Semiannual Report

Templeton Russia and East European Fund, Inc.

Your Fund’s Goal and Main Investments: Templeton Russia and East European Fund seeks long-term capital appreciation. Under normal market conditions, the Fund invests at least 80% of its net assets in investments that are tied economically to Russia or East European countries.

Dear Shareholder:

This semiannual report for Templeton Russia and East European Fund covers the period ended September 30, 2012.

Economic and Market Overview

Russia’s gross domestic product grew 2.9% year-over-year in the third quarter, compared to 4.0% in the second quarter.1 Key reasons for the moderation included slower growth in agricultural output and commodities exports.

With higher utility and gasoline prices as well as food price increases due to a drought that started in May, the inflation rate rose from a record low of 3.6% year-over-year in April and May to 5.9% in August, leading the Central Bank of Russia to raise its benchmark interest rate 0.25 percentage points to 8.25% in September.1 After 18 years of negotiations, Russia finally joined the World Trade Organization (WTO) as its 156th member. The membership will likely have a long-term positive impact on Russia’s trade, economic and investment relations with members globally. President-elect Vladimir Putin was inaugurated on May 7 for his third term as president, after serving two terms as president from 1999 to 2008 and prime minister from 2008 to 2012. As many

1. Source: Federal State Statistics Service, Russia.

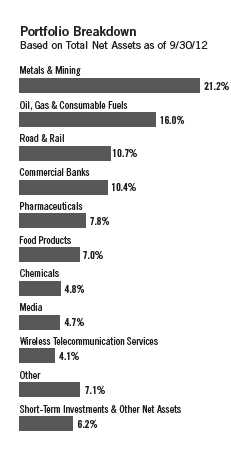

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 9.

Semiannual Report | 1

observers expected, former president Dmitry Medvedev was confirmed as the

new prime minister and chairman of the United Russia party.

Investor concerns about the eurozone debt crisis and slowing global eco-

nomic growth weighed on investor sentiment in the first two months of the

reporting period, contributing to a global stock market correction. Investor

confidence returned in subsequent months as many developed and emerging

market governments and central banks announced stimulus measures and

liquidity injections, leading emerging market stocks to partially offset earlier

losses. In this environment, Eastern European stocks, as measured by the

MSCI Emerging Markets Eastern Europe Index, had a -3.33% total return

in U.S. dollar (USD) terms for the six months ended September 30, 2012.2

Polish stocks significantly outperformed their Eastern European peers, but

Russian stocks, as measured by the MSCI Russia Index, ended the period

with a -5.93% total return in USD terms, largely due to lower oil prices and

the ruble’s depreciation.2

Investment Strategy

Our investment strategy employs a company-specific, value-oriented, long-

term approach. We focus on the market price of a company’s securities relative

to our evaluation of the company’s long-term earnings, asset value and cash

flow potential. As we look for investments, we consider specific companies in

the context of their sector and country. We perform in-depth research to con-

struct an Action List from which we construct the portfolio. Our emphasis is

on value and not attempting to match or beat an index. During our analysis,

we also consider a company’s position in its sector, the economic framework

and political environment.

Performance Overview

Templeton Russia and East European Fund had cumulative total returns of

-6.69% based on market price and -4.78% based on net asset value for the

six months ended September 30, 2012. In line with our long-term investment

strategy, we are pleased with our long-term results. For the 10-year period

ended September 30, 2012, the Fund delivered cumulative total returns of

2. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar

and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or

timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of

this information. Past performance is no guarantee of future results. The index is unmanaged and includes reinvested

dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

2 | Semiannual Report

+365.64% in market price terms and +360.60% in net asset value terms. You can find more of the Fund’s performance data in the Performance Summary on page 6.

Manager’s Discussion

During the six months under review, key contributors to the Fund’s absolute performance included Globaltrans Investment, one of Russia’s leading private freight rail transportation operators; Phosagro, a Russia-based leading global producer of phosphate-based fertilizers and phosphate rock; and Egis Pharmaceuticals, one of Hungary’s largest generic pharmaceutical companies. A key beneficiary of Russia’s economic recovery, Globaltrans reported solid financial results for the first half of 2012 and remained an attractive investment, in our view, due to its dominant market position, expansion through organic growth and strategic acquisitions as it seeks to take advantage of the liberalization of the Russian freight rail industry, and long-term earnings growth potential. Phosagro’s flexible production and sales models, which included continued production capacity increases, led the company to report stronger-than-expected earnings for the first half of 2012. The company’s purchase of an additional stake in government-owned Apatit, one of the world’s largest producers of high-quality apatite concentrate used to produce fertilizers, further supported its share price. Egis reported high gross profit margins for the second quarter of 2012 resulting from its product mix, cost efficiency and a generally weaker Hungarian forint. In our long-term view, the company’s plans to enter the biosimilars market, where it can distribute drugs highly similar to those already approved, in 2013 could further improve its sales and earnings growth potential.

In contrast, key detractors from the Fund’s absolute performance included Agroton Public, one of Ukraine’s major diversified agricultural companies; CTC Media, a leading Russian independent media company; and Nord Gold, a gold mining company with operations in Russia, West Africa and Kazakhstan. Agroton’s share price declined primarily due to a weak 2011 financial report and independent credit rating agency Standard & Poor’s May 2012 downgrade of the company’s long-term corporate and senior unsecured debt ratings to CCC+ from B-. The downgrade was in response to an independent auditor’s qualified opinion based on a lack of adequate documentation for 2011 sales transactions. We learned that the company was unable to obtain shipment documentation for exports and therefore had no evidence to support its 2011 sales receivables. However, if the company is able to collect all the receivables, we believe the reason for the auditor’s qualified opinion would be nullified. The company has sought to increase operational efficiency and improve investor sentiment. In our long-term view

Semiannual Report | 3

at period-end, we remained positive on the company due to what we considered to be its attractive valuations, expert management and favorable position as one of Ukraine’s largest diversified agricultural companies. CTC Media reported weak second-quarter 2012 financial results reflecting poor television ratings and the ruble’s depreciation. We believe the company’s stock was fundamentally undervalued and looked inexpensive compared to its peers. Its strong cash flow generation, good dividend yield, and valuations we considered attractive led us to continue to favor the company. Nord Gold’s share price was pressured by high costs, the company’s lower 2012 production guidance and weak operating results for the first half of 2012. The company had valuations we considered to be attractive, and management’s execution of 2013 growth projects could improve its growth prospects and build market sentiment, according to our analysis.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended September 30, 2012, the U.S. dollar rose in value relative to many currencies in which the Fund’s investments were traded. As a result, the Fund’s performance was negatively affected by the portfolio’s investment predominantly in securities with non-U.S. currency exposure.

