NEVSUN RESOURCES LTD.

ANNUAL INFORMATION FORM

For the fiscal year ended December 31, 2005

March 22, 2006

- i -

TABLE OF CONTENTS

PRELIMINARY NOTES

II

FOIRWARD LOOKING STATEMENTS

II

INCORPORATION OF FINANCIAL STATEMENTS AND TECHNICAL REPORTS

II

INFORMATION CONCERNING PREPARATION OF RESOURCE ESTIMATES

II

GLOSSARY AND DEFINED TERMS

III

REPORTING CURRENCY

X

ITEM 1.

CORPORATE STRUCTURE

1

1.1

NAME AND INCORPORATION

1

1.2

INTERCORPORATE RELATIONSHIPS

1

ITEM 2.

GENERAL DEVELOPMENT OF THE BUSINESS

2

2.1

THREE YEAR HISTORY

2

2.2

SIGNIFICANT ACQUISITIONS AND SIGNIFICANT DISPOSITIONS

3

ITEM 3.

DESCRIPTION OF THE BUSINESS

3

3.1

GENERAL

3

3.2

TABAKOTO / SEGALA, MALI

7

3.3

BISHA, ERITREA

13

ITEM 4.

DIVIDENDS

22

ITEM 5.

DESCRIPTION OF CAPITAL STRUCTURE

22

ITEM 6.

MARKET FOR SECURITIES

23

6.1

MARKET FOR SECURITIES

23

ITEM 7.

DIRECTORS AND OFFICERS

23

7.1

NAME, OCCUPATION AND SECURITY HOLDING

23

7.2

CORPORATE CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS

25

7.3

CONFLICTS OF INTEREST

27

7.4

AUDIT COMMITTEE

27

ITEM 8.

INTEREST OF MANAGEMENT

34

ITEM 9.

TRANSFER AGENTS AND REGISTRARS

34

ITEM 10.

MATERIAL CONTRACTS

34

ITEM 11.

INTERESTS OF EXPERTS

34

ITEM 12.

ADDITIONAL INFORMATION

36

12.1

ADDITIONAL INFORMATION

36

- ii -

PRELIMINARY NOTES

Incorporation of Financial Statements and Technical Reports

The following documents are incorporated by reference and form part of this annual information form (the “Annual Information Form” or “AIF”) which is prepared in accordance with Form 51-102F2. These documents may be accessed using the System for Electronic Documents Analysis and Retrieval (“SEDAR”) on the internet atwww.sedar.com:

1.

Consolidated financial statements for the year ended December 31, 2005, together with the auditors’ report thereon dated March 1, 2006;

2.

Management’s discussion and analysis (MD&A) for the year ended December 31, 2005;

3.

Bisha Property, Gash-Barka District, Eritrea 43-101 Technical Report and Preliminary dated December 1, 2005 (the “Bisha Technical Report”);

4.

Technical Report on the Bisha Property and Resource Estimate of the Bisha Deposit, Gash-Barka District, Eritrea dated October 1, 2004;

5.

Technical Report for the Segala Property, Mali West Africa dated May 17, 2004, (the “Segala Technical Report”);

6.

Technical Report on the Tabakoto property, Mali West Africa dated May 17, 2004, (the “Tabakoto Technical Report”), excluding sections 15 and 21 for the reasons explained under Item 11 – Interest of Experts.

Forward Looking Statements

This report contains forward-looking statements concerning anticipated developments on the Company's mineral properties in Mali and Eritrea and in the Company's other operations; planned exploration and development activities; the adequacy of the Company's financial resources; financial projections, including, but not limited to, estimates of operating costs, processing rates, life of mine, metal prices, exchange rates, reclamation costs, net present value and internal rates of return; and other events or conditions that may occur in the future. Forward-looking statements are frequently, but not always, identified by words such as "expects," "anticipates," "believes," "intends," "estimates," "potential," "possible" and similar expressions, or statements that events, conditions or results "will," "may," "could" or "should" occur or be achieved. Information concerning the interpretation of drill results and mineral resource and reserve estimates also may be deemed to be forward-looking statements, as such information constitutes a prediction of what mineralization might be found to be present if and when a project is actually developed. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those described in this Annual Information Form.

- iii -

The Company's forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made and the Company assumes no obligation to update such forward-looking statements in the future. For the reasons set forth above, investors should not place undue reliance on forward-looking statements.

Information Concerning Preparation of Resource Estimates

All resource estimates included in this Annual Information Form have been prepared in accordance with Canadian National Instrument 43-101 and the Canadian Institute of Mining and Metallurgy Classification System. These standards differ significantly from the requirements of the United States Securities and Exchange Commission, and resource information included herein may not be comparable to similar information concerning U.S. companies. In particular, the term “resource” does not equate to the term “reserves”. Under U.S. standards, mineralization may not be classified as a “reserve” unless the determination has been made, that according to definition is, “that part of a mineral deposit which could be economically and legally produced or extracted at the time of the reserve determination”. The Securities and Exchange Commis sion’s disclosure standards normally do not permit the inclusion of information concerning “measured mineral resources”, “indicated mineral resources” or “inferred mineral resources” in documents filed with the Securities and Exchange Commission, unless such information is required to be disclosed by the law of the company’s jurisdiction of incorporation or of a jurisdiction in which its securities are traded. Accordingly, information concerning descriptions of mineralization and resources contained in this Annual Information Form may not be comparable to information made public by U.S. companies subject to the reporting and disclosure requirements of the United States Securities and Exchange Commission.

Glossary and Defined Terms

The following is a glossary ofcertain mining terms used in this Annual Information Form.

AEM:

Airborne electro-magnetic geophysical survey.

Albite:

Sodium plagioclase.

Alluvial:

Sedimentary accumulations often as sand or gravel deposited or formed by the action of running water, as in a stream channel or alluvial fan.

Alteration:

Refers to process of changing primary rock minerals (such as quartz, feldspar and hornblende) to secondary minerals (quartz, carbonate, and clay minerals) by hydrothermal fluids (hot water).

Airborne geophysical

Survey:

A helicopter or fixed wing operated geophysical evaluation of a property.

- iv -

Anticline:

Part of the fold or the flexure that forms an arch with the older rocks occupy the core of this arch and the younger rocks the outer portion.

Argillite:

Low grade metamorphic clay rich sedimentary rock (shale, mudstone, siltstone).

Arsenopyrite:

The common arsenic mineral and principal ore of arsenic; occurs in many sulphide ore deposits, particularly those containing lead, silver, and gold.

Block model:

The representation of geologic units using three-dimensional blocks of predetermined sizes.

Breccia:

A rock in which angular fragments are surrounded by a mass of fine-grained minerals.

CIM:

Canadian Institute of Mining and Metallurgy.

Carbonatization:

The formation of carbonate minerals as calcite, dolomite, magnesite, ankerite, cerussite, malachite, etc.

Chlorite:

Light to dark-green, black; pearly, and vitreous mica whose general composition is that of a basic iron, magnesium, aluminum silicate (Mg, Fe)6(AlSi3)O13(OH)8.

Conglomerate:

Rudaceous rocks consisting of rounded or sub-rounded fragments, implying rather more transport than breccias.

Cross section:

A representative display of geology perpendicular to the general trend of the mineralization.

Diamond drill:

A machine using diamond embedded bits to extract a known sample size from the ground.

Differential GPS:

A survey system using instruments that provides an accurate global position from known satellite positions in space.

Diorite:

A coarse-grained plutonic intermediate igneous rock, consisting essentially of intermediate plagioclase, and one or more of the ferromagnesian minerals (biotite, hornblende, augite).

Dolerite:

Fine to medium-grained gabbro, replaced in North America by diabase, usually occur as dykes.

Dyke:

A tabular igneous intrusion that cuts across the bedding or foliation of the country rock.

- v -

EM:

An instrument that measures the change in electro-magnetic conductivity of different geological units below the surface of the earth.

Feasibility study:

Group of reports that determine the economic viability of a given mineral occurrence.

Felsic:

An acronym word derived from feldspar and silica, and used to describe light-coloured silica minerals such as quartz, feldspar, and feldspathoids.

