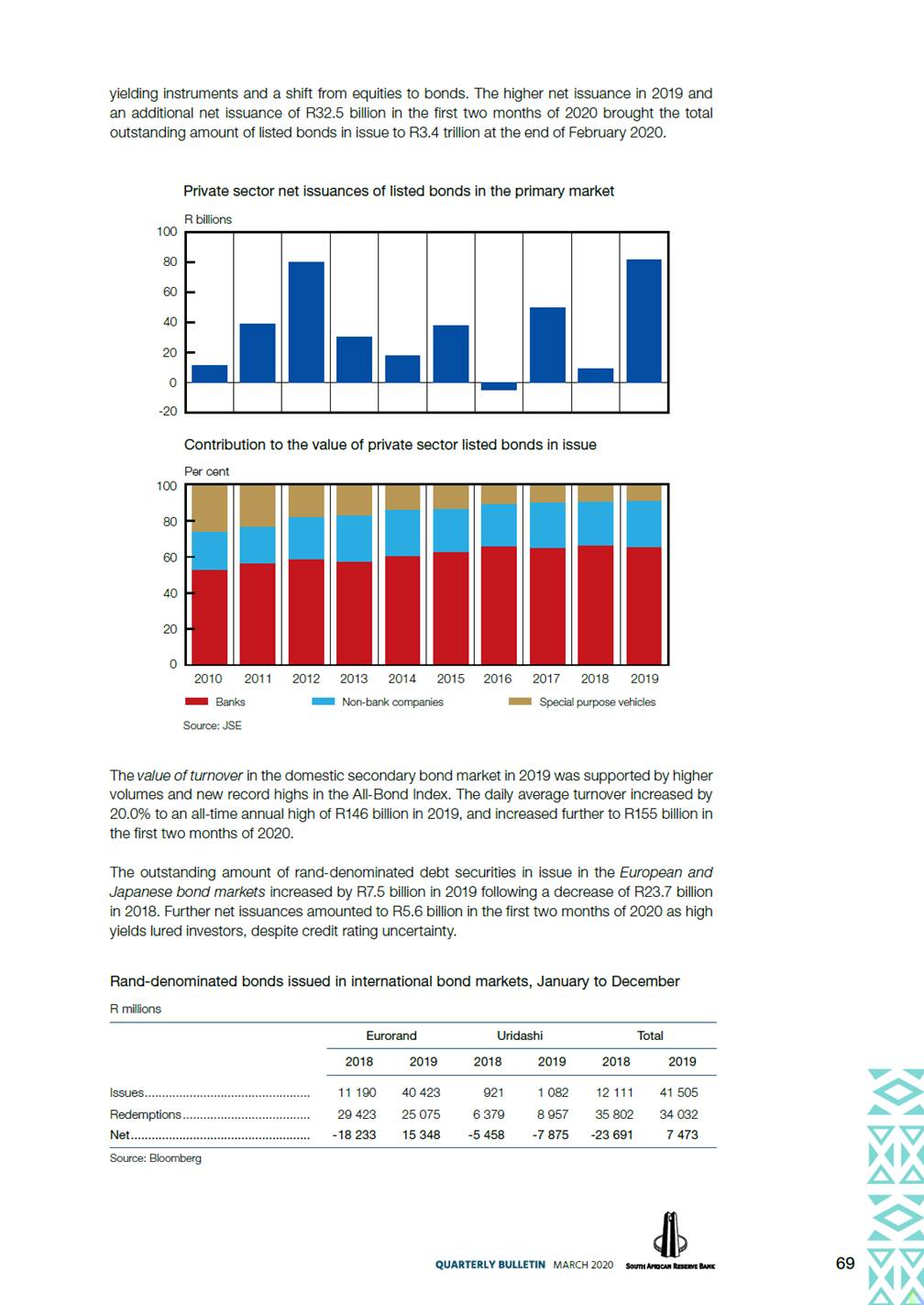

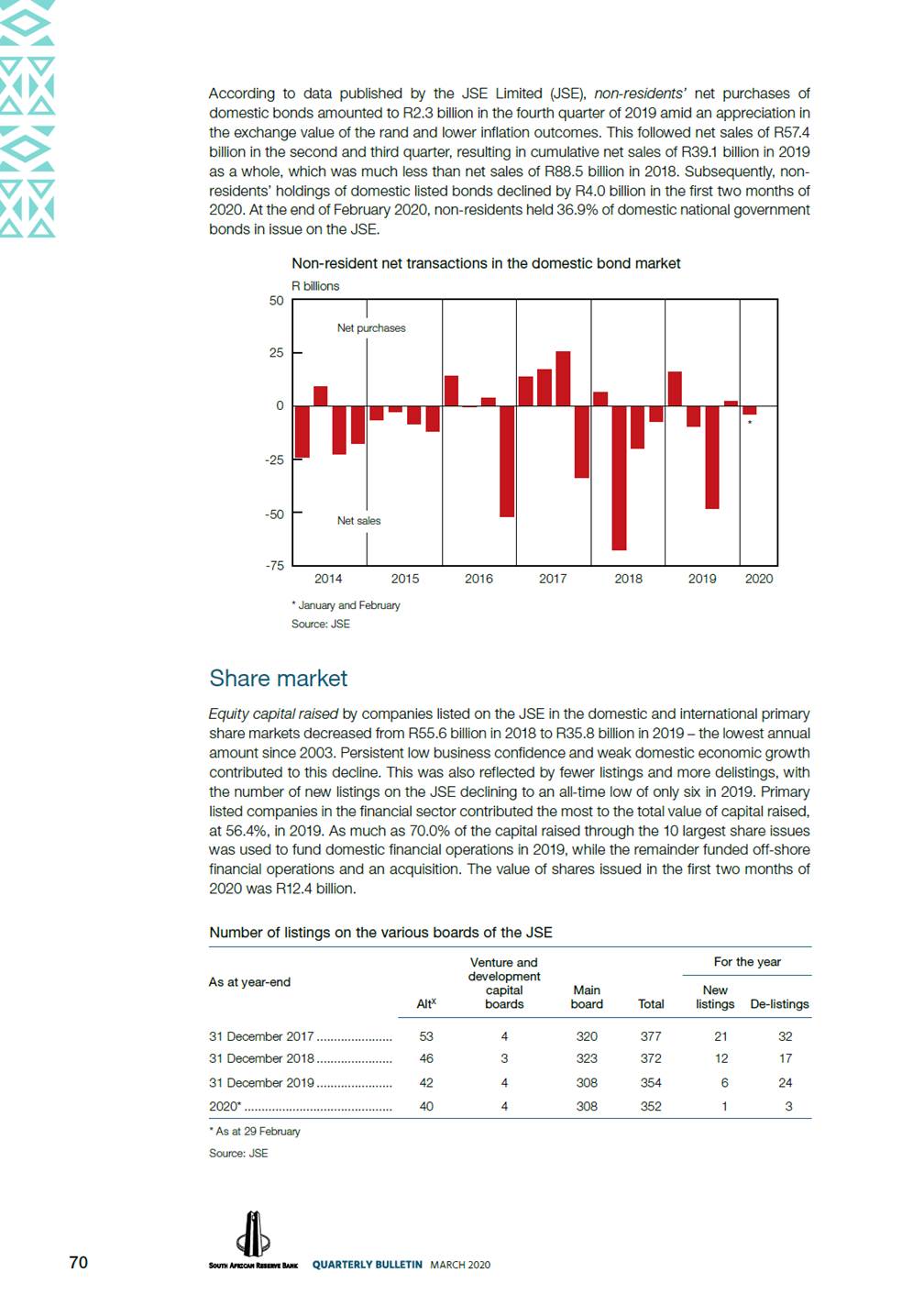

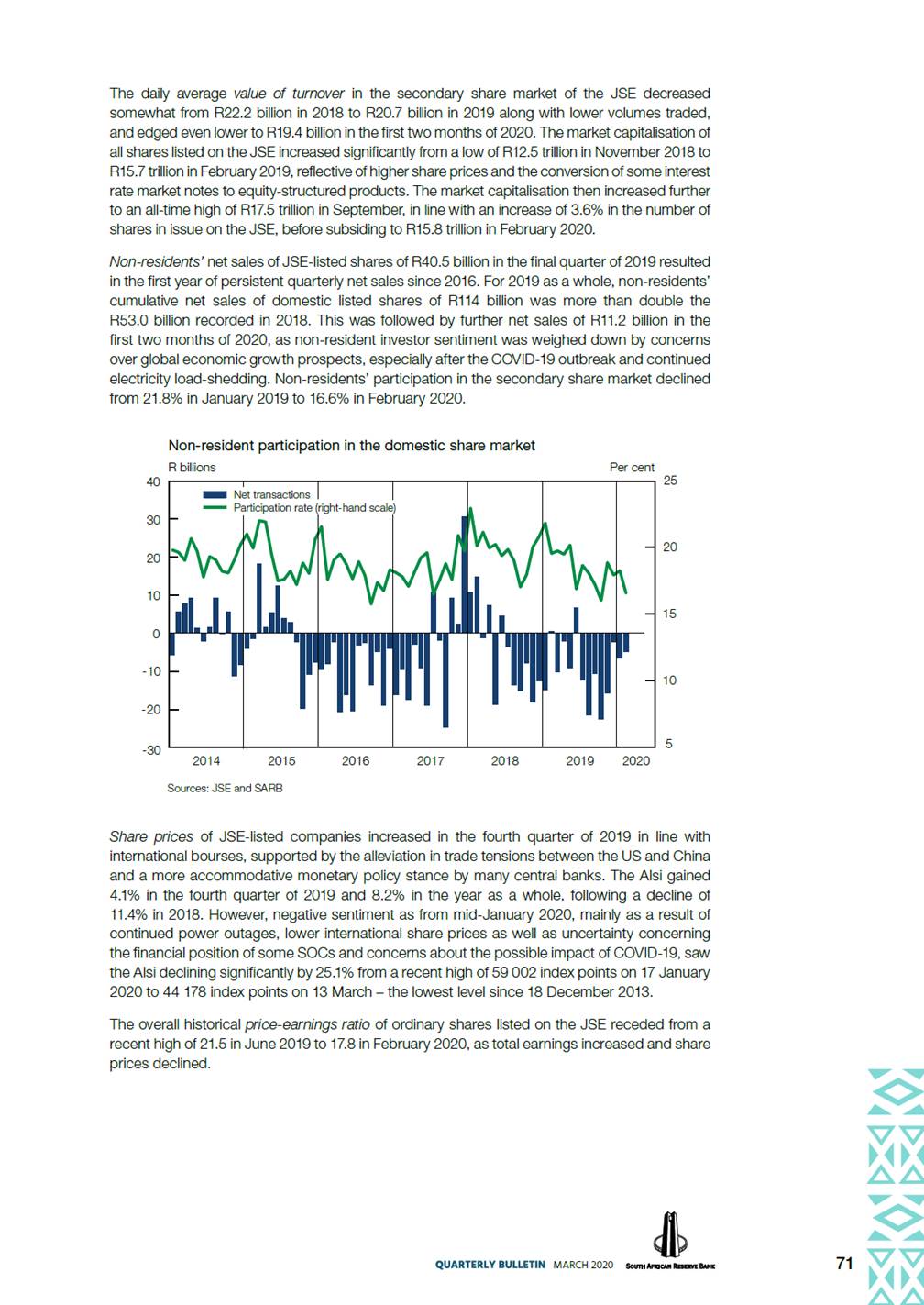

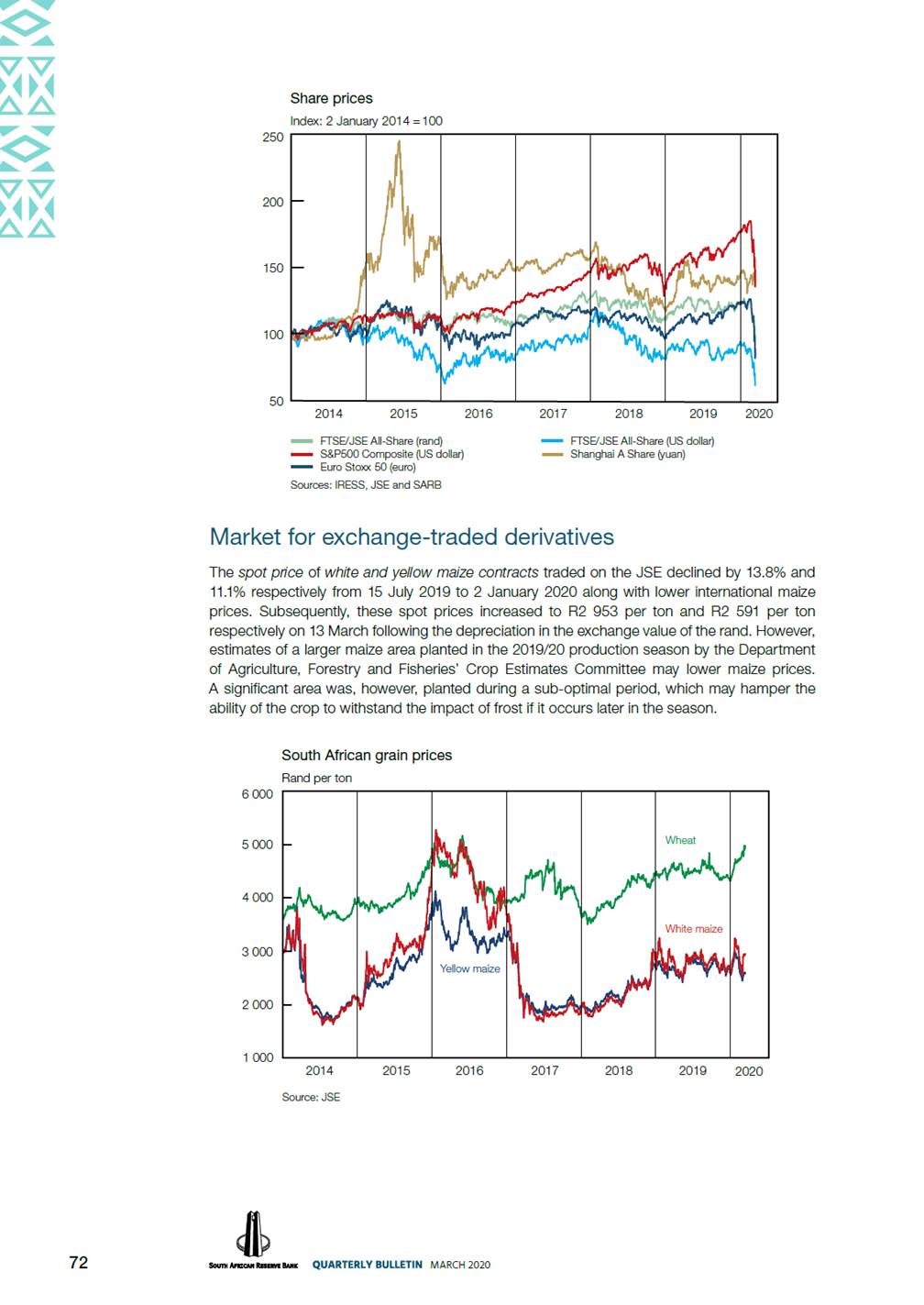

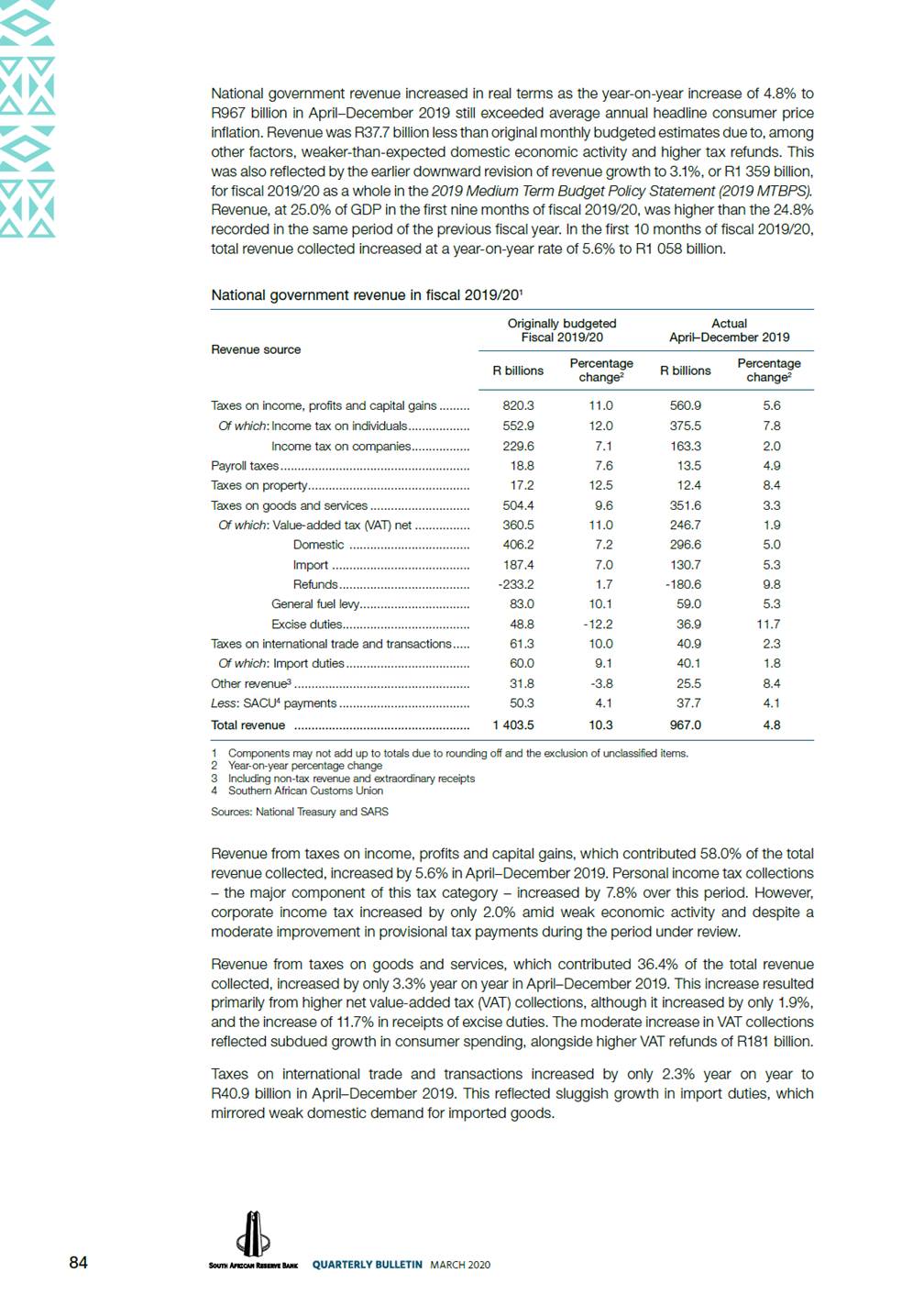

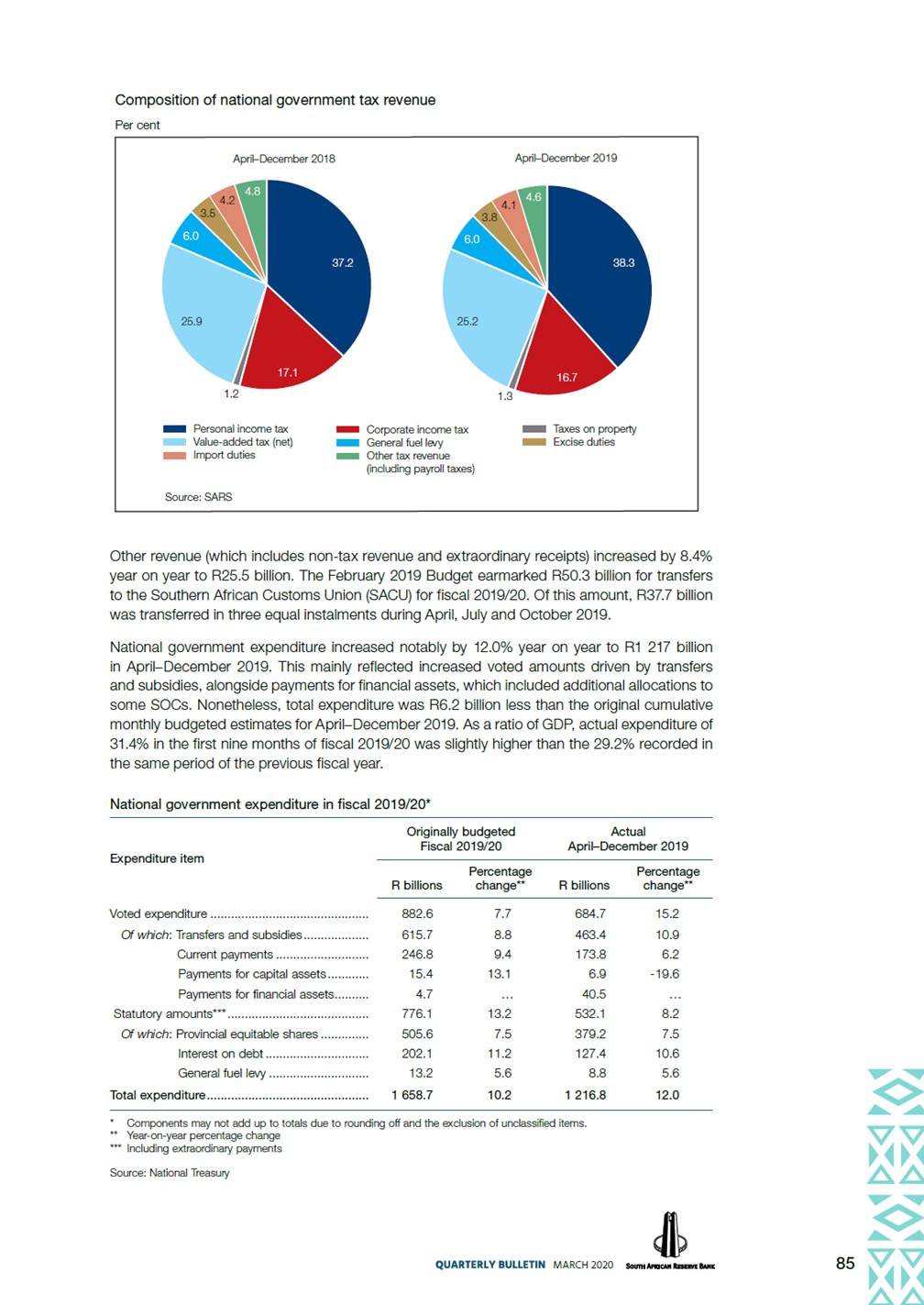

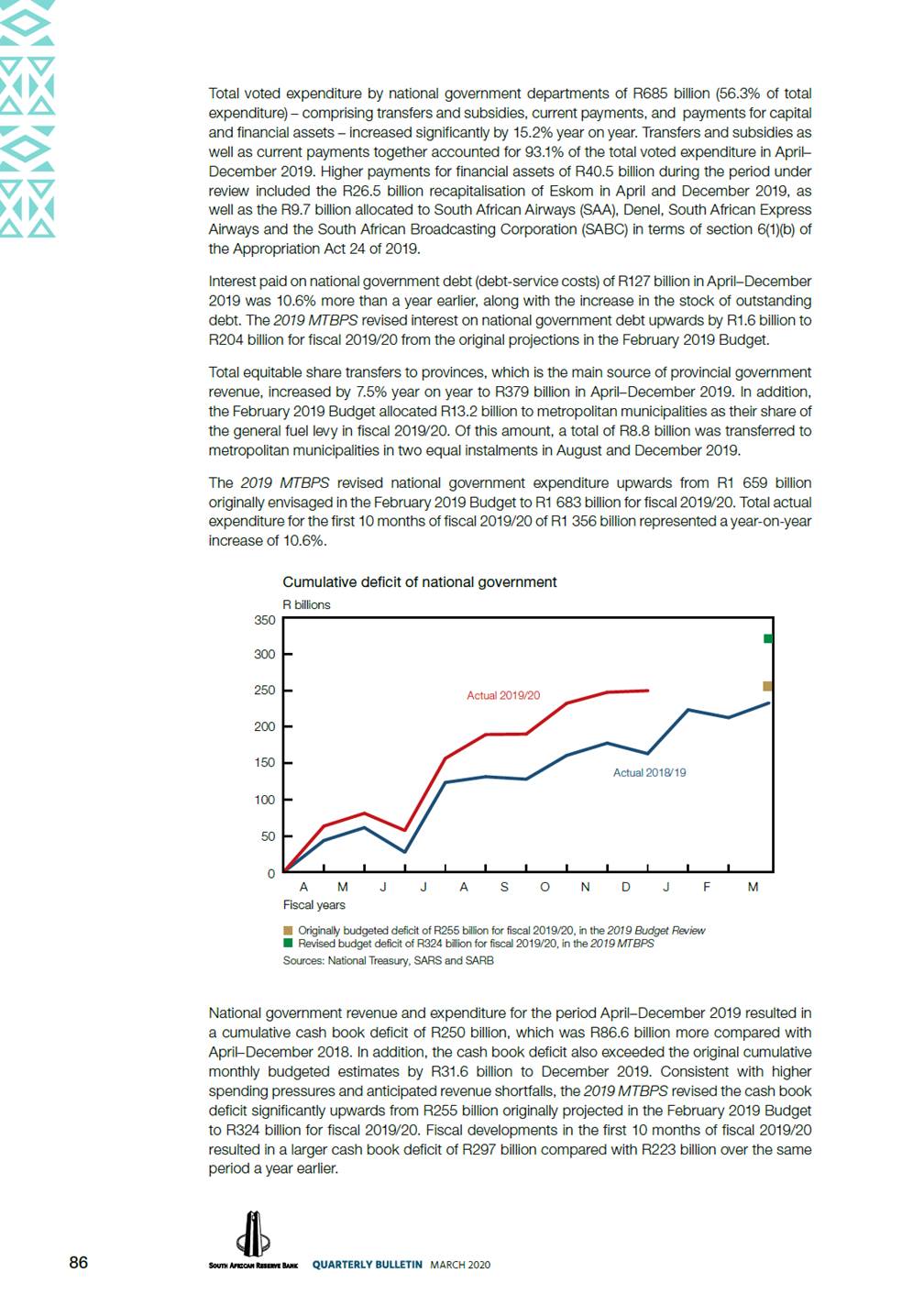

© South African Reserve Bank All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without fully acknowledging the Quarterly Bulletin of the South African Reserve Bank as the source. The contents of this publication are intended for general information only and are not intended to serve as financial or other advice. While every precaution is taken to ensure the accuracy of information, the South African Reserve Bank shall not be liable to any person for inaccurate information or opinions contained in this publication. Enquiries relating to this Bulletin should be addressed to: Head: Economic Statistics Department South African Reserve Bank P O Box 427 Pretoria 0001 Tel. +27 12 313 3668/3676 http://www.resbank.co.za ISSN 0038-2620 Android IOS Windows Printed by Publishing Section of South African Reserve Bank MARCH 2020

Contents Quarterly Economic Review Introduction ............................................................................................................................... Global economic developments ................................................................................................ Domestic economic developments ........................................................................................... Domestic output ............................................................................................................... Real gross domestic expenditure ...................................................................................... Gross nominal saving ........................................................................................................ Employment ...................................................................................................................... Labour cost and productivity ............................................................................................ Prices ................................................................................................................................ External economic accounts ..................................................................................................... Current account ................................................................................................................ Financial account .............................................................................................................. Foreign-owned assets in South Africa ............................................................................... South African-owned assets abroad ................................................................................. Foreign debt...................................................................................................................... International investment position ....................................................................................... International reserves and liquidity .................................................................................... Exchange rates ................................................................................................................. Turnover in the South African foreign exchange market..................................................... Monetary developments, interest rates and financial markets ................................................... Money supply.................................................................................................................... Credit extension ................................................................................................................ Interest rates and yields .................................................................................................... Money market ................................................................................................................... Bond market ..................................................................................................................... Share market..................................................................................................................... Market for exchange-traded derivatives ............................................................................ Non-bank financial intermediaries ..................................................................................... Flow of funds..................................................................................................................... Public finance............................................................................................................................ Non-financial public sector borrowing requirement ........................................................... Budget comparable analysis of national government finance ............................................ 1 4 7 7 13 25 28 32 33 41 41 46 47 48 49 50 51 52 54 56 56 58 62 66 68 70 72 76 77 79 79 83 Boxes Box 1 Box 2 Household wage and income statistics......................................................................... The link between the deficit and surplus funding positions of domestic institutional sectors and the rest of the world .................................................................................. Introducing collateral substitution for repurchase auctions ........................................... Unpacking the drivers of residential property prices ..................................................... The 2020 Budget Review.............................................................................................. 