Exhibit 99.1

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FOR THE THREE MONTHS ENDED MARCH 31, 2018

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with the condensed interim consolidated financial statements of Goldcorp Inc. (“Goldcorp” or “the Company”) for the three months ended March 31, 2018 and related notes thereto which have been prepared in accordance with International Accounting Standard 34 – Interim Financial Reporting of International Financial Reporting Standards (“GAAP” or “IFRS”) as issued by the International Accounting Standards Board (“IASB”). All figures are in United States (“US”) dollars unless otherwise noted. References to C$ are to Canadian dollars. This MD&A has been prepared as of April 25, 2018.

TABLE OF CONTENTS

|

| | |

| | Page Number |

| Cautionary Statements | |

| Quarter Highlights | |

| Business Overview and Strategy | |

| Corporate Developments | |

| Market Overview | |

| Quarterly Results | |

| Liquidity and Capital Resources | |

| Guidance | |

| Operational and Projects Review | |

| Non-GAAP Performance Measures | |

| Risks and Uncertainties | |

| Accounting Matters | |

| Controls and Procedures | |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This MD&A contains "forward-looking statements" within the meaning of Section 27A of the United States Securities Act of 1933, as amended, Section 21E of the United States Exchange Act of 1934, as amended, the United States Private Securities Litigation Reform Act of 1995, or in releases made by the United States Securities and Exchange Commission ("SEC"), all as may be amended from time to time, and "forward-looking information" under the provisions of applicable Canadian securities legislation, concerning the business, operations and financial performance and condition of Goldcorp. Forward-looking statements include, but are not limited to, statements with respect to the future price of gold, silver, zinc, copper and lead, the estimation of Mineral Reserves and Mineral Resources (as each term is defined below), the realization of Mineral Reserve estimates, the timing and amount of estimated future production, costs of production, targeted cost reductions, capital expenditures, free cash flow, costs and timing of the development of new deposits, success of exploration activities, permitting and certification time lines, timing and cost of construction and expansion projects, hedging practices, currency exchange rate fluctuations, requirements for additional capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, health, safety and diversity initiatives, timing and possible outcome of pending litigation, title disputes or claims and limitations on insurance coverage. Generally, these forward-looking statements can be identified by the use of words such as "plans", "expects", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates", "believes", or variations or comparable language of such words and phrases or statements that certain actions, events or results "may", "could", "would", "should", "might" or "will", "occur" or "be achieved" or the negative connotation thereof.

Forward-looking statements are necessarily based upon a number of factors and assumptions that, if untrue, could cause the actual results, performances or achievements of Goldcorp to be materially different from future results, performances or achievements expressed or implied by such statements. Such statements and information are based on numerous assumptions regarding Goldcorp’s present and future business strategies and the environment in which Goldcorp will operate in the future, including the price of gold, anticipated costs and ability to achieve goals. Certain important factors that could cause actual results, performances or achievements to differ materially from those in the forward-looking statements include, among others, gold price volatility, discrepancies between actual and estimated production, Mineral Reserves and Mineral Resources and metallurgical recoveries, mining operational and development risks, litigation risks, regulatory restrictions (including environmental regulatory restrictions and liability), changes in national and local government legislation, taxation, controls or regulations and/or change in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States, Mexico, Argentina, the Dominican Republic, Chile or other jurisdictions in which the Company does or may carry on business in the future, delays, suspension and technical challenges associated with capital projects, higher prices for fuel, steel, power, labour and other consumables, currency fluctuations, the speculative nature of gold exploration, the global economic climate, dilution, share price volatility, competition, loss of key employees, additional funding requirements and defective title to mineral claims or property. Although Goldcorp believes its expectations are based upon reasonable assumptions and has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended.

Forward-looking statements are subject to known and unknown risks, uncertainties and other important factors that may cause the actual results, level of activity, performance or achievements of Goldcorp to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: future prices of gold, silver, zinc, copper and lead; mine development and operating risks; possible variations in ore reserves, grade or recovery rates; risks related to international operations, including economic and political instability in foreign jurisdictions in which Goldcorp operates; risks related to current global financial conditions; risks related to joint venture operations; actual results of current exploration activities; actual results of current reclamation activities; environmental risks; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes and other risks of the mining industry; risks associated with restructuring and cost-efficiency initiatives; delays in obtaining governmental approvals or financing or in the completion of development or construction activities; risks related to the integration of acquisitions; risks related to indebtedness and the service of such indebtedness, as well as those factors discussed in the section entitled "Description of the Business - Risk Factors” in Goldcorp’s most recent annual information form available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov. Although Goldcorp has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Forward-looking statements are made as of the date hereof and, accordingly, are subject to change after such date. Except as otherwise indicated by Goldcorp, these statements do not reflect the potential impact of any non-recurring or other special items or of any disposition, monetization, merger, acquisition, other business combination or other transaction that may be announced or that may occur after the date hereof. Forward-looking statements are provided for the purpose of providing information about management’s current expectations and plans and allowing investors and others to get a better understanding of Goldcorp's operating environment. Goldcorp does not intend or undertake to publicly update any forward-looking statements that are included in this document, whether as a result of new information, future events or otherwise, except in accordance with applicable securities laws.

CAUTIONARY STATEMENT REGARDING CERTAIN MEASURES OF PERFORMANCE

This MD&A presents certain measures, including "total cash costs: by-product", "total cash costs: co-product", "all-in sustaining costs", "adjusted operating cash flow", "EBITDA", "adjusted EBITDA" and "adjusted net debt", that are not recognized measures under IFRS. This data may not be comparable to data presented by other gold producers. For a reconciliation of these measures to the most directly comparable financial information presented in the consolidated financial statements prepared in accordance with IFRS, see Non-GAAP Financial Performance Measures in this MD&A. The Company believes that these generally accepted industry measures are realistic indicators of operating performance and are useful in performing year over year comparisons. However, these non-GAAP measures should be considered together with other data prepared in accordance with IFRS, and these measures,

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

taken by themselves, are not necessarily indicative of operating costs or cash flow measures prepared in accordance with IFRS. This MD&A also contains information as to estimated future all-in sustaining costs. The estimates of future all-in sustaining costs are not based on total production cash costs calculated in accordance with IFRS, which forms the basis of the Company’s cash costs: by-product. The estimates of future all-in sustaining costs are anticipated to be adjusted to include sustaining capital expenditures, corporate administrative expense, exploration and evaluation costs and reclamation cost accretion and amortization, and exclude the effects of expansionary capital, tax payments, dividends and financing costs. Projected IFRS total production cash costs for the full year would require inclusion of the projected impact of future included and excluded items, including items that are not currently determinable, but may be significant, such as sustaining capital expenditures, reclamation cost accretion and amortization and tax payments. Due to the uncertainty of the likelihood, amount and timing of any such items, the Company does not have information available to provide a quantitative reconciliation of projected all-in sustaining costs to a total production cash costs projection.

CAUTIONARY NOTE REGARDING MINERAL RESERVES AND MINERAL RESOURCES

Scientific and technical information contained in this MD&A, including the Mineral Reserves and Mineral Resources, was reviewed and approved by Ivan Mullany, FAusIMM, Senior-Vice President, Technical Services for Goldcorp, and a "qualified person" as defined by Canadian Securities Administrators' National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101"). All Mineral Reserves and Mineral Resources have been estimated in accordance with the standards of the Canadian Institute of Mining, Metallurgy and Petroleum ("CIM") and NI 43-101, or the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves equivalent. All Mineral Resources are reported exclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Information on data verification performed on the mineral properties mentioned in this MD&A that are considered to be material mineral properties to the Company are contained in Goldcorp’s most recent annual information form and the current technical report for each of those properties, all available on SEDAR at www.sedar.com.

Cautionary Note to United States investors concerning estimates of measured, indicated and inferred resources: The Mineral Resource and Mineral Reserve estimates contained in this MD&A have been prepared in accordance with the requirements of Canadian securities laws, which differ from the requirements of United States securities laws and use terms that are not recognized by the SEC. Canadian reporting requirements for disclosure of mineral properties are governed by NI 43-101. The definitions used in NI 43-101 are incorporated by reference from the CIM Definition Standards adopted by CIM Council on May 10, 2014 (the "CIM Definition Standards"). U.S. reporting requirements are governed by the SEC Industry Guide 7 ("Industry Guide 7") under the United States Securities Act of 1933, as amended. These reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but embody different approaches and definitions. For example, the terms "Mineral Reserve", "Proven Mineral Reserve" and "Probable Mineral Reserve" are Canadian mining terms as defined in in NI 43-101, and these definitions differ from the definitions in Industry Guide 7. Under Industry Guide 7 standards, a "final" or "bankable" feasibility study is required to report reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. Further, under Industry Guide 7, mineralization may not be classified as "reserve" unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made.

