January 03, 2013

Tia L. Jenkins

Senior Assistant Chief Accountant

United States Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, DC 20549

| Re: | Viña Concha y Toro S.A. |

| Form 20-F for Fiscal Year Ended December 31, 2011 | |

| Filed April 30, 2012 | |

| File No. 001-13358 |

Dear Ms. Jenkins,

In my capacity as Chief Financial Officer of Viña Concha y Toro S.A.(“Concha y Toro”, “we” or the “Company”), I transmit for your review this letter that provides the Company’s responses to the comments of the Staff of the Securities and Exchange Commission (the “Commission”)received in the letter dated December 06, 2012 (the “Comment Letter”) regarding the Company’s Annual Report on Form 20-F (“Form 20-F”) for the Fiscal Year Ended December 31, 2011, filed with the Commission on April 30, 2012. This letter is keyed to the headings and comment numbers contained in the Comment Letter. For ease of reference, each comment contained in the Comment Letter is printed below in bold and is followed by the Company’s response.

Form 20-F for the fiscal year ended December 31, 2011

Notes to the Consolidated Financial Statements, page F-13

Note 15. Biological Assets, page F-67

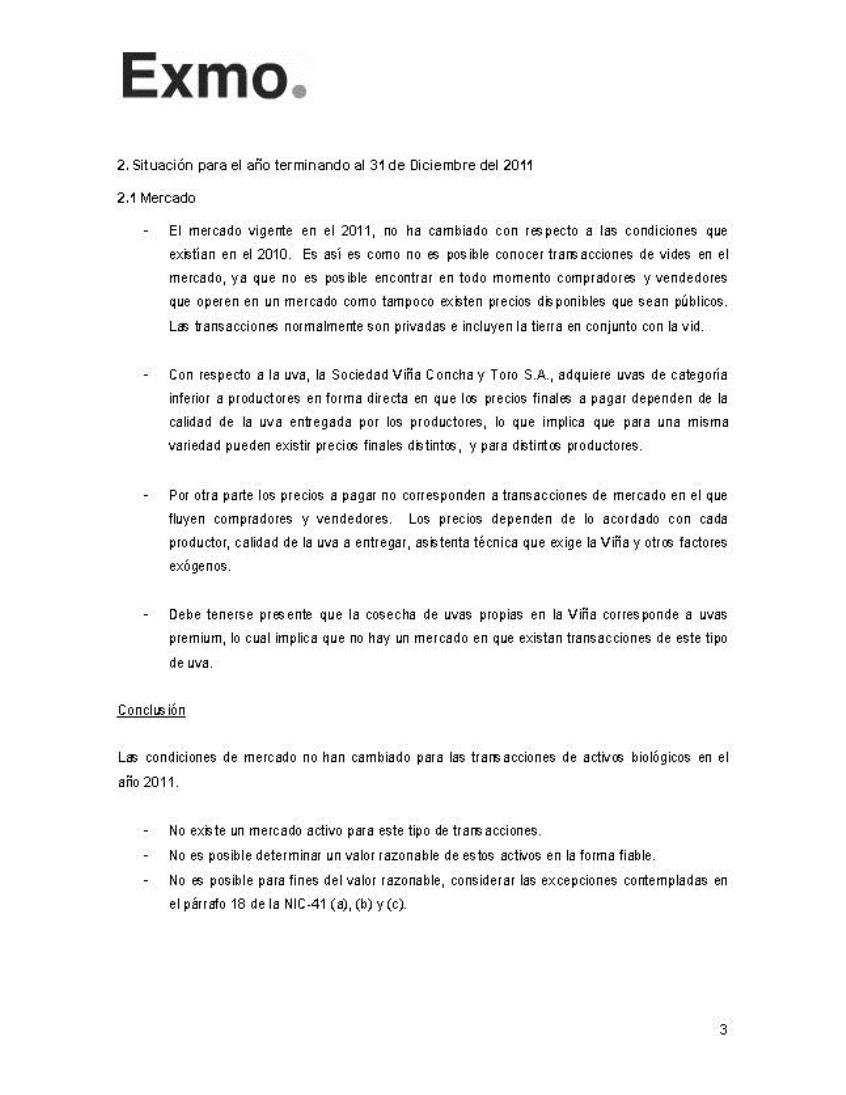

| 1. | We note your reference to a technical study conducted by an external consultant “A Biological Assets Valuation Model” in your response to comments one and two of our letter dated November 6, 2012. We further note your statement that in 2011, you requested external consultants to go through the findings of previous years and determine whether they were still valid. Please provide us with a courtesy copy of the referenced technical study. Also confirm to us that your accounting for biological assets is based on the conclusions of Company management and not your external consultants. |

