively affected by $0.12 per share of non-cash or other items that the Company believes are not reflective of the performance of the underlying operations.

Operating cash flows of $799 million and adjusted operating cash flows of $1.1 billion(1). Available liquidity was $3.17 billion at December 31, 2016.

Gold production of 2,873,000 ounces at all-in sustaining costs ("AISC") of $856 per ounce, compared to 3,464,000 ounces at AISC of $894 in 2015(1). Gold production was in line with the Company's 2016 guidance with AISC at the low end of the Company's guidance of between $850 and $925 per ounce and was $38 per ounce, or 4%, lower than 2015. The decrease in AISC during the year reflects the Company's focus on cost reductions and the positive effects of the strengthening US dollar. The impact of these reductions was partially offset by lower production at Peñasquito and the exhaustion of surface stockpiles at Cerro Negro and Éléonore.

Renewed growth strategy projected to achieve a 20% increase in gold production, 20% increase in gold reserves and a 20% reduction in our AISC over the next five years. The Company expects the ramp-up to nameplate capacity at Cerro Negro and Éléonore, a continued focus on productivity and efficiency improvements at our existing camps and the advancement of our robust project pipeline to position the Company to deliver significant growth in net asset value per share.

Identified 60% of the targeted $250 million in sustainable efficiencies; 40% delivered by the end of 2016. The Company is well underway toward achieving its $250 million target in sustainable annual efficiencies by 2018 as initiatives at Cerro Negro and corporate offices have been implemented with associated annual savings of $65 million and $50 million, respectively. A further $35 million of improvement initiatives have been identified at Porcupine.

Optimized the portfolio. Following the acquisition of the Coffee project in July 2016, the Company announced in January 2017 that it entered into agreements to sell each of its Los Filos mine in Mexico for estimated consideration of $438 million, and its 100% interest in the Cerro Blanco project in Guatemala for potential consideration of up to approximately $50 million, including contingent consideration. Both transactions are expected to close in the first quarter of 2017. The acquisition and asset sales are aligned with the Company's strategy to focus on large scale camps, that it believes can deliver economies of scale.

| |

| (1) | The Company has included non-GAAP performance measures on an attributable (or Goldcorp's share) basis throughout this document. AISC per ounce and adjusted operating cash flows are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 46-52 of this MD&A. |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

OVERVIEW

Goldcorp is a leading gold producer focused on responsible mining practices, with production from a portfolio of long-life high quality assets throughout the Americas that it believes positions the Company to deliver long-term value.

The Company’s principal producing mining properties are comprised of the Éléonore, Musselwhite, Porcupine and Red Lake mines in Canada; the Peñasquito mine in Mexico; the Cerro Negro mine in Argentina; and the Pueblo Viejo mine (40.0% interest) in the Dominican Republic.

The Company’s current sources of operating cash flows are primarily from the sale of gold, silver, lead, zinc and copper. Goldcorp's principal product is gold doré with the refined gold bullion sold primarily in the London spot market. As a result, Goldcorp is not dependent on a particular purchaser with regard to the sale of the gold doré. In addition to gold, the Company also produces silver, copper, lead and zinc primarily from concentrate produced at the Peñasquito and Alumbrera mines, which is sold to third party smelters and refineries.

Goldcorp has an investment-grade credit rating, supported by a strong balance sheet, and remains 100% unhedged to gold sales, providing full exposure to gold prices.

STRATEGY

Goldcorp's vision is to create sustainable value for all of its stakeholders by focusing on growing net asset value (“NAV”) per share to generate long-term shareholder value. With a portfolio of large, long-life assets that provide economies of scale, coupled with low cash costs and underpinned by a strong balance sheet, Goldcorp continues to optimize its portfolio of assets and reinvest in the pipeline of organic opportunities to drive increasing NAV per share.

The Company completed a reorganization of its leadership and operations in 2016, moving to a lean, decentralized model. Under the decentralized model, the mine general managers are accountable for growing the NAV of their individual businesses while the focus of the corporate office will be to provide governance, oversight and allocate capital. These changes are expected to result in a streamlined organization focused on delivering long-term shareholder value.

The Company has laid out a growth strategy that is expected to deliver a 20% increase in gold production, a 20% increase in gold reserves and a 20% reduction in all-in sustaining costs over the next five years. In this pursuit, Goldcorp is committed to being responsible stewards of the environment and building collaborative partnerships with communities, governments and all other stakeholders for mutual success.

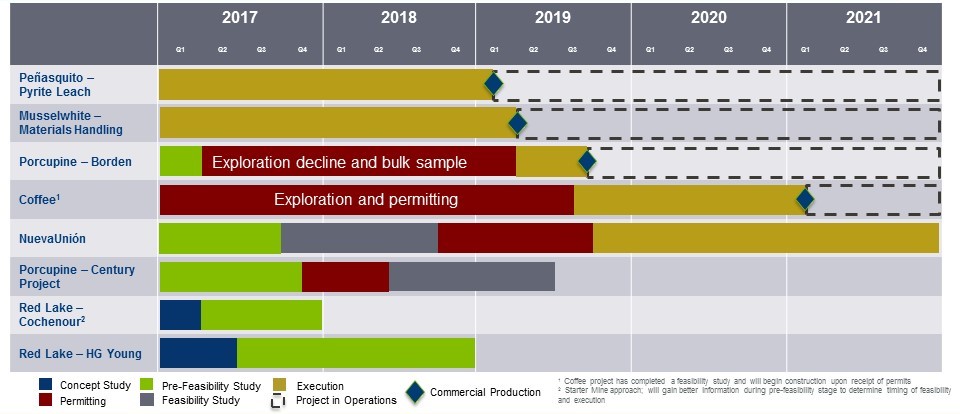

Over the next five years, the Company expects gold production to increase to approximately 3 million ounces. This is a result of the ramp-up to nameplate capacity at Cerro Negro and Éléonore, increased grades at Peñasquito following an intensive stripping campaign, the execution of the Pyrite Leach project at Peñasquito and the Materials Handling project at Musselwhite, and initial production from the Borden project and the Coffee project. This growth profile excludes production potential from the Cochenour and HG Young projects at the Red Lake camp, the Century project at the Porcupine camp and the NuevaUnión project in Chile.

The Company expects AISC to decrease by 20% to approximately $700(1) per ounce over the next five years, driven by a company-wide program launched in 2016 to drive down costs and deliver productivity improvements which is expected to result in approximately $250 million in annual sustainable efficiencies. Costs are also expected to decrease as a result of increased metal production, lower sustaining capital expenditures and continued portfolio optimization. The Company expects reserves to increase by 20% to 50 million ounces over the next five years from the conversion of existing resources at the Century project, Peñasquito, Cerro Negro and Pueblo Viejo and exploration at our extensive and diversified portfolio of mining camps in the Americas.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

With a solid balance sheet, Goldcorp believes it is well-positioned to weather gold price volatility. The Company's capital allocation strategy focuses on investing in its pipeline of organic growth opportunities, further debt reduction and returning capital to its shareholders by paying a sustainable dividend. Furthermore, Goldcorp has the flexibility to take advantage of corporate development opportunities in lower political risk jurisdictions that would be accretive to NAV per share, and leverage its exploration spending in the most efficient way possible through small toehold investments in junior mining companies.

(1) Refer to footnote (3) on page 23 of this MD&A regarding the Company's projection of AISC.

