SCHEDULE 14A

(Rule 14A-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

¨ Preliminary Proxy Statement ¨ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

x Definitive Proxy Statement

¨ Definitive Additional Materials

¨ Soliciting Material Pursuant to Rule 14a-11(c) or Rule 14a-12.

DaVita, Inc.

(Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

¨ | Fee paid previously with preliminary materials. |

¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

1

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

April 11, 2002

TO OUR STOCKHOLDERS:

We will hold our 2002 annual meeting of the stockholders of DaVita Inc., a Delaware corporation, on Thursday, April 11, 2002 at 9:30 a.m., Los Angeles time, at the Torrance Marriott, 3635 Fashion Way, Torrance, California 90503. As further described in the accompanying proxy statement, at this meeting we will:

| (1) | Elect seven directors to our board of directors to serve for a term of one year or until their successors are duly elected and qualified; |

| (2) | Consider and act upon a proposal to approve the proposed DaVita Inc. 2002 Equity Compensation Plan; and |

| (3) | Transact other business as may properly come before the meeting or any meetings held upon adjournment of the meeting. |

Our board of directors has fixed the close of business on March 11, 2002 as the record date for the determination of stockholders entitled to vote at the meeting or any meetings held upon adjournment of the meeting. Only record holders of our common stock at the close of business on that day will be entitled to vote. A copy of our 2001 annual report to stockholders is enclosed with this notice, but is not part of the proxy soliciting material.

We invite you to attend the meeting and vote in person.If you cannot attend, to assure that you are represented at the meeting, please sign and return the enclosed proxy card as promptly as possible in the enclosed postage prepaid envelope. If you attend the meeting, you may vote in person, even if you previously returned a signed proxy.

| By | order of the board of directors, |

| Steven J. Udicious |

| Vice President, Secretary |

| and General Counsel |

Torrance, California

March 18, 2002

PROXY STATEMENT

GENERAL INFORMATION

We are sending you this proxy statement on or about March 18, 2002 in connection with the solicitation of proxies by our board of directors. The proxies are for use at our 2002 annual meeting of stockholders, which we will hold on Thursday, April 11, 2002, at 9:30 a.m., Los Angeles time, at the Torrance Marriott, 3635 Fashion Way, Torrance, California 90503. The proxies will remain valid for use at any meetings held upon adjournment of that meeting. The record date for the meeting is the close of business on March 11, 2002. All holders of record of our common stock on the record date are entitled to notice of the meeting and to vote at the meeting and any meetings held upon adjournment of that meeting. Our principal executive offices are located at 21250 Hawthorne Boulevard, Torrance, California 90503, and our telephone number is (310) 792-2600.

A proxy form is enclosed. Whether or not you plan to attend the meeting in person, please date, sign and return the enclosed proxy as promptly as possible, in the postage prepaid envelope provided, to ensure that your shares will be voted at the meeting. You may revoke your proxy at any time prior to its use by filing with our secretary an instrument revoking it or a duly executed proxy bearing a later date or by attending the meeting and voting in person.

Unless you instruct otherwise in the proxy, any proxy, if not revoked, will be voted at the meeting:

| • | for our board’s slate of nominees; |

| • | to approve the DaVita Inc. 2002 Equity Compensation Plan; and |

| • | as recommended by our board with regard to all other matters, in its discretion. |

Our only voting securities are the outstanding shares of our common stock. At the record date, we had approximately 82,500,000 shares of common stock outstanding and approximately 2,500 stockholders of record. If the stockholders of record present in person or represented by their proxies at the meeting hold at least a majority of our outstanding shares of common stock, a quorum will exist for the transaction of business at the meeting. Stockholders of record who abstain from voting, including brokers holding their customers’ shares who cause abstentions to be recorded, are counted as present for quorum purposes.

For each share of common stock you hold on the record date, you are entitled to one vote on each matter that we will consider at this meeting. You are not entitled to cumulate your votes.

Brokers holding shares of record for their customers generally are not entitled to vote on some matters unless their customers give them specific voting instructions. If the broker does not receive specific instructions, the broker will note this on the proxy form or otherwise advise us that it lacks voting authority. The votes that the brokers would have cast if their customers had given them specific instructions are commonly called “broker non-votes.”

The voting requirements for the proposals we will consider at the meeting are:

| • | Election of directors. The seven candidates who receive the highest number of affirmative votes will be elected. Votes against a candidate and votes withheld from voting for a candidate will have no effect on the election. |

2

| • | Approval of the DaVita Inc. 2002 Equity Compensation Plan. A majority of the votes cast on this proposal by the holders of shares of our common stock present, or represented, and entitled to vote at the annual meeting must approve this proposed plan and the total votes cast on this proposal must represent over fifty percent of all shares entitled to vote on this proposal. Abstentions count as votes cast and have the effect of a vote against the proposal. Broker non-votes are not counted as votes cast and will have no effect on the outcome. |

We will pay for the cost of preparing, assembling, printing and mailing this proxy statement and the accompanying form of proxy to our stockholders, as well as the cost of soliciting proxies relating to the meeting. We may request banks and brokers to solicit their customers who beneficially own our common stock listed of record in names of nominees. We will reimburse these banks and brokers for their reasonable out-of-pocket expenses regarding these solicitations. We have also retained Georgeson Shareholder, or Georgeson, to assist in the distribution and solicitation of proxies and to verify records related to the solicitation at a fee of $9,500 plus expenses. Georgeson and our officers, directors and employees may supplement the original solicitation by mail of proxies by telephone, facsimile, e-mail and personal solicitation. We will pay no additional compensation to our officers, directors and employees for these activities. We will indemnify Georgeson against liabilities and expenses arising in connection with the proxy solicitation, including liabilities under the federal securities laws, unless caused by Georgeson’s gross negligence or willful misconduct.

3

PROPOSAL NO. 1

ELECTION OF DIRECTORS

At the meeting, you will elect seven directors to serve for a term of office consisting of the coming year or until their respective successors are elected and qualified. Our board has nominated Kent J. Thiry, Richard B. Fontaine, Peter T. Grauer, C. Raymond Larkin, Jr., John M. Nehra, Nancy-Ann DeParle, and William L. Roper for election as directors. All are current members of our board. Each nominee has consented to being named in this proxy statement as a nominee and has agreed to serve as a director if elected.

The persons named as proxies in the accompanying form of proxy have advised us that at the meeting they intend to vote the shares covered by the proxies for the election of the nominees named above. If one or more of the nominees are unable to serve, or for good cause will not serve, the persons named as proxies may vote for the election of the substitute nominees that our board may propose. The accompanying form of proxy contains a discretionary grant of authority with respect to this matter. The persons named as proxies may not vote for a greater number of persons than the number of nominees named above.

No arrangement or understanding exists between any nominee and any other person or persons pursuant to which any nominee was or is to be selected as a director or nominee. None of the nominees has any family relationship with any other nominee or with any of our executive officers.

Information concerning members of our board of directors

Name | Age | Position | ||

| Kent J. Thiry | 46 | Chairman of the Board and Chief Executive Officer | ||

| Richard B. Fontaine | 58 | Director | ||

| Peter T. Grauer | 56 | Director | ||

| C. Raymond Larkin, Jr. | 53 | Director | ||

| John M. Nehra | 53 | Director | ||

| Nancy-Ann DeParle | 45 | Director | ||

| William L. Roper | 53 | Director |

Kent J. Thirybecame our chairman of the board and chief executive officer on October 18, 1999. From June 1997 until he joined us, Mr. Thiry served as chairman of the board and chief executive officer of Vivra Holdings, Inc., which was formed to operate the non-dialysis business of Vivra Incorporated, or Vivra, after Gambro AB acquired the dialysis services business of Vivra in June 1997. At the time, Vivra was the second largest provider of dialysis services in the United States. From September 1992 to June 1997, Mr. Thiry was the president and chief executive officer of Vivra. From April 1992 to August 1992, Mr. Thiry served as president and co-chief executive officer of Vivra, and from September 1991 to March 1992, as president and chief operating officer of Vivra. From 1983 to 1991, Mr. Thiry was associated with Bain & Company, first as a consultant, and then as vice president. Mr. Thiry is also a director of Oxford Health Plans, Inc.

