UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08786

Pioneer Variable Contracts Trust

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Terrence J. Cullen, Amundi Pioneer Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742-7825

Date of fiscal year end: December 31, 2020

Date of reporting period: January 1, 2020 through June 30, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

PIONEER VARIABLE CONTRACTS TRUST

Pioneer Bond VCT Portfolio — Class I and II Shares

Beginning in February 2021, as permitted by regulations adopted by the Securities and Exchange Commission, you may not be receiving paper copies of the Portfolio’s shareholder reports like this one by mail, unless you specifically request paper copies of the reports from the insurance company that offers your variable annuity or variable life insurance contract or from your financial intermediary. Instead, the insurance company may choose to make the reports available on a website, and will notify you by mail each time a shareholder report is posted and provide you with a website link to access the report. Instructions for requesting paper copies will be provided by your insurance company.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the insurance company or your financial intermediary electronically by following the instructions provided by the insurance company or by contacting your financial intermediary.

You may elect to receive all future Portfolio shareholder reports in paper free of charge from the insurance company. You can inform the insurance company or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by following the instructions provided by the insurance company or by contacting your financial intermediary. Your election to receive reports in paper will apply to all funds available under your contract with the insurance company.

SEMIANNUAL REPORT

June 30, 2020

Please refer to your contract prospectus to determine the applicable share class offered under your contract.

PIONEER VARIABLE CONTRACTS TRUST

Pioneer Bond VCT Portfolio | |

This report is authorized for distribution only when preceded or accompanied by a prospectus for the Portfolio being offered.

Pioneer Variable Contracts Trust files a complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. Shareholders may view the filed Form N-PORT by visiting the Commission’s web site at https://www.sec.gov.

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

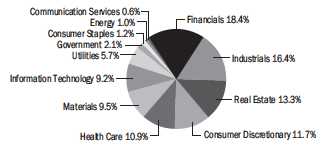

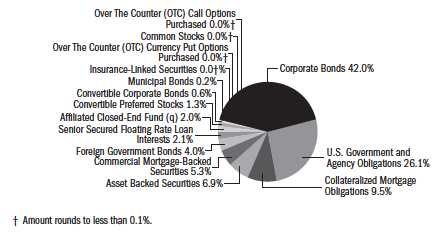

Portfolio Diversification

(As a percentage of total investments)*

(As a percentage of total investments)*

5 Largest Holdings

(As a percentage of total investments)*

(As a percentage of total investments)*

| 1. | United States Treasury | |

| Bill, 9/17/20 | 2.20% | |

| 2. | U.S. Treasury Bill, 8/27/20 | 1.65 |

| 3. | U.S. Treasury Inflation Indexed | |

| Bonds, 1.0%, 2/15/48 | 1.61 | |

| 4. | Pioneer ILS Interval Fund (k) | 1.51 |

| 5. | U.S. Treasury Inflation Indexed | |

| Bonds, 1.0%, 2/15/49 | 1.27 |

* | Excludes temporary cash investments and all derivative contracts except for options purchased. The Portfolio is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities. |

(k) | Pioneer ILS Interval Fund is an affiliated closed-end fund managed by Amundi Pioneer Asset Management, Inc. |

PERFORMANCE UPDATE 6/30/20

Prices and Distributions

| Net Asset Value per Share | 6/30/20 | 12/31/19 |

| Class I | $11.29 | $11.17 |

| Class II | $11.32 | $11.19 |

| Net | |||

| Distributions per Share | Investment | Short-Term | Long-Term |

| (1/1/20 – 6/30/20) | Income | Capital Gains | Capital Gains |

| Class I | $0.1709 | $ – | $ – |

| Class II | $0.1575 | $ – | $ – |

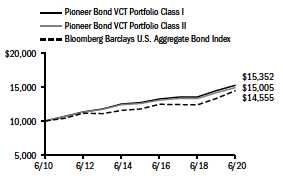

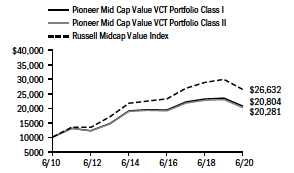

Performance of a $10,000 Investment

The following chart shows the change in value of an investment made in Class I and Class II shares of Pioneer Bond VCT Portfolio at net asset value during the periods shown, compared to that of the Bloomberg Barclays U.S. Aggregate Bond Index. Portfolio returns are based on net asset value and do not reflect any applicable insurance fees or surrender charges.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged, market value-weighted measure of Treasury and agency issues, corporate bond issues and mortgage-backed securities. Index returns are calculated monthly, assume reinvestment of dividends and, unlike Portfolio returns, do not reflect any fees, expenses or sales charges. It is not possible to invest directly in an index.

Average Annual Total Returns

(As of June 30, 2020)

(As of June 30, 2020)

| Bloomberg Barclays | |||

| U.S. Aggregate | |||

| Class I | Class II | Bond Index | |

10 Years | 4.38% | 4.14% | 3.82% |

5 Years | 3.77% | 3.53% | 4.30% |

1 Year | 5.48% | 5.31% | 8.74% |

All total returns shown assume reinvestment of distributions at net asset value.

The performance table does not reflect the deduction of taxes that a shareowner would pay on distributions or the redemption of shares.

Call 800-688-9915 or visit www.amundipioneer.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The returns for the Portfolio do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges. These expenses would reduce the overall returns shown.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers, performance would be lower. Waivers may not be in effect for all portfolios. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

2

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

As a shareowner in the Portfolio, you incur two types of costs:

(1) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses; and

(2) transaction costs, including sales charges (loads) on purchase payments.

This example is intended to help you understand your ongoing expenses (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds offered through your variable annuity contract. The example is based on an investment of $1,000 at the beginning of the Portfolio’s latest six-month period and held throughout the six months.

Using the Tables

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period as follows:

1. Divide your account value by $1,000

Example: an $8,600 account value ÷ $1,000 = 8.6

2. Multiply the result in (1) above by the corresponding share class’s number in the third row under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Expenses Paid on a $1,000 Investment in Pioneer Bond VCT Portfolio

Based on actual returns from January 1, 2020 through June 30, 2020.

| Share Class | I | II | ||||||

Beginning Account Value on 1/1/20 | $ | 1,000.00 | $ | 1,000.00 | ||||

Ending Account Value on 6/30/20 | $ | 1,026.50 | $ | 1,026.10 | ||||

Expenses Paid During Period* | $ | 3.02 | $ | 4.28 | ||||

* | Expenses are equal to the Portfolio’s annualized expense ratio of 0.60% and 0.85% for Class I and Class II shares multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You may use this information to compare the ongoing costs of investing in the Portfolio and other variable annuities. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other variable annuities.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) that are charged at the time of the transaction. Therefore, the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different variable annuities. In addition, if these transaction costs were included, your costs would have been higher.

Expenses Paid on a $1,000 Investment in Pioneer Bond VCT Portfolio

Based on a hypothetical 5% per year return before expenses, reflecting the period from January 1, 2020 through June 30, 2020.

| Share Class | I | II | ||||||

Beginning Account Value on 1/1/20 | $ | 1,000.00 | $ | 1,000.00 | ||||

Ending Account Value on 6/30/20 | $ | 1,021.88 | $ | 1,020.64 | ||||

Expenses Paid During Period* | $ | 3.02 | $ | 4.27 | ||||

* | Expenses are equal to the Portfolio’s annualized expense ratio of 0.60% and 0.85% for Class I and Class II shares multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

3

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

Call 1-800-688-9915 or visit www.amundipioneer.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The returns for the Portfolio do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges. These expenses would reduce the overall returns shown.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers, performance would be lower. Waivers may not be in effect for all portfolios. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

In the following interview, Brad Komenda discusses the factors that affected the performance of Pioneer Bond VCT Portfolio during the six-month period ended June 30, 2020. Mr. Komenda, Senior Vice President, Deputy Director of Investment Grade Corporates, and a portfolio manager at Amundi Pioneer Asset Management, Inc. (Amundi Pioneer), is responsible for the daily management of the Portfolio, along with Kenneth J. Taubes, Executive Vice President and Chief Investment Officer, U.S., and a portfolio manager at Amundi Pioneer, and Timothy Rowe, Managing Director, Director of Multisector Fixed Income, and a portfolio manager at Amundi Pioneer.

Q: How did the Portfolio perform during the six-month period ended June 30, 2020?

A: Pioneer Bond VCT Portfolio’s Class I shares returned 2.65% at net asset value during the six-month period ended June 30, 2020, and Class II shares returned 2.61%, while the Portfolio’s benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index (the Bloomberg Barclays Index), returned 6.14%.

Q: How would you describe the investment environment in the fixed-income markets during the six-month period ended June 30, 2020?

A. After a benign opening to the 2020 calendar year, credit-sensitive fixed-income markets experienced a historic disruption in March, as the emergence of the COVID-19 virus and the related lockdown policies implemented to help curb its spread all but shuttered the global economy. Investors fled riskier assets on a broad scale and moved into so-called “safe havens” such as U.S. Treasuries, which had the effect of driving Treasury yields to all-time lows. Significant selling in U.S. dollar (USD) fixed-income markets eventually stressed market functionality and led to price dislocations in all segments, even Treasury bonds. As the “liquidity grab” by investors gathered pace in mid-March, historical asset-class return relationships broke down and performance became almost entirely correlated. (Correlation is defined as the degree to which assets or asset-class prices have moved in relation to one another. Correlation ranges from -1, always moving in opposite directions; through 0, absolutely independent; to 1, always moving together.)

The liquidity stress was greatest in the securitized credit sectors of nonagency mortgage-backed securities (MBS), asset-backed securities (ABS), and commercial-mortgage backed securities (CMBS), which have traditionally had a narrower buyer base than corporate bonds. Those markets faced forced selling by real estate investment trusts (REITs) and other leveraged investors, and by certain mutual funds, as concerns escalated over the impact of the pandemic on the U.S. employment situation and on the ability of homeowners and businesses to service their mortgages.

The policy response to the market and economic turmoil from both central banks and government authorities was swift, as they sought to keep businesses and consumers from going under. The U.S. Federal Reserve (Fed) slashed the target range of the benchmark federal funds rate to zero in mid-March, resurrected its 2008 financial crisis-era lending facilities, and launched a wide-ranging bond-purchase program. On the fiscal side, the U.S. Congress and the White House agreed upon a $2.2 trillion stimulus package in late March, and later approved additional aid packages in the second quarter.

