Exhibit 99.2 |

Forward-Looking Statements 2 Important Additional Information and Where to Find It In connection with the proposed merger, BB&T will file with the SEC a Registration Statement on Form S-4 that will include a Proxy Statement of Susquehanna and a Prospectus of BB&T, as well as other relevant documents concerning the proposed transaction. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. SHAREHOLDERS OF SUSQUEHANNA ARE URGED TO READ THE REGISTRATION STATEMENT AND THE PROXY STATEMENT/PROSPECTUS REGARDING THE MERGER WHEN IT BECOMES AVAILABLE AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. A free copy of the Proxy Statement/Prospectus, as well as other filings containing information about BB&T and Susquehanna, may be obtained at the SEC’s Internet site (http://www.sec.gov). You will also be able to obtain these documents, free of charge, from BB&T at www.bbt.com under the heading “About” and then under the heading “Investor Relations” and then under “BB&T Corporation SEC Filings” or from Susquehanna by accessing Susquehanna’s website at www.susquehanna.net under the heading “Investor Relations” and then under “SEC Filings”. Copies of the Proxy Statement/Prospectus can also be obtained, free of charge, by directing a request to BB&T Corporation, 150 South Stratford Road, Suite 300, Winston-Salem, North Carolina 27104, Attention: Shareholder Services, Telephone: (336) 733-3065 or to Susquehanna Bancshares, Inc., 26 North Cedar Street, Lititz, Pennsylvania 17543, Attention: Investor Relations, Telephone: (717) 626-9801. Susquehanna and certain of its directors and executive officers may be deemed to be participants in the solicitation of proxies from the shareholders of Susquehanna in connection with the proposed merger. Information about the directors and executive officers of Susquehanna and their ownership of Susquehanna common stock is set forth in the proxy statement for Susquehanna’s 2014 annual meeting of shareholders, as filed with the SEC on Schedule 14A on March 21, 2014. Additional information regarding the interests of those participants and other persons who may be deemed participants in the transaction may be obtained by reading the Proxy Statement/Prospectus regarding the proposed merger when it becomes available. Free copies of this document may be obtained as described in the preceding paragraph. This communication contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 including, but not limited to, BB&T’s and Susquehanna’s expectations or predictions of future financial or business performance or conditions. Forward-looking statements are typically identified by words such as “believe,” “expect,” “anticipate,” “intend,” “target,” “estimate,” “continue,” “positions,” “prospects” or “potential,” by future conditional verbs such as “will,” “would,” “should,” “could” or “may”, or by variations of such words or by similar expressions. These forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. Forward- looking statements speak only as of the date they are made and we assume no duty to update forward-looking statements. Actual results may differ materially from current projections. In addition to factors previously disclosed in BB&T’s and Susquehanna’s reports filed with the U.S. Securities and Exchange Commission (the “SEC”) and those identified elsewhere in this document, the following factors among others, could cause actual results to differ materially from forward-looking statements or historical performance: ability to obtain regulatory approvals and meet other closing conditions to the merger, including approval by Susquehanna shareholders on the expected terms and schedule; delay in closing the merger; difficulties and delays in integrating the Susquehanna business or fully realizing cost savings and other benefits; business disruption following the merger; changes in asset quality and credit risk; the inability to sustain revenue and earnings growth; changes in interest rates and capital markets; inflation; customer acceptance of BB&T products and services; customer borrowing, repayment, investment and deposit practices; customer disintermediation; the introduction, withdrawal, success and timing of business initiatives; competitive conditions; the inability to realize cost savings or revenues or to implement integration plans and other consequences associated with mergers, acquisitions and divestitures; economic conditions; and the impact, extent and timing of technological changes, capital management activities, and other actions of the Federal Reserve Board and legislative and regulatory actions and reforms. Annualized, pro forma, projected and estimated numbers are used for illustrative purposes only, are not forecasts and may not reflect actual results. |