| In accordance to your request we are submitting the following: | ||

| • | Exhibit 1: Technical study “Modelo de Valuación Activos Biológicos” (english translation: “A Biological Assets Valuation Model”). | |

| • | Exhibit 2: “Análisis situación criterio adoptado para el tratamiento de los activos biológicos para el año 2011” (english translation: “Analysis of issues concerning the treatment used for biological assets valuation in 2011”). |

| 1 |

| Both reports are submitted in their original versions, which are Spanish only. | |

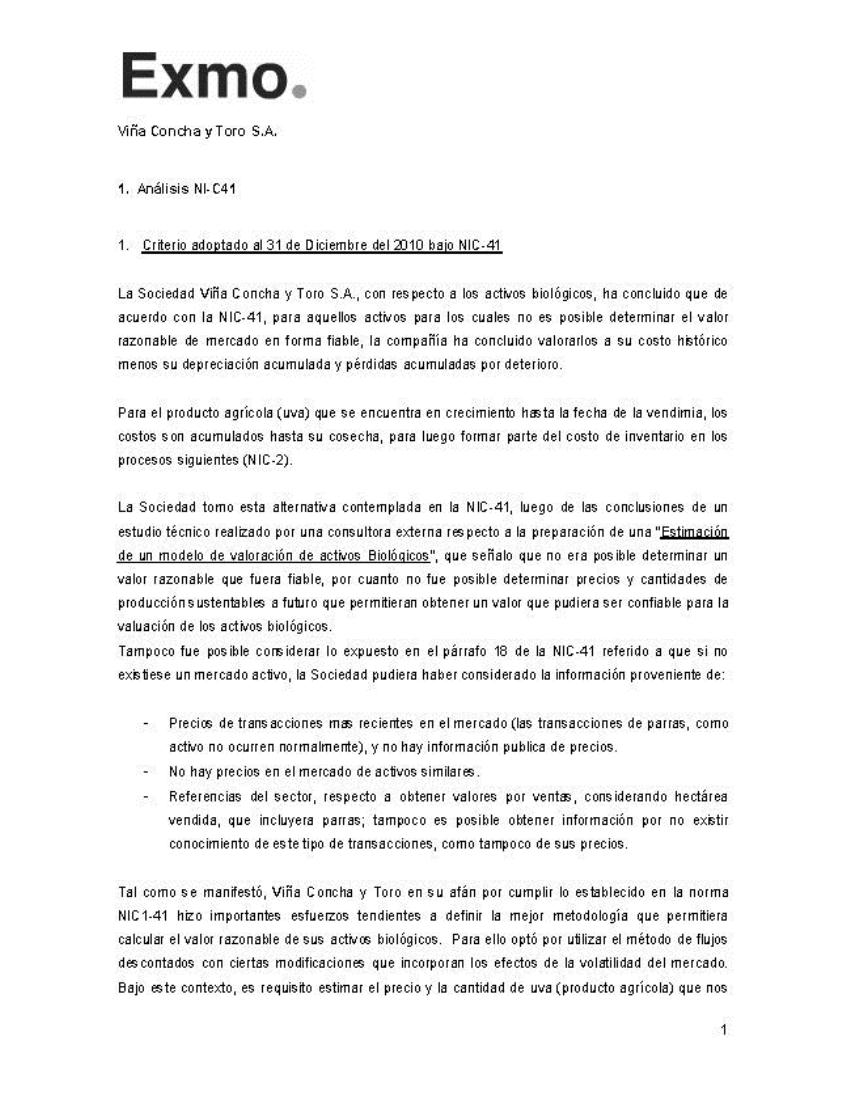

| We confirm that the criteria adopted for the treatment of biological assets are based on the Company’s Management (“Management”) analysis and conclusions. The technical study prepared by a third party specialist called “A Biological Assets Valuation Model” only confirms Management’s position, i.e. that it is not possible to reliably determine the fair value of biological assets, using either the market value for grapes or using the present value of net cash flows from vines (IAS 41 paragraph 20). |

