Exhibit 99.1

Annual Meeting of Shareholders Thursday, April 23, 2015

Safe Harbor During the course of this presentation, we will be providing you with a discussion of some of the factors we currently anticipate may influence the future results of Republic Bancorp, Inc. (“Republic” or the “Company”), as well as certain financial projections. We want to emphasize that these forward-looking statements involve judgment, and that individual judgments may vary. Moreover, these statements are based on limited information available to us now, which is subject to change. Actual results may differ substantially from what we say today and no one should assume later that the comments we provide today are still valid. They speak only as of today. Specific risk factors that could change causing our projections not to be achieved are discussed in the “Risk Factors” section of our Form 10-K filed with the Securities and Exchange Commission (“SEC”) on March 13, 2015, and other reports filed with the SEC from time to time.

Steve Trager Chairman and Chief Executive Officer

Highlights Year ended December 31, 2014

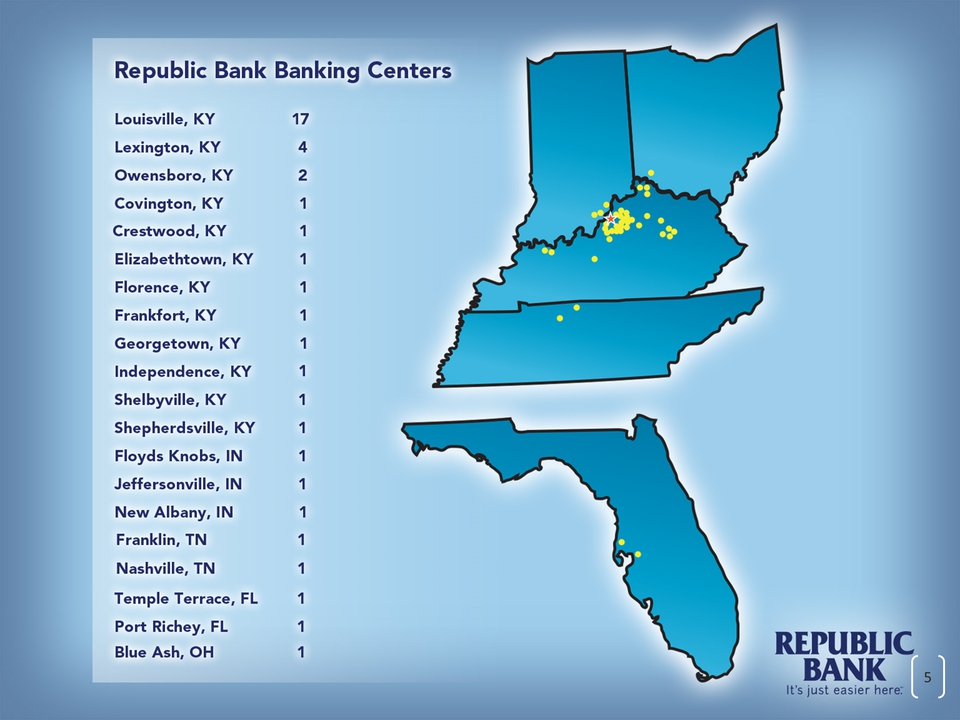

Republic Bank Banking Centers Louisville, KY 17 Lexington, KY 4 Owensboro, KY 2 Covington, KY 1 Crestwood, KY 1 Elizabethtown, KY 1 Florence, KY 1 Frankfort, KY 1 Georgetown, KY 1 Independence, KY 1 Shelbyville, KY 1 Shepherdsville, KY 1 Floyds Knobs, IN 1 Jeffersonville, IN 1 New Albany, IN 1 Franklin, TN 1 Nashville, TN 1 Temple Terrace, FL 1 Port Richey, FL 1 Blue Ash, OH 1

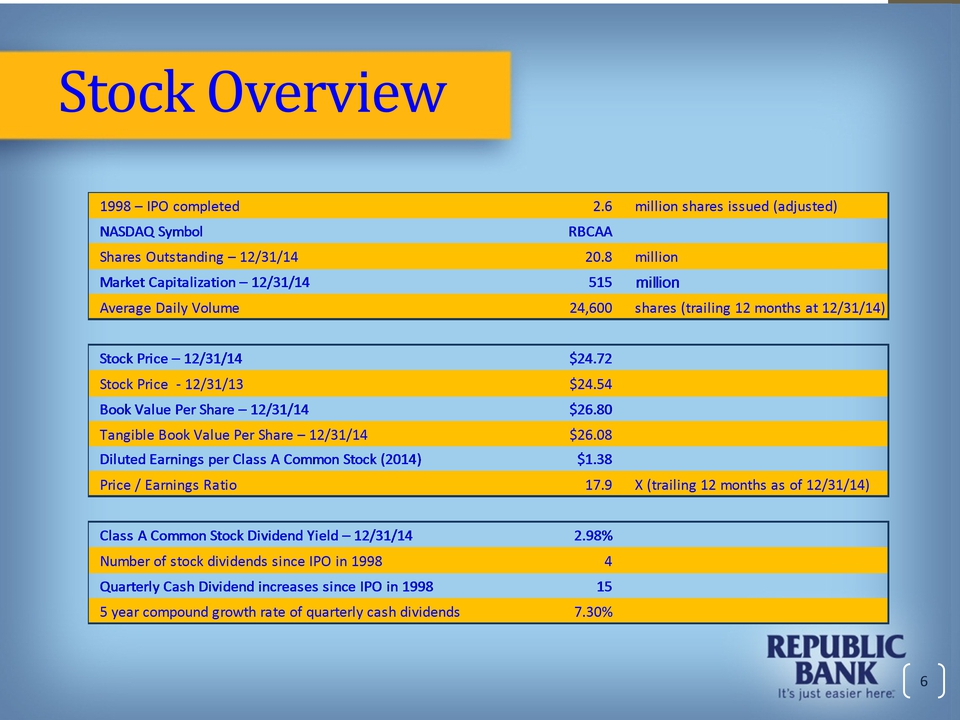

Stock Overview 1998 – IPO completed2.6million shares issued (adjusted)NASDAQ Symbol RBCAA Shares Outstanding – 12/31/1420.8million Market Capitalization – 12/31/14515million Average Daily Volume 24,600 shares (trailing 12 months at 12/31/14)Stock Price – 12/31/14$24.72 Stock Price - 12/31/13$24.54 Book Value Per Share – 12/31/14$26.80 Tangible Book Value Per Share – 12/31/14 $26.08 Diluted Earnings per Class A Common Stock (2014)$1.38 Price / Earnings Ratio17.9X (trailing 12 months as of 12/31/14)Class A Common Stock Dividend Yield – 12/31/142.98%Number of stock dividends since IPO in 19984Quarterly Cash Dividend increases since IPO in 1998 155 year compound growth rate of quarterly cash dividends 7.30%