During the reporting period, our continued search for companies with valuations we considered to be attractive led us to increase the Fund’s holdings in oil, gas and consumable fuels companies and pharmaceuticals companies. Key purchases included a new position in TNK-BP Holding, a Russia-based integrated oil and gas company, as well as additional investments in LUKOIL Holdings, Russia’s largest oil company; Veropharm, a Russian pharmaceutical manufacturer; and Raspadskaya, a major Russian metallurgical coal producer.

Conversely, we undertook selective sales as certain stocks reached their sale targets and as we sought to invest in companies we considered to be more attractively valued within our investment universe. Key sales included elimination of our positions in Egyptian telecommunication services companies Orascom Telecom Holding and Orascom TMT (Telecom Media and Technology) Holding, Russian vodka producer Synergy and Russian independent power producer TGC-5. We also reduced the Fund’s holdings in TMK, a manufacturer of pipes for oil and gas companies. As a result of these sales, we eliminated the Fund’s exposure to Egypt. Additionally, we eliminated the Fund’s position in beverage companies and reduced the

4 | Semiannual Report

Fund’s investments in wireless telecommunication services, independent

power producers and energy traders, and energy equipment and services

companies.

Thank you for your continued participation in Templeton Russia and East

European Fund. We look forward to serving your future investment needs.

The foregoing information reflects our analysis, opinions and portfolio holdings as of September 30, 2012, the end

of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings

may change depending on factors such as market and economic conditions. These opinions may not be relied

upon as investment advice or an offer for a particular security. The information is not a complete analysis of

every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources consid-

ered reliable, but the investment manager makes no representation or warranty as to their completeness or

accuracy. Although historical performance is no guarantee of future results, these insights may help you under-

stand our investment management philosophy.

Semiannual Report | 5

Performance Summary as of 9/30/12

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s

portfolio, adjusted for operating expenses. Capital gain distributions are net profits realized from

the sale of portfolio securities. Total return reflects reinvestment of the Fund’s dividends and capi-

tal gain distributions, if any, and any unrealized gains or losses. Total returns do not reflect any

sales charges paid at inception or brokerage commissions paid on secondary market purchases.

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends,

capital gain distributions, if any, or any realized gains on the sale of Fund shares.

Performance data represent past performance, which does not guarantee future results. Investment return and principal

value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from

figures shown.

Endnotes

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency volatil-

ity, economic instability, and social and political developments of countries where the Fund invests. Emerging markets involve heightened risks

related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Investments in Russian and East

European securities involve significant additional risks, including political and social uncertainty (for example, regional conflicts and risk of

war), currency exchange rate volatility, pervasiveness of corruption and crime in the Russian and East European economic systems, delays in

settling portfolio transactions, and risk of loss arising out of the system of share registration and custody used in Russia and East European

countries. Also, as a nondiversified investment company investing in Russia and East European countries, the Fund may invest in a relatively

small number of issuers and, as a result, be subject to greater risk of loss with respect to its portfolio securities. The Fund is actively managed

but there is no guarantee that the manager’s investment decisions will produce the desired results.

1. Total return calculations represent the cumulative and average annual changes in value of an investment over the periods indicated. Six-month

returns have not been annualized.

2. Assumes reinvestment of distributions based on net asset value.

3. Assumes reinvestment of distributions based on the dividend reinvestment and cash purchase plan.

6 | Semiannual Report

Important Notice to Shareholders

Share Repurchase Program

The Fund’s Board previously authorized management to implement an open-

market share repurchase program pursuant to which the Fund may purchase

Fund shares, from time to time, in open-market transactions, at the discretion of

management. This authorization remains in effect.

Semiannual Report | 7

Templeton Russia and East European Fund, Inc.

Financial Highlights

8 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Templeton Russia and East European Fund, Inc.

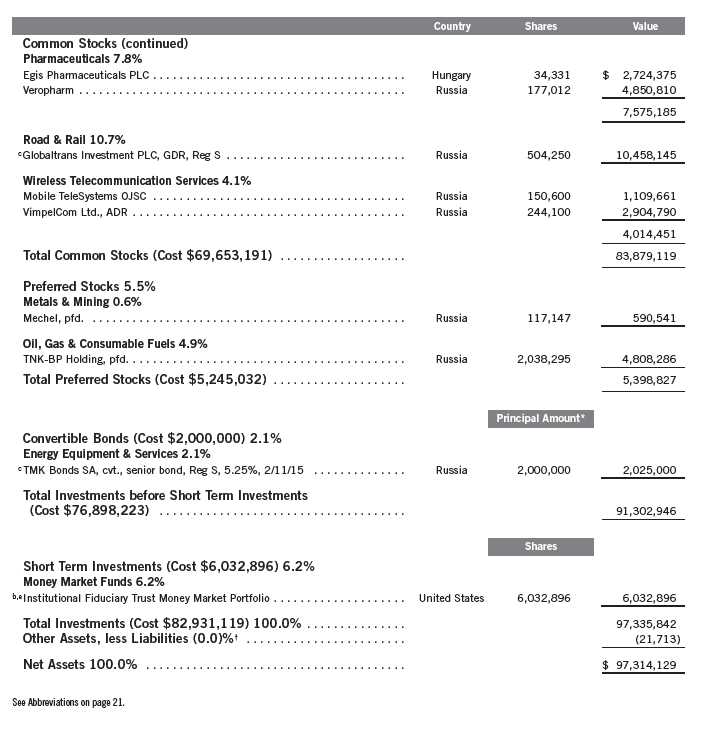

Statement of Investments, September 30, 2012 (unaudited)

Semiannual Report | 9

Templeton Russia and East European Fund, Inc.

