Exhibit 99.2

Exhibit 99.2

2Q11 Earnings Conference Call

Supplemental Materials

July 26, 2011

Forward Looking Statements

Safe Harbor

Statements contained in this presentation which are not historical facts and which pertain to future operating results of IBERIABANK Corporation and its subsidiaries constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve significant risks and uncertainties. Actual results may differ materially from the results discussed in these forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in the Company’s periodic and other filings with the SEC.

Introductory Comments

Introductory Comments

Summary – Position

Favorable Balance Sheet Composition

Very Balanced; Core Funded; Low C&D Exposure

Continued Good Asset Quality; Extraordinary Capital

Favorable Interest Rate And Credit Risk Positioning

Some of the Highest Capital Ratios of Bank Holding Companies With More Than $5 Billion in Assets

Legacy Deposit Growth in 2Q11 And Improved Deposit Mix

Future Growth Engines in Multiple Markets

Strategic Recruiting Continued During The 2nd Quarter

Fortunately, We Avoided What Ails The Banking Industry

Remain Well Positioned For Future Opportunities

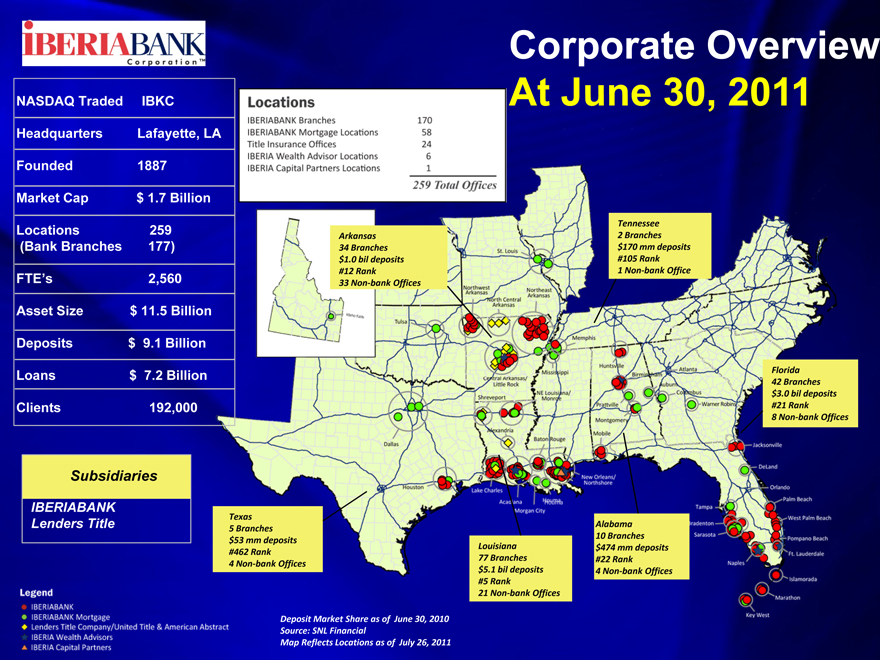

Corporate Overview At June 30, 2011

NASDAQ Traded IBKC Headquarters Lafayette, LA Founded 1887 Market Cap $ 1.7 Billion

Locations 259 (Bank Branches 177)

FTE’s 2,560 Asset Size $ 11.5 Billion Deposits $ 9.1 Billion Loans $ 7.2 Billion Clients 192,000

Subsidiaries

IBERIABANK Lenders Title

Deposit Market Share as of June 30, 2010 Source: SNL Financial Map Reflects Locations as of July 26, 2011

Texas

5 | | Branches $53 mm deposits #462 Rank |

Louisiana

77 Branches $5.1 bil deposits

#5 Rank

21 Non? bank Offices

Alabama

10 Branches $474 mm deposits #22 Rank

Arkansas

34 Branches $1.0 bil deposits #12 Rank

33 Non? bank Offices

Tennessee

2 | | Branches $170 mm deposits #105 Rank |

Florida

42 Branches $3.0 bil deposits #21 Rank

Legend

IBERIABANK

IBERIABANK Mortgage

Lenders Title Company/United Title & American Abstract

IBERIA Wealth Advisors

IBERIA Capital Partners

Locations 170

IBERIABANK Branches 58

IBERIABANK Mortgage Locations 24

Title Insurance Offices 6

IBERIA Wealth Advisors Locations 1

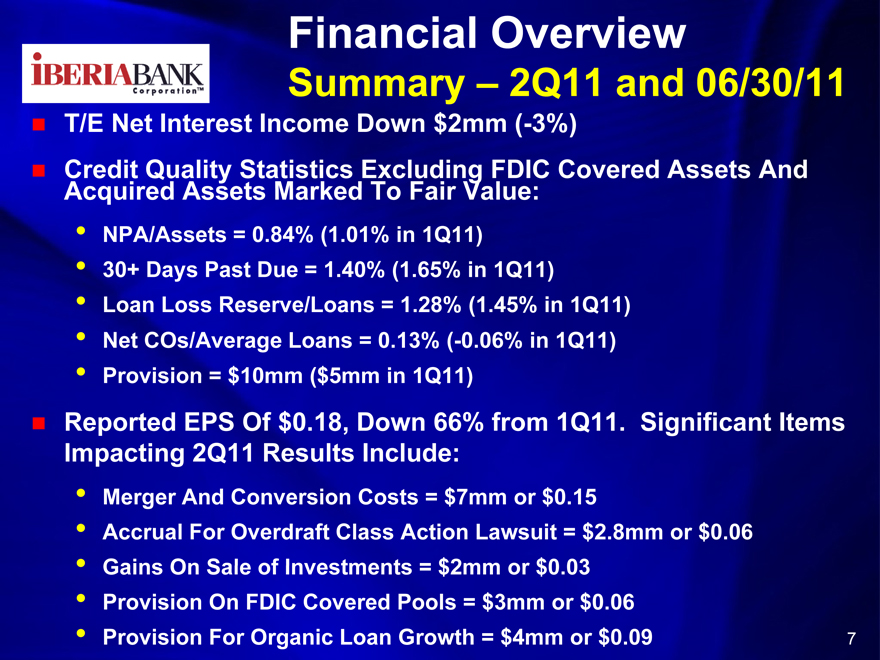

Financial Overview

Financial Overview

Summary – 2Q11 and 06/30/11

T/E Net Interest Income Down $2mm (-3%)

Credit Quality Statistics Excluding FDIC Covered Assets And Acquired Assets Marked To Fair Value:

• NPA/Assets = 0.84% (1.01% in 1Q11)

• 30+ Days Past Due = 1.40% (1.65% in 1Q11)

• Loan Loss Reserve/Loans = 1.28% (1.45% in 1Q11)

• Net COs/Average Loans = 0.13% (-0.06% in 1Q11)

• Provision = $10mm ($5mm in 1Q11)

Reported EPS Of $0.18, Down 66% from 1Q11. Significant Items Impacting 2Q11 Results Include:

• Merger And Conversion Costs = $7mm or $0.15

• Accrual For Overdraft Class Action Lawsuit = $2.8mm or $0.06

• Gains On Sale of Investments = $2mm or $0.03

• Provision On FDIC Covered Pools = $3mm or $0.06

• Provision For Organic Loan Growth = $4mm or $0.09

7

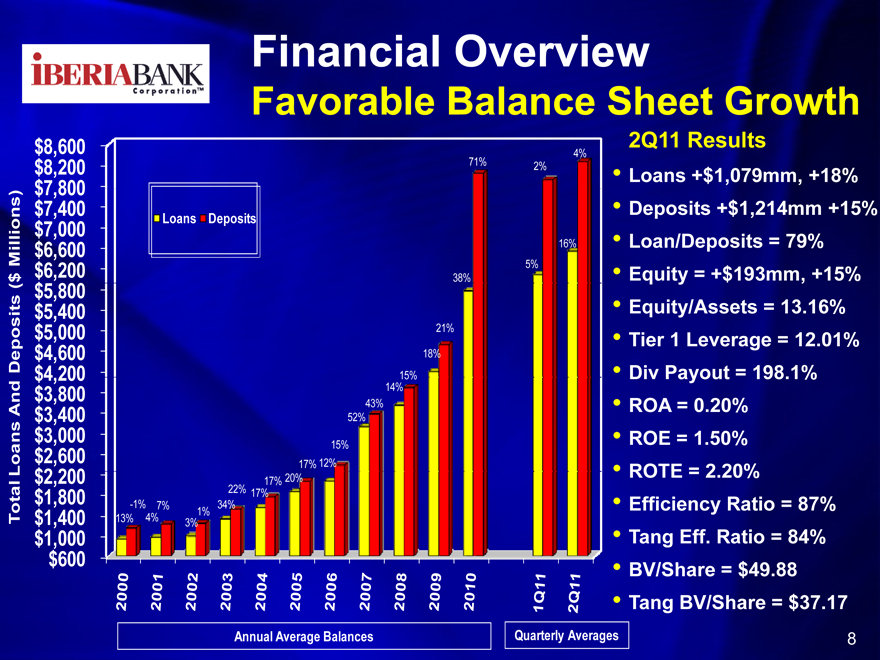

Financial Overview

Favorable Balance Sheet Growth

2Q11 Results

• Loans +$1,079mm, +18%

• Deposits +$1,214mm +15%

• Loan/Deposits = 79%

• Equity = +$193mm, +15%

• Equity/Assets = 13.16%

• Tier 1 Leverage = 12.01%

• Div Payout = 198.1%

• ROA = 0.20%

• ROE = 1.50%

• ROTE = 2.20%

• Efficiency Ratio = 87%

• Tang Eff. Ratio = 84%

• BV/Share = $49.88

• Tang BV/Share = $37.17

Annual Average Balances

Quarterly Averages

$8,600 $8,200 $7,800 $7,400 $7,000 $6,600 $6,200 $5,800 $5,400 $5,000 $4,600 $4,200 $3,800 $3,400 $3,000 $2,600 $2,200 $1,800 $1,400 $1,000 $600

Loans Deposits

13% 16% 5% 38%

21%

18% 15% 14% 43% 52%

15% 17% 12% 17% 20% 22% 17% -1% 7% 34% 1% 4%4% 71% 2%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q11 2Q11

Total Loans And Deposits ($ Millions)

8

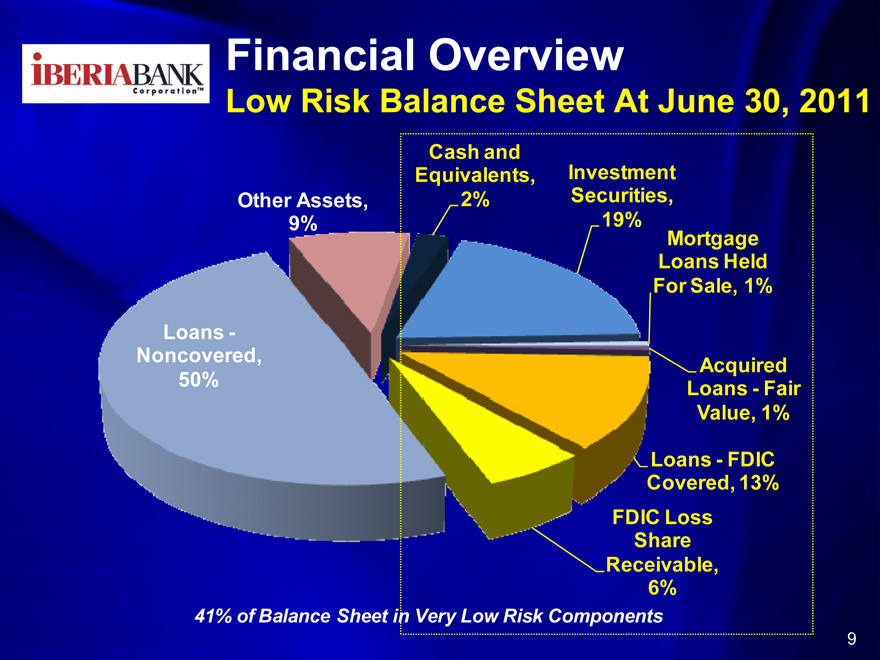

Financial Overview

Low Risk Balance Sheet At June 30, 2011

Other Assets, 9%

Cash and Equivalents, 2%

Investment Securities, 19%

Mortgage Loans Held For Sale, 1%

Acquired Loans—Fair Value, 1%

FDIC Loss Share Receivable, 6%

41% of Balance Sheet in Very Low Risk Components

Loans -Noncovered, 50%

9

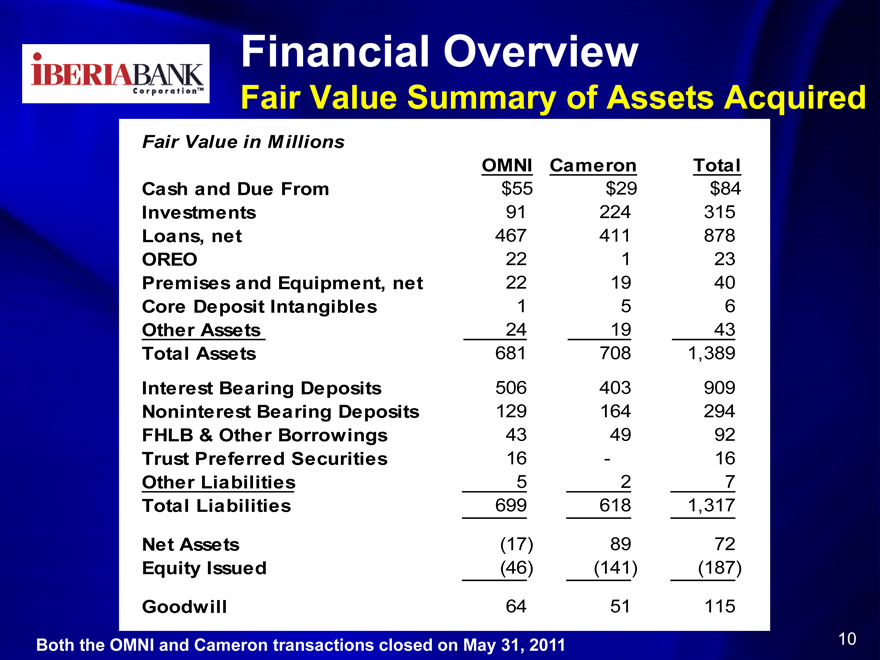

Financial Overview

Fair Value Summary of Assets Acquired

Fair Value in Millions

OMNI Cameron Total

Cash and Due From $55 $29 $84

Investments 91 224 315

Loans, net 467 411 878

OREO 22 1 23

Premises and Equipment, net 22 19 40

Core Deposit Intangibles 1 5 6

Other Assets 24 19 43

Total Assets 681 708 1,389

Interest Bearing Deposits 506 403 909

Noninterest Bearing Deposits 129 164 294

FHLB & Other Borrowings 43 49 92

Trust Preferred Securities 16—16

Other Liabilities 5 2 7

Total Liabilities 699 618 1,317

Net Assets(17) 89 72

Equity Issued(46)(141)(187)

Goodwill 64 51 115

Both the OMNI and Cameron transactions closed on May 31, 2011

10

IBERIA BANK

Corporationtm

Financial Overview

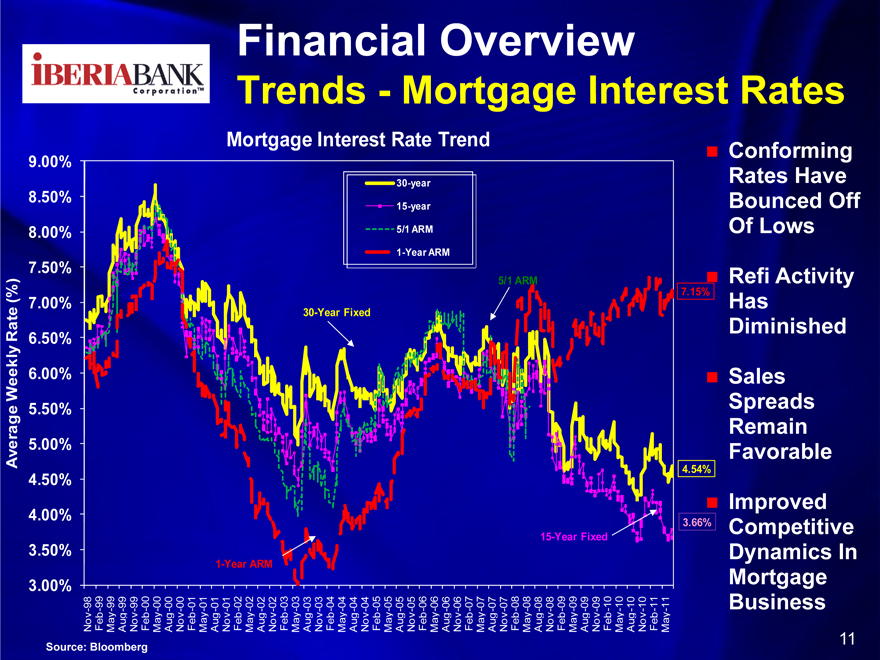

Trends—Mortgage Interest Rates

Mortgage Interest Rate Trend

30-year

15-year 5/1 ARM

1-Year ARM

9.00% 8.50% 8.00%

7.50% (%) 7.00% Rate 6.50% Weekly 6.00% 5.50% Average 5.00% 4.50%

4.00% 3.50% 3.00%

Nov-98 Feb-99 May-99 Aug-99 Nov-99 Feb-00 May-00 Aug-00 Nov-00 Feb-01 May-01 Aug-01 Nov-01 Feb-02 May-02 Aug-02 Nov-02 Feb-03 May-03 Aug-03 Nov-03 Feb-04 May-04 Aug-04 Nov-04 Feb-05 May-05 Aug-05 Nov-05 Feb-06 May-06 Aug-06 Nov-06 Feb-07 May-07 Aug-07 Nov-07 Feb-08 May-08 Aug-08 Nov-08 Feb-09 May-09 Aug-09 Nov-09 Feb-10 May-10 Aug-10 Nov-10 Feb-11 May-11

