September 1, 2011

By Electronic Submission

Larry Spirgel, Assistant Director

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, NE

Washington, DC 20549

Re: World Surveillance Group Inc.

Registration Statement on Form S-1

Filed July 1, 2011

File No. 333-175307

Mr. Spirgel:

This letter reflects our responses to the comments of the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) as set forth in your letter dated July 28, 2011 to Mr. Glenn D. Estrella, our President and Chief Executive Officer (the “Comment Letter”). The Comment Letter relates to our Form S-1 filed with the Commission byWorld Surveillance GroupInc. (“WSGI” or the "Company") on July 1, 2011.

Please note that the Company’s Form S-1 has also been modified in the Amendment No. 1 to reflect the filing of the Company’s Quarterly Report on Form 10-Q for the three months ended June 30, 2011 and the Company’s Current Report on Form 8-K/A filing the required financial statements and information relating to its acquisition of Global Telesat Corp. as well as corporate events subsequent to the initial filing.

The responses and supplementary information set forth below have been organized in the same manner in which the Staff’s comments were organized.

General

COMMENT 1: We note your references to the fact that you “design, develop, market and sell” lighter- than-air unmanned aerial vehicles. However, we also note your disclosure on page seven that you have not yet sold any of your airships in the commercial marketplace. It appears that the only unmanned aerial vehicles you have built are the Argus One airship and the SkySat airship. We further note that you had no revenue for the three months ended March 31, 2011 and that current assets as of such date were $17,323. Please revise your disclosure throughout your registration statement to clearly distinguish between your current business operations and the operations you intend to perform in the future. Your revised disclosure should include management’s estimated timetable for generating revenue with respect to both your unmanned aerial vehicle business and your GTC business.

State Road 405, Building M6-306A, Room 1400

Kennedy Space Center, FL 32815

RESPONSE 1: Please see the revised disclosure throughout the Company’s Amendment No. 1 to Form S-1.