Statement of Investments, September 30, 2012 (unaudited) (continued)

10 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Statement of Investments, September 30, 2012 (unaudited) (continued)

†Rounds to less than 0.1% of net assets.

*The principal amount is stated in U.S. dollars unless otherwise indicated.

aSecurity was purchased pursuant to Rule 144A under the Securities Act of 1933 and may be sold in transactions exempt from registration only to qualified institutional buyers or in a

public offering registered under the Securities Act of 1933. These securities have been deemed liquid under guidelines approved by the Fund’s Board of Directors. At September 30,

2012, the aggregate value of these securities was $8,522,590, representing 8.76% of net assets.

bNon-income producing.

cSecurity was purchased pursuant to Regulation S under the Securities Act of 1933, which exempts from registration securities offered and sold outside of the United States. Such a

security cannot be sold in the United States without either an effective registration statement filed pursuant to the Securities Act of 1933, or pursuant to an exemption from regis-

tration. These securities have been deemed liquid under guidelines approved by the Fund’s Board of Directors. At September 30, 2012, the aggregate value of these securities was

$18,632,969, representing 19.15% of net assets.

dAt September 30, 2012, pursuant to the Fund’s policies and the requirements of applicable securities law, the Fund may be restricted from trading these securities for a limited or

extended period of time due to ownership limits and/or potential possession of material non-public information.

eSee Note 7 regarding investments in the Institutional Fiduciary Trust Money Market Portfolio.

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 11

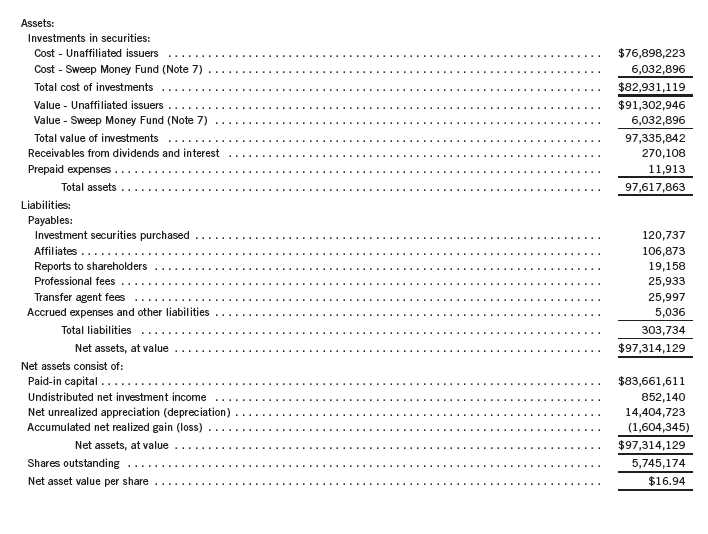

Templeton Russia and East European Fund, Inc.

Financial Statements

Statement of Assets and Liabilities

September 30, 2012 (unaudited)

12 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

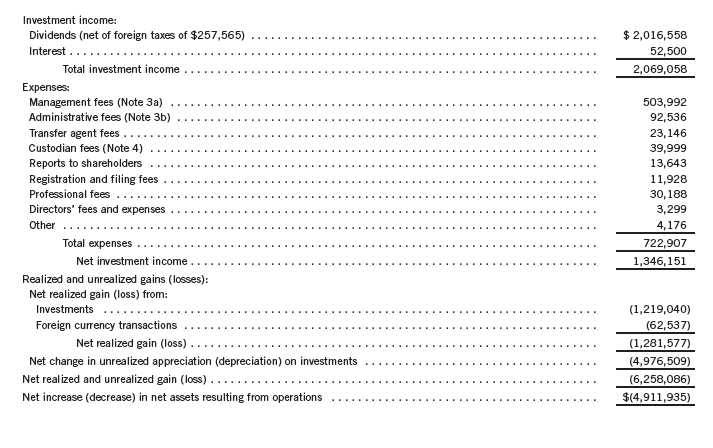

Templeton Russia and East European Fund, Inc.

Financial Statements (continued)

Statement of Operations

for the six months ended September 30, 2012 (unaudited)

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 13

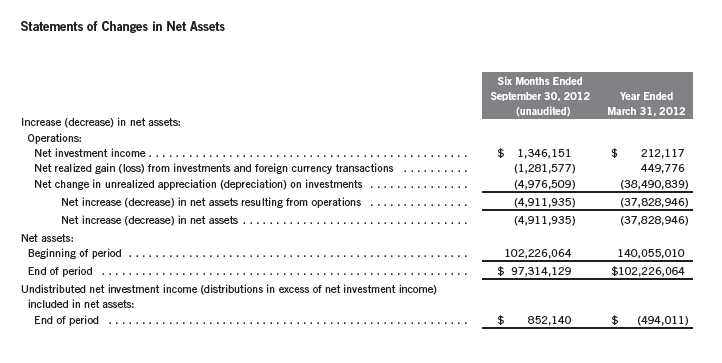

Templeton Russia and East European Fund, Inc.

Financial Statements (continued)

14 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Templeton Russia and East European Fund, Inc. (Fund) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as a closed-end investment company.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Directors (the Board), the Fund’s administrator, investment manager and other affiliates have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter (OTC) securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities. Investments in open-end mutual funds are valued at the closing net asset value.

Debt securities generally trade in the OTC market rather than on a securities exchange. The Fund’s pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services also utilize proprietary valuation models which may consider market characteristics such as benchmark yield curves, credit spreads, estimated default rates, anticipated market interest rate volatility, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair value. Securities denominated in a foreign currency are converted into their U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the date that the values of the foreign debt securities are determined.

Semiannual Report | 15

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

The Fund has procedures to determine the fair value of financial instruments for which market prices are not reliable or readily available. Under these procedures, the VLOC convenes on a regular basis to review such financial instruments and considers a number of factors, including significant unobservable valuation inputs, when arriving at fair value. The VLOC primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. An income-based valuation approach may also be used in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. The VLOC employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis, and reviews of any related market activity.

