File No. 333-[ ]

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON MAY 14, 2018

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [ ]

Post-Effective Amendment No. [ ]

JNL Series Trust

(Exact Name of Registrant as Specified in Charter)

1 Corporate Way

Lansing, Michigan 48951

(Address of Principal Executive Offices)

(517) 381-5500

(Registrant’s Area Code and Telephone Number)

225 West Wacker Drive

Chicago, Illinois 60606

(Mailing Address)

With copies to:

EMILY J. BENNETT, ESQ. JNL Series Trust 1 Corporate Way Lansing, Michigan 48951 | PAULITA PIKE, ESQ. Ropes & Gray LLP 191 North Wacker Drive Chicago, Illinois 60606 |

Approximate Date of Proposed Public Offering:

As soon as practicable after this Registration Statement becomes effective.

It is proposed that this Registration Statement will become effective on June 18, 2018, pursuant to Rule 488 under the Securities Act of 1933, as amended.

Title of securities being registered: Class A and Class I Shares of beneficial interest in the series of the registrant designated as the JNL/PIMCO Real Return Fund.

No filing fee is required because the registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of shares (File Nos. 033-87244 and 811-08894).

JNL SERIES TRUST

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Contract Owners

Notice of Special Meeting

Contract Owner Voting Instructions

Part A - Proxy Statement/Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibits

JACKSON NATIONAL LIFE INSURANCE COMPANY

JACKSON NATIONAL LIFE INSURANCE COMPANY OF NEW YORK

1 Corporate Way

Lansing, Michigan 48951

June 18, 2018

Dear Contract Owner:

Enclosed is a notice of a Special Meeting of Shareholders of the JNL Real Assets Fund (the “Real Assets Fund” or the “Acquired Fund”), a series of the Jackson Variable Series Trust (“JVST”). The Special Meeting of Shareholders of the Acquired Fund is scheduled to be held at the offices of Jackson National Life Insurance Company, 1 Corporate Way, Lansing, Michigan, 48951, on July 12, 2018, at 9:00 a.m., Eastern Time (the “Meeting”). At the Meeting, the shareholders of the Acquired Fund will be asked to approve the proposal described below.

JVST’s Board of Trustees (the “JVST Board”) called the Meeting to request shareholder approval of the reorganization (the “Reorganization”) of the Acquired Fund into the JNL/PIMCO Real Return Fund (the “Acquiring Fund”), a series of the JNL Series Trust (“JNLST”).

The JVST Board, after careful consideration, approved the Reorganization. After considering the recommendation of Jackson National Asset Management, LLC (“JNAM”), the investment adviser to the Funds, the JVST Board concluded that: (i) the Reorganization will benefit the shareholders of the Acquired Fund; (ii) the Reorganization is in the best interests of the Acquired Fund; and (iii) the interests of the shareholders of the Acquired Fund will not be diluted as a result of the Reorganization.

Both the Acquired Fund and the Acquiring Fund are managed by JNAM, but only the Acquiring Fund is sub-advised by an investment sub-adviser. If the Reorganization is approved and implemented, each person that invests indirectly in the Acquired Fund will automatically become an investor indirectly in the Acquiring Fund.

Pending shareholder approval, effective as of the close of business on August 10, 2018, or on such later date as may be deemed necessary in the judgment of the JVST Board or JNLST’s Board of Trustees in accordance with the Plan of Reorganization (the “Closing Date”), you will invest indirectly in shares of the Acquiring Fund in an amount equal to the dollar value of your interest in the Acquired Fund on the Closing Date. No sales charge, redemption fees, or other transaction fees will be imposed in the Reorganization. The Reorganization will not cause any fees or charges under your contract to be greater after the Reorganization than before the Reorganization, and the Reorganization will not alter your rights under your contract or the obligations of the insurance company that issued the contract.

You may wish to take actions relating to your future allocation of premium payments under your insurance contract to the various investment divisions (the “Divisions”) of the separate account. You may execute certain changes prior to the Reorganization, in addition to participating in the Reorganization with regard to the Acquiring Fund, such as allocating your premium payments to other Divisions.

