Acquisition of Georgia Commerce Bancshares, Inc. December 8, 2014 Exhibit 99.2 |

Safe Harbor And Legend 2 Statements contained in this presentation which are not historical facts and which pertain to future operating results of IBERIABANK Corporation and its subsidiaries constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward- looking statements involve significant risks and uncertainties. Actual results may differ materially from the results discussed in these forward-looking statements. Factors that might cause such a difference include, but are not limited to, those discussed in IBERIABANK Corporation’s periodic filings with the SEC. In connection with the proposed merger, IBERIABANK Corporation will file a Registration Statement on Form S-4 that will contain a proxy statement / prospectus. INVESTORS AND SECURITY HOLDERS ARE URGED TO CAREFULLY READ THE PROXY STATEMENT / PROSPECTUS REGARDING THE PROPOSED TRANSACTION WHEN IT BECOMES AVAILABLE, BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain a free copy of the proxy statement / prospectus (when it is available) and other documents containing information about the pending transactions with Florida Bank Group, Inc. and Old Florida Bancshares, Inc., and the merger with Georgia Commerce Bancshares, Inc., without charge, at the SEC’s website at http://www.sec.gov. Copies of the proxy statement / prospectus and the SEC filings that will be incorporated by reference in the proxy statement / prospectus may also be obtained for free from the IBERIABANK Corporation website, www.iberiabank.com, under the heading “Investor Information”. This communication is not a solicitation of any vote or approval, is not an offer to purchase shares of Georgia Commerce Bancshares, Inc. common stock, nor is it an offer to sell shares of IBERIABANK Corporation common stock which may be issued in any proposed merger with Georgia Commerce Bancshares, Inc. The issuance of IBERIABANK Corporation common stock in any proposed merger with Georgia Commerce Bancshares, Inc. would have to be registered under the Securities Act of 1933, as amended (the “Act”), and such IBERIABANK Corporation common stock would be offered only by means of a prospectus complying with the Act. |

Compelling Strategic Rationale 3 3 3 3 3 3 Transaction Rationale • New market acquisition of an Atlanta, Georgia-based commercial bank • High quality entrance in a strong growth market • Established and complementary customer profile • Strong core deposit franchise with $826 million in low-cost deposits • Nine bank offices located in Atlanta, MSA – serving the most attractive growth sub-markets in central and northern metro Atlanta • Emphasis on small to mid-market C&I / owner-occupied CRE with $731 million in gross loans • Adds approximately $1.0 billion in total assets • Approximately 1.6% accretive to EPS in 2016 and 5% accretive in 2017 • Tangible book value dilution of approximately 1.8% at consummation • Tangible book value breakeven, including one-time acquisition and conversion related costs, in approximately three and one-half years • Transaction has neutral impact on capital ratios • Anticipate internal rate of return in excess of 20% • Comprehensive due diligence completed, including credit review • Strong credit / underwriting culture and excellent asset quality • Limited loss content expected (1.8% of gross loans on a par basis) • Conversion and integration experience reduces integration risk Financially Attractive Low Risk |

Notes: (1) The agreement provides for a fixed exchange ratio with pricing collars that fix the value received by Georgia Commerce’s shareholders if the weighted average trading price of IBERIABANK Corporation’s common stock were to decline below $58.69 per share, or exceed $71.73 per share, over a specified period. (2) Assumes common shares and full exercise of outstanding warrants. No exercise of stock options outstanding. (3) Assumes all stock options outstanding are cashed out at consummation. 4 4 4 4 4 4 Transaction Overview • Tax-free, stock-for-stock exchange • Fixed exchange ratio of 0.6134 share of IBERIABANK common stock for each Georgia Commerce Bancshares, Inc. (“Georgia Commerce") share within price collars and floating exchange ratios outside collars (1) Consideration Deal Value Valuation Multiples Required Approvals Timing • $189 million for total equity (2) outstanding based on IBERIABANK Corporation’s closing price of $65.21 on December 5, 2014 • $40.00 per Georgia Commerce common share outstanding (2) • Estimated $6 million in cash liquidation value of all options outstanding (3) • Georgia Commerce shareholder approval • Customary regulatory approvals • Expected closing in first half of 2015 Shareholders’ Aggregate Value Equity (2) Including Options (3) • 181% 186% • 196% 202% Price / Total Book: Price / Tangible Book: |

