Exhibit 99.6

![]()

575 Lexington Avenue, New York, New York 10022

Tel: 212.906.9400 Fax: 212.935.5935

Appraisal of

Peak at Vinings

100 Woodbridge Drive

Atlanta, Georgia 30339

![]()

January 28, 2013

Ms. Lisa Cohn

Executive Vice President

Fox Partners II

c/o AIMCO

4582 South Ulster Street, Suite 1100

Denver, CO 80237

| Re: | Appraisal of Peak at Vinings |

100 Woodbridge Drive

Atlanta, Georgia 30339

KTR No. 12-1-00362 (A)

Dear Ms. Cohn:

In accordance with our agreement dated December 20, 2012, KTR Real Estate Advisors LLC (“KTR”) has performed an Appraisal of the above-referenced property and has communicated the results in the attached Self-contained Appraisal Report. The purpose of this appraisal is to determine the Market Value of the Leased Fee Interest in the subject property as of January 18, 2013, the date of inspection.

Situated as noted, the subject property consists of a 22.00-acre site improved with a 280-unit gated garden-style apartment complex. The subject was developed in 1981 and underwent a major renovation between 2008 and 2009. It contains 272,390 square feet of rentable area. Additional site improvements include a clubhouse with business center, meeting room, kitchen/gaming area, fitness center, swimming pool and mature landscaping. The property is operating at stabilized occupancy and is in good physical condition. The subject property is more fully described, legally and physically, within the attached report.

Based on the analysis contained in the attached report, the Market Value of the Leased Fee Interest in the subject property free and clear of financing, as of January 18, 2013 is:

THIRTY FOUR MILLION SIX HUNDRED THOUSAND DOLLARS

($34,600,000)

The attached report, in its entirety, including all assumptions and limiting conditions, which is an integral part of, and inseparable from, this transmittal letter, contains the data, information, analyses and calculations upon which the value conclusion indicated herein are based. The report was prepared in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP) as set forth by the Appraisal Foundation and in accordance with the Code of Professional Ethics and Standards of Professional Practice of the Appraisal Institute.

575 Lexington Avenue, New York, NY 10022

TEL 212.906.9400 •FAX 212.935.5935

Fox Partners II Peak at Vinings January 28, 2013 Page 2 |

It has been a pleasure to be of service to you. Please do not hesitate to call either Terence Tener at (212) 906-9403 or Thomas Tener at (212) 906-9499 with any questions you may have regarding our assumptions, observations or conclusions.

Respectfully submitted,

KTR REAL ESTATE ADVISORS LLC | ||||||||

|  | |||||||

| By: | Terence Tener, MAI, ASA Managing Partner | By: | Thomas J. Tener Managing Partner | |||||

| ||||||||

| By: | Shaun Kest Appraiser | |||||||

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page i |

| INTRODUCTION | ||||

Title Page | ||||

Letter of Transmittal | ||||

Table of Contents | i | |||

Certificate of Appraisal | ii | |||

Basic Assumptions and Limiting Conditions | iii | |||

Subject Property Photographs | v | |||

Location Map | vi | |||

| PREMISES OF THE APPRAISAL | ||||

Summary of Salient Facts and Conclusions | 1 | |||

Property Identification | 2 | |||

Sales History | 2 | |||

Purpose and Scope of the Appraisal | 2 | |||

Definition of Market Value | 3 | |||

Property Rights Appraised | 3 | |||

Intended Use and User | 3 | |||

Exposure Time | 4 | |||

| PRESENTATION OF DATA | ||||

Regional and Area Analysis | 5 | |||

Neighborhood Analysis | 9 | |||

Site Analysis | 11 | |||

Improvement Analysis | 14 | |||

Zoning Analysis | 17 | |||

Real Estate Assessments and Taxes | 19 | |||

Apartment Market Analysis | 20 | |||

| ANALYSIS OF DATA AND CONCLUSIONS | ||||

Highest and Best Use | 31 | |||

Valuation Process | 32 | |||

Income Capitalization Approach | 34 | |||

Sales Comparison Approach | 43 | |||

Reconciliation and Final Value Conclusion | 52 | |||

| ADDENDA | ||||

Additional Subject Property Photographs | ||||

Submitted Information | ||||

Qualifications of the Appraiser | ||||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page ii |

CERTIFICATE OF APPRAISAL

We, Terence Tener, MAI, ASA, Thomas J. Tener and Shaun Kest certify that to the best of our knowledge and belief:

The statements of fact contained in this report are true and correct.

The reported analyses, opinions, and conclusions are limited only by the reported assumptions and limiting conditions, and are our personal, unbiased professional analyses, opinions, and conclusions.

We have no present or prospective interest in the property that is the subject of this report, and we have no personal interest or bias with respect to the parties involved.

Our compensation is not contingent upon the reporting of a predetermined value or direction in value that favors the cause of the client, the value estimate, the attainment of a stipulated result, or the occurrence of a subsequent event.

Our analyses, opinions, and conclusions were developed, and this report has been prepared, in conformity with theUniform Standards of Professional Appraisal Practice.

Shaun Kest has made a personal inspection of the property that is the subject of this report.

Terence Tener, MAI, ASA and Thomas J. Tener have not made a personal inspection of the property that is the subject of this report.

This appraisal was not prepared in conjunction with a request for a specific value or a value within a given range or predicated upon loan approval.

The reported analyses, opinions and conclusions were developed, and this report has been prepared, in conformity with the requirements of the Code of Professional Ethics and the Standards of Professional Appraisal Practice of the Appraisal Institute.

The use of this report is subject to the requirements of the Appraisal Institute relating to review by its duly authorized representatives.

As of the date of this report, Terence Tener, MAI, ASA has completed the continuing education program of the Appraisal Institute.

Thomas J. Tener has been certified to transact business in Georgia as a Real Estate General Appraiser (License No. 343948).

Terence Tener, MAI, ASA, Thomas J. Tener and Shaun Kest have extensive experience in the appraisal of similar properties.

We have not performed an appraisal and appraisal consulting services regarding the subject property within the three-year period immediately preceding this assignment.

KTR REAL ESTATE ADVISORS LLC

|  |  | ||||||||

| By: | Terence Tener, MAI, ASA | By: | Thomas J. Tener | By: | Shaun Kest | |||||

| Managing Partner | Managing Partner | Appraiser | ||||||||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page iii |

BASIC ASSUMPTIONS AND LIMITING CONDITIONS

This appraisal report is subject to the following assumptions and limiting conditions:

| 1. | No responsibility is assumed for the legal description or for matters including legal or title considerations. Title to the property is assumed to be good and marketable unless otherwise stated. |

| 2. | The property is appraised free and clear of any or all liens or encumbrances unless otherwise stated. |

| 3. | Responsible ownership and competent property management are assumed. |

| 4. | The information furnished by others is believed to be reliable. However, no warranty is given for its accuracy. |

| 5. | All engineering is assumed to be correct. The plot plans and illustrative material in this report are included only to assist the reader in visualizing the property. |

| 6. | It is assumed that there are no hidden or unapparent conditions of the property, subsoil, or structures that render it more or less valuable. No responsibility is assumed for such conditions or for arranging for engineering studies that may be required to discover them. |

| 7. | It is assumed that there is full compliance with all applicable federal, state, and local environmental regulations and laws unless noncompliance is stated, defined, and considered in the appraisal report. |

| 8. | It is assumed that all applicable zoning and use regulations and restrictions have been complied with, unless nonconformity has been stated, defined, and considered in the appraisal report. |

| 9. | It is assumed that all required licenses, certificates of occupancy, consents, or other legislative or administrative authority from any local, state, or national government or private entity or organization have been or can be obtained or renewed for any use on which the value estimate contained in this report is based. |

| 10. | It is assumed that the utilization of the land and improvements is within the boundaries or property lines of the property described and that there is no encroachment or trespass unless noted in the report. |

| 11. | The distribution, if any, of the total valuation in this report between land and improvements applies only under the stated program of utilization. The separate allocations for land and buildings must not be used in conjunction with any other appraisal and are invalid if so used. |

| 12. | Unless otherwise stated, possession of this report, or a copy thereof, does not carry with it the right of publication. |

| 13. | The appraiser, by reason of this appraisal, is not required to give further consultation, testimony, or be in attendance in court with reference to the property in question unless arrangements have been previously made. |

| 14. | Unless otherwise stated, neither all nor any part of the contents of this report (especially any conclusions as to value, the identity of the appraiser, or the firm with which the appraiser is connected) shall be disseminated to the public through advertising, public relations, news, sales, or other media without prior written consent and approval of the appraisers. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page iv |

| 15. | Unless otherwise stated in this report, the existence of hazardous substances, including without limitation asbestos, polychlorinated biphenyls, petroleum leakage, or agricultural chemicals, which may or may not be present on the property, or other environmental conditions, were not called to the attention of nor did the appraiser become aware of such during the appraiser’s inspection. The appraiser has no knowledge of the existence of such materials on or in the property unless otherwise stated. The appraiser, however, is not qualified to test such substances or conditions. If the presence of such substances, such as asbestos, urea formaldehyde foam insulation, or other hazardous substances or environmental conditions, may affect the value of the property, the value is predicated on the assumption that there is no such condition on or in the property or in such proximity thereto that it would cause a loss in value. No responsibility is assumed for any such conditions, or for any expertise or engineering knowledge required to discover them. The client is urged to retain an expert in this field, if desired. |

| 16. | The Americans with Disabilities Act (“ADA”) became effective January 26, 1992. The appraiser has not made a specific compliance survey and analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the ADA. It is possible that a compliance survey of the property, together with a detailed analysis of the requirements of the ADA, could reveal that the property is not in compliance with one or more of the requirements of the Act. If so, this fact could have a negative effect upon the value of the property. Since the appraiser has no direct evidence relating to this issue, he did not consider possible non-compliance with the requirements of the ADA in estimating the value of the property. |

| 17. | Former personal property items such as kitchen and bathroom appliances are now either permanently affixed to the real estate or are implicitly part of the real estate in that tenants expect the use of such items in exchange for rent and never gain any of the rights of ownership. Furthermore, the intention of the owners is not to remove the articles which are required under the implied or express Warranty of Habitability. The accounting for the short-lived nature of such items is reflected in a reserves for replacement expense category. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page v |