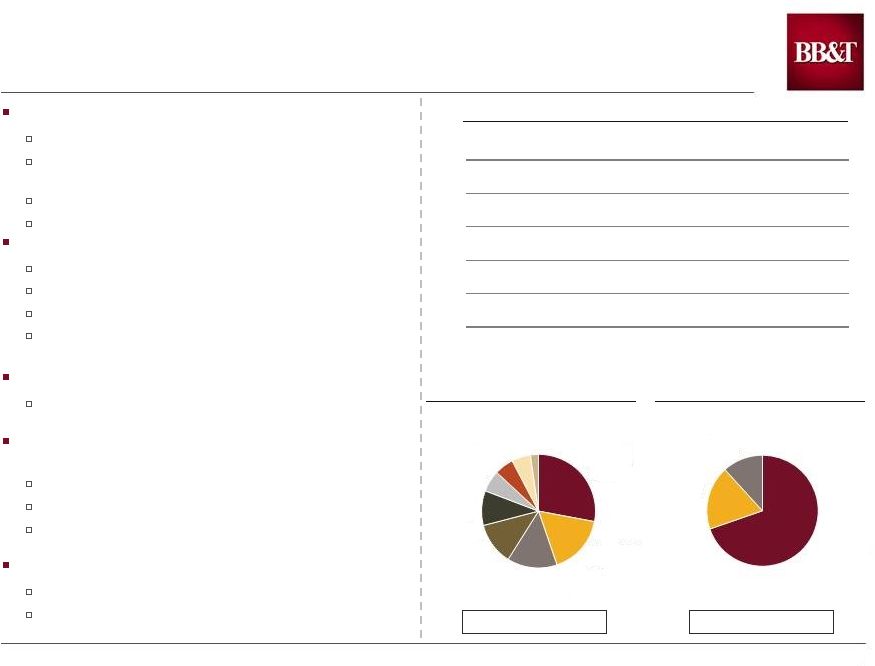

3 3 Strategic and Compelling Acquisition of Susquehanna Note: Financial data at September 30, 2014. Susquehanna Financial Highlights Loan Composition Deposit Composition Total: $13,426MM Total: $13,589MM Strategically compelling New and attractive contiguous markets Top 5 pro forma market share in Susquehanna’s markets Adds to the diversity of BB&T’s footprint Leverages BB&T’s proven practices Financially attractive Approximately $2.5 billion aggregate deal value EPS accretive and exceeds IRR hurdle Compelling use of capital Tier 1 Common ratio at close expected to decline by 50 – 60 bps Significant expansion of attractive Mid-Atlantic footprint Central PA, Western MD and the Philadelphia and Baltimore MSAs BB&T well prepared to successfully execute on this acquisition Extensive due diligence process Careful planning to ensure preparedness mitigates risk BB&T’s near-term priority will be to focus on successful closing and integration of announced acquisitions Compatible culture with BB&T Client oriented community bank model Experienced management team with deep knowledge of its markets Assets ($MM) $18,583 Total Loans ($MM) 13,426 Deposits ($MM) 13,589 Common Equity ($MM) 2,751 TCE / TA 8.4% Tier 1 Common Ratio 10.9 Leverage Ratio 9.6 Transaction / MMDA / Savings 70% Retail Time 18% Jumbo Time 12% Commercial Real Estate 28% Closed End 1-4 Family 17% Commercial & Industrial 14% HELOCs 12% Leases 10% Construction 6% Consumer 6% Other 5% Multifamily 2% |

4 4 Key Transaction Terms Purchase Price $2.5 billion aggregate consideration $13.50 per Susquehanna common share (1) Price / LTM EPS: 16.3x Price / TBV: 1.69x 7.4% deposit premium Consideration 70% stock / 30% cash 0.253 BB&T shares and $4.05 cash for each Susquehanna share Tax free transaction for stock component Cost Savings Approximately $160 million pre-tax (fully phased-in) Approximately 32% of Susquehanna’s non-interest expense Merger & Integration Costs Approximately $250 million (pre-tax) Credit Mark 4.5% of loans and leases Expected Closing Second half of 2015 Closing Conditions Susquehanna shareholder approval Other customary closing conditions including regulatory approval Board Representation William J. Reuter, Susquehanna’s Chairman & CEO, and Christine Sears, a Susquehanna Board member, will join BB&T’s Board of Directors (1): Based on BB&T’s average closing stock price for the trailing 45 trading days through 11/10/14. |

