Exhibit 99.2 Loss Share and Covered Assets Update April 15, 2013 |

2 Safe Harbor Language Safe Harbor Language To the extent that statements in this presentation and the accompanying press release relate to future plans, objectives, financial results or performance of IBERIABANK Corporation, these statements are deemed to be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements, which are based on management’s current information, estimates and assumptions and the current economic environment, are generally identified by the use of the words “plan", “believe”, “expect”, “intend”, “anticipate”, “estimate”, “project” or similar expressions. IBERIABANK Corporation’s actual strategies and results in future periods may differ materially from those currently expected due to various risks and uncertainties. Actual results could differ materially because of factors such as the level of market volatility, our ability to execute our growth strategy, including the availability of future FDIC-assisted failed bank opportunities, unanticipated losses related to the integration of, and refinements to purchase accounting adjustments for, acquired businesses and assets and assumed liabilities in these transactions, adjustments of fair values of acquired assets and assumed liabilities and of deferred taxes in acquisitions, actual results deviating from the Company’s current estimates and assumptions of timing and amounts of cash flows, credit risk of our customers, effects of the on-going correction in residential real estate prices and reduced levels of home sales, sufficiency of our allowance for loan losses, changes in interest rates, access to funding sources, reliance on the services of executive management, competition for loans, deposits and investment dollars, reputational risk and social factors, changes in government regulations and legislation, increases in FDIC insurance assessments, geographic concentration of our markets and economic conditions in these markets, rapid changes in the financial services industry, dependence on our operational, technological, and organizational systems or infrastructure and those of third-party providers of those services, hurricanes and other adverse weather events, the modest trading volume of our common sock, and valuation of intangible assets. These and other factors that may cause actual results to differ materially from these forward-looking statements are discussed in the Company’s Annual Report on Form 10-K and other filings with the Securities and Exchange Commission (the “SEC”), available at the SEC’s website, http://www.sec.gov, and the Company’s website, http://www.iberiabank.com, under the heading “Investor Information.” All information in this presentation and the accompanying press release is as of the date of this release. The Company undertakes no duty to update any forward-looking statement to conform to the statement to actual results or changes in the Company’s expectations. Certain tabular presentations may not reconcile because of rounding. |

33 Accounting Standard Adoption • The adoption of ASU No. 2012-06 requires shorter amortization period over which to amortize our indemnification assets on commercial loss share agreements associated with prior FDIC- assisted acquisitions (8 years down to 5 years). • Expected to result in a reduction to net covered yield on the covered loan portfolio of approximately 200 bps for the next 7 to 8 quarters due to accelerated amortization on the indemnification assets. • Aggregate increased amortization impact over next 8 quarters is approximately $24 million on a pre tax basis. • As of March 31, 2013, credit quality relative to original estimates has improved by approximately $310 million. Introductory Comments Introductory Comments Indemnification Asset and Covered Loan Update |

4 Impairment Charge of Indemnification Assets (IA) • The timing to Resolve FDIC assets continues to extend for various reasons: • Credit Quality continues to improve and is significantly better than originally expected. Improvement in credit performance is reflected in increased accretion over the remaining life of the loans – typically longer than the loss share agreement and loss collection periods. • The ability to entertain bulk sales and note sales continues to be challenged • Probable losses starting to bridge the loss share coverage period • Judicial Court system continues to delay timely foreclosure on collateral dependent or troubled assets • Expected valuation allowance (noninterest expense) of $32 million on a pre tax basis ($0.70 per share after tax) against the IA. • Impact to Capital Ratios expected to be approximately 25 basis points. Introductory Comments Introductory Comments Indemnification Asset and Covered Loan Update 4 |

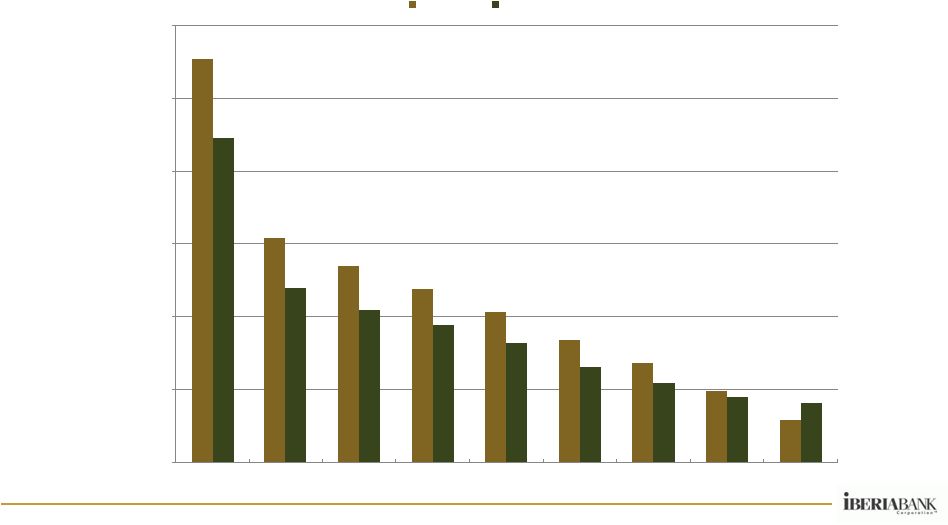

5 Financial Overview Financial Overview Expected Amortization Comparison (Dollars in thousands) $(30,000) $(25,000) $(20,000) $(15,000) $(10,000) $(5,000) $- Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Indemnification Asset Expected Amortization Post Adoption Pre Adoption |

6 Financial Overview Financial Overview Expected Future Performance Metrics (Dollars in thousands) Projected Average Loan Balances and Net Yields (%) Projected Average Balance (Left Hand Scale) Projected Net Yield (Right Hand Scale) |

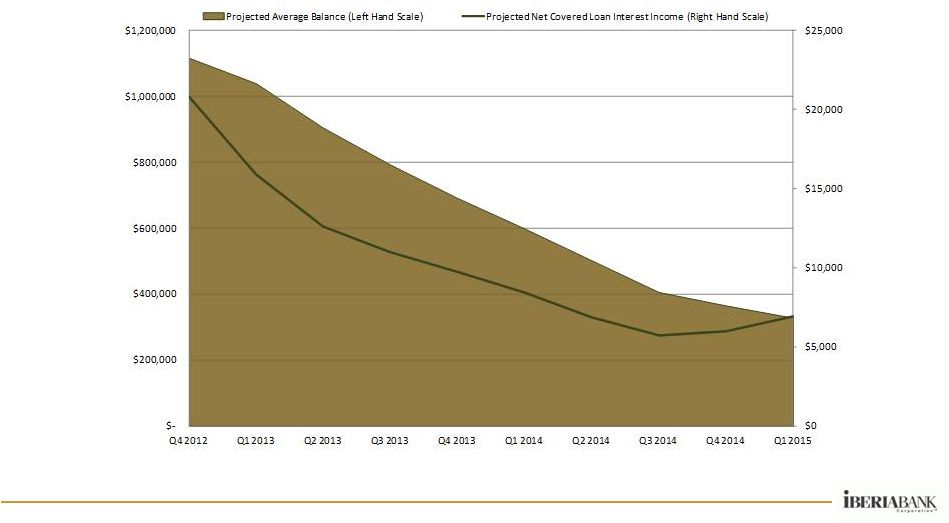

7 Financial Overview Financial Overview Expected Future Performance Metrics (Dollars in thousands) Projected Average Loan Balances and Net Yields ($) |

8 Financial Overview Financial Overview Performance Metrics – Yields |