UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

September 13, 2010

(Date of earliest event reported)

LABORATORY CORPORATION OF

AMERICA HOLDINGS

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 1-11353 | 13-3757370 | ||

| (State or other jurisdiction of Incorporation) | (Commission File Number) | (I.R.S. Employer Identification No.) |

| 358 South Main Street, | ||||

| Burlington, North Carolina | 27215 | 336-229-1127 | ||

| (Address of principal executive offices) | (Zip Code) | (Registrant’s telephone number including area code) |

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| [ ] | Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| [ ] | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| [ ] | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| [ ] | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 7.01 | Regulation FD Disclosure |

Summary information of the Company in connection with the presentation at the Morgan Stanley Global Healthcare Conference on September 13, 2010.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

LABORATORY CORPORATION OF AMERICA HOLDINGS

Registrant

| By: | /s/ F. SAMUEL EBERTS III | |

| F. Samuel Eberts III | ||

| Chief Legal Officer and Secretary |

September 13, 2010

September 13, 2010

New York, NY

Morgan Stanley Global

Healthcare Conference

2

This slide presentation contains forward-looking

statements which are subject to change based

on various important factors, including without

limitation, competitive actions in the marketplace

and adverse actions of governmental and other

third-party payors.

statements which are subject to change based

on various important factors, including without

limitation, competitive actions in the marketplace

and adverse actions of governmental and other

third-party payors.

Actual results could differ materially from those

suggested by these forward-looking statements.

Further information on potential factors that

could affect the Company’s financial results is

included in the Company’s Form 10-K for the

year ended December 31, 2009, and

subsequent SEC filings.

suggested by these forward-looking statements.

Further information on potential factors that

could affect the Company’s financial results is

included in the Company’s Form 10-K for the

year ended December 31, 2009, and

subsequent SEC filings.