4

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

The extraordinary support from policy makers in the wake of the pandemic had a positive effect on the markets as the second quarter got underway. Investor optimism also rose on the prospects that steps taken towards re-opening the economy could support something resembling a “V-shaped” recovery (that is, a swift, sharp rise). The result was a revival of sentiment towards the riskier assets that the market had been so quick to shun at the height of the pandemic crisis. The shift in investors’ appetites allowed credit-sensitive areas of the bond market to recover much of their earlier losses over April and May. June saw the return of some market volatility as well as a widening in credit spreads as COVID-19 cases surged in a few states that had re-opened earlier than others, reigniting shutdown concerns. (Credit spreads are commonly defined as the differences in yield between Treasuries and other types of fixed-income securities with similar maturities.)

For the six-month period ended June 30, 2020, the investment-grade corporate bond market posted a positive return of 5.02%, while high-yield corporates returned -3.80% (as measured by the Bloomberg Barclays U.S. Corporate Bond Index and Bloomberg Barclays U.S. Corporate High Yield Index, respectively). Treasuries led performance within the investment-grade sectors, given the steep decline in yields seen over the first quarter of 2020. After their earlier struggles, securitized assets ended the six-month period in positive territory, though the asset class lagged the performance of both investment-grade corporates and Treasuries.

Q: What factors influenced the Portfolio’s performance relative to the Bloomberg Barclays Index during the six-month period ended June 30, 2020?

A: The Portfolio’s benchmark-relative underperformance for the six-month period derived mainly from asset allocation, while a tilt toward lower-quality holdings within spread sectors also weighed on relative returns. Positioning with respect to overall Portfolio duration was another detractor from benchmark-relative results, while security selection was a modest, positive contributor to relative performance. (Spread sectors represent non-governmental fixed-income market sectors that offer higher yields, at greater risk, than governmental investments. Duration is a measure of the sensitivity of the price, or the value of principal, of a fixed-income investment to a change in interest rates, expressed as a number of years.)

With respect to sector allocations, detractors from the Portfolio’s relative returns during the six-month period primarily reflected overweights to securitized sectors and corporate credit, and a corresponding underweight to U.S. Treasuries. The Portfolio’s significant exposure to non-agency MBS within securitized assets had the largest negative effect on benchmark-relative results. Non-agency MBS sold off in March due to the illiquidity issues discussed earlier, and because of fundamental concerns over the potential for increased delinquencies and defaults in the wake of the economic damage wrought by COVID-19. While valuations of securitized assets have not recovered to the same degree as we have seen with corporate bonds, we view the anticipated impairment reflected in current price levels within the securitized sectors as overstated. The Portfolio did realize losses on some securitized positions that we sold during the six-month period in order to fund purchases of new corporate issues that came into the market at historically wide spreads.

5

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

PORTFOLIO MANAGEMENT DISCUSSION 6/30/20 | (continued) |

The Portfolio’s lack of exposure to nominal U.S. Treasuries detracted significantly from benchmark-relative returns during the six-month period, as credit-sensitive securities underperformed in the flight-to-quality market environment that characterized the first quarter of 2020. We had based the Portfolio’s positioning within Treasuries on our view heading into the six-month period that the U.S. economy was poised for strong performance in 2020, a forecast that was derailed by the emergence of COVID-19. The Treasury exposure we did maintain in the Portfolio was a roughly 5% allocation to Treasury inflation-protected securities (TIPS), which underperformed as liquidity became a significant issue and inflation expectations fell dramatically.

Within investment-grade corporates, the Portfolio’s overweight to financials detracted from benchmark-relative performance. An overweight to industrials proved a headwind as well, but security selection within the sector largely offset that negative. The Portfolio’s positioning in the utilities sector had a modest, positive effect on relative returns.

The Portfolio’s duration positioning versus the benchmark detracted from relative performance in the declining-rate environment that prevailed during the six-month period. We had maintained the Portfolio’s duration in a range modestly below that of the Bloomberg Barclays Index, which acted as a drag on performance as Treasury yields declined. In addition, the Portfolio’s allocation to securitized assets felt the negative effects of declining rates due to the market’s expectations for an uptick in prepayment activity as rates moved sharply lower.

Q: Did the Portfolio have any exposure to derivative securities during the six-month period ended June 30, 2020. If so, did the derivatives have any material impact on performance?

A: Yes, we invested the Portfolio in Treasury futures and credit-default swaps during the six-month period. We invest in Treasury futures as part of our duration-management strategy for the Portfolio. We believe the use of Treasury futures allows us to express our views on duration and yield-curve positioning in the most efficient manner. We invest in credit-default swaps to either gain or reduce Portfolio exposure to corporate bonds very quickly, as cash-bond transactions take a little more time to settle.

The use of derivatives has allowed the Portfolio to benefit from the performance of the targeted asset classes, while retaining a better liquidity profile, which in turn may help to reduce risk. Treasury futures generally have not had an impact on the Portfolio’s performance, as we have used them primarily for hedging purposes. The credit-based derivatives had a modest effect on the Portfolio’s performance during the six-month period.

Q: What factors affected the Portfolio’s yield, or distributions* to shareholders, during the six-month period ended June 30, 2020?

A: The sharp, downward trajectory of Treasury yields weighed on the Portfolio’s distributions during the six-month period, although the widening of credit spreads helped to offset some of the decline.

* Distributions are not guaranteed.

6

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

Q: What is your investment outlook and how is the Portfolio positioned going into the second half of the fiscal year?

A: We expect that U.S. economic activity may continue to recover, but at a slower and more uneven pace relative to the re-opening “bounce” we witnessed for much of the second quarter. We believe there is a strong case to be made for additional federal government support for the economy in the near term. Enhanced unemployment benefits are scheduled to expire shortly, state and local governments need help bridging tax-revenue shortfalls, and delayed or suspended re-openings in some states could very well increase financial stress on small businesses. While passage of a fourth fiscal stimulus package seems likely, the legislative and political process may create near-term market volatility.

On the monetary side, we believe the Fed could keep its benchmark overnight lending rate at effectively zero for quite some time, possibly until the end of 2022. Should that scenario unfold, short-dated Treasury yields would likely remain low. In addition, we believe the yield curve could steepen further, with longer-maturity yields rising as economic activity picks up and issuance of Treasury notes increases substantially.

On balance, we do not look for the U.S. economic activity to return to pre-COVID levels until well into 2021, as many segments such as travel, hospitality, and consumer services could continue to struggle due to lingering concerns about the virus as well as structural changes.

The combination of attractive spreads, positive economic momentum, and supportive supply/demand dynamics have led us to enter the second half of 2020 with a constructive stance on the credit markets. As of the end of the six-month period, corporate bond and securitized credit spreads were offering attractive long-term value across a number of sectors, in our opinion. That said, we expect that selectivity with regard to choosing investments will become even more important, given the partial recovery in spreads during the second quarter of 2020 and the eventual dialing back of policy support from the Fed and the U.S. government.

As the world waits for a medical solution and learns how to live with the virus, we believe the key question still awaiting an answer is what type of activities are acceptable, without leading to an unacceptable rise in infections? Government restrictions and other recommendations seem to have had a material impact on virus spread over the past few months. Therefore, at this point, we believe individuals’ choices about what activities they are and are not comfortable with will be as important a driver of economic re-engagement and recovery as any other factor currently in play.

Within the Portfolio’s allocation to corporates, we have been focused on investments of what we believe are higher-quality issuers that have lower sensitivity to the economic cycle, and issuers that have so far been less-affected by the COVID-19 shutdowns. As we noted earlier, valuations of securitized assets have not recovered to the same degree as corporates, but we have continued to hold the Portfolio’s securitized positions, as we believe there remains a liquidity premium in the sector and we do not anticipate any meaningful impairment. As noted earlier, the Portfolio did realize some

7

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

PORTFOLIO MANAGEMENT DISCUSSION 6/30/20 | (continued) |

A Word About Risk:

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

When interest rates rise, the prices of fixed-income securities in the Portfolio will generally fall. Conversely, when interest rates fall, the prices of fixed-income securities in the Portfolio will generally rise.

Investments in the Portfolio are subject to possible loss due to the financial failure of the issuers of the underlying securities and their inability to meet their debt obligations.

Prepayment risk is the chance that an issuer may exercise its right to prepay its security, if falling interest rates prompt the issuer to do so. Forced to reinvest the unanticipated proceeds at lower interest rates, the Portfolio would experience a decline in income and lose the opportunity for additional price appreciation.

Investments in high-yield or lower-rated securities are subject to greater-than-average price volatility, illiquidity and possibility of default.

The securities issued by U.S. Government-sponsored entities (i.e., FNMA, Freddie Mac) are neither guaranteed nor issued by the U.S. Government.

The Portfolio may invest in mortgage-backed securities, which during times of fluctuating interest rates may increase or decrease more than other fixed-income securities. Mortgage-backed securities are also subject to prepayments.

At times, the Portfolio’s investments may represent industries or industry sectors that are interrelated or have common risks, making the Portfolio more susceptible to any economic, political, or regulatory developments or other risks affecting those industries and sectors.

These risks may increase share price volatility.

modest losses on some securitized positions we sold during the six-month period in order to fund purchases of new corporate issues that came to the market at historically wide spreads, which in our view offered better risk/return profiles.

Please refer to the Schedule of Investments on pages 9 to 37 for a full listing of Portfolio securities.

Past performance is no guarantee of future results.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Portfolio’s historical or future performance are statements of opinion as of the date of this report.

