Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of: March 2007

ADECCO SA

(Exact name of Registrant as specified in its charter)

Commission # 0-25004

Sägereistrasse 10

CH-8152 Glattbrugg

Switzerland

+41 1 878 88 88

(Address of principal executive offices)

[Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or 40-F]

Form 20-F x Form 40-F ¨

[Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934]

Yes ¨ No x

Attached:

| - | Annual Report 2006 |

Table of Contents

Table of Contents

Table of Contents

Mission

We inspire individuals and organisations to create greater efficiencies, effectiveness, and choice in the domain of work, for the benefit of all stakeholders. As the world’s largest employment services group, a business that positively impacts millions of people every year, we are conscious of our global role and mission. |

1

Table of Contents

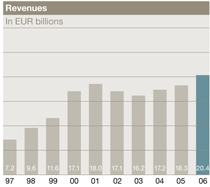

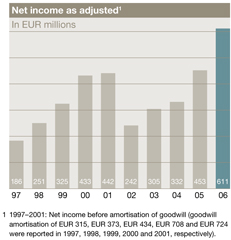

Key figures

| For the fiscal years (in million EUR)1 | 2006 | 2005 | 2004 | 2003 | 2002 | |||||

Statement of operations data | ||||||||||

Revenues | 20,417 | 18,303 | 17,239 | 16,226 | 17,085 | |||||

Gross profit | 3,546 | 3,086 | 2,874 | 2,757 | 3,039 | |||||

Operating income2 | 816 | 614 | 530 | 509 | 454 | |||||

Net income | 611 | 453 | 332 | 305 | 242 | |||||

Other financial indicators | ||||||||||

Cash flow from operating activities | 747 | 298 | 542 | 453 | 442 | |||||

Free cash flow3 | 662 | 230 | 475 | 401 | 342 | |||||

Net debt4 | 556 | 424 | 299 | 924 | 1,411 | |||||

Key ratios (as % of revenues) | ||||||||||

Gross margin | 17.4% | 16.9% | 16.7% | 17.0% | 17.8% | |||||

SG&A ratio | 13.3% | 13.5% | 13.6% | 13.9% | 15.1% | |||||

Operating income margin | 4.0% | 3.4% | 3.1% | 3.1% | 2.7% | |||||

Per share figures | ||||||||||

Basic EPS in EUR5 | 3.28 | 2.43 | 1.77 | 1.63 | 1.30 | |||||

Diluted EPS in EUR6 | 3.14 | 2.34 | 1.69 | 1.61 | 1.28 | |||||

Cash dividend in CHF | 1.207 | 1.00 | 1.00 | 0.70 | 0.60 | |||||

Number of shares | ||||||||||

Basic weighted-average shares | 186,343,724 | 186,599,019 | 187,074,416 | 186,744,214 | 186,527,178 | |||||

Diluted weighted-average shares | 196,532,960 | 196,546,937 | 201,328,174 | 195,777,267 | 193,469,123 | |||||

Outstanding (year end) | 184,836,462 | 186,097,645 | 187,330,240 | 186,989,728 | 186,697,162 | |||||

| 1 | For 2006, the Company’s fiscal year included the full calendar year ending December 31, 2006. In 2005 and 2004, the Company’s fiscal year contained 52 weeks ending December 31, 2005 and 53 weeks ending January 2, 2005, respectively. In 2003 and 2002, the Company’s fiscal year contained 52 weeks ending December 28, 2003 and December 29, 2002, respectively. |

| 2 | Operating income includes amortisation of intangibles of EUR 12, EUR 3, EUR 1, EUR 6, and EUR 4 for 2006, 2005, 2004, 2003, and 2002, respectively. |

| 3 | Free cash flow is a non-U.S. GAAP measure and is defined herein as cash flow from operating activities minus capital expenditures, net. |

| 4 | Net debt is a non-U.S. GAAP measure and comprises short-term and long-term debt, and off-balance sheet debt of EUR 36 and EUR 59, in 2003 and 2002, respectively, relating to the securitisation of receivables, less cash and cash equivalents and short-term investments. There was no off-balance sheet debt at the end of 2006, 2005, and 2004. |

| 5 | Basic earning per share including the impact of discontinued operations of EUR 0.16, EUR (0.01), and EUR (0.04) in 2004, 2003, and 2002, respectively, and the cumulative effect of change in accounting principle of EUR (0.02) in 2003. There were no discontinued operations in 2006 and 2005. |

| 6 | Diluted earning per share including the impact of discontinued operations of EUR 0.15, EUR (0.01), and EUR (0.04) in 2004, 2003, and 2002, respectively, and the cumulative effect of change in accounting principle of EUR (0.01) in 2003. There were no discontinued operations in 2006 and 2005. |

| 7 | Proposed by Board of Directors. |

2

Table of Contents

| ||||||||

Tickers | ||||||||

SWX/virt-x | ADEN | |||||||

NYSE | ADO | |||||||

Euronext | ADE | |||||||

Reuters | ADEN.VX | |||||||

Reuters (ADR) | ADO.N | |||||||

Bloomberg | ADEN VX | |||||||

Bloomberg (ADR) | ADO US | |||||||

ISIN | CH0012138605 | |||||||

ISIN (ADS) | US0067541054 | |||||||

Share price 2006 | ||||||||

Year-end | 83.25 CHF | |||||||

Average | 74.37 CHF | |||||||

3

Table of Contents

Table of Contents

6 | ||||||

9 | ||||||

15 | ||||||

18 | ||||||

22 | ||||||

26 | ||||||

32 | ||||||

38 | ||||||

44 | ||||||

48 | ||||||

53 | ||||||

85 | ||||||

5

Table of Contents

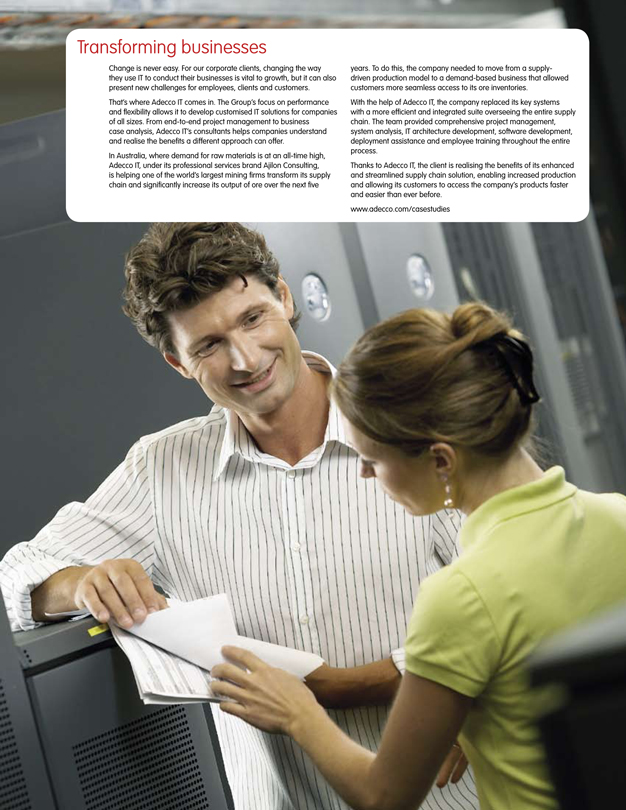

For Adecco Group, 2006 was a year of transition and positive results. The company delivered a strong performance across the board, posting robust increase in income, improved margins and revenue growth. | ||||||

We welcomed a new CEO and CFO who continued our strategy of expanding our professional and specialised business offering, consolidating our brand portfolio and delivering on our vision of “better work, better life” for all our associates. | ||||||

Net income increased by 35% in 2006, a significant improvement over the previous year, and organic revenue grew by a strong 9%. Operating margins improved 60 basis points to 4.0% as a result of the growing contribution from professional staffing, as well as acquisitions, better temporary staffing margins for the Office and Industrial businesses, permanent placements and better cost management. | ||||||

At the beginning of 2006, Adecco acquired DIS AG, the leader in professional staffing in Germany. This investment has further increased our professional and specialised business and given us a leading position in the expanding German market. Professional and specialised staffing represents the highest-margin and fastest-growing market segment in the industry. With this acquisition and our organic growth, Adecco is positioned to expand its competence in high-value services including engineering, finance and IT. | ||||||