| 2. | We note in your response to comments one and two of our letter dated November 6, 2012 that the Company grows grapes for its Reserve, Premium and Ultra-Premium wines in its own vineyards, and purchases mostly lower quality grapes used to produce Bi Varietal and Varietal wines sold at lower price points. We further note your disclosure on pages seven and 92 that in 2011, 68% of the grapes used in the production of your premium, varietal, bi-varietals and sparkling wines were purchased by the Company from independent growers in Chile. Please tell us if the Company currently purchases or has ever purchased higher quality grapes used for Reserve, Premium or Ultra-Premium wines from independent growers or if the Company has ever sold any of its higher quality grapes from Company vineyards to third parties, including any sold to Viñedos Emiliana or Viña Almaviva (pages 70-71) or related parties (page F-49) and, if so, tell us how those transaction prices were considered for purposes of determining the fair value of Company-grown grapes under IAS 41. In this regard, it appears that any such premium grape contract prices may be relevant for purposes of estimating the fair value of grapes grown by the Company using a cash flow model. |

| The Company purchases grapes for premium, varietal and generic wines from independent producers: | ||

| • | Acquisitions are direct and exclusive contracts with independent producers, in which the price has been negotiated, consisting in a fixed base and a variable component depending on the grapes’ alcohol content at the time of reception. | |

| • | Sales made to Emiliana Vineyards and Almaviva, related companies, are of surplus premium grape production, where sales prices were agreed directly between the parties and do not originate from market prices, as transactions of these varieties of grapes do not have a active market value as the transaction takes place between two related companies.(paragraph 8, IAS-41). | |

| • | As noted in the previous paragraph the values established for these transactions with related companies do not originate from market prices, as there is no active market for this type of asset, and thus these values cannot be used to determine a fair value of the Company’s grapes. | |

| • | For the preparation of the biological assets valuation model (paragraph 20, IAS-41), it is not possible to use the value of transactions for production and price projections, given that these sales are occasional, exclusive and non-repetitive, and take place with related companies. In addition, the grape variety sold in transactions occurring in subsequent years may be quite different from that sold in 2011, and at different prices. | |

| • | These sales prices from transactions with related companies do not ensure that the results from the discounted cash flow model are reliable, as these prices are not determined by an active market, nor the quality and/or varieties that were sold. | |

