The Bank Behind Your Business November 2024

OUTLINE 2 I. Overview 3 II. 3Q24 Highlights / Topics of Interest 9 » Earning Assets 10 » Funding 15 » Net Interest Margin (NIM) 19 » Risk Management 24 » Capital 29 » Non - Interest Income Highlights 33 » Revenue 38 » Non - Interest Expense 41 » Net Income 44 Impacting Lives for Success and Significance

OVERVIEW Impacting Lives for Success and Significance

6 4

OUR IDENTITY 5

» Began in 1995 » Focused on Organic Growth, Augmented with Opportunistic Acquisitions ▪ 2004 – Newberry Federal ▪ 2006 – Bank of Camden ▪ 2008 – EAH Financial Planning Practice ▪ 2011 – Palmetto South Mortgage Corp. ▪ 2014 – Savannah River Financial Corp. ▪ 2017 – Cornerstone National Bank » Executive Leadership Team stability with leadership transition plan designed to be seamless » September 30, 2024 ▪ $1.9 billion total assets ▪ Twenty - one (21) banking offices ▪ Largest community bank in SC Midlands ▪ Fourth largest bank in SC » Dividends ▪ 91 Consecutive Quarters ▪ Current Yield – 2.53% 1 OVERVIEW Highlights 1 Based on 10/31/24 closing pricing of $23.74. 6

» Columbia (Midlands of SC) ▪ State Capitol ▪ University of SC ▪ Fort Jackson ▪ Quality Public Schools ▪ Lake Murray ▪ Riverbanks Zoo » Greenville (Upstate of SC) ▪ Great Pure Business Market ▪ Attractive to Millennials » Augusta (CSRA) ▪ Cybersecurity x Fort Gordon x Private Sector ▪ Augusta University ▪ Excellent Medical Community ▪ The Masters Tournament » Rock Hill (Piedmont) ▪ Winthrop University ▪ Lake Wylie ▪ Included in the Charlotte MSA ▪ Home of Sports & Event Center, as well as “Come - See - Me” & Christmasville Festivals Geographically Diverse and Growing Markets OVERVIEW 7

Three Lines of Business OVERVIEW 8

3Q24 HIGHLIGHTS / TOPICS OF INTEREST Impacting Lives for Success and Significance

EARNING ASSETS Impacting Lives for Success and Significance

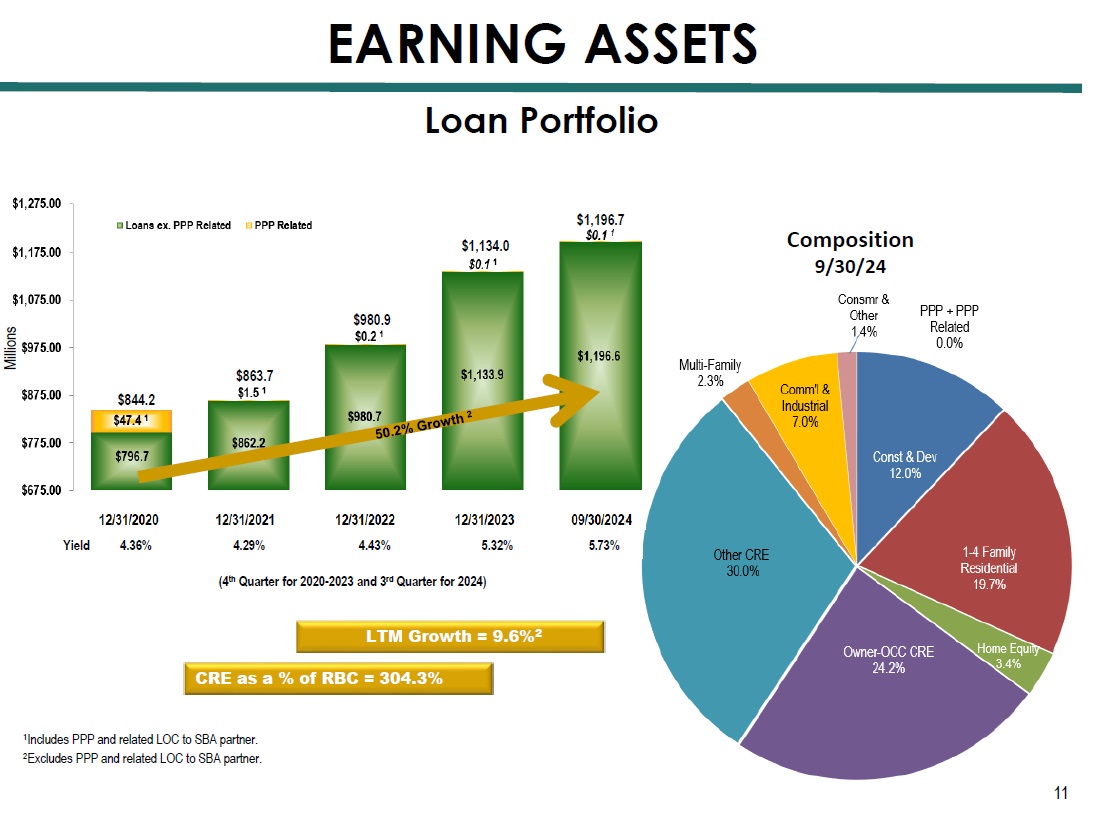

Yield 4.36% 4.29% 4.43% 5.32% 5.73% Loan Portfolio LTM Growth = 9.6% 2 1 Includes PPP and related LOC to SBA partner. 2 Excludes PPP and related LOC to SBA partner. CRE as a % of RBC = 304.3% (4 th Quarter for 2020 - 2023 and 3 rd Quarter for 2024) $980.9 $1,134.0 $844.2 11 EARNING ASSETS $1,196.7 Composition 9/30/24 Millions $863.7

