UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________

FORM 10-Q

________________________________

CHECK ONE:

|

| |

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended: March 31, 2017

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file No.: 1-12996

________________________________

Diversicare Healthcare Services, Inc.

(exact name of registrant as specified in its charter)

________________________________

|

| | |

| Delaware | | 62-1559667 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification No.) |

1621 Galleria Boulevard, Brentwood, TN 37027

(Address of principal executive offices) (Zip Code)

(615) 771-7575

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and a “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | |

| Large accelerated filer | | ¨ | Accelerated filer | | ¨ |

| | | | |

| Non-accelerated filer | | ¨(do not check if a smaller reporting company) | Smaller reporting company | | ý |

| | | | Emerging growth company | | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| | ¨

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

6,458,836

(Outstanding shares of the issuer’s common stock as of May 1, 2017)

Part I. FINANCIAL INFORMATION

ITEM 1 – FINANCIAL STATEMENTS

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED BALANCE SHEETS

(in thousands)

|

| | | | | | | |

| | March 31,

2017 | | December 31,

2016 |

| | (Unaudited) | | |

| CURRENT ASSETS: | | | |

| Cash and cash equivalents | $ | 3,931 |

| | $ | 4,263 |

|

| Receivables, less allowance for doubtful accounts of $10,824 and $10,326, respectively | 66,916 |

| | 62,152 |

|

| Other receivables | 1,149 |

| | 1,193 |

|

| Prepaid expenses and other current assets | 3,115 |

| | 3,623 |

|

| Income tax refundable | — |

| | 431 |

|

| Current assets of discontinued operations | 28 |

| | 28 |

|

| Total current assets | 75,139 |

| | 71,690 |

|

| PROPERTY AND EQUIPMENT, at cost | 131,038 |

| | 128,822 |

|

| Less accumulated depreciation and amortization | (71,389 | ) | | (69,022 | ) |

| Property and equipment, net | 59,649 |

| | 59,800 |

|

| OTHER ASSETS: | | | |

| Deferred income taxes | 20,785 |

| | 21,185 |

|

| Deferred lease and other costs, net | 180 |

| | 193 |

|

| Other noncurrent assets | 3,588 |

| | 3,108 |

|

| Acquired leasehold interest, net | 6,979 |

| | 7,075 |

|

| Total other assets | 31,532 |

| | 31,561 |

|

| | $ | 166,320 |

| | $ | 163,051 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED BALANCE SHEETS

(in thousands, except share and per share amounts)

(continued)

|

| | | | | | | |

| | March 31,

2017 | | December 31,

2016 |

| | (Unaudited) | | |

| CURRENT LIABILITIES: | | | |

| Current portion of long-term debt and capitalized lease obligations | $ | 7,715 |

| | $ | 7,715 |

|

| Trade accounts payable | 13,913 |

| | 12,972 |

|

| Current liabilities of discontinued operations | 430 |

| | 427 |

|

| Income tax payable | 61 |

| | — |

|

| Accrued expenses: | | | |

| Payroll and employee benefits | 18,538 |

| | 20,108 |

|

| Self-insurance reserves, current portion | 10,157 |

| | 9,401 |

|

| Provider taxes | 2,535 |

| | 3,114 |

|

| Other current liabilities | 3,863 |

| | 4,432 |

|

| Total current liabilities | 57,212 |

| | 58,169 |

|

| NONCURRENT LIABILITIES: | | | |

| Long-term debt and capitalized lease obligations, less current portion and deferred financing costs, net | 75,648 |

| | 72,145 |

|

| Self-insurance reserves, noncurrent portion | 11,685 |

| | 11,766 |

|

| Other noncurrent liabilities | 9,133 |

| | 9,551 |

|

| Total noncurrent liabilities | 96,466 |

| | 93,462 |

|

| COMMITMENTS AND CONTINGENCIES |

| |

|

| SHAREHOLDERS’ EQUITY: | | | |

| Common stock, authorized 20,000,000 shares, $.01 par value, 6,691,000 and 6,592,000 shares issued, and 6,459,000 and 6,361,000 shares outstanding, respectively | 67 |

| | 66 |

|

| Treasury stock at cost, 232,000 shares of common stock | (2,500 | ) | | (2,500 | ) |

| Paid-in capital | 22,044 |

| | 21,935 |

|

| Accumulated deficit | (7,301 | ) | | (8,276 | ) |

| Accumulated other comprehensive loss | 332 |

| | 195 |

|

| Total shareholders’ equity | 12,642 |

|

| 11,420 |

|

| | $ | 166,320 |

| | $ | 163,051 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share amounts, unaudited)

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| PATIENT REVENUES, net | $ | 141,500 |

| | $ | 97,945 |

|

| EXPENSES: | | | |

| Operating | 110,667 |

| | 78,618 |

|

| Lease and rent expense | 13,743 |

| | 7,252 |

|

| Professional liability | 2,670 |

| | 2,066 |

|

| General and administrative | 8,973 |

| | 6,734 |

|

| Depreciation and amortization | 2,487 |

| | 2,003 |

|

| Total expenses | 138,540 |

| | 96,673 |

|

| OPERATING INCOME | 2,960 |

| | 1,272 |

|

| OTHER INCOME (EXPENSE): | | | |

| Equity in net income of unconsolidated affiliate | — |

| | 33 |

|

| Gain on sale of investment in unconsolidated affiliate | 733 |

| | — |

|

| Interest expense, net | (1,483 | ) | | (1,070 | ) |

| Debt retirement costs | — |

| | (351 | ) |

| Total other expense | (750 | ) | | (1,388 | ) |

| INCOME (LOSS) FROM CONTINUING OPERATIONS BEFORE INCOME TAXES | 2,210 |

| | (116 | ) |

| BENEFIT (PROVISION) FOR INCOME TAXES | (862 | ) | | 42 |

|

| INCOME (LOSS) FROM CONTINUING OPERATIONS | 1,348 |

| | (74 | ) |

| LOSS FROM DISCONTINUED OPERATIONS: | | | |

| Operating loss, net of tax benefit (expense) of ($9) and $21, respectively | (15 | ) | | (37 | ) |

| NET INCOME (LOSS) | $ | 1,333 |

| | $ | (111 | ) |

| NET INCOME (LOSS) PER COMMON SHARE: | | | |

| Per common share – basic | | | |

| Continuing operations | $ | 0.22 |

| | $ | (0.01 | ) |

| Discontinued operations | — |

| | (0.01 | ) |

| | $ | 0.22 |

| | $ | (0.02 | ) |

| Per common share – diluted | | | |

| Continuing operations | $ | 0.21 |

| | $ | (0.01 | ) |

| Discontinued operations | — |

| | (0.01 | ) |

| | $ | 0.21 |

| | $ | (0.02 | ) |

| COMMON STOCK DIVIDENDS DECLARED PER SHARE OF COMMON STOCK | $ | 0.055 |

| | $ | 0.055 |

|

| WEIGHTED AVERAGE COMMON SHARES OUTSTANDING: | | | |

| Basic | 6,233 |

| | 6,160 |

|

| Diluted | 6,440 |

| | 6,160 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(in thousands and unaudited)

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| NET INCOME (LOSS) | $ | 1,333 |

| | $ | (111 | ) |

| OTHER COMPREHENSIVE INCOME: | | | |

| Change in fair value of cash flow hedge, net of tax | 254 |

| | 311 |

|

| Less: reclassification adjustment for amounts recognized in net income | (117 | ) | | (144 | ) |

| Total other comprehensive income | 137 |

| | 167 |

|

| COMPREHENSIVE INCOME | $ | 1,470 |

| | $ | 56 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands and unaudited)

