As compensation for its services, JNAM receives a fee from the Trust computed separately for the Acquiring Fund, accrued daily and payable monthly. The fee JNAM receives from the Acquiring Fund is set forth below as an annual percentage of the net assets of the Acquiring Fund.

| Acquiring Fund | Assets | Advisory Fee (Annual Rate

Based on Average Net Assets) | Aggregate Fee Paid to

Adviser in Fiscal Year

Ended December 31,

2015 (Annual Rate Based on Average Net Assets) |

| T. Rowe Price Fund | $0 to $150 million Over $150 million | 0.75% 0.70% | 0.70% |

JNAM selects, contracts with, and compensates sub-advisers to manage the investment and reinvestment of the assets of the Funds of the Trust. JNAM monitors the compliance of such sub-advisers with the investment objectives and related policies of each Fund, reviews the performance of such sub-advisers, and reports periodically on such performance to the Board of Trustees of the Trust. Under the terms of each of the Sub-Advisory Agreements, the sub-adviser manages the investment and reinvestment of the assets of the assigned Fund, subject to the supervision of the Board of Trustees of the Trust. The sub-adviser formulates a continuous investment program for each such Fund consistent with its investment objectives and policies outlined in its Prospectus. Each sub-adviser implements such programs by purchases and sales of securities. Each sub-adviser regularly reports to JNAM and the Board of Trustees of the Trust with respect to the implementation of such programs. As compensation for its services, each sub-adviser receives a fee from JNAM computed separately for the applicable Fund, stated as an annual percentage of the net assets of such Fund.

As compensation for its services for the Acquiring Fund, the Sub-Advisers, T. Rowe Price Associates, Inc. and Mellon Capital Management Corporation, receive a sub-advisory fee that is payable by JNAM. The sub-advisory fee schedule for each Sub-Adviser is set forth below:

| Acquiring Fund | Assets | Sub-Advisory Fee

(Annual Rate Based on

Average Net Assets) |

T. Rowe Price Fund 1 (T. Rowe Price Associates, Inc.) | $0 to $20 million $20 to $50 million $50 million to $200 million Over $200 million | 0.60% 0.50% 0.50% 0.50% 3 |

T. Rowe Price Fund 2 (Mellon Capital Management Corporation) | $0 to $50 million $50 to $100 million $100 million to $750 million Over $750 million | 0.09% 0.06% 0.03% 0.015% |

1 Fees will be paid based on assets invested in the actively managed portion of the Fund managed by T. Rowe Price Associates, Inc., not including assets from the mid-cap growth index strategy portion of the Fund managed by Mellon Capital Management Corporation.

2 Fees will be paid based on assets invested in the mid-cap growth index strategy portion of the JNL/T. Rowe Price Fund managed by Mellon Capital Management Corporation.

3 When net assets exceed $200 million, the annual rate is applicable to all the amounts in the T. Rowe Price Fund.

A discussion of the basis for the Board of Trustees’ approval of the investment advisory and sub-advisory agreements is available in the Trust’s Annual Report to shareholders for the year ended December 31, 2015 and will be available in the Trust’s Annual Report to shareholders for the year ended December 31, 2016.

In addition to the investment advisory fee, the Acquiring Fund currently pays to JNAM (the “Administrator”) an Administrative Fee as an annual percentage of the average daily net assets of the Fund as set forth below.

| Acquiring Fund | Assets | Administrative Fee (Annual Rate Based on Average Net Assets) |

| T. Rowe Price Fund | $0 to $3 billion Assets over $3 billion | 0.10% 0.09% |

In return for the Administrative Fee, the Administrator provides or procures all necessary administrative functions and services for the operation of the Funds. In addition, the Administrator, at its own expense, arranges and pays for routine legal, audit, fund accounting, custody (except overdraft and interest expense), printing and mailing, a portion of the Chief Compliance Officer costs and all other services necessary for the operation of each Fund. Each Fund is responsible for trading expenses, including brokerage commissions, interest and taxes, and other non-operating expenses. Each Fund is also responsible for nonrecurring and extraordinary legal fees, registration fees, licensing costs, a portion of the Chief Compliance Officer costs, Independent Trustees liability insurance, and the fees and expenses of the Independent Trustees and of independent legal counsel to the Independent Trustees.

The Trust has adopted a multi-class plan pursuant to Rule 18f-3 under the 1940 Act. Under the multi-class plan, the Acquiring Fund has two classes of shares, Class A and Class B. The Class A shares and Class B shares of the Acquiring Fund represent interests in the same portfolio of securities, and will be substantially the same except for “class expenses.” The expenses of the Acquiring Fund will be borne by each Class of shares based on the net assets of the Fund attributable to each Class, except that class expenses will be allocated to each Class. “Class expenses” will include any distribution or administrative or service expense allocable to the appropriate Class and any other expense that JNAM determines, subject to ratification or approval by the Board, to be properly allocable to that Class, including: (i) printing and postage expenses related to preparing and distributing to the shareholders of a particular Class (or Contract Owners funded by shares of such Class) materials such as Prospectuses, shareholder reports and (ii) professional fees relating solely to one Class.

Distributio

n Arrangements

Jackson National Life Distributors LLC (the “Distributor”), 7601 Technology Way, Denver, Colorado 80237, is the principal underwriter to the Trust. The Trust has adopted, in accord with the provisions of Rule 12b-1 under the 1940 Act, a Distribution Plan (“Plan”). The Board of Trustees, including all of the Independent Trustees, must approve, at least

annually, the continuation of the Plan. Under the Plan, certain Funds will pay a Rule 12b-1 fee at an annual rate of up to 0.20% of the Fund’s average daily net assets attributed to Class A interests, to be used to pay or reimburse distribution and administrative or other service expenses with respect to Class A interests. The Distributor, as principal underwriter, to the extent consistent with existing law and the Plan, may use the Rule 12b-1 fee to reimburse fees or to compensate broker-dealers, administrators, or others for providing distribution, administrative or other services.

The Distributor also has certain relationships with the sub-advisers and their affiliates. The Distributor receives payments from certain of the sub-advisers to assist in defraying the costs of certain promotional and marketing meetings in which they participate. The amounts paid depend on the nature of the meetings, the number of meetings attended, the costs expected to be incurred, and the level of the sub-adviser’s participation. A brokerage affiliate of the Distributor participates in the sales of shares of retail mutual funds advised by certain of the sub-advisers and receives selling and other compensation from them in connection with those activities, as described in the prospectus or statement of additional information for those funds. In addition, the Distributor acts as distributor of the Contracts issued by the Insurance Companies.

Pay

ments to Broker-Dealers and Financial Intermediaries

Only Separate Accounts, registered investment companies, and certain non-qualified plans of the Insurance Companies may purchase shares of the Acquiring Fund. If an investor invests in the Fund under a Contract or a plan that offers a Contract as a plan option through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and the salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s web-site for more information.

Investme

nt in Trust Shares

Shares of the Trust are currently sold to Separate Accounts of the Insurance Companies to fund the benefits under certain Contracts; to certain unqualified retirement plans; and to other regulated investment companies that in turn are sold to Separate Accounts. The Separate Accounts, through their various sub-accounts, invest in designated Funds and purchase and redeem the shares of the Funds at their net asset value (“NAV”). There is no sales charge.

Shares of the Acquiring Fund are not available to the general public directly. The Acquiring Fund is managed by a sub-adviser who also may manage publicly available mutual funds having similar names and investment objectives. While the Acquiring Fund may be similar to, and may in fact be modeled after, publicly available mutual funds, purchasers should understand that the Acquiring Fund is not otherwise directly related to any publicly available mutual fund. Consequently, the investment performance of any such publicly available mutual funds and the Acquiring Fund may differ substantially.

The NAV per share of the Acquiring Fund is generally determined once each day on which the New York Stock Exchange (“NYSE”) is open at the close of the regular trading session of the NYSE (normally 4:00 p.m., Eastern Time, Monday through Friday). Calculations of the NAV per share of the Acquiring Fund may be suspended by the Trust’s Board of Trustees in accordance with Rule 22c-1 under the 1940 Act. The NAV per share is calculated by adding the value of all securities and other assets of a Fund, deducting its liabilities, and dividing by the number of shares outstanding. Purchase orders must be received by the Insurance Company, as the agent of the Funds, by the close of the regular trading session of the NYSE on any given day in order to obtain that day’s NAV per share. Generally, the value of exchange-listed or exchange-traded securities is based on their respective market prices, bonds are valued based on prices provided by an independent pricing service and short-term debt securities are valued at amortized cost, which approximates market value.

The Board of Trustees has adopted procedures pursuant to which JNAM may determine, subject to Board verification, the “fair value” of a security for which a current market price is not available or the current market price is considered unreliable or inaccurate. Under these procedures, in general the “fair value” of a security shall be the amount, determined by JNAM in good faith that the owner of such security might reasonably expect to receive upon its current sale.

