QuickLinks -- Click here to rapidly navigate through this document

Filed by REMEC, Inc.

pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Spectrian Corporation

Commission File No.: 000-24360

This filing relates to a planned merger between REMEC, Inc. ("REMEC") and Spectrian Corporation ("Spectrian") pursuant to the terms of an Amended and Restated Agreement and Plan of Merger and Reorganization, dated as of October 29, 2002, by and among REMEC, Reef Acquisition Corp. and Spectrian (the "Merger Agreement"). The Merger Agreement is on file with the Securities and Exchange Commission as an exhibit to the Current Report on Form 8-K filed by Spectrian on October 31, 2002, and is incorporated by reference into this filing.

The following is a series of slides used in connection with presentations by Ronald Ragland, REMEC's Chairman and Chief Executive Officer, David Morash, REMEC's Executive Vice President and Chief Financial Officer, and Thomas Waechter, Spectrian's President and Chief Executive Officer, at an AeA Conference held on November 4-5, 2002, relating to the proposed acquisition of Spectrian by REMEC. The slides are also posted on REMEC's internal web site.

Safe Harbor

Forward-looking Statements

Certain statements in this presentation, including statements regarding anticipated cost savings and synergies of the proposed acquisition of Spectrian by REMEC and the opportunities that it will bring the combined company, are forward-looking statements that are subject to risks and uncertainties. Results could differ materially based on various factors including, and without limitation: the parties' ability to achieve the anticipated cost savings; the parties' ability to achieve the expected synergies, customer uncertainties related to the proposed acquisition or the economy in general, economic conditions and the related impact on wireless communication infrastructure spending; demand for REMEC's and Spectrian's products; rapid technological change and evolving industry standards and adverse changes in market conditions in both the United States and internationally. Further information on factors that could affect REMEC's results are included in REMEC's Annual Report on Form 10-K for the year ended January 31, 2002 on file with the Securities and Exchange Commission. Further information on factors that could affect Spectrian's results are included in Spectrian's Annual Report on Form 10-K for the year ended March 31, 2001 and Forms 10-Q for the interim quarters.

Overview

- •

- Record Performance Defense Business

- •

- Solid Pole Position for Telecom Recovery

- •

- Downturn has Enabled Competition Leap

- •

- Broad Technology & Integration Leadership

- •

- Manufacturing Transition Offshore going well

- •

- Global Capability & Capacity Solidified

- •

- Major Strides With Top Telecom Customers

- •

- Downturn at REMEC appears Bottomed

- •

- Retain very Competitive Balance Sheet

- •

- Spectrian Merger Agreement Amended

REMEC Focus

| Defense and Space | |

| Mobile Wireless Infrastructure | |

| Broadband Wireless | |

| Global Manufacturing | |

| Advanced Technologies |

REMEC Locations

Market Assessment

- •

- Bubble Funded Non-viable Competitors & Customers—Excessive Government License Fees—Funded us too!

- •

- Customers Stopped Buying—REMEC without Fundamental Execution Issues

- •

- Extremely Painful Process—Major RIF &Restructure

- •

- Competitors Gone or Weakened

- •

- Customer Forced to Assess Supplier Big Picture

- •

- Strong Customers are Solidifying—Next-Gen Procurement Beginning—Ready to Partner

- •

- CHINA is a Huge Factor—Sales and Leverage

- •

- Spectrian Merger Strengthens REMEC Position

- •

- 1st & 2nd Level Consolidation Inevitable

RF and microwave products

for space, electronic warfare,

missile and communications/

navigation systems.

Design, development and production

of subsystems, integrated assemblies

and components for lower cost and

improved performance.

F-22 Stealth Fighter

| CNI TRW EW LOCKHEED MARTIN RADAR NORTHROP GRUMMAN |  | |

| EXPECT TO SUPPLY COMPARABLE PRODUCT TO JSF |

A range of products

in demand for wireless

communications systems including

cellular, GSM, PCS / PCN and UMTS.

Complete systems, integrated modules

and components for signal conditioning,

transport and distribution to improve

performance and decrease rollout cost.

Mobile Wireless

| Coverage enhancement |  |

| Cellular / PCS basestations |

| In-building solutions |  |

Delivers a broad spectrum

of microwave products for

fixed wireless access systems.

Subsystems, modules and components

to collect, transport, condition,

and distribute radio signals for

a variety of radio-based technologies.

Broadband Wireless

| TRANSCEIVERS and MODULES |

| FIXED WIRELESS ACCESS |  |

| MODULAR POINT-to-POINT RADIO |

Manufacture and testing of

equipment for a range of

applications and technologies both

for internal design/development divisions

and for external customers.