8

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Shares | Value | ||

| UNAFFILIATED ISSUERS – 99.1% | |||

| CONVERTIBLE PREFERRED STOCKS – 1.2% of Net Assets | |||

| Banks – 1.2% | |||

| 529(a) | Bank of America Corp., 7.25% | $ 710,024 | |

| 1,048(a) | Wells Fargo & Co., 7.5% | 1,359,256 | |

| Total Banks | $ 2,069,280 | ||

| TOTAL CONVERTIBLE PREFERRED STOCKS | |||

(Cost $2,136,481) | $ 2,069,280 |

| Principal | |||

| Amount | |||

| USD ($) | |||

| ASSET BACKED SECURITIES – 12.2% of Net Assets | |||

| 250,000(b) | 522 Funding CLO I, Ltd., Series 2019-1A, Class D, 5.749% (3 Month USD LIBOR + 420 bps), | ||

1/15/33 (144A) | $ 244,615 | ||

| 500,000 | American Credit Acceptance Receivables Trust, Series 2019-2, Class E, 4.29%, 6/12/25 (144A) | 493,871 | |

| 100,000 | Amur Equipment Finance Receivables VI LLC, Series 2018-2A, Class C, 4.27%, 1/20/23 (144A) | 103,923 | |

| 200,000 | Amur Equipment Finance Receivables VI LLC, Series 2018-2A, Class D, 4.45%, 6/20/23 (144A) | 207,761 | |

| 100,000 | Avid Automobile Receivables Trust, Series 2018-1, Class B, 3.85%, 7/15/24 (144A) | 101,213 | |

| 250,000(b) | Battalion CLO XV, Ltd., Series 2020-15A, Class D, 4.912% (3 Month USD LIBOR + 325 bps), | ||

1/17/33 (144A) | 233,419 | ||

| 100,000 | BCC Funding XIV LLC, Series 2018-1A, Class B, 3.39%, 8/21/23 (144A) | 101,555 | |

| 250,000(b) | Benefit Street Partners CLO XIX, Ltd., Series 2019-19A, Class E, 8.898% (3 Month USD | ||

LIBOR + 702 bps), 1/15/33 (144A) | 228,712 | ||

| 250,000(b) | Carlyle US CLO, Ltd., Series 2019-4A, Class C, 5.559% (3 Month USD LIBOR + 400 bps), | ||

1/15/33 (144A) | 239,878 | ||

| 400,000 | CIG Auto Receivables Trust, Series 2019-1A, Class B, 3.59%, 8/15/24 (144A) | 411,912 | |

| 160,000 | Conn’s Receivables Funding LLC, Series 2019-B, Class B, 3.62%, 6/17/24 (144A) | 153,929 | |

| 300,000 | Continental Credit Card ABS LLC, Series 2019-1A, Class A, 3.83%, 8/15/26 (144A) | 295,058 | |

| 100,000 | CoreVest American Finance Trust, Series 2017-1, Class C, 3.756%, 10/15/49 (144A) | 100,456 | |

| 298,500 | Domino’s Pizza Master Issuer LLC, Series 2019-1A, Class A2, 3.668%, 10/25/49 (144A) | 312,706 | |

| 250,000 | Drive Auto Receivables Trust, Series 2019-1, Class C, 3.78%, 4/15/25 | 253,063 | |

| 70,000 | Drive Auto Receivables Trust, Series 2020-2, Class C, 2.28%, 8/17/26 | 70,697 | |

| 50,000 | Drive Auto Receivables Trust, Series 2020-2, Class D, 3.05%, 5/15/28 | 50,707 | |

| 150,000 | Elm Trust, Series 2018-2A, Class A2, 4.605%, 10/20/27 (144A) | 149,804 | |

| 25,780(c) | Equifirst Mortgage Loan Trust, Series 2003-1, Class IF1, 4.01%, 12/25/32 | 26,339 | |

| 111,190 | FCI Funding LLC, Series 2019-1A, Class A, 3.63%, 2/18/31 (144A) | 112,045 | |

| 100,000+(d) | Finance of America Structured Securities Trust, Series 2019-HB1, Class M2, 3.676%, | ||

4/25/29 (144A) | 101,300 | ||

| 100,000+(d) | Finance of America Structured Securities Trust, Series 2019-HB1, Class M3, 3.813%, | ||

4/25/29 (144A) | 90,720 | ||

| 393,592 | Finance of America Structured Securities Trust, Series 2019-JR3, Class JR2, 2.0%, 9/25/69 | 407,362 | |

| 24,437 | First Investors Auto Owner Trust, Series 2015-2A, Class D, 4.22%, 12/15/21 (144A) | 24,471 | |

| 250,000 | Foundation Finance Trust, Series 2019-1A, Class B, 4.22%, 11/15/34 (144A) | 233,068 | |

| 250,000 | Foursight Capital Automobile Receivables Trust, Series 2019-1, Class D, 3.27%, | ||

6/16/25 (144A) | 255,093 | ||

| 220,000 | Genesis Sales Finance Master Trust, Series 2019-AA, Class A, 4.68%, 8/20/23 (144A) | 218,892 | |

| 250,000(b) | Goldentree Loan Management US CLO 6, Ltd., Series 2019-6A, Class D, 4.985% (3 Month | ||

USD LIBOR + 385 bps), 1/20/33 (144A) | 244,939 | ||

| 119,712(b) | Home Partners of America Trust, Series 2018-1, Class A, 1.094% (1 Month USD LIBOR + | ||

90 bps), 7/17/37 (144A) | 117,953 | ||

| 96,103 | Home Partners of America Trust, Series 2019-1, Class D, 3.406%, 9/17/39 (144A) | 94,914 | |

| 19,470 | Icon Brand Holdings LLC, Series 2013-1A, Class A2, 4.352%, 1/25/43 (144A) | 13,046 |

The accompanying notes are an integral part of these financial statements.

9

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| ASSET BACKED SECURITIES – (continued) | |||

| 100,000(b) | Invitation Homes Trust, Series 2018-SFR1, Class C, 1.444% (1 Month USD LIBOR + | ||

125 bps), 3/17/37 (144A) | $ 98,311 | ||

| 160,000(b) | Invitation Homes Trust, Series 2018-SFR2, Class D, 1.635% (1 Month USD LIBOR + | ||

145 bps), 6/17/37 (144A) | 154,989 | ||

| 240,000(b) | Invitation Homes Trust, Series 2018-SFR3, Class D, 1.844% (1 Month USD LIBOR + | ||

165 bps), 7/17/37 (144A) | 234,796 | ||

| 540,000(b) | Invitation Homes Trust, Series 2018-SFR3, Class E, 2.194% (1 Month USD LIBOR + | ||

200 bps), 7/17/37 (144A) | 513,331 | ||

| 19,403 | JG Wentworth XXII LLC, Series 2010-3A, Class A, 3.82%, 12/15/48 (144A) | 20,143 | |

| 241,412 | JG Wentworth XLIII LLC, Series 2019-1A, Class A, 3.82%, 8/17/71 (144A) | 266,003 | |

| 500,000 | Kabbage Funding LLC, Series 2019-1, Class B, 4.071%, 3/15/24 (144A) | 425,097 | |

| 250,000(b) | Madison Park Funding XXXVI, Ltd., Series 2019-36A, Class E, 9.192% (3 Month USD | ||

LIBOR + 725 bps), 1/15/33 (144A) | 237,998 | ||

| 4,910 | Marlette Funding Trust, Series 2018-3A, Class A, 3.2%, 9/15/28 (144A) | 4,907 | |

| 150,000 | Marlette Funding Trust, Series 2019-2A, Class C, 4.11%, 7/16/29 (144A) | 130,895 | |

| 479,277(d) | Mill City Mortgage Loan Trust, Series 2018-2, Class M1, 3.75%, 5/25/58 (144A) | 502,895 | |

| 153,189 | Mosaic Solar Loan Trust, Series 2019-2A, Class A, 2.88%, 9/20/40 (144A) | 152,318 | |

| 116,512(b) | Newtek Small Business Loan Trust, Series 2017-1, Class A, 2.185% (1 Month USD LIBOR + | ||

200 bps), 2/15/43 (144A) | 113,734 | ||

| 142,608 | NFAS LLC, Series 2019-1, Class A, 4.172%, 8/15/24 (144A) | 138,332 | |

| 300,000 | NMEF Funding LLC, Series 2019-A, Class B, 3.06%, 8/17/26 (144A) | 303,927 | |

| 43,102(b) | NovaStar Mortgage Funding Trust, Series 2005-3, Class M1, 0.86% (1 Month USD LIBOR + | ||

68 bps), 1/25/36 | 43,012 | ||

| 130,000 | Progress Residential Trust, Series 2017-SFR1, Class E, 4.261%, 8/17/34 (144A) | 132,392 | |

| 100,000 | Progress Residential Trust, Series 2017-SFR2, Class B, 3.196%, 12/17/34 (144A) | 100,770 | |

| 130,000 | Progress Residential Trust, Series 2017-SFR2, Class E, 4.142%, 12/17/34 (144A) | 131,414 | |

| 350,000 | Progress Residential Trust, Series 2018-SFR2, Class A, 3.712%, 8/17/35 (144A) | 358,748 | |

| 100,000 | Progress Residential Trust, Series 2018-SFR2, Class D, 4.338%, 8/17/35 (144A) | 102,844 | |

| 110,000 | Progress Residential Trust, Series 2018-SFR2, Class E, 4.656%, 8/17/35 (144A) | 112,683 | |

| 190,000 | Progress Residential Trust, Series 2018-SFR3, Class E, 4.873%, 10/17/35 (144A) | 195,816 | |

| 300,000 | Progress Residential Trust, Series 2019-SFR2, Class E, 4.142%, 5/17/36 (144A) | 309,286 | |

| 300,000 | Republic Finance Issuance Trust, Series 2019-A, Class A, 3.43%, 11/22/27 (144A) | 298,484 | |

| 100,000(d) | RMF Buyout Issuance Trust, Series 2019-1, Class M3, 3.011%, 7/25/29 (144A) | 97,161 | |

| 36,928 | SCF Equipment Leasing LLC, Series 2017-2A, Class A, 3.41%, 12/20/23 (144A) | 37,020 | |

| 200,000 | SCF Equipment Leasing LLC, Series 2019-1A, Class C, 3.92%, 11/20/26 (144A) | 189,263 | |

| 200,000 | SCF Equipment Leasing LLC, Series 2019-2A, Class C, 3.11%, 6/21/27 (144A) | 177,972 | |

| 200,000 | Small Business Lending Trust, Series 2019-A, Class B, 3.42%, 7/15/26 (144A) | 167,689 | |

| 250,000(b) | Sound Point CLO XXV, Ltd., Series 2019-4A, Class D, 5.941% (3 Month USD LIBOR + | ||

411 bps), 1/15/33 (144A) | 218,873 | ||

| 362,656 | SpringCastle Funding Asset-Backed Notes, Series 2019-AA, Class A, 3.2%, 5/27/36 | ||

(144A) | 366,548 | ||

| 97,417 | STORE Master Funding I LLC, Series 2015-1A, Class A1, 3.75%, 4/20/45 (144A) | 96,114 | |

| 250,000(b) | Symphony CLO XXII, Ltd., Series 2020-22A, Class C, 3.464% (3 Month USD LIBOR + | ||

215 bps), 4/18/33 (144A) | 239,850 | ||

| 250,000(d) | Towd Point Mortgage Trust, Series 2015-2, Class 1B3, 3.745%, 11/25/60 (144A) | 241,762 | |

| 104,755(d) | Towd Point Mortgage Trust, Series 2015-3, Class A1B, 3.0%, 3/25/54 (144A) | 105,545 | |

| 300,000(d) | Towd Point Mortgage Trust, Series 2015-6, Class B1, 4.022%, 4/25/55 (144A) | 316,414 | |

| 300,000(d) | Towd Point Mortgage Trust, Series 2016-1, Class B1, 4.22%, 2/25/55 (144A) | 317,906 | |

| 300,000(d) | Towd Point Mortgage Trust, Series 2016-2, Class B2, 3.525%, 8/25/55 (144A) | 302,955 |

The accompanying notes are an integral part of these financial statements.