» 3Q24 $7.5 million 2.5% annualized growth rate » YTD 2024 $62.6 million 7.4% annualized growth rate Notes: » Percent of Growth : 3Q24 YTD24 ▪ CRE (57%) 30% ▪ C&I 20% 11% ▪ Residential Mortgage 128% 56% ▪ Other 9% 3% » Interest Rate Sensitivity (9/30/24) : ▪ Principal cash flows, including prepayment estimates 1 • 10/01/24 – 12/31/24 = $88.6 1 million at a weighted average rate of 5.63% • 2025 = $282.4 1 million at a weighted average rate of 5.39% 12 1 Excluding prepayments, 10/01/24 – 12/31/24 = $49.6 million and 2025 = $166.8 million. Loan Portfolio Growth EARNING ASSETS

Investment Portfolio Yield 1.98% 1.56% 2.78% 3.59% 3.53% AOCI/(AOCL) 1 $11.3 $3.3 ($32.4) ($28.2) ($23.2) (4 th Quarter for 2020 - 2023, and 3 rd Quarter for 2024) Average Life: 5.3 years Effective Duration: 3.4 Composition 9/30/24 $361.9 $564.8 $506.2 EARNING ASSETS Millions $486.8 13 $566.6 1 AOCI is accumulated other comprehensive income and (AOCL) is accumulated other comprehensive loss.

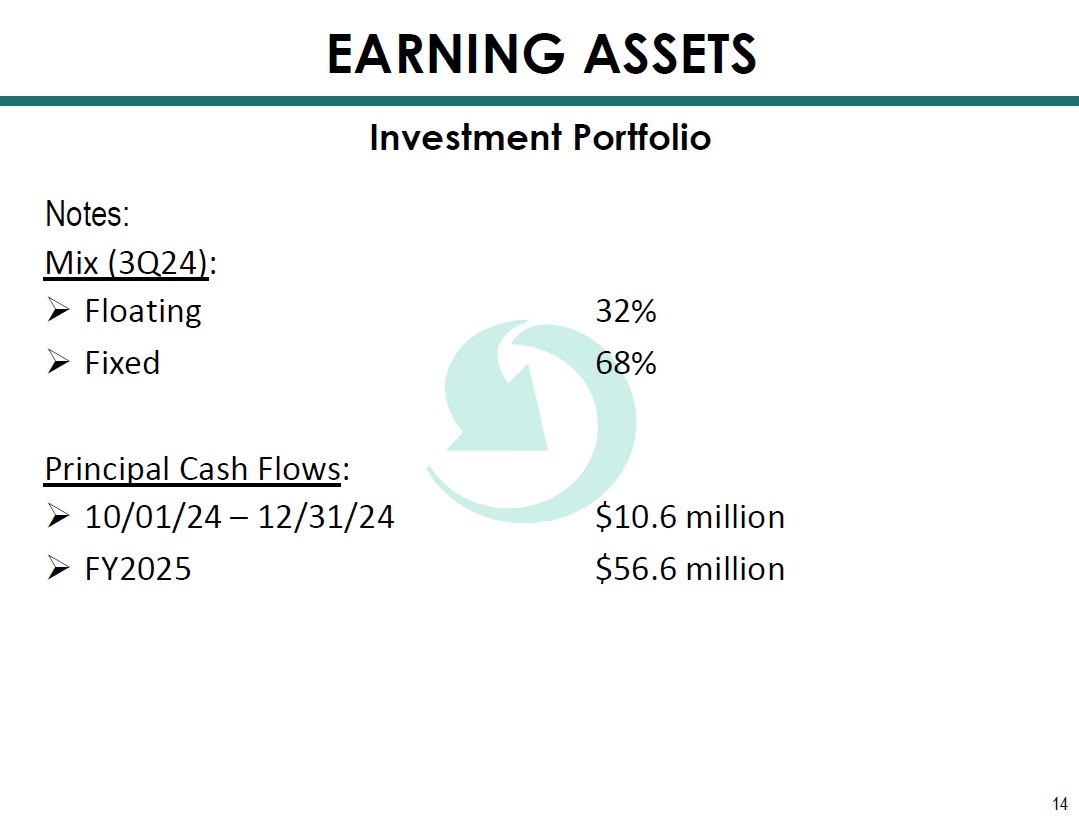

Notes: Mix (3Q24) : » Floating 32% » Fixed 68% Principal Cash Flows : » 10/01/24 – 12/31/24 $10.6 million » FY2025 $56.6 million 14 Investment Portfolio EARNING ASSETS

FUNDING Impacting Lives for Success and Significance

Total Deposit Cost 0.20% 0.11% 0.25% 1.69% 2.03% Non - Interest Bearing 32% 33% 33% 29% 27% Millions $1,230.3 $1,415.5 $1,454.1 $1,573.9 (4 th Quarter for 2020 - 2023 & 3 rd Quarter for 2024) 16 High Quality Deposit Franchise $1,711.0 FUNDING 12/31/2020 12/31/2021 12/31/2022 12/31/2023 09/30/2 024

3Q24 Notes: » 37.5% Cumulative Cycle Beta 1 – Cost of Deposits » 40.2% Cumulative Cycle Beta 1 – Cost of Funds » Uninsured deposits of $492.5 million (30.0% of total), of which $88.3 million (5.4% of total) are public funds that are secured or collateralized ▪ Average balance of customer deposits accounts - $24,281 ▪ Total remaining credit availability in excess of $505.0 million 2 17 High Quality Deposit Franchise FUNDING 1 Trough to peak. 2 Subject to collateral requirements.