All actions with regard to the Acquired Fund need to be completed by the Closing Date. In the absence of new instructions prior to the Closing Date, future premium payments previously allocated to the Acquired Fund Division will be allocated to the Acquiring Fund Division. The Acquiring Fund Division will be the Division for future allocations under the Dollar Cost Averaging, Earnings Sweep, and Rebalancing Programs (together, the “Programs”). In addition to the Acquiring Fund Division, there are other Divisions investing in mutual funds that seek maximum real return, consistent with preservation of real capital and prudent investment management. If you want to transfer all or a portion of your Contract value out of the Acquired Fund Division prior to the Reorganization, you may do so and that transfer will not be treated as a transfer for the purpose of determining how many subsequent transfers may be made in any period or how many may be made in any period without charge. In addition, if you want to transfer all or a portion of your Contract value out of the Acquiring Fund Division after the Reorganization, you may do so within 60 days following the Closing Date and that transfer will not be treated as a transfer for the purpose of determining how many subsequent transfers may be made in any period or how many may be made in any period

without charge. You will be provided with an additional notification of this free-transfer policy on or about August 13, 2018.

If you want to change your allocation instructions as to your future premium payments or the Programs or if you require summary descriptions of the other underlying funds and Divisions available under your contract or additional copies of the prospectuses for other funds underlying the Divisions, please contact:

For Jackson variable annuity policies:

| Annuity Service Center |

| P.O. Box 30314 |

| Lansing, Michigan 48909-7814 |

| 1-800-644-4565 |

| www.jackson.com |

For Jackson New York variable annuity policies:

| Jackson of NY Service Center |

| P.O. Box 30313 |

| Lansing, Michigan 48909-7813 |

| 1-800-599-5651 |

| www.jackson.com |

An owner of a variable annuity contract or certificate that participates in the Acquired Fund through the Divisions of separate accounts established by Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York (each, an “Insurance Company”) is entitled to instruct the applicable Insurance Company how to vote the Acquired Fund shares related to the ownership interest in those accounts as of the close of business on May 18, 2018. The attached Notice of Special Meeting of Shareholders and Proxy Statement and Prospectus concerning the Meeting describe the matters to be considered at the Meeting.

You are cordially invited to attend the Meeting. Because it is important that your vote be represented whether or not you are able to attend, you are urged to consider these matters and to exercise your right to vote your shares by completing, dating, signing, and returning the enclosed voting instruction card in the accompanying return envelope at your earliest convenience or by relaying your voting instructions via telephone or the Internet by following the enclosed instructions. Of course, we hope that you will be able to attend the Meeting, and if you wish, you may vote your shares in person, even if you may have already returned a voting instruction card or submitted your voting instructions via telephone or the Internet. At any time prior to the Meeting, you may revoke your voting instructions by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone, or the Internet, or appearing and voting in person at the Meeting. Please respond promptly in order to save additional costs of proxy solicitation and to make sure you are represented.

| | Very truly yours, |

| | |

| | |

| | |

| | Mark D. Nerud |

| | Trustee, President, and Chief Executive Officer |

| | JNL Series Trust |

| | |

JACKSON VARIABLE SERIES TRUST

JNL Real Assets Fund

1 Corporate Way

Lansing, Michigan 48951

________________________

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD ON JULY 12, 2018

________________________

To the Shareholders:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders of the JNL Real Assets Fund (the “Real Assets Fund” or the “Acquired Fund”), a series of the Jackson Variable Series Trust (“JVST”), will be held on July 12, 2018 at 9:00 a.m., Eastern Time, at the offices of Jackson National Life Insurance Company, 1 Corporate Way, Lansing, Michigan 48951 (the “Meeting”).

The Meeting will be held to act on the following proposals:

| 1. | To approve the Plan of Reorganization, adopted by the JVST’s Board of Trustees (the “JVST Board”), which provides for the reorganization of the Real Assets Fund into the JNL/PIMCO Real Return Fund, a series of the JNL Series Trust. |

| 2. | To transact other business that may properly come before the Meeting or any adjournments thereof. |

Please note that owners of variable annuity contracts or certificates (the “Contract Owners”) issued by Jackson National Life Insurance Company or Jackson National Life Insurance Company of New York (each, an “Insurance Company”) who have invested in shares of the Acquired Fund through the investment divisions of a separate account or accounts of an Insurance Company (“Separate Account”) will be given the opportunity, to the extent required by law, to provide the applicable Insurance Company with voting instructions on the above proposals.

You should read the Proxy Statement and Prospectus attached to this notice prior to completing your proxy or voting instruction card. The record date for determining the number of shares outstanding, the shareholders entitled to vote, and the Contract Owners entitled to provide voting instructions at the Meeting and any adjournments thereof has been fixed as the close of business on May 18, 2018. If you attend the Meeting, you may vote or give your voting instructions in person.

YOUR VOTE IS IMPORTANT.

PLEASE RETURN YOUR PROXY CARD OR VOTING INSTRUCTION CARD PROMPTLY.

