EX.__._

THIS IS NOT A SOLICITATION OF ACCEPTANCE OR REJECTION OF THE SEVENTH AMENDED PLAN. ACCEPTANCES OR REJECTIONS MAY NOT BE SOLICITED UNTIL A DISCLOSURE STATEMENT HAS BEEN APPROVED BY THE BANKRUPTCY COURT. THIS DISCLOSURE STATEMENT IS BEING SUBMITTED FOR APPROVAL BUT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT.

UNITED STATES BANKRUPTCY COURT

DISTRICT OF DELAWARE

| : | ||

| In re | : | Chapter 11 |

| : | ||

| WASHINGTON MUTUAL, INC., et al. , 1 | : | |

| : | Case No. 08-12229 (MFW) | |

| : | ||

| Debtors. | : | (Jointly Administered) |

| : | ||

| : |

DISCLOSURE STATEMENT FOR THE SEVENTH AMENDED

JOINT PLAN OF AFFILIATED DEBTORS PURSUANT TO

CHAPTER 11 OF THE UNITED STATES BANKRUPTCY CODE

WEIL, GOTSHAL & MANGES LLP

767 Fifth Avenue

New York, New York 10153

(212) 310-8000

-and-

RICHARDS, LAYTON & FINGER, P.A.

One Rodney Square

920 North King Street

Wilmington, Delaware 19801

(302) 651-7700

Attorneys for Debtors

and Debtors in Possession

Dated: December 12, 2011

1 The Debtors in these chapter 11 cases along with the last four digits of each Debtor’s federal tax identification number are: (i) Washington Mutual, Inc. (3725); and (ii) WMI Investment Corp. (5395). The Debtors’ principal offices are located at 925 Fourth Avenue, Suite 2500, Seattle, Washington 98104.

TABLE OF CONTENTS

| I. | INTRODUCTION | 1 | |||

| A. | Background | 1 | |||

| B. | The Sixth Amended Plan and the January Opinion | 2 | |||

| C. | The Modified Sixth Amended Plan and the September Opinion | 3 | |||

| D. | The Equity Committee Standing Motion | 4 | |||

| E. | The September Opinion Appeals | 5 | |||

| F. | Mediation | 5 | |||

| G. | The Seventh Amended Plan Incorporates Modifications Resulting From the Mediation Among the Debtors, the Creditors’ Committee, the Equity Committee, AAOC, and Certain Other Creditor Constituencies | 6 | |||

| 1. | Issuance of Runoff Notes to Certain Creditors and Distribution of Reorganized Common Stock to Certain Holders of Equity Interests | 11 | |||

| 2. | Commitment by AAOC to Provide Exit Financing | 12 | |||

| 3. | Resolution of Certain Governance-Related Issues | 13 | |||

| H. | The Seventh Amended Plan | 13 | |||

| 1. | Plan Modifications Consistent with the September Opinion | 14 | |||

| I. | The Global Settlement Agreement | 16 | |||

| 1. | Background | 16 | |||

| 2. | Bankruptcy Court Approval of the Global Settlement Agreement | 17 | |||

| 3. | Subsequent Amendments to the Global Settlement Agreement and Bankruptcy Court Approval Thereof | 17 | |||

| II. | THE DISCLOSURE STATEMENT | 18 | |||

| III. | GENERAL OVERVIEW OF THE SEVENTH AMENDED PLAN | 19 | |||

| A. | Chapter 11 Overview | 19 | |||

| B. | Significant Features of the Seventh Amended Plan | 19 | |||

| 1. | Reorganization | 19 | |||

| 2. | Credit Facility | 24 | |||

| 3. | Creditor Cash | 26 | |||

| 4. | The Liquidating Trust | 27 | |||

| 5. | Reorganized WMI’s Board of Directors | 31 | |||

| 6. | General Overview of Treatment Pursuant to the Seventh Amended Plan of Allowed Claims and Equity Interests | 31 | |||

| 7. | Releases | 48 | |||

| C. | Approximate Amounts of Certain Fees and Expenses Incurred, Payment of Which May Be Requested Pursuant to Sections 31.12 and 41.18 of the Seventh Amended Plan | 48 | |||

| 1. | Section 31.12 of the Seventh Amended Plan | 48 | |||

i

TABLE OF CONTENTS

| 2. | Section 41.18 of the Seventh Amended Plan | 48 | |||

| IV. | Overview of the debtors’ operations | 48 | |||

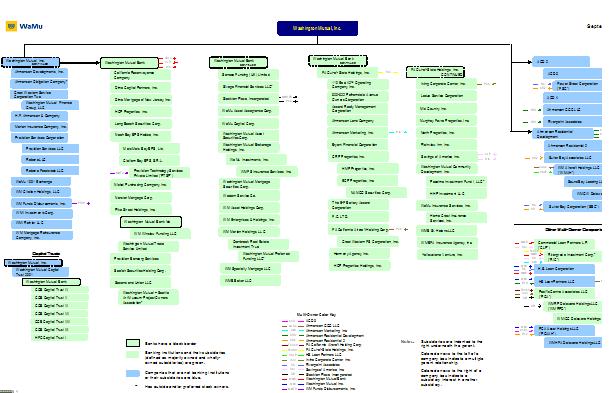

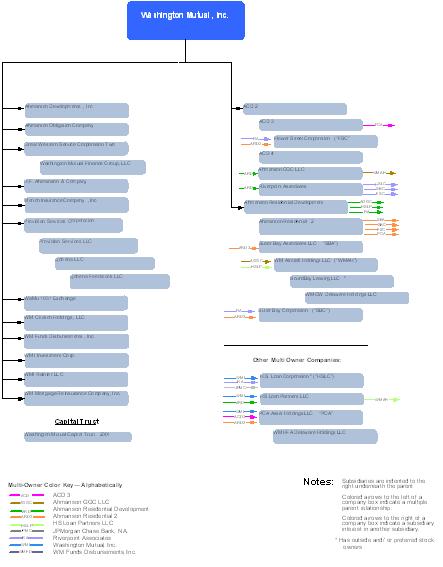

| A. | The Debtors’ Corporate History and Past and Current Organizational Structure and Assets | 48 | |||

| 1. | Overview | 48 | |||

| 2. | List of WMI’s Current Directors | 49 | |||

| 3. | WMI’s Consolidated Corporate Organizational Structure | 49 | |||

| 4. | Analysis of Subsidiary Equity | 54 | |||

| 5. | Assets of WMI Investment | 59 | |||

| 6. | WM Mortgage Reinsurance Company, Inc. (“WMMRC”) | 60 | |||

| 7. | Assets of WMI’s Non-Debtor Subsidiaries, Other than WMMRC | 61 | |||

| 8. | WMI Non-Debtor Subsidiary Balance Sheets | 68 | |||

| 9. | Other Assets | 72 | |||

| B. | The Debtors’ Capital Structure And Significant Prepetition Indebtedness | 74 | |||

| 1. | Overview | 74 | |||

| 2. | Senior Notes | 74 | |||

| 3. | Senior Subordinated Notes | 76 | |||

| 4. | Guarantees of Commercial Capital Bank, Inc. Securities (the “CCB Guarantees”) | 77 | |||

| 5. | Junior Subordinated Debentures Related to the PIERS Claims | 77 | |||

| 6. | Preferred Equity Interests | 79 | |||

| 7. | Common Stock | 81 | |||

| V. | overview of the chapter 11 cases | 81 | |||

| A. | Significant Events Leading To Commencement Of The Chapter 11 Cases | 81 | |||

| B. | The Chapter 11 Cases | 82 | |||

| 1. | Certain Administrative Matters | 82 | |||

| 2. | Litigation with the FDIC and JPMC | 84 | |||

| 3. | The Global Settlement Agreement | 88 | |||

| 4. | The Appointment of the Examiner and the Examiner’s Report | 94 | |||

| 5. | Certain Significant Litigations | 96 | |||

| 6. | Certain Other Litigations and Claims | 110 | |||

| 7. | Government Investigations and Hearings | 125 | |||

| 8. | Employee Benefits | 126 | |||

| VI. | SUMMARY OF THE SEVENTH AMENDED PLAN | 130 | |||

| A. | Provisions For Payment Of Administrative Expense Claims And Priority Tax Claims Under The Seventh Amended Plan | 130 | |||

ii

TABLE OF CONTENTS

| 1. | Administrative Expense Claims | 130 | |||

| 2. | Professional Compensation and Reimbursement Claims | 131 | |||

| 3. | Priority Tax Claims | 132 | |||

| 4. | Statutory Fees | 132 | |||

| B. | Classification Of Claims And Equity Interests Under The Seventh Amended Plan | 132 | |||

| 1. | Priority Non-Tax Claims (Class 1) | 133 | |||

| 2. | Senior Notes Claims (Class 2) | 133 | |||

| 3. | Senior Subordinated Notes Claims (Class 3) | 135 | |||

| 4. | WMI Medical Plan Claims (Class 4) | 137 | |||

| 5. | JPMC Rabbi Trust/Policy Claims (Class 5) | 137 | |||

| 6. | Other Benefit Plan Claims (Class 6) | 138 | |||

| 7. | Qualified Plan Claims (Class 7) | 138 | |||

| 8. | WMB Vendor Claims (Class 8) | 138 | |||

| 9. | Visa Claims (Class 9) | 139 | |||

| 10. | Bond Claims (Class 10) | 139 | |||

| 11. | WMI Vendor Claims (Class 11) | 139 | |||

| 12. | General Unsecured Claims (Class 12) | 139 | |||

| 13. | Late-Filed Claims (Class 12A) | 141 | |||

| 14. | Convenience Claims (Class 13) | 142 | |||

| 15. | CCB-1 Guarantees Claims (Class 14) | 142 | |||

| 16. | CCB-2 Guarantees Claims (Class 15) | 144 | |||

| 17. | PIERS Claims (Class 16) | 146 | |||

| 18. | WMB Notes Claims (Class 17) | 148 | |||

| 19. | Subordinated Claims (Class 18) | 150 | |||

| 20. | Preferred Equity Interests (Class 19) | 151 | |||

| 21. | Dime Warrants (Class 21) | 152 | |||

| 22. | Common Equity Interests (Class 22) | 153 | |||

| C. | Provision For Treatment Of Disputed Claims and Disputed Equity Interests | 153 | |||