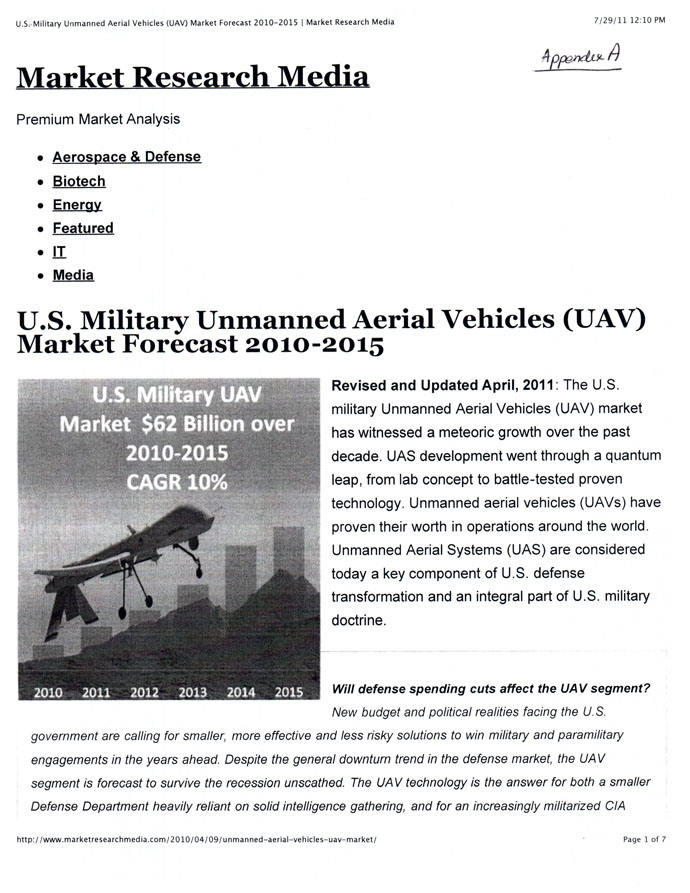

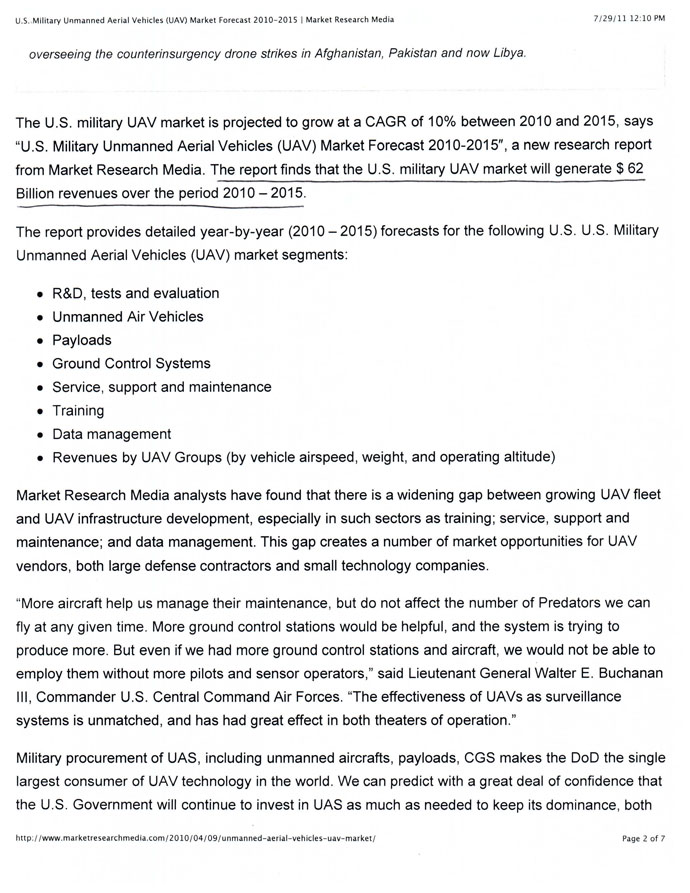

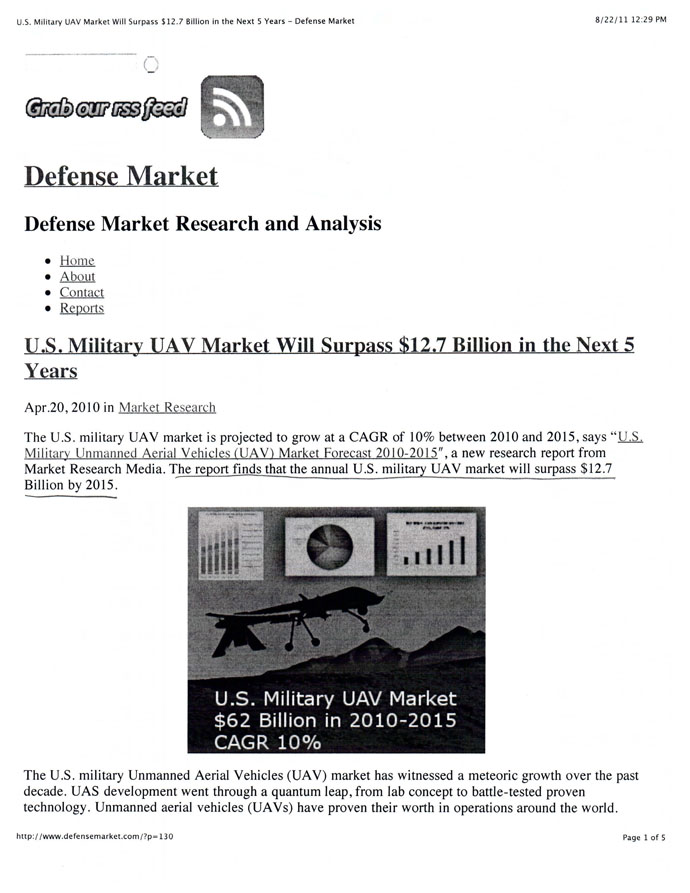

COMMENT 2: Provide us with copies of any industry analysis that you cite or upon which you rely, including, but not limited to, market research data from Market Research Media Ltd. Confirm that this analysis is publicly available. Please highlight the specific portions that you are relying upon so that we can reference them easily. In addition, if any of this analysis has been prepared specifically for this filing, please file a consent from the relevant party. In addition, provide support for your statements that over $2 billion in lighter-than-air UAV contracts have been issued by the Department of Defense and the market for UAVs has grown “significantly” over the last several years (pages 27-28).

