Acquisition of First Private Acquisition of First Private Holdings, Inc. Holdings, Inc. February 11, 2014 February 11, 2014 Exhibit 99.2 |

Safe Harbor Language 2 Statements contained in this presentation which are not historical facts and which pertain to future operating results of IBERIABANK Corporation and its subsidiaries constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve significant risks and uncertainties. Actual results may differ materially from the results discussed in these forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in IBERIABANK Corporation’s periodic filings with the SEC. In connection with the proposed merger, IBERIABANK Corporation will file a Registration Statement on Form S-4 that will contain a proxy statement / prospectus. INVESTORS AND SECURITY HOLDERS ARE URGED TO CAREFULLY READ THE PROXY STATEMENT / PROSPECTUS REGARDING THE PROPOSED TRANSACTION WHEN IT BECOMES AVAILABLE, BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain a free copy of the proxy statement / prospectus (when it is available) and other documents containing information about IBERIABANK Corporation and First Private Holdings, Inc., without charge, at the SEC’s website at http://www.sec.gov. Copies of the proxy statement / prospectus and the SEC filings that will be incorporated by reference in the proxy statement / prospectus may also be obtained for free from the IBERIABANK Corporation website, www.iberiabank.com, under the heading “Investor Information”. This communication is not a solicitation of any vote or approval, is not an offer to purchase shares of First Private Holdings, Inc. common stock, nor is it an offer to sell shares of IBERIABANK Corporation common stock which may be issued in any proposed merger with First Private Holdings, Inc. The issuance of IBERIABANK Corporation common stock in any proposed merger with First Private Holdings, Inc. would have to be registered under the Securities Act of 1933, as amended, and such IBERIABANK Corporation common stock would be offered only by means of a prospectus complying with the Act. |

3 3 3 3 3 3 Transaction Rationale • New banking market acquisition of Dallas, Texas based private bank • Established and complementary customer profile • Two branch offices located in the Dallas Metro market • Private Banking focus with $318 million in deposits and $257 million in gross loans • Adds approximately $357 million in assets • Limited cost savings, but significant revenue and client growth potential • C&I lending, wealth management, and mortgage lending opportunities • Slightly dilutive to 2015 earnings per share; accretive in 2016 and beyond • Slightly accretive to tangible book value excluding one-time acquisition and conversion related costs on a pro forma basis at December 31, 2013 • Transaction has limited impact on capital ratios • Anticipate internal rate of return in excess of 20% • Favorable pricing for attractive, high quality Texas franchise • Comprehensive due diligence completed, including credit review • Strong credit culture and excellent asset quality • Historically, no credit issues, no non-performing assets or charge-offs • Limited loss content in loan portfolio projected (1.5% of gross loans) • Conversion and integration experience reduces integration risk Compelling Strategic Rationale Financially Attractive Low Risk |

4 4 4 4 4 4 Transaction Overview • Tax-free, stock-for-stock exchange • Fixed exchange ratio of 0.27 shares of IBKC common stock for each First Private Holdings, Inc. share within price collars and floating exchange ratios outside collars (1) • $64 million (2) for common stock outstanding based on IBKC closing price of $63.62 on February 10, 2014 • $17.18 per First Private Holdings, Inc. share outstanding (2) • Price / Total Book (2) : 164% • Price / Tangible Book (2) : 164% • Completed comprehensive due diligence • First Private Holdings, Inc. shareholder approval • Customary regulatory approvals • Expected closing in second quarter of 2014 (1) The agreement provides for a fixed exchange ratio with pricing collars that fix the value received by First Private Holdings, Inc., shareholders if the weighted average trading price of IBERIABANK common stock were to decline below $62.96 per share, or exceed $69.44 per share, over a specified period (2) Assumes exercise of vested options and warrants Consideration Deal Value Valuation Multiples Due Diligence Required Approvals Timing |

