Exhibit 99.2

| | | | | | | | | | |

| | | | |

| | FINANCIAL RESULTS | | | 2 | | | | | |

| | CHAIRMAN’S REVIEW | | | 4 | | | | | |

| | OPERATIONAL & FINANCIAL REVIEW | | | 6 | | | | | |

| | GLOBAL OPERATIONS | | | 6 | | | | | |

| | GROUP OVERVIEW | | | 8 | | | | | |

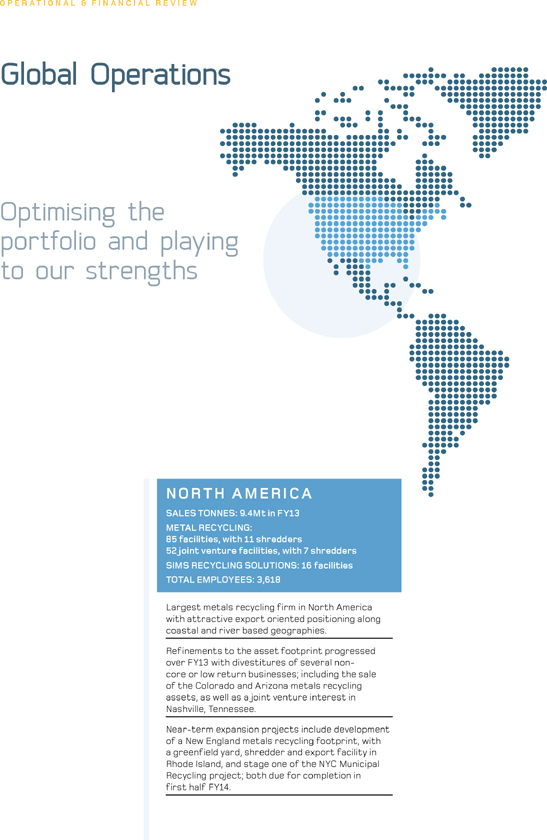

| | NORTH AMERICA | | | 10 | | | | | |

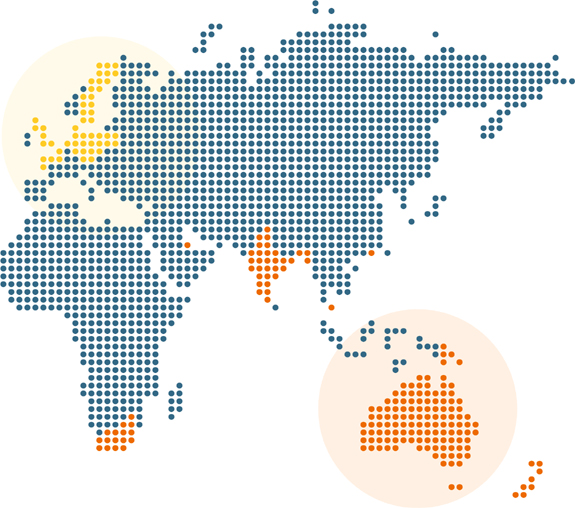

| | EUROPE | | | 12 | | | | | |

| | AUSTRALASIA | | | 14 | | | | | |

| | SUSTAINABILITY | | | 16 | | | | | |

| | FINANCIAL REVIEW | | | 20 | | | | | |

| | CORPORATE GOVERNANCE STATEMENT | | | 22 | | | | | |

| | DIRECTORS’ REPORT | | | 33 | | | | | |

| | BOARD OF DIRECTORS | | | 36 | | | | | |

| | REMUNERATION REPORT | | | 38 | | | | | |

| | FINANCIAL STATEMENTS | | | 57 | | | | | |

| | OTHER INFORMATION | | | 121 | | | | | |

| | DIRECTORS’ DECLARATION | | | 120 | | | | | |

| | INDEPENDENT AUDITOR’S REPORT | | | 121 | | | | | |

| | AUDITOR’S INDEPENDENT DECLARATION | | | 122 | | | | | |

| | ANNUAL FINANCIAL REPORT EXTRACTS | | | 123 | | | | | |

| | SHAREHOLDER INFORMATION | | | 127 | | | | | |

| | FIVE YEAR TREND SUMMARY | | | 128 | | | | | |

| | CORPORATE DIRECTORY | | | IBC | | | | | |

PREPARED FOR TODAY.

POSITIONED FOR TOMORROW.

Sims Metal Management is the world’s largest listed metal and electronics recycler with approximately 270 facilities and 6,400 employees globally. Our mission is to drive the highest possible returns for shareholders through lowest cost material processing and best-in-class trading platforms. Our commitment to employees is to create a zero-harm workplace, while being exemplary community members and responsible stewards of the environment.

Financial Results

| | | | | | | | | | | | |

| YEAR ENDED 30 JUNE (A$m) | | FY 2013 | | | FY 2012

Restated | | | Change (%) | |

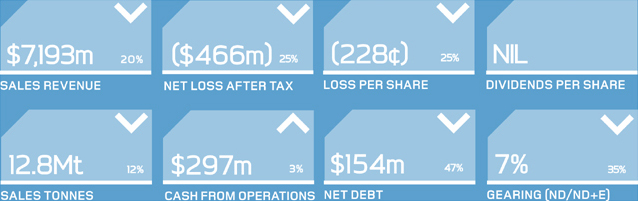

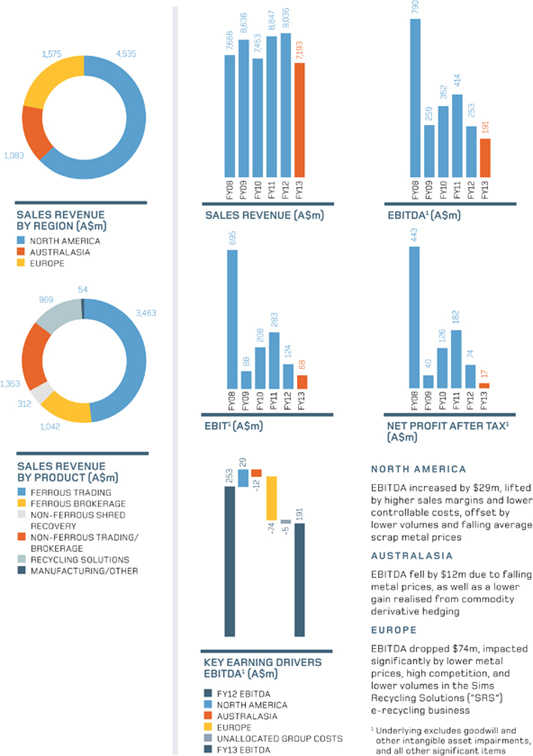

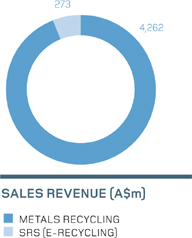

Sales Revenue | | | 7,193.0 | | | | 9,035.7 | | | | (20.4) | |

EBITDA | | | (41.5) | | | | 182.2 | | | | (122.8) | |

Underlying EBITDA1 | | | 191.4 | | | | 253.4 | | | | (24.5) | |

Goodwill & Intangible Asset Impairment | | | 304.4 | | | | 675.6 | | | | (54.9) | |

Depreciation | | | 101.1 | | | | 103.1 | | | | (1.9) | |

Amortisation | | | 22.4 | | | | 26.8 | | | | (16.4) | |

EBIT | | | (469.4) | | | | (623.3) | | | | (24.7) | |

Underlying EBIT1 | | | 67.9 | | | | 123.5 | | | | (45.0) | |

Net Interest Expense | | | (17.6) | | | | (21.2) | | | | (17.0) | |

Tax Benefit | | | 20.9 | | | | 22.0 | | | | (5.0) | |

Underlying Tax (Expense)1 | | | (33.2) | | | | (28.3) | | | | 17.3 | |

NPAT | | | (466.1) | | | | (622.5) | | | | (25.1) | |

Underlying NPAT1 | | | 17.1 | | | | 74.0 | | | | (76.9) | |

EPS (cents per share) – Diluted | | | (228.1) | | | | (302.4) | | | | (24.6) | |

Underlying EPS (cents per share) – Diluted1 | | | 8.3 | | | | 35.6 | | | | (76.7) | |

Full Fiscal Year Dividend (cents per share) | | | 0.0 | | | | 20.0 | | | | (100.0) | |

Total Assets | | | 2,916.8 | | | | 3,509.0 | | | | (16.9) | |

Total Liabilities | | | 988.0 | | | | 1,225.3 | | | | (19.4) | |

Net Assets | | | 1,928.8 | | | | 2,283.7 | | | | (15.5) | |

Net Debt | | | 153.8 | | | | 292.2 | | | | (47.4) | |

Net Debt/(Net Debt + Equity) (%) | | | 7.4 | | | | 11.3 | | | | NMF | |

Net Tangible Assets | | | 1,664.9 | | | | 1,710.8 | | | | (2.7) | |

Net Tangible Assets per share (A$ per share) | | | 8.15 | | | | 8.35 | | | | (2.4) | |

Net Cash Inflow From Operating Activities | | | 297.3 | | | | 289.6 | | | | 2.7 | |

Capital Expenditures | | | 149.0 | | | | 161.1 | | | | (7.5) | |

Net Cash Outflow From Investing Activities | | | (118.8) | | | | (342.6) | | | | (65.3) | |

Net Cash Inflows (Outflows) From | | | | | | | | | | | | |

Operating & Investing Activities | | | 178.5 | | | | (53.0) | | | | NMF | |

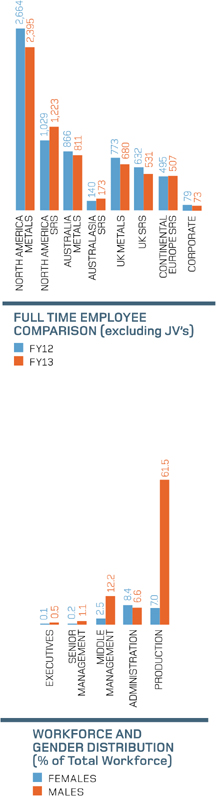

Employees | | | 6,393 | | | | 6,678 | | | | (4.3) | |

Intake Tonnes (‘000) | | | 12,453 | | | | 14,386 | | | | (13.4) | |

Sales Tonnes (‘000) | | | 12,786 | | | | 14,503 | | | | (11.8) | |

| 1 | Underlying excludes goodwill and other intangible asset impairments, and all other significant items |

NMF = Not meaningful percentage change

FY 2013 ANNOUNCEMENTS

23 AUGUST 2012

Sims Metal Management (SMM) announced underlying profit after tax of $74 million, excluding significant items, for the year ended 30 June 2012.

