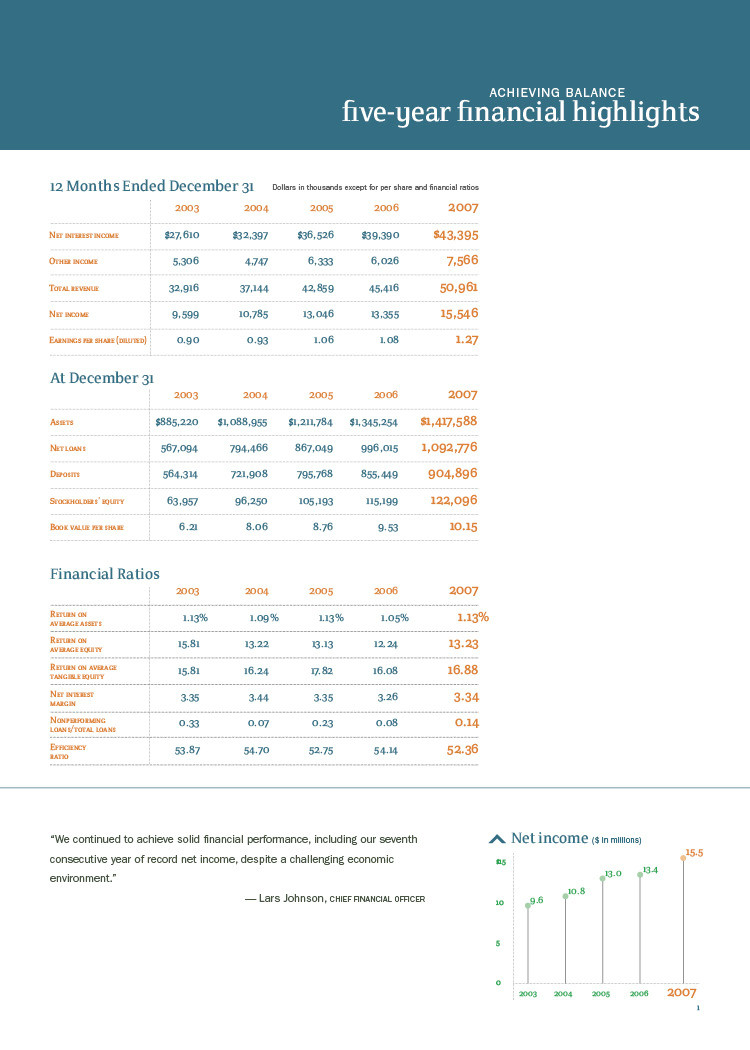

CASCADE FINANCIAL CORPORATION SELECTED FINANCIAL DATA

(Dollars in thousands, except per share data)

| | | FOR THE YEARS ENDED | |

| | | DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Interest income | | $ | 93,935 | | | $ | 82,658 | | | $ | 67,802 | | | $ | 55,316 | | | $ | 50,363 | |

| Interest expense | | | 50,540 | | | | 43,268 | | | | 31,276 | | | | 22,919 | | | | 22,753 | |

| Net interest income | | | 43,395 | | | | 39,390 | | | | 36,526 | | | | 32,397 | | | | 27,610 | |

| Provision for loan losses | | | 1,350 | | | | 1,000 | | | | 945 | | | | 675 | | | | 1,275 | |

| Net interest income after provision for loan losses | | | 42,045 | | | | 38,390 | | | | 35,581 | | | | 31,722 | | | | 26,335 | |

| | | | | | | | | | | | | | | | | | | | | |

| Other income | | | 7,566 | | | | 6,026 | | | | 6,333 | | | | 4,747 | | | | 5,306 | |

| Other expense | | | 26,682 | | | | 24,586 | | | | 22,606 | | | | 20,317 | | | | 17,733 | |

| Income before provision for income taxes | | | 22,929 | | | | 19,830 | | | | 19,308 | | | | 16,152 | | | | 13,908 | |

| Net income | | | 15,546 | | | | 13,355 | | | | 13,046 | | | | 10,785 | | | | 9,599 | |

Net income per common share, basic (1) | | | 1.29 | | | | 1.11 | | | | 1.09 | | | | 0.96 | | | | 0.94 | |

Net income per common share, diluted (1) | | | 1.27 | | | | 1.08 | | | | 1.06 | | | | 0.93 | | | | 0.90 | |

Book value per common share (1) | | | 10.15 | | | | 9.53 | | | | 8.76 | | | | 8.06 | | | | 6.21 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | AT DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Assets | | $ | 1,417,588 | | | $ | 1,345,254 | | | $ | 1,211,784 | | | $ | 1,088,955 | | | $ | 885,220 | |

| Loans, net | | | 1,092,776 | | | | 996,015 | | | | 867,049 | | | | 794,466 | | | | 567,094 | |

| Cash and securities | | | 246,548 | | | | 282,301 | | | | 278,747 | | | | 228,644 | | | | 290,537 | |

| Deposits | | | 904,896 | | | | 855,449 | | | | 795,768 | | | | 721,908 | | | | 564,314 | |

| Borrowings | | | 147,512 | | | | 121,485 | | | | 66,270 | | | | 36,356 | | | | 50,123 | |

| FHLB advances | | | 231,000 | | | | 243,000 | | | | 236,000 | | | | 228,000 | | | | 200,000 | |

| Stockholders’ equity | | | 122,096 | | | | 115,199 | | | | 105,193 | | | | 96,250 | | | | 63,957 | |

| Nonperforming loans | | | 1,523 | | | | 851 | | | | 1,987 | | | | 532 | | | | 1,921 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | FINANCIAL RATIOS | |

| | | FOR THE YEARS ENDED | |

| | | DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Return on average assets | | | 1.13 | % | | | 1.05 | % | | | 1.13 | % | | | 1.09 | % | | | 1.13 | % |

| Return on average equity | | | 13.23 | | | | 12.24 | | | | 13.13 | | | | 13.22 | | | | 15.81 | |

| Return on average tangible equity | | | 16.88 | | | | 16.08 | | | | 17.82 | | | | 16.24 | | | | 15.81 | |

| Net interest margin | | | 3.34 | | | | 3.26 | | | | 3.35 | | | | 3.44 | | | | 3.35 | |

| Efficiency ratio | | | 52.36 | | | | 54.14 | | | | 52.75 | | | | 54.70 | | | | 53.87 | |

| Dividend payout ratio | | | 25.98 | | | | 28.43 | | | | 25.66 | | | | 25.81 | | | | 18.31 | |

| Average stockholders’ equity to average assets | | | 8.58 | | | | 8.55 | | | | 8.60 | | | | 8.25 | | | | 7.15 | |

| Total risk-based capital to risk-weighted assets | | | 10.80 | | | | 11.22 | | | | 10.86 | | | | 11.18 | | | | 13.42 | |

| Tier 1 capital to average total assets | | | 8.90 | | | | 8.99 | | | | 8.23 | | | | 8.14 | | | | 8.49 | |

This statement has not been reviewed, or confirmed for accuracy or relevance, by the Federal Deposit Insurance Corporation.

MANAGEMENT DISCUSSION AND ANALYSIS

The following discussion is provided for the consolidated operations of Cascade Financial Corporation (the “Corporation”) as of December 31, 2007. The Corporation has only one operating subsidiary: Cascade Bank (the “Bank”). The purpose of this discussion is to focus on significant factors concerning the Corporation’s financial condition and results of operations, and to provide a more comprehensive review of the Corporation’s operating results and financial condition than can be obtained from reading the consolidated financial statements alone. This discussion should be read with the consolidated financial statements and the notes thereto.

In addition to historical information, this report contains certain "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 ("PSLRA"). This statement is included for the express purpose of availing the Corporation of the protections of the safe harbor provisions of the PSLRA. The forward-looking statements contained herein are subject to factors, risks, and uncertainties that may cause actual results to differ materially from those projected. The following items are among the factors that could cause actual results to differ materially from the forward-looking statements: higher than expected loan delinquency rates; general economic conditions, including their impact on capital expenditures; business conditions in the banking industry; recent world events and their impact on interest rates, businesses, and customers; the regulatory environment; new legislation; vendor quality and efficiency; employee retention factors; rapidly-changing technology; competitive factors, including increased competition with community, regional, and national financial institutions; fluctuating interest rate environments; and similar matters. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect management's analysis only as of the date of the statement. The Corporation undertakes no obligation to publicly revise or update these forward-looking statements to reflect events or circumstances that arise after the date of this report. Readers should carefully review the risk factors described in this and other documents the Corporation files from time to time with the Securities and Exchange Commission.

Critical Accounting Estimates

Corporations may apply certain critical accounting estimates requiring management to make subjective or complex judgments, often as a result of the need to estimate the effect of matters that are inherently uncertain. The Bank considers its only material critical accounting estimate to be the allowance for loan losses. We believe that the accounting estimate related to the allowance for loan losses is a "critical accounting estimate" because: (1) it is highly susceptible to change from period to period because it requires management to make assumptions about future collectability of loans; and (2) the impact of a sudden large loss could significantly reduce the allowance and would require increased provisions to replenish the allowance, which would negatively affect earnings.

