Fraser Trebilcock Davis & Dunlap, P.C.

Lawyers

PETER L. DUNLAP3 | JONATHAN E. RAVEN | 124 West Allegan Street, Suite 1000 | DETROIT OFFICE |

| DOUGLAS J. AUSTIN | THADDEUS E. MORGAN | lansing, michigan 48933 | TELEPHONE (313) 237-7300 |

MICHAEL E. CAVANAUGH9 | ANNE BAGNO WIDLAK | TELEPHONE (517) 482-5800 | FACSIMILE (313) 961-1651 |

| JOHN J. LOOSE | ANITA G. FOX4 | FACSIMILE (517) 482-0887 | |

DAVID E.S. MARVIN4 | ELIZABETH H. LATCHANA | website www.fraserlawfirm.com | |

| STEPHEN L. BURLINGAME | TODD D. CHAMBERLAIN | archie c. fraser | |

| DARRELL A. LINDMAN | RYAN M. WILSON | (1902-1998) | |

| IRIS K. LINDER | KENNETH S. WILSON2 | everett r. trebilcock | |

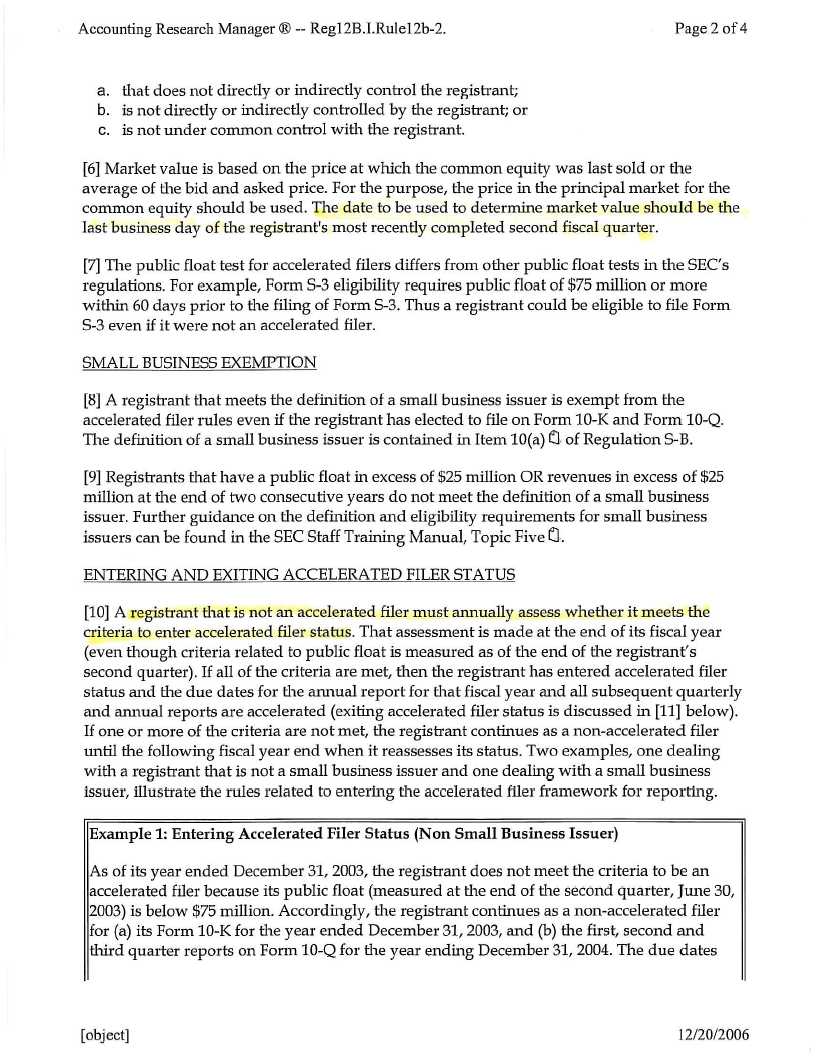

| GARY C. ROGERS | ROBERT B. NELSON | (1918-2002) | |

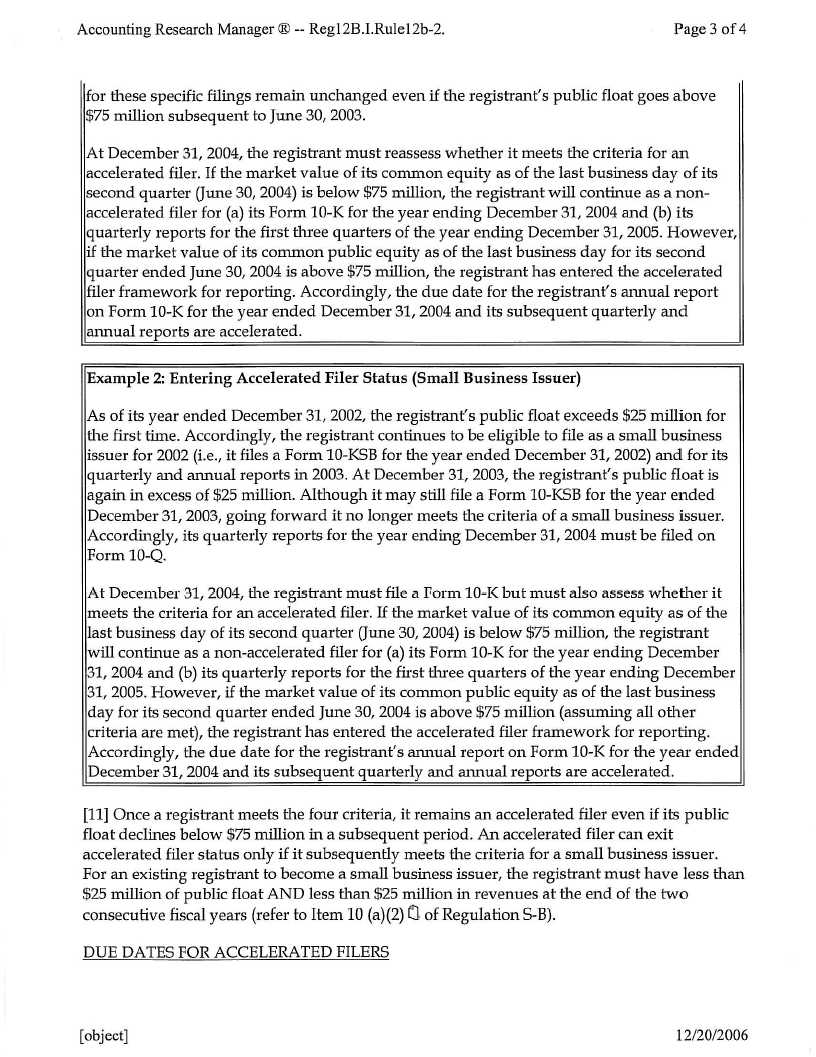

| MARK A. BUSH | BRIAN P. MORLEY6 | ||

| MICHAEL H. PERRY | MARY M. MOYNE8 | james r. davis | |

| BRANDON W. ZUK | JOHN D. MILLER7 | (1918-2005) | |

| MICHAEL C. LEVINE | TONI L. HARRIS8 | ||

| THOMAS J. WATERS | RYAN K. KAUFFMAN | retired | |

MARK R. FOX2,4 | JENNIFER UTTER HESTON | donald a. hines | |

| MICHAEL S. ASHTON | NICOLE L. PROULX | ronald r. pentecost | |

| H. KIRBY ALBRIGHT | MATTHEW A. CARMONA | ||

| GRAHAM K. CRABTREE | VINCENT M. PECORA | 1RETIRED CIRCUIT JUDGE | |

| MICHAEL P. DONNELLY | G. ALAN WALLACE | 2ALSO LICENSED IN FLORIDA | |

EDWARD J. CASTELLANI5 | LOUIS A. BROWN | 3ALSO LICENSED IN COLORADO | |

| NAN ELIZABETH CASEY | SAMANTHA A. KOPACZ | January 30, 2008 | 4ALSO LICENSED IN DISTRICT OF |

PETER D. HOUK1 | COLUMBIA | ||

5ALSO CERTIFIED PUBLIC | |||

| ACCOUNTANT | |||

