Exhibit 1

Oshkosh Corporation

A COMPANY IN NEED OF A NEW DIRECTION

Special note regarding this presentation

2

T H I S P R E S E N T A T I O N I N C L U D E S I N F O R M A T I O N B A S E D O N D A T A F O U N D I N F I L I N G S W I T H T H E S E C , I N D E P E N D E N T I N D U S T R Y P U B L I C A T I O N S A N D O T H E R S O U R C E S . A L T H O U G H W E B E L I E V E T H A T T H E D A T A I S R E L I A B L E , W E D O N O T G U A R A N T E E T H E A C C U R A C Y O R C O M P L E T E N E S S O F T H I S

I N F O R M A T I O N A N D H A V E N O T I N D E P E N D E N T L Y V E R I F I E D A N Y S U C H I N F O R M A T I O N . W E H A V E N O T S O U G H T , N O R H A V E W E R E C E I V E D , P E R M I S S I O N F R O M A N Y T H I R D—P A R T Y T O I N C L U D E T H E I R I N F O R M A T I O N I N T H I S P R E S E N T A T I O N .

M A N Y O F T H E S T A T E M E N T S I N T H I S P R E S E N T A T I O N R E F L E C T O U R S U B J E C T I V E B E L I E F . A L T H O U G H W E H A V E R E V I E W E D A N D A N A L Y Z E D T H E I N F O R M A T I O N T H A T H A S I N F O R M E D O U R O P I N I O N S , W E D O N O T G U A R A N T E E T H E A C C U R A C Y O F A N Y S U C H B E L I E F S .

S E C T I O N S O F T H I S P R E S E N T A T I O N R E F E R T O T H E E X P E R I E N C E O F O U R N O M I N E E S A S D I R E C T O R S O R O F F I C E R S O F O T H E R C O M P A N I E S . W E B E L I E V E T H E I R E X P E R I E N C E A T T H E S E C O M P A N I E S W A S A S U C C E S S A N D R E S U L T E D I N A N I N C R E A S E I N S H A R E H O L D E R V A L U E T H A T B E N E F I T E D A L L

S H A R E H O L D E R S . H O W E V E R , T H E S U C C E S S A T T H E S E C O M P A N I E S I S N O T N E C E S S A R I L Y I N D I C A T I V E O F F U T U R E R E S U L T S A T O S H K O S H I F O U R N O M I N E E S W E R E T O B E E L E C T E D T O T H E O S H K O S H B O A R D O F D I R E C T O R S .

A L L S T O C K H O L D E R S O F O S H K O S H A R E A D V I S E D T O R E A D T H E D E F I N I T I V E P R O X Y S T A T E M E N T , T H E G O L D P R O X Y C A R D A N D O T H E R D O C U M E N T S R E L A T E D T O T H E S O L I C I T A T I O N O F P R O X I E S B Y T H E P A R T I C I P A N T S F R O M T H E S T O C K H O L D E R S O F O S H K O S H F O R U S E A T T H E 2 0 1 2 A N N U A L M E E T I N G O F S H A R E H O L D E R S O F O S H K O S H B E C A U S E T H E Y C O N T A I N I M P O R T A N T I N F O R M A T I O N . T H E D E F I N I T I V E P R O X Y S T A T E M E N T A N D F O R M O F P R O X Y A L O N G W I T H O T H E R R E L E V A N T D O C U M E N T S A R E

A V A I L A B L E A T N O C H A R G E O N T H E S E C ‘ S W E B S I T E A T H T T P : / / W W W . S E C . G O V O R B Y C O N T A C T I N G D . F . K I N G & C O . , I N C . B Y T E L E P H O N E A T T H E F O L L O W I N G N U M B E R S : S T O C K H O L D E R S C A L L T O L L —F R E E : ( 8 0 0 ) 6 5 9—5 5 5 0 A N D B A N K S A N D B R O K E R A G E F I R M S C A L L : ( 2 1 2 ) 2 6 9—5 5 5 0 . I N A D D I T I O N , T H E P A R T I C I P A N T S W I L L P R O V I D E C O P I E S O F T H E

D E F I N I T I V E P R O X Y S T A T E M E N T W I T H O U T C H A R G E U P O N R E Q U E S T . I N F O R M A T I O N R E L A T I N G T O T H E P A R T I C I P A N T S I S C O N T A I N E D I N T H E D E F I N I T I V E S C H E D U L E 1 4 A F I L E D B Y T H E P A R T I C I P A N T S W I T H T H E S E C O N D E C E M B E R 1 5 , 2 0 1 1 ..

Oshkosh Corporation

3

EXECUTIVE SUMMARY

Executive Summary – How we got here

4

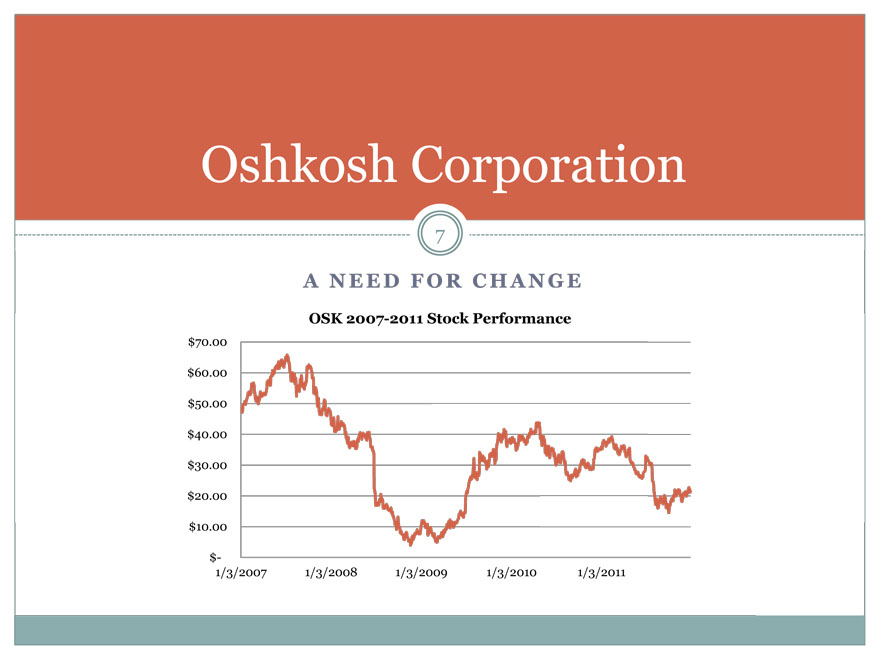

A decline in OSK stock price from $65.76 in 2007 to the low $20s today despite substantial cash generated in the last five years due to several factors

?In 2006 Oshkosh borrowed over $3 billion to purchase JLG, a construction equipment company which we believe was a poor strategic fit at too high a price; which was then hit by the housing downturn and recession

?Oshkosh recently began production of the FMTV, a product which represents up to 40% of their defense segment and is currently generating a loss

?Despite the company’s restructuring efforts the traditional non-defense businesses combined to generate negative operating income in 2011

?Weak end markets have exacerbated these problems

Oshkosh recently announced a new strategic initiative, MOVE, which we believe is insufficient to deal with current challenges the company faces

Executive Summary – Where do we go from here

5

We believe that Oshkosh needs a new strategic plan to generate the maximum shareholder value over the coming years

JLG – Explore alternatives including a potential sale of JLG

Defense – Position the company to participate in future industry consolidation

Core Business – Use the weak economy to consolidate smaller companies in Oshkosh business lines and consider expanding to other niche vehicle markets

Develop a new international growth plan including acquisitions, joint ventures, and organic actions to bring Oshkosh core products to developing markets

{ Focus on streamlined manufacturing and integration of existing operations

Executive Summary – Where do we go from here

6

Icahn purchased a 10% stake in Oshkosh and is currently the company’s largest shareholder After several discussions with management we decided the best course of action was to nominate a minority slate of new directors with a breadth of experience and who have familiarity in dealing with a company in crisis We believe that with the right board leadership Oshkosh shares could prove undervalued at current prices We have conducted the analysis contained herein and drawn conclusions solely on the basis of public information, focusing on some but not all of the company’s product lines and businesses