18 YTD 2024 » Sources of funds (Millions) Customer Deposits $ 158.8 Customer Cash Management 4.1 Investment Portfolio 19.4 Capital 12.3 Other 7.1 Total $ 201.7 » Uses of funds Loans (includes held held - for - sale) $ 62.1 Short - Term Investments & CDs 77.6 Brokered CDs 25.7 FHLB Borrowings / FFP 36.3 Total $ 201.7 Summary: During 2024, we utilized customer deposit growth to fund loan growth , reduce wholesale funding and enhance our overnight liquidity . Sources and Uses FUNDING

NET INTEREST MARGIN Impacting Lives for Success and Significance

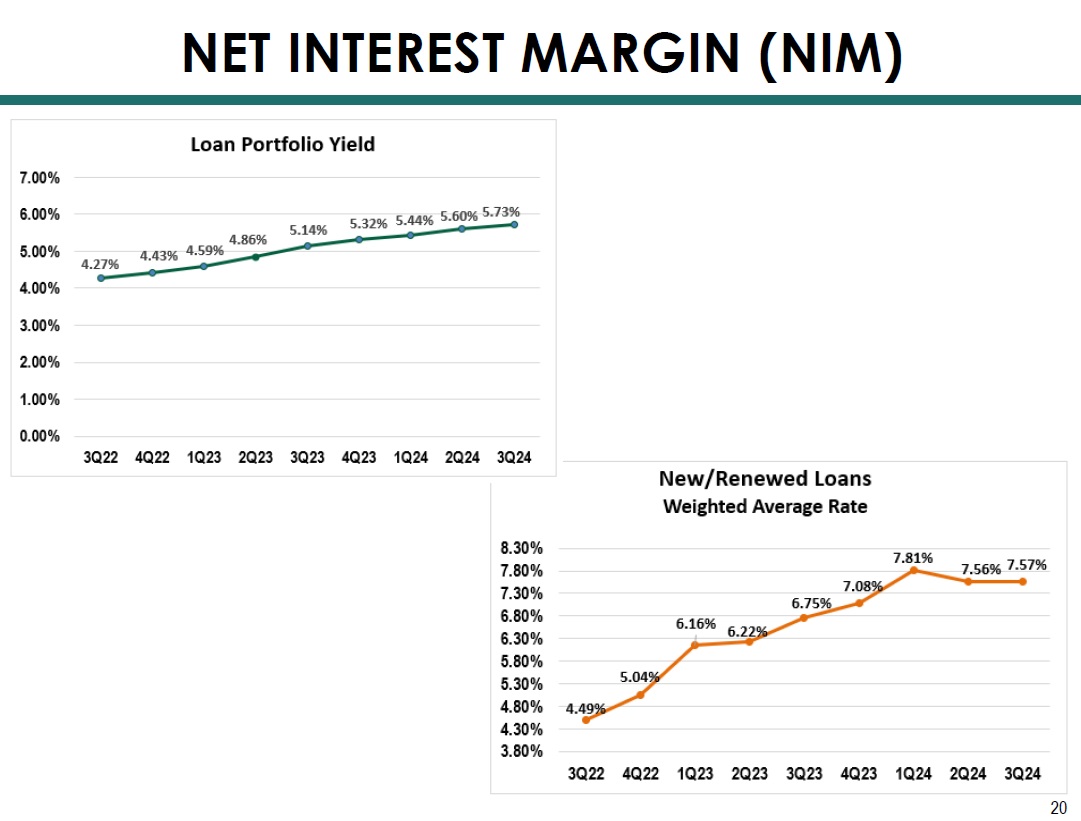

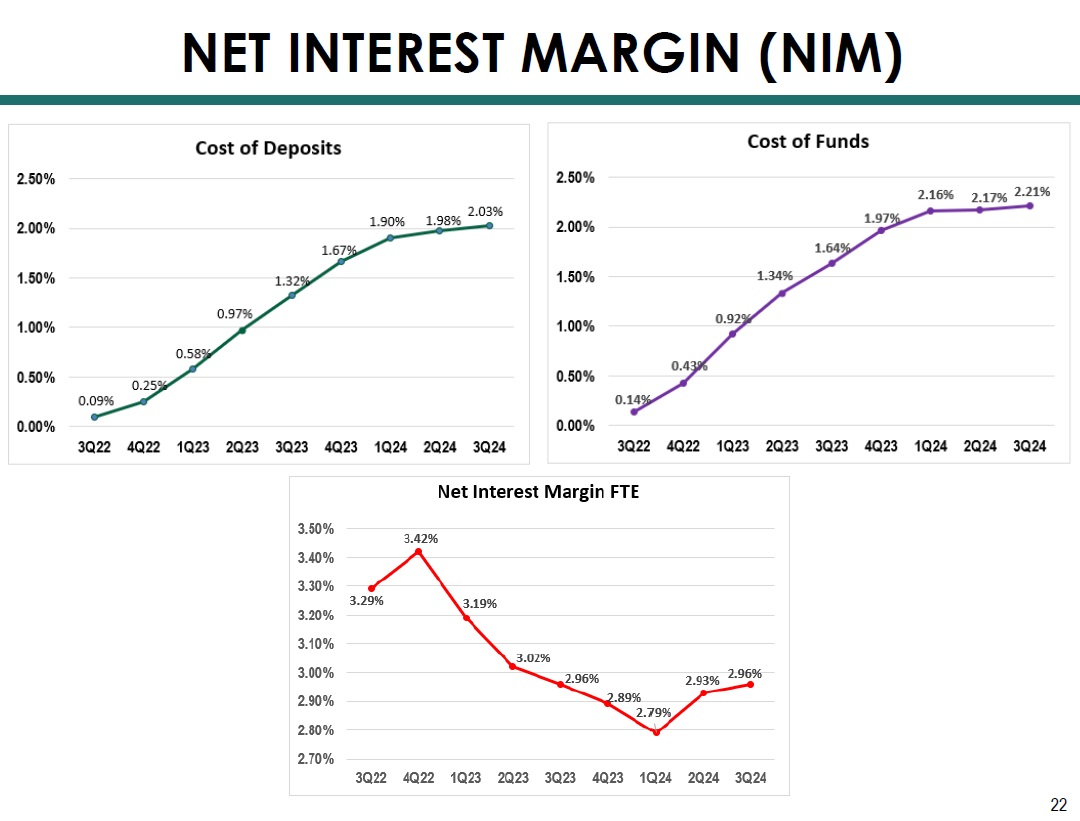

20 NET INTEREST MARGIN (NIM)

21 NET INTEREST MARGIN (NIM)

22 NET INTEREST MARGIN (NIM)

23 Notes: » NIM Inflection began 2Q24 » $12.0 Million Brokered CD • All - in cost of 5.15% • Called on October 31, 2024 » Effective May 5, 2023, entered into a pay - fixed /receive floating interest rate • Notional amount: $150 million • Synthetically converts approximately 13% of the Loan Portfolio from fixed to floating • Pay a fixed rate of 3.58% • Receive a floating rate of overnight SOFR • Matures on May 5, 2026 • 3Q24 Impact ▪ Interest Income $681 thousand ▪ Loan Portfolio Yield 23 bps ▪ Net Interest Margin 15 bps NET INTEREST MARGIN (NIM)