| 2 |

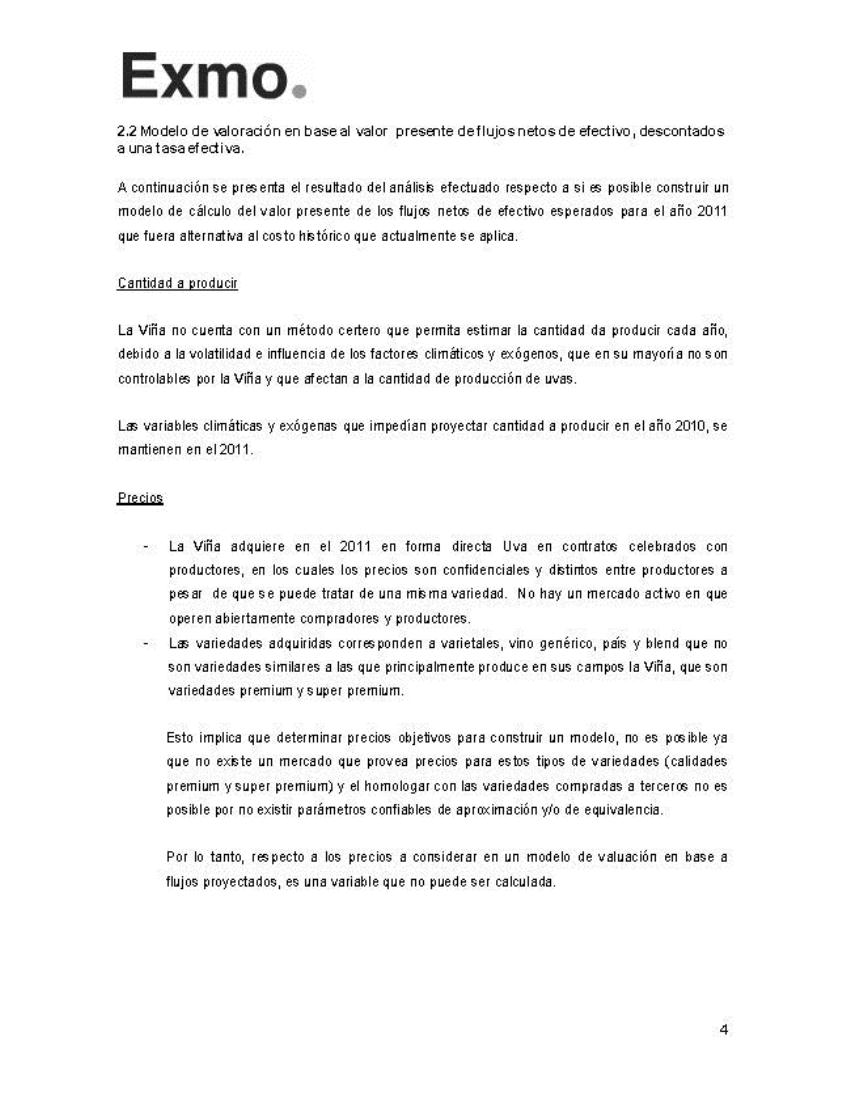

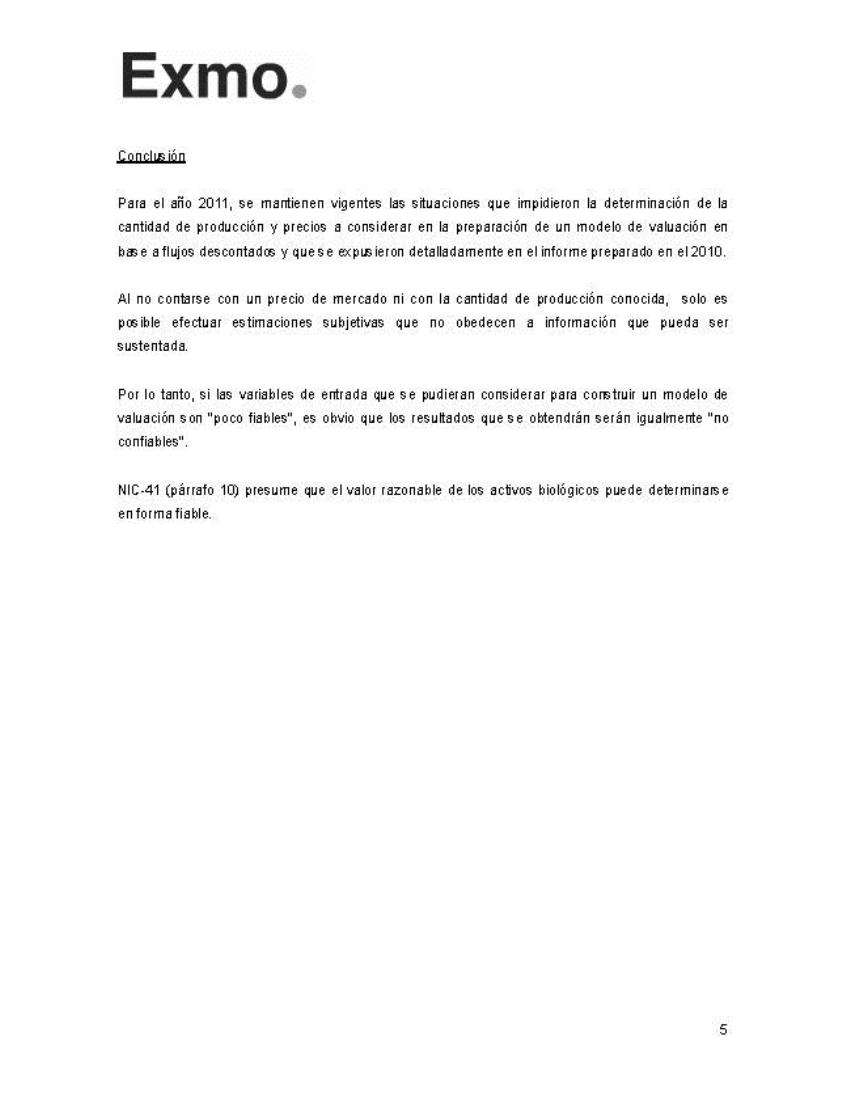

| 3. | We note in your response to comments one and two of our letter dated November 6, 2012 that the Company still does not have a precise method that allows it to estimate the quantity produced each year, and that to date you cannot estimate the quantity of grapes produced by the biological assets with any degree of confidence. Please advise us of the following: |

