UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-08510 |

Matthews International Funds

| (Exact name of registrant as specified in charter) |

Four Embarcadero Center, Suite 550 San Francisco, CA | 94111 | |

| (Address of principal executive offices) | (Zip code) |

Mark W. Headley, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: 415-788-6036

Date of fiscal year end: December 31

Date of reporting period: June 30, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

The Report to Shareholders is attached herewith.

The views and opinions in this report were current as of June 30, 2007. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors, and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of the Funds’ future investment intent.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy. | ||||

| C O N T E N T S | Message to Shareholders | 2 | ||

| Redemption Fee Policy and Investor Disclosure | 5 | |||

| Manager Commentaries, Fund Characteristics and Schedules of Investments: | ||||

| 6 | ||||

| 12 | ||||

| 18 | ||||

| 24 | ||||

| 32 | ||||

| 38 | ||||

| 46 | ||||

| 52 | ||||

| 58 | ||||

| Disclosure of Fund Expenses | 64 | |||

| Statements of Assets and Liabilities | 66 | |||

| Statements of Operations | 68 | |||

| Statements of Changes in Net Assets | 70 | |||

| Financial Highlights | 75 | |||

| Notes to Financial Statements | 84 | |||

FROM THE INVESTMENT ADVISOR

Dear Fellow Shareholders,

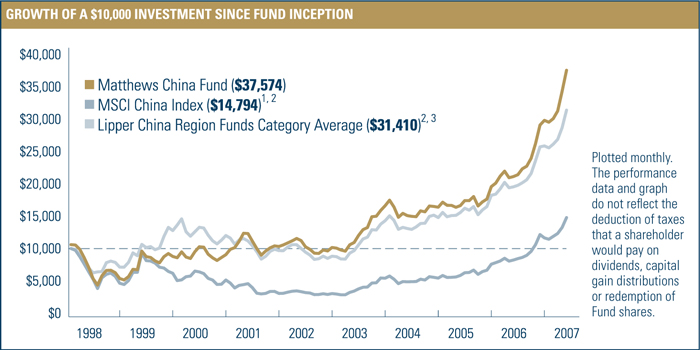

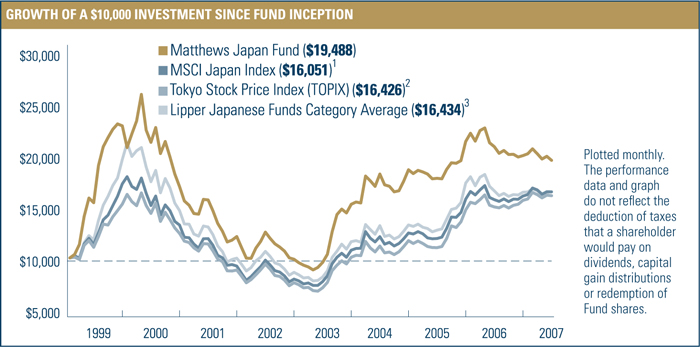

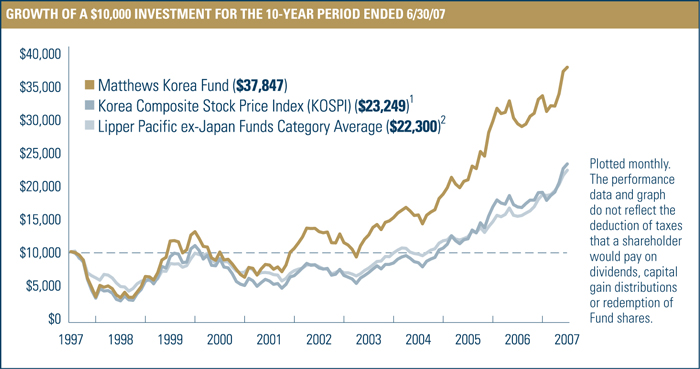

We are very pleased to be able to report that for most Asian financial markets (Japan was the major exception) the second quarter and first half of 2007 saw substantial absolute gains. While both periods were punctuated by occasional sharp corrections, particularly for domestic Chinese equities, the most recent calendar quarter generally provided solid returns for regional investors. The major differentiator of performance for regional funds during both periods was relative exposure to the Japanese equity market. Among the Matthews Asian Funds the best performer for the second quarter and year-to-date was the Matthews China Fund, while the worst was the Matthews Japan Fund.

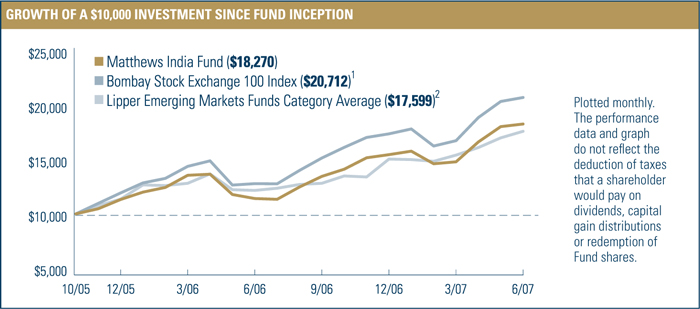

During the quarter ended June 30, the continued relatively strong performance of China and India led the regional markets. Notably, some other markets that lagged in prior periods, such as South Korea, had a strong second quarter. Asian markets outside Japan have seen generally positive returns in recent years helped by relatively strong regional growth—led again by China and India—without as many of the sudden financial shocks that have characterized the region in prior periods. The rapid development of the Chinese and Indian financial markets has dramatically changed the character and composition of regional markets, with Japan’s role declining consistently over the last ten years. This change is most dramatically seen in the composition of regional benchmarks, such as the MSCI All Country Asia Pacific Index. As recently as 1997, this benchmark had a 61% weighting to Japan, while today that weighting is only 51%. On the other hand, China and India combined now represent almost 10% of the index, versus 4% ten years ago. The current composition of many benchmarks remains constrained by the lack of convertibility of the Chinese currency, the renminbi (RMB). This means that for most investors, the close to U.S. $2 trillion in Chinese equities traded exclusively on local exchanges is not available for investment by international investors, and is generally not included in the regional benchmarks. Similarly, while India’s currency markets are more open, still many artificial barriers prevent the free flow of capital into and out of that country. Other regional markets also practice some forms of capital controls or attempt to manage local currency exchange rates, and many still impose limits on foreign ownership of some stocks and sectors. When all of these factors are taken into account, it is clear the region is likely only part way through a multi-year evolution that will continue to transform its financial markets in general, and the benchmarks of stock market performance in particular.

| 2 | MATTHEWS ASIAN FUNDS |

June 30, 2007

The lack of convertibility of the RMB is the major reason that the sudden corrections in the local Chinese equity markets—so widely reported in the Western financial press during February and June—did not have a greater impact on markets elsewhere in Asia. While the currency is closed on the capital account, the number of indirect ways in which investors can effectively gain exposure to the local currency, or conversely hedge their local currency exposure if they are locals, has increased substantially in recent years. This has increased the risk that a sudden change in the perceived value of the Chinese currency could have a ripple effect elsewhere, but for the most part China’s local markets remain somewhat insulated from outside influence. The continued transition from a closed capital market structure to one that is fully open remains probably the single greatest challenge facing China’s economic planners, but the continued success of the Chinese banks in raising capital has elevated expectations for success. While full currency convertibility for most Asian countries will eventually allow markets to more efficiently value local equities, the intervening period is likely to include more volatility as this evolutionary process unfolds.

The relative decline of Japan’s weighting in the region may not be over, but we believe that valuations across the region are no longer so obviously imbalanced and that regional integration at the corporate level is a major ongoing trend. While Japan may not currently be growing as fast as China and India, it is still the most successful economy in Asia and offers many benefits for investors that are not yet enjoyed in some less developed markets.

At Matthews Asian Funds, we have worked hard to be good stewards for our shareholders. As such, we are encouraged that Morningstar reports its Stewardship Grades. These grades go beyond a typical review of strategy, risk and return, and offer shareholders another way to evaluate fund companies, their portfolio managers and board of trustees. These ratings evaluate the extent to which a firm is aligning its interests with those of its shareholders.

Morningstar currently provides Stewardship Grades for six of the nine Matthews Asian Funds. As your investment partner, we are delighted to report that these six funds all received an A—Morningstar’s highest Stewardship Grade. In addition, each fund earned a rating of “Excellent” in at least four out of five categories. On the following page is a breakdown by category.

continued on page 4

| 800.789.ASIA [2742] www.matthewsfunds.com | 3 |

MESSAGE TO SHAREHOLDERS

continued from page 3

MORNINGSTAR STEWARDSHIP GRADESSMAS OF | OVERALL GRADE | CORPORATE CULTURE | BOARD QUALITY | MANAGER INCENTIVES | FEES | REGULATORY ISSUES | ||||||

Matthews Asia Pacific Fund | A | Excellent | Excellent | Excellent | Good | Excellent | ||||||

Matthews Pacific Tiger Fund | A | Excellent | Excellent | Excellent | Good | Excellent | ||||||

Matthews Asian Growth and Income Fund | A | Excellent | Excellent | Excellent | Excellent | Excellent | ||||||

Matthews China Fund | A | Excellent | Excellent | Good | Excellent | Excellent | ||||||

Matthews Japan Fund | A | Excellent | Excellent | Excellent | Good | Excellent | ||||||

Matthews Korea Fund | A | Excellent | Excellent | Excellent | Good | Excellent |

On a related note, we are pleased to announce that Jon Zeschin was appointed to the Matthews Asian Funds Board of Trustees in May 2007. Mr. Zeschin is the President and Founder of Essential Advisers and has more than 25 years of experience in the investment management business, encompassing virtually all aspects of managing investments for clients. Mr. Zeschin’s extensive industry experience will complement the strength of Matthews’ diverse board membership and his insights will serve our shareholders well.