3 DECEMBER 2012

SMM announced the sale of its Metal Recycling assets in Arizona to the Company’s JV partner SA Recycling for uS$35 million.

19 DECEMBER 2012

SMM announced a trading update.

21 JANUARY 2013

SMM announced it had identified the carrying value of inventory in its UK business had been overstated, and that a Special Committee had been formed to investigate the cause and scope of the issue.

15 FEBRUARY 2013

SMM issued the conclusion of the Special Committee investigation into UK issues, previously announced 21 January 2013. the Special Committee determined a $78 million write-down of inventory would be taken. no other control issues existed at sites outside of the UK, and corrective actions are being implemented.

15 FEBRUARY 2013

SMM announced impairment charges related to goodwill and other intangible assets of $354 million. $291 million of the charge relating to north America Metals to be recorded in the FY2013 result, with $63 million of the impairment relating to UK Metals and UK SRS, to be reflected in the restatement of results for prior periods.

22 FEBRUARY 2013

SMM announced underlying profit after tax of $10 million, excluding significant items, for the half year ended 31 December 2012.

22 FEBRUARY 2013

SMM announced the retirement of Group CEO Daniel W. Dienst, effective 30 June 2013.

20 MARCH 2013

SMM announced CEO europe and Global SRS Graham Davy had left the Company, effective immediately.

15 MAY 2013

SMM announced UK restructuring charges of $115 million.

C H A I R M A N’S R E V I E W

Chairman’s Review

GEOFFREY N BRUNSDON

The past year was a challenging one for the Company as it continued to face weak commodity markets and intense competition for raw materials. At the same time we have been managing significant organisational change.

In all the markets in which we operate, we have been reducing costs and improving operational efficiency. We made a number of divestments of under-performing and non-core assets in the united States and Australia, as well as a substantial restructure of the united Kingdom (UK) operations. The positive impact of these initiatives are intended to deliver considerable value in FY14 and will position us to take advantage of increased volumes as economic activity in our key markets recover.

FINANCIAL PERFORMANCE

Sales revenue of $7.2 billion in FY13 compared with $9.0 billion in the prior year. The decrease in sales revenue was as a result of a combination of lower average ferrous and non-ferrous scrap prices as well as lower sales volumes, which decreased 12% on the prior year to 12.8 million tonnes.

Underlying earnings before interest, tax, depreciation and amortisation (EBITDA) of $191 million was 24% lower than FY12, primarily due to weak business conditions, which led to intensified competition for the limited supply of raw materials. In Europe especially, lower non-ferrous and precious metal prices negatively impacted our e-recycling business (SRS), compressing margins. These adverse impacts were partially offset in FY13 by improving sales margins in North America and lower underlying controllable costs of $45 million versus FY12.

Cash flow from operating activities of $297 million in FY13 was higher by $8 million versus FY12, highlighting the significant cash generating capacity of the business. Strong cash flows assisted in materially reducing net debt, which declined by $138 million, to $154 million, bringing gearing to 7.4% of total capitalisation as at 30 June 2013.

Maintaining low gearing is a focus of the Company, especially in tough economic times as currently exists in our industry. The Group’s strong cash flow and low gearing provides the capacity to fund ongoing operational requirements of the business, as well as potential increased working capital requirements, as and when industry conditions improve.

The Company’s FY13 financial results were considerably impacted by a number of adverse significant items totaling $537 million ($483 million after-tax). Goodwill impairment charges of $292 million made up just over half of these charges, principally relating to our business in North America. Impairments associated with our inventory write down in the UK and subsequent organisational changes also contributed materially to significant items. Statutory net profit after tax (NPAT), inclusive of significant items, was a loss of $466 million. Excluding significant items, underlying NPAT was $17 million, 77% lower than FY12.

SAFETY

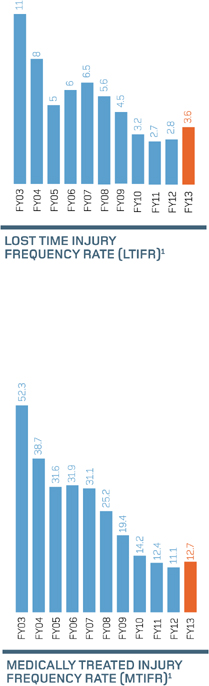

Safety remains the Company’s first priority from which all operational activities must take their lead. During FY13, over 100,000 safety conversations were undertaken, recorded and analysed across all regions. Safety-based training also comprises a substantial part of the nearly 280,000 hours of employee training delivered annually across the Group. While we achieved a promising 9% reduction in the total injury frequency rate during FY13, compositionally LTI and MTI frequency rates increased to 3.6 from 2.8, and to 12.7 from 11.1 in FY13 respectively. This trend is not acceptable, and the Board and management remain committed to our unrelenting focus on safety.

UK SPECIAL COMMITTEE

During the first half of FY13, senior management and the Board identified a breakdown in the Company’s internal control environment in the UK, leading to a significant overstatement of the value of inventories at two UK-based facilities. In response, the Board formed a Special Committee to investigate the root cause of this breakdown, take rapid remedial action, and oversee disciplinary actions where required. Following the investigation, the Special Committee was able to conclude that the control breakdown, and conditions which allowed the overstatement to occur, were isolated to the UK. Substantial progress has been made in the implementation of the Group’s standard inventory controls across the UK business. The effectiveness of the recently strengthened control environment in the UK will be subject to detailed internal audit review during FY14.

ABOVE CLAREMONT TERMINAL,

NEW JERSEY, US – METALS RECYCLING

MIDDLEST MARY’S, NEW SOUTH WALES, AUSTRALIA – METALS RECYCLING

BELOW NEWPORT, UK – METALS RECYCLING

MANAGEMENT TRANSITION

The past year was also a period of substantial management change. After leading the organisation since the merger of Sims Group and Metal Management in 2008, we announced, in February 2013, the retirement of Daniel Dienst as Group CEO, effective 30 June 2013. Following Mr Dienst’s retirement, the Company has been managed through an executive group known as our Global Leadership Team, chaired by myself and including non-executive director Jim Thompson and the leaders of all the Company’s key operations. We continue our international search for a new CEO.

Additionally, in the second half of FY13, new management teams were selected to lead the Global SRS and UK Metals Recycling businesses.

At the Board level, I was pleased to announce the appointment of Robert Bass as a new independent non-executive director, effective 10 September 2013. Mr Bass was a partner at Deloitte & Touche from 1982, and Vice Chairman Deloitte LLP from 2006, until his retirement in June 2012. I am delighted to have Bob serve on the Board, and bring with him his broad commercial experience and financial credentials.

STRATEGY AND OUTLOOK

Leading indicators for scrap generation in our key market of the United States continue to show improvement across new vehicle and major appliance sales, as well as broader US consumer confidence. While these signals are encouraging, they have yet to translate into the generation of higher levels of scrap metal, and the competition for available material remains high. We expect this condition may persist until a more substantial improvement in employment aggregate numbers is seen, and consumer confidence levels rebound beyond what are still historically low levels.

In Europe, economic growth in the UK and Germany continues to track at anemic levels. While it may appear that the worst of the EU financial crisis has passed, we remain mindful from recent experience in the US of the lag which can occur between initial economic recovery and sustainable recovery that impacts scrap generation.

Australia has continued to out-perform other developed economies since the 2009 global financial crisis. However, we are cognisant of the turn of the commodity cycle and the impact on the heavily mining-dependent Australian economy.

Under these uncertain economic conditions, it is critical that the Company manages the aspects of the business within its control. To this end, the Company remains committed to maintaining capital discipline and balance sheet strength, continued attention to reducing controllable costs, and streamlining the business to focus on our higher returning assets. While we expect near-term challenges to persist, we believe we are better prepared and positioned to deal with them.

GEOFFREY N BRUNSDON

CHAIRMAN

| | | | | | | | |

| | | | | | | | AUSTRALASIA SALES TONNES: 1.8Mt in FY13 METAL RECYCLING: 48 facilities, with 5 shredders 9 joint venture facilities, with 2 shredders SIMS RECYCLING SOLUTIONS: 10 facilities TOTAL EMPLOYEES: 984 |

EUROPE SALES TONNES: 1.6Mt in FY13 METAL RECYCLING: 37 facilities, with 3 shredders SIMS RECYCLING SOLUTIONS: 16 facilities TOTAL EMPLOYEES: 1,718 | | | | |

| | | | | Largest metals recycling firm in Australia, with operations extending into New Zealand and Papua New Guinea. FY13 investments in the Australian Metals business include the acquisition of a ferrous metal business in South Australia, a capital upgrade of the St Mary’s facility in New South Wales, and the installation of a downstream non-ferrous extraction system in Victoria. Additional steps were taken to divest non-core manufacturing assets, with the commitment to close the Melbourne-based lead smelting operation. Only a small aluminium smelting operation remains in the manufacturing division. |

Second largest metals recycling firm in the UK, with strategic deep water export capabilities. Controllable cost reductions remained a focus of the UK Metals recycling business throughout FY13. Headcount in the UK Metals business was reduced by 12% with two of five shredders idled and several small yards closed. Initial business review in the European SRS operations has led to action to restructure material flow, reduce headcount, accelerate inventory turnover and close low returning facilities. European SRS headcount reduced by 8% in FY13. | | | | |

