PSS World Medical Investor Day Conference June 1, 2006 Atlanta Georgia Exhibit 99.1 |

Robert Weiner Vice President, Investor Relations Investor Day Conference June 1, 2006 Atlanta Georgia * * * * * ******************************************************************************************* ***** ****************************************************************************************** ****** |

Forward-Looking Statements All statements in this presentation that are not historical facts, including, but not limited to, statements regarding anticipated growth in revenue, gross and operating margins, cash flow from operations and earnings, statements regarding the Company’s current business strategy, the Company’s ability to complete and integrate acquired businesses and generate acceptable rates of return, the Company’s projected sources and uses of cash, and the Company’s plans for future development and operations, are based upon current expectations. Specifically, forward-looking statements in this presentation include, without limitation, the Company’s expected results in GAAP EPS, revenue, operating income and operating margins for continuing operations and discontinued operations for both the consolidated company and for each of its businesses in fiscal years 2007 - 2009; the expected operational cash flow in fiscal years 2007 - 2009; the ability to sustain revenue growth and expected growth rates of the marketing programs in its Physician and Elder Care Businesses; expected flu vaccine sales during fiscal year 2007 and subsequent fiscal years; expected sales growth from durable medical equipment, housekeeping, revenues derived from home care, hospice and assisted living customers, expectations for revenue, operating income, operating margin, cash flow from operations and earnings per share for fiscal years 2007 - 2009, as well as other expectations of growth and financial and operational performance. These statements are forward -looking in nature and involve a number of risks and uncertainties. Actual results may differ materially. Among the factors that could cause results to differ materially are the following: pricing and customer credit quality pressures; the loss of any of our distributorship agreements and our reliance on relationships with our vendors; our reliance on a limited number of elder care customers; the availability of sufficient capital to finance the Company’s business plans on terms satisfactory to the Company; competitive factors; the ability of the Company to adequately defend or reach a settlement of outstanding litigations and investigations involving the Company or its management; changes in labor, equipment and capital costs; changes in regulations affecting the Company’s business, such as the Medicare reimbursements and cliffs, changes in malpractice insurance rates and tort reform; future acquisitions or strategic partnerships; general business and economic conditions; and other factors described from time to time in the Company’s reports filed with the Securities and Exchange Commission. Many of these factors are outside the control of the Company. The Company wishes to caution readers not to place undue reliance on any such forward -looking statements, which statements are made pursuant to the Private Securities Litigation Reform Act of 1995 and, as such, speak only as of the date made. The Company also wishes to caution readers that it undertakes no duty or is under no obligation to update or revise any forward-looking statements. |

Investor Day 2006 Building a unique culture of: • Sustainable above market growth • Customer & market focus • Execution & operational excellence |

Meeting Agenda • David Smith President & CEO • Gary Corless COO • David Bronson EVP & CFO • John Sasen CMO & Kevin English SVP, Shared Services • PSSI: We Are Unique • Our Environment • Growth • What Keeps the CEO Up at Night • What is the CEO Focused On • Vision for Our Future • Physician Business: FY 2007 Plan • Elder Care Business: FY 2007 Plan • Financial Performance Review • Financial Goals • Evaluation of Our Brand, Select Medical Products |

David A. Smith President and Chief Executive Officer Investor Day Conference June 1, 2006 Atlanta Georgia |

Investor Day 2006 Building a unique culture of: • Sustainable above market growth • Customer & market focus • Execution & operational excellence |

PSSI: Investors Benefit from our Strategies and Execution -20 20 60 100 140 180 220 260 300 340 380 10/10/00 12/31/01 12/31/02 12/31/03 12/31/04 12/31/05 5/22/06 Prices as of May 22, 2006 PSSI HSIC PDCO MCK CAH |

PSSI : We Are Unique • Performance-driven culture – Balance of customer satisfaction and profitability – Ethics – doing more than legal – doing what is right – Customer, vendor and employee surveys help to guide programs • Stick to the Strengths of Our Business Model – Unique and unparalleled customer service model – Delivery advantage, customer relationship advantage – Innovative programs and technologies • Focus on execution – Alignment of customer, shareholder, employee and vendors’ interests with our 3 – year strategic plan – Focus on core competencies and competitive advantages – Limited by time, talent and money |

5 10 15 20 25 30 35 PSSI: Employer of Choice 30% 26% 17% 16% 17% 15% 8/1/00 3/31/01 3/29/02 3/28/03 4/2/04 4/1/05 12% 4/1/06 % of Employee Turnover |