As always, thank you for your investment in the Matthews Asian Funds.

|  | |

| G. Paul Matthews | Mark W. Headley | |

Chairman and Chief Investment Officer | Chief Executive Officer and Portfolio Manager | |

| Matthews International Capital Management, LLC | Matthews International Capital Management, LLC |

The Stewardship Grade is determined using some quantitative measures, but is primarily based on qualitative information gathered by Morningstar fund analysts. Each fund is assigned a letter grade from A (best) to F (worst). All funds are graded on an absolute basis. Morningstar analysts’ evaluation of the following five components determines the grade for each fund: Regulatory Issues, Board Quality, Manager Incentives, Fees and Corporate Culture. Each component is worth a maximum of 2 points, for a total, overall score of 10 possible points. Points for each component are awarded in increments as small as 0.5. With the exception of Regulatory Issues, the minimum score a fund can receive in each component is zero. For Regulatory Issues, the lowest possible score is –2. Each component score corresponds to one of the following qualitative terms: Excellent = 2 points; Good = 1.5 points; Fair = 1 point; Poor = 0.5 points; Very Poor = 0 points or fewer. The overall Stewardship Grade is based on the sum of the five component scores: A: 9 - 10 points; B: 7 - 8.5 points; C: 5 - 6.5 points; D: 3 - 4.5 points; F: 2.5 points or fewer.

© 2007 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

| 4 | MATTHEWS ASIAN FUNDS |

JUNE 30, 2007

The Funds assess a redemption fee of 2.00% of the total redemption proceeds if you sell or exchange your shares within 90 calendar days after purchasing them. The redemption fee is paid directly to the Funds and is designed to discourage frequent short-term trading and to offset transaction costs associated with such trading of Fund shares. For purposes of determining whether the redemption fee applies, the shares that have been held longest will be redeemed first. The redemption fee does not apply to redemptions of shares held in certain omnibus accounts and retirement plans that cannot currently implement the redemption fee. While these exceptions exist, the Funds are not accepting any new accounts that cannot implement the redemption fee or provide adequate alternative controls. For more information on this policy, please see the Funds’ prospectus.

INVESTOR DISCLOSURE

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. Returns are net of the Funds’ management fee and other operating expenses. If certain of the Funds’ fees and expenses had not been waived, returns would have been lower. For the Funds’ most recent month-end performance, please call 1-800-789-ASIA [2742] or visit www.matthewsfunds.com.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Please see the Funds’ prospectus and Statement of Additional Information for more risk disclosure.

Fund Holdings: The portfolios shown in this report should not be relied upon as complete listings of the Funds’ holdings, as information on particular holdings may have been withheld if it was in the Funds’ interest to do so. Holdings are subject to change at any time, so holdings shown in this report may not reflect current Fund holdings. The Funds file complete schedules of portfolio holdings with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Form N-Q is filed with the SEC within 60 days of the end the quarter to which it relates, and is available on the SEC’s website at www.sec.gov. It may also be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

Proxy Voting Record: The Funds’ Statement of Additional Information containing a description of the policies and procedures that the Matthews Asian Funds use to vote proxies relating to portfolio securities, along with each Fund’s proxy voting record relating to portfolio securities held during the 12-month period ended June 30, 2007, is available upon request, at no charge, at the Funds’ website at www.matthewsfunds.com or by calling 1-800-789-ASIA [2742], or on the SEC’s website at www.sec.gov.

This report has been prepared for Matthews Asian Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asian Funds prospectus, which contains more complete information about the Funds’ investment objectives, risks and expenses. You should read the prospectus carefully before investing. Additional copies of the prospectus may be obtained by calling 800-789-ASIA [2742] or by visiting www.matthewsfunds.com. Please read the prospectus carefully before you invest or send money, as it explains the risks associated with investing in international markets. These include risks related to social and political instability, market illiquidity and currency volatility.

The Matthews Asian Funds are distributed by PFPC Distributors, Inc., 760 Moore Road, King of Prussia, PA 19406.

| 800.789.ASIA [2742] www.matthewsfunds.com | 5 |

FUND DESCRIPTION | SYMBOL: MPACX | |

Under normal market conditions, the Matthews Asia Pacific Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies located in the Asia Pacific region. The Asia Pacific region includes Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam. The Fund may also invest in the convertible securities, of any duration or quality, of Asia Pacific companies. | ||

PORTFOLIO MANAGES

Lead Manager: Mark W. Headley

Co-Managers: Richard H. Gao, Taizo Ishida and Sharat Shroff, CFA

PORTFOLIO MANAGER COMMENTARY

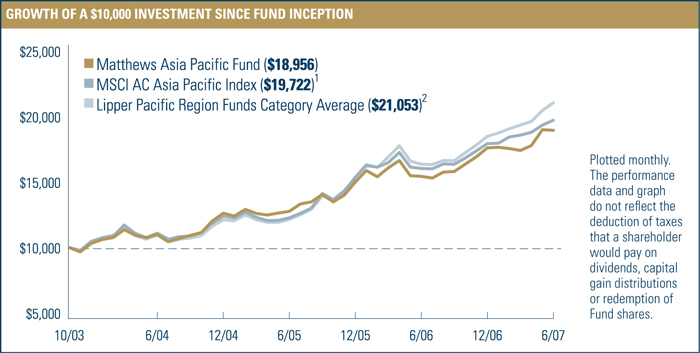

The Matthews Asia Pacific Fund gained 7.63% in the first half of 2007 while its benchmark, the MSCI All Country Asia Pacific Index gained 9.95%. The Lipper Pacific Region Funds Category Average returned 12.58% for the same period. The year began on a volatile note with considerable variation in performance across the different markets. However, barring a momentary blip in the mainland Chinese stock market and the sideways trend in Japan, the region experienced a period of steady gains in the second quarter, overcoming record levels of equity issuance. The portfolio gained some ground in the second quarter, helped by a rally in financials, but trailed its benchmark on a year-to-date basis due to limited exposure to commodities and industrials.

The lackluster performance of the Japanese markets continued to be a drag on the Fund’s absolute performance. In spite of the fourth consecutive year of profit growth in corporate Japan, investor skepticism on the pace of recovery remains high. That said, we believe there are attractive opportunities, and our firm conviction in the long-term potential of individual Japanese companies led us to increase our exposure to the market during the period. Such a contrarian action during a period where all eyes are on the developing Asian markets has been painful, but is consistent with our long-term search for an appropriate balance between growth and value.

Some of the Fund’s holdings in the Chinese financial sector were the biggest contributors to performance; these companies benefited from aggressive buying by investors on the domestic “A share” markets in Shanghai and Shenzhen (note: the Fund has no positions in

continued on page 8

| 6 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

PERFORMANCE AS OF JUNE 30, 2007

| Average Annual Total Returns | |||||||||||||||

Fund Inception: 10/31/03 | 3 MO | YTD | 1 YR | 3 YRS | SINCE INCEPTION | ||||||||||

Matthews Asia Pacific Fund | 8.85 | % | 7.63 | % | 22.79 | % | 19.89 | % | 19.06 | % | |||||

MSCI All Country Asia Pacific Index 1 | 6.13 | % | 9.95 | % | 22.98 | % | 21.11 | % | 20.35 | % | |||||

Lipper Pacific Region Funds Category Average 2 | 8.00 | % | 12.58 | % | 28.35 | % | 24.15 | % | 22.29 | % | |||||

All performance quoted is past performance and is no guarantee of future results. Assumes reinvestment of all dividends and/or distributions. Unusually high returns may not be sustainable. Investment return and principal value will fluctuate with changing market conditions so that shares, when redeemed, may be worth more or less than their original cost. The performance of foreign indices may be based on different exchange rates than those used by the Fund and, unlike the Fund’s NAV, is not adjusted to reflect fair value at the close of the NYSE. Current performance may be lower or higher than the return figures quoted. Returns are net of the Funds’ management fee and other operating expenses. Returns would have been lower if certain of the Funds’ fees and expenses had not been waived. For the Funds’ most recent month-end performance please call 800-789-ASIA [2742] or visit www.matthewsfunds.com.

OPERATING EXPENSES3

Net Ratio: 6 months ended 6/30/07 (annualized) 4,5 | 1.18 | % | |

Net Ratio: Fiscal Year 2006 5 | 1.24 | % | |

Gross Ratio: Fiscal Year 2006 | 1.26 | % |

PORTFOLIO TURNOVER6

6 months ended 6/30/07 (annualized) 4 | 58.03 | % | |

Fiscal Year 2006 | 40.45 | % |

1 | The MSCI All Country Asia Pacific Index is a free float-adjusted market capitalization–weighted index of the stock markets of Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, Philippines, Singapore, South Korea, Taiwan and Thailand. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by PFPC Inc. |

2 | As of 6/30/07, the Lipper Pacific Region Funds Category Average consisted of 33 funds for the three-month and YTD periods, 28 funds for the one-year period, and 25 funds for the three-year period and since 10/31/03. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains, for the stated periods. |

3 | Matthews Asian Funds do not charge 12b-1 fees. |

4 | Unaudited. |

5 | Includes management fee, administration and shareholder services fees after reimbursement, waiver or recapture of expenses by Advisor. Voluntary fee waivers by the Advisor may be discontinued at any time. |

6 | The lesser of fiscal year-to-date long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 800.789.ASIA [2742] www.matthewsfunds.com | 7 |