Forward Looking Statement

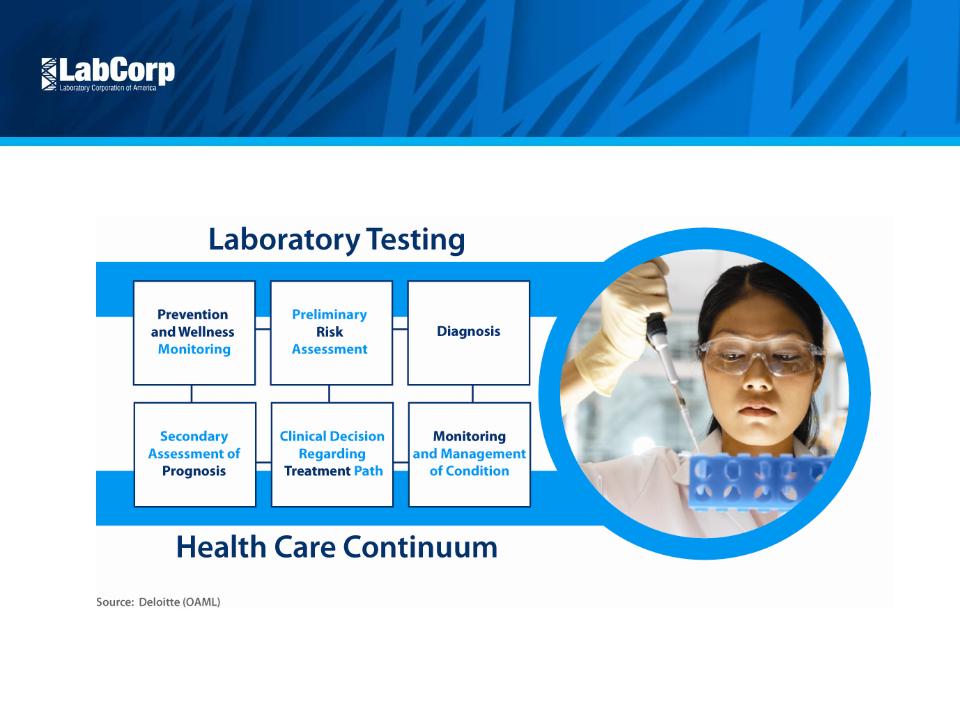

Introduction

3

Leading National

Lab Provider

• Fastest growing national lab

• $55 billion market

• Clinical, Anatomic and Genomic Testing

• Serving clients in all 50 states and Canada

• Foremost clinical trials testing business

Introduction

4

Valuable Service

• Small component of total cost

influences large percentage

of clinical decisions

• Screening, early detection,

and monitoring reduce

downstream costs

• Companion diagnostics

improve drug efficacy and

reduce adverse drug effects

Attractive Market

5

Attractive Market

6

Growth Drivers

• Aging population

• Industry consolidation

• Advances in genomics

• Pharmacogenomics /

companion diagnostics

• Cost pressures

Source: CDC National Ambulatory Medical Care Survey and Company Estimates

Attractive Market

7