18 26 66 73 80 Box 3 Box 4 Box 5 Notes to tables ......................................................................................................................... 90 Abbreviations ........................................................................................................................... 91 Statistical tables Contents ..................................................................................................................................... S–0 Statistical tables .......................................................................................................................... S–2 Key information ....................................................................................................................... S–148 MARCH 2020

[LOGO]

Quarterly Economic Review Introduction Global economic growth slowed further to 2.5% in the fourth quarter of 2019 as output growth decelerated sharply in the advanced economies and moderated in emerging markets. The annual expansion of 3.0% in the world economy in 2019 was the weakest since the 2007–08 global financial crisis. With the exception of the United States (US), growth in most advanced economies slowed significantly in the fourth quarter. Latin America and emerging Europe led the moderation in emerging markets, which was contrasted by a slight acceleration in China and India. World trade volumes contracted for the seventh consecutive month in December 2019, particularly in emerging markets, as trade tensions continued to weigh on sentiment. Global inflation remained muted throughout 2019. In the fourth quarter of 2019, a further decline in the international prices of metals and minerals contrasted a modest increase in that of agricultural products and energy. The price of Brent crude oil initially rose to a recent high of US$69 per barrel in early January 2020 amid optimism that a US–China trade deal would boost global economic growth prospects. In mid-February, however, oil prices decreased sharply due to concerns that the outbreak of the coronavirus disease 2019 (COVID-19) would weaken global demand. Oil prices declined further in early March as the virus spread to several countries. With Russia not cutting production in line with the Organization of the Petroleum Exporting Countries (OPEC), and Saudi Arabia then announcing an increase in production, oil prices fell significantly to around US$31 per barrel in mid-March. These developments contributed to a significant change in investors’ risk appetite, with global equity and bond prices falling sharply in the first two weeks of March. The South African economy entered a second technical recession since the first quarter of 2018, with real gross domestic product (GDP) contracting by a further 1.4% in the fourth quarter of 2019 following a revised contraction of 0.8% in the third quarter. The weakness in economic activity in the fourth quarter was broad-based, with output contracting in the primary, secondary and tertiary sectors. Annual output growth slowed further from 0.8% in 2018 to only 0.2% in 2019 – the lowest growth rate since the sharp contraction in 2009 following the global financial crisis. The faster pace of contraction in the real output of the agricultural sector was the main driver of the decrease in the real gross value added (GVA) by the primary sector in the fourth quarter of 2019 as mining output increased somewhat. On an annual basis, both agricultural and mining output contracted for a second successive year in 2019. Encouragingly, expectations of a much larger domestic maize crop could support agricultural output in 2020. The real GVA by the secondary sector decreased further in the fourth quarter of 2019 as output contracted in all the subsectors. The renewed implementation of load-shedding, and the intensity thereof, weighed on electricity production and also adversely affected manufacturing output in addition to continued weak demand. The real output of the construction sector, which decreased for a sixth successive quarter in the fourth quarter of 2019 and for a third consecutive year, reflected subdued fixed investment amid persistent low business confidence and sluggish economic activity. The real output of the tertiary sector reverted from an increase in the third quarter of 2019 to a decrease in the fourth quarter. Despite fairly strong Black Friday sales, which boosted retail trade in the fourth quarter, declines in wholesale and motor trade resulted in a contraction in the real GVA by the commerce sector. The output of the transport, storage and communication sector contracted notably further in the fourth quarter of 2019, consistent with the decline in import volumes. By contrast, growth in real economic activity in the finance, insurance, real estate and business services sector accelerated. Real gross domestic expenditure (GDE) decreased by a further 4.6% in the fourth quarter of 2019 following a similar decrease in the third quarter. Both real gross fixed capital formation and real final consumption expenditure by general government reverted from increases to contractions, alongside a much faster pace of real inventory de-accumulation. Real net exports contributed the most to growth in real GDP in the fourth quarter of 2019, but were offset by the run-down of inventories. Growth in real final consumption expenditure by households accelerated somewhat in the fourth quarter of 2019, supported by faster growth in real disposable income. Real spending on services, non-durable goods and, in particular, semi-durable goods increased at a faster pace, boosted by 1 MARCH 2020