MATTHEWS ASIA PACIFIC FUND

TOP TEN HOLDINGS1

COUNTRY | % OF NET ASSETS | |||

Sony Corp. | Japan | 2.5% | ||

Amorepacific Corp. | South Korea | 2.4% | ||

Lenovo Group, Ltd. | China/Hong Kong | 2.3% | ||

AXA Asia Pacific Holdings, Ltd. | Australia | 2.2% | ||

Nintendo Co., Ltd. | Japan | 2.2% | ||

Hana Financial Group, Inc. | South Korea | 2.1% | ||

China Life Insurance Co., Ltd. | China/Hong Kong | 2.1% | ||

Hanmi Pharmaceutical Co., Ltd. | South Korea | 2.1% | ||

Pico Far East Holdings, Ltd. | China/Hong Kong | 2.0% | ||

Advanced Info Service Public Co., Ltd. | Thailand | 1.9% | ||

% OF ASSETS IN TOP 10 | 21.8% |

COUNTRY ALLOCATION

Japan | 42.9 | % | |

China/Hong Kong | 20.7 | % | |

South Korea | 14.2 | % | |

India | 6.2 | % | |

Thailand | 5.0 | % | |

Singapore | 3.5 | % | |

Taiwan | 2.8 | % | |

Indonesia | 2.3 | % | |

Australia | 2.2 | % | |

Cash, cash equivalents and other | 0.2 | % |

SECTOR ALLOCATION

Financials | 34.0 | % | |

Information Technology | 20.8 | % | |

Consumer Discretionary | 19.8 | % | |

Consumer Staples | 9.1 | % | |

Health Care | 6.7 | % | |

Telecommunication Services | 3.4 | % | |

Industrials | 3.4 | % | |

Materials | 2.6 | % | |

Cash, cash equivalents and other | 0.2 | % |

MARKET CAP EXPOSURE

Large cap (over $5 billion) | 58.0 | % | |

Mid cap ($1–$5 billion) | 28.5 | % | |

Small cap (under $1 billion) | 13.3 | % | |

Cash, cash equivalents and other | 0.2 | % |

NUMBER OF SECURITIES | NAV | FUND ASSETS | REDEMPTION FEE | 12B-1 FEES | ||||||

73 | $ | 18.21 | $ | 471.7 million | 2.00% within 90 calendar days | None | ||||

1 | Holdings may combine more than one security from same issuer. |

PORTFOLIO MANAGER COMMENTARY continued from page 6

Chinese “A shares”). This enthusiasm spilled over to the Hong Kong markets where Chinese companies are available to international investors. This spillover effect is likely to remain a source of serious volatility. The Fund continues to participate in the growth of the Chinese economy through its investment in “H shares” listed in Hong Kong, and some exposure to “B shares” of higher quality mainland stocks, although we trimmed our exposure during the first half of the year.

By contrast, we modestly raised the Fund’s allocation to Korea, and in particular the financial services sector. The recent passage

| 8 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

of the Capital Market Consolidation Act (CMCA) is a significant development aimed at liberalizing Korea’s capital markets along two key dimensions. CMCA is likely to lead to greater innovation in product and service offerings, and jump start consolidation in Korea’s financial services landscape, making it more competitive globally. Separately, the Fund’s holdings in media and pharmaceuticals have staged a modest recovery, but continue to lag the overall market on concerns over the recently signed free-trade agreement between Korea and the U.S.

The portfolio has a relatively defensive tilt to India where the market is in its fourth year of strong gains. Inflation, as measured by Wholesale Price Index (WPI) based metrics, seems to have receded from its high base a year ago. This change was aided by a strengthening currency; however, demand trends remain robust and inflation may pick up in the second half of the year. Further, there seems to be an accelerating trend of cross-border acquisitions as Indian companies strive to build a broader platform for growth. Sun Pharmaceuticals is one of the companies that has demonstrated effective management capabilities in this regard. Relative to some of its industry peers, Sun’s management has successfully acquired struggling companies and turned them around. Keen understanding of the industry coupled with a solid price discipline have enabled Sun to generate profitability from these companies even in competitive markets like the U.S.

Ten years after the Asian financial crisis, corporate balance sheets are much healthier. Looking ahead, one of the key questions facing investors is the ability of the region to withstand a global slowdown. In that context, it is encouraging to see signs of greater integration within the Asia Pacific region: whether it is Indian companies hiring from Chinese universities, Chinese companies seeking to list on the Tokyo exchange, or Australian skiers buying condominiums in Hokkaido. Beyond just companies and consumers, even the governments have shown a willingness to cooperate more closely. In early May, finance ministers from the ASEAN+3 countries stitched together an initial agreement to pool their foreign reserves in an effort to bring greater stability to the currencies in the region. Over time, such efforts can become substantial drivers to sustaining growth and we continue to look for investment ideas that are beneficiaries of this long-term trend.

| 800.789.ASIA [2742] www.matthewsfunds.com | 9 |

MATTHEWS ASIA PACIFIC FUND

SCHEDULE OF INVESTMENTS (UNAUDITED)

EQUITIES: 99.8%*

| SHARES | VALUE | ||||

JAPAN: 42.9% | |||||

Sony Corp. ADR | 227,800 | $ | 11,702,086 | ||

Nintendo Co., Ltd. | 27,800 | 10,182,985 | |||

The Sumitomo Trust & Banking Co., Ltd. | 907,000 | 8,655,634 | |||

Nitto Denko Corp. | 157,200 | 7,941,393 | |||

Sekisui House, Ltd. | 578,000 | 7,722,315 | |||

Daibiru Corp. | 551,700 | 7,662,189 | |||

Benesse Corp. | 258,700 | 7,500,987 | |||

Nomura Research Institute, Ltd. | 254,000 | 7,488,487 | |||

Sysmex Corp. | 198,500 | 7,335,431 | |||

Funai Zaisan Consultants Co., Ltd. | 1,232 | 7,224,398 | |||

Ichiyoshi Securities Co., Ltd. | 498,400 | 7,221,487 | |||

Toyota Motor Corp. ADR | 55,600 | 6,998,928 | |||

Hoya Corp. | 209,400 | 6,955,906 | |||

Sumitomo Realty & Development Co., Ltd. | 213,000 | 6,954,396 | |||

Ito En, Ltd. | 211,000 | 6,940,508 | |||

Point, Inc. | 111,470 | 6,618,036 | |||

Canon, Inc. ADR | 109,050 | 6,394,692 | |||

ORIX Corp. | 23,490 | 6,190,867 | |||

Takeda Pharmaceutical Co., Ltd. | 95,600 | 6,180,516 | |||

Mitsubishi Estate Co., Ltd. | 226,000 | 6,149,036 | |||

Unicharm Petcare Corp. | 149,000 | 6,014,457 | |||

Yahoo! Japan Corp. | 17,612 | 5,986,292 | |||

Nitori Co., Ltd. | 111,900 | 5,589,320 | |||

Mizuho Financial Group, Inc. | 794 | 5,500,767 | |||

Pigeon Corp. | 334,300 | 5,424,824 | |||

Keyence Corp. | 24,100 | 5,271,172 | |||

Monex Beans Holdings, Inc. | 5,700 | 4,768,325 | |||

Nidec Corp. | 79,500 | 4,674,761 | |||

The Chiba Bank, Ltd. | 519,000 | 4,611,460 | |||

Nippon Shokubai Co., Ltd. | 500,000 | 4,446,700 | |||

Total Japan | 202,308,355 | ||||

CHINA/HONG KONG: 20.7% | |||||

Lenovo Group, Ltd. | 18,634,000 | 10,986,129 | |||

China Life Insurance Co., Ltd. H Shares | 2,771,000 | 9,958,193 | |||

Pico Far East Holdings, Ltd. | 29,774,000 | 9,519,516 | |||

China Merchants Bank Co., Ltd. H Shares | 2,721,500 | 8,283,674 | |||

Dah Sing Financial Holdings, Ltd. | 969,200 | 8,174,588 | |||

China Vanke Co., Ltd. B Shares | 3,752,514 | 7,769,746 | |||

China Mobile, Ltd. ADR | 135,300 | 7,292,670 | |||

Hang Lung Group, Ltd. | 1,553,000 | 7,011,063 | |||

The9, Ltd. ADR** | 145,900 | 6,749,334 | |||

Dairy Farm International Holdings, Ltd. | 1,256,400 | 5,678,928 | |||

Television Broadcasts, Ltd. | 788,000 | 5,542,766 | |||

Shangri-La Asia, Ltd. | 2,276,000 | 5,501,381 | |||

NetEase.com, Inc. ADR** | 301,000 | 5,123,020 | |||

Belle International Holdings, Ltd.** | 51,000 | 56,288 | |||

China High Speed Transmission Equipment Group Co., Ltd.**,***,**** | 23,000 | 26,694 | |||

Total China/Hong Kong | 97,673,990 | ||||

SOUTH KOREA: 14.2% | |||||

Amorepacific Corp. | 14,262 | 11,300,305 | |||

Hana Financial Group, Inc. | 205,120 | 10,002,334 | |||

Hanmi Pharmaceutical Co., Ltd. | 63,131 | 9,703,525 | |||

ON*Media Corp.** | 714,300 | 6,618,399 | |||

NHN Corp.** | 32,651 | 5,955,180 | |||

CDNetworks Co., Ltd.** | 231,427 | 5,648,838 | |||

Kiwoom.com Securities Co., Ltd. | 72,512 | 5,533,470 | |||

Hyundai Department Store Co., Ltd. | 45,970 | 5,423,748 | |||

Samsung Electronics Co., Ltd. | 5,465 | 3,348,152 | |||

Kookmin Bank ADR | 35,540 | 3,117,569 | |||

Kiwoom.com Securities Co., Ltd. Rights, expire 07/11/07***, **** | 14,509 | 207,307 | |||