Richard B. Fontainehas been one of our directors since November 1999. Mr. Fontaine has been an independent health care consultant since 1992. Mr. Fontaine has also been an adjunct instructor at Westminster College since 1992. From June 1995 to September 1995, he served as interim chief executive officer of Health Advantage, Inc., a subsidiary of Vivra Specialty Partners, Inc. In 1993, he served as interim chief executive officer of Vivocell Therapy, Inc. From 1988 to 1992, he served as senior vice president of CRamp;R Incorporated. From 1984 to 1988, he served as vice president, business development, of Caremark, Inc. Mr. Fontaine is also a director of Celeris Corp.

4

Peter T. Grauerhas been one of our directors since August 1994. Mr. Grauer has been chairman of the board since April 2001, and president and treasurer since March 2002, of Bloomberg, Inc. From November 2000 until March 2002, Mr. Grauer was a managing director of Credit Suisse First Boston. From September 1992 until November 2000, upon the merger of Donaldson, Lufkin & Jenrette, or DLJ, into Credit Suisse First Boston, Mr. Grauer was a managing director of DLJ Merchant Banking. From April 1989 to September 1992, he was co-chairman of Grauer & Wheat, Inc., an investment firm specializing in leveraged buyouts.

C. Raymond Larkin, Jr.has been one of our directors since December 1999. Mr. Larkin has been a principal of 3x NELL, which invests in and provides consulting services to the medical device, biotechnology and pharmaceutical industries, since July 1998. From 1983 to March 1998, he held various executive positions with Nellcor Incorporated, a medical products company, for which he served as president and chief executive officer from 1989 until August 1995, when he became president and chief executive officer of Nellcor Puritan Bennett Incorporated upon the merger of Nellcor Incorporated with Puritan-Bennett Corporation. Mr. Larkin is also a director of Applied Medical Devices, Inc., ArthroCare Corporation, Cerus Corporation and Vital Signs Inc.

John M. Nehrahas been one of our directors since November 2000. Mr. Nehra has been affiliated with New Enterprise Associates, a venture capital firm, since 1989, including, since 1993, as general partner of several of its affiliated venture capital limited partnerships. Mr. Nehra has also been managing general partner of Catalyst Ventures, a venture capital firm, since 1989. Mr. Nehra is also a director of Aradigm Corporation, Celeris Corp., and Iridex Corporation.

Nancy-Ann DeParlehas been one of our directors since May 2001. Ms. DeParle served as the Administrator of the Health Care Financing Administration, or HCFA, from 1997 until 2000. From 1993 until joining HCFA, Ms. DeParle was Associate Director for Health and Personnel at the White House Office of Management and Budget. She is currently a senior advisor with JP Morgan Partners, LLC, a private equity firm, and an adjunct professor at the Wharton School of the University of Pennsylvania. Ms. DeParle is also a director of Cerner Corporation, Guidant Corporation, Specialty Laboratories, Inc. and Triad Hospitals, Inc.

William L. Roper has been one of our directors since May 2001. Dr. Roper served as the administrator of HCFA, from 1986 to 1989. He is currently dean of the School of Public Health at The University of North Carolina at Chapel Hill (UNC). He is also a professor of health policy and administration in the School of Public Health and a professor of pediatrics in the School of Medicine at UNC. Before joining UNC in 1997, Dr. Roper served as senior vice president of Prudential Health Care. He also served as Director of the Centers for Disease Control and Prevention from 1990 to 1993 and on the senior White House staff in 1989 and 1990. Dr. Roper is also a director of Luminex Corporation.

Information regarding our board of directors and its committees

Our board of directors met eleven times during 2001. Each of our directors attended 75% or more of the total number of meetings of the board and meetings of the committees of the board on which he or she served during 2001.

From January 2001 until June 2001 our audit committee consisted of Maris Andersons, C. Raymond Larkin, Jr. and Shaul G. Massry. Mr. Andersons was the chairperson of the audit committee until June 2001. In June 2001, Mr. Andersons’ and Mr. Massry’s term of office on the board of directors expired. From June 2001 through December 2001 our audit committee consisted of C. Raymond Larkin, Jr., Nancy-Ann DeParle and John M. Nehra. Since June 2001, Mr. Larkin has been the chairperson of the audit committee. Each of the members of our audit committee was independent in accordance with the listing standards of the New York Stock Exchange. Mr. Andersons received consulting fees from us in 1999 and 2000 during a period when we did not have a chief financial officer. Notwithstanding Mr. Andersons’ performance of these consulting services, our board of directors determined that Mr. Andersons’ continued participation on the audit committee was in our best interests. Our board of directors has adopted a written charter for our audit committee. Our audit committee

5

monitors the integrity of our financial reporting process and systems of internal accounting and financing controls, monitors the independence and performance of our independent auditors and internal auditing department and provides an avenue of communication among the independent auditors, management, the internal auditing department and our board of directors. The audit committee also recommends the selection of our independent auditors and determines the appropriateness of the auditor’s overall fees. The audit committee met seven times during 2001.

In 2001, our compensation committee consisted of Richard B. Fontaine, C. Raymond Larkin, Jr., and John M. Nehra. Mr. Fontaine is the chairperson of the compensation committee. Our compensation committee reviews the performance of our chief executive officer and other executives and makes specific recommendations and decisions regarding their compensation, with the goal of ensuring that our compensation system for our executives, as well as our philosophy for compensation for all employees, is aligned with the long term interests of our stockholders. The compensation committee also establishes policies relating to the compensation of our executive officers and other key employees that further this goal. The compensation committee met twice during 2001.

From January 2001 until May 2001 our compliance committee consisted of Thomas A. Scully and Shaul G. Massry. Mr. Scully was the chairperson of the compliance committee until May 2001. In May 2001, Mr. Scully resigned from our board of directors upon being appointed the Administrator of HCFA (subsequently renamed the Centers for Medicare & Medicaid Services, or CMS). From June 2001 through December 2001 our compliance committee consisted of John M. Nehra and William L. Roper. Since June 2001, Mr. Nehra has been the chairperson of our compliance committee. Our compliance committee oversees and monitors the effectiveness of our corporate compliance program, reviews significant compliance risk areas and the steps management is taking to monitor, control and report risk exposures and meets regularly with our chief compliance officer and management compliance committee. The compliance committee met four times during 2001.

Compensation of directors

Directors who are our employees or officers do not receive compensation for service on our board of directors or any committee of the board. Each of our directors who is not one of our officers or employees is entitled to receive $24,000 per year paid quarterly in arrears (half in cash and half in deferred stock units that must be held for one year), and additional cash compensation of $4,000 for each board meeting attended in person and $2,000 for each meeting held via telephone conference that lasts more than one and one half hours. For committee meetings, additional cash compensation of $2,000 per meeting is paid, whether attended in person or by telephone. No committee meeting fees are paid for committee meetings held on regular board meeting dates.

Committee chairpersons and the lead independent director also receive an additional $20,000 per year paid quarterly in arrears (half in cash and half in deferred stock units that must be held for one year). If the lead independent director also serves as a committee chairperson, he or she will only receive a total additional retainer of $20,000 (i.e., not $40,000) per year. C. Raymond Larkin, Jr. serves as our lead independent director. We also reimburse our directors for their reasonable out-of-pocket expenses in connection with their travel to and attendance at meetings of the board.

In addition, each director who is not one of our officers or employees is entitled to receive options to purchase 8,000 shares of our common stock for each year the director is elected to serve on our board, issued upon election or re-election to the board. The director options have an exercise price equal to the fair market value of our common stock on the date of grant and vest over two years at an annual rate of 50% beginning on the first anniversary of the date of grant, with acceleration of vesting upon a change in control.