While the terms "Mineral Resource", "Measured Mineral Resource", "Indicated Mineral Resource" and "Inferred Mineral Resource" are defined in and required to be disclosed by NI 43-101, these terms are not defined terms under Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. United States readers are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves. In addition, "Inferred Mineral Resources" have a great amount of uncertainty as to their existence and their economic and legal feasibility. A significant amount of exploration must be completed in order to determine whether an Inferred Mineral Resource may be upgraded to a higher category. Under Canadian regulations, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. United States readers are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable. Disclosure of "contained ounces" in a resource is permitted disclosure under Canadian regulations if such disclosure includes the grade or quality and the quantity for each category of Mineral Resource and Mineral Reserve; however, the SEC normally only permits issuers to report mineralization that does not constitute "reserves" by SEC standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this MD&A containing descriptions of Goldcorp’s mineral deposits may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

FINANCIAL AND OPERATIONAL HIGHLIGHTS FOR THE THREE MONTHS ENDED MARCH 31, 2018

Net earnings were $67 million, or $0.08 per share, compared to net earnings of $170 million, or $0.20 per share, for the three months ended March 31, 2017. Operating cash flows and adjusted operating cash flows(1)for the three months ended March 31, 2018 were $271 million and $350 million, respectively, compared to $227 million and $315 million, respectively, for the three months ended March 31, 2017.

Gold production of 590,000 ounces at all-in sustaining costs(1) ("AISC") of $810 per ounce, compared to 655,000 ounces at AISC of $800 per ounce for the three months ended March 31, 2017. Full year 2018 guidance reconfirmed for gold production of 2.5 million ounces (+/-5%) at AISC of $800(2) per ounce (+/- 5%).

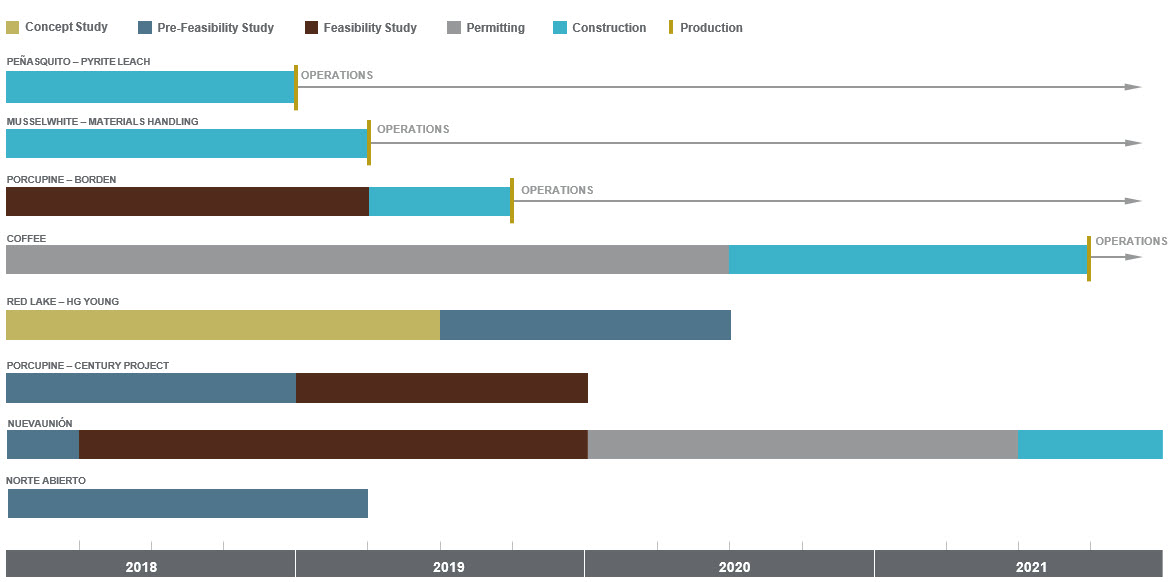

Solid execution on project pipeline in support of the Company's 20/20/20 growth plan. The Peñasquito Pyrite Leach project advanced to 86% completion, ahead of schedule, the Musselwhite Materials Handling project advanced to 65% completion, on schedule and 10% below budget, and the Borden project is on track for commercial production by the second half of 2019.

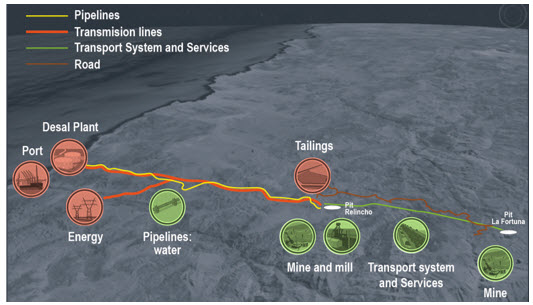

Key milestone achieved with the completion of pre-feasibility study at NuevaUnión and advancement to the feasibility stage. The pre-feasibility study outlines a combined and phased approach to the development of the Relincho and La Fortuna deposits at NuevaUnión with a project containing 8.9 million ounces of proven and probable gold mineral reserves and 17.9 billion pounds of proven and probable copper mineral reserves (100% basis) to be produced over a 36 year mine life. The NuevaUnión project is foundational to the Company's Beyond 20/20 program and its feasibility study is expected in 2019.

Program to implement $250 million of sustainable annual efficiencies by the middle of 2018 is on track with $210 million achieved as at the end of the first quarter of 2018 across the Company's portfolio. More than 100% of the $250 million of efficiencies have been identified, with the program likely to be extended and the efficiency target increased, after the Company achieves its current target.

| |

| (1) | The Company has included non-GAAP performance measures on an attributable (or Goldcorp's share) basis throughout this document. Adjusted operating cash flows and AISC per ounce are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 31-38 of this MD&A. |

| |

| (2) | Refer to footnote (4) on page 15 of this MD&A regarding the Company's projection of AISC. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

BUSINESS OVERVIEW

Goldcorp is a leading gold producer focused on responsible mining practices, with production from a portfolio of long-life, high quality assets throughout the Americas that it believes position the Company to deliver long-term value.

The Company’s principal producing mining properties are comprised of the Éléonore, Musselwhite, Porcupine and Red Lake mines in Canada; the Peñasquito mine in Mexico; the Cerro Negro mine in Argentina; and the Pueblo Viejo mine (40.0% interest) in the Dominican Republic. The Company's significant projects include the Borden, Century and Coffee projects in Canada, and the NuevaUnión (50% interest) and Norte Abierto (50% interest) projects in Chile.

The Company’s current sources of operating cash flows are primarily from the sale of gold, silver, zinc, copper and lead. Goldcorp's principal product is refined gold bullion sold primarily in the London spot market. In addition to gold, the Company also produces silver, zinc, copper and lead primarily from concentrate produced at the Peñasquito mine, which is sold to third party smelters and refineries.

Goldcorp has an investment-grade credit rating, supported by a strong balance sheet, and remains 100% unhedged to gold sales, providing full exposure to gold prices.

STRATEGY

Goldcorp's vision is to create sustainable value for its stakeholders by growing net asset value ("NAV") per share to generate long-term shareholder value. With a portfolio of long-life, high quality assets that provide economies of scale, coupled with low AISC and underpinned by a strong balance sheet, Goldcorp has optimized its portfolio of assets and is reinvesting in a strong pipeline of organic opportunities to drive increasing margins and returns on investment.

In 2016, the Company outlined its 20/20/20 growth plan under which it expects to deliver a 20% increase in gold production, a 20% increase in gold reserves and a 20% reduction in AISC by 2021. In the first quarter of 2018, the Company introduced its Beyond 20/20 program which is focused on the potential for organic growth through the development of the Company's long-term portfolio, such as the Century project at the Porcupine camp, NuevaUnión and Norte Abierto.

Goldcorp is also committed to being a responsible steward of the environment and building collaborative partnerships with communities, governments and all other stakeholders for mutual success.

Goldcorp believes its strong balance sheet provides the Company with flexibility and the ability to manage the risk of gold and commodity price volatility. The Company's capital allocation strategy focuses on investing in its pipeline of organic growth opportunities, further debt reduction and returning capital to its shareholders by paying a sustainable dividend. Furthermore, Goldcorp leverages its exploration spending in the most efficient way possible through investments in junior mining companies.

