The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement and the accompanying product supplement, prospectus supplement and prospectus are not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject To Completion, dated August 30, 2024 PRICING SUPPLEMENT No. ELN3008 dated September __, 2024 (To Product Supplement No. WF1 dated July 20, 2022, | Filed Pursuant to Rule 433 Registration Statement No. 333-264388 |

Prospectus Supplement dated May 26, 2022 and Prospectus dated May 26, 2022) |  |

Bank of Montreal Senior Medium-Term Notes, Series I ETF Linked Securities | |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| n | Linked to the Energy Select Sector SPDR® Fund (the "Fund") |

| n | Unlike ordinary debt securities, the securities do not pay interest or repay a fixed amount of principal at maturity and are subject to potential automatic call upon the terms described below. Whether the securities are automatically called for a fixed call premium or, if not automatically called, the maturity payment amount, will depend, in each case, on the performance of the Fund. |

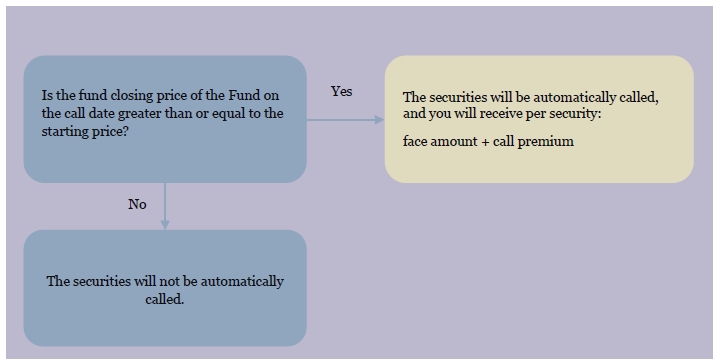

| n | Automatic Call. If the fund closing price of the Fund on the call date occurring approximately one year after issuance is greater than or equal to the starting price, the securities will be automatically called for the face amount plus a call premium of at least 14.25% of the face amount (to be determined on the pricing date) |

| n | Maturity Payment Amount. If the securities are not automatically called, you will receive a maturity payment amount that could be greater than, equal to or less than the face amount depending on the ending price of the Fund as follows: |

n If the ending price is greater than the starting price, you will receive the face amount plus a positive return equal to 125% of the percentage increase in the price of the Fund from the starting price

n If the ending price is equal to or less than the starting price but not by more than the buffer amount of 10%, you will receive the face amount

n If the ending price is less than the starting price by more than the buffer amount, you will receive less than the face amount and have 1-to-1 downside exposure to the decrease in the price of the Fund in excess of the buffer amount

| n | Investors may lose up to 90% of the face amount |

| n | If the securities are automatically called, the positive return on the securities will be limited to the call premium, and you will not participate in any appreciation of the Fund beyond the call premium, which may be significant. If the securities are automatically called, you will no longer have the opportunity to participate in any appreciation of the Fund at the upside participation rate |

| n | All payments on the securities are subject to the credit risk of Bank of Montreal, and you will have no ability to pursue the Fund or any securities held by the Fund for payment; if Bank of Montreal defaults on its obligations, you could lose some or all of your investment |

| n | No periodic interest payments or dividends |

| n | No exchange listing; designed to be held to maturity or automatic call |

On the date of this preliminary pricing supplement, the estimated initial value of the securities is $985.60 per security. The estimated initial value of the securities on the pricing date may differ from this value but will not be less than $918.00 per security. However, as discussed in more detail in this pricing supplement, the actual value of the securities at any time will reflect many factors and cannot be predicted with accuracy. See “Estimated Value of the Securities” in this pricing supplement.

The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See "Selected Risk Considerations" beginning on page PRS-8 herein and "Risk Factors" beginning on page PS-5 of the accompanying product supplement.

The securities are the unsecured obligations of Bank of Montreal, and, accordingly, all payments on the securities are subject to the credit risk of Bank of Montreal. If Bank of Montreal defaults on its obligations, you could lose some or all of your investment. The securities are not insured by the Federal Deposit Insurance Corporation, the Deposit Insurance Fund, the Canada Deposit Insurance Corporation or any other governmental agency.

Neither the Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this pricing supplement or the accompanying product supplement, prospectus supplement and prospectus. Any representation to the contrary is a criminal offense.

Original Offering Price | Agent Discount(1)(2) | Proceeds to Bank of Montreal | |

| Per Security | $1,000.00 | Up to $25.75 | $974.25 |

| Total |

| (1) | Wells Fargo Securities, LLC is the agent for the distribution of the securities and is acting as principal. See “Terms of the Securities—Agent” and “Estimated Value of the Securities” in this pricing supplement for further information. |

| (2) | In respect of certain securities sold in this offering, our affiliate, BMO Capital Markets Corp., may pay a fee of up to $3.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers. |

Wells Fargo Securities

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Terms of the Securities |

| Issuer: | Bank of Montreal. |

| Market Measure: | Energy Select Sector SPDR® Fund (the "Fund"). |

| Fund Underlying Index: | The Energy Select Sector Index. |

| Pricing Date*: | September 27, 2024. |

| Issue Date*: | October 2, 2024. |

| Original Offering Price: | $1,000 per security. |

| Face Amount: | $1,000 per security. References in this pricing supplement to a "security" are to a security with a face amount of $1,000. |

| Automatic Call: | If the fund closing price of the Fund on the call date is greater than or equal to the starting price, the securities will be automatically called, and on the call settlement date, you will receive the face amount per security plus the call premium.

If the securities are automatically called, the positive return on the securities will be limited to the call premium, and you will not participate in any appreciation of the Fund beyond the call premium, which may be significant. If the securities are automatically called, you will no longer have the opportunity to participate in any appreciation of the Fund at the upside participation rate.