The Board of Trustees has established a pricing committee to review fair value determinations. The pricing committee will also review restricted and illiquid security values, securities and assets for which a current market price is not readily available, and securities and assets for which there is reason to believe that the most recent market price does not accurately reflect current value (e.g., disorderly market transactions) and determine/review fair values pursuant to the “Pricing Policies and Procedures” adopted by the Board of Trustees of the Trust.

The Acquiring Fund may invest in securities primarily listed on foreign exchanges and that trade on days when the Acquiring Fund does not price its shares. As a result, the Acquiring Fund’s NAV may change on days when shareholders are not able to purchase or redeem the Acquiring Fund’s shares.

Because the calculation of the Acquiring Fund’s NAV does not take place contemporaneously with the determination of the closing prices of the majority of foreign portfolio securities used in the calculation, there exists a risk that the value of foreign portfolio securities will change after the close of the exchange on which they are traded, but before calculation of the Acquiring Fund’s NAV (“time-zone arbitrage”). Accordingly, the Trust’s procedures for pricing of portfolio securities also authorize JNAM, subject to verification by the Trustees, to determine the “fair value” of such foreign securities for purposes of calculating the Acquiring Fund’s NAV. When fair valuing such foreign securities, JNAM will adjust the closing prices of all foreign securities held in the Acquiring Fund’s portfolio, based upon an adjustment factor for each such security provided by an independent pricing service, in order to reflect the “fair value” of such securities for purposes of determining the Acquiring Fund’s NAV. When fair-value pricing is employed, the foreign securities prices used to calculate the Acquiring Fund’s NAV may differ from quoted or published prices for the same securities.

These procedures seek to minimize the opportunities for time zone arbitrage in the Acquiring Fund that invests all or substantial portions of its assets in foreign securities, thereby seeking to make the Fund significantly less attractive to “market timers” and other investors who might seek to profit from time zone arbitrage and seeking to reduce the potential for harm to other Fund investors resulting from such practices. However, these procedures may not completely eliminate opportunities for time zone arbitrage because it is not possible to predict in all circumstances whether post-closing events will have a significant impact on securities prices.

All investments in the Trust are credited to the shareholder’s account in the form of full and fractional shares of the designated Fund (rounded to the nearest 1/1000 of a share). The Trust does not issue share certificates.

The interests of the Acquiring Fund’s long-term shareholders may be adversely affected by certain short-term trading activity by other Contract Owners invested in the Separate Accounts. Such short-term trading activity, when excessive, has the potential to interfere with efficient portfolio management, generate transaction and other costs, dilute the value of Acquiring Fund shares held by long-term shareholders and have other adverse effects on the Acquiring Fund. This type of excessive short-term trading activity is referred to herein as “market timing.” The Acquiring Fund is not intended as a vehicle for market timing. The Board of Trustees has adopted the policies and procedures set forth below with respect to frequent trading of Acquiring Fund shares.

The Acquiring Fund, directly and through its service providers, and the insurance company and qualified retirement plan service providers (collectively, “service providers”) with the cooperation of the insurance companies takes various steps designed to deter and curtail market timing. For example, regarding round trip transfers, redemptions by a shareholder from a sub-account investing in the Acquiring Fund is permitted; however, once a complete or partial redemption has been made from a sub-account that invests in the Acquiring Fund, through a sub-account transfer, shareholders will not be permitted to transfer any value back into that sub-account (and the Acquiring Fund) within fifteen (15) calendar days of the redemption. We will treat as short-term trading activity any transfer that is requested into a sub-account that was previously redeemed within the previous fifteen (15) calendar days, whether the transfer was requested by the shareholders or a third party authorized by the shareholder. The Insurance Companies have entered into agreements with the Trust to provide upon request certain information on the trading activities of Contract Owners in an effort to help curtail market timing.

In addition to identifying any potentially disruptive trading activity, the Acquiring Fund’s Board of Trustees has adopted a policy of “fair value” pricing to discourage investors from engaging in market timing or other excessive trading strategies for the Acquiring Fund. The Trust’s “fair value” pricing policy applies to all Funds where a significant event has occurred. The Acquiring Fund’s “fair value” pricing policy is described under “Investment in Trust Shares” above.

The practices and policies described above are intended to deter and curtail market timing in the Acquiring Fund. However, there can be no assurance that these policies, together with those of the Insurance Companies, and any other insurance company that may invest in the Acquiring Fund in the future, will be totally effective in this regard.

Investors redeem shares to make benefit or withdrawal payments under the terms of the Contracts or other arrangements. Redemptions typically are processed on any day on which the Trust and the NYSE are open for business and are effected at net asset value next determined after the redemption order, in proper form, is received by the Insurance Company. Redemption requests must be received by the Insurance Company, as the agent of the Funds, by the close of the regular trading session of the NYSE on any given business day in order to obtain that day’s NAV per share.

The Trust may suspend the right of redemption only under the following unusual circumstances:

| ● | When the New York Stock Exchange is closed (other than weekends and holidays) or trading is restricted; |

| ● | When an emergency exists, making disposal of portfolio securities or the valuation of net assets not reasonably practicable; or |

| ● | During any period when the SEC has by order permitted a suspension of redemption for the protection of shareholders. |

Dividends a

nd Other Distributions

The Funds generally distribute most or all of their net investment income and their net realized gains, if any, no less frequently than annually. Dividends and other distributions by a Fund are automatically reinvested at net asset value in shares of the distributing class of that Fund.

The Acquiring Fund intends to continue to qualify as a “regulated investment company” under Subchapter M of the Code. The Acquiring Fund intends to distribute all its net investment income and net capital gains to shareholders and, therefore, does not expect to be required to pay any federal income or excise taxes. The interests in the Acquiring Fund are owned by one or more Separate Accounts that hold such interests pursuant to Contracts and by various funds of the Trust and Jackson Variable Series Trust, which are regulated investment companies under Subchapter M of the Code, and by Jackson National.

The Acquiring Fund is treated as a corporation separate from the Trust for purposes of the Code. Therefore, the assets, income, and distributions of the Acquiring Fund are considered separately for purposes of determining whether or not the Acquiring Fund qualifies for treatment as a regulated investment company.

Because the shareholders of the Acquiring Fund are Separate Accounts of variable insurance contracts and certain other registered investment companies, there are no tax consequences to those shareholders from buying, holding, exchanging, and selling shares of the Acquiring Fund. Distributions from the Acquiring Fund are not taxable to those shareholders. However, owners of Contracts should consult the applicable Separate Account Prospectus for more detailed information on tax issues related to the Contracts.

The Acquiring Fund intends to comply with the diversification requirements currently imposed by the Code and U.S. Treasury regulations thereunder, on separate accounts of insurance companies as a condition of maintaining the tax-advantaged status of the Contracts issued by Separate Accounts. The Investment Advisory and Management Agreement and Sub-Advisory Agreement require the Acquiring Fund to be operated in compliance with these diversification requirements. The Sub-Adviser may depart from the investment strategy of the Acquiring Fund only to the extent necessary to meet these diversification requirements.

The financial highlights table is intended to help you understand the financial performance of the Acquired Fund and the Acquiring Fund for the period of the Acquired Fund’s and the Acquiring Fund’s operations. The total returns in the table represent the rate that an investor would have earned or lost on an investment in the Acquired Fund or the Acquiring Fund (assuming reinvestment of all dividends and distributions). The following table provides selected per share data for one share of the Acquired Fund and the Acquiring Fund. The information does not reflect any charges imposed under a Contract. If charges imposed under a variable contract were reflected, the returns would be lower. You should refer to the appropriate Contract prospectus regarding such charges.

The annual information below has been derived from financial statements audited by KPMG LLP, an independent registered public accounting firm, and should be read in conjunction with the financial statements and notes thereto, together with the report of KPMG LLP thereon, in the Annual Report. The information as of June 30, 3016 has not been audited. Each Fund’s financial statements are included in the Trust’s Annual and Semi-Annual Reports, which are available upon request.