RISK MANAGEMENT Impacting Lives for Success and Significance

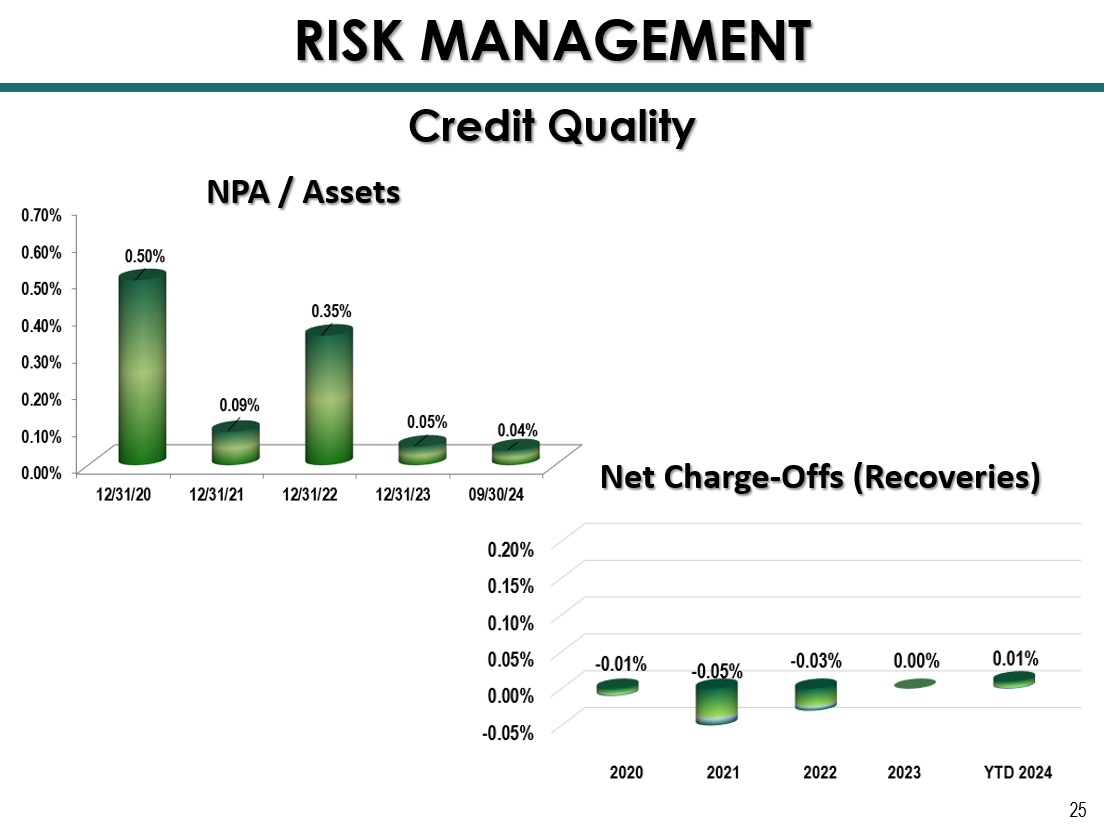

25 Credit Quality RISK MANAGEMENT NPA / Assets Net Charge - Offs (Recoveries)

26 Provision for (Release of) Credit Losses (000s omitted) Credit Quality RISK MANAGEMENT Allowance for Credit Losses on Loans to Loans

3Q24 Notes: » Key Loan Portfolio Sectors 27 • There are only four loans secured by office buildings in excess of 50,000 square feet of rentable space. These four represent $10.7 million in loans outstanding and have a 33% weighted average loan - to - value. Credit Quality RISK MANAGEMENT

28 RISK MANAGEMENT

CAPITAL Impacting Lives for Success and Significance

30 Leverage Ratio (Bank) Total Capital Ratio (Bank) CAPITAL *On 5/14/24, announced a plan to utilize up to $7.1 million of capital to repurchase shares of FCCO’s common stock (5.3% of total shareholders’ equity at the time of the announcement).

31 Tangible Book Value CAPITAL Tangible Common Equity

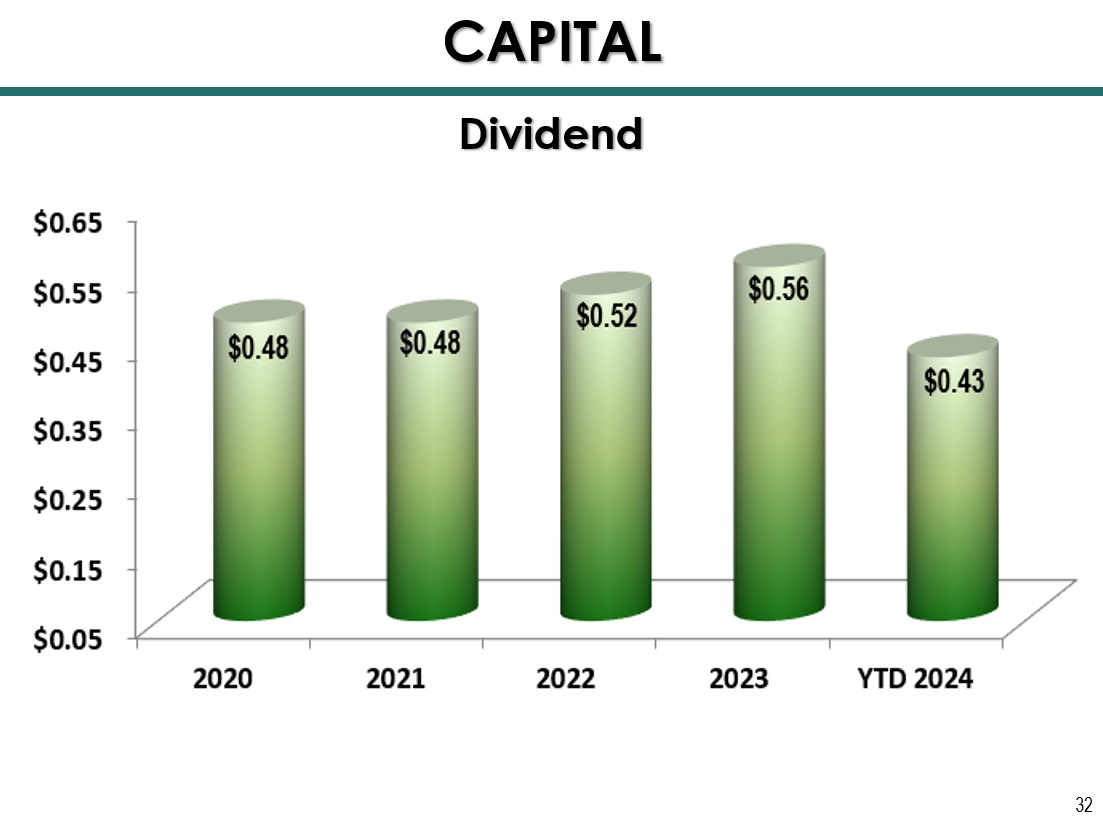

Dividend 32 CAPITAL

NON - INTEREST INCOME HIGHLIGHTS Impacting Lives for Success and Significance

Financial Planning / Investment Advisory Services AUM (millions) 34 NON - INTEREST INCOME HIGHLIGHTS

Financial Planning / Investment Advisory Services Revenue and Pre - Tax Income (thousands) 35 Pre - tax Profit Margin 29.7% 30.5% 33.9% 31.0% 32.8% NON - INTEREST INCOME HIGHLIGHTS