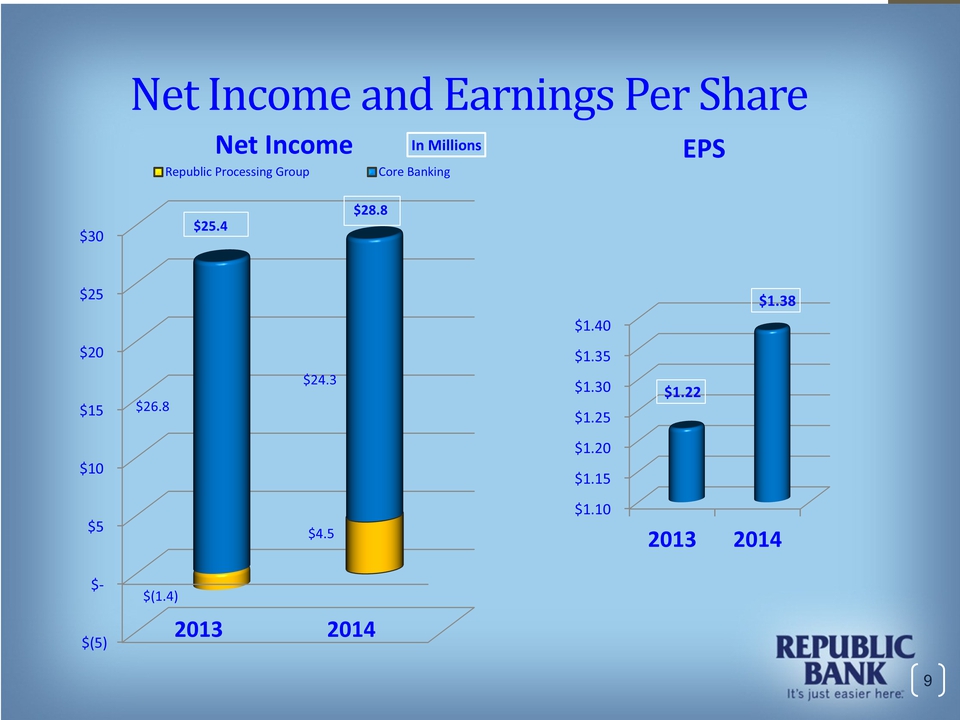

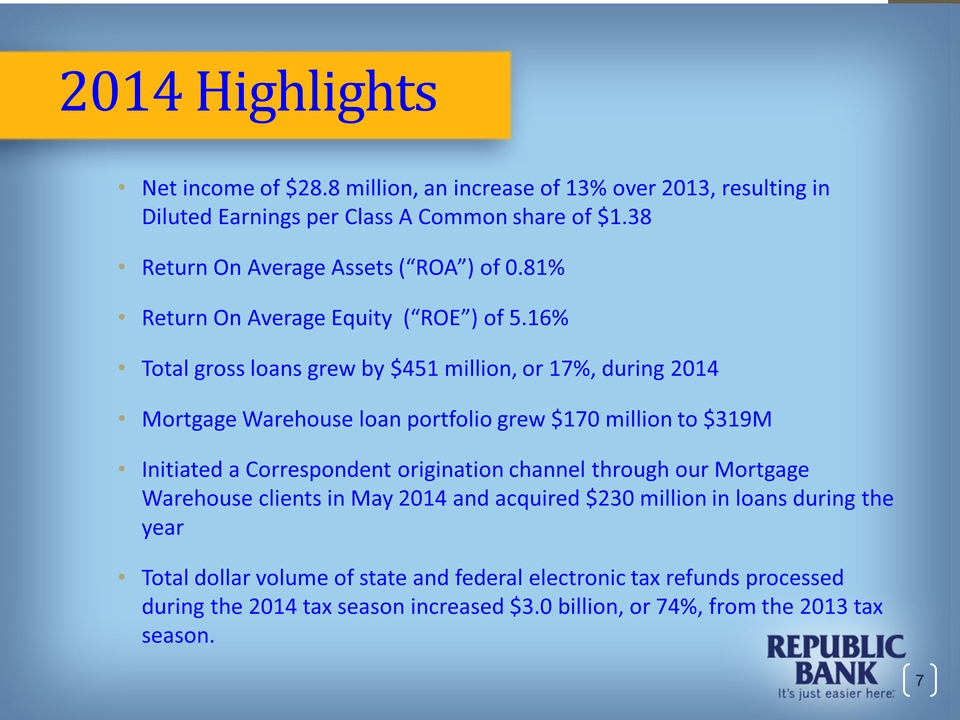

2014 Highlights Net income of $28.8 million, an increase of 13% over 2013, resulting in Diluted Earnings per Class A Common share of $1.38 Return On Average Assets (“ROA”) of 0.81% Return On Average Equity (“ROE”) of 5.16% Total gross loans grew by $451 million, or 17%, during 2014 Mortgage Warehouse loan portfolio grew $170 million to $319M Initiated a Correspondent origination channel through our Mortgage Warehouse clients in May 2014 and acquired $230 million in loans during the year Total dollar volume of state and federal electronic tax refunds processed during the 2014 tax season increased $3.0 billion, or 74%, from the 2013 tax season.

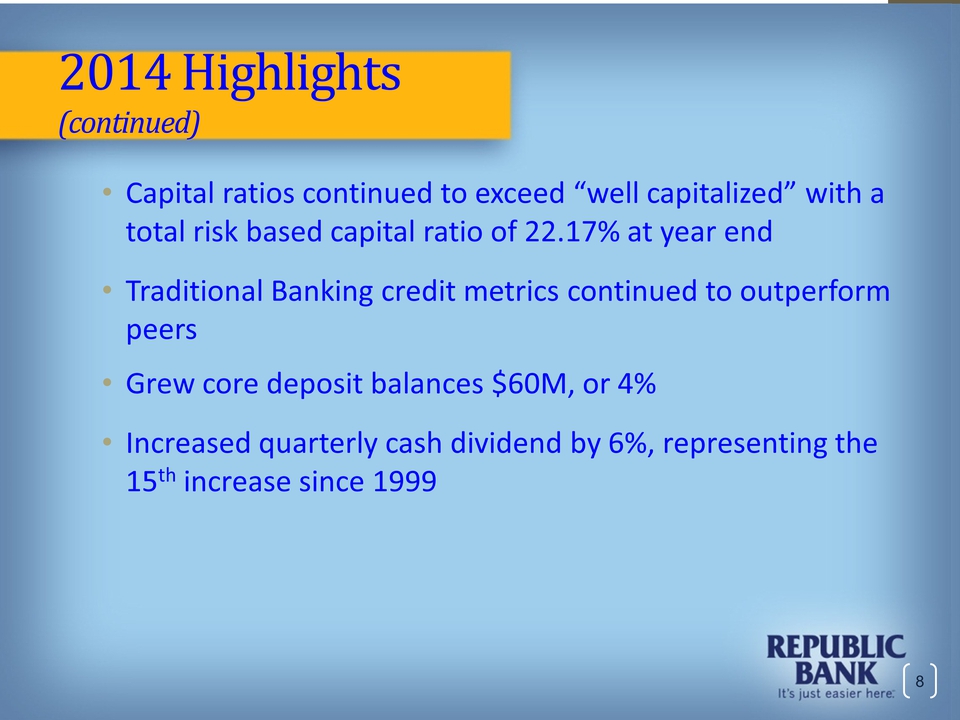

2014 Highlights (continued) Capital ratios continued to exceed “well capitalized” with a total risk based capital ratio of 22.17% at year end Traditional Banking credit metrics continued to outperform peers Grew core deposit balances $60M, or 4% Increased quarterly cash dividend by 6%, representing the 15th increase since 1999

Net Income and Earnings Per Share $(5) $- $5 $10 $15 $20 $25 $30 2013 2014 $(1.4) $4.5 $26.8 $24.3 In Millions Net Income Republic Processing Group Core Banking $25.4 $28.8 $1.10 $1.15 $1.20 $1.25 $1.30 $1.35 $1.40 2013 2014 $1.22 $1.38 EPS