SUBJECT PROPERTY PHOTOGRAPHS

View of typical building

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page vi |

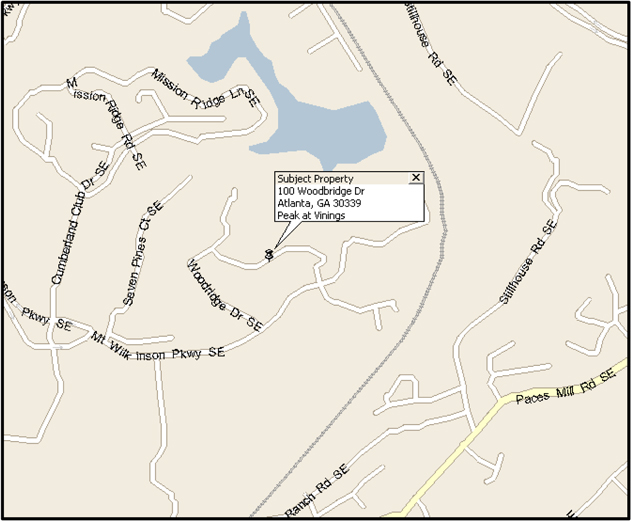

LOCATION MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 1 |

| SUMMARY OF SALIENT FACTS AND CONCLUSIONS | ||

| Date of Value | January 18, 2013 | |

| Date of Inspection | January 18, 2013 | |

| Property Name | Peak at Vinings | |

| Property Address | 100 Woodbridge Drive | |

| Atlanta, Georgia 30339 | ||

| Property Location | North side of Mt. Wilkinson Parkway (where the street dead ends), in an unincorporated section of the City of Atlanta, Georgia. | |

| Tax Identification | 17-0910-0-006-0. | |

| Purpose of the Appraisal | The purpose of the appraisal is to estimate the market value of the Leased Fee Interest in the subject property as of the date of value. | |

| Site Size | Irregular shaped site that contains a total of 22.00 acres | |

| Zoning | RM – 12 (Residential) | |

| Improvements | A 280-unit gated garden apartment complex completed in 1981 with 14 apartment buildings, a clubhouse with business center, meeting room, kitchen/gaming area, fitness center, swimming pool and mature landscaping. It is noted that there was a major renovation spanning between 2008 and 2009 upgrading all of the units and amenities at the property. The property is operating at stabilized occupancy and is in good physical condition. | |

| 2012 Assessed Value | $8,948,312 | |

| Highest and Best Use | ||

As If Vacant | Residential development. | |

As Improved | Continued use of the existing improvements. | |

| VALUATION INDICATIONS | ||

| Income Capitalization | $34,600,000 | |

Stabilized NOI | $1,992,038 | |

Cap Rate | 5.75% | |

Value per Unit | $123,581 | |

Value per Sq Ft | $127.02 | |

| Sales Comparison | $35,000,000 | |

Value per Unit | $125,000 | |

Value per Sq Ft | $128.49 | |

| Cost Approach | N/A | |

| APPRAISED VALUE | $34,600,000 | |

Value per Unit | $123,581 | |

Value per Sq Ft | $127.02 | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 2 |

| PREMISES OF THE APPRAISAL | ||

| Identification | The subject property consists of the land and improvements at 100 Woodbridge Drive within an unincorporated area of Atlanta, Cobb County, Georgia. The Cobb County Assessor identifies the property as Tax Parcel Identification Number 17-0910-0-006-0. The property consists of a 22.00- acre site improved with 280-unit apartment complex known as Peak at Vinings. | |

| Sales History of the Subject Property | According to public records, the current owner of the subject property is Peak at Vinings LLC, who has owned the property since October 2009 when it was transferred from Century Properties Fund XIX for $20,325,000. It is noted that the recent sale included the adjacent property, Lakeside at Vinings and was a related transfer. We are not aware of any transfers of ownership within the three-year period prior to the effective date of value. It is our understanding that the subject property is not being listed for sale and we are not aware of any contracts of sale pending as of the date this report was prepared. | |

| Purpose and Scope of the Appraisal | The purpose of the appraisal is to estimate the market value of the subject property as of the date of value. It is the intent of the appraisers that the analysis, opinions and conclusions of this report be considered an unbiased, objective investigation performed by a disinterested third party with complete objectivity as to the outcome of the analysis. | |

| According to the Appraisal Institute’s Code of Professional Ethics and Uniform Standards of Professional Appraisal Practice, the scope of the appraisal is cited as “the extent of the process of collecting, confirming, and reporting data” included in an appraisal report. All appropriate data deemed pertinent to the solution of the appraisal problem has been collected and confirmed. In the appraisal, we have: | ||

1. Inspected the subject property and its environs. | ||

2. Reviewed demographic and other socioeconomic trends pertaining to the city and region. | ||

3. Examined regional apartment market conditions, with special emphasis on the subject’s submarket. | ||

4. Investigated lease and sale transactions involving comparable properties in the influencing market. | ||

5. Reviewed the existing rent roll and discussed the leasing status with the building manager and leasing agent. In addition, we have reviewed the subject property’s recent operating history and those of competing properties. | ||

6. Utilized appropriate appraisal methodology to derive estimates of value. | ||

7. Reconciled the estimates of value into a single value conclusion. | ||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 3 |

| Definition of Market Value | The definition of Market Value used in this appraisal report is taken from the Appraisal Institute’sThe Dictionary of Real Estate Appraisal, Fifth Edition, Chicago, Illinois, Appraisal Institute, 2010, which states:

“The most probable price that a property should bring in a competitive and open market under all conditions requisite to a fair sales, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: | |

1. Buyer and seller are typically motivated; | ||

2. Both parties are well informed or well advised and acting in what they consider their best interests; | ||

3. A reasonable time is allowed for exposure in the open market; | ||

4. Payment is made in terms of cash in U.S. dollars or in terms of financial arrangements comparable thereto; and | ||

5. The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.” | ||

| Property Rights Appraised | The interest being appraised is the Leased Fee Interest. Leased Fee Interest is defined in The Dictionary of Real Estate Appraisal, Fifth Edition, Chicago, Illinois, Appraisal Institute, 2010, as:

“An ownership interest where the possessory interest has been granted to another party by creation of a contractual landlord tenant relationship, i.e. a lease. The rights of the lessor (the leased fee owner) and the leased fee are specified by contract terms contained within the lease.” | |

| Intended Use and Intended User | The intended user of the report is Fox Partners VII. It is understood that this appraisal will be utilized by the intended user as an aid in asset evaluation and financial reporting. All others reading or relying on this appraisal are considered unintended users. The appraisal cannot be used for any other reason than that stated above. The appraisers are not responsible for unauthorized use of this report. | |

| This appraisal has been prepared in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP) as promulgated by the Appraisal Standards Board of the Appraisal Foundation as well as the Code of Professional Ethics and Standards of Professional Appraisal Practice of the Appraisal Institute. The presentation of data and results of our analysis are presented in a Self-Contained Report format as set forth under Standards Rule 2-2 of the USPAP. | ||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 4 |

| Exposure Time | According to the previously stated definition of Market Value, the property must be allowed a reasonable time to be exposed in the open market to achieve the appraised value. Exposure is defined by the Appraisal Institute,The Dictionary of Real Estate Appraisal, Fifth Edition, Chicago, Illinois, Appraisal Institute, 2010, as: | |

| “1. The time a property remains on the market. | ||

| 2. The estimated length of time the property interest being appraised would have been offered on the market prior to the hypothetical consummation of a sale at market value on the effective date of the appraisal; a retrospective estimate based upon an analysis of past events assuming a competitive and open market.” | ||

| Exposure time is always presumed to occur prior to the effective date of the appraisal. The overall concept of reasonable exposure encompasses not only adequate, sufficient and reasonable time but also adequate, sufficient and reasonable effort. Exposure time is different for various types of real estate and value ranges and under various market conditions. | ||

| Review of transfer records suggests that there is an active investor market for good quality apartment properties; however, conventional sources of capital is somewhat limited and mortgage underwriting has remained conservative with a greater level of equity required to obtain financing in comparison to the period leading up to September 2008. These factors have impacted sales activity for most types of investment grade real estate. | ||