strong Black Friday promotion sales. By contrast, households purchased less durable goods in the fourth quarter, as consumer confidence and wage growth remained weak. Household debt increased at a faster pace than disposable income in the fourth quarter of 2019, with the ratio of debt to disposable income rising slightly to 73.0%. However, households’ net wealth still increased as the value of equity portfolios and housing stock increased at a faster pace than the increase in household debt. Equity holdings were boosted by an increase of 4.1% in the FTSE/JSE All-Share Price Index (Alsi) in the fourth quarter of 2019, which was in line with international bourses. Real gross fixed capital formation contracted sharply in the fourth quarter of 2019, following two consecutive quarters of expansion. Private business enterprises, public corporations and general government all reduced capital outlays in the fourth quarter. On an annual basis, real capital expenditure decreased for a second successive year in 2019, affected by persistent low business confidence, sluggish real economic activity and the further deterioration in the fiscal position. Consequently, the ratio of nominal fixed capital formation to nominal GDP declined further to 17.9% in 2019 – the lowest since 2005. South Africa’s official unemployment rate remained unchanged at a record-high of 29.1% in the fourth quarter of 2019, with the seasonally adjusted unemployment rate increasing to a new all-time high of 29.6%. Contrary to the usual sharp seasonal decrease in unemployment in the fourth quarter of each year, the number of unemployed people remained fairly elevated in the fourth quarter of 2019 due to a significant number of new entrants in search of employment. The downward trend in wage growth continued as the pace of increase in the nominal remuneration per worker in the formal non-agricultural sector decelerated notably to an all-time low year-on-year rate of 3.0% in the third quarter of 2019, with both public and private sector remuneration growth slowing. The deceleration in public sector remuneration growth was exacerbated by the high base following the delayed implementation of the annual public sector wage increase in 2018. In addition, the average wage settlement rate in collective bargaining agreements decreased further to a 12-year low of 6.7% in 2019. The moderation in wage growth resulted in a deceleration in the growth of formal non-agricultural nominal unit labour cost to 3.4% in the third quarter of 2019. In line with the muted growth in unit labour cost and subdued demand pressures in the domestic economy, both producer and consumer price inflation slowed significantly throughout 2019. The moderation in domestic inflationary pressures was driven by a marked deceleration in fuel price inflation, muted food price increases and a renewed slowdown in underlying inflation. Core inflation slowed to 3.7% in January 2020, driven largely by the deceleration in consumer services price inflation to a record-low of 4.0%. Consumer goods price inflation accelerated somewhat in December 2019 and January 2020 as fuel price inflation quickened notably, largely due to base effects. South Africa’s trade surplus with the rest of the world more than doubled from the third to the fourth quarter of 2019 as the value of merchandise imports decreased further, while that of net gold and merchandise exports increased further. The value of merchandise exports was boosted by mining exports, in particular of platinum group metals (PGMs) as well as pearls and semi-precious stones. The value of PGM exports benefitted from higher prices, especially palladium and rhodium. Despite a notable increase in the value of crude oil imports in the fourth quarter of 2019, lower volumes of manufacturing imports reduced the total value of merchandise imports. The deficit on the services, income and current transfer account narrowed markedly from the third to the fourth quarter of 2019, mainly due to a notably smaller deficit on the income account as gross dividend payments receded from an exceptionally high level in the third quarter. This, together with the larger trade surplus, resulted in a significant narrowing in the deficit on the current account of the balance of payments as a ratio of GDP from 3.7% in the third quarter of 2019 to 1.3% in the fourth quarter – the smallest deficit since the fourth quarter of 2010. The net inflow of capital on the financial account of the balance of payments decreased sharply from R73.9 billion in the third quarter of 2019 to R10.1 billion in the fourth quarter. On a net basis, portfolio investment, financial derivatives and reserve assets recorded inflows, while direct and other investment recorded outflows. South Africa’s positive net international investment position decreased further from the end of June 2019 to the end of September as the value of foreign assets decreased more than that of foreign liabilities. Both foreign assets and liabilities declined as a result of the restructuring of a large South 2 MARCH 2020