Committee chairpersons and the lead independent director also receive additional options to purchase 10,000 shares of our common stock for each year of service in these roles, issued upon the date of the annual

6

meeting. The committee chairpersons and lead independent director options have an exercise price equal to the fair market value of our common stock on the date of grant and generally vest over three years at an annual rate of 33 1/3% beginning on the first anniversary of the date of grant, with acceleration of vesting upon a change in control. Vesting of the committee chairpersons and lead independent director options continues so long as the director continues to serve on our board. If the lead independent director also serves as a committee chairperson, he or she will receive a total additional option grant of 10,000 shares (i.e., not 20,000 shares).

Each new member of our board receives a one-time grant of options to purchase 15,000 shares of our common stock issued upon initial appointment to our board, priced at the fair market value of our common stock on the date of grant and vesting over four years at an annual rate of 25% beginning on the first anniversary of the date of grant.

All of the foregoing options have a five year term, and vest immediately in the event of a change in control.

In accordance with the foregoing, in 2001 Messrs. Fontaine, Larkin, and Nehra each received options to purchase 18,000 shares, Ms. DeParle and Dr. Roper each received options to purchase 23,000 shares, and Mr. Grauer received options to purchase 8,000 shares.

7

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL

OWNERS AND MANAGEMENT

The following table sets forth information regarding the ownership of our common stock as of March 11, 2002 by (a) all those persons known by us to own beneficially more than 5% of our common stock, (b) each of our directors and executive officers, and (c) all directors and executive officers as a group. Unless otherwise set forth in the following table, the address of each beneficial owner is 21250 Hawthorne Boulevard, Torrance, California 90503. Except as otherwise noted in the “Certain Relationships and Related Transactions” section of this proxy statement, we know of no agreements among our shareholders which relate to voting or investment power over our common stock or any arrangement the operation of which may at a subsequent date result in a change of control of us.

Name of beneficial owner | Number of shares beneficially owned | Percentage of shares beneficially owned | |||

| FMR Corp. (1) | 6,499,157 | 7.9 | % | ||

82 Devonshire Street Boston, Massachusetts 02109 | |||||

| T. Rowe Price Associates, Inc. (2) | 6,431,739 | 7.8 | % | ||

100 E. Pratt Street Baltimore, Maryland 21202 | |||||

| Barclays Global Investors, N.A. and affiliates (3) | 4,745,679 | 5.8 | % | ||

45 Fremont Street San Francisco, California 94105 | |||||

| Kent J. Thiry (4) | 911,666 | 1.1 | % | ||

| Joseph C. Mello (5) | 90,000 | * | |||

| Richard K. Whitney (6) | 246,381 | * | |||

| Gary W. Beil (7) | 140,500 | * | |||

| Charles J. McAllister, M.D. (8) | 43,166 | * | |||

| Steven J. Udicious (9) | 60,331 | * | |||

| Richard B. Fontaine (10) | 49,250 | * | |||

| Peter T. Grauer (11) | 112,750 | * | |||

| C. Raymond Larkin Jr. (12) | 34,250 | * | |||

| John M. Nehra (13) | 14,250 | * | |||

| Nancy-Ann DeParle | 0 | * | |||

| William L. Roper | 0 | * | |||

| All directors and executive officers as a group (12 persons) (14) | 1,702,544 | 2.0 | % |

| * | Amount represents less than 1% of our common stock. |

| (1) | Based upon information contained in a Schedule 13G filed with the SEC on February 14, 2002. FMR Corp. is the beneficial owner of these shares through its control of the following entities: Fidelity Management & Research Company, beneficial owner of 5,487,731 shares; Fidelity Management Trust Company, beneficial owner of 915,146 shares; and Fidelity International Limited, beneficial owner of 96,280 shares. These shares include a total of 4,672,957 shares issuable upon conversion of convertible subordinated |

8

| notes. Mr. Edward C. Johnson 3d is the chairman of FMR Corp. By virtue of his position as chairman of FMR Corp. and his and Abigail Johnson’s ownership of FMR Corp., they may be deemed to have the sole power to dispose of and vote the 5,487,731 shares owned by Fidelity Management & Research Company. They may be deemed to have the sole power to dispose of 915,146 shares and the sole power to vote 576,919 of the shares owned by Fidelity Management Trust Company. By virtue of Mr. Johnson’s position as chairman of Fidelity International Limited, he may be deemed to have the sole power to dispose of and vote the 96,280 shares owned by Fidelity International Limited. |

| (2) | Based upon information contained in a Schedule 13G/A filed with the SEC on February 22, 2002. These shares are owned by various individual and institutional investors which T. Rowe Price Associates, Inc. serves as investment adviser with power to direct investments and/or sole power to vote the shares. These shares include a total of 393,506 shares issuable upon conversion of convertible subordinated notes. T. Rowe Price Associates, Inc. has the sole power to vote 778,600 of the shares and sole power to dispose of 6,309,825 of the shares. |

| (3) | Based upon information contained in a Schedule 13G filed with the SEC on February 11, 2002. Barclays Global Investors, N.A. is the beneficial owner of 4,538,469 shares with the sole power to vote 4,147,439 the shares and the sole power to dispose of 4,538,469 of the shares. Barclays Global Fund Advisors is the beneficial owner of 174,507 shares with the sole power to vote and dispose of the shares. Barclays Global Investors, LTD. is the beneficial owner of 31,121 shares with the sole power to vote and dispose of the shares. Barclays Fund Limited is the beneficial owner of 1,582 shares with the sole power to vote and dispose of the shares. |

| (4) | Includes 49,500 shares held in a family trust and 858,000 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (5) | Includes 90,000 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (6) | Includes 245,152 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (7) | Includes 100,500 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (8) | Includes 42,500 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (9) | Includes 60,000 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (10) | Includes 34,250 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (11) | Includes 106,750 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (12) | Includes 34,250 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (13) | Includes 4,250 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

| (14) | All directors and executive officers in office on March 11, 2002. Includes 1,575,652 shares issuable upon the exercise of options which are exercisable as of, or will become exercisable within 60 days after, March 11, 2002. |

9

Information concerning our executive officers

Name | Age | Position | ||

| Kent J. Thiry | 46 | Chairman of the Board and Chief Executive Officer | ||

| Joseph C. Mello | 43 | Chief Operating Officer | ||

| Richard K. Whitney | 34 | Chief Financial Officer | ||

| Gary W. Beil | 49 | Vice President and Controller | ||

| Charles J. McAllister, M.D. | 54 | Chief Medical Officer | ||

| Steven J. Udicious | 34 | Vice President, Secretary and General Counsel |

Our executive officers are elected by and serve at the discretion of our board of directors. Set forth below is a brief description of the business experience of all executive officers other than Mr. Thiry, who is also a director and whose business experience is set forth above in the “Information concerning members of our board of directors” section of this proxy statement.

Joseph C. Mellobecame our chief operating officer in June 2000. Prior to joining us, from April 1998, Mr. Mello served as president and chief executive officer of Vivra Asthma & Allergy. From August 1994 to April 1998, Mr. Mello held various positions with MedPartners, Inc., including senior vice president/chief operating officer—southeastern region from March 1997 to April 1998. Prior to joining MedPartners, Mr. Mello was a partner with KPMG LLP, from 1984 to 1994. Mr. Mello is a director of Radiologix, Inc.

Richard K. Whitneybecame our chief financial officer in February 2000. From September 1998 until his appointment as chief financial officer, Mr. Whitney served as vice president and general manager of our international operations. Mr. Whitney joined us in June 1995 and has also served as director of corporate development and vice president of corporate development. Prior to joining us, Mr. Whitney was associated with RFE Investment Partners, a private equity investment firm, and Deloitte & Touche.