The allowance for loan losses is established through a provision for loan losses charged against earnings. The balance of the allowance for loan losses is maintained at the amount management believes will be adequate to absorb known and inherent losses in the loan portfolio. The appropriate balance of the allowance for loan losses is determined by applying estimated loss factors to the credit exposure from outstanding loans. Estimated loss factors are based on subjective measurements including management’s assessment of the internal risk classifications, changes in the nature of the loan portfolio, industry concentrations, and the impact of current local, regional and national economic factors on the quality of the loan portfolio. Changes in these estimates and assumptions are reasonably possible and may have a material impact on the Corporation’s consolidated financial statements and results of operation.

For additional information regarding the allowance for loan losses, its relation to the provision for loan losses and risk related to asset quality, see Note 4 in the Consolidated Financial Statements for the year ended December 31, 2007, and “Management’s Discussion and Analysis of Financial Condition and Results of Operation – Provision for Loan Losses.”

Critical Accounting Policies

The Corporation’s significant accounting policies are described in Note 1 of the Notes to Consolidated Financial Statements and are essential to understanding Management's Discussion and Analysis of Financial Condition and Results of Operations. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions which affect the reported amounts and disclosures. Actual results may differ from these estimates under different assumptions or conditions. The following policies involve a higher degree of judgment than do our other significant accounting policies detailed in Note 1 of the Notes to Consolidated Financial Statements.

Allowance for Loan Losses

The Bank reviews historical origination and charge-off relationships, charge-off experience factors, collection data, delinquency reports, estimates of the value of the underlying collateral, and other information in order to make the necessary judgments as to the appropriateness of the provision for loan losses and the allowance for loan losses. The Bank also uses Qualitative (“Q”) Factors to analyze the adequacy of the loan loss allowance and determine an unallocated portion of the allowance. Factors such as regional/local economic trends, the health of the real estate market, loan and collateral concentrations, size of borrowing relationships, trends in loan delinquencies and charge-offs and changes in asset classifications are now included in the Bank’s analysis of the allowance for loan losses. Loans losses are charged-off against the allowance when management confirms the

uncollectability of a loan balance or when the liquidation value of the collateral is less than the amount of the loan. The Bank believes that the allowance for loan losses is adequate to cover probable losses inherent in its loan portfolio. However, because the allowance for loan losses is based on estimates, there can be no assurance that the ultimate charge-off amount will not exceed the estimates.

Investments

The Bank classifies its investments as held-for-trading, available-for-sale, or held-to-maturity. Held-for-trading securities are marked to market with the change in value recognized in the income statement. Available-for-sale securities are reported at their fair value, which is determined by obtaining quoted market prices. Unrealized gains and losses on available-for-sale securities are included in other comprehensive income and excluded from earnings. Realized gains and losses and declines in fair value judged to be other than temporary are included in earnings. The fair value of financial instruments is discussed in more detail in Note 15 of the Notes to Consolidated Financial Statements. Held-to-maturity securities are carried at amortized cost.

Income Taxes

The Bank estimates tax expense based on the amount it expects to owe various tax authorities. Taxes are discussed in more detail in Note 10 of the Notes to Consolidated Financial Statements. Accrued taxes represent the net estimated amount due or to be received from taxing authorities. In estimating accrued taxes, management assesses the relative merits and risks of the appropriate tax treatment of transactions taking into account statutory, judicial and regulatory guidance in the context of our tax position.

Fair Value

Effective January 1, 2007, we adopted SFAS No. 157, Fair Value Measurements, which among other things, requires enhanced disclosures about financial instruments carried at fair value. SFAS No. 157 establishes a hierarchical disclosure framework associated with the level of pricing observability utilized in measuring financial instruments at fair value. The degree of judgment utilized in measuring the fair value of financial instruments generally correlates to the level of pricing observability. Financial instruments with readily available active quoted prices or for which fair value can be measured from actively quoted prices generally will have a higher degree of pricing observability and a lesser degree of judgment utilized in measuring fair value. Conversely, financial instruments rarely traded or not quoted will generally have little or no pricing observability and a higher degree of judgment utilized in measuring fair value. Pricing observability is impacted by a number of factors, including the type of financial instrument, whether the financial instrument is new to the market and not yet established and the characteristics specific to the transaction. See Note 15 of the Notes to Consolidated Financial Statements for additional information about the level of pricing transparency associated with financial instruments carried at fair value.

FINANCIAL CONDITION

Total Assets

The Corporation’s total assets at December 31, 2007, were $1.4 billion, compared to $1.3 billion at December 31, 2006, an increase of 5.4%. The increase in 2007 is due entirely to internal growth. The Corporation’s total assets at December 31, 2005, were $1.2 billion.

Investment Securities

Total securities held decreased by $7.4 million to $232.0 million as of December 31, 2007. Securities designated as available-for-sale decreased to $94.8 million at December 31, 2007, versus $142.6 million at December 31, 2006. Securities designated as available-for-sale includes $11.9 million in Federal Home Loan Bank of Seattle stock at December 31, 2007 and 2006. Securities designated as held-to-maturity increased to $137.2 million at December 31, 2007, from $96.8 million a year earlier. The securities in both portfolios consist of notes issued by Government Sponsored Enterprises (“GSE” e.g. FHLB, FNMA) or mortgage-backed securities issued by either FNMA or FHLMC or a mortgage conduit. There were no investment securities that were backed by subprime loans and all investments received the highest credit rating from at least one of the major rating agencies.

Loan Portfolio

Net loans increased to $1.1 billion at December 31, 2007, a 9.7% increase over $996.0 million at December 31, 2006. Net loans were $867.0 million at December 31, 2005.

Business banking loans increased from $442.4 million at December 31, 2006, to $468.5 million at December 31, 2007, a 5.9% increase. Growth in this portfolio was the result of our ability to win new borrowing customers in a very competitive market. Construction loans (net of loans in process) increased to $381.8 million from $295.1 million during the year. This portfolio experienced solid growth as the housing market remained relatively strong during the year. Commercial real estate loans increased from $119.3 million at December 31, 2006, to $120.4 million at December 31, 2007. The Corporation’s loan focus remains on small businesses, builders and developers in the Puget Sound Area. Construction lending is directed toward building single-family housing and land development for single-family housing. The Bank generally confines its lending to the Puget Sound Region of Washington State.

Total single-family residential loans increased from $91.3 million at December 31, 2006, to $98.4 million at December 31, 2007. The Corporation sells the vast majority of its originations of 30-year fixed-rate loans, its 15-year fixed-rate loans, and many of its conforming intermediate term hybrid adjustable rate mortgages (“ARMs”) in the secondary mortgage market.

Multifamily loans outstanding decreased from $34.7 million at December 31, 2006, to $11.4 million at December 31, 2007. The Corporation has de-emphasized this product line due to intense pricing pressure, so loan payoffs were not replaced with the same category of loan.

Consumer loans remained flat at $27.7 million as of December 31, 2007. The Bank’s consumer loan portfolio is comprised of home equity loans and lines of credit, installment loans, and credit card loans. Home equity loans generally take the form of a second mortgage. In terms of direct consumer loans, the Bank has not emphasized this line of business, concluding that it is at a competitive disadvantage against the very aggressive pricing of large banks, captive finance companies and the specialty credit card issuers.

The chart below indicates the mix of the loan portfolio as of the dates indicated:

| | | DECEMBER 31, 2007 | | | DECEMBER 31, 2006 | | | DECEMBER 31, 2005 | |

| (Dollars in thousands) | | AMOUNT | | | PERCENT | | | AMOUNT | | | PERCENT | | | AMOUNT | | | PERCENT | |

| | | | | | | | | | | | | | | | | | | |

| Business | | $ | 468,453 | | | | 42 | % | | $ | 442,391 | | | | 44 | % | | $ | 394,034 | | | | 45 | % |

| Construction | | | 381,810 | | | | 34 | | | | 295,087 | | | | 29 | | | | 171,964 | | | | 20 | |

| Commercial real estate | | | 120,421 | | | | 11 | | | | 119,298 | | | | 12 | | | | 141,109 | | | | 16 | |

| Core commercial loans | | | 970,684 | | | | 87 | | | | 856,776 | | | | 85 | | | | 707,107 | | | | 81 | |

| Residential | | | 98,384 | | | | 9 | | | | 91,256 | | | | 10 | | | | 89,422 | | | | 10 | |

| Consumer | | | 27,688 | | | | 3 | | | | 27,686 | | | | 2 | | | | 32,160 | | | | 3 | |

| Multifamily | | | 11,397 | | | | 1 | | | | 34,719 | | | | 3 | | | | 52,057 | | | | 6 | |

| Total loans | | | 1,108,153 | | | | 100 | % | | | 1,010,437 | | | | 100 | % | | | 880,746 | | | | 100 | % |

| Deferred loan fees, net | | | (3,724 | ) | | | | | | | (3,434 | ) | | | | | | | (3,443 | ) | | | | |

| Allowance for losses on loans | | | (11,653 | ) | | | | | | | (10,988 | ) | | | | | | | (10,254 | ) | | | | |

| Loans, net | | $ | 1,092,776 | | | | | | | $ | 996,015 | | | | | | | | 867,049 | | | | | |

Allowance for Loan Losses

Management provides for possible loan losses by maintaining an allowance. The allowance for loan losses reflects management’s best estimate of probable losses as of a particular balance sheet date, but there is no guarantee that management’s estimate will be sufficient to cover actual loan losses. The allowance for loan losses is maintained at a level considered adequate based on management’s assessment of various factors affecting the loan portfolio, including delinquencies, trends in credit quality, local economic conditions, growth of the loan portfolio, past loss experience, and the portfolio’s composition. Increases in the allowance for loan losses made through provisions primarily reflect loan growth, loan loss risks inherent in lending, and the impact of the economic climate on the loan portfolio.

