UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2024

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________to__________

Commission File Number: 001-35455

SSR MINING INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

British Columbia (State or Other Jurisdiction of Incorporation or Organization) | | 98-0211014

(I.R.S. Employer Identification No.) |

| Suite 1300 - 6900 E. Layton Ave, Denver, Colorado 80237 |

(Address of Principal Executive Offices)

Registrant’s telephone number, including area code (303) 292-1299

Securities registered pursuant to Section 12(b) of the Act.

| | | | | | | | |

| Title of each class | Trading symbol | Name of each exchange on which registered |

| Common shares without par value | SSRM | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act. None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12-b2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12-b2 of the Exchange Act). ☐ Yes ☒ No

At June 30, 2024, the aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates of the registrant was $906,492,068 based on the closing sale price as reported on Nasdaq Global Market on that date. There were 202,386,185 common shares outstanding on January 31, 2025.

DOCUMENTS INCORPORATED BY REFERENCE

Designated portions of the registrant’s definitive Proxy Statement for its 2025 Annual Meeting of Shareholders, which is to be filed subsequent to the date hereof, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| | | | | |

| Page |

| PART I |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| PART II |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| PART III |

| |

| |

| |

| |

| |

| PART IV |

| |

| |

| |

PART I

Çöpler Incident

On February 13, 2024, SSR Mining Inc. and its subsidiaries (collectively, “SSR Mining,” or the “Company”) suspended all operations at its Çöpler property, in Türkiye, as a result of a significant slip on the heap leach pad (the “Çöpler Incident”). Nine employees lost their lives in connection with the Çöpler Incident. The Company continues to support the employees, families, and community members impacted by the Çöpler Incident.

In partnership with the Turkish authorities, the Company has worked to remediate the site. As of December 31, 2024, all of the displaced heap leach material in the Sabırlı Valley has been moved to temporary storage locations. As part of the remediation work, the heap leach pad will be permanently closed, and heap leach processing will no longer take place at Çöpler. Public statements from Turkish government officials have consistently confirmed that there has been no recordable contamination to local soil, water or air in the sampling locations resulting from the displaced heap leach material.

Following the Çöpler Incident, the Company commissioned Call & Nicholas, Inc. (“CNI”), an international mining consulting firm that specializes in geological engineering, geotechnical engineering, and hydrology, to conduct an independent review of the heap leach failure at Çöpler. After analysis of the engineering design, construction, and operation of the heap leach facility, and comprehensive reverse-engineering of the failure, CNI determined that the most likely cause of the Çöpler Incident was a deeply-rooted flaw in the third-party engineered design of the heap leach pad. The review found that in the third-party engineered design, the assessment of the test data overestimated the shear strength properties of the liner system at the base of the heap leach, which inflated the calculated factor of safety values in the third-party engineered design. This error resulted in insufficient shear strength along the liner interface to support the as-designed heap leach facility. CNI also determined that in all material respects, the heap leach pad construction and operation was carried out in conformance with the issued-for-construction engineered design parameters. In addition, CNI’s review did not find any substantiation that excess water, ground vibrations from blasting, nor stacking beyond the design caused the event.

As previously disclosed, on August 20, 2024, a local court issued a decision cancelling the Çöpler mine’s environmental impact assessment, which was approved in 2021 (the “2021 EIA”). The Turkish Ministry of Environment, Urbanization and Climate Change filed an appeal of the decision, and the Company filed a simultaneous intervener appeal as well. On February 11, 2025 the Turkish Council of State affirmed the finding of the lower court. As previously disclosed, with the cancellation of the 2021 EIA, the operating guidelines at Çöpler revert to those outlined in the Company’s prior Environmental Impact Assessment, which was issued in 2014 (the “2014 EIA”). Among other operating considerations, the 2014 EIA prescribes a lower throughput rate for the sulfide plant operations of 6,000 tonnes per day, as compared to 9,000 tonnes per day under the 2021 EIA.

SSR Mining continues to work closely with the relevant authorities to advance the restart of the Çöpler mine. When all necessary regulatory approvals, including the operating permits, are reinstated, it is anticipated that initial operations at Çöpler could restart within 20 days and would consist of processing a combination of stockpiled ore and ore mined from Çakmaktepe, while the remediation work continues. At this time, we are not able to estimate or predict when and under what conditions we will resume operations at Çöpler.

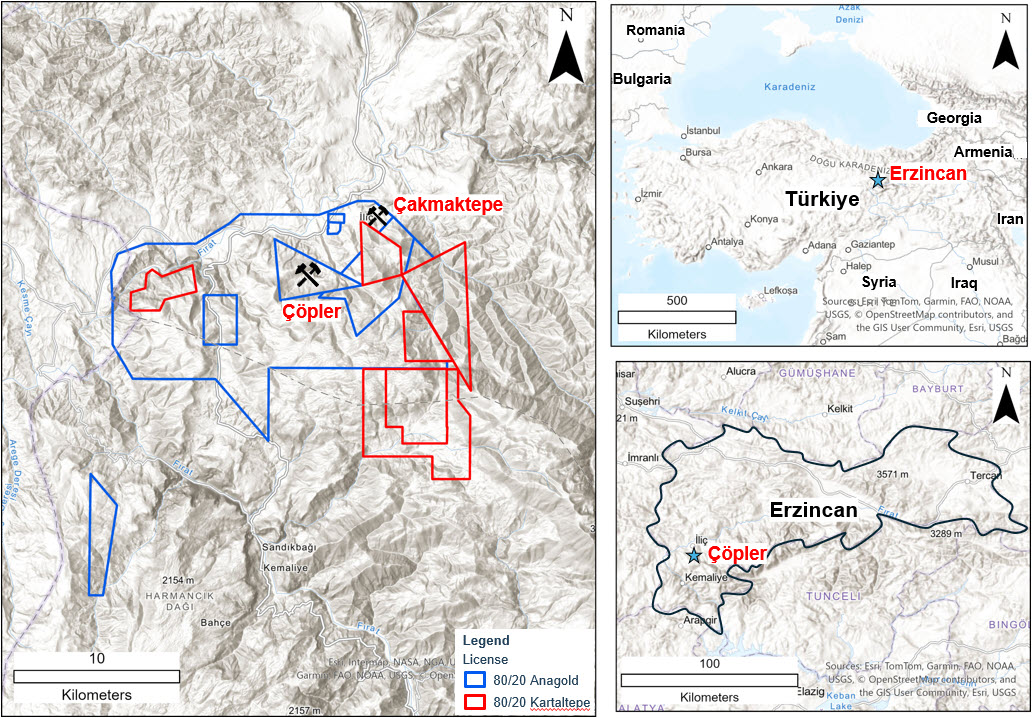

For further information on the Çöpler mine, including its ownership structure, see Item 2. Properties under the heading “Çöpler Property, Erzincan Province, Türkiye.” Çöpler constitutes a single reporting segment for the Company, as do each of the Company's three other mines, Marigold, Puna, and Seabee. For financial information of the Company’s segments for the years ended December 31, 2024, 2023 and 2022, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 5 to the Consolidated Financial Statements.

See Item 1A. Risk Factors for additional information.