Trading in securities on foreign securities stock exchanges and OTC markets may be completed before the daily close of business on the NYSE. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Fund. As a result, differences may arise between the value of the Fund’s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the VLOC monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depositary Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for each specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Fund. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

b. Foreign Currency Translation

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Fund may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Portfolio securities and assets and liabilities denominated in foreign currencies contain risks that those currencies will decline in value relative to the U.S. dollar. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by the Board.

16 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| b. | Foreign Currency Translation (continued) |

The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments on the Statement of Operations.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

c. Income and Deferred Taxes

It is the Fund’s policy to qualify as a regulated investment company under the Internal Revenue Code. The Fund intends to distribute to shareholders substantially all of its taxable income and net realized gains to relieve it from federal income and excise taxes. As a result, no provision for U.S. federal income taxes is required.

The Fund may be subject to foreign taxation related to income received, capital gains on the sale of securities and certain foreign currency transactions in the foreign jurisdictions in which it invests. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests. When a capital gain tax is determined to apply the Fund records an estimated deferred tax liability in an amount that would be payable if the securities were disposed of on the valuation date.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is “more likely than not” to be sustained upon examination by the tax authorities based on the technical merits of the tax position. As of September 30, 2012, and for all open tax years, the Fund has determined that no liability for unrecognized tax benefits is required in the Fund’s financial statements related to uncertain tax positions taken on a tax return (or expected to be taken on future tax returns). Open tax years are those that remain subject to examination and are based on each tax jurisdiction statute of limitation.

d. Security Transactions, Investment Income, Expenses and Distributions

Security transactions are accounted for on trade date. Realized gains and losses on security transactions are determined on a specific identification basis. Interest income and estimated expenses are accrued daily. Amortization of premium and accretion of discount on debt securities are included in interest income. Dividend income is recorded on the ex-dividend date except that certain dividends from foreign securities are recognized as soon as the Fund is notified of the ex-dividend date. Distributions to shareholders are recorded on the ex-dividend date and are determined according to income tax regulations (tax basis). Distributable earnings determined

Semiannual Report | 17

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| d. | Security Transactions, Investment Income, Expenses and Distributions (continued) |

on a tax basis may differ from earnings recorded in accordance with accounting principles generally accepted in the United States of America. These differences may be permanent or temporary. Permanent differences are reclassified among capital accounts to reflect their tax character. These reclassifications have no impact on net assets or the results of operations. Temporary differences are not reclassified, as they may reverse in subsequent periods.

e. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

f. Guarantees and Indemnifications

Under the Fund’s organizational documents, its officers and directors are indemnified by the Fund against certain liabilities arising out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. Currently, the Fund expects the risk of loss to be remote.

2. CAPITAL STOCK

At September 30, 2012, there were 100 million shares authorized ($0.01 par value). During the year ended March 31, 2012 and the period ended September 30, 2012, there were no shares issued; all reinvested distributions were satisfied with previously issued shares purchased in the open market.

The Board previously authorized an open-market share repurchase program pursuant to which the Fund may purchase, from time to time, Fund shares in open-market transactions, at the discretion of management. This authorization remains in effect. During the year ended March 31, 2012 and the period ended September 30, 2012, there were no shares repurchased.

18 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

3. TRANSACTIONS WITH AFFILIATES

Franklin Resources, Inc. is the holding company for various subsidiaries that together are referred

to as Franklin Templeton Investments. Certain officers and directors of the Fund are also officers

and/or directors of the following subsidiaries:

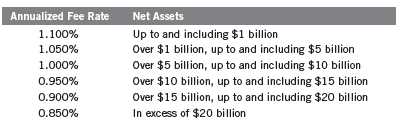

a. Management Fees

The Fund pays an investment management fee to TAML based on the average weekly net assets

of the Fund as follows:

b. Administrative Fees

The Fund pays an administrative fee to FT Services of 0.20% per year of the average weekly net

assets of the Fund.

4. EXPENSE OFFSET ARRANGEMENT

The Fund has entered into an arrangement with its custodian whereby credits realized as a result

of uninvested cash balances are used to reduce a portion of the Fund’s custodian expenses.

During the period ended September 30, 2012, there were no credits earned.

5. INCOME TAXES

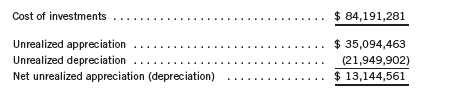

At September 30, 2012, the cost of investments and net unrealized appreciation (depreciation)

for income tax purposes were as follows:

Differences between income and/or capital gains as determined on a book basis and a tax basis

are primarily due to differing treatments of passive foreign investments company shares and

corporate actions.

Semiannual Report | 19

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

6. INVESTMENT TRANSACTIONS

Purchases and sales of investments (excluding short term securities) for the period ended September 30, 2012, aggregated $6,498,180 and $4,343,376, respectively.

7. INVESTMENTS IN INSTITUTIONAL FIDUCIARY TRUST MONEY MARKET PORTFOLIO

The Fund invests in the Institutional Fiduciary Trust Money Market Portfolio (Sweep Money Fund), an open-end investment company managed by Franklin Advisers, Inc. (an affiliate of the investment manager). Management fees paid by the Fund are reduced on assets invested in the Sweep Money Fund, in an amount not to exceed the management and administrative fees paid by the Sweep Money Fund.

8. CONCENTRATION OF RISK

Investing in equity securities of Russian companies may include certain risks not typically associated with investing in countries with more developed securities markets, such as political, economic and legal uncertainties, delays in settling portfolio transactions and the risk of loss from Russia’s underdeveloped systems of securities registration and transfer. At September 30, 2012, the Fund had 83.1% of its net assets invested in Russia.