If the securities are automatically called, they will cease to be outstanding on the related call settlement date and you will have no further rights under the securities after such call settlement date. You will not receive any notice from us if the securities are automatically called.

|

| Call Date*: | October 2, 2025, subject to postponement. |

| Call Premium: | At least 14.25% of the face amount, or at least $142.50 per $1,000 face amount of the securities (the actual call premium will be determined on the pricing date) |

| Call Settlement Date: | Three business days after the call date (as the call date may be postponed pursuant to “—Market Disruption Events and Postponement Provisions” below, if applicable). |

| Maturity Payment Amount: | If the securities are not automatically called on the call date, then on the stated maturity date, you will be entitled to receive a cash payment per security in U.S. dollars equal to the maturity payment amount. The "maturity payment amount" per security will equal:

• if the ending price is greater than the starting price: $1,000 plus:

$1,000 × fund return × upside participation rate

• if the ending price is less than or equal to the starting price, but greater than or equal to the threshold price: $1,000; or

• if the ending price is less than the threshold price:

$1,000 + [$1,000 × (fund return + buffer amount)]

|

| If the securities are not automatically called, and the ending price is less than the threshold price, you will have 1-to-1 downside exposure to the decrease in the price of the Fund in excess of the buffer amount and will lose some, and possibly up to 90%, of the face amount of your securities at maturity. | |

Stated Maturity Date*:

| September 30, 2027, subject to postponement. The securities are not subject to repayment at the option of any holder of the securities prior to the stated maturity date. |

| Starting Price: | [ ], the fund closing price of the Fund on the pricing date. |

| Fund Closing Price: | Fund closing price, closing price and adjustment factor have the meanings set forth under "General Terms of the Securities—Certain Terms for Securities Linked to a Fund—Certain Definitions" in the accompanying product supplement. |

| Ending Price: | The "ending price" will be the fund closing price of the Fund on the final calculation day. |

| Threshold Price: | [ ], which is equal to 90% of the starting price. |

| PRS-2 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Buffer Amount: | 10%. |

| Upside Participation Rate: | 125%. |

| Fund Return: | The "fund return" is the percentage change from the starting price to the ending price, measured as follows: ending price – starting price starting price

|

| Final Calculation Day*: | September 27, 2027, subject to postponement. |

| Market Disruption Events and Postponement Provisions: | The call date and the final calculation day are subject to postponement due to non-trading days and the occurrence of a market disruption event. In addition, the call payment date and the stated maturity date will be postponed if the call date or the final calculation day, as applicable, is postponed, and will be adjusted for non-business days.

For more information regarding adjustments to the call date, the final calculation day, the call settlement date, and the stated maturity date, see "General Terms of the Securities—Consequences of a Market Disruption Event; Postponement of a Calculation Day—Securities Linked to a Single Market Measure" and "—Payment Dates" in the accompanying product supplement. For purposes of the product supplement, each of the call date and the final calculation day is a "calculation day," and the call settlement date and the stated maturity date is a "payment date." In addition, for information regarding the circumstances that may result in a market disruption event, see "General Terms of the Securities—Certain Terms for Securities Linked to a Fund—Market Disruption Events" in the accompanying product supplement.

|

| Calculation Agent: | BMO Capital Markets Corp. ("BMOCM"). |

Material Tax Consequences:

| For a discussion of the material U.S. federal income and certain estate tax consequences and the Canadian federal income tax consequences of the ownership and disposition of the securities, see “United States Federal Tax Considerations" below, and the sections of the product supplement entitled "United States Federal Tax Considerations" and "Canadian Federal Income Tax Consequences." |

| Agent: | Wells Fargo Securities, LLC (“WFS”) is the agent for the distribution of the securities. The agent will receive an agent discount of up to $25.75 per security. The agent may resell the securities to other securities dealers at the original offering price of the securities less a concession not in excess of $20.00 per security. Such securities dealers may include Wells Fargo Advisors (“WFA”) (the trade name of the retail brokerage business of WFS’s affiliates, Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC). In addition to the concession allowed to WFA, WFS may pay $0.75 per security of the agent discount that it receives to WFA as a distribution expense fee for each security sold by WFA.

In addition, in respect of certain securities sold in this offering, BMOCM may pay a fee of up to $3.00 per security to selected securities dealers in consideration for marketing and other services in connection with the distribution of the securities to other securities dealers.

WFS, BMOCM and/or one or more of their respective affiliates expects to realize hedging profits projected by their proprietary pricing models to the extent they assume the risks inherent in hedging our obligations under the securities. If WFS or any other dealer participating in the distribution of the securities or any of their affiliates conduct hedging activities for us in connection with the securities, that dealer or its affiliates will expect to realize a profit projected by its proprietary pricing models from those hedging activities. Any such projected profit will be in addition to any discount, concession or fee received in connection with the sale of the securities to you.

|

| Denominations: | $1,000 and any integral multiple of $1,000. |

| CUSIP: | 06376BKZ0 |

| ________________________ |

| * | To the extent that we make any change to the expected pricing date or expected issue date, the call date, the final calculation day and stated maturity date may also be changed in our discretion to ensure that the term of the securities remains the same. |

| PRS-3 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Additional Information About the Issuer and the Securities |

You should read this pricing supplement together with product supplement No. WF1 dated July 20, 2022, the prospectus supplement dated May 26, 2022 and the prospectus dated May 26, 2022 for additional information about the securities. Information included in this pricing supplement supersedes information in the product supplement, prospectus supplement and prospectus to the extent it is different from that information. Certain defined terms used but not defined herein have the meanings set forth in the product supplement, prospectus supplement or prospectus.

Our Central Index Key, or CIK, on the SEC website is 927971. When we refer to “we,” “us” or “our” in this pricing supplement, we refer only to Bank of Montreal.

You may access the product supplement, prospectus supplement and prospectus on the SEC website www.sec.gov as follows (or if that address has changed, by reviewing our filing for the relevant date on the SEC website):

| • | Product Supplement No. WF1 dated July 20, 2022: |

https://www.sec.gov/Archives/edgar/data/927971/000121465922009020/r715220424b5.htm

| • | Prospectus Supplement and prospectus dated May 26, 2022: |

https://www.sec.gov/Archives/edgar/data/927971/000119312522160519/d269549d424b5.htm

We have filed a registration statement (including a prospectus) with the SEC for the offering to which this document relates. Before you invest, you should read the prospectus in that registration statement and the other documents that we have filed with the SEC for more complete information about us and this offering. You may obtain these documents free of charge by visiting the SEC’s website at http://www.sec.gov. Alternatively, we will arrange to send to you the prospectus (as supplemented by the prospectus supplement if you request it by calling BMOCM toll-free at 1-877-369-5412.

| PRS-4 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Estimated Value of the Securities |

Our estimated initial value of the securities on the date of this preliminary pricing supplement, and that will be set forth on the cover page of the final pricing supplement relating to the securities, equals the sum of the values of the following hypothetical components:

| · | a fixed-income debt component with the same tenor as the securities, valued using our internal funding rate for structured notes; and |

| · | one or more derivative transactions relating to the economic terms of the securities. |

The internal funding rate used in the determination of the initial estimated value generally represents a discount from the credit spreads for our conventional fixed-rate debt. The value of these derivative transactions is derived from our internal pricing models. These models are based on factors such as the traded market prices of comparable derivative instruments and on other inputs, which include volatility, dividend rates, interest rates and other factors. As a result, the estimated initial value of the securities on the pricing date will be determined based on market conditions at that time.