G/t or gpt:

Grams per metric tonne.

Gabbro:

A coarse-grained, plutonic basic (mafic) igneous rock consisting of basic plagioclase (labradorite to anorthosite), feldspar, Pyroxene (augite and/or hypersthene), olivine, hornblende, biotite. Equivalent extrusive basalt

Geotechnical work:

Tasks that provide representative data of the geological rock quality in a known volume.

Gossan:

An iron-bearing weathered product overlying a sulphide deposit. It is formed by the oxidation of sulphides and the leaching-out of the sulphur and most metals, leaving hydrated iron oxides and rarely sulphates.

Graphite:

A soft black form of native carbon found in metamorphic rocks, crystalline limestones, igneous rocks, veins, and pegmatites.

Gravity:

A methodology using instrumentation allowing the accurate measuring of the difference between densities of various geological units in situ.

Greywacke:

A sedimentary rocks with fine to coarse, angular to sub-angular particles which are mainly rock fragments (lithic fragments). They are usually poorly sorted and the cementing material is generally argillaceous.

Induced Polarization (IP):

A method of ground geophysical surveying employing an electrical current to determine indications of mineralization.

Laterite:

Residual deposit formed under special climatic conditions in tropical regions, it consists essentially of hydrated iron oxides. The original rocks are mafic, ultramafic, and iron rich lithologies.

Long section:

A representative display of geology along the axis of mineralization.

- vi -

Mafic:

Igneous rocks composed mostly of dark, iron- and magnesium-rich minerals.

Magnetometer:

An instrument that measures the difference in magnetic response of different geological units.

Metasediments:

Metamorphic sedimentary rocks.

Mineral Reserve:

The economically mineable part of a measured or indicated mineral resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A mineral reserve includes diluting materials and allowances for losses that may occur when the material is mined and processed.

The terms “mineral reserve”, “proven mineral reserve”, “probable mineral reserve”, and “measured, indicated and inferred mineral resource” used in this Annual Information Form are Canadian mining terms as defined in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resource and Mineral Reserves Definitions and guidelines adopted by the CIM Council on August 20, 2000 as those definitions may be amended from time to time by CIM (the “CIM Standards”).

Under United States standards, a “mineral reserve” is defined as a part of a mineral deposit which could be economically and legally extracted or produced at the time the mineral reserve determination is made, where:

·

A “final” or “bankable” feasibility study is required to meet the requirements to designate reserves;

·

A historic three year average price is to be used in any reserve or cash flow analysis to designate reserves; and

·

To meet the “legal” part of the reserve definition, the primary environmental analysis or document should have been submitted to governmental authorities.

Mineral reserves are categorized as follows on the basis of the degree of confidence in the estimate of the quantity and grade of the deposit.

Under United States standards, proven or measured reserves are defined as reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; (b) grade and/or quality are computed from the results of detailed sampling and (c) the sites for

- vii -

inspection, sampling and measurement are spaced so closely and the geographic character is so well defined that size, shape, depth and mineral content of reserves are well established.

Under United States standards, probable or indicated reserves are defined as reserves for which quantity and grade and/or quality are computed from information similar to that of proven reserves (under United States standards), but the sites for inspection, sampling, and measurement are further apart or are otherwise less adequately spaced, and the degree of assurance, although lower than that for proven mineral reserves, is high enough to assume continuity between points of observation. The degree of assurance, although lower than that for proven mineral reserves, is high enough to assume continuity between points of observation.

Mineral Resource:

A concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge.

Inferred Mineral Resource:

That part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

Indicated Mineral Resource:

That part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.

Measured Mineral Resource:

That part of a Mineral Resource for which quantity, grade or quality, densities, shape, physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters, to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered

- viii -

through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity.

While the terms “mineral resource,” “measured mineral resource,” “indicated mineral resource,” and “inferred mineral resource” are recognized and required by Canadian regulations, they are not defined terms under standards in the United States. As such, information contained in this report concerning descriptions of mineralization and resources under Canadian standards may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements of the Securities and Exchange Commission. “Indicated mineral resource” and “inferred mineral resource” have a great amount of uncertainty as to their existence and a great uncertainty as to their economic and legal feasibility. It can not be assumed that all or any part of an “indicated mineral resource” or “inferred mi neral resource” will ever be upgraded to a higher category. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves.

Mineralization

An anomalous occurrence of metal or other commodity of value defined by any method of sampling (surface outcrops, drill core, underground channels). Under United States Securities and Exchange Commission standards, such a deposit does not qualify as a reserve until comprehensive evaluation, based on unit cost, grade, recoveries and other factors, concludes that the mineralization could be legally and economically produced or extracted at the time the reserve determination is made

Mottled clay:

Spotted clay with different colour.

Multiple indicator kriging:

The probability in the distribution of values using deciles that are transformed to 1, if equal or less than the value or 0, if greater than the value, used to determine the average of a group of values.

Ore:

Rock, generally containing metallic or non-metallic materials, which can be mined and processed at a profit.

Porphyry:

An igneous rock characterized by visible crystals in a fine–grained matrix.

Pulse EM:

Ground electro-magnetic, time domain, prospecting technique.

Pyrite:

An iron sulphide mineral (FeS2), the most common naturally occurring sulphide mineral.

Quartz diorite:

Diorite with quartz as usually accessory minerals (<10%).

Return water dam:

Water collected in a storage area from a mining site.

- ix -

Reverse Circulation (RC):

A type of drilling using dual-walled drill pipe in which the material drilled, water, and mud are circulated up the center pipe while the air is blown down the outside pipe.

Saprolite:

Clay and iron oxide rich weathered and altered rock.

Schist:

A medium to course grained foliated metamorphic rock the grains of which have a roughly parallel arrangement; generally developed by shearing.

Shear Zone:

A zone in which shearing has occurred on a large scale so that the rock is crushed and brecciated.

Silica:

SiO2 (quartz and chalcedony).

Sphalerite:

Zinc sulphide mineral (ZnS).

Stockwork:

A three–dimensional network of closely spaced planar to irregular veinlets.

Strike:

The direction, or bearing from true north, of a vein or rock formation measured on a horizontal surface.

Sulphide (Sulfide):

A compound of sulphur (sulfur) and some other metallic element.

Supergene:

A word suggesting an origin literally “from above”. It is used almost exclusively for processes involving water, with or without dissolved material, percolating down from the surface. Typical supergene processes are solution, hydration, oxidation, deposition from solution, reactions of ions in solution with ions in existing minerals (replacement or enrichment).

Syncline:

A flexure or fold in a form of a trough, the younger rocks occupy the core and the older rocks the outer portion.

Tailings:

Gangue minerals extracted from ore through various mineral processes and deposited in an enclosed ground storage area.

Tpa:

Tonnes per annum.

Trenching:

The mechanical or human excavation of ground material to expose material below surface.

VMS:

Volcanic hosted massive sulphides.

Waste rock dump:

Rock determined as having no economic value in a mining scenario that is removed to a location and deposited.

- x -

Water storage dam:

Water collected from rain or another hydrological system and trapped in a storage area.

Reporting Currency

All dollar amounts are expressed in United States dollars unless otherwise indicated. The Company’s quarterly and annual financial statements are presented in United States dollars.

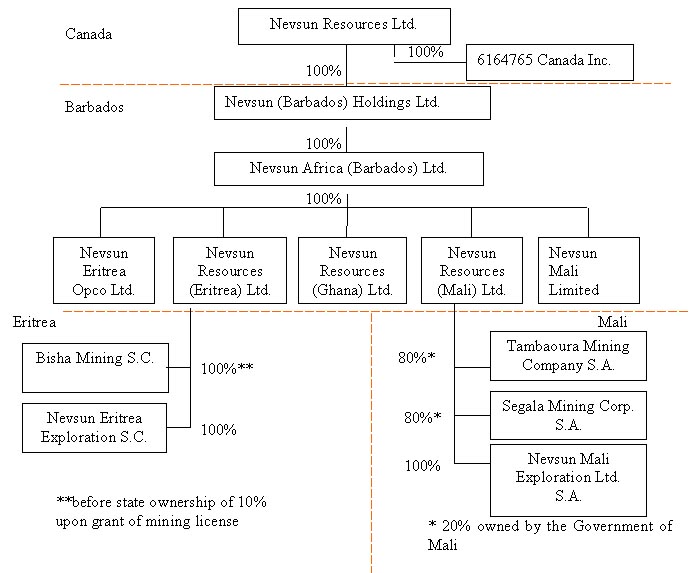

CORPORATE STRUCTURE

1.1

Name and Incorporation

The head office of Nevsun Resources Ltd. (“Nevsun” or the “Company”) is located at 800-1075 West Georgia Street, Vancouver, British Columbia, V6E 3C9 and its registered and records office is located at 1000-840 Howe Street, Vancouver, British Columbia, V6Z 2M1.