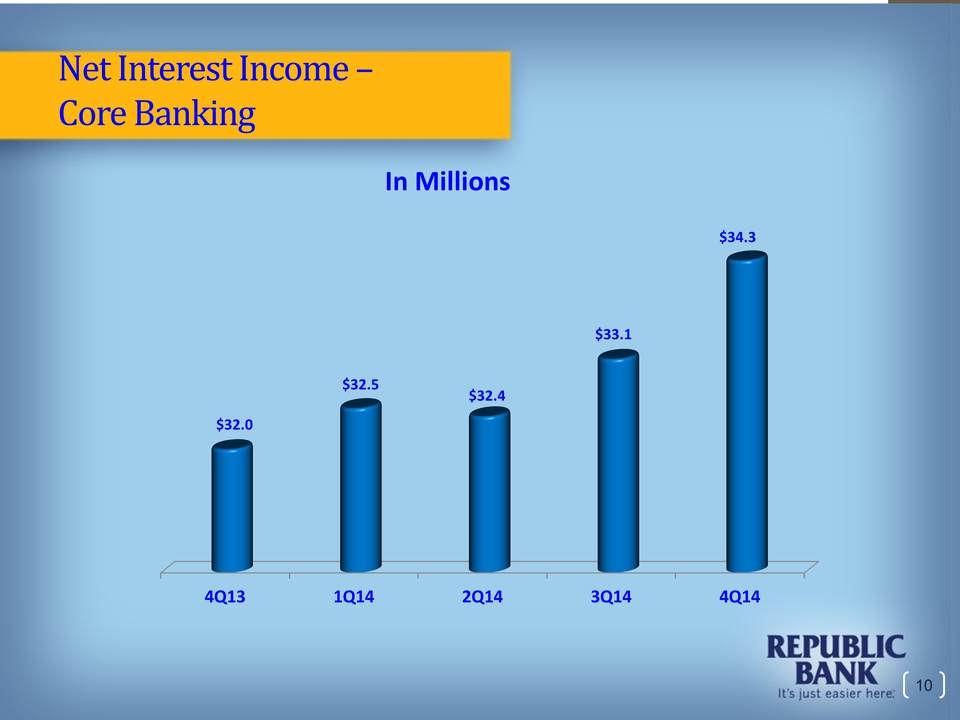

Net Interest Income – Core Banking 4Q13 1Q14 2Q14 3Q14 4Q14 $32.0 $32.5 $32.4 $33.1 $34.3 In Millions

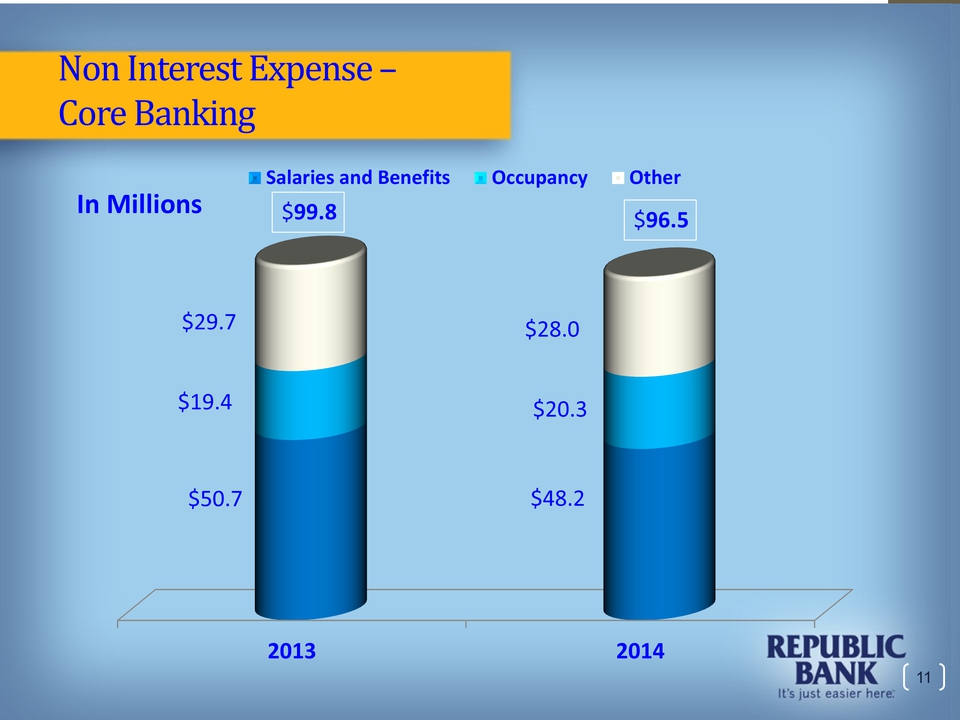

Non Interest Expense – Core Banking 2013 2014 $50.7 $48.2 $19.4 $20.3 $29.7 $28.0 In Millions Salaries and Benefits Occupancy Other $99.8 $96.5

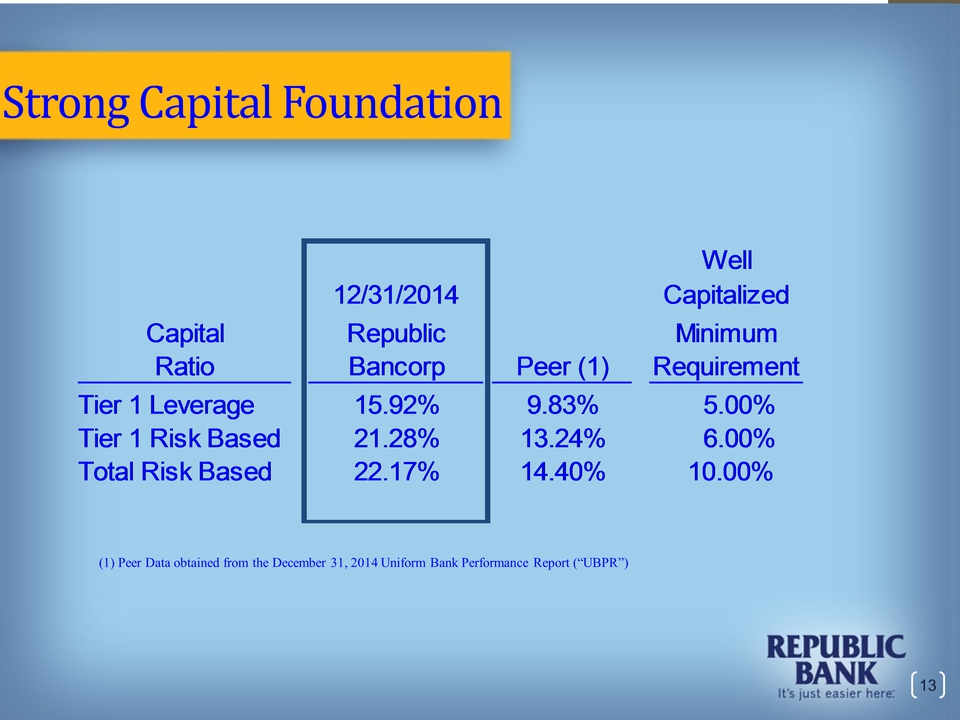

Well 12/31/2014 Capitalized Capital Republic Minimum Ratio Bancorp Peer (1) Requirement Tier 1 Leverage 15.92% 9.83% 5.00% Tier 1 Risk Based 21.28% 13.24% 6.00% Total Risk Based 22.17% 14.40% 10.00% Strong Capital Foundation (1) Peer Data obtained from the December 31, 2014 Uniform Bank Performance Report (“UBPR”)