Regardless of whether you plan to attend the Meeting, you should vote or give voting instructions by promptly completing, dating, signing, and returning the enclosed proxy or voting instruction card for the Acquired Fund in the enclosed postage-paid envelope. You also can vote or provide voting instructions through the Internet or by telephone using the 12-digit control number that appears on the enclosed proxy or voting instruction card and following the simple instructions. At any time prior to the Meeting, you may revoke your voting instructions by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone, or the Internet, or appearing and voting in person at the Meeting. If you are present at the Meeting, you may change your vote or voting instructions, if desired, at that time. The JVST Board recommends that you vote or provide voting instructions to vote FOR the proposal.

| | By order of the JVST Board, |

| | |

| | |

| | |

| | Mark D. Nerud |

| | Trustee, President, and Chief Executive Officer |

June 18, 2018

Lansing, Michigan

JACKSON NATIONAL LIFE INSURANCE COMPANY

JACKSON NATIONAL LIFE INSURANCE COMPANY OF NEW YORK

CONTRACT OWNER VOTING INSTRUCTIONS

REGARDING A SPECIAL MEETING OF SHAREHOLDERS OF

JNL REAL ASSETS FUND

A SERIES OF THE JACKSON VARIABLE SERIES TRUST

TO BE HELD ON JULY 12, 2018

DATED: JUNE 18, 2018

GENERAL

These Contract Owner voting instructions are being furnished by Jackson National Life Insurance Company (“Jackson National”), or Jackson National Life Insurance Company of New York (each, an “Insurance Company” and, together, the “Insurance Companies”), to owners of their variable annuity contracts or certificates (the “Contracts”) (the “Contract Owners”) who, as of May 18, 2018 (the “Record Date”), had net premiums or contributions allocated to the investment divisions of their separate accounts (the “Separate Accounts”) that are invested in shares of the JNL Real Assets Fund (the “Real Assets Fund” or “Acquired Fund”), a series of the Jackson Variable Series Trust (“JVST”).

JVST is a Massachusetts business trust registered with the Securities and Exchange Commission (the “SEC”) as an open-end management investment company.

Each Insurance Company is required to offer Contract Owners the opportunity to instruct it, as the record owner of all of the shares of beneficial interest in the Acquired Fund (the “Shares”) held by its Separate Accounts, as to how it should vote on the reorganization proposal (the “Proposal”) to be considered at the Special Meeting of Shareholders of the Acquired Fund referred to in the preceding Notice and at any adjournments (the “Meeting”). The enclosed Proxy Statement and Prospectus, which you should retain for future reference, concisely sets forth information about the proposed reorganization involving the Acquired Fund and a series of the JNL Series Trust (“JNLST”) that a Contract Owner should know before completing the enclosed voting instruction card.

These Contract Owner Voting Instructions and the accompanying voting instruction card are being mailed to Contract Owners on or about June 19, 2018.

HOW TO INSTRUCT AN INSURANCE COMPANY

To instruct an Insurance Company as to how to vote the Shares held in the investment divisions of its Separate Accounts, Contract Owners are asked to promptly complete their voting instructions on the enclosed voting instruction card(s) and sign, date, and mail the voting instruction card(s) in the accompanying postage-paid envelope. Contract Owners also may provide voting instructions by phone at 1-866-256-0779 or by Internet at our website at www.proxypush.com/JNL.

If a voting instruction card is not marked to indicate voting instructions but is signed, dated, and returned, it will be treated as an instruction to vote the Shares in favor of the Proposal.

The number of Shares held in the investment division of a Separate Account corresponding to the Acquired Fund for which a Contract Owner may provide voting instructions was determined as of the Record Date by dividing (i) a Contract’s account value (minus any Contract indebtedness) allocable to that investment division by (ii) the net asset value of one Share of the Acquired Fund. At any time prior to an Insurance Company’s voting at the Meeting, a Contract Owner may revoke his or her voting instructions with respect to that investment division by providing the Insurance Company with a properly executed written revocation of such voting instructions, properly executing later-dated voting instructions by a voting instruction card, telephone or the Internet, or appearing and voting in person at the Meeting.

HOW AN INSURANCE COMPANY WILL VOTE

An Insurance Company will vote the Shares for which it receives timely voting instructions from Contract Owners in accordance with those instructions. Shares in each investment division of a Separate Account for which an Insurance Company receives a voting instruction card that is signed, dated, and timely returned but is not marked to indicate voting instructions will be treated as an instruction to vote the Shares in favor of the Proposal. Shares in each investment division of a Separate Account for which an Insurance Company receives no timely voting instructions from a Contract Owner, or that are attributable to amounts retained by an Insurance Company or its affiliate as surplus or seed money, will be voted by the applicable Insurance Company either for or against approval of the Proposal, or as an abstention, in the same proportion as the Shares for which Contract Owners (other than the Insurance Company) have provided voting instructions to the Insurance Company. Similarly, the Insurance Companies and their affiliates will vote their own shares and will vote shares of the regulated investment companies (also known as “RICs”) that are held by the Fund of Funds whose shares are held by a Separate Account in the same proportion as voting instructions timely given by Contract Owners for those respective regulated investment companies. As a result of proportionate voting, a small number of Contract Owners could determine the outcome of the Proposal. Please see “Additional Information about the Funds – Tax Status” below for further information regarding regulated investment companies.