2016 ACHIEVEMENTS

Progress Delivering $250 million of Sustainable Annual Cash Flow Improvements:

During 2016, the Company began implementing a productivity and cost optimization program to deliver $250 million in sustainable annual efficiencies by 2018. Cerro Negro initiated the effort in the second quarter with substantial workforce reductions and other improvement initiatives to reduce costs by $65 million, which were partially offset by temporary setbacks in lower productivity caused by labour disruptions. Goldcorp continues to work on optimizing productivity at Cerro Negro through intensive training of its workforce and productivity improvements. At Porcupine, the Company is targeting $35 million in efficiency improvements and cost reductions in 2017 resulting from improved development rates and productivity at Hoyle Pond, improved productivity at Hollinger and improved recovery and costs at the mill. Further, Goldcorp identified and began executing $50 million in cost reductions in 2016 from general and administrative expenses and capital expenditures from its corporate offices, relative to its 2016 budget. Peñasquito is in the early stages of the productivity and cost optimization efforts, but Goldcorp expects to realize over $50 million in operating cash flow improvements relative to 2016 actual results. Potential opportunities at Peñasquito relate to improved mining and processing and overall equipment effectiveness, and ongoing cost reductions from major contracts. Red Lake and Éléonore started their productivity and cost optimization improvement programs in the first quarter of 2017 and, along with Musselwhite, Goldcorp expects it will attain the balance of the $250 million target by 2018.

Organizational Restructuring and Executive and Senior Management Appointments:

Effective January 1, 2017, Todd White, most recently Senior Vice President, Technical Services and Business Excellence, was appointed Executive Vice-President and Chief Operating Officer. Todd has over two decades of experience in the mining sector. Prior to joining Goldcorp in 2014, he was the Senior Vice President, South America at Newmont Mining Corporation. Since joining Goldcorp he has focused on driving a culture of continuous performance improvement and implemented advancements in efficiency and sustainability through technical innovation.

As part of the Company's organizational re-design in 2016, the Company strengthened the senior management team with the recruitment of several key individuals. Paul Harbidge was appointed Senior Vice President, Exploration reporting to Todd White. Paul is responsible for the development, implementation and management of the global exploration function within the decentralized model. Paul brings over 20 years of mining experience to Goldcorp, most recently as head of exploration at Randgold Resources Limited.

Jason Attew was appointed Senior Vice President, Corporate Development & Strategy, reporting to Russell Ball, Executive Vice President, Chief Financial Officer and Corporate Development. In his role, Jason leads the optimization of the Company’s portfolio of assets, while evaluating new opportunities that are consistent with the Company's strategy of increasing NAV per share. Jason is a mining and metals banking executive with over 20 years of experience.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Wade Bristol was appointed Senior Vice President, Canada, and is responsible for the overall leadership of the Canadian mining operations. Wade joined Goldcorp in July 2014 as the Vice President, Mine Improvement & Support. Prior to Goldcorp he served in various General Manager capacities for Newmont Mining Corporation in North America.

Steven Thomas was appointed to the new role of Chief Financial Officer, Canada, reporting to Wade Bristol, Senior Vice President, Canada and David Splett was appointed to the new role of Chief Financial Officer, Latin America, reporting to Joe Dick, Senior Vice President, Latin America. As part of the regional leadership teams, Steven and David provide financial analysis, interpretation and metrics to facilitate strategic decision making related to the management of the regional businesses. Steven brings over 30 years of financial experience to Goldcorp, with the last 13 years in the mining industry with De Beers Canada Inc. David brings with him over 24 years of experience in the resource industry, most recently as Vice President, Finance for Mosaic Corporation.

Board of Directors Appointment:

In September 2016, the Company announced the appointment Charlie Sartain to its Board of Directors, effective as of January 1, 2017. Mr. Sartain is a mining engineer with over 30 years of mining experience and was previously the Chief Executive Officer of Xstrata's global copper business. His extensive technical knowledge and operational experience will be invaluable as the Company continues to optimize its portfolio and advance the organic pipeline of opportunities.

Advanced Project Pipeline:

Aligned with the Company's strategy to reinvest returns in a pipeline of organic opportunities, Goldcorp committed over a billion dollars of growth capital in 2016. This capital will support the growth in NAV of the Company through an estimated 20% growth in production over the next five years and a 20% decrease in AISC. Growth capital for 2016 included expenditures on the Coffee project following its acquisition on July 19, 2016, Peñasquito's Pyrite Leach project ("PLP"), with an expected capital investment of approximately $420 million, and Musselwhite's Materials Handling project ("MHP"), with an expected capital investment of approximately $90 million. Each of the PLP and MHP are expected to increase gold production commencing in 2019 and the Company is targeting to achieve commercial production at the Coffee project in the first quarter of 2021. During 2016, Goldcorp also advanced the Borden project, located approximately 180 kilometres south-west of Goldcorp's Porcupine mine, where first gold is targeted for 2019.

Renewed Exploration Focus:

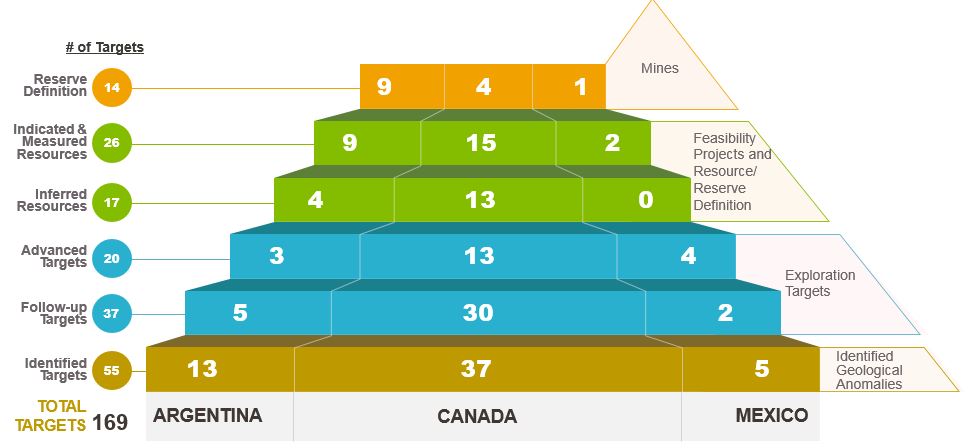

Goldcorp’s exploration strategy is twofold. Firstly, mineral reserve replacement is expected through the conversion of mineral resources and extending known mineralization at the mine sites. Secondly, the development of a pipeline of targets with increasing degrees of confidence are expected to deliver opportunities for future discoveries. The Company implemented this strategy in the third quarter of 2016 by applying both rigorous geological and stringent economic filters to rank and prioritize targets which will then either be advanced or rejected, while generative work ensures a constant supply of new targets. Goldcorp's primary focus is on brownfields exploration and the leverage of the exploration potential within the mining camps to increase the project NAV through new discoveries at Porcupine, Red Lake, Musselwhite, Éléonore, the Coffee project, Peñasquito, Cerro Negro and Pueblo Viejo.

The Company's approach to greenfield exploration is to make toehold investments in junior mining companies which operate in geological prospective terranes and have the technical capabilities to make discoveries that meet Goldcorp’s strategic filters.