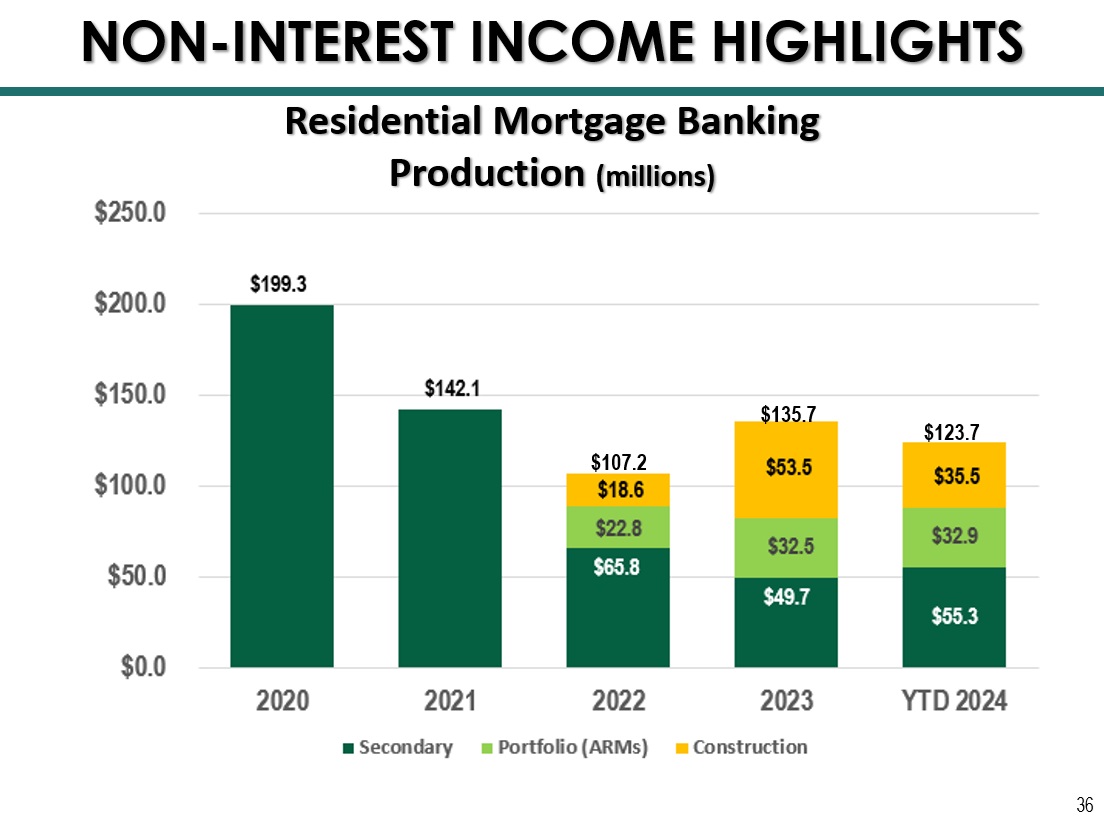

36 Residential Mortgage Banking Production (millions) NON - INTEREST INCOME HIGHLIGHTS $123.7 $107.2 $135.7

Pre - tax Profit Margin 31.6% 11.9% 3.6% 34.3% 59.4% Residential Mortgage Banking Revenue and Pre - Tax Income (000’s omitted) 37 $7,294.7 $ 5,327.8 $6,708.6 1 $3,763.8 1 $5,201.3 1 Note: Pre - tax net income does not include fund transfer pricing or ACL allocations. 1 Includes mortgage late charges and other mortgage revenue. NON - INTEREST INCOME HIGHLIGHTS

REVENUE Impacting Lives for Success and Significance

39 (Millions) $53.1 $56.2 $60.6 $59.5 Total Revenue 1, 2 Strength in Diversity of Revenue REVENUE 1 Adjusted for PPP deferred fees. 2 Adjusted for Securities Gains/Losses. 2 1 $48.6

40 (Thousands) $15,216 $16,982 $15,261 Total Revenue 1 Strength in Diversity of Revenue 1 Adjusted for Securities Gains/Losses. 1 $15,226 REVENUE $16,336