10

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| ASSET BACKED SECURITIES – (continued) | |||

| 460,000(d) | Towd Point Mortgage Trust, Series 2016-3, Class B1, 4.128%, 4/25/56 (144A) | $ 475,999 | |

| 300,000(d) | Towd Point Mortgage Trust, Series 2016-4, Class B1, 3.979%, 7/25/56 (144A) | 305,069 | |

| 550,000(d) | Towd Point Mortgage Trust, Series 2016-4, Class M1, 3.25%, 7/25/56 (144A) | 557,955 | |

| 125,000(d) | Towd Point Mortgage Trust, Series 2016-5, Class M2, 3.375%, 10/25/56 (144A) | 124,785 | |

| 325,000(d) | Towd Point Mortgage Trust, Series 2017-2, Class M2, 3.75%, 4/25/57 (144A) | 329,735 | |

| 640,000(d) | Towd Point Mortgage Trust, Series 2017-4, Class M2, 3.25%, 6/25/57 (144A) | 652,271 | |

| 500,000(d) | Towd Point Mortgage Trust, Series 2017-6, Class M1, 3.25%, 10/25/57 (144A) | 527,719 | |

| 780,000(d) | Towd Point Mortgage Trust, Series 2018-2, Class A2, 3.5%, 3/25/58 (144A) | 819,723 | |

| 325,000(d) | Towd Point Mortgage Trust, Series 2018-3, Class M1, 3.875%, 5/25/58 (144A) | 330,453 | |

| 350,000(d) | Towd Point Mortgage Trust, Series 2018-3, Class M2, 3.875%, 5/25/58 (144A) | 339,322 | |

| 600,000(d) | Towd Point Mortgage Trust, Series 2018-5, Class A1B, 3.25%, 7/25/58 (144A) | 635,169 | |

| 100,000(d) | Towd Point Mortgage Trust, Series 2018-5, Class M1, 2.852%, 7/25/58 (144A) | 100,241 | |

| 189,768(d) | Towd Point Mortgage Trust, Series 2018-SJ1, Class A1, 4.0%, 10/25/58 (144A) | 191,479 | |

| 850,000(d) | Towd Point Mortgage Trust, Series 2019-2, Class A2, 3.75%, 12/25/58 (144A) | 917,888 | |

| 500,000(b) | Towd Point Mortgage Trust, Series 2019-HY2, Class A2, 1.585% (1 Month USD LIBOR + 140 | ||

| bps), 5/25/58 (144A) | 480,360 | ||

| 400,000(b) | Towd Point Mortgage Trust, Series 2019-HY2, Class M2, 2.085% (1 Month USD LIBOR + 190 | ||

| bps), 5/25/58 (144A) | 306,935 | ||

| 233,196(d) | Towd Point Mortgage Trust, Series 2019-HY2, Class XA, 5.0%, 5/25/58 (144A) | 233,297 | |

| 118,330(d) | Towd Point Mortgage Trust, Series 2019-MH1, Class A1, 3.0%, 11/25/58 (144A) | 120,563 | |

| 310,000 | Tricon American Homes Trust, Series 2019-SFR1, Class A, 2.75%, 3/17/38 (144A) | 322,761 | |

| 100,000 | US Auto Funding LLC, Series 2019-1A, Class B, 3.99%, 12/15/22 (144A) | 101,177 | |

| 9,415 | Welk Resorts LLC, Series 2015-AA, Class A, 2.79%, 6/16/31 (144A) | 9,380 | |

| 164,705 | Welk Resorts LLC, Series 2019-AA, Class D, 4.03%, 6/15/38 (144A) | 138,027 | |

| 122,183 | Westgate Resorts LLC, Series 2018-1A, Class C, 4.1%, 12/20/31 (144A) | 116,347 | |

| 140,000 | Westlake Automobile Receivables Trust, Series 2018-3A, Class E, 4.9%, 12/15/23 (144A) | 144,016 | |

| 49,126 | WRG Debt Funding II LLC, Series 2017-1, Class A, 4.458%, 3/15/26 (144A) | 49,556 | |

| TOTAL ASSET BACKED SECURITIES | |||

| (Cost $21,989,250) | $ 21,981,845 | ||

| COLLATERALIZED MORTGAGE OBLIGATIONS – 11.6% of Net Assets | |||

| 100,000 | American Homes 4 Rent Trust, Series 2015-SFR1, Class C, 4.11%, 4/17/52 (144A) | $ 108,966 | |

| 100,000(d) | Angel Oak Mortgage Trust I LLC, Series 2019-1, Class M1, 4.5%, 11/25/48 (144A) | 98,437 | |

| 230,000(d) | Angel Oak Mortgage Trust I LLC, Series 2019-2, Class M1, 4.065%, 3/25/49 (144A) | 229,753 | |

| 326,658(d) | Bayview Opportunity Master Fund IVa Trust, Series 2017-SPL5, Class A, 3.5%, 6/28/57 (144A) | 336,560 | |

| 182,653(b) | Bear Stearns ALT-A Trust, Series 2005-7, Class 11A1, 0.725% (1 Month USD LIBOR + | ||

| 54 bps), 8/25/35 | 181,718 | ||

| 67,206(b) | Bellemeade Re, Ltd., Series 2018-1A, Class M1B, 1.785% (1 Month USD LIBOR + 160 bps), | ||

| 4/25/28 (144A) | 66,526 | ||

| 93,772(b) | Bellemeade Re, Ltd., Series 2018-2A, Class M1B, 1.535% (1 Month USD LIBOR + 135 bps), | ||

| 8/25/28 (144A) | 93,205 | ||

| 275,589(b) | Bellemeade Re, Ltd., Series 2018-3A, Class M1B, 2.035% (1 Month USD LIBOR + 185 bps), | ||

| 10/25/28 (144A) | 272,946 | ||

| 180,000(b) | Bellemeade Re, Ltd., Series 2018-3A, Class M2, 2.935% (1 Month USD LIBOR + 275 bps), | ||

| 10/25/28 (144A) | 165,313 | ||

| 150,000(b) | Bellemeade Re, Ltd., Series 2019-1A, Class M1B, 1.935% (1 Month USD LIBOR + 175 bps), | ||

| 3/25/29 (144A) | 139,642 | ||

| 150,000(b) | Bellemeade Re, Ltd., Series 2019-1A, Class M2, 2.885% (1 Month USD LIBOR + 270 bps), | ||

| 3/25/29 (144A) | 116,646 | ||

| 450,000(d) | BRAVO Residential Funding Trust, Series 2020-RPL1, Class A2, 3.0%, 5/26/59 (144A) | 467,060 |

The accompanying notes are an integral part of these financial statements.

11

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| COLLATERALIZED MORTGAGE OBLIGATIONS – (continued) | |||

| 100,000 | Bunker Hill Loan Depositary Trust, Series 2020-1, Class A2, 2.6%, 2/25/55 (144A) | $ 99,996 | |

| 100,000 | Bunker Hill Loan Depositary Trust, Series 2020-2, Class A3, 3.253%, 2/25/55 (144A) | 100,000 | |

| 161,586(b) | Chase Mortgage Reference Notes, Series 2019-CL1, Class M1, 1.535% (1 Month USD | ||

LIBOR + 135 bps), 4/25/47 (144A) | 149,976 | ||

| 300,000(d) | CIM Trust, Series 2020-R2, Class M2, 3.0%, 10/25/59 (144A) | 288,109 | |

| 312,935(d) | Citigroup Mortgage Loan Trust, Inc., Series 2018-RP2, Class A1, 3.5%, 2/25/58 (144A) | 325,999 | |

| 762 | Colony American Finance, Ltd., Series 2015-1, Class A, 2.896%, 10/15/47 (144A) | 761 | |

| 333,006(b) | Connecticut Avenue Securities Trust, Series 2019-R01, Class 2M2, 2.635% (1 Month USD | ||

LIBOR + 245 bps), 7/25/31 (144A) | 324,868 | ||

| 127,173(b) | Connecticut Avenue Securities Trust, Series 2019-R02, Class 1M2, 2.485% (1 Month USD | ||

LIBOR + 230 bps), 8/25/31 (144A) | 125,259 | ||

| 110,581(b) | Connecticut Avenue Securities Trust, Series 2019-R03, Class 1M2, 2.335% (1 Month USD | ||

LIBOR + 215 bps), 9/25/31 (144A) | 109,195 | ||

| 350,000(b) | Connecticut Avenue Securities Trust, Series 2019-R06, Class 2M2, 2.285% (1 Month USD | ||

LIBOR + 210 bps), 9/25/39 (144A) | 339,474 | ||

| 410,000(b) | Connecticut Avenue Securities Trust, Series 2019-R07, Class 1M2, 2.285% (1 Month USD | ||

LIBOR + 210 bps), 10/25/39 (144A) | 397,422 | ||

| 120,000(b) | Connecticut Avenue Securities Trust, Series 2020-R02, Class 2M2, 2.185% (1 Month USD | ||

LIBOR + 200 bps), 1/25/40 (144A) | 113,604 | ||

| 160,000(b) | Connecticut Avenue Securities Trust, Series 2020-SBT1, Class 1M2, 3.835% (1 Month USD | ||

LIBOR + 365 bps), 2/25/40 (144A) | 149,590 | ||

| 200,000(b) | Connecticut Avenue Securities Trust, Series 2020-SBT1, Class 2M2, 3.835% (1 Month USD | ||

LIBOR + 365 bps), 2/25/40 (144A) | 192,011 | ||

| 206,094(d) | CSMC Trust, Series 2013-IVR3, Class B4, 3.435%, 5/25/43 (144A) | 202,018 | |

| 66,891(d) | Deephaven Residential Mortgage Trust, Series 2017-3A, Class A1, 2.577%, 10/25/47 (144A) | 67,549 | |

| 60,702(d) | Deephaven Residential Mortgage Trust, Series 2018-1A, Class A1, 2.976%, 12/25/57 (144A) | 61,286 | |

| 65,384(b) | Eagle Re, Ltd., Series 2018-1, Class M1, 1.885% (1 Month USD LIBOR + 170 bps), | ||

11/25/28 (144A) | 63,268 | ||

| 228,595(b) | Eagle Re, Ltd., Series 2019-1, Class M1B, 1.985% (1 Month USD LIBOR + 180 bps), | ||

4/25/29 (144A) | 226,705 | ||

| 138,882(d) | EverBank Mortgage Loan Trust, Series 2013-2, Class A, 3.0%, 6/25/43 (144A) | 145,466 | |

| 217,584(b) | Fannie Mae Connecticut Avenue Securities, Series 2016-C05, Class 2M2, 4.635% (1 Month | ||