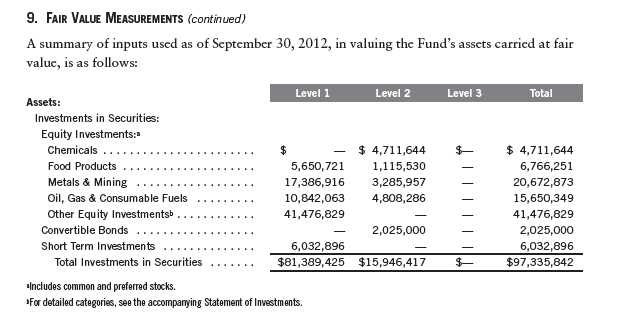

9. FAIR VALUE MEASUREMENTS

The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund’s financial instruments and are summarized in the following fair value hierarchy:

- Level 1 – quoted prices in active markets for identical financial instruments

- Level 2 – other significant observable inputs (including quoted prices for similar financial instruments, interest rates, prepayment speed, credit risk, etc.)

- Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of financial instruments)

The inputs or methodology used for valuing financial instruments are not an indication of the risk associated with investing in those financial instruments.

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

20 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Notes to Financial Statements (unaudited) (continued)

10. NEW ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board issued Accounting Standards

Update (ASU) No. 2011-11, Balance Sheet (Topic 210): Disclosures about Offsetting Assets and

Liabilities. The amendments in the ASU enhance disclosures about offsetting of financial assets

and liabilities to enable investors to understand the effect of these arrangements on a fund’s

financial position. The ASU is effective for interim and annual reporting periods beginning on or

after January 1, 2013. The Fund believes the adoption of this ASU will not have a material

impact on its financial statements.

11. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the issuance of the financial statements and

determined that no events have occurred that require disclosure.

ABBREVIATIONS

Selected Portfolio

ADR - American Depositary Receipt

GDR - Global Depositary Receipt

Semiannual Report | 21

Templeton Russia and East European Fund, Inc.

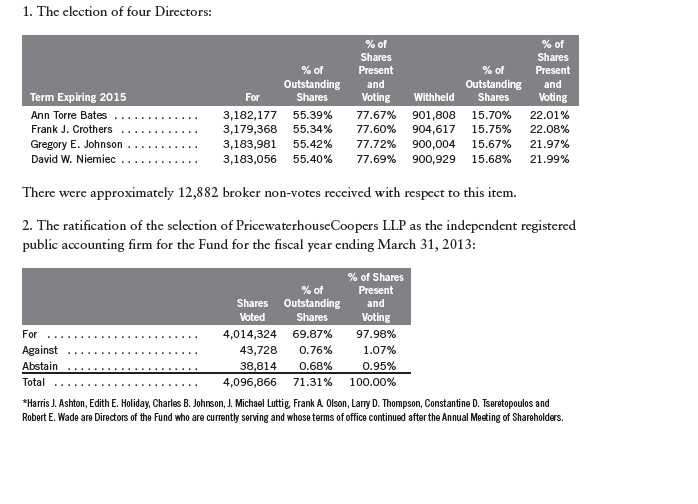

Annual Meeting of Shareholders, August 24, 2012 (unaudited)

The Annual Meeting of Shareholders of the Fund was held at the Fund’s offices, 300 S.E. 2nd

Street, Fort Lauderdale, Florida, on August 24, 2012. The purpose of the meeting was to elect

four Directors of the Fund and to ratify the selection of PricewaterhouseCoopers LLP as the

independent registered public accounting firm for the Fund for the fiscal year ending March 31,

2013. At the meeting, the following persons were elected by the shareholders to serve as

Directors of the Fund: Ann Torre Bates, Frank J. Crothers, Gregory E. Johnson and David W.

Niemiec.* Shareholders also ratified the selection of PricewaterhouseCoopers LLP as the inde-

pendent registered public accounting firm for the Fund for the fiscal year ending March 31,

2013. No other business was transacted at the meeting.

The results of the voting at the Annual Meeting are as follows:

22 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Dividend Reinvestment and Cash Purchase Plan

The Fund offers a Dividend Reinvestment and Cash Purchase Plan (the “Plan”) with the following features:

If shares of the Fund are held in the shareholder’s name, the shareholder will automatically be a participant in the Plan unless he elects to withdraw. If the shares are registered in the name of a broker-dealer or other nominee (i.e., in “street name”), the broker-dealer or nominee will elect to participate in the Plan on the shareholder’s behalf unless the shareholder instructs them otherwise, or unless the reinvestment service is not provided by the broker-dealer or nominee.

Participants should contact Computershare Shareowner Services, LLC, P.O. Box 358015, Pittsburgh, PA 15252-8015, to receive the Plan brochure.

To receive dividends or distributions in cash, the shareholder must notify Computershare Trust Company, N.A. (formerly, The Bank of New York Mellon) (the “Plan Administrator”) at the address above or the institution in whose name the shares are held. The Plan Administrator must receive written notice ten business days before the record date for the distribution.

Whenever the Fund declares dividends in either cash or common stock of the Fund, if the market price is equal to or exceeds net asset value at the valuation date, the participant will receive the dividends entirely in new shares at a price equal to the net asset value, but not less than 95% of the then current market price of the Fund’s shares. If the market price is lower than net asset value or if dividends and/or capital gains distributions are payable only in cash, the participant will receive shares purchased on the New York Stock Exchange or otherwise on the open market.

A participant has the option of submitting additional cash payments to the Plan Administrator, in any amounts of at least $100 each, up to a maximum of $5,000 per month, for the purchase of Fund shares for his or her account. These payments can be made by check payable to Computershare Trust Company, N.A. (formerly, The Bank of New York Mellon) and sent to Computershare Shareowner Services, LLC, P.O. Box 382009, Pittsburgh, PA 15252-8009, Attention: Templeton Russia and East European Fund, Inc. The Plan Administrator will apply such payments (less a $5.00 service charge and less a pro rata share of trading fees) to purchases of Fund shares on the open market.

The automatic reinvestment of dividends and/or capital gains does not relieve the participant of any income tax that may be payable on dividends or distributions.

Whenever shares are purchased on the New York Stock Exchange or otherwise on the open market, each participant will pay a pro rata portion of trading fees. Trading fees will be deducted from amounts to be invested. The Plan Administrator’s fee for a sale of shares through the Plan is $15.00 per transaction plus a $0.12 per share trading fee.

Semiannual Report | 23

Templeton Russia and East European Fund, Inc.