| 1. | Objections to Claims; Prosecution of Disputed Claims and Disputed Equity Interests | 153 | |||

| 2. | Estimation of Claims | 154 | |||

| 3. | Payments and Distributions on Disputed Claims and Disputed Equity Interests | 154 | |||

| D. | Liquidating Trust | 157 | |||

| 1. | Execution of the Liquidating Trust Agreement | 157 | |||

iii

TABLE OF CONTENTS

| 2. | Purpose of the Liquidating Trust | 157 | |||

| 3. | Liquidating Trust Assets | 157 | |||

| 4. | Administration of the Liquidating Trust | 157 | |||

| 5. | The Liquidating Trustee | 157 | |||

| 6. | Role of the Liquidating Trustee | 158 | |||

| 7. | Liquidating Trustee’s Tax Power for Debtors | 158 | |||

| 8. | Transferability of Liquidating Trust Interests | 159 | |||

| 9. | Cash | 159 | |||

| 10. | Distribution of Liquidating Trust Assets | 159 | |||

| 11. | Costs and Expenses of the Liquidating Trust | 159 | |||

| 12. | Compensation of the Liquidating Trustee | 160 | |||

| 13. | Retention of Professionals/Employees by the Liquidating Trustee | 160 | |||

| 14. | Federal Income Tax Treatment of the Liquidating Trust | 160 | |||

| 15. | Indemnification of Liquidating Trustee | 163 | |||

| 16. | Privileges and Obligation to Respond to Ongoing Investigations | 163 | |||

| E. | Prosecution And Extinguishment Of Claims Held By The Debtors | 164 | |||

| 1. | Prosecution of Claims | 164 | |||

| F. | Seventh Amended Plan Provisions Governing Distributions | 164 | |||

| 1. | Time and Manner of Distributions | 164 | |||

| 2. | Timeliness of Payments | 165 | |||

| 3. | Distributions by the Disbursing Agent | 165 | |||

| 4. | Manner of Payment under the Seventh Amended Plan | 165 | |||

| 5. | Delivery of Distributions | 165 | |||

| 6. | Undeliverable/Reserved Distributions | 166 | |||

| 7. | Withholding and Reporting Requirements | 168 | |||

| 8. | Time Bar to Cash Payments | 168 | |||

| 9. | Distributions After Effective Date | 169 | |||

| 10. | Setoffs | 169 | |||

| 11. | Allocation of Plan Distributions Between Principal and Interest | 169 | |||

| 12. | Payment of Trustee Fees and Expenses | 169 | |||

| 13. | Runoff Notes | 170 | |||

| G. | Means Of Implementation Of The Seventh Amended Plan | 171 | |||

| 1. | Incorporation and Enforcement of the Global Settlement Agreement | 171 | |||

| 2. | Intercompany Claims | 171 | |||

| 3. | Merger/Dissolution/Consolidation | 171 | |||

iv

TABLE OF CONTENTS

| 4. | Cancellation of Existing Securities and Agreements | 171 | |||

| 5. | Claims of Subordination | 172 | |||

| 6. | Surrender of Instruments | 172 | |||

| 7. | Issuance of Runoff Notes, Liquidating Trust Interests and Reorganized Common Stock | 173 | |||

| 8. | Exemption from Securities Laws | 173 | |||

| 9. | Hart-Scott-Rodino Compliance | 173 | |||

| 10. | Fractional Stock or Other Distributions | 173 | |||

| 11. | Credit Facility | 173 | |||

| 12. | Creditors’ Committee And Equity Committee | 174 | |||

| H. | Executory Contracts And Unexpired Leases | 175 | |||

| 1. | Rejection or Assumption of Remaining Executory Contracts and Unexpired Leases | 175 | |||

| 2. | Approval of Rejection or Assumption of Executory Contracts and Unexpired Leases | 175 | |||

| 3. | Inclusiveness | 175 | |||

| 4. | Cure of Defaults | 176 | |||

| 5. | Rejection Damage Claims | 176 | |||

| 6. | Indemnification and Reimbursement Obligations | 176 | |||

| 7. | Termination of Benefit Plans | 176 | |||

| 8. | Termination of Vendor Stipulation | 177 | |||

| I. | Rights and Powers of Disbursing Agent | 177 | |||

| 1. | Exculpation | 177 | |||

| 2. | Powers of the Disbursing Agent | 177 | |||

| 3. | Fees and Expenses Incurred From and After the Effective Date | 178 | |||

| J. | Conditions Precedent to Effective Date of the Seventh Amended Plan | 178 | |||

| 1. | Conditions Precedent to Confirmation of the Seventh Amended Plan | 178 | |||

| 2. | Waiver of Conditions Precedent to Confirmation | 179 | |||

| K. | Conditions Precedent to Effective Date of the Seventh Amended Plan | 179 | |||

| 1. | Conditions Precedent to Effective Date of the Seventh Amended Plan | 179 | |||

| 2. | Waiver of Conditions Precedent | 180 | |||

| L. | Retention of Jurisdiction | 180 | |||

| M. | Modification, Revocation, or Withdrawal of the Seventh Amended Plan | 182 | |||

| 1. | Modification of Plan | 182 | |||

| 2. | Revocation or Withdrawal | 182 | |||

| 3. | Amendment of Plan Documents | 182 | |||

v

TABLE OF CONTENTS

| 4. | No Admission of Liability | 182 | |||

| N. | Corporate Governance and Management of the Reorganized Debtors | 183 | |||

| 1. | Corporate Action | 183 | |||

| 2. | Reincorporation | 183 | |||

| 3. | Amendment of Articles of Incorporation and By-Laws | 184 | |||

| 4. | Directors of the Reorganized Debtors | 184 | |||

| 5. | Officers of the Reorganized Debtors | 184 | |||

| O. | Miscellaneous Provisions | 184 | |||

| 1. | Title to Assets | 184 | |||

| 2. | Discharge and Release of Claims and Termination of Equity Interests | 184 | |||

| 3. | Injunction on Claims | 186 | |||

| 4. | Integral to Plan | 186 | |||

| 5. | Releases by the Debtors, the Creditors’ Committee and the Equity Committee | 187 | |||

| 6. | Releases by Holders of Claims and Equity Interests | 187 | |||

| 7. | Injunction Related to Releases | 190 | |||

| 8. | Exculpation | 190 | |||

| 9. | Bar Order | 191 | |||

| 10. | Deemed Consent | 191 | |||

| 11. | No Waiver | 192 | |||

| 12. | Supplemental Injunction | 192 | |||

| 13. | Term of Existing Injunctions or Stays | 193 | |||

| 14. | Payment of Statutory Fees | 193 | |||

| 15. | Post-Effective Date Fees and Expenses | 193 | |||

| 16. | Exemption from Transfer Taxes | 193 | |||

| 17. | Withdrawal of Equity Committee Proceedings | 193 | |||

| 18. | Payment of Fees and Expenses of Certain Creditors | 194 | |||

| 19. | Securities Litigations Documents | 194 | |||

| 20. | Severability | 194 | |||

| 21. | Governing Law | 195 | |||

| 22. | Closing of Cases | 195 | |||

| VII. | FINANCIAL INFORMATION AND PROJECTIONS | 195 | |||

| A. | Projected Financial Information | 195 | |||

| B. | Projected Statements of Operations (Unaudited) | 198 | |||

vi

TABLE OF CONTENTS

| C. | Projected Balance Sheets (Unaudited) | 199 | |||

| D. | Projected Statements of Cash Flow – Indirect Method (Unaudited) | 200 | |||

| E. | Projected Statements of Cash Flow – Direct Method (Unaudited) | 201 | |||

| F. | Assumptions to the Projections | 202 | |||

| 1. | Projections | 202 | |||

| 2. | Key Assumptions | 202 | |||

| VIII. | CERTAIN FEDERAL INCOME TAX CONSEQUENCES OF THE SEVENTH AMENDED PLAN | 205 | |||

| A. | Consequences to the Debtors | 206 | |||

| 1. | Cancellation of Debt | 208 | |||

| 2. | Potential Limitations on NOL Carryforwards and Other Tax Attributes | 208 | |||

| 3. | Debt Status of the Second Lien Runoff Notes | 211 | |||

| 4. | Alternative Minimum Tax | 212 | |||

| 5. | Transfer of Assets to the Liquidating Trust | 212 | |||

| B. | Consequences to Holders of Certain Claims and Equity Interests | 213 | |||

| 1. | Allowed Convenience Claims and Priority Non-Tax Claims | 214 | |||

| 2. | Certain Unsecured Claims, Subordinated Claims and Equity Interests | 214 | |||

| 3. | Ownership and Disposition of Runoff Notes | 218 | |||

| 4. | Ownership and Disposition of Reorganized Common Stock | 225 | |||

| C. | Tax Treatment of Liquidating Trust and Holders of Beneficial Interests | 226 | |||

| 1. | Classification of the Liquidating Trust | 226 | |||

| 2. | General Tax Reporting by the Liquidating Trust and its Beneficiaries | 226 | |||

| 3. | Tax Reporting for Assets Allocable to Disputed Claims and Distributions from the Liquidating Trust Claims Reserve | 228 | |||

| D. | Tax Reporting for Assets Allocable to the Disputed Equity Escrow and Distributions from the Disputed Equity Escrow | 229 | |||

| E. | Information Reporting and Withholding. | 229 | |||

| IX. | CONSEQUENCES UNDER THE FEDERAL SECURITIES LAWS | 230 | |||

| A. | General Application of section 1145 to New Interests | 230 | |||

| B. | Reorganized WMI Interests | 231 | |||

| 1. | Transfer Restrictions Under the Securities Laws | 231 | |||

| 2. | Listing and SEC Reporting | 232 | |||

| 3. | Transfer Restrictions under the New Certificate of Incorporation of Reorganized WMI with respect to the Reorganized Common Stock | 232 | |||

vii

TABLE OF CONTENTS

| 4. | Transfer Restrictions under the Indenture for the Second Lien Runoff Notes | 233 | |||