RESPONSE 2: Attached as Appendix A is a copy of the market research data from Market Research Media Ltd. and Forecast International, Inc. with the specific portions that we rely on underlined. These analyses are publicly available and were not prepared specifically for this filing. Attached as Appendix B is support for our statements that over $2 billion in lighter than air UAV contracts have been issued by the Department of Defense and for the statement that the market for UAVs has grown significantly over the last several years, in addition to the support provided in Appendix A for such statements. Please see the revised disclosure on page 28 of the Company’s Amendment No. 1 to Form S-1.

COMMENT 3: We note your acquisition of GTC on May 25, 2011. Based on your disclosure, it appears that this was a significant acquisition for the company. Please explain to us your consideration of whether historical financial statements for GTC should be included in your registration statement pursuant to Article 8-04 of Regulation S-X. If significant, it would also be necessary for you to provide pro forma information pursuant to Article 8- 05 of Regulation S-X. Refer to Article 11 of Regulation S-X for guidance in the preparation of pro forma information. Please include as part of your response to this comment, the details of your tests of significance prepared in accordance with Article 8- 04(b) of Regulation S-X.

RESPONSE 3: We note the Staff’s comments and have included in Amendment No. 1 to our Form S-1 audited financial statements for the years ended December 2010 and 2009 for GTC, unaudited financial statements for the three month periods ended March 31, 2011 and 2010 for GTC, and unaudited pro forma financial statements of the Company for the three months ended March 31, 2011 and the year ended December 31, 2010, each of which was filed with the Commission by the Company as an exhibit to our Current Report on Form 8-K/A filed on August 8, 2011.

Market, Industry and Other Data

COMMENT 4: We note your characterization of market data as “generally reliable” and “inherently imprecise.” Please explain.

RESPONSE 4: Please see the revised disclosure under the “Market, Industry and Other Data” section of the Company’s Amendment No. 1 to Form S-1 where we have removed the subject language.

Prospectus summary, page 1

COMMENT 5: In order to provide greater balance to your summary, include disclosure to address the following: (i) the risk that you may need to cease operations if you cannot obtain additional financing (as noted on page three); (ii) the risk that you have not yet sold any of your airships in the commercial marketplace (as noted on page seven); and (iii) the risks associated with your failure to generate revenue in the three month period ended March 31, 2011.

RESPONSE 5: Please see the revised disclosure on page 2 of the Company’s Amendment No. 1 to Form S-1 to reflect (i) the risk that the Company may need to cease operations if we cannot obtain additional financing; (ii) the risk that we have not yet sold any of our airships in the commercial marketplace; and (iii) the risks associated with our generation of limited revenue in the six month period ended June 30, 2011.

“We need to raise a significant amount of additional capital...” page 3

COMMENT 6: Please expand the heading of this risk factor to highlight your assertion that if you do not receive adequate additional financing you would likely have to delay, curtail, scale back or terminate some or all of your operations or possibly merge with or be acquired by another company.

RESPONSE 6: Please see the expanded risk factor heading on page 3 of the Company’s Amendment No. 1 to Form S-1.

COMMENT 7: Revise this risk factor to indicate that you will not receive any proceeds from this offering.

RESPONSE 7: Please see the revised disclosure on page 3 of the Company’s Amendment No. 1 to Form S-1, to reflect that the Company will not receive any proceeds from this offering.

“We rely exclusively on our technical partner, Eastcor Engineering, for the development and commercialization of our products,” page 4

COMMENT 8: Please clarify whether you have entered into any contracts with Eastcor Engineering governing your on-going relationship or any of your products.

RESPONSE 8: The Company and Eastcor Engineering are currently negotiating an agreement to replace an agreement that has expired. The Company intends to file such agreement as an exhibit to its future filings when it is finalized, which we expect to occur in the third quarter of 2011. We have revised the disclosure in the Company’s Amendment No. 1 to Form S-1 to reflect the status of our arrangement with Eastcor.

“Our subsidiary GTC relies heavily on the Globalstar satellite network to provide its services and generate revenue,” page 5

COMMENT 9: We note your statement that the deterioration of the Globalstar satellite constellation has impacted GTC’s ability to provide reliable service on certain government contracts. Please expand your disclosure to provide additional information about these difficulties and indicate whether they may result in the termination of such contracts.

RESPONSE 9: Please see the revised disclosure on pages 4 and 27 of the Company’s Amendment No. 1 to Form S-1.