Goldcorp restructured its Geology group in 2016 to support its exploration strategy, adding a core team of expert geoscientists covering the principal disciplines of structural geology, geophysics and geochemistry, together with a chief geologist and Directors for the Canadian and Latin American regions who will provide support to the field teams in achieving their objectives.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Corporate Developments:

Acquisition of Kaminak Gold Corporation

On July 19, 2016, the Company completed the acquisition of 100% of the issued and outstanding common shares of Kaminak Gold Corporation ("Kaminak") pursuant to a plan of arrangement (the "Arrangement") for total consideration of approximately C$530 million, including transaction costs. Under the Arrangement, each common share of Kaminak was exchanged for 0.10896 common shares of Goldcorp.

Kaminak's principal asset is the 100% owned Coffee project ("Coffee"), a hydrothermal gold deposit located approximately 130 kilometres south of the City of Dawson, Yukon. Coffee is a high-grade, open pit, heap leach mining project with total gold indicated mineral resources of 3.0 million ounces, inclusive of total gold probable mineral reserves of 2.2 million ounces, and inferred mineral resources of 2.2 million ounces as outlined in the feasibility study prepared for Kaminak by JDS Energy and Mining Inc. in January 2016. The Company estimates average annual gold production of approximately 200,000 ounces for the first five years of production based on Kaminak's feasibility study. The Coffee land package, comprising over 60,000 hectares, demonstrates potential for near-mine discoveries and the potential for the development of a large scale camp that can deliver economies of scale.

The acquisition of Kaminak is consistent with the Company's strategy of partnering with junior exploration companies to identify and develop mining districts with significant exploration potential. Coffee is located within a politically stable jurisdiction and provides Goldcorp with an opportunity to add high quality ounces to our development pipeline at low AISC.

Divestitures

Aligned with the Company's strategy to continually upgrade its portfolio through the divestiture of non-core assets and strengthen its balance sheet, Goldcorp entered into agreements in January 2017 to sell each of its Los Filos Mine in Mexico and its 100% interest in the Cerro Blanco project in Guatemala as described below.

On January 4, 2017, the Company entered into an agreement to sell its 100% interest in the Cerro Blanco project, located in Guatemala, to Bluestone Resources Inc. (“Bluestone”). Under the terms of the agreement, Goldcorp will receive consideration at closing of $18 million in cash, a 1% Net Smelter Return royalty on production, and common shares of Bluestone representing approximately 9.9% of the issued and outstanding shares upon completion of the transaction. Goldcorp will receive an additional $15 million in cash upon declaration of commercial production at Cerro Blanco.

On January 11, 2017, Goldcorp entered into a share purchase agreement (the “Agreement”) with Leagold Mining Corporation (“Leagold”), pursuant to which it has agreed to sell its Los Filos mine in Mexico to Leagold. Under the terms of the Agreement, Goldcorp will receive estimated consideration of $438 million, consisting of $279 million in cash (subject to certain closing adjustments), $71 million in Leagold common shares, and retain certain tax receivables of approximately $88 million. The common shares issued to Goldcorp as consideration are expected to represent approximately 30% of the issued and outstanding shares of Leagold following the closing of the transaction. In connection with the transaction, Goldcorp recognized a reversal of a 2015 impairment in mining interests at Los Filos of approximately $59 million. The transaction is subject to customary closing conditions and is expected to close in the first quarter of 2017.

Acquisition of Gold Stream at El Morro

On February 7, 2017, the Company entered into a binding agreement with New Gold Inc. pursuant to which it agreed to purchase New Gold's 4% gold stream on the El Morro deposit, part of the company's 50/50 NuevaUnión joint venture, for cash consideration of $65 million. The transaction is expected to close in the first quarter of 2017.

Strengthened Balance Sheet:

As Goldcorp exited an intensive phase of capital spending with the completion of construction of the Cerro Negro and Éléonore mines in 2015, the Company focused on deleveraging and strengthening its balance sheet in 2016. At December 31, 2016, the Company's debt was $2.5 billion, a $180 million, or 7%, decrease from December 31, 2015. Including the debt of the Company's associates, at December 31, 2016, the Company's debt was $2.7 billion, a $330 million, or 11%, decrease from December 31, 2015(1). The decrease in the Company's debt was primarily due to the repayment of the Company's Argentine debt in the fourth quarter of 2016. With the repayment of these loans, the Company has no debt repayable until March 2018, when the Company's $500 million notes become due. The remaining $2.0 billion, or 80%, of the Company's debt is not repayable until after 2020.

Liquidity is expected to further improve in the first quarter of 2017 from the expected closing of the sale of the Los Filos mine and Cerro Blanco project.

(1) Includes the Company's share of debt of $160 million and $nil and debt repayments (net) of $100 million and $50 million relating to the Company's investments in Pueblo Viejo and Alumbrera, respectively.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

MARKET OVERVIEW

Gold

The market price of gold is the primary driver of Goldcorp's profitability. The price of gold can fluctuate widely and is affected by a number of industry and macroeconomic factors including the sale or purchase of gold by central banks and financial institutions, interest rates, exchange rates, inflation or deflation, global and regional supply and demand and the political and economic conditions of major gold-producing and gold-consuming countries throughout the world.

The gold market was split during 2016, with a promising rally over the first six months all but erased in a seven-week period following the November US presidential elections. Despite the decline in gold prices in late 2016, in the face of a strong US dollar and the threat of higher interest rates, gold still managed to finish the year with a gain of approximately 8%. After starting 2016 at its lowest price for the year at $1,063 per ounce, the metal rallied steadily to a peak of $1,375 per ounce in early July, aided by geopolitical uncertainty surrounding Britain’s future in the European Union. The metal, however, failed to hold these gains, and closed the year at $1,151 per ounce, well off its peak. The Company realized an average gold price of $1,244 per ounce in 2016 (an 8% increase compared to $1,153 per ounce in 2015) and $1,181 per ounce in the fourth quarter of 2016. Political uncertainty surrounding the transition to a new US government in 2017 is likely to influence the market over the next 12 months, as will elections in a number of European countries and the unknown impact on long-term physical demand of India’s recent demonetization of high value bank notes and efforts to reduce the use of cash in the economy.

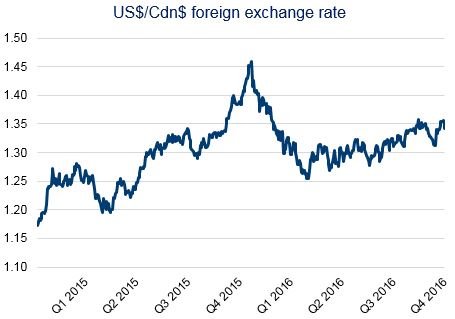

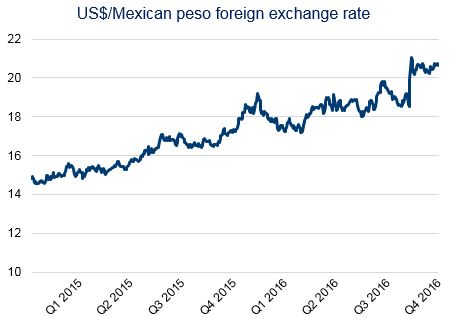

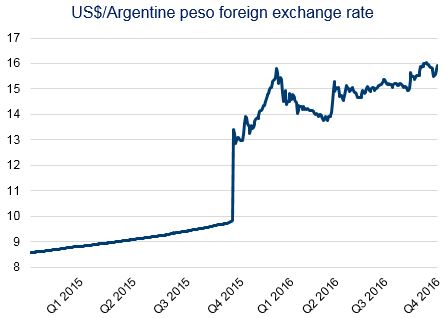

Currency markets

The results of Goldcorp's mining operations are affected by the US dollar exchange rates. The Company has exposure to the Canadian dollar relating to its Red Lake, Éléonore, Porcupine and Musselwhite operations, exposure to the Mexican peso relating to its Peñasquito and Los Filos operations, exposure to the Argentine peso relating to its Cerro Negro operation, exposure to the Dominican Republic peso relating to its investment in Pueblo Viejo and exposure to the Guatemalan quetzal relating to its Marlin operation. The Company's exposure to the Mexican peso and Guatemalan quetzal is expected to partially decrease in the second quarter of 2017 after the expected closing of the sale of the Los Filos mine and closure of the Marlin mine, respectively.