NON - INTEREST EXPENSE Impacting Lives for Success and Significance

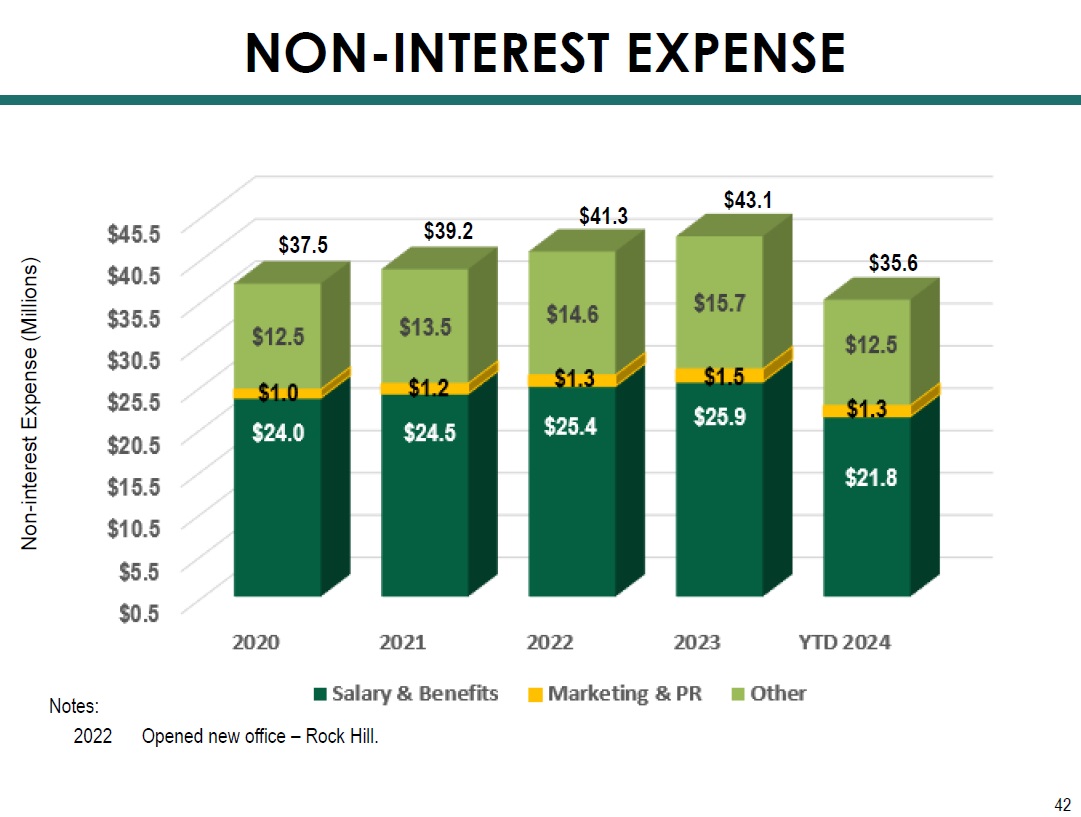

NON - INTEREST EXPENSE 42 Non - interest Expense (Millions) $37.5 $39.2 $35.6 Notes: 2022 Opened new office – Rock Hill. $41.3 $43.1

NON - INTEREST EXPENSE 43 Non - interest Expense (Millions) $11.3 $12.0 NOTE: Closed downtown banking office at 771 Broad Street, Augusta, GA, as of June 27, 2024. Cost savings are estimated to be $327,000 annually going forward. $10.7 $11.8 $11.8

NET INCOME Impacting Lives for Success and Significance

1 Core net income and EPS exclude gains (losses) on sale of securities and bank premises, write - downs on bank premises held - for - sa le, non - recurring BOLI income, gains on insurance proceeds, and collection of summary judgements on two loans charged off at an FCCO acquired bank. S ee non - GAAP reconciliation on pages 48 and 49. 2 Includes $738 thousand in non - recurring PPP - related fee income. 3 Includes $2.955 million in non - recurring PPP - related fee income. 4 Includes $46 thousand in non - recurring PPP - related fee income. 5 This compares to YTD results of $9,423 thousand in Core Net Income and $1.23 in Core EPS. 6 This compares to YTD results of $11,623 thousand in pre - tax pre - provision earnings. Thousands Core Net Income 1 / Core EPS 1 / Pre - Tax Pre - Provision Earnings 45 NET INCOME 2 3 2 3 4 4 5 6

FORWARD - LOOKING STATEMENTS 46 SAFE HARBOR STATEMENT – In this presentation, unless the context suggests otherwise, references to the “Company” or “FCCO” refer to First Community Corporation and references to “we,” “us,” and “our” mean the combined business of the Company, First Community Bank (or FCB) and its wholly - owned subsidiaries . This presentation and other written reports and statements made by us and our management from time to time may contain forward - looking statements . These statements include, without limitation, statements regarding our operating philosophy, growth plans and opportunities, strategies and financial performance, industry and economic trends and estimates and assumptions underlying accounting policies . Words such as “believe,” “expect,” “anticipate,” “intend,” “target,” “estimate,” “focus,” “continue,” “positions,” “plan,” “predict,” “project,” “forecast,” “guidance,” “goal,” “objective,” “prospects,” “possible” or “potential,” by future conditional verbs such as “assume,” “will,” “would,” “should,” “could” or “may,” or by variations of such words or by similar expressions are intended to identify such forward - looking statements . These forward - looking statements are subject to numerous assumptions, risks and uncertainties, which change over time, are difficult to predict and are generally beyond our control . Although we believe that the assumptions underlying the forward - looking statements are reasonable, any of the assumptions could prove to be inaccurate . Therefore, we can give no