O P E R A T I O N A L & F I N A N C I A L R E V I E W

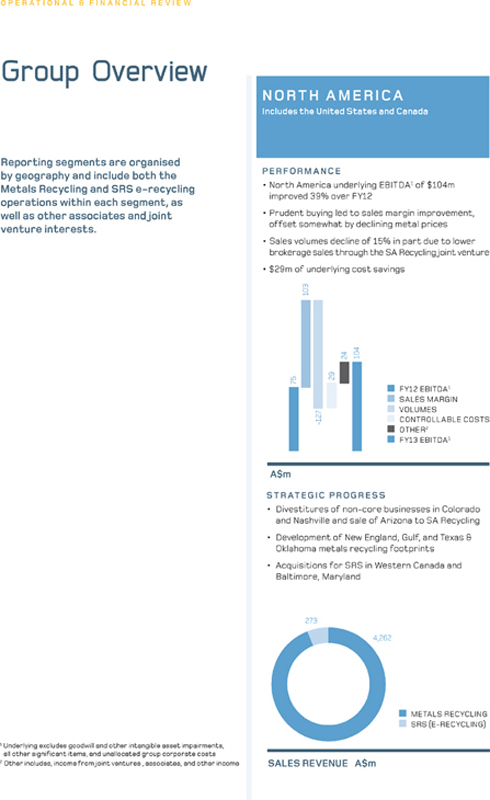

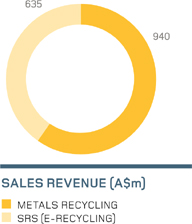

North America

OUR BUSINESS

METALS RECYCLING

North America’s largest metals recycling firm, with over 130 wholly owned and joint venture facilities, specialising in the collection, processing and trading of post-consumer and post-industrial ferrous and non-ferrous scrap metal. export oriented asset positioning along coastal and river based geographies, leveraging emerging market steel making and non-ferrous secondary metals smelting demand.

RECYCLING SOLUTIONS

Sixteen e-recycling facilities across the united States and Canada, specialising in environmentally responsible solutions for the disposal of post-consumer electronic products, including It assets recycled for commercial customers.

RESULTS AT A GLANCE

| | | | | | | | | | | | |

| A$m | | FY 2013 | | | FY 2012 | | | Change (%) | |

| Revenue | | | 4,534.6 | | | | 6,027.0 | | | | (24.8 | ) |

| EBITDA1 | | | 104.4 | | | | 75.1 | | | | 39.0 | |

| EBIT1 | | | 36.7 | | | | (1.5 | ) | | | – | |

| Sales Volumes (Mt) | | | 9.377 | | | | 11.080 | | | | (15.4 | ) |

| Sales Margin (%) | | | 15.4 | | | | 11.7 | | | | – | |

|

1 Underlying excludes goodwill and other intangible asset impairments, all other significant items, and unallocated group corporate costs | |

PERFORMANCE

Sales revenue for the North America region of $4,534.6 million was down 25% on FY12, due to a mix of lower sales tonnes and declines in ferrous and non-ferrous metal prices. Sales volumes slowed significantly in the first half of FY13 due to softer demand in export markets for ferrous scrap metal. The impact of weaker offshore demand during the period contributed to a decline in ferrous brokerage volumes.

Underlying EBITDA of $104.4 million was up 39% on FY12, attributable to increased sales margins and lower underlying controllable costs. Correspondingly, underlying EBITDA margins rose to 2.3% from 1.3% in FY12. Underlying controllable cost savings within the North American Metals business were $48.4 million during FY13. These cost savings are expected to be sustainable at this level until intake volumes change materially. Total controllable cost savings for North America were offset slightly by increased costs from small bolt-on acquisitions made by SRS of Genesis Recycling in British Columbia, Canada and E-Structors in Baltimore, Maryland during FY13.

OPPOSITE PAGE SALT LAKE CITY,

UTAH – METAL RECYCLING

ABOVE CLAREMONT TERMINAL,

NEW JERSEY – METALS RECYCLING

BELOW REDWOOD CITY, CALIFORNIA – METAL RECYCLING

STRATEGIC PROGRESS

Refinements to the North American asset footprint progressed over FY13 with the divestitures of several non-core or low return businesses. These sales included the divestitures of the Colorado and Arizona metals recycling assets, as well as a joint venture interest in Nashville, Tennessee. The Arizona metals recycling assets were sold into the Company’s joint venture, SA Recycling (“SAR”), in order to better leverage SAR’s strong asset footprint in Southern California, Arizona and Nevada.

Capital from these asset sales is being invested in projects anticipated to have higher returns. Near-term projects include the development of a New England metals recycling footprint, with a greenfield yard, shredder and export facility in Rhode Island, and stage one of the NYC Municipal Recycling project; both due to be completed in the first half of FY14.

Subsequent to 30 June 2013, additional divestments have taken place to drive higher returns on the North American asset portfolio. The divestitures in FY14 have related to non-core businesses and included Aerospace Metals, a business focused on the recycling of titanium alloys and high temperature metals; as well as the Birmingham, Alabama shredder and an associated yard, due to limited synergies with the Group’s Gulf and Mississippi river system based assets.

MARKET OUTLOOK

Underlying fundamentals for scrap generation showed improvement in the US during FY13 though scrap generation tends to lag the fundamentals. Consumer confidence, a key leading indicator for consumer scrap creation, reached a five year high in June 2013. Correspondingly, auto and major household appliances sales also increased. New auto sales in the US reached an annualized rate of 15.9 million vehicles in June, up 10% year-over-year. US manufacturer’s shipments of major appliances were up 7% year-to-date in June. Due to the severity of the 2009 US recession and persistently lower employment aggregates post global financial crisis (“GFC”), auto scrapping rates are expected to lag new auto sales. Scrap from auto and major appliances combine to account for 50% to 70% of source material for metal shredders in the US.

Despite improving macro-economic data, installed processing capacity in the US scrap industry remains in excess of scrap generation available for processing, resulting in aggressive competition for scrap intake. Some signals of industry capacity rationalisation are beginning to emerge. A trend has begun to develop amongst metals recycling firms, both in the US and other markets, to address industry overcapacity through cost reductions and facility rationalisation. While these developments are positive for the industry, at present the challenges of excess capacity still persist.

O P E R A T I O N A L & F I N A N C I A L R E V I E W

Europe

OUR BUSINESS

METALS RECYCLING

One of the UK’s largest metals recycling firms, with over 35 wholly owned facilities, specialising in the collection, processing and trading of post-consumer and post-industrial ferrous and non-ferrous scrap metal.

RECYCLING SOLUTIONS

Sixteen e-recycling facilities across the United Kingdom, Sweden, Belgium, the Netherlands, Germany, Poland, the Czech Republic, Hungary, Austria and Croatia, specialising in environmentally responsible solutions for the disposal of post-consumer electronic products, including IT assets recycled for commercial customers.

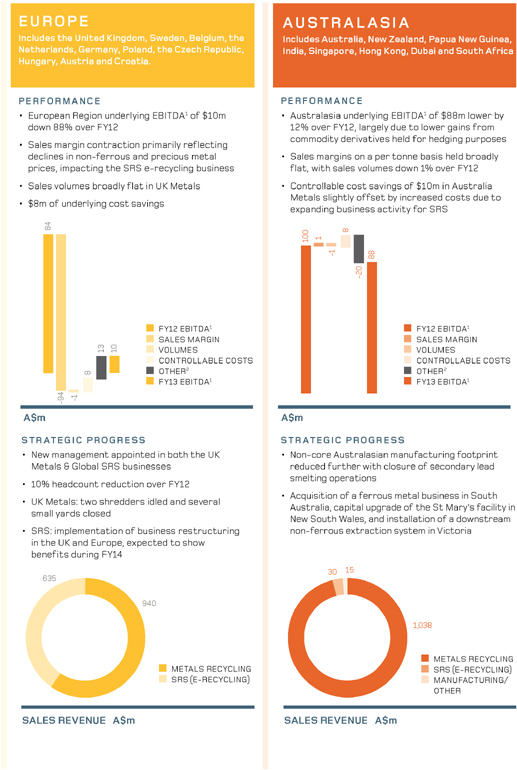

RESULTS AT A GLANCE

| | | | | | | | | | | | |

| A$m | | FY 2013 | | | FY 2012 | | | Change (%) | |

Revenue | | | 1,575.3 | | | | 1,780.6 | | | | (11.5 | ) |

EBITDA1 | | | 10.2 | | | | 84.0 | | | | (87.9 | ) |

EBIT1 | | | (19.2 | ) | | | 56.1 | | | | (134.2 | ) |

Sales Volumes (Mt) | | | 1.645 | | | | 1.651 | | | | (0.4 | ) |

Sales Margin (%) | | | 14.2 | | | | 17.9 | | | | – | |

|

1 Underlying excludes goodwill and other intangible asset impairments, and all other significant items | |

PERFORMANCE

Sales revenue for the Europe region of $1,575.3 million was down 12% on FY12, due to lower sales volumes and lower commodities prices. UK Metals Recycling sales volumes were broadly flat compared to the prior year at 1.65 million tonnes.

Underlying EBITDA of $10.2 million was down 88% relative to FY12, due to several factors including: 1) sustained weak scrap generation in the UK which elevated competition across both the traditional metals recycling and the SRS e-recycling businesses, 2) lower non-ferrous and precious metal prices which decreased metal recovery margins in the SRS business, and 3) negative impact from lower average ferrous scrap metal prices causing sales margins to decline in the UK Metals business. Underlying controllable cost savings in the UK Metals business were $1.3 million in FY13.

OPPOSITE PAGE NEWPORT, UK –

METALS RECYCLING

ABOVE PETERBOROUGH, UK –

METALS RECYCLING

BELOW NEWPORT, UK – SRS E-RECYCLING

UK SPECIAL COMMITTEE

On 21 January 2013, the Board formed a Special Committee to investigate inventory write-downs in the UK. As a result of the findings of the Special Committee, substantial progress has been made in the implementation of the Group’s standard inventory controls in the UK operations. The operation of the control environment will be subject to detailed internal audit review during FY14.