USD LIBOR + 445 bps), 1/25/29 | 222,330 | ||

| 28,210 | Federal Home Loan Mortgage Corp. REMICS, Series 2944, Class OH, 5.5%, 3/15/35 | 33,085 | |

| 369,241(b)(e) | Federal Home Loan Mortgage Corp. REMICS, Series 4091, Class SH, 6.365% (1 Month USD | ||

LIBOR + 655 bps), 8/15/42 | 83,857 | ||

| 3,747 | Federal National Mortgage Association REMICS, Series 2009-36, Class HX, 4.5%, 6/25/29 | 3,957 | |

| 550,000 | Federal National Mortgage Association REMICS, Series 2013-61, Class BY, 3.0%, 6/25/43 | 605,912 | |

| 565,376(d) | Flagstar Mortgage Trust, Series 2020-1INV, Class A3, 3.0%, 3/25/50 (144A) | 580,991 | |

| 260,000(b) | Freddie Mac Stacr Remic Trust, Series 2020-DNA2, Class M2, 2.035% (1 Month USD | ||

LIBOR + 185 bps), 2/25/50 (144A) | 246,507 | ||

| 240,000(b) | Freddie Mac Stacr Remic Trust, Series 2020-HQA2, Class M2, 3.285% (1 Month USD | ||

LIBOR + 310 bps), 3/25/50 (144A) | 229,784 | ||

| 290,000(b) | Freddie Mac Stacr Trust, Series 2018-HQA2, Class B1, 4.435% (1 Month USD LIBOR + 425 bps), | ||

10/25/48 (144A) | 271,642 | ||

| 310,000(b) | Freddie Mac Stacr Trust, Series 2018-HQA2, Class M2, 2.485% (1 Month USD LIBOR + 230 bps), | ||

10/25/48 (144A) | 298,523 | ||

| 188,783(b) | Freddie Mac Stacr Trust, Series 2019-DNA2, Class M2, 2.635% (1 Month USD LIBOR + 245 bps), | ||

3/25/49 (144A) | 186,073 | ||

| 166,502(b) | Freddie Mac Stacr Trust, Series 2019-HQA1, Class M2, 2.535% (1 Month USD LIBOR + 235 bps), | ||

2/25/49 (144A) | 162,951 |

The accompanying notes are an integral part of these financial statements.

12

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| COLLATERALIZED MORTGAGE OBLIGATIONS – (continued) | |||

| 110,000(b) | Freddie Mac Stacr Trust, Series 2019-HQA2, Class B2, 11.435% (1 Month USD LIBOR + | ||

1,125 bps), 4/25/49 (144A) | $ 106,205 | ||

| 91,411(b) | Freddie Mac Stacr Trust, Series 2019-HQA2, Class M2, 2.235% (1 Month USD LIBOR + | ||

205 bps), 4/25/49 (144A) | 89,533 | ||

| 320,000(b) | Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2017-DNA2, Class M2, | ||

3.635% (1 Month USD LIBOR + 345 bps), 10/25/29 | 324,307 | ||

| 410,000(b) | Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2017-DNA3, Class M2, | ||

2.685% (1 Month USD LIBOR + 250 bps), 3/25/30 | 412,018 | ||

| 240,635(d) | FWDSecuritization Trust, Series 2019-INV1, Class A1, 2.81%, 6/25/49 (144A) | 246,165 | |

| 24,270 | Government National Mortgage Association, Series 2005-61, Class UZ, 5.25%, 8/16/35 | 25,618 | |

| 8,141 | Government National Mortgage Association, Series 2012-130, Class PA, 3.0%, 4/20/41 | 8,328 | |

| 1,222,795(e) | Government National Mortgage Association, Series 2019-159, Class CI, 3.5%, 12/20/49 | 138,126 | |

| 816,495(b)(e) | Government National Mortgage Association, Series 2020-9, Class SA, 3.16% (1 Month USD | ||

LIBOR + 335 bps), 1/20/50 | 78,615 | ||

| 148,932(d) | GS Mortgage-Backed Securities Corp. Trust, Series 2020-PJ2, Class B2, 3.6%, 7/25/50 (144A) | 142,017 | |

| 200,000(d) | GS Mortgage-Backed Securities Trust, Series 2019-SL1, Class A2, 2.875%, 1/25/59 (144A) | 196,139 | |

| 68,968(b) | Home Re, Ltd., Series 2019-1, Class M1, 1.835% (1 Month USD LIBOR + 165 bps), | ||

5/25/29 (144A) | 67,937 | ||

| 313,820(d) | JP Morgan Mortgage Trust, Series 2013-2, Class B2, 3.632%, 5/25/43 (144A) | 315,843 | |

| 301,512(d) | JP Morgan Mortgage Trust, Series 2018-LTV1, Class A3, 4.5%, 4/25/49 (144A) | 308,178 | |

| 395,839(d) | JP Morgan Mortgage Trust, Series 2019-9, Class B1A, 3.325%, 5/25/50 (144A) | 399,637 | |

| 345,840(d) | JP Morgan Mortgage Trust, Series 2019-HYB1, Class B1, 3.948%, 10/25/49 (144A) | 319,368 | |

| 287,941(d) | JP Morgan Mortgage Trust, Series 2019-LTV1, Class A3, 4.0%, 6/25/49 (144A) | 296,118 | |

| 347,699(d) | JP Morgan Mortgage Trust, Series 2020-2, Class B2A, 3.471%, 7/25/50 (144A) | 343,463 | |

| 248,738(d) | JP Morgan Mortgage Trust, Series 2020-3, Class B1A, 3.051%, 8/25/50 (144A) | 254,032 | |

| 86,990(b) | La Hipotecaria Panamanian Mortgage Trust, Series 2007-1GA, Class A, 4.5% (Panamanian | ||

Mortgage Reference Rate + -125 bps), 12/23/36 (144A) | 89,327 | ||

| 25,227(b) | La Hipotecaria Panamanian Mortgage Trust, Series 2010-1GA, Class A, 2.75% (Panamanian | ||

Mortgage Reference Rate + -300 bps), 9/8/39 (144A) | 25,905 | ||

| 905,635(d) | Mill City Mortgage Loan Trust, Series 2018-4, Class A1B, 3.5%, 4/25/66 (144A) | 956,644 | |

| 668,768(d) | Mill City Mortgage Loan Trust, Series 2019-1, Class M2, 3.5%, 10/25/69 (144A) | 649,715 | |

| 250,000(d) | Mill City Mortgage Loan Trust, Series 2019-GS1, Class M1, 3.0%, 7/25/59 (144A) | 252,292 | |

| 370,000(b) | Mortgage Insurance-Linked Notes, Series 2020-1, Class M1C, 1.935% (1 Month USD | ||

LIBOR + 175 bps), 2/25/30 (144A) | 320,276 | ||

| 359,069(d) | New Residential Mortgage Loan Trust, Series 2019-NQM4, Class A1, 2.492%, 9/25/59 (144A) | 361,529 | |

| 177,626(d) | New Residential Mortgage Loan Trust, Series 2019-RPL2, Class A1, 3.25%, 2/25/59 (144A) | 185,767 | |

| 219,135(d) | PMT Loan Trust, Series 2013-J1, Class A11, 3.5%, 9/25/43 (144A) | 228,479 | |

| 7,458(b) | Radnor Re, Ltd., Series 2018-1, Class M1, 1.585% (1 Month USD LIBOR + 140 bps), | ||

3/25/28 (144A) | 7,439 | ||

| 197,944(b) | Radnor Re, Ltd., Series 2019-1, Class M1B, 2.135% (1 Month USD LIBOR + 195 bps), | ||

2/25/29 (144A) | 196,097 | ||

| 230,833(d) | RMF Proprietary Issuance Trust, Series 2019-1, Class A, 2.75%, 10/25/63 (144A) | 229,582 | |

| 584,597(d) | Sequoia Mortgage Trust, Series 2013-5, Class A2, 3.0%, 5/25/43 (144A) | 607,871 | |

| 315,878(d) | Sequoia Mortgage Trust, Series 2013-6, Class A1, 2.5%, 5/25/43 | 323,388 | |

| 278,887(d) | Sequoia Mortgage Trust, Series 2013-7, Class A2, 3.0%, 6/25/43 | 289,276 | |

| 163,733(d) | Sequoia Mortgage Trust, Series 2018-CH3, Class A1, 4.5%, 8/25/48 (144A) | 171,780 | |

| 272,424(d) | Sequoia Mortgage Trust, Series 2019-CH3, Class A1, 4.0%, 9/25/49 (144A) | 280,595 | |

| 380,000(b) | STACR Trust, Series 2018-HRP2, Class B1, 4.385% (1 Month USD LIBOR + 420 bps), | ||

2/25/47 (144A) | 350,767 |

The accompanying notes are an integral part of these financial statements.

13

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| COLLATERALIZED MORTGAGE OBLIGATIONS – (continued) | |||

| 220,000(b) | STACR Trust, Series 2018-HRP2, Class M3, 2.585% (1 Month USD LIBOR + 240 bps), | ||

2/25/47 (144A) | $ 204,124 | ||

| 200,000(b) | Starwood Waypoint Homes Trust, Series 2017-1, Class B, 1.355% (1 Month USD LIBOR + | ||

117 bps), 1/17/35 (144A) | 198,331 | ||

| 320,000(d) | Towd Point Mortgage Trust, Series 2015-5, Class M1, 3.5%, 5/25/55 (144A) | 336,415 | |

| 265,000(d) | Towd Point Mortgage Trust, Series 2015-6, Class M1, 3.75%, 4/25/55 (144A) | 282,305 | |

| 52,894(d) | Towd Point Mortgage Trust, Series 2017-5, Class XA, 3.5%, 2/25/57 (144A) | 52,848 | |

| 550,000(d) | Towd Point Mortgage Trust, Series 2019-4, Class M1, 3.5%, 10/25/59 (144A) | 544,297 | |

| 430,368(d) | Visio Trust, Series 2019-2, Class A1, 2.722%, 11/25/54 (144A) | 434,770 | |

| 610,000(d) | Vista Point Securitization Trust, Series 2020-1, Class A3, 3.201%, 3/25/65 (144A) | 609,990 | |

| TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS | |||

(Cost $21,042,205) | $ 20,946,396 | ||

COMMERCIAL MORTGAGE-BACKED SECURITIES – 5.8% of Net Assets | |||

| 226,978 | A10 Term Asset Financing LLC, Series 2017-1A, Class B, 3.15%, 3/15/36 (144A) | $ 224,378 | |

| 410,000 | BANK, Series 2017-BNK7, Class AS, 3.748%, 9/15/60 | 437,242 | |

| 221,617(c)(e) | Bayview Commercial Asset Trust, Series 2007-2A, Class IO, 0.0%, 7/25/37 (144A) | — | |

| 125,000 | Benchmark Mortgage Trust, Series 2018-B5, Class A3, 3.944%, 7/15/51 | 144,975 | |

| 250,000 | Benchmark Mortgage Trust, Series 2018-B8, Class A4, 3.963%, 1/15/52 | 290,720 | |

| 265,000 | Benchmark Mortgage Trust, Series 2019-B14, Class AS, 3.352%, 12/15/62 | 287,836 | |

| 200,000(d) | Benchmark Mortgage Trust, Series 2020-IG3, Class B, 3.387%, 9/15/48 (144A) | 204,811 | |

| 200,000(b) | BX Commercial Mortgage Trust, Series 2020-BXLP, Class D, 1.435% (1 Month USD LIBOR + | ||