Source: Bloomberg

Conforming Rates Have Bounced Off Of Lows

Refi Activity Has Diminished

Sales Spreads Remain Favorable

Improved Competitive Dynamics In Mortgage Business 30-Year Fixed 1-Year ARM 5/1 ARM 4.54% 3.66% 15-Year Fixed 7.15% 1-Year ARM

11

IBERIA BANK

Corporationtm

Financial Overview

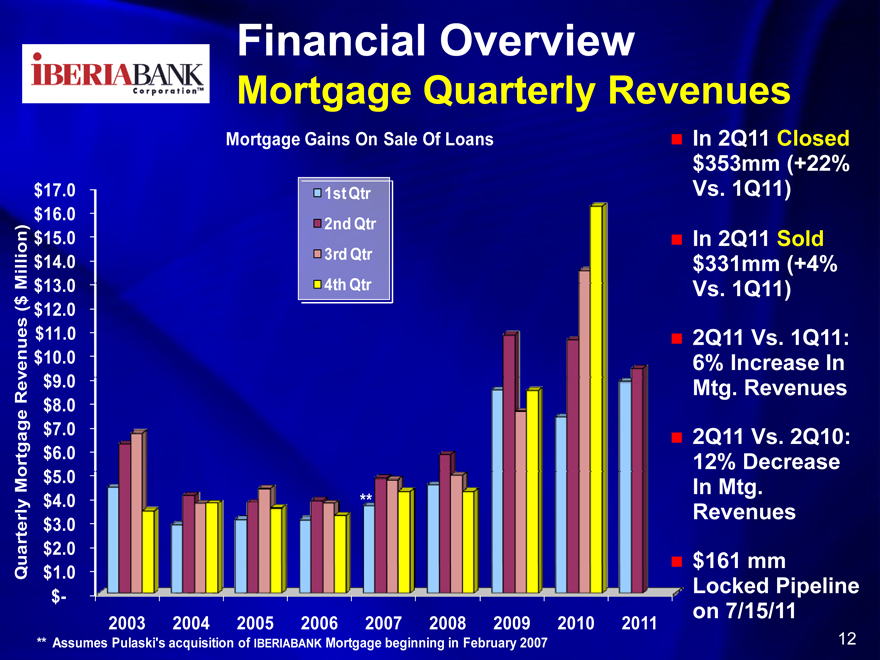

Mortgage Quarterly Revenues

Mortgage Gains On Sale Of Loans

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

$17.0 $16.0 $15.0 Million) $14.0 $13.0

( $ $12.0 $11.0 Revenues $10.0 $9.0 $8.0 $7.0 Mortgage $6.0 $5.0 $4.0 $3.0 Quarterly $2.0 $1.0 $-

2003 2004 2005 2006 2007 2008 2009 2010 2011

** Assumes Pulaski’s acquisition of IBERIABANK Mortgage beginning in February 2007

In 2Q11 Closed $353mm (+22% Vs. 1Q11)

In 2Q11 Sold $331mm (+4% Vs. 1Q11)

2Q11 Vs. 1Q11:

6% Increase In Mtg. Revenues

2Q11 Vs. 2Q10: 12% Decrease In Mtg.

Revenues

$161 mm Locked Pipeline on 7/15/11

12**

IBERIA BANK

Corporationtm

Financial Overview

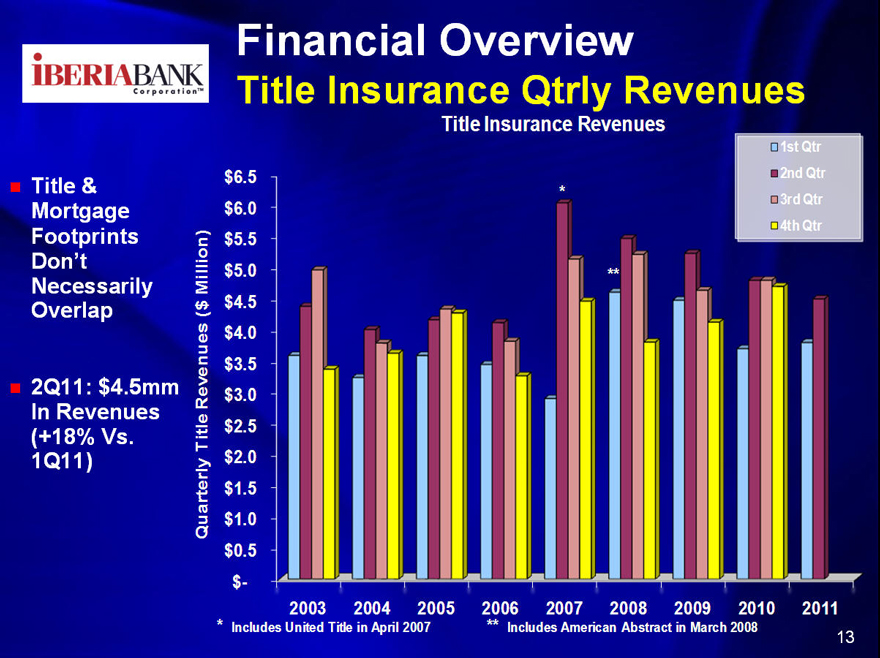

Title Insurance Qtrly Revenues

Title Insurance Revenues

Title & Mortgage Footprints Don’t Necessarily Overlap

2Q11: $4.5mm In Revenues (+18% Vs. 1Q11)

$6.5 $6.0 $5.5 ( $ Million) $5.0 $4.5 Revenues $4.0 $3.5 $3.0 Title $2.5 $2.0 $1.5 Quarterly $1.0 $0.5 $-

2003 2004 2005 2006 2007 2008 2009 2010 2011

* Includes United Title in April 2007 ** Includes American Abstract in March 2008

13 * **

IBERIA BANK

Corporationtm

Financial Overview

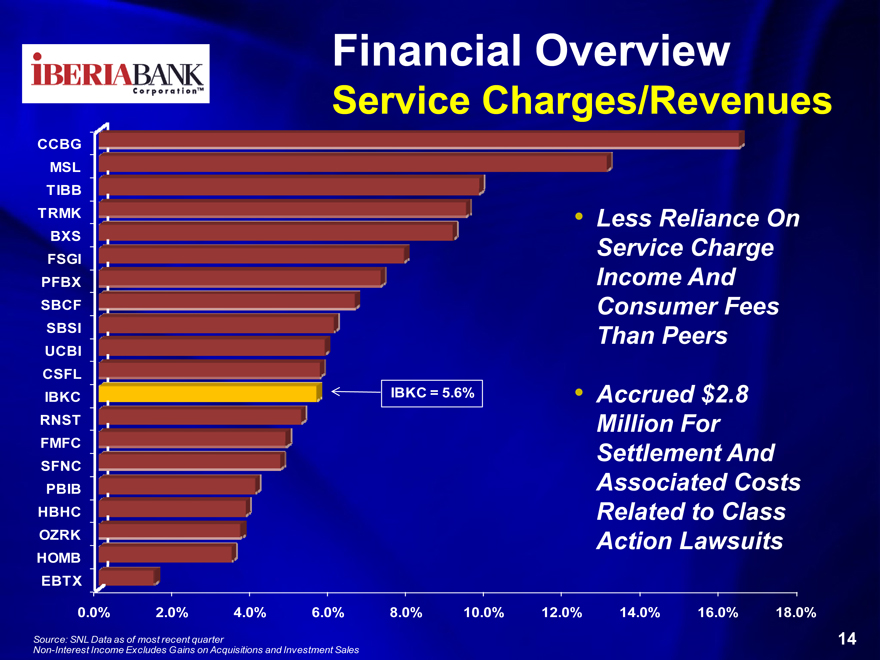

Service Charges/Revenues

CCBG MSL

TIBB TRMK

BXS FSGI PFBX SBCF SBSI UCBI CSFL IBKC RNST FMFC SFNC PBIB HBHC OZRK HOMB EBTX

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

• Less Reliance On Service Charge Income And Consumer Fees Than Peers

• Accrued $2.8 Million For Settlement And Associated Costs Related to Class Action Lawsuits

IBKC = 5.6%

Source: SNL Data as of most recent quarter

Non-Interest Income Excludes Gains on Acquisitions and Investment Sales

14

IBERIA BANK

Corporationtm

Financial Overview

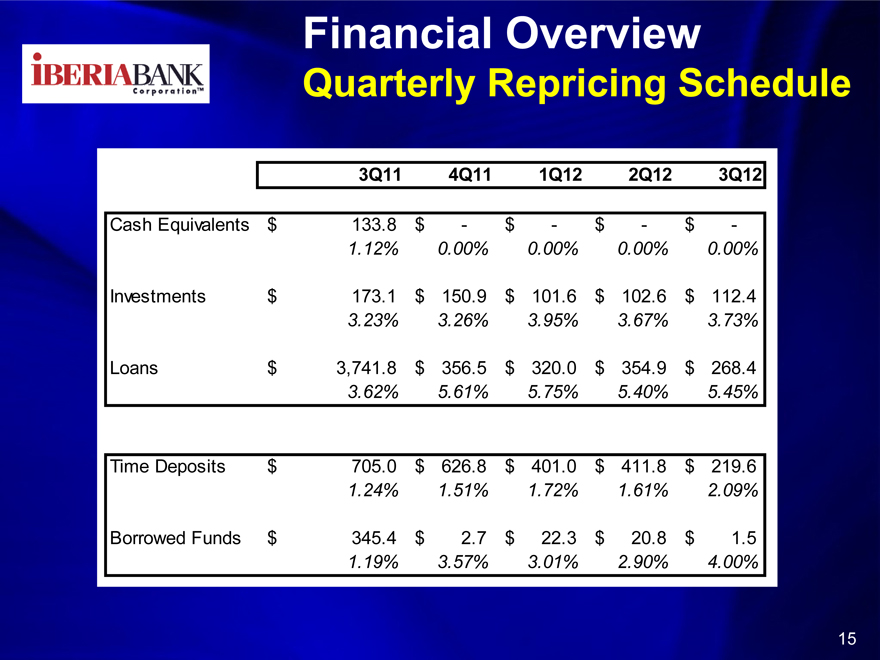

Quarterly Repricing Schedule

3Q11 4Q11 1Q12 2Q12 3Q12

Cash Equivalents $ 133.8 $ — $ — $ — $ -

1.12% 0.00% 0.00% 0.00% 0.00%

Investments $ 173.1 $ 150.9 $ 101.6 $ 102.6 $ 112.4

3.23% 3.26% 3.95% 3.67% 3.73%

Loans $ 3,741.8 $ 356.5 $ 320.0 $ 354.9 $ 268.4

3.62% 5.61% 5.75% 5.40% 5.45%

Time Deposits $ 705.0 $ 626.8 $ 401.0 $ 411.8 $ 219.6

1.24% 1.51% 1.72% 1.61% 2.09%

Borrowed Funds $ 345.4 $ 2.7 $ 22.3 $ 20.8 $ 1.5

1.19% 3.57% 3.01% 2.90% 4.00%

15

IBERIABANK

Corporation tm

Financial Overview

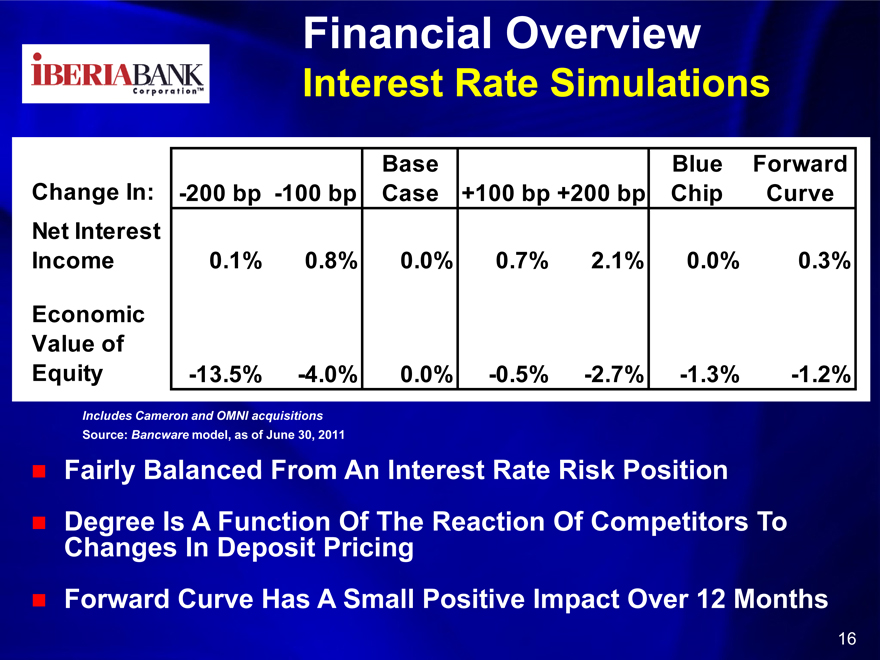

Interest Rate Simulations

Base Blue Forward

Change In: -200 bp -100 bp Case +100 bp +200 bp Chip Curve

Net Interest

Income 0.1% 0.8% 0.0% 0.7% 2.1% 0.0% 0.3%

Economic

Value of

Equity -13.5% -4.0% 0.0% -0.5% -2.7% -1.3% -1.2%

Includes Cameron and OMNI acquisitions

Source: Bancware model, as of June 30, 2011

Fairly Balanced From An Interest Rate Risk Position Degree Is A Function Of The Reaction Of Competitors To Changes In Deposit Pricing Forward Curve Has A Small Positive Impact Over 12 Months