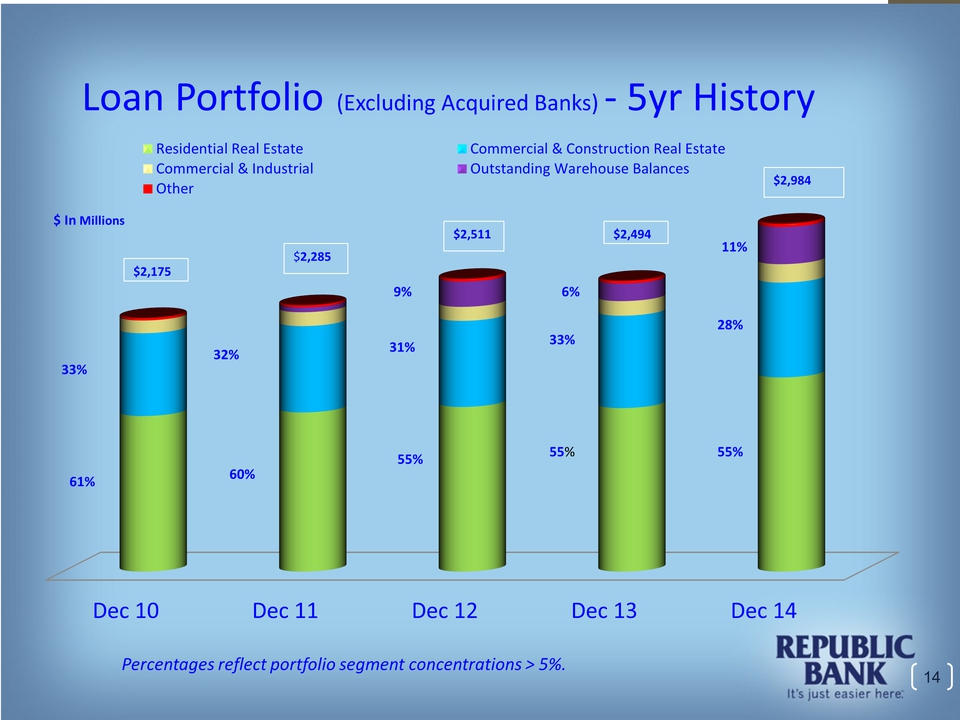

Loan Portfolio (Excluding Acquired Banks) - 5yr History Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Residential Real Estate Commercial & Construction Real Estate Commercial & Industrial Outstanding Warehouse Balances Other $ In Millions $2,175 $2,285 $2,511 $2,494 $2,984 61% 60% 55% 55% 55% 33% 32% 31% 33% 28% 11% 6% 9% Percentages reflect portfolio segment concentrations > 5%.

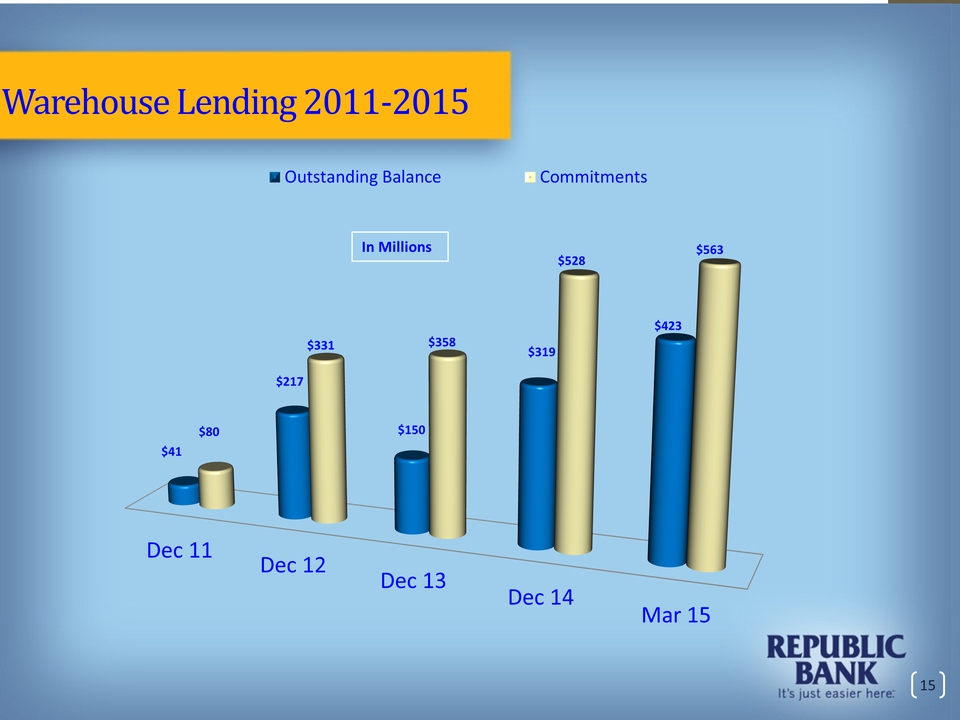

Warehouse Lending 2011-2015 Dec 11 Dec 12 Dec 13 Dec 14 Mar 15 $41 $217 $150 $319 $423 $80 $331 $358 $528 $563 Outstanding Balance Commitments In Millions

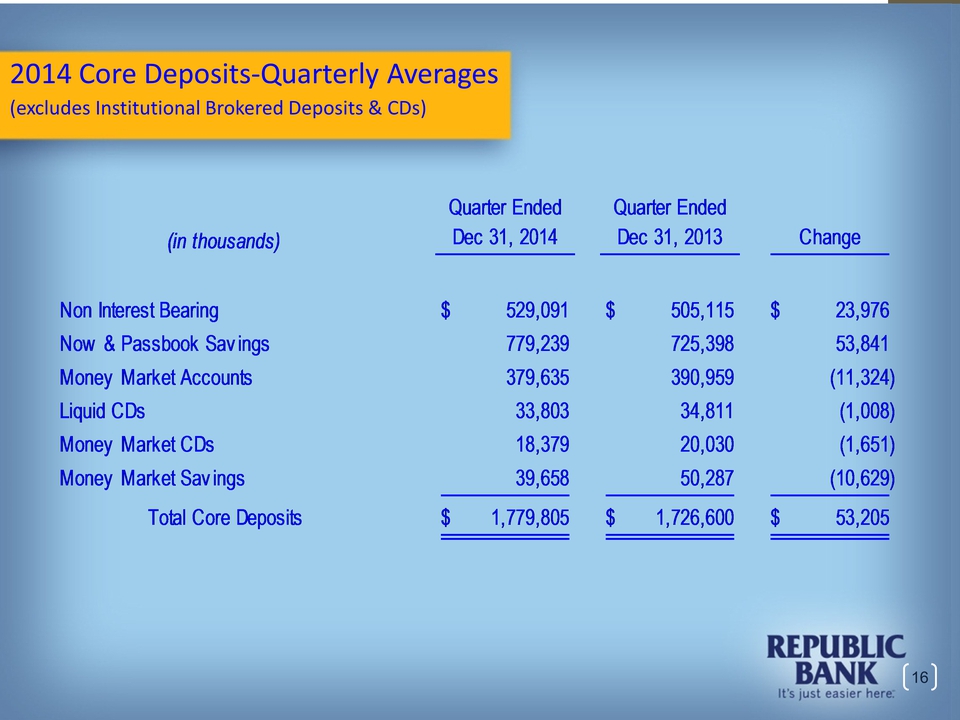

Quarter Ended Quarter Ended (in thousands) Dec 31, 2014 Dec 31, 2013 Change Non Interest Bearing $ 529,091 $ 505,115 $ 23,976 Now & Passbook Sav ings 779,239 725,398 53,841 Money Market Accounts 379,635 390,959 (11,324) Liquid CDs 33,803 34,811 (1,008) Money Market CDs 18,379 20,030 (1,651) Money Market Sav ings 39,658 50,287 (10,629) Total Core Deposits $ 1,779,805 $ 1,726,600 $ 53,205 2014 Core Deposits-Quarterly Averages (excludes Institutional Brokered Deposits & CDs)