Focused on Leveraging the Strengths of Our Business Model 1000 1200 1400 1600 1800 FY 03 FY 04 FY 05 FY 06 $1,178 $1,350 $1,474 $1,619 ($ in millions) |

Focused on Execution of our Strategic Plan 0 0.15 0.3 0.45 0.6 0.75 FY 03 FY 04 FY 05 FY 06 $0.12 $0.42 $0.51 $0.66 Earning Per Diluted Share from continued operations 1 1 Excludes non-recurring tax benefit of $5.6 million, or $0.09 per diluted share |

Environment |

Non-durable Medical Product Home Health Care Nursing Home Care Physicians’ Care Admin. and Net Cost of Private Health Insurance Prescription Drugs Hospital Care Source: CMS 1975 Health Expenditures As % of GDP 13.8% 1995 Health Expenditures As % of GDP 14.4% 2005 Health Expenditures As % of GDP 15.5% 2015 Health Expenditures As % of GDP 19.3% National Health Expenditures by type ($bn, chained 2000 dollars) Accelerating to 3x the rate of growth In the next 10 years (2005-2015) compared to previous 10 years (1995-2005 24.5% expected total growth 2005-2015 7.6% actual total growth 1995-2005 US Healthcare Spending is Accelerating Expected to Approach 20% of GDP |

What Do the Experts Say? U.S. Healthcare: • Growth in [health care] spending over the coming decade is projected to average 7.2% a year.” –Wall Street Journal, February 2006 Physicians: • The AMA has forecasted physician market growth to accelerate to 4% - 6% in 2006. • “[The American College of Physicians] has proposed a [federally-based] solution… put primary care doctors in charge of organizing a patient's care and giving patients more responsibility for monitoring their own health and scheduling regular visits.” – Reuters News Service, January 2006 • “According to the American Society for Aesthetic Plastic Surgery (ASAPS)… the largest increase occurred in non-surgical procedures, which grew 51 percent over the previous year.” - Dermatology Times, May 2005 Home Care and Hospice: • “Home Health Agencies and Hospice organizations will see exponential growth over the next two decades”, CMS – January 2006 • Lewin Associates “estimates that for every $1.00 spent on hospice care, approximately $1.50 of spend is avoided in other medical care categories.” Diagnostic products: • “VC’s increase funding for medical-device firms by 25% to 2.11 Billion in 2005.” – Wall Street Journal, March 2006 |

PSSI: Profitable & Sustainable Above Market Growth |

Where are We Focused: FY 2007 • Continued execution of customer-solutions- focused programs • Offensive launch of surgery center programs • Increased sales rep productivity Physician Business: Consistent Performance |

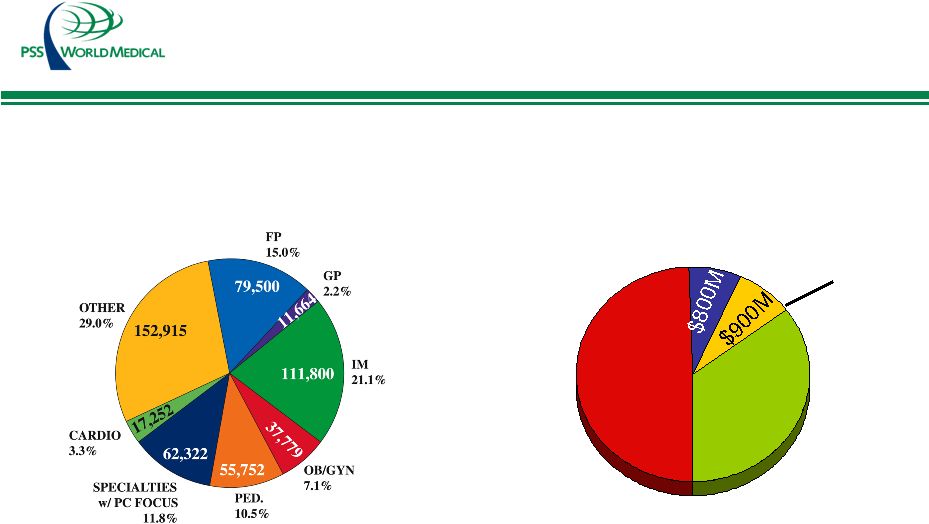

Where Are We Focused: FY 2007 - FY 2009 • We are targeting $3 Billion owned exclusively by practicing physicians – 1,470 Targeted ASC locations; 4,900 total market – 11,500,000 Cosmetic & Non-Surgical Procedures – Medicare payments to ASC’s up 19% in 2005 Physician 83% Non Physician 17% Physician Market: New PSS Opportunity Total Ambulatory Surgery Center Markets: $10.0 Billion |