ITEM 1. BUSINESS

Introduction

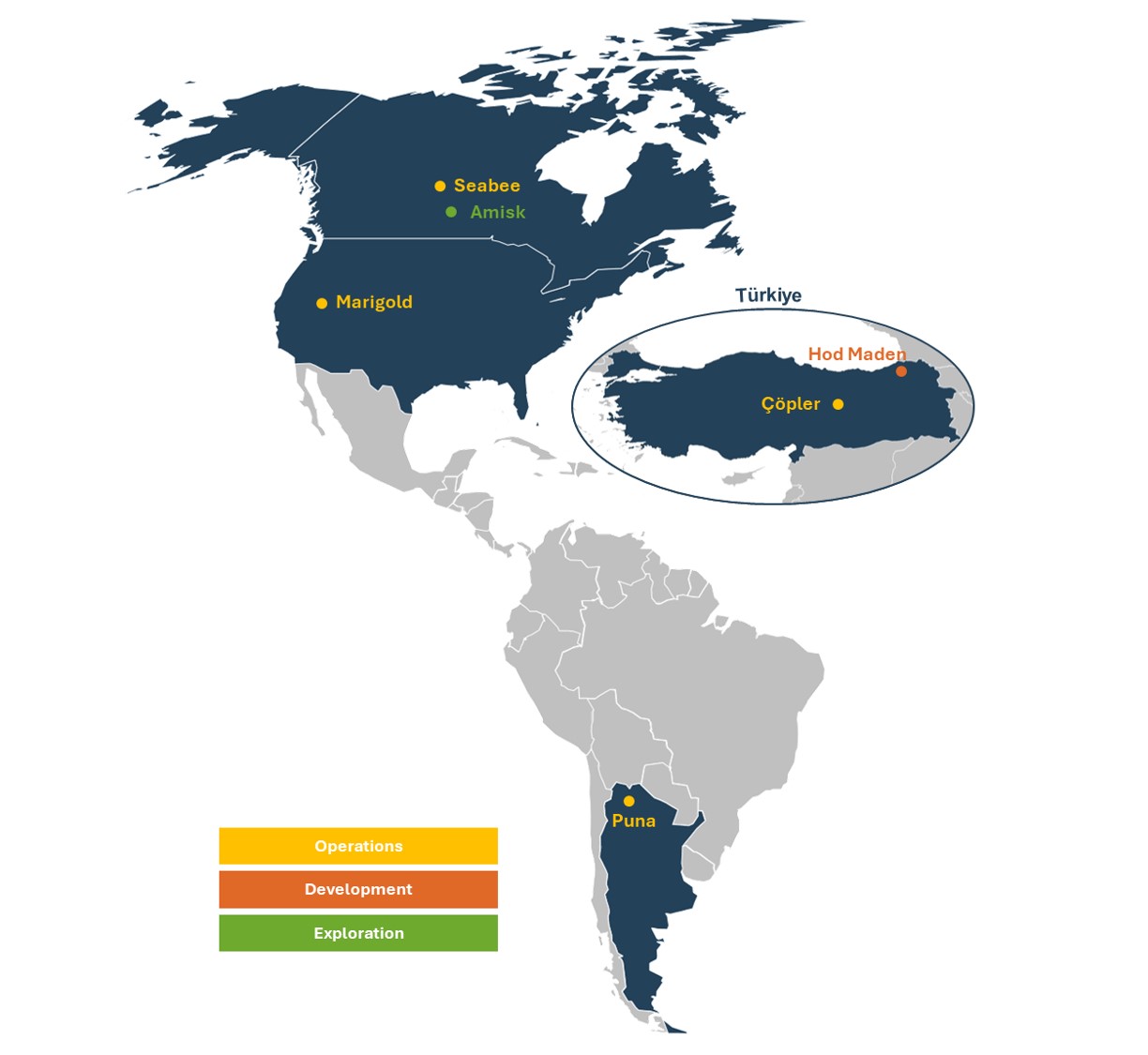

SSR Mining Inc. and its subsidiaries (collectively, “SSR Mining,” or “Company”) is a precious metals mining company with four assets located in the United States, Türkiye, Canada and Argentina. The Company is primarily engaged in the operation, acquisition, exploration and development of precious metal resource properties located in Türkiye and the Americas. The Company produces gold doré as well as copper, silver, lead and zinc concentrates.

In this report, “SSR Mining,” the “Company,” “our,” “us” and “we” refer to SSR Mining Inc. together with its affiliates and subsidiaries, unless the context otherwise requires. All currency references herein are in United States dollars (“USD”) unless otherwise indicated. References to “CAD” or the use of the symbol “C$” refers to Canadian dollars. References to “TRY” are to the lawful currency of Türkiye, the Turkish Lira. References to “ARS” are to the lawful currency of Argentina, the Argentine peso.