CORPORATE DEVELOPMENTS

Advanced Project Pipeline

The Company continued to execute on its project pipeline during the first quarter of 2018. At March 31, 2018, construction of Peñasquito's Pyrite Leach project ("PLP") was 86% complete and commissioning is expected to commence in the fourth quarter of 2018, three months ahead of schedule. At Musselwhite, the Materials Handling project was 65% complete at March 31, 2018, progressing on schedule and expected to be approximately 10% under budget. In addition, a significant milestone was reached on the NuevaUnión project during the first quarter of 2018 with the completion of a pre-feasibility study on the combined Relincho and La Fortuna deposits. The pre-feasibility study includes updated capital and operating cost estimates for the combined projects and reflects a phased development approach. Trade-off studies, including the evaluation of environmental, social and technological options, are ongoing. Lastly, at the Coffee project, the adequacy review process advanced as planned. In April 2018, the Company submitted additional information to the Yukon's Environmental and Socio-economic Assessment Board in response to their request which is part of the normal course review of the project at this stage. In addition, Tr’ondëk Hwëch’in First Nation ("TH"), whose Traditional Territory covers 100% of Coffee's project footprint, and Goldcorp are continuing to make progress towards finalizing a broad benefits agreement that will address the impacts of the Coffee project on TH’s Treaty Rights. The negotiators for TH and Goldcorp have agreed in principle to the majority of the terms of the collaboration benefits agreement which remain subject to definitive documentation and final approval of both TH and Goldcorp.

Progress Towards Delivering $250 million of Sustainable Annual Efficiencies

The Company continues to make progress in executing its productivity and cost optimization programs with $210 million of sustainable annual efficiencies achieved as at the end of the first quarter of 2018 across the Company's portfolio. Much of the additional improvement in 2018 will result from decreasing costs of goods and services throughout the supply chain. In addition to these cost reductions, further productivity gains are expected at Hoyle underground as Porcupine progresses toward the goal of delivering ore at the rate of 1,300 tonnes per day. In addition to improved blasting practices, further productivity gains are also expected at Musselwhite through the use of tele-remote mucking.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

At Éléonore, incremental improvements are expected to metal recoveries through 2018 and enhancements to Peñasquito’s process plant are also expected to yield improved recoveries. The Company expects further productivity improvements at Cerro Negro and cost reductions at Red Lake to successfully extend the program beyond $250 million of annual sustainable efficiencies in the second half of 2018.

Advances in Innovation

In 2017, Goldcorp launched its innovation strategy with a series of projects to advance innovative technologies, covering every stage of the mining life cycle, aimed at increasing productivity, improving safety, operating in a more environmentally sustainable manner and ultimately increasing NAV.

During the first quarter of 2018, the Company advanced its innovation strategy with the completion of construction of a demonstration plant at Porcupine to evaluate the effectiveness of ore sorting technology (the "Waste to Ore" project). Assuming the technology is successful on a large scale, it will be incorporated into the trade-off studies being conducted for the Century project at Porcupine, along with testing its application at Goldcorp's other sites. Benefits of the Waste to Ore project include a smaller environmental footprint associated with reduced waste and reductions in emissions and energy consumption, which align with the Company's 20/20/20 plan and support Goldcorp's commitment to being a responsible steward of the environment.

Debt Refinancing

On March 14, 2018, the Company entered into three one-year non-revolving term loan agreements, totaling $400 million. The term loans bear interest at LIBOR plus 0.65%, reset monthly, and are repayable before March 14, 2019 without penalty. The proceeds from the term loans were used to repay the $500 million 2.125% notes that were due on March 15, 2018.

Executive Appointment

As part of a planned succession, Patrick Merrin, formerly Vice President, Canada Operations, assumed the role of Senior Vice President, Canada Operations as of February 1, 2018. Mr. Merrin joined Goldcorp in September 2017. Prior to joining Goldcorp, he held various executive and management positions in the mining industry, having most recently served as Vice President of the Arizona Business unit with Hudbay Minerals Inc. Mr. Merrin holds a Bachelor in Chemical Engineering from McGill University and a Masters of Business Administration from the University of Toronto and has been a member of the Professional Engineers of Ontario since 1997.

MARKET OVERVIEW

Gold

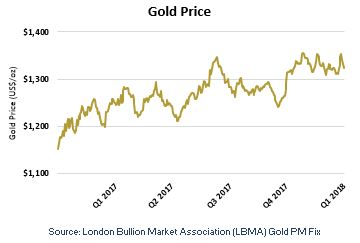

The market price of gold is the primary driver of Goldcorp's profitability. The price of gold can fluctuate widely and is affected by a number of macroeconomic factors, including the sale or purchase of gold by central banks and financial institutions, interest rates, exchange rates, inflation or deflation, global and regional supply and demand and the political and economic conditions of major gold-producing and gold-consuming countries throughout the world.

The price of gold started 2018 at $1,303 per ounce and rallied throughout January to a high of $1,366 per ounce before settling into a broad trading range between these two levels. The price of gold closed the first quarter of 2018 at $1,326 per ounce, a gain of approximately 2% for the quarter. On an attributable basis, the Company realized an average gold price of $1,337 per ounce in the first quarter of 2018, an 8% increase compared to $1,236 per ounce in the first quarter of 2017, and a 4% increase compared to $1,286 per ounce in the fourth quarter of

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

2017. During the first quarter of 2018 there was a change in leadership at the U.S. Federal Reserve with Jerome Powell assuming the role of Chairman from Janet Yellen. Despite the change in leadership, the Federal Reserve continued its recent policy of gradual interest rate hikes at its March 2018 meeting, and market expectations are for further increases throughout 2018 which should continue to influence sentiment and gold price performance.

Currency Markets

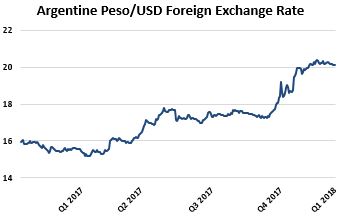

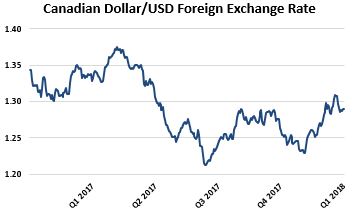

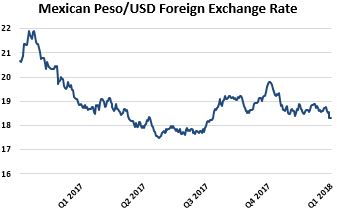

The results of Goldcorp's mining operations are affected by changes in the US dollar exchange rate compared to currencies of the countries in which Goldcorp has foreign operations. The Company has exposure to the Canadian dollar relating to its Éléonore, Musselwhite, Porcupine and Red Lake operations and the Coffee and Century projects, exposure to the Mexican peso relating to its Peñasquito operation, exposure to the Argentine peso at its Cerro Negro operation, exposure to the Dominican Republic peso relating to its investment in Pueblo Viejo and exposure to the Chilean peso with respect to its NuevaUnión and Norte Abierto joint ventures.

Fluctuations in the US dollar can cause volatility of costs reported in US dollars. In addition, monetary assets and liabilities that are denominated in non-US dollar currencies, such as cash and cash equivalents and value-added taxes, are subject to currency risk. Goldcorp is further exposed to currency risk through non-monetary assets and liabilities of entities whose taxable profit or tax loss are denominated in non-US dollar currencies. Changes in exchange rates give rise to temporary differences resulting in deferred tax assets and liabilities with the resulting deferred tax charged or credited to income tax expense.

Goldcorp's financial risk management policy allows the hedging of foreign exchange exposure to reduce the risk associated with currency fluctuations. The Company enters into Mexican peso currency hedge contracts to purchase Mexican pesos at pre-determined US dollar amounts. These contracts are entered into to normalize operating expenses and capital expenditures at Peñasquito, expressed in US dollar terms.

Currency markets exhibited volatility during the first quarter of 2018 largely due to the instability of the US dollar influenced by the Federal Reserve Bank interest rate hike as well as other US economic policy decisions. The Canadian dollar depreciated since the end of February 2018 despite strong economic data, driven by the uncertainty over the NAFTA negotiations and interest rate expectations. On the other hand, the Mexican peso strengthened by 7%, ending the first quarter at 18.33. The probability of a US withdrawal from NAFTA has lessened as the United States is showing some flexibility on key issues, which is a positive development ahead of the Presidential Election in Mexico in July 2018.