| C. | Liquidating Trust Interests | 233 | |||

| 1. | Transfer Restrictions Under the Securities Laws | 233 | |||

| 2. | Listing and SEC Reporting | 233 | |||

| X. | CERTAIN FACTORS TO BE CONSIDERED | 234 | |||

| A. | Certain Bankruptcy Law Considerations | 234 | |||

| 1. | Risk of Non-Confirmation of the Seventh Amended Plan | 234 | |||

| 2. | Non-Consensual Confirmation | 234 | |||

| 3. | Risk of Non-Occurrence of the Effective Date | 234 | |||

| 4. | Conversion into Chapter 7 Cases | 234 | |||

| B. | Additional Factors To Be Considered | 234 | |||

| 1. | The Debtors Have No Duty to Update | 234 | |||

| 2. | No Representations Outside This Disclosure Statement Are Authorized | 235 | |||

| 3. | Claims Could Be More Than Projected | 235 | |||

| 4. | The Debtors Estimate That a Three (3) Months’ Delay in Confirmation Will Eliminate All Recoveries for Holders of Allowed PIERS Claims, and That Additional Delay Will Begin to Reduce, and May Eliminate, Recoveries for Holders of Allowed Claims That Are Senior in Recovery to Holders of Allowed PIERS Claims | 235 | |||

| 5. | Projections and Other Forward-Looking Statements Are Not Assured, and Actual Results May Vary | 235 | |||

| 6. | Non-Recourse Nature of the Runoff Notes; Full Satisfaction of Principal and Interest due on the Runoff Notes Is Not Assured | 236 | |||

| 7. | The Runoff Notes Will Be Effectively Subordinate to the Liabilities of WMMRC | 236 | |||

| 8. | Any Trading Market that Develops for the Runoff Notes May Not Be Liquid, and There are Restrictions on Transfers of the Second Lien Runoff Notes | 236 | |||

| 9. | Holders of Runoff Notes May Be Required to Pay U.S. Federal Income Tax on Such Notes Even if Reorganized WMI Does Not Pay Cash Interest | 237 | |||

| 10. | No Legal or Tax Advice is Provided to You By This Disclosure Statement | 237 | |||

| 11. | No Admission Made | 237 | |||

| 12. | Certain Tax Consequences | 237 | |||

| 13. | Debtors Could Withdraw Plan | 237 | |||

viii

TABLE OF CONTENTS

| 14. | Subject to Certain Limited Exceptions, the Liquidating Trust Interests Are Not Transferable or Assignable | 237 | |||

| 15. | Ability to Transfer Reorganized Common Stock | 237 | |||

| XI. | VOTING AND ELECTION PROCEDURES | 238 | |||

| A. | Solicitation of Votes With Respect to the Seventh Amended Plan | 238 | |||

| 1. | The Debtors Will Solicit Votes from Holders of Claims in Classes 2, 3, 5, 6, 8, 9, 10, 11, 12, 12A, 13, 14, 15, 16, 18, 19, and 22 | 238 | |||

| 2. | Classes 1, 4, 7, and 17A Will Be Deemed to Accept the Seventh Amended Plan, While Classes 17B and 21 Will Be Deemed to Reject | 239 | |||

| 3. | holders of Disputed Claims Are Not Entitled to Vote | 240 | |||

| 4. | Ballots | 240 | |||

| B. | Solicitation of Elections With Respect to the Seventh Amended Plan | 241 | |||

| 1. | Certain Holders of Claims and Equity Interests Must Elect to Be Bound by the Non-Debtor Release Provision (Section 41.6 of the Seventh Amended Plan) to Receive a Distribution Pursuant to the Seventh Amended Plan | 241 | |||

| 2. | Solicitation of Runoff Notes Elections | 245 | |||

| 3. | Solicitation of Reorganized Common Stock Election | 246 | |||

| 4. | Voting and Election Procedures | 247 | |||

| 5. | Notice to Holders of Publicly Traded Securities | 248 | |||

| XII. | CONFIRMATION OF THE SEVENTH AMENDED PLAN | 249 | |||

| A. | The Confirmation Hearing | 249 | |||

| B. | Objections To Confirmation | 249 | |||

| C. | Requirements For Confirmation Of The Seventh Amended Plan | 250 | |||

| 1. | Requirements of Section 1129(a) of the Bankruptcy Code | 250 | |||

| 2. | Requirements of Section 1129(b) of the Bankruptcy Code | 254 | |||

| XIII. | ALTERNATIVES TO THE SEVENTH AMENDED PLAN | 255 | |||

| A. | Liquidation Under Chapter 7 | 256 | |||

| B. | Alternative Chapter 11 Plans | 256 | |||

| XIV. | CONCLUSION | 257 | |||

EXHIBIT A: Seventh Amended Plan

EXHIBIT B: Disclosure Statement Order

EXHIBIT C: Updated Liquidation Analysis

ix

THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT (THE “DISCLOSURE STATEMENT”)1 IS INCLUDED HEREIN FOR PURPOSES OF SOLICITING ACCEPTANCES AND ELECTIONS WITH RESPECT TO OF THE SEVENTH AMENDED JOINT PLAN OF WASHINGTON MUTUAL, INC. AND WMI INVESTMENT CORP. AND MAY NOT BE RELIED UPON FOR ANY PURPOSE OTHER THAN TO DETERMINE HOW TO VOTE ON THE SEVENTH AMENDED PLAN OR IN CONNECTION WITH AN ELECTION. NO SOLICITATION OF VOTES TO ACCEPT THE SEVENTH AMENDED PLAN MAY BE MADE EXCEPT PURSUANT TO SECTION 1125 OF TITLE 11 OF THE UNITED STATES CODE (THE “BANKRUPTCY CODE”).

HOLDERS OF CLAIMS AND EQUITY INTERESTS ENTITLED TO VOTE AND/OR TO MAKE CERTAIN ELECTIONS WITH RESPECT TO THE SEVENTH AMENDED PLAN ARE ADVISED AND ENCOURAGED TO READ THIS DISCLOSURE STATEMENT AND THE SEVENTH AMENDED PLAN IN THEIR ENTIRETY BEFORE VOTING TO ACCEPT OR REJECT THE SEVENTH AMENDED PLAN OR MAKING ANY ELECTION WITH RESPECT THERETO, AND, WHERE POSSIBLE, CONSULT WITH COUNSEL OR OTHER ADVISORS PRIOR TO VOTING OR ELECTING. ALL HOLDERS OF CLAIMS AND EQUITY INTERESTS SHOULD CAREFULLY READ AND CONSIDER FULLY THE RISK FACTORS SET FORTH IN ARTICLE X OF THIS DISCLOSURE STATEMENT BEFORE VOTING TO ACCEPT OR REJECT THE SEVENTH AMENDED PLAN AND BEFORE MAKING ANY ELECTION WITH RESPECT THERETO. A COPY OF THE SEVENTH AMENDED PLAN IS ANNEXED HERETO AS EXHIBIT A. SUMMARIES AND STATEMENTS MADE IN THIS DISCLOSURE STATEMENT ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO THE SEVENTH AMENDED PLAN AND THE EXHIBITS ANNEXED THERETO. THE STATEMENTS CONTAINED IN THIS DISCLOSURE STATEMENT ARE MADE ONLY AS OF THE DATE HEREOF, UNLESS OTHERWISE SPECIFIED HEREIN, AND THE DELIVERY OF THIS DISCLOSURE STATEMENT DOES NOT IMPLY THAT THERE HAS BEEN NO CHANGE IN THE INFORMATION SET FORTH HEREIN SINCE SUCH DATE. IN THE EVENT OF ANY CONFLICT BETWEEN THE DESCRIPTIONS SET FORTH IN THIS DISCLOSURE STATEMENT AND THE TERMS OF THE SEVENTH AMENDED PLAN, THE TERMS OF THE SEVENTH AMENDED PLAN WILL GOVERN. IN THE EVENT OF ANY CONFLICT BETWEEN THE TERMS OF THE SEVENTH AMENDED PLAN AND THE CONFIRMATION ORDER, THE TERMS AND PROVISIONS OF THE CONFIRMATION ORDER WILL GOVERN AND BE DEEMED A MODIFICATION OF THE SEVENTH AMENDED PLAN; PROVIDED, HOWEVER, THAT UNDER NO CIRCUMSTANCES SHALL THE CONFIRMATION ORDER MODIFY THE ECONOMIC TERMS SET FORTH IN THE SEVENTH AMENDED PLAN.

THIS DISCLOSURE STATEMENT HAS BEEN PREPARED IN ACCORDANCE WITH SECTION 1125 OF THE BANKRUPTCY CODE AND RULE 3016(b) OF THE FEDERAL RULES OF BANKRUPTCY PROCEDURE AND NOT NECESSARILY IN ACCORDANCE WITH OTHER NON-BANKRUPTCY LAW.

CERTAIN OF THE STATEMENTS CONTAINED IN THIS DISCLOSURE STATEMENT ARE FORWARD LOOKING PROJECTIONS AND FORECASTS, BASED UPON CERTAIN ESTIMATES AND ASSUMPTIONS. THERE CAN BE NO ASSURANCE THAT SUCH STATEMENTS WILL BE REFLECTIVE OF ACTUAL OUTCOMES. THIS DISCLOSURE STATEMENT MAY NOT BE RELIED UPON BY ANY PERSONS FOR ANY OTHER PURPOSE OTHER THAN BY HOLDERS OF CLAIMS AND EQUITY INTERESTS ENTITLED TO VOTE FOR THE PURPOSE OF DETERMINING WHETHER TO VOTE TO ACCEPT OR REJECT THE

2 Capitalized terms not defined herein shall have the meaning ascribed to them in the Seventh Amended Plan (as defined below).

SEVENTH AMENDED PLAN, AND NOTHING CONTAINED HEREIN SHALL CONSTITUTE AN ADMISSION OF ANY FACT OR LIABILITY BY ANY PARTY, OR BE ADMISSIBLE IN ANY PROCEEDING INVOLVING THE DEBTORS OR ANY OTHER PARTY, OR BE DEEMED CONCLUSIVE EVIDENCE OF THE TAX OR LEGAL EFFECTS OF THE SEVENTH AMENDED PLAN ON HOLDERS OF CLAIMS OR EQUITY INTERESTS.

