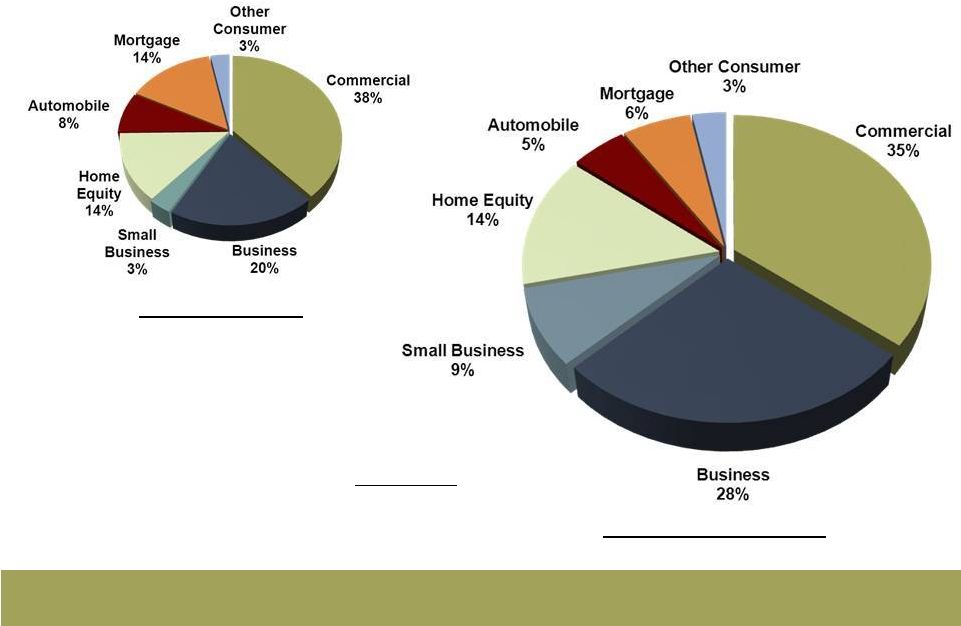

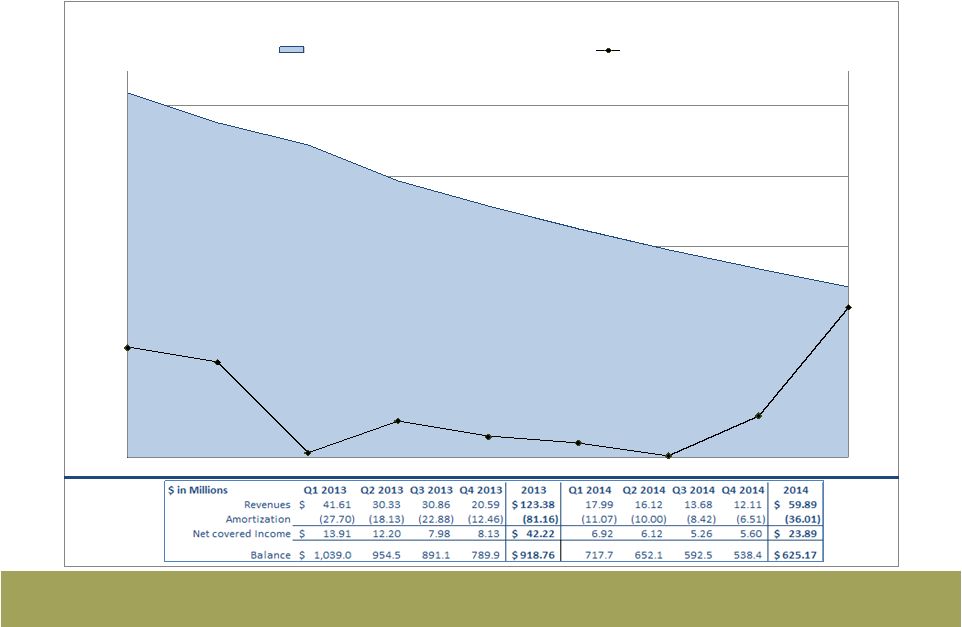

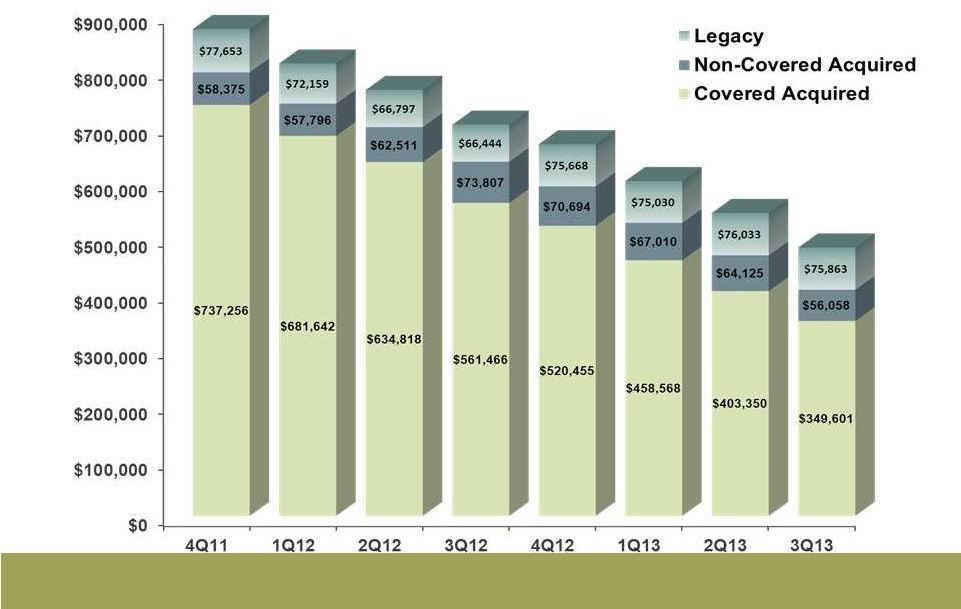

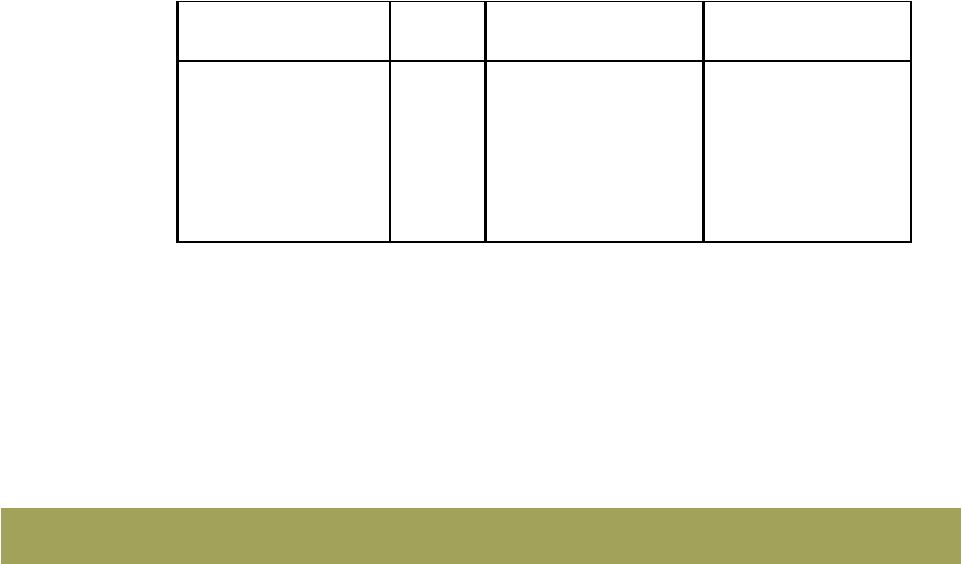

28 Appendix FDIC Covered Loan Portfolio Roll Forward Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Covered Loans 1,112,153 49,550 17.528% 1,039,469 41,607 16.047% 954,555 30,324 12.619% 871,768 30,858 13.896% Mortgage Loans 155,989 5,318 13.636% 180,902 4,398 9.724% 170,420 4,135 9.706% 163,485 2,718 6.650% Indirect Automobile (0) - 0.000% (0) - 0.000% - - 0.000% - - 0.000% Credit Card 860 14 6.664% 824 13 6.565% 789 14 7.147% 728 13 6.971% Consumer 148,001 5,308 14.267% 130,960 3,509 10.867% 126,164 2,594 8.248% 104,668 3,029 11.481% Line Of Credit-Consumer Loans 69,910 3,661 20.831% 41,802 3,200 31.044% 40,543 2,967 29.355% 50,939 (190) -1.476% Commercial & Business Banking 737,394 35,250 18.706% 684,981 30,487 17.803% 616,642 20,613 13.224% 551,950 25,288 17.928% Loans in Process (1) - 0.000% (1) - 0.000% (3) - 0.000% (2) - 0.000% Overdrafts 