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| CASH FLOWS FROM OPERATING ACTIVITIES: | | | |

| Net income (loss) | $ | 1,333 |

| | $ | (111 | ) |

| Discontinued operations | (15 | ) | | (37 | ) |

| Income (loss) from continuing operations | 1,348 |

| | (74 | ) |

| Adjustments to reconcile income (loss) from continuing operations to net cash provided by (used in) operating activities: | | | |

| Depreciation and amortization | 2,487 |

| | 2,003 |

|

| Provision for doubtful accounts | 1,970 |

| | 1,640 |

|

| Deferred income tax provision (benefit) | 354 |

| | (35 | ) |

| Provision for self-insured professional liability, net of cash payments | (83 | ) | | 1,013 |

|

| Stock-based compensation | 241 |

| | 252 |

|

| Equity in net income of unconsolidated affiliate, net of investment | — |

| | (33 | ) |

| Gain on sale of unconsolidated affiliate | (733 | ) | | — |

|

| Debt retirement costs | — |

| | 351 |

|

| Deferred bonus | 500 |

| | — |

|

| Other | 32 |

| | (254 | ) |

| Changes in assets and liabilities affecting operating activities: | | | |

| Receivables, net | (6,518 | ) | | 2,085 |

|

| Prepaid expenses and other assets | 1,081 |

| | (275 | ) |

| Trade accounts payable and accrued expenses | (1,468 | ) | | (1,438 | ) |

| Net cash provided by (used in) continuing operations | (789 | ) | | 5,235 |

|

| Discontinued operations | (67 | ) | | (1,862 | ) |

| Net cash provided by (used in) operating activities | (856 | ) | | 3,373 |

|

| CASH FLOWS FROM INVESTING ACTIVITIES: | | | |

| Purchases of property and equipment | (2,237 | ) | | (8,492 | ) |

| Change in restricted cash | — |

| | 1,658 |

|

| Net cash used in continuing operations | (2,237 | ) | | (6,834 | ) |

| Discontinued operations | — |

| | — |

|

| Net cash used in investing activities | (2,237 | ) | | (6,834 | ) |

| CASH FLOWS FROM FINANCING ACTIVITIES: | | | |

| Repayment of debt obligations | (9,193 | ) | | (57,885 | ) |

| Proceeds from issuance of debt | 12,567 |

| | 62,566 |

|

| Financing costs | (10 | ) | | (1,833 | ) |

| Issuance and redemption of employee equity awards | (94 | ) | | (95 | ) |

| Payment of common stock dividends | (346 | ) | | (342 | ) |

| Payment for preferred stock restructuring | (163 | ) | | (158 | ) |

| Net cash provided by financing activities | 2,761 |

| | 2,253 |

|

| Discontinued operations | — |

| | — |

|

| Net cash provided by financing activities | $ | 2,761 |

| | $ | 2,253 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

INTERIM CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands and unaudited)

(continued)

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| NET DECREASE IN CASH AND CASH EQUIVALENTS | $ | (332 | ) | | $ | (1,208 | ) |

| CASH AND CASH EQUIVALENTS, beginning of period | 4,263 |

| | 4,585 |

|

| CASH AND CASH EQUIVALENTS, end of period | $ | 3,931 |

| | $ | 3,377 |

|

| SUPPLEMENTAL INFORMATION: | | | |

| Cash payments of interest | $ | 1,231 |

| | $ | 919 |

|

| Cash payments of income taxes | $ | 6 |

| | $ | 229 |

|

The accompanying notes are an integral part of these interim consolidated financial statements.

DIVERSICARE HEALTHCARE SERVICES, INC. AND SUBSIDIARIES

NOTES TO INTERIM CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2017 AND 2016

Diversicare Healthcare Services, Inc. (together with its subsidiaries, “Diversicare” or the “Company”) provides long-term care services to nursing center patients in ten states, primarily in the Southeast, Midwest, and Southwest. The Company’s centers provide a range of health care services to their patients and residents that include nursing, personal care, and social services. Additionally, the Company’s nursing centers also offer a variety of comprehensive rehabilitation services, as well as nutritional support services. The Company's continuing operations include centers in Alabama, Florida, Indiana, Kansas, Kentucky, Mississippi, Missouri, Ohio, Tennessee, and Texas.

As of March 31, 2017, the Company’s continuing operations consist of 76 nursing centers with 8,453 licensed nursing beds. The Company owns 17 and leases 59 of its nursing centers. Our nursing centers range in size from 48 to 320 licensed nursing beds. The licensed nursing bed count does not include 496 licensed assisted and residential living beds.

| |

| 2. | CONSOLIDATION AND BASIS OF PRESENTATION OF FINANCIAL STATEMENTS |

The interim consolidated financial statements include the operations and accounts of Diversicare Healthcare Services and its subsidiaries, all wholly-owned. All significant intercompany accounts and transactions have been eliminated in consolidation. The Company had one equity method investee, which was sold during the fourth quarter of 2016. The Company's share of the profits and losses from this investment are reported as equity in earnings of investment in an unconsolidated affiliate and the proceeds received from the sale are reported under the heading "Gain on sale of investment in unconsolidated affiliate" in the accompanying interim consolidated statement of operations. The sale resulted in a $1,366,000 gain in the fourth quarter of 2016. Subsequently, we recognized an additional gain of $733,000 for the three-month period ended March 31, 2017, related to the liquidation of remaining assets affiliated with the partnership.

The interim consolidated financial statements for the three month periods ended March 31, 2017 and 2016, included herein have been prepared by the Company, without audit, pursuant to the rules and regulations of the Securities and Exchange Commission. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been condensed or omitted pursuant to such rules and regulations. In the opinion of management of the Company, the accompanying interim consolidated financial statements reflect all normal, recurring adjustments necessary to present fairly the Company’s financial position at March 31, 2017, and the results of operations for the three month periods ended March 31, 2017 and 2016, and cash flows for the three month periods ended March 31, 2017 and 2016. The Company’s balance sheet information at December 31, 2016, was derived from its audited consolidated financial statements as of December 31, 2016.

The results of operations for the periods ended March 31, 2017 and 2016 are not necessarily indicative of the operating results that may be expected for a full year. These interim consolidated financial statements should be read in connection with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2016.

| |

| 3. | RECENT ACCOUNTING GUIDANCE |

In May 2014, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2014-09, Revenue from Contracts with Customers (Topic 606), which requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. In March 2016, the FASB issued an update to ASU No. 2014-09 in the form of ASU No. 2016-08, which amended the principal-versus-agent implementation guidance and illustrations in the new revenue guidance. The update clarifies that an entity should evaluate whether it is the principal or the agent for each specified good or service promised in a contract with a customer. In April 2016, the FASB issued another update to the new revenue standard in the form of ASU No. 2016-10, which amends the guidance on identifying performance obligations and the implementation guidance on licensing. In May 2016, ASU No. 2016-12 was issued, which amends the new revenue recognition guidance on transition, collectability, noncash consideration and the presentation of taxes. The new revenue standard (including updates) will be effective for annual and interim reporting periods beginning after December 15, 2017, with early adoption permitted only as of annual reporting periods beginning after December 15, 2016. The Company will adopt the requirements of this standard effective January 1, 2018. We are in the early stages of evaluating the expected adoption method of ASU No. 2014-09, and we are analyzing whether enhancements are needed to our business and accounting systems.

In November 2015, the FASB issued ASU No. 2015-17, Balance Sheet Classification of Deferred Taxes, which changes how deferred taxes are classified on the Company's balance sheets. The Company adopted ASU No. 2015-17 as of January 1, 2017,

and the new standard was applied on a retrospective basis. The adoption of this guidance resulted in a $7,644,000 reclassification between current deferred income taxes and non-current deferred income taxes.