STRATEGIC PROGRESS

Towards the end of the second half of FY13, business reviews were completed under the direction of Group management which resulted in inventory and asset write-downs, and costs related to restructuring actions in the UK operations. The implementation of the findings of the business review led to a contraction of the UK Metals operations, including headcount reductions and consolidation of shredding activities at Newport into nearby Avonmouth. In total, headcount in the UK Metals business was reduced by 13% during FY13 with two shredders idled and several small yards closed. Furthermore, the UK SRS business is being repositioned towards a lower working capital and higher turnover model, while looking at additional strategies to further decrease operational costs. Headcount was reduced in the UK SRS operations by 16%, with the majority of these reductions taking place in the second half of FY13. Management believes initial restructuring actions have stabilised the business and should lead to improved outcomes in FY14.

Complimenting these actions, at the end of FY13 new management was appointed for both the UK Metals and Global SRS businesses as management realignment separated these businesses to enhance operational focus. The new management teams will continue to examine further cost saving opportunities across the European businesses as a priority during FY14.

MARKET OUTLOOK

Economic conditions in the UK and Europe remained extremely challenging during FY13. Consumer confidence in the UK persisted near post GFC lows for the majority of the year, with GDP growth continuing to languish at anemic levels. Low scrap arisings intensified competition for raw materials for the UK Metals Recycling business, placing pressure on margins. Operations at several of the Company’s small inefficient feeder yards have been consolidated. The idling of two shredders, and shifting material to the remaining three shredders, is expected to result in higher utilisation rates for active operations. Further to the actions already taken, the new UK Metals management team appointed at the end of FY13, is conducting a detailed review of the business to respond to these market challenges.

O P E R A T I O N A L & F I N A N C I A L R E V I E W

Australasia

OUR BUSINESS

METALS RECYCLING

Australia’s and New Zealand’s leading metals recycling firm, with over 55 wholly owned and joint venture facilities, specialising in the collection, processing and trading of post-consumer and post-industrial ferrous and non-ferrous scrap metal.

RECYCLING SOLUTIONS

Ten e-recycling facilities across Australia, New Zealand, Singapore, India, Dubai, and South Africa, specialising in environmentally responsible solutions for the disposal of post-consumer electronic products, including IT assets recycled for commercial customers.

MANUFACTURING AND OTHER

As of 30 June 2013, the manufacturing division is composed solely of a small aluminium smelting facility. Also included within Australasia is a 16% interest in China-based metals recycling firm CTG and a 50% interest in Australian renewable energy company LMS Energy Pty Ltd.

RESULTS AT A GLANCE

| | | | | | | | | | | | |

| | | | |

| A$m | | FY 2013 | | | FY 2012 | | | Change (%) | |

| Revenue | | | 1,083.1 | | | | 1,228.1 | | | | (11.8 | ) |

| EBITDA1 | | | 87.7 | | | | 99.5 | | | | (11.8 | ) |

| EBIT | | | 61.7 | | | | 74.6 | | | | (17.2 | ) |

| Sales Volumes (Mt) | | | 1.764 | | | | 1.772 | | | | (0.5 | ) |

| Sales Margin (%) | | | 23.9 | | | | 21.1 | | | | – | |

|

1 Underlying excludes goodwill and other intangible asset impairments, and all other significant items | |

PERFORMANCE

Sales revenue for the Australasia region of $1,083.1 million was down 12% on FY12, due to lower ferrous and non-ferrous scrap metal prices, while sales volume remained broadly unchanged. Underlying EBITDA of $87.7 million was down 12% compared to FY12, primarily due to lower gains from commodity derivatives held for hedging purposes in FY13.

Underlying EBITDA margins held steady at 8.1% due to the offsetting compression in revenue and underlying EBITDA. Underlying controllable cost reductions in the Australia Metals Recycling business were $10.0 million for FY13. These cost savings are expected to be sustainable at this rate based on current activity levels.

OPPOSITE PAGE BROOKLYN, VICTORIA – METAL RECYCLING

ABOVE CAR BODY STACK – METALS RECYCLING

MIDDLE ST MARY’S – NEW SOUTH WALES, METALS RECYCLING

BELOW HAMPTON PARK – SOUTH AUSTRALIA, LMS ENERGY

JOINT VENTURES AND ASSOCIATES

With 20 operating projects in Australia, the Company’s joint venture LMS Energy Pty Ltd (LMS), generated in excess of 340,000 megawatt hours in FY13, the equivalent to power approximately 50,000 homes. Moreover, LMS generated over 340,000 Large-Scale Generation Certificates, and abated an estimated 2,000,000 tonnes (CO2e) of carbon during FY13.

Earnings from the Company’s 16% ownership stake in China-based metals recycling firm Chiho-Tiande Group (CTG) were impacted by net losses at CTG for the six month period ending 30 June 2013. Due to net losses, and a corresponding decline in the CTG share price, the Company took a charge of $14.9 million to record impairment in the CTG investment, and incurred $21.3 million of charges related to the write-down of derivatives held in CTG and equity accounted losses in FY13.

STRATEGIC PROGRESS

Refinements to the Australasia asset footprint continued to occur over FY13. Further investments were made into the Australian Metals business with the acquisition of a ferrous metal business in South Australia, a capital upgrade of the St Mary’s facility in New South Wales, and the installation of a downstream non-ferrous extraction system in Victoria.

Additionally, steps were taken to further contract the Australian manufacturing operations including the commitment to close the non-core lead smelting operation. Only a small aluminium smelting facility in Melbourne, Australia currently remains in the manufacturing division.

MARKET OUTLOOK

Business activity driving scrap generation in Australia continues to track below mid-cycle levels. Consumer sentiment fell for the second consecutive year in FY13 and GDP growth began to slow due to a decline in commodity prices and mining activity. Key drivers of scrap generation, manufacturing and construction, remain severely depressed. Australian manufacturing PMI data for July 2013 indicated its 25th consecutive month in contraction territory, while Australian construction PMI data in June 2013 entered its 37th uninterrupted month of contraction. The Australian management team has responded to these challenges by reducing operating shifts and headcount, and temporarily idling yards where necessary.

O P E R A T I O N A L & F I N A N C I A L R E V I E W

Sustainability

HIGHLIGHTS

ENVIRONMENT

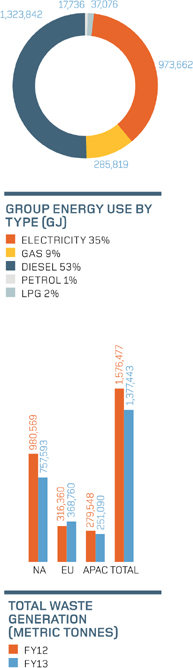

Waste generation reduced by 13% over FY12 to 1.38 million tonnes, related to significant waste reductions in Australasia and North America.

HEALTH AND SAFETY

Group LTIFR increased from 2.8 in FY12 to 3.6 in FY13 and MTIFR from 11.1 in FY12 to 12.7 in FY13.

PEOPLE AND DIVERSITY

Encouring diversity among its workforce saw the percentage number of females employed by the Group lift from 17% to 18%.

COMMUNITY ENGAGEMENT

The Company has a particular focus on engaging with people in the localities of its operations, and sponsors hundreds of projects each year.

The sustainability agenda is crucial to how we measure and manage all the non-financial components of our activities. Our workforce has a strong affinity with these issues, realising the importance they play in how we conduct ourselves as a public company.

| | | | | | | | | | | | | | |

| | | | | |

| KEY PARAMETERS/ REGION | | FY13 | | | FY12 | | | CHANGE% | | | TREND |

Energy Use (GJ) | | | | | | | | | | | | | | |

North America Total | | | 1,597,189 | | | | 1,746,250 | | | | -9 | | | i |

Europe and UK Total | | | 520,407 | | | | 465,577 | | | | 12 | | | h |

Asia Pacific Total | | | 520,538 | | | | 517,318 | | | | 1 | | | h |

Group Total | | | 2,638,134 | | | | 2,729,145 | | | | -3 | | | i |

CO2 Emissions (tCO2 e) | | | | | | | | | | | | | | |

North America Total | | | 142,162 | | | | 153,681 | | | | -7 | | | i |

Europe and UK Total | | | 48,307 | | | | 42,108 | | | | 15 | | | h |

Asia Pacific Total | | | 63,188 | | | | 60,426 | | | | 5 | | | h |

Group Total | | | 253,657 | | | | 256,215 | | | | -1 | | | i |

Scope 1 | | | 111,131 | | | | 117,886 | | | | -6 | | | i |

Scope 2 | | | 142,526 | | | | 138,329 | | | | 3 | | | h |

Water Consumption (Mega Litres) | | | | | | | | | | | | | | |

North America Total | | | 527.8 | | | | 652.6 | | | | -19 | | | i |

Europe and UK Total | | | 141.6 | | | | 101.3 | | | | 40 | | | h |

Asia Pacific Total | | | 82.5 | | | | 105.0 | | | | -21 | | | i |

Group Total | | | 751.9 | | | | 858.9 | | | | -12 | | | i |

Waste Generation (Tonnes) | | | | | | | | | | | | | | |

North America Total | | | 757,593 | | | | 980,569 | | | | -23 | | | i |

Europe and UK Total | | | 368,760 | | | | 316,360 | | | | 17 | | | h |

Asia Pacific Total | | | 251,090 | | | | 279,548 | | | | -10 | | | i |

Group Total | | | 1,377,443 | | | | 1,576,477 | | | | -13 | | | i |

Key OH&S Indicators | | | | | | | | | | | | | | |

Group LTIFR (LTIx1,000,000/exposed hours) | | | 3.6 | | | | 2.8 | | | | 29 | | | h |

Group MTIFR (MTIx1,000,000/exposed hours) | | | 12.7 | | | | 11.1 | | | | 14 | | | h |

Number of employees | | | | | | | | | | | | | | |

Male | | | 5,243 | | | | 5,518 | | | | -5 | | | i |

Female | | | 1,150 | | | | 1,160 | | | | -1 | | | i |

Group Total | | | 6,393 | | | | 6,678 | | | | -4 | | | i |

Training | | | | | | | | | | | | | | |

Group Total Hours (Corporate training only) | | | 277,142 | | | | 259,519 | | | | 7 | | | h |

ENVIRONMENT

ENERGY, FUEL AND ELECTRICITY

The total energy use of the Group for FY13 was 2,638,134 GJ, a 3% decrease compared to FY12. This was in part due a decrease in total annual production, as well as continued energy efficiency measures. Overall energy usage profile remained unchanged from FY12, with diesel fuel as the highest component at 53% followed by electricity at 35%. Gas accounted for a total of 9%, with LPG and petrol at 2% and 1% respectively. The Company continually seeks to reduce energy use and find alternative energy sources where operationally and financially viable. Notable projects in FY13 include:

North America: A significant upgrade of mobile equipment to new units, comprising Tier 4 diesel engines combined with other initiatives resulted in a greater than 20% reduction in weighted average hourly diesel consumption in the replaced equipment.