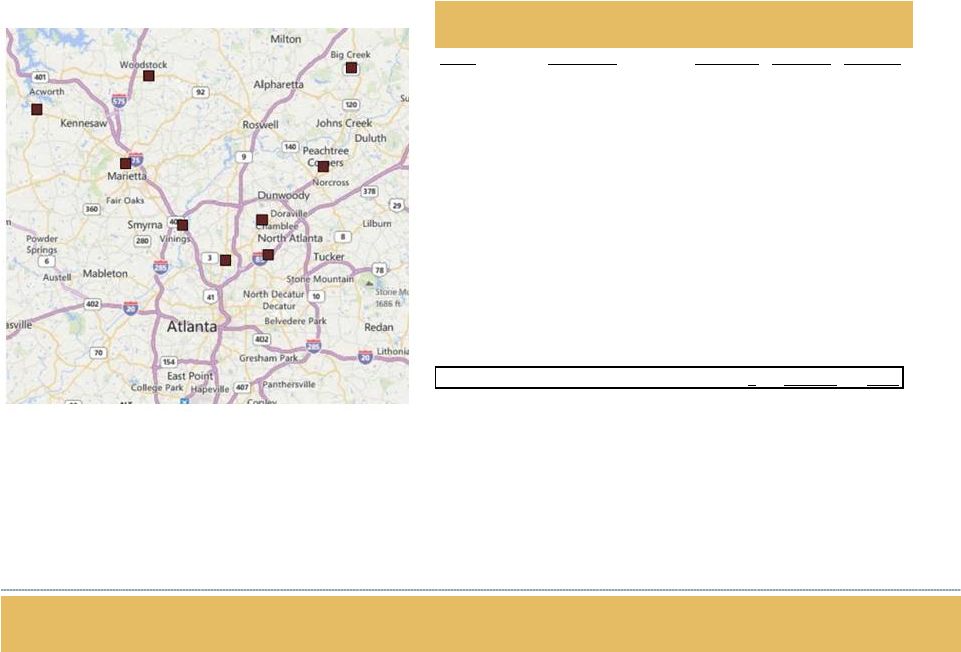

Rank Institution Branches Deposits Share % 1 SunTrust Banks Inc. 167 34,822,284 26.8% 2 Wells Fargo & Co. 196 26,377,193 20.3% 3 Bank of America Corp. 139 23,950,719 18.4% 4 BB&T Corp. 90 7,657,337 5.9% 5 Synovus Financial Corp. 43 3,982,474 3.1% 6 Regions Financial Corp. 73 3,310,360 2.6% 7 JPMorgan Chase & Co. 83 2,187,460 1.7% 8 Fidelity Southern Corp. 37 2,172,664 1.7% 9 United Community Banks Inc. 36 2,148,788 1.7% 10 Community & Southern Hldgs Inc 34 2,083,955 1.6% 11 PNC Financial Services Group 67 1,950,726 1.5% 12 Brand Group Holdings Inc. 7 1,511,697 1.2% 13 State Bank Finl Corp. 8 1,221,623 0.9% 14 Hamilton State Bancshares 22 1,216,062 0.9% 15 BankCap Equity Fund LLC 1 995,399 0.8% 17 Georgia Commerce Bancshares 9 831,395 0.6% Total For Institutions In Market 1,312 129,912,998 100.0% Entrance Into Georgia • IBERIABANK Corporation will have a meaningful presence in the Atlanta market with significant growth potential • Metro Atlanta is a strong commercial banking market and provides a natural fill-in for IBERIABANK Corporation in the Southeastern U.S. banking market • IBERIABANK Executive Management (CEO, COO, CCO, and other Senior Credit Officers, etc.) have significant experience in the Atlanta market • Atlanta is the fourth largest MSA in the South. IBERIABANK Corporation will now operate in all of the top five MSAs in that region 5 Source: SNL Financial as of June 30, 2014 Regulatory Data Atlanta-Sandy Springs-Marietta Market Share & Rankings |