JNL Series Trust

Financial Highlights

For a Share Outstanding

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Increase (Decrease) from

Investment Operations | | Distributions from | | | | | | | | Supplemental Data | | Ratios(a) | |

Period

Ended | | Net Asset Value, Beginning of Period | | Net Investment Income (Loss)(b) | | Net Realized & Unrealized Gains (Losses) | | Total from Investment Operations | | Net

Investment Income | | Net Realized Gains on Investment Transactions | | Net Asset Value, End

of Period | | Total Return(c) | | Net Assets,

End of

Period (in

thousands) | | Portfolio Turnover (d) | | Net Expenses to Average Net Assets | | Total Expenses to Average Net Assets | | Net Investment Income (Loss) to Average Net Assets | |

| JNL/Morgan Stanley Mid Cap Growth Fund |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 06/30/2016 | | $ | 11.86 | | $ | (0.01 | ) | $ | (0.70 | ) | $ | (0.71 | ) | $ | — | | $ | — | | $ | 11.15 | | | (5.99 | )% | | 211,818 | | | 14 | | | 1.08 | % | | 1.10 | % | | (0.18 | )% |

| 12/31/2015 | | | 12.95 | | | (0.09 | ) | | (0.48 | ) | | (0.57 | ) | | — | | | (0.52 | ) | | 11.86 | | | (4.32 | ) | | 236,038 | | | 24 | | | 1.10 | | | 1.10 | | | (0.66 | ) |

| 12/31/2014 | | | 13.13 | | | (0.06 | ) | | 0.01 | | | (0.05 | ) | | — | | | (0.13 | ) | | 12.95 | | | (0.40 | ) | | 214,231 | | | 75 | | | 1.10 | | | 1.10 | | | (0.49 | ) |

| 12/31/2013 | | | 9.55 | | | (0.06 | ) | | 3.66 | | | 3.60 | | | — | | | (0.02 | ) | | 13.13 | | | 37.73 | | | 209,418 | | | 41 | | | 1.10 | | | 1.10 | | | (0.48 | ) |

| 12/31/2012* | | | 10.00 | | | 0.04 | | | (0.45 | ) | | (0.41 | ) | | (0.04 | )(g) | | — | | | 9.55 | | | (4.13 | ) | | 17,008 | | | 28 | | | 1.11 | | | 1.11 | | | 0.59 | |

| Class B | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 06/30/2016 | | | 11.94 | | | 0.00 | | | (0.70 | ) | | (0.70 | ) | | — | | | — | | | 11.24 | | | (5.86 | ) | | 13 | | | 14 | | | 0.88 | | | 0.90 | | | 0.03 | |

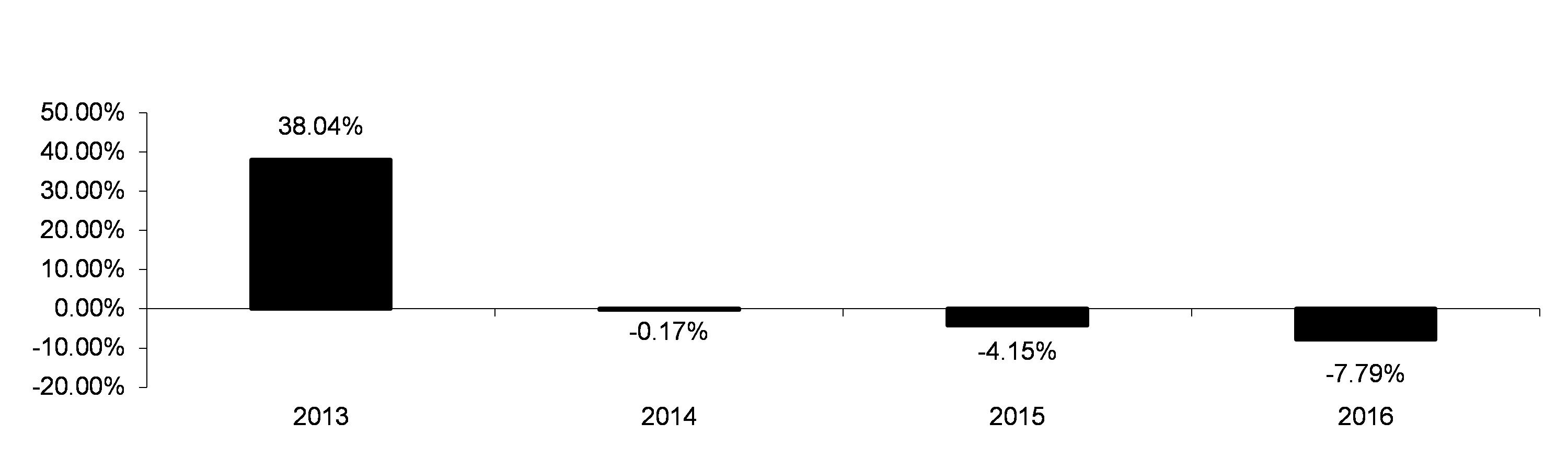

| 12/31/2015 | | | 13.01 | | | (0.06 | ) | | (0.49 | ) | | (0.55 | ) | | — | | | (0.52 | ) | | 11.94 | | | (4.15 | ) | | 14 | | | 24 | | | 0.90 | | | 0.90 | | | (0.47 | ) |

| 12/31/2014 | | | 13.16 | | | (0.04 | ) | | 0.02 | | | (0.02 | ) | | — | | | (0.13 | ) | | 13.01 | | | (0.17 | ) | | 136 | | | 75 | | | 0.90 | | | 0.90 | | | (0.28 | ) |

| 12/31/2013 | | | 9.55 | | | (0.01 | ) | | 3.64 | | | 3.63 | | | — | | | (0.02 | ) | | 13.16 | | | 38.04 | | | 133 | | | 41 | | | 0.90 | | | 0.90 | | | (0.12 | ) |

| 12/31/2012* | | | 10.00 | | | 0.05 | | | (0.45 | ) | | (0.40 | ) | | (0.05 | )(g) | | — | | | 9.55 | | | (4.05 | ) | | 96 | | | 28 | | | 0.91 | | | 0.91 | | | 0.86 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| JNL/T. Rowe Price Mid-Cap Growth Fund |

| Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

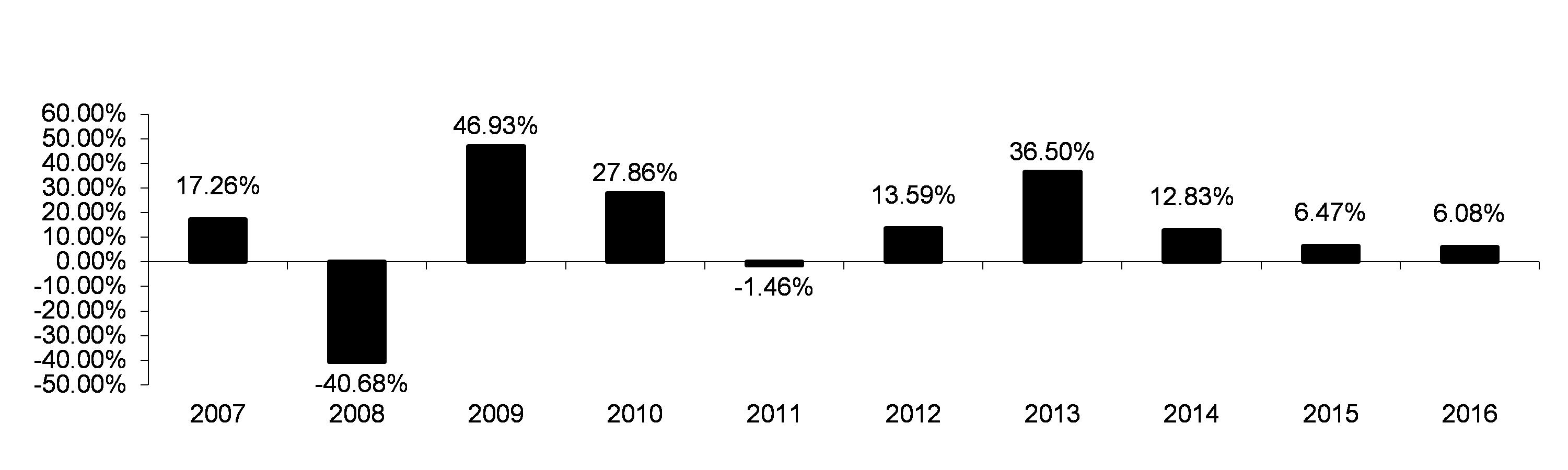

| 06/30/2016 | | | 37.87 | | | (0.02 | ) | | 0.55 | | | 0.53 | | | — | | | — | | | 38.40 | | | 1.40 | | | 3,649,611 | | | 11 | | | 1.00 | | | 1.00 | | | (0.10 | ) |

| 12/31/2015 | | | 38.87 | | | (0.10 | ) | | 2.58 | | | 2.48 | | | — | | | (3.48 | ) | | 37.87 | | | 6.47 | | | 3,635,887 | | | 31 | | | 1.00 | | | 1.00 | | | (0.25 | ) |

| 12/31/2014 | | | 37.47 | | | (0.14 | ) | | 4.98 | | | 4.84 | | | (0.06 | ) | | (3.38 | ) | | 38.87 | | | 12.83 | | | 2,992,442 | | | 30 | | | 1.01 | | | 1.01 | | | (0.36 | ) |