IRS CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH IRS CIRCULAR 230, HOLDERS OF CLAIMS AND EQUITY INTERESTS ARE HEREBY NOTIFIED THAT: (A) ANY DISCUSSION OF U.S. FEDERAL TAX ISSUES CONTAINED OR REFERRED TO IN THIS DISCLOSURE STATEMENT IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, BY HOLDERS OF CLAIMS OR EQUITY INTERESTS FOR THE PURPOSE OF AVOIDING PENALTIES THAT MAY BE IMPOSED ON THEM UNDER THE TAX CODE; (B) SUCH DISCUSSION IS WRITTEN IN CONNECTION WITH THE PROMOTION OR MARKETING BY THE DEBTORS OF THE TRANSACTIONS OR MATTERS ADDRESSED HEREIN; AND (C) HOLDERS OF CLAIMS AND EQUITY INTERESTS SHOULD SEEK ADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

ii

DISCLOSURE STATEMENT FOR THE SEVENTH AMENDED

JOINT PLAN OF AFFILIATED DEBTORS PURSUANT TO

CHAPTER 11 OF THE UNITED STATES BANKRUPTCY CODE

On September 26, 2008 (the “Petition Date”), Washington Mutual, Inc. (“WMI”) and WMI Investment Corp. (“WMI Investment” and, together with WMI, the “Debtors”) each commenced with the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) a voluntary case pursuant to chapter 11 of the Bankruptcy Code.

The Debtors submit this Disclosure Statement pursuant to section 1125 of the Bankruptcy Code in connection with the solicitation of acceptances and elections with respect to the Seventh Amended Joint Plan of Affiliated Debtors Pursuant to Chapter 11 of the United States Bankruptcy Code (the “Seventh Amended Plan”).

Similar to the prior versions of the Debtors’ plan of reorganization, the Seventh Amended Plan is premised upon and incorporates the terms of the Global Settlement Agreement (defined below), which the Bankruptcy Court has determined is fair, reasonable and in the best interests of the Debtors’ estates. In addition, the Seventh Amended Plan incorporates each modification the Bankruptcy Court has specified as necessary to permit confirmation thereof. Furthermore, to resolve certain pending motions, appeals and anticipated objections that stood as potential impediments to, and were certain to further delay, confirmation, the Seventh Amended Plan contains a compromise and settlement among, and has the full support of, each of the Debtors, the Creditors’ Committee, the Equity Committee and certain Creditor constituencies. Accordingly, the Debtors, together with the Creditors’ Committee and the Equity Committee, believe the Seventh Amended Plan is in the best interest of all parties in interest and represents the most expeditious means for the Debtors to successfully emerge from the Chapter 11 Cases.

Unless otherwise defined herein, capitalized terms used, but not defined, herein shall have the same meanings ascribed to them in the Seventh Amended Plan. Annexed as exhibits to this Disclosure Statement are copies of the following documents:

1. Seventh Amended Plan – Exhibit A

| 2. | Disclosure Statement Order – Exhibit B |

| 3. | Liquidation Analysis – Exhibit C |

All exhibits to this Disclosure Statement are incorporated into and are part of this Disclosure Statement as if set forth in full herein.

I.

INTRODUCTION

| A. | Background |

WMI, a holding company incorporated in the State of Washington, is the direct parent of WMI Investment, a Delaware corporation, which, as of the Petition Date, held a variety of securities and investments.

Prior to the Petition Date, WMI was a multiple savings and loan holding company that owned Washington Mutual Bank (“WMB”) and, indirectly, WMB’s subsidiaries, including Washington

Mutual Bank fsb (“FSB”). As of the Petition Date, WMI also had several non-banking, non-debtor subsidiaries. Like all savings and loan holding companies, prior to the Petition Date, WMI was subject to regulation by the Office of Thrift Supervision (the “OTS”). WMB and FSB, in turn, like all depository institutions with federal thrift charters, were subject to regulation and examination by the OTS. In addition, WMI’s banking and non-banking subsidiaries were overseen by various federal and state authorities, including the Federal Deposit Insurance Corporation (“FDIC”).

On September 25, 2008 (the “Receivership Date”), the OTS, by order number 2008-36, closed WMB, appointed the FDIC as receiver for WMB (the “FDIC Receiver”) and advised that the FDIC Receiver was immediately taking possession of WMB’s assets. Immediately after its appointment as receiver, the FDIC Receiver sold substantially all the assets of WMB, including, among other things, the stock of FSB, to JPMorgan Chase Bank, National Association (“JPMC”), pursuant to that certain Purchase and Assumption Agreement, Whole Bank, effective September 25, 2008 (the “Purchase and Assumption Agreement”) (publicly available at http://www.fdic.gov/about/freedom/popular.html), in exchange for payment of $1.88 billion and the assumption of all of WMB’s deposit liabilities.

| B. | The Sixth Amended Plan and the January Opinion |

On October 6, 2010, the Debtors filed the Sixth Amended Plan3 and a corresponding disclosure statement. The Debtors solicited votes and certain elections with respect to the Sixth Amended Plan and, as set forth in more detail in the materials filed by the Debtors in support of confirmation of the Sixth Amended Plan, four (4) impaired Classes voted to accept the Sixth Amended Plan, while an additional ten (10) Classes were deemed to accept the Sixth Amended Plan. A hearing to consider confirmation of the Sixth Amended Plan (the “December Confirmation Hearing”) commenced on December 2, 2010 and concluded on December 7, 2010.

On January 7, 2011, the Bankruptcy Court entered an opinion [D.I. 6528] (the “January Opinion”)4 and related order [D.I. 6529] denying confirmation of the Sixth Amended Plan, but noting certain modifications to the Sixth Amended Plan that, if made, would permit confirmation thereof. As discussed in more detail in Section I.I.2 below, pursuant to the January Opinion, the Bankruptcy Court also determined that the compromise and settlement embodied in the Initial Global Settlement Agreement,5 upon which the Sixth Amended Plan was premised, and the transactions contemplated therein, are fair, reasonable, and in the best interests of the Debtors and their estates.

On January 19, 2011, the Equity Committee filed a notice of appeal of that portion of the January Opinion finding that the Initial Global Settlement Agreement satisfies the requisite standards for approval [D.I. 6575]. This action, styled as Official Committee of Equity Security Holders v. Washington Mutual, Inc., et al., Civil Action No. 11-158 (the “January Equity Committee Appeal”), is

3 Sixth Amended Joint Plan of Affiliated Debtors Pursuant to Chapter 11 of the Bankruptcy Code, dated October 6, 2010, as modified by (a) the first plan modification, dated October 29, 2010 [D.I. 5714], and (b) the second plan modification, dated November 24, 2010 [D.I. 6081] (collectively, the “Sixth Amended Plan”).

4 A full and complete copy of the January Opinion is available at http://www.kccllc.net/wamu or the Bankruptcy Court’s website, www.deb.uscourts.gov, and also is available for inspection during regular business hours in the office of the Clerk of the Bankruptcy Court, 824 Market Street, 3rd Floor, Wilmington, Delaware 19801.

5 Amended and Restated Settlement Agreement, dated as of October 6, 2010, by and among WMI and WMI Investment Corp., JPMC, the FDIC Receiver, FDIC Corporate, the Creditors’ Committee and certain other creditor constituencies (the “Initial Global Settlement Agreement”).

2

currently pending in the United States District Court for the District of Delaware (the “Delaware District Court”), as, by order, dated February 8, 2011 [D.I. 6703], the Bankruptcy Court denied the Equity Committee’s motion for a direct appeal to the United States Court of Appeals for the Third Circuit. In the Delaware District Court, among other things, the Equity Committee has filed a motion for leave to appeal, which the Debtors opposed, and on which the Delaware District Court has not yet ruled. The January Equity Committee Appeal is discussed in more detail in Section V.B.5.b hereof.

| C. | The Modified Sixth Amended Plan and the September Opinion |

In accordance with the January Opinion, the Debtors revised the Sixth Amended Plan and, on February 8, 2011, filed the Modified Sixth Amended Plan.6 Thereafter, the Debtors solicited votes and elections with respect thereto. As set forth in more detail in the materials filed by the Debtors in support of confirmation of the Modified Sixth Amended Plan twelve (12) of the fifteen (15) Classes entitled to vote on the Modified Sixth Amended Plan voted overwhelmingly to accept, while an additional four (4) Classes were deemed to accept the Modified Sixth Amended Plan.

Subsequently, with the full support of the Creditors’ Committee, Equity Committee and major creditor constituencies, the Debtors adjourned the hearing on confirmation of the Modified Sixth Amended Plan, to permit, among other things, the negotiation and documentation of an agreed upon and announced understanding among the Equity Committee and certain other parties in interest regarding modifications to the Modified Sixth Amended Plan. After several weeks of efforts to document such understanding, the Equity Committee withdrew from negotiations and suggested the Debtors proceed with confirmation of the Modified Sixth Amended Plan.

Consequently, the Bankruptcy Court held a hearing to consider, among other things (as discussed below), confirmation of the Modified Sixth Amended Plan. The hearing commenced on July 13, 2011, and concluded on July 21, 2011 (the “July Confirmation Hearing”). Subsequent thereto, on August 10, 2011, various parties submitted post-hearing briefing with respect to, among other things, confirmation of the Modified Sixth Amended Plan, and, on August 24, 2011, the Bankruptcy Court held closing arguments (the “Closing Arguments”).

On September 13, 2011, the Bankruptcy Court entered an Opinion [D.I. 8612] (the “September Opinion”)7 and related order [D.I. 8613] (the “September Order”) that, among other things: (i) found that the Bankruptcy Court has jurisdiction to approve the Global Settlement Agreement8 (September Opinion at 16, 22-23); (ii) reaffirmed its conclusion that the Global Settlement Agreement and all the transactions contemplated therein, including the settlement with holders of WMB Senior Notes

6 Modified Sixth Amended Joint Plan of Affiliated Debtors Pursuant to Chapter 11 of Bankruptcy Code, dated February 7, 2011 [D.I. 6696], as modified by (a) the first plan modification, dated March 16, 2011 [D.I. 6964], (b) the second plan modification, dated March 25, 2011 [D.I. 7040], and (c) the third plan modification, dated August 10, 2011 [D.I. 8423] (collectively, the “Modified Sixth Amended Plan”).