Management determines the amount of the allowance for loan losses by utilizing a loan grading system to determine risk in the loan portfolio and by considering the results of credit reviews. The loan portfolio is separated by quality and then by loan type. Loans of acceptable quality are evaluated as a group, by loan type, with a specific loss rate assigned to the total loans in each type, but unallocated to any individual loan. Conversely, each adversely classified loan is individually analyzed to determine an estimated loss amount. A valuation allowance is also assigned to these adversely classified loans, but at an assumed higher reserve rate due to the greater risk of loss. Past due and impaired loans are actively managed to minimize the potential loss of principal.

At December 31, 2007, the allowance for loan losses was $11.7 million (1.05% of total loans) compared to $11.0 million (1.09% of total loans) at December 31, 2006, and $10.3 million (1.16% of total loans) at December 31, 2005. During 2007, the Corporation added $1.4 million to the allowance compared to $1.0 million in 2006 and $945,000 in 2005. In 2007, the Bank segregated a valuation reserve against off-balance sheet commitments, such as loans in process. As of December 31, 2007, that valuation reserve account was $142,000. Total allowance for loan losses, which includes the allowance for off-balance sheet commitments, was $11.8 million (1.06% of total loans) as of December 31, 2007.

Net loan charge-offs were $543,000 in 2007 (or 0.05% of average loans outstanding) compared to $266,000 in 2006 (or 0.03% of average loans outstanding). Net charge-offs were $254,000 (or 0.03% of average loans outstanding) for the year ended December 31, 2005. The coverage ratio (the allowance for loan losses to nonperforming loans) was 765% at December 31, 2007, 1,291% at December 31, 2006, and 516% at December 31, 2005. Including the allowance for off-balance sheet commitments, the coverage ratio was 774% at December 31, 2007.

Deposit Accounts

Deposit accounts totaled $904.9 million at December 31, 2007, an increase of $49.5 million or 5.8% over $855.4 million at December 31, 2006. Deposits totaled $795.8 million at December 31, 2005. Checking account balances were $138.2 million as of December 31, 2007, compared to $139.5 million in the prior year. With the High Performance Checking program, the Bank was able to maintain its totals even as checking balances declined on a national basis. Money market deposit account balances grew by 14.8% to $316.0 million with rates competitive with those offered by money market funds. Certificates of deposit increased 3.3% to $439.4 million. As business banking activity increases, management’s goal is to increase its noninterest-bearing or low interest accounts through the growth of commercial checking accounts.

The market for deposits has remained very competitive. It remains a key objective of the Bank to increase its demand deposit account balances and other low rate accounts.

Other Borrowings

The Bank uses Federal Home Loan Bank of Seattle (“FHLB”) advances to provide intermediate and longer term funding, as well as to augment deposits. At December 31, 2007, the Bank had $231.0 million in FHLB advances compared to $243.0 million as of December 31, 2006. For 2007, FHLB advances averaged 16.0% of assets compared to 18.6% in 2006. Subject to its Line of Credit with the FHLB, the availability of collateral, and the parameters of liquidity management, the Bank will continue to use advances as a funding source.

The Bank also uses repurchase agreements for funding. At December 31, 2007, the Bank had executed $120.6 million in repurchase agreements compared to $95.7 million a year earlier. In 2000, the Corporation issued $10.3 million in trust preferred securities, which are termed “junior subordinated debentures payable.” These junior subordinated debentures payable have a fixed rate of 11% and mature on March 1, 2030, but are callable at a premium beginning March 1, 2010. In December 2004, the Corporation issued an additional $5.2 million in junior subordinated debentures payable. These debentures have a fixed rate of 5.82% for the first 5 years and then float at the three-month LIBOR plus 1.90% for the remaining 25 years. The debentures are callable at par after 5 years. On March 30, 2006, the Corporation issued an additional $10.3 million in junior subordinated debentures payable. These debentures have an initial rate of 6.65% set for 5 years and then convert to a three-month LIBOR plus 1.40% for the remaining 25 years. The debentures are callable at par after 5 years. Junior subordinated debentures payable are considered Tier 1 capital by financial institution regulators.

Capital

Banking regulations require the Bank to maintain minimum levels of capital. As of December 31, 2007, the Bank remained a “well-capitalized” institution (the FDIC’s highest rating), under regulatory guidelines, with a core capital-to-asset ratio of 9.00% and a risk-based capital-to-asset ratio of 10.91%. The Bank’s regulatory capital ratios are discussed in more detail in Note 12 of the Notes to Consolidated Financial Statements.

Federal Reserve guidelines require the Corporation, on a consolidated basis, to maintain minimum levels of capital as well. At December 31, 2007, the Corporation's total risk-based capital to risk-weighted assets was 10.80%, compared to 11.22% at December 31, 2006, and 10.86% at December 31, 2005. The Corporation projects that earnings retention and existing capital will be sufficient to fund anticipated asset growth and the existing level of cash dividends, while maintaining a “well-capitalized” designation under the FDIC and Federal Reserve guidelines. The Corporation has paid its shareholders a cash dividend on a quarterly basis since 2002. Average shares outstanding, stock options, net income per share and book value per share for all periods presented have been retroactively adjusted to reflect stock splits. For the year, the Corporation returned $4.1 million in dividends to its shareholders compared to $3.7 million in 2006. The dividend payout ratio (the ratio of dividends paid to net income) for 2007 was 26%.

The Corporation is committed to managing capital for maximum shareholder benefit and maintaining protection for depositors and creditors. The Corporation manages various capital levels at both the holding company and subsidiary bank level to attempt to maintain adequate capital ratios and levels in accordance with external regulations and capital guidelines established by the Board of Directors.

RESULTS OF OPERATIONS

Earnings

Cascade Financial Corporation earned net income for the year ended December 31, 2007, of $15.5 million, an increase of 16.4% over the $13.4 million net income in the year ended December 31, 2006. Earnings per fully diluted share (EPS) were $1.27 in 2007 and $1.08 in 2006. Higher net interest income due to increased earning assets and an expanded net interest margin contributed to the improved results. Income was also enhanced by increased checking fees and other service fees, and fair value gains on items subject to mark to market accounting, which partially offset the decline in gains on the sale of loans and the decline in other income. The Corporation earned net income of $13.0 million or $1.06 per fully diluted share for the fiscal year ended December 31, 2005.

Return on Average Equity

Return on average equity for the year ended December 31, 2007, was 13.23% compared to 12.24% for the same period of 2006. Return on average equity for the fiscal year ending December 31, 2005 was 13.13%.

Return on Average Tangible Equity

Return on average tangible equity (average equity less average goodwill) was 16.88% compared to 16.08% in 2006, and 17.82% in 2005. The June 2004 acquisition of Issaquah Bancshares, Inc. (“Issaquah”) generated $26.3 million in goodwill and intangibles as assets and a like amount of capital. Eliminating the average intangible asset and reducing the capital by the same amount produces average tangible equity.

Return on average tangible equity is determined by methods other than those in accordance with accounting principles generally accepted in the United States of America (“GAAP”). This measure excludes the average balance of acquisition-related goodwill and intangibles in determining average tangible shareholders’ equity. Management believes the presentation of this financial measure, excluding the impact of these items, provides useful supplemental information that is essential for a proper understanding of the financial results of Cascade

Financial Corporation. This disclosure should not be viewed as a substitute for results determined to be in accordance with GAAP, nor is it necessarily comparable to non-GAAP performance measures that may be presented by other companies.

A summary of tangible equity follows:

| (Dollars in thousands) | | 2007 | | | 2006 | |

| Net income | | $ | 15,546 | | | $ | 13,355 | |

| Average equity | | $ | 117,534 | | | $ | 109,103 | |

| Average goodwill & intangibles | | | 25,439 | | | | 26,040 | |

| Average tangible equity | | $ | 92,095 | | | $ | 83,063 | |

| Return on average tangible equity | | | 16.88 | % | | | 16.08 | % |

The largest component of the Corporation’s earnings is net interest income. Net interest income is the difference between interest earned on earning assets (primarily loans, interest-bearing deposits with banks, and investment securities) and the interest expense associated with interest-bearing liabilities (deposits and borrowings). Interest earned and interest paid is affected by general economic conditions, including the demand for loans, cost of deposits, market rates of interest and government policies. The Corporation’s operations may be sensitive to changes in interest rates and the resulting impact on net interest income.

Net interest income for the year ended December 31, 2007, increased by 10.2%, or $4.0 million, to $43.4 million from $39.4 million for the year ended December 31, 2006. The improvement in net interest income was primarily due to the growth in our level of average earning assets of $90.8 million and an 8 basis point increase in the net interest margin. Net interest income for the fiscal year ended December 31, 2005 was $36.5 million.