6 6 Franchise Highlights • One of metro Atlanta's most successful community banks in terms of quality growth and earnings performance • 3Q14 crossed threshold to over $1 billion in total assets • Successful integrator of three prior acquisitions – two FDIC and one whole-bank transaction • One of few banks in Georgia to issue TARP preferred stock, and the first to repurchase the instrument • Successfully raised unregistered common equity capital in two offerings to fund growth • High quality management and executive staff with proven performance in Atlanta market • Mark Tipton will become EVP and Georgia Regional President • Rodney Hall will become EVP and Atlanta Market President Source: SNL Financial as of September 30, 2014 • Total Gross Loans: $731 million • Total Assets: $1,005 million • Total Deposits: $826 million • Total Equity: $101 million common equity 3Q14 Performance • ROAA 1.09% • ROAE 10.73% • Net Interest Margin 4.69% • Cost of Deposits 0.40% • Tier 1 Leverage Ratio 10.41% • Total RBC Ratio 13.64% |

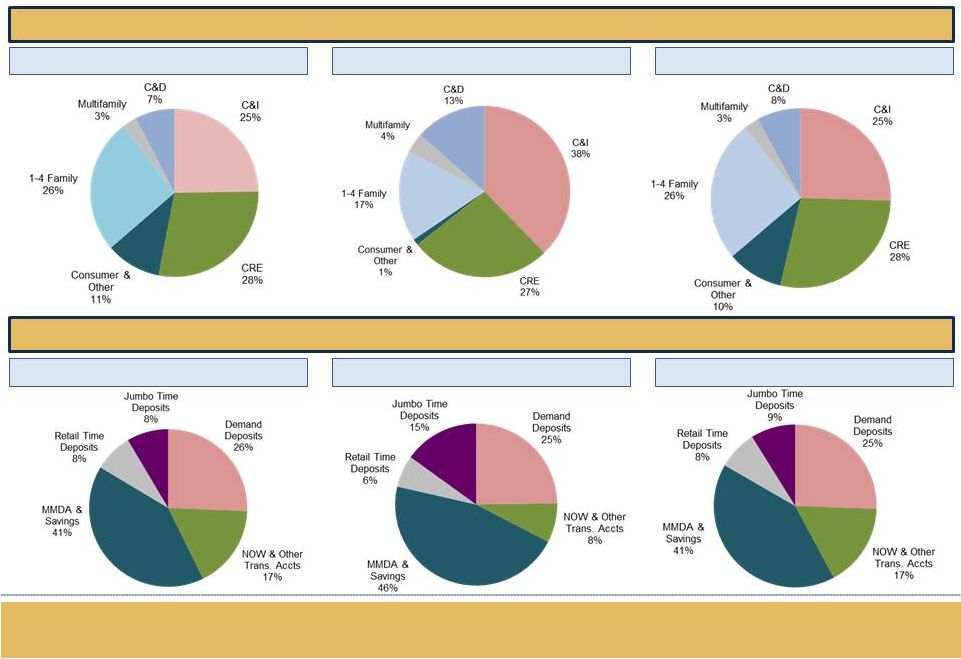

Loan and Deposit Composition IBKC GCB Pro Forma (1) Data as of 9/30/14 (1) Excludes purchase accounting adjustments IBKC GCB Pro Forma (1) Loan Composition Deposit Composition 7 |