6ALSO LICENSED IN NORTH | |||

| CAROLINA | |||

7ALSO LICENSED IN GEORGIA | |||

8ALSO LICENSED BY U.S. PATENT | |||

| AND TRADEMARK OFFICE | |||

9ALSO LICENSED IN OHIO |

E-mail: ilinder@fraserlawfirm.com

DID: 517-377-0803

Division of Corporation Finance

United States Securities and Exchange Commission

100 F. Street, N.E.

Mail Stop 7010

Washington, DC 20549-1090

| RE: | Aurora Oil & Gas Corporation (the "Company") Post-Effective Amendment No. 5 to Registration Statement on Form SB-2 on Form S-3 Filed December 21, 2007 File No. 333-129695 Post-Effective Amendment No. 5 to Registration Statement on Form SB-2 on Form S-3 Filed December 21, 2007 File No. 333-130769 |

Dear Mr. Schwall:

Reference is made to your comment letter (your “Letter”) of January 14, 2008 regarding Aurora Oil & Gas Corporation’s Post-Effective Amendments No. 5 to Registration Statements numbers 333-129695 and 333-130769 on Form SB-2 on Form S-3, filed with the Securities and Exchange Commission (the “SEC”) on December 21, 2007 (the “Registration Statements”). The comment numbers and headings below in this response letter (this “Response Letter”) correspond with those set forth in your Letter.

Mr. H. Roger Schwall, Assistant Director

January 30, 2008

Page 2

General Comment No. 1: We have issued under separate cover comments relating to your confidential treatment request for Exhibit 10.11 to your quarterly report on Form 10-Q filed August 7, 2006. Until all open matters including the request for confidential treatment have been resolved, we will not be in a position to consider a request to accelerate the effectiveness of your registration statements.