The Company was incorporated in British Columbia under theCompanies Act (British Columbia) on July 19, 1965, originally under the name of Hogan Mines Ltd. Since inception the Company has undergone four name changes until December 19, 1991 when it adopted the name of Nevsun Resources Ltd. The Company is now governed by theBusiness Corporations Act (British Columbia).

1.2

Intercorporate Relationships

- 2 -

ITEM 2.

GENERAL DEVELOPMENT OF THE BUSINESS

2.1

Three Year History

The Company is a natural resource company primarily engaged in the acquisition, exploration and development of mineral properties. Currently the Company’s portfolio is focussed on properties in Africa with gold and base metal (copper and zinc) resources/reserves. Most recently the Company has commenced the commissioning of its first gold mine in Mali.

The Company’s principal mineral properties include the Tabakoto/Segala properties located in Mali, West Africa, and the Bisha property located in Eritrea, North-East Africa. Certain less significant exploration properties are located in Mali, Ghana and Eritrea. The following is a description of the general development of the Company’s business during the past three years.

The development of the Tabakoto mine, significant mineral discoveries in Eritrea, together with the funding of the Company’s operations, have had a significant impact on the level of activity during this period. In 2003 and 2005 a series of equity issues raised approximately $120 million to allow the advancement of its projects in Mali and Eritrea.

Mali

In Mali, after a number of years of extensive exploration on the Tabakoto/Segala properties, in 2002/2003 the Company initiated a feasibility study prepared by an independent engineer, for the purpose of taking the project into development and production. The feasibility study was delivered to the Company in late 2002 and during 2003 the feasibility study was updated and the Company initiated arrangements for financing the Tabakoto mine.

During 2004 and 2005 the Company’s principal activity in Mali was the construction of the Tabakoto mine. The construction contract for Tabakoto was awarded in May 2004 and construction carried on throughout 2005 with commissioning of the mine commencing in February 2006. Full commercial production is anticipated during Q2 2006.

Eritrea

During 2003 the Company continued extensive exploration on its Bisha property, a significant high-grade gold, copper, zinc VMS (volcanogenic massive sulphide) discovery. Work in 2003 included drilling, an airborne geophysical survey, and EM, mag, and gravity ground geophysical surveys. By July 2004 the Company had drilled the original Bisha Main discovery to 25m centers along a 1200m strike of its extensive VMS structure. The Bisha Main high grade gold oxide, supergene copper, and primary sulphide resources were published in October 2004.

During September 2004 a temporary stop-work order for all mineral exploration in the country was issued by the Government of Eritrea however by January 2005 the Company had recommenced work with full support of the Government.

In February 2005 the Company engaged an independent engineer, AMEC Americas, to carry out a scoping study for the Bisha Project, and in this regard the Bisha Technical report was delivered by AMEC in December 2005. This scoping study identified a robust economic project over at least 10 years. AMEC is currently engaged to complete the detailed feasibility study and the

- 3 -

environmental impact assessment for Bisha both of which are expected to be completed in the second half of 2006. In January 2006 an improved updated resource estimate was delivered to the Company from AMEC.

Ghana

In Ghana the Company’s main interest is the Kubi property, which since 1999 has been under an arrangement with Anglogold Ashanti Ltd. whereby the Company transferred the surface rights to Anglogold Ashanti in exchange for cash and an ongoing royalty. Anglogold Ashanti obtained a mining license and commenced mining the property in 1999. In 2000, Anglogold Ashanti suspended operations awaiting a grant to access within a forestry reserve area. Anglogold Ashanti received permission by the Government to recommence mining of the Kubi property during 2004 and resumed surface mining throughout 2005 until early 2006 when it advised the Company that it will return the property to the Company after clearing all environmental requirements.

The Company currently holds the underground rights to the Kubi property and the surface rights are expected to be returned to the Company later in 2006.

2.2

Significant Acquisitions

During 2005 the Company was not involved in any significant acquisitions.

ITEM 3.

DESCRIPTION OF THE BUSINESS

3.1

General

A general description of the business is also contained under item 2.1 of this AIF.

During 2004/2005 the Company was heavily involved with the construction of the Tabakoto mine in Mali. After some delays and cost overruns, the Tabakoto mine is now undergoing commissioning, with full commercial production anticipated during Q2 2006.

During 2005 the Company added management and staff to all aspects of its operations. Corporately, a chief operating officer was added in August, as was a general manager for the Eritrea operations. Operating mine management was added for the Mali operations in preparation for production. At the end of 2005 the Company had ten employees in Canada and over two hundred employees in Africa. In addition, the Company also employed several additional temporary project related staff and consultants in order to carry out its seasonal exploration and development programs.

3.2

Risk Factors

The operations of the Company are highly speculative due to the high-risk nature of its business, which is the acquisition, financing, exploration and development of mineral properties. The risks below are not the only ones facing the Company. Additional risks not currently known to the

- 4 -

Company, or that the Company currently deems immaterial, may also impair the Company’s operations. If any of the following risks actually occur, the Company’s business, financial condition and operating results could be adversely affected.

Exploration risk. Exploration for mineral deposits involves significant risk that even a combination of careful evaluation, experience and knowledge may not eliminate. It is impossible to ensure that the Company’s exploration programs will establish economically recoverable reserves.

Development risk. Mineral property development is a speculative business and involves a high degree of risk. The marketability of natural resources that may be acquired or discovered by the Company will be affected by numerous factors beyond its control. These factors include market fluctuations, the proximity and capacity of natural resource markets and processing equipment, and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in the Company not receiving an adequate return on invested capital.

Infrastructure risk. Mining, processing, development and exploration activities depend, to some degree, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important determinants which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect the Company’s operations, financial condition and results of operations.

Commodity price risk. The price of gold and other metals can and has experienced volatile and significant price movements over short periods of time, and is affected by numerous factors beyond the control of the Company, including international economic and political trends, expectations of inflation, currency exchange fluctuations (specifically, the U.S. dollar relative to other currencies), interest rates, global or regional consumption patterns, speculative activities and increased production due to improved mining and production methods. The supply of and demand for metals are affected by various factors, including political events, economic conditions and production costs, and governmental policies.

Reserve and resource estimate risk. The figures for reserves and resources presented herein are estimates, and no assurance can be given that the anticipated tonnages and grades will be achieved or that the indicated level of recovery will be realized. Market fluctuations in the price of mineral commodities or increases in the costs to recover minerals may render the mining of ore reserves uneconomical and require the Company to take a write-down of the asset or to discontinue development or production. Moreover, short-term operating factors relating to the reserves, such as the need for orderly development of the ore body or the processing of new or different ore grades, may cause a mining operation to be unprofitable in any particular accounting period.

Proven and probable reserves were calculated based upon a gold price of $325 per ounce and measured and indicated resources were calculated based upon a gold price of $325 per ounce. Prolonged declines in the market price of gold may render reserves containing relatively lower

- 5 -

grades of gold mineralization uneconomic to exploit and could reduce materially the Company’s reserves and resources. Should such reductions occur, material write downs of the Company’s investment in mining properties or the discontinuation of development or production might be required, and there could be material delays in the development of new projects, increased net losses and reduced cash flow.