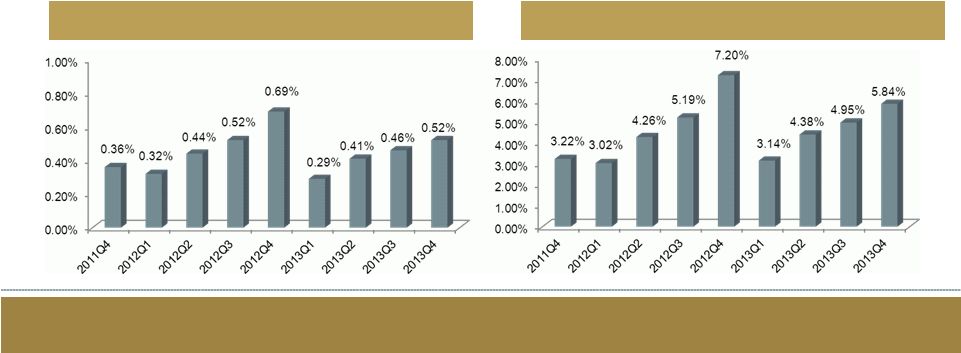

5 5 5 5 5 5 First Private Holdings, Inc. Source: SNL Financial Data as of 12/31/13 • Headquartered in Dallas, TX • First Private Bank was founded in 2007 • Operates as a Private Bank focusing on personal, high-touch and individualized services • In addition, the Bank offers investment, wealth management, financial planning, tax and risk management services for clientele • Total Gross Loans: $257 million • Total Assets: $357 million • Total Deposits: $318 million • Total Equity: $33 million common equity • No intangibles Overview Financial Highlights At December 31, 2013 ROAA (%) ROATE (%) |

6 6 6 6 6 6 Enhances Our Texas Franchise Deposit Market Share Source: SNL Financial, June 30, 2013 Rank Institution Branches Deposits ($ mm) Market Share % 1 Bank of America Corp. 155 53,193,319 28.64 2 JPMorgan Chase & Co. 258 41,795,744 22.50 3 Wells Fargo & Co. 197 16,451,121 8.86 4 BBVA 103 7,901,079 4.25 5 Texas Capital Bancshares Inc. 7 5,597,302 3.01 6 Comerica Inc. 54 4,971,684 2.68 7 Cullen/Frost Bankers Inc. 32 4,695,270 2.53 8 ViewPoint Financial Group Inc 51 3,627,771 1.95 9 BOK Financial Corp. 29 3,289,074 1.77 10 Hilltop Holdings Inc. 14 2,728,313 1.47 50 First Private Holdings Inc. 2 305,169 0.16 Total For Institutions In Market 1,748 185,739,319 Dallas-Fort Worth-Arlington, TX - MSA Rank Institution Branches Deposits ($ mm) Market Share % 1 JPMorgan Chase & Co. 677 125,917,659 22.52 2 Bank of America Corp. 432 81,600,495 14.59 3 Wells Fargo & Co. 690 60,385,882 10.80 4 BBVA 357 30,267,506 5.41 5 Cullen/Frost Bankers Inc. 129 20,362,980 3.64 6 Prosperity Bancshares Inc. 266 13,981,896 2.50 7 Capital One Financial Corp. 178 10,409,789 1.86 8 Zions Bancorp. 87 10,358,246 1.85 9 Comerica Inc. 138 9,870,437 1.77 10 Texas Capital Bancshares Inc. 13 7,720,950 1.38 11 Hilltop Holdings Inc. 84 6,925,219 1.24 12 International Bancshares Corp. 171 6,767,147 1.21 13 BOK Financial Corp. 46 4,988,023 0.89 14 First Financial Bankshares 64 3,965,897 0.71 15 ViewPoint Financial Group Inc 52 3,725,283 0.67 16 Regions Financial Corp. 84 3,717,756 0.66 17 Citigroup Inc. 78 3,340,711 0.60 18 Woodforest Financial Grp Inc. 207 3,021,936 0.54 19 Amarillo National Bancorp Inc. 17 2,924,142 0.52 20 BB&T Corp. 81 2,774,152 0.50 21 Independent Bk Group Inc. 37 2,534,545 0.45 22 Southside Bancshares Inc. 40 2,502,007 0.45 23 Broadway Bancshares Inc. 40 2,439,266 0.44 24 Industry Bancshares Inc. 20 2,178,055 0.39 25 CBFH Inc. 35 2,055,834 0.37 46 Pro Forma IBKC 8 1,036,520 0.19 70 IBERIABANK Corporation 6 731,351 0.13 158 First Private Holdings Inc. 2 305,169 0.05 Total For Institutions In Market 6,873 559,153,428 State Of Texas |