16

IBERIABANK

Corporation tm

Financial Overview

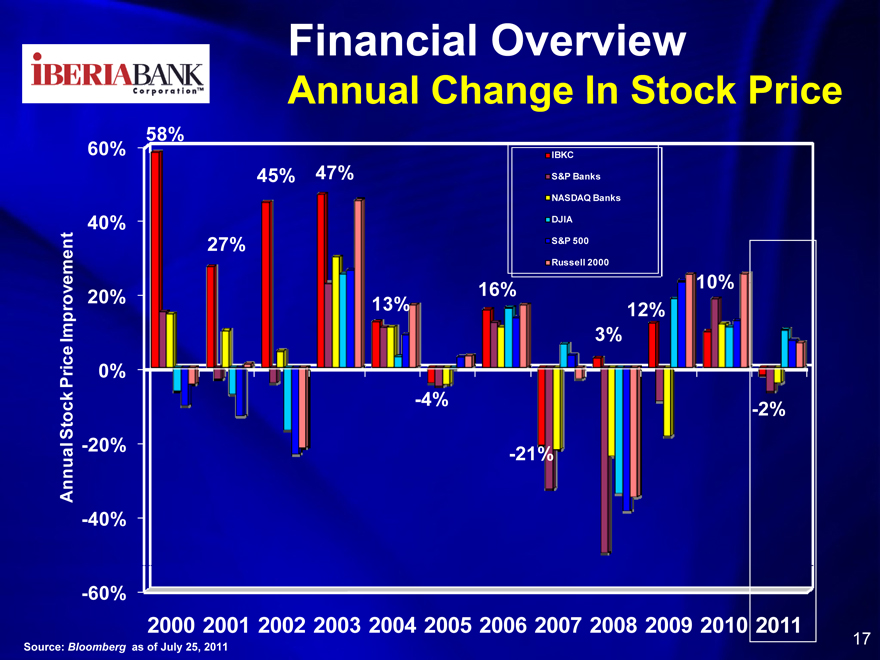

Annual Change In Stock Price

Annual Stock Price Improvement

— -

60% 40% 20% 0%- 20%- 40%- 60%

58% 27% 45% 47% 13% 16% 3% 12% 10% -4% -21% -2%

IBKC S&P Banks NASDAQ Banks DJIA

S&P 500

Russell 2000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20102011

Source: Bloomberg as of July 25, 2011

17

IBERIABANK

Corporation tm

Financial Overview

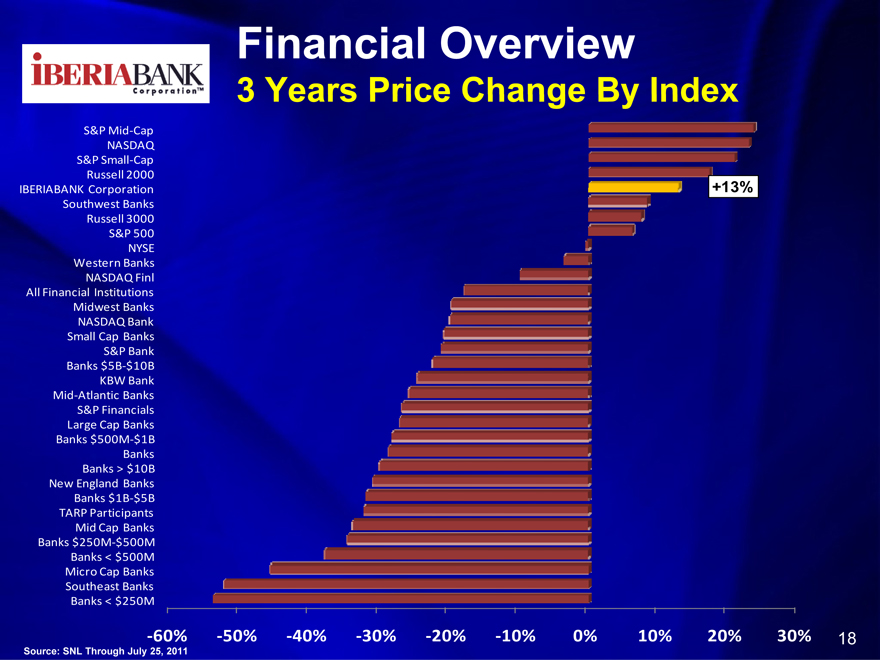

3 Years Price Change By Index

S&P Mid-Cap

NASDAQ

S&P Small-Cap

Russell 2000

IBERIABANK Corporation

Southwest Banks

Russell 3000

S&P 500

NYSE

Western Banks

NASDAQ Finl

All Financial Institutions

Midwest Banks

NASDAQ Bank

Small Cap Banks

S&P Bank

Banks $5B-$10B

KBW Bank

Mid-Atlantic Banks

S&P Financials

Large Cap Banks

Banks $500M-$1B

Banks

Banks > $10B

New England Banks

Banks $1B-$5B

TARP Participants

Mid Cap Banks

Banks $250M-$500M

Banks < $500M

Micro Cap Banks

Southeast Banks

Banks < $250M

+13%

-60% -50% -40% -30% -20% -10% 0% 10% 20% 30%

Source: SNL Through July 25, 2011

18

IBERIABANK

Corporation tm

Asset Quality

19

IBERIABANK

Corporation tm

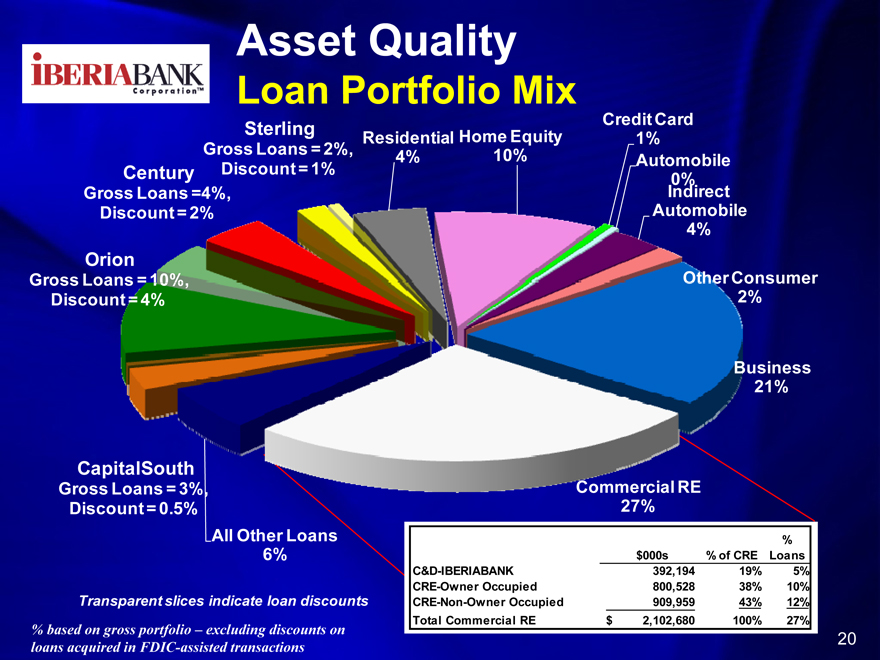

Asset Quality

Loan Portfolio Mix

Sterling Gross Loans = 2%, Discount = 1%

Century Gross Loans =4%, Discount = 2%

Orion Gross Loans = 10%, Discount = 4%

CapitalSouth Gross Loans = 3%, Discount = 0.5%

All Other Loans 6%

Transparent slices indicate loan discounts

% based on gross portfolio – excluding discounts on loans acquired in FDIC-assisted transactions

Residential Home Equity

4% 10%

Credit Card 1% Automobile 0% Indirect Automobile 4%

Other Consumer 2%

Business 21%

Commercial RE 27%

% Loans

$000s % of CRE

C&D-IBERIABANK 392,194 19% 5%

CRE-Owner Occupied 800,528 38% 10%

CRE-Non-Owner Occupied 909,959 43% 12%

Total Commercial RE $ 2,102,680 100% 27%

20

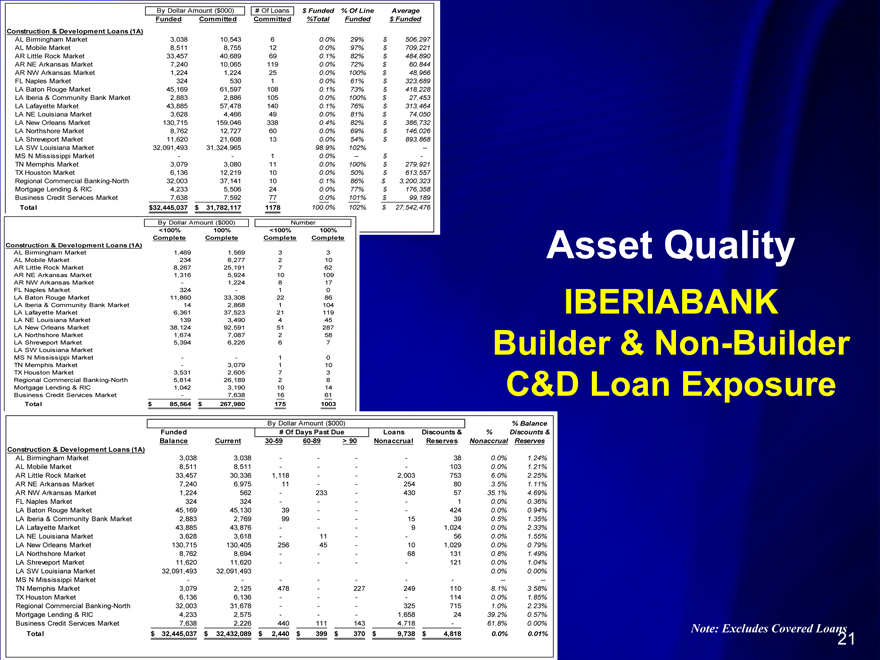

Asset Quality

IBERIABANK Builder & Non-Builder C&D Loan Exposure

By Dollar Amount ($000) # Of Loans $ Funded % Of Line Average

Funded Committed Committed %Total Funded $ Funded Construction & Development Loans (1A)

AL Birmingham Market 3,038 10,543 6 0.0% 29% $ 506,297 AL Mobile Market 8,511 8,755 12 0.0% 97% $ 709,221 AR Little Rock Market 33,457 40,689 69 0.1% 82% $ 484,890 AR NE Arkansas Market 7,240 10,065 119 0.0% 72% $ 60,844 AR NW Arkansas Market 1,224 1,224 25 0.0% 100% $ 48,966 FL Naples Market 324 530 1 0.0% 61% $ 323,689 LA Baton Rouge Market 45,169 61,597 108 0.1% 73% $ 418,228 LA Iberia & Community Bank Market 2,883 2,886 105 0.0% 100% $ 27,453 LA Lafayette Market 43,885 57,478 140 0.1% 76% $ 313,464 LA NE Louisiana Market 3,628 4,466 49 0.0% 81% $ 74,050 LA New Orleans Market 130,715 159,046 338 0.4% 82% $ 386,732 LA Northshore Market 8,762 12,727 60 0.0% 69% $ 146,026 LA Shreveport Market 11,620 21,608 13 0.0% 54% $ 893,868 LA SW Louisiana Market 32,091,493 31,324,965 98.9% 102% — MS N Mississippi Market — —1 0.0% — $ -TN Memphis Market 3,079 3,080 11 0.0% 100% $ 279,921 TX Houston Market 6,136 12,219 10 0.0% 50% $ 613,557 Regional Commercial Banking-North 32,003 37,141 10 0.1% 86% $ 3,200,323 Mortgage Lending & RIC 4,233 5,506 24 0.0% 77% $ 176,358 Business Credit Services Market 7,638 7,592 77 0.0% 101% $ 99,189

Total $ 32,445,037 $ 31,782,117 1178 100.0% 102% $ 27,542,476

By Dollar Amount ($000) Number

<100% 100% <100% 100%

Complete Complete Complete Complete

Construction & Development Loans (1A)

AL Birmingham Market 1,469 1,569 3 3 AL Mobile Market 234 8,277 2 10 AR Little Rock Market 8,267 25,191 7 62 AR NE Arkansas Market 1,316 5,924 10 109 AR NW Arkansas Market — 1,224 8 17 FL Naples Market 324 —1 0 LA Baton Rouge Market 11,860 33,308 22 86 LA Iberia & Community Bank Market 14 2,868 1 104 LA Lafayette Market 6,361 37,523 21 119 LA NE Louisiana Market 139 3,490 4 45 LA New Orleans Market 38,124 92,591 51 287 LA Northshore Market 1,674 7,087 2 58 LA Shreveport Market 5,394 6,226 6 7 LA SW Louisiana Market MS N Mississippi Market — —1 0 TN Memphis Market — 3,079 1 10 TX Houston Market 3,531 2,605 7 3 Regional Commercial Banking-North 5,814 26,189 2 8 Mortgage Lending & RIC 1,042 3,190 10 14 Business Credit Services Market — 7,638 16 61

Total $ 85,564 $ 267,980 175 1003

By Dollar Amount ($000) % Balance

Funded # Of Days Past Due Loans Discounts & % Discounts & Balance Current 30-59 60-89 > 90 Nonaccrual Reserves Nonaccrual Reserves Construction & Development Loans (1A)

AL Birmingham Market 3,038 3,038 — — — — 38 0.0% 1.24% AL Mobile Market 8,511 8,511 — — — — 103 0.0% 1.21% AR Little Rock Market 33,457 30,336 1,118 — — 2,003 753 6.0% 2.25% AR NE Arkansas Market 7,240 6,975 11 — — 254 80 3.5% 1.11% AR NW Arkansas Market 1,224 562 — 233 — 430 57 35.1% 4.69% FL Naples Market 324 324 — — — — 1 0.0% 0.36% LA Baton Rouge Market 45,169 45,130 39 — — — 424 0.0% 0.94% LA Iberia & Community Bank Market 2,883 2,769 99 — — 15 39 0.5% 1.35% LA Lafayette Market 43,885 43,876 — — — 9 1,024 0.0% 2.33% LA NE Louisiana Market 3,628 3,618 — 11 — — 56 0.0% 1.55% LA New Orleans Market 130,715 130,405 256 45 — 10 1,029 0.0% 0.79% LA Northshore Market 8,762 8,694 — — — 68 131 0.8% 1.49% LA Shreveport Market 11,620 11,620 — — — — 121 0.0% 1.04% LA SW Louisiana Market 32,091,493 32,091,493 0.0% 0.00% MS N Mississippi Market — — — — — — —— — TN Memphis Market 3,079 2,125 478 — 227 249 110 8.1% 3.58% TX Houston Market 6,136 6,136 — — — — 114 0.0% 1.85% Regional Commercial Banking-North 32,003 31,678 — — — 325 715 1.0% 2.23% Mortgage Lending & RIC 4,233 2,575 — — — 1,658 24 39.2% 0.57% Business Credit Services Market 7,638 2,226 440 111 143 4,718 —61.8% 0.00%

Total $ 32,445,037 $ 32,432,089 $ 2,440 $ 399 $ 370 $ 9,738 $ 4,818 0.0% 0.01%

Note: Excludes Covered Loans

21

Asset Quality

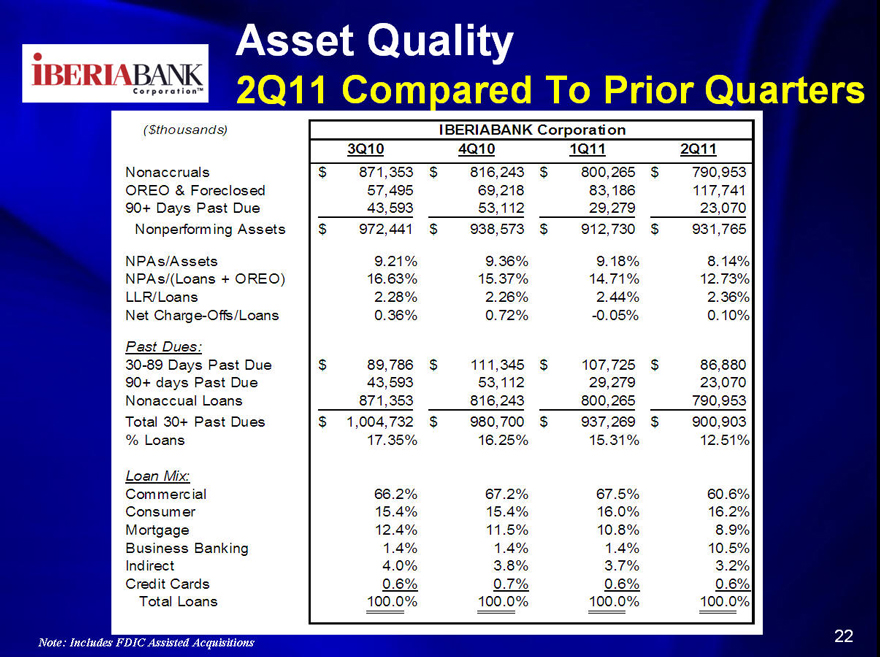

2Q11 Compared To Prior Quarters

($thousands) IBERIABANK Corporation

3Q10 4Q10 1Q11 2Q11

Nonaccruals $ 871,353 $ 816,243 $ 800,265 $ 790,953 OREO & Foreclosed 57,495 69,218 83,186 117,741 90+ Days Past Due 43,593 53,112 29,279 23,070 Nonperforming Assets $ 972,441 $ 938,573 $ 912,730 $ 931,765

NPAs/Assets 9.21% 9.36% 9.18% 8.14% NPAs/(Loans + OREO) 16.63% 15.37% 14.71% 12.73% LLR/Loans 2.28% 2.26% 2.44% 2.36% Net Charge-Offs/Loans 0.36% 0.72% -0.05% 0.10%

Past Dues:

30-89 Days Past Due $ 89,786 $ 111,345 $ 107,725 $ 86,880 90+ days Past Due 43,593 53,112 29,279 23,070 Nonaccual Loans 871,353 816,243 800,265 790,953 Total 30+ Past Dues $ 1,004,732 $ 980,700 $ 937,269 $ 900,903

% Loans 17.35% 16.25% 15.31% 12.51%

Loan Mix:

Commercial 66.2% 67.2% 67.5% 60.6% Consumer 15.4% 15.4% 16.0% 16.2% Mortgage 12.4% 11.5% 10.8% 8.9% Business Banking 1.4% 1.4% 1.4% 10.5% Indirect 4.0% 3.8% 3.7% 3.2% Credit Cards 0.6% 0.7% 0.6% 0.6% Total Loans 100.0% 100.0% 100.0% 100.0%

Note: Includes FDIC Assisted Acquisitions

22

Asset Quality

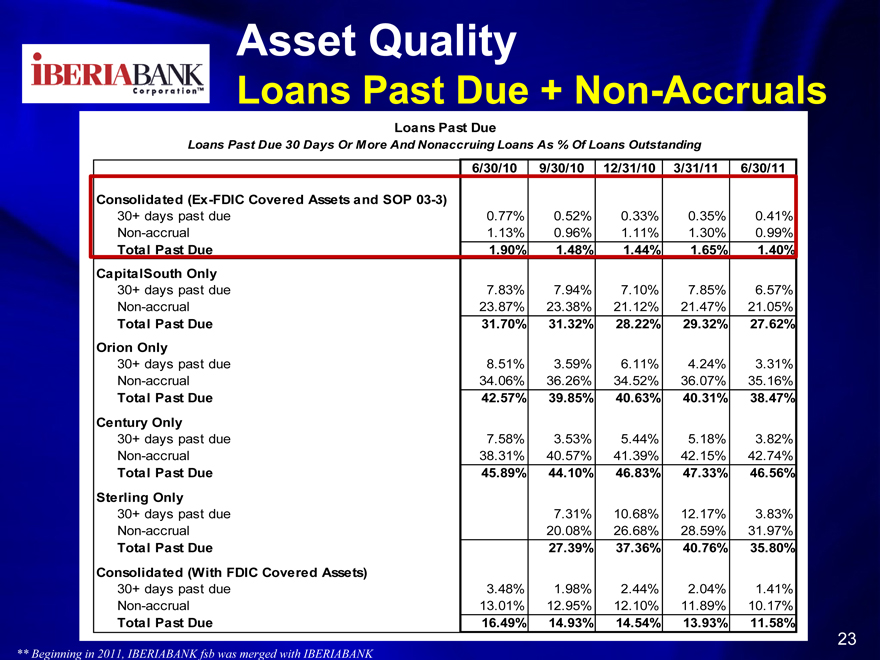

Loans Past Due + Non-Accruals

Loans Past Due

Loans Past Due 30 Days Or More And Nonaccruing Loans As % Of Loans Outstanding

6/30/10 9/30/10 12/31/10 3/31/11 6/30/11

Consolidated (Ex-FDIC Covered Assets and SOP 03-3)

30+ days past due 0.77% 0.52% 0.33% 0.35% 0.41% Non-accrual 1.13% 0.96% 1.11% 1.30% 0.99%

Total Past Due 1.90% 1.48% 1.44% 1.65% 1.40% CapitalSouth Only

30+ days past due 7.83% 7.94% 7.10% 7.85% 6.57% Non-accrual 23.87% 23.38% 21.12% 21.47% 21.05%