Dividend Reinvestment and Cash Purchase Plan (continued)

The participant may withdraw from the Plan without penalty at any time by written notice to the Plan Administrator sent to Computershare Shareowner Services, LLC, P.O. Box 358015, Pittsburgh, PA 15252-8015. Upon withdrawal, the participant will receive, without charge, share certificates issued in the participant’s name for all full shares held by the Plan Administrator; or, if the participant wishes, the Plan Administrator will sell the participant’s shares and send the proceeds to the participant, less a service charge of $15.00 and less trading fees of $0.12 per share. The Plan Administrator will convert any fractional shares held at the time of withdrawal to cash at current market price and send a check to the participant for the net proceeds.

Direct Deposit Service for Registered Shareholders

Cash distributions can now be electronically credited to a checking or savings account at any financial institution that participates in the Automated Clearing House (“ACH”) system. The Direct Deposit service is provided for registered shareholders at no charge. To enroll in the service, access your account online by going to www.cpushareownerservices.com or dial (800) 416-5585 (toll free) and follow the instructions. Direct Deposit will begin with the next scheduled distribution payment date following enrollment in the service.

24 | Semiannual Report

Templeton Russia and East European Fund, Inc.

Transfer Agent

Computershare Shareowner Services, LLC

P.O. Box 358015

Pittsburgh, PA 15252-8015

(800) 416-5585

www.cpushareownerservices.com

Direct Registration

If you are a registered shareholder of the Fund, purchases of shares of the Fund can be electronically credited to your Fund account at Computershare Shareowner Services, LLC through Direct Registration. This service provides shareholders with a convenient way to keep track of shares through book entry transactions, electronically move book-entry shares between broker-dealers, transfer agents and DRS eligible issuers, and eliminate the possibility of lost certificates. For additional information, please contact Computershare Shareowner Services, LLC at (800) 416-5585.

Shareholder Information

Shares of Templeton Russia and East European Fund, Inc. are traded on the New York Stock Exchange under the symbol “TRF.” Information about the net asset value and the market price is published each Monday in the Wall Street Journal, weekly in Barron’s and each Saturday in The New York Times and other newspapers. Daily market prices for the Fund’s shares are published in “New York Stock Exchange Composite Transactions” section of newspapers.

For current information about distributions and shareholder accounts, call (800) 416-5585. Registered shareholders can now access their Fund account on-line with the Investor ServiceDirect™ website. For information go to Computershare Shareowner Services, LLC’s web site at www.cpushareownerservices.com and follow the instructions.

The daily closing net asset value as of the previous business day may be obtained when available by calling Franklin Templeton Fund Information after 7 a.m. Pacific time any business day at (800) DIAL BEN®/342-5236. The Fund’s net asset value and dividends are also listed on the NASDAQ Stock Market, Inc.’s Mutual Fund Quotation Service (“NASDAQ MFQS”).

Shareholders not receiving copies of the reports to shareholders because their shares are registered in the name of a broker or a custodian can request that they be added to the Fund’s mailing list by writing Templeton Russia and East European Fund, Inc., 100 Fountain Parkway, P.O. Box 33030, St. Petersburg, FL 33733-8030.

Semiannual Report | 25

Templeton Russia and East European Fund, Inc.

Shareholder Information

Proxy Voting Policies and Procedures

The Fund’s investment manager has established Proxy Voting Policies and Procedures (Policies) that the Fund uses to determine how to vote proxies relating to portfolio securities. Shareholders may view the Fund’s complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301, Attention: Proxy Group. Copies of the Fund’s proxy voting records are also made available online at franklintempleton.com and posted on the U.S. Securities and Exchange Commission’s website at sec.gov and reflect the most recent 12-month period ended June 30.

Quarterly Statement of Investments

The Fund files a complete statement of investments with the U.S. Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission’s website at sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling (800) SEC-0330.

Certifications

The Fund’s Chief Executive Officer – Finance and Administration is required by the New York Stock Exchange’s Listing Standards to file annually with the Exchange a certification that she is not aware of any violation by the Fund of the Exchange’s Corporate Governance Standards applicable to the Fund. The Fund has filed such certification.

In addition, the Fund’s Chief Executive Officer – Finance and Administration and Chief Financial Officer and Chief Accounting Officer are required by the rules of the U.S. Securities and Exchange Commission to provide certain certifications with respect to the Fund’s Form N-CSR and Form N-CSRS (which include the Fund’s annual and semiannual reports to shareholders) that are filed semiannually with the Commission. The Fund has filed such certifications with its Form N-CSR for the 12 months ended March 31, 2012. Additionally, the Fund expects to file, on or about November 30, 2012, such certifications with its Form N-CSRS for the six months ended September 30, 2012.

26 | Semiannual Report

This page intentionally left blank.

This page intentionally left blank.

Item 2. Code of Ethics.

(a) The Registrant has adopted a code of ethics that applies to its principal

executive officers and principal financial and accounting officer.

(c) N/A

(d) N/A

(f) Pursuant to Item 12(a)(1), the Registrant is attaching as an exhibit a copy

of its code of ethics that applies to its principal executive officers and

principal financial and accounting officer.

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant has an audit committee financial expert serving on its

audit committee.

(2) The audit committee financial expert is David W. Niemiec and he is

"independent" as defined under the relevant Securities and Exchange Commission

Rules and Releases.

Item 4. Principal Accountant Fees and Services. N/A

Item 5. Audit Committee of Listed Registrants.

Members of the Audit Committee are: Ann Torre Bates, Frank J. Crothers, David

W. Niemiec and Constantine D. Tseretopoulos.

Item 6. Schedule of Investments. N/A

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End

Management Investment Companies.

The board of directors of the Fund has delegated the authority to vote proxies

related to the portfolio securities held by the Fund to the Fund’s investment

manager Templeton Asset Management Ltd. in accordance with the Proxy Voting

Policies and Procedures (Policies) adopted by the investment manager.