Total South Korea | 66,858,827 | ||||

| 10 | MATTHEWS ASIAN FUNDS |

JUNE 30, 2007

| SHARES | VALUE | ||||

INDIA: 6.2% | |||||

Sun Pharmaceutical Industries, Ltd. | 298,907 | $ | 7,530,503 | ||

Dabur India, Ltd. | 2,973,060 | 7,512,080 | |||

HDFC Bank, Ltd. | 260,636 | 7,342,693 | |||

Infosys Technologies, Ltd. | 125,678 | 5,956,004 | |||

Sun Pharma Advanced Research Co., Ltd.**,***,**** | 298,907 | 986,345 | |||

Total India | 29,327,625 | ||||

THAILAND: 5.0% | |||||

Advanced Info Service Public Co., Ltd. | 3,611,600 | 9,048,614 | |||

Bangkok Bank Public Co., Ltd. | 1,658,500 | 5,860,594 | |||

Land & Houses Public Co., Ltd. | 22,417,300 | 4,869,797 | |||

Major Cineplex Group Public Co., Ltd. | 7,285,400 | 4,051,548 | |||

Total Thailand | 23,830,553 | ||||

SINGAPORE: 3.5% | |||||

DBS Group Holdings, Ltd. | 442,700 | 6,593,866 | |||

Fraser and Neave, Ltd. | 1,462,000 | 5,205,226 | |||

Hyflux, Ltd. | 2,476,812 | 4,740,852 | |||

Total Singapore | 16,539,944 | ||||

TAIWAN: 2.8% | |||||

Taiwan Semiconductor Manufacturing Co., Ltd. | 3,392,999 | 7,319,529 | |||

Taiwan Secom Co., Ltd. | 3,579,160 | 6,098,490 | |||

Total Taiwan | 13,418,019 | ||||

INDONESIA: 2.3% | |||||

PT Astra International | 3,000,500 | 5,612,446 | |||

Bank Rakyat Indonesia | 7,889,500 | 5,020,988 | |||

Total Indonesia | 10,633,434 | ||||

AUSTRALIA: 2.2% | |||||

AXA Asia Pacific Holdings, Ltd. | 1,647,685 | 10,379,046 | |||

Total Australia | 10,379,046 | ||||

TOTAL INVESTMENTS: 99.8% (Cost $382,525,452*****) | 470,969,793 | ||||

CASH AND OTHER ASSETS, LESS LIABILITIES: 0.2% | 718,394 | ||||

NET ASSETS: 100.0% | $ | 471,688,187 | |||

| * | As a percentage of net assets as of June 30, 2007 |

| ** | Non–income producing security |

| *** | Fair valued under direction of the Board of Trustees |

| **** | Illiquid security |

| ***** | Cost of investments is $382,525,452 and net unrealized appreciation consists of: |

Gross unrealized appreciation | $ | 107,065,464 | ||

Gross unrealized depreciation | (18,621,123 | ) | ||

Net unrealized appreciation | $ | 88,444,341 | ||

| ADR | American Depositary Receipt |

See accompanying notes to financial statements.

| 800.789.ASIA [2742] www.matthewsfunds.com | 11 |

MATTHEWS ASIA PACIFIC EQUITY INCOME FUND

FUND DESCRIPTION | SYMBOL: MAPIX |

Under normal market conditions, the Matthews Asia Pacific Equity Income Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in income-paying publicly traded common stocks, preferred stocks, convertible preferred stocks, and other equity-related instruments (including, for example, investment trusts and other financial instruments) of companies located in the Asia Pacific region, which includes Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam.

PORTFOLIO MANAGERS

Lead Manager: Andrew T. Foster | Co-Manager: Jesper Madsen, CFA |

PORTFOLIO MANAGER COMMENTARY

The Matthews Asia Pacific Equity Income Fund returned 10.80% for the first six months of 2007. By comparison, its benchmark the MSCI All Country Asia Pacific Index, gained 9.95%. The Fund paid its inaugural semi-annual income distribution of 10.3 cents per share on June 26, as per its stated intention to distribute investment income twice per year.

Relative calm returned to the region’s markets in the second quarter after the sharp sell-off in late February, and most equity markets saw positive returns during the period. The notable exception was Japan. The broad TOPIX Index ended only 2.3% shy of its highest level since 1991, but returns from Japanese equities were weighed down by the 3.3% depreciation of the yen year-to-date. In fact, the yen was the only major Asian currency to lose value relative to the U.S. dollar during the first six months of the year. Japan has now experienced positive real economic growth in 19 consecutive quarters, but consumer price inflation has yet to definitively beat out deflation. This, coupled with political pressure on the Bank of Japan to refrain from hiking interest rates, heightened the uncertainty surrounding the outlook for interest rates.

Much like other markets around the world, Asia Pacific has seen the privatization of an increasing number of publicly listed companies, either through leveraged buyouts or private equity deals. This activity is in part fuelled by the low cost of borrowing relative to the cash flows generated by the targeted companies, enabling larger deals to take place. This is particularly true in industries that exhibit stable cash flows, such as telecommunication service providers. In fact, during the first half of the year the main contributor to Fund performance, Maxis Communications, was taken private by its largest shareholder.

continued on page 14

| 12 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

PERFORMANCE AS OF JUNE 30, 2007

Fund Inception: 10/31/06 | 3 MO | YTD | SINCE INCEPTION1 | ||||||

Matthews Asia Pacific Equity Income Fund | 8.19 | % | 10.80 | % | 19.56 | % | |||

MSCI All Country Asia Pacific Index 2 | 6.13 | % | 9.95 | % | 17.06 | % |

All performance quoted is past performance and is no guarantee of future results. Assumes reinvestment of all dividends and/or distributions. Unusually high returns may not be sustainable. Investment return and principal value will fluctuate with changing market conditions so that shares, when redeemed, may be worth more or less than their original cost. The performance of foreign indices may be based on different exchange rates than those used by the Fund and, unlike the Fund’s NAV, is not adjusted to reflect fair value at the close of the NYSE. Current performance may be lower or higher than the return figures quoted. Returns are net of the Funds’ management fee and other operating expenses. Returns would have been lower if certain of the Funds’ fees and expenses had not been waived. For the Funds’ most recent month-end performance please call 800-789-ASIA [2742] or visit www.matthewsfunds.com.

OPERATING EXPENSES3

Net Ratio: 6 months ended 6/30/07 (annualized) 4,5 | 1.47 | % | |

Net Ratio: Fiscal Period 2006 (annualized) 5,7 | 1.50 | % | |

Gross Ratio: Fiscal Period 2006 (annualized) 7 | 2.93 | % |

PORTFOLIO TURNOVER6

6 months ended 6/30/07 (annualized) 4 | 19.12 | % | |

Fiscal Period 2006 (annualized) 7 | 0.00 | % |

TOP TEN HOLDINGS8

COUNTRY | % OF NET ASSETS | |||

Taiwan Semiconductor Manufacturing Co., Ltd. | Taiwan | 4.9% | ||

HSBC Holdings PLC | United Kingdom | 4.6% | ||

Lawson, Inc. | Japan | 3.1% | ||

SK Telecom Co., Ltd. | South Korea | 2.8% | ||

BOC Hong Kong Holdings, Ltd. | China/Hong Kong | 2.6% | ||

Globe Telecom, Inc. | Philippines | 2.6% | ||

Monex Beans Holdings, Inc. | Japan | 2.4% | ||

Eisai Co., Ltd. | Japan | 2.4% | ||

Public Bank BHD | Malaysia | 2.4% | ||

Hana Finacial Group, Inc. | South Korea | 2.4% | ||

% OF ASSETS IN TOP 10 | 30.2% |

1 | Actual returns, not annualized. |

2 | The MSCI All Country Asia Pacific Index is a free float-adjusted market capitalization–weighted index of the stock markets of Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, Philippines, Singapore, South Korea, Taiwan and Thailand. The Matthews Asia Pacific Equity Income Fund invests in countries that are not included in the MSCI All Country Asia Pacific Index. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by PFPC Inc. |

3 | Matthews Asian Funds do not charge 12b-1 fees. |

4 | Unaudited. |

5 | Includes management fee, administration and shareholder services fees after reimbursement, waiver or recapture or expenses by Advisor. The Advisor has agreed to waive fees and reimburse expenses to the extent needed to limit total annual operating expenses until October 31, 2009. Voluntary fee waivers by the Advisor may be discontinued at any time. |

6 | The lesser of fiscal year-to-date long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

7 | The Matthews Asia Pacific Equity Income Fund commenced operations on 10/31/06. |

8 | Holdings may combine more than one security from same issuer. |

| 800.789.ASIA [2742] www.matthewsfunds.com | 13 |

MATTHEWS ASIA PACIFIC EQUITY INCOME FUND

COUNTRY ALLOCATION

China/Hong Kong | 18.7 | % | |

Japan | 17.8 | % | |

Taiwan | 12.8 | % | |

Malaysia | 9.1 | % | |

Singapore | 7.1 | % | |

Australia | 6.8 | % | |

Thailand | 5.6 | % | |

South Korea | 5.1 | % | |

United Kingdom 1 | 4.6 | % | |

India | 4.1 | % | |

Philippines | 2.5 | % | |

Indonesia | 1.5 | % | |

New Zealand | 1.5 | % | |

Cash, cash equivalents and other2 | 2.8 | % |

SECTOR ALLOCATION

Financials | 24.7 | % | |

Consumer Discretionary | 17.3 | % | |

Information Technology | 14.5 | % | |

Telecommunication Services | 14.5 | % | |

Consumer Staples | 6.8 | % | |

Industrials | 5.8 | % | |

Health Care | 5.6 | % | |

Energy | 4.4 | % | |

Utilities | 3.6 | % | |

Cash, cash equivalents and other2 | 2.8 | % |

MARKET CAP EXPOSURE

Large cap (over $5 billion) | 54.6 | % | |

Mid cap ($1–$5 billion) | 28.6 | % | |

Small cap (under $1 billion) | 14.0 | % | |

Cash, cash equivalents and other2 | 2.8 | % |

NUMBER OF SECURITIES2 | NAV | FUND ASSETS | REDEMPTION FEE | 12B-1 FEES | ||||

54 | $11.83 | $63.1 million | 2.00% within 90 calendar days | None |

1 | The United Kingdom is not included in the MSCI All Country Asia Pacific Index. |

2 | Includes BNY Hamilton Money Fund. |

PORTFOLIO MANAGER COMMENTARY continued from page 12

Maxis Communications is a leading Malaysian telecommunications provider with a strong position in Malaysia and a growing business in India. While the growth of new wireless subscribers in the Malaysian market was decelerating as mobile phone penetration rose, we believed the company could increasingly afford to pay higher dividends, and yet still invest in overseas expansion opportunities. We felt the market was discounting the company’s future growth prospects in Malaysia, as well as the likelihood of success in its Indian expansion. This resulted in both an attractive current dividend yield and good potential for dividend growth.