There are numerous uncertainties inherent in estimating quantities of mineral reserves and resources. The estimates in this short form prospectus are based on various assumptions relating to metal prices and exchange rates during the expected life of production, mineralization of the area to be mined, the projected cost of mining, and the results of additional planned development work. Actual future production rates and amounts, revenues, taxes, operating expenses, environmental and regulatory compliance expenditures, development expenditures and recovery rates may vary substantially from those assumed in the estimates. Any significant change in these assumptions, including changes that result from variances between projected and actual results, could result in material downward or upward revision of current estimates.

Operating risk. Mining operations generally involve a high degree of risk. Hazards such as unusual or unexpected formations and other conditions are involved. The Company may become subject to liability for pollution, cave-ins or hazards against which it cannot insure or against which it may elect not to insure. The payment of such liabilities may have a material, adverse effect on the Company’s financial position.

Ownership risk. There is no guarantee that title to the properties in which the Company has an interest will not be challenged or impugned. These properties may be subject to prior unregistered agreements or transfers and title may be affected by undetected defects. There is no guarantee that any of the prospecting licences or exploration permits granted in connection with the properties will be renewed upon their normal expiry. If the Company fails to meet its contractual obligations with respect to a property, it may lose its rights or interests in the particular property.

Political risk. The Company’s material properties are located in Mali and Eritrea and may be subject to sovereign risks, including political and economic instability, government regulations relating to mining, military repression, currency fluctuations and inflation, all or any of which may impede the Company’s activities in those countries or may result in the impairment or loss of part or all of the Company’s interest in one or all of the properties.

The Company temporarily withdrew from active operations in Eritrea from mid-2000 to mid-2002 as a result of a border conflict between Ethiopia and Eritrea.

Although it appears to be an isolated incident, in April 2003 a geologist engaged by the Company was killed while carrying out mapping activities near the Bisha property. The government of Eritrea considered this to be an act of terrorism. The government has increased security around the Company’s operations but acts of violence could re-occur.

In September 2004 a temporary stop work order for all mineral exploration in the country was issued by the government of Eritrea. In January 2005 the order was lifted and the Company re-commenced operations with full government support.

- 6 -

Funding risk. Additional future funds may be required for further exploration programs, or if such exploration programs are successful, for the development of economic ore bodies and the placing of them in commercial production. Historically, the only sources for such funds has been the sale of equity capital and limited debt. There is no assurance that sources of financing will be available on acceptable terms or at all.

Share price risk. The market price of a publicly traded stock, particularly a junior resource issuer like the Company, is affected by many variables not directly related to the success of the Company, including the market for all junior resource sector shares, the breadth of the public market for the stock, and the attractiveness of alternative investment. The affect of these and other factors on the market price of the Common Shares on the exchanges in which the Company trades suggests that the Company’s shares will be volatile. The Company’s shares have traded in a range between Cdn $0.12 and Cdn $9.25 in the last four fiscal years.

Foreign operation risk. The Company conducts operations through foreign subsidiaries with operations in Barbados, Mali, Eritrea and Ghana, and substantially all of its assets are held in such entities. Accordingly, any limitation on the transfer of cash or other assets between the parent corporation and such entities, or among such entities, could restrict the Company’s ability to fund its operations efficiently. Any such limitations, or the perception that such limitations may exist now or in the future, could have an adverse impact on the Company’s valuation and stock price.

Currency risk. At present all of the Company’s activities are carried on outside of Canada. Accordingly, it is subject to risks associated with fluctuations of the rate of exchange of the Canadian dollar and foreign currencies.

Environmental risk. The Company’s operations may be subject to environmental regulations promulgated by the governments in the countries in which it operates from time to time. Environmental legislation provides for restrictions and prohibitions on spills, releases or emissions of various substances produced in association with certain mining industry operations, such as seepage from tailings disposal areas that could result in environmental pollution. A breach of such legislation may result in the imposition of fines and penalties. In addition, certain types of operations require the submission and approval of environmental impact assessments. Environmental legislation is evolving in a manner that means standards and enforcement, fines and penalties for non-compliance are more stringent. Environmental assessments for proposed projects carry a heightened degree of responsibi lity for companies, directors, officers and employees. The cost of compliance with changes in government regulations has the potential to reduce the profitability of operations. The Company intends to fully comply with all environmental regulations in the countries in which the Company has operations and comply with prudent international standards.

Key executive risk. The Company is dependent on the services of key executives, including its President and Chief Executive Officer and a small number of highly skilled and experienced executives and personnel. Due to the relatively small size of the Company, the loss of these persons or the Company’s inability to attract and retain additional highly skilled employees may adversely affect its business and future operations.

- 7 -

Competition risk. The mineral exploration and mining business is competitive in all of its phases. The Company competes with numerous other companies and individuals, including competitors with greater financial, technical and other resources than the Company, in the search for and the acquisition of attractive mineral properties. The ability of the Company to acquire properties in the future will depend not only on its ability to develop its present properties, but also on its ability to select and acquire suitable properties for mineral exploration or development. There is no assurance that the Company will continue to be able to compete successfully with its competitors in acquiring such properties or prospects on terms it considers acceptable, if at all.

Mineral Properties

The Company has two material mineral properties, the Tabakoto/Segala properties located in Mali and the Bisha property located in Eritrea. The Tabakoto and Segala properties are separate but contiguous holdings and are considered by management as one Tabakoto/Segala mining project because all ore from the Segala property will be processed through the Tabakoto plant. Technical reports on these properties are incorporated by reference in this AIF and may be accessed on SEDAR on the internet atwww.sedar.com (see Preliminary Notes at the beginning of this AIF).

3.3

Tabakoto / Segala, Mali

The following summary should be read in conjunction with the Tabakoto and Segala Technical Reports.

Tabakoto

In early 2003 the Company completed an infill drilling program and commissioned Snowden to update its resource estimate for Tabakoto alone, which was completed in March 2003 and detailed in the report “Tabakoto Gold Deposit, 2003 Update to Northern Extension Area Resource”. The results of the updated resource estimate are the subject of the Tabakoto Technical Report. The Company has carried out exploration work in the Tabakoto area of southwestern Mali, West Africa since 1993. The Tabakoto area was an area of intense local artisan mining activity for a number of years. A number of exploration permits were converted to an exploitation permit in late 1999 and revised in 2002, and the exploitation licensed area currently consists of 60 square kilometers.

Past work has consisted of geological mapping, soil sampling, geophysical surveys, diamond drilling and reverse circulation drilling. Several resource estimates have been calculated and a pre-feasibility study was first prepared in 1998. Independent consultants have documented all of this work and reports are available at the Company’s corporate office in Vancouver.

The Tabakoto gold deposit is a high grade/low volume, structurally controlled, porphyry and quartz vein associated orebody, outlined through definition drilling programs along a strike length of 1650 meters to a subsurface depth of 350 meters.

- 8 -

The deposit occurs within the core of a tight, upright anticline (or anticline couple), whose axial surface dips steeply (70°-85°) eastward. The folded metasediments are monotonously intermixed such that no distinct marker units exist, and the anticline is defined strictly by common sedimentary facing directions. A suite of meter to decameter scale, intermediate to felsic (+/- quartz) feldspar-porphyritic dykes cuts the folded sequence along the length of the core of the anticline. The porphyritic dykes are concentrated within two main intrusive corridors in the northern portion of the deposit, namely a western corridor (15-30 meters wide) dominated by intermediate (diorite, quartz diorite) dykes and an eastern corridor (20-75 meters wide) dominated by felsic dykes. The corridors are generally about 40 meters apart (up to 80 meters in the north) and merge into one principal cor ridor (50-110 meters wide) in the central part of the deposit. Brittle faults and gabbro-dolerite dykes transect the folded assembly.

The in-situ oxide zone, composed of saprolite with successive mottled clay zone and local laterite, ranges between 6-50 meters thick, and is overlain by a cap of locally lateritized alluvial material between 4-18 meters thick.