Segment Information

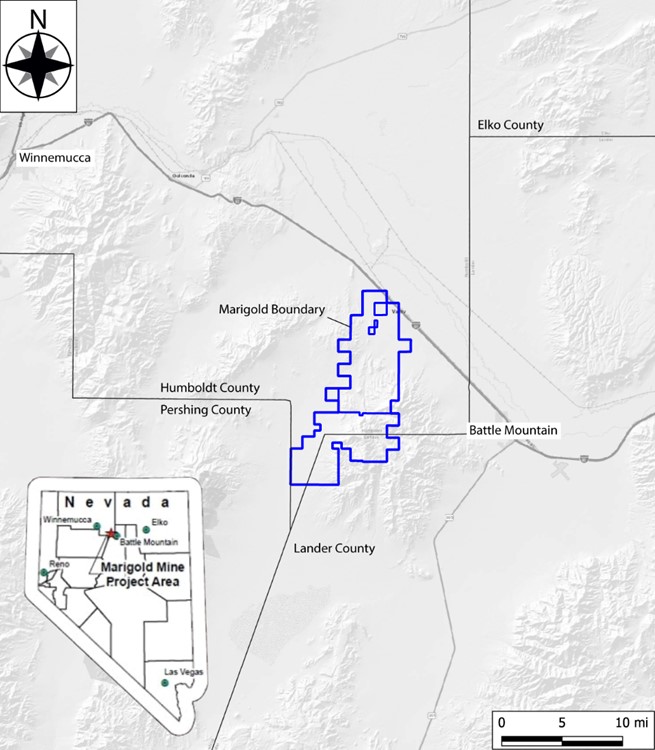

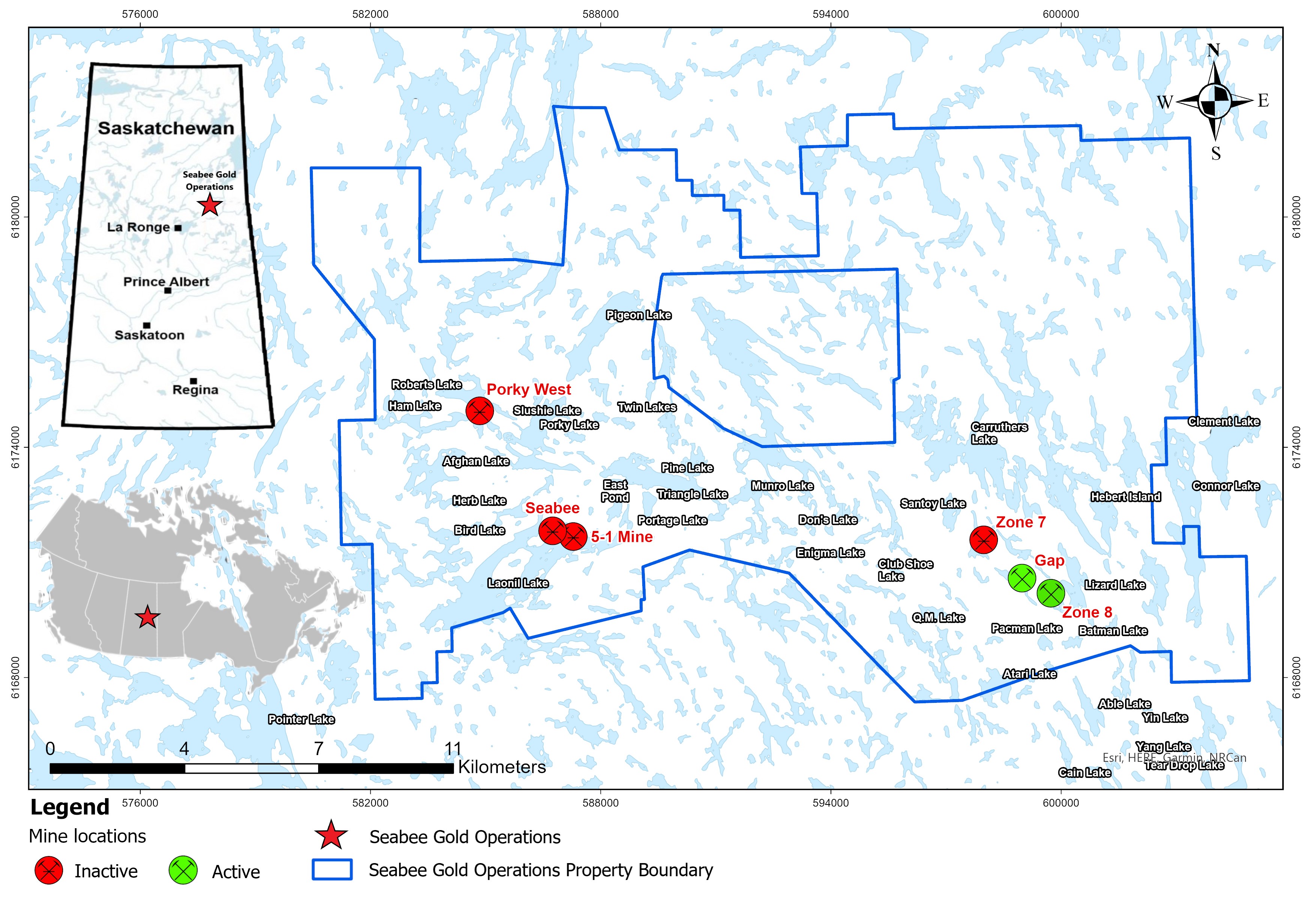

The Company’s operations consist of four mine sites - Çöpler, located in Erzincan Province, Türkiye (“Çöpler”), Marigold, located in Nevada, United States (“Marigold”), Seabee, located in Saskatchewan, Canada (“Seabee”), and Puna, located in Jujuy Province, Argentina (“Puna”) - each of which is a reportable operating segment and which are also referred to as producing assets. The contributions to revenue by reportable operating segment for the year ended December 31, 2024 were 7% from Çöpler (2023 – 31%; 2022 – 31%), 41% from Marigold (2023 – 38%; 2022 – 30%), 19% from Seabee (2023 – 11%; 2022 – 21%) and 33% from Puna (2023 – 20%; 2022 – 18%). See Note 5 to the Consolidated Financial Statements for further information relating to reportable operating segments.

The Company also participates in exploration and development activities at properties located in the United States, Argentina, Canada and Türkiye. See Item 2. Properties, for further information about the Company’s production and exploration properties.

Principal Products

Çöpler, Marigold and Seabee produce gold doré. Doré is unrefined gold bullion bars usually consisting of in excess of 90% gold, which is subsequently refined by a third party to gold bullion. The Company sells gold doré produced at Marigold and Seabee primarily to banks, and sells gold doré produced at Çöpler to the Central Bank of Türkiye. Puna produces silver, lead and zinc concentrates, which are sold to smelters or traders for further refining.

During 2024, sales of gold doré accounted for 67% of revenue, with 30% sold to Canadian Imperial Bank of Commerce (“CIBC”) and 13% sold to Asahi Refining. During 2023, sales of gold doré accounted for 80% of revenue, with 31% sold to Central Bank of Türkiye and 33% to CIBC. During 2022, sales of gold doré accounted for 82% of revenue, with 31% sold to Central Bank of Türkiye, 28% to CIBC and 16% to Bank of Montreal.

The Company sells lead and zinc concentrate with high silver content, through contractual arrangements with smelters and traders located in Asia and Europe. The concentrates are sold under supply contracts updated annually or as needed through spot sales, with processing fees based on the demand for the concentrates in the global marketplace.

The Company’s product revenue by category for the following years was as follows:

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

Product Revenue (1) | 2024 | | 2023 | | 2022 |

| Gold | 67 | % | | 80 | % | | 82 | % |

| Silver | 27 | % | | 15 | % | | 14 | % |

| Lead | 5 | % | | 3 | % | | 3 | % |

| Zinc | — | % | | 1 | % | | 1 | % |

Other (2) | 1 | % | | 1 | % | | — | % |

(1) The Company also realizes de minimis revenue from copper.

(2) Other revenue includes: changes in the fair value of concentrate trade receivables due to changes in silver and base metal prices; and silver and copper by-product revenue arising from the production and sale of gold doré.

For information on the mineral resources and mineral reserves for each operating asset, see Item 2, “Proven and Probable Reserve Estimates” and “Resource Estimates.”

The market prices of gold and silver are key drivers of the Company’s profitability. The prices of gold and silver can fluctuate widely and are affected by a number of macroeconomic factors, including global or regional consumption patterns, the supply of, and demand for gold and silver, interest rates, exchange rates, inflation or deflation, and the political and economic conditions of major gold- and silver-producing and gold- and silver-consuming countries throughout the world. Importantly, the price of gold and silver can be impacted by their role as safe havens during periods of market turmoil and as defense against the perceived inflationary impacts and currency depreciation caused by the responses of governments and central banking authorities to various economic threats. See Item 1A. Risk Factors, for further information.

The London Bullion Market Association (“LBMA”) average gold and silver prices for the following years were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, | | |

| | 2024 | | 2023 | | 2022 | | | | |

| LBMA Average Gold Prices Per Ounce | | $ | 2,387 | | $ | 1,943 | | $ | 1,800 | | | | |

| LBMA Average Silver Prices Per Ounce | | $ | 28.25 | | $ | 23.39 | | $ | 21.73 | | | | |

See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, below, for further information relating to metal prices.

For further details, see “Consolidated Results” and “Results of Operations” in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Competition

The precious and base metals mineral exploration and mining business is competitive. Competition with other mining and exploration companies is significant and is primarily for: mineral properties that can be developed and produced economically; technical experts that can find, develop and mine such mineral properties; labor to operate the mineral properties; and capital to finance exploration, development and operations. Many larger competitors have additional financial and technical resources available to them. If the Company is unsuccessful in acquiring or retaining the required technical, financial or personnel resources, the Company may not be able to replace mineral reserves, maintain production or grow. See Item 1A. Risk Factors for further information.

Licenses and Concessions

Other than operating licenses for our mining and processing facilities, there are no third party patents, licenses or franchises material to our business. However, we conduct our mining and exploration activities pursuant to concessions granted by, or under contracts with, the host government, including the United States, Canada, Argentina, and Türkiye. The concessions and contracts are subject to the political risks associated with the host country. Additionally, community reaction to our presence, which can be influenced by the manner in which we operate our mine, address human capital considerations, focus on environmental and sustainability concerns and other factors may impact our ability to continue to operate in a jurisdiction and could impact our ability to gain a license or franchise to operate in a new jurisdiction. See Item 1A. Risk Factors for further information.

Condition of Physical Assets and Insurance

Our business is capital intensive and requires ongoing capital investment for the replacement, modernization or expansion of equipment and facilities. See Results of Consolidated Operations and Liquidity and Capital Resources within Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, for further information.

We maintain insurance policies against property loss and business interruption and insure against risks that are typical in the operation of our business, in amounts that we believe to be reasonable. Such insurance, however, contains exclusions and limitations on coverage, particularly with respect to environmental liability and political risk. There can be no assurance that claims would be paid under such insurance policies in connection with a particular event. Additionally, any insurance recovery which the Company may receive may not be adequate to cover the total losses and liabilities resulting from a particular event, including, but not limited to, the Çöpler Incident or the temporary closure of the Seabee mine during the third quarter of 2024 as a result of forest fires in the vicinity of the mine. At this time, we do not expect our potential insurance coverage will fully cover the losses and liabilities that are expected to result from the Çöpler Incident, and we have not determined if they will be adequate to cover the losses and liabilities that are expected to result from the temporary closure of Seabee, if at all. See Item 1A. Risk Factors, below for further information.

Environmental, Social and Governance (“ESG”)

The Company’s approach to environmental and social development is underpinned by the goal of minimizing the impact of our operations to the environment and leaving a positive legacy in the communities where the Company operates. For the Company, being a responsible corporate citizen means protecting the natural environment associated with its business activities, providing a safe workplace and work processes for its employees and contractors, and investing in the communities where the Company operates in an effort to enhance the lives of those who live and work in these communities beyond the life of its operations. The Company takes a long-term view of its corporate responsibility, which is reflected in the policies that guide the Company’s business decisions, and in its corporate culture that fosters safe and ethical behavior across all levels of the Company.

The Company’s Environmental & Sustainability Policy defines the organization’s commitments to responsible environmental stewardship and to the health and welfare of the people and communities in which the Company operates. The policy is designed to guide the Company in advancing each of those commitments. The Company publishes an ESG and Sustainability Report, which outlines the Company’s approach to sustainability across a range of areas and summarizes the Company’s sustainability performance. The Company’s Environmental & Sustainability Policy and its ESG and Sustainability Data are available on the Company’s website.

The Company’s Board of Directors (the “Board”) has also established a Technical, Safety and Sustainability Committee (the “TSS Committee”) that, as part of its mandate, is responsible for reviewing the Company’s safety, health, security, risk, environment, community relations and sustainability policies and practices, and monitoring the Company’s performance in these areas. Additionally, under the TSS Committee charter, the TSS Committee reviews significant incidents relating to these areas. The TSS Committee’s charter is available on the Company’s website.