| • | Based on your response, it appears to us that you are unable to estimate the quantity of grapes that you produce and harvest each year. Please confirm our understanding and, if so, explain to us the process or method that the Company undertakes to attempt to estimate the quantity of grapes produced and harvested each year and tell us how this affects other aspects of your business such as your ability to estimate impairment for obsolescence of raw materials (page F-25), test your long-lived assets for impairment and prepare budgets, forecasts or projections. | |

| • | To the extent that you are actually able to estimate the quantity of grapes that are produced and harvested each year, it would appear to us that those estimates would become more reliable as the growing season progresses up to the point of harvest. If true, please further explain to us how this factor was considered for purposes of estimating fair value of grapes grown by the Company using a cash flow model. |

| Regarding the management of the winery, each year, an estimate of a season’s grape production is undertaken internally by the agriculture department, a figure which is also exposed to exogenous risks that may occur at the date of harvest. Based on this estimate of the amount of grapes produced in a year, the Company determines risk of impairment for obsolescence and/or write-down of raw materials. Also, with respect to vineyard plantings, assets subject to long term depreciation, impairment tests are carried out as required by IFRS, considering resulting margins to be reasonable, and also considering the technical studies for these effects (see item No. 4 of this response). | |

| With respect to the preparation of a biological assets valuation model based on discounted cash flows, the quantity produced and the price are base variables of the study. | |

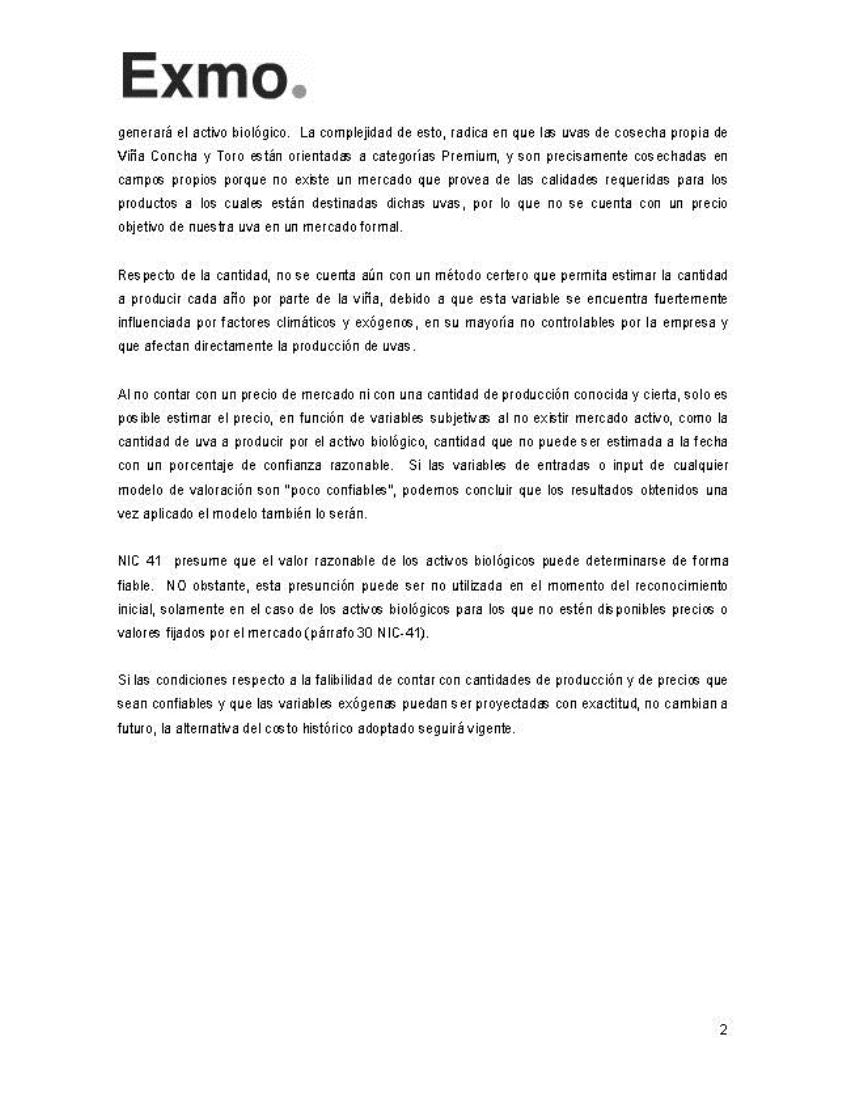

| To project the quantity of grape production in a minimum a10-year horizon, for the valuation study based on cash flows, there is no accurate basis which allows a reliable projection of production quantities, as this variable is strongly influenced by climate and other exogenous factors, mostly uncontrollable by the company and which directly affect grape production. | |