Opportunity to

Take Share

• Approximately 5,000

independent labs

• High cost competitors

Source: Washington G-2 Reports and company estimates

$55 Billion US Lab Market

55%

14%

9%

4%

19%

Hospital Affiliated

Quest

LabCorp

Physician Office

Other Independent

Attractive Market

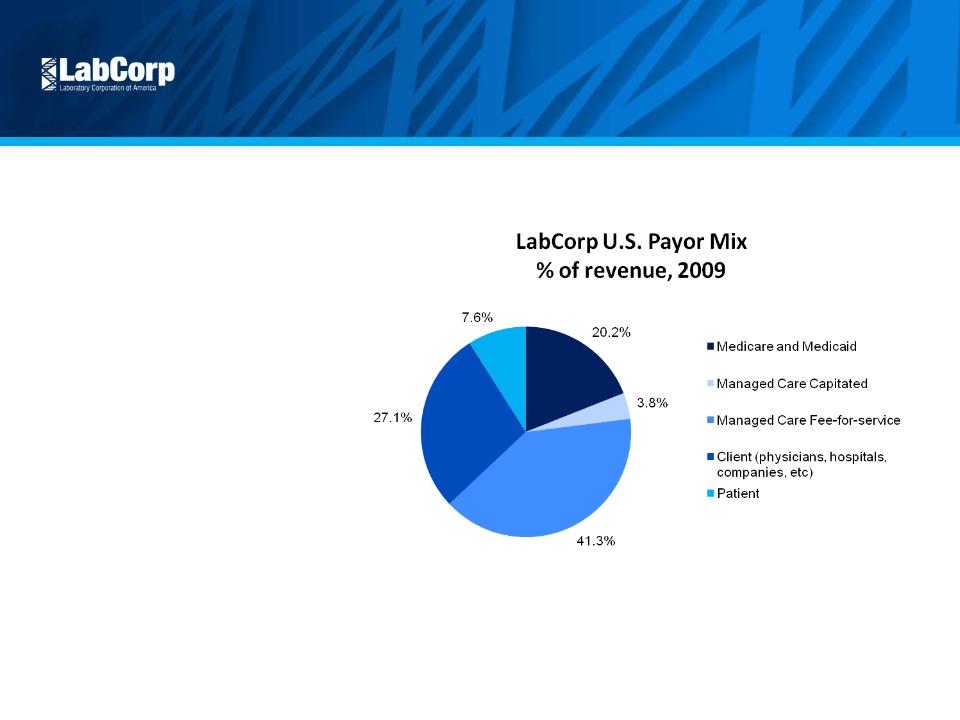

Diversified Payor Mix

• No customer > 9% of revenue

• Limited government exposure

8

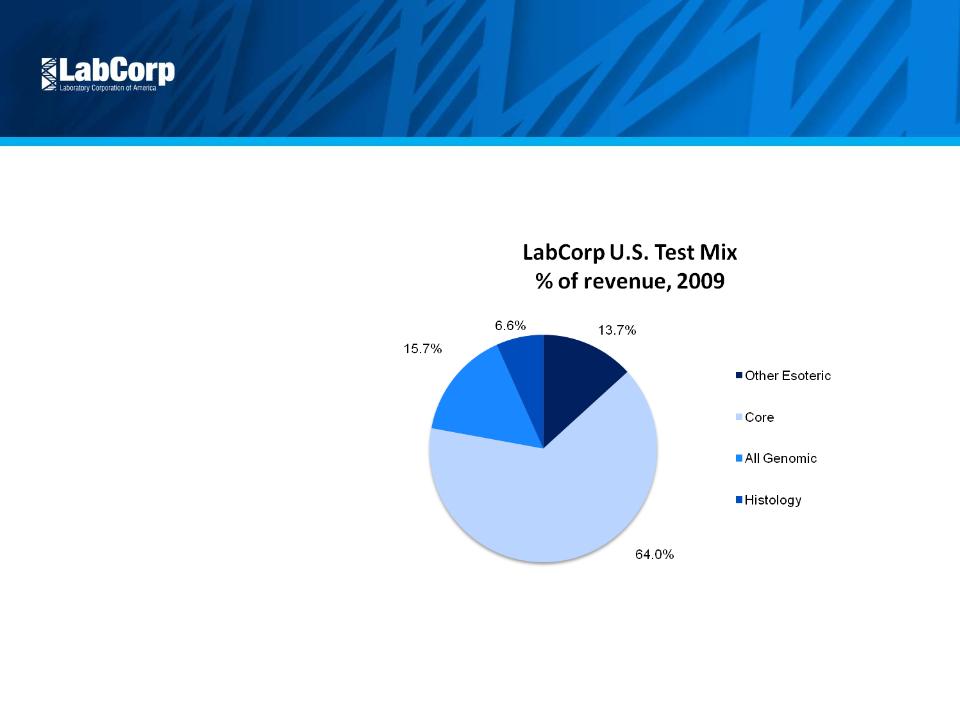

Attractive Market

Diversified Test Mix

• Esoteric 36% of revenue

• Goal of 40% in 3 - 5 years

• Higher priced business

9

Competitive Position

Scale and Scope

• National infrastructure

• Broad test offering

• Managed care contracts

• Economies of scale

10

Primary LabCorp Testing Locations*

Esoteric Lab Locations

(CET, CMBP, Dianon, Esoterix, Monogram Biosciences, NGI, OTS, US Labs, Viromed)