| 12/31/2013 | | | 29.14 | | | (0.13 | ) | | 10.74 | | | 10.61 | | | — | | | (2.28 | ) | | 37.47 | | | 36.50 | (f) | | 2,508,258 | | | 33 | | | 1.01 | | | 1.01 | | | (0.39 | ) |

| 12/31/2012 | | | 26.86 | | | (0.04 | ) | | 3.69 | | | 3.65 | | | (0.06 | ) | | (1.31 | ) | | 29.14 | | | 13.59 | | | 1,729,982 | | | 33 | | | 1.01 | | | 1.01 | | | (0.12 | ) |

| 12/31/2011 | | | 29.78 | | | (0.14 | ) | | (0.32 | ) | | (0.46 | ) | | (0.00 | )(e) | | (2.46 | ) | | 26.86 | | | (1.46 | ) | | 1,437,209 | | | 38 | | | 1.01 | | | 1.01 | | | (0.47 | ) |

| Class B | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

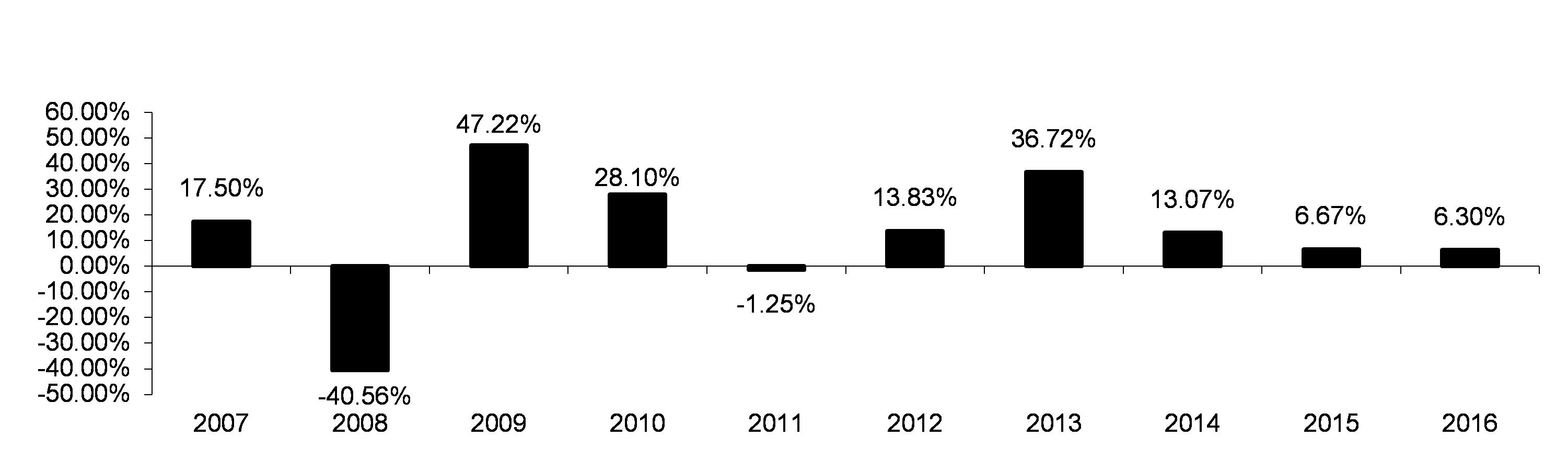

| 06/30/2016 | | | 39.23 | | | 0.02 | | | 0.58 | | | 0.60 | | | — | | | — | | | 39.83 | | | 1.53 | | | 71,034 | | | 11 | | | 0.80 | | | 0.80 | | | 0.10 | |

| 12/31/2015 | | | 40.07 | | | (0.02 | ) | | 2.66 | | | 2.64 | | | — | | | (3.48 | ) | | 39.23 | | | 6.67 | | | 71,922 | | | 31 | | | 0.80 | | | 0.80 | | | (0.06 | ) |

| 12/31/2014 | | | 38.45 | | | (0.06 | ) | | 5.12 | | | 5.06 | | | (0.06 | ) | | (3.38 | ) | | 40.07 | | | 13.07 | | | 64,631 | | | 30 | | | 0.81 | | | 0.81 | | | (0.16 | ) |

| 12/31/2013 | | | 29.81 | | | (0.07 | ) | | 10.99 | | | 10.92 | | | — | | | (2.28 | ) | | 38.45 | | | 36.72 | (f) | | 57,214 | | | 33 | | | 0.81 | | | 0.81 | | | (0.19 | ) |

| 12/31/2012 | | | 27.44 | | | 0.02 | | | 3.78 | | | 3.80 | | | (0.12 | ) | | (1.31 | ) | | 29.81 | | | 13.83 | | | 41,608 | | | 33 | | | 0.81 | | | 0.81 | | | 0.06 | |

| 12/31/2011 | | | 30.31 | | | (0.08 | ) | | (0.32 | ) | | (0.40 | ) | | (0.01 | ) | | (2.46 | ) | | 27.44 | | | (1.25 | ) | | 38,236 | | | 38 | | | 0.81 | | | 0.81 | | | (0.27 | ) |

| * | Commencement of operations were as follows: JNL/Morgan Stanley Mid Cap Growth Fund - April 30, 2012 |

| (a) | Annualized for periods less than one year. |

| (b) | Calculated using the average shares method. |

| (c) | Total return assumes reinvestment of all distributions for the period. Total return does not reflect payment of the expenses that apply to the variable accounts or any annuity charges. |

| (d) | Portfolio turnover is not annualized for periods of less than one year. |

| (e) | Amount represents less than $0.005. |

| (f) | Total return for the Fund includes class action settlement proceeds. The return for Class A and Class B, respectively, without the class action settlement proceeds was as follows: JNL/T. Rowe Price Mid-Cap Growth Fund - 36.47% and 36.69%. |

| (g) | Distribution amount for the JNL/Morgan Stanley Mid Cap Growth Fund includes a return of capital distribution for Class A and Class B shares of $0.01 and $0.01 per share, respectively, for the year ended December 31, 2012. |

Outstanding Shares and Principal Shareholders

[to be provided after February 24, 2017]

As of February 24, 2017, the Trustees and officers of the Trust, as a group, beneficially owned less than 1% of the outstanding shares of the Acquired Fund and Acquiring Fund.

Because the shares of the Funds are sold only to the Insurance Companies, certain funds of the Trust and the Jackson Variable Series Trust organized as funds-of-funds, and certain nonqualified retirement plans, the Insurance Companies, through the Separate Accounts which hold shares in the Trust as funding vehicles for the Contracts and certain retirement plans, are the owner of record of substantially all of the shares of the Trust. In addition, Jackson National, through its general account, is the beneficial owner of shares in certain of the Funds, in some cases representing the initial capital contributed at the inception of a Fund, and in other cases representing investments made for other corporate purposes. The table below shows the number of outstanding shares of the Acquired Fund as of the Record Date.

| Fund | Total Number of Outstanding Shares |

| Morgan Stanley Fund – Class A | [ ] |

| Morgan Stanley Fund – Class B | [ ] |

As of the Record Date, February 24, 2017, the following persons owned 5% or more of the shares of the Funds either beneficially or of record:

| Contract Owner’s Name/Address | Percent Ownership of Shares of the Fund | Percent Ownership of Shares of the Combined Fund (assuming the Reorganization occurs) |

| [ ] | [ ] | [ ] |

* * * * *

PLAN OF REORGANIZATION

JNL SERIES TRUST

JNL/MORGAN STANLEY MID CAP GROWTH FUND

JNL/T. ROWE PRICE MID-CAP GROWTH FUND

This Plan of Reorganization has been entered into on April 21, 2017, by JNL SERIES TRUST (the “Trust”), a Massachusetts business trust, on behalf of its JNL/MORGAN STANLEY MID CAP GROWTH FUND (the “Morgan Stanley Fund,” or the “Acquired Fund”) and JNL/T. ROWE PRICE MID-CAP GROWTH FUND (the “T. Rowe Price Fund,” or the “Acquiring Fund”).

WHEREAS, the Trust is registered with the U.S. Securities and Exchange Commission in accord with the provisions of the Investment Company Act of 1940, as amended (the “1940 Act”), each as an open-end management investment company, and each has established several separate series of shares (“funds”), with each fund having its own assets and investment policies;

WHEREAS, the Trust’s Board of Trustees, including a majority of the Trustees who are not interested persons of the Trust, has determined that the transaction described herein is fair and reasonable, that participation in the transaction described herein is in the best interests of the Acquired Fund, and that the interests of the existing shareholders of the Acquired Fund and the Acquiring Fund will not be diluted as a result of the transaction described herein;

WHEREAS, Article IV, Section 3 of the Trust’s Declaration of Trust, dated June 1, 1994 (the “Declaration of Trust”), authorizes the Board of Trustees to conduct the business of the Trust and carry on its operations;

WHEREAS, the Trust’s Board of Trustees, including a majority of the Trustees who are not interested persons of the Trust, has approved the reorganization of the Acquired Fund with and into the Acquiring Fund; and

WHEREAS, this Plan of Reorganization is intended to be and is adopted as a plan of reorganization within the meaning of Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”).