In February 2016, the FASB issued ASU No. 2016-02, Leases. The new standard establishes a right-of-use (ROU) model that requires a lessee to record a ROU asset and a lease liability on the balance sheet for all leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. The new standard is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. A modified retrospective transition approach is required for lessees for capital and operating leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements, with certain practical expedients available. Disclosures will be required to meet the objective of enabling users of financial statements to assess the amount, timing, and uncertainty of cash flows arising from leases. We anticipate this standard will have a material impact on our consolidated financial statements. While we are continuing to assess all potential impacts of the standard, we currently believe the most significant impact relates to our accounting for building and equipment operating leases and will result in a significant increase in the assets and liabilities on the consolidated balance sheet.

In March 2016, the FASB issued ASU No. 2016-09, Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. The ASU was issued as part of the FASB Simplification Initiative and involves several aspects of accounting for shared-based payment transactions, including the income tax consequences and classification on the statement of cash flows. We adopted this standard as of January 1, 2017. The adoption did not have a material impact on our financial position, results of operations or cash flows.

In June 2016, the FASB issued ASU No. 2016-13, Measurement of Credit Losses on Financial Instruments. This update is intended to improve financial reporting by requiring timelier recognition of credit losses on loans and other financial instruments that are not accounted for at fair value through net income, including loans held for investment, held-to-maturity debt securities, trade and other receivables, net investment in leases and other such commitments. This update requires that financial statement assets measured at an amortized cost be presented at the net amount expected to be collected, through an allowance for credit losses that is deducted from the amortized cost basis. This standard is effective for the fiscal year beginning after December 15, 2019 with early adoption permitted. The Company is in the initial stages of evaluating the impact from the adoption of this new standard on the consolidated financial statements and related notes.

In August 2016, the FASB issued ASU No. 2016-15, Statement of Cash Flows (Topic 230). The ASU provides clarification regarding how certain cash receipts and cash payments are presented and classified in the statement of cash flows. The guidance addresses eight specific cash flow issues with the objective of reducing the existing diversity in practice. The ASU is effective for annual and interim periods beginning after December 15, 2017, which will require the Company to adopt these provisions in the first quarter of fiscal 2018 using a retrospective approach. Early adoption is permitted. The Company is currently evaluating the impact this standard will have on our consolidated financial statements.

In November 2016, the FASB issued ASU No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash, which requires that the Statement of Cash Flows explain the changes during the period of cash and cash equivalents inclusive of amounts categorized as Restricted Cash. As a result, amounts generally described as restricted cash and restricted cash equivalents should be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. The standard is effective for periods beginning after December 15, 2017. The Company plans to adopt this standard on January 1, 2018, and is currently evaluating the impact this standard will have on our consolidated financial statements.

| |

| 4. | LONG-TERM DEBT AND INTEREST RATE SWAP |

The Company has agreements with a syndicate of banks for a mortgage term loan ("Original Mortgage Loan") and the Company’s revolving credit agreement ("Original Revolver"). On February 26, 2016, the Company executed an Amended and Restated Credit Agreement (the "Credit Agreement") which modified the terms of the Original Mortgage Loan and the Original Revolver Agreements dated April 30, 2013. The Credit Agreement increases the Company's borrowing capacity to $100,000,000 allocated between a $72,500,000 Mortgage Loan ("Amended Mortgage Loan") and a $27,500,000 Revolver ("Amended Revolver"). The Amended Mortgage Loan consists of a $60,000,000 term loan facility and a $12,500,000 acquisition loan facility. Loan acquisition costs associated with the Amended Mortgage Loan and the Amended Revolver were capitalized in the amount of $2,162,000 and are being amortized over the five-year term of the agreements.

Under the terms of the amended agreements, the syndicate of banks provided the Amended Mortgage Loan with an original principal balance of $72,500,000 with a five-year maturity through February 26, 2021, and a $27,500,000 Amended Revolver through February 26, 2021. The Amended Mortgage Loan has a term of five years, with principal and interest payable monthly based on a 25-year amortization. Interest on the term and acquisition loan facilities is based on LIBOR plus 4.0% and 4.75%, respectively. A portion of the Amended Mortgage Loan is effectively fixed at 5.79% pursuant to an interest rate swap with an initial notional amount of $30,000,000. As of March 31, 2017, the interest rate related to the Amended Mortgage Loan was 5.0%. The Amended Mortgage Loan balance was $63,679,000 as of March 31, 2017, consisting of $58,390,000 on the term loan facility

and $5,289,000 on the acquisition loan facility. The Amended Mortgage Loan is secured by seventeen owned nursing centers, related equipment and a lien on the accounts receivable of these centers. The Amended Mortgage Loan and the Amended Revolver are cross-collateralized and cross-defaulted. The Company’s Amended Revolver has an interest rate of LIBOR plus 4.0% and is secured by accounts receivable and is subject to limits on the maximum amount of loans that can be outstanding under the revolver based on borrowing base restrictions.

Effective October 3, 2016, the Company entered into the Second Amendment to the Third Amended and Restated Revolver ("Second Amendment"). The Second Amendment increased the Amended Revolver capacity from the $27,500,000 in the Amended Revolver to $52,250,000; provided that the maximum revolving facility be reduced to $42,250,000 on August 1, 2017.

On December 29, 2016, the Company executed a Third Amendment to the Third Amended and Restated Revolver ("Third Amendment"). The Third Amendment modifies the terms of the Amended Mortgage Loan Agreement by increasing the Company’s letter of credit sublimit from $10,000,000 to $15,000,000.

As of March 31, 2017, the Company had $20,000,000 borrowings outstanding under the Amended Revolver compared to $15,000,000 outstanding as of December 31, 2016. The outstanding borrowings on the revolver were used primarily to compensate for accumulated Medicaid and Medicare receivables at recently acquired facilities as these facilities proceed through the change in ownership process with Centers for Medicare & Medicaid Services (“CMS”). Annual fees for letters of credit issued under the Amended Revolver are 3.00% of the amount outstanding. The Company has twelve letters of credit with a total value of $12,352,000 outstanding as of March 31, 2017. Considering the balance of eligible accounts receivable, the letters of credit, the amounts outstanding under the revolving credit facility and the maximum loan amount of $46,308,000, the balance available for borrowing under the Amended Revolver was $9,456,000 at March 31, 2017.

The Company’s debt agreements contain various financial covenants, the most restrictive of which relates to debt service coverage ratios. The Company is in compliance with all such covenants at March 31, 2017.

Interest Rate Swap Transaction

As part of the debt agreements entered into in April 2013, the Company entered into an interest rate swap agreement with a member of the bank syndicate as the counterparty. The Company designated its interest rate swap as a cash flow hedge and the earnings component of the hedge, net of taxes, is reflected as a component of other comprehensive income (loss). In conjunction with the February 26, 2016 amendment to the Credit Agreement, the Company amended the terms of its interest rate swap. The interest rate swap agreement has the same effective date and maturity date as the Amended Mortgage Loan, and has an amortizing notional amount that was $29,125,000 as of March 31, 2017. The interest rate swap agreement requires the Company to make fixed rate payments to the bank calculated on the applicable notional amount at an annual fixed rate of 5.79% while the bank is obligated to make payments to the Company based on LIBOR on the same notional amount.