Average earning assets increased 7.5% to $1.3 billion for the year ended December 31, 2007, from $1.2 billion for the year ended December 31, 2006. Average earning assets were $1.1 billion for the year ended December 31, 2005.

Net interest margin is net interest income expressed as a percent of average earning assets. The net interest margin for the year ended December 31, 2007, was 3.34%, compared to 3.26% for the year ended December 31, 2006. While the yield on assets has improved over the last year, liability costs have also increased. The yield on earning assets increased 39 basis points to 7.24% in 2007. The cost of interest-bearing liabilities increased 37 basis points to 4.38% for the year as new liabilities were generally booked at higher rates than the average cost of existing liabilities.

Average Balances and an Analysis of Average Rates Earned and Paid

The following table shows average balances and interest income or interest expense, with the resulting average yield or rate by category or average earning asset or interest-bearing liability.

| | | FOR THE YEARS ENDED DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | |

| (Dollars in thousands) | | AVERAGE BALANCE | | INTEREST AND DIVIDEND | | YIELD/ COST | | | AVERAGE BALANCE | | INTEREST AND DIVIDEND | | YIELD/ COST | | | AVERAGE BALANCE | | INTEREST AND DIVIDEND | | | YIELD / COST | |

| | | | | | | | | | | | | | | | | | | | | | | |

| ASSETS | | | | | | | | | | | | | | | | | | | | | | |

Interest-earning assets (1) | | | | | | | | | | | | | | | | | | | | | | |

| Residential loans | | $ | 94,608 | | $ | 5,753 | | 6.08 | % | | $ | 98,476 | | $ | 5,582 | | 5.67 | % | | $ | 104,789 | | $ | 5,882 | | | 5.61 | % |

| Multifamily loans | | | 18,467 | | | 1,416 | | 7.67 | | | | 42,574 | | | 2,863 | | 6.72 | | | | 74,650 | | | 4,910 | | | 6.58 | |

| Commercial real estate loans | | | 117,952 | | | 8,259 | | 7.00 | | | | 144,094 | | | 9,821 | | 6.82 | | | | 166,736 | | | 10,957 | | | 6.57 | |

| Construction loans | | | 332,467 | | | 30,094 | | 9.05 | | | | 214,290 | | | 19,376 | | 9.04 | | | | 133,975 | | | 10,199 | | | 7.61 | |

| Consumer loans | | | 27,575 | | | 2,128 | | 7.72 | | | | 30,064 | | | 2,304 | | 7.66 | | | | 31,352 | | | 2,210 | | | 7.05 | |

| Business banking loans | | | 455,024 | | | 33,908 | | 7.45 | | | | 426,194 | | | 31,158 | | 7.31 | | | | 343,182 | | | 23,441 | | | 6.83 | |

| Total loans | | | 1,046,093 | | | 81,558 | | 7.80 | | | | 955,692 | | | 71,104 | | 7.44 | | | | 854,684 | | | 57,599 | | | 6.74 | |

Securities available-for-sale | | | 102,613 | | | 4,828 | | 4.71 | | | | 148,917 | | | 6,735 | | 4.52 | | | | 134,157 | | | 5,582 | | | 4.16 | |

| Securities held-to-maturity | | | 88,535 | | | 4,527 | | 5.11 | | | | 96,668 | | | 4,563 | | 4.72 | | | | 93,069 | | | 4,306 | | | 4.63 | |

| Securities held-for-trading | | | 38,614 | | | 1,884 | | 4.88 | | | | - | | | - | | - | | | | - | | | - | | | - | |

| Daily interest-earning deposits | | | 21,607 | | | 1,138 | | 5.27 | | | | 5,356 | | | 256 | | 4.78 | | | | 6,912 | | | 315 | | | 4.56 | |

Total securities and interest-earning deposits | | | 251,369 | | | 12,377 | | 4.92 | | | | 250,941 | | | 11,554 | | 4.60 | | | | 234,138 | | | 10,203 | | | 4.36 | |

| Total interest-earning assets | | | 1,297,462 | | | 93,935 | | 7.24 | | | | 1,206,633 | | | 82,658 | | 6.85 | | | | 1,088,822 | | | 67,802 | | | 6.23 | |

| Noninterest-earning assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Office properties andequipment, net | | | 13,744 | | | | | | | | | 12,093 | | | | | | | | | 12,741 | | | | | | | |

| Real estate, net | | | - | | | | | | | | | - | | | | | | | | | 328 | | | | | | | |

Other noninterest-earning assets | | | 59,103 | | | | | | | | | 56,830 | | | | | | | | | 53,847 | | | | | | | |

| Total assets | | $ | 1,370,309 | | | | | | | | $ | 1,275,556 | | | | | | | | $ | 1,155,738 | | | | | | | |

| | | FOR THE YEARS ENDED DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | |

(Dollars in thousands) | | AVERAGE BALANCE | | | INTEREST AND DIVIDEND | | YIELD/ COST | | | AVERAGE BALANCE | | | INTEREST AND DIVIDEND | | YIELD/ COST | | | AVERAGE BALANCE | | | INTEREST AND DIVIDEND | | | YIELD/ COST | |

| LIABILITIES AND EQUITY | | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-bearing liabilities | | | | | | | | | | | | | | | | | | | | | | | | | |

| Savings accounts | | $ | 13,261 | | | $ | 66 | | 0.50 | % | | $ | 14,748 | | | $ | 75 | | 0.51 | % | | $ | 15,465 | | | $ | 67 | | | 0.43 | % |

| Checking accounts | | | 51,021 | | | | 747 | | 1.46 | | | | 45,039 | | | | 656 | | 1.46 | | | | 39,618 | | | | 245 | | | 0.62 | |

| Money market accounts | | | 284,843 | | | | 12,314 | | 4.32 | | | | 229,788 | | | | 8,505 | | 3.70 | | | | 170,641 | | | | 3,255 | | | 1.91 | |

| Certificates of deposit | | | 444,726 | | | | 22,093 | | 4.97 | | | | 446,437 | | | | 19,339 | | 4.33 | | | | 467,388 | | | | 14,747 | | | 3.16 | |

| Total interest-bearing deposits | | | 793,851 | | | | 35,220 | | 4.44 | | | | 736,012 | | | | 28,575 | | 3.88 | | | | 693,112 | | | | 18,314 | | | 2.64 | |

| Other interest-bearing liabilities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| FHLB advances | | | 226,124 | | | | 10,240 | | 4.53 | | | | 237,888 | | | | 11,194 | | 4.71 | | | | 239,896 | | | | 11,031 | | | 4.60 | |

| Other interest-bearing liabilities | | | 134,410 | | | | 5,080 | | 3.78 | | | | 104,085 | | | | 3,499 | | 3.36 | | | | 39,495 | | | | 1,931 | | | 4.89 | |

| Total interest-bearing liabilities | | | 1,154,385 | | | | 50,540 | | 4.38 | | | | 1,077,985 | | | | 43,268 | | 4.01 | | | | 972,503 | | | | 31,276 | | | 3.22 | |

| Other liabilities | | | 98,390 | | | | | | | | | | 88,468 | | | | | | | | | | 83,865 | | | | | | | | |

| Total liabilities | | | 1,252,775 | | | | | | | | | | 1,166,453 | | | | | | | | | | 1,056,368 | | | | | | | | |

| Stockholders’ equity | | | 117,534 | | | | | | | | | | 109,103 | | | | | | | | | | 99,370 | | | | | | | | |

| Total liabilities and stockholders’ equity | | $ | 1,370,309 | | | | | | | | | $ | 1,275,556 | | | | | | | | | $ | 1,155,738 | | | | | | | | |

Net interest income (2) | | | | | | $ | 43,395 | | | | | | | | | $ | 39,390 | | | | | | | | | $ | 36,526 | | | | |

Interest rate spread (3) | | | | | | | | | 2.86 | % | | | | | | | | | 2.84 | % | | | | | | | | | | 3.01 | % |

Net interest margin (4) | | | | | | | | | 3.34 | % | | | | | | | | | 3.26 | % | | | | | | | | | | 3.35 | % |

| Average interest-earning assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

to average interest-bearing liabilities | | | 112.39 | % | | | | | | | | | 111.93 | % | | | | | | | | | 111.96 | % | | | | | | | |

(1) Does not include interest on loans 90 days or more past due.

(2) Interest and dividends on total interest-earning assets less interest on total interest-bearing liabilities.

(3) Total interest-earning assets yield less total interest-bearing liabilities cost.

(4) Net interest income as an annualized percentage of total interest-earning assets.

Other Income

Other income is derived from sources other than interest and fees on earning assets. The Corporation’s primary sources of other income are service charge fees on deposit accounts, other service fees, the accretion of cash surrender value of bank owned life insurance (“BOLI”), gains on the sale of single-family residential and other loans, gains on the sale of securities, and rental income, primarily on space at the building that formerly served as the headquarters of Issaquah Bank. Other income for the year ended December 31, 2007, was $7.6 million, compared to $6.0 million and $6.3 million for the same periods in 2006 and 2005, respectively. In 2007, the implementation of Statement of Financial Accounting Standards (“SFAS”) No. 159 resulted in $1.1 million of net fair value gain. There were no corresponding gains in 2006 or 2005. The fair value of financial instruments is discussed in more detail in Note 15 of the Notes to Consolidated Financial Statements.