The Fund built its position in Maxis with the intention of holding shares over the long term. However, shareholders in Maxis Communications received a 20% takeover premium on top of the more than 30% price appreciation in the months leading up to the offer. We felt the company might be worth a great deal more to patient investors; yet as the vast majority of shareholders indicated a preference for a quick gain, we had little choice but to submit our shares in the tender so as to avoid seeing the Fund’s holdings in Maxis forcibly privatized.

While we are pleased to report that the Fund outperformed its benchmark during the first

| 14 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

half of 2007, there were sources of weakness in the portfolio during the period. For example, the Fund’s holdings in large banks were a drag on aggregate performance. The valuation of these banks are to some extent penalized for having a lower growth rate than their smaller peers and are often perceived as too large to be acquisition targets. Furthermore, investors have focused on the impact of rising subprime mortgage defaults, and their spillover effects on growth and interest rates in the U.S. Despite having liquid balance sheets, good (if underrated) growth prospects, strong dividend policies and very reasonable yields, the performance of Asia’s larger banks has generally lagged the markets, weighed down by this sort of global sentiment.

In addition, the Fund would have benefited from greater exposure to Korean equities during the first half of the year. The Korea Composite Stock Price Index gained 22.39% during the second quarter alone. However, even though Korean valuations measured via price to earnings multiples were some of the cheapest in Asia Pacific, this was not reflected in higher dividend yields. The reason is simple: On average, Korean companies pay out a smaller portion of their earnings as dividends to shareholders, relative to companies elsewhere in the region. To date, this has made it harder to justify having a more substantial exposure to Korea.

We continue to look for companies offering reasonably priced and growing dividends. This explains our ongoing exposure to Japanese companies, which we still believe offer good potential for dividend growth, as we discussed in the previous quarterly report. We are also maintaining substantial exposure to the region’s larger banks, across several geographies. We believe their underperformance thus far this year represents an opportunity, and their lower valuations may also prove more defensive if a downturn were to occur.

| 800.789.ASIA [2742] www.matthewsfunds.com | 15 |

MATTHEWS ASIA PACIFIC EQUITY INCOME FUND

SCHEDULE OF INVESTMENTS (UNAUDITED)

EQUITIES: 97.2%*

| SHARES | VALUE | ||||

CHINA/HONG KONG: 18.7% | |||||

BOC Hong Kong Holdings, Ltd. | 692,000 | $ | 1,647,872 | ||

CLP Holdings, Ltd. | 195,500 | 1,311,384 | |||

Hang Seng Bank, Ltd. | 91,300 | 1,235,362 | |||

Café de Coral Holdings, Ltd. | 648,000 | 1,228,177 | |||

SA SA International Holdings, Ltd. | 3,156,000 | 1,162,431 | |||

ASM Pacific Technology, Ltd. | 142,000 | 1,028,788 | |||

VTech Holdings, Ltd. | 121,000 | 1,021,332 | |||

Huaneng Power International, Inc. H Shares | 836,000 | 949,417 | |||

PetroChina Co., Ltd. H Shares | 614,000 | 904,604 | |||

China Mobile, Ltd. | 65,500 | 703,234 | |||

PetroChina Co., Ltd. ADR | 4,200 | 624,456 | |||

Total China/Hong Kong | 11,817,057 | ||||

JAPAN: 17.8% | |||||

Lawson, Inc. | 56,700 | 1,961,762 | |||

Monex Beans Holdings, Inc. | 1,834 | 1,534,229 | |||

Eisai Co., Ltd. | 34,700 | 1,516,231 | |||

The Sumitomo Trust & Banking Co., Ltd. | 154,000 | 1,469,645 | |||

Benesse Corp. | 41,800 | 1,211,988 | |||

Takeda Pharmaceutical Co., Ltd. | 17,200 | 1,111,976 | |||

Hisamitsu Pharmaceutical Co., Inc. | 32,500 | 897,462 | |||

Tokyu REIT, Inc. | 80 | 773,198 | |||

Nintendo Co., Ltd. | 2,000 | 732,589 | |||

Total Japan | 11,209,080 | ||||

TAIWAN: 12.8% | |||||

Taiwan Semiconductor Manufacturing Co., Ltd. | 1,336,287 | 2,882,699 | |||

Chunghwa Telecom Co., Ltd. | 780,000 | 1,488,042 | |||

Taiwan Secom Co., Ltd. | 762,000 | 1,298,363 | |||

Giant Manufacturing Co., Ltd. | 647,000 | 1,187,066 | |||

President Chain Store Corp. | 372,000 | 1,059,429 | |||

Taiwan Semiconductor Manufacturing Co., Ltd. ADR | 17,587 | 195,747 | |||

Total Taiwan | 8,111,346 | ||||

MALAYSIA: 9.1% | |||||

Public Bank BHD | 527,800 | 1,498,172 | |||

Maxis Communications BHD**,*** | 279,500 | 1,243,482 | |||

Media Prima BHD | 1,375,000 | 1,202,752 | |||

Malayan Banking BHD | 285,300 | 991,629 | |||

Berjaya Sports Toto BHD | 541,200 | 822,969 | |||

Total Malaysia | 5,759,004 | ||||

SINGAPORE: 7.1% | |||||

Singapore Press Holdings, Ltd. | 479,000 | 1,451,942 | |||

Venture Corp., Ltd. | 106,000 | 1,087,180 | |||

Singapore Post, Ltd. | 1,301,000 | 1,079,386 | |||

Yellow Pages (Singapore), Ltd. | 933,000 | 835,022 | |||

Total Singapore | 4,453,530 | ||||

AUSTRALIA: 6.8% | |||||

Coca-Cola Amatil, Ltd. | 159,498 | 1,290,025 | |||

Insurance Australia Group, Ltd. | 257,554 | 1,244,622 | |||

TABCORP Holdings, Ltd. | 62,393 | 907,182 | |||

St. George Bank, Ltd. | 27,964 | 839,972 | |||

Total Australia | 4,281,801 | ||||

THAILAND: 5.6% | |||||

Advanced Info Service Public Co., Ltd. | 540,600 | 1,354,436 | |||

PTT Public Co., Ltd. | 160,000 | 1,251,267 | |||

Hana Microelectronics Public Co., Ltd. | 1,120,600 | 916,928 | |||

Total Thailand | 3,522,631 | ||||

SOUTH KOREA: 5.1% | |||||

Hana Financial Group, Inc. | 30,590 | 1,491,670 | |||

SK Telecom Co., Ltd. | 3,913 | 902,169 | |||

SK Telecom Co., Ltd. ADR | 31,300 | 856,055 | |||

Total South Korea | 3,249,894 | ||||

| 16 | MATTHEWS ASIAN FUNDS |

JUNE 30, 2007

| SHARES | VALUE | ||||

UNITED KINGDOM: 4.6% | |||||

HSBC Holdings PLC ADR | 16,900 | $ | 1,550,913 | ||

HSBC Holdings PLC | 73,600 | 1,341,314 | |||

Total United Kingdom | 2,892,227 | ||||

INDIA: 4.1% | |||||

HCL-Infosystems, Ltd. | 280,167 | 1,307,400 | |||

Ashok Leyland, Ltd. | 1,365,000 | 1,269,261 | |||

Total India | 2,576,661 | ||||

PHILIPPINES: 2.5% | |||||

Globe Telecom, Inc. | 54,950 | 1,609,886 | |||

Total Philippines | 1,609,886 | ||||

INDONESIA: 1.5% | |||||

PT Telekomunikasi Indonesia | 559,000 | 609,424 | |||

PT Telekomunikasi Indonesia ADR | 8,200 | 353,420 | |||

Total Indonesia | 962,844 | ||||

NEW ZEALAND: 1.5% | |||||

Fisher & Paykel Appliances Holdings, Ltd. | 345,798 | 927,680 | |||

Total New Zealand | 927,680 | ||||

TOTAL EQUITIES (Cost $56,860,534) | 61,373,641 | ||||

MONEY MARKET MUTUAL FUND: 1.2%* | |||||

BNY Hamilton Money Fund (Cost $ 752,625) | 752,625 | 752,625 | |||

TOTAL INVESTMENTS: 98.4% (Cost $57,613,159****) | 62,126,266 | ||||

CASH AND OTHER ASSETS, LESS LIABILITIES: 1.6% | 998,373 | ||||

NET ASSETS: 100.0% | $ | 63,124,639 | |||

| * | As a percentage of net assets as of June 30, 2007 |

| ** | Fair valued under direction of the Board of Trustees |

| *** | Illiquid security |

| **** | Cost of investments is $57,613,159 and net unrealized appreciation consists of: |

Gross unrealized appreciation | $ | 5,443,849 | ||

Gross unrealized depreciation | (930,742 | ) | ||

Net unrealized appreciation | $ | 4,513,107 | ||

ADR American Depositary Receipt

REIT Real Estate Investment Trust

See accompanying notes to financial statements.

| 800.789.ASIA [2742] www.matthewsfunds.com | 17 |

MATTHEWS PACIFIC TIGER FUND (CLOSED TO MOST NEW INVESTORS)

FUND DESCRIPTION | SYMBOL: MAPTX |

Under normal market conditions, the Matthews Pacific Tiger Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies located in the Pacific Tiger countries of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam.