| The main factors affecting the estimation of grape production quantities are: |

| • | Soil variables: Characteristics of the terroir. | |

| • | Technology: Trellising, irrigation and harvest. This technology plan influences the quality and quantity of grapes to be harvested each year. | |

| • | Climate: Depending on the geographical areas of plantations, variations in temperature, rainfall, drought, pests, frost and sun radiation. |

| Regarding the last comment raised in point 3 of your letter dated December 6, 2012, we can confirm that as discussed in the previous point, the ten-year crop production and harvest estimates necessary to determine a biological asset value based the discounted cash flow method cannot be established, given the great amount of climatological and exogenous factors that affect the reliability of the model’s final outcome (see Biological Assets Valuation Model, page 50 of the technical study). |

| 3 |

| 4. | We note on page F-28 that the Company depreciates its biological assets on a straight-line basis considering the estimated useful lives of grapevines and subjecting the value to impairment test in each year. Please explain to us in sufficient detail how you test the biological assets for impairment, including how you measure the recoverable amount and the IFRS guidance you follow. |

| The Company performs annual impairment tests of the biological asset “Grapevines”. | |

| To this end, an internal technical report is prepared to determine whether there is any sign of deterioration that could indicate possible impairment of the asset “Grapevines”. The procedures set out in IAS 36 paragraph 12 are followed, considering factors such as: |

| a) | Whether any adverse significant changes have taken place with respect to the legal, economic, technological or market environment in which these assets operate. | |

| b) | If rates of return on investments have increased, affecting the discount rate of the asset and its final value. | |

| c) | If the market capitalization value exceeds the book value of this asset. | |

| d) | Whether the Company could present significant changes in use of the asset and/or whether there is physical impairment of the asset (uprooting of “Grapevines”). | |

| e) | That in accordance with technical plans prepared by the Company, decisions have been made to uproot “Grapevines” in different geographical areas, which involve making an immediate write-down of the assets’ value. | |

| f) | Internal reports of “Grapevine” yields are analyzed in order to be aware of low yields per hectare, as compared to yields estimated by the Company. |

| Through the Agricultural Area, responsible for agricultural land and plantations, the Company prepares on an annual basis, a form to evaluate the behavior of the parameters that can indicate signs of impairment for the grapevine biological asset. | |

| The form prepared by Agricultural Area includes the following scope: |

| i. | Evaluation of technological change in the plantings’ growth process depending on the years set for start of grape production (5 years after planting). The object is to ensure that plantings are treated with current technologies, to in turn ensure meeting deadlines for start of production, obtaining savings on maintenance and ensuring the quality of the product in development. The information is obtained from professional sources, the persons responsible for the agricultural areas of the different vineyards. As a result of this analysis, the Company has concluded that it is using cutting-edge technology for the treatment and development of its plantings. | |

| ii. | Projections for the removal of grape vines that are performed every year in the northern, central and southern areas. In case budgeting these removals, the cost of these removals and soil cleanup costs are calculated, which along with the value of the vines are provisioned to income on an annual basis. |

| 4 |

| iii. | Another factor that is analyzed and evaluated is the plantings’ grape yield per hectare, estimated by the Company. Lower yields attributable to climatic factors can affect the vines’ performance and its value. If this were the case, an estimation of the damage to plantings is performed together with a calculation of the necessary write-offs. | |

| iv. | An analysis of Chile in its context as a wine-exporting country is also carried out, considering information of both export and domestic wine sales. In the past ten years Chile’s wine exports have tripled, with Concha y Toro being the number one winery in the domestic market and the seventh largest wine exporting company in the world. The Company’s export sales represent around 35% of total Chilean exports, and this growth has led to a strong increase in the value of land and of grapevine plantings. The Company’s plantings are several years old, dating from 20 to 25 years back. |