The Argentine peso remained under pressure during the first quarter of 2018 as the Central Bank of Argentina struggles to meet the 15% inflation target in 2018, which led to the Central Bank Monetary Policy Committee ("MPC") maintaining the interest rate at 27.25%. The worst drought in decades is expected to negatively impact agricultural exports in 2018, putting further pressure on the currency in 2018. However, the MPC is preserving its hawkish guidance notwithstanding some inflationary headwinds from what it believes are transitory factors such as foreign exchange pass-through from the recent depreciation in the Argentine peso and significant adjustments in regulated tariffs. The MPC is somewhat optimistic that once these transitory factors pass that the path towards disinflation will return due to the restrictive policy stance and the expectation that the cycle of large increases in regulated prices will end in April 2018. In addition, the MPC believes that the Argentine peso is unlikely to depreciate significantly going forward given the actions of the Central Bank and the already high level of the real exchange rate following the large depreciation of the Argentine peso between December 2017 and February 2018.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Foreign Exchange Rate Sources:

| |

| (a) | Canadian Dollar/USD: Bank of Canada Noon rate (January 1, 2017 - April 28, 2017), Bank of Canada Daily Average (April 29, 2017 - March 31, 2018) |

| |

| (b) | Mexican Peso/USD: Central Bank of Mexico Current Day Fixing |

| |

| (c) | Argentine Peso/USD: Central Bank of Argentina Current Day Fixing |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

OVERVIEW OF QUARTERLY FINANCIAL AND OPERATING RESULTS

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31 | December 31 | September 30 | June 30 |

| | 2018 |

| 2017 |

| 2017 |

| 2016 |

| 2017 |

| 2016 |

| 2017 |

| 2016 |

|

| Financial Results | | | | | | | | |

| Revenues | $ | 846 |

| $ | 882 |

| $ | 853 |

| $ | 898 |

| $ | 866 |

| $ | 915 |

| $ | 822 |

| $ | 753 |

|

| Net earnings (loss) | $ | 67 |

| $ | 170 |

| $ | 242 |

| $ | 101 |

| $ | 111 |

| $ | 59 |

| $ | 135 |

| $ | (78 | ) |

| Net earnings (loss) per share | | | | | | | | |

| – Basic and diluted | $ | 0.08 |

| $ | 0.20 |

| $ | 0.28 |

| $ | 0.12 |

| $ | 0.13 |

| $ | 0.07 |

| $ | 0.16 |

| $ | (0.09 | ) |

| Operating cash flow | $ | 271 |

| $ | 227 |

| $ | 511 |

| $ | 239 |

| $ | 315 |

| $ | 267 |

| $ | 158 |

| $ | 234 |

|

Adjusted operating cash flow (1) | $ | 350 |

| $ | 315 |

| $ | 401 |

| $ | 306 |

| $ | 308 |

| $ | 401 |

| $ | 320 |

| $ | 204 |

|

Adjusted EBITDA (1) | $ | 433 |

| $ | 427 |

| $ | 448 |

| $ | 477 |

| $ | 400 |

| $ | 491 |

| $ | 432 |

| $ | 269 |

|

| Expenditures on mining interests (cash basis) | $ | 287 |

| $ | 186 |

| $ | 420 |

| $ | 217 |

| $ | 291 |

| $ | 168 |

| $ | 233 |

| $ | 177 |

|

| – Sustaining | $ | 119 |

| $ | 113 |

| $ | 187 |

| $ | 145 |

| $ | 143 |

| $ | 112 |

| $ | 133 |

| $ | 140 |

|

| – Expansionary | $ | 168 |

| $ | 73 |

| $ | 233 |

| $ | 72 |

| $ | 148 |

| $ | 56 |

| $ | 100 |

| $ | 37 |

|

| Dividends paid | $ | 14 |

| $ | 15 |

| $ | 16 |

| $ | 16 |

| $ | 15 |

| $ | 14 |

| $ | 16 |

| $ | 16 |

|

Operating Results (1) | | | | | | | | |

| Gold produced (thousands of ounces) | 590 |

| 655 |

| 646 |

| 761 |

| 633 |

| 715 |

| 635 |

| 613 |

|

Gold sold (thousands of ounces) | 585 |

| 646 |

| 633 |

| 768 |

| 606 |

| 686 |

| 649 |

| 616 |

|

| Silver produced (thousands of ounces) | 6,800 |

| 7,100 |

| 7,100 |

| 7,400 |

| 7,000 |

| 7,700 |

| 7,400 |

| 5,300 |

|

| Copper produced (thousands of pounds) | 5,400 |

| 9,700 |

| 4,500 |

| 20,400 |

| 6,300 |

| 16,900 |

| 7,900 |

| 14,400 |

|

| Lead produced (thousands of pounds) | 27,000 |

| 32,400 |

| 36,500 |

| 29,600 |

| 38,300 |

| 33,700 |

| 26,100 |

| 17,100 |

|

| Zinc produced (thousands of pounds) | 88,700 |

| 80,700 |

| 96,500 |

| 78,300 |

| 98,400 |

| 75,200 |

| 84,100 |

| 38,300 |

|

| Average realized gold price (per ounce) | $ | 1,337 |

| $ | 1,236 |

| $ | 1,286 |

| $ | 1,181 |

| $ | 1,287 |

| $ | 1,333 |

| $ | 1,256 |

| $ | 1,277 |

|

Cash costs: by-product (per ounce) (2) | $ | 511 |

| $ | 540 |

| $ | 462 |

| $ | 481 |

| $ | 483 |

| $ | 554 |

| $ | 510 |

| $ | 728 |

|

Cash costs: co-product (per ounce) (3) | $ | 696 |

| $ | 701 |

| $ | 627 |

| $ | 619 |

| $ | 663 |

| $ | 657 |

| $ | 644 |

| $ | 716 |

|

| All-in sustaining costs (per ounce) | $ | 810 |

| $ | 800 |

| $ | 870 |

| $ | 747 |

| $ | 827 |

| $ | 812 |

| $ | 800 |

| $ | 1,067 |

|

| |

| (1) | The Company has presented the non-GAAP performance measures on an attributable (or Goldcorp's share) basis in the table above. Adjusted operating cash flows, Adjusted EBITDA and AISC are non-GAAP financial performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 31-38 of this report. |

| |

| (2) | Total cash costs: by-product, per ounce, is calculated net of Goldcorp’s share of by-product sales revenues (by-product silver sales revenues for Cerro Negro, Marlin and Pueblo Viejo; by-product lead, zinc and copper sales revenues and 75% of silver sales revenues for Peñasquito at market silver prices, and 25% of silver sales revenues for Peñasquito at $4.17 per silver ounce (2017 – $4.13 per silver ounce) sold to Wheaton Precious Metals Corp. ("Wheaton") and by-product copper sales revenues for Alumbrera). |

| |

| (3) | Total cash costs: co-product, per ounce, is calculated by allocating Goldcorp’s share of production costs to each co-product (Alumbrera (copper); Marlin (silver); Pueblo Viejo (silver and copper); Peñasquito (silver, lead and zinc)) based on the ratio of actual sales volumes multiplied by budget metal prices (see page 32). |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

REVIEW OF FIRST QUARTER FINANCIAL RESULTS

Three months ended March 31, 2018 compared to the three months ended March 31, 2017

Net earnings for the three months ended March 31, 2018 were $67 million, or $0.08 per share, compared to net earnings of $170 million, or $0.20 per share, for the three months ended March 31, 2017. The decrease in net earnings in the first quarter of 2018 compared to the same period in 2017 was primarily due to a decrease in net earnings relating to the Company's associates and joint venture and an increase in the Company's income tax expense compared to the same period in 2017 partially offset by the impact of increases in average realized gold and zinc prices.

Net earnings and earnings per share for the three months ended March 31, 2018 and 2017 were affected by, among other things, the following non-cash or other items that management believes are not reflective of the performance of the underlying operations (items are denoted as having (increased)/decreased net earnings and net earnings per share in the three months ended March 31, 2018 and 2017):

|

| | | | | | | | | | | | | | | | | | |

| | Three months ended March 31, 2018 | Three months ended March 31, 2017 |

| (in millions, except per share) | Pre-tax | After-tax |

| Per share ($/share) |

| Pre-tax | After-tax | Per share

($/share) |

| Reduction in Goldcorp's share of Pueblo Viejo's earnings relating to settlement of a Dominican Republic tax audit | $ | 17 |