The Company assesses the effectiveness of its interest rate swap on a quarterly basis, and at March 31, 2017, the Company determined that the interest rate swap was highly effective. The interest rate swap valuation model indicated a net liability of $8,000 at March 31, 2017. The fair value of the interest rate swap is included in “other noncurrent liabilities” on the Company’s interim consolidated balance sheet. The liability related to the change in the interest rate swap included in accumulated other comprehensive loss at March 31, 2017 is $5,000, net of the income tax benefit of $3,000. As the Company’s interest rate swap is not traded on a market exchange, the fair value is determined using a valuation based on a discounted cash flow analysis. This analysis reflects the contractual terms of the interest rate swap agreement and uses observable market-based inputs, including estimated future LIBOR interest rates. The interest rate swap valuation is classified in Level 2 of the fair value hierarchy, in accordance with the FASB guidance set forth in ASC 820, Fair Value Measurement.

| |

| 5. | COMMITMENTS AND CONTINGENCIES |

Professional Liability and Other Liability Insurance

The Company has professional liability insurance coverage for its nursing centers that, based on historical claims experience, is likely to be substantially less than the claims that are expected to be incurred. Effective July 1, 2013, the Company established a wholly-owned, offshore limited purpose insurance subsidiary, SHC Risk Carriers, Inc. (“SHC”), to replace some of the expiring commercial policies. SHC covers losses up to specified limits per occurrence. All of the Company's nursing centers in Florida, and Tennessee are now covered under the captive insurance policies along with most of the nursing centers in Alabama, Kentucky, and Texas. The SHC policy provides coverage limits of either $500,000 or $1,000,000 per medical incident with a sublimit per center of $1,000,000 and total annual aggregate policy limits of $5,000,000. The remaining nursing centers are covered by one of seven claims made professional liability insurance policies purchased from entities unaffiliated with the Company. These policies provide coverage limits of $1,000,000 per claim and have sublimits of $3,000,000 per center, with varying self-insured retention levels per claim and varying aggregate policy limits.

Reserve for Estimated Self-Insured Professional Liability Claims

Because the Company’s actual liability for existing and anticipated professional liability and general liability claims will likely exceed the Company’s limited insurance coverage, the Company has recorded total liabilities for reported and estimated future claims of $19,839,000 as of March 31, 2017. This accrual includes estimates of liability for incurred but not reported claims, estimates of liability for reported but unresolved claims, actual liabilities related to settlements, including settlements to be paid over time, and estimates of legal costs related to these claims. All losses are projected on an undiscounted basis and are presented without regard to any potential insurance recoveries. Amounts are added to the accrual for estimates of anticipated liability for claims incurred during each period, and amounts are deducted from the accrual for settlements paid on existing claims during each period.

The Company evaluates the adequacy of this liability on a quarterly basis. Semi-annually, the Company retains a third-party actuarial firm to assist in the evaluation of this reserve. Since May 2012, Merlinos & Associates, Inc. (“Merlinos”) has assisted management in the preparation of the appropriate accrual for incurred but not reported general and professional liability claims based on data furnished as of May 31 and November 30 of each year. Merlinos primarily utilizes historical data regarding the frequency and cost of the Company's past claims over a multi-year period, industry data and information regarding the number of occupied beds to develop its estimates of the Company's ultimate professional liability cost for current periods.

On a quarterly basis, the Company obtains reports of asserted claims and lawsuits incurred. These reports, which are provided by the Company’s insurers and a third-party claims administrator, contain information relevant to the actual expense already incurred with each claim as well as the third-party administrator’s estimate of the anticipated total cost of the claim. This information is reviewed by the Company quarterly and provided to the actuary semi-annually. Based on the Company’s evaluation of the actual claim information obtained, the semi-annual estimates received from the third-party actuary, the amounts paid and committed for settlements of claims and on estimates regarding the number and cost of additional claims anticipated in the future, the reserve estimate for a particular period may be revised upward or downward on a quarterly basis. Any increase in the accrual decreases results of operations in the period and any reduction in the accrual increases results of operations during the period.

As of March 31, 2017, the Company is engaged in 68 professional liability lawsuits. Ten lawsuits are currently scheduled for trial or arbitration during the next twelve months, and it is expected that additional cases will be set for trial or hearing. The Company’s cash expenditures for self-insured professional liability costs from continuing operations were $2,071,000 and $613,000 for the three months ended March 31, 2017 and 2016, respectively.

Although the Company adjusts its accrual for professional and general liability claims on a quarterly basis and retains a third-party actuarial firm semi-annually to assist management in estimating the appropriate accrual, professional and general liability claims are inherently uncertain, and the liability associated with anticipated claims is very difficult to estimate. Professional liability cases have a long cycle from the date of an incident to the date a case is resolved, and final determination of the Company’s actual liability for claims incurred in any given period is a process that takes years. As a result, the Company’s actual liabilities may vary significantly from the accrual, and the amount of the accrual has and may continue to fluctuate by a material amount in any given period. Each change in the amount of this accrual will directly affect the Company’s reported earnings and financial position for the period in which the change in accrual is made.

Civil Investigative Demand ("CID")

In July 2013, the Company learned that the United States Attorney for the Middle District of Tennessee (DOJ) had commenced a civil investigation of potential violations of the False Claims Act (FCA).

In October 2014, the Company learned that the investigation was started by the filing under seal of a false claims action against the two facilities that were the subject of the original CID. In connection with this matter, between July 2013 and early February 2016, the Company has received three civil investigative demands (a form of subpoena) for documents and information relating to our practices and policies for rehabilitation, and other services, our preadmission evaluation forms ("PAEs") required by TennCare and our Pre-Admission Screening and Resident Reviews ("PASRRs"). The DOJ has also issued CID's for testimony from current and former employees of the Company. The DOJ’s civil investigation of the Company's practices and policies for rehabilitation now covers all of the Company’s centers, but thus far only documents from six of our centers have been requested.

In June 2016, the Company received an authorized investigative demand (a form of subpoena) for documents in connection with a criminal investigation by the DOJ related to our practices with respect to PAEs and PASRRs. The Company has responded to this subpoena and the CID's and continues to provide additional information as requested. The Company cannot predict the outcome of these investigations or the related lawsuits, and the outcome could have a materially adverse effect on the Company, including the imposition of treble damages, criminal charges, fines, penalties and/or a corporate integrity agreement. The Company is committed to provide caring and professional services to its patients and residents in compliance with applicable laws and regulations.

Other Insurance

With respect to workers’ compensation insurance, substantially all of the Company’s employees became covered under either an indemnity insurance plan or state-sponsored programs in May 1997. The Company is completely self-insured for workers’ compensation exposures prior to May 1997. The Company has been and remains a non-subscriber to the Texas workers’ compensation system and is, therefore, completely self-insured for employee injuries with respect to its Texas operations. From June 30, 2003 until June 30, 2007, the Company’s workers’ compensation insurance programs provided coverage for claims incurred with premium adjustments depending on incurred losses. For the period from July 1, 2007 until June 30, 2008, the Company is completely self-insured for workers' compensation exposure. From July 1, 2008 through March 31, 2017, the Company is covered by a prefunded deductible policy. Under this policy, the Company is self-insured for the first $500,000 per claim, subject to an aggregate maximum of $3,000,000. The Company funds a loss fund account with the insurer to pay for claims below the deductible. The Company accounts for premium expense under this policy based on its estimate of the level of claims subject to the policy deductibles expected to be incurred. The liability for workers’ compensation claims is $515,000 at March 31, 2017. The Company has a non-current receivable for workers’ compensation policies covering previous years of $1,138,000 as of March 31, 2017. The non-current receivable is a function of payments paid to the Company’s insurance carrier in excess of the estimated level of claims expected to be incurred.

As of March 31, 2017, the Company is self-insured for health insurance benefits for certain employees and dependents for amounts up to $175,000 per individual annually. The Company provides reserves for the settlement of outstanding self-insured health claims at amounts believed to be adequate. The liability for reported claims and estimates for incurred but unreported claims is $1,488,000 at March 31, 2017. The differences between actual settlements and reserves are included in expense in the period finalized.

| |

| 6. | STOCK-BASED COMPENSATION |

Overview of Plans

In December 2005, the Compensation Committee of the Board of Directors adopted the 2005 Long-Term Incentive Plan (“2005 Plan”). The 2005 Plan allows the Company to issue stock options and other share and cash based awards. Under the 2005 Plan, 700,000 shares of the Company's common stock have been reserved for issuance upon exercise of equity awards granted thereunder. All grants under this plan expire 10 years from the date the grants were authorized by the Board of Directors.