The investment manager has delegated its administrative duties with respect to

the voting of proxies to the Proxy Group within Franklin Templeton Companies,

LLC (Proxy Group), an affiliate and wholly owned subsidiary of Franklin

Resources, Inc. All proxies received by the Proxy Group will be voted based

upon the investment manager’s instructions and/or policies. The investment

manager votes proxies solely in the interests of the Fund and its shareholders.

To assist it in analyzing proxies, the investment manager subscribes to

Institutional Shareholder Services, Inc. (ISS), an unaffiliated third-party

corporate governance research service that provides in-depth analyses of

shareholder meeting agendas, vote recommendations, recordkeeping and vote

disclosure services. In addition, the investment manager subscribes to Glass,

Lewis & Co., LLC (Glass Lewis), an unaffiliated third-party analytical research

firm, to receive analyses and vote recommendations on the shareholder meetings

of publicly held U.S. companies, as well as a limited subscription to its

international research. Although ISS’ and/or Glass Lewis’ analyses are

thoroughly reviewed and considered in making a final voting decision, the investment manager does not consider recommendations from ISS, Glass Lewis or any other third party to be determinative of the investment manager’s ultimate decision. As a matter of policy, the officers, directors/trustees and employees of the investment manager and the Proxy Group will not be influenced by outside sources whose interests conflict with the interests of the Fund and its shareholders. Efforts are made to resolve all conflicts in the interests of the investment manager’s clients. Material conflicts of interest are identified by the Proxy Group based upon analyses of client, distributor, broker-dealer and vendor lists, information periodically gathered from directors and officers, and information derived from other sources, including public filings. In situations where a material conflict of interest is identified, the Proxy Group may defer to the voting recommendation of ISS, Glass Lewis or those of another independent third-party provider of proxy services; or send the proxy directly to the Fund's board or a committee of the board with the investment manager's recommendation regarding the vote for approval.

Where a material conflict of interest has been identified, but the items on which the investment manager’s vote recommendations differ from Glass Lewis, ISS, or another independent third-party provider of proxy services relate specifically to (1) shareholder proposals regarding social or environmental issues, (2) “Other Business” without describing the matters that might be considered, or (3) items the investment manager wishes to vote in opposition to the recommendations of an issuer’s management, the Proxy Group may defer to the vote recommendations of the investment manager rather than sending the proxy directly to the Fund's board or a board committee for approval.

To avoid certain potential conflicts of interest, the investment manager will employ echo voting, if possible, in the following instances: (1) when the Fund invests in an underlying fund in reliance on any one of Sections 12(d) (1) (E), (F), or (G) of the 1940 Act, the rules thereunder, or pursuant to a U.S. SEC exemptive order thereunder; (2) when the Fund invests uninvested cash in affiliated money market funds pursuant to the rules under the 1940 Act or any exemptive orders thereunder (“cash sweep arrangement”); or (3) when required pursuant to the Fund’s governing documents or applicable law. Echo voting means that the investment manager will vote the shares in the same proportion as the vote of all of the other holders of the Fund’s shares.

The recommendation of management on any issue is a factor that the investment manager considers in determining how proxies should be voted. However, the investment manager does not consider recommendations from management to be determinative of the investment manager’s ultimate decision. As a matter of practice, the votes with respect to most issues are cast in accordance with the position of the company's management. Each issue, however, is considered on its own merits, and the investment manager will not support the position of the company's management in any situation where it deems that the ratification of management’s position would adversely affect the investment merits of owning that company’s shares.

Investment manager’s proxy voting policies and principles The investment manager has adopted general proxy voting guidelines, which are summarized below. These guidelines are not an exhaustive list of all the issues that may arise and the investment manager cannot anticipate all future situations. In all cases, each proxy will be considered based on the relevant facts and circumstances.

Board of directors. The investment manager supports an independent board of directors, and prefers that key committees such as audit, nominating, and compensation committees be comprised of independent directors. The investment manager will generally vote against management efforts to classify a board and will generally support proposals to declassify the board of directors. The investment manager will consider withholding votes from directors who have attended less than 75% of meetings without a valid reason. While generally in favor of separating Chairman and CEO positions, the investment manager will review this issue as well as proposals to restore or provide for cumulative voting on a case-by-case basis, taking into consideration factors such as the company’s corporate governance guidelines or provisions and performance. The investment manager generally will support non-binding shareholder proposals to require a majority vote standard for the election of directors; however, if these proposals are binding, the investment manager will give careful review on a case-by-case basis of the potential ramifications of such implementation.

Ratification of auditors of portfolio companies. The investment manager will closely scrutinize the independence, role and performance of auditors. On a case-by-case basis, the investment manager will examine proposals relating to non-audit relationships and non-audit fees. The investment manager will also consider, on a case-by-case basis, proposals to rotate auditors, and will vote against the ratification of auditors when there is clear and compelling evidence of a lack of independence, accounting irregularities or negligence.

Management and director compensation. A company’s equity-based compensation plan should be in alignment with the shareholders’ long-term interests. The investment manager believes that executive compensation should be directly linked to the performance of the company. The investment manager evaluates plans on a case-by-case basis by considering several factors to determine whether the plan is fair and reasonable, including the ISS quantitative model utilized to assess such plans and/or the Glass Lewis evaluation of the plans. The investment manager will generally oppose plans that have the potential to be excessively dilutive, and will almost always oppose plans that are structured to allow the repricing of underwater options, or plans that have an automatic share replenishment “evergreen” feature. The investment manager will generally support employee stock option plans in which the purchase price is at least 85% of fair market value, and when potential dilution is 10% or less.

Severance compensation arrangements will be reviewed on a case-by-case basis, although the investment manager will generally oppose “golden parachutes” that are considered to be excessive. The investment manager will normally support proposals that require a percentage of directors’ compensation to be in the form of common stock, as it aligns their interests with those of shareholders.

The investment manager will review non-binding say-on-pay proposals on a case-by-case basis, and will generally vote in favor of such proposals unless compensation is misaligned with performance and/or shareholders’ interests, the company has not provided reasonably clear disclosure regarding its compensation practices, or there are concerns with the company’s remuneration practices.