PORTFOLIO MANAGERS

Lead Manager: Mark W. Headley | Co-Manager: Richard H. Gao |

PORTFOLIO MANAGER COMMENTARY

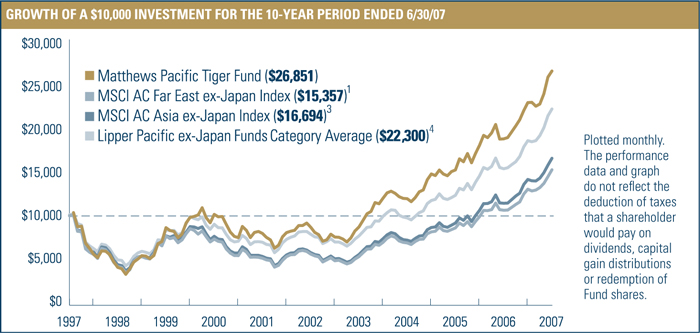

The Matthews Pacific Tiger Fund participated in a strong rally in the second quarter of 2007, giving the Fund a return of 15.86% for the first six months of the year. While the Fund outperformed both its indices and the Lipper averages in the second quarter, this was not enough to catch up after the underperformance in the first quarter. For the first half of the year, the MSCI All Country Far East ex-Japan Index gained 17.27% and the MSCI All Country Asia ex-Japan Index, which includes India, advanced 17.31%. During the same period, the Lipper Pacific ex-Japan Funds Category Average gained 20.39%. Markets were generally strong during the second quarter with China, India and Korea all enjoying significant rallies on the back of greater economic confidence in the regional environment.

On a geographic basis, China and Hong Kong were the dominant sources of returns for the portfolio in the first half of the year. Lenovo in China and Hang Lung Group in Hong Kong had the largest positive impact on performance. Korea, Singapore, Thailand and India all made positive contributions, with positions in Korea and Thailand showing real strength in the last few months. From an industry perspective, financials have been the primary source of returns. Property exposure in China and brokerage in Korea are examples of strong performing non-banking financials in the portfolio; the returns for bank holdings, however, were quite mixed. The information technology and consumer discretionary sectors were also areas of strength for the portfolio. The Fund’s large position in health care–related companies was the weakest area for the portfolio, with pharmaceuticals underperforming badly in a period of general market strength.

Why has the portfolio underperformed indices and competitors in the recent one- and three-year periods? It is a complex question that involves multiple issues. Certainly, we have managed the Fund with an eye to avoiding excessive risk. One example is the avoidance of ultra–high valuation growth stocks. This approach has generally not helped in a period of great enthusiasm with many top growth companies

continued on page 21

| 18 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

PERFORMANCE AS OF JUNE 30, 2007

| Average Annual Total Returns | |||||||||||||||||||||

Fund Inception: 9/12/94 | 3 MO | YTD | 1 YR | 3 YRS | 5 YRS | 10 YRS | SINCE INCEPTION | ||||||||||||||

Matthews Pacific Tiger Fund | 16.70 | % | 15.86 | % | 41.66 | % | 30.82 | % | 25.34 | % | 10.38 | % | 10.27 | % | |||||||

MSCI All Country Far East ex-Japan Index 1 | 15.58 | % | 17.27 | % | 44.21 | % | 30.94 | % | 22.61 | % | 4.38 | % | 4.05 | %2 | |||||||

MSCI All Country Asia ex-Japan Index 3 | 16.09 | % | 17.31 | % | 45.68 | % | 32.56 | % | 23.92 | % | 5.26 | % | 4.45 | %2 | |||||||

Lipper Pacific ex-Japan Funds Category Average 4 | 16.09 | % | 20.39 | % | 46.62 | % | 33.48 | % | 23.25 | % | 7.69 | % | 6.89 | %2 | |||||||

All performance quoted is past performance and is no guarantee of future results. Assumes reinvestment of all dividends and/or distributions. Unusually high returns may not be sustainable. Investment return and principal value will fluctuate with changing market conditions so that shares, when redeemed, may be worth more or less than their original cost. The performance of foreign indices may be based on different exchange rates than those used by the Fund and, unlike the Fund’s NAV, is not adjusted to reflect fair value at the close of the NYSE. Current performance may be lower or higher than the return figures quoted. Returns are net of the Funds’ management fee and other operating expenses. Returns would have been lower if certain of the Funds’ fees and expenses had not been waived. For the Funds’ most recent month-end performance please call 800-789-ASIA [2742] or visit www.matthewsfunds.com.

OPERATING EXPENSES5

Net Ratio: 6 months ended 6/30/07 (annualized) 6,7 | 1.11 | % | |

Net Ratio: Fiscal Year 2006 7 | 1.16 | % | |

Gross Ratio: Fiscal Year 2006 | 1.18 | % |

PORTFOLIO TURNOVER8

6 months ended 6/30/07 (annualized) 6 | 31.42 | % | |

Fiscal Year 2006 | 18.80 | % |

1 | The MSCI All Country Far East ex-Japan Index is a free float–adjusted market capitalization–weighted index of the stock markets of China, Hong Kong, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand. The Matthews Pacific Tiger Fund invests in countries that are not included in the MSCI All Country Far East ex-Japan Index. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by PFPC Inc. |

2 | Calculated from 8/31/94. |

3 | The MSCI All Country Asia ex-Japan Index is a free float–adjusted market capitalization–weighted index of the stock of markets of China, Hong Kong, India, Indonesia, Malaysia, Pakistan, Philippines, Singapore, South Korea, Taiwan, and Thailand. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by PFPC Inc. |

4 | As of 6/30/07, the Lipper Pacific ex-Japan Funds Category Average consisted of 46 funds for the three-month period, YTD and one-year periods; 44 funds for the three-year period; 41 funds for the five-year period; 22 funds for the 10-year period; and 9 funds since 8/31/94. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains, for the stated periods. |

5 | Matthews Asian Funds do not charge 12b-1 fees. |

6 | Unaudited. |

7 | Includes management fee, administration and shareholder services fees after reimbursement, waiver or recapture of expenses by Advisor. Voluntary fee waivers by the Advisor may be discontinued at any time. |

8 | The lesser of fiscal year-to-date long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 800.789.ASIA [2742] www.matthewsfunds.com | 19 |

MATTHEWS PACIFIC TIGER FUND (CLOSED TO MOST NEW INVESTORS)

TOP TEN HOLDINGS1

COUNTRY | % OF NET ASSETS | |||

Lenovo Group, Ltd. | China/Hong Kong | 4.5% | ||

Hang Lung Group, Ltd. | China/Hong Kong | 3.4% | ||

Amorepacific Corp. | South Korea | 3.3% | ||

Advanced Info Service Public Co., Ltd. | Thailand | 3.3% | ||

Hana Financial Group, Inc. | South Korea | 2.8% | ||

NHN Corp. | South Korea | 2.6% | ||

DBS Group Holdings, Ltd. | Singapore | 2.5% | ||

Dah Sing Financial Holdings, Ltd. | China/Hong Kong | 2.5% | ||

Taiwan Semiconductor Manufacturing Co., Ltd. | Taiwan | 2.4% | ||

Swire Pacific, Ltd. | China/Hong Kong | 2.4% | ||

% OF ASSETS IN TOP 10 | 29.7% |

COUNTRY ALLOCATION

China/Hong Kong | 33.3 | % | |

South Korea | 21.3 | % | |

India 2 | 10.6 | % | |

Singapore | 10.6 | % | |

Thailand | 9.2 | % | |

Indonesia | 5.5 | % | |

Taiwan | 4.8 | % | |

Malaysia | 3.8 | % | |

Philippines | 0.5 | % | |

Cash, cash equivalents and other3 | 0.4 | % |

SECTOR ALLOCATION

Financials | 31.7 | % | |

Information Technology | 16.0 | % | |

Consumer Discretionary | 15.3 | % | |

Consumer Staples | 12.5 | % | |

Health Care | 10.0 | % | |

Industrials | 8.3 | % | |

Telecommunication Services | 5.8 | % | |

Cash, cash equivalents and other3 | 0.4 | % |

MARKET CAP EXPOSURE

Large cap (over $5 billion) | 47.4 | % | |

Mid cap ($1–$5 billion) | 43.4 | % | |

Small cap (under $1 billion) | 8.8 | % | |

Cash, cash equivalents and other3 | 0.4 | % |

NUMBER OF SECURITIES3 | NAV | FUND ASSETS | REDEMPTION FEE | 12B-1 FEES | ||||

69 | $27.47 | $3.64 billion | 2.00% within 90 calendar days | None |

1 | Holdings may combine more than one security from same issuer. |

2 | India is not included in the MSCI All Country Far East ex-Japan Index. |

3 | Includes BNY Hamilton Money Fund. |

| 20 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

PORTFOLIO MANAGER COMMENTARY continued from page 18

carrying current multiples of over 50 times earnings. Often the best performing companies of the last year have been very expensive companies that are becoming extremely expensive companies. The Fund has always been willing to own exceptional growth companies that have higher valuations, but we have to be able to rationally justify the valuations.

The Fund’s long-term avoidance of highly cyclical, commodity-oriented companies has also hurt recent performance. Throughout its history, the Fund has generally avoided energy and commodity companies where we believe forward earnings are unpredictable—essentially, a roll of the dice. For the last couple of years, those companies have often been strong performers with significant earnings growth tied to the high prices of everything from oil to ship manufacturing. We do not try to predict where commodity prices are going and prefer to make our investment decisions and take our risks around industries where we see exceptional potential to build value over time.

It must be said that in some cases we have probably held on to underperforming positions too long based on valuations that seemed very attractive versus growth potential that may have been somewhat limited. Such positions appeared very defensive and hence attractive in markets where we are concerned about risks, but the price paid in a rip-roaring bull market has been significant. We have worked hard to reassess the potential of companies that have underperformed versus the potential of newer and higher growth companies that the market seems to gravitate towards. Very few significant changes have been made and we are very pleased to see a company like Lenovo move from being a significant underperformer to the portfolio’s top contributor.