NOW, THEREFORE, all the assets, liabilities and interests of the Acquired Fund shall be transferred on the Closing Date to the Acquiring Fund, as described below; provided, however, that the Board of Trustees may terminate this Plan of Reorganization at or prior to the Closing Date:

| 1. | The Closing Date shall be April 21, 2017, or if the New York Stock Exchange or another primary trading market for portfolio securities of the Acquired Fund or the Acquiring Fund (each, an “Exchange”) is closed to trading or trading thereon is restricted, or trading or the reporting of trading on an Exchange or elsewhere is disrupted so that, in the judgment of the Board of Trustees, accurate appraisal of the value of either the Acquired Fund’s or the Acquiring Fund’s net assets and/or the net asset value per Class A share of Acquiring Fund shares is impracticable, the Closing Date shall be postponed until the first business day after the day when such trading has been fully resumed and such reporting has been restored; |

| 2. | On or before the Closing Date, and before effecting the reorganization transaction described herein, the Trust shall have received a satisfactory written opinion of legal counsel as to such transaction that the securities to be issued in connection with such transaction have been duly authorized and, when issued in accordance with this Plan of Reorganization, will have been validly issued and fully paid and will be non-assessable by the Trust on behalf of the Acquiring Fund. |

| 3. | In exchange for all of its shares of the Acquired Fund, each shareholder of such Acquired Fund shall receive a number of shares, including fractional shares, of the Acquiring Fund equal in dollar value to the number of whole and fractional shares that such shareholder owns in such Acquired Fund. Each shareholder of such Acquired Fund shall thereupon become a shareholder of the Acquiring Fund. |

| 4. | For purposes of this transaction, the value of the shares of the Acquiring Fund and the Acquired Fund shall be determined as of 4:00 p.m., Eastern Time, on the Closing Date. Those valuations shall be made in the usual manner as provided in the relevant prospectus of the Trust. |

| 5. | Upon completion of the foregoing transactions, the Acquired Fund shall be terminated and no further shares shall be issued by it. The classes of the Trust’s shares representing such Acquired Fund shall thereupon be closed and the shares previously authorized for those classes shall be reclassified by the Board of Trustees. The Trust’s Board of Trustees and management of the Trust shall take whatever actions may be necessary under Massachusetts law and the 1940 Act to effect the termination of the Acquired Fund. |

| 6. | The costs and expenses associated with the Reorganization relating to preparing, filing, printing and mailing of material, and related disclosure documents, and the costs and expenses related to obtaining a consent of independent registered public accounting firm will be borne by JNAM, and no sales or other charges will be imposed on Contract Owners in connection with the Reorganization. The legal fees incurred in connection with the analysis under the Code of the tax treatment of this transaction, will also be borne by Jackson National Asset Management, LLC. |

| 7. | The obligations of the Acquired Fund and the Acquiring Fund to complete the transactions described herein shall be subject to receipt by the Acquired Fund and the Acquiring Fund of an opinion of tax counsel substantially to the effect that, on the basis of existing provisions of the Code, U.S. Treasury Regulations promulgated thereunder, current administrative rules, pronouncements, and court decisions, and subject to certain qualifications, the Reorganization is more likely than not to qualify as a tax-free reorganization under Section 368(a)(1) of the Code. The delivery of such opinion is conditioned upon receipt by tax counsel of representations it shall request from the Acquired Fund and the Acquiring Fund. |

A copy of the Declaration of Trust is on file with the Secretary of the Commonwealth of Massachusetts. Notice is hereby given that this instrument is executed on behalf of the Trustees as Trustees, and is not binding on any of the Trustees, officers, or shareholders of the Trust individually, but only binding on the assets and properties of the Trust.

IN WITNESS WHEREOF, JNL Series Trust, on behalf of the JNL/Morgan Stanley Mid Cap Growth Fund and JNL/T. Rowe Price Mid-Cap Growth Fund has caused this Plan of Reorganization to be executed and attested in the City of Chicago, State of Illinois, on the date first written above.

| | JNL SERIES TRUST | |

| | | | |

| | By: | | |

| | | Mark D. Nerud, President and CEO | |

| | | | |

| | Attest: | | |

| | | Susan S. Rhee, Vice President | |

More Information on Strategies and Risk Factors

JNL/T. Rowe Price Mid-Cap Growth Fund

Class A and Class B

Investment Objective. The investment objective of the JNL/T. Rowe Price Mid-Cap Growth Fund is long-term growth of capital.

Principal Investment Strategies. The Fund seeks to achieve its objective by investing at least 80% of its assets (net assets plus the amount of any borrowings for investment purposes), under normal circumstances, in a broadly diversified portfolio of common stocks of medium-sized (mid-capitalization) companies whose earnings T. Rowe Price Associates, Inc. (“T. Rowe” or “Sub-Adviser”) expects to grow at a faster rate than the average company. The Sub-Adviser defines mid-capitalization companies as those whose market capitalization, at the time of acquisition by the Fund, falls within the capitalization range of companies in the S&P Mid Cap 400 Index or Russell MidCap® Growth Index. As of December 31, 2015, the market capitalization range for the S&P Mid Cap 400 is $661.41 million to $12,586.61 million. As of December 31, 2015, the market capitalization range for the Russell MidCap Growth is $715.58 million to $30,429.31 million. The market capitalization of companies in the Fund’s portfolio and the Standard & Poor’s and Russell indices changes over time. However, the Fund will not automatically sell or cease to purchase stock of a company it already owns just because the company’s market capitalization subsequently grows or otherwise falls outside these ranges. As a growth investor, the Sub-Adviser believes that when a company increases its earnings faster than both inflation and the overall economy, the market will eventually reward it with a higher stock price.

Depending upon cash flows into and out of the Fund, the Adviser may direct up to 20% of the portfolio be invested in a mid-capitalization growth index strategy (“index sleeve”) managed by Mellon Capital Management Corporation (“Mellon Capital”). For the index sleeve, Mellon Capital does not employ traditional methods of active investment management, which involves the buying and selling of individual securities based upon security analysis. The index sleeve attempts to replicate the Russell MidCap® Growth Index by investing all or substantially all of its assets in the stocks that make up the Russell MidCap® Growth Index in proportion to their market capitalization weighting in the Russell MidCap® Growth Index.

The index sleeve managed by Mellon Capital attempts to replicate the Russell MidCap® Growth Index by replicating a majority of the Russell MidCap® Growth Index and sampling from the securities remaining in the index. To the extent that the Fund seeks to replicate the Russell MidCap® Growth Index using sampling techniques, a close correlation between the Fund’s performance and the performance of the Russell MidCap® Growth Index may be anticipated in both rising and falling markets. The Fund may invest in derivative instruments to manage cash flows and to equitize dividend accruals.

In addition, the Fund on occasion will purchase stocks of some larger and smaller companies that have qualities consistent with the portfolio’s core characteristics but whose market capitalization is outside the capitalization range of mid-capitalization companies (as defined above) at the time of purchase. The Fund may also invest up to 25% of its total assets (excluding reserves) in foreign securities.

Stock selection is based on a combination of fundamental bottom-up analysis in an effort to identify companies with superior long-term appreciation prospects. In addition, a portion of the portfolio will be invested using T. Rowe Price’s fundamental research. The Portfolio will be broadly diversified, and this should help to mitigate the downside risk attributable to any single poorly-performing security on overall fund performance.

As Sub-Adviser to the Fund, T. Rowe Price generally favor companies with one or more of the following selects stocks using a growth approach and looks for companies that have:

| · | A demonstrated potential to sustain earnings growth; |

| · | A record of above-average earnings growth; |

| · | Connection to an industry experiencing increasing demand; |

| · | Proven products or services; or |

| · | Stock prices that appear to undervalue their growth prospects. |

In pursuing its investment objective, the Fund’s Sub-Adviser has the discretion to deviate from its normal investment criteria, as described above, and purchase securities that it believes may provide an opportunity for a substantial appreciation. These situations might arise when the Fund’s Sub-Adviser believes a security could increase in value for a variety of reasons including a change in management, an extraordinary corporate event, a new product introduction or innovation, or a favorable competitive development.