OTHER MATTERS

The Insurance Companies are not aware of any matters, other than the Proposal, to be acted on at the Meeting. If any other matters come before the Meeting, an Insurance Company will vote the Shares upon such matters in its discretion. Voting instruction cards may be solicited by employees of Jackson National or its affiliates as well as officers and agents of JVST. The principal solicitation will be by mail, but voting instructions may also be solicited by telephone, fax, personal interview, the Internet, or other permissible means.

The Meeting may be adjourned whether or not a quorum is present, by the chairperson of the Meeting from time to time to reconvene at the same or some other place as determined by the chairperson of the Meeting for any reason, including failure of a Proposal to receive sufficient votes for approval. No shareholder vote shall be required for any adjournment. No notice need be given that the Meeting has been adjourned other than by announcement at the Meeting. Any business that might have been transacted at the original Meeting may be transacted at any adjourned Meeting.

It is important that your Contract be represented. Please promptly mark your voting instructions on the enclosed voting instruction card; then sign, date, and mail the voting instruction card in the accompanying postage-paid envelope. You may also provide your voting instructions by telephone at 1-866-256-0779 or by Internet at our website at www.proxypush.com/JNL.

PROXY STATEMENT

for

JNL Real Assets Fund, a series of Jackson Variable Series Trust

and

PROSPECTUS

for

JNL/PIMCO Real Return Fund, a series of JNL Series Trust

Dated

June 18, 2018

1 Corporate Way

Lansing, Michigan 48951

(517) 381-5500

This Proxy Statement and Prospectus (the “Proxy Statement/Prospectus”) is being furnished to owners of variable annuity contracts or certificates (the “Contracts”) (the “Contract Owners”) issued by Jackson National Life Insurance Company (“Jackson National”) or Jackson National Life Insurance Company of New York (each, an “Insurance Company” and together, the “Insurance Companies”) who, as of May 18, 2018, had net premiums or contributions allocated to the investment divisions of an Insurance Company’s separate accounts (the “Separate Accounts”) that are invested in shares of beneficial interest in the JNL Real Assets Fund (the “Real Assets Fund” or the “Acquired Fund”), a series of the Jackson Variable Series Trust (“JVST”), an open-end management investment company registered with the Securities and Exchange Commission (“SEC”). The purpose of this Proxy Statement/Prospectus is for shareholders of the Real Assets Fund to vote on a Plan of Reorganization, adopted by the JVST’s Board of Trustees (the “JVST Board”), which provides for the reorganization of the Real Assets Fund into the JNL/PIMCO Real Return Fund (the “Real Return Fund” or the “Acquiring Fund”), a series of the JNL Series Trust (“JNLST”).

This Proxy Statement/Prospectus also is being furnished to the Insurance Companies as the record owners of shares and to other shareholders that were invested in the Acquired Fund as of May 18, 2018. Contract Owners are being provided the opportunity to instruct the applicable Insurance Company to approve or disapprove the proposal contained in this Proxy Statement/Prospectus in connection with the solicitation by the JVST Board of proxies to be used at the Special Meeting of Shareholders of the Acquired Fund to be held at 1 Corporate Way, Lansing, Michigan 48951, on July 12, 2018, at 9:00 a.m., Eastern Time, or any adjournment or adjournments thereof (the “Meeting”).

| THE SEC HAS NOT APPROVED OR DISAPPROVED THE SECURITIES DESCRIBED IN THIS PROXY STATEMENT/PROSPECTUS OR DETERMINED IF THIS PROXY STATEMENT/PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. |

The proposal described in this Proxy Statement/Prospectus is as follows:

| Proposal | Shareholders Entitled to Vote on the Proposal |

| 1. To approve the Plan of Reorganization, adopted by the JVST Board, which provides for the reorganization of the Real Assets Fund into the Real Return Fund. | Shareholders of the Real Assets Fund |

The reorganization referred to in the above proposal is referred to herein as the “Reorganization.”