| $ | 17 |

| $ | 0.02 |

| $ | — |

| $ | — |

| $ | — |

|

| Non-cash foreign exchange gain on deferred tax balances | $ | — |

| $ | (16 | ) | $ | (0.02 | ) | $ | — |

| $ | (61 | ) | $ | (0.07 | ) |

| Gain from reduction in provision for Alumbrera's reclamation costs | $ | — |

| $ | — |

| $ | — |

| $ | (26 | ) | $ | (26 | ) | $ | (0.03 | ) |

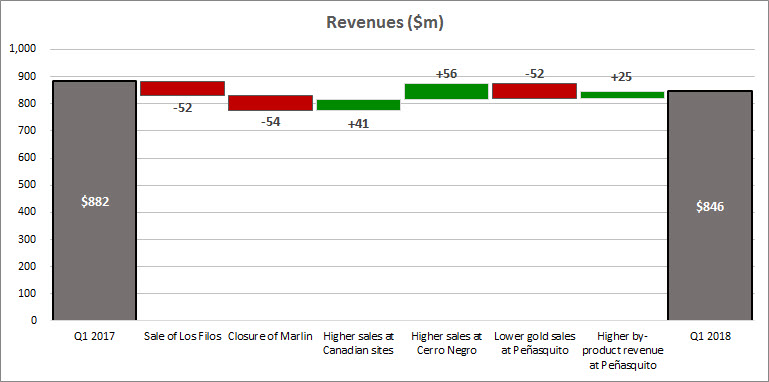

Revenues

|

| | | | | | | | | |

| Three months ended March 31 | 2018 (1) | 2017 (1) | Change |

| Gold | | | |

| | Revenue (millions) | $ | 620 |

| $ | 664 |

| (7 | )% |

| | Ounces sold (thousands) | 466 |

| 539 |

| (14 | )% |

| | Average realized price ($/ounce) | $ | 1,334 |

| $ | 1,236 |

| 8 | % |

| Silver | | | |

| | Revenue (millions) | $ | 81 |

| $ | 100 |

| (19 | )% |

| | Ounces sold (thousands) | 6,003 |

| 6,769 |

| (11 | )% |

| | Average realized price ($/ounce) | $ | 14.21 |

| $ | 15.47 |

| (8 | )% |

| Zinc | | | |

| | Revenue (millions) | $ | 121 |

| $ | 93 |

| 30 | % |

| | Pounds sold (thousands) | 88,000 |

| 88,500 |

| (1 | )% |

| | Average realized price | $ | 1.51 |

| $ | 1.32 |

| 14 | % |

| Other metals | | | |

| | Revenue (millions) | $ | 24 |

| $ | 25 |

| (4 | )% |

| Total revenue (millions) | $ | 846 |

| $ | 882 |

| (4 | )% |

| |

| (1) | Excludes attributable share of revenues from the Company's associates. Revenues are shown net of applicable treatment and refining charges. |

Revenues decreased by $36 million, or 4%, primarily due to decreases in gold and silver sales volumes of 14% and 11%, respectively, and an 8% decrease in the average realized price of silver. These decreases were offset partially by a 30% increase in zinc revenues, driven by a 14% increase in the average realized price and lower treatment and refining charges, and an 8% increase in the average realized price of gold. The decrease in gold sales volumes was primarily due to the impacts of the sale of Los Filos in April 2017 and closure of Marlin in the second quarter of 2017. In addition, gold sales volumes were lower at Peñasquito due to lower grade ore as a result of the planned transition from the higher grade area of Phase 5 at the bottom of the Peñasco pit to primarily lower grade ore from the beginning of Phase 6 and lower grade stockpiles. These decreases in gold sales volume were partially offset by an increase in sales volumes at Cerro Negro, primarily due to higher grade as a result of mine sequencing. The decrease in silver sales volumes was primarily due to the closure of Marlin in 2017.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Production Costs

Production costs in the first quarter of 2018 decreased by $56 million, or 11%, when compared to the same period in 2017 primarily due to the divestiture of Los Filos in April 2017 ($39 million) and the closure of Marlin in the second quarter of 2017 ($35 million), partially offset by an increase in production costs at Cerro Negro due primarily to an increase royalties and production taxes due to higher sales, and higher employee costs.

Depreciation and Depletion

|

| | | | | | | | |

| Three months ended March 31 | 2018 (1) | 2017 (1) | Change |

| Depreciation and depletion (millions) | $ | 251 |

| $ | 246 |

| 2 | % |

| Sales ounces (thousands) | 466 |

| 539 |

| (14 | )% |

| Depreciation and depletion per ounce | $ | 539 |

| $ | 456 |

| 18 | % |

| |

| (1) | Excludes attributable share of depreciation and depletion from the Company's associates. |

Depreciation and depletion increased by $5 million, or 2%, mainly due to a higher depletable cost base at Peñasquito in 2018 and higher sales volumes at Cerro Negro, offset partially by the impacts of the sale of Los Filos in April 2017 and closure of Marlin in the second quarter of 2017.

Share of Net Earnings Related to Associates and Joint Venture

|

| | | | | | | | |

| Three months ended March 31 | 2018 | 2017 | Change |

| Pueblo Viejo | $ | 9 |

| $ | 27 |

| (67 | )% |

| Alumbrera | — |

| 33 |

| (100 | )% |

| Share of net earnings related to associates and joint venture | $ | 9 |

| $ | 60 |

| (85 | )% |

The Company’s share of net earnings related to associates and joint venture decreased by $51 million in the first quarter of 2018 compared to the same period in 2017 primarily due to a $33 million reduction in the Company's provision to fund its share of Alumbrera’s reclamation costs in the first quarter of 2017, and a decrease in net earnings from Pueblo Viejo. The decrease in net earnings from Pueblo Viejo was due to an increase in tax expense of $17 million arising from the settlement of a Dominican Republic tax audit, higher depreciation and depletion relating to the impact of the reversal of impairment recognized at December 31, 2017, and higher production costs related to higher power and planned maintenance costs.

Impairment reversal

The Company recorded a net impairment reversal of $3 million in the three months ended March 31, 2017. The net impairment reversal was comprised of a reversal of impairment at Cerro Blanco of $19 million, which was based on the expected proceeds from the sale to Bluestone being greater than the carrying value of the asset, partially offset by an impairment expense at Los Filos of $16 million, based on changes to the assessed fair value of the Los Filos assets that were subsequently sold to Leagold.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Corporate Administration

Corporate administration expenses increased by $5 million in the first quarter of 2018 compared to the first quarter of 2017, primarily due to a reduction in employee costs in the first quarter of 2017 relating to the impact of a lower bonus payout than accrued in the prior year and higher consulting expenses in the first quarter of 2018 compared to the same period in the prior year associated with strategic sourcing and procurement services. The Company partnered with a vendor and is in the process of centralizing these services for all its mine sites and corporate offices as part of its program to realize $250 million in annual sustainable efficiencies. The cost of these services is expected to be more than offset by savings in operating expenses and other corporate expenditures.

Income Tax Expense

The income tax expense of $4 million for three months ended March 31, 2018 resulted in a 6% tax rate (three months ended March 31, 2017 - $48 million income tax recovery and a negative 39% tax rate) and was impacted primarily by currency translations.

Currency translation

The impact of changes in foreign exchange rates on deferred tax balances and intra-group financing arrangements resulted in a $16 million income tax recovery for the three months ended March 31, 2018 (three months ended March 31, 2017 - $61 million income tax recovery).

The impact of changes in foreign exchange rates on current tax balances resulted in a $4 million income tax expense for the three months ended March 31, 2018 (three months ended March 31, 2017 - $4 million income tax recovery).

Effective tax rate

Earnings before income taxes of $71 million for three months ended March 31, 2018 was impacted by the following items: $7 million of non-deductible share-based compensation expense (three months ended March 31, 2017 - $9 million); nil non-deductible reversals of impairment (three months ended March 31, 2017 - $3 million reversal of impairment); and $9 million of after-tax income from associates (particularly Pueblo Viejo) that are not subject to further income tax in the accounts of the Company (three months ended March 31, 2017 - $60 million).

After adjusting for the above mentioned items, the effective income tax rate for three months ended March 31, 2018 was 25% (three months ended March 31, 2017 - 25%).

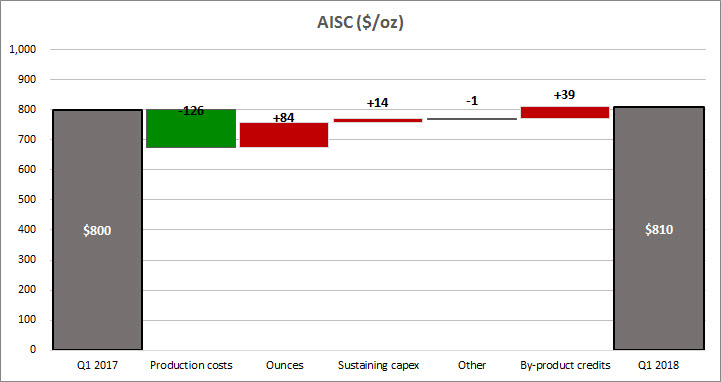

AISC

AISC(1) were $810 per ounce for the three months ended March 31, 2018, compared to $800 per ounce for the three months ended March 31, 2017. The increase in AISC was due primarily to lower gold sales ($84 per ounce), lower by-product credits ($39 per ounce), and higher sustaining capital ($14 per ounce), partially offset by lower production costs ($126 per ounce). The decrease in gold sales was primarily due to lower sales at Peñasquito due to mine sequencing, and the impacts of the sale of Los Filos and closure of Marlin in the first half of 2017, partially offset by an increase in gold sales at Cerro Negro due to higher gold grade. The decrease in production costs was primarily due to the sale of Los Filos and closure of Marlin in 2017. The increase in sustaining capital was primarily due to higher capitalized stripping tonnes driven by the start of Moore phase 6 and higher spend on tailings facilities construction at Pueblo Viejo, and costs associated with increased development and an expansion of the tailings area at Cerro Negro. The decrease in by-product credits was primarily due to lower by-product production for all metals, which were impacted partially by the closure of Marlin in 2017, partially offset by 14% increase in the average realized price of zinc.

| |

| (1) | AISC per ounce is a non-GAAP financial performance measure with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 31-38 of this report. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

FINANCIAL POSITION AND LIQUIDITY

The following table summarizes Goldcorp's cash flow activity:

|

| | | | | | |

| | Three Months Ended March 31 |

| | 2018 |

| 2017 |

|

| Cash flow | | |

| From continuing operations provided by operating activities | $ | 271 |

| $ | 227 |

|

| From continuing operations used in investing activities | (268 | ) | (247 | ) |

| From continuing operations used in financing activities | (66 | ) | 54 |

|

| Increase (decrease) in cash and cash equivalents | (63 | ) | 34 |

|

| Cash and cash equivalents, beginning of period | 186 |

| 157 |

|

| Increase in cash and cash equivalents reclassified as held for sale | — |

| (22 | ) |

| Cash and cash equivalents, end of period | $ | 123 |

| $ | 169 |

|

Cash flow provided by operating activities for the three months ended March 31, 2018 increased compared to the three months ended March 31, 2017 primarily due an increase in earnings from mine operations driven by an 8% increase in realized gold prices and a 14% increase in realized zinc prices. In addition, during the first quarter of 2018, cash provided by operating activities increased by $28 million as compared to the same period in 2017 due to positive changes in non-cash working capital and other operating activities.