125 bps), 12/15/36 (144A) | 192,991 | ||

| 400,000 | BX Trust, Series 2019-OC11, Class A, 3.202%, 12/9/41 (144A) | 416,704 | |

| 100,000 | CCRESG Commercial Mortgage Trust, Series 2016-HEAT, Class A, 3.357%, 4/10/29 (144A) | 99,014 | |

| 120,000 | CD Mortgage Trust, Series 2018-CD7, Class A3, 4.013%, 8/15/51 | 138,753 | |

| 140,000 | CFCRE Commercial Mortgage Trust, Series 2016-C3, Class A2, 3.597%, 1/10/48 | 154,063 | |

| 250,000(d) | Citigroup Commercial Mortgage Trust, Series 2014-GC19, Class B, 4.805%, 3/10/47 | 263,207 | |

| 250,000(d) | Citigroup Commercial Mortgage Trust, Series 2014-GC25, Class B, 4.345%, 10/10/47 | 257,931 | |

| 125,000(d) | Citigroup Commercial Mortgage Trust, Series 2015-GC33, Class B, 4.724%, 9/10/58 | 130,658 | |

| 250,000 | Citigroup Commercial Mortgage Trust, Series 2016-P5, Class D, 3.0%, 10/10/49 (144A) | 156,142 | |

| 300,000 | Citigroup Commercial Mortgage Trust, Series 2019-SMRT, Class A, 4.149%, 1/10/36 (144A) | 322,755 | |

| 241,251 | COMM Mortgage Trust, Series 2012-CR3, Class A3, 2.822%, 10/15/45 | 245,269 | |

| 250,000 | COMM Mortgage Trust, Series 2012-CR4, Class AM, 3.251%, 10/15/45 | 254,060 | |

| 200,000(d) | COMM Mortgage Trust, Series 2013-CR11, Class C, 5.286%, 8/10/50 (144A) | 192,683 | |

| 233,783(d) | COMM Mortgage Trust, Series 2014-CR20, Class C, 4.662%, 11/10/47 | 217,134 | |

| 238,711 | COMM Mortgage Trust, Series 2014-UBS3, Class A3, 3.546%, 6/10/47 | 254,825 | |

| 150,000 | COMM Mortgage Trust, Series 2014-UBS4, Class A4, 3.42%, 8/10/47 | 159,730 | |

| 175,000(d) | COMM Mortgage Trust, Series 2015-DC1, Class B, 4.035%, 2/10/48 | 176,265 | |

| 188,302 | COMM Mortgage Trust, Series 2016-CR28, Class AHR, 3.651%, 2/10/49 | 200,781 | |

| 250,000(b) | Credit Suisse Mortgage Capital Certificates, Series 2019-ICE4, Class E, 2.335% (1 Month | ||

USD LIBOR + 215 bps), 5/15/36 (144A) | 238,737 | ||

| 300,000(d) | CSAIL Commercial Mortgage Trust, Series 2016-C5, Class C, 4.724%, 11/15/48 | 271,818 | |

| 53,849(b) | FREMF Mortgage Trust, Series 2014-KF05, Class B, 4.183% (1 Month USD LIBOR + 400 bps), | ||

9/25/22 (144A) | 53,670 | ||

| 50,100(b) | FREMF Mortgage Trust, Series 2014-KS02, Class B, 5.183% (1 Month USD LIBOR + 500 bps), | ||

8/25/23 (144A) | 44,106 | ||

| 125,000(d) | FREMF Mortgage Trust, Series 2015-K51, Class B, 4.089%, 10/25/48 (144A) | 132,850 | |

| 90,000(d) | FREMF Mortgage Trust, Series 2017-K66, Class B, 4.173%, 7/25/27 (144A) | 97,178 |

The accompanying notes are an integral part of these financial statements.

14

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| COMMERCIAL MORTGAGE-BACKED SECURITIES – (continued) | |||

| 100,000(d) | FREMF Mortgage Trust, Series 2019-K88, Class C, 4.525%, 2/25/52 (144A) | $ 103,401 | |

| 149,983(b) | FREMF Mortgage Trust, Series 2019-KF64, Class B, 2.483% (1 Month USD LIBOR + 230 | ||

bps), 6/25/26 (144A) | 142,080 | ||

| 178,455(d) | FRESB Mortgage Trust, Series 2018-SB52, Class A7F, 3.39%, 6/25/25 | 188,752 | |

| 1,387,256(d)(e) | Government National Mortgage Association, Series 2017-21, Class IO, 0.767%, 10/16/58 | 83,923 | |

| 200,000 | GS Mortgage Securities Trust, Series 2015-GC28, Class A5, 3.396%, 2/10/48 | 215,040 | |

| 323,000 | ILPT Trust, Series 2019-SURF, Class A, 4.145%, 2/11/41 (144A) | 363,250 | |

| 450,000 | JP Morgan Chase Commercial Mortgage Securities Trust, Series 2016-JP2, Class A4, | ||

2.822%, 8/15/49 | 479,070 | ||

| 200,000(d) | JP Morgan Chase Commercial Mortgage Securities Trust, Series 2018-BCON, Class C, | ||

3.881%, 1/5/31 (144A) | 199,280 | ||

| 250,000 | JP Morgan Chase Commercial Mortgage Securities Trust, Series 2018-WPT, Class AFX, | ||

4.248%, 7/5/33 (144A) | 264,912 | ||

| 150,000(d) | JPMDB Commercial Mortgage Securities Trust, Series 2016-C2, Class B, 3.99%, 6/15/49 | 147,164 | |

| 200,000 | JPMDB Commercial Mortgage Securities Trust, Series 2016-C4, Class A3, 3.141%, 12/15/49 | 217,661 | |

| 100,000(d) | JPMDB Commercial Mortgage Securities Trust, Series 2016-C4, Class D, 3.217%, | ||

12/15/49 (144A) | 60,543 | ||

| 250,000 | JPMDB Commercial Mortgage Securities Trust, Series 2018-C8, Class A4, 4.211%, 6/15/51 | 292,923 | |

| 1,600,000(d)(e) | JPMDB Commercial Mortgage Securities Trust, Series 2018-C8, Class XB, 0.193%, 6/15/51 | 15,967 | |

| 122,754 | Morgan Stanley Bank of America Merrill Lynch Trust, Series 2012-C6, Class A4, 2.858%, 11/15/45 | 126,090 | |

| 80,000(d) | Morgan Stanley Bank of America Merrill Lynch Trust, Series 2015-C21, Class C, 4.282%, 3/15/48 | 72,609 | |

| 250,000(d) | Morgan Stanley Capital I Trust, Series 2018-MP, Class A, 4.418%, 7/11/40 (144A) | 270,244 | |

| 142,173(b) | Multifamily Connecticut Avenue Securities Trust, Series 2019-01, Class M7, 1.885% | ||

(1 Month USD LIBOR + 170 bps), 10/15/49 (144A) | 131,492 | ||

| 260,000 | Wells Fargo Commercial Mortgage Trust, Series 2015-NXS3, Class A4, 3.617%, 9/15/57 | 284,139 | |

| 250,000 | Wells Fargo Commercial Mortgage Trust, Series 2016-C32, Class A3, 3.294%, 1/15/59 | 269,597 | |

| 200,000 | Wells Fargo Commercial Mortgage Trust, Series 2016-LC24, Class A3, 2.684%, 10/15/49 | 210,896 | |

| 104,974 | WFRBS Commercial Mortgage Trust, Series 2013-C16, Class A4, 4.136%, 9/15/46 | 111,731 | |

| TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES | |||

(Cost $10,452,915) | $ 10,512,050 | ||

| CORPORATE BONDS – 43.0% of Net Assets | |||

| Advertising – 0.7% | |||

| 407,000 | Interpublic Group of Cos., Inc., 4.75%, 3/30/30 | $ 479,897 | |

| 40,000 | Lamar Media Corp., 3.75%, 2/15/28 (144A) | 37,712 | |

| 25,000 | Lamar Media Corp., 4.0%, 2/15/30 (144A) | 23,930 | |

| 75,000 | Lamar Media Corp., 4.875%, 1/15/29 (144A) | 75,375 | |

| 445,000 | Omnicom Group, Inc., 2.45%, 4/30/30 | 454,044 | |

| 125,000 | Outfront Media Capital LLC/Outfront Media Capital Corp., 6.25%, 6/15/25 (144A) | 125,819 | |

| Total Advertising | $ 1,196,777 | ||

| Aerospace & Defense – 1.4% | |||

| 774,000 | Boeing Co., 3.75%, 2/1/50 | $ 694,979 | |

| 480,000 | Boeing Co., 3.9%, 5/1/49 | 441,029 | |

| 430,000 | Boeing Co., 5.805%, 5/1/50 | 507,824 | |

| 470,000 | Raytheon Technologies Corp., 3.2%, 3/15/24 (144A) | 506,425 | |

| 270,000 | United Technologies Corp., 4.125%, 11/16/28 | 318,029 | |

| Total Aerospace & Defense | $ 2,468,286 |

The accompanying notes are an integral part of these financial statements.