For more information about the estimated initial value of the securities, see “Selected Risk Considerations” below.

| PRS-5 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Investor Considerations |

The securities are not appropriate for all investors. The securities may be an appropriate investment for investors who:

| § | seek a fixed return equal to the call premium if the securities are automatically called on the call date; |

| § | understand that the securities may be automatically called prior to the stated maturity and that the term of the securities may be as short as approximately one year; |

| § | seek 125% leveraged exposure to the upside performance of the Fund if the securities are not automatically called and the ending price is greater than the starting price; |

| § | desire to limit downside exposure to the Fund through the buffer amount; |

| § | are willing to accept the risk that, if the securities are not automatically called and the ending price is less than the starting price by more than the buffer amount, they will lose some, and possibly up to 90%, of the face amount per security at maturity; |

| § | are willing to forgo interest payments on the securities and dividends on the shares of the fund and the securities held by the Fund; and |

| § | are willing to hold the securities until maturity or automatic call. |

The securities may not be an appropriate investment for investors who:

| § | seek a liquid investment or are unable or unwilling to hold the securities to maturity or automatic call; |

| § | seek a security with a fixed term; |

| § | are unwilling to accept the risk that the securities will not be automatically called and the ending price of the Fund may decrease from the starting price by more than the buffer amount; |

| § | seek full return of the face amount of the securities at stated maturity; |

| § | are unwilling to purchase securities with an estimated value as of the pricing date that is lower than the original offering price and that may be as low as the lower estimated value set forth on the cover page; |

| § | seek current income over the term of the securities; |

| § | are unwilling to accept the risk of exposure to the Fund; |

| § | seek exposure to the Fund but are unwilling to accept the risk/return trade-offs inherent in the maturity payment amount for the securities; |

| § | are unwilling to accept the credit risk of Bank of Montreal to obtain exposure to the Fund generally, or to the exposure to the Fund that the securities provide specifically; or |

| § | prefer the lower risk of fixed income investments with comparable maturities issued by companies with comparable credit ratings. |

The considerations identified above are not exhaustive. Whether or not the securities are an appropriate investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the appropriateness of an investment in the securities in light of your particular circumstances. You should also review carefully the "Selected Risk Considerations" herein and the "Risk Factors" in the accompanying product supplement for risks related to an investment in the securities. For more information about the Fund, please see the section entitled "The Energy Select Sector SPDR® Fund" below.

| PRS-6 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Determining Timing and Amount of Payment on the Securities |

Whether the securities are automatically called on the call date for the call premium will each be determined based on the fund closing price of the Fund on the call date as follows:

If the securities have not been automatically called, then on the stated maturity date, you will receive a cash payment per security (the maturity payment amount) calculated as follows:

| PRS-7 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Selected Risk Considerations |

The securities have complex features and investing in the securities will involve risks not associated with an investment in conventional debt securities. Some of the risks that apply to an investment in the securities are summarized below, but we urge you to read the more detailed explanation of the risks relating to the securities generally in the "Risk Factors" section of the accompanying product supplement. You should reach an investment decision only after you have carefully considered with your advisors the appropriateness of an investment in the securities in light of your particular circumstances.

Risks Relating To The Terms And Structure Of The Securities

If The Securities Are Not Automatically Called And The Ending Price Is Less Than The Threshold Price, You Will Lose Some, And Possibly Up To 90%, Of The Face Amount Of Your Securities At Maturity.

If the securities are not automatically called, we will not repay you a fixed amount on the securities on the stated maturity date. The maturity payment amount will depend on the direction of and percentage change in the ending price of the Fund relative to the starting price and the other terms of the securities. Because the price of the Fund will be subject to market fluctuations, the maturity payment amount may be more or less, and possibly significantly less, than the face amount of your securities.

If the securities are not automatically called and the ending price is less than the threshold price, the maturity payment amount will be less than the face amount and you will have 1-to-1 downside exposure to the decrease in the price of the Fund in excess of the buffer amount, resulting in a loss of 1% of the face amount for every 1% decline in the Fund in excess of the buffer amount. The threshold price is 90% of the starting price. As a result, if the ending price is less than the threshold price, you will lose some, and possibly up to 90%, of the face amount per security at maturity. This is the case even if the price of the Fund is greater than or equal to the starting price or the threshold price at certain times during the term of the securities.

If the securities are not automatically called, even if the ending price is greater than the starting price, the maturity payment amount may only be slightly greater than the face amount, and your yield on the securities may be less than the yield you would earn if you bought a traditional interest-bearing debt security of Bank of Montreal or another issuer with a similar credit rating with the same stated maturity date.

No Periodic Interest Will Be Paid On The Securities.

No periodic payments of interest will be made on the securities. However, if the agreed-upon tax treatment is successfully challenged by the Internal Revenue Service (the "IRS"), you may be required to recognize taxable income over the term of the securities. You should review the section of this pricing supplement entitled "United States Federal Tax Considerations."

If The Securities Are Automatically Called, Your Return Will Be Limited to the Call Premium.

If the securities are automatically called, the positive return on the securities will be limited to the call premium, and you will not participate in any appreciation of the Fund beyond the call premium, which may be significant. Accordingly, if the securities are automatically called, the return on the securities may be less than the return in a direct investment in the securities represented by the Fund. If the securities are automatically called, you will no longer have the opportunity to participate in any appreciation of the Fund at the upside participation rate.

You Will Be Subject To Reinvestment Risk.

If your securities are automatically called, the term of the securities may be reduced to as short as approximately one year. There is no guarantee that you would be able to reinvest the proceeds from an investment in the securities at a comparable return for a similar level of risk in the event the securities are automatically called prior to maturity.

The Securities Are Subject To Credit Risk.