The increase in cash flow used in investing activities for the three months ended March 31, 2018 compared to the three months ended March 31, 2017 was due mainly to an $87 million increase in expenditures on mining interests and an $18 million reduction in funds received from Pueblo Viejo as return of capital, partially offset by a decrease of $28 million in purchases of equity securities as compared to the same period in 2017. Cash flows used in investing activities for the three months ended March 31, 2017 also included the purchase of the gold stream on the El Morro deposit, part of the Company's NuevaUnión joint venture, from New Gold Inc. for $65 million.

Expenditures on mining interests (including deposits on mining interest expenditures) were as follows:

|

| | | | | | |

| | Three Months Ended March 31 |

| | 2018 |

| 2017 |

|

| Éléonore | $ | 17 |

| $ | 29 |

|

| Musselwhite | 24 |

| 11 |

|

| Porcupine | 28 |

| 14 |

|

| Red Lake | 21 |

| 17 |

|

| Peñasquito | 129 |

| 73 |

|

| Cerro Negro | 19 |

| 16 |

|

| Other | 29 |

| 20 |

|

| Total | $ | 267 |

| $ | 180 |

|

The increase in expenditures on mining interests during the three months ended March 31, 2018 compared to the three months ended March 31, 2017 was due primarily to an increase in expansionary capital of $95 million related to the construction of the PLP at Peñasquito, the Waste to Ore project at Porcupine, construction activities at the Borden and Century projects, as well as the Materials Handling project at Musselwhite.

Cash flow used in financing activities for the three months ended March 31, 2018 increased by $120 million as compared to the same period in 2017. The increase compared to 2017 was primarily due to net debt and credit facility repayments of $50 million in the first quarter of 2018 as compared to a net credit facility draw down of $70 million in the same period in 2017.

On March 14, 2018, the Company entered into three one-year non-revolving term loan agreements, totaling $400 million. The term loans bear interest at LIBOR plus 0.65%, reset monthly, and are repayable before March 14, 2019 without penalty. The proceeds from the term loans were used to repay the $500 million note that was due on March 15, 2018.

At March 31, 2018, the Company's net debt and adjusted net debt(1) was $2.3 billion and $2.1 billion, respectively. At March 31, 2018, excluding cash and cash equivalents held at associates of $186 million, the Company had $3.1 billion of available liquidity, comprised of $0.2 billion of cash and cash equivalents and short term investments, and $2.95 billion available on its $3.0 billion credit facility.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

The Company may from time to time seek to retire or repurchase its outstanding debt in open market purchases, privately negotiated transactions or otherwise. Such repurchases, if any, will depend upon prevailing market conditions, the Company's liquidity requirements, contractual restrictions and other factors. The amount of debt retired or repurchased may be material.

| |

| (1) | The Company has presented the non-GAAP performance measures on an attributable (or Goldcorp's share) basis. Adjusted net debt is a non-GAAP financial performance measure with no standardized definition under IFRS. For further information, please see pages 31-38 of this report. |

Outstanding Share Data

As at April 25, 2018, there were 869 million common shares of the Company issued and outstanding and 6 million stock options outstanding, which are exercisable into common shares at exercise prices ranging between C$20.27 per share to C$30.41 per share, and 3 million restricted share units outstanding.

GUIDANCE (1)

Goldcorp expects to produce 2.5 million ounces (+/- 5%) of gold in 2018, consistent with previous 2018 guidance. AISC are expected to be $800 per ounce (+/- 5%) in the same period.

The Company’s 20/20/20 plan remains unchanged. As previously guided, gold production is expected to increase 20% to 3.0 million ounces by 2021 compared to baseline production of 2.5 million ounces in 2017. AISC are expected to decrease by 20% to approximately $700 per ounce over the same period driven by the ongoing focus on cost efficiencies and productivity improvements. Gold mineral reserves are expected to increase by 20% to 60 million ounces by 2021 supported by the exploration potential and ongoing programs across the Company's operating assets, joint ventures and projects.

Complete production and cost guidance to 2021 is provided below.

|

| | | | | |

Production (+/- 5%) (2) | Units | 2018E | 2019E | 2020E | 2021E |

| Gold Production | Moz | 2.5 | 2.7 | 3.0 | 3.0 |

| Silver Production | Moz | 30 | 50 | 40 | 35 |

| Zinc Production | Mlbs | 300 | 425 | 450 | 400 |

| Lead Production | Mlbs | 160 | 300 | 250 | 150 |

|

| | | | | |

Costs (+/- 5%) (2, 3) | Units | 2018E | 2019E | 2020E | 2021E |

AISC (4) | $/oz | 800 | 750 | 700 | 700 |

| By-product Cash Costs | $/oz | 450 | 400 | 400 | 400 |

|

| | | | | |

| Capital Expenditures (+/- 5%) | Units | 2018E | 2019E | 2020E | 2021E |

Sustaining Capital (2, 5) | $M | 550 | 575 | 575 | 575 |

Expansionary Capital (2, 5) | $M | 750 | 250 | 300 | 300 |

|

| |

| Other 2018 Estimates | 2018E |

| Corporate Administration ($M) (including non-cash stock compensation of $40M) | $140 |

Exploration ($M) (2, 6) | $125 |

Depreciation and depletion ($/oz) (2) | $485 |

Tax rate (2) | 40 - 45% |

| |

| (1) | Guidance projections (“Guidance”) are considered “forward-looking statements” and represent management’s good faith estimates or expectations of future production results as of the date hereof. Guidance is based upon certain assumptions, including, but not limited to, metal prices, fuel prices, certain exchange rates and other assumptions. Such assumptions may prove to be incorrect and actual results may differ materially from those anticipated. Consequently, Guidance cannot be guaranteed. As such, investors are cautioned not to place undue reliance upon Guidance and forward-looking statements as there can be no assurance that the plans, assumptions or expectations upon which they are placed will occur. See the "Cautionary Statement Regarding Forward-Looking Statements". |

| |

| (2) | The Company has presented the non-GAAP performance measures on an attributable (or Goldcorp's share) basis. AISC per ounce and cash costs: by-product are non-GAAP financial performance measures with no standardized definition under IFRS. For further information, please see pages 31-38 of this report. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

| |

| (3) | The assumptions below were used to forecast total cash costs: |

|

| | |

| | 2018 - 2019 | 2020 - 2021 |

| Gold (oz) | $1,300 | $1,300 |

| Silver (oz) | $19.00 | $18.00 |

| Copper (lb) | $2.75 | $3.00 |

| Zinc (lb) | $1.30 | $1.15 |

| Lead (lb) | $1.10 | $1.00 |

| Foreign exchange (respectively to the US$) | | |

| Canadian dollar | $1.25 | $1.25 |

| Mexican peso | 19.00 | 19.00 |

| |

| (4) | The Company’s projected AISC are not based on GAAP total production cash costs, which forms the basis of the Company’s cash costs: by-product. The projected range of AISC is anticipated to be adjusted to include sustaining capital expenditures, corporate administrative expense, mine-site exploration and evaluation costs and reclamation cost accretion and amortization, and exclude the effects of expansionary capital and non-sustaining expenditures. Projected GAAP total production cash costs for the full year would require inclusion of the projected impact of future included and excluded items, including items that are not currently determinable, but may be significant, such as sustaining capital expenditures, reclamation cost accretion and amortization. Due to the uncertainty of the likelihood, amount and timing of any such items, the Company does not have information available to provide a quantitative reconciliation of projected AISC to a total production cash costs projection. |

| |

| (5) | Excludes capitalized exploration costs (see footnote 6). Expansionary capital includes capital costs for those projects which are in execution and/or have an approved feasibility study. Projects without an approved feasibility study only include capital costs to the next stage gate. |

| |

| (6) | Approximately 40% of exploration spending is expected to be expensed and approximately 60% is expected to be capitalized. Approximately 50% of exploration spending considered sustaining and approximately 50% is considered expansionary. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

OPERATIONAL REVIEW

The Company’s principal producing mining properties are comprised of the Éléonore, Musselwhite, Porcupine and Red Lake mines in Canada; the Peñasquito mine in Mexico; the Cerro Negro mine in Argentina; and the Pueblo Viejo mine (40.0% interest) in the Dominican Republic.