As we look forward, we continue to be enthusiastic about the strong underlying economic growth across most of the region—growth that has allowed a period of exceptionally strong corporate earnings. We do not believe that the overall valuations for the region are extreme, but significant areas of the markets are very expensive by historical standards. Anything that dents the earnings outlook could lead to a significant pullback across the markets. Such a pullback, which we have highlighted as a possibility for some time, might be quite significant given the very large inflows of investment into the markets from both international and domestic investors. The impact of an ever growing weight of passive money in the markets will be a new wrinkle for the region to handle.

For the portfolio, we continue to focus on finding individual companies where we find compelling business models, strong management teams and good corporate governance practices. Such a fundamental approach is often challenging during periods of market enthusiasm, where unknown companies are frequently given extraordinarily high valuations, but we are confident in our long term approach and the performance it has generated over time.

| 800.789.ASIA [2742] www.matthewsfunds.com | 21 |

MATTHEWS PACIFIC TIGER FUND

SCHEDULE OF INVESTMENTS (UNAUDITED)

EQUITIES: 99.6%*

| SHARES | VALUE | ||||

CHINA/HONG KONG: 33.3% | |||||

Lenovo Group, Ltd. | 277,656,000 | $ | 163,698,864 | ||

Hang Lung Group, Ltd. | 27,746,000 | 125,260,103 | |||

Dah Sing Financial Holdings, Ltd. | 10,893,600 | 91,880,617 | |||

Swire Pacific, Ltd. A Shares | 7,990,500 | 88,803,771 | |||

Agile Property Holdings, Ltd. | 63,112,000 | 82,651,279 | |||

Television Broadcasts, Ltd. | 10,362,700 | 72,890,897 | |||

Ping An Insurance (Group) Co. of China, Ltd. H Shares | 10,077,500 | 71,207,013 | |||

NWS Holdings, Ltd. | 24,775,636 | 61,786,999 | |||

Shangri-La Asia, Ltd. | 22,824,000 | 55,168,508 | |||

Dairy Farm International Holdings, Ltd. | 11,984,900 | 54,171,748 | |||

NetEase.com, Inc. ADR** | 2,581,300 | 43,933,726 | |||

Integrated Distribution Services Group, Ltd. | 11,833,000 | 37,379,156 | |||

Tencent Holdings, Ltd. | 9,211,000 | 37,106,929 | |||

China Mobile, Ltd. ADR | 668,250 | 36,018,675 | |||

Travelsky Technology, Ltd. H Shares † | 40,812,000 | 34,918,186 | |||

China Merchants Bank Co., Ltd. H Shares | 11,316,500 | 34,445,045 | |||

Dickson Concepts International, Ltd. † | 28,334,900 | 32,976,211 | |||

Dynasty Fine Wines Group, Ltd. † | 77,862,000 | 31,765,370 | |||

China Vanke Co., Ltd. B Shares | 13,792,093 | 28,557,140 | |||

Glorious Sun Enterprises, Ltd. | 35,727,000 | 17,271,340 | |||

SCMP Group, Ltd. | 32,396,000 | 13,216,600 | |||

Belle International Holdings, Ltd.** | 383,000 | 422,715 | |||

China High Speed Transmission Equipment Group Co., Ltd.**,***,**** | 168,000 | 194,982 | |||

Total China/Hong Kong | 1,215,725,874 | ||||

SOUTH KOREA: 21.3% | |||||

Amorepacific Corp. | 152,635 | 120,938,275 | |||

Hana Financial Group, Inc. | 2,119,653 | 103,361,333 | |||

NHN Corp.** | 521,132 | 95,048,701 | |||

Samsung Securities Co., Ltd. | 817,796 | 65,770,680 | |||

Hanmi Pharmaceutical Co., Ltd.† | 422,133 | 64,883,786 | |||

S1 Corp. | 973,120 | 52,508,559 | |||

Nong Shim Co., Ltd. | 161,478 | 45,969,274 | |||

Yuhan Corp. | 212,450 | 39,783,354 | |||

ON*Media Corp.** | 4,276,360 | 39,622,928 | |||

Hyundai Development Co. | 532,704 | 37,941,141 | |||

MegaStudy Co., Ltd. | 188,305 | 36,688,748 | |||

Hite Brewery Co., Ltd. | 271,488 | 35,263,906 | |||

GS Home Shopping, Inc. | 234,698 | 21,720,711 | |||

SK Telecom Co., Ltd. ADR | 680,300 | 18,606,205 | |||

Total South Korea | 778,107,601 | ||||

INDIA: 10.6% | |||||

Cipla, Ltd. | 12,782,652 | 65,365,656 | |||

Titan Industries, Ltd. | 1,859,344 | 61,282,297 | |||

Infosys Technologies, Ltd. | 1,246,624 | 59,078,738 | |||

Sun Pharmaceutical Industries, Ltd. | 2,296,352 | 57,853,064 | |||

HDFC Bank, Ltd. | 1,952,568 | 55,008,165 | |||

Dabur India, Ltd. | 19,600,098 | 49,523,893 | |||

Bank of Baroda | 4,547,022 | 30,188,741 | |||

Sun Pharma Advanced Research Co., Ltd.**,***,**** | 2,296,352 | 7,577,595 | |||

Total India | 385,878,149 | ||||

SINGAPORE: 10.6% | |||||

DBS Group Holdings, Ltd. | 6,168,750 | 91,881,431 | |||

Fraser and Neave, Ltd. | 23,422,750 | 83,393,100 | |||

Hyflux, Ltd. † | 34,829,187 | 66,666,352 | |||

Venture Corp., Ltd. | 5,732,800 | 58,797,949 | |||

Parkway Holdings, Ltd. | 19,226,050 | 50,239,556 | |||

Keppel Land, Ltd. | 5,964,000 | 34,091,132 | |||

Total Singapore | 385,069,520 | ||||

| 22 | MATTHEWS ASIAN FUNDS |

JUNE 30, 2007

| SHARES | VALUE | ||||

THAILAND: 9.2% | |||||

Advanced Info Service Public Co., Ltd. | 47,888,300 | $ | 119,980,824 | ||

Bangkok Bank Public Co., Ltd. | 21,025,400 | 74,296,852 | |||

Bank of Ayudhya Public Co., Ltd. NVDR | 61,539,600 | 43,848,636 | |||

Land & Houses Public Co., Ltd. | 173,222,300 | 37,629,754 | |||

Thai Beverage Public Co., Ltd. | 189,105,000 | 32,119,745 | |||

Amata Corp. Public Co., Ltd. † | 59,894,900 | 29,318,575 | |||

Total Thailand | 337,194,386 | ||||

INDONESIA: 5.5% | |||||

PT Kalbe Farma | 322,238,500 | 49,575,154 | |||

PT Bank Central Asia | 69,945,500 | 42,191,807 | |||

PT Astra International | 21,155,730 | 39,571,869 | |||

PT Telekomunikasi Indonesia | 33,473,500 | 36,492,969 | |||

PT Ramayana Lestari Sentosa | 277,326,000 | 31,001,578 | |||

Total Indonesia | 198,833,377 | ||||

TAIWAN: 4.8% | |||||

Taiwan Semiconductor Manufacturing Co., Ltd. | 41,390,673 | 89,289,804 | |||

President Chain Store Corp. | 29,591,000 | 84,273,036 | |||

Total Taiwan | 173,562,840 | ||||

MALAYSIA: 3.8% | |||||

Resorts World BHD | 60,482,500 | 60,613,888 | |||

Public Bank BHD | 16,107,900 | 45,722,642 | |||

Top Glove Corp. BHD | 13,027,480 | 30,941,444 | |||

Total Malaysia | 137,277,974 | ||||

PHILIPPINES: 0.5% | |||||

SM Prime Holdings, Inc. | 70,090,000 | 17,806,649 | |||

Total Philippines | 17,806,649 | ||||

TOTAL EQUITIES (Cost $2,414,902,994) | 3,629,456,370 | ||||

MONEY MARKET MUTUAL FUND: 0.3%* | |||||

BNY Hamilton Money Fund (Cost $13,670,310) | 13,670,310 | 13,670,310 | |||

TOTAL INVESTMENTS: 99.9% (Cost $2,428,573,304*****) | 3,643,126,680 | ||||

CASH AND OTHER ASSETS, LESS LIABILITIES: 0.1% | 1,810,433 | ||||

NET ASSETS: 100.0% | $ | 3,644,937,113 | |||

| * | As a percentage of net assets as of June 30, 2007 |

| ** | Non–income producing security |

| *** | Fair valued under direction of the Board of Trustees |

| **** | Illiquid security |

| ***** | Cost of investments is $2,428,573,304 and net unrealized appreciation consists of: |

Gross unrealized appreciation | $ | 1,228,933,539 | ||

Gross unrealized depreciation | (14,380,163 | ) | ||

Net unrealized appreciation | $ | 1,214,553,376 | ||

| † | Affiliated Issuer, as defined under the Investment Company Act of 1940 (ownership of 5% or more of the outstanding voting securities of this issuer) |

| ADR | American Depositary Receipt |

| NVDR | Non-voting Depositary Receipt |

See accompanying notes to financial statements.

| 800.789.ASIA [2742] www.matthewsfunds.com | 23 |

MATTHEWS ASIAN GROWTH AND INCOME FUND

(CLOSED TO MOST NEW INVESTORS)

FUND DESCRIPTION | SYMBOL: MACSX | |

| Under normal market conditions, the Matthews Asian Growth and Income Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in dividend-paying equity securities and the convertible securities, of any duration or quality, of companies located in Asia. Asia includes China, Hong Kong, India, Indonesia, Japan, Malaysia, Pakistan, Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam. | ||

| PORTFOLIO MANAGERS | ||

| Lead Manager: G. Paul Matthews | Co-Manager: Andrew T. Foster | |

PORTFOLIO MANAGER COMMENTARY

During the first half of 2007, the Matthews Asian Growth and Income Fund gained 11.57%, while the benchmark MSCI All Country Far East ex-Japan Index rose 17.27% and the Lipper Pacific ex-Japan Funds Category Average advanced 20.39%. Amid the volatility of the first quarter, the Fund managed to outpace its benchmark. However, as markets rallied sharply and consistently during the second quarter, the Fund’s defensive orientation constrained its ability to keep pace. The Fund returned 8.89% during the second quarter, while the index gained 15.58%.