Gary W. Beilhas been our vice president and controller since November 1999. Prior to joining us, from April 1999 to October 1999, Mr. Beil was an independent business consultant. From March 1996 to March 1999, Mr. Beil served as vice president and controller of The Boeing Company, and from 1979 to 1996 held a variety of divisional and corporate finance positions with The Boeing Company.

Charles J. McAllister, M.D., a nephrologist, became our chief medical officer in July 2000. From 1977 until joining us, Dr. McAllister was in private practice in Florida, including, from 1978, as medical director of two dialysis centers. Dr. McAllister also served as vice president of clinical affairs for Vivra Renal Care, the dialysis services business of Vivra, from 1992 until June 1997, when Gambro acquired Vivra Renal Care. Dr. McAllister continued as vice president of clinical affairs for Gambro until December 1998.

Steven J. Udiciousbecame our vice president, secretary and general counsel in April 2000. Mr. Udicious served as our assistant general counsel from February 1998 until February 2000, when he became secretary and acting general counsel. Mr. Udicious served as assistant general counsel of Renal Treatment Centers, Inc., or RTC, from March 1997 until RTC’s merger with us in February 1998. Prior to joining RTC, Mr. Udicious was associated with the law firm Duane, Morris & Heckscher, LLP in Philadelphia, Pennsylvania.

None of the executive officers has any family relationship with any other executive officer or with any of our directors.

10

Section 16(a) beneficial ownership reporting compliance

Section 16(a) of the Exchange Act requires “insiders,” including our executive officers, directors and beneficial owners of more than 10% of our common stock, to file reports of ownership and changes in ownership of our common stock with the Securities and Exchange Commission and the New York Stock Exchange, and to furnish us with copies of all Section 16(a) forms they file. Based solely on our review of the copies of such forms received by us, or written representations from our insiders, we believe that our insiders complied with all applicable Section 16(a) filing requirements during 2001. However, Peter T. Grauer failed to file a Form 5 in 1999 that should have disclosed an option grant that he received in February 1998. Subsequently, Mr. Grauer reported the option grant on a Form 5 that was filed in February 2002.

11

EXECUTIVE COMPENSATION

The following table sets forth the compensation for each of the fiscal years in the three-year period ended December 31, 2001 of the following persons:

| • | Each individual who served as our chief executive officer or acted in a similar capacity during 2001; and |

| • | Our four most highly compensated executive officers other than our chief executive officer at December 31, 2001. |

Compensation is presented only for the years in which each person was an executive officer, and may include partial year salary and pro rata bonus payments, based upon the officer’s start date.

Summary Compensation Table

Long Term Compensation | |||||||||||||||||

Annual Compensation | Awards | Payouts | |||||||||||||||

Name and Principal Position | Year | Salary ($) | Bonus ($)(1) | Other Annual Compensation ($) | Restricted Stock Award(s) ($) | Securities Underlying Options (#) | LTIP Payouts ($) | All Other Compensation ($) | |||||||||

| Kent J. Thiry | 2001 | 600,000 | 735,000 | — | 1,250,000 | (2) | 300,000 | — | 5,769(3) | ||||||||

| Chairman of the Board | 2000 | 499,980 | 250,000 | — | — | 1,300,000 | — | 5,384(4) | |||||||||

and Chief Executive Officer | 1999 | 83,074 | — | — | — | 500,000 | — | — | |||||||||

| Joseph C. Mello | 2001 | 325,000 | 120,000 | — | 400,000 | (5) | 50,000 | — | 10,744(6) | ||||||||

| Chief Operating Officer | 2000 | 108,358 | — | — | — | 500,000 | — | — | |||||||||

| Richard K. Whitney | 2001 | 289,241 | 268,938(7) | — | 300,000 | (8) | — | — | 3,000(9) | ||||||||

| Chief Financial Officer | 827,500(10) | ||||||||||||||||

| 2000 | 270,769 | 95,333(11) | — | — | 500,000 | — | 16,300(12) | ||||||||||

| Gary W. Beil | 2001 | 154,500 | 52,500 | — | — | — | — | 217,328(13) | |||||||||

| Vice President and Controller | 2000 | 151,038 | 7,500 | — | — | 130,000 | — | 41,615(14) | |||||||||

| Charles J. McAllister, M.D. | 2001 | 200,000 | 16,700 | — | — | 30,000 | — | 7,770(15) | |||||||||

| Chief Medical Officer | 2000 | 86,153 | — | — | — | 160,000 | — | — | |||||||||

| (1) | Bonuses are reported in the year in which they were paid. The report of the compensation committee discusses the determination of bonuses to be paid in 2002 based on corporate and individual performance in 2001. |

| (2) | Consists of 81,168 shares of deferred stock units granted on February 13, 2001, vesting in three equal annual installments beginning on February 13, 2002. The value of such shares is based on the closing price of our common stock on the New York Stock Exchange on February 13, 2001. As of December 31, 2001, these shares were valued at $1,984,558 based on the closing price of our common stock on December 31, 2001. |

| (3) | Consists of contributions to our profit sharing plan of $5,769. |

| (4) | Consists of contributions to our profit sharing plan of $5,384. |

12

| (5) | Consists of 25,974 shares of deferred stock units granted on February 13, 2001, vesting in three equal annual installments beginning on February 13, 2002. The value of such shares is based on the closing price of our common stock on the New York Stock Exchange on February 13, 2001. As of December 31, 2001, these shares were valued at $635,064 based on the closing price of our common stock on December 31, 2001. |

| (6) | Consists of payment for accrued paid time off of $6,994 and contributions to our profit sharing plan of $3,750. |

| (7) | Includes $60,938 in bonuses required to be paid in 2001 under a key employee retention program implemented in September 1999. |

| (8) | Consists of 19,482 shares of deferred stock units granted on February 13, 2001, vesting in three equal annual installments beginning on February 13, 2002. The value of such shares is based on the closing price of our common stock on the New York Stock Exchange on February 13, 2001. As of December 31, 2001, these shares were valued at $476,335 based on the closing price of our common stock on December 31, 2001. |

| (9) | Consists of contributions to our profit sharing plan of $3,000. |

| (10) | Entire amount is a one-time bonus paid in 2001, which was determined pursuant to a pre-established formula based on the proceeds realized from, and timing of, the sale of our international operations. This formula was agreed to with Mr. Whitney prior to our offering the chief financial officer position to him. |

| (11) | Includes $82,500 in bonuses required to be paid in 2000 under a key employee retention program implemented in September 1999. |

| (12) | Consists of payment for a waiver of medical insurance of $1,000, payment for accrued paid time off of $12,500, and contributions to our profit sharing plan of $2,800. |

| (13) | Consists of payment for accrued paid time off of $15,545, contributions to our profit sharing plan of $1,783, and accrued post-retirement benefits of $200,000, vesting in four equal annual installments beginning in January 2002. |

| (14) | Consists of a relocation allowance of $40,000 and contributions to our profit sharing plan of $1,615. |

| (15) | Consists of payment for accrued paid time off of $6,847 and contributions to our profit sharing plan of $923. |

13

The following table sets forth information concerning options granted to each of the named executive officers during 2001:

Option Grants in Last Fiscal Year

Individual Grants | |||||||||||

Name | Number of Securities Underlying Options Granted (#)(1) | % of Total Options Granted to Employees in Fiscal Year | Exercise Or Base Price ($/Sh) | Expiration Date | Grant Date Present Value ($)(2) | ||||||

| Kent J. Thiry | 300,000 | 18.6 | % | 15.40 | 2/13/06 | 1,686,060 | |||||

| Joseph C. Mello | 50,000 | 3.1 | % | 15.40 | 2/13/06 | 281,010 | |||||

| Richard K. Whitney | — | — | — | — | — | ||||||

| Gary W. Beil | — | — | — | — | — | ||||||

| Charles J. McAllister, M.D. | 10,000 | 0.6 | % | 15.40 | 2/13/06 | 56,202 | |||||

| 20,000 | 1.2 | % | 18.10 | 11/2/06 | 127,750 | ||||||

| (1) | All options are nonqualified stock options. The options vest over four year periods at an annual rate of 25% beginning on the first anniversary of the date of grant, with accelerated vesting upon a change of control. |

| (2) | The estimated grant date present value reflected in the above table was determined using the Black-Scholes model. The material assumptions and adjustments incorporated in the Black-Scholes model in estimating the value of the options reflected in the above table include the following: (a) the respective option exercise price for each individual grant, equal to the fair market value of the underlying stock on the date of grant; (b) the exercise of options within three to four years of the date of grant; (c) a risk-free interest rate of 3.84% to 4.72% per annum; (d) annual volatility of 40% calculated using the daily prices of our common stock; and (e) a dividend yield of 0%. The ultimate values of the options will depend on the future market price of our common stock, which cannot be forecasted with reasonable accuracy. The actual value, if any, an optionee will realize upon exercise of an option will depend on the excess of the market value of our common stock over the exercise price on the date the option is exercised. We cannot assure that the value realized by an optionee will be at or near the value estimated by the Black-Scholes model or any other model that may be applied to value the options. |

The following table sets forth information concerning the aggregate number of options exercised by and year-end option values for each of the named executive officers during 2001:

Aggregated Option Exercises in Last Fiscal Year and

Fiscal Year-End Option Values

Number of Securities Underlying Unexercised Options at FY-End | Value of Unexercised In-the-Money Options at FY-End | |||||||

Name | Shares Acquired on Exercise (#) | Value Realized ($)(1) | Exercisable/ Unexercisable (#) | Exercisable/ Unexercisable ($)(2) | ||||

| Kent J. Thiry | 417,000 | 6,780,581 | 658,000/1,025,000 | 12,277,749/16,900,888 | ||||

| Joseph C. Mello | 120,000 | 1,847,418 | 117,500/ 312,500 | 2,220,219/ 5,396,406 | ||||

| Richard K. Whitney | 100,000 | 1,598,419 | 204,167/ 300,000 | 3,851,882/ 6,041,250 | ||||

| Gary W. Beil | 22,000 | 339,508 | 78,000/ 90,000 | 1,553,100/ 1,761,750 | ||||

| Charles J. McAllister, M.D. | 40,000 | 479,735 | 40,000/ 110,000 | 683,000/ 1,583,500 |

| (1) | Value realized upon exercise is determined by subtracting the exercise price from the closing price for our common stock on the date of exercise as reported by the New York Stock Exchange or, for same-day sales, from the actual sale price, and multiplying the remainder by the number of shares of common stock purchased. |

| (2) | Year-end value is determined by subtracting the exercise price from the fair market value of $24.45 per share, the closing price for our common stock on December 31, 2001, as reported by the New York Stock Exchange, and multiplying the remainder by the number of underlying shares of common stock. |

14

Employment agreements

On October 18, 1999, we entered into an employment agreement with Kent J. Thiry. This agreement was subsequently amended on May 20 and November 28, 2000. As amended, the employment agreement provides for an initial term through December 31, 2001 and will continue thereafter with no further action by either party for successive one-year terms. Mr. Thiry will be entitled to receive a bonus of up to 150% of his base salary each year, based upon our achievement of performance goals agreed upon by our compensation committee. In the event of a constructive discharge following a change in control or a termination for any reason other than material cause or disability, Mr. Thiry will be entitled to a lump sum payment equal to 2.99 times the sum of his then-current base salary and average bonus. Any additional compensation payable to Mr. Thiry upon a change in control would not be reduced by tax obligations possibly imposed by sections 280G or 4999 of the Internal Revenue Code of 1986, as amended.

On June 15, 2000, we entered into an employment agreement with Joseph C. Mello. The agreement provides for employment at will, with either party permitted to terminate the agreement at any time, with or without cause. Mr. Mello is entitled to receive an annual performance bonus with the actual amount decided by our chief executive officer and/or board of directors. In the event of a constructive discharge following a change in control or a termination for any reason other than material cause, Mr. Mello will be entitled to lump sum payment of his then-current base salary and a lump sum payment equal to two times the sum of the normal bonus he received for the immediately preceding calendar year. Any additional compensation payable to Mr. Mello upon a change in control would not be reduced by tax obligations possibly imposed by sections 280G or 4999 of the Internal Revenue Code of 1986, as amended.

On November 29, 1999, we entered into an employment agreement with Gary W. Beil. The agreement provides for employment at will, with either party permitted to terminate the agreement at any time, with or without cause. Mr. Beil was also entitled to a relocation allowance of $40,000, which was paid in 2000. If Mr. Beil is constructively discharged following a change in control, he is entitled to continuation of his then-current base salary for a period of 12 months following termination, reduced by any amounts Mr. Beil earns from other employment during that period.

On July 19, 2000, we entered into an employment agreement with Charles J. McAllister, M.D. The employment agreement provides for an initial term through July 19, 2002. Thereafter, Dr. McAllister’s employment will be at will, with either party permitted to terminate the agreement at any time, with or without cause. Dr. McAllister is entitled to receive a performance bonus of up to $100,000, with the actual amount to be decided by our chief executive officer and/or board of directors. If Mr. Thiry is not our chief executive officer, chairman of the board or chief operating officer at any time prior to July 19, 2002, Dr. McAllister’s term of employment will be for a term of two and one-half years after the occurrence of that event.

On April 19, 2000, we entered into an employment agreement with Steven J. Udicious. The agreement provides for employment at will, with either party permitted to terminate the agreement at any time, with or without cause. We paid relocation expenses of approximately $16,000 for Mr. Udicious in 2000. If, within one year of a change in control, Mr. Udicious is terminated for any reason other than good cause, is no longer our General Counsel, or is no longer performing the job duties and responsibilities of the General Counsel, as those duties and responsibilities existed before the change in control, he is entitled to continuation of his then-current base salary for a period of 12 months following termination, reduced by any amounts Mr. Udicious earns from other employment during that period.

Each of the employment agreements set forth above include provisions limiting the officer’s ability to compete or solicit our employees and customers for a period of one or two years following termination of employment.

15

REPORT OF THE COMPENSATION COMMITTEE

REGARDING COMPENSATION

The compensation committee of our board of directors is currently composed of three independent, nonemployee directors. The committee regularly meets at least once each year and holds additional meetings as required. The compensation committee met twice during 2001.

Compensation objectives

We have two primary objectives in setting executive officer compensation:

| • | Attract and retain outstanding leadership; and |

| • | Align executive compensation with the yearly and long-term goals of the company, with an emphasis on variable (as opposed to fixed) compensation tied to corporate and individual performance. |

Executive compensation

Toward the end of each fiscal year or at the beginning of the following fiscal year, a compensation review is conducted by our Chief Executive Officer for each executive officer. Annual salary and bonus recommendations are then made to and reviewed and voted upon by the compensation committee at the regular year-end meeting.

Philosophically, the compensation committee is attempting to relate executive compensation to those variables over which the individual executive generally has control. Included in the committee’s criteria for approval of recommended salary adjustments, and particularly bonuses and stock option awards, are achievements against annual financial and non-financial targets set at the beginning of the fiscal year for each executive. The financial objectives include improvements in company net operating profit, cost per treatment, EBITDA growth, revenue growth and capital structure. The non-financial objectives include improvements in quality of care, selection and implementation of financial and clinical information systems, enhancement of management performance throughout our organization and advancement of business initiatives supporting our mission to be the provider, partner and employer of choice.

For 2001, incentive awards for executive officers included cash bonuses and stock options. Compensation was weighted heavily toward these variable components, with the long-term objective of shifting to more variable pay for performance.