| We believe that if the subject property were exposed to the market for a reasonable period of time prior to the effective date of this appraisal, which we consider to be a period of up to 12 months, the subject would transfer at an appropriate price, that is to say, the appraised value. Support for this exposure period is provided by thePwC Real Estate Investor Survey Fourth Quarter 2012, which indicates that marketing times for apartment properties in the national market range from none to 18 months. The average marketing time equates to 5.1 months, down slightly from 5.2 months reported one year ago. In addition, thePwC Surveyindicates that marketing time for apartment properties in the Southeast Region range from one to 18 months. The average marketing time equates to 6.5 months, down slightly from 6.7 months reported one year ago. This marketing period is supported by data in the local market. | ||

| We acknowledge that in appraising the property to sell after the aforementioned exposure period, we must place most emphasis on the buyer’s expectations and yield requirements. The value conclusion rendered for the property through implementation of the Income Capitalization Approach has been accorded most weight as this technique most closely emulates buyer’s expectations and yield requirements. The market value estimate concluded herein assumes an exposure and marketing period of up to 12 months. | ||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 5 |

| REGIONAL ANALYSIS | ||

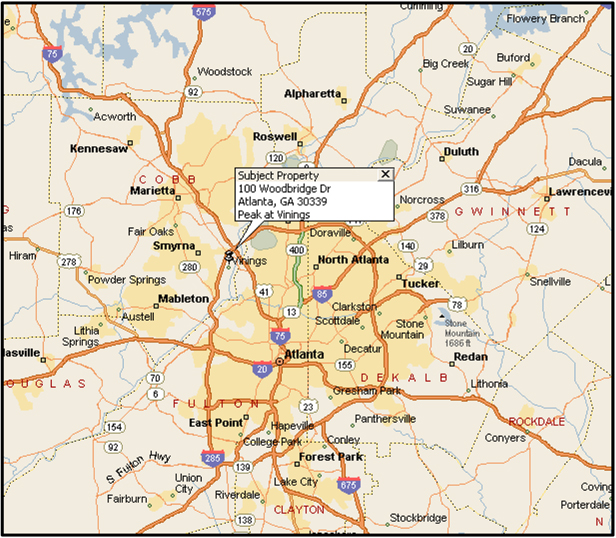

| Overview | The subject is located in Cobb County which is part of the Atlanta-Sandy Springs-Marietta Metropolitan Statistical Area (MSA). The MSA is comprised of 28 counties including Barrow, Bartow, Butts, Carroll, Cherokee, Clayton, Cobb, Coweta, Dawson, DeKalb, Douglas, Fayette, Forsyth, Fulton, Gwinnett, Haralson, Heard, Henry, Jasper, Lamar, Meriwether, Newton, Paulding, Pickens, Pike, Rockdale, Spalding and Walton. The Atlanta metropolitan area is located in north central Georgia in the foothills of the Appalachian Mountains. Once a rail hub in the mid-nineteenth century, Atlanta is now the major distribution, trade and financial center of the southeastern United States. | |

| During the 1980s, Atlanta enjoyed high levels of growth, reaching new levels of social and economic diversity. Much of the momentum built in the 1980s, however, was lost during the recessionary period of the early 1990s and the region suffered its first year-over-year job loss since the mid-1970s. Growth returned in 1992 and Metropolitan Atlanta enjoyed another period of substantial growth in jobs, population, households and personal income. The rate of growth surpassed that of the United States as a whole during this period. The geographic expansion and decentralization of metropolitan areas is perhaps best exemplified by the evolution and development of the Atlanta metropolitan area. Much of the region’s growth has been concentrated in the area north of the City’s downtown from I-75 to I-85. When built in the 1970s, the I-285 beltway defined the northern boundary with the Perimeter neighborhood and mall named to reflect at the time this edge location. Since then, the continued push north has been dramatic particularly along the region’s extensive expressway network. | ||

Population | The population of the MSA has grown steadily since 1980 at rates exceeding the State of Georgia as a whole. In fact, approximately 70.0% of the State’s population growth has occurred within the MSA. This trend is projected to continue over the next five years. The Atlanta MSA, with the addition of 1.0+ million new residents was the nation’s fastest growing MSA since 2000. Population estimates for Cobb County as of 2012 were 700,521, indicating an average annual increase of 1.27% over the 2000 population of 607,746. The County’s population is forecast to increase at a slightly slower pace through 2017 to 737,098. The rate of growth in the County has been less than the MSA and State. Population growth has been concentrated in Counties outside the beltway along major interstates such as Forsyth, Newton, Henry, Barrow, Cherokee, Walton, Dawson, Douglas and Pickens. The following table details historic and projected population trends for the County, MSA and the State. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 6 |

| POPULATION TRENDS | ||||||||||||||||||||

| Average Annual Growth | ||||||||||||||||||||

| 2000 Census | 2012 Estimate | 2017 Projection | 2000 - 2012 | 2012 -2017 | ||||||||||||||||

Cobb County | 607,746 | 700,521 | 737,098 | 1.27 | % | 1.04 | % | |||||||||||||

Atlanta MSA | 4,247,984 | 5,405,084 | 5,809,570 | 2.27 | % | 1.50 | % | |||||||||||||

Georgia | 8,186,384 | 9,890,616 | 10,479,874 | 1.73 | % | 1.19 | % | |||||||||||||

| Source: DemographicsNow.com; Compiled by KTR | ||||||||||||||||||||

| Economic Overview | According to the United States Bureau of Labor Statistics, the MSA’s total civilian labor force was 2,743,100 as of October 2012. The non-farm labor force as of October 2012 was 2,354,200. The unemployment rate stood at 8.2% as of October 2012, lower than the State and above the National unemployment rate of 8.7% and 7.9%, respectively. Unemployment in the MSA is down from 9.4% one year ago.

The MSA is ranked third after New York and Houston as a Fortune 500 headquarter city. Numerous major companies have made Atlanta their headquarters including The Coca-Cola Company, Home Depot and the United Parcel Service. AT&T (formerly Bell South), Delta Airlines, Turner Broadcasting and Cox Enterprises also have a large presence in the area. | |

| A majority of the MSA’s work force is employed in the Trade, Transportation and Utilities, Services, and Government sectors. Total employment in the MSA increased by 1.5% or 34,400 jobs over the past year. The Construction sector has been hit the hardest over the past year with a decrease of 3.7%. The following table illustrates the diversification of the Atlanta MSA’s work force as of October 2012, the most recent information available at the time of the report. | ||

ATLANTA-SANDY SPRINGS-MARIETTA MSA WORK FORCE BY INDUSTRY – AS OF OCTOBER 2012 | ||||||||

Industry Category | Number Employed (In Thousands) | 12-Month Percent Change | ||||||

Mining and Logging | 1.3 | 0.0 | % | |||||

Construction | 86.9 | -3.7 | % | |||||

Manufacturing | 152.6 | 3.3 | % | |||||

Trade, Transportation and Utilities | 547.6 | 3.5 | % | |||||

Information | 79.0 | 0.4 | % | |||||

Financial Activities | 134.3 | -3.3 | % | |||||

Professional and Business Services | 423.1 | 3.4 | % | |||||

Educational and Health Services | 300.4 | 2.3 | % | |||||

Leisure and Hospitality | 223.6 | 0.7 | % | |||||

Other Services | 93.8 | 1.2 | % | |||||

Government | 311.6 | -1.6 | % | |||||

|

|

|

| |||||

Total Nonfarm Employment | 2,354.2 | 1.5 | % | |||||

Source: Bureau of Labor Statistics; Compiled by KTR

| Income | According to DemographicsNow.com, the 2012 average household income in Cobb County was $88,590 indicating an average annual increase of 1.70% over the 2000 average of $73,549. The average household income |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 7 |

| is projected to reach $96,214 in 2017, a projected average annual increase of 1.72%. The County’s average household income growth was below the MSA and State between 2000 and 2012. This trend is projected to continue over the next five years. The County’s median household income grew at a slower pace increasing from $58,562 to $62,478 between 2000 and 2012 indicating an average annual increase of 0.56%. The median household income is projected to reach $71,913 in 2017 indicating an average annual increase of 3.02%. The County’s median household income growth was less than the MSA and State between 2000 and 2012, however, it is projected to growth is at a faster rate than both over the next five years. The average, median and per capita household incomes (2000 census, 2012 estimates and 2017 projections) for Cobb County, the Atlanta MSA and Georgia are presented in following table: |

| INCOME TRENDS | ||||||||||||||||||||

Category | 2000 Census | 2012 Estimates | 2017 Projections | Avg. Annual Growth 2000 - 2012 | Avg. Annual Growth 2012 - 2017 | |||||||||||||||

Average HH Income | ||||||||||||||||||||

Cobb County | $ | 73,549 | $ | 88,590 | $ | 96,214 | 1.70 | % | 1.72 | % | ||||||||||

Atlanta MSA | $ | 66,875 | $ | 81,219 | $ | 90,067 | 1.79 | % | 2.18 | % | ||||||||||

Georgia | $ | 56,611 | $ | 69,537 | $ | 77,310 | 1.90 | % | 2.24 | % | ||||||||||