Other Expense

Other expense represents costs not associated with deposits and other interest-bearing liabilities. It includes expenses associated with personnel, premises and equipment, marketing, and other operations.

Other expense increased by $2.1 million to $26.7 million for the year ended December 31, 2007, from $24.6 million and $22.6 million for 2006 and 2005, respectively. Salaries and employee benefits increased overall by $1.1 million to $13.8 million during 2007 compared to the prior year. B&O tax increased $346,000 to $1.4 million and other expenses increased $410,000 to $6.7 million during 2007 compared to the prior year.

A standard measurement used to calculate the overhead costs of financial institutions is the efficiency ratio. The efficiency ratio is calculated by dividing other expense by total revenue, which generally indicates how much an institution spends to generate a dollar of revenue. The lower the efficiency ratio, the more efficient the institution. For the years ending December 31, 2007, 2006, and 2005, the Corporation’s efficiency ratio was 52.36%, 54.14%, and 52.75%, respectively. Management continues to look for ways to improve the efficiency ratio by increasing other income and net interest income while diligently controlling costs and maintaining high standards of service.

Liquidity Management

Liquidity is a term used to define the Corporation's ability to meet its financial commitments. The Corporation is required by prudent business practice and its regulators to maintain adequate levels of liquidity. The main liquidity requirements are funding customer loan requests and deposit outflows of the Bank. Primary sources of liquidity are cash and cash equivalents, which include highly liquid investments. At December 31, 2007, December 31, 2006, and December 31, 2005, cash and cash equivalents totaled $14.5 million, $42.9 million,

and $31.1 million, respectively. Another source of liquidity is the Corporation’s investment portfolio, which consists of investment-grade securities. These securities are of the highest credit quality and can be sold or used as collateral to secure borrowings.

The primary source of borrowings are Federal Home Loan Bank of Seattle (FHLB-Seattle) advances and repurchase agreements. At December 31, 2007, $264.7 million of additional borrowing capacity remained under the Bank’s existing credit line from the FHLB-Seattle, which is 35% of the Bank’s assets. The use of this Line of Credit is subject to the availability of eligible collateral, which includes residential mortgages, investment grade securities, and commercial real estate mortgages. At December 31, 2007, the Bank had unencumbered eligible collateral of approximately $85.5 million to pledge against the line. In addition, the Bank has the ability to borrow through repurchase agreements. Under these agreements, borrowings are collateralized with mortgage-backed securities or other investment securities.

The Bank has Fed funds borrowing lines with three of its correspondent banks. The Bank used each of these lines during the year. The Bank also has a Line of Credit with the Federal Reserve Bank of San Francisco. As of December 31, 2007, there were no outstanding balances on any of these lines.

Liquidity management is of critical importance to the Bank in that it significantly relies upon wholesale sources of funds (e.g. FHLB-Seattle advances). While these sources have proven to be stable and reliable, an interruption in the availability of these sources could have an adverse impact on the operations of the Corporation. Also see the Consolidated Statement of Cash Flows in the financial statement section of this filing for further information regarding liquidity.

Interest Rate Risk Management

Management considers interest rate risk to be a significant market risk that could have a material effect on the Corporation’s financial condition and results of operations.

The Corporation has taken steps to balance its sensitivity to changes in interest rates by altering its asset and liability mix. The origination of floating-rate loans such as business, construction and other prime-based loans is emphasized. The vast majority of fixed-rate loans have repricing periods with a maximum of five years. The mix of floating- and fixed-rates assets is designed to mitigate the impact of rate changes on the Corporation’s net interest income. Virtually all fixed-rate residential loans are sold into the secondary market. However, the Bank has sought to add prepayment provisions to its newly originated loans with 5 year fixed and adjustable rate loans. Many of the Bank’s fixed-rate loans do not have such provisions for prepayment fees, and as a result, a drop in rates can precipitate a refinancing of the Bank’s assets.

Interest rate risk is monitored using several methodologies, principally financial modeling. The earnings exposure to interest rate changes is evaluated in the context of certain upward and downward interest rate changes occurring instantaneously. At December 31, 2007, a 200 basis point increase in rates would increase forecasted net interest income over a twelve-month period by approximately 1.8%. A 200 basis point decrease in rates would decrease interest income by 5.6% according to the model.

The changes of the fair value of assets and liabilities and the resulting impact on the fair value of equity are also modeled under different rate scenarios. In the 200 basis point increase scenario, the fair value of equity declines by $1.9 million or 1.2%, a 200 basis point decrease in rates would decrease the fair value of equity by $34.6 million or 21.3%. Both are within the guideline established by the Bank’s Asset/Liability Policy.

The Corporation maintained a trading account for financial instruments during 2007, however there was no balance as of December 31, 2007. Moreover, the Corporation is not subject to foreign currency exchange rate risk or commodity price risk.

The individual categories of assets and liabilities that are subject to interest rate sensitivity as of December 31, 2007, are shown in the following table.

| | | INTEREST REPRICING ASSUMPTIONS | |

(Dollars in thousands) | | <1 YEAR | | | 1-3 YEARS | | | 3-5 YEARS | | | 5-10 YEARS | | | 10 YEARS AND UP | | | TOTAL | | | FAIR VALUE | |

| | | | | | | | | | | | | | | | | | | | | | |

| Interest-Sensitive Assets | | | | | | | | | | | | | | | | | | | | | |

| Total loans | | $ | 769,203 | | | $ | 184,515 | | | $ | 142,227 | | | $ | 11,988 | | | $ | 220 | | | $ | 1,108,153 | | | $ | 1,126,274 | |

Investments and other interest-earning assets | | | 47,646 | | | | 20,426 | | | | 36,305 | | | | 102,551 | | | | 27,711 | | | | 234,639 | | | | 232,694 | |

| Interest-Sensitive Liabilities | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Checking accounts | | $ | 11,185 | | | $ | 12,202 | | | $ | 18,302 | | | $ | 8,236 | | | $ | 915 | | | $ | 50,840 | | | $ | 50,840 | |

| Money market accounts | | | 311,214 | | | | 1,462 | | | | 2,194 | | | | 987 | | | | 110 | | | | 315,967 | | | | 315,967 | |

| Savings accounts | | | 2,485 | | | | 2,711 | | | | 4,067 | | | | 1,830 | | | | 204 | | | | 11,297 | | | | 11,297 | |

| Certificates of deposit | | | 401,800 | | | | 25,080 | | | | 3,016 | | | | 9,546 | | | | - | | | | 439,442 | | | | 442,262 | |

| Borrowings | | | 142,625 | | | | 10,000 | | | | 35,000 | | | | 139,000 | | | | 25,000 | | | | 351,625 | | | | 364,499 | |

Junior subordinated debentures payable | | | - | | | | - | | | | 15,465 | | | | - | | | | 10,310 | | | | 25,775 | | | | 26,887 | |

Off-Balance Sheet Arrangements: Credit Commitments

Commitments to extend credit are agreements to lend to a customer as long as there is no violation of any condition established in the contract. Commitments generally have fixed expiration dates or other termination clauses and may require payment of a fee. Since many of the commitments are expected to expire without being drawn upon, the total commitment amounts do not necessarily represent future cash requirements.

The Bank underwrites its standby letters of credit using its policies and procedures applicable to loans in general. Standby letters of credit are made on an unsecured and secured basis. The Bank had not incurred any losses on its commitments in 2007 or 2006.

A summary of the notional amount of the Bank’s financial instruments with off-balance sheet risk at December 31, 2007 follows:

| (Dollars in thousands) | | TOTAL | |

| Commitments to extend credit | | $ | 308,753 | |

| Standby letters of credit and financial guarantees written | | | 5,171 | |

| Unused commitments on bankcards | | | 12,840 | |

| Total | | $ | 326,764 | |

The following table sets forth the Corporation’s long-term contractual obligations:

| | | PAYMENTS DUE PER PERIOD | |

| (Dollars in thousands) | | <1 YEAR | | | 1-3 YEARS | | | 3-5 YEARS | | | THEREAFTER | | | TOTAL | |

| Certificates of deposit | | $ | 401,800 | | | $ | 25,080 | | | $ | 3,016 | | | $ | 9,546 | | | $ | 439,442 | |

| Federal Home Loan Bank advances | | | 2,000 | | | | 10,000 | | | | 50,000 | | | | 169,000 | | | | 231,000 | |

| Operating lease obligations | | | 813 | | | | 1,541 | | | | 1,463 | | | | 7,445 | | | | 11,262 | |

| Junior subordinated debentures payable | | | - | | | | - | | | | - | | | | 26,887 | | | | 26,887 | |

| Total | | $ | 404,613 | | | $ | 36,621 | | | $ | 54,479 | | | $ | 212,878 | | | $ | 708,591 | |

The Corporation also has operating leases comprised of leases for office space.