In June 2008, the Company adopted the Advocat Inc. 2008 Stock Purchase Plan for Key Personnel (“Stock Purchase Plan”). The Stock Purchase Plan provides for the granting of rights to purchase shares of the Company's common stock to directors and officers and 150,000 shares of the Company's common stock has been reserved for issuance under the Stock Purchase Plan. The Stock Purchase Plan allows participants to elect to utilize a specified portion of base salary, annual cash bonus, or director compensation to purchase restricted shares or restricted share units (“RSU's”) at 85% of the quoted market price of a share of the Company's common stock on the date of purchase. The restriction period under the Stock Purchase Plan is generally two years from the date of purchase and during which the shares will have the rights to receive dividends, however, the restricted share certificates will not be delivered to the shareholder and the shares cannot be sold, assigned or disposed of during the restriction period. In June 2016, our shareholders approved an amendment to the Stock Purchase Plan to increase the number of shares of our common stock authorized under the Plan from 150,000 shares to 350,000 shares. No grants can be made under the Stock Purchase Plan after April 25, 2028.

In April 2010, the Compensation Committee of the Board of Directors adopted the 2010 Long-Term Incentive Plan (“2010 Plan”), followed by approval by the Company's shareholders in June 2010. The 2010 Plan allows the Company to issue stock appreciation rights, stock options and other share and cash based awards. Under the 2010 Plan, 380,000 shares of the Company's common stock have been reserved for issuance upon exercise of equity awards granted. In April 2017, the Board amended the 2010 Plan, subject to shareholder approval, to increase the shares under the plan to 680,000 and to extend the 2010 Plan to May 31, 2027.

Equity Grants and Valuations

During the three months ended March 31, 2017 and 2016, the Compensation Committee of the Board of Directors approved grants totaling approximately 88,000 and 83,000 shares of restricted common stock to certain employees and members of the Board of Directors, respectively. The fair value of restricted shares are determined as the quoted market price of the underlying common shares at the date of the grant. The restricted shares typically vest 33% on the first, second and third anniversaries of the grant date. Unvested shares may not be sold or transferred. During the vesting period, dividends accrue on the restricted shares, but are paid in additional shares of common stock upon vesting, subject to the vesting provisions of the underlying restricted shares. The restricted shares are entitled to the same voting rights as other common shares. Upon vesting, all restrictions are removed. Summarized activity of the equity compensation plans is presented below:

|

| | | | | | |

| | | | Weighted |

| | Options/ | | Average |

| | SOSARs | | Exercise Price |

| Outstanding, December 31, 2016 | 231,000 |

| | $ | 6.97 |

|

| Granted | — |

| | — |

|

| Exercised | — |

| | — |

|

| Expired or cancelled | (16,000 | ) | | 11.59 |

|

| Outstanding, March 31, 2017 | 215,000 |

| | $ | 6.64 |

|

| | | | |

| Exercisable, March 31, 2017 | 210,000 |

| | $ | 6.56 |

|

|

| | | | | | |

| | | | Weighted |

| | | | Average |

| | Restricted | | Grant Date |

| | Shares | | Fair Value |

| Outstanding, December 31, 2016 | 153,000 |

| | $ | 9.47 |

|

| Granted | 88,000 |

| | 9.98 |

|

| Dividend Equivalents | 1,000 |

| | 10.48 |

|

| Vested | (74,000 | ) | | 9.03 |

|

| Cancelled | — |

| | — |

|

| Outstanding, March 31, 2017 | 168,000 |

| | $ | 9.94 |

|

Summarized activity of the Restricted Share Units for the Stock Purchase Plan is as follows:

|

| | | | | | |

| | | | Weighted |

| | | | Average |

| | Restricted | | Grant Date |

| | Share Units | | Fair Value |

| Outstanding, December 31, 2016 | 54,000 |

| | $ | 11.10 |

|

| Granted | 26,000 |

| | 9.98 |

|

| Dividend Equivalents | 1,000 |

| | 10.48 |

|

| Vested | (37,000 | ) | | 12.11 |

|

| Cancelled | — |

| | — |

|

| Outstanding, March 31, 2017 | 44,000 |

| | $ | 9.58 |

|

Prior to 2016, the Compensation Committee of the Board of Directors also approved grants of Stock Only Stock Appreciation Rights (“SOSARs”) and Stock Options at the market price of the Company's common stock on the grant date. The SOSARs and Options vest 33% on the first, second and third anniversaries of the grant date, and expire 10 years from the grant date. The SOSARs and Options were valued and recorded in the same manner, and will be settled with issuance of new stock for the difference between the market price on the date of exercise and the exercise price. The Company estimated the total recognized and unrecognized compensation related to SOSARs and stock options using the Black-Scholes-Merton equity grant valuation model.

In computing the fair value estimates using the Black-Scholes-Merton valuation model, the Company took into consideration the exercise price of the equity grants and the market price of the Company's stock on the date of grant. The Company used an expected volatility that equals the historical volatility over the most recent period equal to the expected life of the equity grants. The risk free interest rate is based on the U.S. treasury yield curve in effect at the time of grant. The Company used the expected dividend yield at the date of grant, reflecting the level of annual cash dividends currently being paid on its common stock.

While no SOSARs or Options were granted during 2017 and 2016, previously granted SOSARs and Options remain outstanding as of March 31, 2017. The following table summarizes information regarding stock options and SOSAR grants outstanding as of March 31, 2017:

|

| | | | | | | | | | | | | | | | | | |

| | | Weighted | | | | | | | | |

| | | Average | | | | Intrinsic | | | | Intrinsic |

| Range of | | Exercise | | Grants | | Value-Grants | | Grants | | Value-Grants |

| Exercise Prices | | Prices | | Outstanding | | Outstanding | | Exercisable | | Exercisable |

| $10.21 to $10.88 | | $ | 10.64 |

| | 46,000 |

| | $ | 4,000 |

| | 41,000 |

| | $ | 3,000 |

|

| $2.37 to $6.21 | | $ | 5.55 |

| | 169,000 |

| | $ | 833,000 |

| | 169,000 |

| | $ | 833,000 |

|

| | | | | 215,000 |

| | | | 210,000 |

| | |

Stock-based compensation expense is non-cash and is included as a component of general and administrative expense or operating expense based upon the classification of cash compensation paid to the related employees. The Company recorded total stock-based compensation expense of $241,000 and $252,000 in the three month periods ended March 31, 2017 and 2016, respectively.

| |

| 7. | EARNINGS (LOSS) PER COMMON SHARE |

Information with respect to basic and diluted net income (loss) per common share is presented below in thousands, except per share:

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| Net income (loss) | | | |

| Income (loss) from continuing operations | $ | 1,348 |

| | $ | (74 | ) |

| Loss from discontinued operations, net of income taxes | (15 | ) | | (37 | ) |

| Net income (loss) | $ | 1,333 |

| | $ | (111 | ) |

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| Net income (loss) per common share: | | | |

| Per common share – basic | | | |

| Income (loss) from continuing operations | $ | 0.22 |

| | $ | (0.01 | ) |

| Loss from discontinued operations | — |

| | (0.01 | ) |

| Net income (loss) per common share – basic | $ | 0.22 |

| | $ | (0.02 | ) |

| Per common share – diluted | | | |

| Income (loss) from continuing operations | $ | 0.21 |

| | $ | (0.01 | ) |

| Loss from discontinued operations | — |

| | (0.01 | ) |

| Net income (loss) per common share – diluted | $ | 0.21 |

| | $ | (0.02 | ) |

| Weighted Average Common Shares Outstanding: | | | |

| Basic | 6,233 |

| | 6,160 |

|

| Diluted | 6,440 |

| | 6,160 |

|

The effects of 46,000 and 62,000 SOSARs and options outstanding were excluded from the computation of diluted earnings per common share in the three months ended March 31, 2017 and 2016, respectively, because these securities would have been anti-dilutive.