Median HH Income | ||||||||||||||||||||

Cobb County | $ | 58,562 | $ | 62,478 | $ | 71,913 | 0.56 | % | 3.02 | % | ||||||||||

Atlanta MSA | $ | 51,888 | $ | 57,247 | $ | 65,855 | 0.86 | % | 3.01 | % | ||||||||||

Georgia | $ | 42,783 | $ | 48,611 | $ | 55,278 | 1.14 | % | 2.74 | % | ||||||||||

Per Capita Income | ||||||||||||||||||||

Cobb County | $ | 27,531 | $ | 33,234 | $ | 36,177 | 1.73 | % | 1.77 | % | ||||||||||

Atlanta MSA | $ | 24,467 | $ | 29,455 | $ | 32,746 | 1.70 | % | 2.23 | % | ||||||||||

Georgia | $ | 20,790 | $ | 25,737 | $ | 28,682 | 1.98 | % | 2.29 | % | ||||||||||

| Source: DemographicsNow.com; Compiled by KTR | ||||||||||||||||||||

| Transportation | Atlanta is at the hub of major highways and interstates connecting it with all major areas within the MSA and with all surrounding regions. Three major interstates, I-20, I 75 and I 85 converge in downtown Atlanta which is circled by I-285. MARTA operates bus and rail service in Dekalb and Fulton Counties with service to Downtown, Midtown, Buckhead and the Central Perimeter submarkets. The Hartsfield-Jackson International Airport is situated on the south side of the city, just inside the beltway. More than 1,300 flights on average leave daily to nearly 165 cities in the U.S. and 85 foreign cities making Hartsfield-Jackson the world’s top airport in passenger traffic. | |

| Conclusion | The Atlanta region benefits from its diverse economy, concentration of quality colleges and universities and high–tech infrastructure. The area has begun to rebound from the national recession with job increases in most industries. Given the regions location, transportation network, diverse and highly educated workforce, the region has good potential for growth over the long-term. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 8 |

REGIONAL MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 9 |

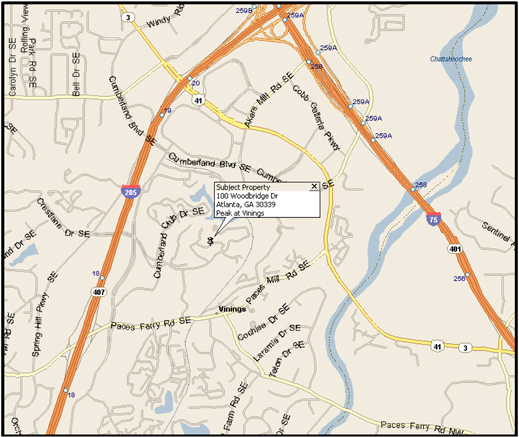

| NEIGHBORHOOD ANALYSIS | ||

| Overview | The subject property is located in an unincorporated suburban neighborhood within the City of Atlanta. Atlanta is the state capital and represents the most populous city in Georgia and is the third largest city in the United States. Atlanta today is the major economic center for the southeast region with a large presence of Fortune 500 companies. Atlanta is at the hub of major highways and interstates and is home to the world’s top airport in passenger traffic making it a major transportation hub for the United States. | |

| Population | The population in the subject’s zip code (30339) grew at an annual rate of 1.12% from 2000 to 2012, slower than the growth rate of Cobb County and the State of Georgia. DemographicsNow.com projects that the growth in the subject’s zip code will continue at a slightly slower pace through 2017. The following table illustrates the population statistics for the 30339 zip code, Cobb County and the State of Georgia from 2000 through 2017. | |

| HISTORICAL POPULATION AND PROJECTIONS | ||||||||||||||||||||

| Average Annual Growth | ||||||||||||||||||||

| 2000 Census | 2012 Estimate | 2017 Projection | 2000 - 2012 | 2012 - 2017 | ||||||||||||||||

30339 Zip Code | 17,849 | 20,248 | 21,142 | 1.12 | % | 0.88 | % | |||||||||||||

Cobb County | 607,746 | 700,521 | 737,098 | 1.27 | % | 1.04 | % | |||||||||||||

Georgia | 8,186,384 | 9,890,616 | 10,479,874 | 1.73 | % | 1.19 | % | |||||||||||||

Source: DemographicsNow |

| |||||||||||||||||||

| Income | According to DemographicsNow.com, the 2012 average household income in the subject’s zip code was $94,868 indicating an average annual increase of 1.38% over the 2000 average of $81,391. The average household income is projected to reach $102,571 in 2017, a projected average annual increase of 1.62%. The subject’s zip code median household income grew at a slower pace increasing from $57,546 to $60,170 between 2000 and 2012 indicating an average annual increase of 0.38%. The median household income is projected to reach $67,823 in 2017 indicating an average annual increase of 2.54%. The subject’s zip code per capita household income increased from $44,287 to $52,888 between 2000 and 2012 indicating an average annual increase of 1.62%. The per capita household income is projected to reach $56,403 in 2017 indicating an average annual increase of 1.33%. The average, median and per capita household incomes (2000 census, 2012 estimates and 2017 projections) for the subject’s zip code are presented in following table: |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 10 |

INCOME TRENDS

| Average Annual Growth | ||||||||||||||||||||

| 2000 Census | 2012 Estimate | 2017 Projection | 2000 -2012 | 2012 -2017 | ||||||||||||||||

Average HH Inc. | $ | 81,391 | $ | 94,868 | $ | 102,571 | 1.38 | % | 1.62 | % | ||||||||||

Median HH Inc. | $ | 57,546 | $ | 60,170 | $ | 67,823 | 0.38 | % | 2.54 | % | ||||||||||

Per Capita HH Inc. | $ | 44,287 | $ | 52,888 | $ | 56,403 | 1.62 | % | 1.33 | % | ||||||||||

Source: DemographicsNow.com; Compiled by KTR

| Transportation | The subject neighborhood is well served by an extensive highway system including I-75 and I-285. Several secondary thoroughfares also traverse the immediate area and include Cumberland Parkway and Paces Ferry Road. Bus service is available via the 12 Howell Mill /Cumberland line. | |

| Surrounding Improvements | Surrounding improvements consist of gated garden style apartment complexes and some commercial uses. | |

| Conclusion | The subject neighborhood is considered to be an attractive residential location because of its excellent highway access and proximity to Atlanta’s Central Business District. | |

NEIGHBORHOOD MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 11 |

| SITE ANALYSIS | ||

| Location | North side of Mt. Wilkinson Parkway, in an unincorporated section of the City of Atlanta, Georgia. Woodbridge Drive is the interior street within the development The physical address of the property is 100 Woodbridge Drive, City of Atlanta Georgia. | |

| Site Area | 22.00 acres, which equates to 958,320 square feet. | |

| Street Frontage | The subject has frontage along the north side of Mt. Wilkinson Parkway. | |

| Topography | The site slopes upward from the Mt. Wilkinson Parkway frontage. | |

| Shape | The parcel is irregularly shaped. The size, shape, and configuration of the subject property provide a functional layout, which is similar to competitors. | |

| Excess/Surplus Land | Traffic circulation throughout the property and an adequate number of parking spaces is provided on concrete paved drives and surface lots. The building setbacks allow for landscaped buffers, similar to surrounding properties. There does not appear to be excess or surplus land. | |

| Utilities | All customary municipal services and utility hookups are provided. | |

| Soil Information | No adverse conditions were readily apparent. | |

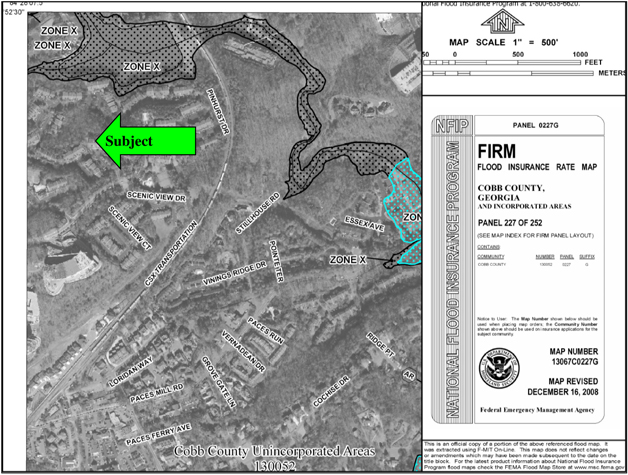

| Flood Information | The subject property is situated in Flood Zone “X”, which is an area outside of the 100-year flood plain, according to the FEMA Map 13067C0227G, dated December 16, 2008. | |

| Easements and Encroachments | No title report or survey showing the location of easements was provided in connection with this assignment. Thus, it is not possible to make a definitive conclusion regarding any potential impacts on value of the location of any such easements or encroachments. Visual observations of the site revealed no adverse easements or encroachments. It appears as though the subject is encumbered by utility and access easements typical of a developed site. It is specifically assumed that any easements, restrictions or encroachments that might appear against the title would have no adverse impact on marketability or value. | |

| Environmental | No readily observable adverse environmental site conditions were noted. No environmental reports were provided for review. | |

| Accessibility/Visibility | Ingress and egress to the property is via the Mt. Wilkinson Parkway frontage. Accessibility of the site is good. The buildings are at street grade and visible to passing traffic. | |

| Improvements | There are 14 apartment buildings, clubhouse with business center, meeting room, kitchen/gaming area, fitness center, swimming pool and mature landscaping. | |

| Conclusions | The site attributes are well suited for the existing development and use. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 12 |