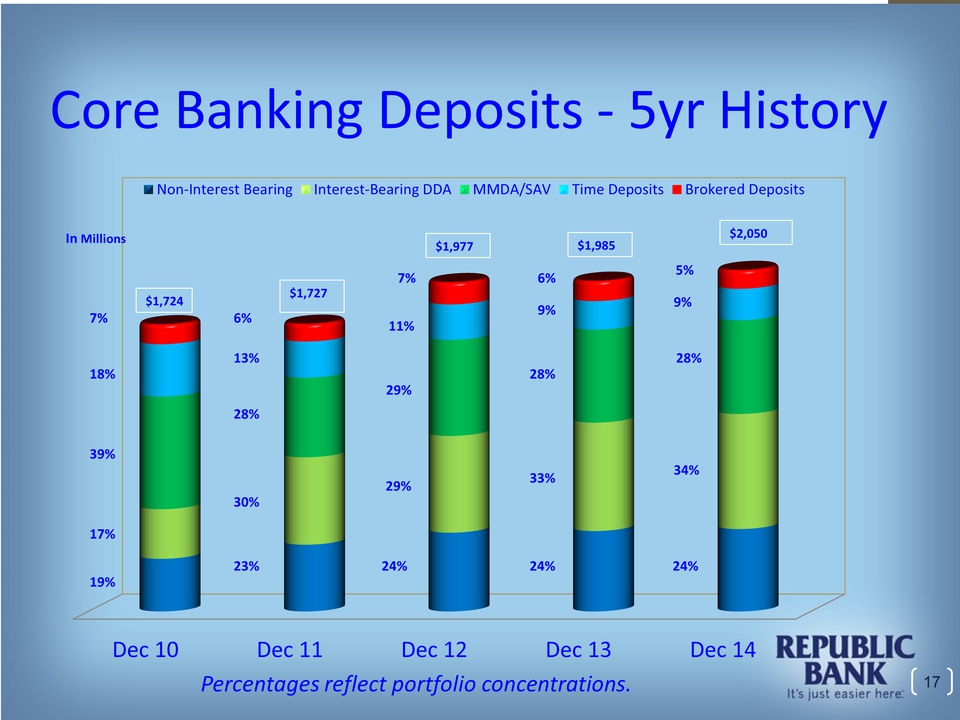

Core Banking Deposits - 5yr History Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Non-Interest Bearing Interest-Bearing DDA MMDA/SAV Time Deposits Brokered Deposits In Millions $1,724 $1,977 $1,985 $2,050 23% 24% 24% 24% 30% 29% 33% 34% 28% 29% 28% 28% 13% 11% 9% 9% 6% 7% 6% 5% 19% 17% 39% 18% 7% $1,727 Percentages reflect portfolio concentrations.

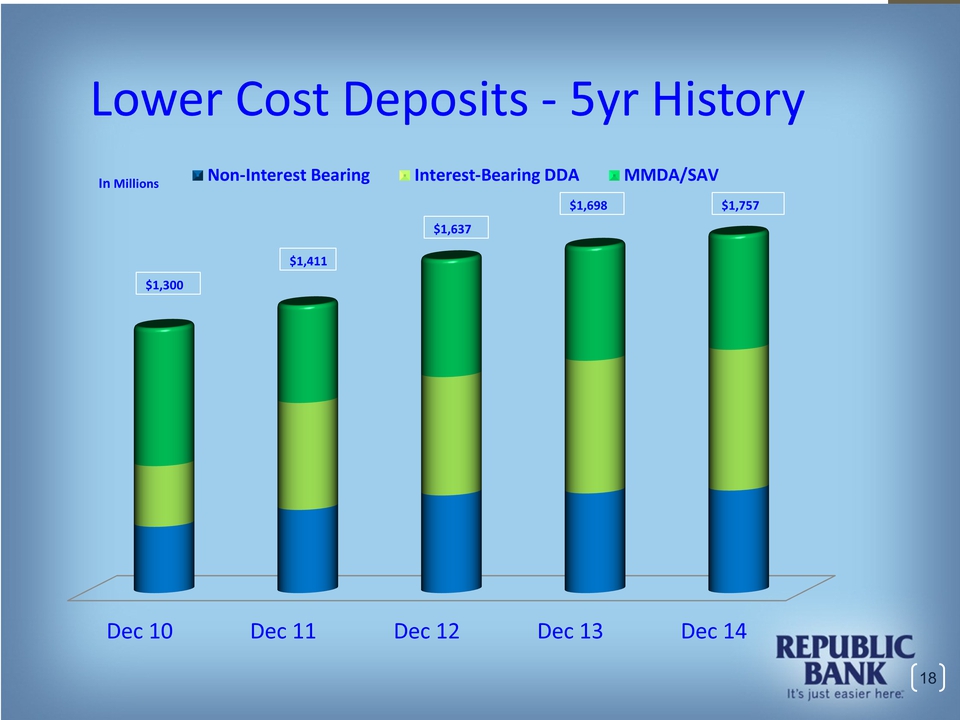

Lower Cost Deposits - 5yr History Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Non-Interest Bearing Interest-Bearing DDA MMDA/SAV In Millions $1,300 $1,411 $1,637 $1,698 $1,757

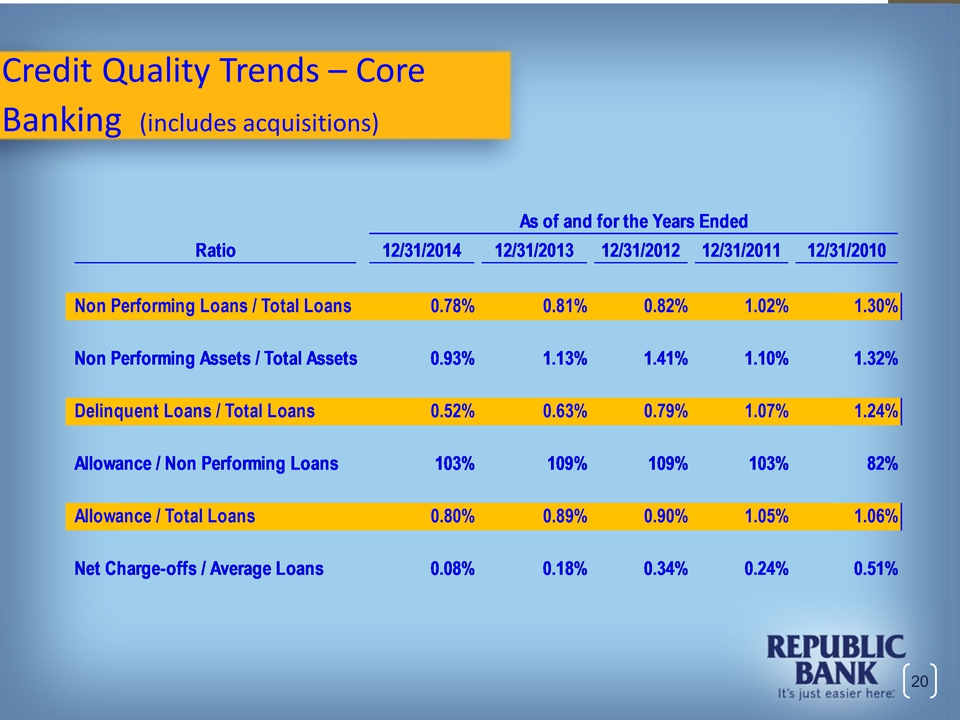

Industry Strong Credit Quality

Credit Quality Trends – Core Banking (includes acquisitions) Ratio 12/31/2014 12/31/2013 12/31/2012 12/31/2011 12/31/2010 Non Performing Loans / Total Loans 0.78% 0.81% 0.82% 1.02% 1.30% Non Performing Assets / Total Assets 0.93% 1.13% 1.41% 1.10% 1.32% Delinquent Loans / Total Loans 0.52% 0.63% 0.79% 1.07% 1.24% Allowance / Non Performing Loans 103% 109% 109% 103% 82% Allowance / Total Loans 0.80% 0.89% 0.90% 1.05% 1.06% Net Charge-offs / Average Loans 0.08% 0.18% 0.34% 0.24% 0.51% As of and for the Years Ended