Producing precious metals is an energy-intensive business, resulting in carbon emissions. The Company’s operations are subject to a range of risks related to transitioning the business to meet regulatory, societal and investor expectations for operating in a low-carbon economy. See Item 1A. Risk Factors, below for further information.

Community Engagement

The Company’s community relations program is based on open and continuous communication with the members of communities located in its areas of operation. The Company takes a shared-value approach to local development activities to promote sustainable long-term economic and social benefits. In addition, the Company strives to ensure that local stakeholders have an opportunity for input and dialogue. Projects aimed at assisting and advancing the Company’s communities include training and employment, development of infrastructure and support for education and medical services, among others. At all times, the Company works to be a partner in the long-term sustainability of the communities in which it operates. In addition to direct investments made by SSR Mining, the Company also invests in the local communities surrounding its operations by supporting education, social programs and infrastructure projects.

Environmental Regulations

The Company’s activities are subject to extensive laws and regulations governing the protection of the environment and natural resources in all jurisdictions where the Company operates throughout the exploration, development and production stages of a mining property. These laws address, among other things, emissions into the air and air quality, discharges into water and water quality, management of waste, management and disposal of solid and hazardous substances, protection of natural resources, fisheries and wildlife protection, antiquities, endangered species, noise and use and reclamation of lands disturbed by mining operations.

The Company is required to obtain governmental permits and, in some instances, provide bonding requirements under federal, state, or provincial air, water quality, and mine reclamation rules and permits. Violations of environmental laws are subject to civil sanctions and, in some cases, criminal sanctions, including the suspension or revocation of permits. Additionally, environmental laws in the countries in which the Company operates require that the Company periodically perform environmental impact studies and updates at its mines.

Turkish government officials have stated that there has been no recordable contamination to local soil, water or air in the sampling locations resulting from the displaced heap leach material in connection with the Çöpler Incident. The Company continues to work with the Ministry of Environment, Urbanization and Climate Change of Türkiye on remediation of the affected areas at Çöpler. See Item 1A. Risk Factors, below for further information.

Reclamation and Remediation

The Company’s mining, exploration and development activities are subject to various federal, provincial, state and municipal laws and regulations relating to the protection of the environment, including requirements for closure and reclamation of mining properties. The Company has certain reclamation obligations at its mineral properties, including Çöpler, Marigold, Seabee and Puna. Reclamation obligations may be backed by bonds or other financial assurances held by the relevant jurisdictional authority. As required by the Company’s environmental permits, all closure plans are periodically updated. The Company accrues remediation costs when it is probable that an obligation has been incurred and the cost can be reasonably estimated. In addition to the remediation costs, estimates may include ongoing care, maintenance, and monitoring costs. The Company recorded reclamation and remediation costs of approximately $272.9 million during 2024 as a result of the Çöpler Incident.

The financial and operational effect of environmental protection requirements on the capital expenditures and earnings of each mineral property are not significantly different than that of similar sized mines in the same jurisdiction, are provided for through bonds and other financial assurance instruments and therefore should not have a negative effect on the Company’s competitive position in the future. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, for further information regarding closure and reclamation cost estimates.

Human Capital Management

Employees and Contractors

As of December 31, 2024, the Company employed approximately 2,300 full-time employees and 1,200 contract employees throughout the United States, Canada, Argentina and Türkiye.

Certain of the Company’s employees in Türkiye and Argentina are represented by a union. As of December 31, 2024, approximately 32% of the Company’s workforce were represented by a union.

Diversity and Inclusion

The Company recognizes that a workforce composed of many individuals with a mix of skills, experience, perspectives, backgrounds and characteristics leads to a more robust understanding of opportunities, issues and risks, and to stronger decision-making. Given the broad geographic footprint of the Company’s operations, we benefit from a meaningfully diverse workforce. The Board also recognizes that a diverse board of directors makes prudent business sense and makes for better oversight and corporate governance and is committed to a merit-based process, which is based on objective criteria, solicits multiple perspectives and is free of conscious or unconscious bias and discrimination, for the identification and selection of nominees to the Board. The Company is a member of the Catalyst Accord 2022 and the 30% Club Canada. These initiatives are aimed at accelerating the advancement of women in the workplace with a target goal of at least 30% representation of women on public-company boards. Over 44% of the current independent Board members self-identify as being “diverse.”

The Company has adopted a Diversity Policy, and the Company’s diversity initiatives are overseen by the Corporate Governance and Nominating Committee at the Board level and by the Compensation and Leadership Development Committee across the Company. The Diversity Policy is reviewed annually and is available on the Company’s website. In addition, the Company’s Code of Business Conduct and Ethics (the “Code of Conduct”), available on the Company's website, promotes and supports diversity and inclusion.

Health and Safety

The Company acknowledges that there are inherent risks associated with the Company’s business and, through proactive risk management, continuously strives to maximize the safety of its operations and minimize and control health and safety risks.

The Company’s safety framework emphasizes effective risk-centered management systems, positive and effective work cultures and proactive leadership. This approach balances the human and technical aspects of safety by blending leadership behaviors with traditional management activities to create a safe, productive culture. The Company ensures that its workers understand their individual roles and contributions to safe production and a safe workplace, maintaining safety awareness, recognizing hazards and assessing risk in their daily activities. The technical aspects of safety are addressed through established systems, policies and procedures describing how risk and controls are managed to reduce the risk of harm to workers. Performance measurement and accountability provides feedback and maintains focus on continuous improvement.

Human Rights

As part of the Company’s commitment to being a responsible corporate citizen, the Company recognizes the important role and responsibility it has in respecting the human rights of its stakeholders. The Company has adopted a Human Rights Policy, available on the Company’s website, which is aligned with the United Nations Guiding Principles on Business and Human Rights, the United Nations Global Compact, and the Organization for Economic Cooperation and Development Guidelines for Multinational Enterprises. This includes support and respect for the human rights expressed in the International Bill of Human Rights and the principles concerning fundamental rights set out in the International Labour Organization’s Declaration on Fundamental Principles and Rights at Work.

Available Information

SSR Mining Inc. was incorporated in British Columbia, Canada in 2005 and its predecessor companies date back to 1946. The corporate office is located at Suite 1300 - 6900 E. Layton Ave Denver, Colorado 80237. SSR Mining’s common shares are listed on the Nasdaq Global Select Market (“Nasdaq”) and the Toronto Stock Exchange (“TSX”) under the trading symbol “SSRM.” The Company’s CHESS depositary interests (“CDIs”) are listed under the ticker symbol “SSR” on Australian Securities Exchange (“ASX”).

General information about the Company is available through the Company’s website at https://www.ssrmining.com. The Company’s press releases and filings with the SEC in the United States and on SEDAR+ in Canada are available free of charge within the Investors section of the Company’s website at https://ir.ssrmining.com/investors. In addition, the SEC maintains an internet site that contains reports, proxy and information statements and other information regarding issuers, such as the Company, that are filed electronically with the SEC. The address of that website is https://www.sec.gov. The documents that the Company files under Canadian securities law requirements are available on SEDAR+ at the following address https://sedarplus.ca. The information on or linked to the Company’s website is neither a part of nor incorporated by reference in this Annual Report or any of the Company’s other SEC filings or filings made on SEDAR+. All references to www.ssrmining.com in this Annual Report are inactive textual references only and information contained at that website is not incorporated herein and does not constitute a part of this Annual Report.