15

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| Agriculture – 0.8% | |||

| 80,000 | Altria Group, Inc., 4.45%, 5/6/50 | $ 87,507 | |

| 570,000 | BAT Capital Corp., 4.54%, 8/15/47 | 618,896 | |

| 170,000 | Cargill, Inc., 2.125%, 4/23/30 (144A) | 178,206 | |

| 435,000 | Philip Morris International, Inc., 3.25%, 11/10/24 | 481,556 | |

| Total Agriculture | $ 1,366,165 | ||

| Airlines – 0.2% | |||

| 244,648 | Air Canada 2017-1 Class AA Pass Through Trust, 3.3%, 1/15/30 (144A) | $ 221,815 | |

| 210,000 | Southwest Airlines Co., 2.625%, 2/10/30 | 188,150 | |

| Total Airlines | $ 409,965 | ||

| Apparel – 0.2% | |||

| 110,000 | NIKE, Inc., 3.25%, 3/27/40 | $ 123,115 | |

| 65,000 | NIKE, Inc., 3.375%, 3/27/50 | 75,136 | |

| 180,000 | Ralph Lauren Corp., 2.95%, 6/15/30 | 184,829 | |

| Total Apparel | $ 383,080 | ||

| Auto Manufacturers – 1.1% | |||

| 165,000 | BMW US Capital LLC, 4.15%, 4/9/30 (144A) | $ 189,758 | |

| 225,000 | Ford Motor Credit Co. LLC, 5.584%, 3/18/24 | 227,182 | |

| 189,000 | General Motors Co., 6.6%, 4/1/36 | 204,311 | |

| 353,000 | General Motors Financial Co., Inc., 4.0%, 1/15/25 | 369,011 | |

| 400,000 | Hyundai Capital Services, Inc., 3.0%, 8/29/22 (144A) | 408,647 | |

| 255,000 | Nissan Motor Acceptance Corp., 3.15%, 3/15/21 (144A) | 254,244 | |

| 400,000 | Volkswagen Group of America Finance LLC, 4.0%, 11/12/21 (144A) | 416,401 | |

| Total Auto Manufacturers | $ 2,069,554 | ||

| Auto Parts & Equipment – 0.2% | |||

| 297,000 | BorgWarner, Inc., 2.65%, 7/1/27 | $ 304,721 | |

| 110,000 | Lear Corp., 3.5%, 5/30/30 | 109,864 | |

| Total Auto Parts & Equipment | $ 414,585 | ||

| Banks – 7.5% | |||

| 535,000(d) | AIB Group Plc, 4.263% (3 Month USD LIBOR + 187 bps), 4/10/25 (144A) | $ 569,960 | |

| 318,000 | Banco Santander Chile, 2.7%, 1/10/25 (144A) | 326,548 | |

| 663,000(d) | Bank of America Corp., 2.884% (3 Month USD LIBOR + 119 bps), 10/22/30 | 717,273 | |

| 318,000(d) | Bank of America Corp., 4.083% (3 Month USD LIBOR + 315 bps), 3/20/51 | 398,474 | |

| 310,000(a)(d) | Bank of America Corp., 4.3% (3 Month USD LIBOR + 266 bps) | 278,194 | |

| 250,000(a)(d) | Barclays Plc, 7.75% (5 Year USD Swap Rate + 484 bps) | 254,062 | |

| 200,000(a)(d) | Barclays Plc, 8.0% (5 Year CMT Index + 567 bps) | 207,250 | |

| 200,000(a)(d) | BNP Paribas SA, 4.5% (5 Year CMT Index + 294 bps) (144A) | 175,250 | |

| 805,000(a)(d) | BNP Paribas SA, 6.625% (5 Year USD Swap Rate + 415 bps) (144A) | 821,100 | |

| 200,000 | BPCE SA, 4.875%, 4/1/26 (144A) | 226,693 | |

| 395,000(a)(d) | Citigroup, Inc., 4.7% (SOFRRATE + 323 bps) | 351,056 | |

| 90,000 | Cooperatieve Rabobank UA, 3.875%, 2/8/22 | 95,011 | |

| 250,000 | Cooperatieve Rabobank UA, 3.95%, 11/9/22 | 264,505 | |

| 574,000(a)(d) | Credit Suisse Group AG, 5.1% (5 Year CMT Index + 329 bps) (144A) | 543,865 | |

| 400,000(a)(d) | Credit Suisse Group AG, 7.125% (5 Year USD Swap Rate + 511 bps) | 412,180 | |

| 250,000 | Credit Suisse Group Funding Guernsey, Ltd., 3.8%, 9/15/22 | 265,617 | |

| 410,000 | Danske Bank AS, 5.375%, 1/12/24 (144A) | 456,257 | |

| 200,000(a)(d) | Danske Bank AS, 6.125% (USD Swap Rate + 390 bps) | 198,000 |

The accompanying notes are an integral part of these financial statements.

16

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| Banks – (continued) | |||

| 286,000(d) | Goldman Sachs Group, Inc., 3.272% (3 Month USD LIBOR + 120 bps), 9/29/25 | $ 308,216 | |

| 215,000(d) | Goldman Sachs Group, Inc., 4.223% (3 Month USD LIBOR + 130 bps), 5/1/29 | 250,150 | |

| 150,000 | HSBC Bank Plc, 7.65%, 5/1/25 | 176,754 | |

| 424,000 | Intesa Sanpaolo S.p.A., 4.7%, 9/23/49 (144A) | 463,798 | |

| 200,000(a)(d) | Intesa Sanpaolo S.p.A., 7.7% (5 Year USD Swap Rate + 546 bps) (144A) | 199,750 | |

| 626,000(a)(d) | JPMorgan Chase & Co., 4.6% (SOFRRATE + 313 bps) | 558,705 | |

| 591,000(a)(d) | JPMorgan Chase & Co., 5.0% (SOFRRATE + 338 bps) | 565,291 | |

| 400,000 | Lloyds Banking Group Plc, 4.65%, 3/24/26 | 444,853 | |

| 325,000 | Morgan Stanley, 4.1%, 5/22/23 | 351,233 | |

| 600,000 | Nordea Bank Abp, 4.25%, 9/21/22 (144A) | 636,853 | |

| 300,000 | Nordea Bank Abp, 4.875%, 5/13/21 (144A) | 310,107 | |

| 435,000(a)(d) | Royal Bank of Scotland Group Plc, 8.625% (5 Year USD Swap Rate + 760 bps) | 452,291 | |

| 400,000(a)(d) | Societe Generale SA, 7.375% (5 Year USD Swap Rate + 624 bps) (144A) | 403,480 | |

| 400,000 | Sumitomo Mitsui Financial Group, Inc., 3.202%, 9/17/29 | 433,401 | |

| 250,000 | Truist Bank, 2.25%, 3/11/30 | 252,340 | |

| 354,000(a)(d) | Truist Financial Corp., 5.1% (5 Year CMT Index + 435 bps) | 365,540 | |

| 250,000 | UBS AG, 7.625%, 8/17/22 | 278,776 | |

| 400,000(a)(d) | UBS Group AG, 7.0% (5 Year USD Swap Rate + 434 bps) (144A) | 415,500 | |

| 200,000(a)(d) | UBS Group Funding Switzerland AG, 7.125% (5 Year USD Swap Rate + 588 bps) | 203,477 | |

| Total Banks | $ 13,631,810 | ||

| Beverages – 1.1% | |||

| 1,034,000 | Anheuser-Busch InBev Worldwide, Inc., 5.55%, 1/23/49 | $ 1,378,518 | |

| 372,000 | Bacardi, Ltd., 5.3%, 5/15/48 (144A) | 459,451 | |

| 185,000 | Coca-Cola Co., 4.2%, 3/25/50 | 241,588 | |

| Total Beverages | $ 2,079,557 | ||

| Biotechnology – 0.1% | |||

| 200,000 | Biogen, Inc., 3.625%, 9/15/22 | $ 212,491 | |

| Total Biotechnology | $ 212,491 | ||

| Building Materials – 0.7% | |||

| 169,000 | Carrier Global Corp., 2.7%, 2/15/31 (144A) | $ 168,505 | |

| 174,000 | Carrier Global Corp., 2.722%, 2/15/30 (144A) | 174,756 | |

| 400,000 | CRH America, Inc., 3.875%, 5/18/25 (144A) | 441,182 | |

| 110,000 | Fortune Brands Home & Security, Inc., 4.0%, 9/21/23 | 119,997 | |

| 180,000 | Martin Marietta Materials, Inc., 2.5%, 3/15/30 | 181,189 | |

| 125,000 | Standard Industries, Inc., 4.375%, 7/15/30 (144A) | 124,688 | |

| Total Building Materials | $ 1,210,317 | ||

| Chemicals – 0.5% | |||

| 375,000 | Albemarle Wodgina Pty, Ltd., 3.45%, 11/15/29 (144A) | $ 363,107 | |

| 54,000 | CF Industries, Inc., 4.95%, 6/1/43 | 58,201 | |

| 270,000 | CF Industries, Inc., 5.375%, 3/15/44 | 291,951 | |

| 103,000 | NOVA Chemicals Corp., 5.25%, 6/1/27 (144A) | 90,421 | |

| 96,000 | Sherwin-Williams Co., 3.3%, 5/15/50 | 97,363 | |

| Total Chemicals | $ 901,043 |

The accompanying notes are an integral part of these financial statements.

17

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| Commercial Services – 1.1% | |||

| 123,000 | Allied Universal Holdco LLC/Allied Universal Finance Corp., 6.625%, 7/15/26 (144A) | $ 129,150 | |

| 460,000 | CoStar Group, Inc., 2.8%, 7/15/30 (144A) | 470,749 | |

| 200,000 | ERAC USA Finance LLC, 3.3%, 12/1/26 (144A) | 203,097 | |

| 165,000 | Garda World Security Corp., 4.625%, 2/15/27 (144A) | 162,525 | |

| 45,000 | Jaguar Holding Co. II/PPD Development LP, 4.625%, 6/15/25 (144A) | 45,796 | |

| 70,000 | Jaguar Holding Co. II/PPD Development LP, 5.0%, 6/15/28 (144A) | 71,662 | |

| 50,000 | President & Fellows of Harvard College, 2.3%, 10/1/23 | 52,582 | |

| 328,000 | Prime Security Services Borrower LLC/Prime Finance, Inc., 6.25%, 1/15/28 (144A) | 309,140 | |

| 200,000 | Sotheby’s, 7.375%, 10/15/27 (144A) | 189,000 | |

| 125,000 | United Rentals North America, Inc., 3.875%, 11/15/27 | 124,688 | |

| 205,000 | Verisk Analytics, Inc., 3.625%, 5/15/50 | 232,080 | |

| 29,000 | Verisk Analytics, Inc., 5.5%, 6/15/45 | 39,772 | |

| Total Commercial Services | $ 2,030,241 | ||

| Cosmetics/Personal Care – 0.2% | |||

| 120,000 | Edgewell Personal Care Co., 5.5%, 6/1/28 (144A) | $ 123,300 | |

| 150,000 | Estee Lauder Cos, Inc., 2.6%, 4/15/30 | 163,195 | |

| Total Cosmetics/Personal Care | $ 286,495 | ||

| Diversified Financial Services – 1.1% | |||

| 30,000 | Avolon Holdings Funding, Ltd., 3.95%, 7/1/24 (144A) | $ 26,065 | |

| 170,000 | Capital One Financial Corp., 3.3%, 10/30/24 | 182,917 | |

| 400,000 | Capital One Financial Corp., 3.75%, 4/24/24 | 433,416 | |

| 180,000 | Capital One Financial Corp., 4.25%, 4/30/25 | 202,260 | |

| 207,000(a)(d) | Charles Schwab Corp., 5.375% (5 Year CMT Index + 497 bps) | 221,142 | |

| 450,000 | GE Capital Funding LLC, 4.55%, 5/15/32 (144A) | 464,612 | |

| 70,000 | Mastercard, Inc., 3.85%, 3/26/50 | 87,080 | |

| 15,000 | Nationstar Mortgage Holdings, Inc., 6.0%, 1/15/27 (144A) | 14,250 | |

| 91,000 | Nationstar Mortgage Holdings, Inc., 9.125%, 7/15/26 (144A) | 96,175 | |

| 195,000 | Visa, Inc., 2.05%, 4/15/30 | 204,331 | |

| 70,000 | Visa, Inc., 2.7%, 4/15/40 | 74,902 | |

| Total Diversified Financial Services | $ 2,007,150 | ||

| Electric – 3.0% | |||

| 282,025 | Adani Renewable Energy RJ, Ltd./Kodangal Solar Parks Pvt, Ltd./Wardha Solar Maharash, | ||