SITE MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 13 |

FLOOD MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 14 |

| IMPROVEMENT ANALYSIS | ||

| Year Built/Renovated | The facility was completed in 1981 as a gated garden-style apartment complex. There was a major renovation of the subject between 2008 and 2009 that upgraded all of the units and the amenities. | |

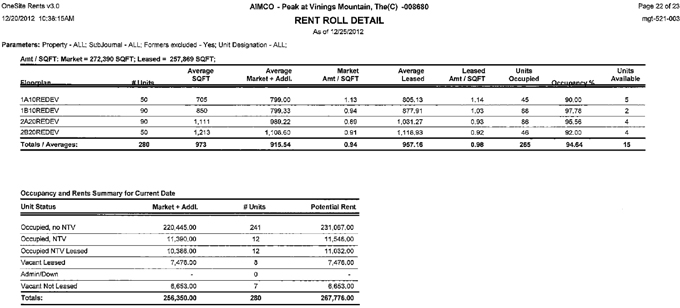

| Layout & Configuration | The complex consists of 280 apartment units within 14 apartment buildings and contains 272,390 square feet of rentable area. The buildings are sited along internal drives that are integrated with the parking lots. In addition, the property also contains a clubhouse with business center, meeting room, kitchen/gaming area, fitness center and swimming pool. | |

| Leasable Area/Unit Mix | The following chart summarizes the unit mix and sizes of the various floor plans at the subject property as indicated by a review of client provided rent roll data and floor plans. | |

UNIT MIX AND FLOOR AREAS

Type | Mix | Size | Total Area | |||||||||

1 Bed/1 Bath | 50 | 705 | 35,250 | |||||||||

1 Bed/1 Bath | 90 | 850 | 76,500 | |||||||||

2 Bed/2 Bath | 90 | 1,111 | 99,990 | |||||||||

2 Bed/2 Bath | 50 | 1,213 | 60,650 | |||||||||

Totals/Averages | 280 | 973 | 272,390 | |||||||||

Source: Client provided rent roll data and floor plans; compiled by KTR

| Floor Plans | As indicated, the property offers a variety of one-and two-bedroom floor plans. Each floor plan provides a living room off a small entry foyer and dining room off the kitchen area. Washer and dryers are provided in all of the units. In addition each unit has a private balcony. | |

| EXTERIOR | ||

| Structure | The foundations consist of reinforced concrete slabs, poured on grade. Structural framing is wood stud walls with interior gypsum-clad drywall. | |

| Floors | The floors are constructed of engineered wood trusses. The ceiling heights are approximately 10 feet. | |

| Walls | The exterior of the buildings are vinyl siding and brick. | |

| Windows | Individual unit windows are double pane glass set in aluminum frames. Entry doors are metal set in wood frames. Glass doors provide access to the balconies. | |

| Roof | The buildings have single pitched roofs with composition shingles. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 15 |

| INTERIOR FINISHES | ||

| Walls and Ceilings | Textured and painted drywall. | |

| Flooring | Flooring consists of carpeting, wood and tile. | |

| Kitchens | Typical appliance package consisting of a refrigerator/freezer, full-size electric range with oven, microwave and dishwasher. Cabinets are wood and countertops are granite. | |

| Bathrooms | Shower/tub, toilet, vanity with sink and mirrored medicine cabinet. Tubs have a ceramic tile wainscoting. | |

| Unit Amenities | All of the units have washers/dryers, walk-in closets and balconies. Some of the units have a fireplace and built in dry or wet-bars. | |

| MECHANICAL | ||

| SYSTEMS HVAC | Air and heat is provided by individual split systems with exterior condensers. The system is similar to competing properties. | |

| Electric Service | Adequate electric service is provided. Each apartment has a separate panel. | |

| Plumbing | Apartment-grade plumbing systems are installed. Each unit is serviced by an electric water heater. | |

| Fire Protection | The subject property is not equipped with a fire sprinkler system. The apartments are fit with smoke detectors. | |

| ANCILLARY AREAS | ||

| Landscaping | Landscaping is of mature vegetation. Native trees and shrubs are plentiful throughout the common areas and between buildings. Seasonal color is provided in beds along the main entrance points and near the pool and office area. | |

| Parking | The internal drive incorporates the surface parking lots. There are an adequate number of parking spaces provided. The drives and parking lots are concrete paved. | |

| Recreational Amenities | A clubhouse with business center, meeting room, kitchen/gaming area, fitness center, swimming pool and mature landscaping. In addition, the property has shared amenities with the 2 adjacent sister properties providing additional swimming pools, fitness center, a golf simulator, movie screening room, billiards/game rooms, massage room, wine tasting room, barbeque areas, putting green and a tennis court. | |

| FF&E | ||

| Personal Property | The subject property has office furnishings at the clubhouse, clubhouse furniture and various chairs and tables for the pool deck. Kitchen appliances are considered personal property. The FF&E is similar to competitive properties. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 16 |

| CONDITION/MAINTENANCE | ||

| Exterior | Good condition. Overall maintenance appears adequate. | |

| Roof | Good condition. | |

| Interiors | Good condition. Overall maintenance appears adequate. | |

| Common Area Amenities | Good condition. Overall maintenance appears adequate. | |

| Sidewalks & Paving | Good condition. Overall maintenance appears adequate. | |

| Landscaping | Good condition. Overall maintenance appears adequate. | |

| Environmental Conditions | No readily observable adverse conditions were noted during the site visit. | |

| ELEMENTS OF DEPRECIATION | ||

| Based on our field inspection, we note that some elements of depreciation are present at the subject property. | ||

| Physical Deterioration | The overall physical condition is average with adequate maintenance levels. Physical deterioration is primarily limited to general aging and normal wear and tear. No material elements of deferred maintenance were noted during the appraiser’s inspection of the property. Carpet and mechanical equipment in the individual units are updated and/or replaced on an as-needed basis. According to Marshall Valuation Service, buildings similar to the subject property have an economic life of approximately 50 years. The actual age of the property is 32 years. As a result of on-going maintenance and the recent renovations, the effective age is estimated to be less than the actual age. | |

Capital Improvements

Functional Obsolescence | No major capital improvements are planned in the near term.

The subject property’s design, systems and floor plans are consistent with traditional garden style apartment complexes. The property has operated at rental rates and occupancy levels that are consistent with that of other similar properties within the influencing market, attesting to its functional adequacy and market acceptance. Considering these factors, no adjustment for functional obsolescence is required. | |

| External Obsolescence | External obsolescence is a loss in value resulting from conditions that are present outside the property and is usually incurable. No site-specific external obsolescence was noted. | |

| Conclusions | The subject improvements have adequate functional utility, conforms well to the general character of the neighborhood and is generally similar to competitors. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 17 |

| ZONING ANALYSIS | ||

| Introduction | According to Cobb County, the subject property is situated in an RM - 12 Residential Multifamily District. The purpose and intent of the RM - 12 District is to provide locations for multifamily residential uses or residentially compatible institutional and recreational uses which are within properties delineated for high density residential and regional activity center categories. | |

| The bulk restrictions in the RM - 12 - Residential Multifamily District are summarized in the following table. | ||

RM - 12 - RESIDENTIAL MULTIFAMILY DISTRICT

RESTRICTION | SIZE | |

Minimum lot area | 80,000 sq. ft | |

Minimum lot width | 75 Feet | |

Minimum front yards | 75 Feet | |

Minimum side yards | 35 Feet | |

Minimum rear yard | 40 Feet | |

Maximum height | 4 stories or 40 Feet | |

Maximum building coverage | 35 Percent | |

Maximum Units Per Acre | 12 | |

Minimum Parking | ||

Multifamily Uses | 1.75 spaces per unit |

Source: Cobb County Code of Ordinances; Compiled by KTR.

| Conclusions | The subject is built to a density of 12.73 units per acre, above the maximum of 12 units per acre. The exact number of parking spaces was not reported to the appraiser; however, according to the zoning department, the number of spaces at the subject meets current requirements. The subject property was constructed prior to the adoption of the RM-12 zoning designation in November 1990. As such, the subject appears to represent a legal and conforming use with a legal and non-complying density. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 18 |

ZONING MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 19 |

| REAL ESTATE ASSESSMENTS AND TAXES | ||

| Overview | According to the Cobb County tax record, the subject property is identified as Parcel Number 17-0910-0-006-0. The taxes are billed annually in July and are paid in October. The taxable value is multiplied by the current tax rate to calculate the taxes payable. Revaluations occur every year. The 2013 assessment has not been released and therefore, the 2012 assessment has been utilized in this report. The subject’s 2012 assessment is shown below. | |