Oshkosh Corporation

7

A NEED FOR CHANGE

OSK 2007-2011 Stock Performance

$70.00 $60.00 $50.00 $40.00 $30.00 $20.00 $10.00

$-

1/3/2007 1/3/2008 1/3/2009 1/3/2010 1/3/2011

A need for change

8

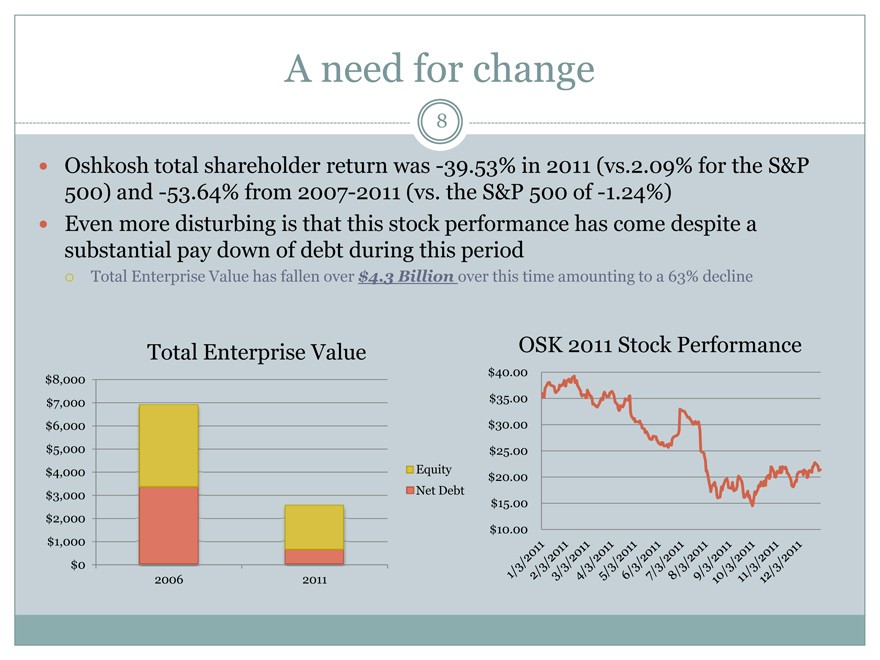

Oshkosh total shareholder return was -39.53% in 2011 (vs.2.09% for the S&P 500) and -53.64% from 2007-2011 (vs. the S&P 500 of -1.24%) y Even more disturbing is that this stock performance has come despite a substantial pay down of debt during this period

??Total Enterprise Value has fallen over $4.3 Billion over this time amounting to a 63% decline

Total Enterprise Value

$8,000 $7,000 $6,000 $5,000 $4,000 $3,000 $2,000 $1,000 $0

2006 2011

Equity Net Debt

OSK 2011 Stock Performance

$40.00

$35.00

$30.00

$25.00

$20.00

$15.00

$10.00

A need for change

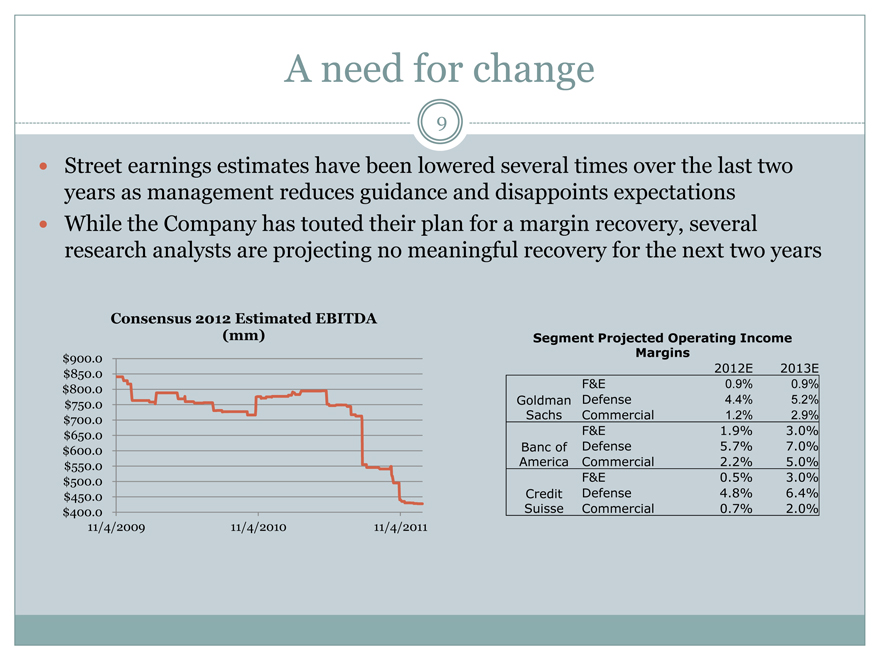

9

Street earnings estimates have been lowered several times over the last two years as management reduces guidance and disappoints expectations y While the Company has touted their plan for a margin recovery, several research analysts are projecting no meaningful recovery for the next two years

Consensus 2012 Estimated EBITDA (mm)

$900.0 $850.0 $800.0 $750.0 $700.0 $650.0 $600.0 $550.0 $500.0 $450.0 $400.0

11/4/2009 11/4/2010 11/4/2011

Segment Projected Operating Income Margins

2012E 2013E F&E 0.9% 0.9%

Goldman Defense 4.4% 5.2% Sachs Commercial 1.2% 2.9% F&E 1.9% 3.0% Banc of Defense 5.7% 7.0% America Commercial 2.2% 5.0% F&E 0.5% 3.0% Credit Defense 4.8% 6.4% Suisse Commercial 0.7% 2.0%

10

A need for change

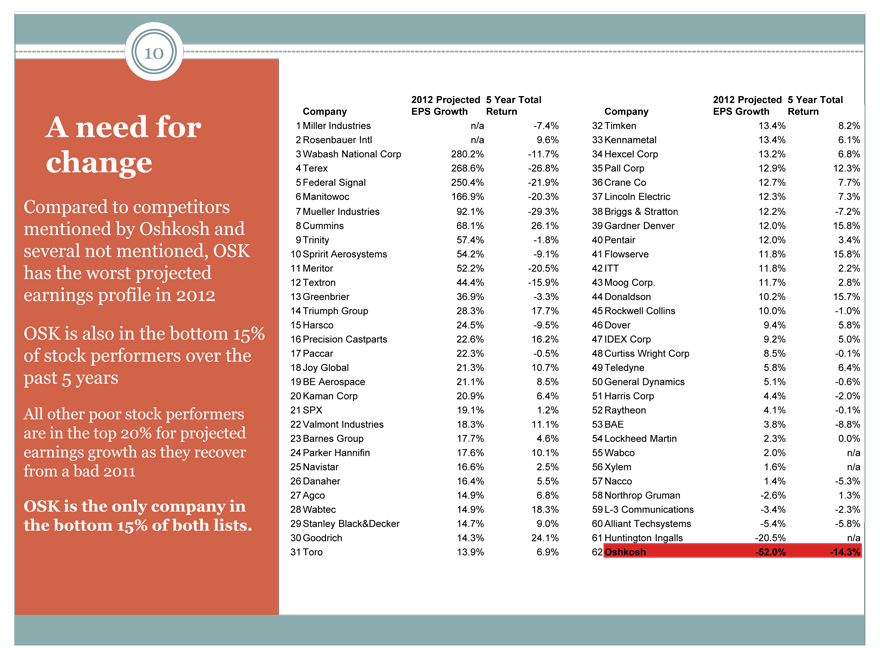

Compared to competitors mentioned by Oshkosh and several not mentioned, OSK has the worst projected earnings profile in 2012

OSK is also in the bottom 15% of stock performers over the past 5 years

All other poor stock performers are in the top 20% for projected earnings growth as they recover from a bad 2011

OSK is the only company in the bottom 15% of both lists.