Summation of Factors That May Affect Financial Condition and Future Results

Credit risk: The most significant risk that may impact Cascade Financial Corporation would be deterioration in the quality of the loan portfolio. The Corporation’s loan growth has been focused on commercial lending. While it has not been the Corporation’s experience, historically for the banking industry, commercial loans have higher levels of losses than residential loans. The Corporation’s ability to meet its profitability and growth goals would be severely compromised with a large number of impaired credits. In addition, the Corporation and its subsidiary, Cascade Bank, could face regulatory restrictions on its activities.

Interest rate risk: While the Corporation actively manages its exposure to changes in interest rates, volatile interest rates and/or changes in the shape of the yield curve could have a meaningful impact on the Corporation’s net income. Many of the assets and liabilities of the Corporation have embedded options, which add another layer of complexity in its interest rate risk management practices.

Liquidity: Disruptions in the capital markets could have a major impact on the Corporation’s net income and balance sheet. As a user of Federal Home Loan Bank advances, repurchase agreements and brokered CDs, interruption or truncation of these sources of funds could force the Corporation to liquidate assets at an inauspicious time or curtail lending activity, which could adversely affect customer relationships.

Recently issued accounting pronouncements: In December 2004, the FASB issued No. 123(R), Share-Based Payment, which is a revision of No. 123, Accounting for Stock-Based Compensation. Statement 123(R) supersedes the Accounting Principles Board (“APB”) Opinion No. 25, which the Corporation had used to report stock options granted to employees and directors. Statement 123(R) requires all share-based payments to employees, including stock options, be recognized in the income statement based on their fair values.

Available Information

A copy of the Corporation’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to such reports filed pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, are available free of charge on or through our website located at www.cascadebank.com as soon as reasonably practicable after filing with the United States Securities and Exchange Commission. These reports are also available to shareholders, at no charge, upon written request to the Secretary of Cascade Financial Corporation at 2828 Colby Avenue, Everett, Washington 98201.

The Board of DirectorsCascade Financial Corporation:

We have audited the accompanying consolidated balance sheets of Cascade Financial Corporation and Subsidiaries (the Corporation) as of December 31, 2007 and 2006, and the related consolidated statements of income, stockholders' equity and comprehensive income, and cash flows for each of the years in the three-year period ended December 31, 2007. We also have audited the Corporation’s internal control over financial reporting as of December 31, 2007, based on criteria established in Internal Control - Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The Corporation’s management is responsible for these financial statements, for maintaining effective internal control over financial reporting, and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Report of Management on Internal Control over Financial Reporting. Our responsibility is to express an opinion on these financial statements and an opinion on the effectiveness of the Corporation's internal control over financial reporting based on our audits.

We conducted our audits in accordance with auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement and whether effective internal control over financial reporting was maintained in all material respects. Our audits of the financial statements included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risks. Our audits also included performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Cascade Financial Corporation and Subsidiaries as of December 31, 2007 and 2006, and the results of their operations and their cash flows for each of the years in the three-year period ended December 31, 2007, in conformity with accounting principles generally accepted in the United States of America. Also in our opinion, Cascade Financial Corporation maintained, in all material respects, effective internal control over financial reporting as of December 31, 2007, based on criteria established in Internal Control - Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

As discussed in Note 7 to the consolidated financial statements, effective January 1, 2007, the Corporation adopted Statement of Financial Accounting Standards No. 159, The Fair Value Option for Financial Assets and Financial Liabilities and No. 157, Fair Value Measurements.

/s/ Moss Adams LLP

Everett, Washington

March 12, 2008

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Consolidated Balance Sheets

December 31, 2007, and 2006

| | | DECEMBER 31, | |

| (Dollars in thousands, except share amounts) | | 2007 | | | 2006 | |

| ASSETS | | | | | | |

| Cash on hand and in banks | | $ | 12,911 | | | $ | 23,707 | |

| Interest-bearing deposits in other financial institutions | | | 1,619 | | | | 19,172 | |

| Securities available-for-sale, fair value | | | 82,860 | | | | 130,656 | |

| Securities held-to-maturity, amortized cost | | | 137,238 | | | | 96,846 | |

| Federal Home Loan Bank (FHLB) stock | | | 11,920 | | | | 11,920 | |

| Loans, net | | | 1,092,776 | | | | 996,015 | |

| Goodwill | | | 24,585 | | | | 25,195 | |

| Core deposit intangible, net | | | 634 | | | | 775 | |

| Premises and equipment, net | | | 14,160 | | | | 12,003 | |

| Cash surrender value of bank owned life insurance (BOLI) | | | 22,658 | | | | 17,974 | |

| Accrued interest receivable and other assets | | | 16,227 | | | | 10,991 | |

| Total assets | | $ | 1,417,588 | | | $ | 1,345,254 | |

| | | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

| Liabilities: | | | | | | | | |

| Deposits | | $ | 904,896 | | | $ | 855,449 | |

| FHLB advances | | | 231,000 | | | | 243,000 | |

| Securities sold under agreements to repurchase | | | 120,625 | | | | 95,710 | |

| Junior subordinated debentures payable | | | 15,465 | | | | 25,775 | |

| Junior subordinated debentures payable, fair value | | | 11,422 | | | | — | |

| Advance payments by borrowers for taxes and insurance | | | 502 | | | | 703 | |

| Dividends payable | | | 1,082 | | | | 967 | |

| Accrued interest payable, expenses, and other liabilities | | | 10,500 | | | | 8,451 | |

| Total liabilities | | | 1,295,492 | | | | 1,230,055 | |

| | | | | | | | | |

| Stockholders’ equity: | | | | | | | | |

| Preferred stock, $.01 par value. Authorized 500,000 shares; no shares issued or outstanding | | | | | | | | |

Common stock, $.01 par value. Authorized 25,000,000 shares; issued and outstanding 12,023,685 shares at December 31, 2007, and 12,093,699 shares at December 31, 2006 | | | 120 | | | | 121 | |

| Additional paid-in capital | | | 40,322 | | | | 39,430 | |

| Retained earnings, substantially restricted | | | 82,169 | | | | 77,952 | |

| Accumulated other comprehensive loss | | | (515 | ) | | | (2,304 | ) |

| Total stockholders’ equity | | | 122,096 | | | | 115,199 | |

| Total liabilities and stockholders’ equity | | $ | 1,417,588 | | | $ | 1,345,254 | |

(See accompanying notes to consolidated financial statements.)

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Consolidated Statements of Income

Years ended December 31, 2007, 2006, and 2005

| | | YEARS ENDED | |

| | | DECEMBER 31, | |

| (Dollars in thousands, except share amounts) | | 2007 | | | 2006 | | | 2005 | |

| Interest income: | | | | | | | | | |

| Loans | | $ | 81,558 | | | $ | 71,104 | | | $ | 57,599 | |

| Securities held-for-trading | | | 1,884 | | | | — | | | | — | |

| Securities available-for-sale | | | 4,756 | | | | 6,723 | | | | 5,534 | |

| Securities held-to-maturity | | | 4,527 | | | | 4,563 | | | | 4,306 | |

| FHLB dividends | | | 72 | | | | 12 | | | | 48 | |

| Interest-bearing deposits | | | 1,138 | | | | 256 | | | | 315 | |

| Total interest income | | | 93,935 | | | | 82,658 | | | | 67,802 | |

| Interest expense: | | | | | | | | | | | | |

| Deposits | | | 35,220 | | | | 28,576 | | | | 18,314 | |

| FHLB advances | | | 10,240 | | | | 11,193 | | | | 11,031 | |

| Securities sold under agreements to repurchase | | | 2,960 | | | | 1,619 | | | | 733 | |

| Junior subordinated debentures payable | | | 2,120 | | | | 1,880 | | | | 1,198 | |

| Total interest expense | | | 50,540 | | | | 43,268 | | | | 31,276 | |

| Net interest income | | | 43,395 | | | | 39,390 | | | | 36,526 | |

| Provision for loan losses | | | 1,350 | | | | 1,000 | | | | 945 | |

| Net interest income after provision for loan losses | | | 42,045 | | | | 38,390 | | | | 35,581 | |

| Other income: | | | | | | | | | | | | |

| Gain on sale of loans | | | 199 | | | | 483 | | | | 865 | |

| (Loss) gain on sale of securities available-for-sale, net | | | (435 | ) | | | — | | | | 67 | |

| Net gain on fair value of financial instruments | | | 1,081 | | | | — | | | | — | |

| Net gain on FHLB advances | | | 569 | | | | — | | | | — | |

| (Loss) gain on sale of REO, net | | | — | | | | (27 | ) | | | 33 | |

| Checking service fees | | | 3,820 | | | | 3,311 | | | | 3,124 | |

| Other service fees | | | 1,059 | | | | 1,156 | | | | 916 | |

| BOLI | | | 803 | | | | 769 | | | | 764 | |

| Other | | | 470 | | | | 334 | | | | 564 | |

| Total other income | | | 7,566 | | | | 6,026 | | | | 6,333 | |

| Other expenses: | | | | | | | | | | | | |

| Salaries and employee benefits | | | 13,817 | | | | 12,691 | | | | 12,114 | |

| Occupancy | | | 3,576 | | | | 3,450 | | | | 3,323 | |

| Marketing | | | 1,182 | | | | 1,094 | | | | 810 | |

| B&O tax | | | 1,373 | | | | 1,027 | | | | 713 | |

| Other | | | 6,734 | | | | 6,324 | | | | 5,646 | |

| Total other expenses | | | 26,682 | | | | 24,586 | | | | 22,606 | |

| Income before provision for income taxes | | | 22,929 | | | | 19,830 | | | | 19,308 | |

| Provision for income taxes | | | 7,383 | | | | 6,475 | | | | 6,262 | |

| Net income | | $ | 15,546 | | | $ | 13,355 | | | $ | 13,046 | |

| | | | | | | | | | | | | |

| Net income per common share, basic | | $ | 1.29 | | | $ | 1.11 | | | $ | 1.09 | |

| Weighted average number of shares outstanding, basic | | | 12,047,792 | | | | 12,060,191 | | | | 11,977,824 | |

| Net income per share, diluted | | $ | 1.27 | | | $ | 1.08 | | | $ | 1.06 | |

| Weighted average number of shares outstanding, diluted | | | 12,284,854 | | | | 12,363,198 | | | | 12,319,873 | |

| | | | | | | | | | | | | |

(See accompanying notes to consolidated financial statements.)