Total Past Due 31.70% 31.32% 28.22% 29.32% 27.62% Orion Only

30+ days past due 8.51% 3.59% 6.11% 4.24% 3.31% Non-accrual 34.06% 36.26% 34.52% 36.07% 35.16%

Total Past Due 42.57% 39.85% 40.63% 40.31% 38.47% Century Only

30+ days past due 7.58% 3.53% 5.44% 5.18% 3.82% Non-accrual 38.31% 40.57% 41.39% 42.15% 42.74%

Total Past Due 45.89% 44.10% 46.83% 47.33% 46.56% Sterling Only

30+ days past due 7.31% 10.68% 12.17% 3.83% Non-accrual 20.08% 26.68% 28.59% 31.97%

Total Past Due 27.39% 37.36% 40.76% 35.80% Consolidated (With FDIC Covered Assets)

30+ days past due 3.48% 1.98% 2.44% 2.04% 1.41% Non-accrual 13.01% 12.95% 12.10% 11.89% 10.17%

Total Past Due 16.49% 14.93% 14.54% 13.93% 11.58%

23

** Beginning in 2011, IBERIABANK fsb was merged with IBERIABANK

23

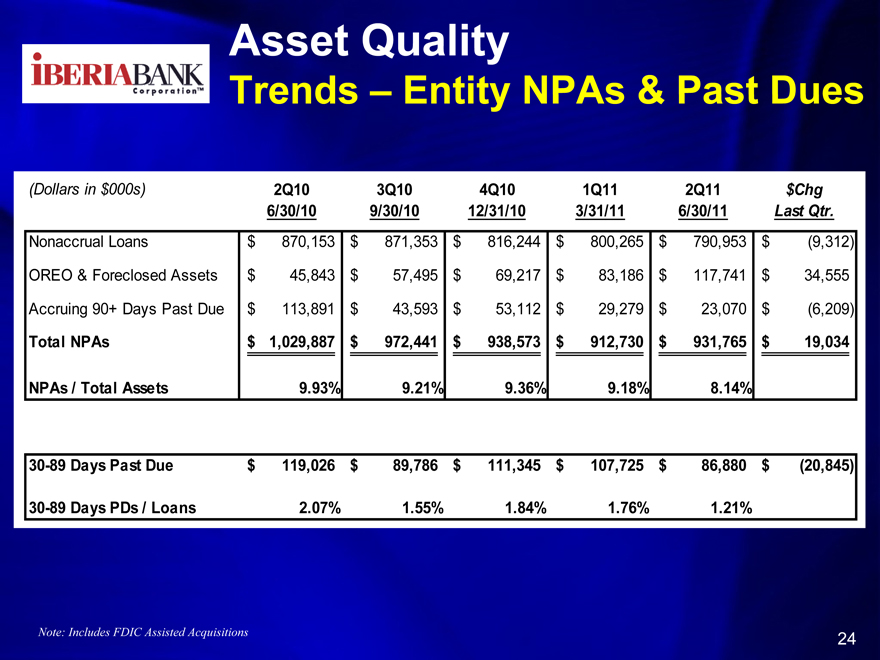

Asset Quality

Trends – Entity NPAs & Past Dues

(Dollars in $000s) 2Q10 3Q10 4Q10 1Q11 2Q11 $Chg 6/30/10 9/30/10 12/31/10 3/31/11 6/30/11 Last Qtr.

Nonaccrual Loans $ 870,153 $ 871,353 $ 816,244 $ 800,265 $ 790,953 $ (9,312)

OREO & Foreclosed Assets $ 45,843 $ 57,495 $ 69,217 $ 83,186 $ 117,741 $ 34,555

Accruing 90+ Days Past Due $ 113,891 $ 43,593 $ 53,112 $ 29,279 $ 23,070 $ (6,209)

Total NPAs $ 1,029,887 $ 972,441 $ 938,573 $ 912,730 $ 931,765 $ 19,034

NPAs / Total Assets 9.93% 9.21% 9.36% 9.18% 8.14%

30-89 Days Past Due $ 119,026 $ 89,786 $ 111,345 $ 107,725 $ 86,880 $ (20,845)

30-89 Days PDs / Loans 2.07% 1.55% 1.84% 1.76% 1.21%

Note: Includes FDIC Assisted Acquisitions

24

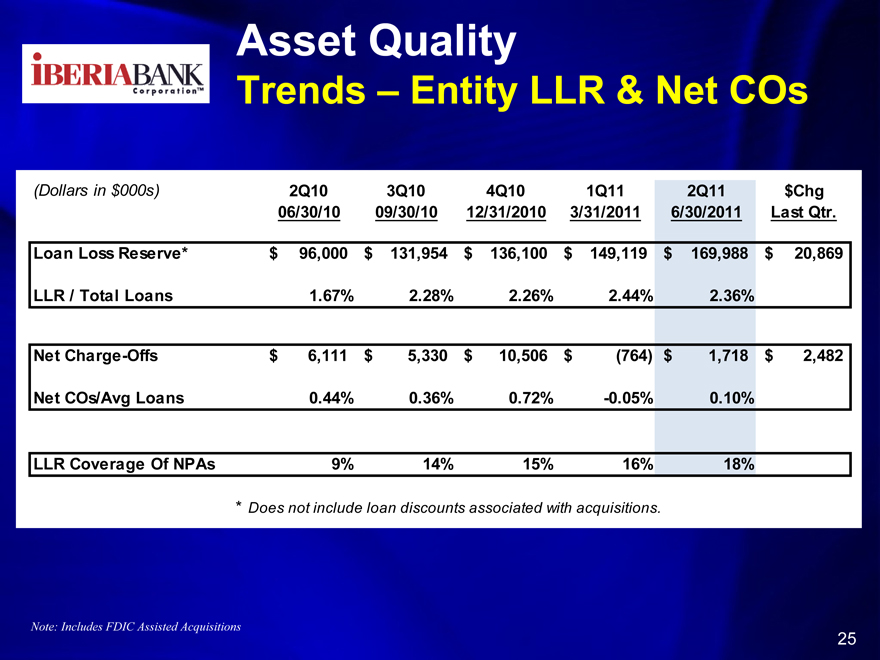

Asset Quality

Trends – Entity LLR & Net COs

(Dollars in $000s) 2Q10 3Q10 4Q10 1Q11 2Q11 $Chg 06/30/10 09/30/10 12/31/2010 3/31/2011 6/30/2011 Last Qtr.

Loan Loss Reserve* $ 96,000 $ 131,954 $ 136,100 $ 149,119 $ 169,988 $ 20,869

LLR / Total Loans 1.67% 2.28% 2.26% 2.44% 2.36%

Net Charge-Offs $ 6,111 $ 5,330 $ 10,506 $ (764) $ 1,718 $ 2,482

Net COs/Avg Loans 0.44% 0.36% 0.72% -0.05% 0.10%

LLR Coverage Of NPAs 9% 14% 15% 16% 18%

* Does not include loan discounts associated with acquisitions.

Note: Includes FDIC Assisted Acquisitions

25

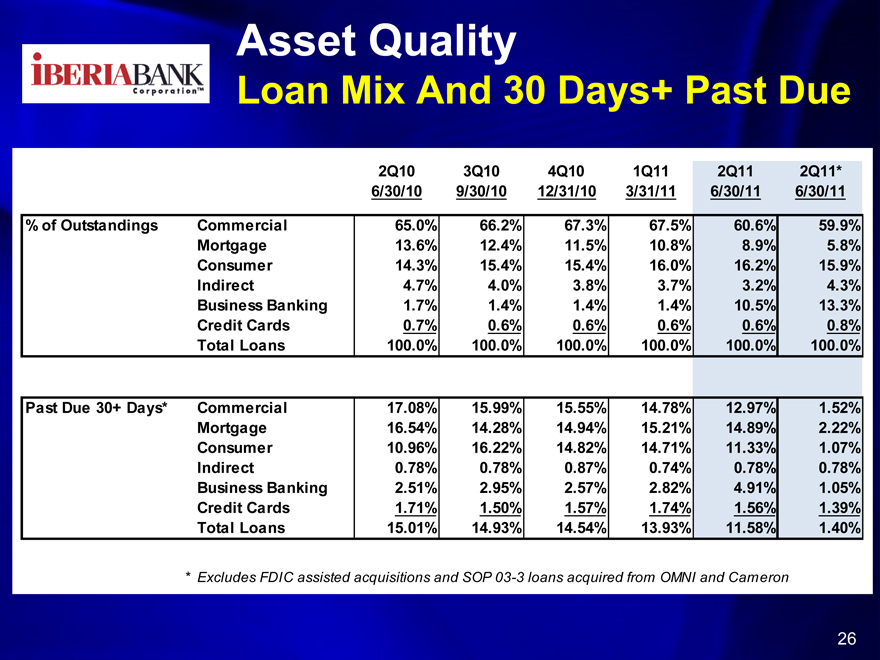

Asset Quality

Loan Mix And 30 Days+ Past Due

2Q10 3Q10 4Q10 1Q11 2Q11 2Q11* 6/30/10 9/30/10 12/31/10 3/31/11 6/30/11 6/30/11

% of Outstandings Commercial 65.0% 66.2% 67.3% 67.5% 60.6% 59.9% Mortgage 13.6% 12.4% 11.5% 10.8% 8.9% 5.8% Consumer 14.3% 15.4% 15.4% 16.0% 16.2% 15.9% Indirect 4.7% 4.0% 3.8% 3.7% 3.2% 4.3% Business Banking 1.7% 1.4% 1.4% 1.4% 10.5% 13.3% Credit Cards 0.7% 0.6% 0.6% 0.6% 0.6% 0.8% Total Loans 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Past Due 30+ Days* Commercial 17.08% 15.99% 15.55% 14.78% 12.97% 1.52% Mortgage 16.54% 14.28% 14.94% 15.21% 14.89% 2.22% Consumer 10.96% 16.22% 14.82% 14.71% 11.33% 1.07% Indirect 0.78% 0.78% 0.87% 0.74% 0.78% 0.78% Business Banking 2.51% 2.95% 2.57% 2.82% 4.91% 1.05% Credit Cards 1.71% 1.50% 1.57% 1.74% 1.56% 1.39% Total Loans 15.01% 14.93% 14.54% 13.93% 11.58% 1.40%

* Excludes FDIC assisted acquisitions and SOP 03-3 loans acquired from OMNI and Cameron

26

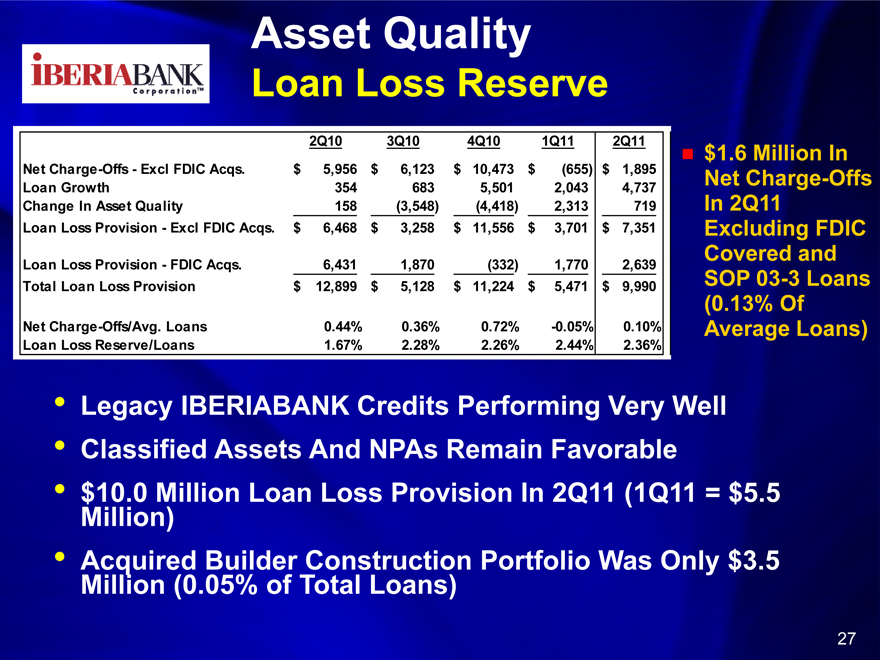

Asset Quality

Loan Loss Reserve

2Q10 3Q10 4Q10 1Q11 2Q11

$1.6 Million In

Net Charge-Offs—Excl FDIC Acqs. $ 5,956 $ 6,123 $ 10,473 $ (655) $ 1,895 Net Charge-Offs Loan Growth 354 683 5,501 2,043 4,737 Change In Asset Quality 158 (3,548) (4,418) 2,313 719 In 2Q11 Loan Loss Provision—Excl FDIC Acqs. $ 6,468 $ 3,258 $ 11,556 $ 3,701 $ 7,351 Excluding FDIC

Covered and

Loan Loss Provision—FDIC Acqs. 6,431 1,870 (332) 1,770 2,639

Total Loan Loss Provision $ 12,899 $ 5,128 $ 11,224 $ 5,471 $ 9,990 SOP 03-3 Loans

(0.13% Of Net Charge-Offs/Avg. Loans 0.44% 0.36% 0.72% -0.05% 0.10% Average Loans) Loan Loss Reserve/Loans 1.67% 2.28% 2.26% 2.44% 2.36%

• Legacy IBERIABANK Credits Performing Very Well

• Classified Assets And NPAs Remain Favorable

• $10.0 Million Loan Loss Provision In 2Q11 (1Q11 = $5.5 Million)

• Acquired Builder Construction Portfolio Was Only $3.5 Million (0.05% of Total Loans)

27

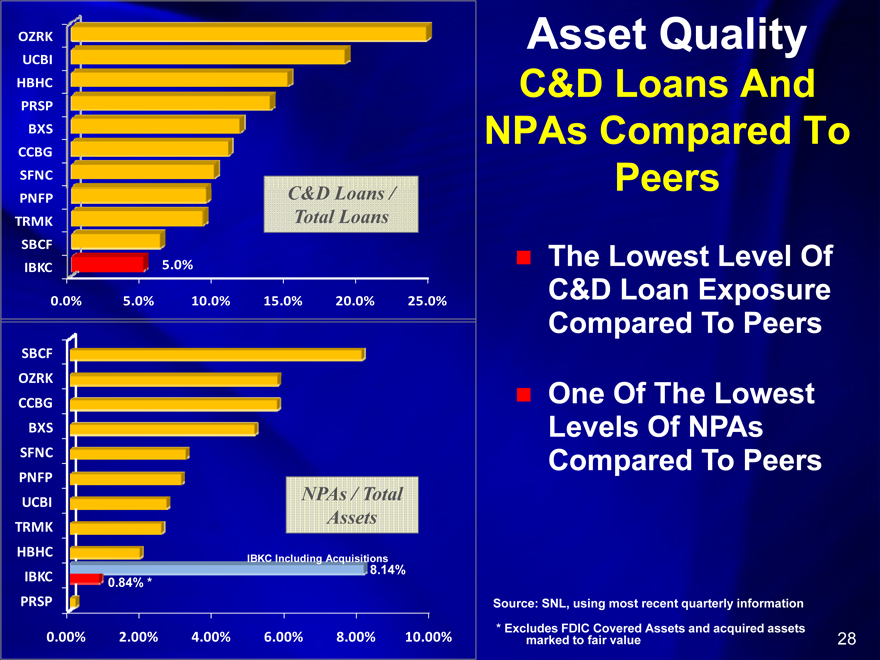

Asset Quality

C&D Loans And NPAs Compared To Peers

The Lowest Level Of C&D Loan Exposure Compared To Peers

One Of The Lowest Levels Of NPAs Compared To Peers

Source: SNL, using most recent quarterly information

* Excludes FDIC Covered Assets and acquired assets marked to fair value

OZRK UCBI HBHC PRSP

BXS CCBG SFNC PNFP TRMK SBCF

IBKC

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

5.0%

C&D Loans / Total Loans

SBCF OZRK CCBG

BXS SFNC PNFP UCBI TRMK HBHC

IBKC PRSP

NPAs / Total Assets

IBKC Including Acquisitions 8.14%

0.84% *

0.00% 2.00% 4.00% 6.00% 8.00% 10.00%

28

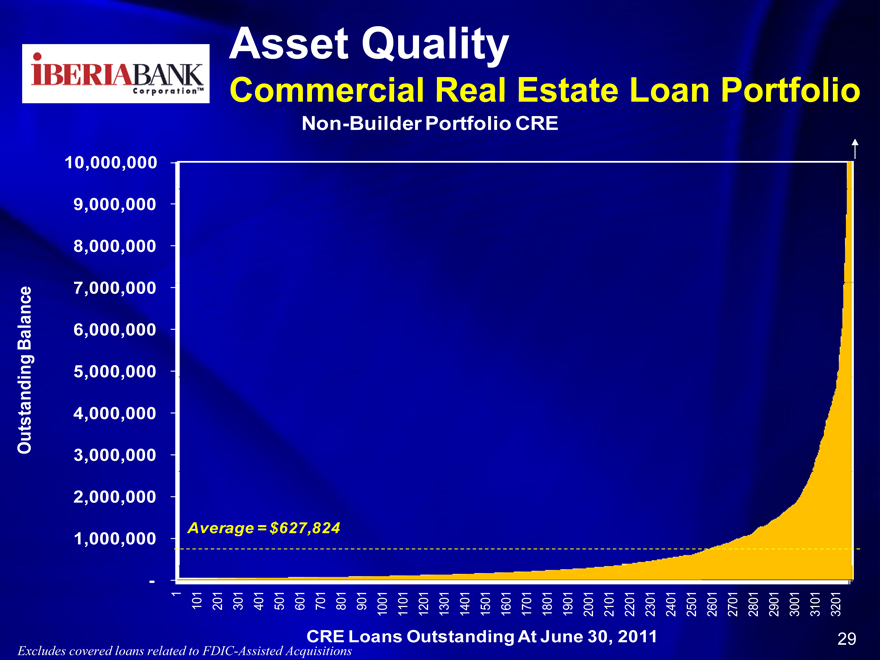

Asset Quality

Commercial Real Estate Loan Portfolio

Non-Builder Portfolio CRE

10,000,000 9,000,000 8,000,000 7,000,000 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000,000