This Proxy Statement/Prospectus, which you should retain for future reference, contains important information regarding the proposal that you should know before voting or providing voting instructions. Additional information about JNLST has been filed with the SEC and is available upon oral or written request without charge. This Proxy Statement/Prospectus is being provided to the Insurance Companies and mailed to Contract Owners on or about June 19, 2018. It is expected that one or more representatives of each Insurance Company will attend the Meeting in person or by proxy and will vote shares held by the Insurance Company in accordance with voting instructions received from its Contract Owners and in accordance with voting procedures established by JVST.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement/Prospectus:

| 1. | The Prospectus and Statement of Additional Information of JVST, each dated April 30, 2018 [, as supplemented], with respect to the Acquired Fund (File Nos. 333-177369 and 811-22613); |

| 2. | The Annual Report to Shareholders of JVST with respect to the Acquired Fund for the fiscal year ended December 31, 2017 (File Nos. 333-177369 and 811-22613); |

| 3. | The Statement of Additional Information dated June 18, 2018, relating to the Reorganization (File No. 333-[ ]). |

For a free copy of any of the above documents, please call or write to the phone numbers or address below.

Contract Owners can learn more about the Acquired Fund and the Acquiring Fund in any of the documents incorporated into this proxy statement/prospectus, including the Annual Report listed above, which have been furnished to Contract Owners. Contract Owners may request a copy thereof, without charge, by calling 1-800-644-4565 (Jackson Service Center) or 1-800-599-5651 (Jackson NY Service Center), by writing the JNL Series Trust, P.O. Box 30314, Lansing, Michigan 48909-7814, or by visiting www.jackson.com.

JNLST is subject to the informational requirements of the Securities Act of 1933, as amended (the “1933 Act”), the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the “1940 Act”). Accordingly, it must file certain reports and other information with the SEC. You can copy and review proxy materials, reports, and other information about JNLST at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC. You may obtain information on the operation of the Public Reference Room by calling the SEC at (202) 551-8090. Proxy materials, reports, and other information about JNLST are available on the EDGAR Database on the SEC’s Internet site at http://www.sec.gov. You may obtain copies of this information, after paying a duplicating fee, by electronic request at the following E-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, SEC Office of Consumer Affairs and Information Services, 100 F Street, N.E., Washington, DC 20549-1520.

TABLE OF CONTENTS

| | | |

| | 1 |

| | 1 |

| | 2 |

| | 4 |

| | 4 |

| | 5 |

| | 5 |

| | 5 |

| | 8 |

| | 10 |

| | 12 |

| | 13 |

| | 13 |

| | 14 |

| | 14 |

| | 15 |

| | 15 |

| | 17 |

| | 17 |

| | 17 |

| | 17 |

| | 17 |

| | 17 |

| | 17 |

| | 18 |

| | 19 |

| | 20 |

| | 21 |

| | 21 |

| | 22 |

| | 22 |

| | 22 |

| | 24 |

| | 24 |

| | 25 |

| | 25 |

| | 26 |

| | 28 |

| | 28 |

| | 28 |

| | 28 |

| | 28 |

| | 29 |

| | 29 |

| | 29 |

| | 30 |

| | A-1 |

| | B-1 |

| | C-1 |

You should read this entire Proxy Statement/Prospectus carefully. For additional information, you should consult the Plan of Reorganization, a copy of which is attached hereto as Appendix A.

T

he Proposed Reorganization

The proposed Reorganization is as follows:

| Proposal | Shareholders Entitled to Vote on the Proposal |

| 1. To approve the Plan of Reorganization, adopted by the JVST Board, which provides for the reorganization of the Real Assets Fund into the Real Return Fund. | Shareholders of the Real Assets Fund |

This Proxy Statement/Prospectus is soliciting shareholders with amounts invested in the Acquired Fund as of May 18, 2018, to approve the Plan of Reorganization, whereby the Acquired Fund will be reorganized into the Acquiring Fund. (The Acquired Fund and Acquiring Fund are each sometimes referred to herein as a “Fund” and collectively, the “Funds.”)

The Acquired Fund has two share classes, designated Class A and Class I shares (“Acquired Fund Shares”). The Acquiring Fund also has two share classes, Class A and Class I shares (“Acquiring Fund Shares”).