The dyke corridors and associated host rocks along the length of the anticlinal axis form the locus of preferential alteration (silicification. sericitization and/or carbonatization), intrusion of narrow (cm to dm scale) gold bearing (+/-albite, carbonate) quartz vein systems, development of quartz crackle vein and quartz flooded breccia zones, and development of fine to medium grained disseminated arsenopyrite with subordinate pyrite and free gold. Visible gold occurs statistically in all lithologies and gold grades range widely owing to a nugget effect. High grade zones of gold mineralization are related to the porphyritic dyke corridors, including the host metasediments, and the zones of alteration and fracturing associated with them, forming a north trending main mineralized zone ranging between 20-50 meters in width along the anticlinal axial trace. Cross and long sections depict a somewhat erratic pattern of h igh grade mineralization, yet infer the presence of moderately south plunging shoots or panels, likely governed by the intersection of brittle structures. NE trending cross structures, such as the major structure that transects the deposit at its south end and other zones cutting the central part of the deposit, also form the locus of porphyritic dyke injection, alteration and gold mineralization.

A mineral resource estimate for Tabakoto in 2003 was prepared by Snowden using multiple indicator kriging to interpolate gold grades from composite drill hole samples into a three-dimensional grade block model constrained by solid models of the mineralization. The estimated mineral resource at Tabakoto, above a cut-off grade of 2.0 g/t, is detailed in the table below. The mineral resource estimates include mineral reserves.

| | | |

Tabakoto Mineral Resource Estimate (2.0 g/t Au cut off) |

Category | Tonnage (000’s) | Au Grade (g/t) | Au (Kg) |

Measured | 3,961 | 5.2 | 20,410 |

Indicated | 4,079 | 5.2 | 21,382 |

Measured + Indicated | 8,040 | 5.2 | 41,791 |

Inferred | 2,656 | 5.6 | 14,905 |

- 9 -

The existing mineral reserve estimate for the Tabakoto deposit is based on the earlier 2002 resource estimate as detailed in the report titled “Tabakoto Gold Deposit Resource Estimation, September 2002”. The estimated Measured and Indicated resource at Tabakoto (above a cut-off grade of 2.0 g/t Au) based on the 2002 resource model was 8.1 million tonnes at a grade of 5.1 g/t Au..

For the purpose of reserve estimation, economic cut-off grades of 2.0 g/t Au for oxide ore and 2.2 g/t Au for fresh ore have been applied. The mineral reserves include allowances for dilution (13% at 0.7 g/t Au) and ore loss (1.5%). The open pit mineral reserve estimated presented in the Snowden report titled “Technical Report on the Tabakoto Property, Mali West African”, dated May 2004 is summarized below.

| | | | | | |

Tabakoto Mineral Reserve Estimate ($325/oz) |

Category | Oxide | Fresh | Total |

| | (000) t | g/t Au | (000) t | g/t Au | (000) t | g/t Au |

Proven | 423 | 4.00 | 1,931 | 5.41 | 2,353 | 5.16 |

Probable | 112 | 4.30 | 715 | 6.60 | 828 | 6.28 |

Total | 535 | 4.06 | 2,646 | 5.73 | 3,181 | 5.45 |

Only mineral resources classified as Measured and Indicated were considered as ore in the mining pre-feasibility study, and the inferred resources within the open pit limits were not valued.

Mine production of 3.18Mt, reaching 650,000 tonnes per annum of ore grading 5.45g/t gold to a depth of 210 meters over 5 years at a 2g/t gold cut-off grade should yield approximately 536,747 ounces of gold at an average waste to ore ratio of 15.4:1 with ore and waste totalling 52 Mt.

Segala

The Segala property is contiguous to the Tabakoto property and is subject to its own mining license over a 23 square kilometer area. It was acquired during 2002 at a value of approximately $10.7 million in the form of cash and shares which was paid over the following three years. Past work by former owners consisted of geological mapping, soil sampling, geophysical surveys, diamond drilling and reverse circulation drilling. Several resource estimates were calculated and a pre-feasibility study was prepared by a former owner in 1998.

The Segala gold deposit is a structurally controlled, alteration and mineralization associated deposit within the core of a tight, upright anticline trending ESE (approx. 110°), whose axial surface dips steeply (-80°) south. The folded metasediments (greywackes and argillites) display variable intensities of alteration including chlorite, carbonate, sericite and silica. A series of quartz stringers and veins intrude this package.

Gold mineralization is associated with later, narrow iron carbonate-quartz veins and stringers that intrude the silicified and carbonatized sediments. The veins and stringers usually display somewhat bleached selvages containing coarse to fine grained arsenopyrite crystals and finer disseminated to patchy pyrite (pyrite is also seen to replace arsenopyrite). Many of these

- 10 -

stringers and veins are parallel to local foliation but there are others that are believed to be oriented northeast-southwest as well as north south. To a significantly lesser degree gold is also associated with fractured felsic and intermediate feldspar porphyry dykes. Mineralization appears to plunge steeply to the east.

The Main Zone has been defined over a strike length of at least 600 meters and attains widths of up to 40 meters. Higher grade gold zones occur within the mineralized envelope. The Northwest Zone located to the north and west of the Main Zone does not display the degree of alteration that is seen in the Main Zone. Consequently, the depth of oxidation is in the order of 40-60 meters as opposed to the Main Zone which has depths of oxidation ranging from 5 meters in the east to 25 meters in the west. The degree of iron carbonate and sericite alteration is significantly less and the mineralization associated with quartz veining is more subtle. Quartz veining and stringers are interpreted to trend both northeast, southwest and east west. The strike of the Northwest Zone appears to be parallel to the Main Zone. Northeast striking structures are suspected to play a significant role in emplacement of gold. Graphitic/c arbonaceous zones are noted to carry some gold values.

The mineral resource estimate for Segala was completed by Snowden using multiple indicator kriging to interpolate gold grades from composite drill hole samples into a three-dimensional grade block model constrained by solid models of the mineralization.

The resource is reported within mineralized envelope boundaries and is classified as Measured, Indicated and Inferred according to National Instrument 43-101, as listed in the table below. The Measured and Indicated resource estimated for the Segala deposit is 7.5 Mt at 3.36 g/t Au (based on a cut-off grade of 2.0 g/t Au). The Inferred resource is 1.2 Mt at 2.84 g/t Au (based on a cut-off grade of 2.0 g/t Au). The mineral resource figures include mineral reserve estimates.

| | | |

Segala Mineral Resource Estimate 2.0g/t Au cut-off |

Category | Tonnes | Au | Au |

| | Mt | g/t | kg |

Measured | 3.3 | 3.34 | 11,132 |

Indicated | 4.2 | 3.37 | 14,273 |

Measured + Indicated. | 7.5 | 3.36 | 25,405 |

Inferred | 1.2 | 2.84 | 3,414 |

The Segala mineral reserve estimate by Snowden has been generated on the premise that the Segala open pit will be mined following the exhaustion of the Tabakoto open pit as an extension to the Tabakoto pit mine life. The Segala mineral reserve estimate is therefore dependent upon a Tabakoto mining operation, as discussed under section 3.4 above.

Mineral reserve estimates are based on $350/oz and $325/oz gold prices presented in the report titled “Technical Report on the Segala Property, Mali West Africa”, dated May 2004 and are summarized in the tables below. The mineral reserves include allowances for dilution (8% at 0.0 g/t Au) and ore loss (1.5%). Cut-off grades of 1.65 g/t Au ($350/oz) and 1.75 g/t Au ($325/oz) have been assumed.

- 11 -

| | | | | | |

Segala Mineral Reserve Estimate - $350/oz Au |

| | Oxide | Fresh | Total |

| | Tonnage | Grade | Tonnage | Grade | Tonnage | Grade |

Category | t’000s | g/t Au | t’000s | g/t Au | t’000s | g/t Au |

Proven | 303 | 2.40 | 2,588 | 2.96 | 2,891 | 2.90 |

Probable | 27 | 2.21 | 1,060 | 3.23 | 1,088 | 3.20 |

Total | 331 | 2.38 | 3,648 | 3.04 | 3,979 | 2.98 |

Waste | 9,166 | | 31,056 | | 40,222 | |

| | | | | | |

Segala Mineral Reserve Estimate - $325/oz Au |

| | Oxide | Fresh | Total |

| | Tonnage | Grade | Tonnage | Grade | Tonnage | Grade |

Category | t’000s | g/t Au | t’000s | g/t Au | t’000s | g/t Au |

Proven | 280 | 2.47 | 2,271 | 3.04 | 2,551 | 2.98 |

Probable | 21 | 2.35 | 682 | 3.21 | 703 | 3.19 |

Total | 301 | 2.46 | 2,953 | 3.08 | 3,254 | 3.02 |

Waste | 7,903 | | 21,908 | | 29,810 | |

The reserves detailed are based on a pre-feasibility study examining the economics of the project assuming a capital investment of $1.84 M to expand the nearby Tabakoto tailings facility and upgrade the haul road between the properties. It is planned to process Segala ore through the Tabakoto process plant at a rate of 870 Ktpa.