“We may not qualify as a U.S. government contractor...” page 8

COMMENT 10: Please revise your disclosure to clarify whether you, as the parent company of GTC, need to be qualified as a government contractor in order for GTC to qualify for new government contracts.

RESPONSE 10: Please see the revised disclosure on page 8 of the Company’s Amendment No. 1 to Form S-1 which indicates that the Company, as the parent company of GTC, is not required to be qualified as a government contractor in order for GTC to qualify for new government contracts.

“Our airships are subject to significant governmental regulation...” page 8

COMMENT 11:Please revise your heading to indicate that the FAA currently does not allow any untethered flights by UAVs in commercial airspace in the U.S.

RESPONSE 11: Please see the revised disclosure on page 8 of the Company’s Amendment No. 1 to Form S-1 that indicates that the FAA currently does not allow any untethered flights by UAVs in commercial airspace in the U.S. without clearance certifications from the FAA.

“We are subject to a number of lawsuits that could result in material judgments against us” page 9

COMMENT 12:Expand to discuss the material adverse effect (financially and operationally) settlement of the SEC’s fraud lawsuit has had on the Company.

RESPONSE 12: The Company does not believe that the settlement of the SEC’s fraud lawsuit has had any material adverse effect (financially or operationally) on the Company, and therefore, does not believe any additional disclosure is required. $250,000 of the $300,000 penalty was provided by our Chairman of the Board in return for the issuance of shares of common stock of the Company, and thus did not materially impact the Company’s cash flows. Furthermore, the undertakings that the Company agreed to in the settlement agreement were corporate governance-related rather than financial. The Company is currently in full compliance with its undertakings set forth in the settlement agreement.

“The control deficiencies in our internal control over financial reporting may until remedied cause errors in our financial statements...” page 10

COMMENT 13: Please revise this risk factor to describe the nature of the control deficiencies you reference.

RESPONSE 13: Please see the revised disclosure on page 10 of the Company’s Amendment No. 1 to Form S-1.

Management’s Discussion and Analysis..., page 17

COMMENT 14: We note your disclosure on page 38 that your agreement with Growth Enterprise Fund, S.A. contains certain earn-out payments. Please describe these payments in your management’s discussion and analysis and address their impact on your liquidity and capital resources.

RESPONSE 14: Please see the revised disclosure on page 20 of the Company’s Amendment No. 1 to Form S-1 to reflect the earn-out payments and their impact on our liquidity and capital resources.

Fiscal Year Ended December 31, 2010 Compared to Fiscal Year Ended December 31, 2009, page 19

COMMENT 15: Please identify the party who purchased the 50% interest in your SkySat airship and provide additional disclosure about the conditions upon which such entity or individual may acquire the remaining 50% interest. Confirm that GTC has paid the original purchase price in full. Note 3 to your financial statements seems to imply that full payment of the original purchase price remained at year-end.

RESPONSE 15: Global Telesat Corp. purchased the interest in our SkySat airship. Subsequent to the filing of the Form 10-K, the Company acquired 100% of the outstanding capital stock of GTC such that it is now a wholly-owned subsidiary of the Company. As a subsidiary of the Company, GTC will not acquire the remaining 50% interest in the SkySat UAV, and therefore the Company does not believe additional disclosure would be beneficial to investors or is required. GTC paid the original purchase price of $250,000 in full for the purchase of the initial 50% interest. Please see the expanded disclosure on page F-11 of the Company’s Form Amendment No. 1 to Form S-1 in Note 3.

Liquidity and Capital Resources, page 19

COMMENT 16: We note your disclosure that your funding commitment is subject to “a number” of conditions. Please expand your disclosure to identify these conditions.

RESPONSE 16: Please see the revised disclosure on page 21 of the Company’s Amendment No. 1 to Form S-1.

COMMENT 17: We note that you may not have enough authorized shares available to fund your operations. Expand to discuss any plans to increase your number of authorized shares or conduct a reverse stock split.

RESPONSE 17: Subsequent to the filing of the Form S-1, the Company held its annual shareholders meeting and the Company’s shareholders approved an amended and restated certificate of incorporation of the Company which, among other things, increased the authorized common stock of the Company from 500,000,000 to 750,000,000 shares. As a result, the Company does not believe any additional disclosure is required and, in fact,has removed this risk factor from the Company’s Amendment No. 1 to Form S-1.