assurance that the results contemplated in the forward - looking statements will be realized . The inclusion of this forward - looking information should not be construed as a representation by the Company or any other person that such future events, plans, or expectations will occur or be achieved . In addition to factors previously disclosed in the reports filed by us with the US Securities and Exchange Commission (the “SEC”), additional risks and uncertainties may include, but are not limited to : ( 1 ) competitive pressures among depository and other financial institutions may increase significantly and have an effect on pricing, spending, third - party relationships and revenues ; ( 2 ) the strength of the US economy in general and the strength of the local economies in which we conduct operations may be different than expected, including unemployment levels, supply chain disruptions, higher inflation, and slowdowns in economic growth ; ( 3 ) the rate of delinquencies and amounts of charge - offs, the level of allowance for credit loss, the rates of loan growth, or adverse changes in asset quality in our loan portfolio, which may result in increased credit risk - related losses and expenses ; ( 4 ) changes in legislation, regulation, policies, or administrative practices, whether by judicial, governmental, or legislative action ; ( 5 ) adverse conditions in the stock market, the public debt markets and other capital markets (including changes in interest rate conditions) could have a negative impact on the Company ; ( 6 ) technology and cybersecurity risks, including potential business disruptions, reputational risks, and financial losses, associated with potential attacks on or failures by our computer systems and computer systems of our vendors and other third parties ; ( 7 ) inflation and changes in the interest rate environment that reduce our margins or reduce the fair value of financial instruments ; and ( 8 ) the ultimate ramifications, if any, of the 2023 and 2024 bank failures with respect to increased regulatory supervision and any increases in the costs of doing business . Additional factors that could cause results to differ materially from those described in the forward - looking statements can be found in our reports (such as the annual report on Form 10 - K, quarterly reports on Form 10 - Q and current reports on Form 8 - K) filed with the SEC and available at the SEC’s internet site (http : //www . sec . gov) . All subsequent written and oral forward - looking statements by us or any person acting on our behalf is expressly qualified in its entirety by the cautionary statements above . The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with other cautionary statements that are included herein . We undertake no obligation to update or revise any forward - looking statement, whether as a result of new information, future events or otherwise, except as required by law .