SUBJECT PROPERTY ASSESSMENT

Land Value | Building Value | Taxable Value | ||||||

$1,568,160 | $ | 7,380,152 | $ | 8,948,312 | ||||

Source: Cobb County Assessor’s Office

| Comparable Assessments | Similar properties within the area were surveyed to ascertain the reasonableness of the subject’s current assessment. The subject’s current assessment is $31,958 per unit. The comparables range between $32,451 and $36,719 per unit. The subject’s assessment falls slightly below the comparable range; however, based on discussions with the County Assessor, the assessment appears reasonable and has been processed. |

TAX COMPARABLES

| Property Name | Tax ID | Taxable Value | Year Built | Assessed Units | Assessment Per Unit | |||||||||||||||

Peaks at Vinings (Subject) | 17-0910-0-006-0 | $ | 8,948,312 | 1981 | 280 | $ | 31,958 | |||||||||||||

Lakeside at Vinings | 17-0950-0-061-0 | $ | 7,315,284 | 1982 | 220 | $ | 33,251 | |||||||||||||

Views at Vinings | 17-0951-0-005-0 | $ | 5,841,256 | 1983 | 180 | $ | 32,451 | |||||||||||||

Magnolia Vinings | 17-0818-0-007-0 | $ | 14,344,308 | 1997 | 400 | $ | 35,861 | |||||||||||||

Stonewood Vinings | 17-0818-0-002-0 | $ | 11,382,945 | 1997 | 310 | $ | 36,719 | |||||||||||||

Source: Cobb County Assessor, compiled by KTR

| Mill Rate | Mill rates have remained relatively stable over the past several years. The 2012 total mill rate applicable for all taxing authorities with jurisdiction over the subject property equates to $30.21 per $1,000 of assessed value. According to the County Assessor, the new mill rate will be published in July 2013. | |

| Real Estate Tax Projection | Future increases in reassessments are expected to reflect annual increases near the anticipated inflation rate during the same period. Tax rates are expected to remain relatively stable. The total amount is anticipated to increase at a rate near the long-term average inflation rate | |

| Tax Calculation | The subject’s real estate tax liability is calculated utilizing the current assessment and the prior year’s tax rate, which equates to $270,328.50. The current tax liability has been adjusted for inflation resulting in a projected tax liability of $278,438, which has been processed in the valuation. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 20 |

| APARTMENT MARKET ANALYSIS | ||

| Area Housing Market | According to Red Capital Group, the subject is located in the Vinings area of the Smyrna submarket. Red Capital Group tracks only the Smyrna market as a whole. The immediate area is comprised of gated garden style apartment complexes with approximately 8,300 apartments. Red Capital Group indicates that as of the First Quarter 2012, the most recent data available, the vacancy rate in the submarket was 4.7%, lower than the previous year vacancy rate of 6.8%. The average asking rental rate was $723 per month an increase over the prior year’s estimate which was $704 per month. Additionally, an article published by Property Management Insider in April 2012, indicates that the Vinings area has outperformed the rest of the Atlanta Metro Area since the recession in 2009. In late 2009, at the height of the recession, occupancy in the area dropped to a low of 91.4%, which was still 300 basis points above the entire Metro Area. The article supports Red Capital Group’s current occupancy estimate at 95% and 96%. New construction in the area consists of a 302-unit project called The Heights at Stillhouse Ridge and a 314-unit project called Walton Riverwood. The Heights at Stillhouse Ridge is a luxury mid-rise community which opened in October 2012 and Walton Riverwood is a luxury mid-rise community which is scheduled to open in the Fall of 2013. | |

| Subject Property | The subject’s units have average sizes and finishes consistent with that of the market. According to the December 25, 2012 rent roll, the subject’s contract rent averages $957.16 per month. The one-bedroom units indicate an average rental range between $805.13 and $877.91 per month and the two-bedroom apartments indicate an average rental range between $1,031.27 and $1,118.93 per month. | |

| According to the December 25, 2012 rent roll, there were 15 units vacant. The average asking rents for the one bedroom apartments are $799 per month and the average asking rents for two-bedroom apartments range between $989 and $1,109 per month. Based on conversations with management, the indicated asking rents on the supplied rent roll is low due to the fact that there was reduced leasing activity in the Fourth Quarter of 2012. Management indicated that commencing in late December leasing activity picked up and asking rates continued to rise with reduced availability. | ||

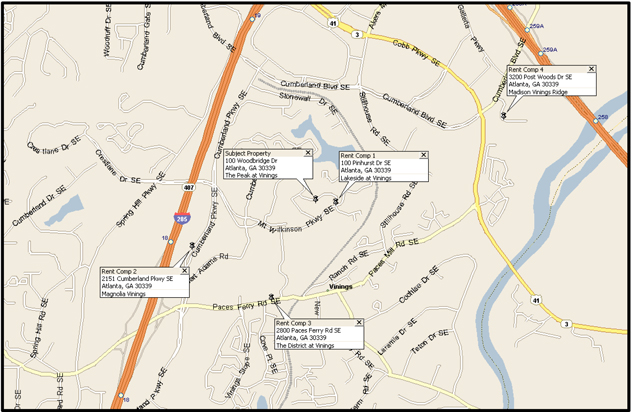

| Competitive Set | In order to determine the reasonableness of the subject’s asking rents, a survey of comparable apartment complexes in the market was conducted. The subject competes with a number of properties in the area. All of the properties are in close proximity to the subject and define the range of unit types and rental rates in the market. The information regarding the rent comparables was obtained through physical inspections and direct interviews with rental agents and property managers. The following map illustrates the location of the comparable properties in relation to the subject. Data sheets summarizing details of the comparable properties follow the map. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 21 |

COMPARABLE RENTAL MAP

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 22 |

| COMPARABLE RENTAL 1 | Lakeside at Vinings 100 Pinhurst Drive Atlanta, GA 30339 |

|  |

| Units | 220 | |

| Year Built/Renovated | 1982/2008 | |

| Occupancy | 92.7% | |

| Amenities | Washer/dryer in each unit, kitchens with standard appliances, balcony/patio and walk-in closets. Complex amenities include a business center, movie room, swimming pool and a car care center. | |

| Concessions | Prices change often and rents for individual floor plans are reduced as needed to help bolster occupancy. There are currently no concessions being offered at this comparable. | |

RENTAL DATA

Type | Size | Rent | Rent/SF | |||||||||

1 Bed/1 Bath | 705 | $ | 829 | $ | 1.18 | |||||||

1 Bed/1 Bath | 850 | $ | 929 | $ | 1.09 | |||||||

2 Bed/1 Bath | 1,111 | $ | 1,165 | $ | 1.05 | |||||||

2 Bed/2 Bath | 1,111 | $ | 1,258 | $ | 1.13 | |||||||

2 Bed/2 Bath | 1,213 | $ | 1,179 | $ | 0.97 | |||||||

3 Bed/2 Bath | 1,415 | $ | 1,389 | $ | 0.98 | |||||||

| Comments | Property is a “sister” property to subject; however, slightly superior. It is noted that the asking rents for this comparable are from the December 25, 2012 rent roll. Based on conversations with management the asking rents for the subject property should be slightly below the asking rents indicated by this comparable. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 23 |

| COMPARABLE RENTAL 2 | Magnolia Vinings 2151 Cumberland Parkway Atlanta, GA 30339 |

| Units | 400 | |

| Year Built | 1997 | |

| Occupancy | 95%-98% | |

| Amenities | Washer/dryer connections, butler’s pantry, walk-in closets, patios/balconies with storage space and kitchens with standard appliances. Complex amenities include a gated entrance, swimming pool, clubhouse with media lounge, tennis courts and fitness center. | |

| Concessions | Prices change often and rents for individual floor plans are reduced as needed to help bolster occupancy. There are currently no concessions being offered at this comparable. | |

RENTAL DATA

Type | Size | Rent | Rent/SF | |||||||||

1 Bed/1 Bath | 572 | $ | 765-$831 | $ | 1.34-$1.45 | |||||||

1 Bed/1 Bath | 753 | $ | 815-$935 | $ | 1.08-$1.24 | |||||||

2 Bed/1 Bath | 967 | $ | 975-1,050 | $ | 1.01-$1.09 | |||||||

2 Bed/2 Bath | 1,113 | $ | 1,015-$1,170 | $ | 0.91-$1.05 | |||||||

3 Bed/2 Bath | 1,366 | $ | 1,200-$1,370 | $ | 0.88-$1.00 | |||||||

| Comments | Property is located approximately 0.6 mile southwest of the subject property. This property is in similar condition to the subject and is in a similar area. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 24 |

| COMPARABLE RENTAL 3 | The District at Vinings 2800 Paces Ferry Road Atlanta, NC 30339 |

| Units | 464 | |

| Year Built/Renovated | 1971/1993 | |

| Occupancy | 95% | |

| Amenities | Washer/dryer connections in some units, patios/balconies, vaulted ceilings, ceiling fan, kitchens with standard appliances including a dishwasher and walk-in closets. Complex amenities include a laundry room, swimming pool, fitness center, putting green, 3 lakes, a Yoga/Pilates room, picnic areas with grills, walking trails, tennis courts, Dog Park, clubhouse and a business center. | |

| Concessions | Prices change often and rents for individual floor plans are reduced as needed to help bolster occupancy. There are currently no concessions being offered at this comparable. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 25 |