2012 Projected 5 Year Total 2012 Projected 5 Year Total Company EPS Growth Return Company EPS Growth Return

1 Miller Industries n/a -7.4% 32 Timken 13.4% 8.2%

2 Rosenbauer Intl n/a 9.6% 33 Kennametal 13.4% 6.1%

3 Wabash National Corp 280.2% -11.7% 34 Hexcel Corp 13.2% 6.8%

4 Terex 268.6% -26.8% 35 Pall Corp 12.9% 12.3%

5 Federal Signal 250.4% -21.9% 36 Crane Co 12.7% 7.7%

6 Manitowoc 166.9% -20.3% 37 Lincoln Electric 12.3% 7.3%

7 Mueller Industries 92.1% -29.3% 38 Briggs & Stratton 12.2% -7.2%

8 Cummins 68.1% 26.1% 39 Gardner Denver 12.0% 15.8%

9 Trinity 57.4% -1.8% 40 Pentair 12.0% 3.4%

10 Spririt Aerosystems 54.2% -9.1% 41 Flowserve 11.8% 15.8%

11 Meritor 52.2% -20.5% 42 ITT 11.8% 2.2%

12 Textron 44.4% -15.9% 43 Moog Corp. 11.7% 2.8%

13 Greenbrier 36.9% -3.3% 44 Donaldson 10.2% 15.7%

14 Triumph Group 28.3% 17.7% 45 Rockwell Collins 10.0% -1.0%

15 Harsco 24.5% -9.5% 46 Dover 9.4% 5.8%

16 Precision Castparts 22.6% 16.2% 47 IDEX Corp 9.2% 5.0%

17 Paccar 22.3% -0.5% 48 Curtiss Wright Corp 8.5% -0.1%

18 Joy Global 21.3% 10.7% 49 Teledyne 5.8% 6.4%

19 BE Aerospace 21.1% 8.5% 50 General Dynamics 5.1% -0.6%

20 Kaman Corp 20.9% 6.4% 51 Harris Corp 4.4% -2.0%

21 SPX 19.1% 1.2% 52 Raytheon 4.1% -0.1%

22 Valmont Industries 18.3% 11.1% 53 BAE 3.8% -8.8%

23 Barnes Group 17.7% 4.6% 54 Lockheed Martin 2.3% 0.0%

24 Parker Hannifin 17.6% 10.1% 55 Wabco 2.0% n/a

25 Navistar 16.6% 2.5% 56 Xylem 1.6% n/a

26 Danaher 16.4% 5.5% 57 Nacco 1.4% -5.3%

27 Agco 14.9% 6.8% 58 Northrop Gruman -2.6% 1.3%

28 Wabtec 14.9% 18.3% 59 L-3 Communications -3.4% -2.3%

29 Stanley Black&Decker 14.7% 9.0% 60 Alliant Techsystems -5.4% -5.8%

30 Goodrich 14.3% 24.1% 61 Huntington Ingalls -20.5% n/a

31 Toro 13.9% 6.9% 62 Oshkosh -52.0% -14.3%

11

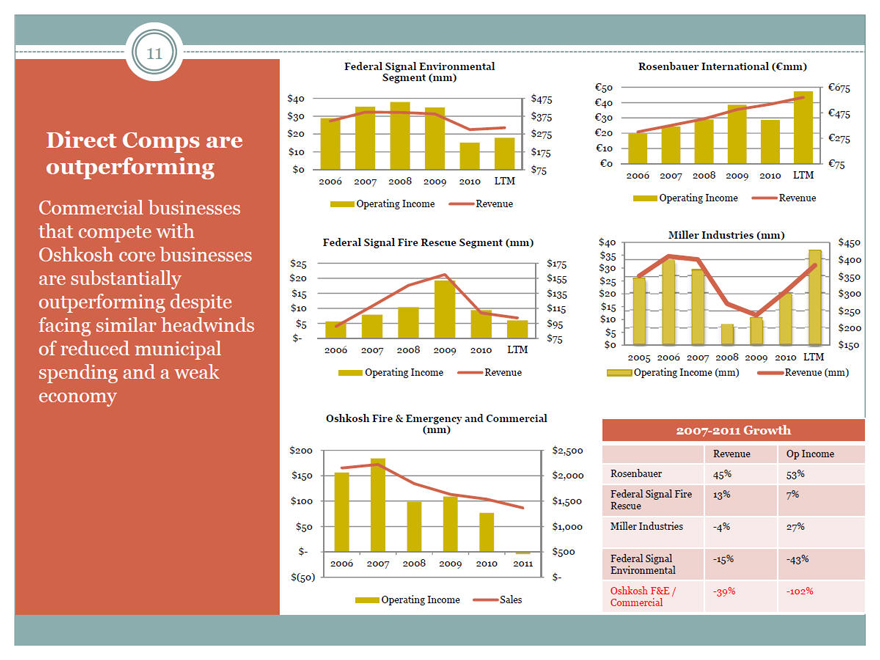

Direct Comps are outperforming

Commercial businesses that compete with Oshkosh core businesses are substantially outperforming despite facing similar headwinds of reduced municipal spending and a weak economy

Federal Signal Environmental Segment (mm)

$40 $475

$30 $375

$20 $275

$10 $175

$0 $75 2006 2007 2008 2009 2010 LTM

Operating Income Revenue

Federal Signal Fire Rescue Segment (mm)

$25 $175

$20 $155

$15 $135

$10 $115

$5 $95

$- $75 2006 2007 2008 2009 2010 LTM

Operating Income Revenue

Oshkosh Fire & Emergency and Commercial (mm)

$200 $150 $100 $50

$-

2006 2007 2008 2009 2010 2011 $(50)

Operating Income Sales

Rosenbauer International (€mm)

€50 €675 €40 €475 €30 €20 €275 €10

€0 €75 2006 2007 2008 2009 2010 LTM

Operating Income Revenue

Miller Industries (mm)

$40 $450

$35 $400

$30 $350 $25

$20 $300

$15 $250

$10 $200 $5

$0 $150 2005 2006 2007 2008 2009 2010 LTM

Operating Income (mm) Revenue (mm)

2007-2011 Growth

$2,500 Revenue Op Income

$2,000 Rosenbauer 45% 53%

Federal Signal Fire 13% 7%

$1,500 Rescue

$1,000 Miller Industries -4% 27%

$500 Federal Signal Environmental -15% -43%

$-Oshkosh F&ECommercial/ -39% -102%

Problems at Core businesses

12

Problems at JerrDan

JerrDan, a tow truck company was combined with JLG, a construction equipment company despite no apparent overlap in distribution

U JerrDan “network of 55 independent distributors” vs. JLG independent rental companies, 140 in house employees spread over 20 international sales and service offices, Caterpillar dealers under a CAT branded product, and SAME

Deutz-Fahr dealers under their own brand name

Dealerships which represent the primary distribution method have fallen from 93 in 2008 to 55 in 2011

The #1 towing company in the U.S., Miller Industries generated record operating profit in the LTM period

Problems at Fire & Emergency

This segment has seen the most extensive restructuring program in the company

U While revenue declined 33% from 2008-2011, Oshkosh consolidated 22 facilities into 7 (partially attributable to the removal of JerrDan and the sale of certain international businesses) U Despite this aggressive cost restructuring, operating income fell from $93.4 million to an $8.2 million operating loss U Productivity increases at the factory level from restructurings have not translated into higher, or even stable margins

Goldman Sachs has projected below 1% operating income margins in Fire & Emergency through 2013