Operating results of operating segments are reviewed by the Company's chief operating decision maker ("CODM") to make decisions about resources to be allocated to the segments and to assess their performance. The Company considers each individual operating mine as an operating segment for financial reporting purposes except for Alumbrera and Leagold. Alumbrera and Leagold are not considered to be reportable operating segments as their financial results do not meet the quantitative threshold required for segment disclosure purposes. As a result, Alumbrera and Leagold are included in Other.

The Company’s 100% interest in the HG Young project is included in the Red Lake reporting operating segment while the Borden and Century projects are included in the Porcupine reportable operating segments. The Company's 50% interests in the NuevaUnión and Norte Abierto projects in Chile, and 100% interest in the Coffee project in the Yukon, are included in Other.

The Company’s principal product is gold bullion which is sold primarily in the London spot market. Concentrate produced at Peñasquito and Alumbrera, containing both gold and by-product metals, is sold to third party smelters and traders.

Segmented Financial and Operating Highlights

|

| | | | | | | | | | | | | |

Three months ended March 31 | | Revenue ($ millions) |

| Gold produced (000's of ounces) |

| Gold sold (000's of ounces) |

| Total cash costs: by-product ($/oz) (1), (4) |

| AISC ($/oz) (3), (4) |

| Earnings (loss) from mine operations ($ millions) |

|

| Peñasquito | 2018 | 329 |

| 98 |

| 90 |

| (315 | ) | 132 |

| 68 |

|

| | 2017 | 356 |

| 137 |

| 138 |

| 85 |

| 391 |

| 91 |

|

| Cerro Negro | 2018 | 177 |

| 118 |

| 120 |

| 451 |

| 600 |

| 34 |

|

| | 2017 | 121 |

| 95 |

| 88 |

| 459 |

| 651 |

| 15 |

|

Pueblo Viejo (4) | 2018 | 139 |

| 94 |

| 97 |

| 423 |

| 591 |

| 64 |

|

| | 2017 | 122 |

| 95 |

| 95 |

| 439 |

| 541 |

| 66 |

|

| Red Lake | 2018 | 81 |

| 60 |

| 61 |

| 902 |

| 1,139 |

| 5 |

|

| | 2017 | 66 |

| 49 |

| 54 |

| 861 |

| 1,149 |

| (2 | ) |

| Éléonore | 2018 | 86 |

| 67 |

| 65 |

| 1,051 |

| 1,204 |

| (15 | ) |

| | 2017 | 88 |

| 78 |

| 72 |

| 850 |

| 1,057 |

| (5 | ) |

| Porcupine | 2018 | 93 |

| 68 |

| 70 |

| 708 |

| 896 |

| 15 |

|

| | 2017 | 76 |

| 61 |

| 62 |

| 843 |

| 1,011 |

| (4 | ) |

| Musselwhite | 2018 | 80 |

| 59 |

| 60 |

| 617 |

| 766 |

| 32 |

|

| | 2017 | 69 |

| 54 |

| 56 |

| 713 |

| 871 |

| 19 |

|

Other mines (2) | 2018 | 42 |

| 26 |

| 22 |

| 1,046 |

| 1,175 |

| 4 |

|

| | 2017 | 146 |

| 86 |

| 81 |

| 691 |

| 773 |

| 17 |

|

Other (3) | 2018 | — |

| — |

| — |

| — |

| 87 |

| (9 | ) |

| | 2017 | — |

| — |

| — |

| — |

| 66 |

| (7 | ) |

Attributable segment total (4) | 2018 | 1,027 |

| 590 |

| 585 |

| 511 |

| 810 |

| 198 |

|

| | 2017 | 1,044 |

| 655 |

| 646 |

| 540 |

| 800 |

| 190 |

|

| Less associates and joint venture | 2018 | (181 | ) | (120 | ) | (119 | ) | (536 | ) | (697 | ) | (67 | ) |

| | 2017 | (162 | ) | (113 | ) | (107 | ) | (436 | ) | (551 | ) | (74 | ) |

| Total - Consolidated | 2018 | 846 |

| 470 |

| 466 |

| 505 |

| 839 |

| 131 |

|

| | 2017 | 882 |

| 542 |

| 539 |

| 561 |

| 849 |

| 116 |

|

| |

| (1) | Total cash costs: by-product, per ounce, is calculated net of Goldcorp’s share of by-product sales revenues (by-product copper sales revenues for Alumbrera; by-product silver sales revenues for Marlin and Pueblo Viejo; and by-product lead and zinc sales revenues and 75% of silver sales revenues for Peñasquito at market silver prices, and 25% of silver sales revenues for Peñasquito at $4.17 per silver ounce (2017 – $4.13 per silver ounce) sold to Wheaton). If silver, copper, lead and zinc were treated as co-products, total cash costs for the three months ended March 31, 2018 would have been $696 per ounce of gold (three months ended March 31, 2017 – $701). Production costs are allocated to each co-product based on the ratio of actual sales volumes multiplied by budget metal prices (see page 32). |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

| |

| (2) | As described above, the Company's investments in Alumbrera and Leagold are included in 'Other' for segment reporting purposes. They have been disclosed separately in these tables, in 'Other mines', along with Los Filos up to the date of its disposal on April 7, 2017 and Marlin up to the date of its closure in the second quarter of 2017, to provide visibility into the impact of the Company's corporate administration expense on AISC. |

| |

| (3) | For the purpose of calculating AISC, the Company included corporate administration expense, capital expenditures incurred at the Company's regional and head corporate offices and regional office exploration expense as corporate AISC in the "Other" category. These costs are not allocated to the individual mine sites as the Company measures its operations' performance on AISC directly incurred at the mine site. AISC for Other was calculated using total corporate expenditures and the Company's total attributable gold sales ounces. |

| |

| (4) | The Company has included certain non-GAAP performance measures including the Company’s share of the applicable production, sales and financial information of Pueblo Viejo, Alumbrera, Leagold and NuevaUnión throughout this document. Total cash costs: by-product and AISC are non-GAAP performance measures with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 31-38 of this report. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

OPERATIONAL REVIEW

Peñasquito, Mexico (100%-owned)

|

| | | | | | | | |

| | Three months ended March 31 |

| Operating Data | 2018 |

| 2017 |

| Change |

|

| Tonnes of ore milled (thousands) | 8,959 |

| 9,510 |

| (6 | )% |

| Mill head grade | | | |

| Gold grade (grams/tonne) | 0.54 |

| 0.75 |

| (28 | )% |

| Silver grade (grams/tonne) | 23.52 |

| 21.19 |

| 11 | % |

| Lead grade | 0.19 | % | 0.22 | % | (14 | )% |

| Zinc grade | 0.64 | % | 0.58 | % | 10 | % |

| Mill Recovery Rate | | | |

| Gold recovery | 67 | % | 66 | % | 2 | % |

| Silver recovery | 85 | % | 82 | % | 4 | % |

| Lead recovery | 76 | % | 76 | % | — | % |

| Zinc recovery | 84 | % | 80 | % | 5 | % |

| Payable Metal Produced | | |

|

|

| Gold (thousands of ounces) | 98 |

| 137 |

| (28 | )% |

| Silver (thousands of ounces) | 5,166 |

| 4,836 |

| 7 | % |

| Lead (thousands of pounds) | 27,000 |

| 32,400 |

| (17 | )% |

| Zinc (thousands of pounds) | 88,700 |

| 80,700 |

| 10 | % |

| Payable Metal Sold | | | |

| Gold (thousands of ounces) | 90 |

| 138 |

| (35 | )% |

| Silver (thousands of ounces) | 4,943 |

| 4,825 |

| 2 | % |

| Lead (thousands of pounds) | 26,000 |

| 31,300 |

| (17 | )% |

| Zinc (thousands of pounds) | 88,000 |

| 88,500 |

| (1 | )% |

| Total Cash Costs: By-product (per ounce) | $ | (315 | ) | $ | 85 |

| (471 | )% |

| Total Cash Costs: Co-product (per ounce) | $ | 708 |

| $ | 668 |

| 6 | % |

| AISC (per ounce) | $ | 132 |

| $ | 391 |

| (66 | )% |

| Financial Data (in millions) | |

| |

Revenues (1) | $ | 329 |

| $ | 356 |

| (8 | )% |

| Production costs | $ | 181 |

| $ | 193 |

| (6 | )% |

| Depreciation and depletion | $ | 80 |

| $ | 72 |

| 11 | % |

| Earnings from mine operations | $ | 68 |

| $ | 91 |

| (25 | )% |

| Expenditures on mining interests (cash basis) | $ | 131 |

| $ | 75 |

| 75 | % |

| – Sustaining | $ | 36 |

| $ | 40 |

| (10 | )% |

| – Expansionary | $ | 95 |

| $ | 35 |

| 171 | % |

| |

| (1) | Includes 25% of silver ounces sold to Wheaton at $4.17 per ounce (2017 – $4.13 ounce). The remaining 75% of silver ounces are sold at market rates. |

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

First Quarter Operating and Financial Highlights

Gold production for the three months ended March 31, 2018 was lower than the same period in the prior year as a result of the planned transition from the higher grade area of Phase 5 at the bottom of the Peñasco pit to lower grade ore from the beginning of Phase 6 and lower grade stockpiles and 10 days of planned mill downtime for maintenance. Production is planned to revert back to higher grade ore in late 2019 when the Phase 6 stripping program exposes higher grade ore in the Peñasco pit.