Where We Are Focused: FY 2007 • Re-align resources & strategies to distinct market segments • Leverage service & delivery model: matched to customers needs • Focus on Select Medical products conversion; and growth of our brand Elder Care Business: Re-Aligning Focus & Resources |

Why Realignment • Shed $110 million of business that did not fit the model • $10 Billion Home Care & Hospice markets have the fastest growth – A better fit to our service model – Less competition – More profit contribution Elder Care Business |

What Keeps Me Up At Night: David Smith, CEO • Sales Rep productivity • IT systems • Reimbursement and U.S. healthcare system |

What Are We Doing About It? $1.0 $1.5 $2.0 $2.5 FY 02 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 ($ in Millions) •Sales Rep Productivity •Training & Development •Solution selling •Automation •New Sales representatives |

What Are We Doing About It? • IT systems – Focus on payoff – Moment of truth impact • Reimbursement and U.S. healthcare system – Financial credit parameters – Focus on gate keeper and patient – Physician market and home care |

What Am I Focused On: David Smith, CEO • Global Sourcing • People • IT systems • Corporate Governance |

$340 Million $340 Million +15%* BRAND IMPORT DIRECT +30%* of purchases, based on today’s volume PSS World Medical opportunity *% of procurement savings Where We Are Focused: FY 2007-FY 2009 Shared Services: Global Product Sourcing |

Where We Are Focused: FY 2007-FY 2009 Shared Services: Global Product Sourcing VP Global Sourcing Tomas D’Innocenzi Admin VP Sourcing Ops JAX Director QA/QC China Sourcing Mgrs: 2 Tiger Specialty Sourcing: 22 LOOP Solution Ltd. (Hong Kong) Quality Control Production Control QA/QC Analyst Sourcing: 3 Logistics: 3 Bus. Analyst SELECT Support: 2 MD Asia (SE Asia):4 Quality Control Production Control 40+ Sourcing Team 5 Marketing Team |

Where We Are Focused: FY 2006 - FY 2008 Shared Services: Global Sourcing 8% Branded 92% 12% Branded 88% Select Medical Product Mix FY 2006 $1.5 Million FY 2008 $10 - $11 Million Pre-Tax Savings: FY 2007 $3.5 – 4.0 Million 10% Branded 90% |

PSSI: CEO’s Vision • Revenue growth 2X the market, with earnings growing faster than revenue • Focused on customers that fit service model • Continued expansion and leadership in Physician market • Meaningful presence in home care and hospice markets • Global sourcing core competency (brand power) • Industry-leading shareholder returns |

Thank You |

Gary A. Corless Chief Operating Officer Investor Day Conference June 1, 2006 Atlanta Georgia ******************************************************************************************* **** ****************************************************************************************** ***** |

Investor Day 2006 Building a unique culture of: • Positioning for growth • Customer & market focus • Execution & operational excellence |

The Physician Business |

The Physician Business: Market Drivers • Office Based Physicians in PSS Market: 528,984 • Total Product Segmentation: $10.4 Billion $5.1B $3.6B Medical & Surgical Pharmaceuticals Injectibles & Vaccines Diagnostic Equipment Non-diagnostic Equipment $ 5.1B |

The Physician Business: Competitive Landscape |

The Physician Business: Unique Value Proposition We offer office - based physicians a clear choice • Customer solutions-focused programs • Industry-leading reliable and efficient delivery services • Personalized sales, services and support • Industry-leading comprehensive diagnostic equipment offering • Biomed services |

The Physician Business: FY 2007 Plan Sales • Focus on Select Medical products conversion and growth • Surgery center market roll-out • Rx focus and roll-out of controlled Rx to PSS field • Continued leverage of industry-leading diagnostic equipment offering |

The Physician Business: FY 2007 Plan Operations • Strengthen delivery advantage • Continuous improvement of customer touch points • Continued focus on driving metrics and performance improvement programs |

The Physician Business: FY 2007 Plan Marketing • Market blitzes • Customized surgery center solutions- based programs • Smartscan growth |

