Welcome to the

Annual General

Meeting of

Shareholders

June 23, 2006

Forward Looking Statements

Certain oral statements made by management of DrugMax, Inc. from time to time, including those contained in this presentation and

the oral presentation that accompanies it, that are not historical facts are “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995. Because such statements involve risks and uncertainties, actual results may differ materially

from those expressed or implied by such forward-looking statements. Forward-looking statements, are statements regarding the intent,

belief or current expectations, estimates or projections of DrugMax, its directors or its officers about DrugMax and the industry in

which it operates, and include among other items, statements regarding (a) DrugMax’s strategies regarding growth and business

expansion, including its strategy of building an integrated specialty drug distribution platform with multiple sales channels, opening

new Worksite locations and acquiring third-party pharmacies, (b) its financing plans, (c) trends affecting its financial condition or

results of operations; and (d) its ability to continue to control costs and to meet its liquidity and other financing needs. Although

DrugMax believes that its expectations are based on reasonable assumptions, it can give no assurance that the anticipated results will

occur. When used in this report, the words “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” and similar

expressions are generally intended to identify forward-looking statements.

Important factors that could cause the actual results to differ materially from those in the forward-looking statements include, among

other items, (i) management’s ability to implement its growth and business strategies, (ii) management’s ability to locate and acquire

suitable acquisition candidates; (iii) management’s ability to negotiate and open new Worksite pharmacies, (iv) management’s ability to

manage the company’s growth, (v) changes in the regulatory and general economic environment related to the health care and

pharmaceutical industries, including possible changes in reimbursement for healthcare products and in manufacturers’ pricing or

distribution policies; (vi) conditions in the capital markets, including the interest rate environment and the availability of capital; (vii)

changes in the competitive marketplace that could affect DrugMax’s revenue and/or cost bases, such as increased competition, lack of

qualified marketing, management or other personnel, and increased labor and inventory costs; and (viii) changes regarding the

availability and pricing of the products which DrugMax distributes, as well as the loss of one or more key suppliers for which

alternative sources may not be available. Further information relating to factors that could cause actual results to differ from those

anticipated is included under the heading Risk Factors in DrugMax’s Form 10-K for the year ended December 31, 2005 filed with the

U.S. Securities and Exchange Commission. DrugMax disclaims any intention or obligation to update or revise forward-looking

statements, whether as a result of new information, future events or otherwise.

DrugMax Today

First integrated specialty pharmaceutical distribution

model:

Targeted location strategy

Specialty product focus

Outpatient pharmacies at point of care:

In or near medical centers

For chronically ill, high value patients with acute prescription

medications

Servicing physicians and clinics for in-office treatment

Nationally recognized brand: Familymeds

78 corporate locations

7 licensed/franchised locations

Presence in 14 states

DrugMax Today & Familymeds Tomorrow

Vision

Build the largest network of on-site & clinic pharmacies in

the U.S. under the Familymeds brand

Value

Focused specialty pharmacy services for chronic/acute

patients and their physician providers

Depth of Experience

Years of

Previous Experience /

Name

Title

Experience

Affiliations

Ed Mercadante

Pharmacist

Chairman and Chief Executive Officer

25

Familymeds, Arrow Corporation, APP, Rite Aid,

GNC, Medibank, ProHealth

Jim Bologa, CPA

Chief Operating Officer

25

Ernst & Young

Jim Beaumariage

Pharmacist

SVP, Pharmacy Operations,

22

Familymeds, CVS, CVS/People’s Drug

Allison Kiene

Pharmacist - Lawyer

VP, General Counsel and Secretary

17

Familymeds, The Stop & Shop Supermarket

Company, Stop & Shop Pharmacy

Rees Pinney

SVP, Employer Sponsored Pharmacy,

16

Familymeds, Healthright, O'Neal & Prelle

Gregg Montgomery

Pharmacist

SVP, Procurement,

25

Familymeds, Rite-Aid, Farmco Ventures,

NeighborCare

Familymeds, Inc.

Familymeds, Inc.

Valley Drug Co.