All this information is analyzed in terms of the final margins obtained. Margins have increased over time, making a possible impairment of plantings value increasingly unlikely, as the grapevines’ production is precisely the source of the Company’s sales growth and profit margins

| 5. | We note in your response to comments one and two of our letter dated November 6, 2012 that sector benchmarks such as the value of hectares of land planted with vines are not possible to obtain as the Company has no knowledge of these types of transactions or the prices involved. We further note that the Company has acquired several new vineyards in the recent past based on the disclosures in your Forms 20-F for the fiscal years 2003-2011. Please advise us of the following: |

| • | How the Company considered its own acquisitions of new vineyards in the recent past for purposes of estimating the fair value your owned grapevines; | |

| • | Whether the Company has sold any of its vineyards in the recent past and, if so, how those transaction prices were considered; and | |

| • | The specific process and steps that the Company undertook in order to ultimately conclude it was not possible to obtain the value of hectares of land planted with vines. |

| Regarding your questions on this point we can inform you of the following: | |

| In the case of the first question, as expressed in the notes to the financial statements, vineyards are valued at their acquisition cost. | |

| It is not possible to value them at fair value as there is no active market for this type of transaction, as defined by IAS 41, paragraph 8. |

| a) | “The items traded within the market are homogeneous”: | |

| There is no exchange of productive grapevines in a formal market so it cannot be determined whether these would be homogeneous products, is these exchanges were to occur. | ||

| From another point of view it can be confirmed thatvitis vinifera plantatings are not homogeneous and there are factors that cause differentiations even in the same variety, such as geographic location, trellis system, soil type, yield per hectare, etc. | ||

| The geographic location affects the vines’ price, for example Chardonnay plantatings in the Limari or Casablanca trades at a higher price than Chardonnay planted in other areas; the same thing occurs with Maipo´s Cabernet Sauvignon. |

| 5 |

| Technical aspects such as the conduction system, planting density, age of the vineyard, mix of grape varieties, soil type, yield per hectare, weather and current conditions of the vineyard (vineyard management) affect the quality of the grape and its price. In the same sector, the same varieties with different technical management may have different qualities and be traded at different prices. |

| b) | “Willing buyers and sellers can normally be found at any time”; | |

| Currently, there is no market in which buyers and sellers operate at all times. Buying and selling of productive vines are not known. | ||

| Transactions are sporadic, and interest shown for the same estate is variable depending on the buyer (for example: depending on the concentration of grape production a vineyard may have in a given region, the buyer will have a lower/greater interest in buying a property in that area, in addition to climate risk,terroir,diversification of logistics, etc.). | ||

| c) | “Prices are available to the public”. | |

| This is another condition that is not met, as there are no prices informed or available to the public regarding transactions of grape vineyard plantings. | ||

| Transactions correspond to private negotiations between parties, there are no official records of prices in these transactions; any information that may be had is unofficial. | ||

| It can be established that there is no active market for transactions of productive grapevines which determines a fair market value for valuation purposes of these vines. This is because the companies do not sell vines that are in production. | ||

| There is no market with available prices or market-determined prices, to establish the fair value of the vines, that is to say, a market which provides a reliable value. | ||

| As noted above, grapevines are managed as a biological asset to produce an agricultural product. | ||

| At closing of the financial statements as of December 31, 2011, no active market exists for grapevines either in the growing or production stages, as these are not a regularly traded asset in this industry. There are an insufficient number of transactions on these assets to identify reference prices for valuation issues. | ||

| Considering the background information discussed it can be concluded that during the useful life (of the grapevine) there is no active market available to determine prices or fair values for them. Therefore as stated in IAS 41, in absence of an active market to determine prices for the grapevines, the use of recent transaction prices (in which there were no significant changes in economic conditions) and adjusted market prices of similar assets should be considered for valuation purposes. | ||

| There are no known recent market prices for transactions involving grapevines. Traders keep information regarding property transactions of agricultural land prices, for some wine regions. |

| 6 |

| Another factor to consider is the differences that may occur in the value of recent transactions due to the geographical location of grapevines. A fully identified specific grapevine variety will have a different market value (transaction value) depending on its geographic location, compared with the transaction values of the same variety located in a different area. | ||