Outstanding Balance

Average = $627, 824

-

1 101 201 301 401 501 601 701 801 901 1001 1101 1201 1301 1401 1501 1601 1701 1801 1901 2001 2101 2201 2301 2401 2501 2601 2701 2801 2901 3001 3101 3201

CRE Loans Outstanding At June 30, 2011

Excludes covered loans related to FDIC-Assisted Acquisitions

29

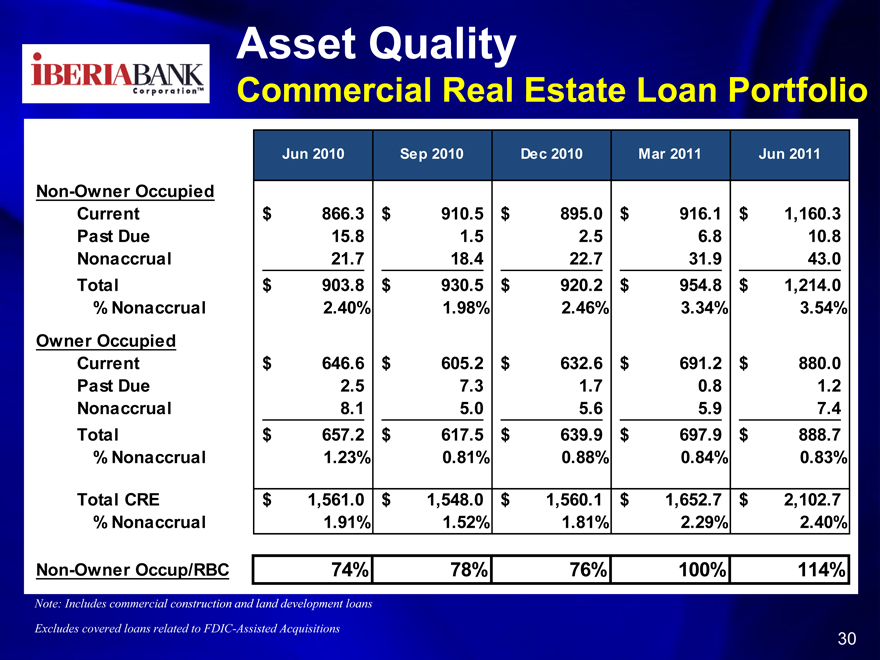

Asset Quality

Commercial Real Estate Loan Portfolio

Jun 2010 Sep 2010 Dec 2010 Mar 2011 Jun 2011

Non-Owner Occupied

Current $ 866.3 $ 910.5 $ 895.0 $ 916.1 $ 1,160.3 Past Due 15.8 1.5 2.5 6.8 10.8 Nonaccrual 21.7 18.4 22.7 31.9 43.0 Total $ 903.8 $ 930.5 $ 920.2 $ 954.8 $ 1,214.0

% Nonaccrual 2.40% 1.98% 2.46% 3.34% 3.54% Owner Occupied Current $ 646.6 $ 605.2 $ 632.6 $ 691.2 $ 880.0 Past Due 2.5 7.3 1.7 0.8 1.2 Nonaccrual 8.1 5.0 5.6 5.9 7.4 Total $ 657.2 $ 617.5 $ 639.9 $ 697.9 $ 888.7

% Nonaccrual 1.23% 0.81% 0.88% 0.84% 0.83%

Total CRE $ 1,561.0 $ 1,548.0 $ 1,560.1 $ 1,652.7 $ 2,102.7

% Nonaccrual 1.91% 1.52% 1.81% 2.29% 2.40% Non-Owner Occup/RBC 74% 78% 76% 100% 114%

Note: Includes commercial construction and land development loans

Excludes covered loans related to FDIC-Assisted Acquisitions

30

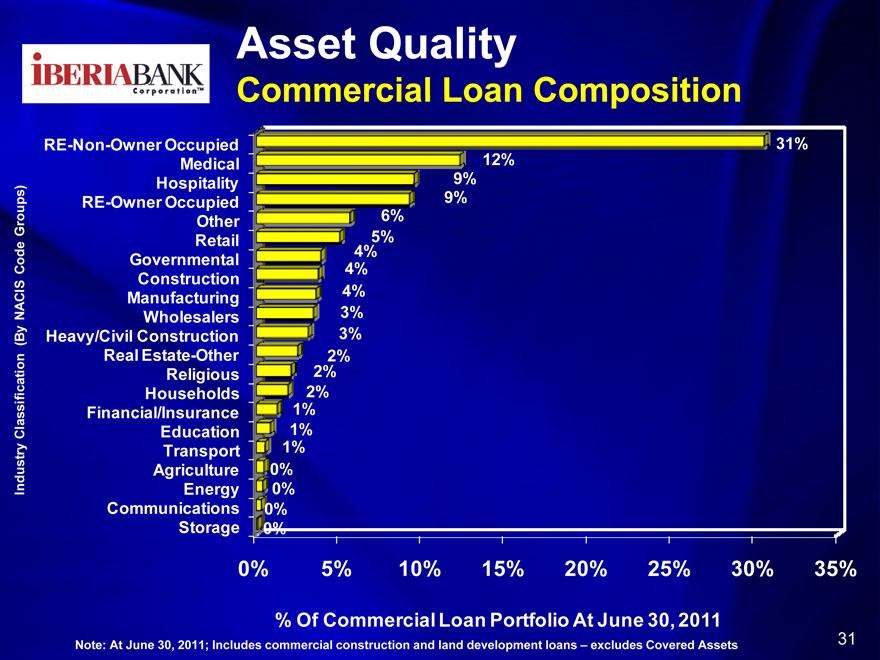

Asset Quality

CorporationTM

Commercial Loan Composition

RE-Non-Owner Occupied Medical Hospitality RE-Owner Occupied

Groups) Other

Retail Code Governmental Construction Manufacturing Wholesalers

NACIS(By

Heavy/Civil Construction Classification Real Estate-Other Religious Households Financial/Insurance

Education

Transport Agriculture Industry Energy Communications Storage

0% 5% 10% 15% 20% 25% 30% 35%

% Of Commercial Loan Portfolio At June 30, 2011

Note: At June 30, 2011; Includes commercial construction and land development loans – excludes Covered Assets

31%

12%

9%

9%

5%

6%

4%

4%

4%

3%

3%

2%

2%

2%

1%

1%

1%

0%

0%

0%

0%

31

CorporationTM

Consumer Loan Portfolio

32

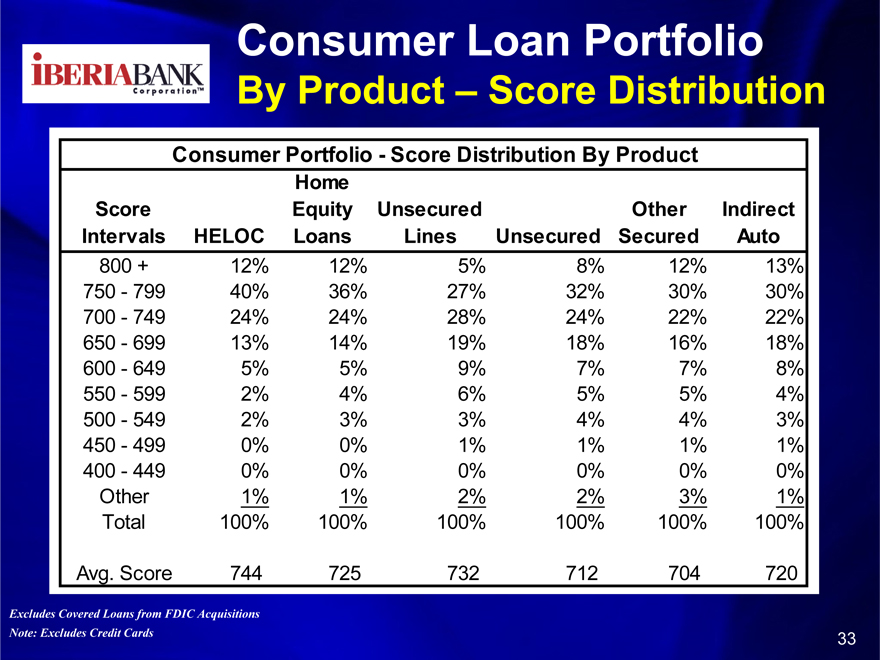

CorporationTM

Consumer Loan Portfolio

By Product – Score Distribution

Consumer Portfolio—Score Distribution By Product Home

Score Equity Unsecured Other Indirect Intervals HELOC Loans Lines Unsecured Secured Auto

800 + 12% 12% 5% 8% 12% 13% 750—799 40% 36% 27% 32% 30% 30% 700—749 24% 24% 28% 24% 22% 22% 650—699 13% 14% 19% 18% 16% 18% 600—649 5% 5% 9% 7% 7% 8% 550—599 2% 4% 6% 5% 5% 4% 500—549 2% 3% 3% 4% 4% 3% 450—499 0% 0% 1% 1% 1% 1% 400—449 0% 0% 0% 0% 0% 0% Other 1% 1% 2% 3% 1% Total 100% 100% 100% 100% 100% 100%

Avg. Score 744 725 732 712 704 720

Excludes Covered Loans from FDIC Acquisitions Note: Excludes Credit Cards

33

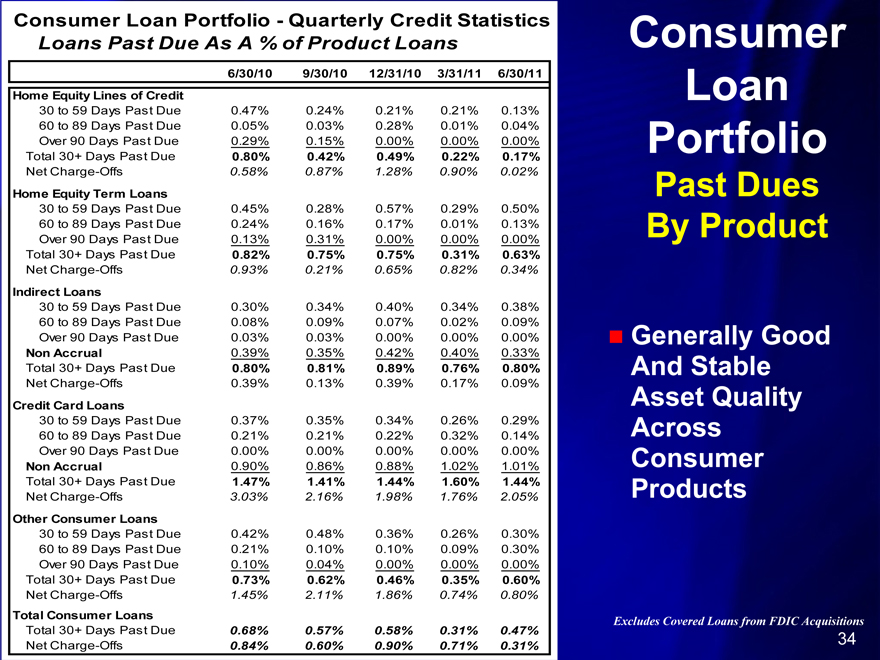

CorporationTM

Consumer Loan Portfolio—Quarterly Credit Statistics

Loans Past Due As A % of Product Loans

6/30/10 9/30/10 12/31/10 3/31/11 6/30/11 Home Equity Lines of Credit

30 to 59 Days Past Due 0.47% 0.24% 0.21% 0.21% 0.13% 60 to 89 Days Past Due 0.05% 0.03% 0.28% 0.01% 0.04% Over 90 Days Past Due 0.29% 0.15% 0.00% 0.00% 0.00% Total 30+ Days Past Due 0.80% 0.42% 0.49% 0.22% 0.17%

Net Charge-Offs 0.58% 0.87% 1.28% 0.90% 0.02%

Home Equity Term Loans

30 to 59 Days Past Due 0.45% 0.28% 0.57% 0.29% 0.50% 60 to 89 Days Past Due 0.24% 0.16% 0.17% 0.01% 0.13% Over 90 Days Past Due 0.13% 0.31% 0.00% 0.00% 0.00% Total 30+ Days Past Due 0.82% 0.75% 0.75% 0.31% 0.63%

Net Charge-Offs 0.93% 0.21% 0.65% 0.82% 0.34%

Indirect Loans

30 to 59 Days Past Due 0.30% 0.34% 0.40% 0.34% 0.38% 60 to 89 Days Past Due 0.08% 0.09% 0.07% 0.02% 0.09% Over 90 Days Past Due 0.03% 0.03% 0.00% 0.00% 0.00% Non Accrual 0.39% 0.35% 0.42% 0.40% 0.33% Total 30+ Days Past Due 0.80% 0.81% 0.89% 0.76% 0.80%

Net Charge-Offs 0.39% 0.13% 0.39% 0.17% 0.09%

Credit Card Loans

30 to 59 Days Past Due 0.37% 0.35% 0.34% 0.26% 0.29% 60 to 89 Days Past Due 0.21% 0.21% 0.22% 0.32% 0.14% Over 90 Days Past Due 0.00% 0.00% 0.00% 0.00% 0.00% Non Accrual 0.90% 0.86% 0.88% 1.02% 1.01% Total 30+ Days Past Due 1.47% 1.41% 1.44% 1.60% 1.44%

Net Charge-Offs 3.03% 2.16% 1.98% 1.76% 2.05%

Other Consumer Loans

30 to 59 Days Past Due 0.42% 0.48% 0.36% 0.26% 0.30% 60 to 89 Days Past Due 0.21% 0.10% 0.10% 0.09% 0.30% Over 90 Days Past Due 0.10% 0.04% 0.00% 0.00% 0.00% Total 30+ Days Past Due 0.73% 0.62% 0.46% 0.35% 0.60%

Net Charge-Offs 1.45% 2.11% 1.86% 0.74% 0.80%

Total Consumer Loans

Total 30+ Days Past Due 0.68% 0.57% 0.58% 0.31% 0.47% Net Charge-Offs 0.84% 0.60% 0.90% 0.71% 0.31%

Consumer Loan Portfolio

Past Dues By Product

Generally Good And Stable Asset Quality Across Consumer Products

Excludes Covered Loans from FDIC Acquisitions

34

CorporationTM

Consumer Loan Portfolio

By Product – Origination Mix

Originations—Product Total %

Home Equity 2nd Home Equity 1st HELOC 2nd HELOC 1st

100% 90% 80%

70% Production 60% 50% Quarterly % Of 40% 30%

20% 10% 0%

1Q07 3Q07 1Q08 3Q08 1Q09 3Q09 1Q10 3Q10 1Q11 Quarter

3%

44%

31%

22%

35

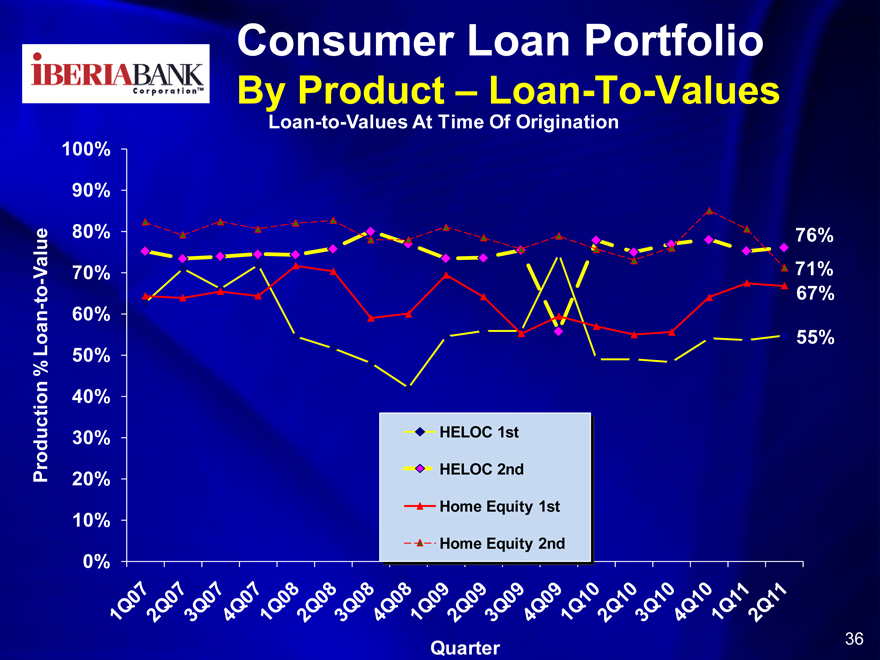

CorporationTM

Consumer Loan Portfolio

By Product – Loan-To-Values

Loan-to-Values At Time Of Origination

HELOC 1st HELOC 2nd Home Equity 1st Home Equity 2nd

100%

90%

Value 80%

- 70%—to 60% Loan% 50%

40% Production 30% 20%

10%

0%

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

Quarter

36

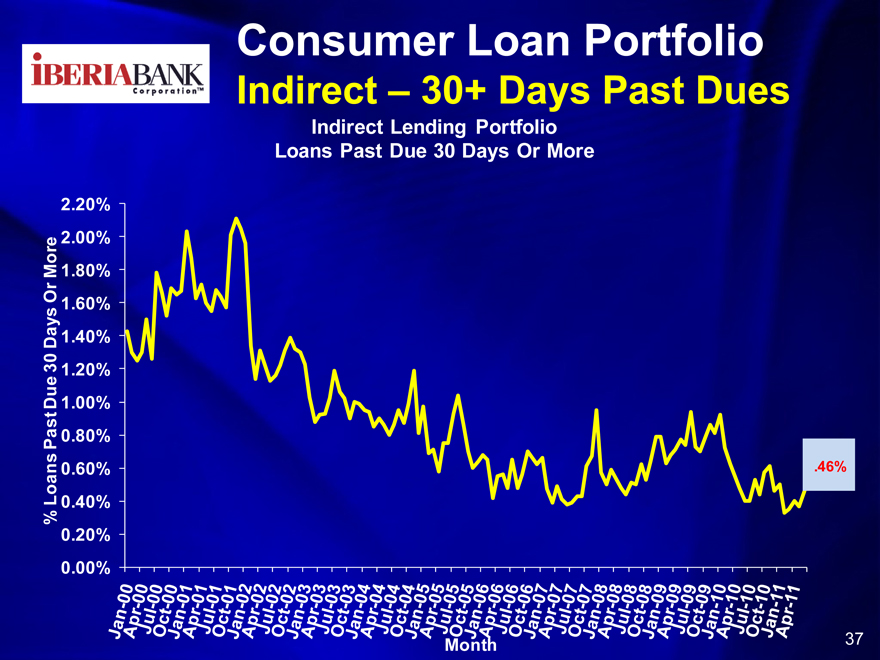

CorporationTM

Consumer Loan Portfolio

Indirect – 30+ Days Past Dues

Indirect Lending Portfolio Loans Past Due 30 Days Or More

% Loans Past Due 30 Days Or More 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60% 1.80% 2.00% 2.20%