African company. In addition, the decrease in the nominal effective exchange rate (NEER) of the rand over the period affected foreign assets more than foreign liabilities. Following its decrease in the third quarter of 2019, the NEER increased by 6.1% in the fourth quarter and outperformed many other emerging market currencies. This reflected notable increases in November and December 2019, attributable to the increased risk appetite of global investors following some relief from geopolitical tensions and an interest rate cut by the US Federal Reserve. However, in January and February 2020, the exchange value of the rand depreciated notably due to, among other factors, renewed downward revisions to South Africa’s economic growth projections, continued electricity-supply interruptions and a further deterioration in the fiscal position. In addition, the COVID-19 outbreak in China resulted in increased risk aversion and capital flows to safe-haven assets. In the first two weeks of March 2020, the exchange value of the rand depreciated further as the rapid spread of the virus disrupted global supply chains and sparked fears of a possible global recession. Yields on South African government bonds increased from mid-July 2019 up to early December, initially reflecting heightened global risk aversion due to the ongoing US–China trade tensions, and later also government’s recapitalisation of some state-owned companies (SOCs), in particular Eskom, as well as the larger government budget deficit and increased debt levels projected in the October 2019 Medium Term Budget Policy Statement (2019 MTBPS). Domestic bond yields then declined up to the end of February 2020, along with lower international yields and optimism over a US-China trade deal as well as notable non-resident net purchases of domestic bonds. However, bond yields increased markedly again in the first two weeks of March as a result of the expected impact of the COVID-19 outbreak on global economic activity and the related domestic currency weakness, as well as higher domestic inflation outcomes and higher debt-to-GDP levels projected in the February 2020 Budget. Domestic short-term money market interest rates trended moderately higher in late 2019, but quickly adjusted lower following the 25 basis point reduction in the repurchase (repo) rate in January 2020. Rates on forward rate agreements (FRAs) had already started to trend lower from late 2019 following the earlier appreciation in the exchange value of the rand and favourable inflation outcomes. FRA rates declined further in March 2020 as market participants started discounting the possibility of even lower interest rates due to the negative implications of COVID-19 for global and domestic economic growth, and following policy rate reductions by a number of major central banks. Growth in the broadly defined money supply (M3) decelerated in both the third and fourth quarter of 2019, in line with weak domestic economic activity. A significant slowdown in corporate sector deposit growth in the second half of 2019 drove the overall moderation in M3, while household deposit growth fluctuated marginally higher. Growth in total loans and advances extended by monetary institutions to the domestic private sector decelerated in the nine months up to January 2020. Similar to the slowdown in M3, the moderation in credit extension was also led by companies, while growth in credit to households continued at a fairly sturdy pace. Credit extension to the household sector was driven by steady growth in mortgage advances and fairly lively growth in general loans. The moderation in corporate credit growth in the fourth quarter of 2019 resulted mainly from a slowdown in loans to non-financial companies. The preliminary non-financial public sector borrowing requirement increased by R70.8 billion year on year in the first nine months of fiscal 2019/20, as the cash book deficit of national government increased markedly. The larger borrowing requirement resulted from the fairly buoyant growth in national government expenditure which continued to outpace the modest growth in revenue. The revenue shortfall reflected continued weaker-than-expected domestic economic activity and higher tax refunds. Higher debt-service costs and, in particular, the recapitalisation of some SOCs boosted government spending. National government’s total gross loan debt increased significantly to 62.2% of GDP as at 31 December 2019, from 56.7% of GDP a year earlier. In the interest of fiscal consolidation and sustainability, the February 2020 Budget proposed a reduction in government expenditure, partly through a decrease in the public sector wage bill as well as the reform of SOCs, despite additional support to some SOCs. On the revenue side, taxes were not increased as in recent years due to the weak economic environment and expected low future growth. The consolidated budget deficit is expected to widen from 6.3% of GDP in fiscal 2019/20 to 6.8% in fiscal 2020/21, before narrowing to 5.7% in fiscal 2022/23. The budget projected a debt-to-GDP ratio of 61.6% at the end of fiscal 2019/20, which is expected to increase to 71.6% at the end of fiscal 2022/23. 3 MARCH 2020

Global economic developments Global economic growth slowed to 2.5% in the fourth quarter of 2019 from an annualised real rate of 3.1% in the third quarter, and to an annual average of 3.0% in 2019 – the weakest pace of economic expansion since the 2007–08 global financial crisis. The slowdown in the fourth quarter reflected a sharp deceleration in the real economic growth momentum of advanced economies and a moderation in emerging markets. Real global output growth and contributions from advanced and emerging market economies Percentage points Percentage change from quarter to quarter 5 5 4 4 3 3 2 2 1 1 0 0 2014 2015 2016 2017 2018 2019 Seasonally adjusted annualised rates Sources: Barclays, Bloomberg, Haver Analytics, IMF, JPMorgan and SARB Most advanced economies, with the exception of the United States (US), recorded weaker economic growth in the fourth quarter of 2019. Real output growth in the US stabilised at 2.1% in the fourth quarter, supported by personal consumption expenditure and government spending. In addition, the sharp decline in imports by the US, partly due to higher tariffs on Chinese goods, contributed 1.3 percentage points to overall growth. Real output growth in selected advanced economies Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Country/region Q1 Q2 Q3 Q4 Year* Q1 Q2 Q3 Q4 Year* United States................. Japan ............................ Euro area....................... United Kingdom ............ Canada ......................... Australia ........................ New Zealand ................. Advanced economies... 2.6 -1.9 1.1 0.2 2.2 3.7 3.0 1.7 3.5 2.0 1.4 2.1 1.6 3.0 3.8 2.4 2.9 -3.3 0.8 2.4 2.5 1.4 2.3 1.4 1.1 2.4 1.6 0.9 1.0 0.7 4.1 1.6 2.9 0.3 1.9 1.3 2.0 2.7 2.8 2.2 3.1 2.2 1.8 2.6 1.0 2.0 1.8 2.3 2.0 2.3 0.6 -0.4 3.4 2.4 0.1 1.6 2.1 0.1 1.2 2.0 1.1 2.2 3.2 1.5 2.1 -7.1 0.5 0.1 0.3 2.1 2.1 0.7 2.3 0.7 1.2 1.4 1.6 1.8 2.2 1.7 * Percentage change over one year Underlined numbers indicate projections. Sources: Bloomberg, Haver Analytics, IMF, JPMorgan and SARB 4 MARCH 2020 Advanced economies Emerging market economies Global growth (right-hand scale)

By contrast, the Japanese economy contracted by 7.1% in the fourth quarter of 2019 following a moderate expansion of 0.1% in the third quarter. The contraction was largely due to front-loaded purchases in the third quarter in anticipation of an increase in consumption tax that came into effect during the fourth quarter. The decline in private investment, which contributed further to the fourth-quarter contraction, was partly offset by the positive contribution of lower imports. Real output growth in the euro area slowed to only 0.5% in the fourth quarter of 2019, from 1.2% in the previous quarter. The deceleration affected the region’s largest economies, namely Germany, France and Italy. In Germany, real gross domestic product (GDP) stagnated in the fourth quarter, following growth of 0.8% in the third quarter, as both manufacturing output and exports suffered from weakness in the automobile industry. Meanwhile, real economic activity in both France and Italy unexpectedly contracted during the fourth quarter by 0.2% and 1.2% respectively. Real GDP growth in the United Kingdom almost came to a halt at 0.1% in the fourth quarter of 2019, following a sharp acceleration in the third quarter. This reversal was mainly attributable to deteriorating sentiment related to Brexit, which weighed heavily on household consumption expenditure and investment spending during the quarter. Real economic growth in emerging markets decelerated modestly from 4.5% in the third quarter of 2019 to 4.2% in the fourth quarter. The slowdown reflected a deceleration in emerging Europe, especially Russia, where real output growth is expected to slow markedly to 1.8% in the fourth quarter, from 5.1% in the previous quarter. In Latin America, real GDP declined by 0.5% in the fourth quarter due to sharp contractions in several countries, especially in Argentina and Chile, where output declined by 3.6% and 15.5% respectively. Real economic activity in Chile was impacted by growing social unrest in the fourth quarter. By contrast, real output growth accelerated in emerging Asia, particularly in China and India, where growth quickened in the fourth quarter, to 6.0% and 4.9% respectively. Real output growth in selected emerging market economies Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Country/region Q1 Q2 Q3 Q4 Year* Q1 Q2 Q3 Q4 Year* China........................... India ............................ Indonesia..................... Emerging Asia ............ Russia ......................... Turkey ......................... Poland......................... Emerging Europe........ Brazil ........................... Mexico ........................ Argentina ..................... Latin America ............. 6.8 1.9 4.7 5.4 6.7 4.8 5.3 5.7 2.6 5.4 -0.1 3.3 7.1 7.0 5.8 6.7 3.3 0.0 5.3 2.9 0.1 -1.0 -18.5 -1.1 6.4 6.9 4.9 6.1 1.3 -4.8 5.3 0.7 2.2 1.2 -0.9 1.1 5.9 6.5 5.3 6.0 0.4 -10.8 2.8 -2.0 0.1 0.3 -4.8 0.4 6.7 6.1 5.2 6.3 2.5 2.8 5.1 3.2 1.3 2.1 -2.5 1.8 6.2 1.8 4.4 4.8 -2.8 8.1 5.7 2.1 0.0 -0.5 -0.2 0.0 6.0 7.7 5.7 6.2 4.4 4.6 2.8 4.2 2.1 -0.4 -2.9 1.4 5.8 4.4 4.8 5.2 5.1 3.1 4.9 4.3 2.5 -0.3 3.8 1.9 6.0 4.9 5.1 5.4 1.8 8.0 1.2 3.7 2.0 -0.5 -3.6 -0.5 6.1 5.0 5.0 5.6 1.3 0.3 4.1 2.0 1.1 -0.1 -2.2 0.8 Emerging economies.. 5.0 5.0 4.6 4.0 4.6 3.6 5.2 4.5 4.2 3.9 * Percentage change over one year Underlined numbers indicate projections. Sources: Barclays, Bloomberg, Haver Analytics, IMF, JPMorgan and SARB 5 MARCH 2020

Global inflation remained muted in the fourth quarter of 2019. In advanced economies, headline consumer price inflation continued to undershoot most central banks’ inflation targets. Inflationary pressures in emerging markets also remained well contained, with the exception of a few countries such as Argentina and Turkey. World trade volumes (using exports as a proxy) declined for the seventh consecutive month in December 2019, at a year-on-year rate (three-month moving average) of 0.5%, as trade tensions continued to weigh on sentiment. Declines in trade volumes were especially pronounced in emerging markets where export volumes contracted by 1.2% over this period, mainly due to lower exports from Africa and the Middle East as well as Latin America and emerging Asia (excluding China). Meanwhile, exports from advanced economies stabilised in December as lower exports from the US, Japan and the euro area were offset by higher exports from other advanced economies. The international prices of agricultural products and energy rose modestly in the fourth quarter of 2019, while the prices of metals and minerals declined further. The price of Brent crude oil rose from around US$58 per barrel in the beginning of October 2019 to a high of US$69 per barrel in early January 2020 amid optimism that a US–China trade deal would boost global economic growth prospects. In mid-February, oil prices decreased sharply to US$53 per barrel due to concerns that the outbreak of the coronavirus disease 2019 (COVID-19) would reduce world growth prospects. Oil prices declined further in early March as the virus spread to several countries across the world. The Organization of the Petroleum Exporting Countries (OPEC) subsequently decided to cut production. Russia, however, refused to join OPEC’s production cut and oil prices initially dropped by 10%. Saudi Arabia then announced that it would boost production and oil prices declined further by almost 30% to US$31 per barrel in mid-March. International commodity prices in US dollars Index: 2010 = 100 150 130 110 90 70 50 30 2013 2014 2015 2016 2017 2018 2019 Sources: World Bank and SARB The international prices of agricultural products, in US dollar terms, increased firmly by 4.4% in the fourth quarter of 2019 amid higher soybean and wheat prices. Metals and minerals prices decreased by 1.8% over the same period, due to pronounced declines in nickel and tin prices. 6 MARCH 2020 Agriculture Metals and minerals Energy