CEO compensation

Mr. Thiry’s compensation was negotiated with him when he agreed to become our Chairman and Chief Executive Officer in October 1999. His initial compensation was established in his employment agreement, and this agreement provides a framework for future compensation decisions. Within this framework, the compensation committee has considerable latitude in determining future salary, and in setting bonus levels and granting stock options.

Early in 2001, working with an executive compensation consultant, the compensation committee reviewed the compensation of chief executive officers within a peer group constructed by the compensation consultant. This peer group is the same peer group used in the comparative performance graph set forth in this proxy statement. With the consultant’s assistance, the compensation committee compared our performance to that of the other companies in the peer group, and compared Mr. Thiry’s performance to that of the other chief executive officers in the peer group. This comparison, together with evaluations of Mr. Thiry’s performance from the other members of the board and from members of the management team who have worked most closely with Mr. Thiry, were used to determine Mr. Thiry’s compensation moving forward.

16

Under his employment agreement, Mr. Thiry’s annual salary was established at $500,000 subject to annual review for merit increases. As a result of the compensation and performance reviews described above, Mr. Thiry’s salary was increased to $600,000 in February 2001.

Under his employment agreement, Mr. Thiry is entitled to receive a bonus of up to 150% of his base salary each year, based upon our achievement of performance goals agreed upon by the compensation committee. In March 2001, the committee determined that Mr. Thiry would be eligible for a cash bonus of up to $900,000 and a deferred stock unit award of up to $2,400,000, each under the DaVita Executive Incentive Plan. Deferred stock units are deferred compensation paid in shares of our common stock, with the number of shares determined by the market price of our common stock on the date awarded. In order for Mr. Thiry to receive these awards, we had to achieve either EBITDA or earnings per share goals that the committee established for these awards in March 2001. Additionally, the committee retained the discretion, even if any or all of the performance goals were met, to reduce the foregoing awards to the extent it deems appropriate. In February 2002, the committee determined that Mr. Thiry’s bonus for 2001 would consist of a cash award of $855,000 and deferred stock units valued at $700,000 vesting in three equal annual installments beginning in February 2003. The committee also granted Mr. Thiry an additional nonqualified stock option in February 2002 for 600,000 shares, vesting in four equal annual installments beginning in February 2003. The exercise price of this option is $24.40 per share, which was the market value on the grant date.

In making these deferred stock unit and stock option awards, the committee seeks to reward Mr. Thiry commensurate with his performance, to align his incentive compensation more closely with long-term shareholder value, and to provide equity compensation competitive to that of similar-performing chief executive officers and companies in the peer group.

Long-term incentive compensation

To be competitive in attracting and retaining qualified executive officers and to provide them with performance incentives in addition to salary and bonuses, we have adopted equity compensation plans. In approving stock option grant recommendations, the compensation committee considers primarily the impact the executive is expected to have on increasing shareholder value, and recent performance toward specific goals that contribute to that result. Such specific goals differ among executives, but all relate to the speed and effectiveness with which the company is achieving its mission to be the provider, partner and employer of choice.

$1 million pay cap

Section 162(m) of the Internal Revenue Code generally limits the deductibility of compensation paid each year to a publicly-held company’s chief executive officer and to its four most highly paid senior executive officers to $1 million per person. Excluded from the $1 million limitation is compensation that meets pre-established performance criteria or results from the exercise of stock options that meet established criteria. The company’s stock option plans and individual grants of stock options under these plans are structured to meet the criteria that exclude them from the $1 million limitation. The DaVita Executive Incentive Plan is designed to result in cash awards for 2001 and after that qualify as performance-based compensation under Section 162(m). The committee intends to structure performance-based compensation to meet the requirements of Section 162(m), including through awards under the DaVita Executive Incentive Plan, but reserves the right to pay compensation that may not be tax deductible when it would be in our best interests and those of our stockholders.

| CO | MPENSATION COMMITTEE |

| Ric | hard B. Fontaine (Chair) |

| C. | Raymond Larkin, Jr. |

| Joh | n M. Nehra |

17

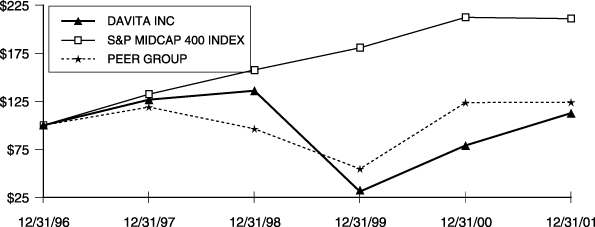

STOCK PRICE PERFORMANCE

The following graph shows a comparison of our cumulative total returns, the Standard & Poor’s MidCap 400 Index and a peer group index that we constructed. The graph assumes that the value of an investment in our common stock and in each such index was $100 on December 31, 1996 and that all dividends have been reinvested. The peer group index consists of the following companies: Advance PCS, Apria Healthcare Group, Caremark RX, Covance, HealthSouth, Laboratory Corp. of America, Lincare Holdings, Omnicare, Priority Healthcare, Quest Diagnostics, Quintiles Transnational and Renal Care Group. The companies in the peer group index are other providers of non-acute, outpatient or related healthcare services whom we believe are most comparable to us. The peer group index is weighted for the market capitalization of each company within the group.

The comparison in the graph below is based solely on historical data and is not intended to forecast the possible future performance of our common stock.

COMPARISON OF FIVE-YEAR

CUMULATIVE TOTAL RETURN AMONG DAVITA INC.,

S&P MIDCAP 400 INDEX, AND PEER GROUP

December 31, 1996 | December 31, 1997 | December 31, 1998 | December 31, 1999 | December 31, 2000 | December 31, 2001 | |||||||||||||

| DaVita Inc. | $ | 100.0 | $ | 126.4 | $ | 135.9 | $ | 30.7 | $ | 78.7 | $ | 112.4 | ||||||

| S&P MidCap 400 Index | $ | 100.0 | $ | 132.2 | $ | 157.5 | $ | 180.7 | $ | 212.3 | $ | 211.0 | ||||||

| Peer Group | $ | 100.0 | $ | 118.8 | $ | 96.3 | $ | 54.6 | $ | 123.5 | $ | 123.9 | ||||||

| Note: | Assumes an initial investment of $100 on December 31, 1996. Total return includes reinvestment of dividends. |

The information contained above under the captions “Report of the compensation committee regarding compensation” and “Stock price performance” will not be considered “soliciting material” or to be “filed” with the Securities and Exchange Commission, nor will that information be incorporated by reference into any future filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent that we specifically incorporate it by reference into a filing.

18

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

Richard K. Whitney, our Chief Financial Officer, received a loan from us in the principal amount of $65,000 in July 1997. In February 2001, Mr. Whitney prepaid this loan in full. Under the terms of the loan, Mr. Whitney was required to pay monthly interest only on the note at a rate of 7% per year from August 1997 through July 2002, at which time the unpaid principal balance was due in full. The loan was secured by all of Mr. Whitney’s options to purchase our common stock. Mr. Whitney used the proceeds of this loan in the purchase of his principal residence.

Joseph C. Mello, our chief operating officer, received a loan from us in the principal amount of $275,000 in December 2000. Mr. Mello is required to pay quarterly interest only on the note from March 2001 through September 2002 at a rate of 7% per year and is current on all such payments through December 31, 2001. Thereafter, Mr. Mello is required to make quarterly interest and principal payments of approximately $15,800 through September 2007, at which time the unpaid principal balance will be repaid in full. The loan is secured by all of Mr. Mello’s options to purchase our common stock. Mr. Mello used the proceeds of this loan in the purchase of his principal residence.

Credit Suisse First Boston, or CSFB, and certain of its affiliates from time to time perform various investment banking and other services for us, for which we pay customary consideration. In addition, affiliates of CSFB are included in the syndicate of lenders under our credit facilities. Peter T. Grauer, who was an affiliate of CSFB until March 2002, serves on our board.