Several factors contributed to the Fund’s absolute gains during the period; chief among them was China. China-related stocks have undergone a marked appreciation during the past 18 months, and this surge in valuations has lifted not only the Fund’s returns, but also Asia Pacific markets more broadly. The top three performing positions within the Fund hail from disparate sectors (real estate, travel and heavy industry), yet they were united by their underlying exposure to the Chinese economy.

The recent and dramatic appreciation of China-related stocks has led some observers to suggest that the Chinese market is susceptible to a correction. This view is not without merit: Chinese shares are priced at lofty valuations and are trading at record highs. Furthermore,

24 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED

such stocks have become volatile in recent months, as was evident in late February, when China’s “A share” markets fell 9% in a single day (note: the Fund has no positions in Chinese “A shares”). The Fund has been cautious in its exposure to Chinese stocks, trimming positions that have experienced outsized gains.

These concerns notwithstanding, we would note that the underlying pace of market reform within China remains formidable–and thus recent gains in Chinese shares are not without basis, either. The country has managed an impressive feat by privatizing and re-capitalizing the bulk of its hobbled banking sector; it has

continued on page 26

PERFORMANCE AS OF JUNE 30, 2007

| Average Annual Total Returns | |||||||||||||||||||||

Fund Inception: 9/12/94 | 3 MO | YTD | 1 YR | 3 YRS | 5 YRS | 10 YRS | SINCE INCEPTION | ||||||||||||||

Matthews Asian Growth and Income Fund | 8.89 | % | 11.57 | % | 28.54 | % | 23.05 | % | 21.25 | % | 14.33 | % | 13.10 | % | |||||||

MSCI All Country Far East ex-Japan Index 1 | 15.58 | % | 17.27 | % | 44.21 | % | 30.94 | % | 22.61 | % | 4.38 | % | 4.05 | %3 | |||||||

Lipper Pacific ex-Japan Funds Category Average 3 | 16.09 | % | 20.39 | % | 46.62 | % | 33.48 | % | 23.25 | % | 7.69 | % | 6.89 | %3 | |||||||

All performance quoted is past performance and is no guarantee of future results. Assumes reinvestment of all dividends and/or distributions. Unusually high returns may not be sustainable. Investment return and principal value will fluctuate with changing market conditions so that shares, when redeemed, may be worth more or less than their original cost. The performance of foreign indices may be based on different exchange rates than those used by the Fund and, unlike the Fund’s NAV, is not adjusted to reflect fair value at the close of the NYSE. Current performance may be lower or higher than the return figures quoted. Returns are net of the Funds’ management fee and other operating expenses. Returns would have been lower if certain of the Funds’ fees and expenses had not been waived. For the Funds’ most recent month-end performance please call 800-789-ASIA [2742] or visit www.matthewsfunds.com.

30-DAY SEC YIELD4

1.12% |

INCOME DISTRIBUTION YIELD5

3.05% |

OPERATING EXPENSES6

Net Ratio: 6 months ended 6/30/07 (annualized) 7,8 | 1.15 | % | |

Net Ratio: Fiscal Year 2006 8 | 1.19 | % | |

Gross Ratio: Fiscal Year 2006 | 1.20 | % |

PORTFOLIO TURNOVER9

6 months ended 6/30/07 (annualized) 6,7 | 24.92 | % | |

Fiscal Year 2006 | 28.37 | % |

1 | The MSCI All Country Far East ex-Japan Index is a free float–adjusted market capitalization–weighted index of the stock markets of China, Hong Kong, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand. The Matthews Asian Growth and Income Fund invests in countries that are not included in the MSCI All Country Far East ex-Japan Index. It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International; total return calculations performed by PFPC Inc. |

2 | As of 6/30/07, the Lipper Pacific ex-Japan Funds Category Average consisted of 46 funds for the three-month,YTD and one-year periods; 44 funds for the three-year period; 41 funds for the five-year period; 22 funds for the 10-year period; and 9 funds since 8/31/94. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains, for the stated periods. |

3 | Calculated from 8/31/94. |

4 | The 30-day SEC Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/07, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-day period. The SEC Yield should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate, the income paid to a shareholder’s account, or the income reported in the Fund’s financial statements. Past yields are no guarantee of future yields. |

5 | The Income Distribution Yield represents the past two dividends (does not include capital gains) paid by the Fund for the period ended 6/30/07, expressed as an annual percentage rate based on the Fund’s share price on 6/30/07. Generally, the Fund has made distributions of net investment income twice each year and of capital gains, if any, annually. Past Income Distribution Yields are no guarantee of future yields or that any distributions will continue to be paid twice each year. |

6 | Matthews Asian Funds do not charge 12b-1 fees. |

7 | Unaudited. |

8 | Includes management fee, administration and shareholder services fees after reimbursement, waiver or recapture of expenses by Advisor. Voluntary fee waivers by the Advisor may be discontinued at any time. |

9 | The lesser of fiscal year-to-date long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 800.789.ASIA [2742] www.matthewsfunds.com | 25 |

MATTHEWS ASIAN GROWTH AND INCOME FUND

(CLOSED TO MOST NEW INVESTORS)

TOP TEN HOLDINGS1

HOLDING | COUNTRY | SECURITY TYPE | % OF NET ASSETS | |||

HSBC Holdings PLC | United Kingdom | Equity | 2.8% | |||

Hongkong Land Ltd., Cnv. | China/Hong Kong | Convertible Bond | 2.7% | |||

Hang Lung Group, Ltd. | China/Hong Kong | Equity | 2.7% | |||

SK Telecom Co., Ltd. | South Korea | Equity | 2.7% | |||

Singapore Press Holdings, Ltd. | Singapore | Equity | 2.4% | |||

Fraser and Neave, Ltd. | Singapore | Equity | 2.4% | |||

Housing Development Finance Corp., Cnv. | India | Convertible Bond | 2.2% | |||

Far EasTone Telecommunications Co., Ltd. | Taiwan | Equity | 2.2% | |||

Rafflesia Capital, Ltd., Cnv. | Malaysia | Convertible Bond | 2.2% | |||

CNOOC Finance, Ltd., Cnv. | China/Hong Kong | Convertible Bond | 2.2% | |||

% OF ASSETS IN TOP 10 | 24.5% |

COUNTRY ALLOCATION

China/Hong Kong | 30.5 | % | |

South Korea | 14.8 | % | |

Singapore | 12.9 | % | |

Taiwan | 11.1 | % | |

India 2 | 8.7 | % | |

Thailand | 4.4 | % | |

Australia 2 | 3.6 | % | |

Malaysia | 3.6 | % | |

Japan 2 | 3.4 | % | |

United Kingdom 2 | 2.8 | % | |

Indonesia | 2.1 | % | |

Philippines | 1.0 | % | |

Cash, cash equivalents and other 3 | 1.1 | % |

SECTOR ALLOCATION

Financials | 28.2 | % | |

Telecommunication Services | 21.0 | % | |

Consumer Discretionary | 16.2 | % | |

Utilities | 9.2 | % | |

Industrials | 7.9 | % | |

Information Technology | 4.4 | % | |

Health Care | 4.3 | % | |

Consumer Staples | 4.1 | % | |

Energy | 3.1 | % | |

Materials | 0.5 | % | |

Cash, cash equivalents and other 3 | 1.1 | % |

MARKET CAP EXPOSURE

Large cap (over $5 billion) | 60.6 | % | |

Mid cap ($1–$5 billion) | 30.7 | % | |

Small cap (under $1 billion) | 7.6 | % | |

Cash, cash equivalents and other 3 | 1.1 | % |

BREAKDOWN BY SECURITY4

Common Equities | 75.2 | % | |

Convertible Bonds | 20.3 | % | |

Preferred Equities | 3.4 | % | |

Cash, cash equivalents and other3 | 1.1 | % |

NUMBER OF SECURITIES3 | NAV | FUND ASSETS | REDEMPTION FEE | 12B-1 FEES | ||||

84 | $20.12 | $2.23 billion | 2.00% within 90 calendar days | None |

1 | Holdings may combine more than one security from same issuer. |

2 | India, Australia, Japan and the United Kingdom are not included in the MSCI All Country Far East ex-Japan Index. |

3 | Includes BNY Hamilton Money Fund. |

4 | As of 6/30/07, convertible bonds, which are not reflected in the Fund’s benchmark, the MSCI All Country Far East ex-Japan Index, accounted for 20.3% of the Matthews Asian Growth and Income Fund. |

PORTFOLIO MANAGER COMMENTARY continued from page 25

revitalized its onshore financial markets via necessary regulatory reforms; lastly—and most importantly—it has demonstrated a gradual but consistent resolve to dismantle the capital controls that have underpinned its currency policy for well over a decade. The cumulative impact of these reforms is substantial, and underscores the Chinese authorities’ intent to modernize the country’s economy and financial system. Thus, even as China’s markets touch precipitous new highs, they have been catalyzed by a series of positive and material fundamental events.

| 26 | MATTHEWS ASIAN FUNDS |

ALL DATA IS AS OF JUNE 30, 2007, UNLESS OTHERWISE NOTED