Dieter Scheiff became Adecco’s CEO in August 2006 and is implementing our winning business strategy, while Klaus J. Jacobs remains Chairman of the Adecco Group. Our new CFO, Dominik de Daniel, is overseeing the roll-out of the Economic Value Added programme to give our decision-makers the right tools to generate sustainable growth as well as greater value for the Group and our shareholders. | ||||||

In Western Europe, we are witnessing a period of unprecedented flexibility in workplace culture. In the UK, for example, where temporary help comprises 4% of the total labour market, the unemployment rate is approximately 5%, whereas in Germany, where temporary work is just 1% of the market, the unemployment rate is approximately 8%. We believe this inverse relationship in Germany reflects the need for further | ||||||

6

Table of Contents

cooperation between employers and governments to facilitate competitiveness, flexibility and the mobility of firms and workers in order to meet the challenges of the 21st century. | ||||||

To increase its knowledge about labour markets, Adecco launched in 2006 the Adecco Institute, a centre for research and learning on work-related issues in today’s global economy. Chaired by Wolfgang Clement, the former German Federal Minister of Economics and Labour (2002–2005), the Adecco Institute, based in London, brings together the expertise and experiences of Adecco’s senior management as well as leaders from across the corporate and academic worlds. | ||||||

As part of its commitment to develop a broad understanding of the markets in which it operates, Adecco maintains an open dialogue with trade unions and other labour organisations. We firmly believe that continuous engagement is the best way to foster a deeper understanding of each others’ needs in an increasingly complex market. | ||||||

We have many good reasons to be optimistic about our future growth. The positive trends in the global staffing industry are offering promising growth opportunities in our markets. The staffing industry is |

7

Table of Contents

witnessing strong, growing demand for both flexible and skilled labour. We will meet this demand for flexibility and skills by focusing not only on recruitment but also on training and continuous learning. Everyone will need to acquire and develop new skills, and lifelong learning will become a necessity for all firms wanting to keep their talent base flexible. | ||||||||||

As we continue our process of cultural transformation, unifying our many brands and consolidating our presence around the world, we believe we are well positioned to benefit from changing labour markets and share our knowledge of the global labour markets with our business partners. Under one brand, Adecco will increase its visibility and be better able to attract the best talents and concentrate its marketing costs. As we bring our brands together, “better work, better life” is the vision that identifies that common purpose. For our associates, Adecco creates a new way to work; a model that suits people’s different lives, plans, needs for flexibility, career opportunities and individual prosperity. For our clients, we will strive to develop successful partnerships by understanding and anticipating their business requirements, by providing them with outstanding and motivated people to meet or exceed their expectations. | ||||||||||

As we look back on a successful year, we would like to recognise and thank everyone who has contributed to Adecco’s success through their passion, hard work and commitment. We have demonstrated that Adecco delivers on its promises to the market. | ||||||||||

We understand that our objectives cannot be achieved overnight and that small, meaningful steps must be taken towards our 2009 goals. In 2007, we will continue to deliver on our promise of “better work, better life” for our associates, clients, society and ourselves. | ||||||||||

| Jürgen Dormann | Klaus J. Jacobs | Dieter Christian Scheiff | ||||||||

| Vice-Chairman | Chairman | Chief Executive Officer | ||||||||

|  |  | ||||||||

8

Table of Contents

Global staffing markets witnessed strong growth in 2006, driven by good economic conditions, skills shortages in the professional and specialised staffing sectors, a greater demand for more labour flexibility by companies, better acceptance levels of temporary staffing amongst associates and clients, and favourable changes in local legislations. | ||||||

The global staffing market in 2006 reached more than EUR 210 billion, not including staffing-related services in the professional consulting and secondment market. | ||||||

Growing demand for skills | ||||||

We believe demand for professional and specialised skills will continue to outgrow demand from all industries, from manufacturing, to services for lower skilled labour. As the highest-margin and fastest-growing market segment in the industry, professional and specialised staffing is a key focus for Adecco’s growth in the years to come. | ||||||

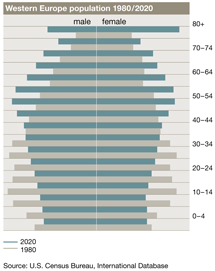

Demographic changes are having a profound effect on labour markets. While longer life expectancy is resulting in more people staying at work for longer, lower birth rates mean fewer young adults are entering the workforce. This is leading to an increase in the proportion of older employees compared to younger ones and ultimately having a dramatic effect on the marketplace. Skill shortages are most | ||||||

| ||||||

9

Table of Contents

pronounced in the Western European labour market, where the repercussions are expected to be higher than in other key Adecco markets, including the US. | ||||||

The increasing scarcity of professional and specialised skills is leading to more flexible staffing patterns and higher job turnover. Adecco is seeking to address these issues by attracting and retaining high-value professional and specialised associates. To meet clients’ demand for skills and greater flexibility in the workforce, Adecco is focusing not only on recruitment, but also on training and continuous learning for its associates, which will increase the general acceptance level of temporary staffing. | ||||||

Market liberalisation | ||||||

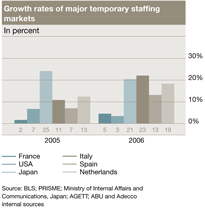

More flexible labour regulations are increasing temporary staffing penetration rates around the globe. In developed economies such as France, Germany, the Netherlands, Spain, Italy and Japan, labour market liberalisation has increased opportunities for employment in the future and, more specifically, for temporary staffing. The introduction of the Borloo Law in France in 2005 has allowed temporary staffing companies to offer permanent placement services out of the same offices they use for temporary services, which has significantly boosted Adecco’s business platform in our key market. | ||||||

As legislative changes are implemented, companies adapt their demand for more temporary labour and specialised skill sets to address a competitive and fast-changing environment. We believe the implementation of more flexible regulations in many of Adecco’s key markets is likely to continue in the foreseeable future. This will allow for greater penetration rates for staffing services and provide the flexibility of labour companies are demanding (see table below). |

Penetration rate (year to December) in % | ||||||

| 1999 | 2006 | 2009F | ||||

France | 2.3 | 2.5 | 3.0–3.5 | |||

US | 2.4 | 2.5 | 2.5–3.0 | |||

UK | 3.6 | 4.5 | 4.0–5.0 | |||

Japan | 0.6 | 0.9 | 2 | |||

Italy | 0.2 | 0.7 | 1.5–2.0 | |||

Spain | 0.8 | 1 | 1.5–2.0 | |||

Netherlands | 4.5 | 4.5 | 4.0–4.5 | |||

Belgium | 1.6 | 2 | 3 | |||

Germany | 0.7 | 1 | 2.0–2.5 | |||

| Source: ABN AMRO Support Services |

10

Table of Contents

| Positive economic outlook | ||||||

Demand for more flexible staffing and human resource solutions is expected to increase as the global economy improves. Historically, there is a correlation between economic development and demand for staffing. This relationship is illustrated in the graphs below in the cases of France and the US. | ||||||

| ||||||

The generally positive outlook for global GDP development indicates that demand for staffing, particularly in Europe and Asia, will remain robust in the foreseeable future. | ||||||

| ||||||

11

Table of Contents

In the emerging markets, where wage levels are low, market sizes are still relatively small today. However these markets represent a significant opportunity for skilled staffing in the future. In 2006, almost a quarter of all Adecco’s placements were in the emerging markets, but only 5% of Group’s revenues were generated there. |