ITEM 1A. RISK FACTORS

Certain statements contained in this report (including information incorporated by reference herein) are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are intended to be covered by the safe harbor provided for under these sections. Forward looking statements can be identified with words such as “may,” “will,” “could,” “should,” “expect,” “plan,” “anticipate,” “believe,” “intend,” “estimate,” “projects,” “predict,” “potential,” “continue” and similar expressions, as well as statements written in the future tense. When made, forward-looking statements are based on information known to management at such time and/or management’s good faith belief with respect to future events. Such statements are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the Company’s forward-looking statements. Many of these factors are beyond the Company’s ability to control or predict. Given these uncertainties, readers are cautioned not to place undue reliance on forward-looking statements. Forward-looking statements include, without limitation: all information related to the Çöpler Incident, including any statements about the impact of the Çöpler Incident on our business, financial condition, results of operations and cash flow, affected individuals and the surrounding community, forecasts and outlook; timing, production, cost, operating and capital expenditure guidance; the Company’s intention to return excess attributable free cash flow to shareholders; the timing and implementation of the Company’s dividend policy; the implementation of any share buyback program; statements regarding plans or expectations for the declaration of future dividends and the amount thereof; future cash costs and all-in sustaining costs (“AISC”) per ounce of gold, silver and other metals sold; the prices of gold, silver, copper, lead, zinc and other metals; mineral resources, mineral reserves, realization of mineral reserves, and the existence or realization of mineral resource estimates; the Company’s ability to discover new areas of mineralization; the timing and extent of capital investment at the Company’s operations; the timing of production and production levels and the results of the Company’s exploration and development programs; current financial resources being sufficient to carry out plans, commitments and business requirements for the next twelve months; movements in commodity prices not impacting the value of any financial instruments; estimated production rates for gold, silver and other metals produced by the Company; the estimated cost of sustaining capital; availability of sufficient financing; receipt of regulatory approvals; the timing of studies, announcements, and analysis; the timing of construction and development of proposed mines and process facilities; ongoing or future development plans and capital replacement; estimates of expected or anticipated economic returns from the Company’s mining projects, including future sales of metals, concentrate or other products produced by the Company and the timing thereof; the Company’s plans and expectations for its properties and operations; the Company's ability to efficiently integrate acquired mines and businesses and to manage the costs related to any such integration, or to retain key technical, professional or management personnel; and all other timing, exploration, development, operational, financial, budgetary, economic, legal, social, environmental, regulatory, and political matters that may influence or be influenced by future events or conditions.

Such forward-looking information and statements are based on a number of material factors and assumptions, including, but not limited to, timing, exploration, development, operational, financial, budgetary, economic, legal, social, geopolitical, regulatory and political factors that may influence future events or conditions. The above list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements and information, and such statements and information will not be updated to reflect events or circumstances arising after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

Risk Factor Summary

The Company is subject to a variety of risks and uncertainties which, if any such risk actually occurs, could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flow. You should carefully consider the risks presented in this section, together with the information included in other sections of this Annual Report. Such risks are not the only ones faced by the Company and additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect the Company’s business and the effect could be material. The following is a summary of the principal risks faced by the Company, including, but not limited to:

Risks Related to the Çöpler Incident:

•As a result of the Çöpler Incident, the Company is subject to new and ongoing risks.

Risks Related to the Company’s Operations and Business:

•The Company’s production, development plans and cost estimates may vary and/or not be achieved.

•Changes in the market prices of gold, silver and other metals, which in the past have fluctuated widely, will affect the Company’s operations.

•The Company’s estimates of mineral reserves and mineral resources ("MRMR") are based on interpretation and assumptions and may yield less mineral production under actual conditions than is currently estimated.

•The Company may be unable to replace its mineral reserves or acquire additional commercially mineable mineral rights.

•The Company faces intense competition in the mining industry.

•Increased operating and capital costs could affect the Company’s profitability.

•The Company is subject to supply chain disruptions and transportation risks.

•The Company’s operations may be adversely affected by rising energy prices or energy shortages.

•Continuation of the Company’s mining production is dependent on the availability of sufficient water supplies to support our mining operations.

•The Company may be exposed to future development risks.

•Land reclamation, mine closure and remediation requirements and costs may be burdensome and actual environmental and asset retirement obligations may exceed estimates and reserves.

•The Company is subject to information systems security threats and other risks.

•The Company’s joint venture interests are subject to risks.

•The Company’s interest in deferred consideration received from divestitures may not be fully realized.

•Reputation loss may result in decreased investor confidence, increased challenges in developing and maintaining community relations and an impediment to the Company’s overall ability to advance its business and projects.

•The Company’s insurance coverage does not cover all of the Company’s potential losses, liabilities and damages related to its business and certain risks are uninsured and uninsurable.

•The Company is exposed to market and/or counterparty risks related to the sale of its concentrates and metals.

•Public health crises have, and could in the future, adversely affect the Company’s business.

Financial Risks and Risks Related to Our Indebtedness:

•General economic conditions may adversely affect the Company’s growth and profitability.

•The Company may be adversely affected by fluctuations in foreign exchange rates.

•Inflation may have a material adverse effect on results of operations.

•The Company is subject to risks associated with hedging activities.

•Future funding requirements may affect the Company’s business or its ability to develop mineral properties, complete exploration and development programs, pay cash dividends or engage in share repurchase transactions.

•The Company may be unable to generate sufficient cash to fund its operations or service its debt.

•The Company’s indebtedness or lack of liquidity may impair the financial health of the Company.

Risks Related to Our Industry and the Jurisdictions in Which We Operate:

•Mining is inherently risky and subject to conditions and events beyond the Company’s control.

•Political or economic instability or unexpected regulatory change in the countries where the Company’s mineral properties are located could adversely affect its business.

•Suitable infrastructure may not be available or damage to existing infrastructure may occur.

•Mining companies are increasingly required to consider and provide benefits to the communities and countries in which they operate in order to maintain operations.

•Indigenous peoples’ title claims and rights to consultation and accommodation may affect the Company’s existing operations as well as development projects and future acquisitions.

•Civil disobedience in certain of the countries where the Company’s mineral properties are located could adversely affect its business.

•The Company and the mining industry face geotechnical challenges, which could adversely impact our production and profitability.

Risks Related to Our Personnel:

•Certain of the Company’s directors and/or officers also serve, or may serve, as directors of other companies involved in natural resource exploration and development, and consequently there exists the possibility for these directors and/or officers to be in a position of conflict.

•The Company could be subject to potential labor unrest or other labor disturbances.

•The Company is dependent on its ability to recruit and retain qualified personnel.

•The Company relies on contractors to conduct a significant portion of its operations and construction projects.

Risks Related to Governmental Regulation and Legal Proceedings:

•The Company is subject to significant governmental regulations.

•The Company is subject to extensive permitting requirements.

•The Company’s activities are subject to environmental laws and regulations that may increase the Company’s costs and restrict its operations.

•Compliance with emerging climate change regulations could result in significant costs and climate change may present physical risks to a mining company’s operations.

•The Company may be required by human rights laws to take actions that delay the Company’s operations or the advancement of its projects.

•The Company’s mineral properties may be subject to uncertain title.

•The Company is subject to claims and legal proceedings that arise in the ordinary course of business.

•The Company is subject to assessment by taxation authorities in multiple jurisdictions that arise in the ordinary course of business.

Risks Related to Ownership of Company Equity:

•The Company’s common shares are publicly traded and are subject to various factors that have historically made the Company’s common share price volatile.

•Holders of our common shares may not receive dividends.

•Future sales or issuances of equity securities could decrease the value of the Company’s common shares, dilute investors’ voting power and reduce the Company’s earnings per share.

Risks Related to the Çöpler Incident

As a result of the Çöpler Incident, we are exposed to a number of new risks, described below, that will have an uncertain and potentially adverse impact on our business, consolidated results of operations, financial position and cash flows, which could be material. In addition, a number of existing risks identified in other sections of this report will be exacerbated as a result of the Çöpler Incident.

Actual and potential losses and liability resulting from the Çöpler Incident could have a material adverse effect on our financial condition, liquidity, cash flows and results of operations.

On February 13, 2024, the Company suspended operations at Çöpler as a result of a significant slip on the heap leach pad. We cannot determine at this time when operations will resume at Çöpler, if at all. The Çöpler Incident is expected to have a significant, ongoing impact on the Company’s cash flows, liquidity and capital resources, even after we are permitted to resume operations. Although the Company currently estimates its existing capital resources and the cash flows generated from its other mine properties will continue to be sufficient to meet the Company’s ongoing cash flow, capital expenditure and other business requirements for the foreseeable future, there are a number of factors that may change the Company’s estimate or that the Company was not able to estimate and, therefore, the Company’s expected cash requirements may increase. These factors include, among other things, the cost of the remediation of the Çöpler site, the potential legal and regulatory obligations and associated fines and penalties that may arise, the extent of third-party liability, the availability and extent of property and liability insurance and the impact of debt covenants and other contractual obligations. If the Company’s estimates of the costs and other expenditures that it will incur in connection with the Çöpler Incident are incorrect or insufficient, it may result in a material adverse effect on Company’s liquidity, cash flows, results of operations and business.

Ongoing investigations and remediation in connection with the Çöpler Incident could have a material adverse effect on the operation.