Anti-takeover mechanisms and related issues. The investment manager generally opposes anti-takeover measures since they tend to reduce shareholder rights. However, as with all proxy issues, the investment manager conducts an independent review of each anti-takeover proposal. On occasion, the investment manager may vote with management when the research analyst has concluded that the proposal is not onerous and would not harm the Fund or its shareholders’ interests. The investment manager generally supports proposals that require shareholder rights’ plans (“poison pills”) to be subject to a shareholder vote

and will closely evaluate such plans on a case-by-case basis to determine whether or not they warrant support. In addition, the investment manager will generally vote against any proposal to issue stock that has unequal or subordinate voting rights. The investment manager generally opposes any supermajority voting requirements as well as the payment of “greenmail.” The investment manager generally supports “fair price” provisions and confidential voting.

Changes to capital structure. The investment manager realizes that a company's financing decisions have a significant impact on its shareholders, particularly when they involve the issuance of additional shares of common or preferred stock or the assumption of additional debt. The investment manager will review, on a case-by-case basis, proposals by companies to increase authorized shares and the purpose for the increase. The investment manager will generally not vote in favor of dual-class capital structures to increase the number of authorized shares where that class of stock would have superior voting rights. The investment manager will generally vote in favor of the issuance of preferred stock in cases where the company specifies the voting, dividend, conversion and other rights of such stock and the terms of the preferred stock issuance are deemed reasonable. The investment manager will review proposals seeking preemptive rights on a case-by-case basis.

Mergers and corporate restructuring. Mergers and acquisitions will be subject to careful review by the research analyst to determine whether they would be beneficial to shareholders. The investment manager will analyze various economic and strategic factors in making the final decision on a merger or acquisition. Corporate restructuring proposals are also subject to a thorough examination on a case-by-case basis.

Environment, social and governance issues. The investment manager will generally give management discretion with regard to social, environmental and ethical issues, although the investment manager may vote in favor of those that are believed to have significant economic benefits or implications for the Fund and its shareholders. The investment manager generally supports the right of shareholders to call special meetings and act by written consent. However, the investment manager will review such shareholder proposals on a case-by-case basis in an effort to ensure that such proposals do not disrupt the course of business or waste company resources for the benefit of a small minority of shareholders.

Global corporate governance. Many of the tenets discussed above are applied to the investment manager's proxy voting decisions for international investments. However, the investment manager must be flexible in these worldwide markets. Principles of good corporate governance may vary by country, given the constraints of a country’s laws and acceptable practices in the markets. As a result, it is on occasion difficult to apply a consistent set of governance practices to all issuers. As experienced money managers, the investment manager's analysts are skilled in understanding the complexities of the regions in which they specialize and are trained to analyze proxy issues germane to their regions.

The investment manager will generally attempt to process every proxy it receives for all domestic and foreign securities. However, there may be situations in which the investment manager may be unable to vote a proxy, or may choose not to vote a proxy, such as where: (i) the proxy ballot was not received from the custodian bank; (ii) a meeting notice was received too late; (iii) there are fees imposed upon the exercise of a vote and it is determined

that such fees outweigh the benefit of voting; (iv) there are legal encumbrances to voting, including blocking restrictions in certain markets that preclude the ability to dispose of a security if the investment manager votes a proxy or where the investment manager is prohibited from voting by applicable law or other regulatory or market requirements, including but not limited to, effective Powers of Attorney; (v) the investment manager held shares on the record date but has sold them prior to the meeting date; (vi) proxy voting service is not offered by the custodian in the market; (vii) the investment manager believes it is not in the best interest of the Fund or its shareholders to vote the proxy for any other reason not enumerated herein; or (viii) a security is subject to a securities lending or similar program that has transferred legal title to the security to another person. The investment manager or its affiliates may, on behalf of one or more of the proprietary registered investment companies advised by the investment manager or its affiliates, determine to use its best efforts to recall any security on loan where the investment manager or its affiliates (a) learn of a vote on a material event that may affect a security on loan and (b) determine that it is in the best interests of such proprietary registered investment companies to recall the security for voting purposes.

Shareholders may view the complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923, Attention: Proxy Group. Copies of the Fund’s proxy voting records are available online at franklintempleton.com and posted on the SEC website at www.sec.gov. The proxy voting records are updated each year by August 31 to reflect the most recent 12-month period ended June 30.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

N/A

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers. N/A

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no changes to the procedures by which shareholders may recommend nominees to the Registrant's Board of Directors that would require disclosure herein.

Item 11. Controls and Procedures.

(a) Evaluation of Disclosure Controls and Procedures. The Registrant maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in the Registrant’s filings under the Securities Exchange Act of 1934 and the Investment Company Act of 1940 is recorded, processed, summarized and reported within the periods specified in the rules and forms of the Securities and Exchange Commission. Such information is accumulated and communicated to the Registrant’s management, including its principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure. The Registrant’s management, including the principal executive officer and the principal financial officer, recognizes that any set of controls and

procedures, no matter how well designed and operated, can provide only

reasonable assurance of achieving the desired control objectives.

Within 90 days prior to the filing date of this Shareholder Report on Form N-

CSR, the Registrant had carried out an evaluation, under the supervision and

with the participation of the Registrant’s management, including the

Registrant’s principal executive officer and the Registrant’s principal

financial officer, of the effectiveness of the design and operation of the

Registrant’s disclosure controls and procedures. Based on such evaluation, the

Registrant’s principal executive officer and principal financial officer

concluded that the Registrant’s disclosure controls and procedures are

effective.

(b) Changes in Internal Controls. There have been no changes in the

Registrant’s internal controls or in other factors that could materially affect

the internal controls over financial reporting subsequent to the date of their

evaluation in connection with the preparation of this Shareholder Report on

Item 12. Exhibits.

(a)(1) Code of Ethics

(a)(2) Certifications pursuant to Section 302 of the Sarbanes-Oxley Act of 2002

of Laura F. Fergerson, Chief Executive Officer - Finance and Administration,

and Mark H. Otani, Chief Financial Officer and Chief Accounting Officer

(b) Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 of

Laura F. Fergerson, Chief Executive Officer - Finance and Administration, and

Mark H. Otani, Chief Financial Officer and Chief Accounting Officer