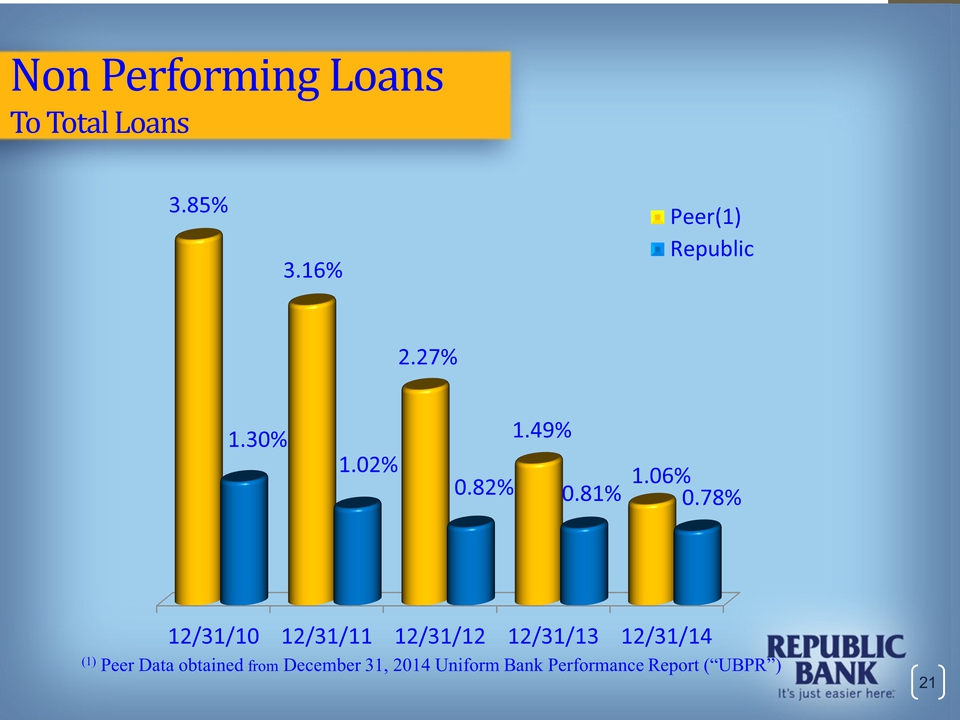

12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 3.85% 3.16% 2.27% 1.49% 1.06% 1.30% 1.02% 0.82% 0.81% 0.78% Peer(1) Republic Non Performing Loans To Total Loans (1) Peer Data obtained from December 31, 2014 Uniform Bank Performance Report (“UBPR”)

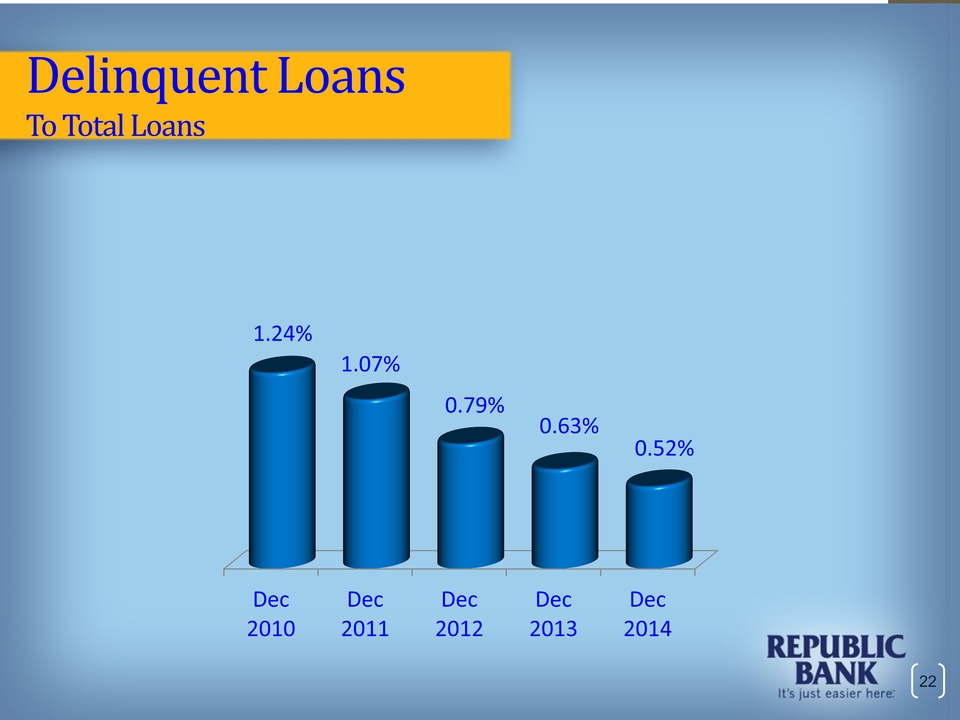

Delinquent Loans To Total Loans Dec 2010 Dec 2011 Dec 2012 Dec 2013 Dec 2014 1.24% 1.07% 0.79% 0.63% 0.52%

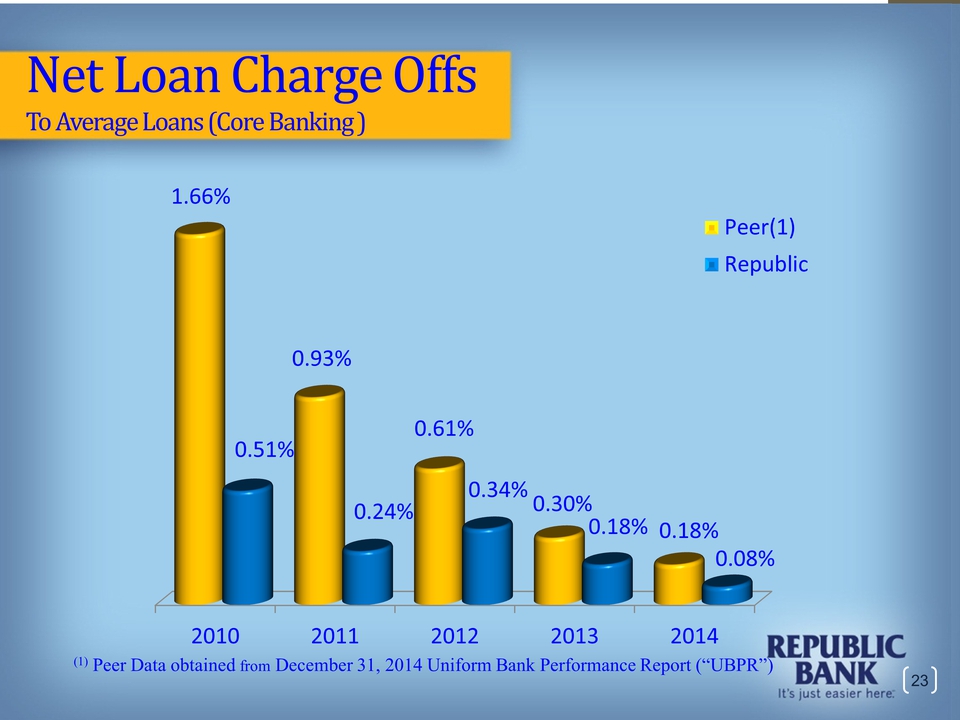

Net Loan Charge Offs To Average Loans (Core Banking )2010 2011 2012 2013 2014 1.66% 0.93% 0.61% 0.30% 0.18% 0.51% 0.24% 0.34% 0.18% 0.08% Peer(1) Republic (1) Peer Data obtained from December 31, 2014 Uniform Bank Performance Report (“UBPR”)

Interest Rate Management Strategy

Interest Rate Sensitivity Asset Repricing: 83% of our total loan portfolio reprices within 5yrs as of December 31, 2014 Commercial Real Estate portfolio repricing within 5yrs increased from 69% in 2013 to 81% in 2014 Commercial & Industrial portfolio repricing within 5yrs increased from 63% in 2013 to 89% in 2014 Mortgage Warehouse outstanding balances, which reprice immediately, increased by $170 million from 2013 to 2014 Liability Repricing: Throughout 2014, the Bank extended $100 million of liabilities through a combination of FHLB advances and Retail CDs, with an average stated maturity of 5yrs The entire long-term borrowing portfolio at December 31, 2014 was approximately $600 million with an average life of 2.75yrs Non-interest bearing deposits accounted for 24% of retail funding at December 31, 2014.