Domestic economic developments Domestic output1, 2 The South African economy entered a technical recession as real gross domestic product (GDP) contracted further at an annualised rate of 1.4% in the fourth quarter of 2019, following a contraction of 0.8% in the third quarter. This is the second time that output has contracted for two successive quarters since the first quarter of 2018. Economic activity decreased in the primary, secondary and tertiary sectors in the fourth quarter of 2019. 1The quarter-to-quarter growth rates referred to in this section are based on seasonally adjusted data and are annualised. 2The analysis in this section of the review is based on a revised set of national accounts estimates for 2019. These revisions are based on more detailed or more appropriate data that have become available. Real gross domestic product Percentage change from quarter to quarter 6 5 4 3 2 1 0 -1 -2 -3 -4 Real gross value added by main sectors Index: first quarter of 2014 = 100 110 108 106 104 102 100 98 96 94 Tertiary Secondary 2014 Source: Stats SA 2015 2016 2017 2018 2019 When excluding the contribution of the generally more weather-reliant agricultural sector, the non-agricultural sector contracted by a lesser 1.1% in the fourth quarter of 2019. Annual output growth slowed significantly from a high of 3.3% in 2011 to only 0.2% in 2019 – the lowest growth rate since the sharp contraction in 2009 following the global financial crisis. Annual growth in real GDP only averaged 1.0% in the current downward phase of the business cycle compared with 2.8% during the previous short upward phase. The further moderation in annual real GDP growth in 2019 reflected a contraction in output in all but the second quarter, and in both the primary and the secondary sectors along with a slowdown in the tertiary sector. 7 MARCH 2020 Primary Seasonally adjusted Total Non-agricultural Seasonally adjusted and annualised

Real gross domestic product Percentage change over one year 6 5 4 3 2 1 0 -1 Average: upward phase -2 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 Downward phases of the business cycle Sources: Stats SA and SARB Real gross domestic product Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Sector Q1 Q2 Q3 Q4 Year* Q1 Q2 Q3 Q4 Year* Primary sector ..................... Agriculture ....................... Mining.............................. Secondary sector ................ Manufacturing.................. Tertiary sector...................... Non-primary sector** ........... Non-agricultural sector*** .... Total .................................... -16.4 -33.7 -9.1 -6.2 -8.4 0.4 -7.3 -42.3 8.1 1.3 1.4 -0.1 -4.0 13.7 -8.9 4.9 7.5 2.9 -1.1 7.9 -3.8 3.0 4.5 1.7 -2.5 -4.8 -1.7 0.5 1.0 1.3 -12.3 -16.8 -10.8 -8.0 -8.8 -0.4 11.7 -4.9 17.4 1.3 2.1 2.9 -5.7 -4.5 -6.1 -5.0 -4.4 0.9 -0.4 -7.6 1.8 -2.9 -1.8 -1.0 -3.1 -6.9 -1.9 -1.4 -0.8 1.2 -1.1 -1.8 -2.7 0.2 0.8 -0.5 3.3 2.2 2.6 2.0 1.5 1.4 1.1 0.9 0.8 -2.1 -2.8 -3.2 2.5 3.7 3.3 -0.4 -0.8 -0.8 -1.4 -1.1 -1.4 0.6 0.4 0.2 * Percentage change over one year ** Non-primary sector is total GVA excluding agriculture and mining *** The non-agricultural sector is total GVA excluding agriculture Source: Stats SA The real gross value added (GVA) by the primary sector contracted by a further 0.4% in the fourth quarter of 2019, following a revised decline of 5.7% in the third quarter. Real output decreased in the agricultural sector, while that in the mining sector increased slightly. Annual growth in the real GVA by the primary sector contracted further by 3.1% in 2019 following a decrease of 2.5% in 2018, as production in both the agriculture and mining sectors decreased further and at a faster pace. The pace of contraction in real output of the agricultural sector accelerated from a revised 4.5% in the third quarter of 2019 to 7.6% in the fourth quarter, subtracting 0.2 percentage points from overall GDP growth. The contraction mainly emanated from a decline in the production of field crops and horticultural products as weather-related dynamics adversely impacted the wheat harvest, soil moisture levels and the quality of some horticultural products. Load-shedding further weighed on the irrigation-reliant and energy-intensive agricultural subsectors. Agricultural output decreased by 6.9% in 2019 – a second consecutive annual contraction – as output decreased in all four quarters of the year. 8 MARCH 2020 Total Average: downward phase

Growth in the components of real gross domestic product Total gross domestic product Agriculture, forestry and fishing Mining and quarrying Manufacturing Electricity, gas and water Construction Wholesale and retail trade, catering and accommodation Transport, storage and communication Finance, insurance, real estate and business services General government services -8 -6 -4 -2 0 2 4 Percentage change over one year Source: Stats SA The first estimate of the commercial maize harvest for the 2019/20 season, at 14.6 million tons, was 29.1% higher than the final 2018/19 crop, despite a fair share of plantings outside the optimal window in some regions following good rainfall. Maize production could exceed estimated domestic consumption of about 10.9 million tons per annum and provide for net exports in the 2020/21 marketing year. The 2.6 million hectares that is expected to be planted in the 2019/20 season is 13.0% more than in the previous season. Commercial maize crop estimates Crop (million tons) Area planted (million hectares) 2018/19: final estimate............................................................ 11.3 2.3 2019/20: first production forecast........................................... 14.6 2.6 Source: Crop Estimates Committee of the Department of Agriculture, Forestry and Fisheries The real output of the mining sector increased by 1.8% in the fourth quarter of 2019 after contracting sharply by 6.1% in the preceding quarter. Mining output contributed 0.1 percentage points to real GDP growth in the fourth quarter as production increased in 7 of the 12 subsectors, particularly in platinum group metals (PGMs), iron ore, gold and other non-metallic minerals. These increases were somewhat offset by the lower production of coal, manganese ore and diamonds. The higher gold production reflected increased global demand. Lower electricity production and consumption weighed on the demand for coal and subsequently the production thereof, as more than half of the country’s coal extraction is used for the production of electricity. 9 MARCH 2020 0.8 0.2 -4.8 -6.9 -1.7 -1.9 1.0 -0.8 0.9 -2.0 -1.2 -3.3 2018 2019 0.6 0.0 1.6 -0.4 1.8 2.3 1.3 1.7

Real gross value added by the mining sector Percentage change from quarter to quarter 20 10 0 -10 -20 -30 Physical volume of mining production: selected subsectors Index: first quarter of 2014 = 100 160 140 metals 120 100 80 Iron ore 60 40 2014 Source: Stats SA 2015 2016 2017 2018 2019 Mining activity contracted for a second successive year – by 1.7% in 2018 and by 1.9% in 2019. During the past decade, the real GVA by the mining sector only expanded in four years, amid low levels of fixed investment, electricity supply constraints, increased operating costs, labour unrest, subdued global demand and declining profitability, especially at deep-level gold mines. As a ratio of total GDP, the nominal GVA by the mining sector of 8.3% in 2019 compares with a high of 9.6% in 2011 and a recent low of 7.8% in 2015, and a notably higher average of 10.4% from 1960 to 2000. Nominal gross value added by the mining sector to gross domestic product Per cent 10.0 9.5 9.0 8.5 8.0 7.5 7.0 6.5 6.0 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 Downward phases of the business cycle Sources: Stats SA and SARB 10 MARCH 2020 Platinum group Coal Seasonally adjustedGold Seasonally adjusted and annualised

The real GVA by the secondary sector contracted at a slower pace of 2.9% in the fourth quarter of 2019 following a revised decrease of 5.0% in the previous quarter. The real output of all the secondary sectors – manufacturing, electricity, gas and water as well as construction – decreased further in the fourth quarter. The real output of the manufacturing sector contracted at a slower pace of 1.8% in the fourth quarter of 2019, subtracting 0.2 percentage points from overall GDP growth. Production decreased in 7 of the 10 manufacturing subsectors due to the impact of renewed electricity load-shedding, continued weak domestic demand, structural constraints and persistent low business confidence. Lower production in the subsectors for motor vehicles, parts and accessories and other transport equipment; wood and wood products, paper, publishing and printing; textiles, clothing, leather and footwear; as well as food and beverages weighed the most on manufacturing output. By contrast, production increased in the subsectors supplying petroleum, chemical, rubber and plastic products; and basic iron and steel, non-ferrous metal products, metal products and machinery. The production of motor vehicles, parts and accessories was impacted by the current subdued economic environment, the enduring pressure on households’ disposable income as well as the early closure of motor vehicle manufacturers in December 2019. The lower level of manufacturing production was consistent with a further decline in the seasonally adjusted utilisation of production capacity in the sector, from 80.4% in the third quarter of 2019 to 79.9% in the fourth quarter. The real GVA by the manufacturing sector contracted in all but one of the four quarters of 2019 and resulted in an annual decrease of only 0.8%, which was the weakest performance in the past decade. The weakness was broad-based as production volumes decreased in the subsectors supplying wood and wood products, paper, publishing and printing; basic iron and steel, non-ferrous metal products and machinery; as well as petroleum, chemical, rubber and plastic products. Activity continued to be impeded by factors such as electricity supply shortages, higher energy costs, subdued global demand and lower world trade following the heightened US–China trade tensions in 2019. Real gross value added by the manufacturing sector Percentage change from quarter to quarter 15 10 5 0 -5 -10 -15 Physical volume of manufacturing production: selected subsectors Index: first quarter of 2014 = 100 115 110 105 100 95 90 85 80 75 Basic iron and steel Textiles, clothing, leather and footwear Seasonally adjusted 2014 Source: Stats SA 2015 2016 2017 2018 2019 11 MARCH 2020 Motor vehicles, parts and other transport equipment Petroleum Seasonally adjusted and annualised

The real output of the sector supplying electricity, gas and water decreased by 4.0% in the fourth quarter of 2019 – the third quarterly contraction for the year. The renewed implementation of load-shedding (which for the first time went up to Stage 6) and the sluggish economic activity in the electricity-intensive mining and manufacturing sectors weighed on both electricity production and consumption. Electricity generation capacity was further constrained by delays in the return to service of power plants due to planned maintenance as well as coal supply shortages and the failure of coal-supplying conveyer belts. The implementation of rotational load-shedding may continue as Eskom prioritises maintenance operations at various plants. Annual electricity production decreased by 1.5% and consumption decreased by 1.9% in 2019, resulting in a decrease of 2.0% in the real GVA by the electricity, gas and water sector after increasing by 0.9% in 2018. Real gross value added by selected subsectors Index: first quarter of 2014 = 100 108 106 104 102 100 98 96 94 2014 2015 2016 2017 2018 2019 Source: Stats SA The real output of the construction sector decreased by a notable 5.9% in the fourth quarter of 2019, marking the sixth successive quarterly contraction. This reflected a significant decrease in non-residential building activity alongside further contractions in both residential building and civil construction activity. As a consequence, real construction output contracted further by 3.3% in 2019 following a contraction of 1.2% in 2018. The real GVA by the tertiary sector reverted to a decrease of 1.0% in the fourth quarter of 2019 from an increase of 0.9% in the third quarter. Real output declined in the commerce and general government services sectors in the fourth quarter alongside a further contraction in the output of the transport, storage and communication sector. By contrast, growth in real economic activity in the finance, insurance, real estate and business services sector accelerated. The real GVA by the commerce sector contracted by 3.8% in the fourth quarter of 2019, subtracting 0.5 percentage points from overall GDP growth, following an increase of 2.6% in the third quarter. Both real wholesale and motor trade activity decreased, while retail trade activity rose marginally. Subdued business and consumer confidence, weak consumer demand and rising input costs constrained the real output of the wholesale trade subsector, while motor trade activity was negatively impacted by lower sales of new and used vehicles as household disposable income remained under pressure. By contrast, retail trade activity increased in the general dealers; food, beverages and tobacco; as well as the household furniture, appliances and equipment categories, boosted by Black Friday specials in November 2019. 12 MARCH 2020 Mining Manufacturing Seasonally adjustedElectricity, gas and water