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Consolidated Statements of Stockholders’ Equity and Comprehensive Income

Years ended December 31, 2007, 2006, and 2005

| Consolidated Statement of Stockholders’ Equity | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands, except share amounts) | | SHARES | | | COMMON STOCK | | | ADDITIONAL PAID-IN CAPITAL | | | RETAINED EARNINGS | | | ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS), NET | | | TOTAL STOCK-HOLDERS’ EQUITY | |

| Balances at December 31, 2004 | | | 9,559,822 | | | $ | 96 | | | $ | 37,326 | | | $ | 59,975 | | | $ | (1,147 | ) | | $ | 96,250 | |

| Cash dividends | | | — | | | | — | | | | — | | | | (3,260 | ) | | | — | | | | (3,260 | ) |

| Options exercised, including related tax benefit | | | 81,019 | | | | — | | | | 803 | | | | — | | | | — | | | | 803 | |

| Net income | | | — | | | | — | | | | — | | | | 13,046 | | | | — | | | | 13,046 | |

| Shares repurchased | | | (40,953 | ) | | | — | | | | (42 | ) | | | (816 | ) | | | — | | | | (858 | ) |

Other comprehensive loss, net of tax (benefit) of $(457) | | | — | | | | — | | | | — | | | | — | | | | (850 | ) | | | (850 | ) |

| Issaquah merger | | | 3,899 | | | | — | | | | 62 | | | | — | | | | — | | | | 62 | |

| Balances at December 31, 2005 | | | 9,603,787 | | | | 96 | | | | 38,149 | | | | 68,945 | | | | (1,997 | ) | | | 105,193 | |

| Stock split (5-for-4) | | | 2,410,282 | | | | 24 | | | | (33 | ) | | | — | | | | — | | | | (9 | ) |

| Cash dividends | | | — | | | | — | | | | — | | | | (3,706 | ) | | | — | | | | (3,706 | ) |

| Options exercised, including related tax benefit | | | 122,920 | | | | 1 | | | | 1,058 | | | | — | | | | — | | | | 1,059 | |

| Stock compensation expense net of tax benefit | | | — | | | | — | | | | 287 | | | | — | | | | — | | | | 287 | |

| Net income | | | — | | | | — | | | | — | | | | 13,355 | | | | — | | | | 13,355 | |

| Shares repurchased | | | (43,290 | ) | | | — | | | | (31 | ) | | | (642 | ) | | | — | | | | (673 | ) |

Other comprehensive loss, net of tax (benefit) of $(165) | | | — | | | | — | | | | — | | | | — | | | | (307 | ) | | | (307 | ) |

| Balances at December 31, 2006 | | | 12,093,699 | | | | 121 | | | | 39,430 | | | | 77,952 | | | | (2,304 | ) | | | 115,199 | |

| Adoption of fair value option | | | — | | | | — | | | | — | | | | (4,532 | ) | | | — | | | | (4,532 | ) |

| Cash dividends | | | — | | | | — | | | | — | | | | (4,094 | ) | | | — | | | | (4,094 | ) |

| Options exercised, including related tax benefit | | | 108,818 | | | | — | | | | 813 | | | | — | | | | — | | | | 813 | |

| Stock compensation expense net of tax benefit | | | — | | | | — | | | | 213 | | | | — | | | | — | | | | 213 | |

| Net income | | | — | | | | — | | | | — | | | | 15,546 | | | | — | | | | 15,546 | |

| Shares repurchased | | | (178,832 | ) | | | (1 | ) | | | (134 | ) | | | (2,703 | ) | | | — | | | | (2,838 | ) |

Other comprehensive income,net of tax provision of $963 | | | — | | | | — | | | | — | | | | — | | | | 1,789 | | | | 1,789 | |

| Balances at December 31, 2007 | | | 12,023,685 | | | $ | 120 | | | $ | 40,322 | | | $ | 82,169 | | | $ | (515 | ) | | $ | 122,096 | |

| Consolidated Statement of Comprehensive Income | | | | | | | | | |

| | | YEARS ENDED DECEMBER 31, | |

| | | 2007 | | | 2006 | | | 2005 | |

| Net income | | $ | 15,546 | | | $ | 13,355 | | | $ | 13,046 | |

| Unrealized gain (loss) on securities available-for-sale, netof tax provision (benefit) of $953, $(165) and $(499) | | | 1,771 | | | | (307 | ) | | | (927 | ) |

| Unrealized (loss) on swaps available-for-sale, net of tax | | | | | | | | | | | | |

provision (benefit) of $0, $0 and $(77) | | | — | | | | — | | | | (146 | ) |

| Reclassification adjustment for gains on securities | | | | | | | | | | | | |

included in net income, net of tax provision of | | | | | | | | | | | | |

$10, $0 and $23 | | | 18 | | | | — | | | | 44 | |

| Reclassification adjustment for gains on swaps included | | | | | | | | | | | | |

in net income, net of tax provision of $0, $0 and $96 | | | — | | | | — | | | | 179 | |

| Comprehensive income | | $ | 17,335 | | | $ | 13,048 | | | $ | 12,196 | |

(See accompanying notes to consolidated financial statements.)

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Consolidated Statements of Cash Flows

Years ended December 31, 2007, 2006, and 2005

| | | YEARS ENDED | |

| | | DECEMBER 31, | |

| (Dollars in thousands) | | 2007 | | | 2006 | | | 2005 | |

| Cash flows from operating activities: | | | | | | | | | |

| Net income | | $ | 15,546 | | | $ | 13,355 | | | $ | 13,046 | |

| Adjustments to reconcile net income to net cash provided by (used in) operating activities: | | | | | | | | | | | | |

| Depreciation and amortization of premises and equipment | | | 1,875 | | | | 1,917 | | | | 1,874 | |

| Provision for losses on loans | | | 1,350 | | | | 1,000 | | | | 945 | |

| Increase in cash surrender value of bank owned life insurance | | | (684 | ) | | | (661 | ) | | | (663 | ) |

| Amortization of retained servicing rights | | | 44 | | | | 6 | | | | 30 | |

| Amortization of core deposit intangible | | | 141 | | | | 141 | | | | 141 | |

| Deferred income taxes | | | 1,982 | | | | 178 | | | | (150 | ) |

| Deferred loan fees, net | | | 290 | | | | (9 | ) | | | 748 | |

| Gain on sale of loans | | | (199 | ) | | | (483 | ) | | | (865 | ) |

| Stock-based compensation | | | 213 | | | | 287 | | | | — | |

| Excess tax benefits from stock-based compensation | | | (231 | ) | | | (314 | ) | | | (301 | ) |

| Purchase of securities held-for-trading | | | (46,413 | ) | | | — | | | | — | |

| Proceeds from sales/calls on securities held-for-trading | | | 112,162 | | | | — | | | | — | |

| Net (loss) gain on sales of securities available-for-sale | | | 435 | | | | — | | | | (67 | ) |

| Net gain on FHLB advances | | | (569 | ) | | | — | | | | — | |

| Loss on sales of premises and equipment | | | — | | | | — | | | | — | |

Net loss (gain) on sale of real estate owned, investment property and other repossessed assets | | | — | | | | 27 | | | | (33 | ) |

| Federal Home Loan Bank stock dividend received | | | — | | | | — | | | | (48 | ) |

| Net change in accrued interest receivable and other assets | | | (1,313 | ) | | | (562 | ) | | | (156 | ) |