The securities are our obligations and are not, either directly or indirectly, an obligation of any third party. Any amounts payable under the securities are subject to our creditworthiness and you will have no ability to pursue any securities held by the Fund for payment. As a result, our actual and perceived creditworthiness may affect the value of the securities and, in the event we were to default on our obligations under the securities, you may not receive any amounts owed to you under the terms of the securities.

Significant Aspects Of The Tax Treatment Of The Securities Are Uncertain.

The tax treatment of the securities is uncertain. We do not plan to request a ruling from the IRS or from the Canada Revenue Agency regarding the tax treatment of the securities, and the IRS, the Canada Revenue Agency or a court may not agree with the tax treatment described in this pricing supplement and/or the accompanying product supplement.

The IRS has issued a notice indicating that it and the U.S. Treasury Department are actively considering whether, among other issues, a holder should be required to accrue interest over the term of an instrument such as the securities even though that holder will not receive any payments with respect to the securities until maturity or earlier sale or exchange and whether all or part of the gain a holder may recognize upon sale, exchange or maturity of an instrument such as the securities should be treated as ordinary income. The outcome of this process is uncertain and could apply on a retroactive basis.

| PRS-8 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

Please read carefully the section entitled “United States Federal Tax Considerations” in this pricing supplement, the section entitled “United States Federal Income Taxation” in the accompanying prospectus and the section entitled “United States Federal Tax Considerations” in the accompanying product supplement. You should consult your tax advisor about your own tax situation.

For a discussion of the Canadian federal income tax consequences of investing in the securities, please read the section entitled “Certain Income Tax Consequences — Certain Canadian Income Tax Considerations” in the accompanying prospectus supplement. You should consult your tax advisor about your own tax situation.

The Call Settlement Date Or The Stated Maturity Date May Be Postponed If The Call Date Or The Final Calculation Day Is Postponed.

The call date or the final calculation day will be postponed if the originally scheduled call date or final calculation day is not a trading day or if the calculation agent determines that a market disruption event has occurred or is continuing on that day. If such a postponement occurs with respect to the call date, then the call settlement date will be postponed. If such a postponement occurs with respect to the final calculation day, the stated maturity date will be the later of (i) the initial stated maturity date and (ii) three business days after the final calculation day as postponed.

Risks Relating To The Estimated Value Of The Securities And Any Secondary Market

The Estimated Value Of The Securities On The Pricing Date, Based On Our Proprietary Pricing Models, Will Be Less Than The Original Offering Price.

Our initial estimated value of the securities is only an estimate, and is based on a number of factors. The original offering price of the securities may exceed our initial estimated value, because costs associated with offering, structuring and hedging the securities are included in the original offering price, but are not included in the estimated value. These costs include the agent discount and selling concessions, the profits that we and our affiliates and/or the agent and its affiliates expect to realize for assuming the risks in hedging our obligations under the securities, and the estimated cost of hedging these obligations. The initial estimated value may be as low as the amount indicated on the cover page of this pricing supplement.

The Terms Of The Securities Are Not Determined By Reference To The Credit Spreads For Our Conventional Fixed-Rate Debt.

To determine the terms of the securities, we will use an internal funding rate that represents a discount from the credit spreads for our conventional fixed-rate debt. As a result, the terms of the securities are less favorable to you than if we had used a higher funding rate.

The Estimated Value Of The Securities Is Not An Indication Of The Price, If Any, At Which WFS Or Any Other Person May Be Willing To Buy The Securities From You In The Secondary Market.

Our initial estimated value of the securities as of the date of this preliminary pricing supplement is, and our estimated value as determined on the pricing date will be, derived using our internal pricing models. This value is based on market conditions and other relevant factors, which include volatility of the Fund, dividend rates and interest rates. Different pricing models and assumptions, including those used by the agent, its affiliates or other market participants, could provide values for the securities that are greater than or less than our initial estimated value. In addition, market conditions and other relevant factors after the pricing date are expected to change, possibly rapidly, and our assumptions may prove to be incorrect. After the pricing date, the value of the securities could change dramatically due to changes in market conditions, our creditworthiness, and the other factors set forth in this pricing supplement. These changes are likely to impact the price, if any, at which WFS or its affiliates or any other party (including us or our affiliates) would be willing to purchase the securities from you in any secondary market transactions. Our initial estimated value does not represent a minimum price at which WFS or any other party (including us or our affiliates) would be willing to buy your securities in any secondary market at any time.

WFS has advised us that if it, WFA or any of their affiliates makes a secondary market in the securities at any time, the secondary market price offered by it, WFA or any of their affiliates will be affected by changes in market conditions and other factors described in the next risk factor. WFS has advised us that if it, WFA or any of their affiliates makes a secondary market in the securities at any time up to the issue date or during the 3-month period following the issue date, the secondary market price offered by it, WFA or any of its affiliates will be increased by an amount reflecting a portion of the costs associated with selling, structuring and hedging the securities that are included in their original offering price. Because this portion of the costs is not fully deducted upon issuance, WFS has advised us that any secondary market price it, WFA or any of their affiliates offers during this period will be higher than it otherwise would be after this period, as any secondary market price offered after this period will reflect the full deduction of the costs as described above. WFS has advised us that the amount of this increase in the secondary market price will decline steadily to zero over this 3-month period. WFS has advised us that, if you hold the securities through an account with WFS, WFA or any of their affiliates, WFS expects that this increase will also be reflected in the value indicated for the securities on your brokerage account statement. If you hold your securities through an account at a broker-dealer other than WFS, WFA or any of their affiliates, the value of the securities on your brokerage account statement may be different than if you held your securities at WFS, WFA or any of their affiliates.

The Value Of The Securities Prior To Stated Maturity Will Be Affected By Numerous Factors, Some Of Which Are Related In Complex Ways.

The value of the securities prior to stated maturity will be affected by the then-current price of the Fund, interest rates at that time and a number of other factors, some of which are interrelated in complex ways. The effect of any one factor may be offset or magnified by the effect of another factor. The following factors, which we refer to as the “derivative component factors,” and which are described in more detail in the accompanying product supplement, are expected to affect the value of the securities: performance of the Fund; interest rates; volatility of the Fund; time remaining to maturity; and dividend yields on securities included in the Fund. When we refer to the “value” of your security, we mean the value you could receive for your security if you are able to sell it in the open market before the stated maturity date.

| PRS-9 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

In addition to the derivative component factors, the value of the securities will be affected by actual or anticipated changes in our creditworthiness. The value of the securities will also be limited by the automatic call feature because if the securities are automatically called, your return will be limited to the call premium, and you will not receive the potentially higher payment that may have been paid if you had held the securities until the stated maturity date. You should understand that the impact of one of the factors specified above, such as a change in interest rates, may offset some or all of any change in the value of the securities attributable to another factor, such as a change in the price of the Fund. Because numerous factors are expected to affect the value of the securities, changes in the price of the Fund may not result in a comparable change in the value of the securities.