Jim Searson, CPA

Chief Financial Officer

20

Daticon, TranSwitch, Katerra, PWC

Chronically Ill

Patients With

Acute Needs

Large Employee

and

Retiree Population

Physicians, Clinics

and Other

Specialty Providers

FamilyMeds Clinic

and

Arrow Apothecary

Pharmacies

Worksite

Employer

Sponsored

Pharmacies

Valley

Medical Supply

Hospital Clinics

and

Medical Campuses

(83 locations)

Fortune 500

Companies with

Large Single Site

Population of

Employees

(2 locations)

Small to Mid-size

Medical and

Healthcare

Provider Locations

Oral & Specialty Pharmaceuticals

HomeCare & Medical Care Specialty Products

Target

Customer

Product

Focus

Targeted

Location

Strategy

Unique Business Model

Focus: Location Strategy

Increased focus from health insurers and employers to

reduce healthcare costs

Growing consumer preference toward point of care

prescription service

To provide a low-cost solution with a focus on convenience, DrugMax

employs a unique location strategy which targets:

Large employer campuses

Hospital clinics and medical campuses

Medical & healthcare provider locations

Focus: Specialty Pharmaceuticals

Specialty Pharmaceuticals

Include:

Biopharmaceuticals

Blood Derived Products

Complex Molecules

Select oral, injectable and

infused medications

Specialty Pharmaceuticals

Require:

Tailored patient education for

safe & cost-effective use

Patient specific dosing

Patient monitoring with acute

needs

Administration via injection,

infusion, inhalation or oral

Usually requires special handling

Drug category driven by advances in drug research &

technology since 2000

Target and treat specific chronic or genetic conditions

Estimated $20-$25B market opportunity

Competitive Pharmacy Metrics

Source: NACDS industry profile 2005

Mass Market

Supermarkets

Our Pharmacies

Independents

Chain

Average Rx Price for

Overall Industry

Overall Selling

Space/Unit (sq. ft.)

Average Sales/

Pharmacy

% of Pharmacy Sales

Average Generic

Utilization

9,062

$4.3 Million

68%

52%

3,087

$2.2 Million

95%

48%

43,814

$2.7 Million

13%

N/A

1,800

$2.9 Million

95%

57%

$54.60

$59.87

Core Business by Therapeutic Category

Percentage of RX Revenue

Patient Demographics by Age Group

Percentage of RX Utilization

Market Dynamics

Medicare Modernization Act - Medicare Part D

Expansion of prescription drug benefit for seniors

Highly variable reimbursement structure for pharmacies

Generics will play a more important role in the future

Fluctuating supply and demand

Prescriptions growth outpacing supply of community pharmacists

Prescriptions +41%: 3.2 B in 2003 to 4.5 B in 2010

Community pharmacists +9.2%

Requirements for disease management services called Medication

Therapeutic Management under new Med D Program

Leveraging Our Platform Strength

Our Expertise

Specialty & complex treatments

Higher transaction value

Infectious disease

Diabetes

Pain & Oncology

Respiratory

Psychological & mental health

Our Relationships

43 pharmacies at point of care

Inside medical office

buildings/campuses

4,000 doctors on medical

campuses within or near our sites

Valley Medical Supply

Natural outlet for medical

specialty distribution

Our Patients

> 400,000 chronic and acute

patients

Active patient and clinical

programs:

Greater medication compliance

Medical therapeutic

management (MTM)

Greater specialty drug

pull-through

Our Pharmacies

80 pharmacies in key medical

locations

>3.6M prescriptions

Estimated market opportunity:

$1.3B in pharmacy & medical

supply sales in our existing

locations

Strategic Initiatives

Build our per unit sales volume

Organic sales growth by location

Deeper product assortment with higher transactional value

Specialty pharmacy and Institutional Rx products & Services

Focus on integrated growth

Direct sales of products and services to doctors

Pro forma estimate $15 million in 2006

Add more Worksite PharmaciesSM

Growing demand by employers to control drug benefit expenditures

Improve employee convenience

Increase automation and technological capabilities

Kiosks connecting patients to pharmacies

Electronic Rx transmission connecting DrugMax to physicians

Grow our network of pharmacies

Fragmented market = > 1,000 location opportunities

2005 Scorecard

Divested “non core” lower margin legacy wholesale

distribution business (December 2005)

Integrated DrugMax distribution facility with pharmacy

operations (December 2005)