Principal Risks of Investing in the Fund. An investment in the Fund is not guaranteed. As with any mutual fund, the value of the Fund’s shares will change, and you could lose money by investing in the Fund. The following descriptions of the principal risks do not provide any assurance either of the Fund’s investment in any particular type of security, or assurance of the Fund’s success in its investment selections, techniques and risk assessments. As a managed portfolio the Fund may not achieve its investment objective for a variety of reasons including changes in the financial condition of issuers (due to such factors as management performance, reduced demand or overall market changes), fluctuations in the financial markets, declines in overall securities prices, or the Sub-Adviser’s investment techniques otherwise failing to achieve the Fund’s investment objective. The principal risks of investing in the Fund include:

| · | Mid-capitalization investing risk |

Please see the “Glossary of Risks” section, which is set forth before the “Management of the Trust” section, for a description of these risks. There may be other risks that are not listed in this Prospectus that could cause the value of your investment in the Fund to decline and that could prevent the Fund from achieving its stated investment objective. This Prospectus does not describe all of the risks of every technique, investment strategy or temporary defensive position that the Fund may use. For additional information regarding the risks of investing in the Fund, please refer to the SAI.

Additional Information About the Other Investment Strategies, Other Investments and Risks of the Fund (Other than Principal Strategies/Risks). The Fund may also invest in securities other than U.S. common stocks, including foreign securities (up to 25% of its assets, excluding reserves), futures and options, convertible securities, preferred stock, registered investment companies, REITs, partnerships, illiquid securities, and warrants, in keeping with Fund objectives. The Fund may also invest in hybrid instruments (up to 10% of total assets).

There may be additional risks that may affect the Fund’s ability to achieve its stated investment objective. Those additional risks are:

| · | Temporary defensive positions and large cash positions risk |

JNL/Morgan Stanley Mid Cap Growth Fund

Class A and Class B

Investment Objective. The investment objective of the JNL/Morgan Stanley Mid Cap Growth Fund is to seek long-term capital growth.

Principal Investment Strategies. Under normal circumstances, at least 80% of the Fund’s assets will be invested in equity securities of mid-capitalization companies. The Portfolio may also use derivative instruments as discussed in this prospectus. These derivative instruments will be counted toward the 80% policy discussed above to the extent they have economic characteristics similar to the securities included within that policy.

The Sub-Adviser seeks long-term capital growth by investing primarily in established and emerging companies with capitalizations within the range of companies included in the Russell MidCap® Growth Index.

The Fund may invest up to 25% of its net assets in securities of foreign issuers, including issuers located in emerging market or developing countries. The Sub-Adviser considers an issuer to be from a particular country if (i) its principal securities trading market is in that country; (ii) alone or on a consolidated basis it derives 50% or more of its annual revenue from goods produced, sales made or services performed in that country; or (iii) it is organized under the laws of, or has a principal office in that country. By applying these tests, it is possible that a particular company could be deemed to be from more than one country. The securities in which the Fund may invest may be denominated in U.S. dollars or in currencies other than U.S. dollars.

The Sub-Adviser emphasizes a bottom-up stock selection process, seeking attractive investments on an individual company basis. The Sub-Adviser seeks to invest in high quality companies it believes have sustainable competitive advantages and the ability to redeploy capital at high rates of return. The Sub-Adviser typically favors companies with rising returns on invested capital, above average business visibility, strong free cash flow generation and what the Sub-Adviser believes to be an attractive risk/reward ratio. The Sub-Adviser generally considers selling a portfolio holding when it determines that the holding no longer satisfies its investment criteria.

In accordance with the Fund’s investment strategy of investing in mid cap companies, the capitalization range of securities in which the Fund may invest is consistent with the capitalization range of the Russell Midcap® Growth Index, which as of December 31, 2015 was between $201.8 million and $28.85 billion. The market capitalization limit is subject to adjustment annually based upon the Sub-Adviser’s assessment as to the capitalization range of companies which possess the fundamental characteristics of mid cap companies. The Fund may invest in convertible securities. The Fund may also invest in privately placed and restricted securities. The Fund may invest in foreign currency forward exchange contracts, which are derivatives, in connection with its investments in foreign securities.

Principal Risks of Investing in the Fund. An investment in the Fund is not guaranteed. As with any mutual fund, the value of the Fund’s shares will change, and you could lose money by investing in the Fund. The following descriptions of the principal risks do not provide any assurance either of the Fund’s investment in any particular type of security, or assurance of the Fund’s success in its investment selections, techniques and risk assessments. As a managed portfolio the Fund may not achieve its investment objective for a variety of reasons including changes in the financial condition of issuers (due to such factors as management performance, reduced demand or overall market changes), fluctuations in the financial markets, declines in overall securities prices, or the Sub-Adviser’s investment techniques otherwise failing to achieve the Fund’s investment objective. The principal risks of investing in the Fund include:

| · | Convertible securities risk |

| · | Emerging markets and less developed countries risk |

| · | Forward foreign currency exchange contracts risk |

| · | Mid-capitalization investing risk |

| · | Privately-placed securities risk |

| · | Restricted securities risk |

Please see the “Glossary of Risks” section, which is set forth before the “Management of the Trust” section, for a description of these risks. There may be other risks that are not listed in this Prospectus that could cause the value of your investment in the Fund to decline and that could prevent the Fund from achieving its stated investment objective. This Prospectus does not describe all of the risks of every technique, investment strategy or temporary defensive position that the Fund may use. For additional information regarding the risks of investing in the Fund, please refer to the SAI.

Additional Information About the Other Investment Strategies, Other Investments and Risks of the Fund (Other than Principal Strategies/Risks). There may be additional risks that may affect the Fund’s ability to achieve its stated investment objective. Those additional risks are:

| · | Depositary receipts risk |

| · | Foreign exchange and currency derivatives trading risk |

| · | Forward and futures contract risk |

| · | Hedging investments risk |

| · | Investments in IPOs risk |

| · | Real estate investment risk |

| · | Structured investments risk |

| · | Temporary defensive positions and large cash positions risk |

Glossary of Risks

Company risk – Investments in U.S. and/or foreign-traded equity securities may fluctuate more than the values of other types of securities in response to changes in a particular company’s financial condition. For example, poor earnings performance of a company may result in a decline of its stock price.

Convertible securities risk – Convertible securities have investment characteristics of both equity and debt securities. Investments in convertible securities may be subject to market risk, credit and counterparty risk, interest rate risk and other risks associated with investments in equity and debt securities, depending on the price of the underlying security and the conversion price. While equity securities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. A convertible security is also subject to the same types of market and issuer-specific risks that apply to the underlying common stock, since it derives a portion of its value from the common stock into which it may be converted. In addition, because companies that issue convertible securities are often small- or mid-capitalization companies, to the extent the Fund invests in convertible securities, it will be subject to the risks of investing in these companies.

The value of convertible and debt securities may fall when interest rates rise. Securities with longer durations tend to be more sensitive to changes in interest rates, generally making them more volatile than securities with shorter durations. Convertible securities normally are “junior” securities, which means that an issuer usually must pay interest on its non-convertible debt before it can make payments on its convertible securities. If an issuer stops making interest or principal payments, these securities may become worthless and the Fund could lose its entire investment. In the event of a liquidation of the issuing company, holders of convertible securities may be paid before the company’s common stockholders but after holders of any senior debt obligations of the company. Due to their hybrid nature, convertible securities are typically more sensitive to changes in interest rates than the underlying common stock, but less sensitive than a fixed rate corporate bond.

Counterparty risk – Transactions involving a counterparty are subject to the credit risk of the counterparty. A Fund that enters into contracts with counterparties, such as repurchase or reverse repurchase agreements or over-the-counter (“OTC”) derivatives contracts, or that lends its securities, runs the risk that the counterparty will be unable or unwilling to make timely settlement payments or otherwise honor its obligations. If a counterparty fails to meet its contractual obligations, files for bankruptcy, or otherwise experiences a business interruption, the Fund could miss investment opportunities or otherwise hold investments it would prefer to sell, resulting in losses for the Fund. Counterparty risk is heightened during unusually adverse market conditions.

Participants in OTC derivatives markets typically are not subject to the same level of credit evaluation and regulatory oversight as are members of exchange-based markets, and, therefore, OTC derivatives generally expose a Fund to greater counterparty risk than exchange-traded derivatives. A Fund is subject to the risk that a counterparty will not settle a derivative in accordance with its terms because of a dispute over the terms of the contract (whether or not bona fide) or

because of a credit or liquidity problem. If a counterparty’s obligation to a Fund is not collateralized, then the Fund is essentially an unsecured creditor of the counterparty. If a counterparty defaults, the Fund will have contractual remedies, but the Fund may be unable to enforce them, which may cause the Fund to suffer a loss. Counterparty risk is greater for derivatives with longer maturities because there is more time for events to occur that may prevent settlement. Counterparty risk also is greater when a Fund has concentrated its derivatives with a single or small group of counterparties. Counterparty risk still exists even if a counterparty’s obligations are secured by collateral because the Fund’s interest in the collateral may not be perfected or additional collateral may not be promptly posted as required.