The Securities Will Not Be Listed On Any Securities Exchange And We Do Not Expect A Trading Market For The Securities To Develop.

The securities will not be listed or displayed on any securities exchange or any automated quotation system. Although the agent and/or its affiliates may purchase the securities from holders, they are not obligated to do so and are not required to make a market for the securities. There can be no assurance that a secondary market will develop. Because we do not expect that any market makers will participate in a secondary market for the securities, the price at which you may be able to sell your securities is likely to depend on the price, if any, at which the agent is willing to buy your securities.

If a secondary market does exist, it may be limited. Accordingly, there may be a limited number of buyers if you decide to sell your securities prior to stated maturity. This may affect the price you receive upon such sale. Consequently, you should be willing to hold the securities to stated maturity.

Risks Relating To The Fund

An Investment In The Securities Is Subject To Risks Associated With Energy-Related Companies.

The Fund’s investment strategy involves exposure to energy-based companies whose primary business or businesses are focused on oil, gas and consumable fuels, energy equipment, and services. Stock prices for these types of companies are mainly affected by the business, financial and operating conditions of the particular company, as well as changes in prices for oil, gas and other types of fuels, which in turn largely depend on supply and demand for various energy products and services. Some of the factors that may influence supply and demand for energy products and services include: general economic conditions and growth rates; weather conditions; the cost of exploring for, producing and delivering oil and gas; technological advances affecting energy efficiency and energy consumption; the ability of the Organization of Petroleum Exporting Countries (OPEC) to establish and maintain production levels of oil; currency fluctuations; inflation; natural disasters; civil unrest, acts of sabotage or terrorism; and other regional or global events. The profitability of energy companies may also be adversely affected by existing and future laws, regulations, government actions and other legal requirements relating to protection of the environment, health and safety matters and others that may increase the costs of conducting their business or may reduce or delay available business opportunities. Increased supply or weak demand for energy products and services, as well as various developments leading to higher costs of doing business or missed business opportunities, would adversely impact the performance of companies in the energy sector.

Whether The Securities Will Be Automatically Called And The Maturity Payment Amount Depend Upon The Performance Of The Fund And Therefore The Securities Are Subject To The Following Risks, Each As Discussed In More Detail In The Accompanying Product Supplement.

| · | Investing In The Securities Is Not The Same As Investing In The Fund. Investing in the securities is not equivalent to investing in the Fund. As an investor in the securities, your return will not reflect the return you would realize if you actually owned and held the securities held by the Fund for a period similar to the term of the securities because you will not receive any dividend payments, distributions or any other payments paid on those securities. As a holder of the securities, you will not have any voting rights or any other rights that holders of the securities held by the Fund would have. |

| · | Historical Prices Of The Fund Should Not Be Taken As An Indication Of The Future Performance Of The Fund During The Term Of The Securities. |

| · | Changes That Affect The Fund Or Its Fund Underlying Index May Adversely Affect The Value Of The Securities And Any Payments On The Securities. |

| · | We Cannot Control Actions By Any Of The Unaffiliated Companies Whose Securities Are Included In The Fund Or Its Fund Underlying Index. |

| · | We And Our Affiliates Have No Affiliation With The Fund Sponsor Or Fund Underlying Index Sponsor And Have Not Independently Verified Their Public Disclosure Of Information. |

| · | An Investment Linked To The Shares Of A Fund Is Different From An Investment Linked To Its Fund Underlying Index. |

| · | There Are Risks Associated With A Fund. |

| PRS-10 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| · | Anti-dilution Adjustments Relating To The Shares Of A Fund Do Not Address Every Event That Could Affect Such Shares. |

Risks Relating To Conflicts Of Interest

Our Economic Interests And Those Of Any Dealer Participating In The Offering Are Potentially Adverse To Your Interests.

You should be aware of the following ways in which our economic interests and those of any dealer participating in the distribution of the securities, which we refer to as a "participating dealer," are potentially adverse to your interests as an investor in the securities. In engaging in certain of the activities described below and as discussed in more detail in the accompanying product supplement, our affiliates or any participating dealer or its affiliates may take actions that may adversely affect the value of and your return on the securities, and in so doing they will have no obligation to consider your interests as an investor in the securities. Our affiliates or any participating dealer or its affiliates may realize a profit from these activities even if investors do not receive a favorable investment return on the securities.

| · | The calculation agent is our affiliate and may be required to make discretionary judgments that affect the return you receive on the securities. BMOCM, which is our affiliate, will be the calculation agent for the securities. As calculation agent, BMOCM will determine any values of the Fund and make any other determinations necessary to calculate any payments on the securities. In making these determinations, BMOCM may be required to make discretionary judgments that may adversely affect any payments on the securities. See the sections entitled "General Terms of the Securities— Certain Terms for Securities Linked to a Fund—Market Disruption Events" and "—Anti-dilution Adjustments Relating to a Fund; Alternate Calculation" in the accompanying product supplement. In making these discretionary judgments, the fact that BMOCM is our affiliate may cause it to have economic interests that are adverse to your interests as an investor in the securities, and BMOCM's determinations as calculation agent may adversely affect your return on the securities. |

| · | The estimated value of the securities was calculated by us and is therefore not an independent third-party valuation. |

| · | Research reports by our affiliates or any participating dealer or its affiliates may be inconsistent with an investment in the securities and may adversely affect the price of the Fund. |

| · | Business activities of our affiliates or any participating dealer or its affiliates with the companies whose securities are held by the Fund may adversely affect the price of the Fund. |

| · | Hedging activities by our affiliates or any participating dealer or its affiliates may adversely affect the price of the Fund. |

| · | Trading activities by our affiliates or any participating dealer or its affiliates may adversely affect the price of the Fund. |

| · | A participating dealer or its affiliates may realize hedging profits projected by its proprietary pricing models in addition to any selling concession and/or fee, creating a further incentive for the participating dealer to sell the securities to you. |

| PRS-11 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Hypothetical Examples and Returns |