7 A full and complete copy of the September Opinion is available at http://www.kccllc.net/wamu or the Bankruptcy Court’s website, www.deb.uscourts.gov, and also is available for inspection during regular business hours in the office of the Clerk of the Bankruptcy Court, 824 Market Street, 3rd Floor, Wilmington, Delaware 19801.

8 Second Amended and Restated Global Settlement Agreement, dated as of February 7, 2011, by and among WMI and WMI Investment Corp., JPMC, the FDIC Receiver, FDIC Corporate, and the Creditors’ Committee (as it has been and may be further amended, and together with all exhibits annexed thereto, the “Global Settlement Agreement”).

3

discussed in Section V.B.5.g(i) hereof, are fair and reasonable (id. at 26, 35, 101); (iii) ordered that its ruling with respect to the Global Settlement Agreement constitutes the “law of the case” (id. at 27); (iv) overruled objections that the Modified Sixth Amended Plan was not proposed in good faith (id. at 73); (v) denied confirmation of the Modified Sixth Amended Plan, but identified certain modifications that, if incorporated, would permit confirmation thereof, as set forth in more detail in Section I.H.1 hereof; and (vi) directed certain parties to mediation (id. at 138), as discussed in more detail in Section I.E below.9

In addition to the foregoing, the Bankruptcy Court determined, pursuant to the September Opinion, that the present value of the projected income stream from the runoff of the existing portfolio of WM Mortgage Reinsurance Company, Inc. (“WMMRC”) (the entity that will be the sole operating subsidiary of Reorganized WMI), excluding any value attributed to potentially available net operating losses (“NOLs”), is $140 million. (Id. at 43-45.) The Bankruptcy Court further determined, in the context of the Modified Sixth Amended Plan, that the total enterprise value for Reorganized WMI (inclusive of both the projected income stream from the runoff of WMMRC’s existing portfolio as well as potentially available NOLs), is $210 million (id. at 62).

| D. | The Equity Committee Standing Motion |

On July 12, 2011, the Equity Committee filed, under seal, a motion seeking authority to prosecute, on the Debtors’ behalf, an action to equitably disallow or, in the alternative, to equitably subordinate certain Claims [D.I. 8179] (the “Standing Motion”). At the July Confirmation Hearing, which, as stated, commenced on July 13, 2011, counsel for the Equity Committee requested that the Court, “take into account the evidence . . . adduced at [the July Confirmation Hearing]” in connection with deciding the Standing Motion. On August 10, 2011, the Debtors, the Creditors’ Committee, certain members of AAOC,10 and certain other parties filed objections to the Standing Motion, arguing, among other things, that neither the evidence nor the law supported the relief requested. During Closing Arguments, certain parties presented argument with respect to the Standing Motion.

In the September Opinion, the Bankruptcy Court denied the Standing Motion with respect to the prosecution of equitable subordination claims. With respect to claims for equitable disallowance, the Bankruptcy Court granted the Standing Motion, but stayed all proceedings related to the Standing Motion pending mediation, discussed below.

_______________________________

9 As described in greater detail in Section I.D below, in the September Opinion, the Bankruptcy Court also granted the Equity Committee standing to prosecute certain claims on behalf of the Debtors’ estates against certain parties.

10 The Seventh Amended Plan defines “AAOC” as each of (a) Appaloosa Management L.P., Appaloosa Investment L.P. I, Palomino Fund Ltd., Thoroughbred Fund, L.P., and Thoroughbred Master Ltd. (collectively, “Appaloosa”), (b) Aurelius Capital Management, LP, Aurelius Capital Partners, LP , Aurelius Convergence Master, Ltd., ACP Master, Ltd., Aurelius Capital Master, Ltd. and Aurelius Investment, LLC (collectively, “Aurelius”), (c) Owl Creek Asset Management, L.P., Owl Creek I, L.P., Owl Creek II, L.P., Owl Creek Overseas Fund, Ltd., Owl Creek Socially Responsible Investment Fund, Ltd., Owl Creek Asia I, L.P., Owl Creek Asia II, L.P., and Owl Creek Asia Master Fund, Ltd. (collectively, “Owl Creek”) and (d) Centerbridge Partners, L.P., Centerbridge Special Credit Partners, L.P., Centerbridge Credit Partners, L.P., and Centerbridge Credit Partners Master, L.P. (collectively, “Centerbridge”) and any other Affiliates of the funds listed in (a) through (d) above which own or, during the Chapter 11 Cases, owned securities issued by and/or have direct or indirect Claims against WMI. Certain members of AAOC were “Settlement Note Holders,” as defined in the Initial Global Settlement Agreement, as discussed in Section I.I.3 hereof. The Standing Motion did not seek to prosecute an action against Appaloosa and Owl Creek.

4

| E. | The September Opinion Appeals |

On September 27, October 4, and October 11, 2011, respectively, each of (i) AAOC, with (a) Aurelius [D.I. 8670] filing individually and (b) Appaloosa, Owl Creek and Centerbridge (collectively, “AOC”) filing jointly [D.I. 8673], (ii) the Creditors’ Committee [D.I. 8726] and (iii) the Debtors [D.I. 8785] filed notices of appeal from that portion of the September Opinion granting the Standing Motion with respect to the equitable disallowance claims. Aurelius [D.I. 8672], AOC [D.I. 8674] and the Creditors’ Committee [D.I. 8727] filed motions for leave to appeal together with such notices, and the Debtors [D.I. 8781] joined the Creditors’ Committee’s motion. Aurelius’s motion also seeks to appeal that portion of the September Opinion concluding, as discussed in Section I.H.1.a hereof, that the Debtors must pay Postpetition Interest Claims at the federal judgment rate rather than the applicable contract rate. The Debtors have opposed Aurelius’s motion in this respect [D.I. 8783].

The WMB Noteholders [D.I. 8679] and Normandy Hill Capital L.P. [D.I. 8671] (“Normandy Hill”) also filed notices of appeal from the September Opinion on September 27, 2011, and, on October 10, 2011, Wells Fargo Bank, National Association, solely in its capacity as the PIERS Trustee, filed its notice of appeal [D.I. 8771].

The Equity Committee, for its part, filed a notice of cross-appeal and a motion for leave to cross-appeal on October 11, 2011, seeking to challenge, among other things, those portions of the September Opinion finding that the Modified Sixth Amended Plan was proposed in good faith and that the settlement with holders of WMB Senior Notes, discussed in more detail in Section V.B.5.g(i) hereof, is fair, reasonable and in the best interests of the Debtors’ estates [D.I. 8790, 8791] (the “October Equity Committee Appeal”). In addition, on October 14, 2011, the Equity Committee filed an opposition to the motions for leave to appeal filed by each of AAOC, the Creditors’ Committee and the Debtors, [D.I. 8811], with respect to which the Creditors’ Committee has filed a reply [D.I. 8866]. In addition, on October 25, 2011, the Debtors [D.I. 8878] and Creditors’ Committee [D.I. 8887] filed oppositions to the Equity Committee’s motion to cross-appeal.

All the motions for leave to appeal, as well as the Equity Committee’s opposition, have been transmitted to, and are pending in, the Delaware District Court.

| F. | Mediation |

Pursuant to the September Opinion and related order, the Bankruptcy Court directed certain parties to participate in mediation to explore a possible settlement of the Standing Motion and any issues that remain an impediment to confirmation of a plan of reorganization (the “Mediation”). On October 10, 2011 [D.I. 8780], the Bankruptcy Court appointed the Honorable Raymond Lyons as mediator (the “Mediator”) and ordered the following parties to participate in the Mediation: (i) the Debtors, (ii) the Creditors’ Committee, (iii) the Equity Committee, (iv) Aurelius, (v) Appaloosa, (vi) Centerbridge, (vii) Owl Creek, (viii) the TPS Consortium and the TPS Group, (ix) the WMB Noteholders, (x) Normandy Hill, (xi) The Bank of New York Mellon Trust Company, N.A., (“BNY Mellon”), in its capacity as Indenture Trustee for the Senior Notes, and (xii) the WMI Noteholders Group (as such term is used in the September Opinion) (collectively, the “Mediation Parties”); provided, however, that Normandy Hill and BNY Mellon were not required to attend the Mediation.

The Mediation commenced on October 19, 2011. At a status conference held on November 7, 2011, the Bankruptcy Court granted the Mediator’s request for additional time to continue

5

the Mediation. As a result of the Mediation, and with the assistance of the Mediator, discussions among the Debtors, the Creditors’ Committee, the Equity Committee, AAOC, and certain other creditor constituencies culminated in certain modifications to the Modified Sixth Amended Plan, described below, which modifications are embodied in the Seventh Amended Plan and resolve, among other things, certain plan-related issues and objections, as well as the Standing Motion.

| G. | The Seventh Amended Plan Incorporates Modifications Resulting From the Mediation Among the Debtors, the Creditors’ Committee, the Equity Committee, AAOC, and Certain Other Creditor Constituencies |