8 8 8 8 8 8 • Approximately 85 people involved in due diligence process; credit team included 21 associates performing both on-site credit file and off-site credit portfolio reviews • Reviewed 94% of outstanding loan balances and nearly 98% of total number of loans • Approximately 60% of outstanding loan balances were reviewed on-site with the remainder analyzed by off-site portfolio review • Majority are in-market loans • Primarily focused on commercial lending • Good asset quality metrics: • $35 million of loans covered under FDIC loss share protection (5% of total loans) • Credit mark of approximately $12.9 million on a pre-tax par basis. Fair value mark to portfolio results in a $8 million write-up to net book value pre-tax • Allowance for loan losses of $7.2 million Credit Summary Source: SNL Financial and company documents as of September 30, 2014 Diligence Scope Loan Portfolio Comments • Non-performing assets /Assets = 0.43% (excluding FDIC) • Non-performing loans/Loans = 0.81% |

9 9 9 9 9 9 Merger Considerations • No corporate or bank board seats • Georgia Commerce board members invited to form the nucleus of IBERIABANK Corporation’s Atlanta Advisory Board • Two employment contracts • Savings equate to approximately 20% compared to Georgia Commerce’s total expenses excluding CDI amortization and FDIC loss share expense • No office consolidations anticipated Approximately $21 million in pre-tax costs: • $4.5 million in executive and officer retention • $3.8 million in contract terminations • $2.4 million in change of control payments • $1.8 million in system conversions • $1.1 million in severance • $0.6 million in marketing/communications • $6.5 million in other merger-related expense Costs & Synergies Merger-Related Costs |

10 10 10 10 10 10 Conservative Financial Assumptions Cost Savings: Merger Related Costs: Gross loan loss estimate of $12.9 million on a pre-tax par basis. $8.8 million FMV increase to loans and a $1.3 million write-down to the indemnification asset on a pre- tax book basis Current allowance for loan losses of $7.2 million Annual run-rate cost savings of approximately $5 million on a pre-tax basis Approximately $21 million on a pre-tax basis Approximately 1.6% accretive to EPS in 2016 and 5% accretive in 2017 Tangible book value dilution of approximately 1.8% at consummation Tangible book value breakeven, including one-time acquisition and conversion related costs, of approximately three and one-half years Strong pro forma capital ratios (2) : Internal rate of return over 20%; well in excess of our cost of capital Credit Mark: Other Marks: Aggregate negative $0.4 million in other marks including securities portfolio, OREO, fixed assets and borrowings Financial Assumptions & Impact Attractive Financial Impact Notes: (1) Excluding CDI amortization and FDIC loss share expense (2) Pro forma capital ratios include pending Florida Bank Group, Inc., Old Florida Bancshares, Inc. and Georgia Commerce Bancshares, Inc. transactions Represents approximately of 20% of Georgia Commerce’s run-rate 2014 non-interest expenses (1) Expect run-rate savings to be achieved within six months of closing Tangible common equity ratio = 8.5% Total risk based capital ratio = 12.2% • • • • • • • • • • • • • • |

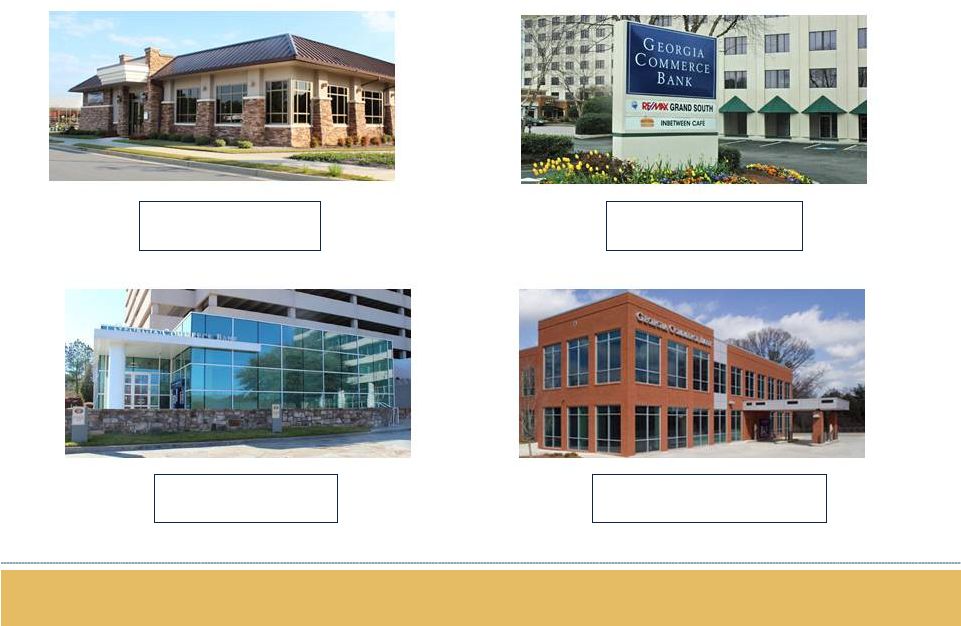

3590 Cobb Pkwy NW Acworth, $29.2 million 2970 Peachtree Rd, NW Atlanta, $147.0 million 3625 Cumberland Blvd Atlanta, $292.1 million 709 Canton Rd. NE, Ste 100 Marietta, $58.3 million Source: Georgia Commerce website and SNL Financial Branch Photos |

200 Scientific Dr Peachtree Corners, $38.9 100 Springfield Dr. Woodstock, $39.7 million 2555 Peachtree Pkwy Cumming, $81.7 2221 Johnson Ferry Rd Atlanta, $41.4 2987 Clairmont Rd NE Atlanta, $103.1 Branch Photos Source: Georgia Commerce website and SNL Financial |

Appendix |

14 14 14 14 14 14 Top MSAs In The South Source: SNL Financial MSA Market Population Total Branches Total Deposits (000's) % Credit Unions Market % Share Top 3 % Market Share Top 10 Market HHI 1 Dallas-Fort Worth, TX TX 6,887,537 2,001 220,191,720 7% 56% 74% 1,474 2 Houston, TX TX 6,352,744 1,890 229,556,456 6% 62% 79% 2,364 3 Miami-Fort Lauderdale-West Palm Beach, FL FL 5,860,668 1,848 192,118,617 3% 39% 69% 782 4 Atlanta, GA GA 5,574,225 1,519 144,245,361 10% 59% 77% 1,558 5 Tampa-St. Petersburg-Clearwater, FL FL 2,886,350 910 66,148,524 17% 43% 75% 1,035 6 Charlotte-Concord-Gastonia, NC NC 2,337,694 689 204,776,078 2% 92% 96% 5,535 7 San Antonio, TX TX 2,294,934 598 43,616,780 37% 44% 79% 2,990 8 Orlando, FL FL 2,277,414 704 44,673,650 9% 55% 81% 1,382 9 Austin-Round Rock, TX TX 1,912,746 623 40,703,576 17% 45% 71% 1,129 10 Nashville, TN TN 1,765,552 691 46,725,597 6% 40% 70% 829 11 Virginia Beach-Norfolk-Newport News, VA VA 1,722,167 531 27,621,538 22% 41% 82% 1,304 12 Jacksonville, FL FL 1,397,575 459 56,478,396 13% 69% 89% 2,808 13 Memphis, TN TN 1,352,761 491 25,719,281 8% 49% 67% 1,176 14 New Orleans-Metairie, LA LA 1,248,999 487 34,642,287 6% 56% 85% 1,647 15 Richmond, VA VA 1,247,586 438 36,340,007 11% 62% 87% 3,223 16 Raleigh, NC NC 1,219,465 392 53,242,215 56% 68% 92% 1,305 17 Birmingham-Hoover, AL AL 1,142,042 456 39,790,121 18% 53% 79% 1,784 18 Greenville-Anderson-Mauldin, SC SC 855,961 331 14,655,727 6% 39% 75% 873 19 Knoxville, TN TN 855,322 402 19,030,553 23% 38% 73% 1,061 20 El Paso, TX TX 846,112 155 10,370,493 34% 50% 89% 1,696 21 McAllen-Edinburg-Mission, TX TX 825,955 183 9,857,503 6% 46% 86% 1,145 22 Baton Rouge, LA LA 824,027 343 21,682,911 15% 57% 80% 2,027 23 Columbia, SC SC 795,973 278 18,128,352 11% 61% 89% 1,882 24 Greensboro-High Point, NC NC 744,253 268 12,744,998 13% 41% 80% 1,022 25 North Port-Sarasota-Bradenton, FL FL 735,292 318 17,143,325 0% 45% 72% 914 26 Little Rock, AR AR 728,263 366 15,942,163 8% 39% 82% 969 27 Charleston-North Charleston, SC SC 719,790 250 11,994,395 15% 44% 79% 1,138 28 Cape Coral-Fort Myers, FL FL 664,763 240 12,794,965 0% 44% 75% 902 29 Winston-Salem, NC NC 653,063 227 42,406,408 7% 84% 96% 6,504 30 Lakeland-Winter Haven, FL FL 623,737 163 8,198,933 29% 46% 89% 1,186 Markets highlighted in yellow indicate current IBKC markets Markets highlighted in red indicate markets for pending transactions |

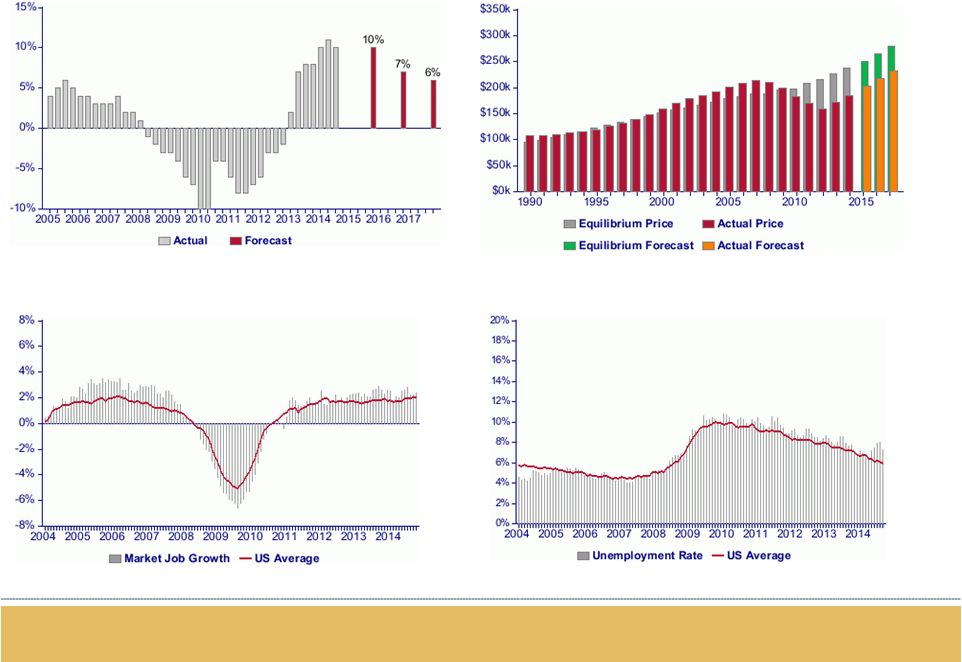

15 15 15 15 15 15 Atlanta Market Home Price Change Home Price Change Home prices in this market peaked in Q1 2008 at $214,962. Since their peak, prices have fallen by 12%. In the last 12 months, prices have gone up by 10 percent. The average home price in this market is currently $188,751. In the past 12 months, jobs in this market have grown by 2.4 percent. This compares to a national increase of 2.0 percent. Job Growth Unemployment The Unemployment Rate in September 2014 was 7.3% versus 7.6% last year. Source: Local Market Monitor Home values for Atlanta- Sandy Springs- Marietta are forecast to increase by 10 percent over the next 12 months. Nationally, prices are forecast to increase by 6.3 percent. In the second and third year, prices are forecast to increase 7% and 6%, respectively. |

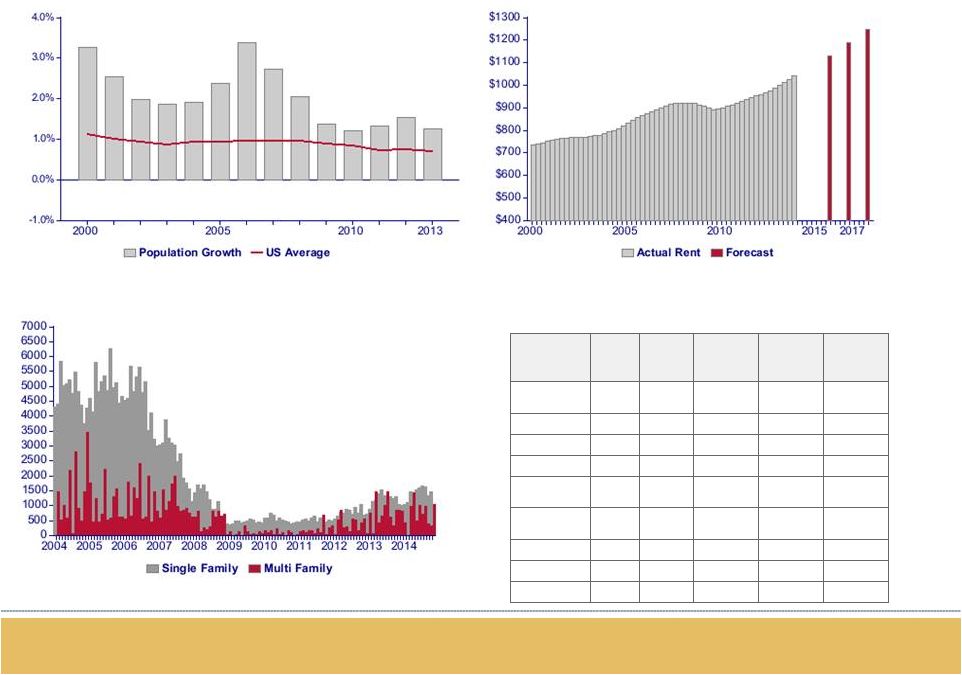

16 16 16 16 16 16 Atlanta Market Population Growth The population in this market grew 1.3% in 2013, while the US population grew 0.7%. Rent Per Month We forecast rents to increase 15 percent over the next three years in this market, to an average of $1247 per month, partly due to higher inflation. Total housing permits in October 2014 were up 18 percent from last year. Single family permits were up 14 percent. Housing Permits Employment By Industry Source: Local Market Monitor Industry % of Total US % of Total Oct-14 12-Month Job Growth Month Job Growth Construction/ Mining 4% 4% 100,700 5.40% 4.00% Manufacturing 6% 9% 153,600 1.60% 1.40% Finance 7% 6% 162,900 3.00% 1.20% Retail Trade 11% 11% 270,200 2.60% 1.80% Business & Prof. Services 18% 14% 456,900 3.70% 3.60% Health Care & Education 12% 16% 300,100 0.50% 2.10% Tourism/Hotels 10% 10% 256,900 3.40% 2.80% Government 13% 16% 319,900 0.60% 0.40% Total 100% 100% 2,489,100 2.40% 2.00% |

|