The real output of the transport, storage and communication sector declined notably by a further 7.2% in the fourth quarter of 2019, following a sharp contraction of 5.4% in the third quarter. This reflected weaker activity in both land and air transport as well as transport support services. The decrease in activity in land freight transportation was consistent with the decline in import volumes. By contrast, the gradual expansion in the telecommunications subsector continued in the fourth quarter. Growth in the real output of the finance, insurance, real estate and business services sector accelerated from an annualised rate of 1.6% in the third quarter of 2019 to 2.7% in the fourth quarter, mainly due to increased activity in the banking subsector. The level of output of the finance, insurance, real estate and business services sector increased by 2.3% in 2019, and expanded at a faster pace than in any other sector. The real GVA by the general government services sector decreased by 0.4% in the final quarter of 2019 from an increase of 2.4% in the third quarter, mainly due to lower employment numbers in national and provincial government and higher education institutions. In 2019, government output expanded by 1.7% compared with an increase of 1.3% in 2018. general Real gross domestic expenditure3, 4 Real gross domestic expenditure (GDE) decreased by a further 4.6% in the fourth quarter of 2019 following a decrease of 4.5% in the third quarter. Both real gross fixed capital formation and real final consumption expenditure by general government reverted from an increase in the third quarter of 2019 to a contraction in the fourth quarter, alongside a much faster pace of de-accumulation in real inventory holdings. The real final consumption expenditure by households increased somewhat over the period. For 2019 as a whole, the pace of expansion in real GDE moderated slightly to 0.7%, from 1.0% in 2018. Annual growth in real GDE has exceeded that in real GDP on 16 occasions since 2000, as the demand for goods and services exceeded the production thereof. 3Unless stated to the contrary, the quarter-to-quarter growth rates referred to in this section are based on seasonally adjusted data and are annualised. 4 The analysis in this section of the review is based on a revised set of national accounts estimates for 2019. These revisions are based on more detailed or more appropriate data that have become available. Real gross domestic product and expenditure Percentage change over one year 10 8 6 4 2 0 -2 2000 2002 2004 2006 2008 2010 2012 20142016 2018 Downward phases of the business cycle Sources: Stats SA and SARB 13 MARCH 2020 Gross domestic product Gross domestic expenditure

Real gross domestic expenditure Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Component Q1 Q2 Q3 Q4 Year1 Q1 Q2 Q3 Q4 Year1 Final consumption expenditure Households.................................. General government..................... Gross fixed capital formation ........... Domestic final demand2 ................. Change in inventories (R billions)3 .... Residual4 ......................................... Gross domestic expenditure5 ......... 1.1 4.6 -9.3 -0.3 13.1 0.0 1.2 0.1 2.1 -3.8 -0.2 4.6 0.0 -1.4 0.6 0.4 -0.7 0.3 14.5 0.1 2.1 3.2 0.6 -2.5 1.6 -53.9 0.0 -7.0 1.8 1.9 -1.4 1.2 -5.4 0.0 1.0 -0.9 2.2 -4.1 -0.9 -11.7 0.1 4.7 2.5 2.7 5.8 3.2 29.4 0.2 9.1 0.3 1.4 4.1 1.2 -13.9 0.1 -4.5 1.4 -0.2 -10.0 -1.2 -40.3 0.0 -4.6 1.0 1.5 -0.9 0.8 -9.1 0.1 0.7 1 2 3 4 5 Percentage change over one year Comprises final consumption expenditure by households and general government as well as gross fixed capital formation At constant 2010 prices The residual as a percentage of GDP Including the residual Sources: Stats SA and SARB Real net exports contributed the most to real GDP growth in the fourth quarter of 2019, adding 3.3 percentage points, while the real final consumption expenditure by households contributed 0.8 percentage points. By contrast, the change in real inventory holdings and real gross fixed capital formation subtracted 3.3 and 2.0 percentage points respectively. In 2019, real final consumption expenditure by households contributed the most to growth in real GDP at 0.6 percentage points, while net exports subtracted from GDP growth to the same extent. Contributions of expenditure components to growth in real gross domestic product Percentage points 2018 2019 Component Q1 Q2 Q3 Q4 Year Q1 Q2 Q3 Q4 Year Final consumption expenditure Households............................ General government............... Gross fixed capital formation ..... Change in inventories ................ Residual .................................... Gross domestic expenditure .... Net exports ............................... Gross domestic product .......... 0.7 0.9 -1.9 1.5 0.0 1.2 -3.9 -2.7 0.1 0.4 -0.8 -1.1 0.0 -1.4 0.9 -0.5 0.3 0.1 -0.1 1.3 0.5 2.1 0.5 2.6 2.0 0.1 -0.5 -8.7 -0.2 -7.3 8.7 1.4 1.1 0.4 -0.3 -0.3 0.1 1.0 -0.2 0.8 -0.5 0.4 -0.8 5.3 0.2 4.6 -7.8 -3.2 1.6 0.5 1.1 5.3 0.5 9.0 -5.7 3.3 0.2 0.3 0.8 -5.5 -0.5 -4.7 3.9 -0.8 0.8 0.0 -2.0 -3.3 -0.2 -4.8 3.3 -1.4 0.6 0.3 -0.2 -0.1 0.1 0.7 -0.6 0.2 Components may not add up to totals due to rounding off. Sources: Stats SA and SARB Growth in the real exports of goods and services slowed further from a non-annualised rate of 0.9% in the third quarter of 2019 to 0.6% in the fourth quarter. The exports of mining products (including gold) increased, while growth in agricultural exports slowed, alongside a contraction in the exports of both manufactured products and services. In the mining sector, strong growth in the export volumes of precious metals (including gold, PGMs and stones) as well as base metals 14 MARCH 2020

and articles more than offset the decline in the exports of mineral products. By contrast, weaker foreign demand for manufactured goods was broad-based, in particular for vehicles and transport equipment. The decline in vegetable exports significantly reduced overall agricultural exports. Real exports and imports of goods and services Quarter-to-quarter percentage change* 2019 Exports Imports Component Percentage of total** Percentage of total** Q3*** Q4*** Q3*** Q4*** Total ............................................................. 100.0 0.9 0.6 100.0 -2.3 -2.2 Mining.......................................................... Of which: Mineral products.................................. Precious metals including gold, platinum group metals and stones ...... Base metals and articles ..................... 45.0 -2.5 7.9 19.9 -14.6 17.8 20.2 -3.4 -7.3 14.5 -18.8 24.8 13.6 11.2 7.1 -10.4 36.7 3.1 1.1 4.4 0.2 -3.3 34.3 -5.8 Manufacturing ............................................. Of which: Vehicles and transport equipment ....... Machinery and electrical equipment .... Chemical products .............................. Prepared foodstuffs, beverages and tobacco ........................................ 34.6 3.1 -8.2 63.5 1.6 -7.8 12.0 6.8 5.5 6.5 4.1 3.2 -17.8 -4.9 -1.1 13.1 25.3 9.4 7.7 2.0 -1.9 -10.3 -12.4 -1.9 3.8 -1.3 -4.5 2.6 -3.4 -0.7 Agriculture ................................................... Of which: Vegetable products ............................. 5.7 17.2 0.3 3.4 0.2 -8.9 4.4 27.8 -1.0 1.5 7.6 -14.0 Services ....................................................... 13.6 -0.3 -0.9 12.3 -3.1 0.5 * Based on seasonally adjusted and annualised data ** Expressed as a percentage of the total in 2019 *** Not annualised Components may not add up to totals due to rounding off and the exclusion of unclassified items. Sources: SARS, Stats SA and SARB The real imports of goods and services declined further in the fourth quarter of 2019 as the import volumes of both manufactured goods and agricultural products contracted. Weaker domestic demand for manufactured goods and vegetable products resulted in the lower growth in imports of all of the major manufactured product categories as well as agricultural products. By contrast, the notable increase in mining imports resulted primarily from the strong demand for precious metals (including gold, PGMs and stones) and mineral products. Real net exports contributed 3.3 percentage points to real GDP growth in the fourth quarter of 2019, as real net manufacturing and agricultural exports contributed 2.9 and 0.4 percentage points respectively. The real net exports of machinery and electrical equipment added the most to overall net manufacturing exports. By contrast, real net mining exports were mainly weighed down by the lower real net exports of mineral products. 15 MARCH 2020

Contributions of real exports and imports and net exports of goods and services to growth in real gross domestic product Percentage points 2019 Exports Imports* Net exports Component Q3 Q4 Q3 Q4 Q3 Q4 Total ............................................................... 1.0 0.7 -2.9 -2.7 3.9 3.3 Mining............................................................ Of which: Mineral products.................................... Precious metals including gold, platinum group metals and stones......... Base metals and articles ....................... -1.3 3.9 -3.7 3.9 2.4 0.0 -0.8 -1.7 -3.5 3.8 2.7 -5.5 0.9 -1.4 5.2 0.4 0.0 -0.2 0.4 -0.3 1.0 -1.2 4.8 0.7 Manufacturing ............................................... Of which: Vehicles and transport equipment ......... Machinery and electrical equipment ...... Chemical products ................................ Prepared foodstuffs, beverages and tobacco .......................................... 1.2 -3.4 1.3 -6.3 0.0 2.9 0.9 0.3 0.2 -2.7 -0.4 -0.1 1.2 0.7 -0.2 -1.7 -4.1 -0.2 -0.3 -0.3 0.4 -1.0 3.7 0.1 -0.1 -0.2 -0.1 0.0 0.1 -0.2 Agriculture ..................................................... Of which: Vegetable products ............................... 1.0 0.0 0.0 -0.4 1.0 0.4 1.2 -0.1 0.1 -0.3 1.1 0.2 Services ......................................................... -0.1 -0.1 -0.5 0.1 0.4 0.3 * A positive contribution by imports subtracts from growth and a negative contribution adds to growth. Components may not add up to totals due to rounding off and the exclusion of unclassified items. Sources: SARS, Stats SA and SARB Real final consumption expenditure by households increased by 1.4% in the fourth quarter of 2019 following a revised increase of 0.3% in the third quarter, supported by faster growth in real disposable income. Real spending on both semi-durable and non-durable goods increased following declines in the third quarter of 2019, while growth in real outlays on services accelerated. By contrast, households purchased less durable goods in the fourth quarter. Real final consumption expenditure and disposable income of households Percentage change from quarter to quarter 8 6 4 2 0 -2 -4 2014 2015 2016 2017 2018 2019 Sources: Stats SA and SARB 16 MARCH 2020 Disposable income Final consumption expenditure Seasonally adjusted and annualised

Growth in household consumption expenditure moderated from 1.8% in 2018 to 1.0% in 2019. Consistent with the adverse impact of rising unemployment, slower growth in households’ real disposable income, a lack of consumer appetite for large purchases and weaker consumer confidence, the pace of increase in real outlays on durable goods, semi-durable goods and services slowed. By contrast, growth in the real purchases of non-durable goods accelerated slightly over the period. Real final consumption expenditure by households Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Category Q1 Q2 Q3 Q4 Year* Q1 Q2 Q3 Q4 Year* Durable goods............ Semi-durable goods ... Non-durable goods .... Services ..................... Total ........................... 2.8 -13.1 0.6 4.8 1.1 -3.7 1.2 -1.8 2.4 0.1 -3.7 9.0 2.7 -2.0 0.6 7.7 8.7 3.0 1.1 3.2 4.5 3.0 0.8 1.9 1.8 -7.2 -11.4 -0.2 2.6 -0.9 8.7 3.7 2.1 1.3 2.5 2.2 -1.6 -0.2 0.7 0.3 -0.6 5.6 0.7 1.4 1.4 0.6 0.5 1.1 1.2 1.0 * Percentage change over one year Source: Stats SA Real spending by households on durable goods contracted by 0.6% in the fourth quarter of 2019 following an increase of 2.2% in the third quarter. Real purchases of personal transport equipment (constituting around 45% of durable spending) decreased substantially in the fourth quarter of 2019. By contrast, real outlays in all other durable goods subcategories increased, particularly computers and related equipment. Real consumption expenditure on semi-durable goods increased by 5.6% in the fourth quarter of 2019 following a decrease of 1.6% in the third quarter. Real spending on clothing and footwear recorded robust growth in the fourth quarter, boosted by strong Black Friday sales, while that on household textiles, furnishings and glassware, and miscellaneous goods also improved. Conversely, real purchases of motorcar tyres and accessories as well as recreational and entertainment goods declined in the fourth quarter of 2019. Real spending on non-durable goods gained some momentum and increased by 0.7% in the fourth quarter of 2019 after contracting slightly by 0.2% in the third quarter. Real purchases of food, beverages and tobacco; household consumer goods; and medical and pharmaceutical products increased in the fourth quarter. By contrast, real expenditure on recreational and entertainment goods; petroleum products; as well as household fuel, power and water contracted as fuel prices increased. Households’ real outlays on services advanced by 1.4% in the fourth quarter of 2019 compared with a more muted increase of 0.7% in the third quarter. Real spending on the majority of subcategories improved, including transport and communication services, medical services, household services and rent. Real outlays on recreational, entertainment and educational services increased at the same subdued rate in the third and fourth quarter. The pace of household debt accumulation accelerated in the fourth quarter of 2019 due to faster growth in the extension of mortgage advances (which includes mortgage securitisation) as well as leasing finance and instalment sale loans. Consequently, growth in household debt exceeded that in disposable income, with the ratio of household debt to nominal disposable income increasing marginally to 73.0% in the fourth quarter of 2019, from 72.6% in the third quarter. Households’ cost of servicing debt as a percentage of nominal disposable income remained unchanged at 9.4% in both the third and fourth quarter of 2019. Growth in household debt accelerated marginally from 5.5% in 2018 to 5.7% in 2019. Household debt as a percentage of nominal disposable income increased from 72.0% to 72.8% over the same period, as the annual increase in household debt exceeded that in household nominal 17 MARCH 2020