RENTAL DATA

Type | Size | Rent | Rent/SF | |||||||||

Studio/1 Bath | 703 | $ | 849 | $ | 1.21 | |||||||

1 Bed/1 Bath | 758 | $ | 899 | $ | 1.19 | |||||||

1 Bed/1 Bath | 770 | $ | 949 | $ | 1.23 | |||||||

2 Bed/2 Bath | 1,048 | $ | 999 | $ | 0.95 | |||||||

2 Bed/2 Bath | 1,051 | $ | 999 | $ | 0.95 | |||||||

2 Bed/2 Bath | 1,100 | $ | 1,029 | $ | 0.94 | |||||||

2 Bed/2 Bath | 1,121 | $ | 1,029 | $ | 0.92 | |||||||

2 Bed/2 Bath | 1,288 | $ | 1,200 | $ | 0.93 | |||||||

3 Bed/2 Bath | 1,366 | $ | 1,300 | $ | 0.95 | |||||||

| Comments | Property is located approximately 0.4 miles south of the subject property. This property is in slightly inferior condition to the subject and located in a similar area. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 26 |

| COMPARABLE RENTAL 4 | Madison at Vinings Ridge 3200 Post Woods Drive Atlanta, NC 30339 |

| Units | 494 | |

| Year Built | 1977 | |

| Occupancy | 96% | |

| Amenities | Washer/dryer in all units, patios/balconies, ceiling fan, kitchens with standard appliances, and fireplaces and sunrooms in select units. Complex amenities include a swimming pool, fitness center, sundeck/lounge area, tennis court, jogging trail, picnic areas with BBQ grills, clubhouse and a business center. | |

| Concessions | Prices change often and rents for individual floor plans are reduced as needed to help bolster occupancy. There are currently no concessions being offered at this comparable. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 27 |

RENTAL DATA

Type | Size | Rent | Rent/SF | |||

1 Bed/1 Bath | 526 | $753-$818 | $1.43-$1.56 | |||

1 Bed/1 Bath | 578 | $785-$852 | $1.36-$1.47 | |||

1 Bed/1 Bath | 731-757 | $916-$995 | $1.21-$1.36 | |||

1 Bed/1 Bath | 849 | $987-$1,071 | $1.16-$1.26 | |||

2 Bed/1 Bath | 1,082 | $982-$1,052 | $0.91-$0.97 | |||

2 Bed/1 Bath | 988-1,068 | $1,043-$1,120 | $0.98-$1.13 | |||

2 Bed/1 Bath | 965-1,071 | $1,068-$1,147 | $1.00-$1.19 | |||

2 Bed/2 Bath | 1,021-1,127 | $1,083-$1,163 | $0.96-$1.14 | |||

2 Bed/2 Bath | 1,055-1,135 | $1,083-$1,159 | $0.95-$1.10 | |||

2 Bed/2 Bath | 1,184 | $1,139-$1,251 | $0.96-$1.06 | |||

2 Bed/2 Bath | 1,308 | $1,189-$1,281 | $0.91-$0.98 | |||

2 Bed/2 Bath | 1,335 | $1,267 | $0.95 | |||

2 Bed/2.5 Bath | 1,375 | $1,114-$1,1196 | $0.81-$0.87 | |||

3 Bed/2 Bath | 1,502 | $1,572-$1,611 | $1.05-$1.07 |

| Comments | Property is located approximately 0.75 miles northeast of the subject property. It is in similar condition and located in a similar area. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 28 |

| ANALYSIS | The comparable rental properties are all in the vicinity of the subject property. The comparable properties were constructed between 1971 and 1997 with subsequent renovations to most. The units and complex amenities are similar to the subject. The rental rates illustrated by the comparable properties provide a good indication as to the appropriate market rent of the subject property. As noted in the beginning of this section, management indicated that the asking rents on the supplied rent roll are low due to the fact that there was reduced leasing activity in the Fourth Quarter of 2012. Management indicated that commencing in late December leasing activity picked up and asking rates will continue to rise with reduced availability. Additionally, management feels that the asking rents for the subject property should be slightly below the asking rents indicated by Lakeside at Vinings, the adjacent “sister” property. | |

| One-Bedroom Units | The subject property offers two variations of one-bedroom floor plans, ranging between 705 and 850 square feet. The asking rental rates for the subject’s units both being $799 per month or between $0.94 and $1.13 per square foot. The following chart outlines rental rates for similar sized one – bedroom floor plans within the competing apartment properties. | |

ONE-BEROOM FLOOR PLANS

| Unit Size (SF) | Rent/Month | Rent/SF | Comment | |||||||||||||

Subject | 705 | $ | 799 | $ | 1.13 | Subject | ||||||||||

| 850 | $ | 799 | $ | 0.94 | Subject | |||||||||||

Lakeside at Vinings | 705 | $ | 829 | $ | 1.18 | Slightly Superior | ||||||||||

| 850 | $ | 929 | $ | 1.09 | Slightly Superior | |||||||||||

Magnolia Vinings | 572 | $ | 765-$831 | $ | 1.34-$1.45 | Smaller | ||||||||||

| 753 | $ | 815-$935 | $ | 1.08-$1.24 | Similar | |||||||||||

The District at Vinings | 758 | $ | 899 | $ | 1.19 | Similar | ||||||||||

| 770 | $ | 949 | $ | 1.23 | Similar | |||||||||||

Madison Vinings Ridge | 526 | $ | 753-$818 | $ | 1.43-$1.56 | Smaller | ||||||||||

| 578 | $ | 785-$852 | $ | 1.36-$1.47 | Smaller | |||||||||||

| 731-757 | $ | 916-$995 | $ | 1.21-$1.36 | Similar | |||||||||||

| 849 | $ | 987-$1,071 | $ | 1.16-$1.26 | Similar | |||||||||||

|

|

|

|

|

| |||||||||||

Subject Range | 705-850 | $ | 799 | $ | 0.94-$1.13 | |||||||||||

Comparable Range | 526-850 | $ | 753-$1,071 | $ | 1.08-$1.56 | |||||||||||

| The comparable one-bedroom units range from 526 to 850 square feet with asking rents between $753 and $1,071 per unit or $1.08 to $1.56 per square foot. The comparable properties are all similar to the subject in terms of location and physical characteristics. Based on the asking rents indicated by Lakeside at Vinings, the subject’s asking rents for the 705 square foot units appear reasonable, whereas the asking rents for the 850 square foot units appears low. Considerate of the $30 per month difference between the 705 square foot units at the two properties, an average asking rent of $899 per month has been processed for the 850 square foot. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 29 |

| Two-Bedroom Units | The subject property offers two variations of the two-bedroom floor plans, which range from 1,111 to 1,213 square feet with asking rents ranging between $989 and $1,109 per month or $0.89 to $0.91 per square foot. The comparable two-bedroom units range in size from 965 to 1,375 square feet and have monthly asking rents ranging from $975 to $1,281 or $0.81 to $1.19 per square foot. |

TWO-BEDROOM FLOOR PLANS

| Unit Size (SF) | Rent/Month | Rent/SF | Comment | |||||||||||||

Subject | 1,111 | $ | 989 | $ | 0.89 | Subject | ||||||||||

| 1,213 | $ | 1,109 | $ | 0.91 | Subject | |||||||||||

Lakeside at Vinings | 1,111 | $ | 1,165 | $ | 1.05 | Slightly Superior | ||||||||||

| 1,111 | $ | 1,258 | $ | 1.13 | Slightly Superior | |||||||||||

| 1,213 | $ | 1,179 | $ | 0.97 | Slightly Superior | |||||||||||

Magnolia Vinings | 967 | $ | 975-1,050 | $ | 1.01-$1.09 | Similar | ||||||||||

| 1,113 | $ | 1,015-$1,170 | $ | 0.91-$1.05 | Similar | |||||||||||

The District at Vinings | 1,048 | $ | 999 | $ | 0.95 | Similar | ||||||||||

| 1,051 | $ | 999 | $ | 0.95 | Similar | |||||||||||

| 1,100 | $ | 1,029 | $ | 0.94 | Similar | |||||||||||

| 1,121 | $ | 1,029 | $ | 0.92 | Similar | |||||||||||

| 1,288 | $ | 1,200 | $ | 0.93 | Similar | |||||||||||

Madison Vinings Ridge | 1,082 | $ | 982-$1,052 | $ | 0.91-$0.97 | Similar | ||||||||||

| 988-1,068 | $ | 1,043-$1,120 | $ | 0.98-$1.13 | Similar | |||||||||||

| 965-1,071 | $ | 1,068-$1,147 | $ | 1.00-$1.19 | Similar | |||||||||||

| 1,021-1,127 | $ | 1,083-$1,163 | $ | 0.96-$1.14 | Similar | |||||||||||

| 1,055-1,135 | $ | 1,083-$1,159 | $ | 0.95-$1.10 | Similar | |||||||||||

| 1,184 | $ | 1,139-$1,251 | $ | 0.96-$1.06 | Similar | |||||||||||

| 1,308 | $ | 1,189-$1,281 | $ | 0.91-$0.98 | Larger | |||||||||||

| 1,335 | $ | 1,267 | $ | 0.95 | Larger | |||||||||||

| 1,375 | $ | 1,114-$1,1196 | $ | 0.81-$0.87 | Larger | |||||||||||

|

|

|

|

|

| |||||||||||

Subject Range | 1,111-1,213 | $ | 989-$1,109 | $ | 0.89-$0.91 | |||||||||||

Comparable Range | 965-1,375 | $ | 975-$1,281 | $ | 0.81-$1.19 | |||||||||||

| The comparable properties are similar to the subject in terms of location and physical characteristics. Although the subject’s asking rents are bracketed by the rents in competing properties, they are considered below market. Considerate of the $30 per month difference between the 705 square foot one-bedroom units at the two properties, an average asking rent of $1,135 per month has been processed for the 1,111 square foot unit and $1,149 per month has been processed for the 1,213 square foot unit. |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 30 |

| Conclusions | The subject is expected to continue to capture a proportionate and resaonable share of the market at the indicated economic rates. The subject’s potential gross on a monthly rent basis is summarized in the following chart. |