Fluctuations in the US dollar can cause the volatility of costs reported in US dollars. In addition, monetary assets and liabilities that are denominated in non-US dollar currencies, such as cash and cash equivalents and value-added taxes are subject to currency risk. Goldcorp is further exposed to currency risk through non-monetary assets and liabilities of entities whose taxable profit or tax loss are denominated in non-US dollar currencies. Changes in exchange rates give rise to temporary differences resulting in deferred tax liabilities with the resulting deferred tax charged or credited to income tax expense.

Goldcorp's financial risk management policy allows the hedging of foreign exchange exposure to reduce the risk associated with currency fluctuations. The Company enters into Mexican peso currency hedge contracts to purchase Mexican pesos at pre-determined US dollar amounts. These contracts are entered into to normalize operating expenses and capital spend at Peñasquito expressed in US dollar terms.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Currency markets were volatile throughout 2016 as markets fluctuated due to changing expectations of interest rate increases in the US, as well as the impact of Brexit and the US presidential elections. The Canadian dollar weakened slightly during the year, whereas the Mexican peso continued to underperform and traded to historic lows against the US dollar late in the year.

Following the Argentine government elimination of currency controls in late 2015, the Argentine peso continued to weaken in 2016, punctuated by significant volatility in the first half of the year.

Argentine Economy

Argentina's political and economic landscape has undergone significant change over the past year, and this has impacted Cerro Negro. The new Argentine government implemented structural measures at the end of 2015 and in the first quarter of 2016 to reduce or remove controls and restrictions on capital flows and foreign exchange. While these changes have eased restrictions, the economy continues to recover slowly with some obstacles yet to be overcome. The official annual inflation rate stands at more than 40 percent. The increase in the inflation rate was expected as many subsidies were eliminated. Economic activity, while slow in 2016, is expected to start recovering in 2017 in response to the government’s market-oriented reforms.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

OVERVIEW OF ANNUAL FINANCIAL AND OPERATING RESULTS

|

| | | | | | | | | |

| | 2016 |

| 2015 |

| 2014 |

|

| Financial Results | | | |

Revenues (1)(2) | $ | 3,510 |

| $ | 4,375 |

| $ | 3,436 |

|

Net earnings (loss) from continuing operations (2) | $ | 162 |

| $ | (4,203 | ) | $ | (2,168 | ) |

| Net earnings (loss) | $ | 162 |

| $ | (4,157 | ) | $ | (2,159 | ) |

Net earnings (loss) from continuing operations per share (2) | | | |

| – Basic and diluted | $ | 0.19 |

| $ | (5.08 | ) | $ | (2.67 | ) |

| Net earnings (loss) per share | | | |

| – Basic and diluted | $ | 0.19 |

| $ | (5.03 | ) | $ | (2.66 | ) |

| Operating cash flow | $ | 799 |

| $ | 1,430 |

| $ | 1,014 |

|

| Adjusted operating cash flow | $ | 1,120 |

| $ | 1,651 |

| $ | 1,393 |

|

| Expenditures on mining interests (cash basis) | $ | 744 |

| $ | 1,238 |

| $ | 2,126 |

|

| – Sustaining | $ | 537 |

| $ | 705 |

| $ | 731 |

|

| – Expansionary | $ | 207 |

| $ | 533 |

| $ | 1,395 |

|

| Dividends paid | $ | 97 |

| $ | 370 |

| $ | 488 |

|

Operating Results (3) | | | |

| Gold produced (thousands of ounces) | 2,873 |

| 3,464 |

| 2,871 |

|

Gold sold (thousands of ounces) (1) | 2,869 |

| 3,591 |

| 2,673 |

|

| Silver produced (thousands of ounces) | 28,100 |

| 40,400 |

| 36,800 |

|

| Copper produced (thousands of pounds) | 68,900 |

| 51,500 |

| 84,800 |

|

| Lead produced (thousands of pounds) | 109,400 |

| 173,900 |

| 152,300 |

|

| Zinc produced (thousands of pounds) | 262,900 |

| 388,800 |

| 329,700 |

|

| Average realized gold price (per ounce) | $ | 1,244 |

| $ | 1,153 |

| $ | 1,264 |

|

Cash costs: by-product (per ounce) (4) | $ | 573 |

| $ | 605 |

| $ | 542 |

|

Cash costs: co-product (per ounce) (5) | $ | 649 |

| $ | 685 |

| $ | 668 |

|

| All-in sustaining costs (per ounce) | $ | 856 |

| $ | 894 |

| $ | 949 |

|

All-injury frequency rate (6) | 1.12 |

| 1.26 |

| 1.50 |

|

| |

| (1) | Excludes pre-commissioning sales ounces from Cerro Negro prior to January 1, 2015, and Éléonore prior to April 1, 2015 as costs incurred, net of proceeds from sales, were credited against capitalized project costs. |

| |

| (2) | In accordance with the requirements of IFRS 5 – Non-current assets held for sale and discontinued operations, the Wharf mine was classified as a discontinued operation for the year ended December 31, 2015, accordingly the 2014 comparative information for Wharf has been re-presented. The sale of Wharf was completed on February 20, 2015. |

| |

| (3) | The Company has presented the non-GAAP performance measures on an attributable (or Goldcorp's share) basis in the table above. AISC and adjusted operating cash flows are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 46-52 of this report. |

| |

| (4) | Total cash costs: by-product, per ounce, is calculated net of Goldcorp’s share of by-product sales revenues (by-product silver sales revenues for Cerro Negro, Marlin and Pueblo Viejo; by-product lead, zinc and copper sales revenues and 75% of silver sales revenues for Peñasquito at market silver prices, and 25% of silver sales revenues for Peñasquito at $4.09 per silver ounce (2015 – $4.07 per silver ounce) sold to Silver Wheaton Corp. and by-product copper and silver sales revenues for Alumbrera). |

| |

| (5) | Total cash costs: co-product, per ounce, is calculated by allocating Goldcorp’s share of production costs to each co-product (Alumbrera (copper); Marlin (silver); Pueblo Viejo (silver and copper); Peñasquito (silver, lead and zinc)) based on the ratio of actual sales volumes multiplied by budget metal prices (see page 46). |

| |

| (6) | Based on 200,000 hours worked. |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

REVIEW OF ANNUAL FINANCIAL RESULTS

Year ended December 31, 2016 compared to the year ended December 31, 2015

Net earnings for the year ended December 31, 2016 were $162 million, or $0.19 per share, compared to a net loss of $4,157 million, or $5.03 per share, for the year ended December 31, 2015. The net loss in 2015 was primarily due to the impairment of mining interests and goodwill recognized in the fourth quarter of 2015, partially offset by gains on the disposition of the investment in Tahoe Resources Inc. and the sale of Wharf in 2015.