Tonnes processed for the three months ended March 31, 2018 were lower than the same period in the prior year due to 10 days of planned shut downs during the month of February for mill relines and completing all tie-ins for the PLP, which reduced the number of operating days for the mill. Subsequent to the shutdown, new records were established for throughput at the primary crusher and concentrator driven by the continued implementation of a management operating system which resulted in more consistent ore delivery to the primary crusher. Ongoing mill improvement projects resulted in higher mill recoveries, despite processing some lower grade material.

Earnings from mine operations for the three months ended March 31, 2018 were lower than the same period in the prior year primarily due to lower gold sales, and higher depreciation and depletion, partially offset by higher zinc revenue due to 14% higher zinc prices, and a higher gold price. Production costs for the three months ended March 31, 2018 decreased when compared with the same period in the prior year due to continuing cost optimization efforts, despite the impact of market price increases for diesel and electricity, and offset by an increase in depreciation and depletion due to a higher depletable cost base in 2018.

AISC for the three months ended March 31, 2018 were lower than the same period in the prior year due to higher by-product metal credits and lower production costs, partially offset by lower gold production.

Expansionary capital of $95 million for the quarter ended March 31, 2018 included $47 million and $48 million relating to the PLP and Chile Colorado pre-stripping, respectively (see the Project Pipeline section below).

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Cerro Negro, Argentina (100%-owned)

|

| | | | | | | | |

| | Three months ended March 31 |

| Operating Data | 2018 |

| 2017 |

| Change |

|

| Tonnes of ore milled (thousands) | 243 |

| 239 |

| 2 | % |

| Mill Gold grade (grams/tonne) | 14.33 |

| 12.61 |

| 14 | % |

| Mill Silver grade (grams/tonne) | 141.3 |

| 106.5 |

| 33 | % |

| Gold recovery rate | 96 | % | 96 | % | — | % |

| Silver recovery rate | 87 | % | 89 | % | (2 | )% |

| Gold Produced (thousands of ounces) | 118 |

| 95 |

| 24 | % |

| Silver Produced (thousands of ounces) | 1,070 |

| 706 |

| 52 | % |

| Gold Sold (thousands of ounces) | 120 |

| 88 |

| 36 | % |

| Silver Sold (thousands of ounces) | 1,060 |

| 675 |

| 57 | % |

| Total Cash Costs: By-product (per ounce) | $ | 451 |

| $ | 459 |

| (2 | )% |

| Total Cash Costs: Co-product (per ounce) | $ | 524 |

| $ | 529 |

| (1 | )% |

| AISC (per ounce) | $ | 600 |

| $ | 651 |

| (8 | )% |

| Financial Data (in millions) | | | |

| Revenues | $ | 177 |

| $ | 121 |

| 46 | % |

| Production costs | $ | 72 |

| $ | 52 |

| 38 | % |

| Depreciation and depletion | $ | 71 |

| $ | 54 |

| 31 | % |

| Earnings from mine operations | $ | 34 |

| $ | 15 |

| 127 | % |

| Expenditures on mining interests (cash basis) | $ | 19 |

| $ | 16 |

| 19 | % |

| – Sustaining | $ | 17 |

| $ | 14 |

| 21 | % |

| – Expansionary | $ | 2 |

| $ | 2 |

| — | % |

First Quarter Operating and Financial Highlights

Gold production for the three months ended March 31, 2018 was higher than the same period in the prior year due primarily to higher grade. Grade was higher due to mine sequencing.

Mariana Norte design and development work continues according to plan, with ore production expected during the second half of 2018. The development of the Emilia vein will continue through 2018. These new veins will supplement declining production from Eureka in 2019. The mine expects to achieve 4,000 tonnes per day to the mill by the fourth quarter of 2018.

Earnings from mine operations for the three months ended March 31, 2018 were higher than the same period in the prior year due to higher gold sales and a higher realized gold price, partially offset by higher production costs and depreciation and depletion due to higher gold production. Production costs for the three months ended March 31, 2018 were higher than the same period in the prior year due to higher royalties and production taxes due to higher sales, and higher employee costs.

AISC for the three months ended March 31, 2018 were lower than the same period in the prior year due to higher gold production, partially offset by planned higher sustaining capital related to increased underground development and tailings area expansion.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Pueblo Viejo, Dominican Republic (40%-owned)

(tabular amounts below represent Goldcorp's proportionate 40% share)

|

| | | | | | | | |

| | Three months ended March 31 |

| Operating Data | 2018 |

| 2017 |

| Change |

|

| Tonnes of ore milled (thousands) | 858 |

| 730 |

| 18 | % |

| Mill head grade (grams/tonne) | 3.75 |

| 4.50 |

| (17 | )% |

| Recovery rate | 92 | % | 90 | % | 2 | % |

| Gold Produced (thousands of ounces) | 94 |

| 95 |

| (1 | )% |

| Gold Sold (thousands of ounces) | 97 |

| 95 |

| 2 | % |

| Total Cash Costs: By-product (per ounce) | $ | 423 |

| $ | 439 |

| (4 | )% |

Total Cash Costs: Co-product (per ounce) | $ | 482 |

| $ | 464 |

| 4 | % |

| AISC (per ounce) | $ | 591 |

| $ | 541 |

| 9 | % |

Financial Data (in millions) (1) | | | |

| Revenues | $ | 139 |

| $ | 122 |

| 14 | % |

| Production costs | $ | 51 |

| $ | 47 |

| 9 | % |

| Depreciation and depletion | $ | 24 |

| $ | 9 |

| 167 | % |

| Earnings from mine operations | $ | 64 |

| $ | 66 |

| (3 | )% |

| Expenditures on mining interests (cash basis) | $ | 15 |

| $ | 9 |

| 67 | % |

| – Sustaining | $ | 15 |

| $ | 9 |

| 67 | % |

| – Expansionary | $ | — |

| $ | — |

| n/a |

|

| |

| (1) | The Company’s 40% interest in Pueblo Viejo is classified as an investment in associate and is accounted for using the equity method with the Company’s share of net earnings and net assets separately disclosed in the Consolidated Statements of Earnings and Consolidated Balance Sheets, respectively. The financial data disclosed in the table represents the financial data of Pueblo Viejo on a proportionate rather than equity basis. For the three months ended March 31, 2018, the Company's equity earnings from Pueblo Viejo were $9 million (three months ended March 31, 2017 – equity earnings of $27 million). |

First Quarter Operating and Financial Highlights

Gold production for the three months ended March 31, 2018 was in line with the same period in the prior year as lower grades were offset by higher tonnage processed and higher recovery rates. The decrease in head grade was attributable to the mining sequence, with higher grade planned in the second half of 2018. Tonnes milled increased for the three months ended March 31, 2018, compared with the three months ended March 31, 2017, primarily due to the deferral of autoclave shutdowns to the second quarter of 2018. Higher gold recovery resulted from improvements in carbon management, cyanide addition and regeneration kiln control.

Earnings from mine operations for the three months ended March 31, 2018 were lower than the same period in the prior year primarily due to higher production costs and higher depreciation and depletion costs as a result of the reversal of a previously recorded impairment at the end of 2017, partially offset by higher gold revenues. Production costs for the three months ended March 31, 2018 were higher than the same period in the prior year primarily due to the impact of higher power costs and additional planned maintenance costs.

AISC for the three months ended March 31, 2018 were higher than the same period in the prior year primarily due to higher production costs, higher sustaining capital expenditures which resulted from higher capitalized stripping tonnes driven by the start of Moore phases 5 and 6, and by higher spend on tailings facilities construction, partially offset by higher gold sales.

Third Quarter Report – 2017

(in United States dollars, tabular amounts in millions, except where noted)

Red Lake, Canada (100%-owned)

|

| | | | | | | | |