Smartscan: Progress Report Smartscan: • Over 1,200 customers have Smartscan • $919 average order size placed on Smartscan – Compared to: • $738 average order placed on MyPSS.com • $516 average order placed with Customer Service • $427 average order placed on ICON (Sales rep ordering technology) |

Smartscan: Progress Report 0 100 200 300 400 500 600 700 800 900 1000 1100 1200 1300 1400 1500 Oct-05 Nov-05 Dec-05 Jan-06 Feb-06 Mar-06 Net sales ($ In thousands) Number of orders $1,370 1,516 |

The Physician Business: FY 2007 Financial Goals • Revenue growth goal of 11% - 14% • Operating margin goal of 7.0% |

The Elder Care Business |

The Elder Care Business: Targeted Approach HME HSP HHA Skilled Nursing Home Care SNF 16,000 Customers 12,000 Customers 2,500 Customers 110,000 Customers Large Medium Small 15% 61% 17% 69% 79% 8% Target 76% or $3.0 Billion Target 86% or $6.9 Billion Target 87% or $1.1 Billion |

The Elder Care Business: Targeted Value Proposition We offer elder care providers a clear choice: • Service and delivery model matches customer needs • Our programs are matched to needs of Home Health and Hospice agencies • Select Medical Products offer compelling value • Technology systems reduce provider costs |

The Elder Care Business: FY 2007 Plan Sales • Focus on Select Medical Products conversion & growth • Align compensation plans to growth opportunities • Expand sales representative bandwidth Operations • Improved patient home delivery Marketing • Enhance product marketing team • Market blitzes |

The Elder Care Business: Market Blitzes Focused Quarterly Blitzes What: • Q1 - Compensation plan • Q2 - Select Medical products • Q3 - Proclaim • Q4 - Answers Plus Why: • Focus drives results Where: • SNF (Reg & Ind) • HHA (Reg & Ind) Success • Growth in sales Measurements • Growth in profit contribution |

The Elder Care Business: FY 2007 Financial Goals • Revenue goal of 3% - 5% (excluding lost business in FY05) • Operating margin goal of 3.9% |

Thank You |

David M. Bronson Executive Vice President and Chief Financial Officer Investor Day Conference June 1, 2006 Atlanta Georgia |

Investor Day 2006 Building a unique culture of: • Positioning for growth • Customer & market focus • Execution & operational excellence |

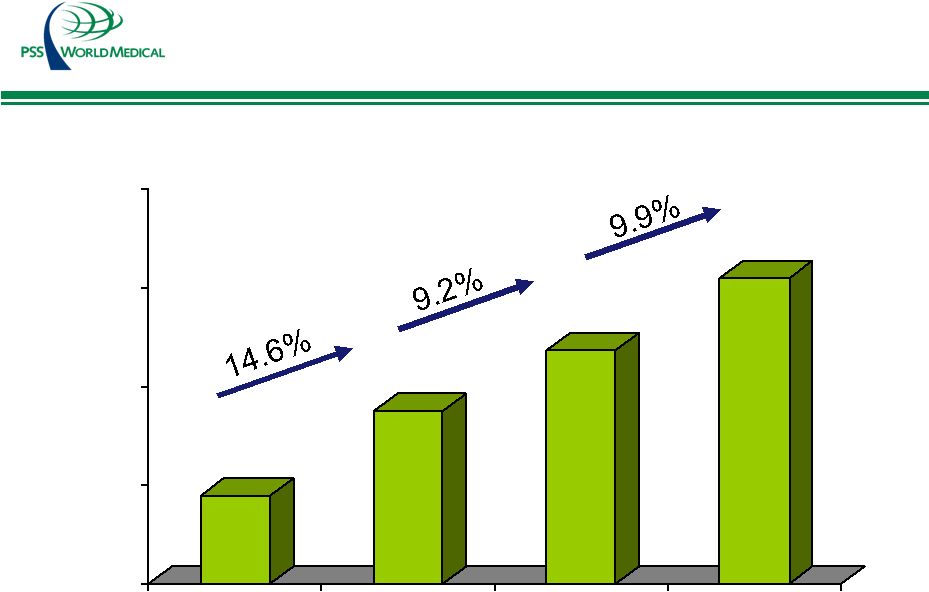

Revenue Growth: FY 2004 - 2006 1000 1200 1400 1600 1800 FY 03 FY 04 FY 05 FY 06 $1,178 $1,350 $1,474 $1,619 ($ in millions) |

