Filed Pursuant to Rule 433

Registration Statement No. 333-264388

Bank of Montreal Market Linked Securities |  |

Market Linked Securities—Auto-Callable with Contingent Downside Principal at Risk Securities Linked to the S&P 500® Index due August 24, 2026 Term Sheet to Preliminary Pricing Supplement No. ARC2979 dated August 15, 2023 |

| Summary of Terms | |

| Issuer: | Bank of Montreal |

| Market Measure: | S&P 500® Index (the “Index”) |

| Pricing Date*: | August 18, 2023 |

| Issue Date*: | August 23, 2023 |

| Face Amount and Original Offering Price: | $1,000 per security |

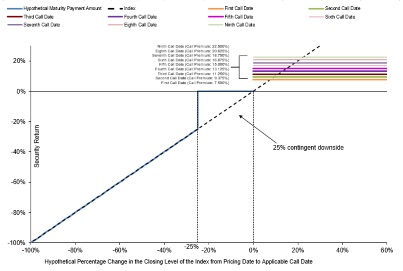

| Automatic Call: | If the closing level of the Index on any call date is greater than or equal to the starting level, the securities will be automatically called for the face amount plus the call premium applicable to that call date. |

| Call Dates* and Call | Call Dates | Call Premium† |

| Premiums: | August 23, 2024 | At least 7.50% |

| November 25, 2024 | At least 9.375% | |

| February 24, 2025 | At least 11.25% | |

| May 23, 2025 | At least 13.125% | |

| August 23, 2025 | At least 15.00% | |

| November 24, 2025 | At least 16.875% | |

| February 23, 2026 | At least 18.75% | |

| May 26, 2026 | At least 20.625% | |

August 17, 2026 (the “final calculation day”) | At least 22.50% | |

| † to be determined on the pricing date. | ||

| Call Settlement Date: | Five business days after the applicable call date (if the securities are called on the last call date, the call settlement date will be the stated maturity date) |

| Maturity Payment Amount (per security): | · if the ending level is less than the starting level, but greater than or equal to the threshold level: $1,000; or · if the ending level is less than the threshold level: $1,000 minus:

|

| Stated Maturity Date*: | August 24, 2026 |

| Starting Level: | The closing level of the Index on the pricing date |

| Ending Level: | The closing level of the Index on the final calculation day |

| Threshold Level: | 75% of the starting level |

| Calculation Agent: | BMO Capital Markets Corp. (“BMOCM”), an affiliate of the issuer |

| Denominations: | $1,000 and any integral multiple of $1,000 |

| Agent Discount**: | Up to 2.575%; dealers, including those using the trade name Wells Fargo Advisors (“WFA”), may receive a selling concession of up to 2.00% and WFA may receive a distribution expense fee of 0.075% |

| CUSIP: | 06375M6U4 |

| Material Tax Consequences: | See the preliminary pricing supplement. |

*subject to change ** In addition, selected dealers may receive a fee of up to 0.35% for marketing and other services | |

Hypothetical Payout Profile***

***assumes a call premium equal to the lowest possible call premium that may be determined on the pricing date.

**** to be determined on the pricing date; the call premium for each call date represents a percentage of the face amount.

If the securities are not automatically called and the ending level is less than the threshold level, you will have full downside exposure to the decrease in the level of the Index from the starting level and will lose more than 25.00%, and possibly all, of the face amount of your securities at maturity.

Any positive return on the securities will be limited to the applicable call premium, even if the closing level of the Index on the applicable call date significantly exceeds the starting level. You will not participate in any appreciation of the Index beyond the applicable call premium.

On the date of the accompanying preliminary pricing supplement, the estimated initial value of the securities is $950.00 per security. The estimated initial value of the securities on the pricing date may differ from this value but will not be less than $910.00 per security. However, as discussed in more detail in the accompanying preliminary pricing supplement, the actual value of the securities at any time will reflect many factors and cannot be predicted with accuracy. See “Estimated Value of the Securities” in the accompanying preliminary pricing supplement.

Preliminary Pricing Supplement:https://www.sec.gov/Archives/edgar/data/927971/000121465923011351/z811230fwp.htm

The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See “Selected Risk Considerations” in this term sheet and the accompanying preliminary pricing supplement and “Risk Factors” in the accompanying product supplement.

This introductory term sheet does not provide all of the information that an investor should consider prior to making an investment decision.

Investors should carefully review the accompanying preliminary pricing supplement, product supplement, prospectus supplement and prospectus before making a decision to invest in the securities.

NOT A BANK DEPOSIT AND NOT INSURED OR GUARANTEED BY THE FDIC OR ANY OTHER GOVERNMENTAL AGENCY

Selected Risk Considerations

The risks set forth below are discussed in detail in the “Selected Risk Considerations” section in the accompanying preliminary pricing supplement and the “Risk Factors” section in the accompanying product supplement. Please review those risk disclosures carefully.

Risks Relating To The Terms And Structure Of The Securities

· If The Securities Are Not Automatically Called And The Ending Level Is Less Than The Threshold Level, You Will Lose More Than 25.00%, And Possibly All, Of The Face Amount Of Your Securities At Maturity.

· No Periodic Interest Will Be Paid On The Securities.

· The Potential Return On The Securities Is Limited To The Call Premium And May Be Lower Than The Return On A Direct Investment In the Index.

· Higher Call Premiums Are Associated With Greater Risk.

· You Will Be Subject To Reinvestment Risk.

· A Call Settlement Date And The Stated Maturity Date May Be Postponed If A Call Date Is Postponed.

· The Securities Are Subject To Credit Risk.

· Significant Aspects Of The Tax Treatment Of The Securities Are Uncertain.

Risks Relating To The Estimated Value Of The Securities And Any Secondary Market

· The Estimated Value Of The Securities On The Pricing Date, Based On Our Proprietary Pricing Models, Will Be Less Than The Original Offering Price.

· The Terms Of The Securities Are Not Determined By Reference To The Credit Spreads For Our Conventional Fixed-Rate Debt.

· The Estimated Value Of The Securities Is Not An Indication Of The Price, If Any, At Which WFS Or Any Other Person May Be Willing To Buy The Securities From You In The Secondary Market. | · The Value Of The Securities Prior To Stated Maturity Will Be Affected By Numerous Factors, Some Of Which Are Related In Complex Ways.

· The Securities Will Not Be Listed On Any Securities Exchange And We Do Not Expect A Trading Market For The Securities To Develop.

Risks Relating To The Index

· Investing In The Securities Is Not The Same As Investing In The Index.

· Historical Levels Of The Index Should Not Be Taken As An Indication Of The Future Performance Of The Index During The Term Of The Securities.

· Changes That Affect The Index May Adversely Affect The Value Of The Securities And Any Payments On The Securities.

· We Cannot Control Actions By Any Of The Unaffiliated Companies Whose Securities Are Included In The Index.

· We And Our Affiliates Have No Affiliation With The Index Sponsor And Have Not Independently Verified Its Public Disclosure Of Information.

Risks Relating To Conflicts Of Interest

· Our Economic Interests And Those Of Any Dealer Participating In The Offering Are Potentially Adverse To Your Interests. |

The Issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this document relates. Before you invest, you should read the prospectus in that registration statement and the other documents that the Issuer has filed with the SEC for more complete information about us and this offering. You may obtain these documents free of charge by visiting the SEC’s website at http://www.sec.gov. Alternatively, the Issuer will arrange to send to you the prospectus (as supplemented by the prospectus supplement) if you request it by calling the Issuer’s agent toll-free at 1-877-369-5412.

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.

2