| Even if it is possible to know the transactions within the same geographical area, for the same grape variety, nevertheless there would also be significant differences due to the different planting areas within the same geographical area. Thus, in a specific sector within an area, vine plantings may produce a better agricultural product (grapes) compared with others vines planted in another sector of the same area. | ||

| On the other hand, the transactions that have taken place in recent years are not significant and the values involved cannot be extrapolated, to be used as comparable figures for valuation effects. | ||

| This information (transaction value) cannot be reliably used, as significant changes in economic conditions generated in the wineries’ market in recent years and due to the technical differences that occur because of vine plantings location, the values that can be retrieved from these sources can significantly distort valuations. | ||

| According to IAS 41, companies often enter into contracts to sell their biological assets or agricultural produce at a future date. The prices of these contracts are not necessarily relevant in determining fair value, as this value reflects the current market in which a willing buyer and seller would enter into a transaction. As a consequence of the above, the value in the type of contract described above will not correspond to the fair value of a biological asset or of an agricultural product. | ||

| Therefore, according to the arguments mentioned, purchases of vineyards that were made in recent years do not provide reliable or comparable background information to use as prices of recent transactions, in order to value the asset “Grapevines”. |

| With respect to the second question above, of whether the Company has sold vineyards in the recent past, we inform that there have been no sales of vineyards in the last 10 years. | |

| Finally, regarding the third question of the fundamentals the Company considered for not using fair value for the value of hectares of land with vine plantings, the background information stated in the response of this point 5 explain and support why it is not possible to determine a reasonable fair value for the Company’s vine plantings. |

| 7 |

| 6. | We note in your response to comments one and two of our letter dated November 6, 2012 that Fetzer’s identifiable assets were measured at fair value in your April 15, 2011 acquisition and that the fair value did not differ significantly from book value. Please tell us the book value of the Fetzer assets on the acquisition date and the fair value that you assigned to these assets on that date. Also identify the method(s) that you used to estimate the fair value of the acquired Fetzer assets. |

| The following table shows the book valued of Fetzer’s assets on the date of acquisition and the fair value determined for such assets at that time. We also indicate the method the Company used to estimate the fair value of the Fetzer assets it acquired. |

| TANGIBLE ASSETS | FAIR VALUE | BOOK VALUE | VALUATION METHOD | |||||||

| US$ | US$ | |||||||||

| Finished Goods | 18,078,408 | 18,078,408 | Replacement cost method (RCM) | |||||||

| Work In Progress | 61,160,828 | 61,160,828 | Replacement cost method (RCM) | |||||||

| Raw Materials | 4,104,071 | 4,104,071 | Replacement cost method (RCM) | |||||||

| Total Inventories | 83,343,307 | 83,343,307 | ||||||||

| — | — | |||||||||

| Land | 15,792,001 | 17,875,935 | Market value | |||||||

| Buildings | 20,460,000 | 21,769,983 | Method of the Cost approach | |||||||

| Equipment | 35,578,808 | 23,709,279 | Method of the Cost approach | |||||||

| Construction in Progress | 783,356 | 770,573 | Method of the Cost approach | |||||||

| Total Fixed Assets | 72,614,164 | 64,125,771 | ||||||||

| — | — | |||||||||

| Goodwill | 43,485,361 | — | Residual method calculation | |||||||

| Brands/Trademarks (*) | 36,900,000 | — | Relief from royalty method (RFRM) | |||||||

| Wholesale Distribution Network | 3,600,000 | — | Replacement cost method (RCM) | |||||||

| Favorable/(unfavorable) supply contracts, | 1,313,054 | — | Comparative Method (Income approach) | |||||||

| Favorable/(unfavorable) leasehold interests, | (1,412,000 | ) | — | Comparative Method (Income approach) | ||||||

| 83,886,415 | — | |||||||||

As requested by the Commission in the Comment Letter, I acknowledge, on behalf of the Company, the following:

| a) | The company is responsible for the adequacy and accuracy of the disclosure in the filing; | |

| b) | Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and | |

| c) | The company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

| 8 |

If you would like to discuss any of the Company’s responses to the comments or any other matters, please call me at (56-2) 2476-5644.

Sincerely,

| /s/ OSVALDO SOLAR VENEGAS | |

| Osvaldo Solar Venegas | |

| Chief Financial Officer | |

| Vina Concha y Toro S.A. |

9

Exhibit 1

Exhibit 2