5 Significant Market Share Expansion in Attractive Mid-Atlantic Region (1): Excludes branches with balance greater than $1 billion. (2): Defined by counties in which Susquehanna operates in Pennsylvania, New Jersey, Maryland and West Virginia. Source: SNL Financial. Branch data as of June 30, 2014 except for Susquehanna which is as of September 30, 2014. Deposit data as of June 30, 2014. Branch and deposit data pro forma for announced M&A through November 7, 2014. Susquehanna's Top 15 MSAs Deposit Deposits Market MSA Rank Branches ($MM) Share Philadelphia, PA 8 58 $3,241 2.7% Lancaster, PA 1 32 2,669 25.8 Baltimore, MD 7 23 1,448 3.2 York, PA 3 18 811 12.4 Hagerstown, MD 1 13 787 24.6 Harrisburg, PA 6 16 661 5.5 Chambersburg, PA 2 9 557 27.8 Reading, PA 8 8 380 5.3 Vineland, NJ 3 5 362 14.3 Cumberland, MD 1 5 289 32.2 Sunbury, PA 1 8 277 21.3 Williamsport, PA 5 5 262 9.8 Atlantic City, NJ 9 6 255 4.9 Allentown, PA 17 7 245 1.6 Pottsville, PA 4 7 196 9.9 (1) (1) Williamsport Washington D.C. Hagerstown Baltimore Philadelphia Reading Harrisburg Camden Lancaster York Ocean City Susquehanna Deposit Deposits Market Rank Institution Branches ($MM) Share 1. Wells Fargo 368 $31,121 13.3% 2. PNC 378 22,929 9.8 3. Toronto-Dominion 168 20,875 8.9 4. M&T Bank 311 18,423 7.8 5. BB&T Pro Forma 312 17,591 7.5 5. Bank of America 203 13,828 5.9 6. Citizens Financial 208 13,504 5.8 7. Susquehanna 245 13,338 5.7 8. Fulton Financial 178 9,936 4.2 9. National Penn 124 6,490 2.8 10. Banco Santander 172 6,413 2.7 11. BB&T 67 4,253 1.8 12. Beneficial Mutual Bancorp 59 3,537 1.5 13. First Niagara 58 2,536 1.1 14. Metro Bancorp 33 2,197 0.9 15. Univest Corp. of Pennsylvania 43 2,187 0.9 Deposit Market Share in Susquehanna’s Footprint (1)(2) |