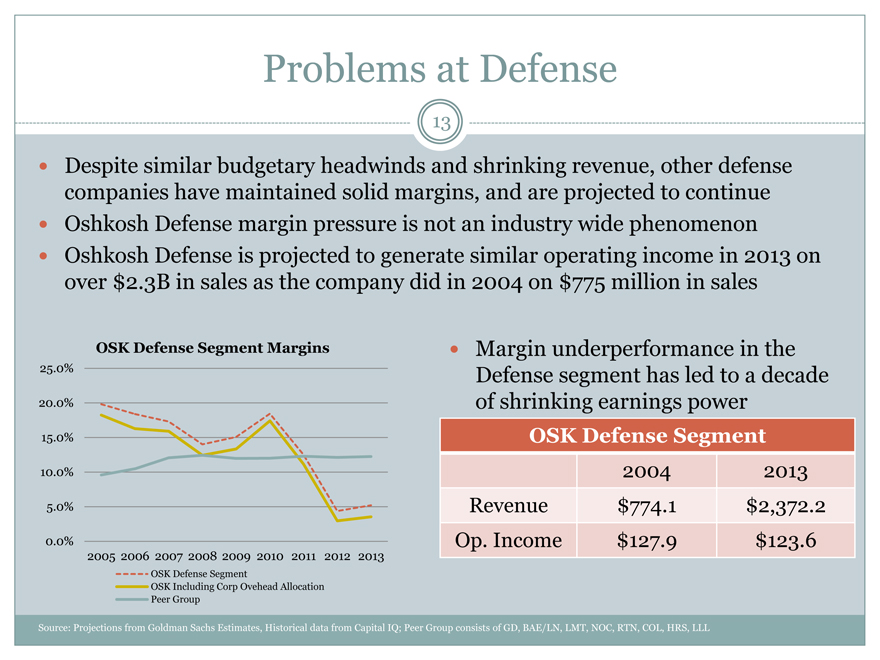

Problems at Defense

13

Despite similar budgetary headwinds and shrinking revenue, other defense companies have maintained solid margins, and are projected to continue y Oshkosh Defense margin pressure is not an industry wide phenomenon y Oshkosh Defense is projected to generate similar operating income in 2013 on over $2.3B in sales as the company did in 2004 on $775 million in sales

OSK Defense Segment Margins

25.0%

20.0%

15.0%

10.0% 5.0%

0.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013

OSK Defense Segment

OSK Including Corp Ovehead Allocation Peer Group

Margin underperformance in the Defense segment has led to a decade of shrinking earnings power

OSK Defense Segment

2004 2013 Revenue $774.1 $2,372.2 Op. Income $127.9 $123.6

Source: Projections from Goldman Sachs Estimates, Historical data from Capital IQ; Peer Group consists of GD, BAE/LN, LMT, NOC, RTN, COL, HRS, LLL

Oshkosh Corporation

14

IN 2006 OSHKOSH ACQUIRED JLG A MOVE THAT SIGNALED THE START OF A PERIOD OF

TURBULENCE AND VALUE DESTRUCTION

JLG – The turning point

15

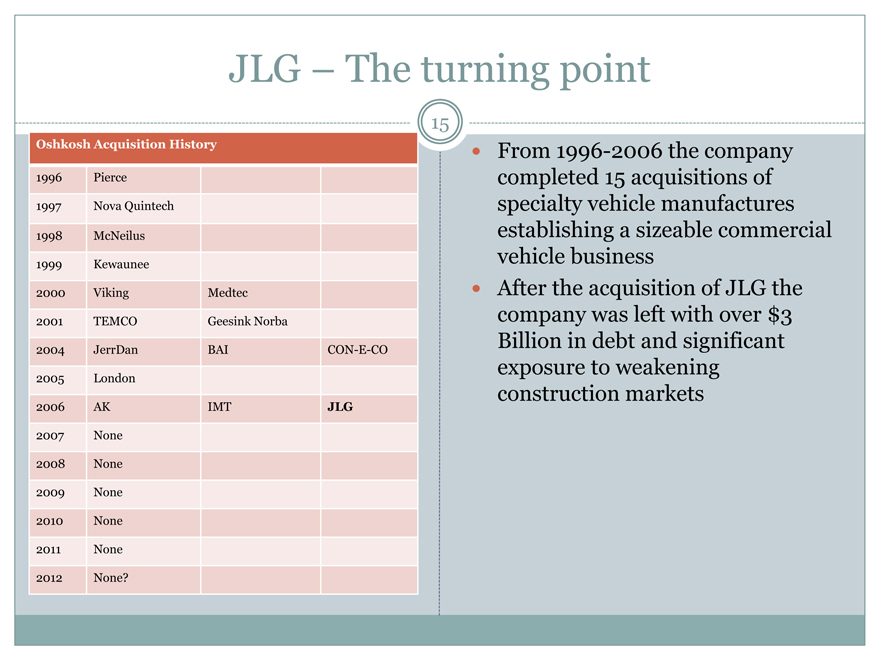

Oshkosh Acquisition History

1996 Pierce

1997 Nova Quintech 1998 McNeilus 1999 Kewaunee

2000 Viking Medtec

2001 TEMCO Geesink Norba

2004 JerrDan BAI CON-E-CO 2005 London 2006 AK IMT JLG 2007 None 2008 None 2009 None 2010 None 2011 None 2012 None

From 1996-2006 the company completed 15 acquisitions of specialty vehicle manufactures establishing a sizeable commercial vehicle business y After the acquisition of JLG the company was left with over $3 Billion in debt and significant exposure to weakening construction markets

JLG – The turning point

16

We believe Oshkosh overpaid for JLG

We believe JLG was the wrong deal, at the wrong price and the wrong time

The leverage, covenant defaults, operating losses and recovery have occupied management resources at a time when other Oshkosh businesses are challenged as well

Management should admit that they made a mistake in buying JLG and explore alternatives for the division

According to Goldman Sachs, JLG will represent almost 60% of segment level operating income for Oshkosh by 2013 y Analysts have suggested that JLG alone could be worth as much as $25 per share, more than the entire current market cap of the company

We believe shareholders will not fully capture the benefit of a recovering JLG if it is wrapped inside a defense/vehicle company with substantial cyclical and operational challenges

We believe shareholders will not fully capture the potential of the defense and vehicle segments if they lack capital and management focus while they are wrapped inside a construction equipment company

JLG – The turning point

17

JLG is a cyclical business in the early stages of recovery

Managing a recovery at JLG will likely drain limited management resources

Leaves in doubt a plan to rebuild a Jerrdan distribution network

While operating performance at JLG may improve along with the market, the strategic rationale for the acquisition appears flawed y Management continues to support the strategic value of this acquisition based on potential synergies and diversification benefits

Synergies are highly questionable

JLG has a separate customer base with separate distribution platform

The two largest rental equipment companies in the U.S. are in the midst of a merger, potentialy gaining substantial purchasing leverage over large suppliers

Distribution deals with Caterpillar and an Italian tractor manufacturer highlight the different distribution channels between construction equipment and specialty vehicles

Shareholders may be better off monetizing JLG to bolster the balance sheet and pursue more synergistic opportunities

JLG – The turning point

18

JLG may be worth more in the hands of another owner

Strategic buyers may be interested in expanding product offerings that can be sold through a single distribution channel

Financial buyers may be more willing to bet on the cycle and international expansion

We believe Oshkosh is worth more as a focused business with the capital and the capacity to grow in an integrated manner

A JLG sale would bolster the balance sheet and achieve management’s debt reduction goal

An unlevered Oshkosh would be free to return capital to shareholders or pursue synergistic acquisitions

A focused Oshkosh would be free to address the challenges in other core businesses

Post a JLG sale Oshkosh would have the flexibility to explore opportunities for a declining defense business

Oshkosh would have the capital to be a consolidator in the Defense and other specialty vehicle segments

Without unrelated businesses Oshkosh may be more attractive as a potential target for a strategic acquirer

Even if a sale now vs. later in the cycle does not generate the maximum gross proceeds, we believe it will provide the maximum positive impact for shareholders y We believe the Icahn board slate will immediately and objectively review all options for JLG

Oshkosh Corporation

19

THE MOVE STRATEGY: THE LATEST ATTEMPT TO PLACATE SHAREHOLDERS

MOVEing nowhere

20

For 10 years Oshkosh followed a simple operating strategy

Develop value added products

Cut costs and maintain lean cost operations

Make strategic acquisitions to grow and diversify the business

Bob Bohn 2/2/2007 “Our core growth strategies of leading in new product development, seeking operational excellence though lean initiatives and the pursuit of strategic acquisitions has served us well”