The payout profile, return table and examples below illustrate hypothetical payments upon an automatic call or at stated maturity for a $1,000 face amount security on a hypothetical offering of securities under various scenarios, with the assumptions set forth in the table below. The terms used for purposes of these hypothetical examples do not represent the actual starting price or threshold price. The hypothetical starting price of $100.00 has been chosen for illustrative purposes only and does not represent the actual starting price. The actual starting price and threshold price will be determined on the pricing date and will be set forth under "Terms of the Securities" in the final pricing supplement. For historical data regarding the actual fund closing prices of the Fund, see the historical information set forth herein. The payout profile, return table and examples below assume that an investor purchases the securities for $1,000 per security. These examples are for purposes of illustration only and the values used in the examples may have been rounded for ease of analysis. The actual amount you receive at stated maturity or upon automatic call, and the resulting pre-tax total rate of return will depend on the actual terms of the securities.

| Hypothetical Call Premium: | 14.25% of the face amount (the lowest possible call premium that may be determined on the pricing date) |

| Upside Participation Rate: | 125% |

| Hypothetical Starting Price: | $100.00 |

| Hypothetical Threshold Price: | $90.00 (90.00% of the hypothetical starting price) |

| Buffer Amount: | 10% |

Hypothetical Payout Profile

| PRS-12 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

Hypothetical Returns

If the securities are automatically called:

If the securities are automatically called prior to stated maturity, you will receive the face amount of your securities plus the call premium, resulting in a hypothetical pre-tax total rate of return of 14.25%.

If the securities are not automatically called:

Hypothetical ending price | Hypothetical fund return(1) | Hypothetical maturity payment amount per security | Hypothetical pre-tax total rate of return(2) |

| $200.00 | 100.00% | $2,250.00 | 125.00% |

| $175.00 | 75.00% | $1,937.50 | 93.75% |

| $150.00 | 50.00% | $1,625.00 | 62.50% |

| $140.00 | 40.00% | $1,500.00 | 50.00% |

| $130.00 | 30.00% | $1,375.00 | 37.50% |

| $120.00 | 20.00% | $1,250.00 | 25.00% |

| $110.00 | 10.00% | $1,125.00 | 12.50% |

| $105.00 | 5.00% | $1,062.50 | 6.25% |

| $100.00 | 0.00% | $1,000.00 | 0.00% |

| $95.00 | -5.00% | $1,000.00 | 0.00% |

| $90.00 | -10.00% | $1,000.00 | 0.00% |

| $89.00 | -11.00% | $990.00 | -1.00% |

| $75.00 | -25.00% | $850.00 | -15.00% |

| $50.00 | -50.00% | $600.00 | -40.00% |

| $25.00 | -75.00% | $350.00 | -65.00% |

| $0.00 | -100.00% | $100.00 | -90.00% |

| (1) | The fund return is equal to the percentage change from the starting price to the ending price (i.e., the ending price minus the starting price, divided by the starting price). |

| (2) | The hypothetical pre-tax total rate of return is the number, expressed as a percentage, that results from comparing the maturity payment amount per security to the face amount of $1,000. |

| PRS-13 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

Hypothetical Examples Of Payment Upon An Automatic Call Or At Stated Maturity

Example 1. The fund closing price of the Fund on the call date is greater than the starting price, and the securities are automatically called on the call date:

| The Fund | |

| Hypothetical starting price: | $100.00 |

| Hypothetical fund closing price on the call date: | $125.00 |

Because the hypothetical fund closing price of the Fund on the call date is greater than the hypothetical starting price, the securities are automatically called on the call date and you will receive on the call settlement date the face amount of your securities plus a call premium of 14.25% of the face amount. Even though the Fund appreciated by 25.00% from its starting price to its fund closing price on the call date in this example, your return is limited to the call premium of 14.25%.

On the call settlement date, you would receive $1,142.50 per security.

Example 2. The securities are not automatically called. The maturity payment amount is greater than the face amount:

| The Fund | |

| Hypothetical starting price: | $100.00 |

| Hypothetical fund closing price on the call date: | $75.00 |

| Hypothetical ending price: | $110.00 |

| Hypothetical threshold price: | $90.00 |

Hypothetical fund return (ending price – starting price)/starting price: | 10.00% |

Because the hypothetical fund closing price of the Fund on the call date is less than the hypothetical starting price, the securities are not automatically called. Because the hypothetical ending price is greater than the hypothetical starting price, the maturity payment amount per security would be equal to the face amount of $1,000 plus a positive return equal to:

$1,000 × fund return × upside participation rate

$1,000 × 10.00% × 125.00%

= $125.00

On the stated maturity date you would receive $1,125.00 per security.

Example 3. The securities are not automatically called. Maturity payment amount is equal to the face amount:

| The Fund | |

| Hypothetical starting price: | $100.00 |

| Hypothetical fund closing price on the call date: | $75.00 |

| Hypothetical ending price: | $95.00 |

| Hypothetical threshold price: | $90.00 |

Hypothetical fund return (ending price – starting price)/starting price: | -5.00% |

Because the hypothetical fund closing price of the Fund on the call date is less than the hypothetical starting price, the securities are not automatically called. Because the hypothetical ending price is less than the hypothetical starting price, but not by more than the buffer amount, you would not lose any of the face amount of your securities.

On the stated maturity date you would receive $1,000.00 per security.

| PRS-14 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

Example 4. The securities are not automatically called. Maturity payment amount is less than the face amount:

| The Fund | |

| Hypothetical starting price: | $100.00 |

| Hypothetical fund closing price on the call date: | $75.00 |

| Hypothetical ending price: | $50.00 |

| Hypothetical threshold price: | $90.00 |

Hypothetical fund return (ending price – starting price)/starting price: | -50.00% |

Because the hypothetical fund closing price of the Fund on the call date is less than the hypothetical starting price, the securities are not automatically called. Because the hypothetical ending price is less than the hypothetical starting price by more than the buffer amount, you would lose a portion of the face amount of your securities and receive the maturity payment amount equal to:

$1,000 + [$1,000 × (fund return + buffer amount)]

$1,000 + [$1,000 × (-50.00% + 10%)]

= $600.00

On the stated maturity date you would receive $600.00 per security.

| PRS-15 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| The Energy Select Sector SPDR® Fund |

Historical Information

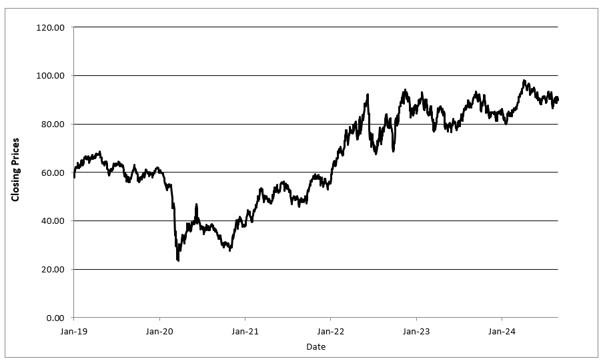

We obtained the fund closing prices of the Energy Select Sector SPDR® Fund in the graph below from Bloomberg Finance L.P., without independent verification.