GDP growth (year to December) in % | ||||||||||||||||

| 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | |||||||||

France | 1.8 | 1.1 | 1.1 | 2.0 | 1.2 | 2.0 | 1.8 | 2.1 | ||||||||

US | 0.8 | 1.6 | 2.5 | 3.9 | 3.2 | 3.3 | 1.7 | 2.3 | ||||||||

UK | 2.4 | 2.1 | 2.7 | 3.3 | 1.9 | 2.6 | 2.3 | 2.2 | ||||||||

Japan | 0.4 | 0.1 | 1.8 | 2.3 | 2.7 | 2.1 | 1.4 | 2.5 | ||||||||

Australia | 2.4 | 3.9 | 3.3 | 3.3 | 2.9 | 2.4 | 2.1 | 3.4 | ||||||||

Italy | 1.7 | 0.3 | 0.1 | 0.9 | 0.1 | 1.8 | 1.3 | 1.4 | ||||||||

Spain | 3.6 | 2.7 | 3.0 | 3.2 | 3.5 | 3.7 | 3.1 | 2.9 | ||||||||

Netherlands | 1.4 | 0.1 | 0.3 | 2.0 | 1.5 | 2.8 | 2.4 | 2.5 | ||||||||

Belgium | 0.7 | 1.4 | 1.0 | 2.7 | 1.5 | 3.0 | 1.8 | 2.1 | ||||||||

Germany | 1.4 | 0.0 | –0.2 | 0.8 | 1.1 | 2.6 | 1.0 | 1.4 | ||||||||

Sweden | 1.2 | 2.0 | 1.8 | 3.3 | 2.7 | 5.1 | 2.8 | 2.7 | ||||||||

China | 8.3 | 9.1 | 10.0 | 10.1 | 10.4 | 10.5 | 9.5 | 8.9 | ||||||||

India | 4.4 | 5.8 | 3.8 | 8.5 | 7.5 | 9.0 | 7.8 | 7.8 | ||||||||

Russia | 5.1 | 4.7 | 7.3 | 7.2 | 6.4 | 6.7 | 7.5 | 7.2 | ||||||||

Source: OECD; National Statistical Authorities, Forecasts (2006–2008) Deutsche Bank Global Markets Research | ||||||

|

12

Table of Contents

Table of Contents

Table of Contents

| The Adecco Group is the world leader in human resource services with a comprehensive offering that includes temporary staffing, outsourcing, permanent recruitment, outplacement and career management, training and consulting. | ||||||

Adecco delivers an unparalleled range of flexible staffing and career resources to clients and qualified associates across virtually every business area, seniority level and age group. | ||||||

Adecco was created in 1996, following the merger of Adia of Switzerland and Ecco of France – two leading personnel services firms with complementary geographical profiles. Headquartered in Zurich, Switzerland, Adecco is managed by a multinational team with expertise in markets spanning the globe. Today we have over 37,000 employees and more than 6,700 offices in over 70 countries and territories. Each day our network connects over 700,000 associates with clients. | ||||||

In addition to its established businesses – Office and Industrial – Adecco operates professionals business line. These are: Adecco Finance & Legal; Adecco Engineering & Technical; Adecco Information Technology; Adecco Medical & Science; Adecco Sales, Marketing & Events; and Adecco Human Capital Solutions. The expansion of these Professional Business Lines leverages our expertise across the world. To better serve clients and associates in the Office and Industrial business we are organised into global practices of specialisation that are virtual networks designed to facilitate the sharing of knowledge among our employees. | ||||||

| Partnerships and opportunities | ||||||

Our competence extends beyond temporary and permanent placements to forging genuine career partnerships. Our strategy is to develop lasting relationships with our associates, enhancing their skills and competencies through continuous learning opportunities and challenging projects. | ||||||

Adecco actively promotes lifelong learning by creating an effective learning environment at the workplace, while providing further education and mentoring | ||||||

15

Table of Contents

programmes. We believe everyone who works with us can receive mentoring and guidance to enhance their value in the workplace. | ||||||

We create opportunities for the associates who work with us through programmes that develop life skills, career progression and access to specialised expertise. We are also committed to helping people for whom finding work can be difficult, due to limited skills or disabilities, enabling them to overcome those obstacles and obtain meaningful employment. | ||||||

| Better work, better life | ||||||

At Adecco we aspire to be a force for good in society by delivering better services to our clients and better careers for our associates. This goal sums up our approach and illustrates what our clients and associates expect from us. | ||||||

For our associates, we seek to inspire and motivate them to get more out of work and life by developing their expertise through training and certification programmes that lead to more senior and rewarding roles. | ||||||

For our clients, we strive to develop successful partnerships by understanding their business requirements and providing outstanding and motivated people. We believe that a complete understanding of their markets and personnel needs is the only basis for a service that meets or exceeds their expectations. | ||||||

| Values | ||||||

At Adecco, we believe our reputation is our most important asset. We strive to build and sustain our reputation through an ongoing commitment to our core values: respect, responsibility, honesty and integrity. We put these values to work every day with our colleagues and associates, customers, suppliers, shareholders and the communities in which we operate. | ||||||

| Commitment to our responsibilities | ||||||

We understand the importance of the role Adecco plays with every client and associate when they entrust us with the responsibility to build their team or their career. Our success is driven by our ability to leverage our expertise, network and passion with | ||||||

16

Table of Contents

each assignment. These important elements are at the core of our leading position in staffing markets around the world. | ||||||

| Expertise and innovation | ||||||

Our roots span almost half a century and our experience in the global HR services industry is second to none. At Adecco, we are focused on the requirements of the world of work every day and have long been committed to designing innovative solutions for our clients and associates. We have the scope and insight to understand employment and labour market issues around the world. We have long-established relationships with thought leaders and opinion formers that allow us to discuss and test new and different approaches to address productivity and business challenges. We have experienced the cyclical nature of work and understand how fast-moving economies affect the labour market. This understanding of industry trends, best practice and new labour and training initiatives gives us greater market knowledge and allows us to maintain a stronger local presence than our competitors. | ||||||

| Network | ||||||

We leverage our global reach and critical mass to create real advantages for our clients and associates. Our network of relationships brings us close to governments, organised labour, employers, employees and universities. We have organised ourselves and used our strengths to build and improve the skills of the human capital we provide. Our commitment to using our network successfully helps associates find the work they want but cannot find on their own and helps our clients find talented associates they would never have met without Adecco. | ||||||

| Passion | ||||||

We have a unique environment at Adecco. Our employees are passionate entrepreneurs who understand that the people they work with seek solutions and need our support in order to be successful. Adecco’s people are focused on creating real advantages that will enhance the opportunities their clients and associates have in work. They are committed to using their industry knowledge and experience to anticipate their requirements. We sustain our position as a leader in labour markets around the world by continually working to attract the best employees and rewarding their creativity, entrepreneurship and flexibility at all levels of the organisation. | ||||||

| ||||||

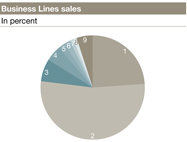

1 | France | 33 | % | ||||||||||

2 | USA & Canada | 18 | % | ||||||||||

3 | UK & Ireland | 9 | % | ||||||||||

4 | Japan | 7 | % | ||||||||||

5 | Italy | 6 | % | ||||||||||

6 | Iberia | 5 | % | ||||||||||

7 | Benelux | 5 | % | ||||||||||

8 | Germany | 4 | % | ||||||||||

9 | Nordics | 4 | % | ||||||||||

10 | Switzerland | 2 | % | ||||||||||

11 | Australia & New Zealand | 2 | % | ||||||||||

12 | Emerging Markets | 5 | % |

17

Table of Contents

Office and Industrial businesses

| Office and Industrial, the Adecco Group’s two largest businesses, offer flexible staffing solutions in response to clients’ business fluctuations and skill shortage needs. | ||||||

The businesses serve large global clients as well as small and mid-sized enterprises across a variety of sectors. | ||||||

The Office and Industrial businesses offer a full range of general staffing services including temporary staffing, permanent placement, assessment, training and integrated human resources solutions. | ||||||

The businesses operate out of Adecco’s 5,100 offices spread across Western Europe, USA and Canada, Japan, Australia and New Zealand. In addition to offering a local response, the business’ office network provides convenient access points for client development and associate recruitment. | ||||||

| Business performance | ||||||

The Office and Industrial businesses, also referred to as our general staffing divisions, represent the core of the Adecco Group’s business, accounting for 77% of the Group’s revenues for the year ended December 31, 2006. The Industrial business accounted for 53 %, and the Office business accounted for 24% of the Group’s revenues. | ||||||

Revenues for the Office business totalled EUR 4.8 billion, and gross profit totalled EUR 0.9 billion. Revenues for the Industrial business totalled EUR 10.9 billion, and gross profit totalled EUR 1.5 billion. | ||||||

Together, the two businesses employ over 500,000 associates each day, serving 122,000 clients. | ||||||

| Strategic objectives | ||||||

In our traditional Office and Industrial businesses, which are highly competitive, Adecco looks for every opportunity to improve its margins and the efficient delivery of services to clients. We are expanding our business from a transactional model, which focuses on providing short-term solutions, to a strategy that focuses on long-term value creation through the retention and development of our associate and client relationships. | ||||||

| Specialisation | ||||||

We are consolidating our leadership position and focusing more on specialised opportunities in high-growth areas such as hospitality, construction and logistics. In this way, Adecco is transforming itself from a general staffing provider to a staffing firm offering specialised solutions across a variety of industries. | ||||||

We are implementing our new strategy and shifting our focus towards higher-value relationships and better | ||||||