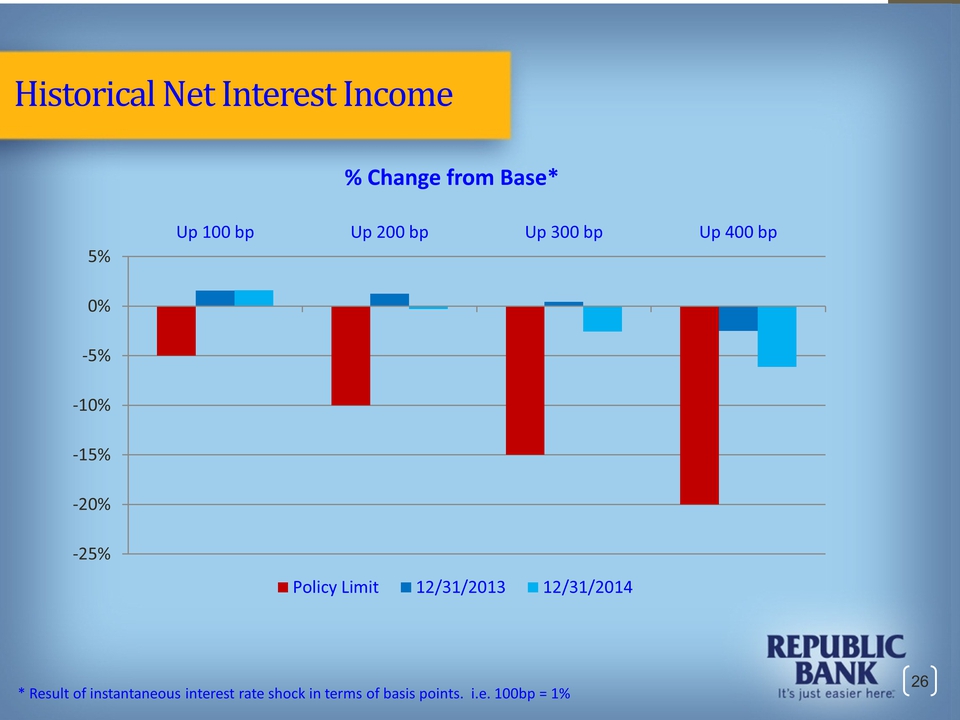

Historical Net Interest Income -25% -20% -15% -10% -5% 0% 5% Up 100 bp Up 200 bp Up 300 bp Up 400 bp % Change from Base* Policy Limit 12/31/2013 12/31/2014 * Result of instantaneous interest rate shock in terms of basis points. i.e. 100bp = 1%

Highlights First Quarter 2015

1Q 2015 Highlights Net income of $13.8 million, an increase of 15% over the first quarter of 2014 Return On Average Assets (“ROA”) of 1.40% Return On Average Equity (“ROE”) of 9.72% Capital ratios under new Basel III standard continued to exceed “well capitalized” with a total risk based capital ratio exceeding 20% Credit metrics continued to outperform peers

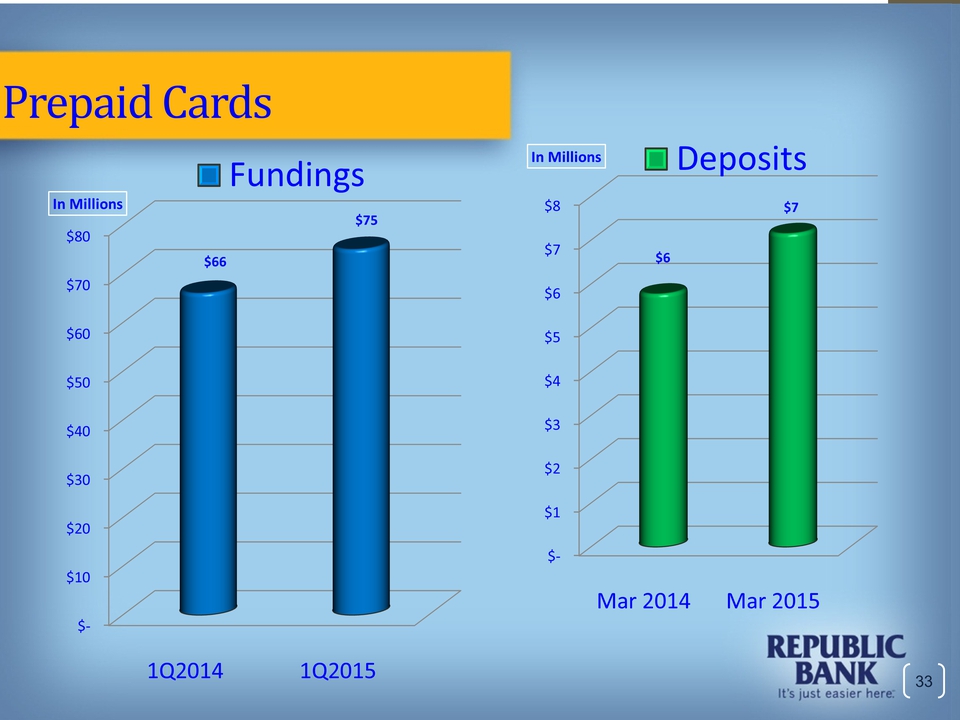

1Q 2015 Highlights – RPG A 39% increase in refund transfers processed from 2014 Over $75 million loaded onto prepaid cards, up $9 million, or 14% from 2014 $4 million in gross loans outstanding for pilot RCS programs Signed agreement with Fenway Summer to pilot FS Card unsecured credit card program Signed agreement with NetSpend to pilot NetSpend prepaid cards