We have entered into indemnity agreements with each of our directors and executive officers, which agreements require us, among other things, to indemnify them against certain liabilities that may arise by reason of their status or service as our directors, officers, employees or agents, other than liabilities arising from conduct in bad faith or which is knowingly fraudulent or deliberately dishonest, and, under certain circumstances, to advance their expenses incurred as a result of proceedings brought against them.

Compensation committee interlocks and insider participation

None of our executive officers or directors serves or has served during our past fiscal year as a member of the board of directors or compensation committee of any other entity which has one or more executive officers serving as a member of our board. Messrs. Fontaine, Larkin and Nehra each served as a member of the compensation committee of our board of directors during 2001.

19

PROPOSAL NO. 2

APPROVAL OF THE

2002 EQUITY COMPENSATION PLAN

At the annual meeting, we will ask our stockholders to approve the DaVita Inc. 2002 Equity Compensation Plan. Our board adopted the 2002 Plan on February 8, 2002, but to become effective upon approval of the 2002 Plan by our stockholders. A summary description of the 2002 Plan is set forth below. This summary description is incomplete and we encourage you to read the full text of the 2002 Plan, which is included with this proxy statement asAppendix A.

Summary description of the 2002 Plan

Purpose of the 2002 Plan. The 2002 Plan allows us to grant to participants options to purchase shares of our common stock. The purpose of the 2002 Plan is to enable us to offer participants an opportunity to acquire an equity interest in us. We believe that this will improve our ability to attract, retain and reward employees, directors and other persons providing services to us. It will also strengthen the mutuality of interests between plan participants and our stockholders by providing those participants with a proprietary interest in pursuing our long-term growth and financial success. Awards under the 2002 Plan will be made solely in the form of the issuance of options; the 2002 Plan does not authorize the issuance of restricted stock.

Eligibility and participation. Generally, all employees, directors, and other persons providing bona fide services to us or any of our subsidiaries are eligible to receive awards of options under the 2002 Plan. However, persons providing services to us only in connection with the offering or sale of securities in a capital raising transaction are not eligible to receive awards. Subject to the adjustments described below, we may not issue more than 1,500,000 shares of common stock pursuant to awards granted to any single participant under the 2002 Plan during any consecutive 24 month period. Currently, we have over 12,000 employees. We have not, however, determined all of the individuals who will receive options or the options that we will grant to any individual or group of individuals.

Administration of the 2002 Plan. Our compensation committee will administer the 2002 Plan. However, our board may delegate to one or more of our officers the power to grant options, within certain limitations. The compensation committee has the authority to interpret the 2002 Plan and to adopt rules and procedures relating to the administration of the 2002 Plan.

Effective date of the 2002 Plan. The 2002 Plan will become effective upon approval of the 2002 Plan by our stockholders. If the 2002 Plan is not so approved, it will terminate, and any options previously granted under the 2002 Plan will be void.

Shares subject to the 2002 Plan. Subject to adjustments to reflect certain corporate events that are described below, we may grant awards with respect to a maximum number of 8,500,000 shares of our common stock under the 2002 Plan plus residual shares of our common stock from the following predecessor plans: 1994 Equity Compensation Plan, 1995 Equity Compensation Plan, 1997 Equity Compensation Plan, and 1999 Equity Compensation Plan. Following stockholder approval of the 2002 Plan, no further grants will be made under these predecessor plans. As of December 31, 2001, options to purchase 8,137,580 shares were outstanding under the predecessor plans and an additional 3,596,165 shares were available for future grants under the predecessor plans. The latter shares would be residual shares immediately available for grants under the 2002 Plan. We may not increase this maximum number of shares without the approval of our stockholders. If an option granted under the 2002 Plan or predecessor plans expires or terminates without having been exercised in full, the shares of common stock remaining unissued under that option will again become available for issuance under the 2002 Plan. We will issue the shares of common stock to be issued under the 2002 Plan directly from our authorized but unissued shares of common stock, or shares that we repurchase.

In the event a participant pays part or all of the exercise price of an option by surrendering shares of common stock that the participant had previously acquired, only the number of shares issuable to the participantin excess of the number that was surrendered will be taken into account for purposes of determining the maximum number of shares that may be issued under the 2002 Plan, both as to that participant and in the

20

aggregate (to all participants). Similarly, shares that are not issued to a participant, but rather, are used to satisfy the income tax withholding obligations upon the exercise of an option arenottaken into account for purposes of determining the maximum number of shares that may be issued under the 2002 Plan.

To the extent permitted by applicable law and the rules of any stock exchange or quotation system on which our common stock is traded or listed, we can also replenish the number of shares available under the 2002 Plan through repurchases of our existing shares, provided that the purchases are effected solely by the use of:

| • | The cash proceeds received by us upon the exercise of options issued under the 2002 Plan or one of the predecessor plans; and |

| • | The actual tax savings achieved by us relating to the exercise of options under the 2002 Plan and the predecessor plans. |

However, the funds available to use for replenishment are limited to amounts relating to those exercises occurringafterthe effective date of the 2002 Plan.

Options. Options granted under the 2002 Plan may be either incentive stock options, or ISOs, or nonqualified stock options, or NQSOs. To date, all of the options we have granted under the predecessor plans have been NQSOs.

We will determine the terms and conditions of each option at the time of grant and include them in a written agreement between the individual and us. The terms of each option will set forth:

| • | the per share exercise price of the option, which will not be less than the closing price of a share of our common stock as reported on the New York Stock Exchange on the date of grant; |

| • | the termination date of the option, which will not be later than five years after the date of grant, except in cases of death or disability; and |

| • | the effect on the option of the termination of the participant’s employment or service (in the case of a non-employee director or independent contractor). |

Each option will also contain other terms and conditions that we may establish. The closing price for our common stock as reported on the New York Stock Exchange on March 11, 2002 was $21.99 per share. Options are not transferable during the individual’s lifetime.

To the extent an option is intended to qualify as an ISO, the option is required to have terms and conditions consistent with the requirements for that treatment under the Internal Revenue Code. ISOs are subject to the following special restrictions:

| • | ISOs may only be granted to our, or our subsidiaries’, employees; |

| • | the exercise price for an ISO must be at least equal to 100%, or 110% in the case of stockholders holding more than 10% of the total combined voting power of all classes of our stock, of the fair market value of our common stock, determined on the date of grant; and |

| • | the aggregate fair market value of the shares of common stock issuable upon exercise of all ISOs granted to a participant, determined at the time each ISO is granted, that become exercisable for the first time during a calendar year cannot exceed $100,000. |

Modification of options. We have the authority to modify any outstanding option as we consider appropriate, including the authority to accelerate the right to exercise any option, and extend or renew any option. However, we may not modify any option in a manner adverse to the participant holding that option without that participant’s consent. Furthermore, we may not reduce the exercise price of any outstanding option, including any repricing effected by issuing replacement stock options for outstanding options that have exercise prices higher than the prevailing market price of the underlying stock, without first obtaining the approval of our stockholders.

21

Adjustments. In connection with certain types of corporate events like stock splits, stock dividends, recapitalizations, reorganizations, mergers, consolidations and spinoffs, we may make appropriate and equitable adjustments to:

| • | the aggregate number and kind of shares for which we can grant options under the 2002 Plan; |

| • | the number and kind of shares covered by outstanding options; and |

| • | the per share exercise price of outstanding options. |

Tax matters. We are obligated to withhold from the compensation of the participants amounts necessary to satisfy the tax withholding obligations arising from the 2002 Plan. If we intend any option to qualify as “qualified performance-based compensation,” as defined in the regulations promulgated under section 162(m) of the Internal Revenue Code, we intend to grant the option in a manner and subject to terms and conditions required for the option to so qualify.

Compliance with securities laws. We are not obligated to issue any common stock under the 2002 Plan if we determine that the issuance would violate applicable state or federal securities laws. We intend to file a registration statement on Form S-8 with the SEC to register the issuance of shares under the 2002 Plan promptly following the approval of the 2002 Plan by our stockholders.