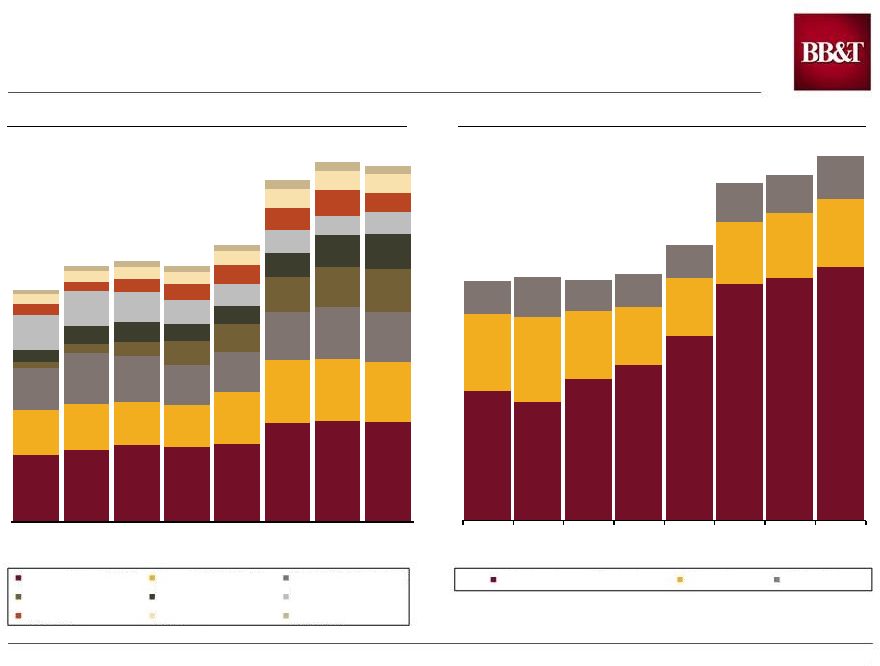

6 6 Susquehanna’s Historical Loan & Deposit Profile Loan Composition ($MM) Deposit Composition ($MM) Source: SNL Financial. Regulatory data. $2,496 $2,697 $2,876 $2,815 $2,941 $3,724 $3,800 $3,753 $1,721 $1,742 $1,620 $1,574 $1,940 $2,365 $2,350 $2,253 $1,563 $1,921 $1,749 $1,529 $1,517 $1,812 $1,931 $1,907 $256 $353 $547 $885 $1,054 $1,343 $1,512 $1,611 $452 $683 $750 $672 $676 $900 $1,219 $1,326 $1,293 $1,314 $1,115 $877 $829 $848 $736 $817 $411 $314 $482 $603 $722 $843 $953 $731 $385 $426 $486 $471 $550 $703 $733 $719 $8,752 $9,654 $9,827 $9,633 $10,448 $12,895 $13,576 $13,426 '07 '08 '09 '10 '11 '12 '13 9/30/14 $4,837 $4,426 $5,268 $5,787 $6,878 $8,835 $9,045 $9,466 $2,877 $3,163 $2,541 $2,169 $2,175 $2,294 $2,424 $2,528 $1,231 $1,478 $1,166 $1,236 $1,238 $1,451 $1,401 $1,595 $8,945 $9,067 $8,975 $9,192 $10,291 $12,580 $12,869 $13,589 '07 '08 '09 '10 '11 '12 '13 9/30/14 Commercial Real Estate Closed End 1- 4 Family Commercial & Industrial HELOCs Leases Construction Consumer Other Multifamily Transaction / MMDA / Savings Retail Time Jumbo Time |