The Plan of Reorganization provides for:

| · | the transfer of all of the assets of the Acquired Fund to the Acquiring Fund in exchange for Acquiring Fund Shares having an aggregate net asset value equal to the Acquired Fund’s net assets; |

| · | the Acquiring Fund’s assumption of all the liabilities of the Acquired Fund; |

| · | the distribution to the shareholders (for the benefit of the Separate Accounts, as applicable, and thus the Contract Owners) of those Acquiring Fund Shares; and |

| · | the complete termination of the Acquired Fund. |

A comparison of the investment objective(s), principal investment policies and strategies and principal risks of the Acquired Fund and the Acquiring Fund is included in the “Comparison of Investment Objectives and Principal Investment Strategies,” “Comparison of Principal Risk Factors” and “Comparison of Fundamental Policies” sections below. The Funds have identical distribution procedures, purchase procedures, exchange rights, and redemption procedures, which are discussed in “Additional Information about the Funds” below. Each Fund offers its shares to Separate Accounts and certain other eligible investors. Shares of each Fund are offered and redeemed at their net asset value without any sales load. You will not incur any sales loads or similar transaction charges as a result of the Reorganization.

The Reorganization is expected to be effective as of the close of business on August 10, 2018, or on such later date as may be deemed necessary in the judgment of the JVST Board or the JNLST Board in accordance with the Plan of Reorganization (the “Closing Date”). As a result of the Reorganization, a shareholder invested in shares of the Acquired Fund would become an owner of shares of the Acquiring Fund. Such shareholder would hold, immediately after the Closing Date, Acquiring Fund Shares having an aggregate net asset value equal to the aggregate net asset value of the Acquired Fund Shares that were held by the shareholder as of the Closing Date. Similarly, each Contract Owner whose Contract values are invested indirectly in shares of the Acquired Fund through the Investment Divisions of a Separate Account would become indirectly invested in shares of the Acquiring Fund through the Investment Divisions of a Separate Account. The Contract value of each such Contract Owner would be invested indirectly through the Investment Divisions of a Separate Account, immediately after the Closing Date, in shares of the Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of the Acquired Fund Shares in which the Contract Owner invested indirectly through the Investment Divisions of a Separate Account as of the Closing Date. It is expected that there will be no adverse tax consequences to Contract Owners as a result of the

Reorganization. Please see “Additional Information about the Reorganization – Federal Income Tax Consequences of the Reorganization” below for further information.

The JVST Board unanimously approved the Plan of Reorganization with respect to the Real Assets Fund. Accordingly, the JVST Board is submitting the Plan of Reorganization for approval by the Acquired Fund’s shareholders. In considering whether to approve the proposal (“Proposal”), you should review the Proposal for the Acquired Fund in which you were invested on the Record Date (as defined under “Voting Information”). In addition, you should review the information in this Proxy Statement/Prospectus that relates to the Proposal and the Plan of Reorganization generally. The JVST Board recommends that you vote “FOR” the Proposal to approve the Plan of Reorganization.

| APPROVAL OF THE PLAN OF REORGANIZATION WITH RESPECT TO THE REORGANIZATION OF THE REAL ASSETS FUND INTO THE REAL RETURN FUND. |

This Proposal requests the approval of Real Assets Fund shareholders of the Plan of Reorganization pursuant to which the Real Assets Fund will be reorganized into the Real Return Fund.

In considering whether you should approve this Proposal, you should note that:

| · | The Funds have comparable investment objectives. The Real Assets Fund seeks long-term real return through an allocation in stocks and other asset classes and strategies through investment in other funds (the “Underlying Funds”), while the Real Return Fund seeks maximum real return, consistent with preservation of real capital and prudent investment management. For a detailed comparison of each Fund’s investment policies and strategies, see “Comparison of Investment Objectives and Principal Investment Strategies” below and Appendix B. |

| · | Although the Funds have comparable investment objectives, they employ different investment strategies in seeking to achieve those objectives. The Real Assets Fund is structured as a fund-of-funds and seeks to achieve its objective by investing, under normal circumstances, at least 80% of its assets (net assets plus the amount of any borrowings made for investment purposes) in Class I shares of the Underlying Funds that focus on investments in one or more of inflation-linked instruments or the commodity, natural resource, or real estate sectors. The Real Return Fund is a stand-alone Fund that is managed by a sub-adviser and under normal circumstances invests at least 80% of its assets in inflation-indexed bonds of varying maturities issued by the U.S. and non-U.S. governments, their agencies or instrumentalities, and corporations, which may be represented by forwards or derivatives such as options, futures contracts, or swap agreements. For a detailed comparison of each Fund’s investment objectives and principal investment strategies, see “Comparison of Investment Objectives and Principal Investment Strategies” and Appendix B. |

| · | Both Funds have similar fundamental policies. However, the Real Return Fund lists one fundamental policy that is not listed for the Real Assets Fund; the Real Return Fund may not invest more than 15% of its net assets in illiquid securities. While the Real Assets Fund does not have the same fundamental policy, the Real Assets Fund may only invest up to 15% of its net assets in securities that are illiquid due to regulatory guidelines that are substantially similar. Furthermore, the Real Return Fund has a more restrictive fundamental investment policy with respect to lending securities. For a detailed comparison of each Fund’s fundamental investment policies, see “Comparison of Fundamental Policies” below. |