Europe: The UK continued its program of replacing its forklift fleet with highly efficient hybrid units, promising fuel efficiencies of between 30% to 38%. Newly installed management systems also provide real-time data, improving idle time and better fuel use management.

Australasia: With shredders accounting for the majority of electricity usage, work continued to improve efficiency in these units, including improved magnetic and air separation systems.

CARBON FOOTPRINT

The Company’s Environmental and Carbon Emissions Policies set the global framework and expectations for energy and carbon reduction efforts, which apply to all activities. Energy consumed by our operations results in the emission of carbon, either directly from the conversion of fuel in our equipment, such as mobile plant, trucks and smelting (Scope 1) or indirectly through the use of externally produced electricity (Scope 2).

Total Group CO2 emissions for FY13 were 253,657 tonnes, down 1% compared to FY12. A small increase in Scope 2 (3%) was offset by a larger decrease in Scope 1 (6%). Electricity was the largest contributor at 54%, followed by diesel at 39%, gas at 5%, with minor contributions from petrol and LPG at 1% each.

Currently, the Company is not subject to the Australian carbon tax and an impost on carbon remains off the federal US policy agenda. The UK operations are affected by the CRC Energy Efficiency Scheme, under which carbon offsets must be purchased annually to offset our energy profile. At the present time, these credits are issued at a fixed cost by the UK government at £12/tonne of CO2e emitted. The stated policy intention is to move to a free carbon market, at which point the Company would need to engage in trading of carbon offsets.

GREEN ENERGY

Our affiliated renewable energy company LMS generated in excess of 340,000MWh of renewable energy during FY13, or close to half of what was consumed by the entire Sims Metal Management Group. This resulted in the creation of a similar amount of Large-Scale Generation Certificates, also known previously as Renewable Energy Certificates. Combined, the renewable energy projects of LMS abated an estimated 2,000,000 tonnes of CO2e during FY13 as LMS continued its expansion of renewable energy facilities.

WATER USE

The Company’s total water consumption profile is relatively small, particularly when compared to industry peers. The majority of our operations are collection yards, where a relatively minor supply of potable water is required for human consumption and ablution. Where water is used for processing purposes, storm water is harvested, where possible, within the facility’s boundaries. Global consumption continued to decrease with 752 Mega litres used, down 12% from 859 Mega litres in FY12.

WASTE GENERATION AND MANAGEMENT

During FY13, the Company generated 1.38 million tonnes of non-usable waste, down 13% on FY12. This was mainly related to significant waste reductions in Australasia and North America, partially offset by increases in Europe from residual waste generated through new plastics and glass recovery processes. Of total waste, 99.4% was non-hazardous, primarily from metal shredding and mostly used for beneficial landfill applications. A small proportion of waste (0.6%) is classified as hazardous, a slight increase on FY12 due to statutory reclassifications of some waste materials.

The Company continues to invest in sophisticated separation technologies. These recover miniscule metallic elements from our processing lines, separating re-usable waste for use in the construction industry, and further refining the extraction of pure and valuable plastics polymers for re-use. Our recently commissioned CRT glass recovery process, in which the hitherto problematic leaded and optical glass component in televisions and monitors is mechanically processed, cleaned and separated in a high volume environment, produces decontaminated high specification glass.

O P E R A T I O N A L & F I N A N C I A L R E V I E W

Sustainability

| 1 | Calculated as the medically treated injuries multiplied by 1 million and divided by the hours worked |

HEALTH AND SAFETY

Safety remains the Company’s first priority from which all other operational activities must take their lead. undertaking all tasks in a safe manner is a non-negotiable work condition and an integral responsibility of every employee, contractor and visitor. During FY13, a total of 104,146 safety conversations were undertaken, recorded and analysed across all regions, the vast majority reflecting positive safety behaviour. These, as well as observed unsafe acts and near misses, provide a valuable insight into where potential issues can arise, allowing us to focus our training and safety delivery accordingly. Every employee can access this information, benefiting from safety experiences across the Group. Considerable training is provided to support these efforts, accounting for a substantial part of the nearly 280,000 hours of corporate training delivered in FY13.

Despite all these efforts, we experienced an unfortunate reversal of our consistent historical decrease in safety statistics in FY13. Group LTIFR increased from 2.8 in FY12 to 3.6 in FY13 and MTIFR from 11.1 in FY12 to 12.7 in FY13. While the overall severity of injuries decreased, this trend is not acceptable. Hence, we will continue to build on our leadership, training and systems to achieve the crucial transformation of where a culture of looking after yourself and your work colleagues is second nature, and any incident is an unacceptable occurrence.

Further enhancing the Company-wide safety framework, each region continues to implement and pursue initiatives of specific relevance to its safety journey. Specific regional safety initiatives included:

North America Metals: SAAFE – “Safe Acts Are For Everyone”, continues to be the main safety platform for strong integration of safety measures into all aspects of operational activities. Several areas were targeted for improvement in FY13, including expanding the use of Operational Behavioural Audits (OBA’s) and specifically targeting higher risk operational activities. The use of “Controlled Access” in shredder stockpile areas was introduced, with all non-essential worker access being restricted and requiring escort. Of particular focus was the use of behavioural tools, OBA’s, Incident Investigation, Hazard Identification and reporting, as well as improving the quality of root cause analysis and associated corrective actions.

UK Metals and SRS Global: The SimsMMway, the core safety platform, was expanded to include all aspects of SHEC as well as including our previously introduced “Take Five”, a simple reminder to all employees of taking 5 SHEC issues on board and doing something about them. Documentation was also significantly shortened to make it more accessible and with an increased focus on outcomes. In line with these revisions, all Annual Site Safety Plans were also revised to include all aspects of SHEC. In respect of SRS Global, the 5S program was successfully introduced, showing immediate benefits to housekeeping and an associated drop in slips, trips and fall injuries.

Australia and New Zealand Metals: The development and implementation of a National Injury Management Manual was undertaken, with associated training of supervisors and yard managers. There was also a specific focus to improve the quality of OBA’s and FY13 saw the introduction of a national Safety Observational Behavioural competency training package for supervisors and managers. The Rapid Induct Management system used for safety induction of contractors was further enhanced to enable a more thorough and automated process to manage all contractors that enter our yards.

| | |

| | PEOPLE AND DIVERSITY DIVERSITY AND RETENTION During FY13, the Company undertook significant restructuring efforts reducing its overall workforce from 6,678 to 6,393 employees, excluding JV operations. Despite these changes, we remained focused on encouraging diversity among our workforce. In FY13, the percentage number of females employed increased to 18.0% from 17.4% the prior year. While the Company overall remains predominately male, because of our industrial nature, females account for more than 55% of our administration sector. Staff leaving voluntarily fell slightly to 16.4% from 18.1% in FY12, while redundancies increased to 8.3% from 5.3% due to our business restructuring activities. TRAINING AND DEVELOPMENT Training and development is a significant contributor to the Company’s ability to attract new talent, while at the same improving the skills and knowledge of our dedicated workforce. During FY13, 277,142 hours of specialist training were delivered, in addition to on-the-job training and general skills improvement. Management training covered subjects such as leadership and strategy, time management, and innovation to name a few. At a technical level, training centred on enhancement skills, such as commodities trading, metal theft and finance. Additionally, mandatory training on anti-corruption and information security, and Code of Conduct training was undertaken. COMMUNITY ENGAGEMENT As the world’s largest listed metals and electronics recycler, the Company’s knowledge of how to preserve and re-use materials is sought by governments, environmental groups and NGO’s alike. We work closely with governments on a range of issues from how levels of recycling in the community can be increased, to what is technically and economically feasible for the conservation of rare compounds used in high tech applications. At the NGO level, the Company works with a range of environmental advocacy groups, including the Baykeeper, Clean up the World and the Total Environment Centre. The Company is also a prominent member of the Bureau of International Recycling (BIR), Institute of Scrap Recycling Industries (ISRI), British Metal Recycling Association (BMRA) and the Australian Council of Recycling (ACOR), as well as many other organisations that seek to engage government, the press and community on issues related to the importance of recycling and waste reduction. The Company has a particular focus on engaging with people in the localities of our operations. There are hundreds of projects each year, ranging from sponsoring local events, to allowing the emergency services to practice fire and car rescue scenarios as well as helping people in distress or need. The following examples are a small selection of such local engagement: North America: Sims Metal Management was approached by Mayor Corey Booker in Newark, New Jersey, to support “Jewellery for a Cause”. Guns used in crimes are shredded and melted down, made into jewellery and sold to fund anti-crime charities in the City of Newark. Europe: Sims Metal Management UK was instrumental in getting the UK government to introduce new legislation banning all cash transactions for scrap to combat metal theft and was also the first UK company to introduce cashless transactions. Australasia: In Queensland, the Company supports the Oxley Creek Catchment Association, participating in a range of community events, including native species tree planting, rubbish removal, weed clearing and water sampling with the help of Watson Road Primary School children. |

O P E R AT I O N A L & F I N AN C I A L R E V I E W

Financial Review

REVENUE

Sales revenue of $7,193.0 million in FY13 was down 20% compared to FY12. The decrease in sales revenue was due to lower average ferrous and non-ferrous scrap prices as well as lower sales volumes which decreased 12% versus FY12.