disposable income. Likewise, households’ cost of servicing debt relative to disposable income inched higher from 9.2% to 9.4% over the same period. Household debt Per cent Percentange change from quarter to quarter 12 85 9 80 75 6 3 70 0 65 2014 2015 2016 2017 2018 2019 Seasonally adjusted and annualised Source: SARB Households’ net wealth increased in the fourth quarter of 2019 as the increase in the value of equity portfolios and housing stock exceeded that in household debt. The ratio of net wealth to nominal disposable income rose slightly to 359.5% in the fourth quarter of 2019 from 359.1% in the previous quarter, and declined in 2019 as a whole, as the increase in nominal disposable income exceeded that in wealth. 18 MARCH 2020 Box 1 Household wage and income statistics1, 2 The sources and methodology applied to compile wage and household disposable income statistics in the national accounts are discussed in this box. These statistics are important, as the moderation in nominal wage growth in recent years has resulted in a slowdown in growth in the nominal disposable income, which has negatively affected households’ ability to spend and borrow. Salaries and wages payable in cash or in kind drive the compensation of employees which, in turn, contributes almost 80% to households’ nominal disposable income. Growth in households’ nominal disposable income is a key driver of domestic demand and therefore their nominal consumption expenditure which, in turn, contributes about 60% to South Africa’s nominal gross domestic product (GDP). Gross earnings3 statistics reflect total nominal salaries and wages in the formal non-agricultural sector, as compiled by Statistics South Africa (Stats SA) and published as the Quarterly Employment Statistics (QES) survey. 1 This box relates to the statistics in the production, distribution and accumulation accounts of South Africa for households and non-profit institutions serving households, available on page S–134 in this edition of the Quarterly Bulletin; Quarterly Employment Statistics (QES) statistical release P0277 and Annual Financial Statistics (AFS) statistical release P0021, both published by Statistics South Africa; as well as the quarterly Wage Settlement Survey published by Andrew Levy Employment Publications. See http://www.statssa.gov.za/?page_id=1854&PPN=P0277&SCH=7642, http://www.statssa.gov.za/?page_id=1854&PPN=P0021&SCH=7681 and https://www.andrewlevy.co.za 2 The compilation of South Africa’s household disposable income statistics within the national accounts framework adheres to the guidelines of the System of National Accounts 2008 (2008 SNA) as the international standard for the measurement of economic activity. See https://unstats.un.org/unsd/nationalaccount/docs/SNA2008.pdf 3 Statistics South Africa, in its QES, defines gross earnings as “the total sum of the earnings, including performance and other bonuses, as well as overtime payments for the three months of the reference quarter” and in more detail as “the payments for ordinary-time, standard or agreed hours during the reference period for all permanent, temporary, casual, managerial and executive employees before taxation and other deductions for the reference period. This includes salaries and wages; commission if a retainer, wage or salary was also paid; employer’s contribution to pension, provident, medical aid, sick pay and other funds; allowances; etc., but excludes earnings of sole proprietors or partners of unincorporated businesses; commission where a retainer, wage or salary was not paid; payments to subcontractors and consultants who are not part of the enterprise; and severance, termination and redundancy payments.” See http://www.statssa.gov. za/?page_id=1854&PPN=P0277&SCH=7642 As a percentage Change in stock of disposable income (right-hand scale)

19 MARCH 2020 The QES is a quarterly enterprise-based sample survey of private businesses as well as national, provincial and local government entities and public enterprises in the South African economy per industry.4 Gross earnings statistics from the QES survey, combined with employment cost sourced from the Annual Financial Statistics (AFS) survey, are applied to estimate the broader measure of households’ nominal compensation of employees5 in the national accounts framework, which includes the agriculture and informal sectors. This measure of the compensation of employees is a major input in deriving both households’ gross and net disposable income, as shown in the accompanying table. Household disposable income in the national accounts framework R millions15 at basic prices surplus/mixed income 4 The industries consist of enterprises engaged in the same or similar kind of economic activity. The definition of industries is based on the 2008 SNA and is in line with the Standard Industrial Classification of all Economic Activities (SIC), fifth edition, Report No. 09-09-02 of January 1993. See http://www.statssa.gov.za/additional_services/sic/sic.htm 5 The 2008 SNA defines compensation of employees as “the total remuneration, in cash or in kind, payable by an enterprise to an employee in return for work done by the latter during the accounting period. Compensation of employees has two main components: (a) Wages and salaries payable in cash or in kind, including enhanced payments and special allowances (e.g. overtime), regular supplementary allowances (e.g. housing), ad hoc bonus payments, as well as commissions, gratuities or tips received by employees; and (b) Social insurance contributions payable by employers, which include contributions to social security schemes; actual social contributions to other employment-related social insurance schemes and imputed social contributions to other employment-related social insurance schemes.” Real economic activity Accounts1 Balancing items5 High-level items 2019 Current2 Production4 Output at basic prices8 Intermediate consumption9 1 455 349 596 250 859 099 -164 241 -30 826 664 032 Gross value added Generation of income Compensation of employees10 Net taxes and subsidies on production Gross operating Distribution3 Allocation of primary income Compensation of employees11 2 416 194 Net property income received/paid 300 187 Gross primary income 3 380 413 Secondary distribution of income Current taxes on income and wealth Net social benefits/contributions Net current transfers received/paid12 -536 625 176 053 51 443 Gross disposable income6 3 071 284 Use of disposable income Adjustment for change in pension entitlements13 Residual Total available household resources14 Consumption of fixed capital 57 278 -4 247 3 124 315 -73 378 Net disposable income7 3 050 93716 1 These accounts are listed according to the accounting framework of the sequence of accounts in the 2008 SNA. 2 The current account records the production of goods and services, the generation of income by production, the subsequent distribution and redistribution of income, as well as the use of income for consumption and saving. 3 This refers to the distribution of income between labour and capital. 4 The production account is the starting point and records the use of inputs to produce output and imputed rental of owner-occupied dwellings. Household production includes goods for own use but excludes services for own consumption, except paid domestic staff and own-account housing services by owner-occupiers. 5 Balancing items are an accounting construct carried forward from one account to the next 6 Gross disposable income excludes holding gains and losses. 7 Net disposable income is total available household resources minus the imputed consumption of fixed capital (depreciation). 8 Output at basic prices is the amount receivable for output minus tax payable and subsidies receivable, and is measured on an accrual basis. 9 This is the value of goods and services consumed as inputs, excluding depreciation. 10 This is the compensation of paid employees of household unincorporated enterprises. 11 Compensation of employees is the total remuneration, in cash or in kind, paid by enterprises to employees. 12 This means the current transfer of goods or services without receiving anything in return. 13 As individuals accrue pension entitlements, it becomes their assets. 14 Total available household resources are calculated as gross disposable income after adjustment for the change in pension entitlements and the residual. 15 The statistics referred to in this table are published on page S–134 in this edition of the Quarterly Bulletin, except for net disposable income. 16 Net disposable income is published on page S–137 in this edition of the Quarterly Bulletin Source: SARB

20 MARCH 2020 The methodology to derive net household disposable income, as depicted on the previous page, builds on the discussion of the compilation of household saving and net lending/borrowing.6 The production of goods and services by unincorporated enterprises owned by households is recorded in the production account and includes imputed rental for owner-occupied dwellings minus intermediate consumption, inclusive of the maintenance of dwellings. This renders gross value added, from which both compensation paid to employees of household unincorporated enterprises and net taxes on production7 are deducted, to derive mixed income. Employed members of households earn income from other sectors in the economy, measured as the compensation of employees which, together with net property income received/paid (interest, dividends and rent on land and subsoil assets), constitutes gross primary income. Households then pay tax on income received and make social contributions, such as those paid by employers on their behalf, while also receiving social benefits such as social security. This, combined with net current transfers received/paid (goods and services without quid pro quo), leaves households with gross disposable income, which is then adjusted for accrued pension entitlements to derive the total available household resources. When consumption of fixed capital is deducted from total available household resources, it renders net disposable income, which is available for final consumption expenditure and saving, followed by gross fixed capital formation and net lending/borrowing. The importance of the compensation of employees statistic is evident from the contribution that it makes to net disposable income, which is used when expressing, for example, household saving, debt and net wealth to income.8 From 2010, the contribution of both net social benefits/contributions and net current transfers received/paid to net disposable income increased, while current taxes on income and wealth subtracted more from disposable income. Except for notable increases in net property income received/paid in 2011 and 2012 due to lower levels of interest paid, its contribution remained more or less unchanged. Contributions to net nominal disposable income of households Per cent 125 100 75 50 25 0 -25 2010201120122013201420152016201720182019 Adjustment for the change in pensionNet current transfers received/paid entitlements and residualNet property income received/paid Net social benefits/contributionsGross operating surplus/mixed income Compensation of employeesConsumption of fixed capital Current taxes on income and wealth Source: SARB 6 See ‘Box 1: Methodology underlying the compilation of household saving and net lending/borrowing’ in the December 2019 edition of the Quarterly Bulletin. 7 Net taxes on production are derived as taxes less subsidies. 8 See these ratios on page S–156 in this edition of the Quarterly Bulletin.

2014 2015 2016 2017 2018 2019 21 MARCH 2020 An analysis of the QES survey data shows that year-on-year growth in the total nominal salaries and wages in the formal non-agricultural sector slowed notably from a peak of 8.4% in the first quarter of 2014 to 3.8% in the third quarter of 2019.9 The trend in this indicator has often been masked by considerable volatility, which has usually resulted from base effects due to the delayed implementation of annual wage increases (such as in the public sector in 2019) or the no-work-no-pay principle applied during labour strikes (such as the protracted platinum mining strike in the first half of 2014). Total nominal salaries and wages in the formal non-agricultural sector Percentage change over four quarters 9 8 7 6 5 4 3 Sources: Stats SA and SARB Number of workdays lost due to strike action Number (millions) 5 4 3 2 1 0 2014 2015 2016 2017 2018 2019 Source: Andrew Levy Employment Publications Similar to gross earnings, an analysis of national accounts statistics shows that growth in the nominal compensation of employees slowed markedly from 11.6% in 2010 to 8.7% in 2014, and further to 4.2% in 2019. This contributed to households’ nominal disposable income growth moderating to 4.6% in 2019 from a recent high of 10.6% in 2011. 9 The gross earnings time series have been statistically linked by the South African Reserve Bank (SARB) to account for the various structural breaks in the QES data. See ‘Box 1: Statistical linking of formal non-agricultural employment and earnings time series’ in the March 2017 edition of the Quarterly Bulletin for the methodology underlying the linking of this statistic. See the related statistics on page S–139 in this edition of the Quarterly Bulletin.

10 2014 2015 2016 2017 2018 2019 2014 2015 2016 2017 2018 2019 22 MARCH 2020 Total nominal compensation of Nominal disposable income of employeeshouseholds Percentage change over four quartersPercentage change over four quarters 1012 9 8 78 66 5 4 4 32 Source: Stats SASource: SARB The slowdown in nominal wage and income growth observed in the official statistics in recent years is corroborated by the decline in the average wage settlement rate in collective bargaining agreements.10 These settlements reflect annual wage increases and exclude bonuses and overtime payments. This measure provides an indication of wage increases for employees who are part of the surveyed collective bargaining units but excludes centralised bargaining agreements through sectoral bargaining councils. The average wage settlement rate moderated from a peak of 8.4% in the fourth quarter of 2014 to 6.4% in the fourth quarter of 2019. Wage settlement rates in collective bargaining agreements Per cent 9 8 7 6 5 4 201420152016201720182019 Sources: Andrew Levy Employment Publications and SARB 10 The wage settlement rate data are sourced from Andrew Levy Employment Publications. All the surveyed bargaining units’ settlement rates are averaged, but not weighted, and are published each quarter as a cumulative average for the year up to the end of that specific quarter. The SARB derives quarterly estimates from the cumulative averages.