18

Table of Contents

service for our clients across all of the countries in which we operate. By leveraging our existing general staffing footprint, we are penetrating into more specialised areas which offer higher profit margin potential. | ||||||

Flexibility | ||||||

Adecco is continuously innovating its product offering to adjust to the flexible working cultures in today’s labour markets. In developed economies throughout Europe and the US, where companies are increasingly turning to flexible working strategies, Adecco offers tailored solutions to meet our clients’ employment needs. | ||||||

At the same time, our focus on flexibility is helping us attract and retain motivated associates of all ages, who are increasingly choosing shorter-term work contracts spread over a longer time period. By providing consecutive assignments, together with skill-enhancing training and competitive wages, Adecco is creating lifetime partnerships with associates that fulfil their lifestyle aspirations while retaining the best talent among our associate pool. | ||||||

We believe that being a “temp” will make for an attractive, lifetime career choice in the future. By fostering the acceptance of flexible work solutions and by developing routes to lifelong learning, Adecco is proactively responding to the needs of its associates as well as those of the global labour market. | ||||||

Changing legislation | ||||||

Reduced obstacles for employment in labour regulations are fostering new growth in many of our core general staffing markets. The demographic shift we face is one of the most powerful drivers for social change in our lifetimes and our children’s. Across the world, governments are recognising these challenges. They deserve our support in facilitating company competitiveness, flexibility and mobility of firms and workers, as well as in bringing labour regulations into line with 21st century needs. | ||||||

Technological innovation | ||||||

Technology has revolutionised the staffing industry, especially in the recruitment and provision of temporary staffing services. We are continuously innovating and investing in our technology platform so we can deliver seamless solutions and improve efficiency. By leveraging our critical mass through global technology, we are facilitating closer relationships with both our clients and associates. | ||||||

Expanding our expertise | ||||||

We continue to pursue opportunistic acquisitions and expansion in developing economies where there is strong demand for the provision of general and professional staffing services. | ||||||

In the growing German market, our acquisition of DIS AG has consolidated our position as the second-largest general and specialist staffing provider. The acquisition has resulted in an even higher quality of service for our German clients and greater opportunities for our associates. Furthermore we have become the clear market leader in the professional staffing segment in Germany. |

19

Table of Contents

Table of Contents

Table of Contents

Adecco has Professional Business Lines dedicated to areas of professional expertise that are of high relevance to our clients. These fast-moving units keep us close to the most important occupational fields and the people that work in them. | ||||||

Strategic focus | ||||||

Our Professional Business Line approach enables us to concentrate and increase industry insight, best practice and to launch new initiatives on a global scale. It perfectly complements our Office and Industrial businesses. | ||||||

In 2006, the sum of revenues from our Professional Business Lines grew by 17%, partly as a result of the acquisition of DIS AG, with the strongest growth coming from Engineering & Technical, and Finance & Legal. Our Professional Business Lines contributed 18% of revenues in 2006 and 26 % to the Group’s gross profits. It was and is our goal to increase revenues from our Professional Business Lines from 17% in 2005 to 21% in 2009. | ||||||

The Professional Business Lines are based on the “experts talk to experts” concept: high-level, specialist points of contact with clients and longer-lasting assignments for associates, along with different pricing points to the general staffing business. The Professional Business Lines supply a range of products to clients and associates, from short-term to long-term projects with specific competencies in project secondment, permanent placements, temporary recruitment solutions, and managed solutions. | ||||||

Engineering & Technical | ||||||

Adecco Engineering & Technical is an international engineering business in this rapidly-changing sector. It has dedicated teams for several key industries, including aeronautics, automotive and railroad, nuclear, oil and gas, and others. | ||||||

In 2006, the Engineering & Technical business grew revenues by 19% and contributed 5 % to the Group’s revenues and 4% to the Group’s gross profit. | ||||||

Finance & Legal | ||||||

This Professional Business Line provides temporary and permanent placements of premier accounting and finance professionals, as well as consulting services in areas such as management, compliance, internal audit, finance and Mergers and Acquisitions (M&A). | ||||||

The Finance & Legal business line achieved revenue growth of 20% in 2006 and represents 2 % of Adecco’s revenues, but 5% of the Group’s gross profit. | ||||||

Human Capital Solutions | ||||||

We are one of the global leaders in a range of restructuring and talent solutions for organisations aiming to optimise their human capital. Under the established brand names of Lee Hecht Harrison (US), Altedia (France) and Adecco Human Capital Solutions (globally), we provide consulting services to companies and organisations while helping individuals develop their career potential and improve their employability. | ||||||

The Human Capital Solutions business grew revenues by 13% in 2006 mainly due to the 2005 acquisition of Altedia. The business line generated 1% of the Group’s revenues, but 6% of the Group’s gross profit. |

22

Table of Contents

Table of Contents

Table of Contents

Information Technology | ||||||

Adecco Information Technology is structured to respond to the needs of companies seeking to integrate, organise and control their information technology services and activities. | ||||||

In 2006, Information Technology increased its revenues by 15%, which resulted in 7% of the Group’s revenues and 8% of the Group’s gross profit. | ||||||

Medical & Science | ||||||

Our Medical & Science business line provides specialised human resources solutions in nursing, para-medical, pharmacy, technical support staff and quality assurance. | ||||||

Medical & Science increased revenues by 15% in 2006 and contributed 1% to the Group’s revenues and gross profit. | ||||||

|

1 | Office | 24 | % | ||

2 | Industrial | 53 | % | ||

3 | Information Technology | 7 | % | ||

4 | Engineering & Technical | 5 | % | ||

5 | Finance & Legal | 2 | % | ||

6 | Sales, Marketing & Events | 2 | % | ||

7 | Medical & Science | 1 | % | ||

8 | Human Capital Solutions | 1 | % | ||

9 | Emerging Markets | 5 | % |

Sales, Marketing & Events Adecco’s global reach provides specialists in every field of Sales, Marketing & Events. We help our clients with a wide range of marketing needs, from launching new products in foreign countries where they have no expertise, to working with them to build a sales force quickly. | ||||||

Sales, Marketing & Events grew revenues by 13% in 2006. The business line accounted for 2% of the Group’s revenues and gross profit. | ||||||

Experts talk to experts | ||||||

Our dedicated Professional Business Lines ensure that experts are always talking to experts. First-hand knowledge of the industries in which we work makes us better equipped to help our clients and candidates meet their present and future needs. | ||||||

Adecco’s long-term strategy for the global professional staffing sector is focused on building lasting relationships with clients and associates. By developing long-term relationships with our associates we are responding to the growing demand for a flexible and professional workforce. | ||||||

As pressure on the worldwide supply of qualified individuals continues to grow, temporary professional assignments are contributing to the efficient allocation of labour and are increasingly attractive to qualified individuals. With pressures and incentives to adopt portfolio careers, our associates value a supportive and highly informed partner through whom they are consistently able to access work that is right for them. | ||||||

We are also dedicated to enhancing the knowledge of our associates through continuous learning opportunities and challenging serial projects. We attract and retain professionals by helping them improve their competencies along the way. |

25

Table of Contents

At Adecco, we aim to build long-term value for all our stakeholders. Whilst we are always focused on our bottom line, we are moving beyond pure accounting profitability as a measurement of value creation, by promoting new tools that encourage investment and growth among our employees, customers and investors. | ||||||

This philosophy of “managing for value” is fundamental to our business strategy and means that we put the perspective of our employees, associates, clients and shareholders at the heart of all our decision-making. It helps us determine how we allocate investment, and understand how those investments deliver profitable, sustainable growth. | ||||||

Our enterprising approach to value creation allows us to pursue new market opportunities, helping us respond to shortages in key areas and rebalance our portfolio towards the fastest-growing sectors in the labour markets. Our strategic move towards professional and specialised staffing, for example, directly reflects this focus on delivering growth and increasing our enterprise value. | ||||||

Our focus on lifelong learning and training for our associates also directly stems from our commitment to value enhancement. By offering a variety of training courses, we attract and recruit the best talent available while providing our clients with highly skilled and motivated workforces. This delivery of expert, professional and specialised skills produces higher profits, allowing us to retain higher value clients and deliver better returns to our investors. | ||||||

In order to deliver the best value and transparency, we have to manage our local decision-making within a group-wide approach to investment. To help us achieve this, we have introduced an Economic Value Added concept. This plays an essential role in ensuring that we have a consistent and dependable approach to our pricing policies and performance-related incentives for our employees. It also allows us to focus on acquisitions and investments that create value and exceed a minimum return. | ||||||