EARNINGS

Statutory NPAT was a loss of $466.1 million. underlying NPAT was $17.1 million, 77% lower than FY12. The principal difference between the statutory and underlying results is accounted for by goodwill impairment charges taken primarily in the first half of FY13. Statutory EBITDA for FY13 was a loss of $41.5 million, 123% lower than FY12. Underlying EBITDA of $191.4 million was 24% lower than FY12. The decline in underlying EBITDA was primarily due to weak business conditions, especially in Europe, leading to intensified competition for the limited supply of unprocessed raw materials. Additionally, lower non-ferrous and precious metal prices negatively impacted the global SRS e-recycling business, decreasing the value of processed material and compressing margins.These adverse impacts were partially offset by improving sales margins in North America and lower underlying controllable costs of $44.9 million versus FY12.

RECONCILIATION OF STATUTORY NPAT TO EBITDA

| | | | | | | | |

| A$m | | FY13 | | | FY12 | |

Net Loss after tax | | | (466.1 | ) | | | (622.5 | ) |

Goodwill and intangible impairment charges | | | 304.4 | | | | 618.1 | |

Impairment of goodwill in jointly controlled entity | | | – | | | | 57.5 | |

Depreciation and amortisation | | | 123.5 | | | | 129.9 | |

Interest expense, net | | | 17.6 | | | | 21.2 | |

Income tax benefit | | | (20.9 | ) | | | (22.0 | ) |

EBITDA | | | (41.5 | ) | | | 182.2 | |

Depreciation and amortisation declined by $6.4 million to $123.5 million, while net interest expense decreased by $3.6 million to $17.6 million in FY13. The reduction in net interest expense reflects the decline in net debt during the period.

Statutory loss per share decreased to a loss of 228.1 cents from a loss of 302.4 cents in FY12. Underlying earnings per share decreased by 77% to 8.3 cents. Net debt as at 30 June 2013 was $153.8 million, a reduction of $138.4 million from 30 June 2012.

The Company’s dividend policy is to distribute 45% to 55% of NPAT, subject to the Board’s discretion. In the absence of statutory NPAT, after looking through goodwill impairment, the Company determined not to pay a final dividend for FY13. The Company’s dividend policy remains unchanged.

CASH FLOW AND BORROWINGS

Cash flow from operating activities of $297.3 million in FY13 increased by $7.7 million versus FY12 due to lower working capital, and lower net interest and tax payments.

Working capital decreased compared with 30 June 2012. Inventory and trade and other receivables decreased by $266.7 million and $67.5 million respectively, while trade and other payables decreased by $131.1 million.

Capital expenditures were $149.0 million during FY13. Significant capital projects included:

| • | | New England metals recycling footprint build out of three greenfield facilities centered around Providence, Rhode Island including: a non-ferrous yard at Fields Point, a yard and shredder in Johnston, and an export facility at Providence port. All facilities are due to be fully operational in first half FY14. |

| • | | NYC Municipal Recycling, with the Brooklyn based facility scheduled to be complete in first half FY14. |

Net debt decreased by $138.4 million, to $153.8 million, bringing gearing to 7.4% of total capitalisation as at 30 June 2013. Net debt equals total borrowings minus cash balances and reflects total borrowings as if borrowings were reduced by cash balances as a pro forma measurement as follows:

| | | | | | | | |

| | | AS AT 30 JUNE | |

| A$m | | 2013 | | | 2012 | |

Total borrowings | | | 200.7 | | | | 343.6 | |

Less: cash and cash equivalents | | | (46.9 | ) | | | (51.4) | |

Net debt | | | 153.8 | | | | 292.2 | |

Plus: total equity | | | 1,928.8 | | | | 2,283.7 | |

Total capital | | | 2,082.6 | | | | 2,575.9 | |

| | |

Gearing ratio | | | 7.4% | | | | 11.3% | |

The Group’s strong cash flow and balance sheet position provides the capacity to fund the ongoing operational requirements of the business, as well as potential increased working capital requirements as and when underlying business conditions improve. In response to current weak global economic growth, maintaining low gearing is a focus of the Company.

RECONCILIATION OF STATUTORY RESULTS TO UNDERLYING RESULTS

FOR THE YEARS ENDED 30 JUNE 2013 AND 2012

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | EBITDA1 | | | EBIT | | | NPAT | |

| | | FY13 | | | FY12 | | | FY13 | | | FY12 | | | FY13 | | | FY12 | |

| | | A$m | | | A$m | | | A$m | | | A$m | | | A$m | | | A$M | |

Statutory Results | | | (41.5 | ) | | | 182.2 | | | | (469.4 | ) | | | (623.3 | ) | | | (466.1 | ) | | | (622.5 | ) |

| | | | | | |

Significant items: | | | | | | | | | | | | | | | | | | | | | | | | |

Goodwill impairment | | | N/A2 | | | | N/A2 | | | | 292.2 | | | | 617.3 | | | | 261.9 | | | | 601.6 | |

Other intangible asset impairment | | | N/A2 | | | | N/A2 | | | | 12.2 | | | | 0.8 | | | | 8.9 | | | | 0.5 | |

Impairment of goodwill in a jointly controlled entity | | | – | | | | N/A2 | | | | – | | | | 57.5 | | | | – | | | | 50.8 | |

Impairment of investment in CTG | | | 14.9 | | | | – | | | | 14.9 | | | | – | | | | 14.9 | | | | – | |

Fixed asset impairment | | | 61.2 | | | | – | | | | 61.2 | | | | – | | | | 54.7 | | | | – | |

Write-down of equipment spares | | | 5.1 | | | | – | | | | 5.1 | | | | – | | | | 5.1 | | | | – | |

Natural disaster expenses, net of insurance recoveries | | | 4.3 | | | | (2.7 | ) | | | 4.3 | | | | (2.7 | ) | | | 2.7 | | | | (1.8 | ) |

Impairment of a loan receivable | | | 4.8 | | | | – | | | | 4.8 | | | | – | | | | 3.0 | | | | – | |

UK inventory write-downs | | | 63.9 | | | | 48.0 | | | | 63.9 | | | | 48.0 | | | | 63.9 | | | | 41.3 | |

Inventory adjustments to net realisable value | | | 6.0 | | | | 21.3 | | | | 6.0 | | | | 21.3 | | | | 4.9 | | | | 13.9 | |

Write-down of CTG derivatives and equity accounted losses | | | 21.3 | | | | 1.2 | | | | 21.3 | | | | 1.2 | | | | 21.3 | | | | 1.2 | |

Lease settlements/onerous leases | | | 13.1 | | | | – | | | | 13.1 | | | | – | | | | 9.7 | | | | – | |

Redundancies | | | 7.3 | | | | 9.9 | | | | 7.3 | | | | 9.9 | | | | 5.0 | | | | 6.6 | |

Settlement of disputes with third parties | | | 4.7 | | | | 12.8 | | | | 4.7 | | | | 12.8 | | | | 4.7 | | | | 7.9 | |

Final settlement of a business arrangement | | | – | | | | 7.9 | | | | – | | | | 7.9 | | | | – | | | | 4.9 | |

Share-based compensation expense related to former CEO3 | | | 3.4 | | | | – | | | | 3.4 | | | | – | | | | 2.1 | | | | – | |

Yard closure/dilapidations | | | 8.5 | | | | – | | | | 8.5 | | | | – | | | | 7.2 | | | | – | |

Credit losses | | | 2.9 | | | | 4.4 | | | | 2.9 | | | | 4.4 | | | | 2.0 | | | | 2.7 | |

Pension plan special charges | | | – | | | | 3.0 | | | | – | | | | 3.0 | | | | – | | | | 1.9 | |

Transaction and other legal costs | | | 3.1 | | | | 2.5 | | | | 3.1 | | | | 2.5 | | | | 2.4 | | | | 1.8 | |

Loss on sale of business divisions | | | 10.1 | | | | – | | | | 10.1 | | | | – | | | | 10.0 | | | | – | |

Commercial settlements | | | (3.3 | ) | | | (1.4 | ) | | | (3.3 | ) | | | (1.4 | ) | | | (2.7 | ) | | | (1.1 | ) |

Loss/(gain) on sale of jointly controlled assets and entities | | | 1.6 | | | | (35.7 | ) | | | 1.6 | | | | (35.7 | ) | | | 1.5 | | | | (35.7 | ) |

Underlying results4 | | | 191.4 | | | | 253.4 | | | | 67.9 | | | | 123.5 | | | | 17.1 | | | | 74.0 | |

| 1 | EBITDA is a measurement of non-conforming financial information. |

| 2 | N/A indicates that EBITDA is calculated to exclude impairment of goodwill and other identified intangible assets in the presentation of both the statutory and underlying results. |

| 3 | Represents expense associated with good leaver determination for the former CEO with respect to long-term incentive plans. |

| 4 | Underlying result is a non-IFRS measure that is presented to provide an understanding of the underlying performance of the Group. The measure excludes the impacts of impairments, disposals as well as items that are subject to significant variability from one period to the next. The non-IFRS financial information is unaudited however the reconciling items above (before tax) have been extracted from the audited financial statements. |

C O R P O R A T E G O V E R N A N C E S T A T E M E N T

The directors and management of Sims Metal Management (the “Company” or the “Group”) are committed to operating the Company’s business ethically and in a manner consistent with high standards of corporate governance. The directors consider the establishment and implementation of sound corporate governance practices to be a fundamental part of promoting investor confidence and creating value for shareholders, through prudent risk management and a culture which encourages ethical conduct, accountability and sound business practices. The Corporate Governance Statement of the Company for the 2013 financial year has been prepared with reference to the Australian Securities Exchange (ASX) Corporate Governance Principles and Recommendations (including 2010 Amendments) (Recommendations). The Company has complied with the Recommendations.