Patient Service Centers*

Competitive Position

11

Managed Care Relationships

• Exclusive national laboratory for UnitedHealthcare

• Sole national strategic partner for WellPoint

• Significant national plans recently renewed or

extended on a multi-year basis, including

WellPoint, Cigna and Humana

• Contracted with numerous local and

regional anchor plans

Scientific

Leadership

• Introduction of new tests

• Acquisitions and licensing

• Collaborations with leading

companies and academic

institutions

Competitive Position

12

Competitive Position

13

Standardized and

Efficient Processes

• Standardized lab and billing

IT systems

• Automation of pre-analytics

• Capacity rationalization

• Logistics optimization

2010 Priorities

14

Our Focus

• Profitable revenue growth

• IT and client connectivity

• Continue scientific leadership

• Maintain price

• Control costs

2010 Accomplishments

15

Our Results

• Profitable revenue growth

• Empire contract

• Esoteric growth

• Acquisitions

• Improved IT and client connectivity

• LabCorp Beacon

• Enhanced experience

for physicians and patients

• Continued scientific leadership

• Clearstone collaboration

• IL-28B

• New Monogram assays

• Maintained price

• Managed care stability

• Strong 1H 2010 results

• Controlled costs

• Gross margin expansion

• Sysmex project

2010 Accomplishments

16

Profitable Revenue Growth

• Empire contract

• In network status as of Aug 1, 2010

• New York’s largest insurer by membership

• Esoteric revenue growth

• 5.1% growth in first half of 2010

• Expansion of Monogram offerings

• Acquisitions

• Westcliff

• DCL

• 3.7% total revenue growth in first half of 2010

• Challenging economic environment

• Positive volume growth, after

adjusting for lost contracts

2010 Accomplishments

17

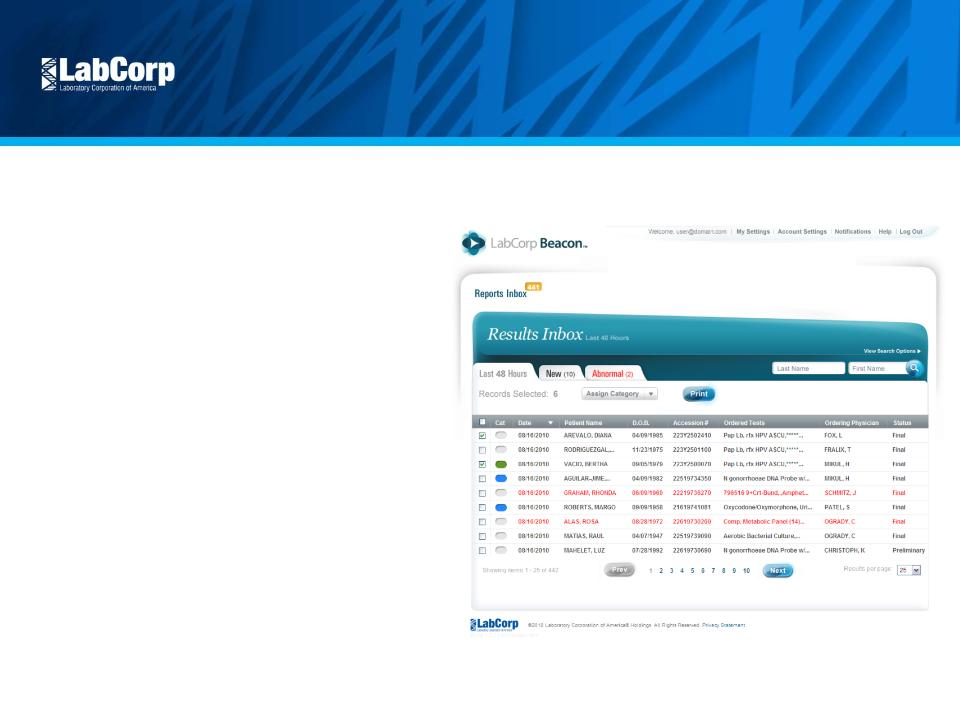

Improved IT and Client

Connectivity

Connectivity

• LabCorp Beacon: A superior physician

experience

• Intuitive Orders and Results

• Unread reports in bold while

abnormal values are displayed in red

abnormal values are displayed in red

• Share results via Email, Fax and Print

• Group patients according to a client’s

needs

needs

• Add notes to any report to share

critical insights

critical insights

2010 Accomplishments

18

• Powerful Analytics

•Graphical views of a patient over

time

time

•Generate trends and averages for

large populations

large populations

2010 Accomplishments

19

“K-RAS testing should be routinely conducted in

all colorectal cancer patients immediately after

diagnosis to ensure the best treatment strategies

for the individual Patient”

all colorectal cancer patients immediately after

diagnosis to ensure the best treatment strategies

for the individual Patient”

- Dr. Eric Van Cutsem, presenter at the June 2008 American

Society of Clinical Oncology meeting

FDA recommends genetic screening prior to

treatment with Abacavir

treatment with Abacavir

ROCKVILLE, Md -- July 24, 2008 -- The US Food and Drug Administration (FDA) has

issued an alert regarding serious, and sometimes fatal, hypersensitivity reactions (HSRs)

caused by abacavir (Ziagen) therapy in patients with a particular human leukocyte antigen

(HLA) allele, HLA-B* 5701.

issued an alert regarding serious, and sometimes fatal, hypersensitivity reactions (HSRs)

caused by abacavir (Ziagen) therapy in patients with a particular human leukocyte antigen

(HLA) allele, HLA-B* 5701.

Genetic tests for HLA-B*5701 are already available, and all patients should be screened for

the HLA-B*5701 allele before starting or restarting treatment with abacavir or abacavir-

containing medications.

the HLA-B*5701 allele before starting or restarting treatment with abacavir or abacavir-

containing medications.

“FDA has approved the expanded use of

Selzentry… to include adult patients with CCR5-

tropic HIV-1 virus who are starting treatment for

the first time.”

Selzentry… to include adult patients with CCR5-

tropic HIV-1 virus who are starting treatment for

the first time.”