The reserves noted above were used to complete a life of mine schedule that in turn was used as a basis for financial analysis. The financial analysis indicated positive project economics at gold prices in excess of $350/oz and $325/oz.

During 2003 the Company hired key project management and engaged an independent engineer to complete the detailed engineering for the plant. In early 2004 the Company commenced building infrastructure required for the project.

In May 2004 the Company proceeded with the construction of the Tabakoto mine. Construction took place over the ensuing twenty-one months, encountering a variety of project management, contractor and supply difficulties. The construction period took seven months longer than originally anticipated and as a result was significantly over its original construction budget. To December 31, 2005 the Company had spent $60 million on the construction in progress and a further $9 million on mobilization and pre-strip mining. Management now expects the pre-commercial production costs for the 23 month build and commissioning period to be approximately $69 million for construction of the plant, of camp and facilities infrastructure, and of country overheads. In addition to the $69 million, the Company expects to have incurred $17 million for pre-stripping, mobilization of the mining fleet and mining prior to commercia l production.

- 12 -

The financial implications of the work undertaken during 2004 and 2005 on the Tabakoto property is displayed in notes 4 and 5 to the audited financial statements for the year ended December 31, 2005. In addition, the Company’s Management Discussion & Analysis for the year provides general descriptions of the work carried out.

1. Project Description & Location

The Tabakoto and Segala Technical Reports provide detailed descriptions of the project and location.

2. Accessibility, Climate, Local Resources, Infrastructure and Physiography

The Tabakoto and Segala Technical Reports provide detailed descriptions of the accessibility, climate, local resources, infrastructure and physiography.

3. History

The Tabakoto and Segala Technical Reports provide detailed descriptions of the property history.

4. Geological Setting

The Tabakoto and Segala Technical Reports provide detailed descriptions of the geological setting for the property.

5. Exploration

The Tabakoto and Segala Technical Reports provide detailed descriptions of the exploration carried out on the property.

6. Mineralization

The Tabakoto and Segala Technical Reports provide detailed descriptions of mineralization.

7. Drilling

The Tabakoto and Segala Technical Reports provide detailed descriptions of the drilling carried out on the property.

8. Sampling and Analysis

The Tabakoto and Segala Technical Reports provide detailed descriptions of the sampling and analysis procedures carried out.

9. Security of Samples

The Tabakoto and Segala Technical Reports provide detailed descriptions of the security procedures taken over the samples.

10. Mineral Resource and Mineral Reserve Estimates

In addition to details above, the Tabakoto and Segala Technical Reports include the details of the independent resource and reserve estimates prepared by Snowden.

11. Mining Operations

- 13 -

The Tabakoto plant is presently in the commissioning process and is expected to be in full commercial production during Q2 2006. The mine is an open pit operation and mining commenced in late 2005. The plant is a carbon leach facility with a capacity of 650,000 tonnes annual mill throughput. The estimated production is approximately 100,000 ounces of gold per year scheduled over an initial five years for Tabakoto plus an additional four years for the Segala deposit. The Company has not entered into any hedge contracts in respect to anticipated gold production from the Tabakoto / Segala project.

12. Exploration and Development

While no material exploration programs are contemplated for Tabakoto/Segala in 2006, the Company will be re-evaluating when to commence the Segala open pit mining for processing through the Tabakoto plant and also intends to commence re-evaluating the underground potential for both Tabakoto and Segala.

3.4

Bisha, Eritrea

The following is a summary only and should be read in conjunction with the Bisha Technical Reports.

Work in 2005 consisted of the following:

1.

establishing an extensive line grid over an area centered on the Harena deposit area;

2.

geophysical surveying using Pulse EM , horizontal loop EM and magnetometer as well as detailed gravity surveys corrected for topographic effects using a differential GPS unit that has sub-centimeter accuracy;

3.

detailed geological mapping and sampling and petrographic studies on selected areas;

4.

prospecting of outside AEM defined target areas;

5.

soil sampling; a total of 11,292 samples have been collected on the Bisha property to the end of 2005

6.

trenching over the Bisha deposit area;

7.

extensive infill diamond drilling conducted on the Bisha deposit during 2005 on sections spaced 12.5 m apart and also additional holes on the 25 m spaced sections. Drilling has defined the mineralization over a strike length of 1,100 meters to an average depth of approximately 200 meters, and a maximum depth of 375 meters;

8.

limited diamond drilling of the Northwest Zone;

9.

expanding the permanent exploration camp.

Exploration drilling in 2005 in-filled the Bisha deposit for over 1.1 km of strike length in a north - south trend. The deposit consists of one very large massive sulphide lens, which can be traced the entire length of the deposit, and two separate smaller lenses of massive sulphides occurring to the west. The large lens forms the eastern arm of a south-plunging antiform, with several minor antiform-synform couples located to the west. This antiform occurs within a larger antiform of regional extent. The massive sulphide deposit outcrops as a gossan at the north end and becomes covered by alluvial material to the south.

- 14 -

Another separate zone of massive sulphides, Harena, was discovered in early 2005 approximately 9.0 km southwest of the Bisha deposit. At this time, it is interpreted that both the Northwest Zone deposit and the Harena deposit occur on the same horizon as the Bisha deposit.

Host rocks to the Bisha deposit include a suite of bimodal pyroclastic volcanics and associated volcano-sedimentary rocks. The volcanics are generally felsic in composition, but in the immediate vicinity of the deposit grade from more intermediate in the east, to intermediate-felsic, to felsic in the west. The felsic pyroclastic volcanic rocks include lapilli and ash fall tuffs, blocky tuffs, and debris flows, plus more massive units that appear to be flows. All units are cut by several generations of thin intermediate to felsic dykes.

In October 2004 AMEC (Perú) S.A. provided a mineral resource estimate for the Bisha deposit.

Summary of the Bisha Resource Estimate (Brisebois, 2004)

| | | | | | | |

Category | Zone | Cut-off | Tonnes (000’s) | Au g/t | Ag g/t | Cu % | Zn % |

Indicated | Oxides (all domains) | 0.5g/t Au | 4,984.1 | 6.51 | 30.0 | 0.10 | 0.08 |

| | Supergene Cu | 0.5% Cu | 7,644.8 | 0.46 | 35.56 | 3.47 | 0.87 |

| | Primary | 2.0% Zn | 1,711.5 | 0.74 | 29.59 | 0.97 | 3.07 |

| | Primary Zn | 2.0% Zn | 8,413.3 | 0.76 | 58.27 | 1.12 | 9.04 |

| | Total tonnes | | 22,753.7 | | | | |

Inferred | Oxides (all domains) | 0.5g/t Au | 122.0 | 3.34 | 18.2 | 0.12 | 0.07 |

| | Supergene Cu | 0.5% Cu | 185.6 | 0.09 | 30.14 | 3.26 | 1.04 |

| | Primary | 2.0% Zn | 392.0 | 0.75 | 35.20 | 1.24 | 3.03 |

| | Primary Zn | 2.0% Zn | 5,150.9 | 0.70 | 59.67 | 0.84 | 8.28 |

| | Total tonnes | | 5,850.5 | | | | |

Other targets on the Bisha Property include the Northwest Zone and Harena deposits. Both have been subjected to a limited amount of drilling and neither deposit is fully defined. A total of 36 holes have tested the Northwest Zone over a strike length of 550 meters and to a maximum depth of approximately 200 meters. In 2005, 22 of the 36 holes were drilled and significant intersections included hole NW-008 that intersected 22.1 meters grading 0.25 g/t Au, 54.7 g/t Ag, 1.42% Cu and 4.67% Zn. Additional drilling is required to fully define the extent and overall grade of this deposit before a mineral resource estimate can be completed..