The Türkiye governmental authorities continue their investigations into the Çöpler Incident. The Türkiye government has arrested and charged certain of our employees as part of this investigation. As a result of the investigations, the Company may face, among other things, criminal and/or civil sanction, which may include significant fines, orders for remediation and restitution and loss of permits and/or the ability to operate Çöpler. The Türkiye government has revoked Çöpler’s environmental and operating permits in connection with the incident, and the Company cannot predict when or if such permits will be reinstated and under what conditions.

Additionally, planning and engineering for the long-term storage and remediation of the displaced heap leach material is ongoing and subject to direction and approval of the applicable Turkish authorities. We cannot predict the final remediation or storage plans, the timing of any such approval or completion of such plans and the costs associated with these plans. Actual costs of long-term storage and remediation may vary significantly from our current estimates, which could have a material adverse impact on our cash flows, results of operations or financial condition.

The Çöpler Incident may result in environmental contamination of the surrounding area.

While we are not aware of any recordable contamination to local soil, water or air from the Çöpler Incident from the sampling to date, there can be no guarantee that there will not be any future environmental impact on the areas surrounding the site or that the Turkish authorities or third parties will not assert that the Çöpler Incident resulted in contamination or some other environmental impact. If the incident resulted (or if applicable Turkish authorities determine that it resulted) in environmental contamination, we may become financially responsible for the remediation, penalties and liable for claims by affected parties, which could be significant. If we are held responsible for an environmental contamination, that could affect, among other things, our ability to operate in Türkiye, our reputation and our business more generally, and results of operations and financial condition.

The Company’s production, development plans and cost estimates for Çöpler may not be achieved.

The Company has prepared estimates of future production, operating costs and capital costs for Çöpler and the Technical Report Summary for Çöpler contains estimates of future production, development plans, operating and capital costs and other economic and technical estimates. As a result of the Çöpler Incident, the Company may not be able to achieve these estimates during the time frame it has set out, if at all, as the operating and economic assumptions, along with the mineral reserves, mineral resources, cost estimates and other findings contained in such TRS, may no longer be accurate. When more information is available regarding the operations at Çöpler, the TRS may need to be amended, and we are not certain as to when this will occur. The Company cannot estimate at this time when Çöpler will resume operations, which may have a material adverse impact on the Company’s future cash flows, profitability, results of operations and financial condition.

Additionally, on August 20, 2024, the local Turkish court issued a decision cancelling the Çöpler mine's environmental impact assessment, which was approved in 2021 (the "2021 EIA"), due to insufficiencies in the 2021 EIA approval process. On February 11, 2025, the Turkish Council of State affirmed the decision of the lower court. As a result of the cancellation of the 2021 EIA, the operating guidelines at Çöpler revert to those outlined in the Company’s prior Environmental Impact Assessment, which was issued in 2014 (the “2014 EIA”), which, among other considerations, prescribes a lower throughput rate for the sulfide plant operations. If the Company is permitted to resume operations at Çöpler, it may not be able to operate the mine under the parameters of the 2014 EIA, if at all. There can be no guarantee that the mine, if operations are permitted to resume, will be able to operate under the parameters of the 2021 EIA in the future, if at all. At this time, the Company cannot fully assess the entire scope of the impact of operating under the 2014 EIA.

Covenants and events of default in our debt instruments could limit our ability to borrow funds under such instruments and adversely affect our liquidity and such debt instruments allow for acceleration of repayment of our borrowings under certain conditions.

Our Second Amended Credit Agreement and the indenture governing the 2019 Notes (as defined herein) contain a number of covenants and events of default, which may be implicated by the Çöpler Incident. Although we do not believe the Çöpler Incident was a material adverse event under the terms of the Second Amended Credit Agreement or that there has been a violation of any covenant or an event of default, if it was later determined that the Çöpler Incident or an event that occurs as a result of the Çöpler Incident, such as an action by Turkish authorities, is a material adverse event or the resulting events triggered a violation of a covenant or an event of default, the lenders under the Second Amended Credit Agreement may be permitted to terminate all commitments to extend credit under the Second Amended Credit Agreement and, if we had outstanding borrowings, to exercise remedies against the collateral pledged to secure the obligations thereunder. As of the date of this report, we do not have any outstanding borrowings under our Second Amended Credit Agreement. The Second Amended Credit Agreement also requires us to maintain specified financial ratios and satisfy other financial tests and make certain representations and warranties whenever we are borrowing under the Second Amended Credit Agreement. Our ability to meet those financial ratios and tests and to be able to make such required representations and warranties may be negatively affected by the Çöpler Incident and we may not be permitted to borrow under the Second Amended Credit Agreement. If our lenders terminate all commitments to extend further credit or restrict our ability to borrow under the Second Amended Credit Agreement, we may not have access to adequate financial resources to fund our business and planned capital expenditures, which may have a material adverse impact on our cash flows, results of operations or financial condition and liquidity position. In addition, our noteholders may choose to assert that the Çöpler Incident has resulted in an event of default or certain other conditions that would permit them to accelerate the repayment of the 2019 Notes, and we may not have sufficient assets to repay that indebtedness. We do not believe that the Çöpler Incident has resulted in any events or conditions that would permit the noteholders to seek to accelerate the 2019 Notes.

Responding to the Çöpler Incident, including remediation effort requires significant management attention.

The health, safety, and well-being of our employees, contractors, and their families following the Çöpler Incident, responding to inquiries from the government of Türkiye and progressing the remediation and the steps necessary to resume operations at Çöpler have been key areas of focus and the priority of the management team since the Çöpler Incident. Our management team will continue to be focused on the remediation effort and responding to the legal and other claims to which the Company has and may in the future become subject. This will continue to require substantial management time and attention, which may divert management from overseeing the operations of the Company’s other mines and focusing on developing and executing on our overall strategy.

The Çöpler Incident could impact the ongoing development of Hod Maden.

While the Çöpler Incident has not impacted our development plan with respect to Hod Maden to date, there can be no guarantee that direct or indirect impacts will not arise in the future. As a result of the Çöpler Incident, the Türkiye government could rescind or revoke permits associated with our Hod Maden development or otherwise prevent us from completing or participating in the development of Hod Maden. The ability to continue with the development or participation in the Hod Maden project may have a material adverse impact on the Company's cash flows, results of operations or financial condition or our ongoing joint venture relationships and operations in Türkiye.

The Company’s access to capital in a timely manner and on acceptable terms may be negatively impacted by the Çöpler Incident.

Although we currently do not believe that we will need to seek external sources of funding to operate our business, fund the remediation of the Çöpler Incident, or support the additional costs and other liabilities that could arise over the next 12 months, the Çöpler Incident may negatively impact our access to capital through available sources of debt and equity financings in a timely manner and on acceptable terms. Additionally, to the extent we are put on a “watch” or our credit rating is downgraded by one or more rating agencies as a result of an event related to the Çöpler Incident our access to capital will be further impacted. If our current expectations regarding our need for external sources of financing are inaccurate and we are unable to access external sources of financing for our business, the remediation of the Çöpler Incident and the associated costs and potential liabilities, our financial condition, liquidity, cash flows and results of operations may be adversely impacted.

The Company’s insurance coverage may not cover all of the Company’s potential losses, liabilities and damages related to Çöpler Incident.

As a result of the Çöpler Incident, the Company and certain of its current and former officers and directors is subject to securities class actions in the United States and Canada, and it is possible that the Çöpler Incident could result in significant additional claims for damages, including, potentially, claims for loss of life and property or environmental damage, or securities losses. We have no ability to estimate the timing, extent or the significance of any of these claims. Therefore, these events could materially affect the Company’s business, reputation, financial condition and results of operations. If the Company is held responsible for loss of life, environmental and other property damage caused by the Çöpler Incident, it could have a material impact on the Company’s financial condition, liquidity, cash flows and results of operations. The Company has insurance coverage for third party claims, but the aggregate losses associated with the Çöpler Incident could significantly exceed the amount of available insurance coverage. The Company is incurring legal and consulting fees to manage current and potential lawsuits and financial implications related to the Çöpler Incident, and those amounts are likely to be material, and are in addition to the claims for damages, which could be significant.

Additionally, to the extent that any liability that we may have in connection with the Çöpler Incident is or may be indemnifiable by a third-party, such third-party may not carry sufficient insurance coverage or have sufficient funds to meet the full extent of any such indemnification claim. There is no guarantee that the Company could recover from any third-party an amount sufficient to cover the aggregate losses associated with the Çöpler Incident, if the Company can recover any amount at all.