Offshore facilities enable significant cost

reduction with quick development and

turnaround capabilities.

Global Manufacturing

| Philippines | ||

| High volume commercial manufacturing Extensive manufacturing and test capability Very attractive economics and tax Low cost skilled labor pool ISO 9002 certified | |

Costa Rica | ||

| High volume commercial manufacturing Very attractive economics Available educated technical labor pool High growth rate/3x expansion ISO 9002 certified | |

Veritek | ||

| Automated high speed surface mount assembly Unique microwave assembly processes Sophisticated supply chain management/product test High growth rate/3x expansion ISO 9002 certified |

Advanced devices and subsystems

including microwave MMICs and highly

integrated assemblies for broadband

wireless and fiber optic applications

STRATEGY

- •

- Focus on Return to Positive Financial Performance—Retain Strong Balance Sheet

- •

- Continued Investment—Defense Technology & Growth

- •

- Complete Manufacturing Transition Offshore

- •

- Broad Technology and Defense Integration Heritage provides most likely Integrated Base Station Solution

- •

- Retain Affordable Advanced MMIC & AI Technology

- •

- Partner Focus on Customers with Industry Leadership

- •

- High Priority on Indigenous CHINA Design, Develop and Manufacturing Capability

- •

- Gain Traction in Fixed Wireless Access and MRI Radio

- •

- Constructive Non-cash Consolidation Opportunities

Spectrian Transaction

- •

- Strategy Remains Intact

- •

- Power Amp Legacy and Critical Mass

- •

- Manufacturing Overhead Absorption

- •

- Balance Sheet Enhancement

- •

- Complimentary Markets & Customers

- •

- Waechter Becomes COO

- •

- Spectrian Performance Nosedive

- •

- Relative Valuations Problematic

- •

- SEC Review of Issues Created Delay

- •

- Expect Clarity Near-Term

REMEC / Spectrian

- •

- A Strong Strategic Combination

- •

- Complementary global customers

- •

- Complete combined RF and microwave product line

- •

- New fully-integrated product offering

- •

- North American, European and Asian engineering centers

- •

- Strong balance sheet and no debt

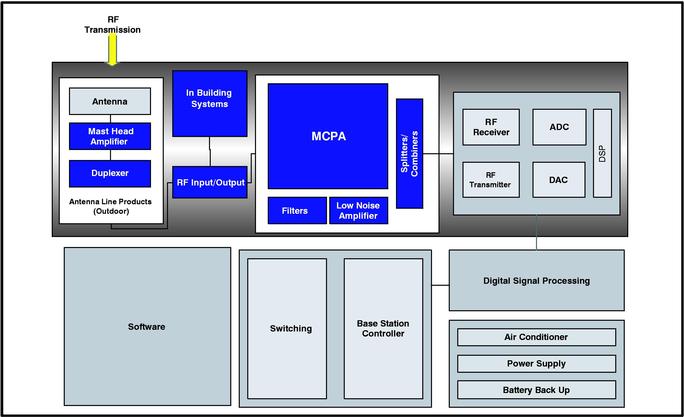

Combined Product Offering

Strategic Synergies

- •

- Operating synergies:

- •

- Revenue growth synergies

- •

- Manufacturing cost reductions

- •

- Operating expense reductions

- •

- Purchasing leverage

- •

- Transition team in place to achieve synergies

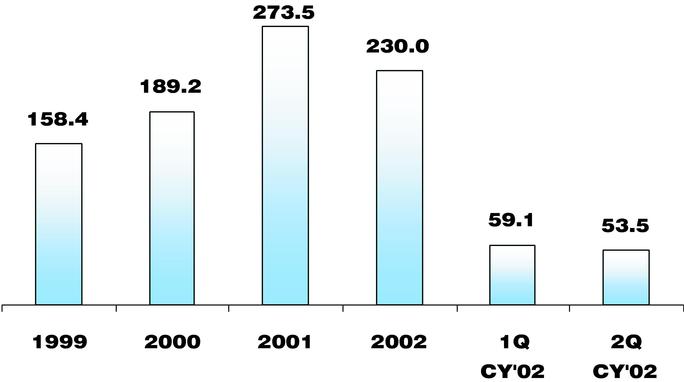

Revenue (Prior to Pooling)