(Q1 2007 Earnings Call)

Oshkosh experienced declining revenue in their commercial segment as early as 2007, since then the downturn has spread to every product line y Since 2007 we believe the company has taken only minimal actions to mitigate or exploit these unprecedented challenges

MOVEing nowhere

21

Five years after volume declines began the Board conducted a “comprehensive strategic planning process” to address the situation

?The Board turned to consultants to “review, analyze, and assess our businesses and the competitive landscape”, with their help the company evaluated “a range of financial and strategic options and determined the best path forward to provide the greatest value for our shareholders” (12/12/11 letter to

shareholders)

After this process the Board along with Management endorsed a new strategic plan which we believe represents NO CHANGE AT ALL y We believe MOVE is simply the old strategy placed in a new format with a catchy acronym

MOVEing nowhere

22

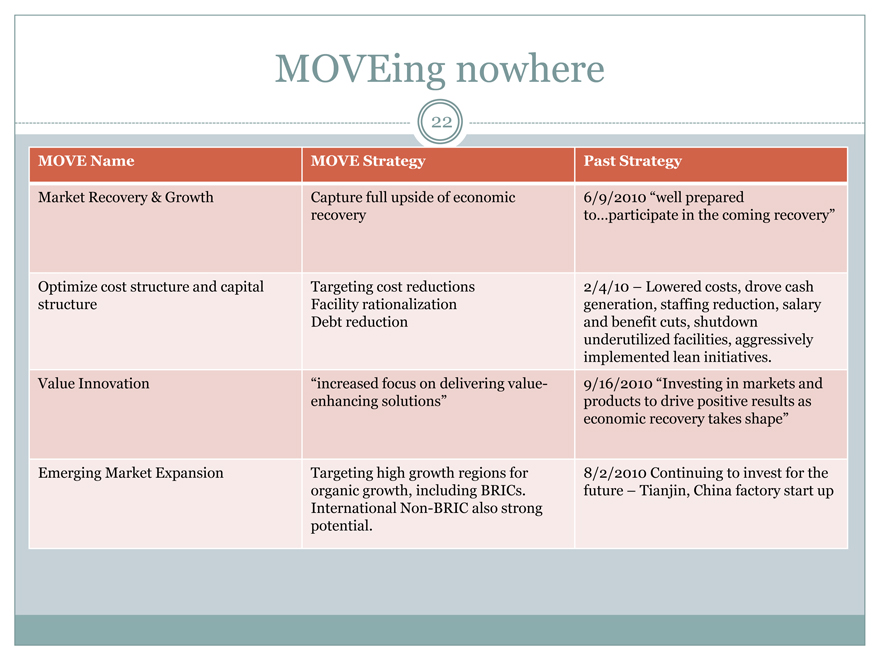

MOVE Name

MOVE Strategy

Past Strategy

Market Recovery & Growth

Capture full upside of economic

6/9/2010 “well prepared

recovery

to…participate in the coming recovery”

Optimize cost structure and capital

Targeting cost reductions

2/4/10 – Lowered costs, drove cash

structure

Facility rationalization

generation, staffing reduction, salary

Debt reduction

and benefit cuts, shutdown

underutilized facilities, aggressively

implemented lean initiatives.

Value Innovation

“increased focus on delivering value-

9/16/2010 “Investing in markets and

enhancing solutions”

products to drive positive results as

economic recovery takes shape”

Emerging Market Expansion

Targeting high growth regions for

8/2/2010 Continuing to invest for the

organic growth, including BRICs.

future – Tianjin, China factory start up

International Non-BRIC also strong

potential.

MOVEing nowhere

23

We believe that MOVE represents an attitude instead of a strategy that ignores the underlying problem and relies on a market recovery

?Waiting to see how things turn out is not a value maximizing strategy for shareholders

?We believe Oshkosh needs a plan to deal with and manage each business during a recession – not just wait for it to end

It appears management wants shareholders to wait indefinitely:

?”We don’t expect the domestic fire truck market to improve until fiscal 2013 at the earliest” Q42011 Earnings

Call

?”there remains little clarity on future US defense spending. What is clear, however, is that there will be cuts to future defense spending…” Q42011 Earnings Call

?”You know, how long can certain markets stay down? For example, in concrete, we’ve been down 90%, 95% in that market since 2006. They’re buying 500, 600 concrete mixers a year since then. By 2012, you’ve got to believe it’s starting to come back.” Q42010 Earnings Call

?”we expect weakness in the domestic concrete mixer market to continue into fiscal 2012 as we believe housing starts and other construction levels will remain weak for much of the fiscal year.” Q32011 Earnings call

MOVEing nowhere

24

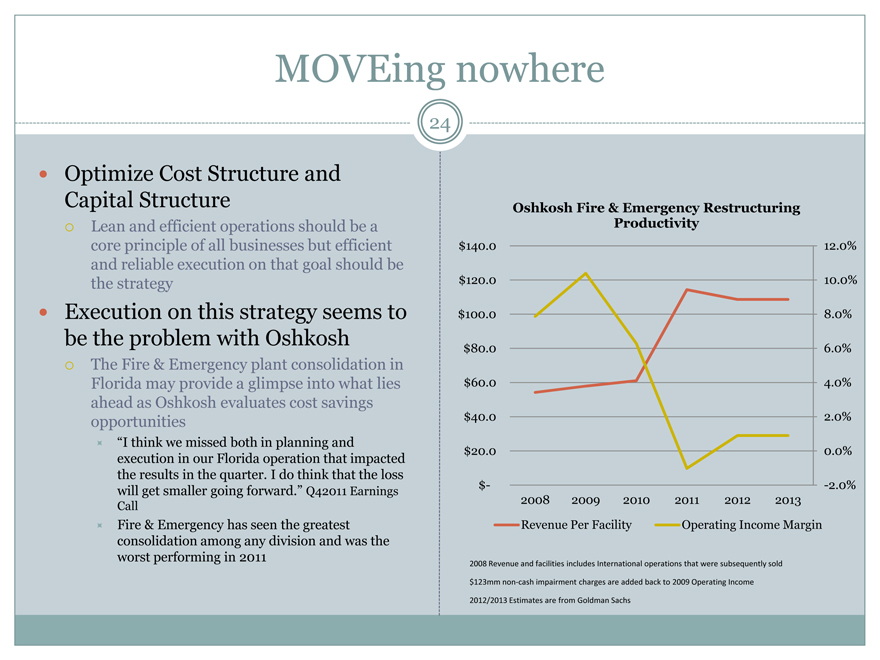

Optimize Cost Structure and Capital Structure

?Lean and efficient operations should be a core principle of all businesses but efficient and reliable execution on that goal should be the strategy

Execution on this strategy seems to be the problem with Oshkosh

?The Fire & Emergency plant consolidation in Florida may provide a glimpse into what lies ahead as Oshkosh evaluates cost savings opportunities

“I think we missed both in planning and execution in our Florida operation that impacted the results in the quarter. I do think that the loss will get smaller going forward.” Q42011 Earnings Call U Fire & Emergency has seen the greatest consolidation among any division and was the worst performing in 2011

Oshkosh Fire & Emergency Restructuring Productivity $140.0 12.0%

$120.0 10.0% $100.0 8.0% $80.0 6.0% $60.0 4.0% $40.0 2.0% $20.0 0.0%

$—2.0% 2008 2009 2010 2011 2012 2013 Revenue Per Facility Operating Income Margin

2008 Revenue and facilities includes International operations that were subsequently sold $123mm non? cash impairment charges are added back to 2009 Operating Income 2012/2013 Estimates are from Goldman Sachs