COMMENT 18: Please revise your disclosure to provide a more detailed discussion of your plans to meet both your short-term and long-term liquidity needs. Such disclosure should specifically identify the costs associated with your growth strategy and address your accumulated deficit as well as your expectation that you will incur net losses from operations for at least the next several quarters (as noted on page four). Note that we consider "long-term" to be the period in excess of the next twelve months. See Section III.C. of Release no. 33-6835 and footnote 43 of Release no. 33- 8350.

RESPONSE 18: Please see the revised disclosure on pages 21 and 22 of the Company’s Amendment No. 1 to Form S-1.

Contractual Obligations, page 23

COMMENT 19: Please revise your table to include notes payable or advise us why you believe they should not be included.

RESPONSE 19: The Company does not believe that its notes payable should be included in the Contractual Obligations table as the notes aggregating $5,997,030 have no stated repayment terms or interest rates. The Company has historically included them, along with imputed interest of 7%, as though payable on demand in current liabilities.

Products, page 25 WSGI, page 25

COMMENT 20: Please define “ISR”.

RESPONSE 20: Please see the revised disclosure on page 26 of the Company’s Amendment No. 1 to Form S-1 to define ISR as “intelligence, surveillance and reconnaissance.”

GTC, page 26

COMMENT 21: Tell us your basis for your belief that if GTC is awarded the contracts for construction of satellite ground stations in Afghanistan, Africa and other locations,” it will produce a highly profitable revenue stream over the next 18-24 months.”

RESPONSE 21: If GTC is awarded the contracts for construction of satellite ground stations in Afghanistan, Africa and other locations, it will produce a highly profitable revenue stream as the cost of each ground station is approximately $5 million and net profit is expected to be approximately 15%. Additionally, GTC has already negotiated terms with Globalstar that allows Globalstar access to the ground station in Afghanistan in return for GTC having free use of up to 10,000 accounts on the Globalstar network. These accounts can be sold to end users without cost to GTC to further increase revenue and profitability relating to the ground stations. GTC also intends to attempt to negotiate similar agreements with Globalstar for additional free accounts in connection with additional ground stations.

Technology, Research and Development, page 30

COMMENT 22: Clarify the nature of your intellectual property interest, if any, in the technology used to create the Argus One and expand your discussion to address any ownership interest Eastcor Engineering has in the Argus One.

RESPONSE 22: The technology used to create the Argus One was developed for the Company by Eastcor Engineering, LLC. George Vojtech, the Managing Director of Eastcor Engineering, who was named as the inventor on the provisional patent application filed by the Company on the Argus One technology, has assigned all of his rights in the patent to the Company. Please see the revised disclosure on page 31 of the Company’s Amendment No. 1 to Form S-1.

Partners, page 31

COMMENT 23: Expand your disclosure to provide the terms of your relationship with Eastcor Engineering and L-3 Communications. File any relevant agreements with these entities as exhibits to your registration statement or tell us why such agreements are not required to be filed pursuant to Item 601 of Regulation S-K.

RESPONSE 23: Please see the expanded disclosure regarding the terms of the Company’s relationships with Eastcor Engineering and L-3 Communications on page 32 of the Company’s Amendment No. 1 to Form S-1. The Company and Eastcor are currently negotiating an agreement to replace an agreement that has expired and the Company intends to file such agreement as an exhibit to its future filings when it is finalized, which is expected to be in the third quarter of 2011. The Company does not believe that its memorandum of understanding with L-3 Communications is required to be filed pursuant to Item 601 of Regulation S-K as the Company does not believe it is material to the Company.

COMMENT 24: Expand your disclosure to provide the terms of the existing contracts between Globalstar and GTC. File any relevant agreements with these entities as exhibits to your registration statement or tell us why such agreements are not required to be filed pursuant to Item 601 of Regulation S-K.

RESPONSE 24: Please see the revised disclosure on page 33 of the Company’s Amendment No. 1 to Form S-1 to reflect the contracts between GTC and Globalstar. The Company has filed the material Globalstar contracts as exhibits to the Amendment No. 1 to Form S-1, although several have been redacted and are subject to a confidential treatment request that the Company intends to file shortly.