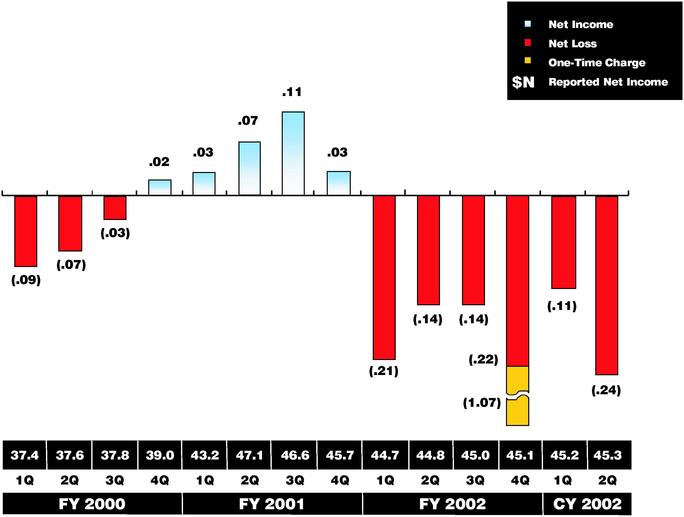

Net Income (Prior to Pooling)

Balance Sheet Highlights ($ Millions)

| | 8/3/02 | ||

|---|---|---|---|

Cash | $ | 51.6 | |

Working Capital | 116.0 | ||

Total Assets | 306.4 | ||

Long Term Debt | — | ||

Equity | 264.5 | ||

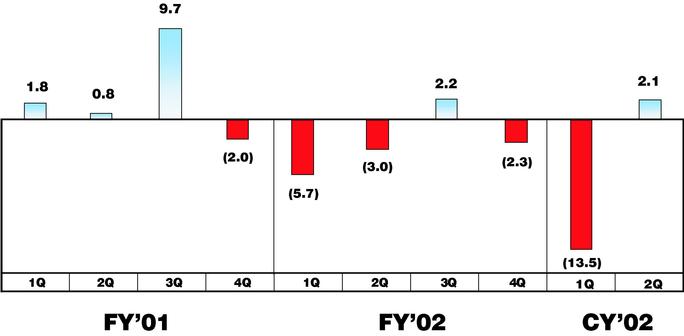

Quarterly Operating Cash Flow

$ in millions

Focus on Shareholder Value

- •

- Restructure business to focus on product lines

- •

- Reorganization to eliminate redundant operations

- •

- Close or consolidate certain facilities

- •

- Potential charge related to reorganization

- •

- Annual cost reductions of ~$15 M by Q4 of CY 2002

- •

- Offshore manufacturing completed by end of Q2 CY 2003

- •

- Maximize efficiency from capital spending

- •

- Centralize cash to use assets more efficiently

Focus on Shareholder Value (cont'd)

- •

- Acquire Spectrian for stock

- •

- Sell buildings to raise approximately $10 M

- •

- Expanded accounting and reporting systems

- •

- Centralize supply chain management to reduce costs

- •

- Worldwide tax planning

- •

- Increased R & D spending

- •

- Bonuses tied to business performance

- •

- Improve cash flow

- •

- Focus on cash ROI

Financial Targets

- •

- Sales of $300 M in CY2003, without Spectrian

- •

- Resume growth, target of

- •

- 30% commercial

- •

- 15% defense

- •

- Profitability during first half of CY 2003

- •

- Gross margin of 26% by Q4 of CY 2003

- •

- Net income of 5% by Q4 of CY 2003

- •

- Operating cash flow of $1 million/month by Q1 CY 2003

Financial Targets (cont'd)

- •

- $25M, two-year bank commitment

- •

- Continuing significant R&D investment in MCPA's/MRI/MMIC's

- •

- Taxes

- •

- Foreign IP shift

- •

- Domestic and foreign net operating loss carry forwards

- •

- Driving to an effective tax rate of 25%

- •

- Acquisitions accretive/synergistic/technology fill

Financial Issues for Spectrian

- •

- Market outlook

- •

- Spending squeeze expected to continue for 6-12 months

- •

- China 3G services postponed into 2H03

- •

- European 3G services postponed into 2004 timeframe

- •

- Spectrian sales outlook

- •

- Relative strength in Asia and US operators

- •

- Good GSM position

- •

- Stand-alone viability of the Spectrian business

- •

- Strong balance sheet vs. significant cash burn rate

- •

- Expected levels of cost savings/joint synergies

- •

- Success depends on aggressive rationalization

Summary

- •

- Break even by Q2 CY'03

- •

- Strong balance sheet

- •

- Spectrian strengthens balance sheet

- •

- Restructured for substantial growth

- •

- Significant market opportunities

- •

- Confident game plan

Defense and Space

Mobile Wireless

Broadband Wireless

Manufacturing

Advanced Technologies

Financials