Jan-00

Apr-00

Jul-00

oct-00

Jan-01

Apr-01

Jul-01

oct-01

Jan-02

Apr-02

Jul-02

oct-02

Jan-03

Apr-03

Jul-03

oct-03

Jan-04

Apr-04

Jul-04

oct-04

Jan-05

Apr-05

Jul-05

oct-05

Jan-06

Apr-06

Jul-06

oct-06

Jan-07

Apr-07

Jul-07

oct-07

Jan-08

Apr-08

Jul-08

oct-08

Jan-09

Apr-09

Jul-09

oct-09

Jan-10

Apr-10

Jul-10

oct-10

Jan-11

Apr-11

.46%

Month

37

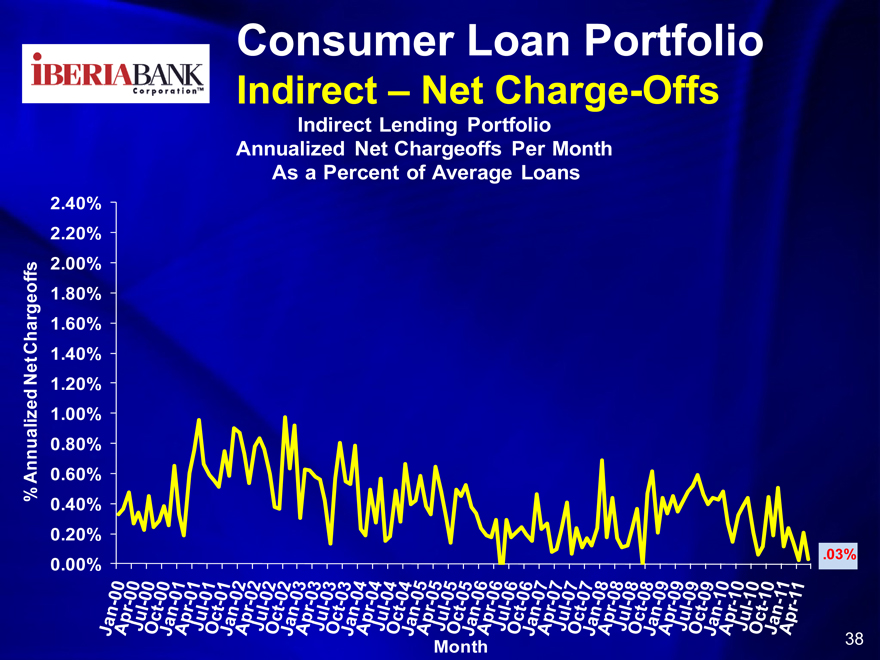

CorporationTM

Consumer Loan Portfolio

Indirect – Net Charge-Offs

Indirect Lending Portfolio Annualized Net Chargeoffs Per Month As a Percent of Average Loans

2.40% 2.20% 2.00% 1.80% Chargeoffs 1.60% Net 1.40% 1.20% 1.00% % Annualized 0.80% 0.60% 0.40% 0.20% 0.00%

Jan-00

Apr-00

Jul-00

oct-00

Jan-01

Apr-01

Jul-01

oct-01

Jan-02

Apr-02

Jul-02

oct-02

Jan-03

Apr-03

Jul-03

oct-03

Jan-04

Apr-04

Jul-04

oct-04

Jan-05

Apr-05

Jul-05

oct-05

Jan-06

Apr-06

Jul-06

oct-06

Jan-07

Apr-07

Jul-07

oct-07

Jan-08

Apr-08

Jul-08

oct-08

Jan-09

Apr-09

Jul-09

oct-09

Jan-10

Apr-10

Jul-10

oct-10

Jan-11

Apr-11

.03%

Month

38

CorporationTM

FDIC Loss Share Performance

39

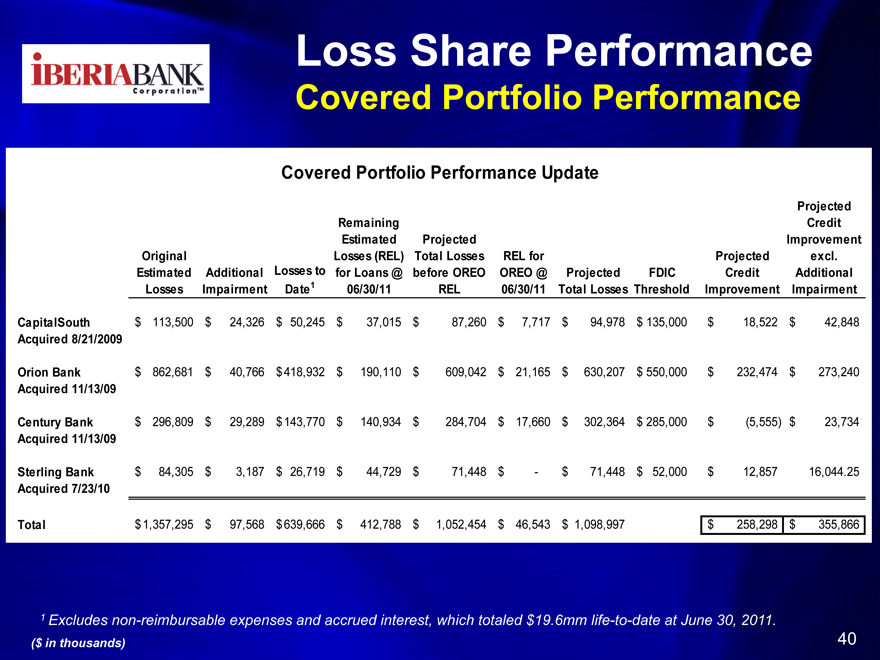

CorporationTM

Loss Share Performance

Covered Portfolio Performance

Covered Portfolio Performance Update

Projected Remaining Credit Estimated Projected Improvement Original Losses (REL) Total Losses REL for Projected excl. Estimated Additional Losses to for Loans @ before OREO OREO @ Projected FDIC Credit Additional Losses Impairment Date1 06/30/11 REL 06/30/11 Total Losses Threshold Improvement Impairment

CapitalSouth $ 113,500 $ 24,326 $ 50,245 $ 37,015 $ 87,260 $ 7,717 $ 94,978 $ 135,000 $ 18,522 $ 42,848

Acquired 8/21/2009

Orion Bank $ 862,681 $ 40,766 $418,932 $ 190,110 $ 609,042 $ 21,165 $ 630,207 $ 550,000 $ 232,474 $ 273,240

Acquired 11/13/09

Century Bank $ 296,809 $ 29,289 $ 143,770 $ 140,934 $ 284,704 $ 17,660 $ 302,364 $ 285,000 $ (5,555) $ 23,734

Acquired 11/13/09

Sterling Bank $ 84,305 $ 3,187 $ 26,719 $ 44,729 $ 71,448 $ —$ 71,448 $ 52,000 $ 12,857 16,044.25

Acquired 7/23/10

Total $ 1,357,295 $ 97,568 $ 639,666 $ 412,788 $ 1,052,454 $ 46,543 $ 1,098,997 $ 258,298 $ 355,866

1 Excludes non-reimbursable expenses and accrued interest, which totaled $19.6mm life-to-date at June 30, 2011.

($ in thousands)

40

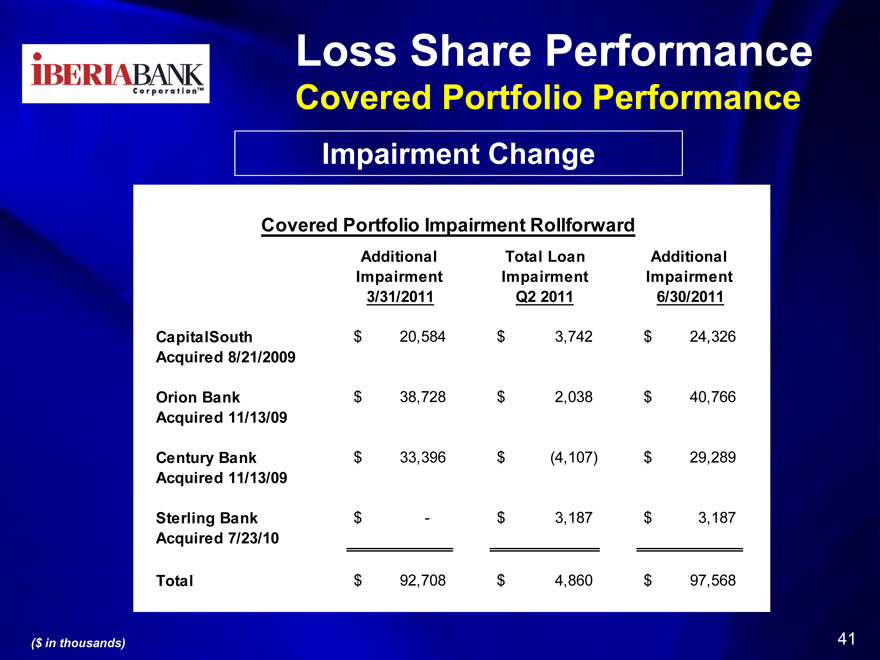

CorporationTM

Loss Share Performance

Covered Portfolio Performance

Impairment Change

Covered Portfolio Impairment Rollforward

Additional Total Loan Additional Impairment Impairment Impairment 3/31/2011 Q2 2011 6/30/2011

CapitalSouth $ 20,584 $ 3,742 $ 24,326

Acquired 8/21/2009

Orion Bank $ 38,728 $ 2,038 $ 40,766

Acquired 11/13/09

Century Bank $ 33,396 $ (4,107) $ 29,289

Acquired 11/13/09

Sterling Bank $ —$ 3,187 $ 3,187

Acquired 7/23/10

Total $ 92,708 $ 4,860 $ 97,568

($ in thousands)

41

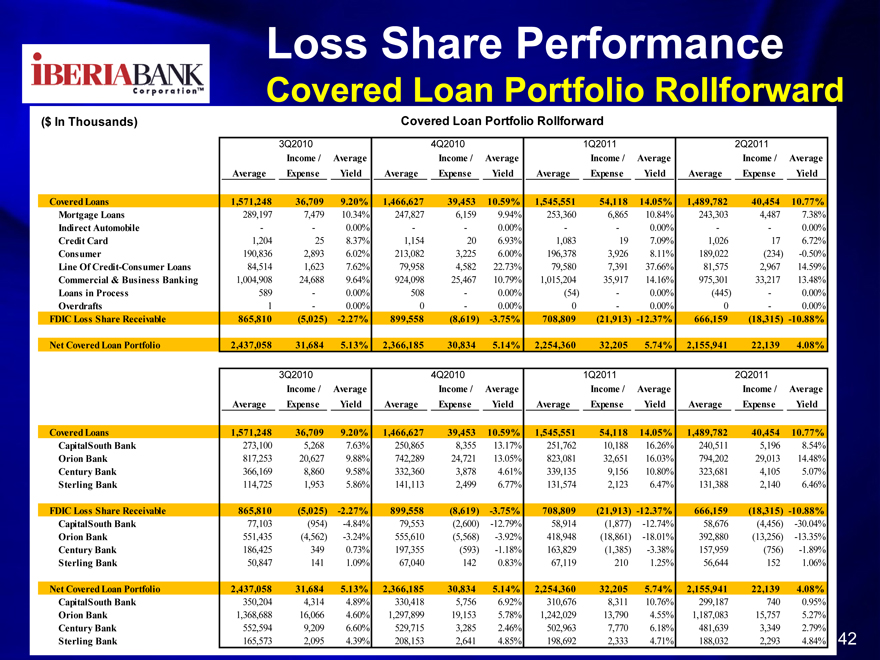

Corporatio TM

Loss Share Performance

Covered Loan Portfolio Rollforward

($ In Thousands) Covered Loan Portfolio Rollforward

3Q2010 4Q2010 1Q2011 2Q2011

Income / Average Income / Average Income / Average Income / Average Average Expense Yield Average Expense Yield Average Expense Yield Average Expense Yield

Covered Loans 1,571,248 36,709 9.20% 1,466,627 39,453 10.59% 1,545,551 54,118 14.05% 1,489,782 40,454 10.77% Mortgage Loans 289,197 7,479 10.34% 247,827 6,159 9.94% 253,360 6,865 10.84% 243,303 4,487 7.38% Indirect Automobile — —0.00% — —0.00% — —0.00% — —0.00% Credit Card 1,204 25 8.37% 1,154 20 6.93% 1,083 19 7.09% 1,026 17 6.72% Consumer 190,836 2,893 6.02% 213,082 3,225 6.00% 196,378 3,926 8.11% 189,022 (234) -0.50% Line Of Credit-Consumer Loans 84,514 1,623 7.62% 79,958 4,582 22.73% 79,580 7,391 37.66% 81,575 2,967 14.59% Commercial & Business Banking 1,004,908 24,688 9.64% 924,098 25,467 10.79% 1,015,204 35,917 14.16% 975,301 33,217 13.48% Loans in Process 589 —0.00% 508 —0.00% (54) —0.00% (445) —0.00% Overdrafts 1 —0.00% 0 —0.00% 0 —0.00% 0 —0.00%

FDIC Loss Share Receivable 865,810 (5,025) -2.27% 899,558 (8,619) -3.75% 708,809 (21,913) -12.37% 666,159 (18,315) -10.88%

Net Covered Loan Portfolio 2,437,058 31,684 5.13% 2,366,185 30,834 5.14% 2,254,360 32,205 5.74% 2,155,941 22,139 4.08%

3Q2010 4Q2010 1Q2011 2Q2011

Income / Average Income / Average Income / Average Income / Average Average Expense Yield Average Expense Yield Average Expense Yield Average Expense Yield

Covered Loans 1,571,248 36,709 9.20% 1,466,627 39,453 10.59% 1,545,551 54,118 14.05% 1,489,782 40,454 10.77% CapitalSouth Bank 273,100 5,268 7.63% 250,865 8,355 13.17% 251,762 10,188 16.26% 240,511 5,196 8.54% Orion Bank 817,253 20,627 9.88% 742,289 24,721 13.05% 823,081 32,651 16.03% 794,202 29,013 14.48% Century Bank 366,169 8,860 9.58% 332,360 3,878 4.61% 339,135 9,156 10.80% 323,681 4,105 5.07% Sterling Bank 114,725 1,953 5.86% 141,113 2,499 6.77% 131,574 2,123 6.47% 131,388 2,140 6.46%

FDIC Loss Share Receivable 865,810 (5,025) -2.27% 899,558 (8,619) -3.75% 708,809 (21,913) -12.37% 666,159 (18,315) -10.88% CapitalSouth

Bank 77,103 (954) -4.84% 79,553 (2,600) -12.79% 58,914 (1,877) -12.74% 58,676 (4,456) -30.04% Orion Bank 551,435 (4,562) -3.24% 555,610 (5,568) -3.92% 418,948 (18,861) -18.01% 392,880 (13,256) -13.35% Century Bank 186,425 349 0.73% 197,355 (593) -1.18% 163,829 (1,385) -3.38% 157,959 (756) -1.89% Sterling Bank 50,847 141 1.09% 67,040 142 0.83% 67,119 210 1.25% 56,644 152 1.06%

Net Covered Loan Portfolio 2,437,058 31,684 5.13% 2,366,185 30,834 5.14% 2,254,360 32,205 5.74% 2,155,941 22,139 4.08% CapitalSouth Bank 350,204 4,314 4.89% 330,418 5,756 6.92% 310,676 8,311 10.76% 299,187 740 0.95% Orion Bank 1,368,688 16,066 4.60% 1,297,899 19,153 5.78% 1,242,029 13,790 4.55% 1,187,083 15,757 5.27% Century Bank 552,594 9,209 6.60% 529,715 3,285 2.46% 502,963 7,770 6.18% 481,639 3,349 2.79% Sterling Bank 165,573 2,095 4.39% 208,153 2,641 4.85% 198,692 2,333 4.71% 188,032 2,293 4.84%