8. EQUITY METHOD INVESTMENT

The Company had one equity method investee, which was sold during the fourth quarter of 2016. The Company's share of the net profits and losses of the unconsolidated affiliate are reported as equity in net earnings or losses of unconsolidated affiliate in our statement of operations. For the three-month period ended March 31, 2017, the equity in the net income of an unconsolidated affiliate was zero compared to $33,000 for the three-month period ended March 31, 2016. The proceeds received from the sale are considered in the calculation of the gain on sale of investment in unconsolidated affiliate in our statement of operations. For the three-month period ended March 31, 2017, the gain on the sale of investment in unconsolidated affiliate was $733,000, related to the liquidation of remaining assets affiliated with the partnership.

| |

| 9. | BUSINESS DEVELOPMENTS AND OTHER SIGNIFICANT TRANSACTIONS |

Golden Living Transaction

On August 15, 2016, the Company entered into an Operation Transfer Agreement with Golden Living (the "Lessor") to assume the operations of 22 centers in Alabama and Mississippi.

On October 1, 2016, the Company entered into a Master Lease Agreement (the "Lease") with Golden Living to directly lease eight centers located in Mississippi from the Lessor, which include: (i) a 152-bed skilled nursing center known as Golden Living Center - Amory; (ii) a 130-bed skilled nursing center known as Golden Living Center - Batesville; (iii) a 58-bed skilled nursing center known as Golden Living Center - Brook Manor; (iv) a 119-bed skilled nursing center known as Golden Living Center - Eupora; (v) a 140-bed skilled nursing center known as Golden Living Center - Ripley; (vi) a 140-bed skilled nursing center known as Golden Living Center - Southaven; (vii) a 120-bed skilled nursing center known as Golden Living Center - Eason Blvd; (viii) a 60-bed skilled nursing center known as Golden Living Center - Tylertown. The Lease is triple net and has an initial term of ten years with two separate five year options to extend the term. The Company also assumed the individual leases of a 120-bed center known as Broadmoor Nursing Home, with an initial lease term of ten years with first year rent of $540,000, escalating to $780,000 in the second year, and 2% annually thereafter, and a 99-bed skilled nursing center known as Leake County Nursing Home, with a lease term of two years with annual rent of $300,000.

On November, 1 2016, the Company amended and restated the Lease ("Amended Lease") with the Lessor to directly lease an additional twelve centers located in Alabama from the Lessor, which include: (i) a 87-bed skilled nursing center known as Golden Living Center - Arab; (ii) a 180-bed skilled nursing center known as Golden Living Center - Meadowood; (iii) a 132-bed skilled nursing center known as Golden Living Center - Riverchase; (iv) a 100-bed skilled nursing center known as Golden Living Center - Boaz; (v) a 154-bed skilled nursing center known as Golden Living Center - Foley; (vi) a 50-bed skilled nursing center known as Golden Living Center - Hueytown; (vii) a 85-bed skilled nursing center known as Golden Living Center - Lanett; (viii) a 138-bed skilled nursing center known as Golden Living Center - Montgomery; (ix) a 120-bed skilled nursing center known as Golden Living Center - Oneonta; (x) a 173-bed skilled nursing center known as Golden Living Center - Oxford; (xi) a 94-bed skilled nursing center known as Golden Living Center - Pell City; (xii) a 123-bed skilled nursing center known as Golden Living Center - Winfield. The Amended Lease is triple net and has an initial term of ten years with two separate five years options to extend the term. Base rent for the amended lease is $24,675,000 for the first year and escalates 2% annually thereafter.

2016 Acquisitions

On February 26, 2016, the Company exercised its purchase options to acquire the real estate assets for Diversicare of Hutchinson in Hutchinson, Kansas and Clinton Place in Clinton, Kentucky for $4,250,000 and $3,300,000, respectively. The Company has operated these facilities since February 2015 and April 2012, respectively. Hutchinson is an 85-bed skilled nursing facility, and Clinton is an 88-bed skilled nursing facility. As a result of the consummation of the Agreements, the Company allocated the purchase price and acquisition costs between the assets acquired. The allocation of the purchase price was determined with the assistance of HealthTrust LLC, a third-party real estate valuation firm. The allocation for the assets acquired is as follows:

|

| | | | | | |

| | Hutchinson | Clinton Place |

| Purchase Price | $ | 4,250,000 |

| $ | 3,300,000 |

|

| Acquisition Costs | 43,000 |

| 34,000 |

|

| | $ | 4,293,000 |

| $ | 3,334,000 |

|

| | | |

| Allocation: | | |

| Buildings | 3,443,000 |

| 2,898,000 |

|

| Land | 365,000 |

| 267,000 |

|

| Furniture, Fixtures and Equipment | 485,000 |

| 169,000 |

|

| | $ | 4,293,000 |

| $ | 3,334,000 |

|

2016 Lease Termination

On May 31, 2016, the Company entered into an Agreement with Avon Ohio, LLC to amend the original lease agreement, thus terminating the Company's right of possession of the facility. As a result, the Company incurred lease termination costs of $2,008,000 in the second quarter of 2016. Under the amended agreement, the Company is required to pay $300,000 per year through the term of the original lease agreement, July 31, 2024. For accounting purposes, this transaction was not reported as a discontinued operation, which is in accordance with the modified authoritative guidance for reporting discontinued operations, effective January 1, 2015. A disposal is now required to be reported in discontinued operations only if the disposal represents a strategic shift that has (or will have) a major effect on the Company's operations and financial results.

2016 Sale of Investment in Unconsolidated Affiliate

On October 28, 2016, the Company and its partners entered into an asset purchase agreement to sell the pharmacy joint venture. The sale resulted in a $1,366,000 gain in the fourth quarter of 2016. Subsequently, we recognized an additional gain of $733,000 for the three-month period ended March 31, 2017, related to the final liquidation of remaining net assets affiliated with the partnership.

ITEM 2 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

Diversicare Healthcare Services, Inc. (together with its subsidiaries, “Diversicare” or the “Company”) provides long-term care services to nursing center patients in ten states, primarily in the Southeast, Midwest, and Southwest. The Company’s centers provide a range of health care services to their patients and residents that include nursing, personal care, and social services. Additionally, the Company’s nursing centers also offer a variety of comprehensive rehabilitation services, as well as nutritional support services. The Company's continuing operations include centers in Alabama, Florida, Indiana, Kansas, Kentucky, Mississippi, Missouri, Ohio, Tennessee, and Texas.

As of March 31, 2017, the Company’s continuing operations consist of 76 nursing centers with 8,453 licensed nursing beds. The Company owns 17 and leases 59 of its nursing centers. Our nursing centers range in size from 48 to 320 licensed nursing beds. The licensed nursing bed count does not include 496 licensed assisted living and residential beds.

Strategic Operating Initiatives

We identified several key strategic objectives to increase shareholder value through improved operations and business development. These strategic operating initiatives include: improving skilled mix in our nursing centers, improving our average Medicare rate, implementing and maintaining Electronic Medical Records (“EMR”) to improve Medicaid capture, and completing strategic acquisitions. We have experienced success in these initiatives and expect to continue to build on these improvements.

