|

ANALYST-INVESTOR DAY

Presentation Materials

February 27, 2015

1

|

Safe Harbor And Legend

To the extent that statements in this presentation relate to future plans, objectives, financial results or performance of IBERIABANK Corporation, these statements are deemed to be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements, which are based on management’s current information, estimates and assumptions and the current economic environment, are generally identified by the use of the words “plan”, “believe”, “expect”, “intend”, “anticipate”, “estimate”, “project” or similar expressions. The Company’s actual strategies, results and financial condition in future periods may differ materially from those currently expected due to various risks and uncertainties. Forward-looking statements are subject to numerous assumptions, risks and uncertainties that change over time and could cause actual results or financial condition to differ materially from those expressed in or implied by such statements. Consequently, no forward-looking statement can be guaranteed. Hypothetical information isnot aprojection of future performance.

In connection with the pending transactions with Florida Bank Group, Inc., Old Florida Bancshares, Inc., and Georgia Commerce Bancshares, Inc., IBERIABANK Corporation has filed Registration Statements on Form S-4 that contain proxy statement / prospectuses. INVESTORS AND SECURITY HOLDERS ARE URGED TO CAREFULLY READ THE PROXY STATEMENT / PROSPECTUSES REGARDING THE PROPOSED TRANSACTIONS, BECAUSE SUCH DOCUMENTS CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain a free copy of the proxy statement / prospectuses (when they are available) and other documents containing information about the pending transactions, without charge, at the SEC’s website at http://www.sec.gov. Copies of the proxy statement / prospectuses and the SEC filings that will be incorporated by reference in the proxy statement / prospectuses may also be obtained forfree from the IBERIABANK Corporation website, www.iberiabank.com, under the heading “Investor Information.”

This communication is not a solicitation of any vote or approval, is not an offer to purchase shares of common stock of Georgia Commerce Bancshares, Inc., nor is it an offer to sell shares of IBERIABANK Corporation common stock which may be issued in the proposed merger. The issuance of IBERIABANK Corporation common stock in any proposed merger would have to be registered under the Securities Act of 1933, as amended, and such IBERIABANK Corporation common stock would be offered only by means of a prospectus complying with the Act.

2

|

DISCUSSION TOPICS

Overview

Welcome, Introductions, and Logistics…

Energy Discussion

Update Regarding Our Recent Initiatives.

Guest Speaker

Our Markets and Growth

M&A Update

Interest Rate Risk

Strategic Goals

Closing

Daryl Byrd Randy Bryan Kevin Rafferty Carmen Jordan Bryan Chapman

Anthony Restel Stephen Moret

Secretary of the Louisiana of Economic Development

Michael Brown John Davis Anthony Restel Anthony Restel Daryl Byrd

3

|

ENERGY DISCUSSION

4

|

ENERGY DISCUSSION

Presenting Today

J. Randolph Bryan – Chief Risk Officer

Energy Lending Team Leadership

Bryan Chapman – EVP / Energy Lending

Carmen Jordan – EVP / Houston Market President

Kevin Rafferty – EVP / Texas State President

IBERIA Capital Partners Leadership / Available for Q&A

Jefferson G. Parker – Vice Chairman & President, IBERIA Capital Partners

Cliff Worley – Managing Director—Investment Banking

5

|

ENERGY DISCUSSION

Risks And Potential Impact

We think about risks presented by the decline in energy commodity prices across four perspectives, and its impact on:

The energy lending portfolio from an asset quality standpoint

The local markets in which we operate that have a significant energy presence, primarily Houston and Lafayette and the individuals and non-energy related businesses that operate there

Our forecast for growth and earnings

Our share price

6

|

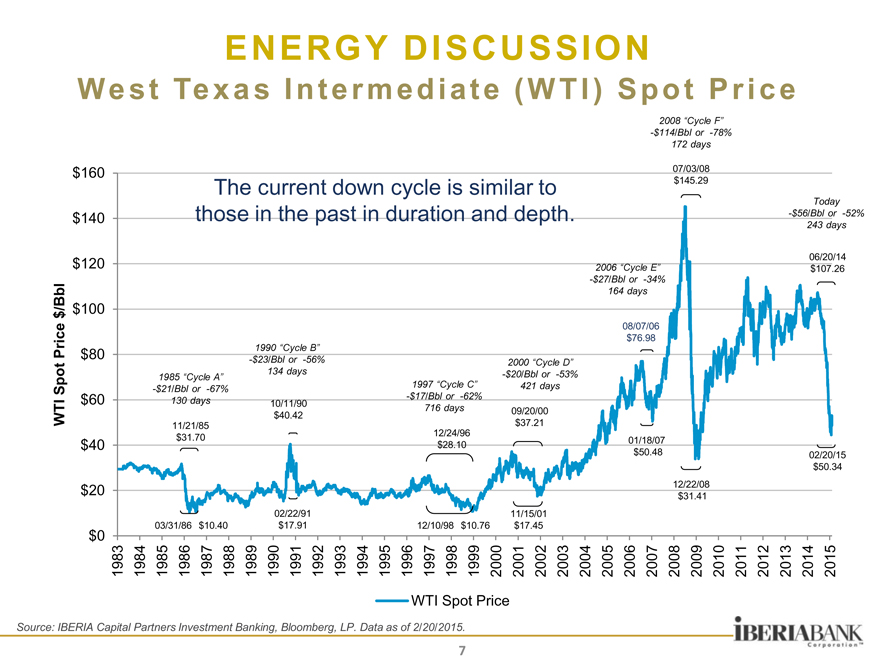

ENERGY DISCUSSION

West Texas Intermediate (WTI) Spot Price

WTI Spot Price

$160 $140 $120 $100 $80 $60 $40 $20 $0

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

The current down cycle is similar to those in the past in duration and depth.

2008 “Cycle F”

-$114/Bbl or -78% 172 days

07/03/08 $145.29

Today

-$56/Bbl or -52% 243 days

06/20/14 $107.26

2006 “Cycle E”

-$27/Bbl or -34% 164 days

08/07/06 $76.98

1985 “Cycle A”

-$21/Bbl or -67% 130 days

11/21/85 $31.70

1990 “Cycle B”

-$23/Bbl or -56% 134 days

10/11/90 $40.42

1997 “Cycle C”

-$17/Bbl or -62% 716 days

12/24/96 $28.10

2000 “Cycle D”

-$20/Bbl or -53% 421 days

09/20/00 $37.21

01/18/07 $50.48

12/22/08 $31.41

02/20/15 $50.34

02/22/91 11/15/01

03/31/86 $10.40 $17.91 12/10/98 $10.76 $17.45

WTI Spot Price

Source: IBERIA Capital Partners Investment Banking, Bloomberg, LP. Data as of 2/20/2015.

7

|

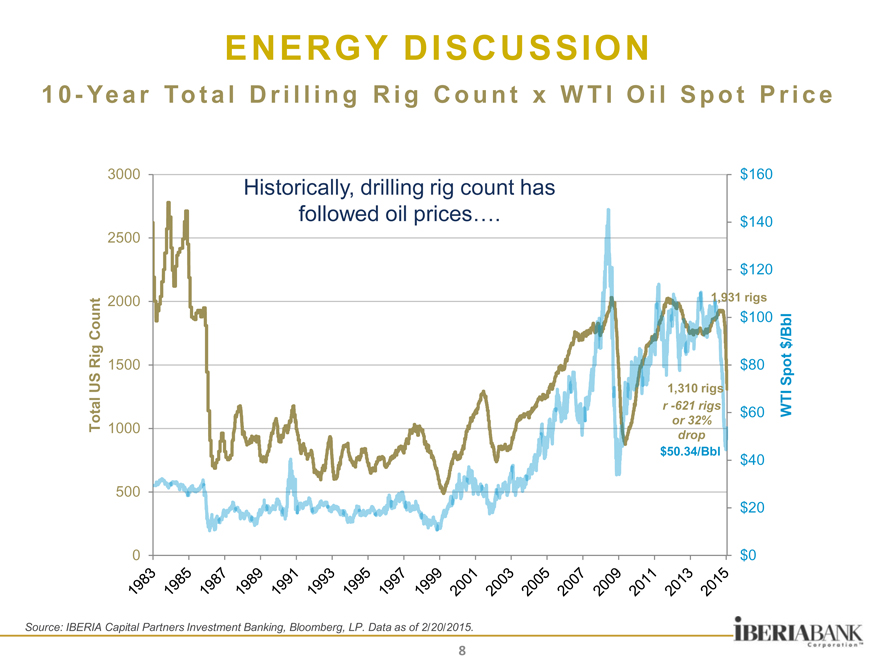

3000 2500 2000 1500 1000 500 0

Total US Rig Count

Historically, drilling rig count has followed oil prices….

1,931 rigs

$160 $140 $120

$100 $80 $60 $40 $20 $0

WTI Spot

1,310 rigs r -621 rigs or 32% drop $50.34/Bbl

Source: IBERIA Capital Partners Investment Banking, Bloomberg, LP. Data as of 2/20/2015.

8

|

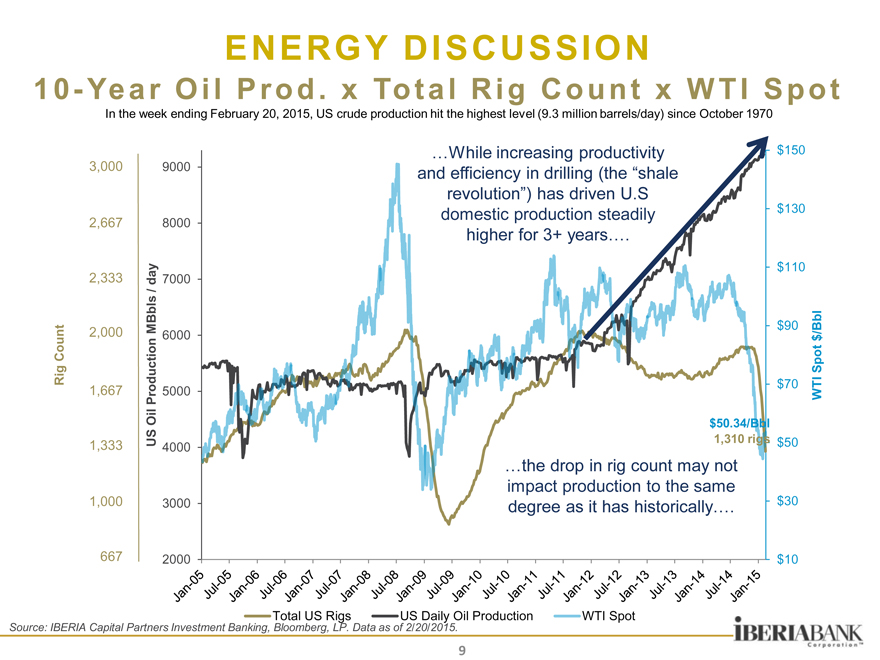

ENERGY DISCUSSION

10-Year Oil Prod. x Total Rig Count x WTI Spot

In the week ending February 20, 2015, US crude production hit the highest level (9.3 million barrels/day) since October 1970

…While increasing productivity and efficiency in drilling (the “shale revolution”) has driven U.S domestic production steadily higher for 3+ years….

3,000

2,667

2,333

2,000

1,667

1,333

1,000

667

Rig Count

US Oil Production MBbls / day

9000 8000 7000 6000 5000 4000 3000 2000

9000 8000 7000 6000 5000 4000 3000 2000

$150

$130

$110

$90 /Bbl $ Spot

$70 WTI $50

$30

$10

$50.34/Bbl 1,310 rigs

Total US Rigs US Daily Oil Production WTI Spot

Source: IBERIA Capital Partners Investment Banking, Bloomberg, LP. Data as of 2/20/2015.

9

|

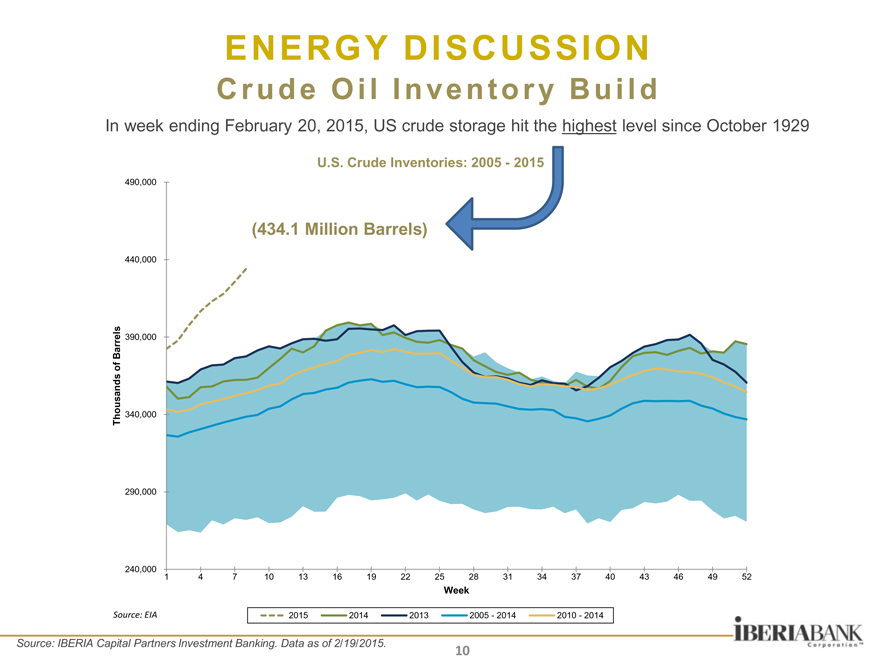

ENERGY DISCUSSION

Crude Oil Inventory Build

In week ending February 20, 2015, US crude storage hit the highest level since October 1929

U.S. Crude Inventories: 2005—2015

490,000

440,000

Barrels 390,000 of s Thousand 340,000

290,000

240,000 1

Source: EIA

(434.1 Million Barrels)

4 7 10 1316 192225 2831 3437 404346 4952

Week

2015 2014 2013 2005—2014 2010—2014

Source: IBERIA Capital Partners Investment Banking. Data as of 2/19/2015.

10

|

ENERGY DISCUSSION

Global Crude Supply Versus Demand

Downside Risk As Supply Continues To Outstrip Demand

Million barrels / day

96 94 92 90 88 86 84 82 80 78

4Q14 oversupply of ~914,000 Barrels / day

projections

6 5 4 3 2 1 0 -1 -2 -3

Million barrels / day

Most recent 4 quarters of oversupply, with 4 more projected

2010 2011 2012 2013 2014 2015 2016

Implied Stock Change and Balance Global Supply Global Demand

Source: EIA, Short-Term Energy Outlook, February 2015.

11

|

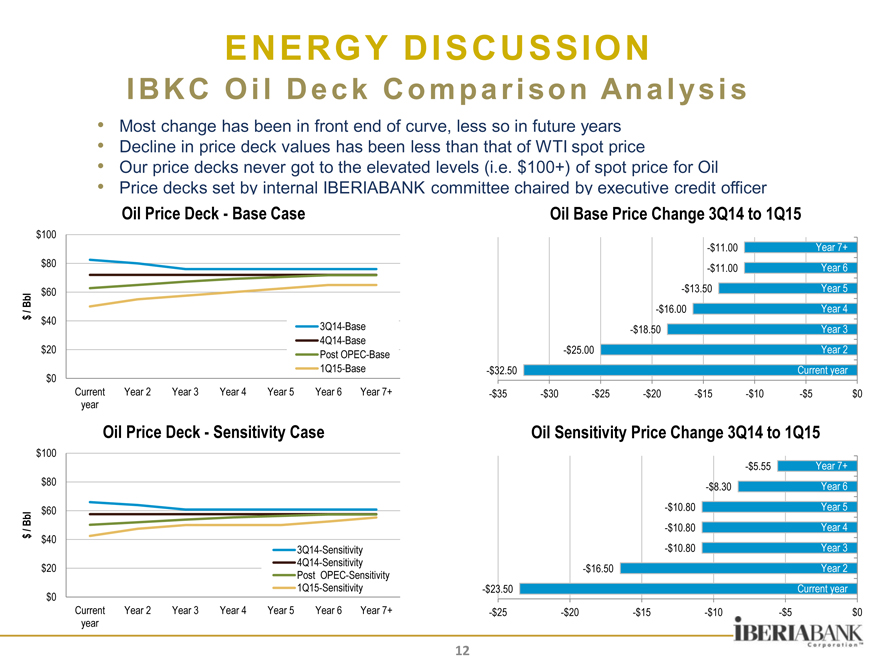

ENERGY DISCUSSION

IBKC Oil Deck Comparison Analysis

Most change has been in front end of curve, less so in future years

Decline in price deck values has been less than that of WTI spot price

Our price decks never got to the elevated levels (i.e. $100+) of spot price for Oil

Price decks set by internal IBERIABANK committee chaired by executive credit officer

Oil Price Deck—Base Case Oil Base Price Change 3Q14 to 1Q15

$100

$80

$60

Bbl / $ $40

$20

$0

$100

$80

$60

Bbl / $ $40

$20

$0

3Q14-Base 4Q14-Base Post OPEC-Base 1Q15-Base

Current Year 2 Year 3 Year 4 Year 5 Year 6 Year 7+ year

Oil Price Deck—Sensitivity Case

3Q14-Sensitivity 4Q14-Sensitivity Post OPEC-Sensitivity 1Q15-Sensitivity Current Year 2 Year 3 Year 4 Year 5 Year 6 Year 7+ year

Oil Base Price Change 3Q14 to 1Q15

-$11.00 Year 7+

-$11.00 Year 6

-$13.50 Year 5

-$16.00 Year 4

-$18.50 Year 3

-$25.00 Year 2

-$32.50 Current year

-$35 -$30 -$25 -$20 -$15 -$10 -$5 $0

Oil Sensitivity Price Change 3Q14 to 1Q15

-$5.55 Year 7+

-$8.30 Year 6

-$10.80 Year 5

-$10.80 Year 4

-$10.80 Year 3

-$16.50 Year 2

-$23.50 Current year

-$25 -$20 -$15 -$10 -$5 $0

|

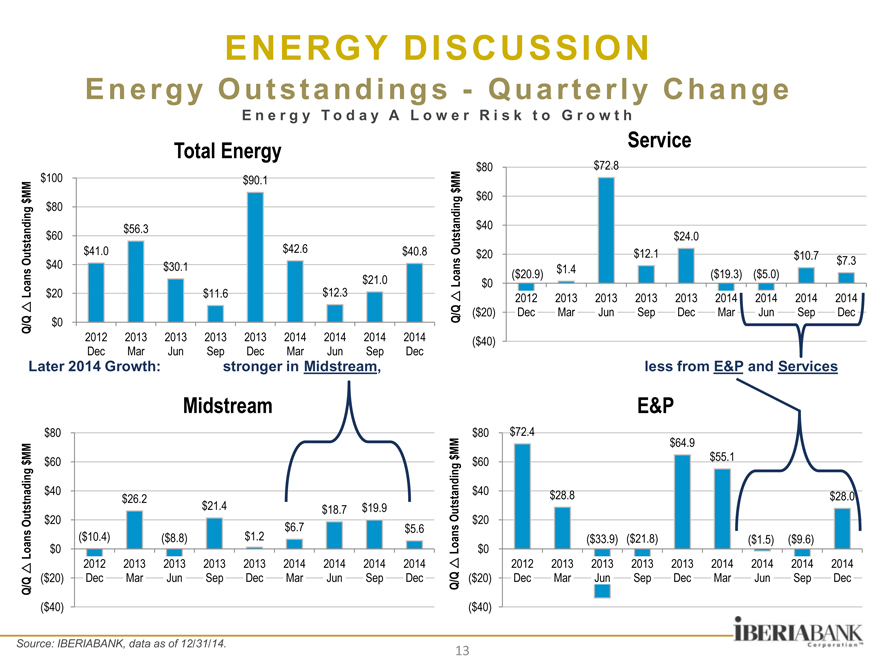

ENERGY DISCUSSION

Energy Outstandings—Quarterly Change

Energy T o d a y A L o w e r R i s k t o G r o w t h

Service Total Energy $72.8

M $100 $90.1 $ M $80

$56.3 $60

Outstanding $41.0 $42.6 $40.8 ns $40 $30.1

$21.0 Loa $20 $11.6 $12.3

Q/Q $0

2012 2013 2013 2013 2013 2014 2014 2014 2014 Dec Mar Jun Sep Dec Mar Jun Sep Dec

Later 2014 Growth: stronger in Midstream,

Midstream

$80

$60 g $40 $26.2 $21.4 $18.7 $19.9

Outstnadin $20 $6.7 $5.6

($10.4) ($8.8) $1.2

Loans $0

2012 2013 2013 2013 2013 2014 2014 2014 2014

($20) Dec Mar Jun Sep Dec Mar Jun Sep Dec

Q/Q

($40)

$80 $72.8 $ MM $60

Outstanding $40 $24.0

$20 $12.1 $10.7 $7.3 oans ($20.9) $1.4 ($19.3) ($5.0) L $0 2012 2013 2013 2013 2013 2014 2014 2014 2014 Q/Q ($20) Dec Mar Jun Sep Dec Mar Jun Sep Dec

($40)

less from E&P and Services

E&P

$80 $72.4 $64.9 $55.1 g $60

Outstandin $40 $28.8 $28.0 $20

($33.9) ($21.8) ($1.5) ($9.6)

Loans $0

2012 2013 2013 2013 2013 2014 2014 2014 2014 Q/Q ($20) Dec Mar Jun Sep Dec Mar Jun Sep Dec

($40)

Source: IBERIABANK, data as of 12/31/14.

13

|

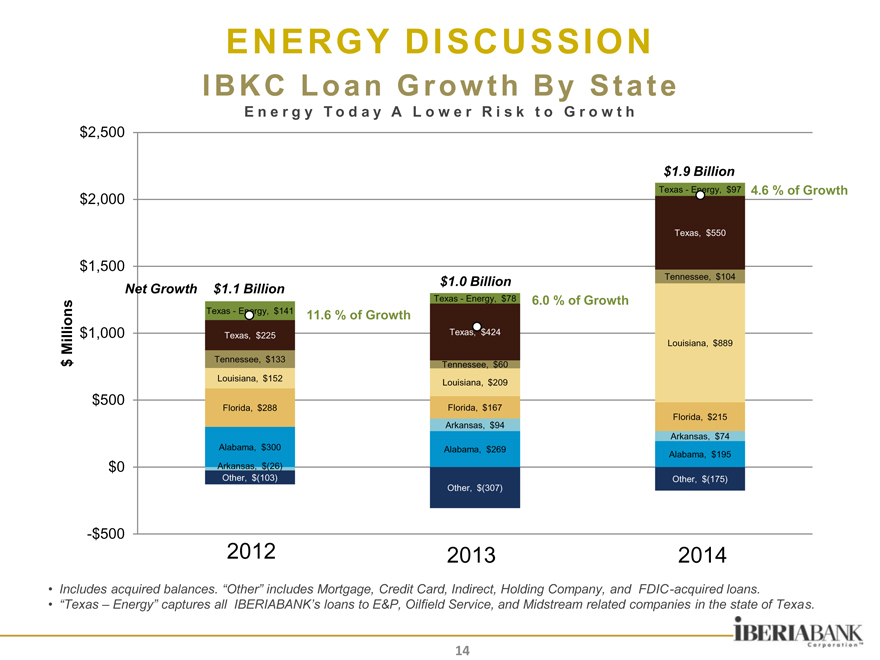

ENERGY DISCUSSION

IBKC LoanGrowthByState

Energy T o d a y A L o w e r R i s k t o G r o w t h

$2,500

$2,000

$1,500

Millions $1,000 $

$500

$0

-$500

$1.9 Billion

Texas—Energy, $97 4.6 % of Growth

Texas, $550

$1.0 Billion Tennessee, $104

Net Growth $1.1 Billion Texas—Energy, $78 6.0 % of Growth

Texas—Energy, $141 11.6 % of Growth

Texas, $225 Texas, $424

Louisiana, $889 Tennessee, $133 Tennessee, $60 Louisiana, $152 Louisiana, $209

Florida, $288 Florida, $167

Arkansas, $94 Florida, $215 Arkansas, $74 Alabama, $300 Alabama, $269 Alabama, $195 Arkansas, $(26) Other, $(103) Other, $(175) Other, $(307)

2012 2013 2014

Includes acquired balances. “Other” includes Mortgage, Credit Card, Indirect, Holding Company, and FDIC-acquired loans.

“Texas – Energy” captures all IBERIABANK’s loans to E&P, Oilfield Service, and Midstream related companies in the state of Texas.

14

|

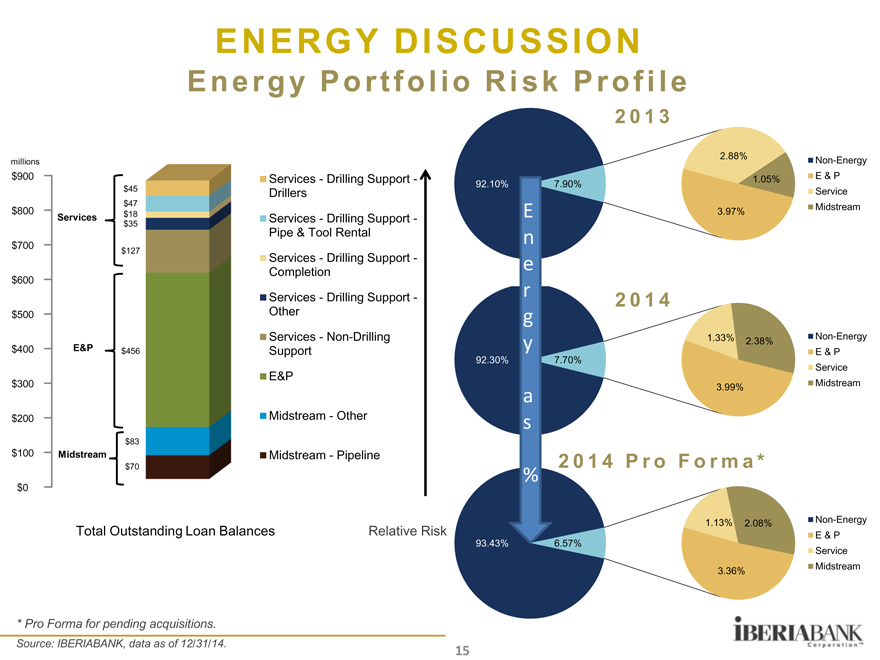

ENERGY DISCUSSION

Energy Portfolio Risk Profile

2013

millions

$900 Services—Drilling Support -

$45 Drillers

$47

$800 Services $18 Services—Drilling Support -

$35

Pipe & Tool Rental

$700 $127

Services—Drilling Support -

Completion

$600

Services—Drilling Support -

$500 Other

Services—Non-Drilling

$400 E&P $456 Support

$300 E&P

$200 Midstream—Other

$83

$100 Midstream Midstream—Pipeline

$70

$0

Total Outstanding Loan Balances Relative Risk

2.88% Non-Energy

1.05% E & P

92.10% 7.90%

Service

E 3.97% Midstream

n

e

r 2014

g

y 1.33% 2.38% Non-Energy

E & P

92.30% 7.70%

Service

Midstream

a 3.99%

s

2 0 1 4 P r o F o r m a *

%

1.13% 2.08% Non-Energy

E & P

93.43% 6.57%

Service

3.36% Midstream

* Pro Forma for pending acquisitions.

Source: IBERIABANK, data as of 12/31/14.

15

|

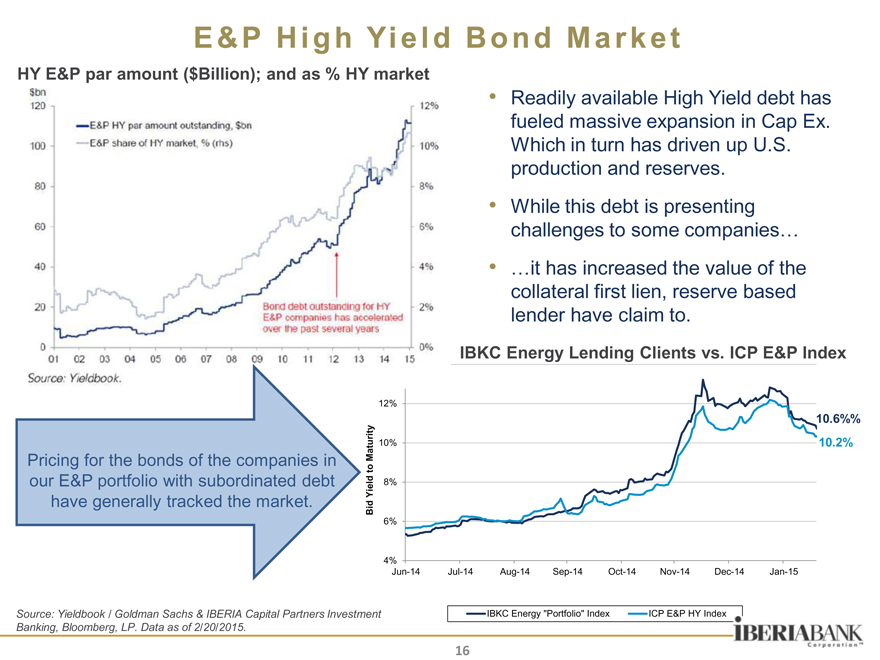

E&P High Yield Bond Market

HY E&P par amount ($Billion); and as % HY market

Source: Yieldbook / Goldman Sachs & IBERIA Capital Partners Investment Banking, Bloomberg, LP. Data as of 2/20/2015.

Readily available High Yield debt has fueled massive expansion in Cap Ex. Which in turn has driven up U.S. production and reserves.

While this debt is presenting challenges to some companies…

…it has increased the value of the collateral first lien, reserve based lender have claim to.

IBKC Energy Lending Clients vs. ICP E&P Index

12%

10.6%%

Maturity 10% 10.2% o t Yield 8% Bid

6%

4%

Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15

IBKC Energy “Portfolio” Index ICP E&P HY Index

16

|

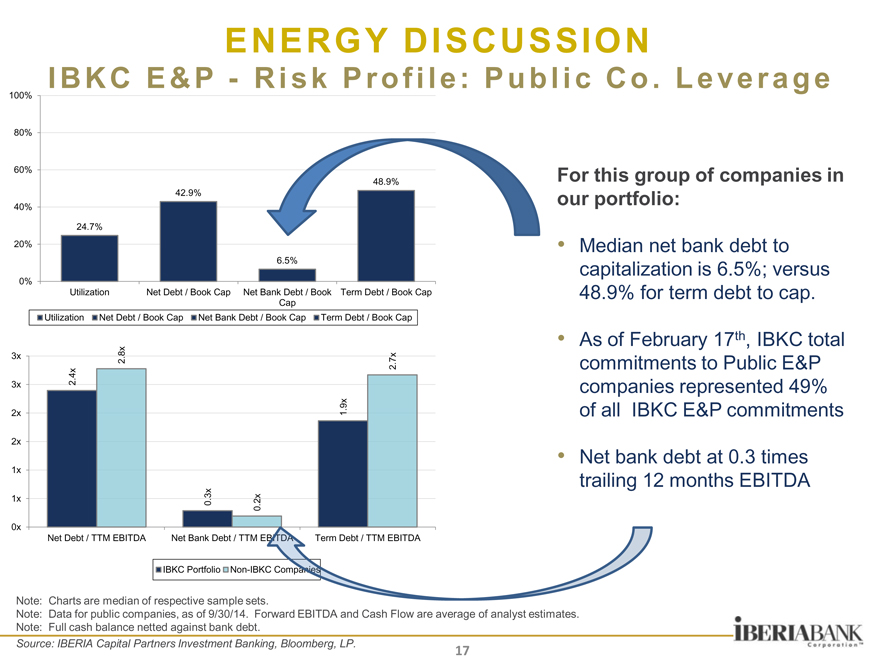

ENERGY DISCUSSION

IBKC E&P—Risk Profile: Public Co. Leverage

100%

80%

60%

48.9%

42.9% 40%

24.7% 20%

6.5%

0%

Utilization Net Debt / Book Cap Net Bank Debt / Book Term Debt / Book Cap Cap Utilization Net Debt / Book Cap Net Bank Debt / Book Cap Term Debt / Book Cap

3x . 8x

2 . 7x 2 . 4x

3x 2

. 9x

2x 1 2x

1x

1x . 3x

0 . 2x 0

0x

Net Debt / TTM EBITDA Net Bank Debt / TTM E rm Debt / TTM EBITDA

IBKC Portfolio Non-IBKC Com

For this group of companies in our portfolio:

Median net bank debt to capitalization is 6.5%; versus 48.9% for term debt to cap.

As of February 17th, IBKC total commitments to Public E&P companies represented 49% of all IBKC E&P commitments

Net bank debt at 0.3 times trailing 12 months EBITDA

Note: Charts are median of respective sample sets.

Note: Data for public companies, as of 9/30/14. Forward EBITDA and Cash Flow are average of analyst estimates. Note: Full cash balance netted against bank debt.

Source: IBERIA Capital Partners Investment Banking, Bloomberg, LP.

17

|

18

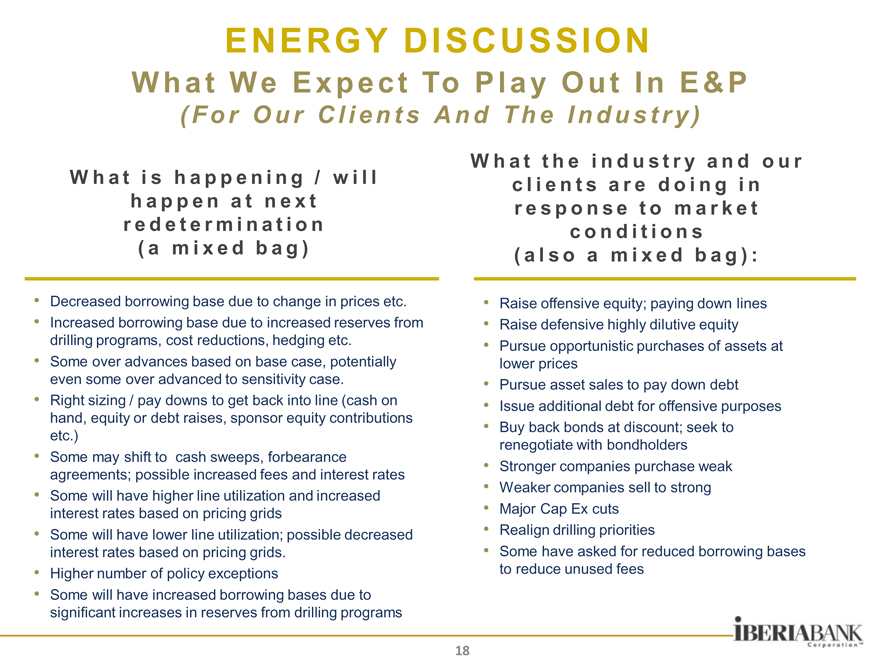

Decreased borrowing base due to change in prices etc.

Increased borrowing base due to increased reserves from drilling programs, cost reductions, hedging etc.

Some over advances based on base case, potentially even some over advanced to sensitivity case.

Right sizing / pay downs to get back into line (cash on hand, equity or debt raises, sponsor equity contributions etc.)

Some may shift to cash sweeps, forbearance agreements; possible increased fees and interest rates

Some will have higher line utilization and increased interest rates based on pricing grids

Some will have lower line utilization; possible decreased interest rates based on pricing grids.

Higher number of policy exceptions

Some will have increased borrowing bases due to significant increases in reserves from drilling programs

Raise offensive equity; paying down lines

Raise defensive highly dilutive equity

Pursue opportunistic purchases of assets at lower prices

Pursue asset sales to pay down debt

Issue additional debt for offensive purposes

Buy back bonds at discount; seek to renegotiate with bondholders

Stronger companies purchase weak

Weaker companies sell to strong

Major Cap Ex cuts

Realign drilling priorities

Some have asked for reduced borrowing bases to reduce unused fees

W h a t t h e i n d u s t r y a n d o u r c l i e n t s a r e d o i n g i n r e s p o n s e t o m a r k e t c o n d i t i o n s ( a l s o a m i x e d b a g ) :

W h a t i s h a p p e n i n g / w i l l h a p p e n a t n e x t r e d e t e r m i n a t i o n ( a m i x e d b a g )

ENERGY DISCUSSION

What We Expect To Play Out In E&P

( F o r O u r C l i e n t s A n d T h e I n d u s t r y )

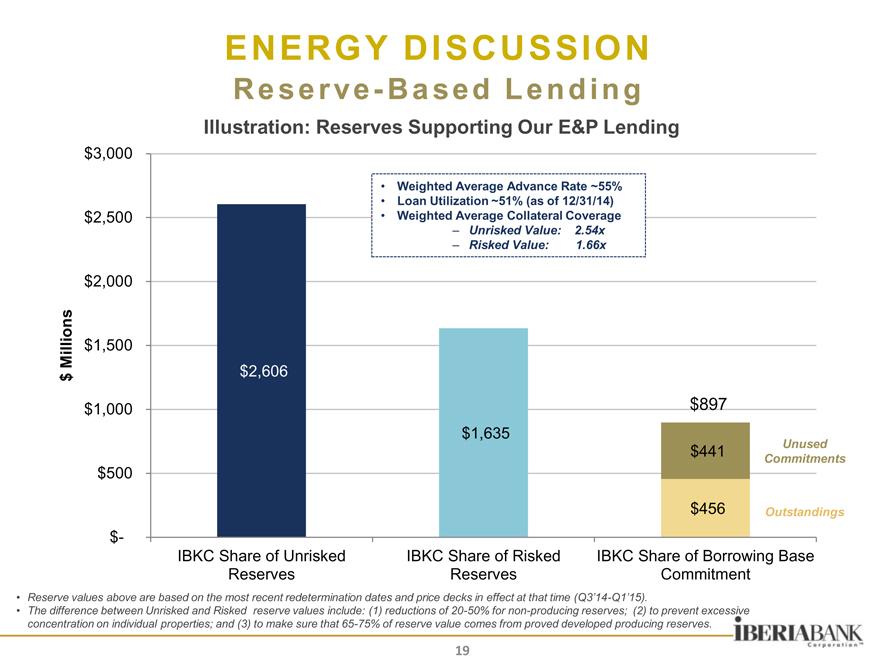

ENERGY DISCUSSION

Reserve-Based Lending

Illustration: Reserves Supporting Our E&P Lending

$ Millions

$3,000 $2,500 $2,000 $1,500 $1,000 $500 $-

Weighted Average Advance Rate ~55%

Loan Utilization ~51% (as of 12/31/14)

Weighted Average Collateral Coverage

– Unrisked Value: 2.54x

– Risked Value: 1.66x

$2,606 $897 $1,635

Unused

$441

Commitments

$456 Outstandings

IBKC Share of Unrisked IBKC Share of Risked IBKC Share of Borrowing Base Reserves Reserves Commitment

Reserve values above are based on the most recent redetermination dates and price decks in effect at that time (Q3’14-Q1’15).

The difference between Unrisked and Risked reserve values include: (1) reductions of 20-50% for non-producing reserves; (2) to prevent excessive concentration on individual properties; and (3) to make sure that 65-75% of reserve value comes from proved developed producing reserves.

19

|

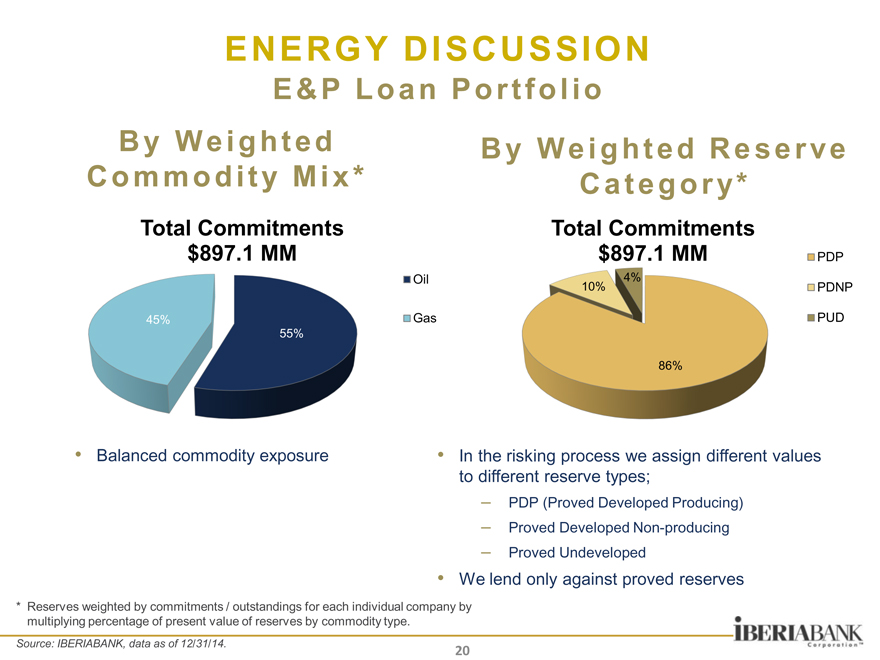

ENERGY DISCUSSION

E&P Loan Portfolio

By Weighted By Weighted Reserve Commodity Mix* Category*

Total Commitments Total Commitments $897.1 MM $897.1 MM PDP

PDNP

PUD

45%

55%

Oil

Gas

Balanced commodity exposure

In the risking process we assign different values to different reserve types;

– PDP (Proved Developed Producing)

– Proved Developed Non-producing

– Proved Undeveloped

We lend only against proved reserves

* Reserves weighted by commitments / outstandings for each individual company by multiplying percentage of present value of reserves by commodity type.

Source: IBERIABANK, data as of 12/31/14.

20

|

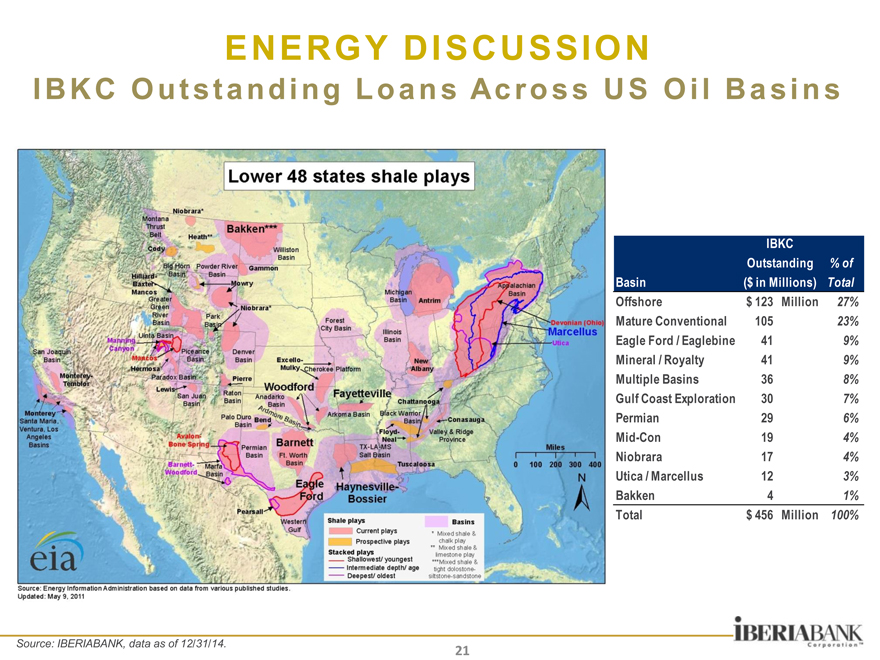

ENERGY DISCUSSION

IBKC Outstanding Loans Across US Oil Basins

IBKC

Outstanding % of

Basin ($ in Millions) Total

Offshore $ 123 Million 27%

Mature Conventional 105 23%

Eagle Ford / Eaglebine 41 9%

Mineral / Royalty 41 9%

Multiple Basins 36 8%

Gulf Coast Exploration 30 7%

Permian 29 6%

Mid-Con 19 4%

Niobrara 17 4%

Utica / Marcellus 12 3%

Bakken 4 1%

Total $ 456 Million 100%

Source: IBERIABANK, data as of 12/31/14.

21

|

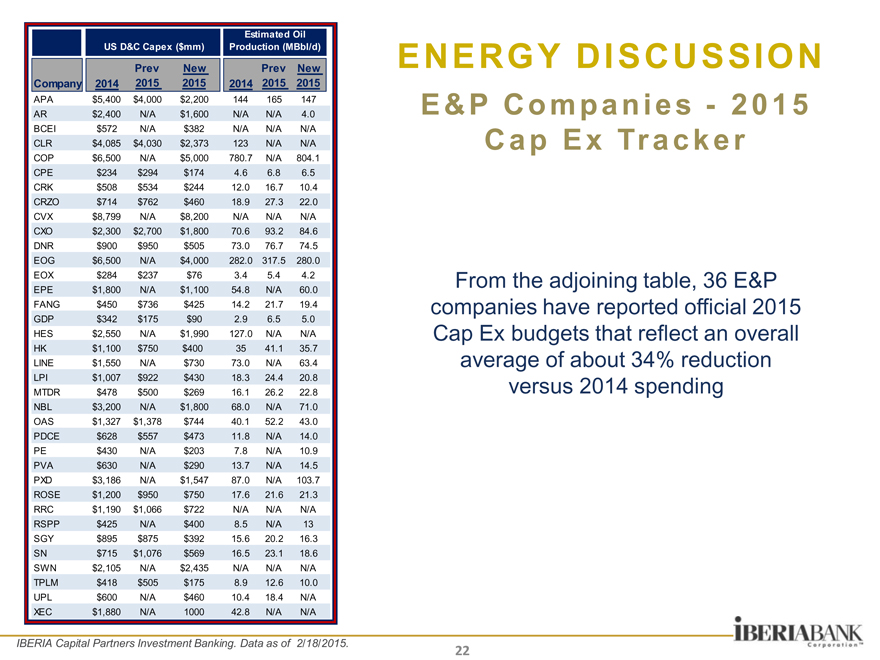

Estimated Oil

US D&C Capex ($mm) Production (MBbl/d)

Prev New Prev New

Company 2014 2015 2015 2014 2015 2015

APA $5,400 $4,000 $2,200 144 165 147

AR $2,400 N/A $1,600 N/A N/A 4.0

BCEI $572 N/A $382 N/A N/A N/A

CLR $4,085 $4,030 $2,373 123 N/A N/A

COP $6,500 N/A $5,000 780.7 N/A 804.1

CPE $234 $294 $174 4.6 6.8 6.5

CRK $508 $534 $244 12.0 16.7 10.4

CRZO $714 $762 $460 18.9 27.3 22.0

CVX $8,799 N/A $8,200 N/A N/A N/A

CXO $2,300 $2,700 $1,800 70.6 93.2 84.6

DNR $900 $950 $505 73.0 76.7 74.5

EOG $6,500 N/A $4,000 282.0 317.5 280.0

EOX $284 $237 $76 3.4 5.4 4.2

EPE $1,800 N/A $1,100 54.8 N/A 60.0

FANG $450 $736 $425 14.2 21.7 19.4

GDP $342 $175 $90 2.9 6.5 5.0

HES $2,550 N/A $1,990 127.0 N/A N/A

HK $1,100 $750 $400 35 41.1 35.7

LINE $1,550 N/A $730 73.0 N/A 63.4

LPI $1,007 $922 $430 18.3 24.4 20.8

MTDR $478 $500 $269 16.1 26.2 22.8

NBL $3,200 N/A $1,800 68.0 N/A 71.0

OAS $1,327 $1,378 $744 40.1 52.2 43.0

PDCE $628 $557 $473 11.8 N/A 14.0

PE $430 N/A $203 7.8 N/A 10.9

PVA $630 N/A $290 13.7 N/A 14.5

PXD $3,186 N/A $1,547 87.0 N/A 103.7

ROSE $1,200 $950 $750 17.6 21.6 21.3

RRC $1,190 $1,066 $722 N/A N/A N/A

RSPP $425 N/A $400 8.5 N/A 13

SGY $895 $875 $392 15.6 20.2 16.3

SN $715 $1,076 $569 16.5 23.1 18.6

SWN $2,105 N/A $2,435 N/A N/A N/A

TPLM $418 $505 $175 8.9 12.6 10.0

UPL $600 N/A $460 10.4 18.4 N/A

XEC $1,880 N/A 1000 42.8 N/A N/A

ENERGY DISCUSSION

E&P Companies—2015 Cap Ex Tracker

From the adjoining table, 36 E&P companies have reported official 2015 Cap Ex budgets that reflect an overall average of about 34% reduction versus 2014 spending

IBERIA Capital Partners Investment Banking. Data as of 2/18/2015.

22

|

ENERGY DISCUSSION

Service Companies Experience In Prior Downturns

Cost reductions were not immediately implemented across the board. Large disparity between management teams and how quickly they reacted to falling commodity prices/rig count.

Experienced energy service-focused private equity-backed companies were among first to reduce headcount, Cap Ex, and other costs.

Some others took a “wait-and-see” approach

Those with higher term debt leverage were forced to work for low-to-negative margins to keep equipment utilized and some cash coming in the door.

Cash flow from working capital contraction (receivables and inventory) was used to pay down debt.

Larger companies with significant owner-occupied real estate sold those properties in sale-leaseback transactions and used proceeds to pay down debt.

Financial crisis exacerbated the detrimental impact of falling commodity prices.

How The Experienced Players Are Reacting This Time

Management teams have kept lower term debt levels since the last downturn.

Rapid cost reductions by almost everyone

Significantly reduced headcount to match falling rig count.

Renegotiating all vendor costs where possible

Reduced/eliminated expansionary Cap Ex. Maintenance Cap Ex only unless surety of quick payback through contracts on other equipment purchases.

Reduced term debt leverage is allowing service companies to cold-stack rigs and idle other equipment rather than working for low/negative margins which will establish a firmer floor for pricing.

23

|

ENERGY DISCUSSION

Labor Impacts

Notable Announced Worldwide Layoffs

Top Ten

Announced % of Total

Company Layoffs Workforce

1 Pemex 10,000 7%

2 Schlumberger 9,000 7%

3 Weatherford 8,000 15%

4 Baker Hughes 7,000 12%

5 Haliburton 6,400 8%

6 Helmerich & Payne 2,000 17%

7 FMC Technologies 2,000 10%

8 Total SA 2,000 2%

9 Technip 1,800 5%

10 Suncor 1,000 8%

Total 49,200 9% average

Note: As of February 2015.

24

|

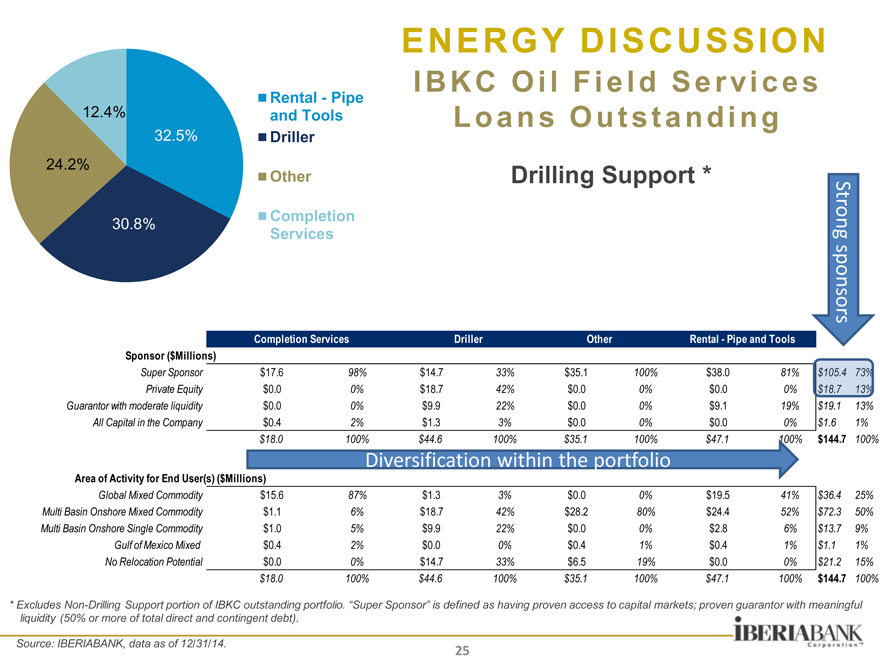

ENERGY DISCUSSION

IBKC Oil Field Services Loans Outstanding

Drilling Support *

Rental—Pipe and Tools Driller

Other

Completion Services

12.4%

32.5%

24.2%

30.8%

Strong sponsors

Completion Services Driller Other Rental—Pipe and Tools

Sponsor ($Millions)

Super Sponsor $17.6 98% $14.7 33% $35.1 100% $38.0 81%

Private Equity $0.0 0% $18.7 42% $0.0 0% $0.0 0%

Guarantor with moderate liquidity $0.0 0% $9.9 22% $0.0 0% $9.1 19% $19.1 13%

All Capital in the Company $0.4 2% $1.3 3% $0.0 0% $0.0 0% $1.6 1%

$18.0 100% $44.6 100% $35.1 100% $47.1 100% $144.7 100%

Diversification within the portfolio

Area of Activity for End User(s) ($Millions)

Global Mixed Commodity $15.6 87% $1.3 3% $0.0 0% $19.5 41% $36.4 25%

Multi Basin Onshore Mixed Commodity $1.1 6% $18.7 42% $28.2 80% $24.4 52% $72.3 50%

Multi Basin Onshore Single Commodity $1.0 5% $9.9 22% $0.0 0% $2.8 6% $13.7 9%

Gulf of Mexico Mixed $0.4 2% $0.0 0% $0.4 1% $0.4 1% $1.1 1%

No Relocation Potential $0.0 0% $14.7 33% $6.5 19% $0.0 0% $21.2 15%

$18.0 100% $44.6 100% $35.1 100% $47.1 100% $144.7 100%

* Excludes Non-Drilling Support portion of IBKC outstanding portfolio. “Super Sponsor” is defined as having proven access to capital markets; proven guarantor with meaningful liquidity (50% or more of total direct and contingent debt).

Source: IBERIABANK, data as of 12/31/14.

25

|

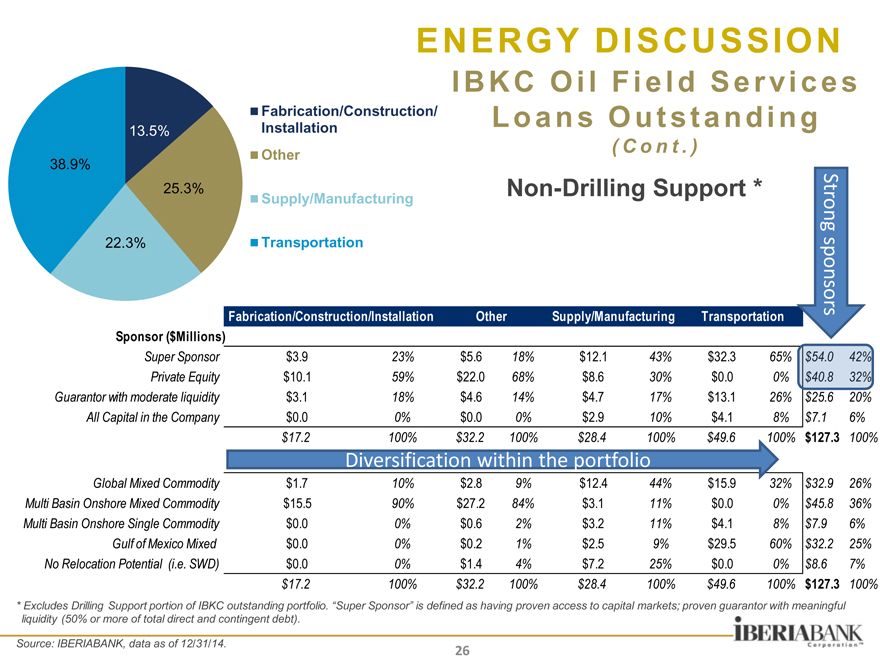

ENERGY DISCUSSION

IBKC Oil Field Services

Fabrication/Construction/ Loans Outstanding Installation

(Cont.)

Other

Supply/Manufacturing Non-Drilling Support * St Transportation rong spon

sors

13.5%

38.9%

25.3%

22.3%

Fabrication/Construction/Installation Other Supply/Manufacturing Transportation

Sponsor ($Millions)

Super Sponsor $3.9 23% $5.6 18% $12.1 43% $32.3 65%

Private Equity $10.1 59% $22.0 68% $8.6 30% $0.0 0%

Guarantor with moderate liquidity $3.1 18% $4.6 14% $4.7 17% $13.1 26% $25.6 20%

All Capital in the Company $0.0 0% $0.0 0% $2.9 10% $4.1 8% $7.1 6%

$17.2 100% $32.2 100% $28.4 100% $49.6 100% $127.3 100%

Diversification within the portfolio

Global Mixed Commodity $1.7 10% $2.8 9% $12.4 44% $15.9 32% $32.9 26%

Multi Basin Onshore Mixed Commodity $15.5 90% $27.2 84% $3.1 11% $0.0 0% $45.8 36%

Multi Basin Onshore Single Commodity $0.0 0% $0.6 2% $3.2 11% $4.1 8% $7.9 6%

Gulf of Mexico Mixed $0.0 0% $0.2 1% $2.5 9% $29.5 60% $32.2 25%

No Relocation Potential (i.e. SWD) $0.0 0% $1.4 4% $7.2 25% $0.0 0% $8.6 7%

$17.2 100% $32.2 100% $28.4 100% $49.6 100% $127.3 100%

* Excludes Drilling Support portion of IBKC outstanding portfolio. “Super Sponsor” is defined as having proven access to capital markets; proven guarantor with meaningful liquidity (50% or more of total direct and contingent debt).

Source: IBERIABANK, data as of 12/31/14.

26

|

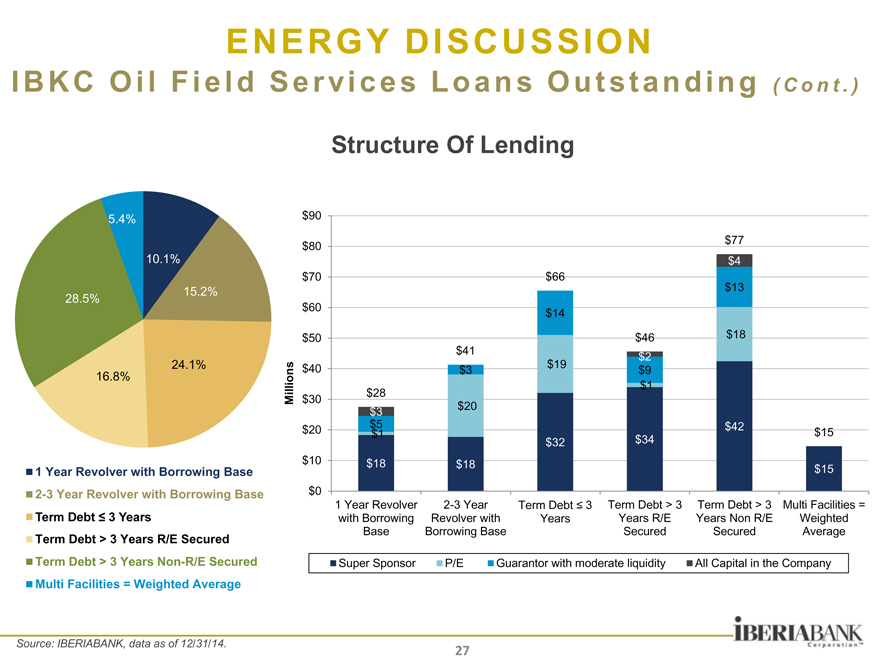

ENERGY DISCUSSION

IBKC Oil Field Services Loans Outstanding ( Cont. )

Structure Of Lending

5.4%

10.1%

15.2%

28.5%

24.1%

16.8%

$90

$80 $77

$4

$70 $66

$13

$60 $14

$50 $46 $18

$41 $2

$40 $3 $19 $9

$1

$30 $28

$3 $20

$20 $$5 1 $42 $ 15

$32 $34

$10 $18 $18 $ 15

$0

1 Year Revolver 2-3 Year Term Debt 3 Term Debt > 3 Term Debt > 3 Multi Facilities =

with Borrowing Revolver with Years Years R/E Years Non R/E Weighted

Base Borrowing Base Secured Secured Average

Millions

1 Year Revolver with Borrowing Base 2-3 Year Revolver with Borrowing Base Term Debt 3 Years Term Debt > 3 Years R/E Secured Term Debt > 3 Years Non-R/E Secured Multi Facilities = Weighted Average

Super Sponsor P/E Guarantor with moderate liquidity All Capital in the Company

Source: IBERIABANK, data as of 12/31/14.

27

|

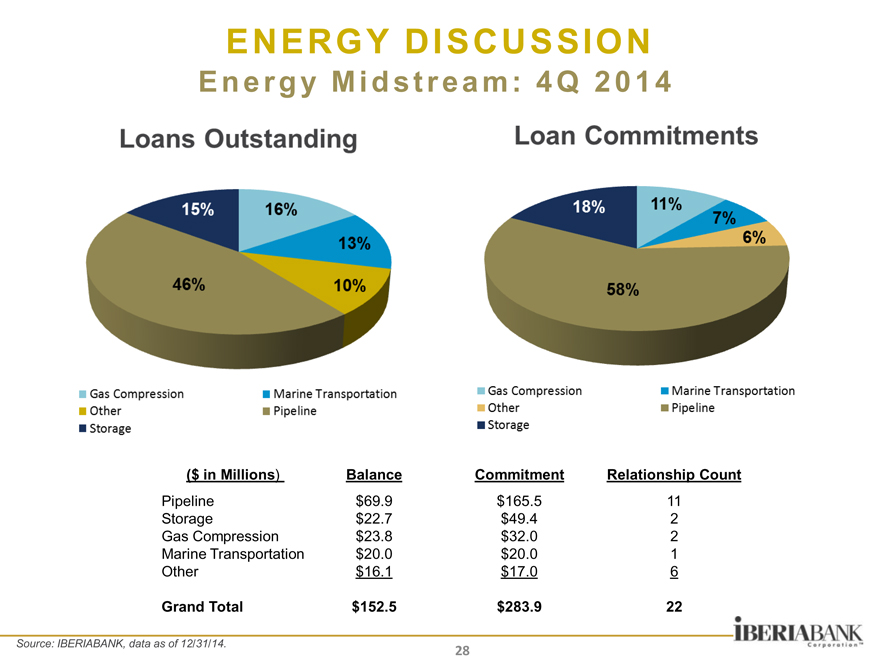

ENERGY DISCUSSION

Energy Midstream: 4Q 2014

($ in Millions) Balance Commitment Relationship Count

Pipeline $69.9 $165.5 11

Storage $22.7 $49.4 2

Gas Compression $23.8 $32.0 2

Marine Transportation $20.0 $20.0 1

Other $16.1 $17.0 6

Grand Total $152.5 $283.9 22

Source: IBERIABANK, data as of 12/31/14.

28

|

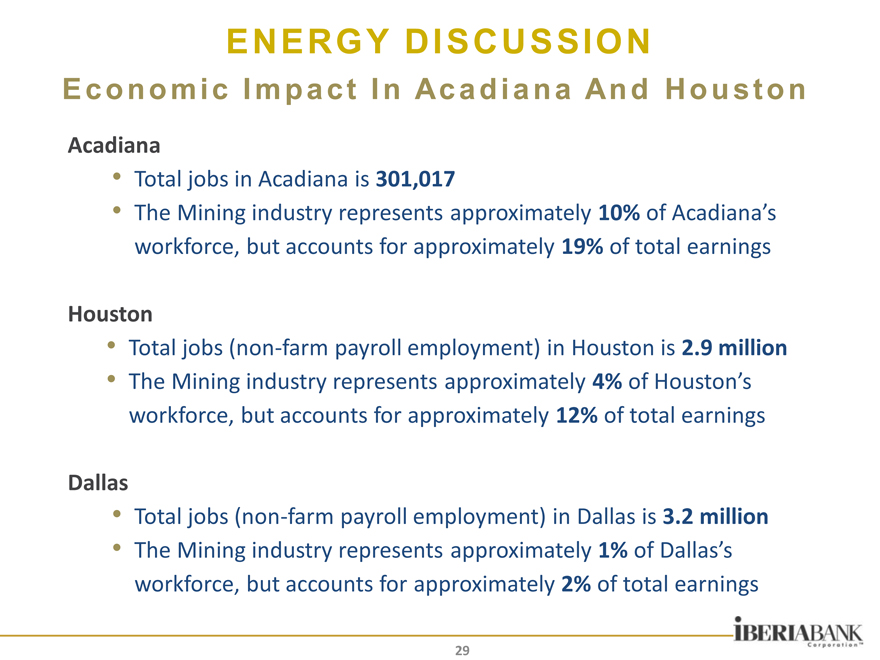

ENERGY DISCUSSION

Economic Impact In Acadiana And Houston

Acadiana

Total jobs in Acadiana is 301,017

The Mining industry represents approximately 10% of Acadiana’s workforce, but accounts for approximately 19% of total earnings

Houston

Total jobs (non farm payroll employment) in Houston is 2.9 million

The Mining industry represents approximately 4% of Houston’s workforce, but accounts for approximately 12% of total earnings

Dallas

Total jobs (non farm payroll employment) in Dallas is 3.2 million

The Mining industry represents approximately 1% of Dallas’s workforce, but accounts for approximately 2% of total earnings

29

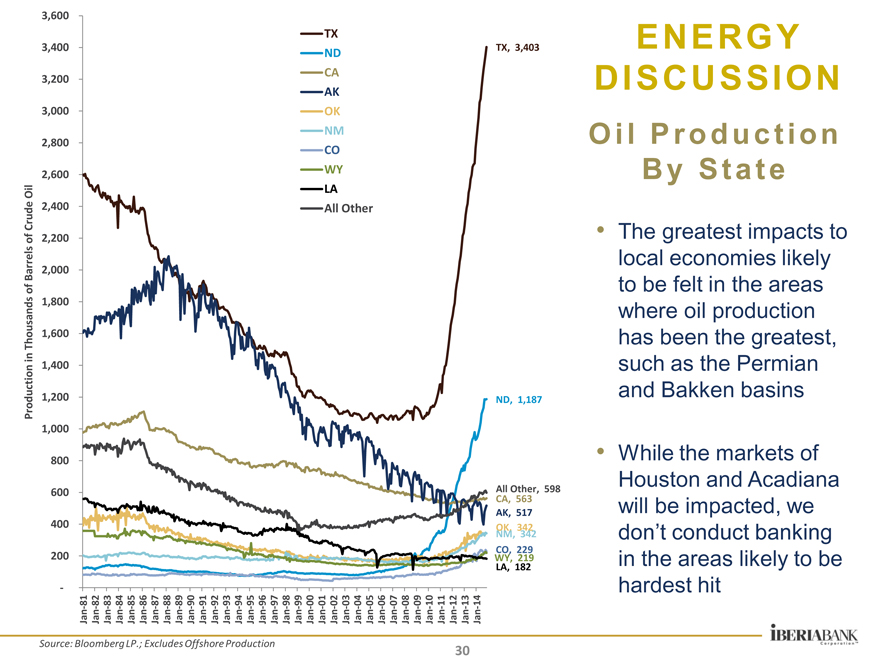

|

3,600

TX

3,400 TX, 3,403

ND

3,200 CA

AK

3,000 OK

NM

2,800

CO

2,600 WY

l

Oi LA

Crude

2,400 All Other

2,200

of

Barrels 2,000

of

1,800

Thousands 1,600

in

on 1,400

Producti 1,200 ND, 1,187

1,000

800

600 All Other, 598

CA, 563

AK, 517

400 OK, 342

NM, 342

CO, 229

200 WY, 219

LA, 182

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan

Source: Bloomberg LP.; Excludes Offshore Production 30

|

ENERGY DISCUSSION

Oil Production By State

The greatest impacts to local economies likely to be felt in the areas where oil production has been the greatest, such as the Permian and Bakken basins

While the markets of Houston and Acadiana will be impacted, we don’t conduct banking in the areas likely to be hardest hit

|

ENERGY DISCUSSION

Economic Impact In Texas

The Company follows five economists that make employment and economic impact forecasts. These forecasts cover the entire Texas economy as well as the Houston and Dallas markets specifically.

Despite the drop in commodity prices and the resulting job losses, each of the forecasts projects job growth for Texas, Dallas, and Houston.

Dallas is likely the least affected by the commodity price decline. Many Dallas industries (such as trucking, transportation, and distribution) will likely experience a positive benefit from the decline in energy prices.

Houston will likely experience a decline in the number of mining-related jobs and a large drop in mining payrolls. This drop will be cushioned by other industries that have previously had difficulty in filling positions and the growth in industrial construction-related job growth. As a result, Houston is still projected to add jobs in both 2015 and 2016.

To date, these Texas markets have not experienced significant issues from layoffs

31

|

ENERGY DISCUSSION

Potential Risk: Non-Owner Occupied RE

Houston

NOO CRE: ~$190 Million

1) Office: ~$50 Million

One ~$20 million commitment. Very strong, very liquid sponsor. Global player.

Next three largest are ~$7 million each o Well secured, cash flowing, strong sponsorship, strong tenants.

2) Multi-family: ~$90 Million

Stayed away from the typical deals with the larger national builders that came to market; Risk profile on those transactions falls outside of what we’re comfortable with.

See more risk in Class A apartments; Most of our multi-family in Houston is well stabilized B and C type properties with strong cash flow and strong guarantors.

Where we do have Class A exposure we have an experienced operator with multiple properties in multiple cities. Stabilized rents, solid cash flows and deposits with us almost equal to loan amounts.

Two ~$20 million exposure, five in the ~$5 million to ~$9 million range.

3) Retail: ~$30 Million

Largest is ~$8 million. Owner occupied, well established business with national customer base. Good liquidity and cash flow.

4) Nursing Homes: ~$8 Million

Lafayette Area

NOO CRE: ~$140 Million

1) Office: ~$35 Million

~$10 million, single credit tenant. Long lease, not energy related

~$10 million, multi-tenant in which IBKC has an office and naming

~$3 million well leased and cash flowing

2) Hotel: ~$20 Million with the largest being:

~$8 million, fully funded. Cash flowing well. Good guarantor liquidity. Some risk of increased vacancy with energy stress.

~$4 million, some susceptibility to energy price declines

$0 outstanding, $9 million commitment on new project for 2016 delivery; 65% LTV, strong guarantor

3) Residential / Lot Development: ~$10 Million:

Firm take-out commitments from national and regional home builders but speculative. Strong guarantors. Loan to value conservative.

32

|

ENERGY DISCUSSION

Potential Risk: State and Local Governments

We have examined our exposure to the state and municipal’s declining tax and royalty revenues

Louisiana

Approximately 13% of state revenues linked to oil and gas

Some exposure to hospitals, nursing homes, as well some road contractors:

that money flows through the state but generally these are dollars flowing from the federal government and are dedicated and should not be affected by lower royalties and taxes.

Don’t have a direct exposure to higher education in Louisiana or Texas, which will likely see some cuts. Could have some residual impact on employment

Have a couple of small relationships with real estate leased to the State of Louisiana where leases are expiring within the next couple of years.

We looked at our exposure to some of the smaller municipalities in Louisiana and their sales tax, excess revenue and utilities exposure, and stressed their revenues by 25% and they all have sufficient cash flow to service the debt.

Reviewed in depth Louisiana municipal exposure in investment portfolio; minimal exposure. Sold $1.4 million in bonds in Feb 2015 to eliminate those we had any potential concerns with, for a gain

Texas

Approximately 10% of state revenues linked to oil and gas

We do not have any loans to municipalities in Texas.

At 12/31/14 = $99 million of Texas Municipal Exposure / 98% General Obligation Issues / 83% carry 3rd party Credit Enhancement / $7.6 million considered “Exposed” to Oil and Gas

Sold $1.1 million of Municipal Bonds out of $7.6 million considered “Exposed” to oil and gas in Feb 2015 for small gain. Eliminates all uninsured Municipal Bonds deemed “Exposed” to Oil and Gas.

33

|

ENERGY DISCUSSION

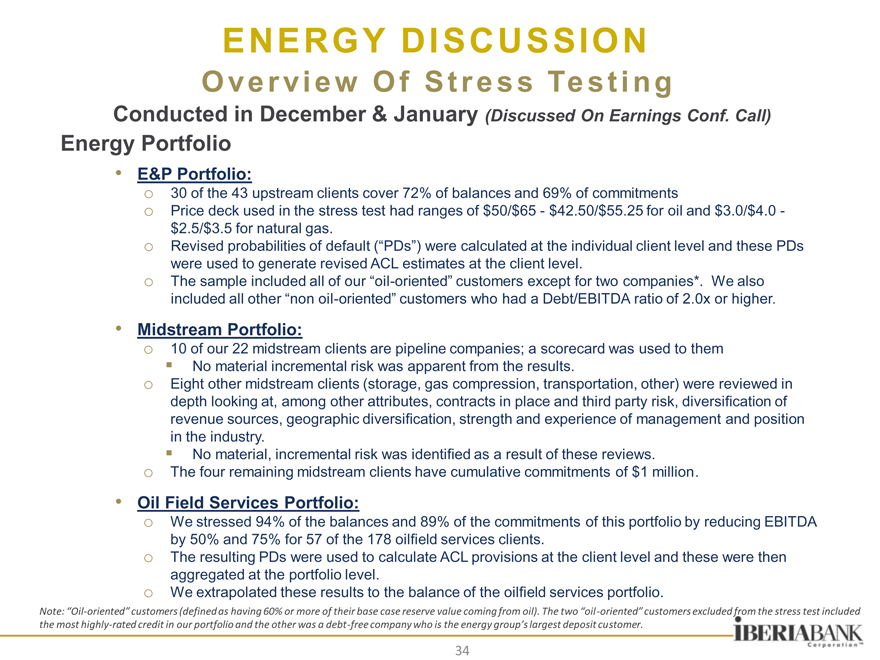

Overview Of Stress Testing

Conducted in December & January (Discussed On Earnings Conf. Call)

Energy Portfolio

E&P Portfolio: o 30 of the 43 upstream clients cover 72% of balances and 69% of commitments o Price deck used in the stress test had ranges of $50/$65—$42.50/$55.25 for oil and $3.0/$4.0 -$2.5/$3.5 for natural gas. o Revised probabilities of default (“PDs”) were calculated at the individual client level and these PDs were used to generate revised ACL estimates at the client level. o The sample included all of our “oil-oriented” customers except for two companies*. We also included all other “non oil-oriented” customers who had a Debt/EBITDA ratio of 2.0x or higher.

Midstream Portfolio: o 10 of our 22 midstream clients are pipeline companies; a scorecard was used to them No material incremental risk was apparent from the results. o Eight other midstream clients (storage, gas compression, transportation, other) were reviewed in depth looking at, among other attributes, contracts in place and third party risk, diversification of revenue sources, geographic diversification, strength and experience of management and position in the industry.

No material, incremental risk was identified as a result of these reviews. o The four remaining midstream clients have cumulative commitments of $1 million.

Oil Field Services Portfolio: o We stressed 94% of the balances and 89% of the commitments of this portfolio by reducing EBITDA by 50% and 75% for 57 of the 178 oilfield services clients. o The resulting PDs were used to calculate ACL provisions at the client level and these were then aggregated at the portfolio level. o We extrapolated these results to the balance of the oilfield services portfolio.

Note: “Oil oriented” customers (defined as having 60% or more of their base case reserve value coming from oil). The two “oil oriented” customers excluded from the stress test included the most highly rated credit in our portfolio and the other was a debt free company who is the energy group’s largest deposit customer.

34

|

ENERGY DISCUSSION

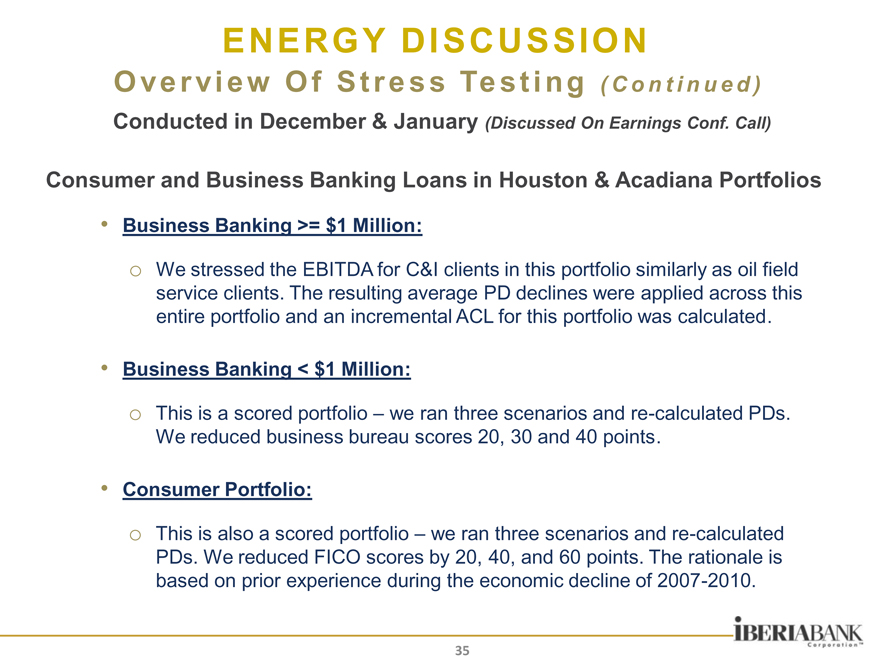

Overview Of Stress Testing ( Continued )

Conducted in December & January (Discussed On Earnings Conf. Call)

Consumer and Business Banking Loans in Houston & Acadiana Portfolios

Business Banking >= $1 Million: o We stressed the EBITDA for C&I clients in this portfolio similarly as oil field service clients. The resulting average PD declines were applied across this entire portfolio and an incremental ACL for this portfolio was calculated.

Business Banking < $1 Million: o This is a scored portfolio – we ran three scenarios and re-calculated PDs.

We reduced business bureau scores 20, 30 and 40 points.

Consumer Portfolio: o This is also a scored portfolio – we ran three scenarios and re-calculated PDs. We reduced FICO scores by 20, 40, and 60 points. The rationale is based on prior experience during the economic decline of 2007-2010.

35

|

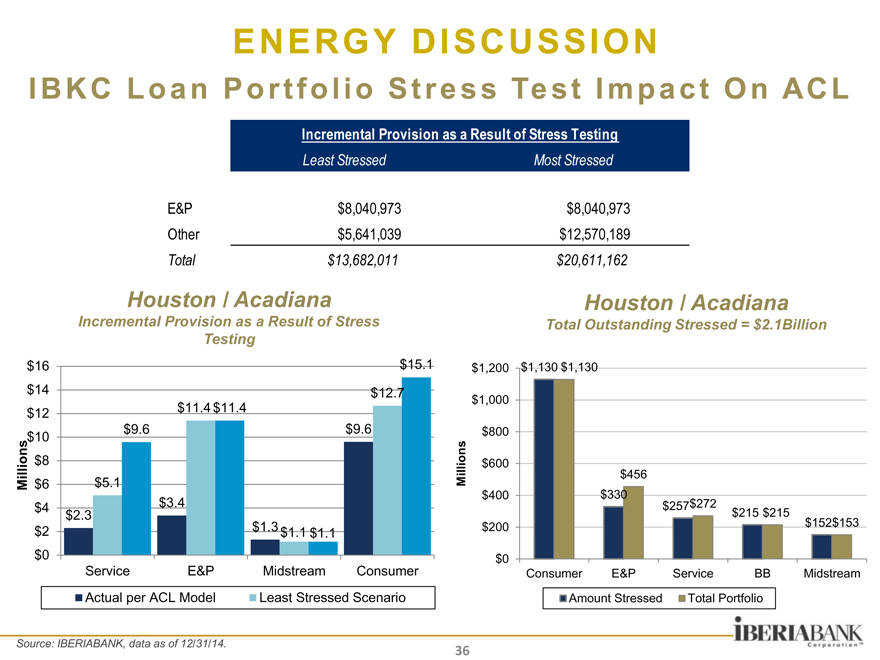

ENERGY DISCUSSION

IBKC Loan Portfolio Stress Test Impact On ACL

Incremental Provision as a Result of Stress Testing

Least Stressed Most Stressed

E&P $8,040,973 $8,040,973 Other $5,641,039 $12,570,189

Total $13,682,011 $20,611,162

Houston / Acadiana Houston / Acadiana

Incremental Provision as a Result of Stress Total Outstanding Stressed = $2.1Billion Testing

$16 $15.1

$14 $12.7

$12 $11.4 $11.4

$10 $9.6 $9.6

lions $8

Mil $6 $5.1

$4 $3.4

$2.3

$2 $1.3 $1.1 $1.1

$0

Service E&P Midstream Consumer

Actual per ACL Model Least Stressed Scenario

$1,200 $1,130 $1,130

$1,000

$800

lions $600

Mil $456

$400 $330

$257$272 $215 $215

$200 $152$153

$0

Consumer E&P Service BB Midstream

Amount Stressed Total Portfolio

Source: IBERIABANK, data as of 12/31/14.

36

|

ENERGY DISCUSSION

IBERIA Capital Partners

Energy Investment Banking Themes

“Finger on the Pulse”

Houston Versus Lafayette

Conversations Between E&P and Oilfield Service Companies

Decreasing Service Costs

Conversations Between Industry and Buyside / Sellside

Capital Availability

M&A

Not All Companies Are Created Equal

Basins

Strategies

Management Teams

37

|

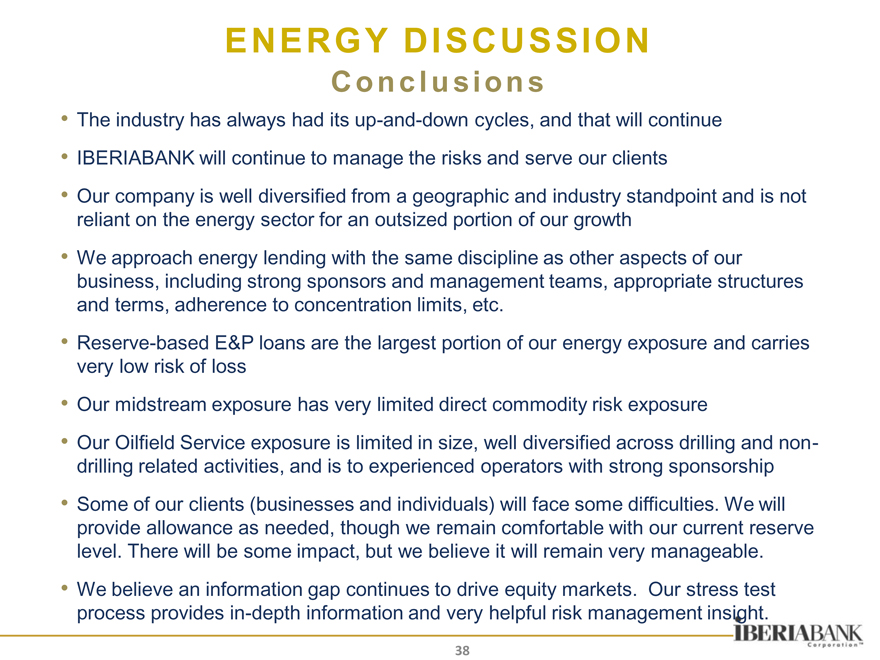

ENERGY DISCUSSION

Conclusions

The industry has always had its up-and-down cycles, and that will continue

IBERIABANK will continue to manage the risks and serve our clients

Our company is well diversified from a geographic and industry standpoint and is not reliant on the energy sector for an outsized portion of our growth

We approach energy lending with the same discipline as other aspects of our business, including strong sponsors and management teams, appropriate structures and terms, adherence to concentration limits, etc.

Reserve-based E&P loans are the largest portion of our energy exposure and carries very low risk of loss

Our midstream exposure has very limited direct commodity risk exposure

Our Oilfield Service exposure is limited in size, well diversified across drilling and non-drilling related activities, and is to experienced operators with strong sponsorship

Some of our clients (businesses and individuals) will face some difficulties. We will provide allowance as needed, though we remain comfortable with our current reserve level. There will be some impact, but we believe it will remain very manageable.

We believe an information gap continues to drive equity markets. Our stress test process provides in-depth information and very helpful risk management insight.

38

|

INITIATIVES UPDATE

“Things do not change, we do.

-Henry David “ Thoreau

39

|

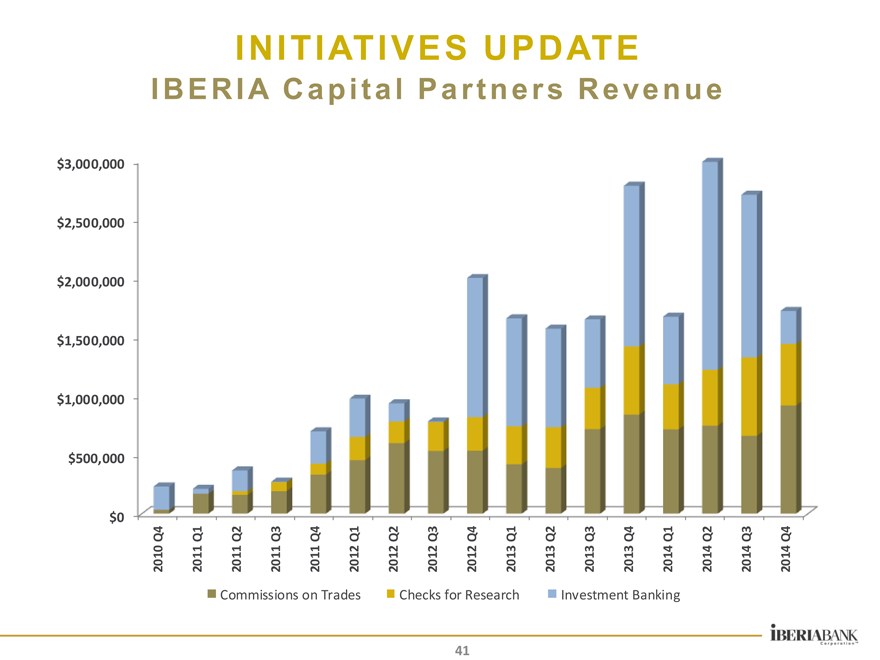

INITIATIVES UPDATE

IBERIA Capital Partners Investment

IBERIA Capital Partners (“ICP”) created in October 2010 with receipt of its broker dealer license

Niche focus on energy related companies

– Exploration & Production, Midstream, Service & Supply, and Shipping

ICP revenue comes from trading, research income and investment banking

35 Full-Time Employees

Current coverage on 79 publicly traded companies

Participated in 58 investment banking transactions since formation

Strong growth in revenues from formation through 3Q14.

Energy commodity price declines in 4Q14 led to significant reduction in investment banking revenue opportunities

– $1 million reduction in revenue compared to 3Q14

40

|

INITIATIVES UPDATE

IBERIA Capital Partners Revenue

$3,000,000 $2,500,000 $2,000,000 $1,500,000 $1,000,000 $500,000 $0

2010 Q4 2011 Q1 2011 Q2 2011 Q3 2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

Commissions on Trades Checks for Research Investment Banking

41

|

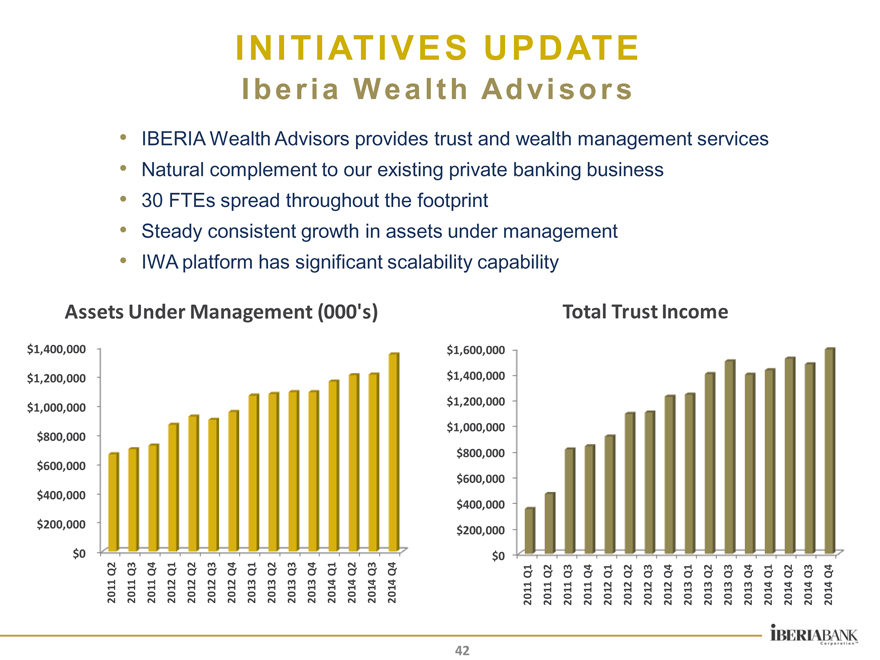

INITIATIVES UPDATE

Iberia Wealth Advisors

IBERIA Wealth Advisors provides trust and wealth management services

Natural complement to our existing private banking business

30 FTEs spread throughout the footprint

Steady consistent growth in assets under management

IWA platform has significant scalability capability

Total Trust Income

$1,600,000 $1,400,000 $1,200,000 $1,000,000 $800,000 $600,000 $400,000 $200,000 $0

2011 Q1 2011 Q2 2011 Q3 2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

Assets Under Management (000’s)

$1,400,000 $1,200,000 $1,000,000 $800,000 $600,000 $400,000 $200,000 $0

2011 Q2 2011 Q3 2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

42

|

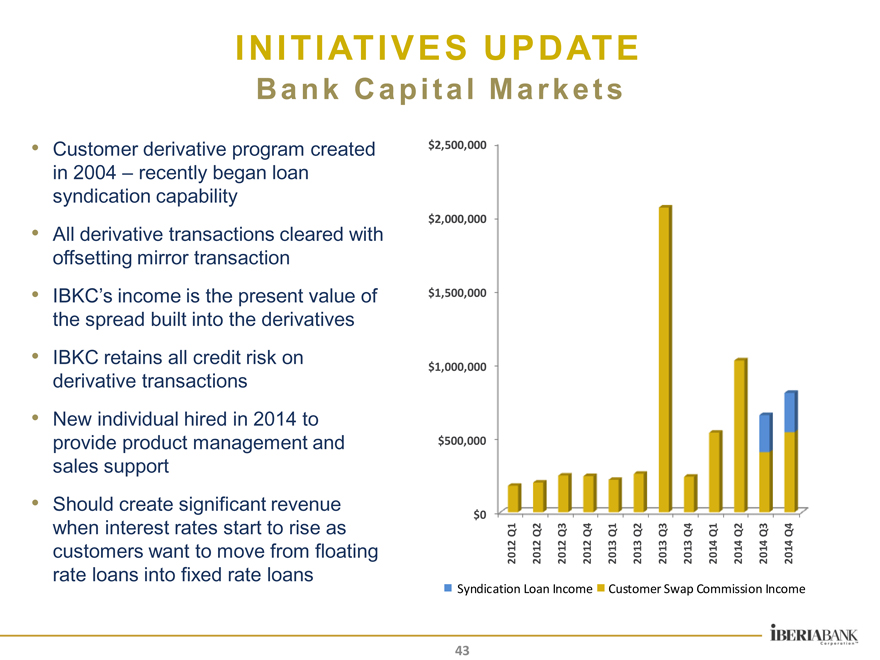

INITIATIVES UPDATE

Bank Capital Markets

Customer derivative program created in 2004 – recently began loan syndication capability

All derivative transactions cleared with offsetting mirror transaction

IBKC’s income is the present value of the spread built into the derivatives

IBKC retains all credit risk on derivative transactions

New individual hired in 2014 to provide product management and sales support

Should create significant revenue when interest rates start to rise as customers want to move from floating rate loans into fixed rate loans

$2,500,000 $2,000,000 $1,500,000 $1,000,000 $500,000 $0

2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

Syndication Loan Income Customer Swap Commission Income

43

|

INITIATIVES UPDATE

Business Banking Investment

Bankers

– Hired experienced Business Bankers

– Implemented performance management process

Business Loan Center

– Relationships $2MM and under

– Hired experienced management and underwriting team

– Implemented enhanced portfolio management systems and processes

Infrastructure

– Implemented Banker’s sales management environment

– New incentive plan and pricing model

Deposits and Fees

– Business Checking product development and marketing plan

– New Merchant Services provider

– Partnership with Treasury Management

– New Credit Card processor

44

|

INITIATIVES UPDATE

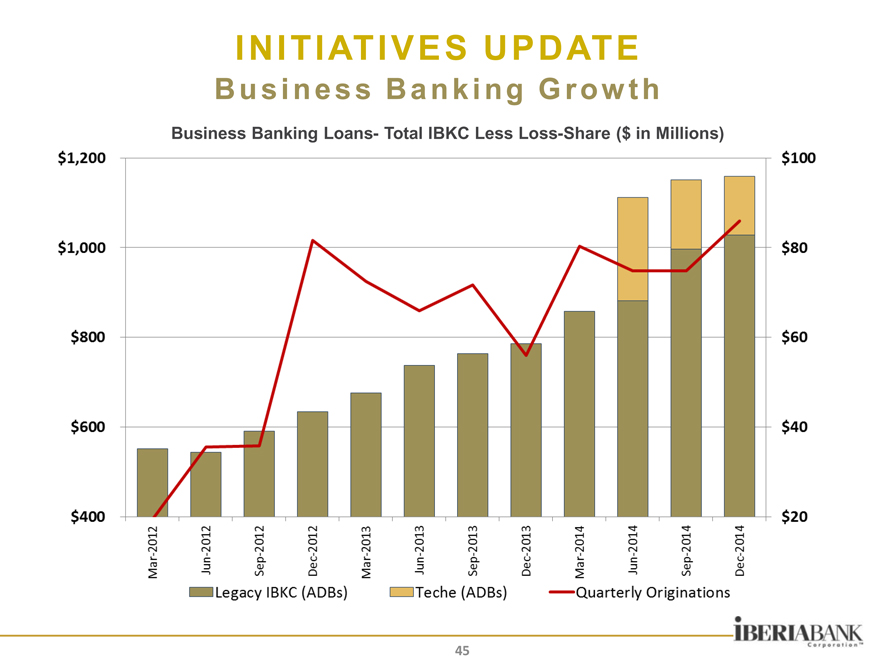

Business Banking Growth

Business Banking Loans- Total IBKC Less Loss-Share ($ in Millions)

45

|

INITIATIVES UPDATE

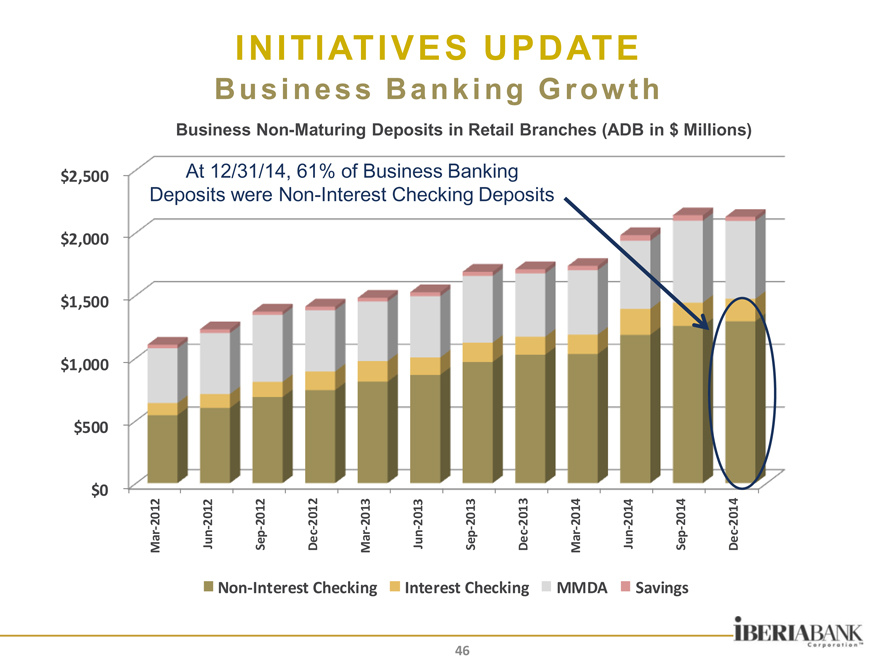

Business Banking Growth

Business Non-Maturing Deposits in Retail Branches (ADB in $ Millions)

$2,500 At 12/31/14, 61% of Business Banking

Deposits were Non-Interest Checking Deposits

$2,000

$1,500

$1,000

$500

$0

2012 2012 2012 2012 2013 2013 2013 2013 2014 2014 2014 2014

Jun Dec Jun Dec Jun Dec

Mar Sep Mar Sep Mar Sep

Non Interest Checking Interest Checking MMDA Savings

46

|

INITIATIVES UPDATE

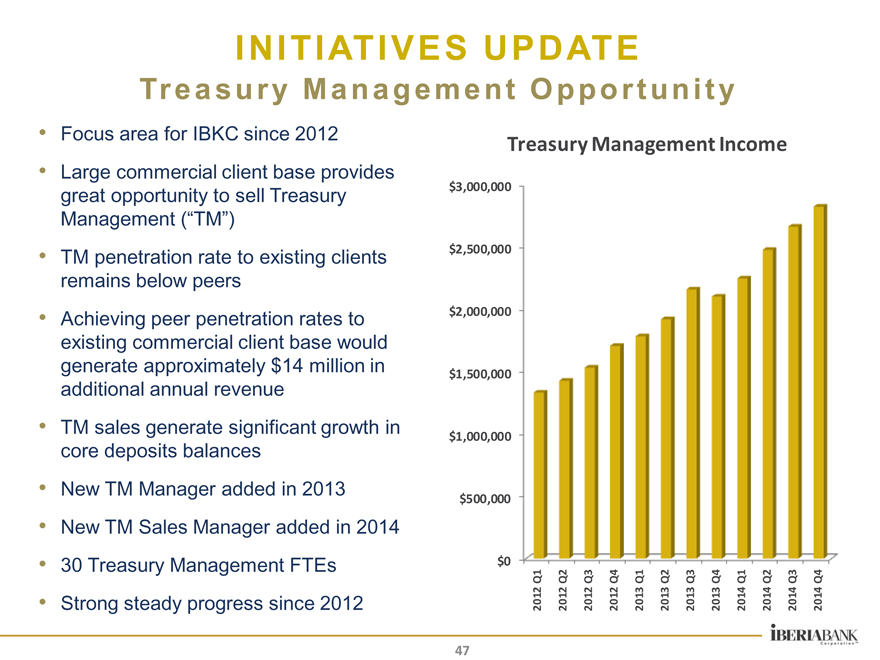

Treasury Management Opportunity

Focus area for IBKC since 2012

Large commercial client base provides great opportunity to sell Treasury Management (“TM”)

TM penetration rate to existing clients remains below peers

Achieving peer penetration rates to existing commercial client base would generate approximately $14 million in additional annual revenue

TM sales generate significant growth in core deposits balances

New TM Manager added in 2013

New TM Sales Manager added in 2014

30 Treasury Management FTEs

Strong steady progress since 2012

Treasury Management Income

$3,000,000 $2,500,000 $2,000,000 $1,500,000 $1,000,000 $500,000 $0

2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4 2014 Q1 2014 Q2 2014 Q3 2014 Q4

47

|

MARKETS & GROWTH

I skate where the puck is going “to be, not where it has been.”

-Wayne Gretzky

48

|

MARKETS

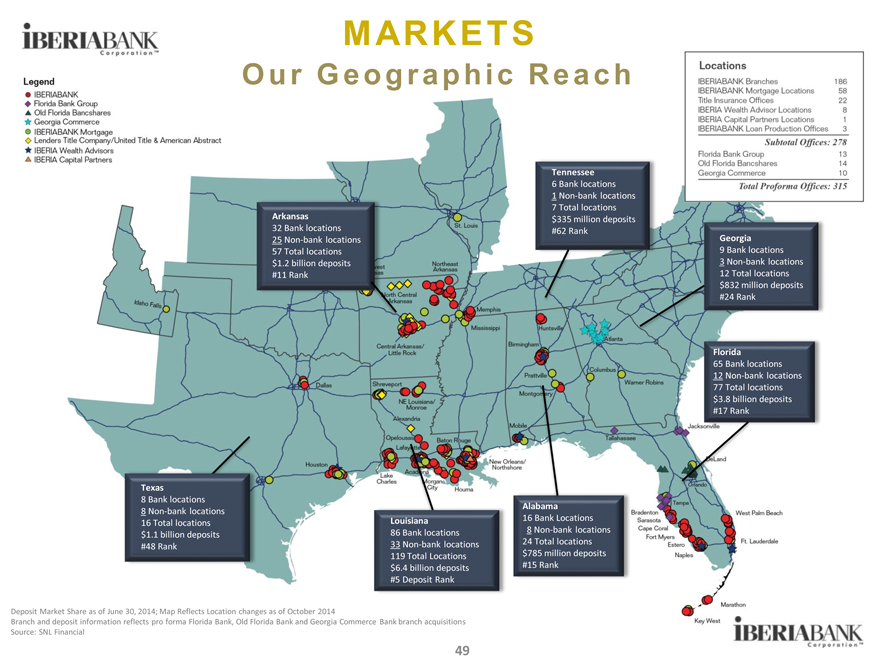

Our Geographic Reach

Arkansas

32 Bank locations

25 Non bank locations

57 Total locations

$1.2 billion deposits #11 Rank

Tennessee

6 Bank locations

1 Non bank locations

7 Total locations $335 million deposits #62 Rank

Georgia

9 Bank locations

3 Non bank locations

12 Total locations $832 million deposits #24 Rank

Florida

65 Bank locations

12 Non bank locations

77 Total locations

$3.8 billion deposits #17 Rank

Alabama

16 Bank Locations

8 Non bank locations

24 Total locations $785 million deposits #15 Rank

Louisiana

86 Bank locations

33 Non bank locations 119 Total Locations

$6.4 billion deposits

#5 Deposit Rank

Texas

8 Bank locations

8 Non bank locations

16 Total locations

$1.1 billion deposits #48 Rank

Deposit Market Share as of June 30, 2014; Map Reflects Location changes as of October 2014

Branch and deposit information reflects pro forma Florida Bank, Old Florida Bank and Georgia Commerce Bank branch acquisitions Source: SNL Financial

49

|

MARKETS

Economic Drivers & Trends— States

State Employment Growth Economic Drivers

2013 2018

Alabama 2nd quintile Manufacturing

Agriculture

Defense

Arkansas 2nd quintile Manufacturing

Medical Center

Logistics

Florida 1st quintile Tourism

Retirees

Financial Center

Georgia 1st quintile Manufacturing

Logistics

Defense

Louisiana 4th quintile Energy

Logistics

Tourism

Tennessee 2nd quintile Manufacturing

Logistics

Agriculture

Texas 1st quintile Energy

Manufacturing

Logistics

Source: Moody’s Analytics November 2014

50

|

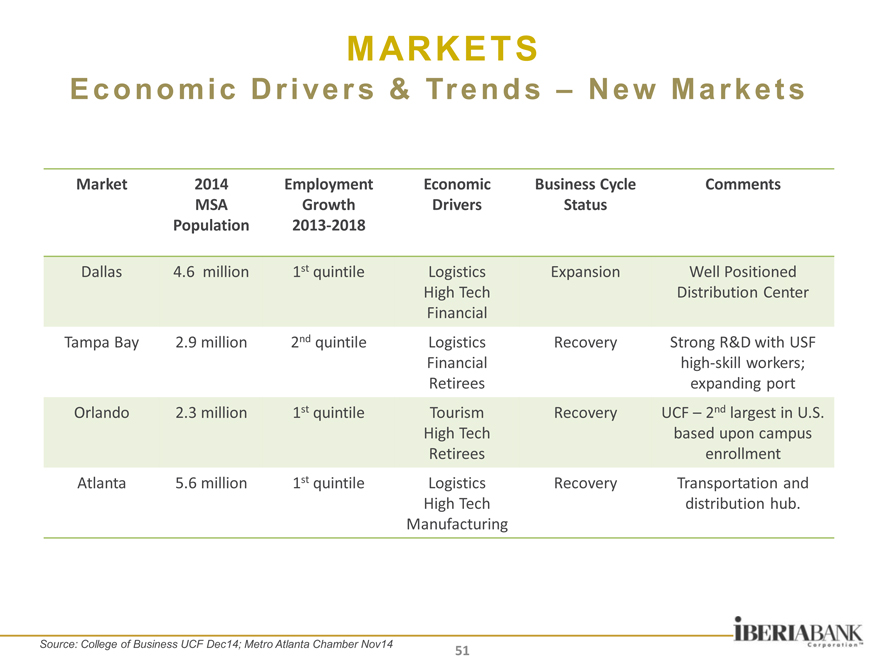

MARKETS

Economic Drivers & Trends – New Markets

Market 2014 Employment Economic Business Cycle Comments

MSA Growth Drivers Status

Population 2013 2018

Dallas 4.6 million 1st quintile Logistics Expansion Well Positioned

High Tech Distribution Center

Financial

Tampa Bay 2.9 million 2nd quintile Logistics Recovery Strong R&D with USF

Financial high skill workers;

Retirees expanding port

Orlando 2.3 million 1st quintile Tourism Recovery UCF – 2nd largest in U.S.

High Tech based upon campus

Retirees enrollment

Atlanta 5.6 million 1st quintile Logistics Recovery Transportation and

High Tech distribution hub.

Manufacturing

Source: College of Business UCF Dec14; Metro Atlanta Chamber Nov14

51

|

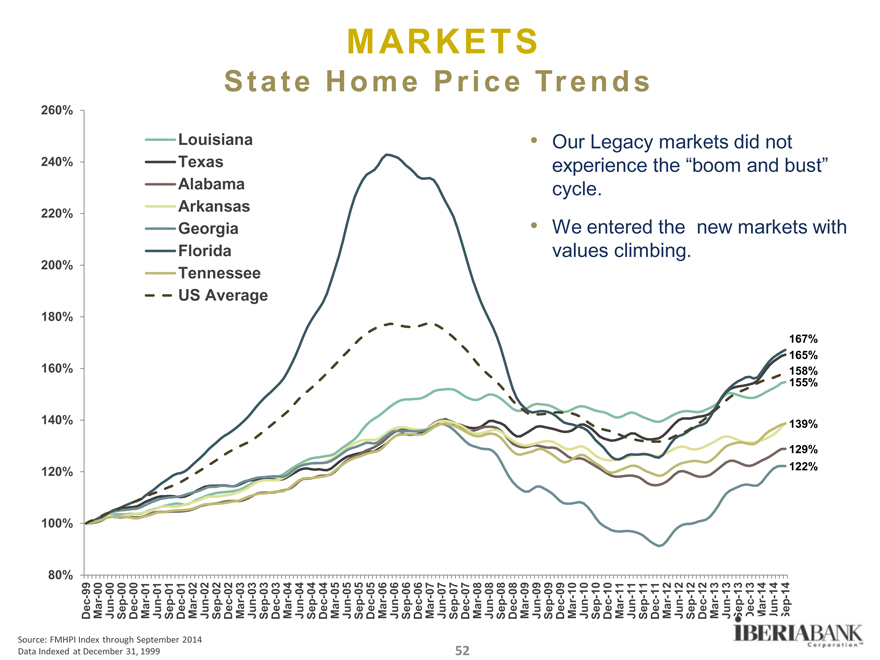

MARKETS

State Home Price Trends

Louisiana Texas Alabama Arkansas Georgia Florida Tennessee US Average

Our Legacy markets did not experience the “boom and bust” cycle.

We entered the new markets with values climbing.

260% 240% 220% 200% 180% 160% 140% 120% 100% 80%

Dec-99

Mar- 00

Jun-00

Sep-00

Dec-00

Mar- 01

Jun-01

Sep-01

Dec-01

Mar- 02

Jun-02

Sep-02

Dec-02

Mar- 03

Jun-03

Sep-03

Dec-03

Mar- 04

Jun-04

Sep-04

Dec-04

Mar- 05

Jun-05

Sep-05

Dec-05

Mar- 06

Jun-06

Sep-06

Dec-06

Mar- 07

Jun-07

Sep-07

Dec-07

Mar- 08

Jun-08

Sep-08

Dec-08

Mar- 09

Jun-09

Sep-09

Dec-09

Mar- 10

Jun-10

Sep-10

Dec-10

Mar- 11

Jun-11

Sep-11

Dec-11

Mar- 12

Jun-12

Sep-12

Dec-12

Mar- 13

Jun-13

Sep-13

Dec-13

Mar- 14

Jun-14

Sep-14

167% 165% 158% 155%

139%

129% 122%

Source: FMHPI Index through September 2014

Data Indexed at December 31, 1999 52

|

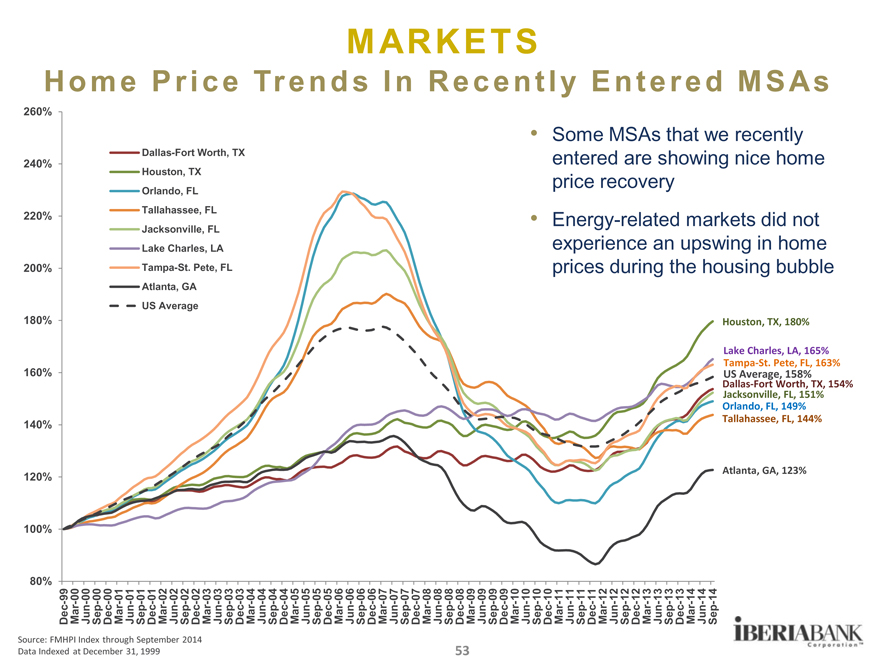

MARKETS

Home Price Trends In Recently Entered MSAs

Dallas-Fort Worth, TX Houston, TX

Orlando, FL Tallahassee, FL Jacksonville, FL Lake Charles, LA Tampa-St. Pete, FL Atlanta, GA US Average

260% 240% 220% 200% 180% 160% 140% 120% 100% 80%

Some MSAs that we recently entered are showing nice home price recovery

Energy-related markets did not experience an upswing in home prices during the housing bubble

Houston, TX, 180%

Lake Charles, LA, 165% Tampa St. Pete, FL, 163%

US Average, 158%

Dallas Fort Worth, TX, 154% Jacksonville, FL, 151% Orlando, FL, 149% Tallahassee, FL, 144%

Atlanta, GA, 123%

Dec-99 Mar-00 Jun-00 Sep-00 Dec-00 Mar-01 Jun-01 Sep-01 Dec-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 Jun-05 Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Source: FMHPI Index through September 2014

Data Indexed at December 31, 1999 53

|

MARKETS

IBKC MSAs – Unemployment Rates

IBKC MSAs – Unemployment

9.4%

7.6%

6.7%

9.2%

9.1%

7.0%

7.1%

8.2%

10.3%

9.7%

6.8%

8.5%

9.6%

10.5%

10.2%

8.3%

9.9%

9.6%

6.9%

7.3%

7.0%

7.5%

5.3%

4.9%

7.6%

7.3%

6.2%

58% of markets have unemployment below the US average

Markets entered via FDIC assisted acquisitions

** Markets to be entered via pending acquisitions of Florida Bank Group, Old Florida Bancshares, and Georgia Commerce Bancshares

Source: BLS Unemployment Rate Seasonally Adjusted

54

|

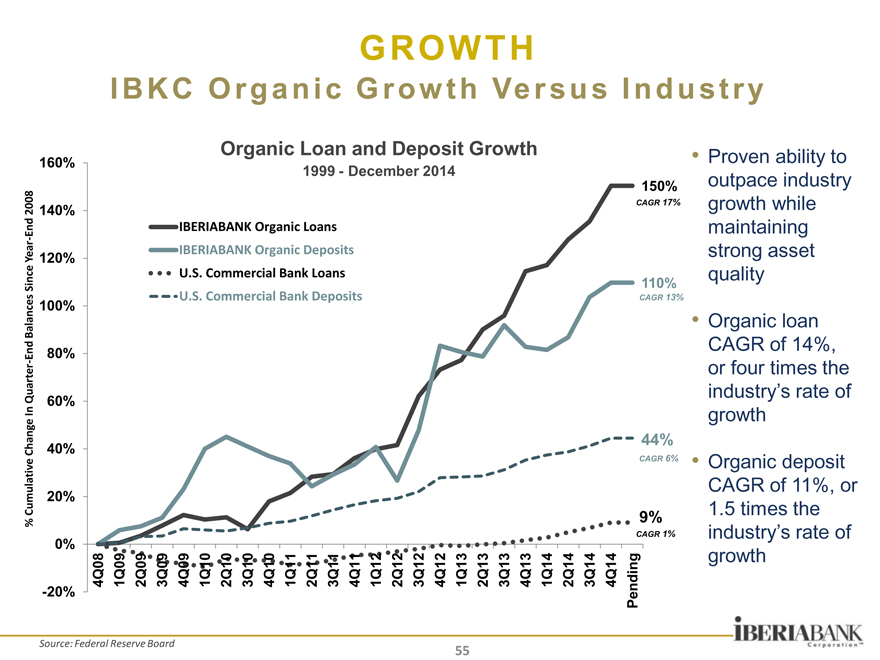

GROWTH

IBKC Organic Growth Versus Industry

% Cumulati ve Change In Quar ter End Balances Si nce Year End 2008

- 20% 40% 60% 80% 100% 120% 140% 160% 20% 0%

Organic Loan and Deposit Growth

1999—December 2014

IBERIABANK Organic Loans IBERIABANK Organic Deposits U.S. Commercial Bank Loans U.S. Commercial Bank Deposits

150%

CAGR 17%

110%

CAGR 13%

44%

CAGR 6%

9%

CAGR 1%

Proven ability to outpace industry growth while maintaining strong asset quality

Organic loan CAGR of 14%, or four times the industry’s rate of growth

Organic deposit CAGR of 11%, or 1.5 times the industry’s rate of growth

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14 Pending

CAGR

Source: Federal Reserve Board

55

|

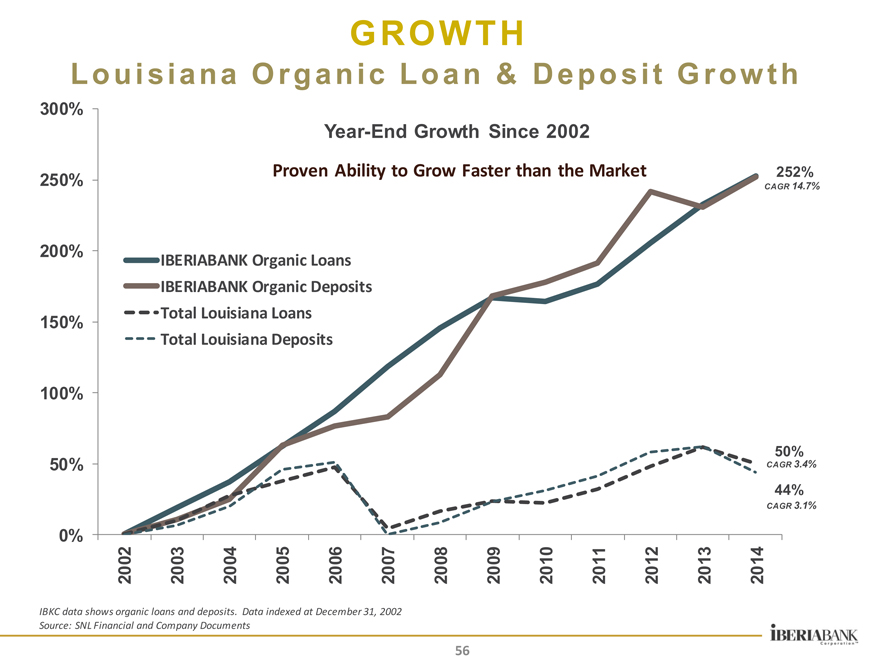

GROWTH

Louisiana Organic Loan & Deposit Growth

Year-End Growth Since 2002

Proven Ability to Grow Faster than the Market

300%

250%

200%

150%

100%

50%

0%

IBERIABANK Organic Loans IBERIABANK Organic Deposits Total Louisiana Loans Total Louisiana Deposits

252%

CAGR 14.7%

50%

CAGR 3.4%

44%

CAGR 3.1%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

IBKC data shows organic loans and deposits. Data indexed at December 31, 2002 Source: SNL Financial and Company Documents

56

|

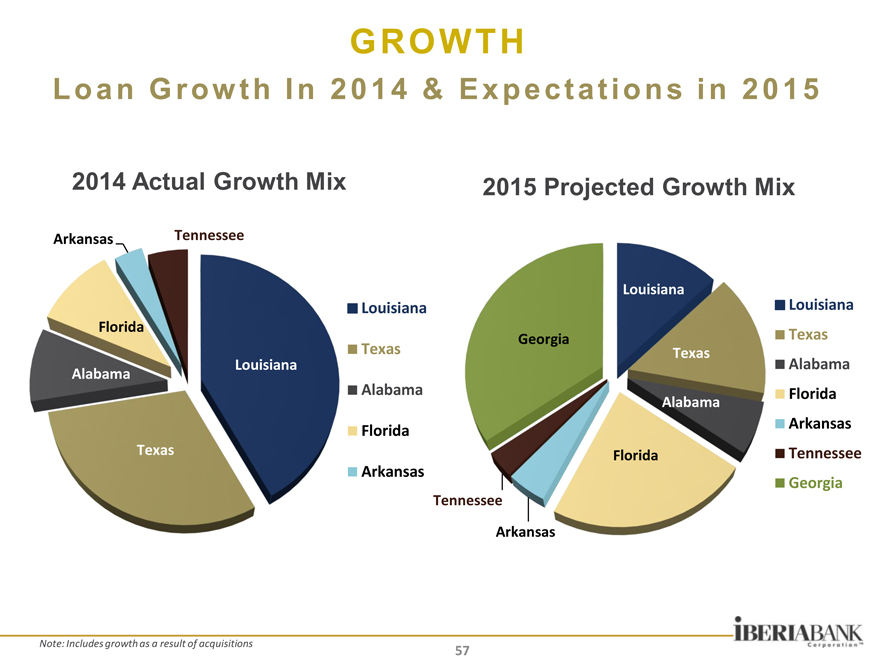

GROWTH

Loan Growth In 2014 & Expectations in 2015

2014 Actual Growth Mix 2015 Projected Growth Mix

Arkansas Tennessee

Florida

Louisiana Alabama

Texas

Louisiana Texas Alabama Florida Arkansas

Louisiana

Georgia

Texas Alabama Florida

Louisiana Texas Alabama Florida Arkansas Tennessee Georgia

Tennessee

Arkansas

Note: Includes growth as a result of acquisitions

57

|

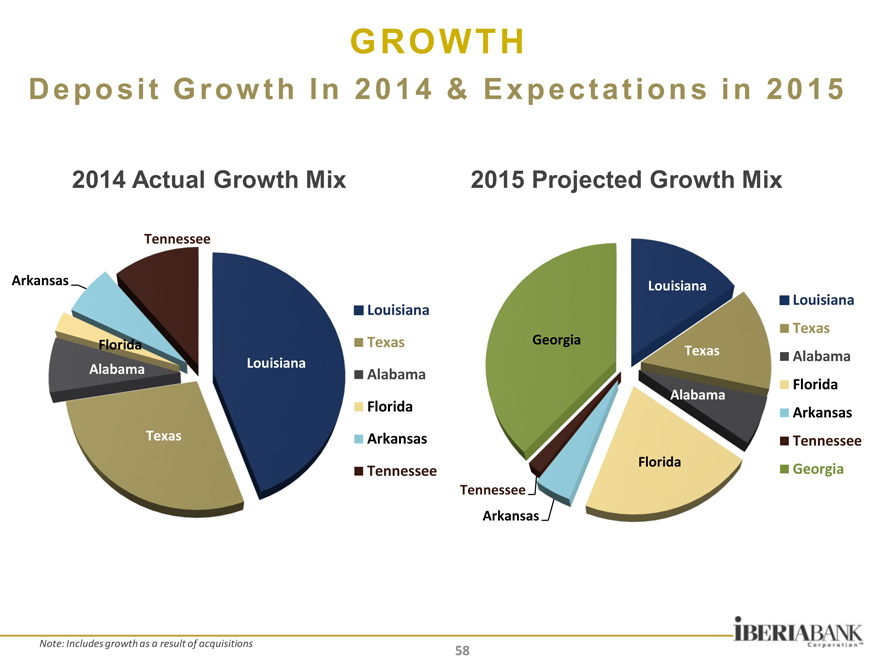

GROWTH

Deposit Growth In 2014 & Expectations in 2015

2014 Actual Growth Mix 2015 Projected Growth Mix

Tennessee

Arkansas Louisiana

Louisiana

Louisiana

Texas

Florida Texas Georgia

Texas Alabama

Alabama Louisiana Alabama

Florida

Alabama

Florida Arkansas

Texas Arkansas Tennessee

Florida

Tennessee Georgia

Tennessee

Arkansas

Note: Includes growth as a result of acquisitions 58

|

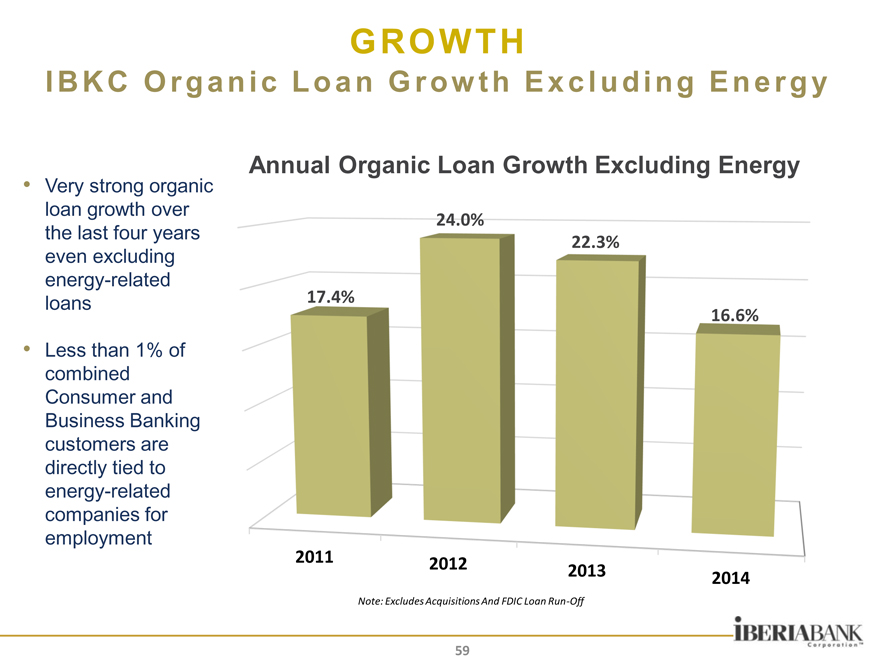

GROWTH

IBKC Organic Loan Growth Excluding Energy

Very strong organic loan growth over the last four years even excluding energy-related loans

Less than 1% of combined Consumer and Business Banking customers are directly tied to energy-related companies for employment

Annual Organic Loan Growth Excluding Energy

24.0%

22.3%

17.4%

16.6%

2011 2012

2013 2014

Note: Excludes Acquisitions And FDIC Loan Run Off

59

|

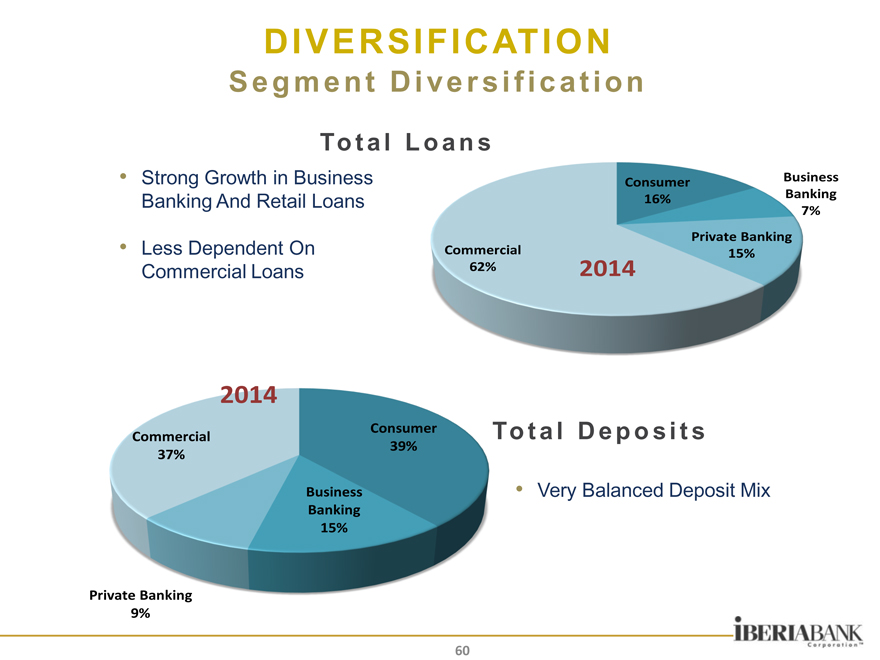

DIVERSIFICATION

Segment Diversification

To t a l L o a n s

Strong Growth in Business Banking And Retail Loans

Less Dependent On Commercial Loans

Consumer Business

16% Banking

7%

Private Banking

Commercial 15%

62% 2014

2014

Consumer Commercial 39% 37%

Business Banking 15%

To t a l D e p o s i t s

Very Balanced Deposit Mix

Private Banking 9%

60

|

DIVERSIFICATION

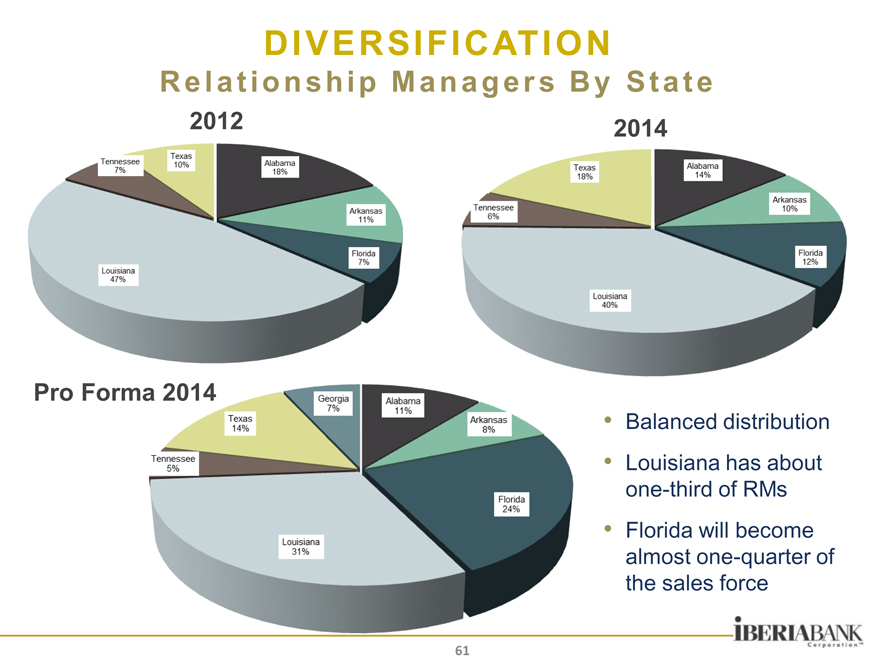

Relationship Managers By State

2012 2014

Pro Forma 2014

Balanced distribution Louisiana has about one-third of RMs Florida will become almost one-quarter of the sales force

61

|

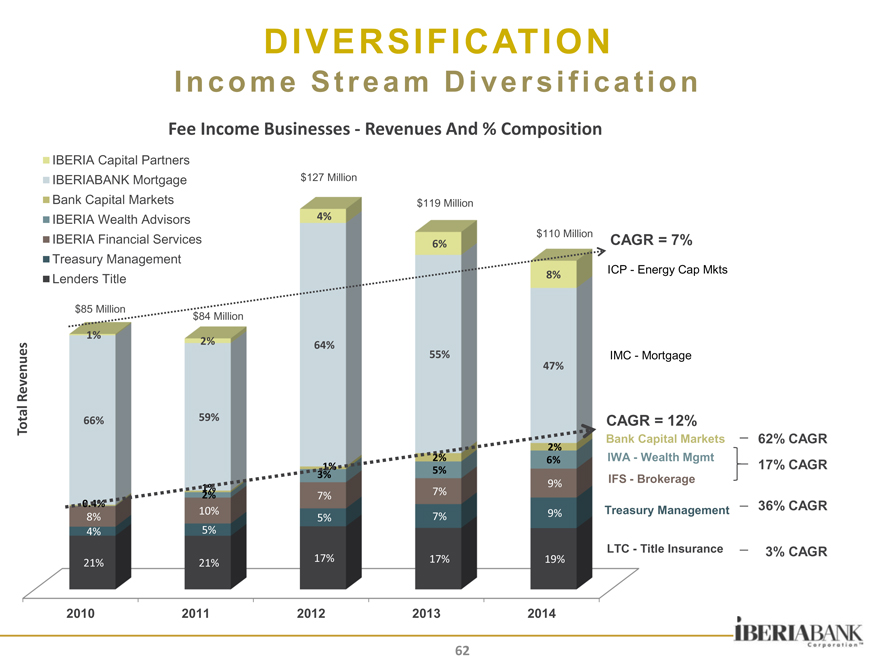

DIVERSIFICATION

I n c o m e S t r e a m D i ve r s i f i c a ti o n

Fee Income Businesses—Revenues And % Composition

IBERIA Capital Partners

IBERIABANK Mortgage $127 Million

Bank Capital Markets $119 Million

IBERIA Wealth Advisors 4%

IBERIA Financial Services $110 Million CAGR = 7%

6%

Treasury Management

ICP—Energy Cap Mkts

Lenders Title 8%

$85 Million

$84 Million

1%

2% 64%

es 55% IMC—Mortgage

enu 47%

Rev

Total 66% 59% CAGR = 12%

Bank Capital Markets 62% CAGR

2%

2% 6% IWA—Wealth Mgmt

1% 5% 17% CAGR

3% IFS—Brokerage

9%

2% 1% 7% 7%

0.4% |

| 10% 9% Treasury Management 36% CAGR |

8% 5% 7%

4% 5%

LTC—Title Insurance 3% CAGR

21% 21% 17% 17% 19%

2010 2011 2012 2013 2014

62

|

DIVERSIFICATION

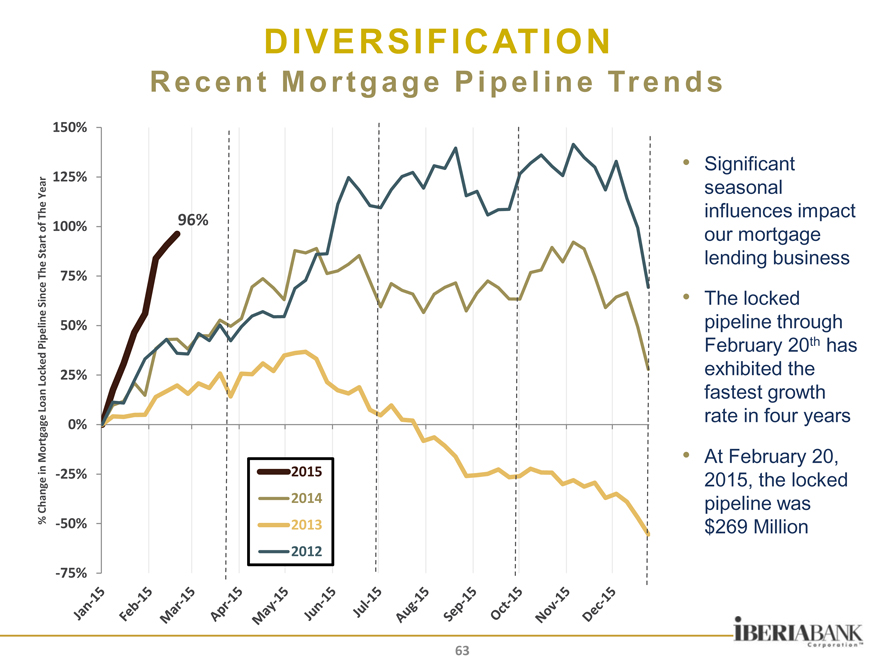

R e c e n t M o r t g a g e P i p e l i n e Tr e n d s

% Change in Mortgage Loan Locked Pipeline Since The Start of The Year

-75% -50% -25% 0% 25% 50% 75% 100% 125% 150%

96%

2012 2013 2014 2015

Significant seasonal influences impact our mortgage lending business

The locked pipeline through February 20th has exhibited the fastest growth rate in four years

At February 20, 2015, the locked pipeline was $269 Million

63

|

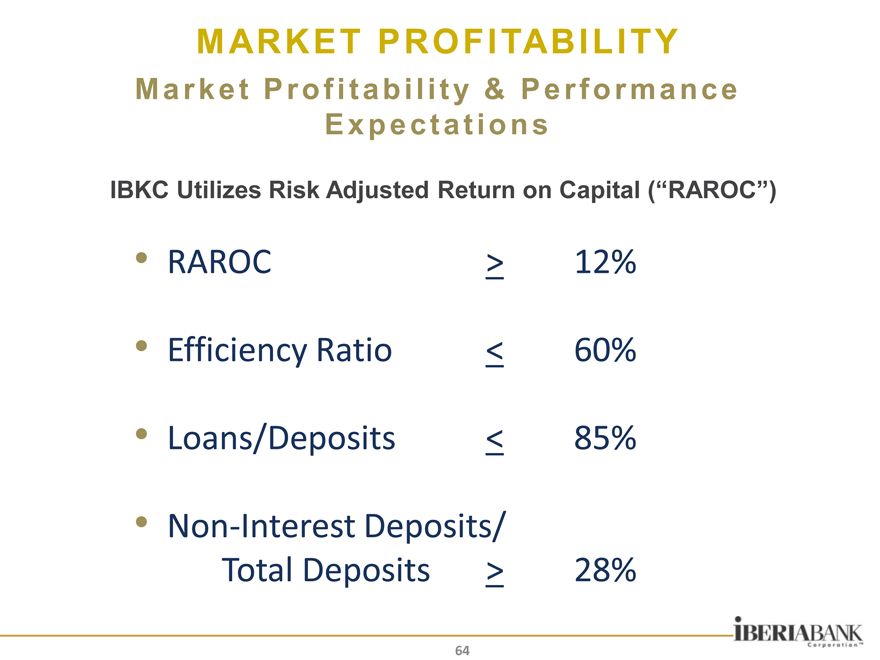

M ARKET PROFITABILITY

M a r k e t P r o f i t a b i l i t y & P e r f o r ma nc e E x p e c t a t i o ns

IBKC Utilizes Risk Adjusted Return on Capital (“RAROC”)

RAROC > 12%

Efficiency Ratio < 60%

Loans/Deposits < 85%

Non-Interest Deposits/

Total Deposits > 28%

64

|

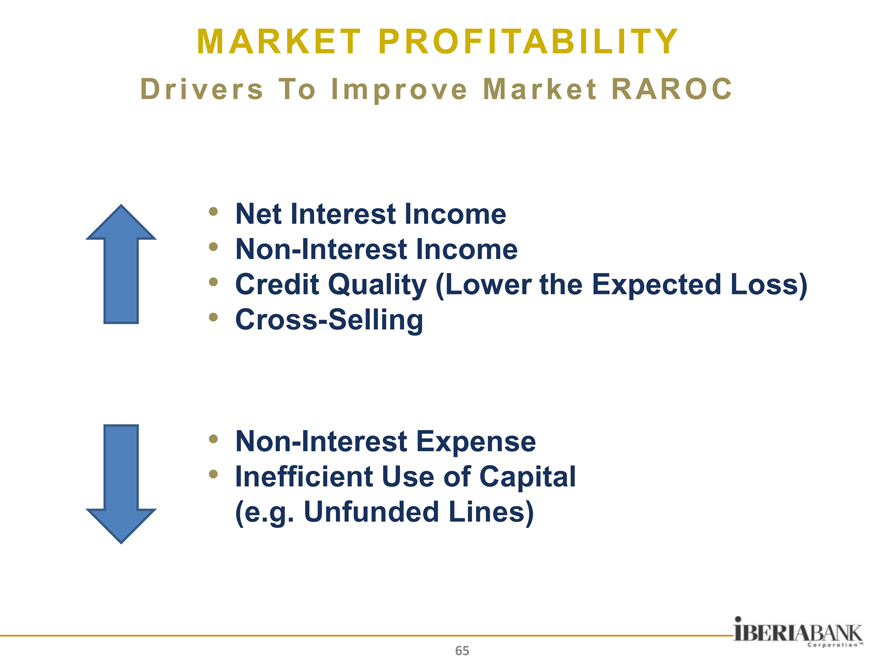

M ARKET PROFITABILITY

D r i ve r s To I m p r o ve M a r k e t R AR O C

Net Interest Income Non-Interest Income

Credit Quality (Lower the Expected Loss) Cross-Selling

Non-Interest Expense Inefficient Use of Capital (e.g. Unfunded Lines)

65

|

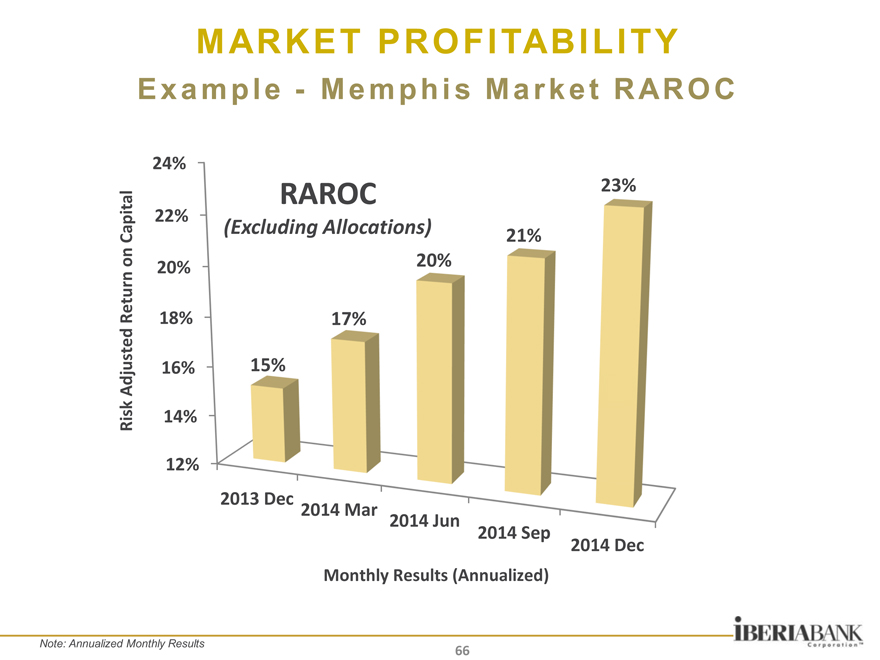

M ARKET PROFITABILITY

E x a m p l e—M e m p h i s M a r k e t R AR O C

24%

RAROC 23%

22%

Capital(Excluding Allocations) 21%

on 20% 20%

turn

Re 18% 17%

d

juste 16% 15%

d

A

isk 14%

R

12%

2013 Dec

2014 Mar 2014 Jun

2014 Sep

2014 Dec

Monthly Results (Annualized)

Note: Annualized Monthly Results

66

|

M ARKET PROFITABILITY

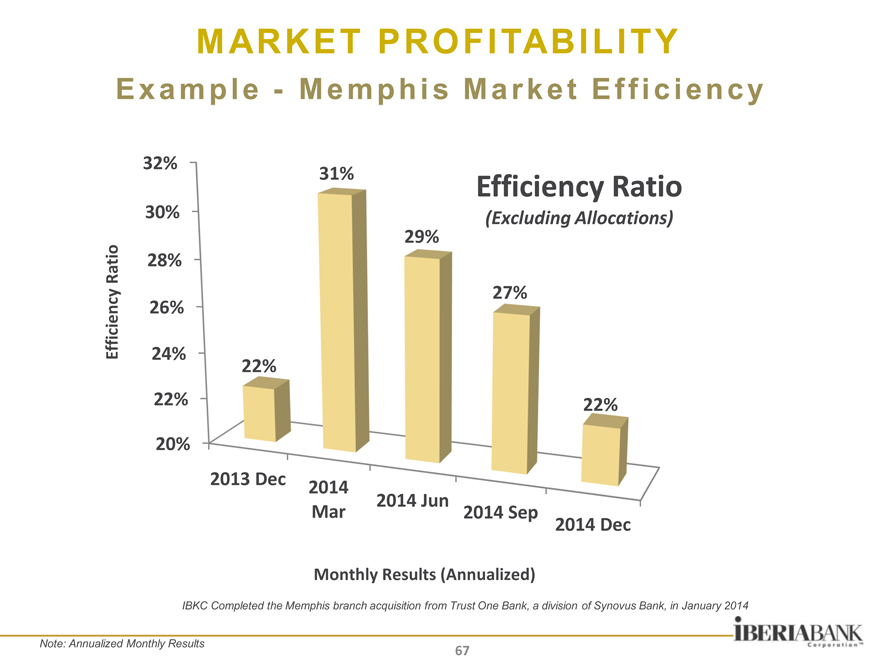

E x a m p l e—M e m p h i s M a r k e t E f f i c i e n c y

32%

31% Efficiency Ratio

30%(Excluding Allocations)

29%

atio 28%

R

27%

ncy 26%

e

i

c

i

Eff 24%

22%

22% 22%

20%

2013 Dec 2014

2014 Jun

Mar 2014 Sep

2014 Dec

Monthly Results (Annualized)

IBKC Completed the Memphis branch acquisition from Trust One Bank, a division of Synovus Bank, in January 2014

Note: Annualized Monthly Results

67

|

M ARKET PROFITABILITY

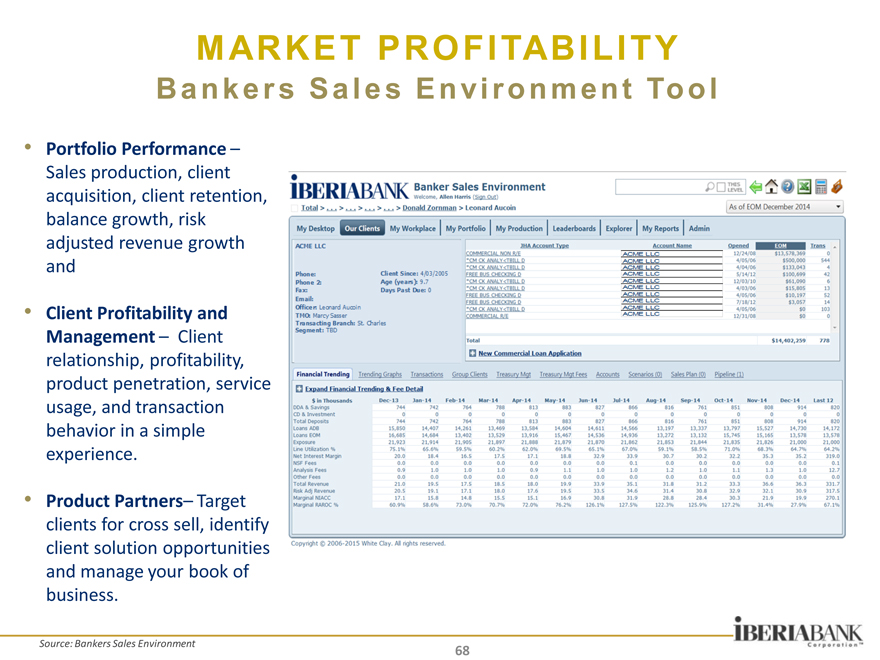

B a n k e r s S a l e s E n vi r o n m e n t To o l

Portfolio Performance –

Sales production, client acquisition, client retention, balance growth, risk adjusted revenue growth and

Client Profitability and Management – Client relationship, profitability, product penetration, service usage, and transaction behavior in a simple experience.

Product Partners– Target clients for cross sell, identify client solution opportunities and manage your book of business.

Source: Bankers Sales Environment

68

|

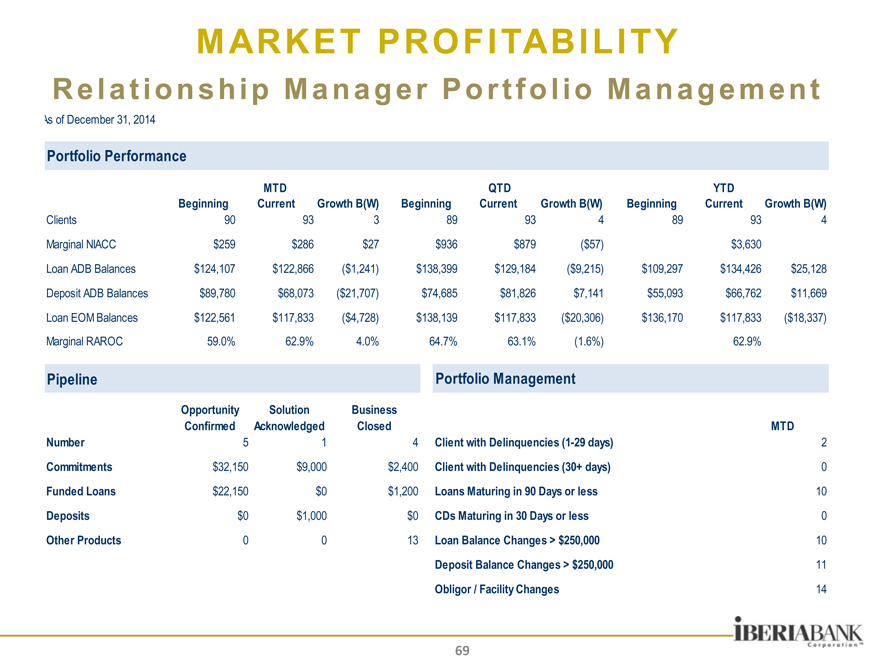

M ARKET PROFITABILITY

R e l a t i o ns hi p M a n a g e r P o r t f o l i o M a n a g e m e nt

As of December 31, 2014

Portfolio Performance

MTD QTD YTD

Beginning Current Growth B(W) Beginning Current Growth B(W) Beginning Current Growth B(W)

Clients 90 93 3 89 93 4 89 93 4

Marginal NIACC $259 $286 $27 $936 $879($57) $3,630

Loan ADB Balances $124,107 $122,866($1,241) $138,399 $129,184($9,215) $109,297 $134,426 $25,128

Deposit ADB Balances $89,780 $68,073($21,707) $74,685 $81,826 $7,141 $55,093 $66,762 $11,669

Loan EOM Balances $122,561 $117,833($4,728) $138,139 $117,833($20,306) $136,170 $117,833($18,337)

Marginal RAROC 59.0% 62.9% 4.0% 64.7% 63.1%(1.6%) 62.9%

Pipeline

Opportunity Solution Business

Confirmed Acknowledged Closed

Number 5 1 4

Commitments $32,150 $9,000 $2,400

Funded Loans $22,150 $0 $1,200

Deposits $0 $1,000 $0

Other Products 0 0 13

Portfolio Management

MTD

Client with Delinquencies (1-29 days) 2

Client with Delinquencies (30+ days) 0

Loans Maturing in 90 Days or less 10

CDs Maturing in 30 Days or less 0

Loan Balance Changes > $250,000 10

Deposit Balance Changes > $250,000 11

Obligor / Facility Changes 14

69

|

M ARKETS & GROWTH

Ar e a s O f P r i m a ry F o c u s

Market and Client Profitability Deposit Growth Diversification Business Banking

Non-Interest Income (Including Treasury Management and Bank Capital Markets) Optimize The Delivery System (Including Electronic Banking)

70

|

M&A DI SCUSSION

Few men have the virtue to “ withstand the highest bidder.

—George “

Washington

71

|

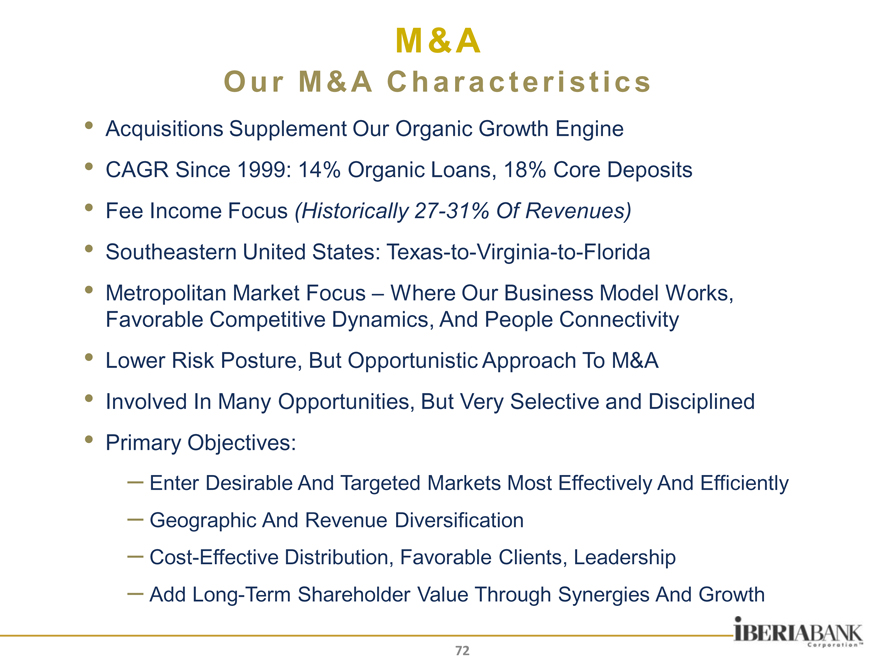

M &A

O u r M & A C h a r a c t e ri s t i c s

Acquisitions Supplement Our Organic Growth Engine

CAGR Since 1999: 14% Organic Loans, 18% Core Deposits

Fee Income Focus (Historically 27-31% Of Revenues)

Southeastern United States: Texas-to-Virginia-to-Florida

Metropolitan Market Focus – Where Our Business Model Works, Favorable Competitive Dynamics, And People Connectivity

Lower Risk Posture, But Opportunistic Approach To M&A

Involved In Many Opportunities, But Very Selective and Disciplined

Primary Objectives:

Enter Desirable And Targeted Markets Most Effectively And Efficiently Geographic And Revenue Diversification Cost-Effective Distribution, Favorable Clients, Leadership Add Long-Term Shareholder Value Through Synergies And Growth

72

|

M &A

H i s t o r i c a l P e r s pe c t i ve

Since 2001, 21 Acquisitions in Five States and Three Pending Deals

Including FDIC-Assisted, Live Bank, Branch Purchases, and Non-Bank

According to SNL, We Were:

– One Of The Most Active FDIC Bidders (25 Bids)

– One Of The Most Active FDIC Acquirers (Completed Five FDIC Deals)

– One Of The Most Active Live Bank Acquirers Since 2010

Aggregate Purchases of $12.3 Billion in Assets, $7.5 Billion in Loans, and $9.8 Billion in Deposits, Including Pending Transactions

On Four Occasions, We Completed Two Deals At The Same Time

On One Occasion, We Completed Three Deals At The Same Time

Our Pending Deals Are The First Time We Are Working Three Deals With

Five Conversions At The Same Time

73

|

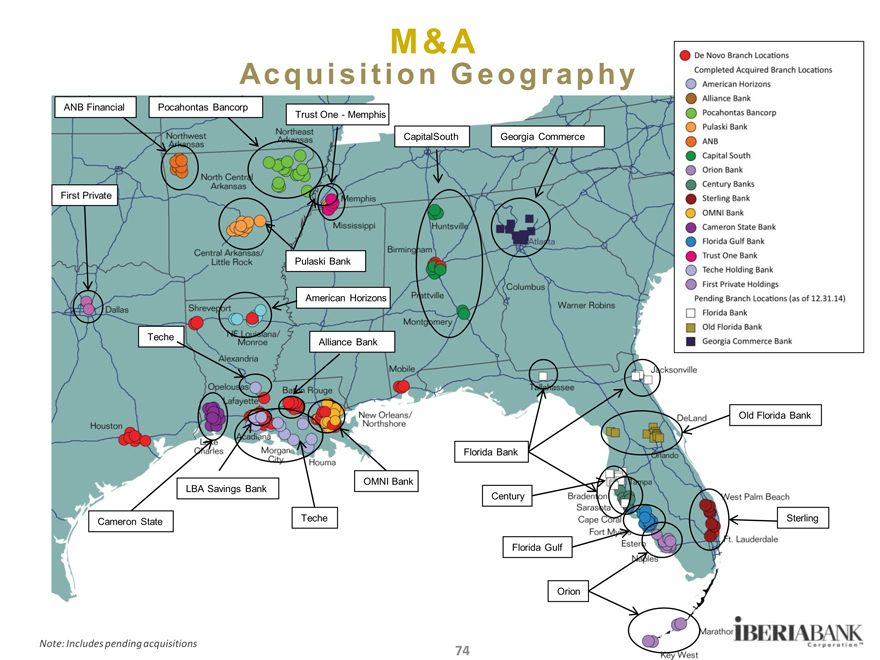

M &A

Ac q u i s i t i o n G e o g r a p hy

ANB Financial Pocahontas Bancorp

Trust One—Memphis

CapitalSouth Georgia Commerce

First Private

Pulaski Bank

American Horizons

Teche Alliance Bank

Old Florida Bank

Florida Bank

OMNI Bank

LBA Savings Bank

Century

Cameron State Teche Sterling

Florida Gulf

Orion

Note: Includes pending acquisitions 74

|

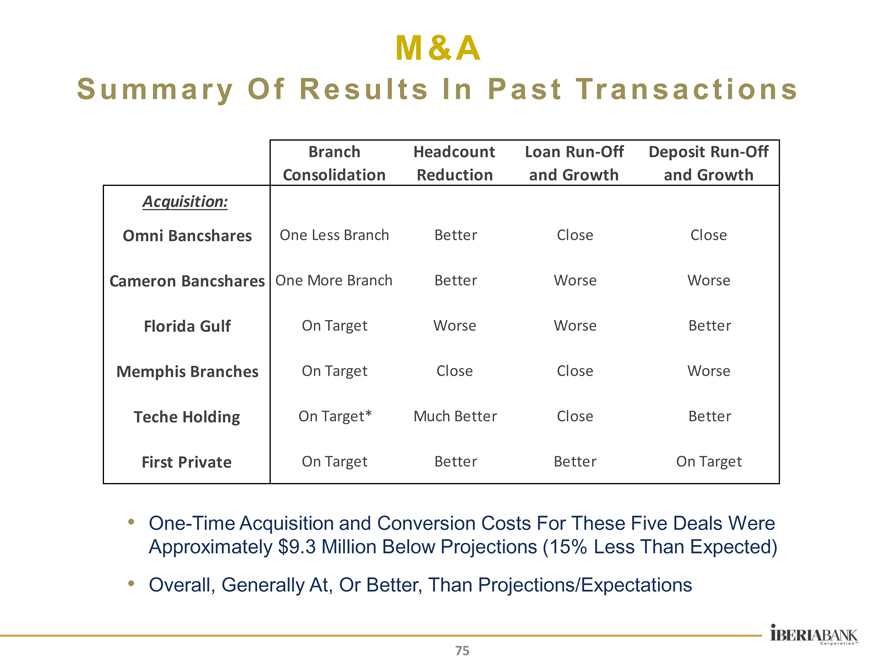

M &A

S u m m a r y O f R e s u l t s I n P a s t Tr a n s a c t i on s

Branch Headcount Loan Run-Off Deposit Run-Off

Consolidation Reduction and Growth and Growth

Acquisition:

Omni Bancshares One Less Branch Better Close Close

Cameron Bancshares One More Branch Better Worse Worse

Florida Gulf On Target Worse Worse Better

Memphis Branches On Target Close Close Worse

Teche Holding On Target* Much Better Close Better

First Private On Target Better Better On Target

One-Time Acquisition and Conversion Costs For These Five Deals Were Approximately $9.3 Million Below Projections (15% Less Than Expected) Overall, Generally At, Or Better, Than Projections/Expectations

75

|

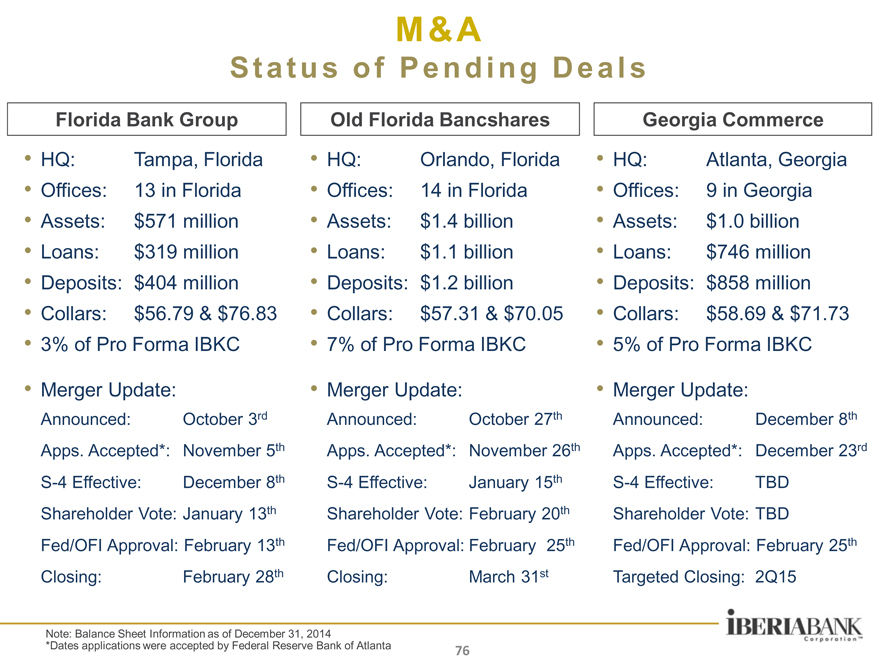

M &A

S t a t u s o f P e n d i ng D e a l s

Florida Bank Group Old Florida Bancshares Georgia Commerce

HQ: Tampa, Florida HQ: Orlando, Florida HQ: Atlanta, Georgia

Offices: 13 in Florida Offices: 14 in Florida Offices: 9 in Georgia

Assets: $571 million Assets: $1.4 billion Assets: $ 1.0 billion

Loans: $319 million Loans: $1.1 billion Loans: $ 746 million

Deposits: $404 million Deposits: $1.2 billion Deposits: $ 858 million

Collars: $56.79 & $76.83 Collars: $57.31 & $70.05 Collars: $ 58.69 & $71.73

3% of Pro Forma IBKC 7% of Pro Forma IBKC 5% of Pro Forma IBKC

Merger Update: Merger Update: Merger Update:

Announced: October 3rd Announced: October 27th Announced: December 8th

Apps. Accepted*: November 5th Apps. Accepted*: November 26th Apps. Accepted*: December 23rd

S-4 Effective: December 8th S-4 Effective: January 15th S-4 Effective: TBD

Shareholder Vote: January 13th Shareholder Vote: February 20th Shareholder Vote: TBD

Fed/OFI Approval: February 13th Fed/OFI Approval: February 25th Fed/OFI Approval: February 25th

Closing: February 28th Closing: March 31st Targeted Closing: 2Q15

Note: Balance Sheet Information as of December 31, 2014

*Dates applications were accepted by Federal Reserve Bank of Atlanta

76

|

POTENTIAL M &A TARGETS

A F i n i t e U n i ve r s e

$6,000 Southeastern Banks By Asset Size

$5,500 34 Banks With Assets Greater Than $5 Billion

$5,000

$4,500 Approximately 133 Banks With Assets

Between $1 Billion And $5 Billion

ions) $4,000

Mill $3,500

in

$

( $3,000

s

sset

A $2,500 Approximately 200 Banks With Assets

l

ta Between $500 and $1 Billion

To $2,000

Approximately 1,100 Banks With

$1,500 Assets Less Than $300 Million

$1,000

$500

$-

1 101 201 301 401 501 601 701 801 901 10011101120113011401150116011701

Financial Institutions in The Southeastern U.S.

Approximately 1,700

Financial Institutions In Our

11-State Targeted Footprint

Only 172, or less than

10%, Are Publicly Traded Companies

About 1,100 Banks Have Less Than $300 Million in

Total Assets

Of The 600 Remaining,

Relatively Few Are Within

MSAs That Are Of Interest To Us

Less Than 8% of the 1,700

Institutions Are Of Even Remote Interest To Us

Source: SNL; Southeastern U.S. includes VA, NC, SC, GA, FL, TN, AL, MS, LA, AR, and TX

77

|

I NTEREST RATE RI SK

We cannot direct the wind, “but we can adjust the sails.

—Bertha “

Calloway

78

|

INTEREST RATE RISK

C u r r e n t I R R P o s i t i on

Asset sensitive in both Net Interest Income and EVE measurements NII assumed to increase over 9% with a 200-basis point shock in rates NII modeled as static balance sheet with new volume assumptions based on recent originations

NII Sensitivity (Year 1)

Sensitivity

- 100 BP -2.0%

Base 0.0%

+ 100 BP 4.5%

+ 200 BP 9.1%

+ 300 BP 13.4%

+ 400 BP 17.8%

Forward 1.1%

Blue Chip 1.3%

EVE Sensitivity

Sensitivity

- 100 BP -12.2%

Base 0.0%

+ 100 BP 8.6%

+ 200 BP 15.3%

+ 300 BP 20.6%

+ 400 BP 25.2%

Forward -0.2%

Blue Chip -0.2%

IRR Net Interest Income Sensitivity—Year 1

17.8%

18.0%

16.0%

13.4%

14.0%

12.0%

10.0% 9.1%

8.0%

6.0% 4.5%

4.0%

1.1% 1.3%

2.0% -2.0% 0.0%

0.0%

-2.0%

—100 BP Base + 100 + 200 + 300 + 400 Forward Blue

BP BP BP BP Chip

79

|

INTEREST RATE RISK

C u r r e n t I R R P o s i t i on

Projected NII By Month—Flat Rates and Impact of

Forward Rates

$44,000,000

$43,000,000

$42,000,000

$41,000,000

$40,000,000

$39,000,000

$38,000,000

$37,000,000

NII By Month—Flat Rates NII By Month—Impact of Fwd Curve

NII Impact of Forward Curve

Higher rates on short-end of curve (implicit bear flattener) drive increase in NII

Projected NII assumes flat balance sheet

EPS estimate assumes 28% effective tax rate

NII Sensitivity to Forward Curve—Flat Balance Sheet

015 Q1 2016 Q2 2016 Q3 2016 Q4 2016

4.2 $ 120.4 $ 121.2 $ 121.6 $ 121.2

6.8 $ 124.5 $ 126.4 $ 127.8 $ 128.6

2.6 $ 4.1 $ 5.1 $ 6.2 $ 7.4

.06 0.09 0.11 0.14 0.16

2015 Impact $ 5.4 0.12

2016 Impact $ 22.9 0.51

80

|

INTEREST RATE RISK

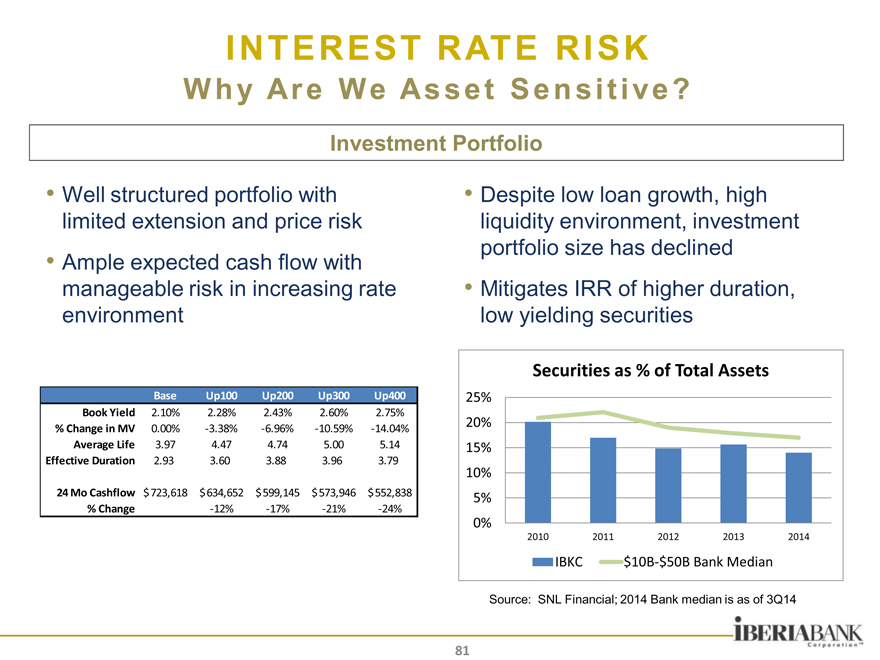

W h y Ar e We As s e t S e n s i t i ve ?

Investment Portfolio

Well structured portfolio with limited extension and price risk Ample expected cash flow with manageable risk in increasing rate environment

Despite low loan growth, high liquidity environment, investment portfolio size has declined

Mitigates IRR of higher duration, low yielding securities

Base Up100 Up200 Up300 Up400

Book Yield 2.10% 2.28% 2.43% 2.60% 2.75%

% Change in MV 0.00% -3.38% -6.96% -10.59% -14.04%

Average Life 3.97 4.47 4.74 5.00 5.14

Effective Duration 2.93 3.60 3.88 3.96 3.79

24 Mo Cashfl ow $ 723,618 $ 634,652 $ 599,145 $ 573,946 $ 552,838

% Change -12% -17% -21% -24%

Securities as % of Total Assets

25%

20%

15%

10%

5%

0%

2010 2011 2012 2013 2014

IBKC $10B-$50B Bank Median

Source: SNL Financial; 2014 Bank median is as of 3Q14

81

|

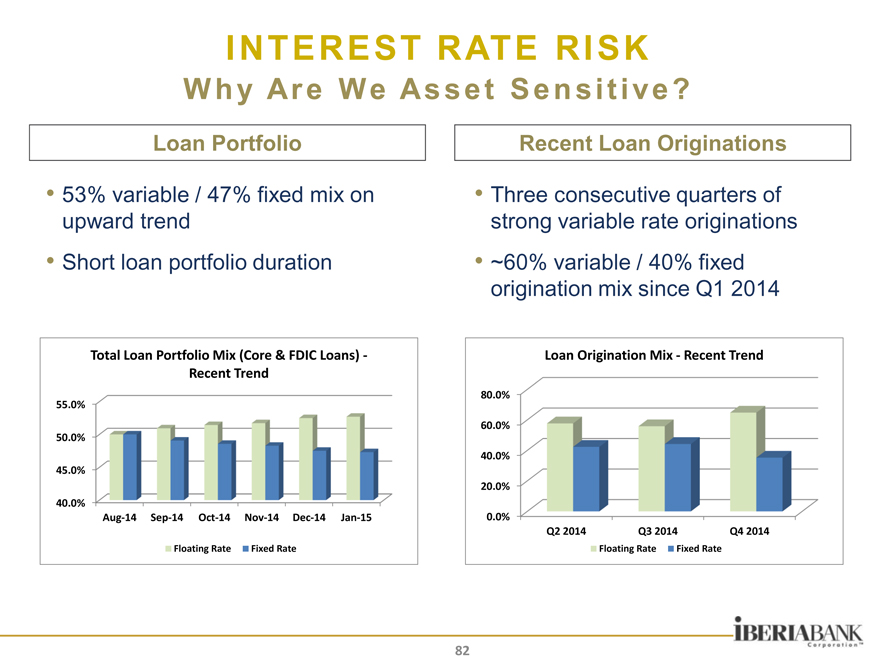

INTEREST RATE RISK

W h y Ar e We As s e t S e n s i t i ve ?

Loan Portfolio

53% variable / 47% fixed mix on upward trend

Short loan portfolio duration

Recent Loan Originations

Three consecutive quarters of strong variable rate originations

~60% variable / 40% fixed origination mix since Q1 2014

Total Loan Portfolio Mix (Core & FDIC Loans) -

Recent Trend

55.0%

50.0%

4

4

Loan Origination Mix—Recent Trend

80.0%

60.0%

40.0%

20.0%

0.0%

Q2 2014 Q3 2014 Q4 2014

Floating Rate Fixed Rate

82

|

INTEREST RATE RISK

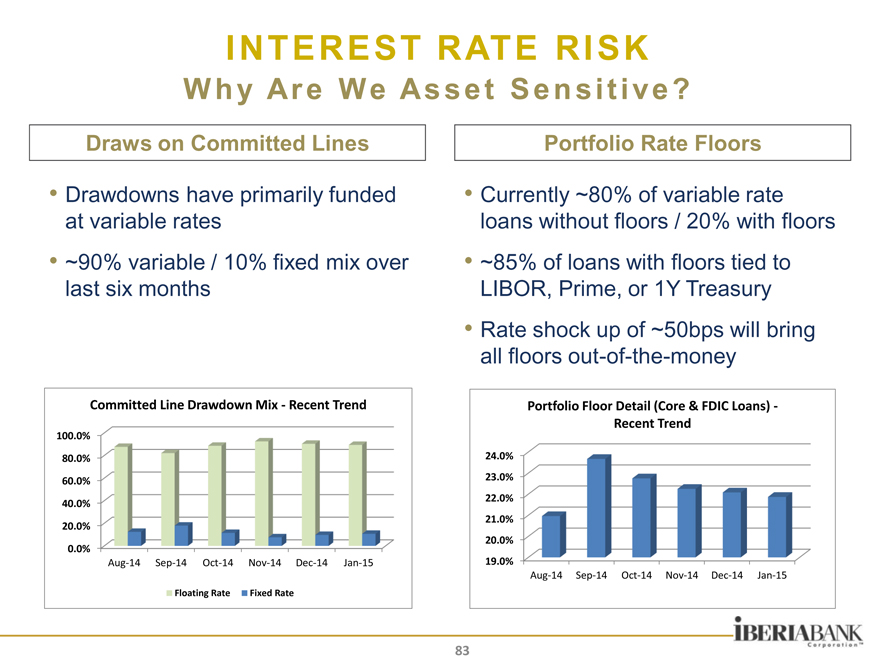

W h y Ar e We As s e t S e n s i t i ve ?

Draws on Committed Lines

Drawdowns have primarily funded at variable rates ~90% variable / 10% fixed mix over last six months

Currently ~80% of variable rate loans without floors / 20% with floors ~85% of loans with floors tied to

LIBOR, Prime, or 1Y Treasury

Rate shock up of ~50bps will bring all floors out-of-the-money

Committed Line Drawdown Mix—Recent Trend

100.0%

80.0%

Portfolio Floor Detail (Core & FDIC Loans) -

Recent Trend

24.0%

23.0%

22.0%

21.0%

20.0%

19.0%

Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15

83

|

INTEREST RATE RISK

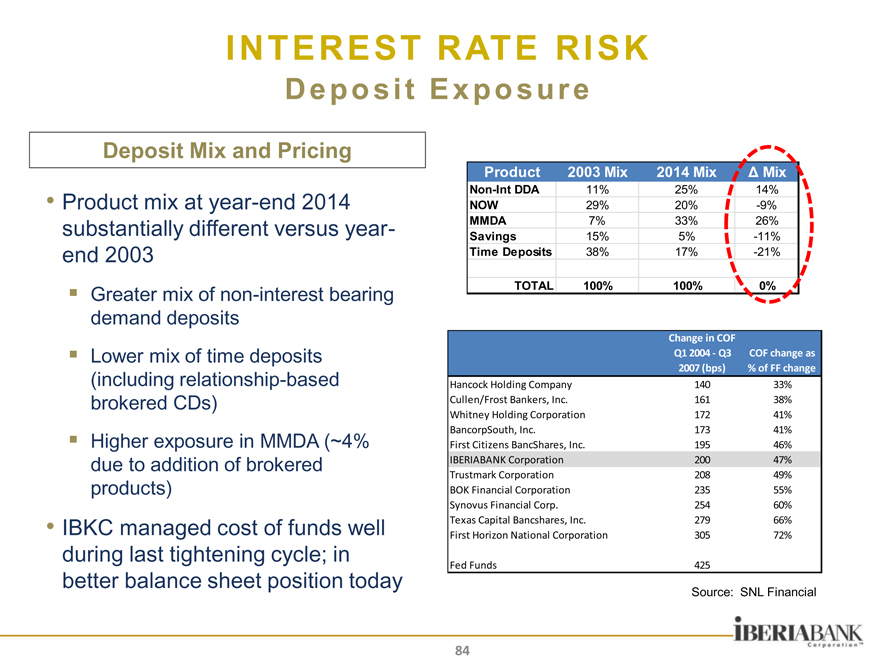

D e p o s i t E x p o s ur e

Deposit Mix and Pricing

Product mix at year-end 2014 substantially different versus year-end 2003

Greater mix of non-interest bearing demand deposits Lower mix of time deposits (including relationship-based brokered CDs) Higher exposure in MMDA (~4% due to addition of brokered products)

IBKC managed cost of funds well during last tightening cycle; in better balance sheet position today

Product 2003 Mix 2014 Mix Ä Mix

Non-Int DDA 11% 25% 14%

NOW 29% 20% -9%

MMDA 7% 33% 26%

Savings 15% 5% -11%

Time Deposits 38% 17% -21%

TOTAL 100% 100% 0%

Change in COF

Q1 2004—Q3 COF change as

2007 (bps)% of FF change

Hancock Holding Company 140 33%

Cullen/Frost Bankers, Inc. 161 38%

Whitney Holding Corporation 172 41%

BancorpSouth, Inc. 173 41%

First Citizens BancShares, Inc. 195 46%

IBERIABANK Corporation 200 47%

Trustmark Corporation 208 49%

BOK Financial Corporation 235 55%

Synovus Financial Corp. 254 60%

Texas Capital Bancshares, Inc. 279 66%

First Horizon National Corporation 305 72%

Fed Funds 425

Source: SNL Financial

84

|

INTEREST RATE RISK

M a i n t a i ni n g As s e t S e n s i t i vi t y

Continued focus on limiting long term, fixed rate asset exposure by prudent underwriting and client selection as well as appropriate use of loan level swaps

Customer Swap Notional ($MM)

$500

$450

$400

$350

$300

$250

$200

$150

$100

$50

$0

2010 2011 2012 2013 2014

Investment in Treasury Management and company-wide focus on low beta, core deposit gathering

Ongoing review to opportunistically extend liability durations

Brokered CD markets

~$100 million floating TRUPS portfolio

~$250 million deposits indexed to LIBOR

~$600 million borrowings maturing < 12 months

85

|

LONG—TERM STRATEGIC GOALS

“Our favorite holding period is forever.”

—Warren

Buffett

86

|

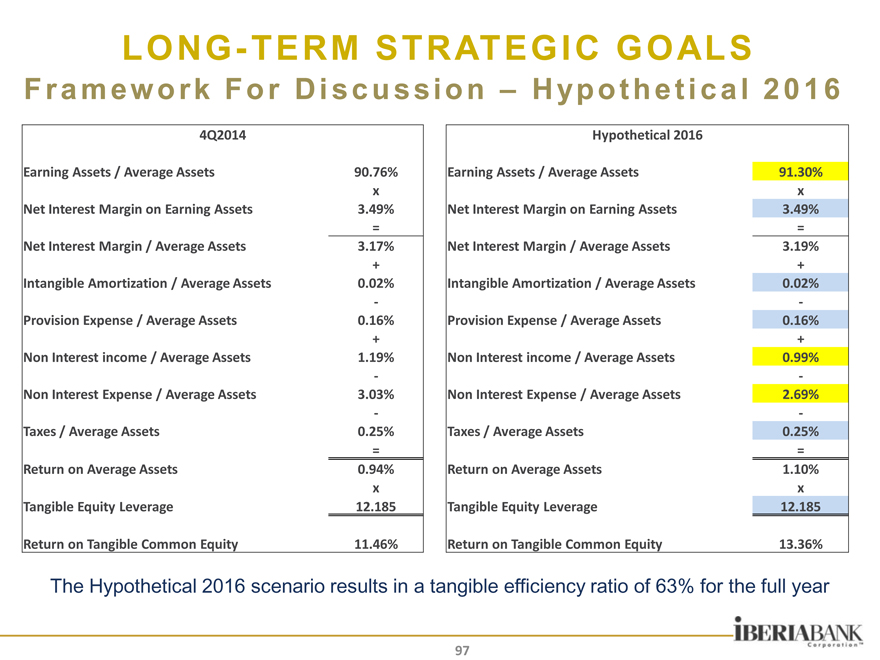

LONG-TERM STRATEGIC GOALS

S t r a t e gi c G o a l s An d E x e c ut i ve C o m p e n s a t i o n

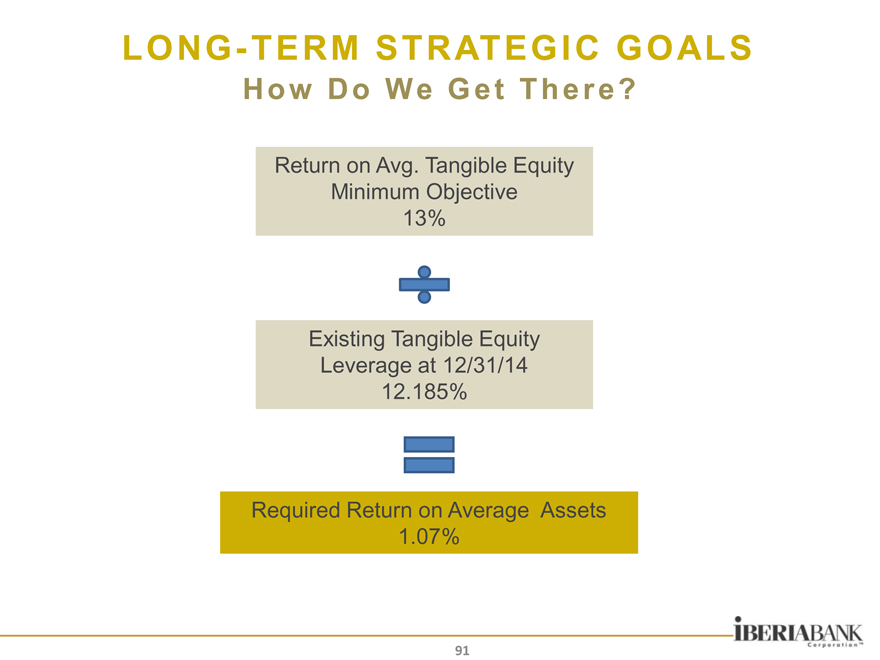

STRATEGIC GOALS

Key long-term financial goals through 2016 are as follows:

Return on average tangible equity of 13% To 17% Tangible efficiency ratio of 60% or less Asset quality in the top 10% of our peers Double-digit percentage growth in fully-diluted operating EPS

Company continues to focus on improving operating efficiency and profitability

EXECUTIVE COMP CHANGES

Executive compensation programs were redesigned to align with strategic goals, profitability focus, and shareholder value creation

Short-term incentive programs place greater emphasis on pre-established performance objectives (as opposed to discretionary objectives)

Long-term incentive programs place greater emphasis on performance-based metrics (as opposed to time-based metrics)

87

|

LONG-TERM STRATEGIC GOALS

H o w D o e s I B K C G e t T h e r e ?

Assuming The Following:

Stable Net Interest Margin

Stable Credit Metrics

No Significant Change in Effective Tax Rate

No Significant Change in Equity Leverage

The Answer:

Improvement in Balance Sheet Efficiency

Balance Sheet Growth

Growth in Non-Interest Income

Expense Containment

88

|

LONG-TERM STRATEGIC GOALS

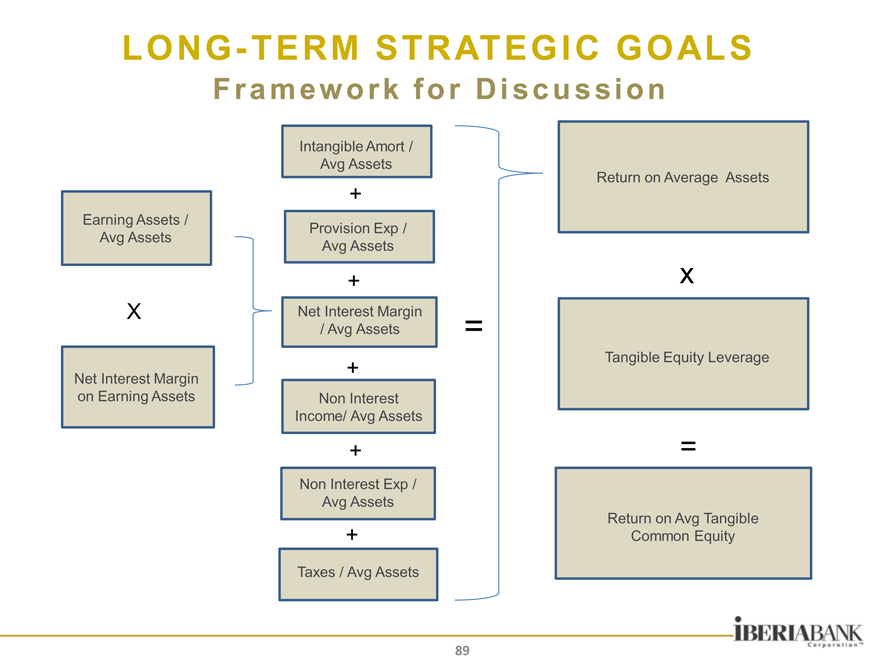

F r a m e w o rk f o r D i s c u s s i on

Intangible Amort /

Avg Assets

Return on Average Assets

+

Earning Assets / Provision Exp /

Avg Assets Avg Assets

+ x

X Net Interest Margin

/ Avg Assets =

+ Tangible Equity Leverage

Net Interest Margin

on Earning Assets Non Interest

Income/ Avg Assets

+ =

Non Interest Exp /

Avg Assets

Return on Avg Tangible

+ Common Equity

Taxes / Avg Assets

89

|

LONG-TERM STRATEGIC GOALS

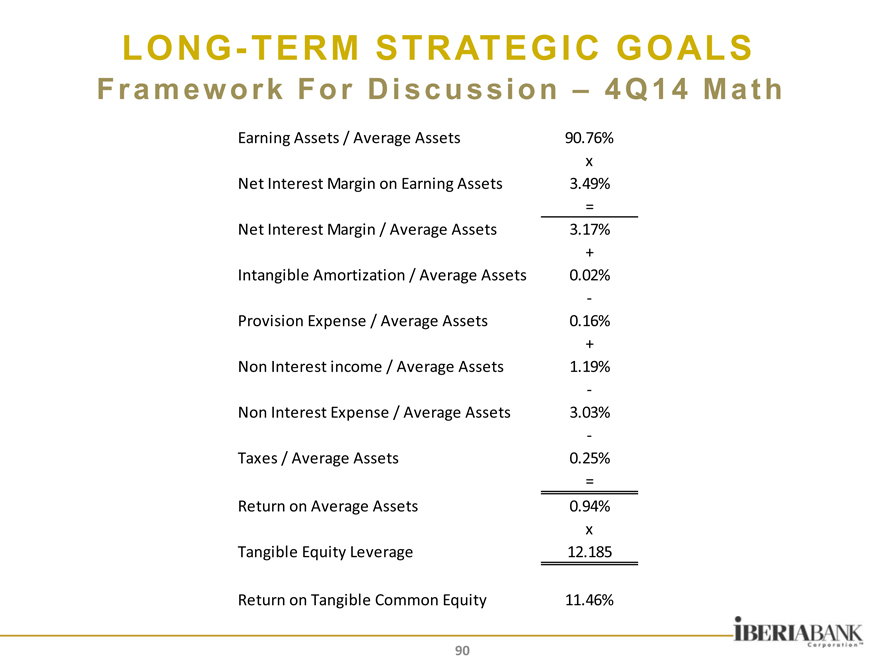

F r a m e w o rk F o r D i s c u s s i o n – 4 Q 1 4 M a t h

Earning Assets / Average Assets 90.76%

x

Net Interest Margin on Earning Assets 3.49%

=

Net Interest Margin / Average Assets 3.17%

+

Intangible Amortization / Average Assets 0.02%

-

Provision Expense / Average Assets 0.16%

+

Non Interest income / Average Assets 1.19%

-

Non Interest Expense / Average Assets 3.03%

-

Taxes / Average Assets 0.25%

=

Return on Average Assets 0.94%

x

Tangible Equity Leverage 12.185

Return on Tangible Common Equity 11.46%

90

|

LONG-TERM STRATEGIC GOALS

H o w D o We G e t T h e r e ?

Return on Avg. Tangible Equity

Minimum Objective

13%

Existing Tangible Equity

Leverage at 12/31/14

12.185%

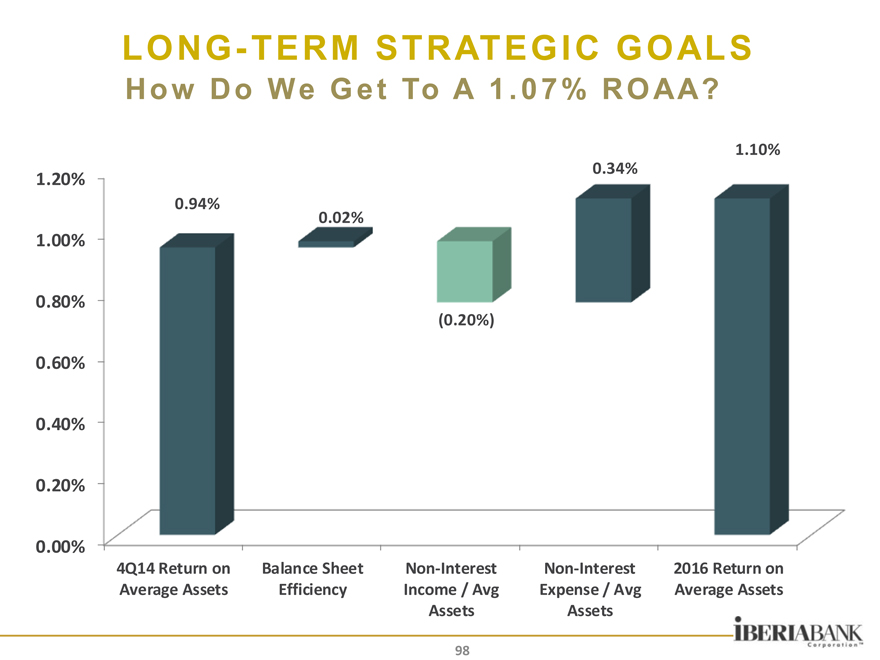

Required Return on Average Assets

1.07%

91

|

LONG-TERM STRATEGIC GOALS

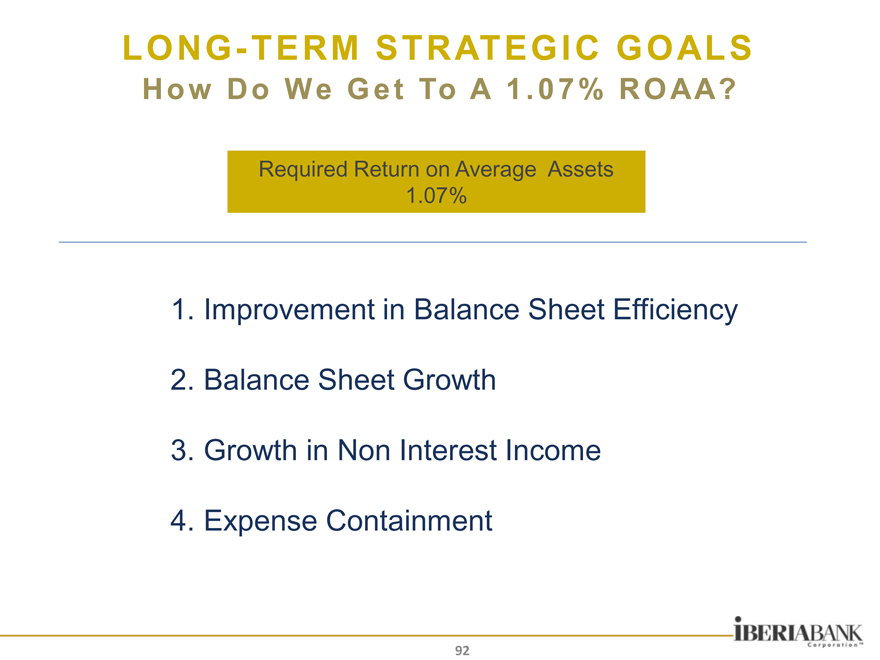

H o w D o We G e t To A 1 . 0 7 % R O AA?

Required Return on Average Assets 1.07%

1. Improvement in Balance Sheet Efficiency

2. Balance Sheet Growth

3. Growth in Non Interest Income

4. Expense Containment

92

|

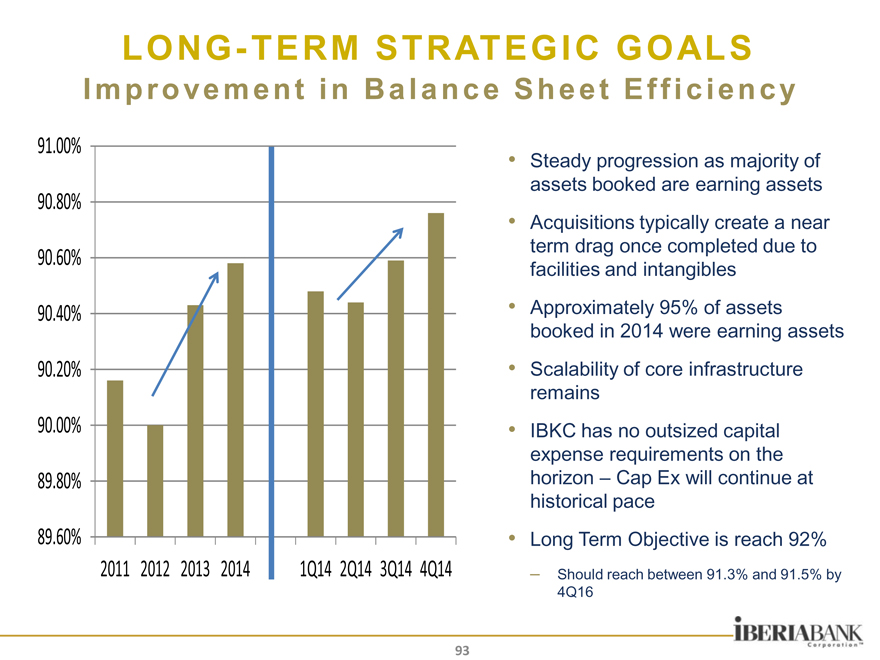

LONG-TERM STRATEGIC GOALS

I m p r o ve m e n t i n B a l a n c e S h e e t E f f i c i e n c y

91.00%

90.80%

90.60%

90.40%

90.20%

90.00%

89.80%

89.60%

2011 2012 2013 2014 1Q14 2Q14 3Q14 4Q14

Steady progression as majority of assets booked are earning assets Acquisitions typically create a near term drag once completed due to facilities and intangibles Approximately 95% of assets booked in 2014 were earning assets Scalability of core infrastructure remains IBKC has no outsized capital expense requirements on the horizon – Cap Ex will continue at historical pace Long Term Objective is reach 92%

– Should reach between 91.3% and 91.5% by 4Q16

93

|

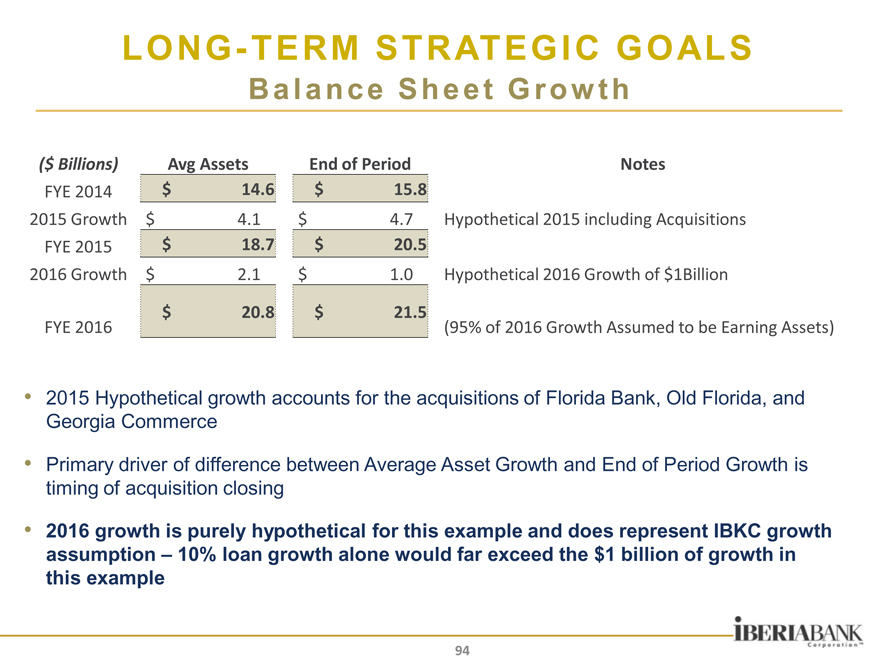

LONG-TERM STRATEGIC GOALS

B a l a n c e S h e e t G r o w t h

($ Billions) Avg Assets End of Period

FYE 2014 $ 14.6 $ 15.8

2015 Growth $ 4.1 $ 4.7

FYE 2015 $ 18.7 $ 20.5

2016 Growth $ 2.1 $ 1.0

$ 20.8 $ 21.5

FYE 2016

Notes

Hypothetical 2015 including Acquisitions

Hypothetical 2016 Growth of $1Billion

(95% of 2016 Growth Assumed to be Earning Assets)

2015 Hypothetical growth accounts for the acquisitions of Florida Bank, Old Florida, and Georgia Commerce

Primary driver of difference between Average Asset Growth and End of Period Growth is timing of acquisition closing

2016 growth is purely hypothetical for this example and does represent IBKC growth assumption – 10% loan growth alone would far exceed the $1 billion of growth in this example

94

|

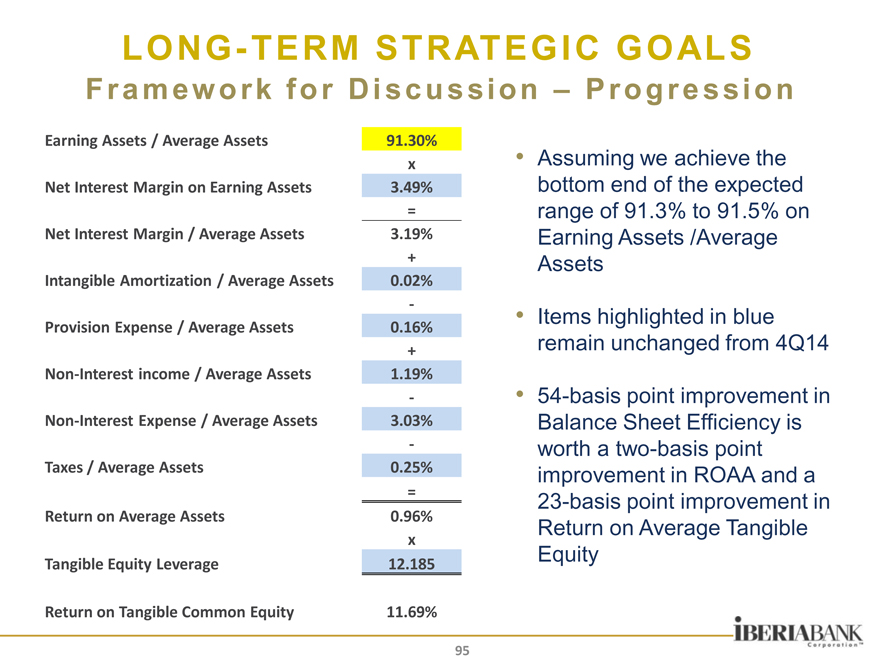

LONG-TERM STRATEGIC GOALS

F r a m e w o rk f o r D i s c u s s i on – P r o g r e s s i o n

Earning Assets / Average Assets 91.30%

x

Net Interest Margin on Earning Assets 3.49%

=

Net Interest Margin / Average Assets 3.19%

+

Intangible Amortization / Average Assets 0.02%

-

Provision Expense / Average Assets 0.16%

+

Non-Interest income / Average Assets 1.19%

-

Non-Interest Expense / Average Assets 3.03%

-

Taxes / Average Assets 0.25%

=

Return on Average Assets 0.96%

x

Tangible Equity Leverage 12.185

Return on Tangible Common Equity 11.69%

Assuming we achieve the bottom end of the expected range of 91.3% to 91.5% on

Earning Assets /Average

Assets

Items highlighted in blue remain unchanged from 4Q14

54-basis point improvement in

Balance Sheet Efficiency is worth a two-basis point improvement in ROAA and a

23-basis point improvement in

Return on Average Tangible

Equity

95

|

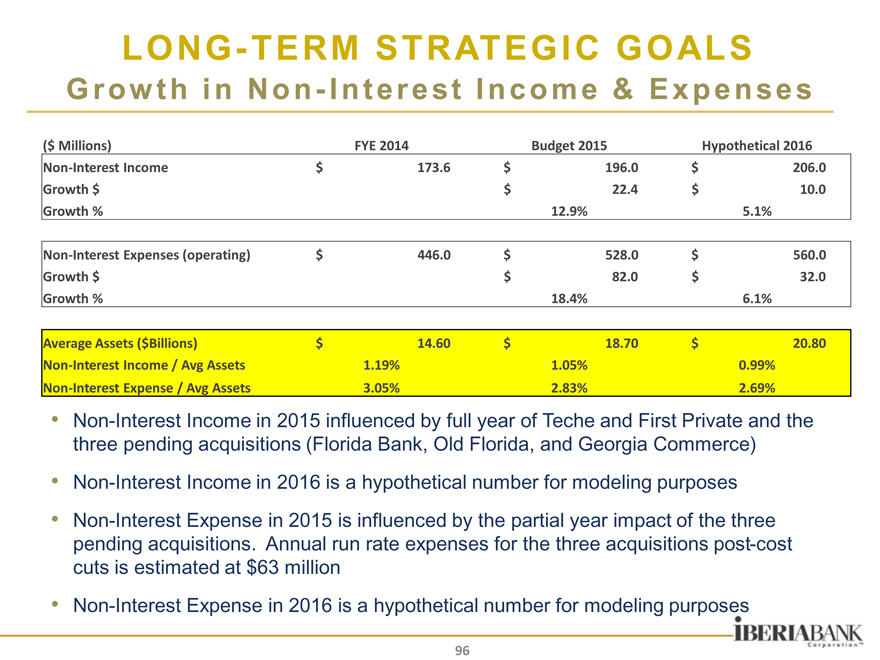

LONG-TERM STRATEGIC GOALS

G r ow t h i n N o n—I n t e r e s t I n c o m e & E x p e ns e s

($ Millions) FYE 2014 Budget 2015 Hypothetical 2016

Non-Interest Income $ 173.6 $ 196.0 $ 206.0

Growth $ $ 22.4 $ 10.0

Growth % 12.9% 5.1%

Non-Interest Expenses (operating) $ 446.0 $ 528.0 $ 560.0

Growth $ $ 82.0 $ 32.0

Growth % 18.4% 6.1%

Average Assets ($Billions) $ 14.60 $ 18.70 $ 20.80

Non-Interest Income / Avg Assets 1.19% 1.05% 0.99%

Non-Interest Expense / Avg Assets 3.05% 2.83% 2.69%