26

Table of Contents

Introducing Economic Value Added | ||||||

The Economic Value Added concept means that every Adecco employee is focused on the goal of value generation while giving them the freedom and flexibility to enter new markets that have been key to Adecco’s global success. It equips our managers with the right tools to retain their entrepreneurial approach to business while making better decisions that deliver long-term growth. | ||||||

Why Economic Value Added? | ||||||

As a global operator, Adecco responds to different degrees of deregulation in temporary labour markets and varying macroeconomic conditions through a decentralised corporate culture. This approach requires good central control systems and management tools to ensure all our operations are in line with the Group’s strategy. | ||||||

The Economic Value Added concept helps us align the interests of our shareholders with those of our colleagues around the world by helping our decision-makers focus on generating value while encouraging the local entrepreneurship that has been key to our global success. | ||||||

As a management tool, the Economic Value Added concept allows us to find the right balance between market share, profitability and invested capital. It improves our managers’ ability to make the right choices and identify the most beneficial client relationships, acquisitions, strategies, incentive schemes and targets. | ||||||

How is Economic Value Added calculated? | ||||||

Economic Value Added is a performance calculation of residual income. It considers value creation only if operating income after the deduction of income taxes is greater than the minimal required rate of return – the company’s weighted-average cost of capital. | ||||||

This calculation is based on the Net Operating Profit After Taxes (NOPAT) of the entity and disregards all non-operational impacts such as financing decisions and takes into account a general income tax rate of 30%. Invested capital is defined as total assets minus liabilities, excluding cash and interest-bearing liabilities. The acquired goodwill and intangible assets are carried at book value. For sustainability and simplicity reasons all of Adecco’s entities apply a cost of capital of 10%. This compares to the weighted-average cost of capital of Adecco of 8.6 %, using a risk-free rate of 2.8%, a beta of 1.23, an equity risk premium of 5 % and an equity ratio at market value of 92%. |

27

Table of Contents

Economic Value Added and ROCE for 2005 and 2006 | ||||

| 2005 | 2006 | |||

Sales | 18,303 | 20,417 | ||

Operating profit | 614 | 816 | ||

Tax | –184 | –245 | ||

Tax rate | 30% | 30% | ||

NOPAT | 430 | 571 | ||

Average invested capital | 2,318 | 2,812 | ||

WACC | 10% | 10% | ||

Cost of capital | –232 | –281 | ||

Economic Value Added | 198 | 290 | ||

ROCE | 18.5% | 20.3% | ||

For the purposes of clarity and due to its better acceptance and understanding in the financial community, Adecco reports its capital efficiency as return on capital employed (ROCE), which is simply NOPAT as a percentage of the invested capital. | ||||||

Implementing Economic Value Added | �� | |||||

There are three main areas where the Economic Value Added concept is applied: | ||||||

– As a performance measure for incentive plans – To determine contract pricing – As a valuation tool for acquisitions | ||||||

The successful introduction and adoption of Economic Value Added methodologies in these areas is central to our goal of reaching above 25% ROCE by 2009 (see graph page 29). | ||||||

Incentive plans | ||||||

In 2006, the Economic Value Added concept was introduced for compensation calculations for senior management at Group level. This has provided better incentives for the implementation of the Group’s strategy and encouraged senior managers to focus on return on investment. Adecco is implementing variations of Economic Value Added for bonus calculations at almost all levels of the organisation in 2007, most notably in the area of account management. |

28

Table of Contents

Contract pricing | ||||||

As a pricing tool, Economic Value Added provides a better understanding of the cost structure and capital needs for doing business with individual clients and is the first step in a long-lasting, beneficial client relationship. During 2006, Adecco account managers implemented Economic Value Added pricing guidelines for all new client contracts and conducted a value analysis of the top existing clients. | ||||||

Valuation of acquisitions | ||||||

The Economic Value Added methodology is also used to test the attractiveness of future acquisitions. The company is better protected against overpaying for acquisitions because goodwill and intangible assets are an incremental part of invested capital and have a strong bearing on managers’ pay incentives.

| ||||||

|

29

Table of Contents

Table of Contents

Table of Contents

Adecco’s focus on training, education and mentoring initiatives is creating opportunities for associates of all ages at every stage of their career paths. Our programmes offer routes to lifelong learning to both strengthen our pool of talent and help enhance our employees’ lives.

| ||||||

Our commitment to further education and skills training is one of the cornerstones of our strategy to embrace changing demographic trends, particularly ageism and lower birth rates, which are fuelling the demand for an increasingly flexible, skilled labour force throughout the developed world. Our investment also serves a broader role in tackling skills shortages and helping societies reduce their dependence on government-sponsored initiatives for further education. | ||||||

In 2006 Adecco invested more than EUR 100 million in training, in compliance with national regulatory requirements, and as part of our commitment to education and developing the skills of our employees. | ||||||

Tools for growth | ||||||

Building sustainable and productive relationships with our associates involves understanding their career aspirations from the very beginning of their employment. Adecco utilises the latest technologies for assessing the capabilities and motivations of all our potential employees and matching them with the right career opportunities. The Adecco Xpert™ analytic and e-Learning software is one way we measure and report on a candidate’s suitability for an individual position, benchmarked against the existing staff profile and industry sector. Third-party analysis of our Xpert system has determined there is a statistically significant correlation between a candidate’s Xpert test results and his or her performance on assignment. | ||||||

Adecco Xpert is used on a worldwide basis and in 2006 we conducted more than 3.8 million assessments of candidates. | ||||||

Training and development | ||||||

Regular training is essential for the professional development of our associates and for ensuring that we maintain a highly skilled, motivated pool of talent. In today’s competitive workplace environment, providing flexible, skills-driven training courses allows our associates to enhance their skills in tandem with their careers. | ||||||

32

Table of Contents

While our commitment to training is global, our approach is local, allowing us to respond to cultural and regional disparities in demands for skills and education. | ||||||

In North America, Adecco’s Virtual University offers over 60 web-based accredited courses for professional associates, so they can grow their careers in their own time and at their own pace. The curriculum is organised into four continuing education modules: business skills, technical skills, professional development and management development. In Cincinnati, Ohio, we have opened the Adecco Training Center, a state-of-the-art facility that serves as our American training hub for Adecco colleagues where they can advance their skills in a range of functional roles and business lines. | ||||||

In the UK, more than 6,500 associates are enrolled in Adecco’s Flexible Learning programme, an online training and development initiative that associates can access at any time, free of charge. Associates can enhance their skills with a wide range of courses including business development, customer service and computer applications which they can tailor to their own speed and style of learning. | ||||||

In France, Spain and Italy, where government regulations require staffing companies to invest in associates’ education and training, Adecco is helping meet staffing requirements for employers by offering online and part-time programmes that continue to attract thousands of associates every year. In France, more than 38,000 associates are enrolled in training courses. | ||||||

In Japan, Adecco offers a wide variety of training programmes, fostering careers from university-leavers to senior workers looking to change careers. Adecco’s “Career-Up” schools offers business skills and development courses in foreign languages, book-keeping and even interviewing techniques. The programme has been extended to more than 25 locations nationwide, reaching more than 25,000 associates. For more information, please refer to the case study on Japanese training programmes on page 36. | ||||||

In India, where demand continues to grow for experienced call centre services personnel, more than 10,000 associates have received training through Adecco’s Enterprise Learning Group, an initiative to provide communication development courses in personality, selling, customer orientation and negotiation skills. |

33

Table of Contents

Productive ageing | ||||||

As life spans across the developed world continue to rise, employers and industries at large will have to embrace longer career lives among their workers. Adecco is committed to supporting productive ageing, offering senior workers career opportunities that meet their lifestyle aspirations while offering them training and development to update their skills and learn new ones. | ||||||

Our programmes are part of our broader recognition that reintegrating senior people into the workforce is vital if we hope to counter rising public expenditure while sustaining economic productivity. | ||||||

Adecco is shifting away from the traditional linear life model – education, work, retirement – and embracing a more integrated approach that allows these three elements to overlap, switch and repeat themselves throughout the career spans of our workers. By adapting ourselves to the needs of our associates, Adecco is providing a working culture that fosters long-term relationships with employees of all levels and helps us retain the best talent. | ||||||

Across Europe and North America, Adecco is working in partnership with governments and academic institutions to understand the impact of ageing workforces in developed economies and provide working solutions for senior worker reintegration. | ||||||