Earnings from operations, associates and joint ventures for the year ended December 31, 2016 was $369 million, compared to a loss from operations, associates and joint ventures of $4,863 million for the year ended December 31, 2015. The increase in earnings was primarily due to the impairment expense recognized in 2015 compared to a reversal of impairment in 2016, favourable foreign exchange impacts on production costs, a reduction in depreciation and depletion due to lower sales volumes and the impact of the impairments recognized in 2015, and higher gold and silver prices, partially offset by lower expected sales volumes and operational challenges at Peñasquito and Cerro Negro.

Net earnings and earnings per share in the years ended December 31, 2016 and 2015 were affected by, among other things, the following non-cash or other items that management believes are not reflective of the performance of the underlying operations (items are denoted as (increases)/decreases to net earnings and net earnings per share):

|

| | | | | | | | | | | | | | | | | | |

| | Year ended December 31, 2016 | Year ended December 31, 2015 |

| (in millions, except per share) | Pre-tax |

| After-tax |

| Per share ($/share) |

| Pre-tax | After-tax | Per share ($/share) |

Negative deferred tax effects of foreign exchange on tax assets and liabilities and losses (1) | $ | — |

| $ | 88 |

| $ | 0.10 |

| $ | — |

| $ | 362 |

| $ | 0.44 |

|

| Impairment (reversal) expense, net | $ | (49 | ) | $ | (49 | ) | $ | (0.06 | ) | $ | 4,906 |

| $ | 3,896 |

| $ | 4.71 |

|

| Restructuring costs | $ | 50 |

| $ | 34 |

| $ | 0.04 |

| $ | — |

| $ | — |

| $ | — |

|

| Unrealized foreign exchange loss on Argentine peso denominated construction value-added tax receivable | $ | 26 |

| $ | 26 |

| $ | 0.03 |

| $ | 75 |

| $ | 75 |

| $ | 0.09 |

|

| Revisions in estimates and liabilities incurred on reclamation and closure cost obligations at inactive and closed sites | $ | (17 | ) | $ | (11 | ) | $ | (0.01 | ) | $ | (39 | ) | $ | (28 | ) | $ | (0.03 | ) |

Mine-site severance (2) | $ | 13 |

| $ | 13 |

| $ | 0.02 |

| $ | — |

| $ | — |

| $ | — |

|

| Gains on dispositions of, and dilution of ownership interest in, mining interests | $ | — |

| $ | — |

| $ | — |

| $ | (414 | ) | $ | (372 | ) | $ | (0.45 | ) |

| Gain on sale of Wharf | $ | — |

| $ | — |

| $ | — |

| $ | (65 | ) | $ | (43 | ) | $ | (0.05 | ) |

| |

| (1) | Negative deferred tax effects of foreign exchange on tax assets and liabilities and losses of $88 million in the year ended December 31, 2016 (year ended December 31, 2015 – $362 million) is composed of a foreign exchange loss on the translation of current and deferred income tax assets and liabilities, arising primarily from acquisitions and dispositions, of $189 million (year ended December 31, 2015 – $544 million), partially offset by Argentine tax deductible foreign exchange losses on US dollar denominated debt in local currency of $101 million (year ended December 31, 2015 – $182 million). |

| |

| (2) | Mine-site severance relates to workforce reductions at the Company's Marlin mine as it is scheduled to close by the end of the first quarter of 2017. |

Revenues

|

| | | | | | | | | |

| | | 2016 (1) | 2015 (1) | Change % |

| Gold | | | |

| | Revenue (millions) | $ | 2,861 |

| $ | 3,502 |

| (18 | )% |

| | Ounces sold (thousands) | 2,308 |

| 3,052 |

| (24 | )% |

| | Average realized price | $ | 1,243 |

| $ | 1,151 |

| 8 | % |

| Silver | | | |

| | Revenue (millions) | $ | 384 |

| $ | 541 |

| (29 | )% |

| | Ounces sold (thousands) | 26,639 |

| 41,776 |

| (36 | )% |

| | Average realized price | $ | 15.14 |

| $ | 13.80 |

| 10 | % |

| Other metals | | | |

| | Revenue (millions) | $ | 265 |

| $ | 332 |

| (20 | )% |

| Total revenue (millions) | $ | 3,510 |

| $ | 4,375 |

| (20 | )% |

| |

| (1) | Excludes attributable share of revenues from the Company's associates. |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Revenues decreased by $865 million, or 20%, primarily due to decreases in gold and silver sales volumes of 24% and 36%, respectively. The lower sales volumes were primarily a result of lower production at Peñasquito due to lower ore grade and recovery, and at Cerro Negro due to lower mill throughput from stockpiled ore processed in 2015. The impact of the decrease in sales volumes was partially offset by higher realized prices for gold and silver of 8% and 10%, respectively.

Production Costs

|

| | | | | | | | |

| Years ended December 31 | 2016 |

| 2015 |

| Change % |

| Raw materials and consumables | $ | 937 |

| $ | 998 |

| (6 | )% |

| Salaries and employee benefits | 500 |

| 582 |

| (14 | )% |

| Contractors | 408 |

| 486 |

| (16 | )% |

| Royalties | 69 |

| 93 |

| (26 | )% |

| Mine-site severance | 13 |

| — |

| — |

|

| Write down of inventories to net realizable value | 10 |

| 158 |

| (94 | )% |

| Revision of reclamation and closure cost provision | (17 | ) | (39 | ) | 56 | % |

| Change in inventories | (5 | ) | 114 |

| (104 | )% |

| Other | 151 |

| 188 |

| (20 | )% |

| Total Production costs | $ | 2,066 |

| $ | 2,580 |

| (20 | )% |

Production costs decreased by $514 million, or 20%, primarily due to the favourable impact of the strengthening US dollar against the Mexican peso (approximately $80 million) and the Canadian dollar (approximately $30 million); the impact of the devaluation of the Argentine peso when it became a floating exchange rate in December 2015 (approximately $75 million), the impact of lower inventory carrying value reductions at Los Filos in 2016 compared to 2015 (approximately $150 million); the impact of 115,000 ounces produced in 2014 at Cerro Negro being sold in 2015 (approximately $80 million) and an overall decrease in costs due to lower production (approximately $100 million).

Depreciation and Depletion

|

| | | | | | | | |

| | 2016 | 2015 | Change % |

| Depreciation and Depletion (millions) | $ | 1,024 |

| $ | 1,493 |

| (31 | )% |

Sales ounces (thousands) (1) | 2,308 |

| 3,052 |

| (24 | )% |

| Depreciation and Depletion per ounce | $ | 444 |

| $ | 489 |

| (9 | )% |

| |

| (1) | Excludes attributable share of revenues from the Company's associates. |

Depreciation and depletion decreased by $469 million, or 31%, mainly due to lower sales volumes at Peñasquito and Cerro Negro and the impact of impairments on mining interests recognized in the fourth quarter of 2015.