Completed refinancing and recapitalization to improve our

financial position (October 2005)

2006 Objectives

Top-line organic growth

Up-sell pharmaceuticals to physicians in current pharmacy locations and

through Valley Medical Supply (VMS)

Super-charge sales referrals from physicians in specialty Rx and through

institutional sectors like assisted living & group homes for Rx sales

Add new pharmacies

Near leading medical institutions and hospitals and large employer

sponsored locations

Expand gross margin to the 20.5% level seen in 2004

Through “Familymeds Formulary” emphasizing Generic Utilization

Through Product strategy geared toward high value patients with chronic

diseases

Through using 5 day a week Wholesaler Base Supply Chain Management

Improve financial performance through

operational integration & leveraged growth:

Focus on Profitability

Increase Gross Margin

Bundle products

Pharmaceuticals with home care products yield higher gross margins of

30+%

Utilization of generic drugs yields higher gross margins of

approximately 50% (2006-2007 will see dramatic shift towards

generics)

Compounded and infusion medications yield higher gross margins of

50+%

Expense Control

Maintain SG&A model of current pharmacy footprint and operation

help control expense

Average size is 1800 sq. ft. with low occupancy expenses

Location/proximity strategy

Being close to physicians drives down operating/marketing expenses

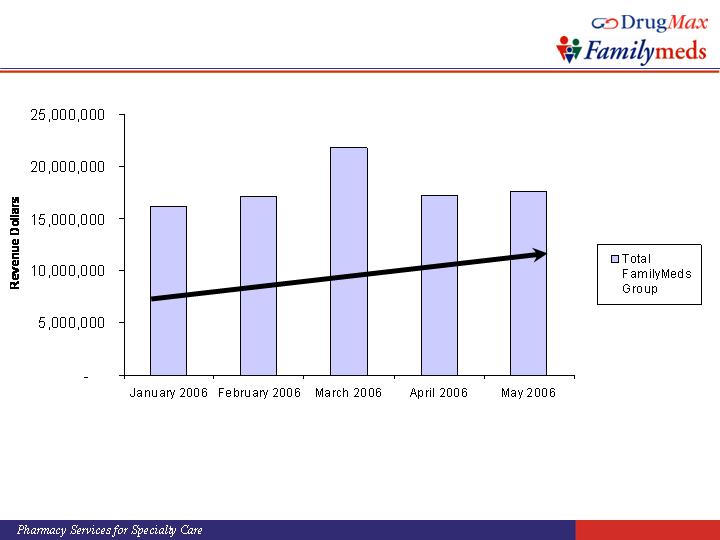

2006 Monthly Sales Trend

$16.2M

$17.4M

$22.5M

$18.4M

$19.0M

April & May 2006 sales of $37.4M grew 10.0% YoY and

11.6% over Jan & Feb 2006 sales.

(4 weeks)

(4 weeks)

(4 weeks)

(4 weeks)

(5 weeks)

~ 4.1M/wk

~ 4.4M/wk

~ 4.5M/wk

~ 4.6M/wk

~ 4.8M/wk

Q1 2006 Financial Highlights

Revenues of $56M, a sequential increase of 6.9%

Gross margin of 19.5%, compared to 18.3% in Q4 2005

Operating loss of $2.9M, an improvement of 36%

compared to loss of $4.5M in Q4 2005

Net loss per share of $.06, compared to net loss of $.47 in

Q4 2005

Nasdaq: DMAX (FMRX)

Shares Outstanding: approximately 66 million

Market Capitalization: $47 million

Fiscal Year End: Saturday closest to December 31

We operate on a 4-4-5 week retail quarterly calendar

As of June 15, 2006

Key Takeaways

Unique locations + specialty products model

Forward focus on core pharmacy operations

Leverage through integrated platform strength

Favorable competitive metrics and market dynamics

Improving financial condition

Positioned to achieve substantial organic revenue growth

in 2006

Expect to be EBITDA positive in 2H 2006

FAMILYMEDS, INC.

NASDAQ: FMRX

(DrugMax, Inc. Nasdaq: DMAX)

312 Farmington Avenue

Farmington, CT 06032-1968

Tel: 860-676-1222

www.drugmax.com

www.familymeds.com

Pharmacy Services for Specialty Care