42

CorporationTM

Markets

43

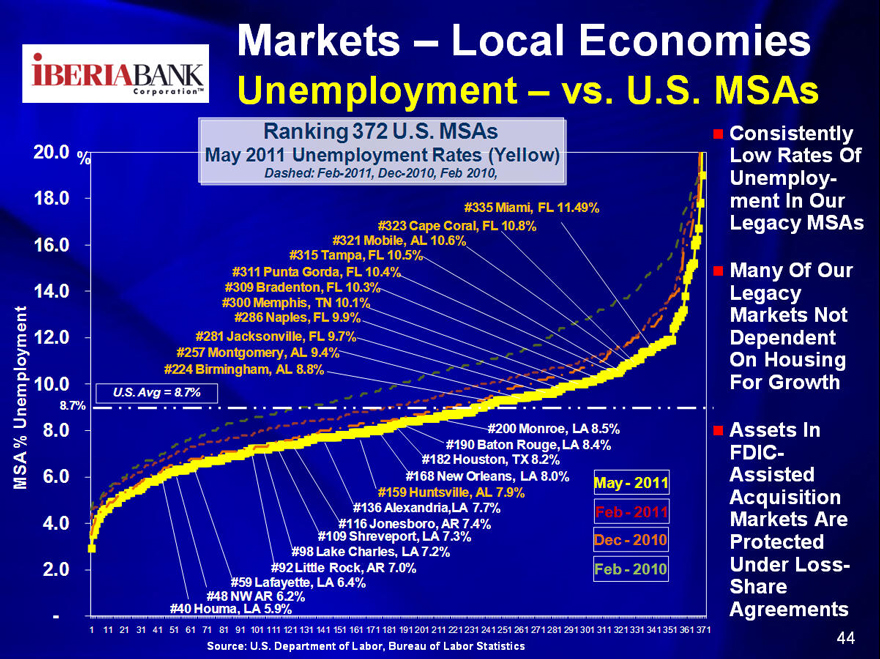

CorporationTM

Markets – Local Economies

Unemployment – vs. U.S. MSAs

Ranking 372 U.S. MSAs May 2011 Unemployment Rates (Yellow)

Dashed: Feb-2011, Dec-2010, Feb 2010,

#335 Miami, FL 11.49% #323 Cape Coral, FL 10.8% #321 Mobile, AL 10.6% #315 Tampa, FL 10.5% #311 Punta Gorda, FL 10.4% #309 Bradenton, FL 10.3% #300 Memphis, TN 10.1% #286 Naples, FL 9.9% #281 Jacksonville, FL 9.7% #257 Montgomery, AL 9.4% #224 Birmingham, AL 8.8%

U.S. Avg = 8.7%

#200 Monroe, LA 8.5% #190 Baton Rouge, LA 8.4% #182 Houston, TX 8.2% #168 New Orleans, LA 8.0% May—2011 #159 Huntsville, AL 7.9% #136 Alexandria,LA 7.7% Feb—2011 #116 Jonesboro, AR 7.4% #109 Shreveport, LA 7.3% Dec—2010 #98 Lake Charles, LA 7.2% #92 Little Rock, AR 7.0% Feb—2010 #59 Lafayette, LA 6.4% #48 NW AR 6.2% #40 Houma, LA 5.9%

Consistently Low Rates Of Unemployment In Our Legacy MSAs

Many Of Our Legacy Markets Not Dependent On Housing For Growth

Assets In FDIC-Assisted Acquisition Markets Are Protected Under Loss-Share Agreements

20.0 18.0 16.0

14.0 12.0 10.0 Unemployment 8.7

% 8.0 MS A%6.0 4.0

2.0

-

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201 211 221 231 241 251 261 271 281 291 301 311 321 331 341 351 361 371

Source: U.S. Department of Labor, Bureau of Labor Statistics

44

IBERIABANK

CorporationTM

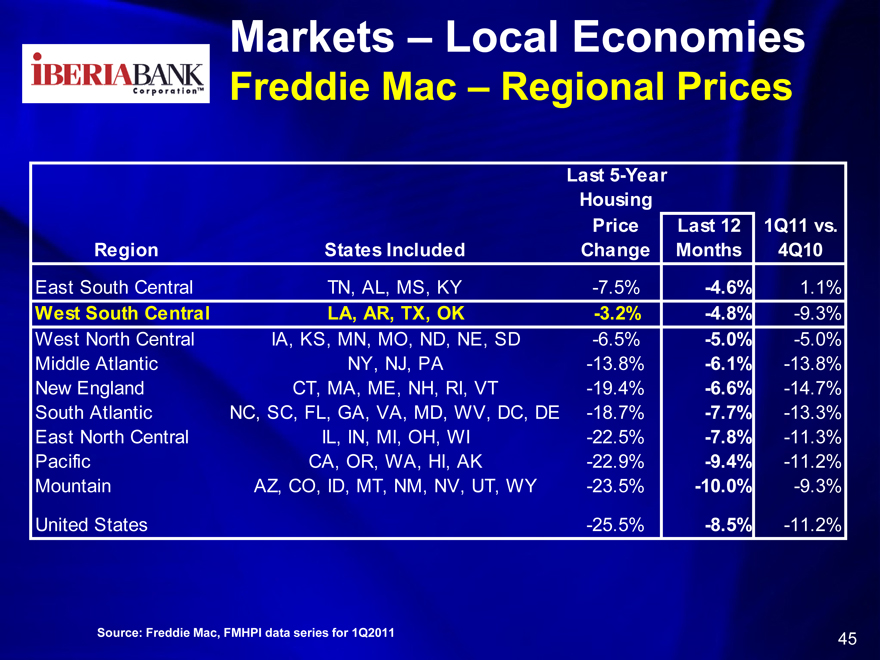

Markets – Local Economies

Freddie Mac – Regional Prices

Last 5-Year Housing

Price Last 12 1Q11 vs. Region States Included Change Months 4Q10

East South Central TN, AL, MS, KY -7.5% -4.6% 1.1%

West South Central LA, AR, TX, OK -3.2% -4.8% -9.3% West North Central IA, KS, MN, MO, ND, NE, SD -6.5% -5.0% -5.0% Middle Atlantic NY, NJ, PA -13.8% -6.1% -13.8% New England CT, MA, ME, NH, RI, VT -19.4% -6.6% -14.7% South Atlantic NC, SC, FL, GA, VA, MD, WV, DC, DE -18.7% -7.7% -13.3% East North Central IL, IN, MI, OH, WI -22.5% -7.8% -11.3% Pacific CA, OR, WA, HI, AK -22.9% -9.4% -11.2% Mountain AZ, CO, ID, MT, NM, NV, UT, WY -23.5% -10.0% -9.3%

United States -25.5% -8.5% -11.2%

Source: Freddie Mac, FMHPI data series for 1Q2011

45

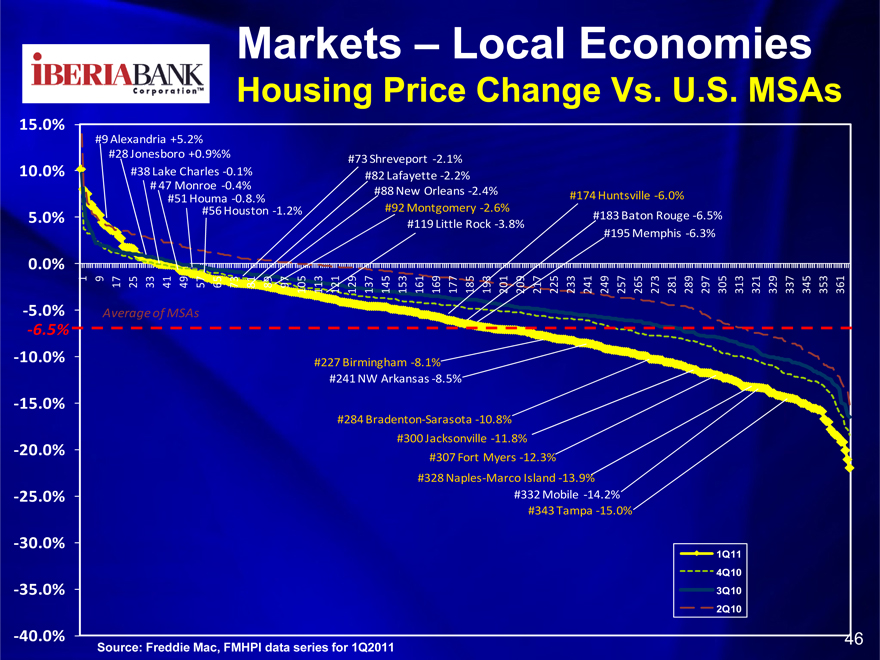

Markets – Local Economies

Housing Price Change Vs. U.S. MSAs

15.0% 10.0% 5.0% 0.0%

- 5.0%

- 6.5%

- 10.0% - 15.0% - 20.0% - 25.0% - 30.0% - 35.0% - 40.0%

#9 Alexandria +5.2% #28 Jonesboro +0.9%% #38 Lake Charles -0 .1%

# 47 Monroe - 0.4% #51 Houma 0- .8.% #56 Houston 1- .2%

#73 Shreveport -2 .1% #82 Lafayette -2 .2% #88 New Orleans -2 .4% #92 Montgomery -2 .6% #119 Little Rock -3 .8%

#174 Huntsville -6 .0% #183 Baton Rouge -6 .5% #195 Memphis -6 .3%

9 17 25 33 41 49 57 65 73 81 89 97 105 113 121 129 137 145 153 161

169

177

185

193

201

209

217

225 233

241 249 257 265 273 281 289 297 305

313

321

329

337

345

353 361

Averageof MSAs

#227 Birmingham -8 .1% #241 NW Arkansas -8 .5%

#284 Bradenton- Sarasota -10 .8% #300 Jacksonville -11 .8% #307 Fort Myers -12 .3% #328 Naples- Marco Island -13 .9% #332 Mobile -14 .2% #343 Tampa -15 .0%