Share of Net Earnings (Loss) of Associates and Joint Venture

|

| | | | | | | | | |

| (in millions) | 2016 | 2015 | Change $ |

| Pueblo Viejo | $ | 169 |

| $ | 53 |

| $ | 116 |

|

| Alumbrera | — |

| (62 | ) | 62 |

|

| NuevaUnión | 2 |

| — |

| 2 |

|

| Tahoe | — |

| 8 |

| (8 | ) |

| Share of net earnings (loss) of associates and joint venture | $ | 171 |

| $ | (1 | ) | $ | 172 |

|

The increase in the Company’s share of earnings of associates and joint venture of $172 million for the year ended December 31, 2016 compared to the year ended December 31, 2015 was primarily due to an increase in net earnings from Pueblo Viejo in 2016 compared to 2015 and a net loss of $62 million from Alumbrera in 2015. The increase in net earnings from Pueblo Viejo in 2016 compared to 2015 was primarily due to higher production, lower operating costs, the receipt of insurance proceeds relating to the oxygen plant failures in 2015 and lower depreciation and depletion costs. With respect to Alumbrera, at December 31, 2015, the Company recognized an impairment of its investment in Alumbrera and the carrying amount of its interest was reduced to zero. As at January 1, 2016, the Company has discontinued recognizing its share of losses of Alumbrera and did not recognize its share of earnings of Alumbrera for the year ended December 31, 2016, as future earnings will be recognized by the Company only after the Company's share of future earnings equals its share of losses not recognized.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Impairment reversal (expense)

|

| | | | | | |

| (in millions) | 2016 |

| 2015 |

|

| Red Lake | $ | — |

| $ | (1,213 | ) |

| Porcupine | — |

| (123 | ) |

| Éléonore | — |

| (398 | ) |

| Peñasquito | — |

| (1,181 | ) |

| Los Filos | 59 |

| (752 | ) |

| Marlin | (10 | ) | (293 | ) |

| Alumbrera | — |

| (107 | ) |

| Project Corridor | — |

| (200 | ) |

| Pueblo Viejo | — |

| (610 | ) |

| Other | — |

| (29 | ) |

| Impairment reversal (expense) | $ | 49 |

| $ | (4,906 | ) |

The 2016 net impairment reversal was comprised of a reversal of impairment at Los Filos of $59 million, which was based on the expected proceeds from the sale to Leagold, offset by an impairment expense at Marlin of $10 million relating to land.

At December 31, 2015, the Company’s market capitalization deficiency was an indicator of impairment. This necessitated a recoverable value assessment on all of the Company's assets and an impairment charge of $4,906 million ($3,896 million, net of tax) of mining interests and goodwill was booked as a result.

Corporate Administration

Corporate administration expenses decreased by $20 million in 2016 compared to 2015 due primarily to reductions in corporate and regional office costs associated with the Company's productivity and cost optimization program to deliver $250 million in sustainable annual efficiencies by 2018 and the favourable impact of the strengthening US dollar of approximately $4 million.

Restructuring Charges

Restructuring costs were $50 million for the year ended December 31, 2016 compared to $nil for the year ended December 31, 2015. The restructuring costs related primarily to severance costs associated with involuntary and voluntary workforce reductions to increase efficiencies at mine sites and corporate offices.

Gain (Loss) on Derivatives

The net gain on derivatives of $3 million for the year ended December 31, 2016 was comprised of unrealized gains on warrants of $9 million, partially offset by net losses on foreign currency contracts. The net loss on derivatives of $54 million for the year ended December 31, 2015 was primarily comprised of net losses on foreign currency and commodity contracts. In 2016, the Company hedged Mexican peso currency exposure, whereas in 2015, the Company hedged Mexican peso and Canadian dollar currency exposure as well as lead, zinc and heating oil. In addition, in 2016, the Company designated a portion of its Mexican peso currency contracts as cash flow hedges, where the effective portion of the change in fair value of the hedge is recognized in Other comprehensive income until the hedged transaction occurs.

Gain on Dilution of Ownership Interest in Associate

The gain on dilution of ownership interest in associate of $99 million ($95 million, net of tax) in the year ended December 31, 2015 related to the dilution of the Company's investment in Tahoe to 25.9% on April 1, 2015 as a result of Tahoe’s acquisition of Rio Alto.

Gain on Disposition of Mining Interests

The $315 million gain on disposition of mining interests in the year ended December 31, 2015 arose on the disposition of the Company's remaining 25.9% investment in Tahoe for a total gain of $299 million ($252 million, net of tax), and the sale of the Arturo project for which the Company recognized a gain of $16 million ($11 million, net of tax).

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Other Expenses

Other expense of $13 million for the year ended December 31, 2016 was mainly comprised of a $68 million foreign exchange loss arising primarily from value-added tax receivables denominated in Mexican and Argentine pesos, partially offset by $49 million of interest income on loans held with Pueblo Viejo and short term investments and gains on dispositions of investments in securities. For the year ended December 31, 2015, other expense of $50 million was comprised primarily of $52 million of net foreign exchange losses arising on value added tax receivables denominated in Mexican and Argentine pesos and losses on sales of investments in securities, partially offset by interest income arising on the Company's loans held with Pueblo Viejo and cash and cash equivalents.

Income Tax Expense (Recovery)

Income tax expense for the year ended December 31, 2016 of $60 million represented a 27% rate (year ended December 31, 2015 – income tax recovery of $485 million representing a 10% rate) and was impacted by:

| |

| • | A $189 million foreign exchange loss on the translation of deferred income tax assets and liabilities arising primarily from acquisitions, compared to a $501 million foreign exchange loss for the year ended December 31, 2015; and |

| |

| • | A higher effective tax rate in 2016 compared to 2015, after adjusting for the above noted item and non-deductible share-based compensation expense. The increase in the effective tax rate for the 2016 year was primarily due to a significant portion of the 2015 impairments not being tax effected due to uncertainty of future loss utilization and the impairment of equity investments not being tax effected. These results were partially offset by higher after-tax income from associates in 2016 (primarily from Pueblo Viejo) compared to 2015. |

Net Earnings from Discontinued Operations

Net earnings from discontinued operations of $46 million for the year ended December 31, 2015 was comprised of a $43 million net gain on the sale of Wharf and $3 million of net earnings of Wharf until February 20, 2015, the date of disposition.

AISC

AISC were $856 per ounce(1) for the year ended December 31, 2016, compared to $894 per ounce for the year ended December 31, 2015. The decrease in AISC was primarily due to the favourable impact of the strengthening US dollar against the Mexican peso and the Canadian dollar, the impact of the devaluation of the Argentine peso when it became a floating exchange rate in December 2015 and lower production costs, partially offset by lower sales volumes at Peñasquito, Cerro Negro, Red Lake and Marlin.

| |

| (1) | AISC per ounce is a non-GAAP financial performance measure with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 46-52 of this report. |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

OVERVIEW OF QUARTERLY FINANCIAL AND OPERATING RESULTS

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2016 | 2015 |

| | Q1 |

| Q2 |

| Q3 |

| Q4 |

| Total |

| Q1 |

| Q2 |

| Q3 |

| Q4 |

| Total |

|

| Financial Results | | | | | | | | | | |

Revenues (1)(2) | $ | 944 |

| $ | 753 |

| $ | 915 |

| $ | 898 |

| $ | 3,510 |

| $ | 1,017 |

| $ | 1,188 |

| $ | 1,098 |

| $ | 1,072 |

| $ | 4,375 |

|

Net earnings (loss) from continuing operations (2) | $ | 80 |

| $ | (78 | ) | $ | 59 |

| $ | 101 |

| $ | 162 |

| $ | (139 | ) | $ | 398 |

| $ | (191 | ) | $ | (4,271 | ) | $ | (4,203 | ) |

| Net earnings (loss) | $ | 80 |

| $ | (78 | ) | $ | 59 |

| $ | 101 |

| $ | 162 |

| $ | (87 | ) | $ | 392 |

| $ | (191 | ) | $ | (4,271 | ) | $ | (4,157 | ) |

Net earnings (loss) from continuing operations per share (2) | | | | | | | | | | |