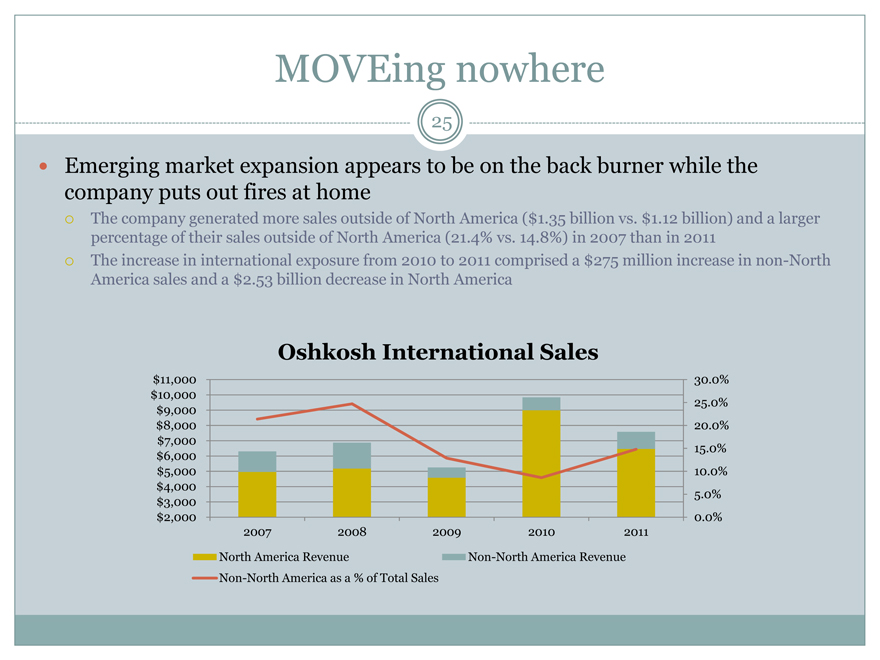

MOVEing nowhere

25

Emerging market expansion appears to be on the back burner while the company puts out fires at home

?The company generated more sales outside of North America ($1.35 billion vs. $1.12 billion) and a larger percentage of their sales outside of North America (21.4% vs. 14.8%) in 2007 than in 2011

?The increase in international exposure from 2010 to 2011 comprised a $275 million increase in non-North America sales and a $2.53 billion decrease in North America

Oshkosh International Sales

$11,000 30.0% $10,000 25.0% $9,000 $8,000 20.0% $7,000 15.0% $6,000 $5,000 10.0% $4,000 5.0% $3,000 $2,000 0.0% 2007 2008 2009 2010 2011 North America Revenue Non-North America Revenue Non-North America as a % of Total Sales

MOVEover

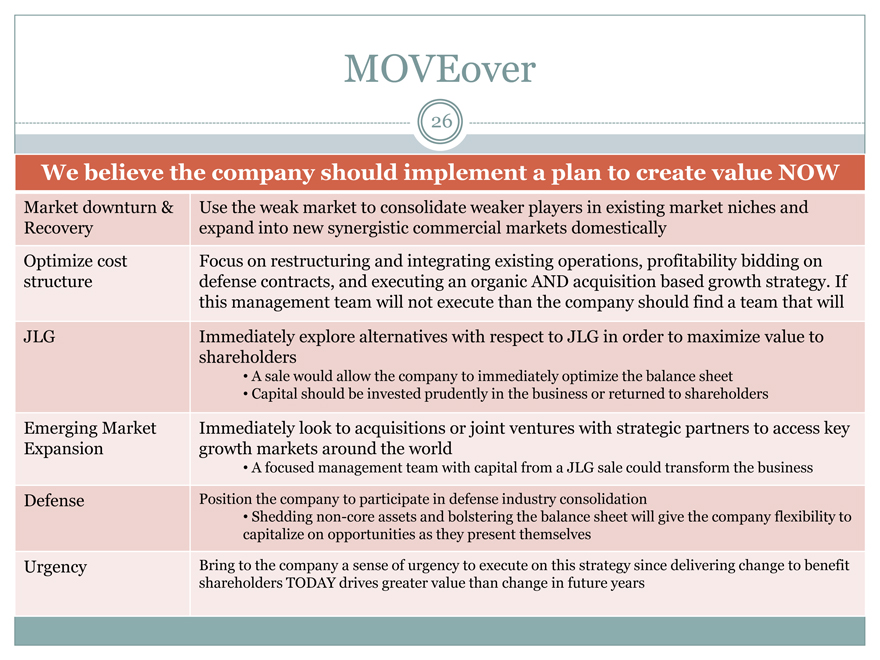

26

We believe the company should implement a plan to create value NOW

Market downturn & Use the weak market to consolidate weaker players in existing market niches and Recovery expand into new synergistic commercial markets domestically Optimize cost Focus on restructuring and integrating existing operations, profitability bidding on structure defense contracts, and executing an organic AND acquisition based growth strategy. If this management team will not execute than the company should find a team that will JLG Immediately explore alternatives with respect to JLG in order to maximize value to shareholders

• A sale would allow the company to immediately optimize the balance sheet

• Capital should be invested prudently in the business or returned to shareholders

Emerging Market Immediately look to acquisitions or joint ventures with strategic partners to access key Expansion growth markets around the world

• A focused management team with capital from a JLG sale could transform the business

Defense Position the company to participate in defense industry consolidation

• Shedding non-core assets and bolstering the balance sheet will give the company flexibility to capitalize on opportunities as they present themselves

Urgency Bring to the company a sense of urgency to execute on this strategy since delivering change to benefit shareholders TODAY drives greater value than change in future years

Oshkosh Corporation

27

AN ALARMING DETERIORATION IN PERFORMANCE AND PROFITABILITY IN THE

CORE BUSINESS: DEFENSE

Defense Failure

28

We believe that the core competency of a defense contractor should be to design products as the military wants them, and profitably bid the contracts y Over the past several years the company has established a very concerning track record of failure in the core defense business

?MRAP—While the company recovered and won the bid on the M-ATV, the company had two MRAP products fail to gain any traction, including one that did not meet survivability requirements

?JLTV – The company was kicked out of early rounds of technology demonstrations because they were the only company that delivered a hybrid-electric vehicle

?FMTV –The company underbid a huge contract and has been scrambling to turn it into a break even effort

FHTV constitutes a substantial portion of the Defense segment; given the FMTV experience, we do not believe that shareholders should be confident that the coming rebid will result in a positive outcome

Defense Failure

29

We believe that the FMTV illustrates the single largest problem with the future of this company

?The manner in which this contract was handled has caused us to doubt the company’s capability and profitability

They entered into the bidding process with two competitors who had substantial advantages over Oshkosh

?BAE had been producing FMTVs for years and required little or no capital to continue production and had experience with component prices and sourcing

?Navistar had a lower cost structure and substantial operating leverage through higher volume production facilities that manufacture commercial vehicles

Oshkosh reportedly bid 33% under the current price and underbid two companies with substantial advantages

?Navistar and BAE both filed a complaint suggesting, among other things, that Oshkosh pricing was unrealistic, that parts could not be delivered at the prices represented and that G&A was too low

?Navistar and BAE allegations turned out to be true and the compliant was upheld by the GAO

Defense Failure

30

Rather than accepting responsibility of the overly aggressive bid, management has offered a string of excuses

?”We experienced some start up issues in the program, typical with what would be expected for a program of this magnitude and complexity” Q12011 Earnings Call

?Errors in the technical data package

?Higher quality requirements than previous contracts

?”The iron removal system on this eco[ating] facility was undersized” Q32011 Earnings Call

?”We can go on all day talking about what we experience in the FMTV program. I mean, number one, we have a smart customer. They ordered 3 times — when they saw a good price they ordered 3 times the quantity right in advance of scheduled price increases in the contract, so they took advantage of that, that’s fine. We had new terms in this contract, we’re building somebody else’s technical data package that they weren’t even building to.” Q42011 Earnings Call

y We believe this unprofitable contract reflects management’s unrealistic expectations and poor planning as well as the board’s lack of oversight on a product that represents almost half of segment revenue

Defense Failure

31

This focus on fixing an unprofitable contract has distracted management from other parts of the business

”The FMTV production launch has consumed many of our resources, but we plan to devote more attention to [reviewing our manufacturing footprint] in the [next] quarter.”Q22011 Earnings Call