- ViiV Healthcare Press Release, November 20th, 2009

Continued Scientific

Leadership

• Clearstone collaboration

• Global clinical trials capability

• Presence in China

• Enhanced offerings in companion

diagnostics and personalized medicine

• IL-28B

• K-RAS

• HLA-B* 5701

• BRAF Gene Mutation Detection

• EGFR Mutation Analysis

• CYP 450 2C19

• Trofile (CCR5 Trophism)

• PhenoSense, PhenoSense GT

• HerMark

• Grew Outcome Improvement Programs

• Relaunch of CKD program

• Litholink kidney stone program

2010 Accomplishments

Maintained Price

• Managed care stability

• Pricing discipline has offset

1.9% Medicare rate decrease

• Promoted high-value tests

• Other recent benefits

• Monogram

• Canadian exchange rate

• Impact from lost government

contracts

20

Controlled Costs

• Y/Y gross margin improvement for

three consecutive quarters

• Sysmex contract

• Fully automated hematology

operations

• One of largest lab automation

projects ever undertaken

• Bad debt reduction of 50bp in

the first half of 2010

• Continued to optimize supply chain

• Used efficiency gains to improve

physician and patient experiences

2010 Accomplishments

21

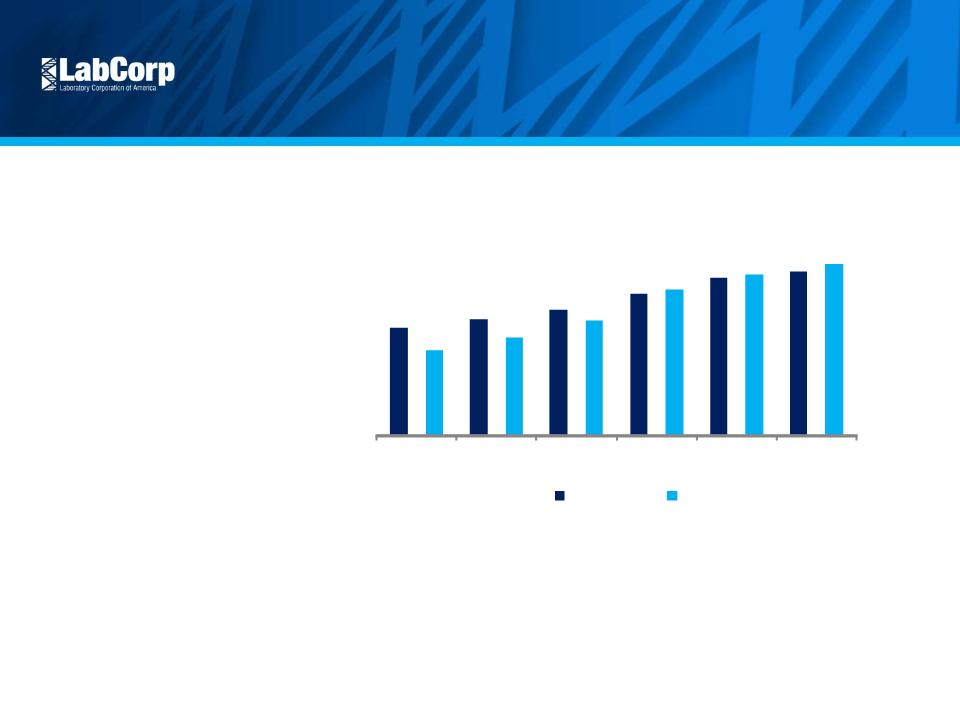

$3,085

$3,328

$3,591

$4,068

$4,513

$4,695

$2.45

$2.80

$3.30

$4.18

$4.60

$4.89

2004

2005

2006

2007

2008

2009

Revenue ($mil)

EPS

Excellent Performance

22

Revenue and

EPS Growth

• 9% Revenue CAGR

• 15% EPS CAGR

(1) Excluding the $0.09 per diluted share impact in 2005 of restructuring and other special

charges, and a non-recurring investment loss; excluding the $0.06 per diluted share

impact in 2006 of restructuring and other special charges; excluding the $0.25 per

diluted share impact in 2007 of restructuring and other special charges; excluding the

(2) EPS, as presented, represents adjusted, non-GAAP financial measures. Diluted EPS,

as reported in the Company’s Annual Report were: $2.45 in 2004; $2.71 in 2005;

$3.24 in 2006; $3.93 in 2007; $4.16 in 2008; and $4.98 in 2009.

$0.44 per diluted share impact in 2008 of restructuring and other special charges; excluding

the ($0.09) per diluted share impact in 2009 of restructuring and other special charges.