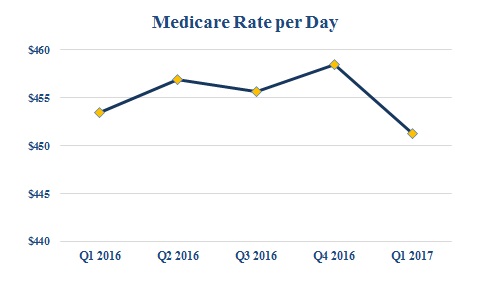

Improving skilled mix and average Medicare rate:

Our strategic operating initiatives of improving our skilled mix and our average Medicare rate required investing in nursing and clinical care to treat more acute patients along with nursing center-based marketing representatives to attract these patients. These initiatives developed referral and Managed Care relationships that have attracted and are expected to continue to attract payor sources for patients covered by Medicare and Managed Care. The Company's skilled mix for the periods ending March 31, 2017 and 2016 was 15.7% and16.3%, respectively. The graph below illustrates our success with increasing our average Medicare rate per day:

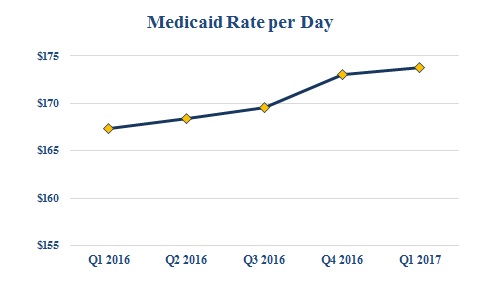

Implementing Electronic Medical Records to improve Medicaid capture:

As another part of our strategic operating initiatives, we implemented EMR to improve Medicaid acuity capture, primarily in our states where the Medicaid payments are acuity based. We completed the implementation of EMR in all our nursing centers in December 2011, on time and under budget, and since implementation, have increased our average Medicaid rate despite rate cuts in certain acuity based states by accurate and timely capture of care delivery. The graph below illustrates our success with increasing our average Medicaid rate per day since implementation:

Completing strategic acquisitions and dispositions:

Our strategic operating initiatives include a renewed focus on completing strategic acquisitions. We continue to pursue and investigate opportunities to acquire, lease or develop new centers, focusing primarily on opportunities within our existing geographic areas of operation.

On October 1, 2016 and November 1, 2016, we assumed the operations of ten centers in Mississippi and 12 centers in Alabama, respectively, which is further discussed in Note 9 to the interim consolidated financial statements. The completion of this acquisition brings the Company's operations to 76 nursing centers with 8,453 skilled nursings beds. These acquired facilities are expected to contribute in excess of $185 million in annual revenues.

As part of our strategic efforts, we have also performed thorough analysis on our existing centers in order to determine whether continuing operations within certain markets or regions was in line with the short-term and long-term strategy of the business. As a result, in May 2016, we ceased operations at our Avon, Ohio, facility, thus terminating our lease with Avon Ohio, LLC. This transaction was not reported as a discontinued operation as described in Note 9 to the interim consolidated financial statements.

Basis of Financial Statements

Our patient revenues consist of the fees charged for the care of patients in the nursing centers we own and lease. Our operating expenses include the costs, other than lease, professional liability, depreciation and amortization expenses, incurred in the operation of the nursing centers we own and lease. Our general and administrative expenses consist of the costs of the corporate office and regional support functions. Our interest, depreciation and amortization expenses include all such expenses across the range of our operations.

Critical Accounting Policies and Judgments

A “critical accounting policy” is one which is both important to the understanding of our financial condition and results of operations and requires management’s most difficult, subjective or complex judgments often involving estimates of the effect of matters that are inherently uncertain. Actual results could differ from those estimates and cause our reported net income or loss to vary significantly from period to period. Our critical accounting policies are more fully described in our 2016 Annual Report on Form 10-K.

Revenue Sources

We classify our revenues from patients and residents into four major categories: Medicaid, Medicare, Managed Care, and Private Pay and other. Medicaid revenues are composed of the traditional Medicaid program established to provide benefits to those in need of financial assistance in the securing of medical services. Medicare revenues include revenues received under both Part A and Part B of the Medicare program. Managed Care revenues include payments for patients who are insured by a third-party entity, typically called a Health Maintenance Organization, often referred to as an HMO plan, or are Medicare beneficiaries who assign

their Medicare benefits to a Managed Care replacement plan often referred to as Medicare replacement products. The Private Pay and other revenues are composed primarily of individuals or parties who directly pay for their services. Included in the Private Pay and other payors are patients who are hospice beneficiaries as well as the recipients of Veterans Administration benefits. Veterans Administration payments are made pursuant to renewable contracts negotiated with these payors.

The following table sets forth net patient and resident revenues related to our continuing operations by payor source for the periods presented (dollar amounts in thousands):

|

| | | | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | | 2016 |

| Medicaid | $ | 72,873 |

| | 51.5 | % | | $ | 47,206 |

| | 48.2 | % |

| Medicare | 38,011 |

| | 26.9 |

| | 28,021 |

| | 28.6 |

|

| Managed Care | 10,806 |

| | 7.6 |

| | 7,401 |

| | 7.6 |

|

| Private Pay and other | 19,810 |

| | 14.0 |

| | 15,317 |

| | 15.6 |

|

| Total | $ | 141,500 |

| | 100.0 | % | | $ | 97,945 |

| | 100.0 | % |

The following table sets forth average daily skilled nursing census by payor source for our continuing operations for the periods presented:

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2017 | 2016 |

| Medicaid | 4,649 |

| | 68.7 | % | | 3,087 |

| | 66.5 | % |

| Medicare | 792 |

| | 11.7 |

| | 574 |

| | 12.4 |

|

| Managed Care | 273 |

| | 4.0 |

| | 180 |

| | 3.9 |

|

| Private Pay and other | 1,056 |

| | 15.6 |

| | 804 |

| | 17.2 |

|

| Total | 6,770 |

| | 100.0 | % | | 4,645 |

| | 100.0 | % |

Consistent with the nursing home industry in general, changes in the mix of a facility’s patient population among Medicaid, Medicare, Managed Care, and Private Pay and other can significantly affect the profitability of the facility’s operations.

Health Care Industry

The health care industry is subject to numerous laws and regulations of federal, state and local governments. These laws and regulations include, but are not necessarily limited to, matters such as licensure, accreditation, government health care program participation requirements, reimbursement for patient services, quality of patient care and Medicare and Medicaid fraud and abuse. Over the last several years, government activity has increased with respect to investigations and allegations concerning possible violations by health care providers of fraud and abuse statutes and regulations, false claims statutes, HIPAA violations, as well as laws and regulations governing quality of care issues in the skilled nursing profession in general. Violations of these laws and regulations could result in exclusion from government health care programs together with the imposition of significant fines and penalties, as well as significant repayments for patient services previously billed. Compliance with such laws and regulations is subject to ongoing government review and interpretation, as well as regulatory actions in which government agencies seek to impose fines and penalties. The Company is involved in regulatory actions of this type from time to time.

Health care and health insurance reform.

In March 2010, significant legislation concerning health care and health insurance was passed, including the “Patient Protection and Affordable Care Act” (“Patient Protection Act”), along with the “Health Care and Education Reconciliation Act of 2010” (“Reconciliation Act”), collectively defined as the “Legislation.” We expect this Legislation to impact our Company, our employees and our patients in a variety of ways. Some aspects of these new laws have been implemented while others will be phased in over the next several years when all mandates become effective. This Legislation significantly changes the future responsibility of employers with respect to providing health care coverage to employees in the United States. We have not estimated the financial impact of the Legislation and the costs associated with complying with the increased levels of health insurance we will be required to provide our employees and their dependents in future years. We expect the Legislation will result in increased operating expenses.

We also anticipate this Legislation will continue to impact our Medicaid and Medicare reimbursement as well, though the timing and ultimate level of that impact is currently unknown as we anticipate that many of the provisions of the Legislation may be subject to further clarification and modification through the rule making process. The Legislation expands the role of home-based and community services, which may place downward pressure on our sustaining population of Medicaid patients. These reforms

include the possible modifications to the conditions of qualification for payment, bundling of payments to cover both acute and post-acute care and the imposition of enrollment limitations on new providers. The provisions of the Legislation discussed above are examples of recently-enacted federal health reform provisions that we believe may have a material impact on the long-term care industry and on our business. However, the foregoing discussion is not intended to constitute, nor does it constitute, an exhaustive review and discussion of the Legislation.

Skilled nursing centers are required to bill Medicare on a consolidated basis for certain items and services that they furnish to patients, regardless of the cost to deliver these services. This consolidated billing requirement essentially makes the skilled nursing center responsible for billing Medicare for all care services delivered to the patient during the length of stay.