| – Basic and diluted | $ | 0.10 |

| $ | (0.09 | ) | $ | 0.07 |

| $ | 0.12 |

| $ | 0.19 |

| $ | (0.17 | ) | $ | 0.48 |

| $ | (0.23 | ) | $ | (4.90 | ) | $ | (5.08 | ) |

| Net earnings (loss) per share | | | | | | | | | | |

| – Basic and diluted | $ | 0.10 |

| $ | (0.09 | ) | $ | 0.07 |

| $ | 0.12 |

| $ | 0.19 |

| $ | (0.11 | ) | $ | 0.47 |

| $ | (0.23 | ) | $ | (5.14 | ) | $ | (5.03 | ) |

| Operating cash flow | $ | 59 |

| $ | 234 |

| $ | 267 |

| $ | 239 |

| $ | 799 |

| $ | 58 |

| $ | 528 |

| $ | 443 |

| $ | 401 |

| $ | 1,430 |

|

Adjusted operating cash flow (3) | $ | 89 |

| $ | 307 |

| $ | 341 |

| $ | 383 |

| $ | 1,120 |

| $ | 118 |

| $ | 523 |

| $ | 506 |

| $ | 504 |

| $ | 1,651 |

|

| Expenditures on mining interests (cash basis) | $ | 182 |

| $ | 177 |

| $ | 168 |

| $ | 217 |

| $ | 744 |

| $ | 408 |

| $ | 330 |

| $ | 249 |

| $ | 251 |

| $ | 1,238 |

|

| – Sustaining | $ | 140 |

| $ | 140 |

| $ | 112 |

| $ | 145 |

| $ | 537 |

| $ | 160 |

| $ | 193 |

| $ | 164 |

| $ | 188 |

| $ | 705 |

|

| – Expansionary | $ | 42 |

| $ | 37 |

| $ | 56 |

| $ | 72 |

| $ | 207 |

| $ | 248 |

| $ | 137 |

| $ | 85 |

| $ | 63 |

| $ | 533 |

|

| Dividends paid | $ | 51 |

| $ | 16 |

| $ | 14 |

| $ | 16 |

| $ | 97 |

| $ | 122 |

| $ | 124 |

| $ | 75 |

| $ | 49 |

| $ | 370 |

|

Operating Results (3) | | | | | | | | | | |

| Gold produced (thousands of ounces) | 784 |

| 613 |

| 715 |

| 761 |

| 2,873 |

| 725 |

| 908 |

| 922 |

| 909 |

| 3,464 |

|

Gold sold (thousands of ounces) (1) | 799 |

| 616 |

| 686 |

| 768 |

| 2,869 |

| 827 |

| 903 |

| 942 |

| 918 |

| 3,591 |

|

| Silver produced (thousands of ounces) | 7,700 |

| 5,300 |

| 7,700 |

| 7,400 |

| 28,100 |

| 8,500 |

| 10,400 |

| 11,300 |

| 10,200 |

| 40,400 |

|

| Copper produced (thousands of pounds) | 17,200 |

| 14,400 |

| 16,900 |

| 20,400 |

| 68,900 |

| 9,200 |

| 8,600 |

| 12,300 |

| 21,400 |

| 51,500 |

|

| Lead produced (thousands of pounds) | 29,000 |

| 17,100 |

| 33,700 |

| 29,600 |

| 109,400 |

| 36,700 |

| 47,500 |

| 49,200 |

| 40,500 |

| 173,900 |

|

| Zinc produced (thousands of pounds) | 71,100 |

| 38,300 |

| 75,200 |

| 78,300 |

| 262,900 |

| 82,500 |

| 105,500 |

| 111,500 |

| 89,300 |

| 388,800 |

|

| Average realized gold price (per ounce) | $ | 1,203 |

| $ | 1,277 |

| $ | 1,333 |

| $ | 1,181 |

| $ | 1,244 |

| $ | 1,217 |

| $ | 1,189 |

| $ | 1,114 |

| $ | 1,098 |

| $ | 1,153 |

|

Cash costs: by-product (per ounce) (4) | $ | 557 |

| $ | 728 |

| $ | 554 |

| $ | 481 |

| $ | 573 |

| $ | 585 |

| $ | 547 |

| $ | 597 |

| $ | 687 |

| $ | 605 |

|

Cash costs: co-product (per ounce) (5) | $ | 604 |

| $ | 716 |

| $ | 657 |

| $ | 619 |

| $ | 649 |

| $ | 670 |

| $ | 656 |

| $ | 670 |

| $ | 739 |

| $ | 685 |

|

| All-in sustaining costs (per ounce) | $ | 836 |

| $ | 1,067 |

| $ | 812 |

| $ | 747 |

| $ | 856 |

| $ | 885 |

| $ | 853 |

| $ | 858 |

| $ | 977 |

| $ | 894 |

|

| |

| (1) | Excludes pre-commissioning sales ounces from and Éléonore prior to April 1, 2015 as costs incurred, net of proceeds from sales, were credited against capitalized project costs. |

| |

| (2) | In accordance with the requirements of IFRS 5 – Non-current assets held for sale and discontinued operations, Wharf was classified as a discontinued operation for the year ended December 31, 2015. The sale of Wharf was completed on February 20, 2015. |

| |

| (3) | The Company has presented the non-GAAP performance measures on an attributable (or Goldcorp's share) basis in the table above. AISC and adjusted operating cash flows are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 46-52 of this report. |

| |

| (4) | Total cash costs: by-product, per ounce, is calculated net of Goldcorp’s share of by-product sales revenues (by-product silver sales revenues for Cerro Negro, Marlin and Pueblo Viejo; by-product lead, zinc and copper sales revenues and 75% of silver sales revenues for Peñasquito at market silver prices, and 25% of silver sales revenues for Peñasquito at $4.09 per silver ounce (2015 – $4.07 per silver ounce) sold to Silver Wheaton Corp. and by-product copper sales revenues for Alumbrera). |

| |

| (5) | Total cash costs: co-product, per ounce, is calculated by allocating Goldcorp’s share of production costs to each co-product (Alumbrera (copper); Marlin (silver); Pueblo Viejo (silver and copper); Peñasquito (silver, lead and zinc)) based on the ratio of actual sales volumes multiplied by budget metal prices (see page 46). |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

REVIEW OF FOURTH QUARTER FINANCIAL RESULTS

Three months ended December 31, 2016 compared to the three months ended December 31, 2015

Net earnings for the three months ended December 31, 2016 were $101 million, or $0.12 per share, compared to a net loss of $4,271 million, or $5.14 per share, for the three months ended December 31, 2015. The net loss in 2015 compared to the net earnings in 2016 was driven by the impairment of mining interest and goodwill in the fourth quarter of 2015 compared to a reversal of impairment in 2016, a decrease in production costs, primarily as result of the strengthening US dollar and decreases in inventory carrying value reductions at Los Filos, a decrease in depreciation and depletion charges as a result of lower sales volumes and the impact of the impairment in the fourth quarter of 2016, an increase in income tax expense, and the impact of a 7% increase in the average realized gold sales price compared to the fourth quarter of 2015. These increases were partially offset by a decrease in revenues as a result of lower sales volumes.