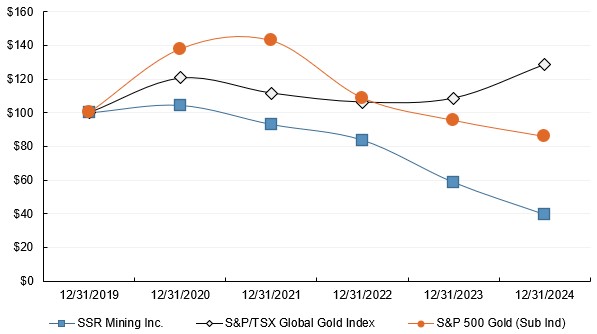

The Company’s share price may continue to be volatile.

As a result of the Çöpler Incident, our share price has experienced a significant decline on both Nasdaq and the TSX and experienced increased trading volume volatility. It is likely that our share price will continue to be volatile as a result of decreased investor confidence in the Company and the release of new information about the Çöpler Incident or the Company, including, among other things,updates regarding the timing or likelihood of returning to operations at Çöpler, actions taken by the Türkiye government, lawsuits or claims filed against us, or financial implications arising from the incident. Additionally, media reports and social media stories, whether or not substantiated, could have an impact on our share price. These factors could subject the market price of our common shares to price fluctuations regardless of our underlying operating performance. As a result, our share price may continue to be volatile.

Risks Related to the Company’s Operations and Business

The Company’s production, development plans and cost estimates may vary and/or not be achieved.

The Company has prepared estimates of future production, operating costs and capital costs for its Çöpler, Marigold, Seabee and Puna operating mines, and the Company’s technical studies and reports for the Company’s operating mines and other projects, as may be amended or updated from time to time, contain estimates of future production, development plans, operating and capital costs and other economic and technical estimates relating to these projects. These estimates are based on a variety of factors and assumptions and there is no assurance that such production, plans, costs or other estimates will be achieved. Actual production, costs and financial returns may vary significantly from the estimates depending on a variety of factors, many of which are not within the Company’s control. For example, on February 13, 2024, the Company suspended operations at Çöpler as a result of the Çöpler Incident and the Company is unable to reasonably estimate the full impact of the Çöpler Incident on the longer-term financial position, results of operations and cash flows at this time. These factors primarily include, but are not limited to: actual ore mined varying from estimates of grade, tonnage, dilution, metallurgical and other characteristics; short-term operating factors, such as the need for sequential development of ore bodies and the processing of new or different ore grades from those planned; mine failures, slope failures, equipment failures or accidents and the exposure for related claims of loss and liabilities; and encountering unusual or unexpected geological conditions. Failure to achieve estimates or material increases in costs could have a material adverse impact on the Company’s future cash flows, profitability, results of operations and financial condition.

Changes in the market prices of gold, silver and other metals, which in the past have fluctuated widely, will affect the Company’s operations.

The Company’s profitability, long-term viability and the economic feasibility of its mineral properties depend, in large part, on the market price of gold, silver, copper, lead and zinc. The market prices for these metals are volatile and are affected by numerous factors beyond the Company’s control, including:

•global or regional consumption patterns;

•the supply of, and demand for, these metals;

•gold sales, purchases or leasing by governments and central banks;

•the monetary policies employed by the world’s major central banks;

•the fiscal policies employed by the world’s major industrialized economies;

•recession or reduced economic activity in the United States and other industrialized or developing countries;

•speculative short positions taken by significant investors or traders in gold, silver, lead, zinc or other metals;

•forward sales by producers in hedging or similar transactions;

•the availability and costs of metal substitutes;

•decreased industrial, jewelry, base metal or investment demand;

•increased import and export taxes;

•inflation and/or expectations for inflation;

•other political and economic conditions, including interest rates and currency values; and

•changing investor or consumer sentiment, including in connection with transition to a low-carbon economy, investor interest in crypto currencies and other investment alternatives and other factors.

The Company cannot predict the effect of these factors on metal prices. For example, average gold prices for 2024 were $2,387 per ounce (2023: $1,943; 2022: $1,800), average silver prices for 2024 were $28.25 per ounce (2023: $23.39; 2022: $21.73), average lead prices for 2024 were $0.93 per pound (2023: $0.99; 2022: $0.91) and average zinc prices for 2024 were $1.14 per pound (2023: $0.92; 2022: $1.60). Any decline in our realized prices adversely impacts our revenues, net income and operating cash flows.

In addition, a decrease in the market price of gold, silver and other metals would affect the profitability of Çöpler, Marigold, Seabee and Puna and could affect the Company’s ability to finance the exploration and development of any of the Company’s other mineral properties. The market price of gold, silver and other metals may not remain at current levels. In particular, an increase in worldwide supply, and consequential downward pressure on prices, may result over the longer term from increased gold or silver production from mines developed or expanded as a result of current metal price levels.

The Company’s estimates of mineral reserves and mineral resources are based on interpretation and assumptions and may yield less mineral production under actual conditions than is currently estimated.

There are numerous uncertainties inherent in estimating mineral reserves and grades of mineralization, including many factors beyond the Company’s control. In making determinations about whether to advance any of the Company’s projects to development or to mine existing mineral reserves, the Company must rely upon estimated calculations as to the mineral reserves and grades of mineralization on its properties. Until ore is actually mined and processed, mineral reserves and grades of mineralization must be considered as estimates only.

These estimates are imprecise and depend upon geological interpretation and statistical inferences drawn from drilling and sampling, which may prove to be unreliable. The Company cannot assure that mineral reserves, mineral resources or other mineralization estimates will be accurate, or that mineralization can be mined or processed profitably. Actual operating and capital cost and economic returns on projects may differ significantly from original estimates. Further, it may take many years from the initial phases of exploration until commencement of production, during which time, the economic feasibility of production may change.

Any material changes in mineral reserves estimates and grades of mineralization will affect the economic viability of placing a property into production and a property’s return on capital. The Company’s estimates of mineral reserves and mineral resources have been determined and valued based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for gold, silver and other precious metals may render portions of the Company’s mineralization uneconomic and result in reduced reported mineral reserves or mineral resources.

Any material reductions in estimates of mineralization, or of the Company’s ability to extract this mineralization, including estimates made in the technical report summaries for the Company’s operating properties and additional projects, could have a material adverse effect on the Company’s results of operations or financial condition. There is no assurance that mineral recovery rates achieved in small scale tests will be duplicated in large scale tests under on-site conditions or in production scale. If our reserve estimations are required to be revised using significantly lower gold, silver, copper, zinc, lead and other metal prices as a result of a decrease in commodity prices, increases in operating costs, reductions in metallurgical recovery or other modifying factors, this could result in material write-downs of our investment in mining properties or increased amortization, reclamation and closure charges.

Additionally, the Company is required to comply with the disclosure standards under Regulation S-K Subpart 1300 (“S-K 1300”) of the U.S. securities laws. The provisions of this disclosure standard are intended to align with those used in the other major mining regulatory jurisdictions, however certain provisions of the disclosure standards may be more restrictive and/or prescriptive, or require a presentation of different information, than those used in other regulatory jurisdictions. Such variation may result in disclosures by the Company that differ, potentially materially, from those of our competitors and non-U.S. joint-venture partner.

The Company may be unable to replace its mineral reserves or acquire additional commercially mineable mineral rights.

The Company must continually replace its depleted mineral reserves to maintain production levels over the long term. Mineral reserves can be replaced by expanding known ore bodies, locating new deposits or making acquisitions. There is a risk that depletion of the Company’s mineral reserves will not be offset by discoveries or acquisitions. The Company’s mineral base may decline if mineral reserves are mined without adequate replacement and the Company may not be able to sustain production beyond the current mine lives, based on current production rates. If, as a result of the Çöpler Incident, the Company is unable to resume operations at Çöpler in a timely manner or at all, the Company may consider acquisitions to replace the mineral reserves associated with Çöpler. The Company may not have adequate financial resources or otherwise be able to fund any such acquisition as a result of a number of factors, including the Çöpler Incident, and/or any such acquisition may not replace the mineral reserves associated with Çöpler. If the Company’s mineral reserves are not replaced either by the development of additional mineral reserves and/or additions to mineral reserves, there may be an adverse impact on the Company’s future cash flows, earnings, results of operations and financial condition, and this may be compounded by requirements to expend funds for reclamation and decommissioning.