1Q11 4Q10 3Q10 2Q10

Source: Freddie Mac, FMHPI data series for 1Q2011

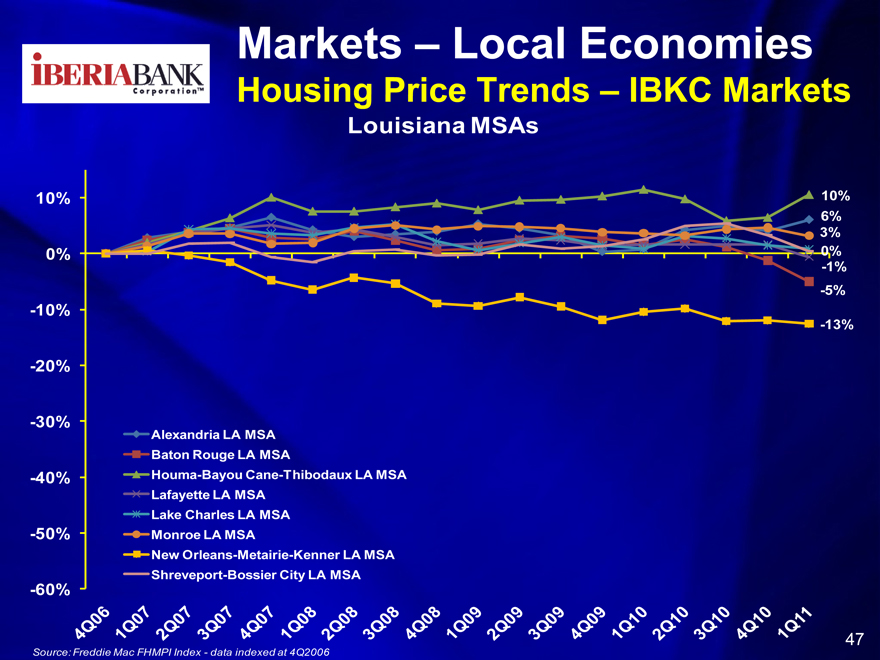

Markets – Local Economies

Housing Price Trends – IBKC Markets

Louisiana MSAs

10% 10%

6% 3%

0% 0%

-1% -5%

-10%

-13%

-20%

-30% Alexandria LA MSA Baton Rouge LA MSA

-40% Houma-Bayou Cane-Thibodaux LA MSA Lafayette LA MSA

Lake Charles LA MSA -50% Monroe LA MSA

New Orleans-Metairie-Kenner LA MSA Shreveport-Bossier City LA MSA

-60%

Source: Freddie Mac FHMPI Index—data indexed at 4Q2006

47

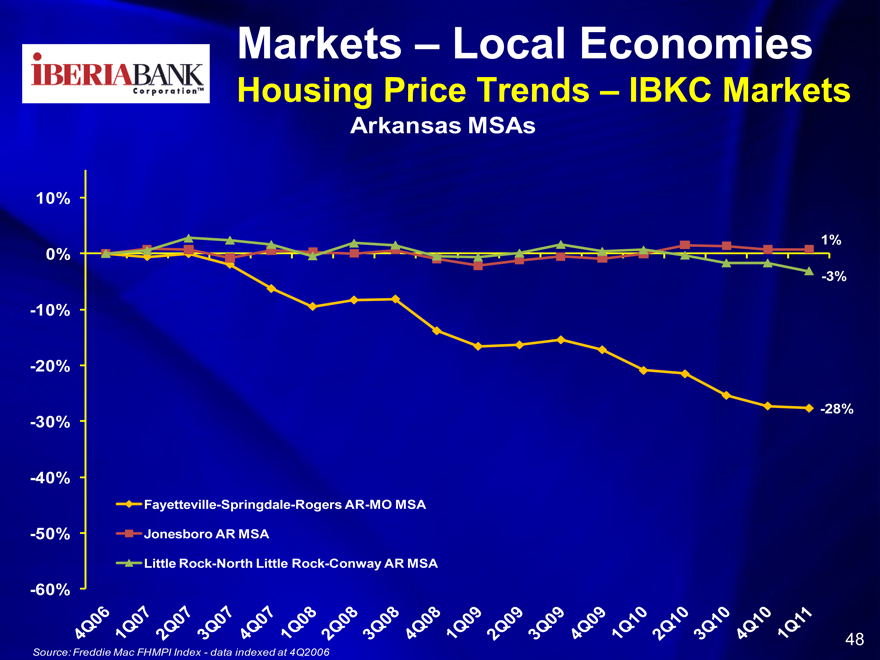

Markets – Local Economies

Housing Price Trends – IBKC Markets

Arkansas MSAs

10%

1%

0%

-3%

-10%

-20%

-30% -28%

-40%

Fayetteville-Springdale-Rogers AR-MO MSA

-50% Jonesboro AR MSA

Little Rock-North Little Rock-Conway AR MSA

-60%

Source: Freddie Mac FHMPI Index-data indexed at 4Q2006

48

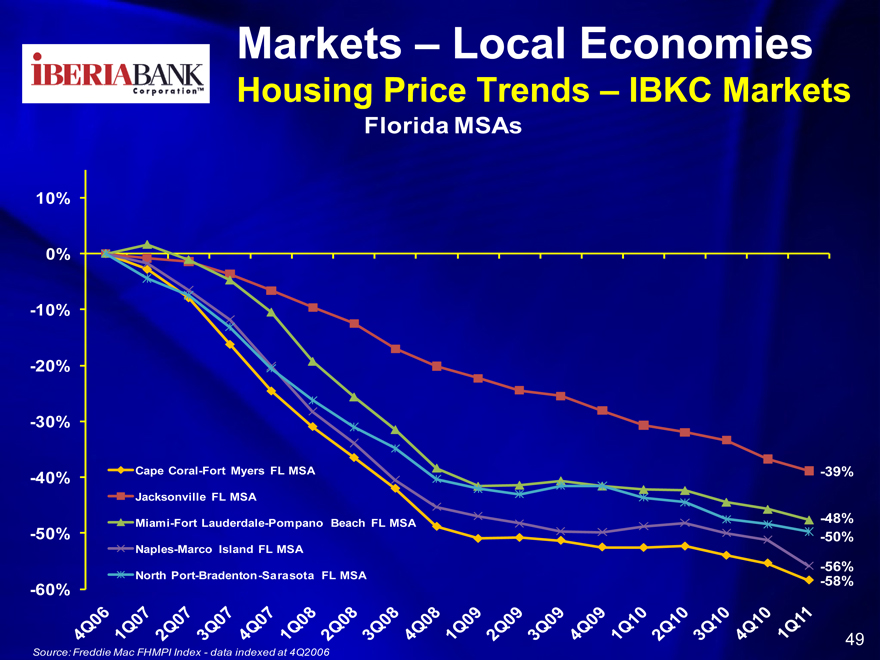

Markets – Local Economies

Housing Price Trends – IBKC Markets

Florida MSAs

10% 0% -10% -20% -30%

-40% Cape Coral-Fort Myers FL MSA -39% Jacksonville FL MSA

Miami-Fort Lauderdale-Pompano Beach FL MSA -48%

-50% -50%

Naples-Marco Island FL MSA

-56%

North Port-Bradenton-Sarasota FL MSA -58%

-60%

4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11

Source: Freddie Mac FHMPI Index-data indexed at 4Q2006

49

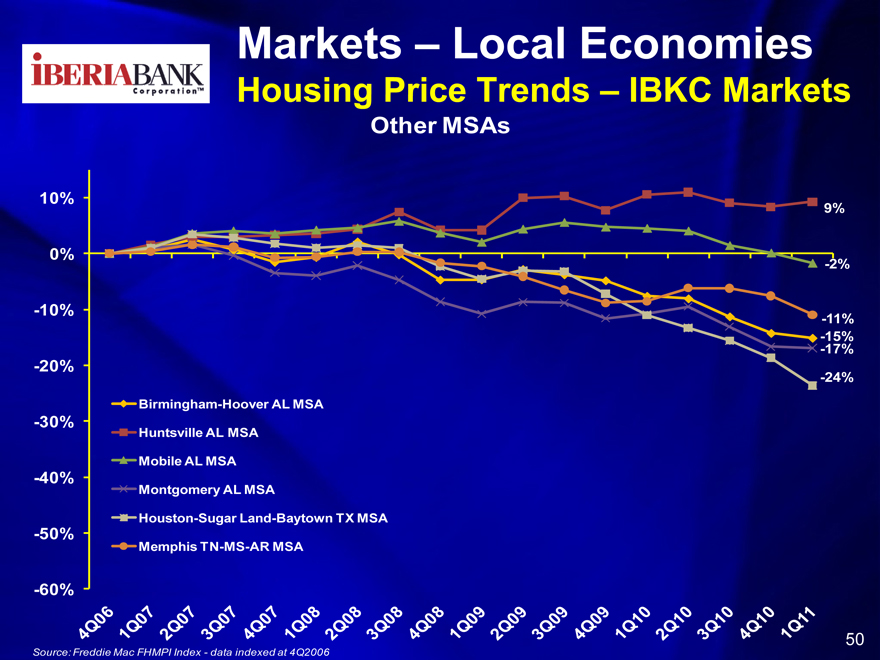

Markets – Local Economies

Housing Price Trends – IBKC Markets

Other MSAs

10%

9%

0%

-2%

-10%

-11%-17%-15%

-20%

-24% Birmingham-Hoover AL MSA

-30%

Huntsville AL MSA

Mobile AL MSA

-40%

Montgomery AL MSA

Houston-Sugar Land-Baytown TX MSA -50% Memphis TN-MS-AR MSA

-60%

4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09

2Q09 3Q09

4Q09

1Q092Q10 3Q10 4Q10 1Q11

Source: Freddie Mac FHMPI Index-data indexed at 4Q2006

50

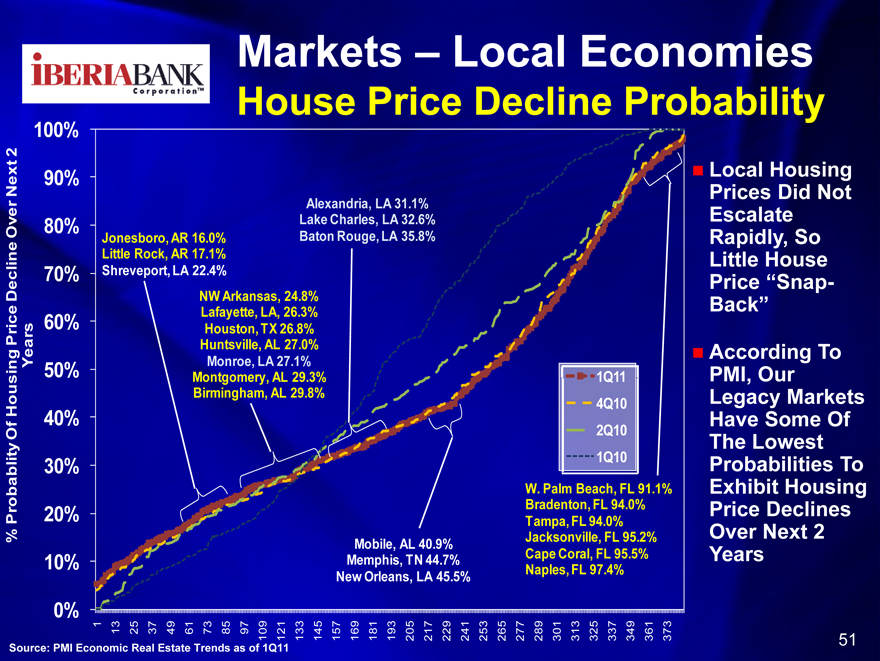

Markets – Local Economies

House Price Decline Probability

100%

2

Local Housing

ext 90%

N Prices Did Not

Alexandria, LA 31.1%

Lake Charles, LA 32.6% Escalate Over 80% Jonesboro, AR 16.0% Baton Rouge, LA 35.8% Rapidly, So Little Rock, AR 17.1% Little House cline 70% Shreveport, LA 22.4%

Price “Snap-

De NW Arkansas, 24.8%

Back”

60% Lafayette, LA, 26.3% Price Houston, TX 26.8%

Huntsville, AL 27.0% According To ing Years 50% Monroe, LA 27.1% Montgomery, AL 29.3% 1Q11 PMI, Our Birmingham, AL 29.8% Legacy Markets Hous 4Q10

Of 40% 2Q10 Have Some Of The Lowest lity 30% 1Q10 Probabilities To

W. Palm Beach, FL 91.1% Exhibit Housing Probab 20% Bradenton, FL 94.0% Price Declines Tampa, FL 94.0%

Over Next 2

% Jacksonville, FL 95.2% Mobile, AL 40.9%

10% Memphis, TN 44.7% Cape Coral, FL 95.5% Years Naples, FL 97.4% New Orleans, LA 45.5%

0% 1 13 25 37 49 61 73 85 97 109 121 133 145 157 169 181 193 205 217 229 241 253 265 277 289 301 313 325 337 349 361 373 51

Source: PMI Economic Real Estate Trends as of 1Q11

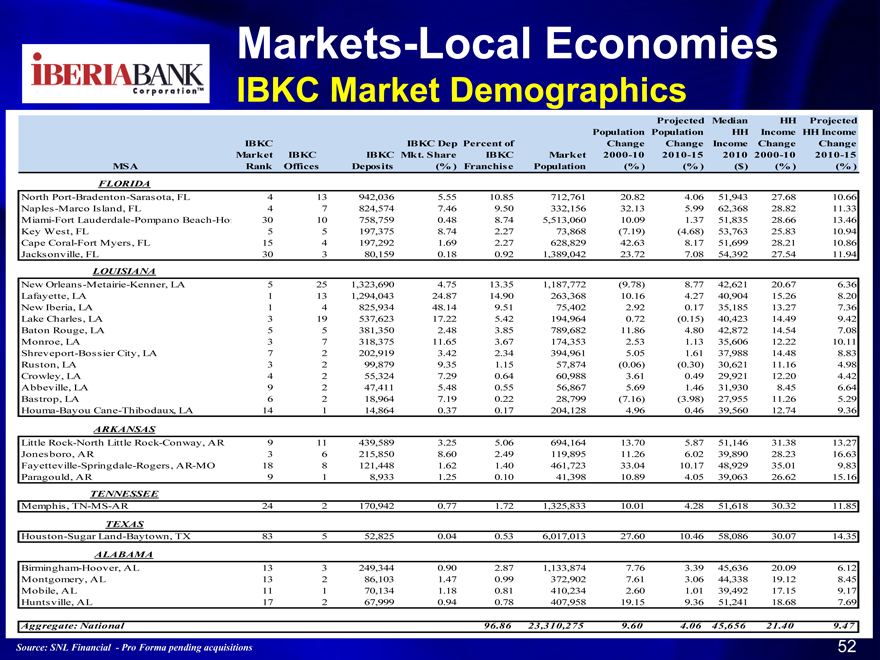

Markets-Local Economies

IBKC Market Demographics

Projected Median

HH Projected

Population Population HH Income HH Income

IBKC IBKC Dep Percent of Change Change Income Change Change Market IBKC IBKC Mkt. Share

IBKC Market 2000-10 2010-15 2010 2000-10

2010-15 MSA Rank Offices Deposits (% ) Franchise Population (% ) (% ) ($) (% ) (% )

FLORIDA North Port-Bradenton-Sarasota, FL 4 13 942,036

5.55 10.85 712,761 20.82 4.06 51,943

27.68 10.66 Naples-Marco Island, FL 4 7

824,574 7.46 9.50 332,156 32.13 5.99 62,368 28.82 11.33

Miami-Fort Lauderdale-Pompano Beach-Ho:

30 10

758,759 0.48

8.74 5,513,060

10.09 1.37

51,835 28.66

13.46 Key West, FL

5 5

197,375

8.74 2.27 73,868 (7.19) (4.68)

53,763 25.83

10.94

Cape Coral-Fort Myers, FL

15 4

197,292 1.69

2.27 628,829

42.63 8.17 51,699 28.21 10.86

Jacksonville, FL 30

3

80,159 0.18 0.92 1,389,042 23.72 7.08

54,392 27.54 11.94

LOUISIANA

New Orleans-Metairie-Kenner, LA

5 25

1,323,690 4.75

13.35 1,187,772 (9.78) 8.77 42,621

20.67 6.36

Lafayette, LA 1 13 1,294,043 24.87 14.90 263,368 10.16 4.27 40,904

15.26 8.20 New Iberia, LA 1 4

825,934 48.14 9.51 75,402

2.92 0.17

35,185 13.27 7.36 Lake Charles, LA 3 19 537,623 17.22 5.42 194,964 0.72 (0.15) 40,423 14.49 9.42 Baton Rouge, LA 5 5

381,350

2.48

3.85 789,682 11.86 4.80 42,872 14.54 7.08

Monroe, LA 3 7 318,375 11.65 3.67 174,353 2.53 1.13 35,606 12.22 10.11 Shreveport-Bossier City, LA 7 2

202,919

3.42

2.34

394,961

5.05

1.61

37,988

14.48

8.83

Ruston, LA

3

2

99,879

9.35

1.15

57,874

(0.06)

(0.30)

30,621

11.16

4.98

Crowley, LA 4 2 55,324 7.29 0.64 60,988 3.61 0.49 29,921 12.20 4.42 Abbeville, LA

9

2 47,411 5.48 0.55 56,867 5.69 1.46 31,930 8.45 6.64 Bastrop, LA 6

2 18,964 7.19 0.22 28,799 (7.16) (3.98) 27,955 11.26 5.29

Houma-Bayou Cane-Thibodaux, LA 14 1 14,864 0.37 0.17 204,128 4.96 0.46 39,560 12.74 9.36

ARKANSAS

Little Rock-North Little Rock-Conway, AR

9 11 439,589 3.25 5.06 694,164 13.70 5.87 51,146 31.38 13.27 Jonesboro, AR 3 6 215,850

8.60 2.49 119,895 11.26 6.02 39,890 28.23 16.63 Fayetteville-Springdale-Rogers, AR-MO 18 8 121,448 1.62

1.40 461,723 33.04 10.17 48,929 35.01 9.83 Paragould, AR 9 1 8,933 1.25 0.10 41,398 10.89 4.05 39,063 26.62 15.16 TENNESSEE

Memphis, TN-MS-AR

24 2 170,942 0.77 1.72 1,325,833 10.01 4.28 51,618 30.32 11.85 TEXAS Houston-Sugar Land-Baytown, TX 83

5 52,825 0.04 0.53 6,017,013 27.60 10.46

58,086

30.07

14.35

ALABAMA

Birmingham-Hoover, AL

13

3

249,344

0.90

2.87

1,133,874

7.76

3.39

45,636

20.09

6.12

Montgomery, AL

13

2

86,103

1.47

0.99

372,902

7.61

3.06

44,338

19.12

8.45

Mobile, AL

11

1

70,134

1.18

0.81

410,234

2.60

1.01

39,492

17.15

9.17

Huntsville, AL

17

2

67,999

0.94

0.78

407,958

19.15

9.36

51,241

18.68

7.69

Aggregate: National

96.86

23,310,275

9.60

4.06

45,656

21.40

9.47

Source: SNL Financial —Pro Forma pending acquisitions

Markets – Local Economies

IBKC Office Optimization

1999 Through 2005 Since 2005

Entered 3 New Markets Entered 27 New Markets

Acquired 12 Offices (All) Acquired 180 Offices (All)

Closed/Consolidated 18 Closed/Consolidated 52 Offices (All Types) Offices (All Types)

Opened 10 New Bank Opened 22 New Bank Offices Offices

Opened 7 Mortgage Opened 26 Mortgage Offices Offices

Divested/Sold 1 Office Opened 2 Title Office

5 Office Realignments 13 Office Realignments

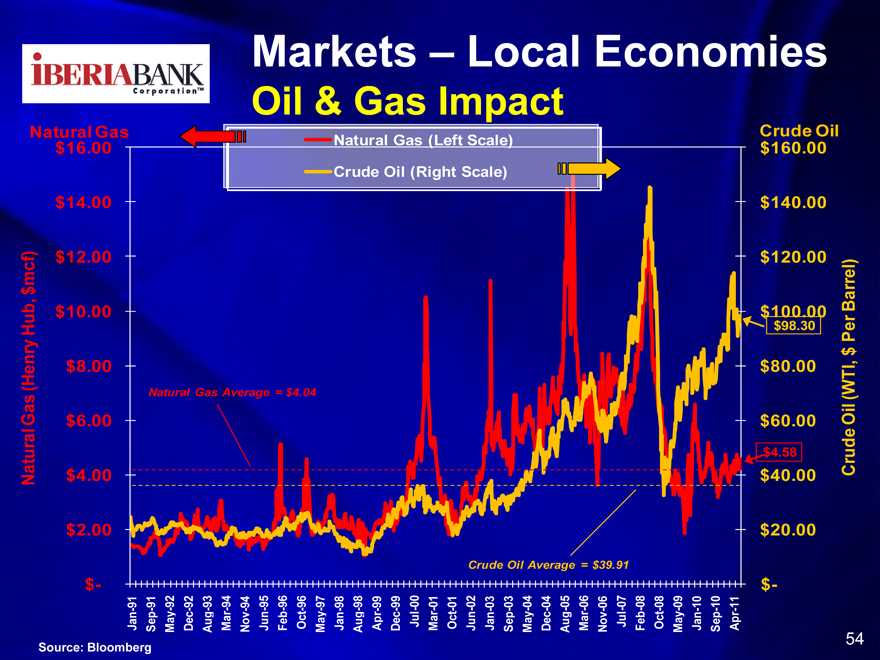

Markets – Local Economies

Oil & Gas Impact

Natural Gas Crude Oil

$16.00 Natural Gas (Left Scale) $160.00 Crude Oil (Right Scale)

$14.00 $140.00

cf) $12.00 $120.00 el) $ m Barr

$10.00 $100.00

Hub, $98.30

Per $ enry $8.00 $80.00 I,

(H Natural Gas Average = $4.04 (WT

Gas Oil

$6.00 $60.00 tural $4.58 rude Na $4.00 $40.00 C

$2.00 $20.00

Crude Oil Average = $39.91

$- $-

Jan-91 Sep -91 May -92 Dec-92 Aug-93 Mar-94 Nov-94 Jun-95 Feb-96 Oct-96 May -97 Jan-98 Aug-98 Apr -99 Dec-99 Jul-00 Mar-01 Oct-01 Jun-02 Jan-03 Sep -03 May -04 Dec-04 Aug-05 Mar-06 Nov-06 Jul-07 Feb-08 Oct-08 May -09 Jan-10 Sep -10 Apr -11

Source: Bloomberg 54

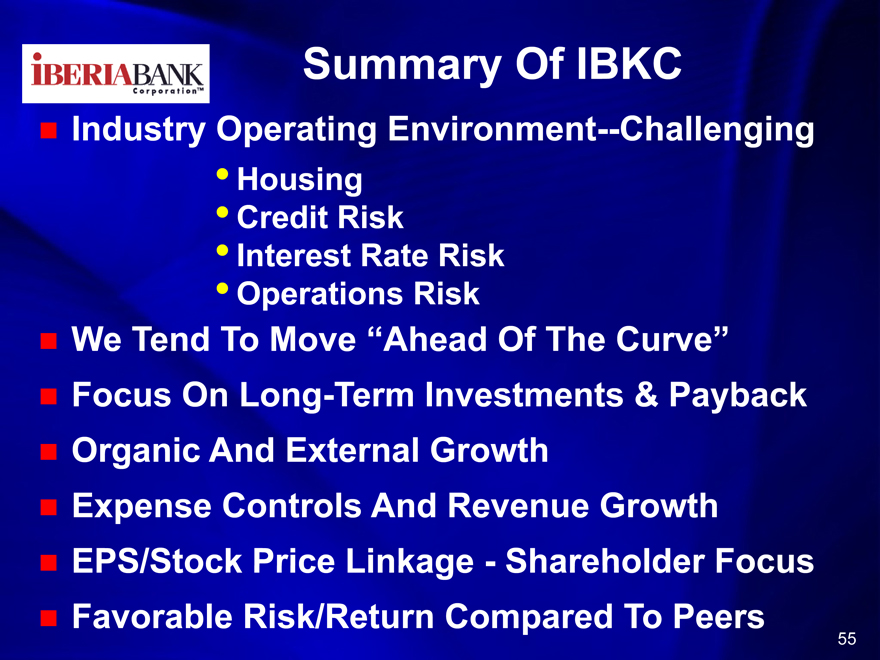

Summary Of IBKC

Industry Operating Environment—Challenging

•Housing

•Credit Risk

•Interest Rate Risk

•Operations Risk

We Tend To Move “Ahead Of The Curve”

Focus On Long-Term Investments & Payback

Organic And External Growth

Expense Controls And Revenue Growth

EPS/Stock Price Linkage—Shareholder Focus

Favorable Risk/Return Compared To Peers