In collaboration with Jacobs University (formerly the International University of Bremen), Germany, Adecco is researching productive ageing. Our findings continue to demonstrate that there is no negative correlation between performance and ageing; in fact, in many cases, job satisfaction, loyalty and overall work ethics are highest among senior workers. As Adecco continues to explore the impact of these trends around the world, our research will serve as a guide for helping us adapt our own workplaces to the needs of our employees. | ||||||

The Renaissance Programme | ||||||

In North America, Adecco created the Renaissance Programme exclusively for mature workers who choose to return to work. The programme offers benefit packages and flexible assignments tailored to the needs of senior workers, while advocating the benefits senior workers can offer to our clients. For the past three years, the Renaissance Programme has been recognised as one of the “Best Employers for | ||||||

34

Table of Contents

Workers Over 50” by the AARP, one of America’s leading organisations dedicated to enhancing the lives of people as they age. | ||||||

Earn & Learn | ||||||

In May 2006 Adecco launched its new Earn & Learn programme, an initiative to improve the skills of our associates in tandem with delivering more specialised staffing to our clients. Through designated career centres, associates can access training and development courses to improve their skills and accelerate their careers. In addition to general skills training, Adecco can also tailor the courses to meet the specific needs of a client, ensuring the company’s staff is fully prepared with the skills they need to fill jobs across a variety of business lines. In the future, we expect to expand the Earn & Learn programme, which is currently being piloted in Germany and Belgium, to Adecco locations worldwide. | ||||||

Coaching and mentoring | ||||||

Internally, Adecco recognises the importance of advancing the skills of our future leaders throughout the organisation. In 2004, Adecco launched the Adecco International University in partnership with the IMD business school in Lausanne, Switzerland. More than 150 employees have participated in the three-year programme, which serves as a high-level leadership training course for Adecco senior managers around the world. Two management training programmes – Top Management and International Executive Development – serve as platforms for discussion and development to ensure leadership is organically transferred through the organisation. | ||||||

With more than 700,000 people across 70 countries and territories, Adecco’s commitment to training, development and mentoring for all our employees underscores our culture of industry innovation, leadership and best practice management throughout our worldwide network. | ||||||

35

Table of Contents

Table of Contents

Table of Contents

Work is about more than just providing for the cost of living. Work provides a sense of purpose and belonging, fostering our dignity and helping us set lifelong goals.

| ||||||

As one of the world’s largest employers, Adecco has a vital responsibility to provide equal opportunities and make the workplace more accessible for people of all circumstances. In this way we are helping bring our ethic of “better work better life” to disadvantaged and disabled people around the globe. | ||||||

Macro-economic trends, including maturing workforces, migration, declining birth rates and the demand for greater flexibility from employers and workers, are driving changes in the way we approach the workplace. It is more important than ever that we actively commit ourselves to integrating people from all backgrounds into our workforces. | ||||||

Our vision for creating a workplace of choice is founded on the following principles: | ||||||

– To be an employer whose colleagues and associates are proud to work with us – To be the HR solutions provider in touch with the social goals of our clients – To be a global enterprise trusted by society at large – To be a business that generates a socially responsible, sustainable return on investment for all stakeholders | ||||||

Our commitment to social equality and integration is about treating all our employees and colleagues as we would wish to be treated ourselves. It is also about delivering a strong and credible equity story to our investors, which in turn strengthens our competitive position and helps us achieve sustained profitability. | ||||||

Social strategy | ||||||

Adecco aims to be a force for good in society at large. To do that, we strive to foster open and sustained dialogues with all our stakeholders, including employees, unions, companies, regulators and the investment community, proactively addressing their concerns and providing products and services to meet their needs. | ||||||

Through training, incentives and internal discussion, we aim to instil our principles and values in the daily lives of our colleagues, encouraging ethical behaviour | ||||||

38

Table of Contents

and respect for everyone around them. This includes defending international labour standards such as non-discrimination, and focusing on health and safety at work. | ||||||

Establishing clear goals is important to ensure we are focusing our social efforts appropriately. By setting benchmarks and identifying tangible performance indicators, we are equipping ourselves with the tools to create real change and measure our achievements. | ||||||

| United Nations Global Compact | ||||||

In November 2003 Adecco became the first global HR services company to join the United Nations Global Compact, an initiative that encourages businesses worldwide to adopt and report on their efforts towards socially responsible working policies. The Compact aims to protect human rights, fight corruption and promote fair working conditions. One of Adecco’s first initiatives as part of the Compact was to partner with the International Labour Organisation’s training centre, providing comprehensive training to our staff in human and labour rights regulations. | ||||||

| Disabled workers | ||||||

Adecco is committed to making work accessible to everybody, including disadvantaged and disabled people who would otherwise find it difficult to access the labour markets. Every year Adecco finds employment for more than 9,000 disabled individuals, helping integrate, train and mentor them towards sustainable long-term careers. | ||||||

| Business & disability network | ||||||

We are a founding member of Business & Disability, a pan-European network founded in 2004 that raises awareness of disability issues in the workplace. The programme promotes disability inclusion initiatives among workers and employers, and provides practical approaches to achieving better integration. Companies are given guidance about how to welcome disabled workers within their teams and prepare their working environments. By focusing on the business case for inclusion, the network is proving that anti-discrimination is not just morally better, it also makes good business sense. | ||||||

| Increasing employability worldwide | ||||||

Adecco is committed to making work accessible to everybody. Although our dedication to social advancement is global, our approach is local, allowing us to target the needs of different social groups around the world. | ||||||

39

Table of Contents

Adecco’s foundation-based operational partnerships in Italy, France, Germany, Spain, Belgium and Switzerland enable us to participate in programmes aimed at the most at-risk social groups on a country-by-country basis. | ||||||

In Italy, the Adecco Foundation has found employment for more than 22,000 disabled workers, mothers and long-term unemployed people. The Foundation also helps organise conferences on equal opportunity issues in the labour markets and, in collaboration with the Cattolica University of Milano, provides research into Italy’s temporary working opportunities and disadvantaged people. | ||||||

The Adecco Foundation France, founded in 2002, helps disadvantaged youths succeed in education and ease their transition into employment. The programme provides more than 300,000 in grants to youth-based programmes every year. | ||||||

The Adecco Foundation Spain, founded in 1999, provides assistance, support and training for hundreds of disabled people and unemployed mothers. As a result, Adecco has been honoured as one of Spain’s most socially responsible employers by Empresa y Sociedad, an organisation promoting workplace rights. | ||||||

In the US, Adecco has partnered with the US-based Jobs for America’s Graduates (JAG) programme, one of the largest and most successful school-to-career transition and drop-out prevention programmes for disadvantaged youths. Through direct grants as well as educational outreach initiatives, Adecco helps JAG train young people across the country. Meanwhile, Adecco’s Career Accelerator programme works with US military spouses who suffer from frequent relocations, providing career counselling, training and job placement to the wives and husbands of those serving in the armed forces. | ||||||

Since 2000, Adecco’s Athletes Career Programme, in partnership with the International Olympic movement, has helped Olympic athletes around the world adapt and move into more conventional careers after their sports careers have ended. Some 95% of the 700 athletes who have completed the programme have found successful career solutions. The programme, which attracts athletes from Spain, Italy, Norway, Denmark, Sweden and the US, is expanding into France, Slovenia and Finland. | ||||||

There is still much that can be done to eradicate workplace discrimination and provide better access to employment for the most disadvantaged groups. For Adecco, we will continue to strive towards better understanding of these challenges in our efforts to serve as a benchmark for employers around the world. |

40

Table of Contents

| Chairman’s Award winners | ||||||

Above all, it is people who make the difference at Adecco, through their day-to-day actions at a local level, throughout the network. Colleagues strive to combine excellent professional performance, commitment to Adecco values and service to their communities. Each year, colleagues who make outstanding contributions on all three fronts are recognised in the Chairman’s Awards and in 2006, the fifteen Award winners were: | ||||||