The Company’s future growth and productivity will also depend, in part, on its ability to identify and acquire additional commercially mineable mineral rights, and on the costs and results of continued exploration and potential development programs. Mineral exploration is highly speculative in nature and is frequently non-productive. Most exploration projects do not result in the discovery of commercially mineable ore deposits, and there is no assurance that any anticipated or estimated level of recovery of mineral reserves will be realized or that any identified mineral deposit will ever qualify as a commercially mineable (or viable) orebody that can be legally and economically exploited. Once a site with mineralization is discovered, it may take several years from the initial phases of drilling until production is possible, during which time the economic feasibility of production may change. Substantial expenditures are also required to establish proven and/or probable mineral reserves and to construct mining and processing facilities. Material changes in mineral reserves, grades, stripping ratios or recovery rates may affect the economic viability of any project. As a result, there is no assurance that current or future exploration programs will be successful.

As part of the Company’s business strategy, it has sought and will continue to seek new operating, development and exploration opportunities in the mining industry. The Company may consider, from time to time, the acquisition of ore reserves from third parties. Such acquisitions are typically based on an analysis of a variety of factors including, but not limited to, historical operating results, estimates of and assumptions regarding the extent of ore reserves, the timing of production from such reserves, cash and other operating costs and the Company’s assumptions for future gold, silver, copper, zinc or lead prices or other mineral prices. In connection with any acquisitions, the Company may rely on data and reports prepared by third parties, which may contain information or data that the Company is unable to independently verify or confirm. Other than historical operating results, all of these factors are uncertain and may have an impact on the Company’s revenue, cash flow and other operating issues, as well as contributing to the uncertainties related to the process used to estimate ore reserves.

In pursuit of such opportunities, the Company may fail to select appropriate acquisition candidates or negotiate acceptable arrangements, including arrangements to finance acquisitions or integrate the acquired opportunities into the Company’s existing business. The Company cannot provide assurance that it can complete any acquisition or business arrangement that it pursues, or is pursuing, on favorable terms, if at all, or that any acquisitions or business arrangements completed will ultimately benefit its business. Further, any acquisition the Company makes will require a significant amount of time and attention of the Company’s management, as well as resources that otherwise could be spent on the operation and development of its existing business. In addition, there may be intense competition for the acquisition of ore reserves and/or attractive mining properties. There can be no assurance that the Company will be able to successfully acquire any desired ore reserves or mining properties.

Any future acquisitions would be accompanied by risks, including the quality of the mineral deposit acquired proving to be lower than expected; the difficulty of assimilating the operations and personnel of any acquired companies; the potential disruption of its ongoing business; the inability of management to realize anticipated synergies and maximize its financial and strategic position; the failure to maintain uniform standards, controls, procedures and policies; and the potential for unknown or unanticipated liabilities associated with acquired assets and businesses, including tax, environmental or other liabilities. There can be no assurance that any business or assets acquired in the future will prove to be profitable, that the Company will be able to integrate the acquired businesses or assets successfully or that the Company will identify all potential liabilities during due diligence. Any of these factors could have a material adverse effect on its business, expansion, results of operations and financial condition.

The Company faces intense competition in the mining industry.

The mining industry is intensely competitive in all phases and the Company competes with many companies, several of which possess greater financial and technical resources than itself. Competition in the base and precious metals mining industry is primarily for mineral rich properties which can be developed and produced economically; the human resources and technical expertise to find, develop, and operate such properties; the labor to operate the properties; and the capital for the purpose of funding such properties. Many competitors not only explore for and mine precious metals, but also conduct refining and marketing operations on a world-wide basis. Such competition may result in the Company being unable to acquire desired properties, recruit or retain qualified employees or acquire the capital necessary to fund its operations and develop its properties. Existing or future competition in the mining industry could materially adversely affect the Company’s prospects for mineral exploration and success in the future.

Increased operating and capital costs could affect the Company’s profitability.

Costs at any particular mining location are subject to variation due to a number of factors, such as variable ore grade, changing metallurgy and revisions to mine plans in response to the physical shape and location of the ore body, as well as the age and utilization rates for the mining and processing related facilities and equipment. In addition, costs are affected by the price and availability of input commodities, such as fuel, electricity, labor, chemical reagents, explosives, steel, concrete and mining and processing related equipment and facilities. Commodity costs are, at times, subject to volatile price movements, including increases that could make production at certain operations less profitable. Further, changes in laws and regulations can affect commodity prices, uses and transport. Reported costs may also be affected by changes in accounting standards. A material increase in costs at any significant location could have a significant effect on our profitability and operating cash flow.

We could have significant increases in capital and operating costs over the next several years in connection with the development of new projects and in the sustaining and/or expansion of existing mining and processing operations. In addition, it is expected that the Company will incur significant costs related to remediation of the Çöpler Incident and be exposed to significant claims for loss and damage, which may not be covered by insurance. Costs associated with capital expenditures may increase in the future as a result of factors beyond our control. Increased capital expenditures may have an adverse effect on the profitability of and cash flow generated from existing operations, as well as the economic returns anticipated from new projects.

The Company is subject to supply chain disruptions and transportation risks.

The Company’s ability to mine, process and sell products is critical to our operations. The Company’s operations depend on the continued availability and delivery of supplies of consumables, including, but not limited to, diesel, tires, sodium cyanide and reagents, and capital items to operate efficiently. In addition to consumables, continuous supplies of energy, water, equipment and labor are critical to the Company’s operations, the costs of which are subject to worldwide supply and demand as well as other factors beyond the Company’s control. Supply chain disruptions, power outages, labor disputes and/or strikes, geopolitical activity, health emergencies in the regions where we operate, weather events and natural disasters could seriously harm the Company’s operations as well as the operations of the Company’s customers and suppliers. Further, the Company’s suppliers may experience capacity limitations in their own operations or may elect to reduce or eliminate certain product lines, all of which is beyond the Company’s control but could have a material adverse effect on the Company’s operations and revenue.

Likewise, disruptions in the transportation and delivery of consumables and other products may impact our ability to sell our own products and deliver them to our customers on time. Transportation of any good is subject to numerous risks including, but not limited to, roadblocks, terrorism, interruption by domesticated and non-domesticated herding animals, theft, weather conditions, environmental liabilities in the event of an accident or spill, inability to transport oversized loads, personal injury and loss of life. In addition, the costs of transporting materials and products through our chain of sourcing and production may increase, and such increases could be significant. If the Company experiences prolonged disruption to the delivery of such consumables, the Company’s production efficiency and ability to effectively complete capital projects requiring such deliveries may be reduced. Separately, if a seasonal access route, including, but not limited to, the seasonal ice road constructed to access Seabee, becomes unusable or unavailable for any reason, the Company may incur significant costs to arrange alternative transportation, if such alternative transportation is even available or possible. There can be no assurance that these transportation risks will not have an adverse effect on any site, particularly Seabee, and therefore on the Company’s profitability.

Failure to take adequate steps to mitigate the likelihood or potential impact of such disruptions, or to effectively manage such disruptions if they occur, could adversely affect our business and results of operations, as well as require additional resources to restore our global supply chain. To address these risks, generally, the Company seeks to have many sources of supply for key materials in order to avoid significant dependence on any one or a few suppliers, however, prices charged for such key materials by suppliers may differ substantially and obtaining key materials from different suppliers may impact the Company’s costs. Although there can be no assurance that such mitigation efforts will prevent future difficulty in obtaining sufficient and timely delivery of certain materials, the Company believes it has adequate programs to ensure a reliable supply of key materials.

The Company’s operations may be adversely affected by rising energy prices or energy shortages.

Our mining operations and development projects require significant amounts of energy, including purchased electricity, diesel fuel, natural gas, propane and coal. Increasing global demand for energy, concerns about nuclear power and the limited growth of new energy sources are affecting the price and supply of energy. A variety of factors, including higher energy usage in emerging market economies, actual and proposed taxation of carbon emissions as well as concerns surrounding continued and new unrest and conflict in the Middle East and Ukraine, could result in increased demand or limited supply of energy and/or sharply escalating prices. Additionally, changes in energy laws and regulations in various jurisdictions may impact energy dispatch rules and the ability to access energy and sell excess energy. Limitations on energy supply and increased energy prices could negatively impact our operating costs and cash flow.