0 - 0.000% 0 - 0.000% 0 - 0.000% - - 0.000% FDIC Loss Share Receivable 411,328 (28,201) -26.828% 384,319 (27,702) -28.832% 268,700 (18,130) -26.692% 228,047 (22,875) -39.252% Net Covered Loan Portfolio 1,523,481 21,349 7.678% 1,423,788 13,905 5.351% 1,223,255 12,194 5.110% 1,099,815 7,983 3.663% Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Average Income / Expense Average Yield Covered Loans 1,112,153 49,550 17.528% 1,039,469 41,607 16.047% 954,555 30,324 12.619% 871,768 31,931 13.896% CapitalSouth Bank 150,872 6,737 17.537% 138,793 4,109 11.855% 131,981 3,610 10.852% 123,412 2,840 10.332% Orion Bank 641,252 29,720 18.235% 597,706 25,287 16.960% 548,977 17,685 12.789% 504,934 20,929 13.924% Century Bank 232,967 7,137 12.108% 219,726 6,401 11.703% 199,836 4,943 9.869% 175,247 5,790 15.184% Sterling Bank 87,063 5,956 26.806% 83,245 5,810 27.941% 73,762 4,087 21.956% 68,174 2,372 16.831% FDIC Loss Share Receivable 411,328 (28,201) -26.828% 384,319 (27,702) -28.832% 268,700 (18,130) -26.692% 228,047 (22,875) -39.252% CapitalSouth Bank 35,811 (3,431) -37.492% 29,301 (2,388) -32.596% 18,955 (2,347) -48.987% 14,720 (2,538) -67.473% Orion Bank 251,749 (17,944) -27.892% 235,594 (17,330) -29.423% 164,219 (10,492) -25.277% 141,213 (12,702) -35.199% Century Bank 92,076 (3,200) -13.601% 90,384 (4,100) -18.146% 65,145 (3,105) -18.857% 55,021 (5,304) -37.719% Sterling Bank 31,691 (3,625) -44.761% 29,040 (3,884) -53.502% 20,382 (2,185) -42.404% 17,093 (2,331) -53.365% Net Covered Loan Portfolio 1,112,153 21,349 7.678% 1,039,469 13,905 5.351% 954,555 12,194 5.110% 871,768 9,056 3.663% CapitalSouth Bank 150,872 3,305 8.764% 138,793 1,721 4.961% 131,981 1,262 3.826% 123,412 301 2.301% Orion Bank 641,252 11,776 7.345% 597,706 7,958 5.326% 548,977 7,192 5.240% 504,934 8,227 4.145% Century Bank 232,967 3,937 6.760% 219,726 2,301 4.188% 199,836 1,837 3.678% 175,247 486 3.304% Sterling Bank 87,063 2,331 10.709% 83,245 1,925 9.252% 73,762 1,903 10.317% 68,174 41 3.480% 4Q2012 1Q2013 2Q2013 4Q2012 1Q2013 2Q2013 3Q2013 3Q2013 |