| · | While there are some similarities in the risk profiles of the Funds, there are also some differences of which you should be aware. Each Fund’s principal risks include credit risk, currency risk, derivatives risk, emerging markets and less developed countries risk, equity securities risk, fixed-income risk, foreign regulatory risk, foreign securities risk, inflation-indexed securities risk, interest rate risk, leverage risk, liquidity risk, managed portfolio risk, non-diversification risk, portfolio turnover risk, and short sales risk. The Real Assets Fund, however, also is subject to allocation risk, commodity risk, counterparty risk, market risk, natural resource related securities risk, real estate investment risk, sector risk, settlement risk, sovereign debt risk, TIPS and inflation-linked bonds risk, and underlying funds risk, while these generally are not principal risks for the Real Return Fund. In addition, the principal risks of investing in the Real Return Fund include call risk, debt securities ratings risk, extension risk, forward and futures contract risk, high yield bonds, lower-rated bonds, and unrated securities risk, investment strategy risk, issuer risk, mortgage-related and other asset- |

backed securities risk, options risk, prepayment risk, swaps risk, and U.S. Government securities risk, which are not principal risks of investing in the Real Assets Fund. For a detailed comparison of each Fund’s risks, see both “Comparison of Principal Risk Factors” below and Appendix B.

| · | Jackson National Asset Management, LLC (“JNAM” or the “Adviser”) serves as the investment adviser and administrator for each Fund and would continue to manage and administer the Real Return Fund after the Reorganization. JNAM has received an exemptive order from the SEC that generally permits JNAM, with approval from the JNLST’s Board of Trustees and the JVST Board of Trustees, respectively, to appoint, dismiss, and replace each Fund’s unaffiliated sub-adviser(s) and to amend the advisory agreements between JNAM and the unaffiliated sub-advisers, without obtaining shareholder approval. However, any amendment to an advisory agreement between JNAM and JVST or JNLST, respectively, that would result in an increase in the management fee rate specified in that agreement (i.e., the aggregate management fee) charged to a Fund will be submitted to shareholders for approval. JNAM is responsible for managing the assets of the Real Assets Fund directly and has not appointed a sub-adviser for the Real Assets Fund. JNAM has appointed Pacific Investment Management Company LLC (“PIMCO”) as sub-adviser to manage the assets of the Real Return Fund. It is anticipated that PIMCO will continue to sub-advise the Real Return Fund after the Reorganization. For a detailed description of JNAM, please see “Additional Information about the Funds - The Adviser” below. |

| · | The Real Assets Fund and Real Return Fund had net assets of approximately $12.15 million and $2,059.13, respectively, as of December 31, 2017. Thus, if the Reorganization had been in effect on that date, the combined Fund (the “Combined Fund”) would have had net assets of approximately $2,071.28 million. |

| · | Class A Shareholders of the Real Assets Fund will receive Class A shares of the Real Return Fund, and Class I Shareholders of the Real Assets Fund will receive Class I shares of the Real Return Fund pursuant to the Reorganization. Shareholders will not pay any sales charges in connection with the Reorganization. Please see “Comparative Fee and Expense Tables,” “Additional Information about the Reorganization,” and “Additional Information about the Funds” below for more information. |

| · | Following the Reorganization, the management fees for the Real Return Fund will be higher than that of the Real Assets Fund currently, but the total annual fund operating expense ratio for the Real Return Fund will be lower than that the Real Assets Fund currently. The lower total annual fund operating expense ratio after the Reorganization is a result of the Real Return Fund not having any acquired fund fees and expenses. For a more detailed comparison of the fees and expenses of the Funds, please see “Comparative Fee and Expense Tables” and “Additional Information about the Funds” below. |

| · | The maximum management fee for the Real Assets Fund is equal to an annual rate of 0.15% of its average daily net assets, while the maximum management fee for the Real Return Fund is equal to an annual rate of 0.39% of its average daily net assets. As of December 31, 2017, the actual management fees of the Real Assets Fund and the Real Return Fund were 0.15% and 0.38%, respectively. In addition, the Real Assets Fund pays an administrative fee to JNAM, at the rate of 0.05% of its average daily net assets, whereas the Real Return Fund pays JNAM an administrative fee of 0.10% of its average daily net assets. For a more detailed description of the fees and expenses of the Funds, please see “Comparative Fee and Expense Tables” and “Additional Information about the Funds” below. |