Revenue and EPS Growth: 2004 - 2009 (1) (2)

Excellent Performance

23

Leading Returns

• Leading returns

• Leading EBIT margin

18.2%

20.5%

21.8%

27.6%

27.5%

25.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2004

2005

2006

2007

2008

2009

LabCorp ROE 2004

-

2009

Excellent Performance

24

Cash Flow

• 11% FCF CAGR

• $2.0 B+ share repurchase

over last three years

Note: $ in Millions

Second Quarter and YTD 2010 Results

25

Three Months Ended Jun 30, | Six Months Ended Jun 30, | |||||||||||

2010 | 2009 | +/(-) | 2010 | 2009 | +/(-) | |||||||

Revenue (1) | $ 1,238.4 | $ 1,188.8 | 4.2% | $ 2,432.0 | $ 2,344.5 | 3.7% | ||||||

Adjusted Operating Income | $ 270.5 | $ 254.9 | 6.1% | $ 514.0 | $ 495.4 | 3.8% | ||||||

Adjusted Operating Income Margin | 21.8% | 21.4% | 40 | bp | 21.1% | 21.1% | - | bp | ||||

Adjusted EPS (1) | $ 1.46 | $ 1.30 | 12.3% | $ 2.76 | $ 2.51 | 10.0% | ||||||

Operating Cash Flow | $ 216.2 | $ 182.4 | 18.5% | $ 448.2 | $ 391.3 | 14.5% | ||||||

Less: Capital Expenditures | $ (34.5) | $ (23.7) | 45.6% | $ (59.0) | $ (54.4) | 8.5% | ||||||

Free Cash Flow | $ 181.7 | $ 158.7 | 14.5% | $ 389.2 | $ 336.9 | 15.5% | ||||||

(1) During the first quarter inclement weather reduced revenue by an estimated $23 million and EPS by approximately eight cents | ||||||||||||

Reconciliation of Non-GAAP Financial Measures

26

Reconciliation of non-GAAP Financial Measures | ||||||||

(In millions, except per share data) | ||||||||

Three Months Ended June 30, | Six Months Ended June 30, | |||||||

2010 | 2009 | 2010 | 2009 | |||||

Adjusted Operating Income | ||||||||

Operating income | $ 270.5 | $ 244.7 | $ 504.7 | $ 485.2 | ||||

Restructuring and other special charges | $ - | $ 10.2 | $ 9.3 | $ 10.2 | ||||

Adjusted operating income | $ 270.5 | $ 254.9 | $ 514.0 | $ 495.4 | ||||

Adjusted EPS | ||||||||

Diluted earnings per common share | $ 1.46 | $ 1.24 | $ 2.70 | $ 2.46 | ||||

Impact of restructuring and other special charges (1) (2) | $ - | $ 0.06 | $ 0.06 | $ 0.05 | ||||

Adjusted EPS | $ 1.46 | $ 1.30 | $ 2.76 | $ 2.51 | ||||

(1) After tax impact of restructuring and other special charges for the three months and six months ended June 30, 2010 ($- million divided by | ||||||||

105.4 million shares and $5.7 million divided by 105.9 million shares, respectively) | ||||||||

(2) After tax impact of restructuring and other special charges for the three months and six months ended June 30, 2009 ($6.0 million divided by | ||||||||

109.5 and 109.4 million shares, respectively) | ||||||||

Supplemental Financial Information

27

Laboratory Corporation of America | ||||||||||||

Other Financial Information | ||||||||||||

FY 2009 and Q1/Q2 2010 | ||||||||||||

($ in millions) | ||||||||||||

Q1 09 | Q2 09 | Q3 09 | Q4 09 | Q1 10 | Q2 10 | |||||||

Bad debt as a percentage of sales | 5.30% | 5.30% | 5.30% | 5.30% | 5.05% | 4.80% | ||||||

Days sales outstanding | 52 | 50 | 48 | 44 | 46 | 45 | ||||||

A/R coverage (Allow. for Doubtful Accts. / A/R) | 19.5% | 20.6% | 21.9% | 23.2% | 21.7% | 20.7% | ||||||

Key Points

• Critical position in health care delivery system

• Attractive market

• Strong competitive position - well positioned to gain share

• Leadership in personalized medicine

• Excellent cash flow

• Strong balance sheet

Conclusion

28

©2010 LabCorp. All rights reserved. 8026-0210