Operating Income Growth : FY 2004 - 2006 20 40 60 80 FY 03 FY 04 FY 05 FY 06 $25.9 $47.8 $61.6 $72.4 ($ in millions) |

Operating Margin Growth: FY2004 - 2006 1 2 3 4 5 FY 03 FY 04 FY 05 FY 06 2.2% 3.5% 4.2% 4.5% (Scale in %) |

Earnings Per Diluted Share Growth*: FY 2004 - 2006 0 0.15 0.3 0.45 0.6 0.75 FY 03 FY 04 FY 05 FY 06 $0.12 $0.42 $0.51 $0.66 *From continued operations 1 1 Excludes non-recurring tax benefit of $5.6 million, or $0.09 per diluted share |

Operating Cash Flow Growth: FY 2004 – FY2006 $21.9 $36.3 $67.7 ($ in millions) 0 10 20 30 40 50 60 70 FY 04 FY 05 FY 06 |

Fiscal Year 2006: Increased Shareholder Value -40 -20 0 20 40 60 80 PSSI - 69.7% MCK - 38.8% CAH - 34.1% HSIC - 33.5% PDCO - (29.5%) 3/31/05 3/31/06 |

Fiscal Year 2006: Shared Services Achievements • Continued to leverage fixed costs on revenue growth • Reduced bank debt by $25.0 million to $0 at year-end FY2006 • Interest expense reduced by $900k to $5.9 million • SAS and CSSI acquisitions completed • Significant investments in contract and rebate administration • Global sourcing traction and profitability |

Shared Services: FY 2007 Plan • Develop and support growth of Select Medical Products brand • Continued focus on cash conversion cycle improvements • Optimize IT platforms – focus on user effectiveness & efficiency • Support Smartscan device and user growth • ETDBW |

Fiscal Years 2007- 2008 Financial Goals |

FY 2006 - FY 2008: EPS Growth Goals Earnings per diluted share from continuing operations FY 2007* $0.77 FY 2008* $0.94 FY 2006 $0.66 FY 2005 $0.51 Growth 29% Growth 17% Growth 22% FY2006 – FY2008: Average Annual Growth of 23% 1 Excludes non-recurring tax benefit of $5.6 million or $0.09 per diluted share * Mid point of goals of FY2007 of $0.76 - $0.78 and FY2008 of $0.93 - $0.95 1 |

Operating Margin Growth: FY 2007 - FY 2008 1 2 3 4 5 6 FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 2.2% 3.5% 4.2% 4.5% 4.8%-5.0% 5.4%-5.6% Actual Goal |

FY 2007: Financial Goals • Consolidated revenue growth 8%-10% (Includes expected sale of 5 million influenza doses) • Operating cash flow $58.0 - $60.0 million • Earnings per diluted share $0.76 - $0.78 • Consolidated operating margin growth 30-50 bps |

Fiscal Year 2003 - 2005: Historical Earnings Progression By Quarter 10% 15% 20% 25% 30% 35% 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr FY 2005 FY 2004 FY 2003 FY 2003 - FY 2005 FY2005: excludes tax benefit of $5.6 million or $0.09 per diluted share |

Fiscal Year 2003 - 2006: Historical Earnings Progression By Quarter 10% 15% 20% 25% 30% 35% 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr FY 2005 FY 2004 FY 2003 FY 2003 - FY 2006 FY 2006 FY2005: excludes tax benefit of $5.6 million or $0.09 per diluted share |

Acquisition Strategy: FY 2007 - FY 2008 • Target assets complementary to core business strategy - Fold-ins - Strategic • Size range $10mm - $50mm of revenues • Accretive within 12 months • Funded with cash flows and bank debt • 1 - 2 each year, both businesses |

What Does the CFO Focus On: FY2007 – FY2008 • Achievement and reporting of business plan metrics • Cost effective sources of capital for growth • Shared services cost leverage • Contingency planning • Acquisition strategy to complement and augment 3-year business plan • Corporate governance and internal business controls |

PSSI: Partner with our growth • Strong corporate governance and ethics • Leader in markets served, with significant new growth opportunities • Unique business and service model – barriers to entry • Strong balance sheet and flexibility to fund growth • Growing operating cash flows and operating margin • Sustainable revenue and earnings growth momentum • 20%+ Compounded EPS growth: FY2006 – FY2008 Investment considerations |

Thank You |