PRINCIPLE 1: LAY SOLID FOUNDATIONS FOR MANAGEMENT AND OVERSIGHT

1.1 BOARD OF DIRECTORS

The board is responsible for the corporate governance and overall performance of the Company and the Group and for providing strategic guidance for the Group. The responsibilities of the board encompass the setting of key objectives, monitoring performance and ensuring the Group’s internal control, risk management and reporting procedures are adequate and effective.

1.2 THE ROLE AND RESPONSIBILITIES OF THE BOARD AND SENIOR EXECUTIVES

The role and responsibilities of the board are formally set out in its charter. The board charter identifies the functions reserved for the board and those delegated to senior executives.

The board’s key responsibilities include:

| – | overall corporate governance of the Group, including oversight of its control and accountability systems; |

| – | appointing, removing and appraising the performance of the Group Chief Executive Officer (CEO); |

| – | monitoring performance of senior management and the implementation of strategy, and ensuring appropriate resources are available; |

| – | enhancing and protecting the reputation of the Company by reviewing and ratifying systems of risk management and internal compliance and control, codes of conduct, and legal compliance; and |

| – | approving and monitoring the progress of major capital expenditure, capital management, acquisitions and divestitures, and financial and other reporting. |

The board has delegated general authority to manage the businesses of the Company to the CEO, who in turn may delegate functions to other senior management. However, the CEO remains answerable to the board and must comply with any limits on his authority established by the board from time to time. Effective 1 July 2013 the board has created a Global Leadership Team to serve in lieu of the CEO while a search is accomplished to appoint a new CEO.

Letters of appointment have been provided to all non-executive directors, covering responsibilities, time commitments, performance evaluation, indemnity and insurance arrangements, and induction and development. The responsibilities and terms of employment of certain senior executives of the Group are also set out in formal contracts of employment.

1.3 PERFORMANCE EVALUATION OF SENIOR EXECUTIVES

Annual performance objectives are set each financial year for all senior executives of the Group. These performance objectives include both financial and non-financial measures. A year-end appraisal is conducted to assess performance against the executive’s personal priorities and the responsibilities and demands of their role. The outcome of the performance review process is reflected in training and development/executive coaching programs, as needed, and succession planning for each executive, as well as an annual remuneration review. For the 2013 financial year, annual performance reviews were completed in August 2013, in accordance with the process disclosed.

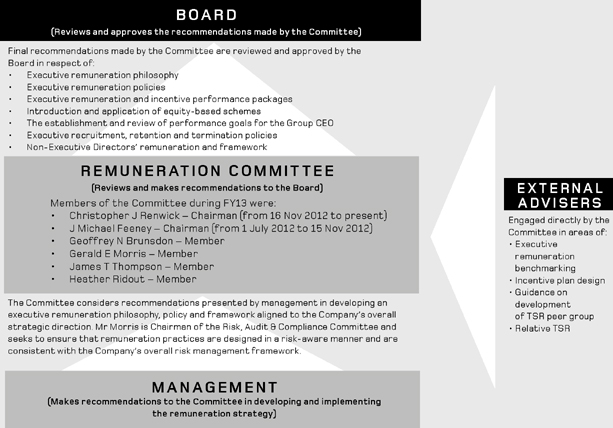

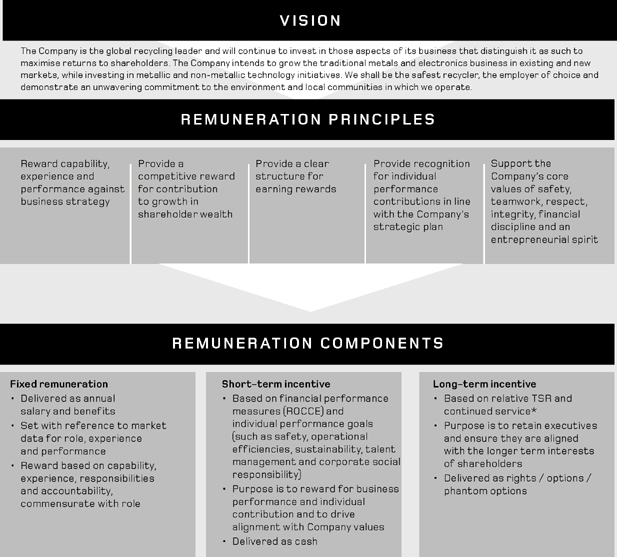

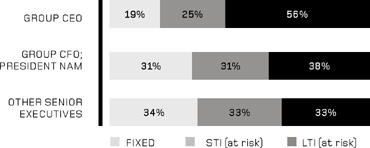

The Remuneration Report on pages 38 to 56 contains further information regarding the process for evaluating the performance of senior executives for the purpose of determining their fixed and variable remuneration.

1.4 EXECUTIVE INDUCTION PROGRAMS

Senior executives are able to attend formal induction programs which provide an overview of the Group, and its key policies and processes. Meetings are arranged with other senior executives in the Group to brief the new executives on the Group’s businesses, strategic objectives, risk management practices and other information necessary to meet the requirements of their roles. Site visits are also arranged to familiarise the executives with the Group’s operations and key operating personnel.

A copy of the board charter is available from the corporate governance section on the Company’s website.

PRINCIPLE 2: STRUCTURE THE BOARD TO ADD VALUE

2.1 COMPOSITION OF THE BOARD

The board charter sets out the composition of the board and relevant criteria for assessing the independence of directors.

The board currently comprises nine non-executive directors. The CEO, the one executive director, retired on 30 June 2013 and a replacement is to be appointed. Mr Robert Bass was appointed a non-executive director on 10 September 2013. Details of board members, including their skills, experience, qualifications and terms in office, are set out on pages 36 and 37.

2.2 BOARD ACCESS TO INFORMATION AND INDEPENDENT ADVICE

A director may, at the Company’s expense and subject to prior approval of the Chairperson, obtain independent professional advice relating to his or her duties and obligations as a board member. Board committees may also seek such independent professional advice. To the extent required to enable them to carry out their duties, all directors and board committees also have access to Company information and records and may consult senior management as required.

2.3 INDEPENDENCE OF DIRECTORS

The board charter states that board members shall be considered independent if they do not have any of the relationships identified in Box 2.1 of the Recommendations, and have been determined by the board to be independent, as defined in and to the extent required by the applicable rules of the United States Securities and Exchange Commission (SEC), the listing standards of the New York Stock Exchange, Inc. (NYSE) and other applicable laws and regulations, as they may be amended from time to time.

Having regard to these criteria, the board has determined that Mrs Heather Ridout and Messrs Gerald Morris, Norman Bobins, Christopher Renwick, Geoffrey Brunsdon, Jim Thompson, and John DiLacqua were independent non-executive directors of the Company during the 2013 financial year, and that recently appointed Mr Robert Bass is an independent non-executive director. Mr Daniel Dienst, the former CEO, was an executive director of the Company during the 2013 financial year.

Mr Tom Sato, a non-executive director, is not considered to be an independent director of the Company as a result of his association with Mitsui & Co., Ltd, which, through its affiliates, owns an 18% shareholding in the Company.

In accordance with Recommendation 2.1, the board has a majority of directors who are independent.

The independence of the directors is regularly reviewed. In accordance with the board charter, all directors must disclose to the board any actual or perceived conflicts of interest, whether of a direct or indirect nature, of which the director becomes aware and which the director reasonably believes may compromise the reputation or performance of the Company.

2.4 CHAIRPERSON

Mr Geoffrey Brunsdon, an independent non-executive director, has held the position of Chairperson of the board since 1 March 2012.

The roles of CEO of the Company and Chairperson of the board are separate, and the Chairperson must not also be the CEO. The Chairperson is responsible for the leadership of the board, establishing the agenda for board meetings, ensuring the board is effective, and chairing board and shareholders’ meetings.

2.5 BOARD PROCESSES

The board charter provides that the board shall meet at least four times per year, and otherwise as it considers necessary. The board met nine times during the 2013 financial year, including three times for full briefing sessions. Details of directors’ attendances at board meetings in the 2013 financial year are reported on page 33.

To assist directors in enhancing their understanding of the Company’s business, directors are briefed from time to time by members of the executive team on divisional performance and key operational and strategic issues, financial matters, risk management, market conditions, compliance and governance. The directors are also provided with an explanation of those proposed activities of the Group which require board approval.

The Group Company Secretary is responsible for ensuring that board procedures and policies are followed, and provides advice to the board on corporate governance and regulatory matters. All directors have unrestricted access to the advice and services of the Group Company Secretary.

2.6 BOARD COMMITTEES

The board has established five board committees to assist in the execution of board functions. Each committee has a written charter which is approved by the board and reviewed periodically. The charters of each of the board committees are available on the Company’s website.

Membership of the board committees is set out in the biographies of directors on pages 36 and 37.

Details of directors’ attendance at each committee meeting in the 2013 financial year are set out on page 33.

To enable each of the committees to discharge its responsibilities adequately and effectively, each committee has the authority to retain advisers and external legal counsel as required.

Each committee reports to the board and, following preparation of the minutes of each committee meeting, provides the board with copies of those minutes at the next occasion the board meets.

2.7 NOMINATION/GOVERNANCE COMMITTEE

The Nomination/Governance (Nom/Gov) Committee is responsible for recommending nominees for membership of the board in accordance with the committee’s Policy and Procedures for the Selection and Appointment of New Directors and the Re-election of Incumbent Directors. The Nom/Gov Committee also assesses necessary and desirable competencies of board members.

The Nom/Gov Committee is also responsible for reviewing the corporate governance procedures of the Company and recommending changes to the board as appropriate; developing a plan for board succession, including the succession of the Chairperson of the board and the CEO of the Company, and monitoring succession plans for the Company’s management levels and key resources; and establishing procedures for and overseeing the evaluation of the board.

C O R P O R A T E G O V E R N A N C E S T A T E M E N T

When considering the mix of skills and diversity which the board is looking to achieve in its membership, the Nom/Gov Committee takes into account the need to have members with relevant industry experience; expertise in particular fields such as financial, human resources and health & safety; and the broad skillset and experience required to effectively serve on the board of a global organisation.