”We have meetings every morning and every afternoon to manage this program so it will be effective.” Q22011

Earnings Call

”We are going to tackle those [cost takeout opportunities] with urgency…We have slowed a little bit with the FMTV launch…But as we ramp up production and are successful at that, we will have more time and attention to these other cost reduction initiatives.”Q32011 Earnings Call

Defense Failure

32

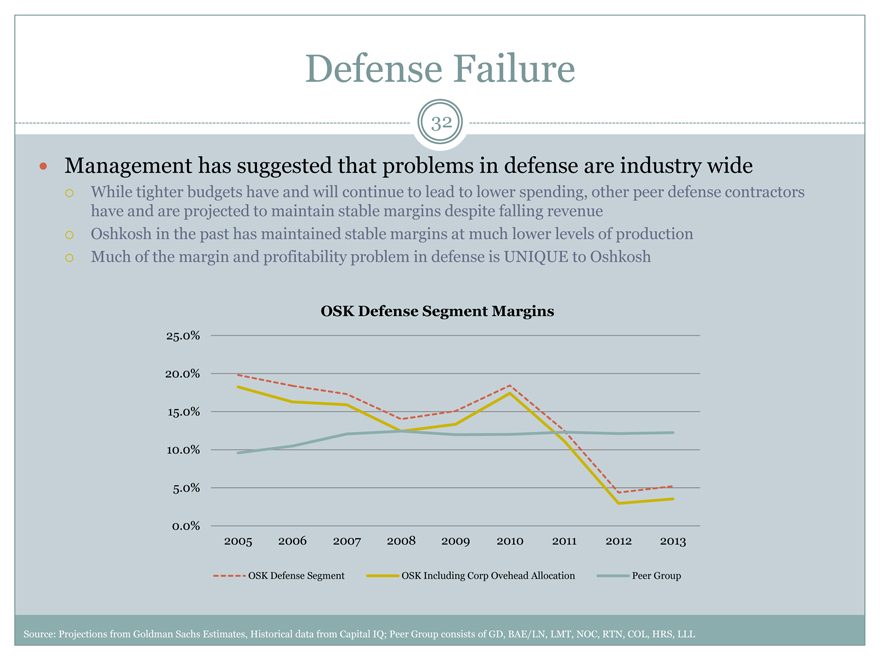

Management has suggested that problems in defense are industry wide

While tighter budgets have and will continue to lead to lower spending, other peer defense contractors have and are projected to maintain stable margins despite falling revenue

Oshkosh in the past has maintained stable margins at much lower levels of production

Much of the margin and profitability problem in defense is UNIQUE to Oshkosh

OSK Defense Segment Margins

25.0% 20.0% 15.0% 10.0% 5.0%

0.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013

OSK Defense Segment OSK Including Corp Ovehead Allocation Peer Group

Source: Projections from Goldman Sachs Estimates, Historical data from Capital IQ; Peer Group consists of GD, BAE/LN, LMT, NOC, RTN, COL, HRS, LLL

Defense Failure

33

We are concerned Oshkosh is setting up for failure again with the FHTV

The Heavy Tactical Vehicle platform has been a long standing program with Oshkosh

It seems that the same group of competitors who bid on the FHTV may bid on this contract again

It appears that the company is already trying to reduce shareholders expectations that defense contracts can be managed profitably

“We are going to be in an interesting environment the next several years where there will be many contractors chasing fewer business opportunities that could impact pricing” Q32011 Earnings Call

If Oshkosh has a similar result on this program, it could destroy the profitability of the entire defense segment

Defense Failure

34

We believe that defense industry consolidation is coming

”we will rely on normal market forces to make the most efficient adjustments to the defense industrial base…These forces will doubtless lead to an uptick in the volume of M&A and other industry adjustments in the coming period, and this is normal. For our part, the Defense Department welcomes needed adjustments that lead to greater overall efficiency. We will examine these transactions to ensure that the Department’s long-term interests in a robust and competitive industrial base dominate any near-term or one-time proposed savings.” Ashton Carter Undersecretary of Defense for Acquisition, Technology and Logistics

General Dynamics recently agreed to purchase Force Protection Inc., both players in the tactical vehicles business

Weak profitability and an organization dominated by non-core businesses might prevent Oshkosh from participating in substantial consolidation in the industry putting the company at a substantial disadvantage going forward

Oshkosh Corporation

35

A NEW DIRECTION TO CREATE SHAREHOLDER VALUE

A New Direction – JLG

36

JLG should expand internationally, something that even Oshkosh management admits

This must be accomplished simultaneously with increased production due to a cyclical recovery

To effectively expand JLG should explore both organic growth and acquisitions which will be capital intensive

A company with a stronger balance sheet may be able to drive market share with financing support for customers

The company may have distribution and manufacturing synergies with other construction product companies which could make a sale very attractive

The company already has distribution deals in place with construction and agricultural equipment manufactures proving that there are distributions synergies

Monetizing this investment for a fair price would allow increased capital and management focus on other parts of the business y The board needs to explore every alternative including running a process to determine if an outright sale or spin would be accretive to shareholders

A New Direction – Defense

37

As DOD programs have become smaller there should be fewer companies bidding on the contracts

Truck products are still attracting interest from several industry players

General Dynamics recently agreed to purchase Force Protection which may be the first of many consolidating transactions in the defense vehicles business

Oshkosh should be a participant in this round of consolidation either as a buyer or seller

To stand alone as industry players are consolidating around Oshkosh will weaken the company competitively

Consolidating activity will allow companies to reduce irrational price competition (like the FMTV situation) and drive substantial overhead and manufacturing synergies over time

Oshkosh does not have the balance sheet to drive accretive transactions and does not seem open to being a seller

Current Management appears to be focused on bidding on new contracts as opposed to focusing on other opportunities

The board needs to be creative in exploring value creative options for Oshkosh’s existing Defense capabilities through acquisitions, partnerships or sales

A New Direction – Commercial/ Fire & Emergency

38

Apparently Oshkosh has not focused on several smaller businesses as they have been distracted with Defense and JLG problems y Despite their size the Company has failed to consolidate several fire & emergency businesses over the last 5 years

The company purchased Med-Tec in 2000 and is still a small player in the Ambulance business

They have been unable to grow market share and have indicated an unwillingness to make acquisitions

Outside of a few areas such as airport products the company has been disappointing at expanding their international footprint in these businesses

The company operates 42 separate manufacturing facilities

The only business which has had a substantial footprint reduction is Fire & Emergency which has also performed poorly

From 2008-2011 the business went from over 10% margins to zero margin while moving from 22 to 7 manufacturing locations. We believe this shows that current management has a poor track record in restructuring activities

A New Direction – Commercial/ Fire & Emergency

39

The board should immediately develop an integration plan for these niche businesses to leverage Oshkosh large size and increase margins

The board should refocus the company on increasing domestic and international market share through operating efficiency and acquisitions

The board should take advantage of a weak economy by expanding the business to include new niche vehicle products

If the current management is unwilling or incapable of carrying out these strategic initiatives then the board should find a management team who will execute

Oshkosh Corporation

40

THE ICAHN SLATE

The Icahn Slate

41

Director

Directors with substantial operations experience

Jose Maria Alapont

Former CEO of Iveco a European commercial, specialty and defense vehicle

manufacturer. Currently CEO of Federal-Mogul a $7 Billion Auto parts supplier.

Marc Gustafson

Former President of American Lafrance Emergency Vehicles and Federal-Signal’s

Emergency One business. President and CEO of Volvo Trucks North America.

Daniel Ninivaggi

Former Chief Administrative Officer of Lear Corp., a global Tier 1 Auto parts supplier.

Directors with substantial financial and investing experience

Vincent Intrieri

Senior Managing Director at Icahn Capital L.P

Samuel Merksamer

Managing Director at Icahn Capital L.P.

Alvin “Buzzy” Krongard

Former CEO/Chairman of Alex Brown Inc., former Executive Director of the Central Intelligence Agency.