Intellectual Property, page 32

COMMENT 25: We note your disclosure on page 32 that you have filed one provisional patent. Please indicate when you filed the patent application and clarify whether that technology was used for either your Argus One or SkySat airships.

RESPONSE 25: Please see the revised disclosure on page 33 of the Company’s Amendment No. 1 to Form S-1 to reflect the fact that the Company filed the U.S. provisional patent application on February 17, 2011 in connection with its Argus One UAV.

Legal Proceedings, page 33

COMMENT 26: With regard to Hudson Bay Fund LP et al, you discuss an action filed June 16, 2009, a non-final Summary Judgment Order granted in March 2011, and a May 17, 2010 Settlement Agreement. The May 17, 2010 settlement date in the Hudson Bay Fund L.P. lawsuit appears incorrect. Please revise and also clarify what actions have been settled, and what actions are continuing. Further, please reconcile your revised disclosure here with your disclosure of litigation and contingencies on page F-18, as appropriate. In addition, clarify whether the shares have been issued to Hudson Bay as part of the settlement agreement.

RESPONSE 26: Please see the revised disclosure on pages 35 and F-33 of the Company’s Amendment No. 1 to Form S-1 that reflects the fact the Settlement Agreement was dated May 17, 2011, the settlement resolved all outstanding matters between the Company and the Hudson Bay parties and all of the settlement shares have been issued by the Company.

COMMENT 27: If the warrant issued to Brio Capital was similar to the warrant issued to Hudson Bay and the matter is being adjudicated in the same court, tell us why a loss in the matter is not reasonably possible.

RESPONSE 27: We believe that the Company has significant defenses to the Brio action that the court did not allow the Company to raise in the Hudson Bay matter that could likely result in a different outcome. Upon its evaluation of the Hudson Bay matter once the new management joined the Company, the Company’s new management team replaced the legal counsel and tried to motion the court for reargument on issues the new management and counsel believed had been missed during the litigation process. However, the timing of this motion was subsequent to a summary judgment motion being heard and a judgment being issued and the court did not allow the Company to reopen arguments. The Company and its new counsel have raised these additional arguments from its initial response to Brio’s complaint and therefore believe they could result in a different outcome in the Brio case.

COMMENT 28: Please refer to your disclosure of matters involving Peter Khoury and Brio Capital and review your disclosure, both here and in Note 14 on page F-17, with respect to all legal proceedings that you are currently involved in to ensure that you identify (i) any and all damages sought, and (ii) the possible loss or range of loss when there is at least a reasonable possibility that a loss or an additional loss in excess of amounts accrued mayhave been incurred. If you have determined that it is not possible to estimate the range of loss, please provide an explanation as to why this is not possible. Refer to ASC 450-20- 50-3 and 450-20-50-4.

RESPONSE 28: Please see the revised disclosure on pages 36 and F-19 of the Company’s Amendment No. 1 to Form S-1. In response to the Staff’s comments, the Company has reviewed its disclosure with respect to its other legal proceedings and believes that such disclosure accurately reflects the current state of the proceedings and adequately reflects the damages sought and the possible losses from such proceedings.

Information with Respect to Directors, page 36

COMMENT 29: In accordance with Item 401(e) of Regulation S-K, please describe in more detail Ms. Hulo and Major General Jackson’s business experience in the last five years.

RESPONSE 29: Please see the revised disclosure on pages 38-39 of the Company’s Amendment No. 1 to Form S-1.

Arrangements or Understandings Regarding the Selection of Certain Directors, page 38

COMMENT 30: The first two sentences under this heading are contradictory. Please revise.

RESPONSE 30: Please see the revised disclosure on page 39 of the Company’s Amendment No. 1 to Form S-1 that reflects the fact that none of our current directors were appointed pursuant to any arrangements but that we have an agreement to appoint two yet-to be named and appointed directors.

Compensation of Directors, page 41

COMMENT 31: We note that you are currently re-negotiating settlement and release agreements with Messrs. Christian and Hotz. Please expand your disclosure to indicate when you anticipate finalizing such agreements.

RESPONSE 31: Please see the revised disclosure on pages 43, 45 and 46 of the Company’s Amendment No. 1 to Form S-1.