Response to General Comment No. 1: In our letter of January 30, 2008 to Special Counsel Timothy Levenberg, we responded to your comment letter dated January 15, 2008 (the “Confidential Treatment Comment Letter”) relating to the confidential treatment request for Exhibit 10.11 to the Company's Form 10-Q filed with the SEC August 7, 2006. On January 30, 2008, the Company filed Amendment No. 4 to the Company's Form 10-QSB for the period ended June 30, 2006, including a redacted copy of the exhibit for which we requested confidential treatment. Although we have not yet received a response from your office on the matter, we believe that we have fully complied with the comments and revisions requested in the Confidential Treatment Comment Letter and that all issues raised in the Confidential Treatment Comment Letter have been resolved.

General Comment No. 2: Please give effect to each comment from our letter to you dated December 18, 2007 regarding your annual report on Form 10-KSB for the fiscal year ended December 31, 2006 and your quarterly report on Form 10-Q for the fiscal quarter ended September 30, 2007, as applicable.

Response to General Comment No. 2: In a letter dated January 17, 2008 to Brad Skinner, Senior Assistant Chief Accountant of the SEC, the Company responded to the December 18, 2007 comment letter.

General Comment No. 3: It appears that you are not eligible to use Form S-3. Instruction I.A.3(b) of the Form S-3 requires that a registrant has filed in a timely manner all reports required to be filed during the twelve calendar months and any portion of a month immediately preceding the filing of the registration statement, other than a report that is required solely pursuant to certain specified items of Form 8-K. It appears that you did not file the quarterly reports for the fiscal quarters ended March 31, 2007 and September 30, 2007 within the time periods prescribed for accelerated filers. Please amend both registration statements on a form for which you qualify.

Response to General Comment No. 3: Based on the following analysis, we respectfully request that you reconsider your apparent assumption in Comment No. 3 that the Company was an accelerated filer with respect to its 2007 quarterly reports on Form 10-Q.

The Company was an SB filer through the year 2006. The Company's annual report for the year ended December 31, 2006 was filed on March 15, 2007 on Form 10-KSB.

Mr. H. Roger Schwall, Assistant Director

January 30, 2008

Page 3

At December 31, 2006, the Company's public float exceeded $25 million for the second consecutive year. Thus, under Reg 228.10(a)(2), for the year 2007, the Company was no longer an SB filer. Reg 228.10(a)(2)(v) provides, "The determination made for a reporting Company at the end of its fiscal year governs all reports relating to the next fiscal year."

During the time the Company was eligible to be an SB filer, it was not an accelerated filer. See Reg 240.12b-2(1)(iv). It was also not an accelerated filer for the quarterly reports in the first fiscal year after exiting SB filer status. The test for determining accelerated filer status is performed at the end of a fiscal year and looks back to the issuer's most recently completed second quarter. Since the Company was still an SB filer at December 31, 2006, and since its most recently completed second quarter at the time was June 30, 2006, for which it was an SB filer, the Company could not have been characterized as an accelerated filer for its 2007 quarterly reports.

The Company has performed the accelerated filer test at December 31, 2007, and based on its public float at June 30, 2007, has now become an accelerated filer. The Company will file its Form 10-K for the period ended December 31, 2007 as an accelerated filer, as required by Reg 240.12b-2(3)(i).

In addition to conducting the foregoing analysis, the Company looked for guidance from experts in determining when it would become an accelerated filer. We are enclosing with this letter an excerpt from CCH Accounting Research Manager®, entitled "Regulation 12B-Interpretations and Guidance". You will see at Example 2 that the CCH guidance matches our own analysis. In an illustration with identical facts, the CCH expert concludes that the issuer exiting SB status does not become an accelerated filer until filing the first Form 10-K after exiting SB filer status. This CCH guidance is widely relied upon in the public company community.

Since the Company was not an accelerated filer for purposes of its 2007 quarterly reports, all of its filings during the preceding 12 months have indeed been timely filed, and the Company is eligible to use Form S-3.

Exhibits 5.1, Comments 4 and 5:

4. Obtain and file new legality opinions issued by Utah counsel and which do not contain the assumption set forth in clause (ii) of the fourth paragraph regarding authorized shares. We note in that regard the qualifications regarding counsel's ability to opine on the laws of Utah.

Mr. H. Roger Schwall, Assistant Director

January 30, 2008

Page 4

5. We note also that counsel's consent to the filing of the opinion as an exhibit to the registration statement (in File No. 333-129695) refers to Post-Effective Amendment No. 4 rather than Post-Effective Amendment No. 5.

Response to Exhibits 5.1, Comments 4 and 5: We have filed amendments to the registration statements with revised opinions at Exhibits 5.1 that respond to your comments.

Should you have any further questions, please feel free to contact me.

Very truly yours,

FRASER TREBILCOCK DAVIS & DUNLAP, P.C.

//Iris K. Linder//

Iris K. Linder

IKL/blv

Enclosure

| cc: | Barbara Lawson |

| Laura Nicholson |