The Harena deposit is 9 km southwest of the Bisha deposit and has a limited surface gossan with associated geochemical and geophysical anomalies.

A total of 20 holes have tested the Harena deposit along a strike length of 400 meters and to a maximum depth of 175 meters. Significant intersections include hole H-011 that intersected 22.4 meters grading 0.34 g/t Au, 20.9 g/t Ag, 0.85% Cu and 3.58% Zn. Additional drilling is required to fully define the extent and overall grade of this deposit.

- 15 -

AMEC Americas Ltd. is carrying out a feasibility study on the Bisha Deposit. The ongoing and recommended activities include:

·

Geotechnical assessment of the potential open pit parameters.

·

Metallurgical samples have been collected from the various mineralized domains and test work is underway to assess process options and provide sufficient information for the feasibility study. SGS Lakefield has been retained to complete this test work.

·

Baseline environmental studies, including social and archaeological studies are in preparation for an Environmental Impact Assessment (EIA).

·

A socio-economic assessment is underway.

·

Hydrological studies are underway.

·

Tailings containment system design is underway.

·

Waste and tailings acid generation assessment is underway.

·

Drilling to infill the near-surface resources of the Bisha Main Deposit has been completed. Closer-spaced drilling on sections 12.5 m apart to provide improved confidence and advance a significant portion of the resources to the Measured category has also been completed.

·

An updated resource estimate has been completed.

1. Property Description and Location

The Bisha Technical Report includes detailed descriptions of the property description and location.

2. Accessibility, Climate, Local Resources, Infrastructure and Physiography

The Bisha Technical Report includes detailed descriptions of the accessibility, climate, local resources, infrastructure and physiography.

3. History

The Bisha Technical Report includes descriptions of the history of the property.

4. Geological Setting

The Bisha Technical Report includes descriptions of thegeological setting.

5. Exploration

The Bisha Technical Report includes descriptions of the exploration on the property to the end of 2004. Subsequent exploration work in 2005 on the Bisha property described at the beginning of this section 3.4.

6. Mineralization

The Bisha Technical Report includes detailed descriptions of the mineralization.

- 16 -

7. Drilling

The Bisha Technical Report includes descriptions of the drilling carried out on the property.

8. Sampling and Analysis

The Bisha Technical Report includes detailed descriptions of the sampling and analysis procedures carried out.

9. Security of Samples

The Bisha Technical Report includes detailed descriptions of the security procedures taken with respect to handling and transport of the samples.

10. Mineral Resources and Mineral Reserve Estimates

The Bisha Technical Report includes detailed descriptions of the mineral resource estimate provided by AMEC in October 2004.

11. Exploration and Development

The Eritrean Government imposed a work stoppage lasting from September 2, 2004 until mid January 2005. A significant exploration program continued at Bisha in 2005, including a diamond drill program that commenced in late January.

Scoping Study 2005

AMEC Americas Ltd. (AMEC) was commissioned by Nevsun to carry out a scoping study to evaluate the Bisha project in Eritrea, Africa, based on the mineral resource estimate developed in October 2004. A feasibility study on this property was started by AMEC in February, 2005 and the scoping study report represents an interim statement of the development of the feasibility study which is ongoing.

The AMEC team visited the project site and the cities of Asmara and Massawa in March and April 2005 to determine sites for the process plant and on-site infrastructure; to participate in collecting samples for metallurgical test work; and to complete scoping study level investigations of the available support facilities and contractors for the project. A subsequent visit was made in October 2005 for geotechnical investigations to provide information for equipment selection, building foundations, and sources of aggregate and borrow materials for dam construction.

The mineral resource estimate includes three types of mineralization – oxide, supergene and primary ore – as described in the scoping study. As noted below, the resource estimate has been revised subsequent to the issue of the scoping study and is reproduced under the heading “2006 Resource Estimate - Bisha”.

Metallurgical samples for each type of mineralization, were prepared from core from four drill hole cores. The samples were prepared at S.G.S. Lakefield Research Ltd. (Lakefield) in Ontario, Canada. Cyanide leach tests were carried out on the oxide samples to extract the contained gold and silver. Conventional flotation was used to produce copper concentrate from the supergene samples, and sequential flotation was used to recover the metals in the primary mineralization into copper and zinc concentrates. Based on the test results, the projected metallurgy is shown below.

- 17 -

Scoping Study Metallurgy

| | | | | | |

| | % Au | % Ag | % Cu | % Cu | % Zn | % Zn |

| | Recovery | Recovery | Grade | Recovery | Grade | Recovery |

Bullion from Oxide Ore | 87 | 45 | - | - | - | - |

Cu Conc from Supergene Ore | 42 | 64 | 30 | 85 | - | - |

Cu Conc from Primary Ore | - | - | 25 | 83 | - | - |

Zn Conc from Primary Ore | 5 | 15 | - | - | 55 | 85 |

The portion of the mineral resource estimate contained within the preliminary open pit is shown below and was determined from the projected metallurgy and the operating costs developed by AMEC.

Portion of Mineral Resources within the Preliminary Open Pit

| | | | | |

| | Oxide | Supergene Cu | Primary | Primary Zn | Total/Avg |

Ore Tonnes (Mt) | 4.1 | 6.3 | 3.1 | 7.0 | 20.5 |

Au Grade (g/t) | 7.6 | 1.0 | 0.7 | 0.8 | 2.2 |

Ag Grade (g/t) | 35.8 | 41.1 | 36.2 | 59.2 | 45.4 |

Cu Grade (%) | 0.1 | 4.1 | 1.4 | 1.2 | 1.9 |

Zn Grade (%) | 0.1 | 0.5 | 1.8 | 9.4 | 3.6 |

Au Contained (Moz) | 1.0 | 0.2 | - | 0.2 | 1.5 |

Ag Contained (Moz) | 4.7 | 8.3 | 3.6 | 13.3 | 30.0 |

Cu Contained (Mlb) | 9.3 | 561.9 | 98.5 | 178.9 | 848.7 |

Zn Contained (Mlb) | 6.6 | 69.4 | 125.3 | 1,439.7 | 1,641.0 |

Waste Tonnes (Mt) |

|

|

|

| 84.8 |

Total Material Moved (Mt) |

|

|

| 105.3 | |

Based on the metallurgical test work and the mineral resources contained within the preliminary open pit, a conceptual development plan has been completed for this scoping study. The plan incorporates an open pit mine, process plant, and on-site and off-site infrastructure designed to accommodate a processing rate of 2 Mt/a. The initial project will include a fleet of mining equipment, a gold leach plant and refinery, tailings and water storage dams, water diversion dams to protect the open pit mine, equipment maintenance facilities, an administration building and an operations camp. A flotation plant to treat the supergene ore will be built in the first two years of operation and will be available to process supergene ore in Year 3. In Year 2 of operation, the copper concentrate shipping facility will be constructed in Massawa, the closest seaport, to transport the copper concentrate to off-shore smelters. In Year 5, a zinc flotation plant will be added to the existing plant to treat the primary ore which will be mined from Year 6 onwards and the concentrate shipping facility will be expanded to store and ship zinc concentrate.

- 18 -

The capital and operating cost estimates (in 3rd quarter 2005 US dollars) for the project are shown below.

The results of the financial analysis, including the pre-tax internal rate of return and net present values for 10 years of mine life, are shown below.

The scoping study is based on preliminary information that has not been confirmed and alternatives that have not been studied in detail. The following list of recommendations were provided by AMEC and are ongoing or will be carried out during the feasibility study phase of the project:

·

The mining plan is based on the indicated mineral reserves, included in the Bisha mineral resource estimate. Since the completion of the October 2004 technical report, Nevsun has completed a substantial drilling program. The resource model has been updated with the new data for the feasibility study.

·

The mining schedule has been completed at a high level with a mine plan and schedule to avoid concurrent production and stockpiling of supergene and primary ores, and therefore to minimize oxidation of the sulphides prior to processing. Detailed pit design and sequencing of mining will be studied in the feasibility study phase of the project to confirm the present mine plan, which could have a significant impact on the operating and capital costs of the mine.