Net change in accrued interest payable, expenses and other liabilities | | | (733 | ) | | | 1,764 | | | | 2,392 | |

| Net cash provided by operating activities | | | 83,896 | | | | 16,646 | | | | 16,893 | |

| Cash flows from investing activities: | | | | | | | | | | | | |

| Loans originated, net of principal repayments | | | (91,242 | ) | | | (133,462 | ) | | | (71,352 | ) |

| Purchases of securities held-to-maturity | | | (64,034 | ) | | | (3,434 | ) | | | (10,054 | ) |

| Proceeds from sales/calls on securities held-to-maturity | | | 5,000 | | | | — | | | | — | |

| Principal repayments on securities held-to-maturity | | | 2,658 | | | | 2,020 | | | | 6,271 | |

| Purchases of securities available-for-sale | | | (76,198 | ) | | | (5,716 | ) | | | (58,289 | ) |

| Proceeds from sales of securities available-for-sale | | | 66,220 | | | | — | | | | 6,488 | |

| Principal repayments on securities available-for-sale | | | 5,677 | | | | 15,184 | | | | 22,318 | |

| Purchases of premises and equipment | | | (4,047 | ) | | | (1,846 | ) | | | (1,345 | ) |

| Proceeds from sales/retirements of premises and equipment and REO | | | 15 | | | | 269 | | | | 25 | |

| Proceeds from loan participations sold | | | (6,818 | ) | | | 3,988 | | | | (1,747 | ) |

| Purchase CRA investment | | | (1,890 | ) | | | — | | | | — | |

| Purchase of bank owned life insurance | | | (4,000 | ) | | | — | | | | — | |

| | | | | | | | | | | | | |

| Net cash used in investing activities | | | (168,659 | ) | | | (122,997 | ) | | | (107,685 | ) |

| Subtotal, carried forward | | $ | (84,763 | ) | | $ | (106,351 | ) | | $ | (90,792 | ) |

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Consolidated Statements of Cash Flows, Continued

Years ended December 31, 2007, 2006, and 2005

| | | YEARS ENDED | |

| | | DECEMBER 31, | |

| (Dollars in thousands) | | 2007 | | | 2006 | | | 2005 | |

| | | | | | | | | | |

| Subtotal, brought forward | | $ | (84,763 | ) | | $ | (106,351 | ) | | $ | (90,792 | ) |

| Cash flows from financing activities: | | | | | | | | | | | | |

| Proceeds from issuance of common stock | | | 582 | | | | 736 | | | | 564 | |

| Dividends paid | | | (3,978 | ) | | | (3,603 | ) | | | (3,163 | ) |

| Repurchase of common stock | | | (2,838 | ) | | | (673 | ) | | | (858 | ) |

| Excess tax benefits from stock-based compensation | | | 231 | | | | 314 | | | | 301 | |

| Net increase in deposits | | | 49,134 | | | | 59,681 | | | | 73,860 | |

| Net increase (decrease) in Federal Home Loan Bank advances | | | (11,431 | ) | | | 7,000 | | | | 8,000 | |

| Net increase (decrease) in securities sold under agreements to repurchase | | | 24,915 | | | | 44,652 | | | | 30,156 | |

| Net increase (decrease) in advance payments by borrowers for taxes and insurance | | | (201 | ) | | | 14 | | | | 12 | |

| Proceeds from junior subordinated debentures payable | | | — | | | | 10,000 | | | | — | |

| Net cash provided by financing activities | | | 56,414 | | | | 118,121 | | | | 108,872 | |

| Net increase (decrease) in cash and cash equivalents | | | (28,349 | ) | | | 11,770 | | | | 18,080 | |

| Cash and cash equivalents at beginning of period | | | 42,879 | | | | 31,109 | | | | 13,029 | |

| Cash and cash equivalents at end of period | | $ | 14,530 | | | $ | 42,879 | | | $ | 31,109 | |

| | | | | | | | | | | | | |

| Supplemental disclosures of cash flow information – | | | | | | | | | | | | |

| Cash paid during the period for: | | | | | | | | | | | | |

| Interest | | $ | 51,457 | | | $ | 40,241 | | | $ | 30,642 | |

| Income taxes | | | 5,600 | | | | 6,700 | | | | 4,716 | |

| | | | | | | | | | | | | |

| Supplemental schedule of non-cash investing activities: | | | | | | | | | | | | |

| Mark-to-market on securities available-for-sale | | | (2,752 | ) | | | 472 | | | | 1,308 | |

| Retirement of common stock in retained earnings | | | 171 | | | | 142 | | | | 60 | |

| Dividends declared | | | 4,094 | | | | 3,706 | | | | 3,260 | |

| Cumulative adjustment to equity for SFAS No.159 | | | (3,162 | ) | | | — | | | | — | |

Notes to Consolidated Financial Statements

(Dollars in thousands, except share amounts)

(1) Summary of Significant Accounting Policies

The accounting and financial reporting policies of Cascade Financial Corporation (the “Corporation”) and its sole subsidiary, Cascade Bank (“the Bank”) conform to accounting principles generally accepted in the United States of America and to general practice within the financial institutions industry, where applicable. In preparing the consolidated financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expense. Actual results could differ from those estimates. A material estimate that is particularly susceptible to significant change relates to the determination of the allowance for losses on loans and the valuation of real estate acquired in connection with foreclosures or in satisfaction of loans. In connection with the determination of the estimated losses on loans and foreclosed assets held-for-sale, management obtains independent appraisals for significant properties.

The following is a description of the more significant policies that the Corporation follows in preparing and presenting its consolidated financial statements.

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Dollars in thousands, except share amounts)

(a) Basis of Presentation

The consolidated financial statements include the accounts of the Corporation and the Bank. All significant intercompany balances and transactions have been eliminated in the consolidation. In January 2003, the Financial Accounting Standards Board (FASB) issued Interpretation No. 46 (FIN 46), Consolidation of Variable Interest Entities and, in December 2003, issued Revised Interpretation No. 46 (FIN 46R), Consolidation of Variable Interest Entities, which replaced FIN 46. Historically, issuer trusts that issued trust preferred securities (junior subordinated debentures payable) have been consolidated by their parent companies and trust preferred securities have been treated as eligible for Tier 1 capital treatment by bank holding companies under Federal Reserve Board (FRB) rules and regulations relating to minority interests in equity accounts of consolidated subsidiaries. As a result of the adoption of FIN 46R, we deconsolidated the Trust and all periods in the consolidated financial statements have been restated to reflect this change.

In a Supervisory Letter dated July 2, 2003, the FRB stated that trust preferred securities continue to qualify as Tier 1 capital until notice is given to the contrary. The FRB will review the regulatory implications of any accounting treatment changes and will provide further guidance if necessary or warranted.

(b) Cash Equivalents

The Corporation considers all interest-bearing deposits and short-term highly liquid investment securities with an original maturity of three months or less to be cash equivalents.

(c) Interest-Bearing Deposits with Financial Institutions

Interest-bearing deposits with other financial institutions are carried at cost and include interest-bearing deposits at the Federal Home Loan Bank. At times throughout the year, the Bank has balances that exceed FDIC insurance limits.

(d) Federal Home Loan Bank (FHLB) Stock

As a member of the FHLB system, the Bank is required to maintain a minimum level of investment in FHLB stock based on specified percentages of its outstanding FHLB advances. The Bank's investment in FHLB stock is carried at par value ($100 per share), which reasonably approximates its fair value. The Bank may request redemption at par value of any stock in excess of the amount the Bank is required to hold. Stock redemptions are at the discretion of the FHLB. During 2002, the FHLB revised its capital structure from the issuance of one class of stock to two, B (1) and B (2) stock. Class B (1) stock can be sold back to the FHLB at cost, but is restricted as to purchase, sale and redemption. Class B (2) is not a required investment for institutions and is not restricted to purchase and sale, but has the same redemption restrictions as Class B (1) stock. Included in the balance sheet as of December 31, 2007, and 2006, the Bank has $11.9 million and $0 of Class B (1) and B (2) stock.

(e) Transfer of Financial Assets

Transfers of financial assets are accounted for as sales when control over the assets has been surrendered. Control over transferred assets is deemed to be surrendered when (1) the assets have been isolated from the Bank, (2) the transferee obtains the right (free of conditions that constrain it from taking advantage of that right) to pledge or exchange the transferred assets, and (3) the Bank does not maintain effective control over the transferred assets through an agreement to repurchase them before their maturity.

(f) Mortgage Servicing Rights

Servicing assets are recognized when rights are acquired through the sale of mortgage loans or when the Bank originates and sells mortgage loans and retains the servicing. Loans serviced for others are not included in the accompanying consolidated balance sheets. In 2006, the Bank sold $34.1 million of commercial real estate and multifamily loans and retained the servicing. In the two previous years, the Bank had not retained the servicing on any loans sold. Capitalized servicing rights are reported in other assets. Mortgage loans serviced for others include whole loans sold. Loans being serviced totaled $32.0 million and $39.0 million at December 31, 2007, and 2006, respectively.

Servicing fee income is recorded for fees earned for servicing loans. The fees are based on a contractual percentage of the outstanding principal or a fixed amount per loan and are recorded as income when earned. The amortization of mortgage servicing rights is netted against loan servicing fee income.

(g) Marketing Costs

The Bank expenses most marketing costs as they are incurred but some marketing costs are capitalized and amortized over the useful life of the expenditure. Marketing expense was $1.2 million, $1.1 million, and $810 for the years ended December 31, 2007, 2006, and 2005, respectively.

CASCADE FINANCIAL CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Dollars in thousands, except share amounts)

(h) Comprehensive Income

Comprehensive income is comprised of net income and other comprehensive income. Other comprehensive income includes items previously recorded directly to equity, such as unrealized gains and losses on securities available-for-

sale and certain derivative instruments. Comprehensive income is presented with the consolidated statement of stockholders equity.

(i) Earnings per Share (EPS) Data