Net earnings and earnings per share in the fourth quarter of 2016 and net loss and loss per share in the fourth quarter of 2015 were affected by, among other things, the following non-cash or other items that management believes are not reflective of the performance of the underlying operations (items are denoted as (increases)/decreases to net earnings and net earnings per share):

|

| | | | | | | | | | | | | | | | | | |

| | Three months ended December 31, 2016 | Three months ended December 31, 2015 |

| (in millions, except per share) | Pre-tax | After-tax |

| Per share ($/share) |

| Pre-tax | After-tax | Per share

($/share) |

| Impairment (reversal) expense, net | $ | (49 | ) | $ | (49 | ) | $ | (0.06 | ) | $ | 4,906 |

| $ | 3,896 |

| $ | 4.69 |

|

Negative deferred tax effects of foreign exchange on tax assets and liabilities and losses (1) | $ | — |

| $ | 46 |

| $ | 0.05 |

| $ | — |

| $ | 99 |

| $ | 0.12 |

|

| Unrealized foreign exchange loss on Argentine peso denominated construction value-added tax receivable | $ | 4 |

| $ | 4 |

| $ | — |

| $ | 55 |

| $ | 55 |

| $ | 0.07 |

|

Mine-site severance (2) | $ | 13 |

| $ | 13 |

| $ | 0.02 |

| $ | — |

| $ | — |

| $ | — |

|

| Restructuring costs | $ | 5 |

| $ | 3 |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

|

| Revisions in estimates and liabilities incurred on reclamation and closure cost obligations at inactive and closed sites | $ | (17 | ) | $ | (12 | ) | $ | (0.01 | ) | $ | (59 | ) | $ | (41 | ) | $ | (0.05 | ) |

| |

| (1) | Negative deferred tax effects of foreign exchange on tax assets and liabilities and losses of $46 million in the three months ended December 31, 2016 (three months ended December 31, 2015 – $99 million) is primarily composed of a foreign exchange loss on the translation of current and deferred income tax assets and liabilities, arising primarily from acquisitions and dispositions, of $68 million (three months ended December 31, 2015 – $242 million), partially offset by Argentine tax deductible foreign exchange losses on US dollar denominated debt in local currency of $22 million (three months ended December 31, 2015 – $143 million). |

| |

| (2) | Mine-site severance relates to workforce reductions at the Company's Marlin mine as it is scheduled to close by the end of the first quarter of 2017. |

Revenues

|

| | | | | | | | | |

| | | 2016 (1) | 2015 (1) | Change % |

| Gold | | | |

| | Revenue (millions) | $ | 713 |

| $ | 877 |

| (19 | )% |

| | Ounces sold (thousands) | 609 |

| 800 |

| (24 | )% |

| | Average realized price | $ | 1,178 |

| $ | 1,099 |

| 7 | % |

| Silver | | | |

| | Revenue (millions) | $ | 95 |

| $ | 125 |

| (24 | )% |

| | Ounces sold (thousands) | 7,114 |

| 10,237 |

| (31 | )% |

| | Average realized price | $ | 14.27 |

| $ | 13.07 |

| 9 | % |

| Other metals | | | |

| | Revenue (millions) | $ | 90 |

| $ | 70 |

| 29 | % |

| Total revenue (millions) | $ | 898 |

| $ | 1,072 |

| (16 | )% |

| |

| (1) | Excludes attributable share of revenues from the Company's associates. |

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Revenues decreased by $174 million, or 16%, primarily due to decreases in gold and silver sales volumes of 24% and 31%, respectively. The lower sales volumes were primarily a result of lower production at Peñasquito due to lower ore grade and recovery, and at Cerro Negro due to lower mill throughput from stockpiled ore processed in the fourth quarter of 2015. The impact of the decrease in sales volumes was partially offset by higher realized prices for gold and silver of 7% and 9%, respectively.

Production Costs

Production costs decreased by $146 million, or 22%, primarily due to the impact of higher inventory carrying value reductions at Los Filos (approximately $110 million) in the fourth quarter of 2015 compared to the fourth quarter of 2016.

Depreciation and Depletion

|

| | | | | | | | |

| | 2016 | 2015 | Change % |

| Depreciation and Depletion (millions) | $ | 254 |

| $ | 421 |

| (40 | )% |

| Sales ounces (thousands) | 609 |

| 800 |

| (24 | )% |

| Depreciation and Depletion per ounce | $ | 417 |

| $ | 526 |

| (21 | )% |

Depreciation and depletion decreased by $167 million, or 40%, mainly due to lower sales volumes at Peñasquito and Cerro Negro and the impact of impairments on mining interests recognized in the fourth quarter of 2015.

Share of Net Earnings (Loss) of Associates and Joint Venture

|

| | | | | | | | | |

| (in millions) | 2016 | 2015 | Change $ |

| Pueblo Viejo | $ | 60 |

| $ | 13 |

| $ | 47 |

|

| Alumbrera | — |

| (37 | ) | 37 |

|

| NuevaUnión | — |

| — |

| — |

|

| Tahoe | — |

| — |

| — |

|

| Share of net earnings (loss) of associates and joint venture | $ | 60 |

| $ | (24 | ) | $ | 84 |

|

The Company’s share of earnings of associates and joint venture increased by $84 million in the fourth quarter of 2016 compared to the same period in the prior year primarily due to an increase in net earnings from Pueblo Viejo and a net loss of $37 million from Alumbrera in the fourth quarter of 2015. The increase in net earnings from Pueblo Viejo in the fourth quarter of 2016 compared to the same period in the prior year was primarily due to higher sales volumes and the receipt of insurance proceeds relating to the oxygen plant failures in 2015. With respect to Alumbrera, at December 31, 2015, the Company recognized an impairment of its investment in Alumbrera and the carrying amount of its interest was reduced to zero. As at January 1, 2016, the Company discontinued recognizing its share of losses of Alumbrera and did not recognize its share of earnings of Alumbrera for the three months ended December 31, 2016 as future earnings will be recognized by the Company only after the Company's share of future earnings equals its share of losses not recognized.

Impairment reversal (expense)

The 2016 net impairment reversal was comprised of a reversal of impairment at Los Filos of $59 million, which was based on the expected proceeds from the sale to Leagold, offset by an impairment expense at Marlin of $10 million relating to land.

At December 31, 2015, the Company’s market capitalization deficiency was an indicator of impairment. This necessitated a recoverable value assessment on all of the Company's assets and an impairment charge of $4,906 million ($3,896 million, net of tax) of mining interests and goodwill was booked as a result.

Corporate Administration

Corporate administration expenses decreased by $10 million in the fourth quarter of 2016 compared to the fourth quarter of 2015 primarily due to the Company's cost savings initiatives.

Restructuring Charges

Restructuring costs were $5 million in the three months ended December 31, 2016 compared to $nil in the three months ended December 31, 2015. The restructuring costs in the fourth quarter of 2016 related primarily to severance costs associated with the involuntary and voluntary workforce reductions to increase efficiencies at mine sites.

Third Quarter Report – 2016

(in United States dollars, tabular amounts in millions, except where noted)

Other Expenses

Other Expenses decreased by $68 million for the three months ended December 31, 2016 compared to the three months ended December 31, 2015 primarily due to a decrease in foreign exchange losses which arose primarily on value added tax receivables denominated in Mexican and Argentine pesos.

Income Tax Expense (Recovery)

Income tax expense for the three months ended December 31, 2016 of $38 million represented a 27% rate (three months ended December 31, 2015 – income tax recovery of $840 million representing a16% rate) and was impacted by:

| |