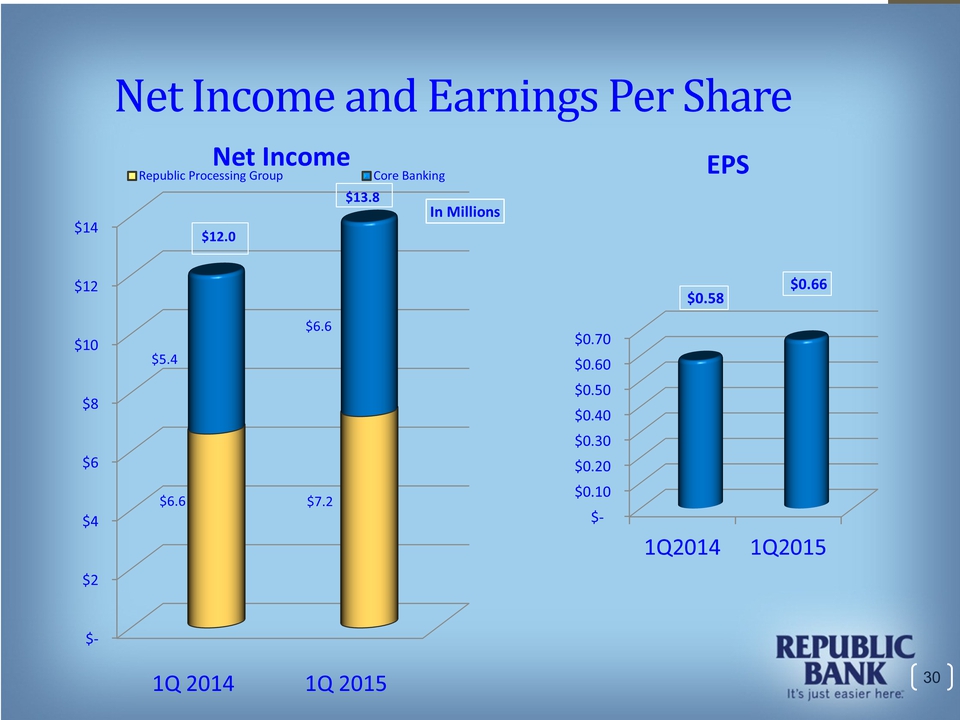

Net Income and Earnings Per Share $- $2 $4 $6 $8 $10 $12 $14 1Q 2014 1Q 2015 $6.6 $7.2 $5.4 $6.6 In Millions Net Income Republic Processing Group Core Banking $12.0 $13.8 $- $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 1Q2014 1Q2015 $0.58 $0.66 EPS 30 Average

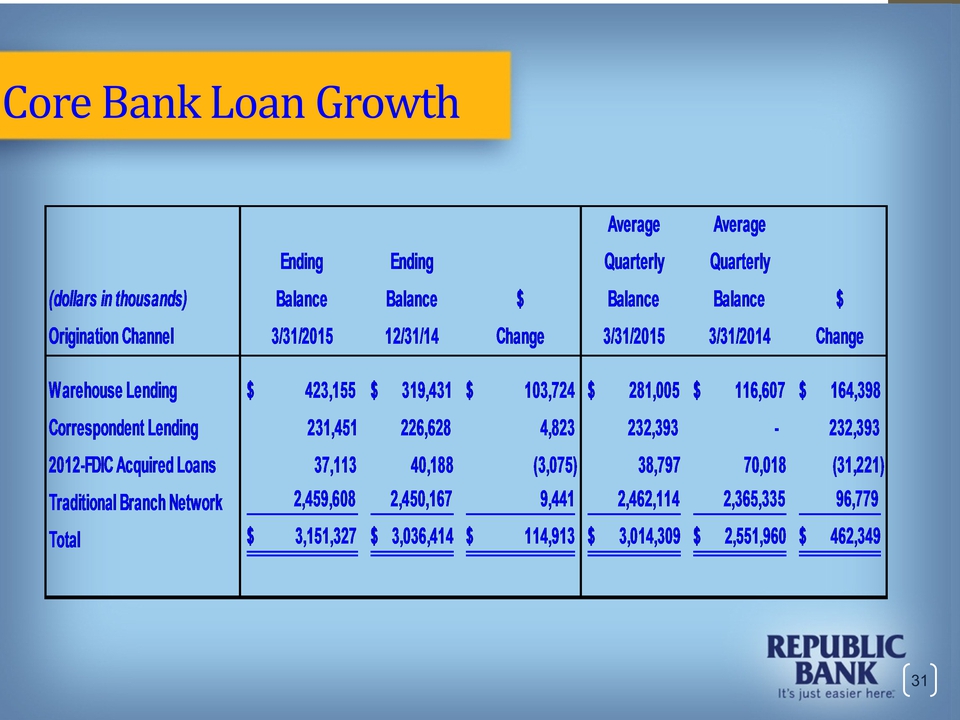

Average Ending Ending Quarterly Quarterly (dollars in thousands) Balance Balance $ Balance Balance $Origination Channel 3/31/2015 12/31/14 Change 3/31/2015 3/31/2014 Change Warehouse Lending $ 423,155 $ 319,431 $ 103,724 $ 281,005 $ 116,607 $ 164,398 Correspondent Lending 231,451 226,628 4,823 232,393 - 232,393 2012-FDIC Acquired Loans 37,113 40,188 (3,075) 38,797 70,018 (31,221) Traditional Branch Network 2,459,608 2,450,167 9,441 2,462,114 2,365,335 96,779 Total $ 3,151,327 $ 3,036,414 $ 114,913 $ 3,014,309 $ 2,551,960 $ 462,349 Core Bank Loan Growth

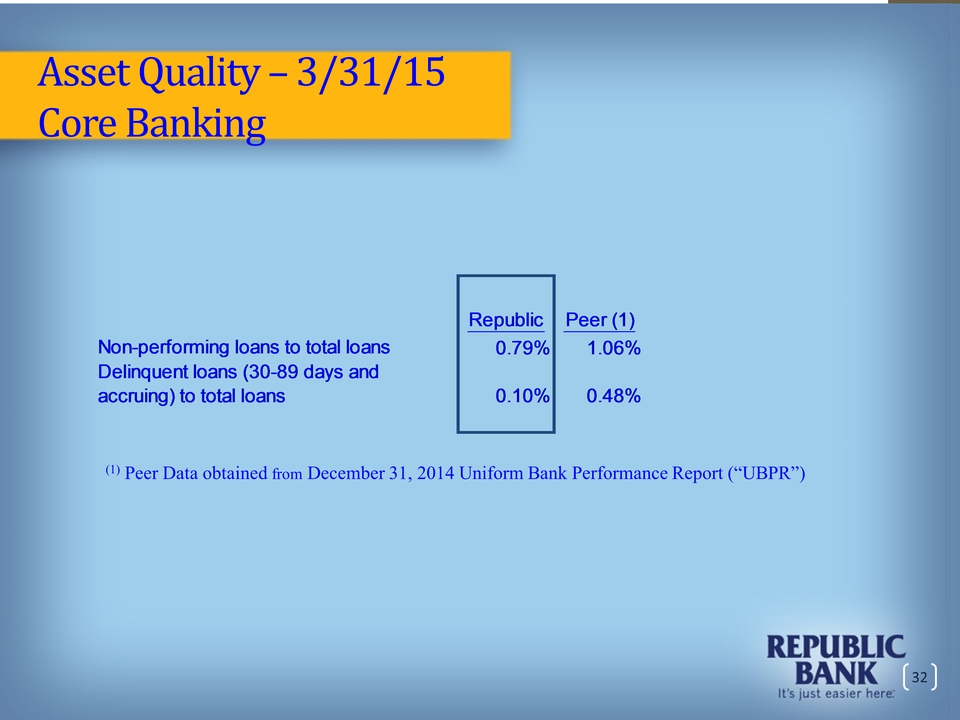

Asset Quality – 3/31/15 Core Banking (1) Peer Data obtained from December 31, 2014 Uniform Bank Performance Report (“UBPR”) RepublicPeer (1)Non-performing loans to total loans0.79%1.06%Delinquent loans (30-89 days and accruing) to total loans0.10%0.48%

Prepaid Cards $- $10 $20 $30 $40 $50 $60 $70 $80 1Q2014 1Q2015 $66 $75 In Millions Fundings $- $1 $2 $3 $4 $5 $6 $7 $8 Mar 2014 Mar 2015 $6 $7 In Millions Deposits

Initiatives Bank acquisitions; either purchase or FDIC-assisted Grow traditional loan portfolios – commercial and retail loans Grow product lines – Warehouse Lending, Dealer Services, Equipment Lease Financing Expand new lines of business – Prepaid Cards, Short-term credit products. Focus on core deposit growth initiatives

It’s just easier here. Republic Bank.