The following graph sets forth daily fund closing prices of the Energy Select Sector SPDR® Fund for the period from January 1, 2019 to August 28, 2024. The fund closing price on August 28, 2024 was $89.77. The historical performance of the Energy Select Sector SPDR® Fund should not be taken as an indication of its future performance during the term of the securities.

| PRS-16 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

We have derived the following information regarding the Fund and the Fund Underlying Index from publicly available documents. We have not independently verified the accuracy or completeness of the following information. Neither we nor our affiliates have made any due diligence inquiry with respect to the Fund or the Fund Underlying Index in connection with the offering of the securities.

The selection of the Fund and the Fund Underlying Index is not a recommendation to invest in this asset. Neither we nor any of our affiliates make any representation to you as to the performance of the Fund or the Fund Underlying Index. Information provided to or filed with the SEC under the Securities Exchange Act of 1934 and the Investment Company Act of 1940 relating to the Fund may be obtained through the SEC’s website at http://www.sec.gov.

Energy Select Sector SPDR® Fund (“XLE”)

The XLE seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of the Energy Select Sector Index. The Energy Select Sector Index is a capped modified market capitalization-based index that measures the performance of the GICS energy sector of the S&P 500® Index, which currently includes companies in the following industries: exploration and production, refining and marketing and storage and transportation of oil and gas and coal and consumable fuels. The XLE trades on the NYSE Arca under the ticker symbol "XLE".

The XLE is an investment portfolio maintained and managed by the investment advisor. The securities are not sponsored, endorsed, sold or promoted by this investment advisor. This investment advisor makes no representations or warranties to the owners of the securities or any member of the public regarding the advisability of investing in the securities. This investment advisor has no obligation or liability in connection with the operation, marketing, trading or sale of the securities.

Eligibility Criteria for Index Components

The stocks included in each Select Sector Index are selected from the universe of companies represented by the S&P 500® Index. Standard & Poor’s Financial Services LLC (“S&P”) acts as index calculation agent in connection with the calculation and dissemination of each Select Sector Index. Each stock in the S&P 500® Index is allocated to only one Select Sector Index, and the Select Sector Indices together comprise all of the companies in the S&P 500® Index.

Index Maintenance

Each Select Sector Index was developed and is maintained in accordance with the following criteria:

| § | Each of the component stocks in a Select Sector Index (the “Component Stocks”) is a constituent company of the S&P 500® Index. |

| § | The eleven Select Sector Indices together will include all of the companies represented in the S&P 500® Index and each of the stocks in the S&P 500® Index will be allocated to one of the Select Sector Indices. |

| § | Each constituent stock of the S&P 500® Index is assigned to a Select Sector Index based on its GICS sector. Each Select Sector Index is made up of all the stocks in the applicable GICS sector. |

| § | Each Select Sector Index is calculated by the index sponsor, Standard & Poor’s, using a capped market capitalization methodology where single index constituents or defined groups of index constituents are confined to a maximum weight and the excess weight is distributed proportionally among the remaining index constituents. Each Select Sector Index is rebalanced from time to time to re-establish the proper weighting. |

| § | For reweighting purposes, each Select Sector Index is rebalanced quarterly after the close of business on the third Friday of March, June September and December using the following procedures: (1) The rebalancing reference date is the second Friday of March, June, September and December; (2) With prices reflected on the rebalancing reference date, and membership, shares outstanding and investable weight factors as of the rebalancing effective date, each company is weighted by float-adjusted market capitalization methodology. Modifications are made as defined below. |

| (i) | If any Component Stock has a weight greater than 24%, that Component Stock has its float-adjusted market capitalization weight capped at 23%. The 23% weight cap creates a 2% buffer to ensure that no Component Stock exceeds 25% as of the quarter-end diversification requirement date. |

| (ii) | All excess weight is equally redistributed to all uncapped Component Stocks within the relevant Select Sector Index. |

| (iii) | After this redistribution, if the float-adjusted market capitalization weight of any other Component Stock(s) then breaches 23%, the process is repeated iteratively until no Component Stocks breaches the 23% weight cap. |

| (iv) | The sum of the Component Stocks with weights greater than 4.8% cannot exceed 50% of the total index weight. These caps are set to allow for a buffer below the 5% limit. |

| PRS-17 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| (v) | If the rule in step (iv) is breached, all the Component Stocks are ranked in descending order of their float-adjusted market capitalization weights and the first Component Stock that causes the 50% limit to be breached has its weight reduced to 4.5%. |

| (vi) | This excess weight is equally redistributed to all Component Stocks with weights below 4.5%. This process is repeated iteratively until step (iv) is satisfied. |

| (vii) | Index share amounts are assigned to each Component Stock to arrive at the weights calculated above. Since index shares are assigned based on prices one week prior to rebalancing, the actual weight of each Component Stock at the rebalancing differs somewhat from these weights due to market movements. |

| (viii) | If, on the second to last business day of March, June, September, or December, a company has a weight greater than 24% or the sum of the companies with weights greater than 4.8% exceeds 50%, a secondary rebalancing will be triggered with the rebalancing effective date being after the close of the last business day of the month. This second rebalancing will use the closing prices as of the second to last business day of March, June, September or December, and membership, shares outstanding, and IWFs as of the rebalancing effective date. |

At times, Component Stocks may be represented in the Select Sector Indices by multiple share class lines. Maximum weight capping is based on Component Stock float-adjusted market capitalization, with the weight of multiple class companies allocated proportionally to each share class line based on its float-adjusted market capitalization as of the rebalancing reference date. If no capping is required, both share classes remain in the Select Sector Index at their natural float-adjusted market capitalization.