The Nom/Gov Committee has a formal charter, a copy of which is available from the corporate governance section on the Company’s website, approved by the board.

COMPOSITION

The Nom/Gov Committee shall comprise at least three directors of the Company, with a majority being independent. The current members of the Nom/Gov Committee are Mrs Heather Ridout and Messrs Norman Bobins (Chairperson), Gerald Morris, and Christopher Renwick, all being independent non-executive directors. Mr Daniel Dienst, the former CEO, was a member of the Nom/Gov Committee during the 2013 financial year. The board may appoint additional directors to the Nom/Gov Committee or remove and replace members of the Nom/Gov Committee by resolution. The Nom/Gov Committee Chairperson shall not be the Chairperson of the board.

MEETINGS OF THE NOMINATION/GOVERNANCE COMMITTEE

The committee charter provides that the Nom/Gov Committee shall meet at least twice each year on a formal basis and additionally as circumstances may require. The Nom/Gov Committee met four times during the 2013 financial year. Details of attendance at meetings of the Nom/Gov Committee are set out on page 33.

2.8 BOARD PERFORMANCE EVALUATION

The Nom/Gov Committee is responsible for establishing procedures and overseeing the evaluation of the board. A formal performance evaluation was conducted involving the directors self-assessing the collective performance of the board. As part of the review process, directors were also asked to assess the board’s composition and structure, and any areas where the effectiveness of the board could be improved. The results of the evaluation, and individual committee assessments, were independently documented and will form the basis for the development of appropriate action plans under the guidance of the Nom/Gov Committee for the 2014 financial year.

2.9 RETIREMENT AND RE-ELECTION OF DIRECTORS

The Nom/Gov Committee considers and nominates to the board candidates for election as directors. The Company’s constitution requires that non-executive directors appointed by the board during the year must offer themselves for election by shareholders at the next Annual General Meeting of the Company. In addition, a non-executive director may not serve without seekingre-election beyond the third Annual General Meeting following the meeting at which the director was last elected or re-elected, or three years, whichever is longer. At least one director, other than the CEO, must retire at each Annual General Meeting. Retiring directors may offer themselves for re-election by the shareholders. The board does not impose a predetermined restriction on the tenure of directors as it considers that this restriction may result in the loss of vital experience and expertise.

2.10 DIRECTOR EDUCATION

A new board member orientation process has been established to provide new directors with an understanding of, and insight into, the industry, Company, management and control environment of the Group. As part of this process, directors receive orientation materials, meet with key senior executives and are given the opportunity to conduct site visits at significant operational facilities. Directors may, from time to time, depending on their particular needs, experience and interests, undertake external education seminars and programs at the expense, and with the approval, of the Company. As part of on-going director education, board meetings are held at various Group locations from time to time during the year which provides directors the opportunity to observe activities at each of the businesses.

PRINCIPLE 3: PROMOTE ETHICAL AND RESPONSIBLE DECISION-MAKING

3.1 CODE OF CONDUCT

The Company’s Code of Conduct applies to all directors, officers and employees of the Group. It underpins Sims Metal Management’s commitment to integrity, fair dealing and compliance with the law in its business affairs, and sets out expected standards of conduct with respect to all stakeholders, including fellow employees, customers, suppliers, shareholders and the community.

The Code of Conduct is designed to encourage ethical and appropriate behaviour by all Group personnel, and addresses a wide range of responsibilities to stakeholders, including conflicts of interest, security of information, use of Company assets and resources, discrimination and harassment, occupational health and safety, and the prohibition of corrupt conduct and the consequences in the event thereof.

The Code of Conduct encourages employees to raise any matters of concern without fear of retribution. The Company has implemented the Sims Metal Management Hotline to enable employees, customers, contractors and the like to report misconduct or unethical behaviour within the Group to an external third party. The Company also conducts employee education and compliance programs on a regular basis to help ensure compliance with various laws around the world.

3.2 ANTI-CORRUPTION CODE

In addition to the Code of Conduct, the Company has adopted an Anti-Corruption Code which has been developed to aid employees, agents, contractors, consultants and partners in ensuring that they comply at all times with applicable anti-corruption laws and policies. Among other matters, the Code of Conduct sets out the Company’s policy in relation to conflicts of interests, gifts and hospitality, relationships with governments and political contributions.

Copies of the Company’s Code of Conduct and Anti-Corruption Code are available from the corporate governance section on the Company’s website.

3.3 DEALING IN COMPANY SECURITIES

Directors and employees of the Group are bound by the Company’s policy on dealing in the securities of the Company. Under the policy, directors, senior executives and other ‘designated persons’ may only buy or sell Company securities during the period 24 hours to 28 days after the release of the Company’s yearly and half-yearly results announcements and the filing of the Company’s Form 20-F with the SEC, or during such period following the conclusion of the Company’s Annual General Meeting, or during the currency of any capital raising prospectus issued by the Company or takeover bid for the Company.

A copy of the Company’s policy titled ‘Dealing in Sims Metal Management Limited Securities’ is available from the corporate governance section on the Company’s website.

3.4 DIVERSITY

Sims Metal Management recognises the value and advantages of having a diversified workforce that reflects the diversity of the communities in which it operates. Accordingly, the Company has adopted a Workplace Diversity Policy, a copy of which can be found on the Company’s website. This policy is designed to support the Company’s organisational core values of respect, integrity and teamwork. The board has responsibility for establishing and monitoring the Company’s overall diversity strategy and policy. The board’s Nom/Gov Committee has responsibility for monitoring the effectiveness of this policy to the extent it relates to board diversity and for reviewing and recommending any updates to this policy as deemed necessary. The board’s Remuneration Committee has an overarching role to establish measurable objectives for achieving diversity, and to assess annually, both the objectives and the Company’s progress in achieving them. The following table shows the objectives in relation to gender diversity that were established for the 2013 financial year and the progress made towards achieving them.

| | | | |

| OBJECTIVE | | PROGRESS |

| 1. | | In accordance with the Global Gender Diversity Plan (Diversity Plan), deliver leadership diversity training to global managers/supervisors. | | Achieved and ongoing. |

| 2. | | Increase female participation at the Senior Management and Executive levels. | | Progress made. The percentage of female participation at the Senior Management level increased from 12% in the 2012 financial year to 14% in the 2013 financial year. The percentage of female participation at the Executive level was 11%, the same as the previous year. |

| 3. | | Following the appointment of a female director in calendar 2011 consider, as retirements permit, appointing at least one further female director within the ensuing two calendar years. | | The reduction in Board size has meant no additional female directors have been appointed in calendars 2012 and 2013. As director retirements permit, further consideration will be given to such an appointment. |

| 4. | | Consider age, cultural and ethnicity issues within the context of the Diversity Plan. | | Action underway in the 2013 financial year. |

| 5. | | Conduct a review of benefits and workplace practices to identify and remove diversity biases, including evaluating current diversity friendly benefits such as maternity leave, and considering additional programs like mentoring and flexible working arrangements for appropriate roles. | | Action underway in the 2013 financial year. |

| 6. | | Establish diversity objectives as part of an executive’s short term incentive personal priorities. | | To achieve by the 2014 financial year. |

| 7. | | Increase the percentage of women recruited into our management trainee, graduate and cadet programs to 25%. | | To achieve by the 2014 financial year. |

As at the end of the 2013 financial year, the proportion of women employees in the whole organisation and in senior executive positions was 18% and 11% respectively. There is one female director on the Company’s board.

C O R P O R A T E G O V E R N A N C E S T A T E M E N T

PRINCIPLE 4: SAFEGUARD INTEGRITY IN FINANCIAL REPORTING

The Chairman and the Group Chief Financial Officer (CFO) have stated in writing to the board in respect of the 2013 financial year:

| – | that the Company’s financial reports present a true and fair view, in all material respects, of the Company’s financial condition and operational results and are in accordance with relevant accounting standards; and |

| – | with the exception of the matters referred to below, that the above statement is founded on a sound system of risk management and internal compliance and control which implements the policies adopted by the board and that the Company’s risk management and internal compliance and control system is operating efficiently and effectively in all material respects. |

During the 2013 financial year the Company restated its prior financial statements for the 2010, 2011 and 2012 financial years due to inventory misstatements in the United Kingdom (UK). In the restatement, the Company identified three material weaknesses within internal controls over financial reporting in the following areas: segregation of duties within the inventory cycle of the UK operations were improper; UK management did not maintain effective period end controls; and UK management failed to perform proper valuation analyses on its inventories.

As at 30 June 2013, the Company has reassessed the internal controls over financial reporting. The Company determined that the material weaknesses relating to segregation of duties within the inventory cycle and the period end controls, both related to the UK operations, have been fully remediated. The material weakness related to inventory valuation in the UK SRS business has also been remediated as of period end by the implementation of new controls. However, those controls were not operating for a sufficient period of time before 30 June 2013 to consider the material weakness closed. Additionally, a new material weakness arose in aggregation across the Group relating to period end management review of journal entries. Management has planned remediation of the material weakness that relates to manual journal entry review through specific delegation of responsibility for reviewing manual journal entries during the 2014 financial year.

4.1 RISK, AUDIT & COMPLIANCE COMMITTEE

The Risk, Audit & Compliance (RAC) Committee assists the board in fulfilling its responsibility to oversee the quality and integrity of accounting, auditing and reporting practices of the Company. In particular, the primary role of the RAC Committee is to assist the board in fulfilling its corporate governance and oversight responsibilities in relation to the Company’s accounting and financial reporting, internal control structure, risk management systems (including the review of risk mitigation, which includes commercial insurance coverage), internal and external audit functions, and compliance with legal and regulatory requirements.

The RAC Committee has a formal charter approved by the board. The RAC Committee reports to the board on all matters relevant to the RAC Committee’s role and responsibilities. The specific functions of the RAC Committee are set out in its charter and include:

| – | reviewing and assessing the internal and external reporting of financial information; |

| – | assessing management processes supporting the integrity and reliability of the Company’s financial and management reporting systems and its external reporting; |