CMS has instituted a number of new exploratory test programs designed to extend the reimbursement and financial responsibilities under consolidated billing beyond the traditional discharge date to include a broader set of bundled services. Such examples may include, but are not exclusive to, home health, durable medical equipment, home and community based services, and the cost of re-hospitalizations during a specified bundled period. Today, these test programs for bundled reimbursement are confined to a small set of clinical conditions. This bundled form of reimbursement could be extended to a broader range of diagnosis related conditions in the future. Because of the untested nature of this new form of reimbursement, the potential impact on skilled nursing center utilization and reimbursement is currently unknown. The process for defining bundled services has not been fully determined by CMS and therefore is subject to change during the rule making process.

Health Insurance Portability and Accountability Act of 1996 Compliance.

The Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) has mandated an extensive set of regulations to standardize electronic patient health, administrative and financial data transactions and to protect the privacy of individually identifiable health information. We have a HIPAA compliance committee and designated privacy and security officers.

The HIPAA transaction standards are intended to simplify the electronic claims process and other healthcare transactions by encouraging electronic transmission rather than paper submission. These regulations provide for uniform standards for data reporting, formatting and coding that we must use in certain transactions with health plans. The HIPAA security regulations establish detailed requirements for safeguarding protected health information that is electronically transmitted or electronically stored. Some of the security regulations are technical in nature, while others are addressed through policies and procedures. We implemented or upgraded computer and information systems as we believe necessary to comply with the new regulations.

The HIPAA regulations related to privacy establish comprehensive federal standards relating to the use and disclosure of individually identifiable health information (“protected health information”). The privacy regulations establish limits on the use and disclosure of protected health information, provide for patients' rights, including rights to access, to request amendment of, and to receive an accounting of certain disclosures of protected health information, and require certain safeguards for protected health information. In addition, each covered entity must contractually bind individuals and entities that furnish services to the covered entity or perform a function on its behalf, and to which the covered entity discloses protected health information, to restrictions on the use and disclosure of that protected health information. In general, the HIPAA regulations do not supersede state laws that are more stringent or grant greater privacy rights to individuals. Thus, we must reconcile the HIPAA regulations and other state privacy laws.

Although we believe that we are in material compliance with these HIPAA regulations, inadvertent violations of these regulations may occur in the course of our business. For this and other reasons, the HIPAA regulations are expected to continue to impact us operationally and financially and may pose increased regulatory risk.

Self-Referral and Anti-Kickback Legislation.

The health care industry is subject to state and federal laws which regulate the relationships of providers of health care services, physicians and other clinicians. These self-referral laws impose restrictions on physician referrals to any entity with which they have a financial relationship, which is a broadly defined term. We believe our relationships with physicians are in compliance with the self-referral laws. Failure to comply with self-referral laws could subject us to a range of sanctions, including civil monetary penalties and possible exclusion from government reimbursement programs. There are also federal and state laws making it illegal to offer anyone anything of value in return for referral of patients. These laws, generally known as “anti-kickback” laws, are broad and subject to interpretations that are highly fact dependent. Given the lack of clarity of these laws, there can be no absolute assurance that any health care provider, including us, will not be found in violation of the anti-kickback laws in any given factual situation. Strict sanctions, including fines and penalties, exclusion from the Medicare and Medicaid programs and criminal penalties, may be imposed for violation of the anti-kickback laws.

Reporting Obligations under Section 111 of the Medicare, Medicaid and SCHIP Extension Act of 2007 (“MMSEA”).

Since January 1, 2010, we have reported specific information regarding all claimants and claim settlements involving Medicare participants so CMS can recover Medicare funds expended to provide healthcare treatment to the claimant. The requirements are to ensure that CMS is notified so that it may recoup the amounts paid for services from the settlement proceeds. This does not

result in us making additional payments to CMS for these services provided and does not result in an incremental cost to us. Strict sanctions, including fines and penalties, exclusion from the Medicare and Medicaid programs and criminal penalties, may be imposed for non-compliance with these reporting obligations.

Medicare and Medicaid Reimbursement

A significant portion of our revenues are derived from government-sponsored health insurance programs. Our nursing centers derive revenues under Medicaid, Medicare, Managed Care, Private Pay and other third party sources. We employ third-party specialists in reimbursement and also use these services to monitor regulatory developments to comply with reporting requirements and to ensure that proper payments are made to our operated nursing centers.

Medicare

Medicare is a federally-funded and administered health insurance program for the aged and for certain chronically disabled individuals. Part A of the Medicare program covers certain services furnished by skilled nursing centers and other institutional providers and inpatient hospital services. Part B covers physician services, durable medical equipment, various outpatient services and certain ancillary services. Medicare generally covers skilled nursing center services for beneficiaries who require nursing care or rehabilitation services after a qualifying hospital stay. Medicare pays a per diem rate for each beneficiary, adjusted for patient acuity and additional factors such as geographic differences in wage rates. The payment rates are set forth under a prospective payment system that uses nursing and therapy indexes to assign a payment rate to each beneficiary. The Centers for Medicare & Medicaid Services (“CMS”) updates the rates annually. The payment rates cover all services to be provided to a beneficiary, including room and board, skilled nursing care, therapy, and medications.

In July 2016, CMS issued its final rule outlining Medicare payment rates and policies for skilled nursing centers for federal fiscal year 2017, which began October 1, 2016. CMS projects that aggregate payments to skilled nursing centers will increase by a net 2.4% for fiscal year 2017. This reflects a 2.7% market basket increase, reduced by a 0.3% multi-factor productivity adjustment required by Patient Protection and Affordable Care Act ("PPACA"). The payment rates for fiscal year 2016, which were projected to increase aggregate payments to skilled nursing centers by 1.2%, reflected a 0.6% forecast error reduction and the 0.5% productivity reduction required by PPACA. For fiscal year 2018, the Medicare Access and CHIP Reauthorization Act of 2015 (“MACRA”) requires the payment update for skilled nursing centers to be 1%.

In addition to the adjustments described above, payment rates are reduced pursuant to ongoing sequestration. The Budget Control Act of 2011 (“BCA”) requires automatic spending reductions to reduce the federal deficit, including Medicare spending reductions of up to 2% per fiscal year, with a uniform percentage reduction across all Medicare programs. CMS began imposing a 2% reduction on Medicare claims in April of 2013. These reductions have been extended through 2025.

CMS has increasingly introduced policies intended to shift Medicare to value-based payment methodologies, tying reimbursement to quality of care rather than quantity. For example, CMS has implemented the Quality Reporting Program, under which skilled nursing centers are required to report quality data. Beginning in fiscal year 2018, skilled nursing centers that fail to submit required data will be subject to a 2% reduction to the annual market basket update. The Skilled Nursing Facility Value-Based Purchasing (“SNF VBP”) Program, which begins on October 1, 2018, will make incentive payments available to skilled nursing centers based on their past performance on a specified quality measure. The first measure under this program is the 30-day potentially preventable readmission measure, which assesses the rate of unplanned, potentially preventable hospital readmissions for skilled nursing center patients within 30 days of discharge from a prior admission to a hospital. CMS will fund the SNF VPB Program incentive payment pool by withholding and then redistributing 2% of skilled nursing center payments, beginning in fiscal year 2019.

In addition, CMS has established the Five-Star Quality Rating System to assist the public in choosing a skilled care provider. Each nursing home is given a rating between 1 and 5 stars, which is published on the Nursing Home Compare website. The overall star rating is determined by three components: information from the last three years of health inspections, staffing information, and quality measures. The rating is based, in part, on the quality data nursing centers are required to report. For example, nursing centers must report the percentage of short-stay residents who are successfully discharged into the community and the percentage who had an outpatient emergency department visit. We remain diligent in continuing to provide outstanding patient care to achieve high rankings for our centers, as well as assuring that our rankings are correct and appropriately reflect our quality results.