– Valery Antipov: Branch Manager, Adecco Russia – Nárcisz Berekhelyi: Branch Manager, Adecco Hungary – Daniel Bossel: Branch Director, Adecco Switzerland – Valentina Chiesa: Project Leader Turin 2006, Adecco Italy – Maria Wellhardh Dahl: Branch Manager, Stockholm City, Adecco Sweden – Urs Kläger: Branch Director, Adecco Switzerland – Anne Lantheaume: Branch Assistant, Adecco France – Hélène Pacini: Branch Manager, Adecco France – Mária Pálinkás: Branch Manager, Adecco Hungary – Torben Sneve: Branch Manager, Oslo Adecco Norway – Darlene Spolar: Client Services Manager, Adecco USA – Randi Turpin: Branch Manager, Adecco USA – Michelle Tutt: Branch Manager, Adecco USA – Estelle Wong: Branch Manager, Adecco Singapore – Francis Wong: Branch Manager, Adecco Singapore | ||||||

| The Chairman’s Award criteria | ||||||

| Outstanding performance: | ||||||

Consistently producing excellent business results, through innovation, creativity, and new ideas that develop and grow Adecco’s business. | ||||||

| Commitment to values: | ||||||

Consistently exhibiting the following Adecco values at work: | ||||||

1. Customer focus 2. Empowerment/entrepreneurial behaviour 3. Innovation and creativity 4. Results orientation 5. Open communication & teamwork 6. Honesty & integrity 7. Social responsibility & good citizenship | ||||||

| Community involvement | ||||||

Conforming to Adecco values in their personal life. This may be donating personal time to a charity or programme that supports youth, seniors, minorities, the underprivileged, disabled, unemployed or other groups in need. | ||||||

41

Table of Contents

Table of Contents

Table of Contents

| “More and more people see temporary staffing as a great opportunity to enhance their employability” – Wolfgang Clement, January 2007 | ||||||

The Adecco Institute was founded in 2006 in London as a centre for research and learning on work-related issues, focused on how changes in the workplace and the workforce will affect individuals, regions and organisations in today’s global economy. | ||||||

The Institute underscores Adecco’s commitment to developing successful partnerships with the business community and understanding the challenges facing our clients and their workforces around the world. Moreover, it reflects our focus on people and, in particular, our goal of delivering improved work prospects and choices for individuals. | ||||||

Through research, conferences and events, the Institute will offer informed perspectives and insights on relevant themes, such as demographic change in the workplace, as well as innovative approaches to help organisations and regions raise employability, productivity and employee satisfaction at work. | ||||||

From governments and academics to employers, unions and employees, the Adecco Institute is committed to facilitating discussions among all stakeholders on the broad topic of work and how work impacts our society. | ||||||

Chaired by Wolfgang Clement, the former German Federal Minister of Economics and Labour (2002–2005), the Adecco Institute brings together the expertise and experiences of leaders from across the corporate world. | ||||||

In October 2006, Peter Siderman was appointed Managing Director of the Adecco Institute, after a decade with McKinsey & Company, where he was most recently global director of mobility, focusing on promoting strategic flows of talent worldwide. | ||||||

The Adecco Institute is just one way in which Adecco is harnessing the inside knowledge of labour markets around the world and developing new approaches to employment. With over 6,700 offices in more than | ||||||

44

Table of Contents

70 countries and territories, and managing a workforce of over four million individuals each year, Adecco’s global employment experience helps the Institute provide innovative research that will benefit the global business community. | ||||||

Demographic Fitness Test | ||||||

In September 2006, the Institute launched its first annual Demographic Fitness Index (DFX), a corporate performance indicator that benchmarks European firms’ readiness for demographic change, particularly workforce ageing. The DFX measures firms across five areas: career, health, knowledge and age diversity management, and lifelong learning. A total of 2,500 companies, of all sizes and sectors from across Europe, participated in the Index, with individual results calculated on a scale of 100 to 400 points. In this year’s DFX, the participating companies averaged just 183 points with two-thirds scoring 200 or less, thus highlighting that European firms have a significant opportunity to improve their preparations for shifts in workforce composition. | ||||||

By benchmarking firms with their corporate peers, the Index provides a strategic planning opportunity for companies to think critically about their future workforce environments. | ||||||

Research initiatives | ||||||

The Institute’s research agenda encompasses a range of important, and inter-related, themes including: | ||||||

– The transition from education to work, and the growing need for career transitions during people’s longer and more dynamic working lives – Regional and global skill shortages, and future skills needs – Public-private partnerships for employment – Flexible employment options, labour regulations, and the staffing industry’s contribution to economic dynamism at both macro and micro levels – International workforce mobility and labour market dynamics in China/India Such initiatives are just some of the ways the Adecco Institute is committed to understanding the challenges and opportunities for companies as they embrace the changing dynamics of their workforces. Through research, dialogue and debate, the Institute is working to develop tools that will help companies translate these changes into business success. | ||||||

45

Table of Contents

Table of Contents

Table of Contents

Adecco shares are listed on the Swiss Exchange (SWX) in Switzerland and on Euronext in France. They are traded on virt-x, an exchange for pan-European blue-chip shares, and on the New York Stock Exchange as American Depositary Receipts (ADRs). | ||||||

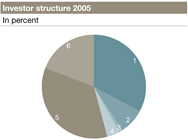

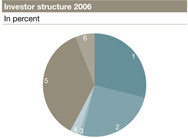

Adecco has a broad investor base of over 15,000 shareholders. At the end of 2006, 55 % of outstanding shares were held by institutional shareholders, representing a 29% increase versus 2005. Most notably, North American institutions increased their holdings threefold to 25% of outstanding shares, while European institutions held 29%. Insider holdings increased slightly to 36 % of all shares. Retail shareholders accounted for 3% of outstanding shares. | ||||||

| Shareholder base | ||||||

| ||||||

| Institutional | |||||||||||

1 | Europe | 33 | % | ||||||||

2 | North America | 8 | % | ||||||||

3 | Rest of world | 1 | % | ||||||||

4 | Retail | 4 | % | ||||||||

5 | Insider | 35 | % | ||||||||

6 | Unassigned | 19 | % |

Daily trading volumes 2006 |

| Symbol | Average volume | |||||||||

Shares | ADEN VX | 1,107,537 shares | ||||||||

Shares | ADE FP | 6,717 shares | ||||||||

ADO US (4 ADRs | ||||||||||

ADR | equal 1 share) | 71,515 ADRs | ||||||||

Source: Bloomberg | ||||||||||

| Institutional | |||||||||||

1 | Europe | 29 | % | ||||||||

2 | North America | 25 | % | ||||||||

3 | Rest of world | 1 | % | ||||||||

4 | Retail | 3 | % | ||||||||

5 | Insider | 36 | % | ||||||||

6 | Unassigned | 6 | % |

48

Table of Contents

Insider holdings | ||||

| % of shares outstanding | ||||

Group represented by | ||||

the Jacobs Holding AG | 29.1 | |||

Akila Finance SA | 5.4 | |||

Treasury shares | 2.1 | |||

Key data | ||||

| 2006 | 2005 | |||

Shares issued | 188,801,167 | 187,607,395 | ||

Treasury shares | 3,964,705 | 1,509,750 | ||

Shares outstanding | 184,836,462 | 186,097,645 | ||

Average number of shares outstanding | 186,343,724 | 186,599,019 | ||

Basic earnings per share in EUR | 3.28 | 2.43 | ||

Diluted earnings per share in EUR | 3.14 | 2.34 | ||

Dividend per share in CHF | 1.201 | 1.00 | ||

Year-end share price in CHF | 83.25 | 60.60 | ||

Highest share price in CHF | 85.15 | 67.80 | ||

Lowest share price in CHF | 62.00 | 54.35 | ||

Year-end market capitalisation in million CHF | 15,388 | 11,278 | ||

Price/earnings ratio2 | 15.8 | 16.0 | ||

Enterprise value3/operating income | 12.4 | 12.5 | ||

ADR | ||||

ADRs outstanding | 15,607,796 | 7,520,804 | ||

Year-end ADR price in USD | 17.13 | 11.54 | ||

Highest ADR price in CHF | 21.36 | 16.99 | ||

Lowest ADR price in CHF | 15.63 | 13.58 | ||

1 Proposed by Board of Directors 2 Based on basic earnings per share and share price at the year end; CHF/EUR per year end 2006: 1.61; 2005: 1.56 3 Equals net debt plus market capitalisation at year end; CHF/EUR per year end 2006: 1.61; 2005: 1.56 | ||||

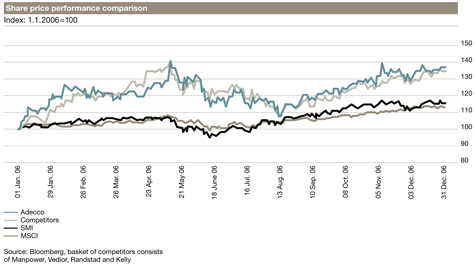

| Performance | ||||||

Adecco shares posted a 37 % increase in 2006, reaching CHF 83.25 on December 29, compared to CHF 60.6 on December 30, 2005. Adecco shares on Euronext and Adecco ADRs in the US were up 34% and 48% respectively. Adecco outperformed the Morgan Stanley Capital Index (MSCI) and the Swiss Market Index (SMI), and was slightly ahead of a basket of its main competitors in the staffing industry. Market capitalisation reached more than CHF 15 billion by the end of 2006, compared to CHF 11 billion a year earlier. |