During the Mediation, the Debtors, the Creditors’ Committee, the Equity Committee, AAOC and other Creditor constituencies engaged in extensive, arms’ length negotiations designed to formulate a chapter 11 plan that addresses the prior opinions of the Bankruptcy Court as well as the concerns of all of the Debtors’ stakeholders. The Seventh Amended Plan is premised upon the Modified Sixth Amended Plan but incorporates modifications thereto made after the Mediation as well as modifications consistent with the September Opinion. For the reasons discussed in more detail herein, such parties believe that the Seventh Amended Plan is in the best interest of all parties in interest and represents the most expeditious means for the Debtors to successfully emerge from the Chapter 11 Cases. The modifications consistent with the September Opinion are discussed in Section I.H.1 hereof. The salient aspects of the modifications made after the Mediation are summarized below:

| · | Subject to the Bankruptcy Court approval, those current holders of WMI’s Equity Interests that elect to grant the releases set forth in Section 41.6 of the Seventh Amended Plan (such provision, the “Non-Debtor Release Provision” and such holders, the “Releasing Equity Interest Holders”) will receive the Reorganized Common Stock (subject to reduction on account of the Reorganized Common Stock Elections (defined and discussed in Section III.B.6.b(iv) below), to be allocated among such holders as described herein, and as set forth in the Seventh Amended Plan. |

| Such releases are described, to a limited extent, below, and are summarized in more detail in Section VI.O.6 hereof. |

| · | In consideration for, and subject in all respects to the grant and approval of, the releases by the Releasing Equity Interest Holders, and to avoid further delay as well as costly litigation, holders of Allowed Senior Notes Claims and Allowed Senior Subordinated Notes Claims will contribute to Reorganized WMI, for and on behalf of each Releasing Equity Interest Holder, respectively, Nine Hundred Sixty-Eight Thousandths of one percent (.968%) and Two and One-Tenth percent (2.1%) of the initial distributions received by them pursuant to the Seventh Amended Plan, having an aggregate value of approximately Seventy Five Million Dollars ($75,000,000.00), with the aggregate amount for all Allowed Senior Notes Claims equal to Forty Million Dollars ($40,000,000.00) (defined in the Seventh Amended Plan as the “Senior Notes Release Consideration”) and the aggregate amount for all Allowed Senior Subordinated Notes Claims equal to Thirty-Five Million Dollars ($35,000,000.00) (defined in the Seventh Amended Plan as the “Senior Subordinated Notes Release Consideration”). |

| · | Subject to Reorganized WMI’s right to seek and obtain financing on better terms and to the right, discussed in Sections III.B.2 and VI.G.11.b hereof, of certain qualifying Creditors and Equity Interest holders to become lenders of such loans, AAOC has collectively committed to provide Reorganized WMI the senior secured multidraw term Credit Facility, in the aggregate original principal amount of One Hundred Twenty Five Million Dollars ($125,000,000.00), to be used by Reorganized WMI to finance working capital and general corporate purposes, as well as certain permitted acquisitions and originations, all subject to the terms and conditions set forth in more detail in the Seventh Amended Plan and the definitive documentation governing such loans. |

6

| · | Subject to availability, and further subject to the relative rights thereto of the holders of Runoff Notes (discussed in Section III.B.1.b below), Reorganized WMI will also be funded by an additional Ten Million Dollars ($10,000,000.00), as well as interest accrued thereon at a rate of thirteen percent (13%) per annum, in the form of a portion of the proceeds from the runoff of WMMRC’s existing portfolio (as defined in the Seventh Amended Plan, the “Runoff Proceeds”) (the majority of which will be used to repay principal and interest on the Runoff Notes), (ii) certain potential litigation proceeds, if realized (defined in the Seventh Amended Plan as the “Litigation Proceeds”), and (iii) all distributions of Runoff Proceeds after all amounts due on the Runoff Notes have been paid in full, solely to the extent any such additional distributions are available. |

Specifically, certain Creditors are eligible to make the Reorganized Common Stock Elections defined and described in Sections I.G.1.a and III.B.6.b(iv) hereof. To the extent such elections are undersubscribed (i.e., if Creditors having the right to make Runoff Notes Elections decline to make Reorganized Common Stock Elections with respect to Runoff Notes having an original principal amount, in the aggregate, of less than Ten Million Dollars ($10,000,000.00) (defined in the Seventh Amended Plan as the “Runoff Threshold”)), then each of AAOC, severally and not jointly, will be deemed to have made Reorganized Common Stock Elections to receive such holder’s Pro Rata Share of the Common Stock Allotment (i.e., Ten Million (10,000,000) shares of Reorganized Common Stock, representing five percent (5%) of the issued and outstanding Reorganized Common Stock as of the Effective Date) in lieu of (i) Runoff Notes (based upon an allocation developed in their sole and absolute discretion) that they would otherwise receive on the Effective Date in their capacity as a holder of Allowed PIERS Claims, in the aggregate amount as is necessary to reach the Runoff Threshold; provided, however, that, to the extent that any of AAOC would not receive Runoff Notes on the Effective Date in its capacity as a holder of Allowed PIERS Claims in an amount sufficient to reach its allocable share of the Runoff Threshold, such AAOC Entity will instead be deemed to have elected to receive such amount of Runoff Notes (based upon an allocation developed in their sole and absolute discretion) in lieu of distributions of Creditor Cash on the Effective Date on account of its Allowed Senior Subordinated Notes Claims, and (ii) fifty percent (50%) of such holders’ Litigation Proceeds Interest (described in Section III.B.6.b(iv) hereof) in their capacity as holders of Allowed PIERS Claims. |

In consideration for, among other things, the foregoing, the Seventh Amended Plan provides for the following releases, among others, as summarized more fully in Sections VI.O.5 and VI.O.6 hereof:

| · | As and to the extent set forth in the Non-Debtor Release Provision (Section 41.6 of the Seventh Amended Plan), summarized more fully in Section VI.O.6 below, to the fullest extent permissible under applicable law, each holder of an Equity Interest that has held, currently holds or may hold any Released Third Party Causes of Action11 or a Released Claim12 (defined below), (ii) is |

11 The Seventh Amended Plan defines “Released Third Party Causes of Action” as any Claims and causes of action, regardless of whether asserted by any of the parties executing and delivering a release in accordance with the Non-Debtor Release Provision (Section 41.6 of the Seventh Amended Plan), whether known, unknown, reduced to judgment, not reduced to judgment, liquidated or unliquidated, fixed, contingent, matured, unmatured, disputed, undisputed, secured or unsecured, and whether asserted or assertable directly or derivatively, in law, equity or otherwise, and whether asserted or unasserted as of the date of entry of the order confirming the Seventh Amended Plan, that are based upon, relate to, or arise out of or in connection with, in whole or in part any act, omission, transaction, event or other circumstance relating to the Debtors and the Chapter 11 Cases and taking place or existing on or prior to the Effective Date, including, without limitation, (a) any such claim relating to the trading of the Debtors’ securities during the period from the Petition Date up to and including the Effective Date and (b) any claim for equitable subordination or equitable disallowance with respect to any Claims held by (i) the AAOC Releasees (as defined in the Seventh Amended Plan), (ii) the Senior Notes Claims Releasees (as defined in the Seventh Amended Plan), (iii) the Senior Subordinated Notes Claims Releasees (as defined in the Seventh Amended Plan), (iv) the PIERS Claims Releasees (as defined in the Seventh Amended Plan), and (v) the CCB Releasees (as defined in the Seventh Amended Plan) against the Debtors or the Debtors’ chapter 11 estates.

12 The Seventh Amended Plan’s definition of “Released Claim” includes, among other things, claims or causes of action that arise in, relate to or have been or could have been asserted (i) in the Chapter 11 Cases, the Receivership or the Related Actions, or (ii) by holders of Equity Interests relating to Equity Interests they have against the Debtors, and (iii) claims that otherwise arise from or relate to the Receivership, the Purchase and Assumption Agreement, the 363 Sale and Settlement, as defined in the Global Settlement Agreement, the Plan, the Global Settlement Agreement, and the negotiations and compromises set forth in the Global Settlement Agreement and the Plan, including, without limitation, in connection with or related to any of the Debtors, the Affiliated Banks (as defined in the Seventh Amended Plan), and their respective subsidiaries, assets, liabilities, operations, property or estates, the assets to be received by JPMC pursuant to the Global Settlement Agreement, the Debtors’ Claims, the JPMC Claims, the FDIC Claim, the WMI/WMB Intercompany Claims, any intercompany claims on the books of WMI or WMB related to the WaMu Pension Plan or the Lakeview Plan, or the Trust Preferred Securities (including, without limitation, the creation of the Trust Preferred Securities, the financing associated therewith, the requested assignment of the Trust Preferred Securities by the Office of Thrift Supervision and the transfer and the asserted assignment of the Trust Preferred Securities subsequent thereto); provided, however, that “Released Claims” does not include (1) any and all claims that the JPMC Entities, the Receivership, the FDIC Receiver and the FDIC Corporate are entitled to assert against each other or any other defenses thereto pursuant to the Purchase and Assumption Agreement, which claims and defenses shall continue to be governed by the Purchase and Assumption Agreement, (2) any and all claims held by Entities against WMB, the Receivership and the FDIC Receiver solely with respect to the Receivership, and (3) subject to the exculpation provisions set forth in the Plan, any avoidance action or claim objection regarding an Excluded Party (as defined in the Seventh Amended Plan ) or the WMI Entities (as defined in the Seventh Amended Plan), WMB, each of the Debtors’ estates, the Reorganized Debtors and their respective Related Persons; and, provided, further, that “Released Claims” is not intended to release, nor shall it have the effect of releasing, any party from the performance of its obligations in accordance with the order confirming the Seventh Amended Plan or the Seventh Amended Plan.

7

entitled to receive, directly or indirectly, a distribution or satisfaction of its Equity Interest pursuant to the Seventh Amended Plan, and (iii) elects, by not checking or checking the appropriate box on its Ballot (as defined in Section XI.A.2 hereof) or Election Form (as defined in Section XI.B.2.a hereof), as the case may be, to grant the releases set forth in the Non-Debtor Release Provision (Section 41.6 of the Seventh Amended Plan), on their own behalf and on behalf of anyone claiming through them, will be deemed to have irrevocably and unconditionally, fully, finally and forever waived, released, acquitted and discharged (1) each and all of the Released Parties (as defined in the Seventh Amended Plan), from any and all Released Claims and/or any claim, act, fact, transaction, occurrence, statement, or omission in connection with or alleged in the Actions or in the Texas Litigation, or that could have been alleged in respect of the foregoing or other similar proceeding, including, without limitation, any such claim demand, right, liability, or cause of action for indemnification, contribution or any other basis in law or equity for damages, costs or fees incurred by the releasors herein arising directly or indirectly from or otherwise relating thereto and (2) each of (a) the AAOC Releasees, (b) the Senior Notes Claims Releasees, (c) the Senior Subordinated Notes Claims Releasees, (d) the PIERS Claims Releasees and (e) the CCB Releasees from any and all Released Third Party Causes of Action.