4.625%, 10/15/39 (144A) | $ 269,334 | ||

| 55,000 | AEP Transmission Co. LLC, 3.65%, 4/1/50 | 63,589 | |

| 100,000 | AES Corp., 3.95%, 7/15/30 (144A) | 105,750 | |

| 185,000 | Berkshire Hathaway Energy Co., 4.25%, 10/15/50 (144A) | 232,968 | |

| 170,000 | Consolidated Edison Co. of New York, Inc., 3.95%, 4/1/50 | 204,633 | |

| 300,000 | Consolidated Edison Co. of New York, Inc., 4.625%, 12/1/54 | 384,153 | |

| 133,000(c) | Dominion Energy, Inc., 3.071%, 8/15/24 | 143,066 | |

| 376,000(a)(d) | Dominion Energy, Inc., 4.65% (5 Year CMT Index + 299 bps) | 368,219 | |

| 135,000 | Iberdrola International BV, 6.75%, 7/15/36 | 187,838 | |

| 200,000 | Indiana Michigan Power Co., 4.55%, 3/15/46 | 253,463 | |

| 12,539 | Kiowa Power Partners LLC, 5.737%, 3/30/21 (144A) | 12,592 | |

| 213,000 | New York State Electric & Gas Corp., 3.3%, 9/15/49 (144A) | 219,433 | |

| 430,000 | NextEra Energy Capital Holdings, Inc., 3.55%, 5/1/27 | 487,429 | |

| 83,000 | NRG Energy, Inc., 5.75%, 1/15/28 | 87,565 | |

| 240,000 | Puget Energy, Inc., 4.1%, 6/15/30 (144A) | 264,967 |

The accompanying notes are an integral part of these financial statements.

18

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| Electric – (continued) | |||

| 28,571 | San Diego Gas & Electric Co., 1.914%, 2/1/22 | $ 28,699 | |

| 335,000 | Sempra Energy, 3.4%, 2/1/28 | 366,498 | |

| 78,571 | Southern California Edison Co., 1.845%, 2/1/22 | 78,637 | |

| 239,000 | Southern California Edison Co., 3.65%, 2/1/50 | 262,291 | |

| 295,000 | Southern California Edison Co., 4.875%, 3/1/49 | 385,827 | |

| 335,000 | Southwestern Electric Power Co., 3.9%, 4/1/45 | 363,113 | |

| 470,000 | Vistra Operations Co. LLC, 3.7%, 1/30/27 (144A) | 484,020 | |

| 150,000 | Xcel Energy, Inc., 3.4%, 6/1/30 | 172,343 | |

| Total Electric | $ 5,426,427 | ||

| Electronics – 0.6% | |||

| 300,000 | Amphenol Corp., 3.125%, 9/15/21 | $ 307,337 | |

| 102,000 | Amphenol Corp., 3.2%, 4/1/24 | 109,212 | |

| 607,000 | Flex, Ltd., 4.875%, 6/15/29 | 669,873 | |

| Total Electronics | $ 1,086,422 | ||

| Energy-Alternate Sources – 0.1% | |||

| 48,620 | Alta Wind Holdings LLC, 7.0%, 6/30/35 (144A) | $ 58,833 | |

| 87,000 | TerraForm Power Operating LLC, 4.75%, 1/15/30 (144A) | 88,305 | |

| Total Energy-Alternate Sources | $ 147,138 | ||

| Environmental Control – 0.0%† | |||

| 72,000 | Covanta Holding Corp., 6.0%, 1/1/27 | $ 72,907 | |

| Total Environmental Control | $ 72,907 | ||

| Food – 0.6% | |||

| 75,000 | Albertsons Cos., Inc./Safeway, Inc./New Albertsons LP/Albertsons LLC, 4.875%, | ||

2/15/30 (144A) | $ 76,735 | ||

| 500,000 | Hershey Co., 2.65%, 6/1/50 | 507,507 | |

| 204,000 | JBS USA LUX SA/JBS USA Food Co./JBS USA Finance, Inc., 5.5%, 1/15/30 (144A) | 209,100 | |

| 150,000 | Kellogg Co., 2.1%, 6/1/30 | 151,941 | |

| 50,000 | Mondelez International, Inc., 2.75%, 4/13/30 | 53,822 | |

| 100,000 | Smithfield Foods, Inc., 2.65%, 10/3/21 (144A) | 98,896 | |

| Total Food | $ 1,098,001 | ||

| Forest Products & Paper – 0.3% | |||

| 120,000 | International Paper Co., 6.0%, 11/15/41 | $ 158,176 | |

| 234,000 | International Paper Co., 7.3%, 11/15/39 | 328,619 | |

| Total Forest Products & Paper | $ 486,795 | ||

| Gas – 0.2% | |||

| 110,000 | Boston Gas Co., 3.15%, 8/1/27 (144A) | $ 120,022 | |

| 188,223 | Nakilat, Inc., 6.267%, 12/31/33 (144A) | 222,103 | |

| Total Gas | $ 342,125 | ||

| Hand/Machine Tools – 0.1% | |||

| 96,000(d) | Stanley Black & Decker, Inc., 4.0% (5 Year CMT Index + 266 bps), 3/15/60 | $ 96,049 | |

| Total Hand/Machine Tools | $ 96,049 | ||

| Healthcare-Products – 0.8% | |||

| 141,000 | Abbott Laboratories, 3.75%, 11/30/26 | $ 164,050 | |

| 390,000 | Boston Scientific Corp., 2.65%, 6/1/30 | 406,411 |

The accompanying notes are an integral part of these financial statements.

19

| Pioneer Bond VCT Portfolio | PIONEER VARIABLE CONTRACTS TRUST |

| SCHEDULE OF INVESTMENTS 6/30/20 (UNAUDITED) | (continued) |

| Principal | |||

| Amount | |||

| USD ($) | Value | ||

| Healthcare-Products – (continued) | |||

| 425,000 | Edwards Lifesciences Corp., 4.3%, 6/15/28 | $ 506,688 | |

| 380,000 | Thermo Fisher Scientific, Inc., 3.0%, 4/15/23 | 402,669 | |

| Total Healthcare-Products | $ 1,479,818 | ||

| Healthcare-Services – 1.1% | |||

| 235,000 | Anthem, Inc., 3.125%, 5/15/50 | $ 243,103 | |

| 164,000 | Anthem, Inc., 3.65%, 12/1/27 | 186,855 | |

| 41,000 | Anthem, Inc., 4.101%, 3/1/28 | 48,048 | |

| 397,000 | Centene Corp., 3.375%, 2/15/30 | 400,855 | |

| 60,000 | Centene Corp., 4.25%, 12/15/27 | 61,915 | |

| 120,000 | Centene Corp., 4.625%, 12/15/29 | 126,600 | |

| 378,000 | HCA, Inc., 3.5%, 9/1/30 | 364,079 | |

| 176,000 | Health Care Service Corp. A Mutual Legal Reserve Co., 3.2%, 6/1/50 (144A) | 179,080 | |

| 130,000 | Humana, Inc., 3.95%, 3/15/27 | 147,395 | |

| 65,000 | LifePoint Health, Inc., 6.75%, 4/15/25 (144A) | 67,112 | |

| 35,000 | Molina Healthcare, Inc., 4.375%, 6/15/28 (144A) | 34,956 | |

| 130,000 | Tenet Healthcare Corp., 5.125%, 11/1/27 (144A) | 128,271 | |

| Total Healthcare-Services | $ 1,988,269 | ||

| Home Builders – 0.2% | |||

| 280,000 | DR Horton, Inc., 2.5%, 10/15/24 | $ 292,447 | |

| 135,000 | Meritage Homes Corp., 6.0%, 6/1/25 | 143,635 | |

| Total Home Builders | $ 436,082 | ||

| Insurance – 2.5% | |||

| 90,000 | AXA SA, 8.6%, 12/15/30 | $ 130,717 | |

| 592,000 | CNO Financial Group, Inc., 5.25%, 5/30/29 | 634,464 | |

| 100,000(d) | Farmers Exchange Capital III, 5.454% (3 Month USD LIBOR + 345 bps), 10/15/54 (144A) | 115,833 | |

| 340,000(d) | Farmers Insurance Exchange, 4.747% (3 Month USD LIBOR + 323 bps), 11/1/57 (144A) | 343,311 | |

| 175,000 | Great-West Lifeco Finance 2018 LP, 4.581%, 5/17/48 (144A) | 214,611 | |

| 645,000 | Liberty Mutual Insurance Co., 7.697%, 10/15/97 (144A) | 983,742 | |

| 500,000 | MassMutual Global Funding II, 2.75%, 6/22/24 (144A) | 534,827 | |

| 200,000 | Nationwide Financial Services, Inc., 3.9%, 11/30/49 (144A) | 199,206 | |

| 475,000 | Nationwide Mutual Insurance Co., 4.35%, 4/30/50 (144A) | 506,598 | |

| 125,000 | New York Life Insurance Co., 3.75%, 5/15/50 (144A) | 141,166 | |

| 245,000 | New York Life Insurance Co., 4.45%, 5/15/69 (144A) | 299,351 | |

| 451,000 | Prudential Financial, Inc., 3.0%, 3/10/40 | 459,399 | |