Potential Payments Upon Termination or Change of Control, page 46

COMMENT 32: We note that the amended employment agreement Mr. Estrella entered into on December 27, 2010 provides for a salary of $250,000 per year and has a minimum term of three years. We also note that under the employment agreement Mr. Estrella is entitled to all unpaid salary that would have been paid to him during the initial term. Therefore, explain why only $375,000 (instead of $750,000) is disclosed in the table.

RESPONSE 32: Please see the revised disclosure on page 48 of the Company’s Amendment No. 1 to Form S-1 to reflect the fact that the amount that should have been disclosed in the table is $625,000 as it would include the remaining amount payable to Mr. Estrella through the end of the Initial Term that ends June 22, 2013. The terms of Mr. Estrella’s employment agreement have been completely disclosed and the employment agreement has been filed as an exhibit to the Company’s filings.

Consolidated Financial Statements, page F-1 Note 3 SkySat Sale, page F-11

COMMENT 33: It is unclear why the company accounted for the $250,000 investment in the SkySat aerial vehicle as revenue. Please provide us with your analysis and reference to authoritative literature used as guidance to support your treatment. In your response, please clarify whether, at the time of the transaction, it was GTC’s intention to purchase the aerial vehicle, to help finance and potentially profit from its development, or if there was some other motivation for the investment.

RESPONSE 33: The Company’s revenue recognition policy is such that the Company recognizes revenue for sales when the following criteria have been met: delivery has occurred, the price is fixed and determinable, collection is probable, and persuasive evidence of an arrangement exists. On April 15, 2010, the Company entered into an agreement to sell a 50% interest in a SkySat airship to Global Telesat Corp. The relevant sections of the sales contract are as follows: Section 1.4 which states “…GTC’s obligations under this Agreement are conditioned upon and subject to GTC’s inspection of the Airship after it arrives at the Facility and GTC’s determination, in its sole discretion, that all of the components thereof have been delivered and are in satisfactory condition…”; Section 2.1 which states “Subject to satisfaction of the conditions set forth in Section 1.4 hereof, GTC will purchase a 50% ownership interest…”; and Section 2.2 which states that upon satisfaction of the Section 1.4 conditions, GTC will commence making payments on the $250,000 purchase price. Based on the provisions of the sales contract and the fact that GTC began to make the required purchase price payments, the Company concluded that the revenue recognition criteria were satisfied and that a sale had taken place, and thus recognized the $250,000 as revenue. Due to the fact that the SkySat had no carrying value on the books and records of the Company since it had previously been expensed, the Company determined that there was no cost of sales related to this revenue. At the time of the transaction, it was GTC’s intention to purchase the remaining interest in the aerial vehicle after working with Eastcor Engineering to further develop the SkySat and demonstrate its capabilities. Following such advancement of the airship, it was GTC’s intention at the time to sell the SkySat.

Note 7 Notes Payable, page F-12

COMMENT 34: Please expand your disclosure to discuss the terms of any convertible debt outstanding at your balance sheet date.

RESPONSE 34: The Company did not have any convertible debt outstanding at the balance sheet date and therefore does not believe any expanded disclosure in Note 7 is required.

Note 8 Warrants, page F-13

COMMENT 35: Both here and in future filings, please disclose the assumptions used to calculate the fair value of your warrant liabilities.

RESPONSE 35: Please see the revised disclosure on pages F-14 and F-32 of the Company’s Amendment No. 1 to Form S-1. In accordance with the Staff’s comments in this regard, the Company will include disclosure of the assumptions used to calculate the fair value of its warrant liabilities in its future filings.

Note 9. Share-based Compensation, page F-34

COMMENT 36: Please disclose the assumptions used to calculate the fair value of stock options granted for each of the periods presented in your filing.

RESPONSE 36: Please see the revised disclosure on page F-37 of the Company’s Amendment No. 1 to Form S-1.

The Company hereby acknowledges that:

| · | The Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| · | Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| · | The Company may not assert staff comments as a defense in any proceeding initiated by the commission or any person under the federal securities laws of the United States. |

**********************

Please do not hesitate to contact the undersigned at 321-452-3545 if you have any questions or comments with regard to these responses, need further supplemental information or would like to discuss any of the information covered in this letter. Thank you.

| Very truly yours, |

| /s/Barbara M. Johnson |

| Barbara M. Johnson |

| Vice President, General Counsel and |

| Secretary |