NON - GAAP FINANCIAL MEASURES The Bank Behind Your Business 47 NON - GAAP FINANCIAL MEASURES – This presentation contains certain non - GAAP financial measures that are not in accordance with US generally accepted accounting principles (GAAP) . We use certain non - GAAP financial measures to provide meaningful, supplemental information regarding our operational results and to enhance investors’ overall understanding of our financial performance . The limitations associated with non - GAAP financial measures include the risk that persons might disagree as to the appropriateness of items comprising these measures and that different companies might calculate these measures differently . These disclosures should not be considered an alternative to our GAAP results . See the end of this presentation for a non - GAAP financial measures reconciliation to the most directly comparable GAAP financial measure .

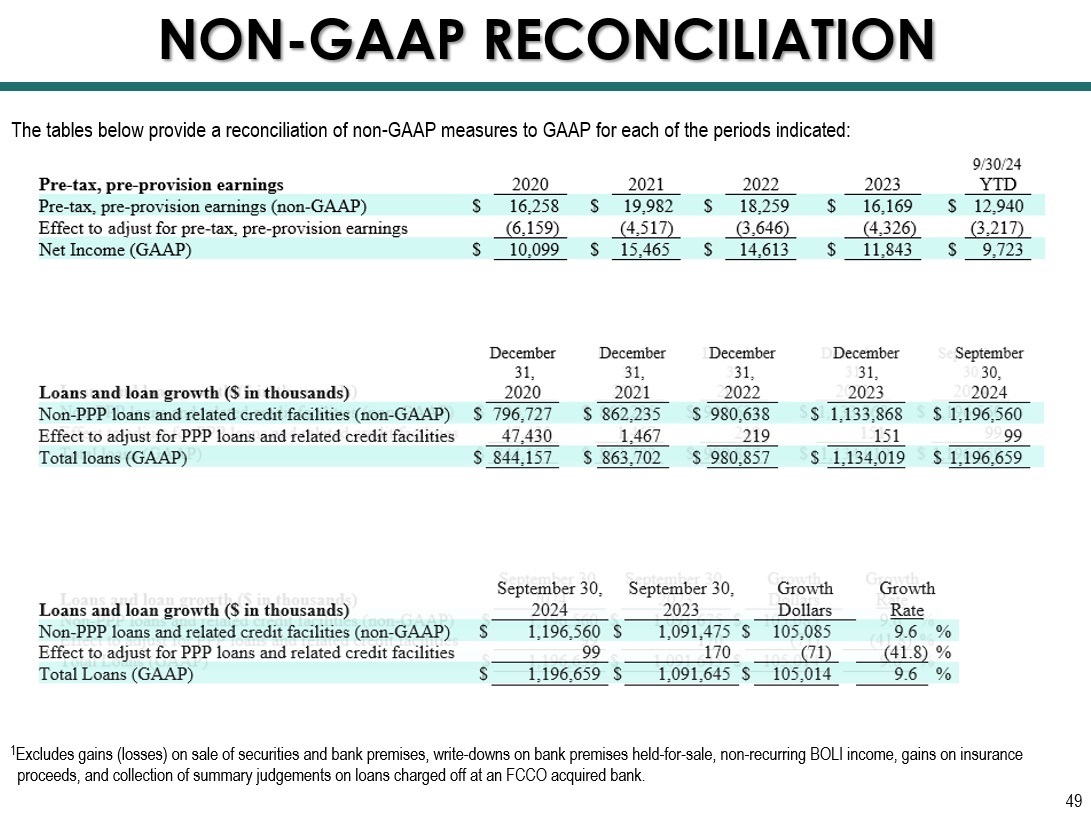

NON - GAAP RECONCILIATION 48 The tables below provide a reconciliation of non - GAAP measures to GAAP for each of the periods indicated:

NON - GAAP RECONCILIATION 49 1 Excludes gains (losses) on sale of securities and bank premises, write - downs on bank premises held - for - sale, non - recurring BOLI income, gains on insuranc e proceeds, and collection of summary judgements on loans charged off at an FCCO acquired bank. The tables below provide a reconciliation of non - GAAP measures to GAAP for each of the periods indicated: