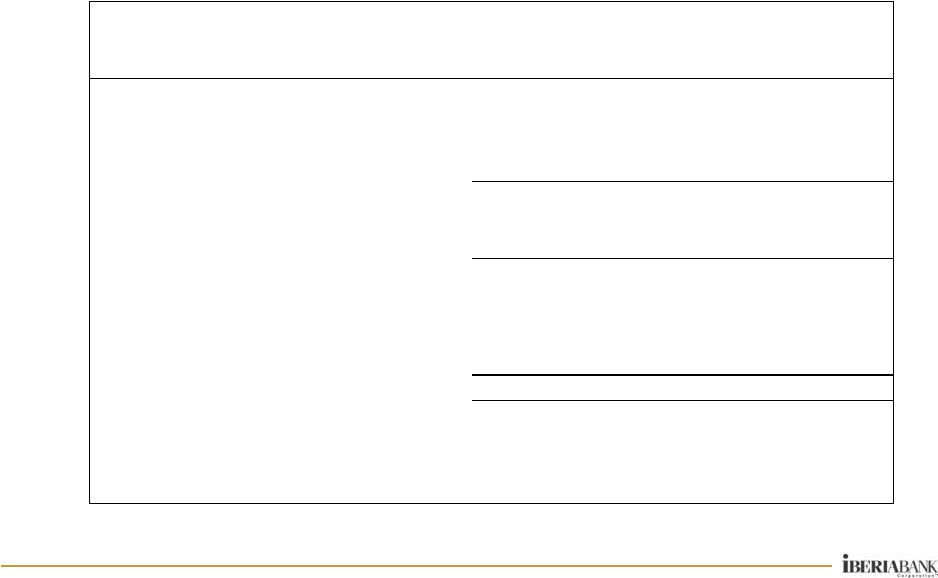

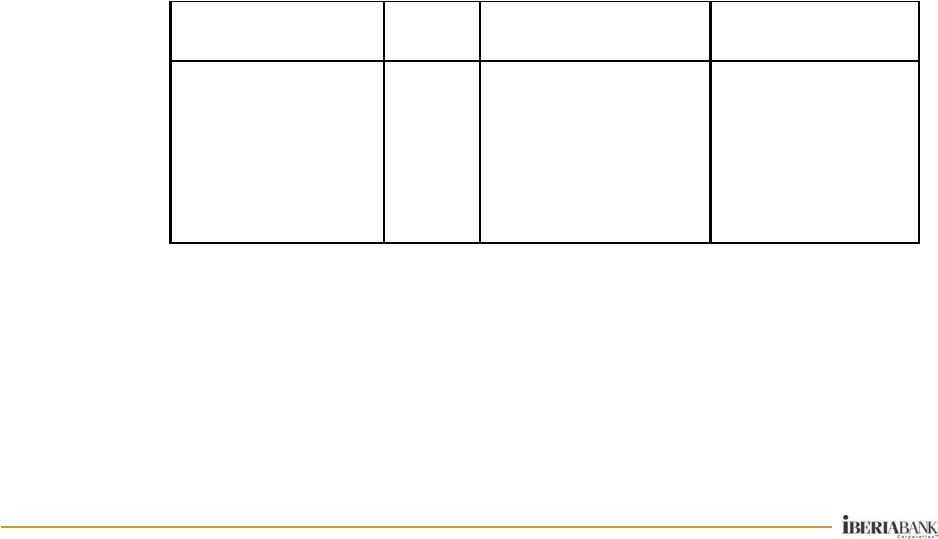

23 Appendix Non-Interest Expense Trends • Non-interest expenses excluding non-operating items up $6.8 million, or 6%, as compared to 4Q14 • Total expenses up $14.0 million, or 12%, in 1Q15 • Severance expense down $0.1 million • Impairment of long-lived assets down $0.5 million • Merger-related expense increased $7.3 million, related primarily to Florida Bank Group and Old Florida transactions • Tangible Operating Efficiency Ratio of 68.5%, up from 65.7% in 4Q14 Linked quarter changes in operating expense: 1Q15 includes one-month of Florida Bank Group results 2.1 0.9 (0.9) (0.7) $0.7 mil Non-interest Expense ($000s) 1Q14 2Q14 3Q14 4Q14 1Q15 $ Change % Change Mortgage Commissions 2,215 $ 3,481 $ 3,912 $ 4,045 $ 4,085 $ 40 $ 1% Hospitalization Expense 3,944 3,661 4,611 4,606 5,181 575 12% Other Salaries and Benefits 53,582 55,921 54,898 56,784 62,091 5,307 9% Salaries and Employee Benefits 59,741 $ 63,063 $ 63,421 $ 65,435 $ 71,357 $ 5,922 $ 9% Credit/Loan Related 3,560 3,093 4,569 2,483 4,183 1,700 68% Occupancy and Equipment 13,775 13,918 14,580 14,526 16,055 1,529 11% Amortization of Acquisition Intangibles 1,218 1,347 1,623 1,618 1,525 (93) -6% All Other Non-interest Expense 27,134 28,567 29,523 31,899 29,667 (2,232) -7% Nonint. Exp. (Ex-Non-Operating Exp.) 105,428 $ 109,988 $ 113,717 $ 115,961 $ 122,787 $ 6,826 $ 6% Severance 119 5,466 1,226 139 41 (98) -71% Occupancy and Branch Closure Costs 17 14 - - - - 100% Storm-related expenses 184 4 1 2 20 18 760% Impairment of Long-lived Assets, net of gains on sales 541 1,241 4,213 1,078 579 (499) -46% Provision for FDIC clawback liability - - (797) - - - 0% Termination of Debit Card Rewards Program (22) - - - - - 0% Consulting and Professional - - - - 430 430 100% Merger-Related Expenses 967 10,419 1,752 1,955 9,296 7,341 376% Total Non-interest Expense 107,234 $ 127,132 $ 120,112 $ 119,135 $ 133,153 $ 14,017 $ 12% Tangible Efficiency Ratio - excl Nonop-Exp 73.5% 69.8% 65.1% 65.7% 68.5% 1Q15 vs. 4Q14 1.4 1.3 0.7 Total Florida Bank Group expenses Payroll taxes Occupancy and equipment expense Provision for unfunded commitment Marketing and business development Benefits expense Professional services OREO costs, net |