The Icahn Slate

42

José Maria Alapont

Mr. Alapont will bring to the board unmatched experience managing global specialty, defense and commercial vehicle businesses and will bring a voice to the board with an established track record of developing and executing international and developing market growth strategies.

Mr. Alapont has been president, chief executive officer and a director of Federal-Mogul, a $7 billion Tier 1 global automotive supplier, since March 2005. Mr. Alapont served as chairman of the board of directors of the company from 2005 to 2007. During his tenure, he has guided the company out of Chapter 11 bankruptcy and delivered strong financial performance and diversified global revenue growth in mature and developing markets with his strategy for Sustainable Global Profitable Growth. Under his leadership, the company has established a leading position in developing and delivering innovative automotive, commercial vehicle and industrial equipment technologies through the implementation of extensive joint ventures, acquisitions and organic growth initiatives. He has more than 35 years of global leadership experience in both vehicle manufacturers and suppliers with business and operations responsibilities in the Americas, Asia Pacific, Europe, Middle East and Africa regions.

Mr. Alapont, between 2003 and 2005, was chief executive officer and a member of the board of directors of IVECO, the commercial trucks and vans, public and commercial buses, recreational, special off-road, firefighting, defense and military vehicles company of the Fiat Group. During this period, he was instrumental in the restructuring of the company, launching a new business model for use of high-value, common design platforms to gain efficiencies and expanded global alliances in growth markets. Prior to IVECO, Mr. Alapont served in various key executive positions at Delphi Corporation, a global automotive supplier from 1997 to 2003, including president of international operations and vice president of sales and marketing, and a member of the company’s strategy board, the top policy group.

Mr. Alapont, from 1990 to 1997, served in several executive roles at Valeo, a global automotive supplier, including vice president of the global heavy-duty engine cooling, clutch and transmission and lighting systems businesses. He was also a member of the Valeo Strategy Board. Mr. Alapont began and developed his automotive career in 1974, spending 15 years at Ford Motor Company, where he progressed through various management and executive positions in quality, testing and validation, manufacturing and purchasing at Ford of Europe.

He serves on the Board of Directors of Mentor Graphics and provides valuable guidance to the boards of automotive supplier trade associations and economic development groups in the U.S., Europe and Asia Pacific countries.

The Icahn Slate

43

Marc Gustafson

Mr. Gustafson brings to the board specialized expertise running companies competing in the specialty vehicle segments such as fire & emergency, construction, refuse and truck mounted platforms. During his 35 year career in the transport industry, he has a demonstrated track record of operating and revitalizing North America based commercial vehicle manufacturers and has led restructuring efforts to transform two multi-national fire truck companies.

Mr. Gustafson was previously President of Federal Signal’s Fire Rescue business unit where he implemented major cost reduction programs to stem financial losses. During Mr. Gustafson’s tenure he divested several underperforming businesses, introduced a new modular product concept to simplify manufacturing and launched several major new products. Prior to joining Federal Signal, Mr. Gustafson was appointed President of American La France, a major fire truck manufacture on an interim basis to stabilize the business, develop a long term plan which involved divesting 4 of 9 divisions, and resolving manufacturing bottlenecks. Prior to joining American La France, he spent 9 years at Volvo Trucks North America (and Mack Trucks Inc., a predecessor). Mr. Gustafson served as President and CEO, turning an underachieving business unit of AB Volvo into a profitable entity. He developed and implemented a new strategic plan which resulted in a 93% increase in sales, with record sales and operating income levels in 1999, a cost savings program which resulted in $3000 per vehicle savings and negotiated a successful six year labor agreement with the UAW to facilitate a $165mm plant expansion. Previously Mr. Gustafson owned and operated a successful multi-franchise heavy truck dealer in North and Central Florida.

|

|

The Icahn Slate

44

Daniel Ninivaggi

Mr. Ninivaggi brings to the board a solid background in analyzing businesses as well as developing and executing strategic plans including the separation and divestiture of non-core assets.

Mr. Ninivaggi is currently the President and Principle Executive Officer of Icahn Enterprises, an investment holding company which owns operating businesses in seven industry sectors. Prior to joining IEP, Mr. Ninivaggi was Executive Vice President and Chief Administrative Officer of Lear Corp, a $17 billion global automotive supplier. While at Lear, Mr. Ninivaggi was responsible for corporate development and strategy, information technology, human resources, legal, environmental, tax, internal audit, and treasury. He was responsible for the separation and ultimate divestiture of Lear’s $3 billion interior components business as well as as a comprehensive strategic review and realignment of the company’s electrical distribution system and electronics segment. Mr. Ninivaggi was also integrally involved in Lear’s debt restructuring before he left the company in July 2009. From 1991-2003 Mr. Ninivaggi was a lawyer with Skadden Arps and Winston & Strawn, specializing in M&A and securities law.

Mr. Ninivaggi currently serves on the board of Motorola Mobility, Federal-Mogul., and Tropicana Entertainment, where he also serves as interim CEO.

The Icahn Slate

45

Alvin “Buzzy” Krongard

Mr. Krongard spent six years in government/national security service in the wake of the substantial build out in U.S. military capacity. He will bring to the board key knowledge and experience of the defense business as well as years of experience in a corporate setting.

Mr. Krongard served as the Executive Director of Central Intelligence Agency where he was employed in various capacities from 1998-2004. Previously Mr. Krongard was employed at Alex Brown, most recently as Chairman and CEO where he led the company through a merger with Bankers Trust when he assumed the position of Vice Chairman of the Board of Bankers Trust, completing a 29 year career in investment banking.

Mr. Krongard is on the Global Board of DLA Piper, is the Lead Director and Audit Committee Chair of Under Armour Inc, is the Vice Chairman of the Johns Hopkins Health System and, Chairman of the Baltimore Police Foundation. He is also a Director of Iridium Communications Inc., In-Q-Tel, and Apollo Global Management, LLC.

The Icahn Slate

46

Vincent Intrieri

Mr. Intrieri brings skills that will be helpful to the company including 17 years of both public and private company investing experience and over 10 years of public accounting and advisory experience, financial restructuring and using corporate actions and M&A to create shareholder value. He has a long established career as a value investor and has participated in many financial and operational restructurings.

Mr. Intrieri is currently a Senior Managing Director at Icahn Capital where he has worked for 13 years. Mr. Intrieri is responsible for the investment portfolio as well as overseeing several operating companies owned by Icahn Enterprises. During his time at Icahn, Mr. Intrieri has led the acquisition, restructuring, emergence from bankruptcy and continued operations via his board activities at Federal-Mogul. Mr. Intrieri also led similar investments involving distressed acquisitions and turnarounds of challenged businesses including Viskase Companies where he has served as Chairman for 8 years and PSC Inc. which Mr. Intrieri led out of bankruptcy, built new management teams and eventually separated into two separate businesses, one of which was sold last year to a financial investor. Prior to this Mr. Intrieri was a Managing Director at Elliot Associates focused on distressed and value investing. Mr. Intrieri began his career in public accounting where he eventually became a Partner at Arthur Anderson in the Financial Restructuring Practice.

Mr. Intrieri currently serves on the board of Federal-Mogul, Dynegy Inc. where he is chairman of the Finance and Restructuring Committee, Motorola Solutions Inc. and Icahn Enterprises

The Icahn Slate

47

Samuel Merksamer

Mr. Merksamer brings skills that will be helpful to the company in building management teams, developing value additive M&A strategies and identifying undervalued companies including financially distressed businesses.

Mr. Merksamer is currently a Managing Director at Icahn Capital where he is responsible for identifying investment opportunities focused on distressed and undervalued companies as well as providing board level input and strategic direction for several portfolio companies controlled by Icahn Enterprises. Previously Mr. Merksamer was employed by the Airlie Group, a high yield and distressed focused hedge fund. Mr. Merksamer currently serves on the board of Dynegy Inc. and participated in a management overhaul and a still-in-progress multi-billion dollar financial restructuring.

Mr. Merksamer also serves on the boards of Federal-Mogul, Viskase Companies, and American Railcar Industries.