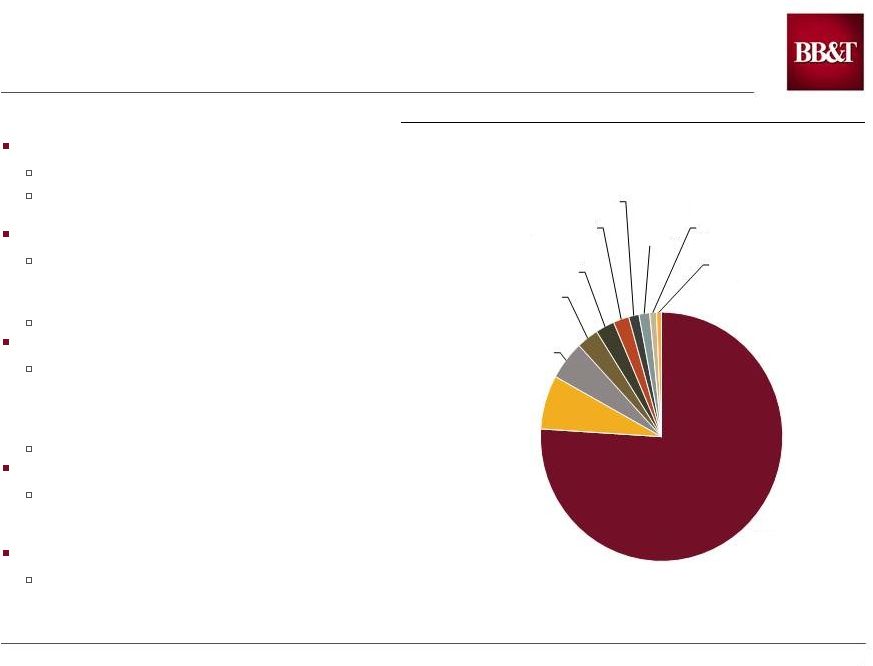

7 7 Susquehanna’s Revenue Profile Source: SNL Financial, Company filings. Susquehanna’s Revenue Composition For the Nine Months Ended September 30, 2014 Susquehanna Bank $18.4 billion of assets as of 9/30/14 Operates a regional community banking model with multiple regional leadership teams Valley Forge Asset Management, LLC Investment advisory, asset management, brokerage services and retirement planning for institutional and high net worth clients $2.8 billion AUM as of 9/30/14 Stratton Management Company Manages mutual funds and provides investment management services to institutions, pensions, endowments and high net worth clients $2.8 billion AUM as of 9/30/14 The Addis Group LLC Provides commercial, property and casualty insurance, and risk management programs for medium and large sized companies Hann Financial Services Corp. Provides comprehensive consumer financing services Net Interest Income 76% Wealth Management Commissions & Fees 7% Service Charges on Deposit Accounts 5% Other Commissions & Fees 3% Property & Casualty Insurance Sales Commissions 3% Other 2% Vehicle Origination & Servicing Fees 1% Mortgage Banking 1% BOLI 1% Capital Markets 1% |

8 8 Leveraging BB&T’s Proven Practices Across a Broader Platform Source: SNL Financial. Branch and deposit data as of June 30, 2014. Texas Acquisition of 63 branches ($3.5 billion in deposits) from Citibank 37 de novo branches since 2012 Branch presence has grown from 22 to 123 since our Colonial acquisition Fastest growing market in our franchise 42% YTD loan growth Cincinnati Acquisition of The Bank of Kentucky ($1.8 billion in assets) #1 in Northern Kentucky #7 in Cincinnati MSA Exciting opportunity to grow around the broader Cincinnati market Pennsylvania Pennsylvania will be the 3 rd most populous state in BB&T’s footprint Lancaster will be the 3 rd most populous MSA where BB&T has a #1 market share Meaningful presence around Lancaster and greater Philadelphia markets Completed acquisition from Citibank in June 2014 and announced acquisition from Citibank in September 2014 BB&T Announced acquisition of The Bank of Kentucky in September 2014 Susquehanna |

9 9 BB&T’s Business Model Thrives Across Markets of Widely Differing Characteristics (1): Total estimated population as of January 1, 2014. (2): Number of firms with sales <$50 million as of November 7, 2014. (3): Real Gross Domestic Product, adjusted for inflation. (4): Represents the average annual growth rate from 12/31/09 – 12/31/13. (5): Preliminary. (6): Seasonally adjusted. Ohio unemployment rate used as a proxy for Cincinnati MSA. (7): Median household income estimated for the calendar year 2014 as of January 1, 2014. Note: Branch data as of June 30, 2014 pro forma for announced M&A through November 7, 2014. Source: SNL Financial, Nielsen, Hoovers, U.S. Bureau of Labor Statistics, U.S. Bureau of Economic Analysis. Cincinnati North West Pennsylvania Texas MSA Carolina Florida Virginia Kentucky Total Population (MM) (1) 12.8 26.7 2.1 9.9 19.7 1.9 4.4 per Bank Branch 2,865 3,908 2,771 3,851 3,613 2,807 2,550 # of Middle Market and Small Businesses (2) 610,398 1,317,817 94,105 465,112 1,341,184 67,331 204,203 per Bank Branch 137 193 122 181 247 102 118 2013 GDP (3) ($BN) $604 $1,388 $111 $440 $751 $69 $171 2013 GDP Growth (3) 0.7% 3.7% 2.1% 2.3% 2.2% 5.1% 1.6% Avg. Annual GDP Growth '09 - (3)(4) '13 1.4 4.4 2.5 1.8 1.0 2.3 2.3 Current Unemployment Rate (September '14) (5)(6) 5.7% 5.2% 5.6% 6.7% 6.1% 6.6% 6.7% 2009 Peak Unemployment (6) 8.6 8.2 10.6 11.2 11.4 8.4 10.7 Historical Population Growth '10 - '14 0.70% 6.06% 1.05% 3.76% 4.54% 0.14% 1.44% Projected Population Growth '14 - '19 0.84 7.60 1.10 4.80 5.74 0.11 1.78 Median Household Income (7) $51,961 $50,464 $53,418 $45,049 $44,318 $41,844 $43,094 |