_______________________________

existing on or prior to the Effective Date, including, without limitation, (a) any such claim relating to the trading of the Debtors’ securities during the period from the Petition Date up to and including the Effective Date and (b) any claim for equitable subordination or equitable disallowance with respect to any Claims held by (i) the AAOC Releasees (as defined in the Seventh Amended Plan), (ii) the Senior Notes Claims Releasees (as defined in the Seventh Amended Plan), (iii) the Senior Subordinated Notes Claims Releasees (as defined in the Seventh Amended Plan), (iv) the PIERS Claims Releasees (as defined in the Seventh Amended Plan), and (v) the CCB Releasees (as defined in the Seventh Amended Plan) against the Debtors or the Debtors’ chapter 11 estates.

8

| · | Each of the Debtors and the Reorganized Debtors, on its own behalf and as representative of its respective estate, the Disbursing Agent and each of the Debtors’ Related Persons, the Creditors’ Committee and the Equity Committee, without giving any legitimacy or merit to any of the allegations raised or asserted with respect to AAOC, holders of Allowed Senior Notes Claims, Allowed Senior Subordinated Notes Claims and holders of Allowed PIERS Claims during the Chapter 11 Cases, will be deemed to have irrevocably and unconditionally, fully, finally and forever waived, released, acquitted, and discharged (1) the AAOC Releasees, (2) the Senior Notes Claims Releasees, (3) the Senior Subordinated Notes Claims Releasees, (4) the PIERS Claims Releasees and (5) the CCB Releasees, and each of their respective officers, directors, agents, employees and, solely in their capacity as counsel with respect to the Chapter 11 Cases, attorneys from any and all Estate Claims13 that the Debtors, the Creditors’ Committee and the Equity Committee, have or may have or claim to have, now or in the future, against (1) the AAOC Releasees, (2) the Senior Notes Claims Releasees, (3) the Senior Subordinated Notes Claims Releasees, (4) the PIERS Claims Releasees and (5) the CCB Releasees, and each of their respective officers, directors, agents, employees and, solely in their capacity as counsel with respect to the Chapter 11 Cases, attorneys. |

In addition to the foregoing, the Equity Committee will (i) support confirmation of the Seventh Amended Plan, and (ii) take any and all action as is necessary to cause the withdrawal and dismissal, with prejudice, of the January Equity Committee Appeal and the October Equity Committee Appeal, each of which is discussed above, as well as the Equity Committee Adversary Proceeding and Equity Committee Motion to Compel (each of which is discussed in Section V.B.5.a hereof).

Upon entry of the order confirming the Seventh Amended Plan, each of the Debtors, Creditors�� Committee and AAOC, among others, will take any and all action as is necessary to cause the withdrawal and dismissal, with prejudice, of their respective appeals related to the September Opinion and September Order.

13 The Seventh Amended Plan defines “Estate Claims” as any Claims and causes of action, regardless of whether asserted by the Debtors, the Liquidating Trust, the Creditors’ Committee or the Equity Committee, whether known, unknown, reduced to judgment, not reduced to judgment, liquidated or unliquidated, fixed, contingent, matured, unmatured, disputed, undisputed, secured or unsecured, and whether asserted or assertable directly or derivatively, in law, equity or otherwise, and whether asserted or unasserted as of the date of entry of the Confirmation Order, that (a) are based upon, relate to, or arise out of or in connection with, in whole or in part any act, omission, transaction, event or other circumstance relating to the Debtors and the Chapter 11 Cases, (b) exist on or prior to the Effective Date, and (c) are or may be asserted against (i) the AAOC Releasees with respect to any conduct or, (ii) any of (1) the PIERS Claims Releasees, (2) the Senior Notes Claims Releasees, (3) the Senior Subordinated Notes Claims Releasees and (4) the CCB Releasees with respect to (A) any and all Claims for equitable disallowance and equitable subordination, (B) any and all Claims with respect to any conduct undertaken during the period from and after the Petition Date and (C) any and all Claims with respect to conduct undertaken during the period prior to the Petition Date solely in their capacity as holders of any securities issued by the Debtors or their subsidiaries, including, without limitation, any claims for insider trading or violations of securities laws; provided, however, that, solely with respect to clause (ii) above, under no circumstances shall Estate Claims include (y) any Claims related to trading in the securities issued by the Debtors or their subsidiaries that are based on an allegation that such trading contributed to the failure of WMB or the commencement of the Chapter 11 Cases, including, without limitation, any Claims discussed on pages 330-338 of that certain Final Report of the Examiner, dated November 1, 2010, issued by Joshua R. Hochberg, appointed as Examiner in these Chapter 11 Cases, and (z) Preserved Avoidance Actions (as defined in the Seventh Amended Plan). For the avoidance of doubt, “Estate Claims” shall include, without limitation, (1) any claim relating to the trading of the Debtors’ securities during the period from the Petition Date up to and including the Effective Date and (2) any claim for equitable subordination or equitable disallowance.

9

The Seventh Amended Plan further provides that the order confirming the Seventh Amended Plan must provide for the withdrawal and vacatur, for all purposes, of (i) the September Order to the extent relating to the Standing Motion, and (ii) those portions of the September Opinion relating to the Standing Motion, including, but not limited to, (i) Section III (H) of the September Opinion, pages 108 through 139, and (ii) the first sentence on page 68, footnote 31 on page 70, and the last paragraph of Section III(D) of the September Opinion, page 73.

As stated, the Seventh Amended Plan is the result of extensive arms’ length negotiations between the Debtors, the Creditors’ Committee, the Equity Committee, AAOC and other Creditor constituencies. Such parties believe that the Seventh Amended Plan and the terms embodied therein are in the best interests of all parties in interest and represent the most expeditious means for the Debtors to successfully emerge from the Chapter 11 Cases. Among other things, unlike the Modified Sixth Amended Plan, the Seventh Amended Plan resolves the Standing Motion and has the support of the Equity Committee. In contrast, an attempt to confirm a plan without the underlying agreements embodied in the Seventh Amended Plan would have invited significant confirmation objections by the Equity Committee, among others, including with respect to issues related to the Standing Motion and the effect that such disputes would have with respect to distributions pursuant to any such plan. For example, the Debtors and the Equity Committee, among others, have opposing views as to whether the Claims subject to the Standing Motion should be treated as Disputed Claims pursuant to any such plan. The Equity Committee has asserted that such Claims would have to be estimated by the Bankruptcy Court before any distributions could be made pursuant to a modified plan. In addition, the Equity Committee indicated that, absent a settlement, it intended to object as to, among other things, whether a plan could be confirmed at all without prior resolution of the issues raised in the Standing Motion, in light of complications regarding distributions or reserves of the Reorganized Common Stock. Without addressing the merits, it is beyond doubt that such issues could lead to further contested confirmation hearings, significant delays in confirmation of a plan, and erosion of Creditor distributions.

The detrimental effects of further delay in confirmation and consummation of a plan in the Chapter 11 Cases—now over three years old—should not be underestimated. Each day of delay is accompanied by a continued accrual of interest and fees and the attendant depletion of estate assets and increase in total Claims, all of which results in eroded recoveries for the Debtors’ junior-most Creditors and stakeholders. To quantify the cost of delay, as a result of (i) the contractual obligations of holders of Allowed PIERS Claims to payover their distributions to certain Creditors that are senior in recovery, on account of such senior Creditors’ Intercreditor Interest Claims at the applicable contract rate, and (ii) the continued depletion of estate assets as a result of the ongoing accrual of professionals’ fees, recoveries for holders of Allowed PIERS Claims decline at a rate of approximately $30 million per month. As a result of the rulings in the September Opinion, the Debtors are obligated to pay Postpetition Interest Claims at the federal judgment rate, rather than at the applicable contract rate, such that the burn rate for holders that are more junior to PIERS claimants is slightly lower than that of the holders of Allowed PIERS Claims. Notwithstanding, the rate of decline in recoveries for such holders is still significant. Specifically, recoveries for such junior holders are reduced by approximately $18 million per month as a result of the ongoing accrual of interest and fees.

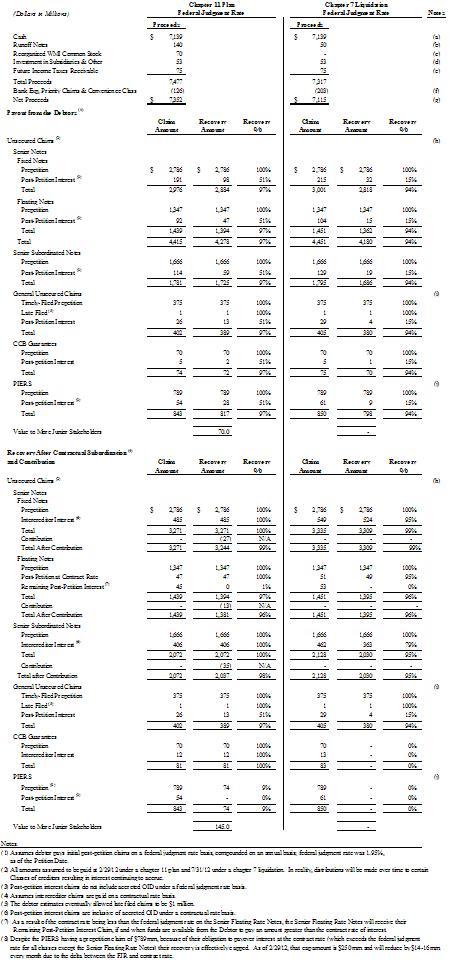

Currently, the Updated Liquidation Analysis (defined below) attached hereto as Exhibit C and the corresponding recovery estimates set forth in Section III.B.6.d hereof assume an Effective Date for the Seventh Amended Plan of February 29, 2012. The Debtors estimate that if the Effective Date is delayed even three (3) months past February 29, 2012, recovery for holders of Allowed PIERS Claims in Class 16 (the first Class to suffer from a deterioration or elimination in recoveries as a result of the continued accrual of interest and fees) will be wiped out. Additionally, the Debtors estimate that if the Effective Date is delayed longer than three (3) months past February 29, 2012, the recoveries for holders

10

of Allowed CCB Guarantee Claims will begin to be reduced, and after approximately three (3) to four (4) additional months, may also be eliminated. After such time, while the accrual of postpetition interest will continue on Allowed Senior Notes Claims and Allowed Senior Subordinated Notes Claims, the rate of recovery on those claims will be reduced.