A Fund also is subject to counterparty risk because it executes its securities transactions through brokers and dealers. If a broker or dealer fails to meet its contractual obligations, goes bankrupt, or otherwise experiences a business interruption, the Fund could miss investment opportunities or be unable to dispose of investments it would prefer to sell, resulting in losses for the Fund.

Counterparty risk with respect to derivatives will be affected by rules and regulations affecting the derivatives market. Some derivatives transactions are required to be centrally cleared, and a party to a cleared derivatives transaction is subject to the credit risk of the clearing house and the clearing member through which it holds its cleared position, rather than the credit risk of its original counterparty to the derivatives transaction. Credit risk of market participants with respect to derivatives that are centrally cleared is concentrated in a few clearing houses, and it is not clear how an insolvency proceeding of a clearing house would be conducted and what impact an insolvency of a clearing house would have on the financial system. A clearing member is obligated by contract and by applicable regulation to segregate all funds received from customers with respect to cleared derivatives transactions from the clearing member’s proprietary assets. However, all funds and other property received by a clearing member from its customers with respect to cleared derivatives are generally held by the clearing member on a commingled basis in an omnibus account, and the clearing member may invest those funds in certain instruments permitted under the applicable regulations. Therefore, a Fund might not be fully protected in the event of the bankruptcy of a Fund’s clearing member because the Fund would be limited to recovering only a pro rata share of all available funds segregated on behalf of the clearing member’s customers for a relevant account class. Also, the clearing member is required to transfer to the clearing house the amount of margin required by the clearing house for cleared derivatives, which amounts are generally held in an omnibus account at the clearing house for all customers of the clearing member. Regulations promulgated by the CFTC require that the clearing member notify the clearing house of the initial margin provided by the clearing member to the clearing house that is attributable to each customer. However, if the clearing member does not accurately report a Fund’s initial margin, the Fund is subject to the risk that a clearing house will use the Fund’s assets held in an omnibus account at the clearing house to satisfy payment obligations of a defaulting customer of the clearing member to the clearing house. In addition, clearing members generally provide the clearing house the net amount of variation margin required for cleared swaps for all of its customers in the aggregate, rather than individually for each customer. A Fund is therefore subject to the risk that a clearing house will not make variation margin payments owed to the Fund if another customer of the clearing member has suffered a loss and is in default, and the risk that the Fund will be required to provide additional variation margin to the clearing house before the clearing house will move the Fund’s cleared derivatives transactions to another clearing member. In addition, if a clearing member does not comply with the applicable regulations or its agreement with a Fund, or in the event of fraud or misappropriation of customer assets by a clearing member, the Fund could have only an unsecured creditor claim in an insolvency of the clearing member with respect to the margin held by the clearing member.

Currency risk – Investments in foreign currencies, securities that trade in or receive revenues in foreign currencies or derivatives that provide exposure to foreign currencies are subject to the risk that those currencies may decline in value, or, in the case of hedging positions, that the currency may decline in value relative to the currency being hedged. Currency exchange rates can be volatile and may be affected by a number of factors, such as the general economics of a country, the actions (or inaction) of U.S. and foreign governments or central banks, the imposition of currency controls, and speculation. The Fund accrues additional expenses when engaging in currency exchange transactions, and valuation of a Fund’s foreign securities may be subject to greater risk because both the price of the currency (relative to the U.S. dollar) and the price of the security may fluctuate with market and economic conditions. A decline in the value of a foreign currency versus the U.S. dollar reduces the value in U.S. dollars of investments denominated in that foreign currency.

Cybersecurity risk - Cyber attacks could disrupt daily operations related to trading and portfolio management. In addition, technology disruptions and cyber attacks may impact the operations or securities prices of an issuer or a group of issuers, and thus may have an adverse impact on the value of the Fund’s investments. Cyber attacks on the Funds’ sub-advisers and service providers could cause business failures or delays in daily processing, and the Funds may not be able to issue a NAV per share. Cyber attacks could impact the performance of the Funds. See the “Technology Disruptions” section in this Prospectus.

Depositary receipts risk – Investments in securities of foreign companies in the form of American Depositary Receipts (“ADRs”), Global Depositary Receipts (“GDRs”), and European Depositary Receipts (“EDRs”) are subject to certain risks. ADRs typically are issued by a U.S. bank or trust company and evidence ownership of underlying securities issued by a foreign corporation. EDRs and GDRs typically are issued by foreign banks or trust companies, although they may be issued by U.S. banks or trust companies, and evidence ownership of underlying securities issued by either a foreign or U.S. corporation. Where the custodian or similar financial institution that holds the issuer’s shares in a trust account is located in a country that does not have developed financial markets, a Fund could be exposed to the credit risk of the custodian or financial institution and greater market risk. In addition, the depository institution may not have physical custody of the underlying securities at all times and may charge fees for various services, including forwarding dividends and interest and corporate actions. A Fund would be expected to pay a share of the additional fees, which it would not pay if investing directly in the foreign securities. A Fund may experience delays in receiving its dividend and interest payments or exercising rights as a shareholder.

Depositary receipts may be issued in sponsored or un-sponsored programs. In a sponsored program, a security issuer has made arrangements to have its securities traded in the form of depositary receipts. In an un-sponsored program, the issuer may not be directly involved in the creation of the program. Although the U.S. regulatory requirements applicable to ADRs generally are similar for both sponsored and un-sponsored programs, in some cases it may be easier to obtain financial and other information from an issuer that has participated in the creation of a sponsored program. To the extent the Fund invests in depositary receipts of an un-sponsored program, there may be an increased possibility the Fund would not become aware of and be able to respond to corporate actions such as stock splits or rights offerings involving the foreign issuer on a timely basis, as the issuers of unsponsored depositary receipts are not obligated to disclose information that is considered material in the U.S.

Depositary receipts involve many of the same risks as direct investments in foreign securities. These risks include: fluctuations in currency exchange rates, which are affected by international balances of payments and other economic and financial conditions; government intervention; and, speculation. With respect to certain foreign countries, there is the possibility of expropriation or nationalization of assets, confiscatory taxation, political and social upheaval, and economic instability. Investments in depositary receipts that are traded over the counter may also subject a Fund to liquidity risk.

Derivatives risk – Certain Funds may invest in derivatives, which are financial instruments whose value depends on, or is derived from, the value of underlying assets, reference rates, or indices. Derivatives can be highly volatile and may be subject to transaction costs and certain risks, such as unanticipated changes in securities prices and global currency investment. Derivatives also are subject to a number of risks described elsewhere in this section, such as leverage risk, liquidity risk, interest rate risk, market risk, counterparty risk, and credit risk. They also involve the risk of mispricing or improper valuation and the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset, interest rate or index. Gains or losses from derivatives can be substantially greater than the derivatives’ original cost. Certain derivatives transactions may subject the Fund to counterparty risk.

The Fund’s investment manager must choose the correct derivatives exposure versus the underlying assets to be hedged or the income to be generated, in order to realize the desired results from the investment. The Fund’s investment manager must also correctly predict price, credit or their applicable movements, during the life of a derivative, with respect to the underlying asset in order to realize the desired results from the investment.

The Fund could experience losses if its derivatives were poorly correlated with its other investments, or if the Fund were unable to liquidate its position because of an illiquid secondary market. The market for many derivatives is, or suddenly can become, illiquid. Changes in liquidity may result in significant, rapid and unpredictable changes in the prices for derivatives. The value of derivatives may fluctuate more rapidly than other investments, which may increase the volatility of the Fund, depending on the nature and extent of the derivatives in the Fund’s portfolio.

If the Fund’s investment manager uses derivatives in attempting to manage or “hedge” the overall risk of the portfolio, the strategy might not be successful and the Fund may lose money. To the extent that the Fund is unable to close out a position because of market illiquidity or counterparty default, the Fund may not be able to prevent further losses of value in its derivatives holdings and the Fund’s liquidity may be impaired to the extent that it has a substantial portion of its otherwise liquid assets marked as segregated on its books to cover its obligations under such derivative instruments.

The Fund may also be required to take or make delivery of an underlying instrument that the manager would otherwise have attempted to avoid. Investors should bear in mind that, while a Fund may intend to use derivative strategies on a regular basis, it is not obligated to actively engage in these transactions, generally or in any particular kind of derivative, if the investment manager elects not to do so due to availability, cost or other factors.

The Fund’s use of derivative instruments may involve risks different from, or possibly greater than, the risks associated with investing directly in securities and other more traditional investments. Certain derivative transactions may have a leveraging effect on the Fund. For example, a small investment in a derivative instrument may have a significant impact on the Fund’s exposure to interest rates, currency exchange rates or other investments. As a result, a relatively small price movement in a derivative instrument may cause an immediate and substantial loss or gain. The Fund may engage in such transactions regardless of whether the Fund owns the asset, instrument or components of the index underlying the derivative instrument. The Fund may invest a portion of its assets in these types of instruments, which could cause the Fund’s investment exposure to exceed the value of its portfolio securities and its investment performance could be affected by securities it does not own.