49

Table of Contents

| ||||||

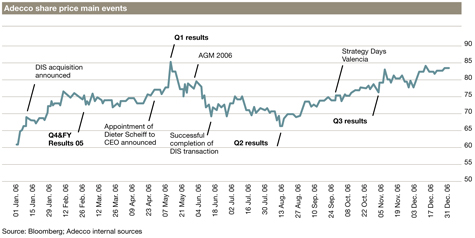

In the first five months of 2006, Adecco’s share price benefited from a positive market reaction to its newly announced strategy and an encouraging global economic outlook. Also the announcement of the intended acquisition of DIS in January was well-received. The Adecco share peaked to the yearly high of CHF 85.15 on May 11. | ||||||

Despite delivering Q2 2006 results in line with market expectations, concerns about the sustainability of economic growth, particularly in the US, led to a more cautious outlook by investors for the second half of the year. The share price dropped 20% before trending steadily upwards again. | ||||||

The outlook remained positive throughout the remainder of 2006. The Adecco Strategy Days in Valencia in late September, combined with strong Q3 results in early November, saw the share price regain significant ground in the last six months of the year. | ||||||

50

Table of Contents

| ||||||

| Investor Relations | ||||||

As part of our ongoing commitment to open and transparent communications with the financial community, Adecco increased its investor relations activities in 2006. A total of 47 days were devoted in 2006 to market communications around our quarterly conference calls, compared to 30 days in 2005. | ||||||

Adecco held more than 240 meetings with analysts and investors in 2006, including conference calls and roadshows to major financial centres including Amsterdam, Boston, Brussels, Chicago, Copenhagen, Denver, Edinburgh, Frankfurt, Liechtenstein, London, Los Angeles, Milan, Munich, New York, Paris, San Francisco, Stockholm, Vienna and Zurich. | ||||||

Adecco’s investor relations team engaged with more than 280 different institutional investors, analysts, portfolio managers and brokers in one-on-one and group meetings, and conferences in 2006. | ||||||

| Coverage | ||||||

The Adecco share story is closely followed by the financial community. In 2006, more than 20 brokers covered Adecco equity including: ABN AMRO, Bank am Bellevue, Bank Sarasin, Bank Vontobel (Lombard Odier Darier Hentsch), Cazenove, Cheuvreux, Citigroup, Credit Suisse, Deutsche Bank, Exane BNP Paribas, Fortis, Goldman Sachs, Helvea, ING, Kepler, Merrill Lynch, Morgan Stanley, Neue Zurcher Bank, Petercam, Sal. Oppenheim, UBS and Zurcher Kantonalbank. | ||||||

51

Table of Contents

Table of Contents

53

Table of Contents

Table of Contents

55

Table of Contents

Corporate Governance

| Company was managed through three divisions: Adecco Staffing, Ajilon Professional, and LHH Career Services. | ||||||

The Company provides services to businesses and organisations located throughout Europe, North America, Asia Pacific, Latin America, and Africa. | ||||||

As of January 1, 2007, the Company’s Executive Committee was composed as follows: | ||||||

– Dieter Scheiff, Chief Executive Officer – Dominik de Daniel, Chief Financial Officer – François Davy, General Manager France (successor of Gilles Quinnez) – Ray Roe, General Manager USA & Canada (until February 28, 2007, succeeded by Theron I (Tig) Gilliam Jr) – René Schuster, General Manager UK & Ireland – Jean-Manuel Bullukian, Head of Global Business Line Adecco Information Technology and Head of Global Business Line Adecco Engineering & Technical – Jim Fredholm, Head of Global Business Line Adecco Finance & Legal (until January 31, 2007, succeeded by Neil Lebovits) – Ekkehard Kuppel, Head of Global Business Line Adecco Human Capital Solutions – Thomas Flatt, Chief Human Resources Officer (until March 31, 2007, succeeded by Christian Vasino) and Head of Global Business Line Adecco Medical & Science (until March 31, 2007) – Jan-Pieter Gommers, Head of Global Business Line Adecco Sales, Marketing & Events – François-Xavier Quilici, Group Chief Information Officer (as of January 8, 2007) – Gonzalo Fernández-Castro, Chief Marketing & Business Development Officer | ||||||

| The Company comprises numerous legal entities around the world. The major consolidated subsidiaries are listed on page 155 of this Annual Report. DIS Deutscher Industrie Service AG (“DIS”), a German subsidiary of the Company with its legal seat in Duesseldorf, is listed on the Frankfurt Stock Exchange (symbol DDE, security number 501690, ISIN DE0005016901). As of December 31, 2006, the market capitalisation of DIS, based on the then issued number of shares and the closing price of shares on the Frankfurt Stock Exchange, amounted to approximately EUR 1 billion. On March 9, 2007, this market capitalisation amounted to approximately EUR 1.2 billion. Adecco owns directly and indirectly approximately 84% of DIS. No other subsidiary is listed on a stock exchange; however, certain subsidiaries have issued convertible notes, as described further in this section. | ||||||

| 1.2 Significant shareholders | ||||||

As of December 31, 2006, the total number of shareholders directly registered with Adecco S.A. was 15,263. The major shareholders and their shareholdings were disclosed as follows (for all disclosures see http://www.swx.com; please note that percentages of shareholdings refer to the date of disclosure unless indicated otherwise): | ||||||

In 2005, the following shareholdings were disclosed to the Company and no changes with respect to these shareholdings have been disclosed under the SWX Swiss Stock Exchange reporting obligations in 2006 (the indicated shareholdings of the below mentioned Group and Akila Finance S.A. reflect the exercise of option during 2006): – 54,904,180 shares, as of December 31, 2006, representing 29.1% of the total Adecco S.A. issued share capital, were held by a group consisting of Jacobs Holding AG (formerly KJ Jacobs AG), Zurich, Switzerland, Jacobs Venture AG, Baar, Switzerland, Triventura AG, Baar, Switzerland, Klaus J. Jacobs, Renata I. Jacobs, Lavinia Jacobs, Nicolas Jacobs, Philippe Jacobs, and Nathalie Jacobs (“the Group”), amongst others agreeing on financing issues and voting. Jacobs Holding AG represents the Group and does not hold any shares outside the Group. Jacobs Holding AG’s own shares and participation certificates are held by Jacobs Foundation and by the association Jacobs Familienrat (both Zurich, Switzerland). For further details, see the disclosure as published in the “Swiss Official Gazette of Commerce” (SHAB No. 245, December 16, 2005). | ||||||

– 10,188,580 shares, as of December 31, 2006, representing 5.4% of the total Adecco S.A. issued share capital, were held by Akila Finance S.A., Luxembourg, which is owned and controlled by Philippe Foriel-Destezet. For further details, see the disclosure as published in the “Swiss Official Gazette of Commerce” (SHAB No. 245, December 16, 2005). | ||||||

– Sonata Securities S.A., Luxembourg, (“Sonata”), on December 29, 2005, disclosed that (1) Sonata has the right to exchange the notes owned by it for up to 10,294,665 shares (5.5%) during the term of the notes and (2) that Deutsche Bank AG has the right – in certain | ||||||

56

Table of Contents

Corporate Governance

| circumstances and subject to additional legal requirements relating to the enforcement of security interests – to deliver to Sonata up to 32,170,829 shares (17.2%) in satisfaction of Deutsche Bank AG’s obligations under the notes. Deutsche Bank AG would only be in a position to exercise their right if there is an event of default under the bilateral equity linked contract between Jacobs Venture AG and Deutsche Bank AG dated as of December 6, 2005. Sonata intended to issue on December 30, 2005 CHF 767,300,000 1.5 percent collateralised equity linked limited liability obligations bonds due 2010 exchangeable for ordinary shares of Adecco S.A. The proceeds of the issuance of the bonds will be used to acquire the notes. These bonds have been issued before December 31, 2005. In 2006, no changes in the holding of Sonata were disclosed to Adecco S.A. For further details see the disclosure of Sonata as published in the “Swiss Official Gazette of Commerce” (SHAB No. 7, January 11, 2006). | ||||||