Unlike the Modified Sixth Amended Plan (or the aforementioned modified version thereof), the Seventh Amended Plan resolves many of the objections and issues that have been or could be raised, regardless of the merits, and is thus more likely to result in an expeditious exit from bankruptcy and prevent further deterioration of Creditors’ recoveries. It is therefore undeniable that swift confirmation of the Seventh Amended Plan will benefit the Debtors and their estates, and is in the best interests of all constituencies.

| 1. | Issuance of Runoff Notes to Certain Creditors and Distribution of Reorganized Common Stock to Certain Holders of Equity Interests |

As discussed in more detail in Sections III.B.1, III.B.6.b(iv), III.B.6.c(ii), III.B.6.c(iii), VI.G.7, VI.F.1.a, VI.F.1.d, XI.B.2, and XI.B.3 hereof, Reorganized WMI will issue two types of securities: (i) the Runoff Notes to be issued in the aggregate original principal amount of One Hundred Forty Million Dollars ($140,000,000.00) (subject to reduction as a result of the Reorganized Common Stock Elections discussed below), maturing on the eighteenth (18th) anniversary of the Effective Date, bearing interest at a rate of thirteen percent (13%) per annum (payable in cash to the extent available and payable in kind through the capitalization of accrued interest at the rate of thirteen percent (13%) per annum to the extent cash is unavailable), the repayment thereof secured by, and having a specified priority in right of payment in, as and to the extent set forth in more detail in the definitive documents governing the Runoff Notes, (a) a securities or deposit account into which Reorganized WMI will deposit distributions it receives of Runoff Proceeds and (b) the equity interests in either WMMRC or such other Entity as holds the WMMRC Trusts (defined below) and their assets, to the extent a lien has been granted therein (with any such lien subject to regulatory approval), and (ii) Reorganized Common Stock.

Pursuant to the Seventh Amended Plan, the Runoff Notes will either (a) be distributed to Entities electing distributions of Runoff Notes in lieu of Creditor Cash received on the Effective Date or (b) to the extent Creditor Cash is unavailable for distribution to Entities to exchange for Runoff Notes in accordance with such elections, the Runoff Notes will constitute Liquidating Trust Assets, as discussed in more detail in Section III.B.6.b(iv) hereof.

Subject to reduction on account of the Reorganized Common Stock Elections, the Reorganized Common Stock will be allocated, subject to reduction as a result of the Reorganized Common Stock Elections, seventy percent (70%) to those Preferred Equity Interest holders that are Releasing Equity Interest Holders, and thirty percent (30%) to those holders of WMI’s common stock (i.e., pari passu to holders of Common Equity Interests and Dime Warrants, to the extent such Dime Warrant holders are determined, pursuant to a Final Order or a compromise and settlement, to hold Equity Interests or Allowed Claims subordinated to the level of Common Equity Interests) that are Releasing Equity Interest Holders, or as otherwise allocated by the Bankruptcy Court. Within each group, the Reorganized Common Stock will be allocated and distributed, pro rata with respect to shares owned, solely among the Releasing Equity Interest Holders (i.e., those current holders of WMI’s Equity Interests that affirmatively agree to grant the releases set forth in the Non-Debtor Release Provision (Section 41.6 of the Seventh Amended Plan)).

11

| a. | The Reorganized Common Stock Election |

As discussed in more detail in Sections III.B.6.b(iv) and XI.B.3 hereof, pursuant to the Seventh Amended Plan (i) each eligible holder of an Allowed Senior Notes Claim, Allowed Senior Subordinated Notes Claim, Allowed General Unsecured Claim, Allowed CCB-1 Guarantees Claim, Allowed CCB-2 Guarantees Claim or Allowed PIERS Claim that made the Runoff Notes Election defined and described in Section III.B.6.b(iv) hereof (i.e., that elected to receive Runoff Notes in lieu of some or all of the Creditor Cash, if any, that such holder is otherwise entitled to receive on the Effective Date) or that is otherwise entitled to receive Runoff Notes pursuant to the Seventh Amended Plan, as well as (ii) each holder of a Disputed Claim or Dime Warrant that made a contingent Runoff Notes Election (which elections will be effective only if and to the extent that (a) such holders are determined pursuant to a Final Order, to hold Allowed General Unsecured Claims and (b) are entitled to receive Creditor Cash on the Effective Date), will have the right to elect, in its sole and absolute discretion, to receive such holder’s Pro Rata Share of the Common Stock Allotment (i.e., Ten Million (10,000,000) shares of Reorganized Common Stock, representing five percent (5%) of the issued and outstanding Reorganized Common Stock as of the Effective Date) in lieu of (i) fifty percent (50%) of such holder’s Litigation Proceeds Interest (described in Section III.B.6.b(iv) hereof) (except with respect to the AAOC Deemed Election (defined below), solely in its capacity as the holder of the Allowed Claim to which the Reorganized Common Stock Election is effective) and (ii) some or all of the Runoff Notes that such holder otherwise is entitled to and, if applicable, has elected to receive pursuant to the Runoff Notes Election. To the extent an electing Creditor receives Reorganized Common Stock pursuant to the foregoing election, such Creditor’s share of the Runoff Notes to which the election was effective (i.e., One Dollar ($1.00) of original principal amount of Runoff Notes for each share of Reorganized Common Stock) will not be issued, and, furthermore, Reorganized WMI will retain an economic interest in certain litigation proceeds such Creditor otherwise would have received on account of its Liquidating Trust Interests (and such proceeds will not constitute a component of the Liquidating Trust Assets, and the Creditor’s rights in respect of distributions from the Liquidating Trust will be adjusted to the extent such proceeds are received by Reorganized WMI).

Deemed AAOC Election. The Seventh Amended Plan further provides that, in the event that holders of Claims with the right to make Reorganized Common Stock Elections decline to tender, in the aggregate, Runoff Notes in the original principal amount necessary to reach the Runoff Threshold (i.e., Ten Million Dollars ($10,000,000.00)), each of AAOC, severally and not jointly, will be deemed to have made Reorganized Common Stock Elections to receive such holder’s Pro Rata Share of the Common Stock Allotment (i.e., Ten Million (10,000,000) shares of Reorganized Common Stock, representing five percent (5%) of the issued and outstanding Reorganized Common Stock as of the Effective Date) in lieu of (i) Runoff Notes (based upon an allocation developed in their sole and absolute discretion) that they would otherwise receive on the Effective Date in their capacity as a holder of Allowed PIERS Claims, in the aggregate amount as is necessary to reach the Runoff Threshold; provided, however, that, to the extent that any of AAOC would not receive Runoff Notes on the Effective Date in its capacity as a holder of Allowed PIERS Claims in an amount sufficient to reach its allocable share of the Runoff Threshold, such AAOC Entity will instead be deemed to have elected to receive such amount of Runoff Notes (based upon an allocation developed in their sole and absolute discretion) in lieu of distributions of Creditor Cash on the Effective Date on account of its Allowed Senior Subordinated Notes Claims, and (ii) fifty percent (50%) of such holders’ Litigation Proceeds Interest (described in Section III.B.6.b(iv) hereof) in their capacity as holders of Allowed PIERS Claims.

12

| 2. | Commitment by AAOC to Provide Exit Financing |

As discussed in more detail in Sections III.B.2 and VI.G.11 hereof, AAOC has committed to make available to Reorganized WMI the four and one half (4½) year or five (5) year, as applicable, senior secured multi-draw term Credit Facility, in an aggregate original principal amount not to exceed One Hundred Twenty Five Million Dollars ($125,000,000.00), bearing interest on amounts outstanding at a rate of seven percent (7.0%) per annum, with Reorganized WMI having the option to pay one percent (1%) thereof in kind, upon which Reorganized WMI may draw during a three (3) year availability period from and after the Effective Date. The Credit Facility will consist of three tranches: a (i) a Tranche A Term Loan in the aggregate principal amount of Ten Million Dollars ($10,000,000.00) and (ii) a Tranche A-1 Term Loan in the aggregate principal amount of Fifteen Million Dollars ($15,000,000.00) will be available to fund working capital and for general corporate purposes of Reorganized WMI and its subsidiaries, subject to the terms and conditions of the definitive documentation governing the Credit Facility (together, the “Tranche A Credit Facility”), and (iii) a Tranche B Term Loan in the aggregate principal amount of One Hundred Million Dollars ($100,000,000.00) will be available for certain specified purposes (the “Tranche B Credit Facility”). Specifically, advances on the Tranche B Credit Facility may only be used to fund acquisitions and originations meeting certain criteria which include, among other things, that at least twenty percent (20%) of the funding for any such transaction is new equity contributions or subordinated indebtedness or Cash on hand (other than proceeds of the Credit Facility, “Restricted Disposition Proceeds” (defined in the documentation governing the Credit Facility to include the proceeds of dispositions of assets or equity interests to the extent purchased with proceeds advanced pursuant to the Credit Facility) and proceeds of other indebtedness) and satisfy certain additional conditions precedent, all as discussed in more detail in Sections III.B.2 and VI.G.11 hereof.

| 3. | Resolution of Certain Governance-Related Issues |

As discussed in more detail in Sections I.H.1.b(i), III.B.4, and III.B.5 hereof, the Seventh Amended Plan incorporates modifications that resolve certain governance-related issues including and in addition to those identified by the Bankruptcy Court in the September Opinion such as, among other things, modifications to the composition of the Trust Advisory Board and Reorganized WMI’s board of directors. In addition, the Liquidating Trust Agreement, a copy of which will be included in the Plan Supplement for the Seventh Amended Plan, contemplates the creation of a Litigation Subcommittee (defined and described below) of the Trust Advisory Board.

| a. | The Establishment of a Litigation Subcommittee |