SUMMARY OF ECONOMIC RENT POTENTIAL

Type | Mix | Size | Total Area | Rent | Rent/SF | Total Rent | ||||||||||||||||||

1 Bed/1 Bath | 50 | 705 | 35,250 | $ | 799 | $ | 1.13 | $ | 39,950 | |||||||||||||||

1 Bed/1 Bath | 90 | 850 | 76,500 | $ | 899 | $ | 1.06 | $ | 80,910 | |||||||||||||||

2 Bed/2 Bath | 90 | 1,111 | 99,990 | $ | 1,135 | $ | 1.02 | $ | 102,150 | |||||||||||||||

2 Bed/2 Bath | 50 | 1,213 | 60,650 | $ | 1,149 | $ | 0.95 | $ | 57,450 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Totals/Averages | 280 | 973 | 272,390 | $ | 1,002 | $ | 1.03 | $ | 280,460 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 31 |

| HIGHEST AND BEST USE | ||

| Introduction | Highest and Best Use is defined by the Appraisal Institute inTheDictionary of Real Estate Appraisal, Fifth Edition, Chicago, Illinois, Appraisal Institute, 2010, which states: | |

| That reasonably probable and legal use of vacant land or an improved property, which is physically possible, appropriately supported, financially feasible and that results in the highest value. The four criteria the highest and best use must meet are legal permissibility, physical possibility, financial feasibility and maximum productivity. | ||

| There are typically two Highest and Best Use scenarios: the Highest and Best Use of the property as vacant and the Highest and Best Use of the site as if improved. | ||

HIGHEST AND BEST USE AS VACANT

| ||

| Definition | Highest and Best Use As Vacant is defined as “among all reasonable, alternative uses, the use that yields the highest present land value, after payments are made for labor, capital, and coordination. The use of a property based on the assumption that the parcel of land is vacant or can be made vacant by demolishing any improvements.” | |

| The site is zoned within the RM - 12 Residential Multifamily Zoning District that allows for a variety of residential uses. The maximum value of a property is typically realized when a reasonable degree of homogeneity is present. Thus, conformity in use is usually a highly desirable aspect of real property, since it creates and/or maintains value. The immediate area is primarily developed with garden style apartment complexes. Based on the principal of conformity and the subject’s zoning, the highest and best use of the property, if vacant, is residential development. | ||

HIGHEST AND BEST USE AS IMPROVED

| Definition | Highest and Best Use As Improved is defined as “the use that should be made of a property as it exists. An existing property should be renovated or retained as is so long as it continues to contribute to the total market value of the property, or until the return from a new improvement would more than offset the cost of demolishing the existing building and constructing a new one”. | |

| The subject represents a legal, conforming improvement relative to current zoning restrictions. No redevelopment of the site would provide a greater return to the land. Based on the fact that the potential income associated with the existing improvements provide a fair return to the land with residual income to the improvements, the highest and best use of the subject, as improved, is its current use. | ||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 32 |

| VALUATION PROCESS | ||

| Introduction | There are three traditional approaches that can be employed in establishing the market value of the subject property. In practice, an approach to value is included or omitted based on the property type and the quality and quantity of information available in the marketplace. These approaches and their applicability to the valuation of the subject are summarized as follows. | |

| Income Approach | The Income Capitalization Approach is based on the premise that value is derived by converting anticipated benefits into property value. Anticipated benefits include the present value of the net income and the present value of the net proceeds resulting from the re-sale of the property. | |

| There are two methods of accomplishing this: (1) direct capitalization of a single year’s income by an overall capitalization rate and; (2) the discounted cash flow in which the annual cash flows and reversionary value are discounted to a present value for the remainder of the property’s productive life or over a reasonable holding (ownership) period. | ||

| The subject property has an adequate operating history to determine the income-producing capabilities over the near future. In addition, performance levels of competitive properties serve as an adequate check as to the reasonableness of the subject property’s actual performance. As such, the income capitalization approach is utilized in this appraisal. | ||

| Sales Comparison Approach | The sales comparison approach is an estimate of value based upon a process of comparing recent sales of similar properties in the surrounding or competing areas to the subject property. Inherent in and central to this approach is the principle of substitution. This comparative process involves judgment as to the similarity of the subject property and the comparable sales with respect to many value factors such as location, contract rent levels, quality of construction, reputation and prestige, age and condition and the interest transferred, among others. The value estimated through this approach represents the probable price at which the subject property would be sold by a willing seller to a willing and knowledgeable buyer as of the date of value. | |

| The reliability of this technique is dependent upon the availability of comparable sales data, the verification of the sales data, the degree of comparability and extent of adjustment necessary for differences and the absence of atypical conditions affecting the individual sales prices. Research revealed adequate sales activity to form a reasonable estimation of value via this approach. | ||

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 33 |

| Cost Approach | The application of the cost approach is based on the principle of substitution. This principle may be stated as follows: no one is justified in paying more for a property than the cost to develop a substitute property of equivalent desirability and utility. In the case of a new building, no deficiencies in the building should exist. The Cost Approach is typically only a reliable indicator of value for (a) new properties; (b) special use properties; and (c) where the cost of reproducing the improvements is easily and accurately quantified and there is no external obsolescence. In all instances, the issue of an appropriate entrepreneurial profit—the reward for undertaking the risk of construction—remains a highly subjective factor. | |

| Investors are generally not buying, selling, or lending with reliance placed on the methodology of the Cost Approach to establish value. Furthermore, based on the age of the improvements and the legal non-conforming zoning of the subject property, the Cost Approach would lend little insight into the market value of the property. Accordingly, the Cost Approach has been excluded from the scope of this appraisal. | ||

| Reconciliation | The final step in the appraisal process is to reconcile the various value indications into a single final estimate. Each approach is reviewed in order to determine its appropriateness relative to the subject. The accuracy of the data available and the quantity of evidence are weighted in each approach. The resulting estimate represents the subject property’s market value as defined in the appraisal. | |

KTR Real Estate Advisors LLC

| Peak at Vinings | January 28, 2013 | |

| Atlanta, Georgia | Page 34 |

| INCOME CAPITALIZATION APPROACH | ||

| Introduction | The Income Capitalization Approach is based on the theory that value is the present worth of future benefits. The future benefits of ownership consist of the present worth of the net income which will accrue to the owner of the property, plus the present value of the net proceeds resulting from the eventual disposition of the property. The two most commonly used techniques of converting net income into value in the Income Capitalization Approach are Direct Capitalization and the Discounted Cash Flow Analysis. | |

| The Direct Capitalization method is considered most relevant and has been processed. Direct Capitalization is a method utilized to convert a single year’s estimate of net income (before debt service) into an indication of value by the use of an Overall Capitalization Rate. | ||

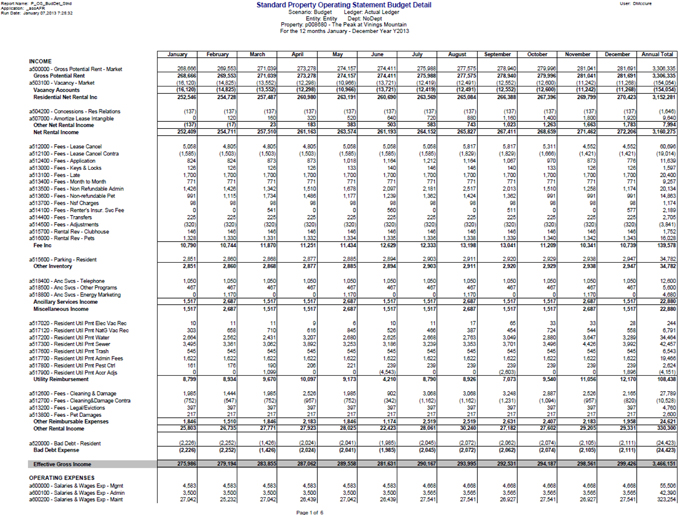

Revenue Analysis Potential Gross Income | The potential gross income has been calculated to be $280,460 per month or $3,365,520 for the appraised year based on the analysis and conclusions derived in the Apartment Market Analysis section. | |

| Loss to Lease/Excess Rent | Loss to lease considers a loss in income due to leases in effect, whereby effective rental rates are lower than asking or market rental rates. Conversely when rental rates are higher than asking, or market rental rates there is excess rent. In the case of the subject property, the loss to lease also accounts partially for concessions that are offered in the form of reduced rent. | |