The U.S. government has enacted legislation that provides for new regulation of the derivatives market, including clearing, margin, reporting, and registration requirements. The CFTC, SEC and other federal regulators have been tasked with developing the rules and regulations enacting the provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”). While certain of the rules are effective, other rules are not yet final and/or effective, so its ultimate impact remains unclear. The Dodd-Frank Act substantially increased regulation of the over-the-counter derivatives market and participants in that market, imposing various requirements on transactions involving instruments that fall within the Dodd-Frank Act’s definition of “swap” and “security-based swap.” It is possible that government regulation of various types of derivative instruments could potentially limit or completely restrict the ability of a Fund to use these instruments as a part of its investment strategy, increase the costs of using these instruments or make them less effective. Limits or restrictions applicable to the counterparties with which a Fund engages in derivative transactions could also prevent a Fund from using these instruments or affect the pricing or other factors relating to these instruments, or may change availability of certain investments.

The CFTC and certain futures exchanges have established limits, referred to as “position limits,” on the maximum net long or net short positions which any person or entity may hold or control in particular options and futures contracts (and certain related swap positions). All positions owned or controlled by the same person or entity, even if in different accounts, may be aggregated for purposes of determining whether the applicable position limits have been exceeded and, as a result, the investment manager’s trading decisions may have to be modified or positions held by a Fund may have to be liquidated in order to avoid exceeding such limits. Even if the Fund does not intend to exceed applicable position limits, it is possible that different clients managed by the investment manager or its affiliates may be aggregated for this purpose. The modification of investment decisions or the elimination of open positions, if it occurs, may adversely affect the profitability of the Fund.

Under the Dodd-Frank Act, a Fund also may be subject to additional recordkeeping and reporting requirements. In addition, the tax treatment of certain derivatives, such as swaps, is unclear under current law and may be subject to future legislation, regulation or administrative pronouncements issued by the IRS. Other future regulatory developments may also impact a Fund’s ability to invest or remain invested in certain derivatives. Legislation or regulation may also change the way in which a Fund itself is regulated. The investment manager cannot predict the effects of any new governmental regulation that may be implemented or the ability of a Fund to use swaps or any other financial derivative product, and there can be no assurance that any new governmental regulation will not adversely affect a Fund’s ability to achieve its investment objective.

Emerging markets and less developed countries risk – Emerging market and less developed countries generally are located in Asia, the Middle East, Eastern Europe, Central and South America and Africa. Investments in, or exposure to, securities that are tied economically to emerging market and less developed countries are subject to all of the risks of investments in, or exposure to, foreign securities, generally to a greater extent than in developed markets, among other risks. Investments in securities that are tied economically to emerging markets involve greater risk from economic and political systems that typically are less developed, and likely to be less stable, than those in more advanced countries. The Fund also will be subject to the risk of adverse foreign currency rate fluctuations. Emerging market and less developed countries may also have economies that are predominantly based on only a few industries or dependent on revenues from particular commodities. There may be government policies that restrict investment by foreigners, greater government influence over the private sector, and a higher risk of a government taking private property in emerging and less developed countries. Moreover, economies of emerging market countries may be dependent upon international trade and may be adversely affected by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries with which they trade. As a result of these risks, investments in securities tied economically to emerging markets tend to be more volatile than investments in securities of developed countries.

Underdeveloped securities exchanges and low or nonexistent trading volume in securities of issuers may result in a lack of liquidity and in price volatility. Emerging market countries often have less uniformity in accounting and reporting

requirements and less reliable clearance and settlement, registration and custodial procedures, which could result in ownership registration being completely lost. Issuers in emerging markets typically are subject to greater risk of adverse changes in earnings and business prospects than are companies in developed markets. Loss may also result from the imposition of exchange controls, confiscations and other government restrictions, including confiscatory taxes on investment proceeds and other restrictions on the ability of foreign investors to withdraw their money at will, or from problems in security registration or settlement and custody. Investments in, or exposure to, emerging market securities may be more susceptible to investor sentiment than investments in developed countries. As a result, emerging market securities may be adversely affected by negative perceptions about an emerging market country’s stability and prospects for continued growth. The Fund will also be subject to the risk of negative foreign currency rate fluctuations. Investments in, or exposure to, emerging market securities tend to be more volatile than investments in developed countries.

Frontier market countries are emerging market countries that are considered to be among the smallest, least mature and least liquid. Frontier market countries generally have smaller economies and less developed capital markets than traditional emerging markets, and, as a result, the risks of investing in emerging market countries are magnified in frontier market countries. The economies of frontier market countries are less correlated to global economic cycles than those of their more developed counterparts and their markets have low trading volumes and the potential for extreme price volatility and illiquidity. This volatility may be further heightened by the actions of a few major investors. For example, a substantial increase or decrease in cash flows of mutual funds investing in these markets could significantly affect local stock prices and, therefore, the price of Fund shares. These factors make investing in frontier market countries significantly riskier than in other countries and any one of them could cause the price of the Fund’s shares to decline.

Equity securities risk – Common and preferred stocks represent equity ownership in a company. Stock markets are volatile, and equity securities generally have greater price volatility than fixed-income securities. The price of equity or equity-related securities will fluctuate and can decline and reduce the value of a portfolio investing in equity or equity-related securities. The value of equity or equity-related securities purchased by the Fund could decline if the financial condition of the companies the Fund invests in decline or if overall market and economic conditions deteriorate. They may also decline due to factors that affect a particular industry or industries, such as labor shortages or an increase in production costs and competitive conditions within an industry. In addition, they may decline due to general market conditions that are not specifically related to a company or industry, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates or generally adverse investor sentiment.

Fixed-income risk – The price of fixed-income securities responds to economic developments, particularly interest rate changes, as well as to perceptions about the credit risk of individual issuers. Rising interest rates generally will cause the price of bonds and other fixed-income debt securities to fall. In addition, falling interest rates may cause an issuer to redeem, call or refinance a security before its stated maturity, which may result in the Fund having to reinvest the proceeds in lower yielding securities. Longer maturity fixed-income securities may be subject to greater price fluctuations than shorter maturity fixed-income securities. Bonds and other fixed-income debt securities are subject to credit risk, which is the possibility that the credit strength of an issuer will weaken and/or an issuer of a fixed income security will fail to make timely payments of principal or interest and the security will go into default. The Fund may be subject to a greater risk of rising interest rates in periods of historically low rates.

Foreign exchange and currency derivatives trading risk – The Fund intends to actively trade in spot and forward currency positions and related currency derivatives in order to increase the value of the Fund. The trading of foreign currencies directly generates risks separate from those associated with inactive or indirect exposures to non-U.S. dollar denominated instruments and currency derivative instruments. Specifically, the Fund may directly take a loss from the buying and selling of currencies without any related exposure to non-U.S. dollar-denominated assets.

Foreign regulatory risk – The Adviser is an indirect wholly-owned subsidiary of Prudential plc, a publicly-traded company incorporated in the United Kingdom and is not affiliated in any manner with Prudential Financial Inc., a company whose principal place of business is in the United States of America. Through its ownership structure, the Adviser has a number of global financial industry affiliates. As a result of this structure, and the asset management and financial industry business activities of the Adviser and its affiliates, the Adviser and the Fund may be prohibited or limited in effecting transactions in certain securities. Additionally, the Adviser and the Fund may encounter trading limitations or restrictions because of aggregation issues or other foreign regulatory requirements. Foreign regulators or foreign laws may impose position limits on securities held by the Fund, and the Fund may be limited as to which securities they may purchase or sell, as well as the timing of such purchases or sales. These foreign regulatory limits may increase the Fund’s expenses and may limit the Fund’s performance.

Foreign securities risk – Investments in, or exposure to, foreign securities involve risks not typically associated with U.S. investments. These risks include, among others, adverse fluctuations in foreign currency values, possible imposition of foreign withholding or other taxes on income payable on the securities, as well as adverse political, social and economic developments, such as political upheaval, acts of terrorism, financial troubles, or natural disasters. Many foreign securities markets, especially those in emerging market countries, are less stable, smaller, less liquid, and less regulated than U.S. securities markets, and the costs of trading in those markets is often higher than in U.S. securities markets. There may also be less publicly-available information about issuers of foreign securities compared to issuers of U.S. securities and foreign issuers may not be subject to the same accounting, auditing and financial recordkeeping standards and requirements as domestic issuers. In addition, the economies of certain foreign markets may not compare favorably with the economy of the United States with respect to issues such as growth of gross national product, reinvestment of capital, resources and balance of payments position. Such factors may adversely affect the value of securities issued by companies in foreign countries or regions.