Real final consumption expenditure by general government decreased slightly by 0.2% in the fourth quarter of 2019 from an increase of 1.4% in the third quarter, as the decline in the real compensation of employees more than offset the renewed increase in spending on non-wage goods and services. For 2019 as a whole, real final consumption expenditure by general government increased by 1.5%, slightly less than the increase of 1.9% in 2018. Growth in real spending on non-wage goods and services decelerated, while temporary appointments by the Electoral Commission of South Africa in preparation for and during the national elections in May 2019 temporarily elevated spending on compensation. However, the ratio of nominal final consumption expenditure by general government to nominal GDP remained broadly unchanged at 21.3% in both 2018 and 2019. Real final consumption expenditure by general government Percentage change over one year 7 6 5 4 3 2 1 0 -1 -2 -3 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 Downward phases of the business cycle Sources: Stats SA and SARB Real gross fixed capital formation contracted anew by a marked 10.0% in the fourth quarter of 2019 following two consecutive quarters of expansion. Private business enterprises, public corporations and general government all reduced capital outlays in the fourth quarter. Real gross fixed capital formation declined by a further 0.9% in 2019, constrained by fiscal pressures, lacklustre real economic activity and weak private sector business confidence. Consequently, the ratio of nominal fixed capital formation to nominal GDP declined to 17.9% in 2019 – the lowest level since 2005. Real gross fixed capital formation Quarter-to-quarter percentage change at seasonally adjusted annualised rates 2018 2019 Sector Q1 Q2 Q3 Q4 Year* Q1 Q2 Q3 Q4 Year* Private business enterprises ... Public corporations................ General government .............. Total ...................................... -6.7 -15.5 -14.1 -9.3 -1.3 -13.8 -4.3 -3.8 2.9 -7.9 -9.0 -0.7 -1.4 -5.6 -4.1 -2.5 2.1 -12.5 -4.4 -1.4 -8.4 16.3 -2.2 -4.1 16.0 -12.0 -16.3 5.8 9.5 0.7 -15.6 4.1 -10.3 -0.3 -17.6 -10.0 1.1 -1.6 -8.9 -0.9 * Percentage change over one year Source: Stats SA 23 MARCH 2020 Compensation of employees Total

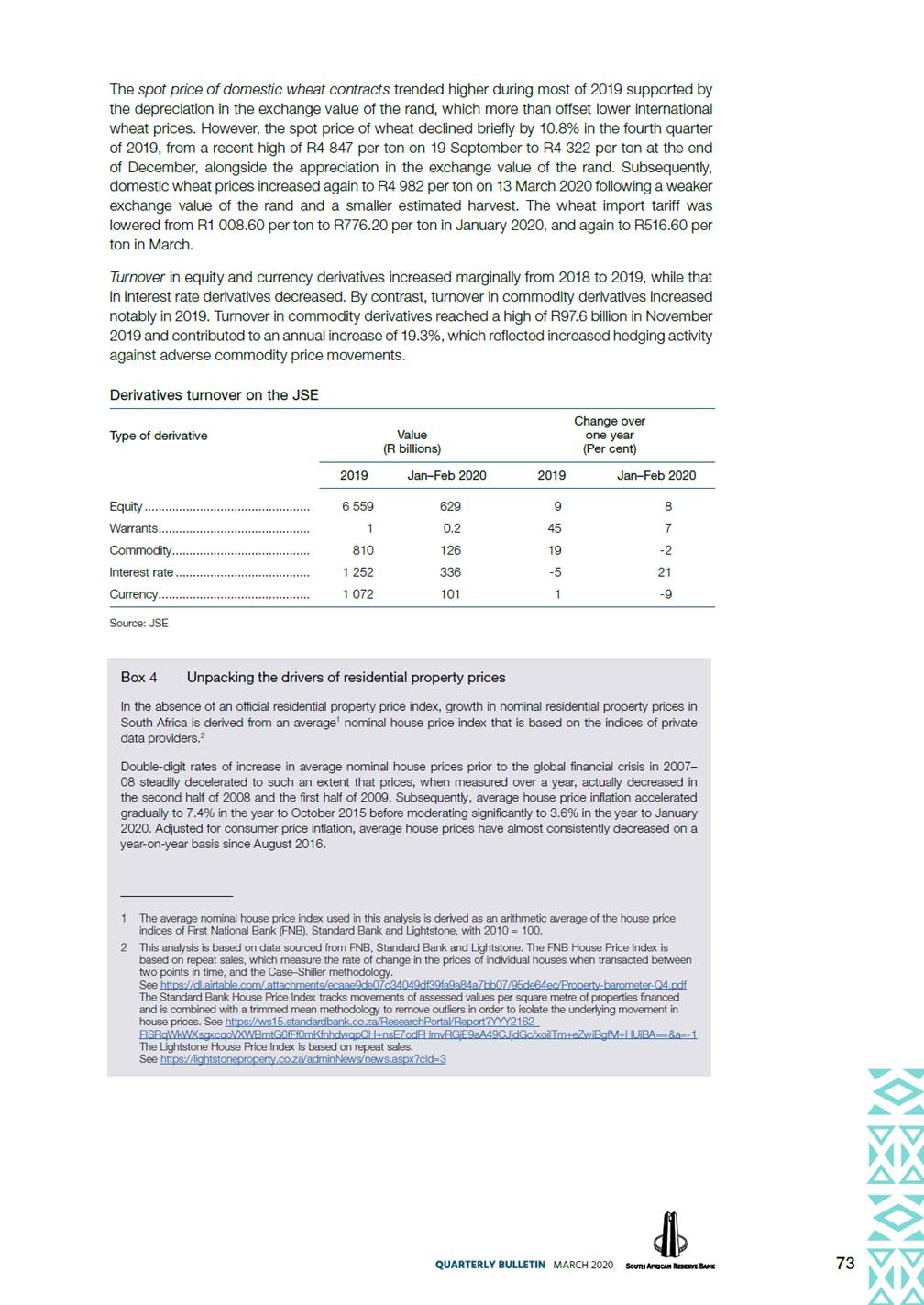

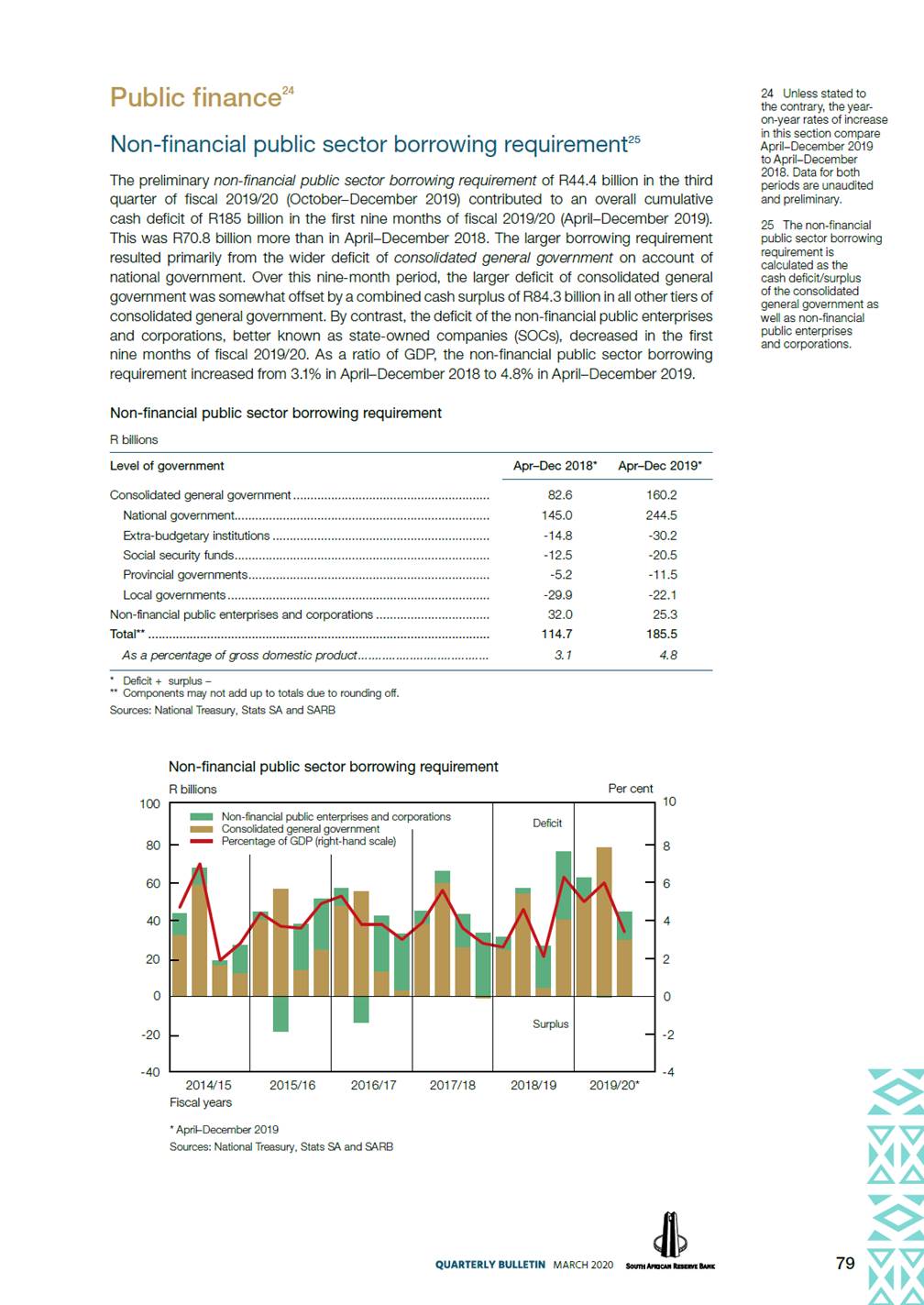

Real gross fixed capital outlays by private business enterprises decreased by 10.3% in the fourth quarter of 2019 following robust growth in the previous two quarters. Capital expenditure on transport equipment, construction works as well as machinery and other equipment receded. In 2019, growth in real gross fixed capital formation by private business enterprises slowed to 1.1%, from 2.1% in 2018. The private sector’s share of total nominal gross fixed capital formation nevertheless increased slightly from 68.5% in 2018 to 70.0% in 2019, as budget constraints negatively impacted capital spending by public corporations and general government. Nominal gross domestic product and fixed capital formation Per cent 30 100 25 90 20 80 15 70 10 60 5 50 0 40 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 Source: Stats SA Real gross fixed capital expenditure by the public sector decreased for a third consecutive quarter in the fourth quarter of 2019, especially due to the lower capital expenditure by general government. Gross fixed capital formation by public corporations contracted anew by 0.3% in the fourth quarter of 2019 after increasing marginally by a revised 0.7% in the third quarter. The slight increase in capital outlays on transport equipment was outweighed by lower capital spending on all the other asset types, most notably on construction works and on machinery and equipment. Real capital spending by general government receded notably further by 17.6% in the fourth quarter of 2019 following a marked decline of 15.6% in the third quarter, as all three spheres of government reduced capital outlays in the fourth quarter. Gross fixed capital formation by general government – constituting 15.1% of total fixed investment in 2019 – has contracted consistently over the past two years, declining by 4.4% in 2018 and a further 8.9% in 2019. Real fixed capital expenditure by the mining and manufacturing sectors increased by 10.8% and 3.2% respectively in 2019, despite contractions in real economic activity in those sectors. Similarly, capital expenditure by the construction sector increased by 4.3% in 2019 following a decrease of 1.3% in 2018. Reduced capital expenditure by Eskom outweighed the increase in construction works related to the recommencement of independent power producer projects, resulting in a 2.4% decrease in fixed capital outlays by the electricity, gas and water sector in 2019. 24 MARCH 2020 Total fixed capital formation as a ratio of GDP Private business enterprises as a ratio of total gross fixed capital formation (right-hand scale) Seasonally adjusted