·

The evaluation of this project is based on open pit mining. The mine life could be extended by underground mining methods which should be investigated in another study.

·

A trade-off study should be carried out on supergene and primary ore throughput. These ores are much softer than the oxide. With the common crushing and grinding circuits, the comminution rate of the sulphide ores could be doubled to increase revenue.

·

A concentrate market survey should be conducted. The net smelter return (NSR) is based on general smelter terms and conditions, which vary with different smelters. The marketability and NSR of the concentrates may directly affect the viability of the project. Nevsun has commissioned a concentrate market study.

·

The cost of diesel fuel (at US$0.85 per litre f.o.b. project site) has been used in this study. Almost half of the milling costs are for generating diesel-electric power. Lower power costs would have a positive impact on project economics and should be further investigated.

·

The schedule for upgrading the local road from Massawa to Keren, which bypasses the Asmara highland, is being confirmed. If this road can be improved to a two-lane paved road in time for project construction, then transportation time and costs could be reduced along with improved traffic safety.

·

The location of the concentrate shipping facility, for the purpose of the study will be at an existing cement plant, but this should be confirmed. The plant is scheduled to be replaced in the near future.

·

A transportation logistics study is being conducted, covering truck delivery equipment during construction; trucking of consumables and supplies to site during operations; land transport of concentrates from Bisha to Massawa; shipment concentrates to off-shore smelters; and shipment of consumables from North America and Europe to Massawa. Transportation represents a large proportion of consumable costs for the project.

- 19 -

Capital Cost Estimate (US$000)

| | | |

Major Area | Initial | Subsequent | Total Capital |

Mining | 9,300 | - | 9,300 |

Concentrator | 40,800 | 19,100 | 59,900 |

Tailings | 6,700 | - | 6,700 |

Site & Services | 3,400 | - | 3,400 |

Ancillaries | 13,700 | - | 13,700 |

Utilities | 4,700 | - | 4,700 |

Concentrate Shipping Facilities | - | 27,000 | 27,000 |

Subtotal Direct Costs | 78,600 | 46,100 | 124,700 |

Owner’s Costs | 13,000 | - | 13,000 |

Indirect Costs | 38,400 | 6,800 | 45,200 |

Contingency | 25,800 | 5,300 | 31,100 |

Total Capital Costs | 155,800 | 58,200 | 214,000 |

Operating Cost Estimate (US$000)

| | | | | | |

Year | G & A | Mining | Milling | Total | Annual Milling Mt/a | Operating cost (US$/t) |

1 | 5,294 | 10,223 | 37,306 | 52,823 | 2.0 | 26.41 |

2 | 5,094 | 10,364 | 37,306 | 52,764 | 2.0 | 26.38 |

3 | 6,529 | 15,473 | 24,893 | 46,895 | 2.0 | 23.45 |

4 | 6,882 | 15,476 | 25,325 | 47,683 | 2.0 | 23.84 |

5 | 6,882 | 15,482 | 25,325 | 47,689 | 2.0 | 23.84 |

6 | 6,882 | 21,551 | 28,670 | 57,103 | 2.0 | 28.55 |

7 | 6,882 | 21,464 | 28,747 | 57,093 | 2.0 | 28.55 |

8 | 7,245 | 21,542 | 28,747 | 57,534 | 2.0 | 28.77 |

9 | 7,001 | 21,540 | 28,747 | 57,288 | 2.0 | 28.61 |

10 | 7,001 | 27,941 | 35,304 | 70,246 | 2.5 | 28.00 |

Pre-taxInternal Rate of Return & Net Present Values

___ __

Bid Price on

____________Units

Base Case

Case 2

Case 3

30/11/2005

Commodity

Copper

US$/lb

1.05

1.20

1.50

1.99

Gold

US$/oz

400.00

425.00

450.00

495.00

Silver

US$/oz

6.00

6.50

7.00

8.27

Zinc

US$/lb

0.50

0.60

0.70

0.76

Pre-Tax

IRR

%

35.1

44.9

56.3

71.2

- 20 -

NPV 0%

US$M

346.0

554.0

857.0

1,271.0

NPV 10%

US$M

145.0

244.0

389.0

598.0

Payback

Years

1.9

1.7

1.6

1.3

Pre-tax Net Present Value

_____

Discount Rate

Base Case

Case 2

Case 3

Bid Price on

(%)

(US$M)

(US$M)

(US$M)

30/11/2005

0.0

346

554

857

1,271

5.0

224

365

571

861

7.5

181

298

470

716

10.0

145

244

389

598

12.5

117

200

323

502

15.0

93

164

269

424

20.0

57

109

188

305

25.0

31

71

131

221

Note: Payback period is calculated from start of production (following 2 years of capital development). Cash flows occur at the end of each year.

2006 Resource Estimate – Bisha

In January 2006 AMEC (Perú) S.A. released an updated resource estimate based on additional drilling and re-modeling of the deposit carried out in 2005. The change from the 2004 resource estimate is not materially significant.

The most recent resource estimate is based on 310 diamond and 9 reverse circulation pre-collar diamond drill holes covering a strike length of 1,200 metres and to depths varying from surface to 375 metres. These drill holes included infill drilling conducted during 2005. No data from RC holes was utilized.

This resource complies with the CIM Definition Standards on Mineral Resources and Mineral Reserves, as required by National Instrument 43-101.

The Bisha VMS deposit has three distinct mineralized zones, the near surface oxide gold zone, a supergene copper zone and the primary sulphide zones. AMEC have tabulated an additional noteworthy resource within the primary sulphide zone that contains >0.5% copper but < 2% zinc that was not included in the 2004 mineral resource tabulation. This has added significant tonnages and contained metal to the tabulation.

Estimation Methodology

The resource model was created using industry standard techniques. The block grades were estimated within domains based on interpretation of geologic parameters logged in drill holes. Sectional spacings of 12.5 to 25 metres were used for the basic interpretations. The sectional interpretations were subsequently rationalized in plan. Solid (wireframe) models were created from these and became the basis for coding the block model. Grades were estimated using multiple passes of ordinary kriging with search neighborhoods conforming to the geological trend and geostatistical properties of the deposit. All assays with less than 60% core recovery were removed from the database. Restriction of extreme grades was used to remove metal at risk as derived from analyses of the assay distributions. The metal at risk analysis is essentially a Monte Carlo simulation study, the output of which is an amount of metal deeme d to be at a sufficiently high risk to be removed from the resource. High grade search restrictions were employed to remove the metal, helping to ensure that model grades and tonnages will be realized during mining. Calibrated in the Measured and Indicated blocks of the model, approximately 8% of the gold in the oxide horizon, 3% of the zinc in the primary zinc domain, 20% of the silver in the oxide horizon and 5% of the copper in the supergene horizon was removed.

- 21 -

Bulk density in the oxide zones was estimated by averaging the measurements from within the modeled mineralization zones. Within the supergene and primary zones, multiple regression was used to establish a relationship between specific gravity determinations and iron, copper, lead, zinc, sulphur and barium analyses. This relationship was then applied to the model blocks.

Variography and confidence limit analyses were used in conjunction with confidence in geological modeling and database integrity to develop resource classification criteria. Measured resources were defined by drillholes spaced 25 metres apart on 12.5 metre spaced sections. Those portions of the resource drilled with holes spaced 25 metres apart on 25 metre spaced sections were classified as Indicated. Inferred resources were defined to be the remainder of the resource within 50 metres of drilling. All categories of resource material were restricted to the geologically interpreted mineralization domains.

The geologic model was formulated by Nevsun under the supervision of Bill Nielsen, P.Geo. Nevsun’s V.P. of Exploration. Geologic modeling was completed by Nevsun and AMEC. The Bisha QA/QC program used to monitor the accuracy of the assay database was reviewed and verified by AMEC’s Qualified Person, Douglas Reddy, P.Geo. Mr. Reddy made a site visit to the Bisha Property in May 2004. Resource modeling was carried out using Gemcomsoftwareby Steve Blower, P.Geo. of AMEC who is also the QP for the mineral resource estimate.