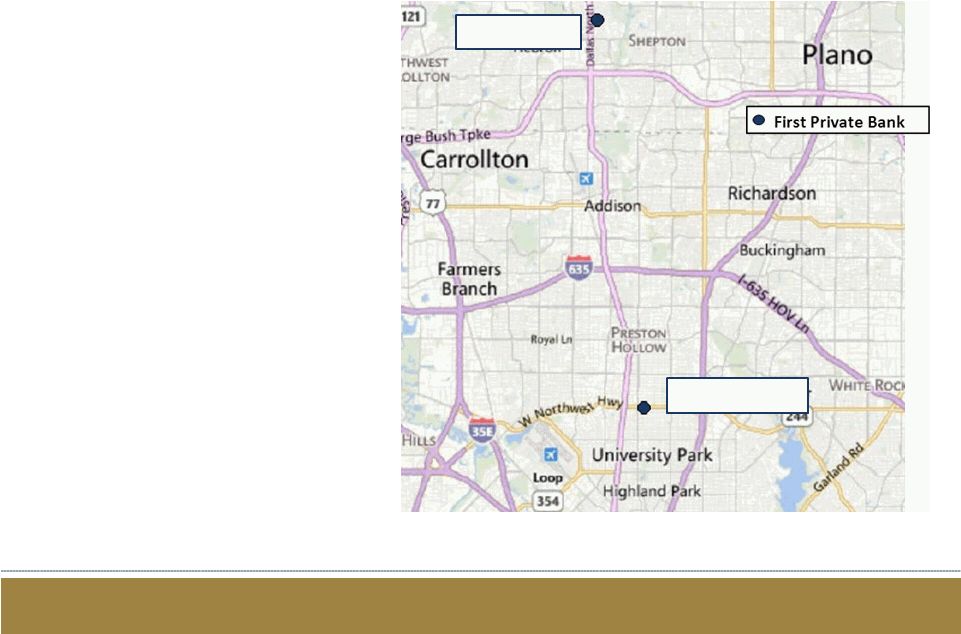

7 7 7 7 7 7 Enhances Our Texas Franchise Source: SNL Financial, June 30, 2013 2500 Dallas Parkway Dallas, $42.7 million 8201 Preston Rd. Dallas, TX $262.5 million • Two full service offices in Dallas, TX market • One office in University Park area • One office in West Plano • 34 FTE employees • Over 3,500 active deposit accounts • Over 650 loan accounts |

8 8 8 8 8 8 Credit Summary Source: Company documents/SNL Financial Data as of December 31, 2013 Diligence Scope • Approximately 71 people involved in due diligence process; credit team included 13 associates performing both on-site file reviews • Reviewed 77% of outstanding loan balances and nearly 34% of total number of loans • Loan review resulted in no expected loss and no additional non-accruals from reviewed loans Loan Portfolio Comments • Majority are in-market loans • High quality loan portfolio with concentration in residential real-estate loans with low LTVs, first position liens and high quality clientele • Stellar asset quality metrics: • NPA / assets = 0.0% • Nonaccrual loans / loans = 0.0% • Allowance for loan losses of $1.2 million • Credit mark of approximately $3.7 million on a pre-tax basis for potential loan losses Loan Portfolio Composition Loan Type Balance ($ millions) % of Total 1-4 Family Residential $147.0 57.4% C&D 38.5 15.0% Commercial & Industrial 24.4 9.5% CRE - Non Owner Occupied 15.0 5.9% Consumer & Other 12.8 5.0% CRE - Owner Occupied 2.2 0.8% Multi family 0.1 0.1% All Other Loans 16.3 6.4% Total Loans $256.3 100.0% |

9 9 9 9 9 9 Costs and Synergies Merger Considerations • No corporate or bank board seats • First Private board members invited to form the nucleus of IBKC’s Dallas Advisory Board • Approximately $0.5 million in pre-tax expense savings • Savings equate to approximately 7% of total First Private expenses • Potential revenue opportunities include C&I, wealth management, and mortgage origination (IBKC’s mortgage origination team is located a few blocks from First Private’s headquarters) Approximately $5 million in pre-tax costs: • $1.3 million in banking/legal/accounting expense • $1.2 million in severance and retention payments • $0.8 million in system conversions • $0.6 million in contract terminations • $0.1 million in marketing/communications • $1.0 million in all other one-time expense Merger-Related Costs |

(1) Pro forma capital ratios include pending Teche Holding Company transaction 10 10 10 10 10 10 Financial Assumptions & Impact Conservative Financial Assumptions Attractive Financial Impact Other Marks: Cost Savings: Merger Related Costs: • Gross loss estimate of $3.7 million on a pre-tax basis (1.5% of gross loan portfolio) • Loss estimate, net of allowance, is $2.5 million on a pre-tax basis and $1.6 million in an after-tax basis • Aggregate positive $8.3 million in interest rate marks after-tax for loans, securities, CDs and FHLB advances • Annual run rate cost savings of approximately $0.5 million on a pre-tax basis • Represents approximately 7% of First Private’s fiscal year 2013 non-interest expenses • Savings expected to be achieved by first quarter of 2015 • Approximately $5 million on a pre-tax basis • Slightly dilutive to EPS in 2015; approximately 2% accretive to EPS in 2016 • Slightly accretive to tangible book value excluding one-time acquisition and conversion related costs on a pro forma basis at December 31, 2013, approximately 0.1% • Strong pro forma capital ratios (1) : • Tangible common equity ratio = 8.9% • Total risk based capital ratio = 12.9% • Internal rate of return greater than 20%; well in excess of our cost of capital Credit Mark: |

11 11 11 11 11 11 Branch Locations Source: Company documents Deposits as of 6/30/2013 8201 Preston Road, DallasTX Deposits - $262 million 2500 Dallas Parkway, Dallas TX Deposits: $43 million |

|