Calculation of the Select Sector Indices

Each Select Sector Index is calculated using the same methodology utilized by S&P in calculating the S&P 500® Index, using a base-weighted aggregate methodology. The daily calculation of each Select Sector Index is computed by dividing the total market value of the companies in the Select Sector Index by a number called the index divisor.

A SPDR® Component Stock which has been assigned to one Select Sector Index may be determined to have undergone a transformation in the composition of its business, and that it should be removed from that Select Sector Index and assigned to a different Select Sector Index. In the event that a SPDR® Component Stock’s Select Sector Index assignment should be changed, S&P will disseminate notice of the change following its standard procedure for announcing index changes, and will implement the change in the affected Select Sector Indexes after the initial dissemination of information on the sector change.

SPDR® Component Stocks removed from and added to the S&P 500® Index will be deleted from and added to the appropriate Select Sector Index on the same schedule used by S&P for additions and deletions from the S&P 500® Index insofar as practicable.

Additional information regarding the calculation and composition of the Select Sector Indices, including the index methodology, may be found on S&P’s website. Information included in that website is not included or incorporated by reference into this document.

| PRS-18 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| United States Federal Tax Considerations |

The following discussion supplements, and to the extent applicable supersedes, the discussion in the accompanying product supplement under the caption “United States Federal Tax Considerations.”

In the opinion of our special U.S. tax counsel, Ashurst LLP, it would generally be reasonable to treat a security with terms described herein as a pre-paid cash-settled derivative contract in respect of the Fund that is treated as an "open transaction" for U.S. federal income tax purposes, and the terms of the securities require a holder (in the absence of a change in law or an administrative or judicial ruling to the contrary) to treat the securities for all tax purposes in accordance with such characterization. However, the U.S. federal income tax consequences of your investment in the securities are uncertain and the Internal Revenue Service (the “IRS”) could assert that the securities should be taxed in a manner that is different from that described in the preceding sentence. If this treatment is respected, a U.S. holder should generally recognize capital gain or loss upon the sale, exchange, redemption or payment on maturity in an amount equal to the difference between the amount it received at such time and the amount that it paid for its securities. Subject to the discussion below under “—Possible Application of Section 1260 of the Code,” such gain or loss should generally be long-term capital gain or loss if the U.S. holder has held the securities for more than one year. Non-U.S. holders should consult the section entitled "United States Federal Tax Considerations - Tax Consequences to Non-U.S. Holders" in the underlying product supplement.

Possible Application of Section 1260 of the Code

It is possible that an investment in the securities will be treated as a “constructive ownership transaction” within the meaning of Section 1260 of the Code. In that case, all or a portion of any long-term capital gain you would recognize in respect of the securities could be recharacterized as ordinary income (the "Excess Gain"). In addition, an interest charge will also apply to any deemed underpayment of tax in respect of any Excess Gain to the extent such gain would have resulted in gross income inclusions for a U.S. holder in taxable years prior to the taxable year of the call, sale, exchange or maturity (assuming such income accrued at a constant rate equal to the applicable federal rate as of the date of call, sale, exchange or maturity). It is possible, for example, that the amount of the Excess Gain (if any) that would be recharacterized as ordinary income in respect of the securities will equal the excess of (i) any long-term capital gain recognized by a U.S. holder in respect of the securities, over (ii) the “net underlying long-term capital gain” (as defined in Section 1260 of the Code) the U.S. holder would have had if the U.S. holder had acquired the Fund at fair market value on the original issue date of the securities for an amount equal to the issue price of the securities and sold the Fund upon the date of call, sale, exchange or maturity of the securities at fair market value. To the extent any gain is treated as long-term capital gain after application of the recharacterization rules of Section 1260 of the Code, such gain would be subject to U.S. federal income tax at the rates that would have been applicable to the net underlying long-term capital gain. The amount of net underlying long-term capital gain may be unclear where a payment at maturity is based on a leverage factor. Unless otherwise established by clear and convincing evidence, the amount of net underlying long-term capital gain is treated as zero.

Under Section 871(m) of the Code, a “dividend equivalent” payment is treated as a dividend from sources within the United States. Such payments generally would be subject to a 30% U.S. withholding tax if paid to a non-U.S. holder. Under U.S. Treasury Department regulations, payments (including deemed payments) with respect to equity-linked instruments (“ELIs”) that are “specified ELIs” may be treated as dividend equivalents if such specified ELIs reference, directly or indirectly, an interest in an “underlying security,” which is generally any interest in an entity taxable as a corporation for U.S. federal income tax purposes if a payment with respect to such interest could give rise to a U.S. source dividend. However, the IRS has issued guidance that states that the U.S. Treasury Department and the IRS intend to amend the effective dates of the U.S. Treasury Department regulations to provide that withholding on dividend equivalent payments will not apply to specified ELIs that are not delta-one instruments and that are issued before January 1, 2027. Based on our determination that the securities are not delta-one instruments, non-U.S. holders should not be subject to withholding on dividend equivalent payments, if any, under the securities. However, it is possible that the securities could be treated as deemed reissued for U.S. federal income tax purposes upon the occurrence of certain events affecting the Fund or the securities (for example, upon the Fund rebalancing), and following such occurrence the securities could be treated as subject to withholding on dividend equivalent payments. Non-U.S. holders that enter, or have entered, into other transactions in respect of the Fund or the securities should consult their tax advisors as to the application of the dividend equivalent withholding tax in the context of the securities and their other transactions. If any payments are treated as dividend equivalents subject to withholding, we (or the applicable withholding agent) would be entitled to withhold taxes without being required to pay any additional amounts with respect to amounts so withheld.

| PRS-19 |

Market Linked Securities—Auto-Callable with Leveraged Upside Participation and Fixed Percentage Buffered Downside Principal at Risk Securities Linked to the Energy Select Sector SPDR® Fund due September 30, 2027 |

| Supplemental Plan of Distribution |

Delivery of the securities will be made against payment therefor on or about the issue date. Under Rule 15c6-1 of the Exchange Act, trades in the secondary market generally are required to settle in one business day, unless the parties to any such trade expressly agree otherwise. Accordingly, purchasers who wish to trade such securities at any time prior to the first business day preceding the issue date will be required, by virtue of the fact that the securities will not settle in T+1, to specify an alternative settlement cycle at the time of any such trade to prevent a failed settlement; such purchasers should also consult their own advisors in this regard.

PRS-20