Termination or amendment of the 2002 Plan. Our board of directors may terminate the 2002 Plan at any time. We cannot grant ISOs under the 2002 Plan after February 7, 2012. Termination of the 2002 Plan will not affect the rights of any participant with respect to any option outstanding as of the time of the termination. Our board of directors may also amend the 2002 Plan at any time. However, no amendment may adversely affect the rights of any participant with respect to any outstanding option without that participant’s consent.

Federal income tax consequences of the 2002 Plan

The following general discussion of the principal federal income tax consequences of participation in the 2002 Plan is based on the statutes and regulations existing as of the date of this proxy statement. In addition, participation in the 2002 Plan may have state and local tax consequences. We encourage participants to consult their own advisors with respect to the tax and other consequences of their participation in the 2002 Plan.

Incentive stock options. A participant will not recognize taxable income upon the grant or the exercise of an ISO, and we are not entitled to an income tax deduction as the result of the grant or exercise of an ISO. Any gain or loss resulting from the subsequent sale of shares of common stock purchased upon exercise of an ISO will be long-term capital gain or loss if the sale is made after the later of:

| • | two years from the date of grant of the ISO; or |

| • | one year from the date of exercise of the ISO. |

If a participant sells common stock acquired upon the exercise of an ISO prior to the expiration of both of these periods, the sale will be a “disqualifying disposition” under the federal tax laws. The participant will generally recognize ordinary income in the year of the disqualifying disposition in an amount equal to the difference between the exercise price of the ISO and the fair market value of the shares of our common stock on the date of exercise of the ISO. However, the amount of ordinary income recognized by the participant generally will not exceed the difference between the amount realized on the sale and the exercise price. We will be entitled to an income tax deduction equal to the amount taxable to the participant. Any additional gain recognized by the

22

participant upon the disqualifying disposition will be taxable as long-term capital gain if the shares of common stock have been held for more than one year before the disqualifying disposition or short-term capital gain if the shares of common stock have been held for less than one year before the disqualifying disposition.

The amount by which the fair market value, determined on the date of exercise, of the shares of common stock purchased upon exercise of an ISO exceeds the exercise price will constitute an adjustment to the participant’s income for purposes of the alternative minimum tax in the year that the ISO is exercised.

Nonqualified stock options. As with an ISO, a participant will not recognize taxable income on the grant of an NQSO, and we are not entitled to an income tax deduction as the result of the grant of an NQSO. Unlike an ISO, however, upon the exercise of an NQSO, the participant generally will recognize ordinary income, and we will be entitled to an income tax deduction, in the amount by which the fair market value of the shares of common stock purchased upon exercise, determined as of the date of exercise, exceeds the exercise price. This income is part of the participant’s “wages” for which we are required to withhold federal and state income as well as employment taxes.

Upon the sale of shares of common stock acquired upon the exercise of an NQSO, the participant will recognize capital gain or loss in an amount equal to the difference between the proceeds received upon the sale and the fair market value of the shares on the date of exercise. If the participant has held the shares for more than one year at the time of the sale, the capital gain or loss will be long-term, otherwise the capital gain will be short-term.

Acceleration of stock options upon a change in control. The 2002 Plan will permit acceleration of exercisability upon a change in control. The acceleration of exercisability may be a “parachute payment” for federal income tax purposes. If the present value of all of a participant’s parachute payments equals or exceeds three times the participant’s average compensation for the past five years, the participant will owe a 20% excise tax on the amount of the parachute payment that is in excess of the greater of:

| • | the average compensation of the participant for the past five years (or period of employment, if less); or |

| • | an amount which the participant establishes as reasonable compensation. |

In addition, we will not be allowed to deduct any such excess parachute payments.

Capital gains and ordinary income tax. Long term capital gains are currently taxed at a maximum federal rate of 20%. However, long term capital gains with respect to stock with a holding period of more than 5 years may qualify to be taxed at a maximum federal rate of 18% if the stock was acquired no earlier than January 1, 2001. Short term capital gains and ordinary income are taxed at marginal federal rates of up to 38.6%.

Million dollar compensation deduction limitation. We generally cannot deduct compensation paid to certain key executives in excess of $1,000,000 per year unless certain conditions are satisfied. In general, only our CEO and our four other highest paid executive officers are subject to this limitation. The income that an executive would recognize by reason of the exercise of an NQSO or on the disqualifying disposition of stock acquired pursuant to an ISO is subject to this deduction limitation. However, this limitation does not apply if:

| • | the 2002 Plan is approved by our stockholders; |

| • | the exercise price of options granted is at least equal to the fair market value of the common stock upon the date of the grant; and |

| • | the options are granted by a committee composed exclusively of members of our board of directors who satisfy certain conditions contained in the Internal Revenue Code. |

We expect to meet all of these conditions.

23

Applicability of ERISA

The 2002 Plan is not subject to any of the provisions of the Employee Retirement Income Security Act of 1974 and it is not a tax-qualified retirement plan under Section 401(a) of the Internal Revenue Code.

Options to be received by or allocated to directors and executive officers

We cannot determine at this time either the number of options that we will allocate to our directors and executive officers participating in the 2002 Plan and to other participants in the future or the number of options that these persons will actually receive in the future because the amount and value of options that we will grant to any participant are within our discretion, subject to the limitations described above.

Recommendation of our board of directors

OUR BOARD BELIEVES THAT APPROVAL OF THE 2002 PLAN IS IN THE BEST INTERESTS OF OUR STOCKHOLDERS AND UNANIMOUSLY RECOMMENDS A VOTE “FOR” APPROVAL OF THIS PROPOSAL. YOUR PROXIES WILL BE VOTED FOR THIS PROPOSAL UNLESS YOU SPECIFICALLY INDICATE OTHERWISE.

24

INDEPENDENT ACCOUNTANTS

Previous independent accountants

On August 17, 2000, we dismissed PricewaterhouseCoopers LLP, or PWC, as our independent audit firm. The decision to change the independent audit firm was recommended by our audit committee and approved by our board of directors.

During the two fiscal years ended December 31, 1999, and the subsequent interim period through August 17, 2000, there were no disagreements with PWC on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedures, which disagreements if not resolved to PWC’s satisfaction, would have caused them to make reference to the subject matter of the disagreement in connection with its reports on the consolidated financial statements for such years.

During the two fiscal years ended December 31, 1999 and through August 17, 2000, PWC had not advised us of any reportable events (as defined in Item 304 (a)(1)(v) of Regulation S-K under the Securities Exchange Act of 1934), except that PWC had informed the Audit Committee in a letter dated May 20, 2000 that a reportable condition existed during fiscal year 1999 (but not as of year end 1999 closing) relating to the reconciliation of general ledger control accounts. The condition did not result in any disagreement or difference in opinion between us and PWC.

We requested that PWC furnish us with a letter addressed to the Securities and Exchange Commission stating whether or not it agrees with the statements above and, if not, stating the respects in which it does not agree. A copy of such letter is attached hereto as Appendix B and is incorporated herein by reference.

Current independent accountants

The audit committee of the board has selected KPMG as independent accountants to audit our consolidated financial statements for 2002. KPMG was engaged in August 2000 to undertake the audit of our consolidated financial statements for 2000 and was subsequently re-engaged to perform the audit of our consolidated financial statements for 2001. A member of that firm is expected to be present at the meeting, will have an opportunity to make a statement if so desired, and will be available to respond to appropriate questions. If KPMG should decline to act or otherwise become incapable of acting, or if KPMG’s engagement is discontinued for any reason, the audit committee will appoint another accounting firm to serve as our independent public accountants for 2002.

The audit reports of KPMG on our consolidated financial statements for each of the years in the two-year period ended December 31, 2001 did not contain any adverse opinion or disclaimer of opinion, nor were they qualified or modified as to uncertainty, audit scope, or accounting principles.

2001 audit fees