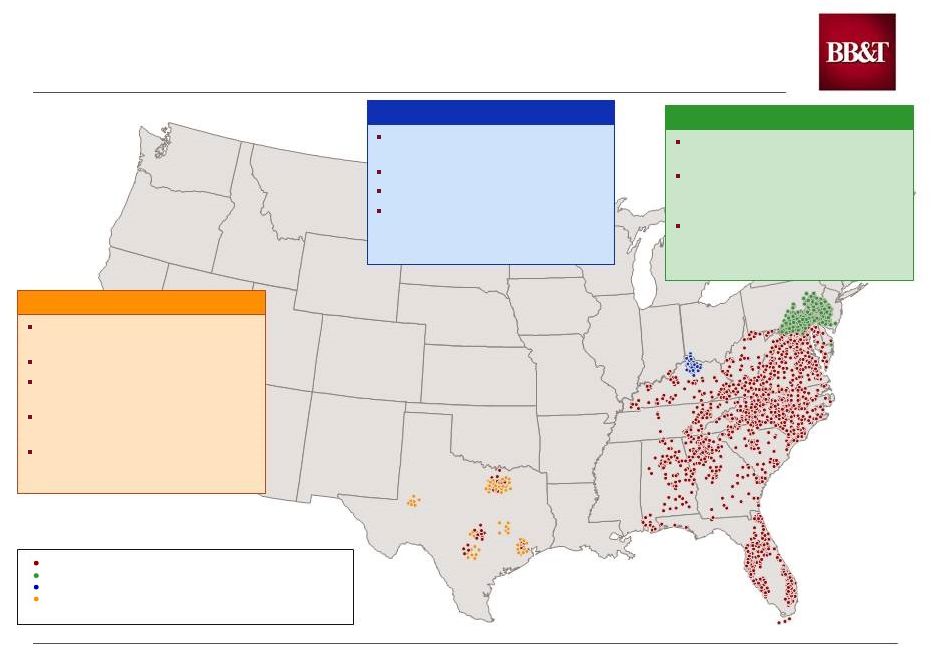

10 10 Community Banking Model is a Key Driver of BB&T’s Success BB&T’s approach to community banking has yielded broad success Collaboration and integration Local, visible leadership Local decision-making Knowing your client Client advocacy: giving voice to the client Partnerships across the bank Seamless perfect client experience Acquisitions are structured to fit with the community banking model Texas – operates in two newly established regions The Bank of Kentucky – a new region will be established Susquehanna – three new regions will be established Shaded counties depict existing regions and new region created for northern Kentucky / greater Cincinnati Anticipated new regions to be established upon the close of Susquehanna and The Bank of Kentucky acquisitions Susquehanna Branches |

11 BB&T’s Culture is Non-negotiable To Create the Best Financial Institution Possible Be The Best of the Best! Helping our CLIENTS achieve economic success and financial security Creating a place where our ASSOCIATES can learn, grow and be fulfilled in their work Making the COMMUNITIES in which we work better places to be, and thereby Optimizing the long-term return to our SHAREHOLDERS, while providing a safe and sound investment. |

12 12 Summary Observations Susquehanna is an attractive opportunity to broaden the BB&T franchise Exciting new contiguous markets Compatible culture Builds on recent expansions in Cincinnati and Texas Value accretive to shareholders Community banking model is a key driver of BB&T’s success Acquisition strategy has been and will remain deliberate and disciplined Consistency around BB&T’s vision, values and mission is non-negotiable |

|