| · | Following the Reorganization, the Combined Fund will be managed in accordance with the investment objective, policies and strategies of the Real Return Fund. It is currently anticipated that roughly 100% of the Real Assets Fund’s holdings will be liquidated in advance and reinvested in the Real Return Fund in connection with the Reorganization. It is not expected that the Real Return Fund will revise any of its investment policies following the Reorganization to reflect those of the Real Assets Fund. |

| · | The costs and expenses associated with the Reorganization relating to the solicitation of proxies, including preparing, filing, printing, and mailing of the proxy statement and related disclosure documents, and the related legal fees, including the legal fees incurred in connection with the analysis under the Internal Revenue Code of 1986, as amended (the “Code”) of the tax treatment of this transaction, and the costs associated with obtaining a consent of independent registered public accounting firm will all be borne by JNAM, and no sales or other charges will be imposed on Contract Owners in connection with this Reorganization. The Reorganization is not expected to result in any material adverse federal income tax consequences to |

shareholders of the Real Assets Fund. Please see “Additional Information about the Reorganization” below for more information.

C

omparative Fee and Expense Tables

The following tables show the fees and expenses of each Fund and the estimated pro forma fees and expenses of Class A and Class I shares of the Acquiring Fund after giving effect to the proposed Reorganization. Fees and expenses for each Fund are based on those incurred for the fiscal year ended December 31, 2017. The pro forma fees and expenses of the Acquiring Fund Shares assume that the Reorganization had been in effect for the year ended December 31, 2017. The tables below do not reflect any fees and expenses related to the Contracts, which would increase overall fees and expenses. See a Contract prospectus for a description of those fees and expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| | Acquired Fund: Real Assets Fund | Acquiring Fund: Real Return Fund | Pro Forma Real Return Fund (assuming expected operating expenses if the Reorganization is approved) |

| | Class A | Class I | Class A | Class I | Class A | Class I |

| Management Fee | 0.15% | 0.15% | 0.38% | 0.38% | 0.38% | 0.38% |

| Distribution and/or Service (12b-1) Fees | 0.30% | 0.00% | 0.30% | 0.00% | 0.30% | 0.00% |

Other Expenses 1, 2 | 0.06% | 0.06% | 0.48% | 0.48% | 0.48% | 0.48% |

Acquired Fund Fees and Expenses 3 | 0.80% | 0.80% | 0.00% | 0.00% | 0.00% | 0.00% |

Total Annual Fund Operating Expenses 4 | 1.31% | 1.01% | 1.16% | 0.86% | 1.16% | 0.86% |

1 “Other expenses” for the Acquiring Fund are based on amounts incurred during the period ended December 31, 2017. The amount includes financing costs associated with secured borrowings. The Acquiring Fund’s annualized ratios of financing costs related to secured borrowings were 0.38%. The Acquiring Fund’s actual financing costs may be significantly higher or lower than the amounts above due to, among other factors, the extent of the Fund’s involvement with secured borrowings and the costs associated with those transactions, each of which is expected to vary over time.

2 “Other expenses” include an Administrative Fee of 0.05% for the Acquired Fund, and 0.10% for the Acquiring Fund, which is payable to JNAM.

3 Acquired Fund Fees and Expenses are the indirect expenses of investing in other investment companies. The Total Annual Fund Operating Expenses disclosed above do not correlate to the Ratio of Total Expenses to Average Net Assets of the Fund stated in the Financial Highlights because the Ratio of Total Expenses to Average Net Assets does not include Acquired Fund Fees and Expenses.

4 Expense information has been restated to reflect current fees.

This example is intended to help you compare the costs of investing in the Funds with the cost of investing in other mutual funds. This example does not reflect fees and expenses related to the Contracts, and the total expenses would be higher if they were included. The example assumes that:

| · | You invest $10,000 in a Fund for the time periods indicated; |

| · | Your investment has a 5% annual return; |

| · | The Fund’s operating expenses remain the same as they were as of December 31, 2017; and |

| · | You redeem your investment at the end of each time period. |

Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| | 1 Year | 3 Years | 5 Years | 10 Years |

| Real Assets Fund (Acquired Fund) | | | | |

| Class A | $133 | $415 | $718 | $1,579 |

| Class I | $103 | $322 | $558 | $1,236 |

| Real Return Fund (Acquiring Fund) | | | | |

| Class A | $118 | $368 | $638 | $1,409 |

| Class I | $88 | $274 | $477 | $1,061 |

Pro Forma Real Return Fund (assuming expected operating expenses if the Reorganization is approved) | | | | |

| Class A | $118 | $368 | $638 | $1,409 |

| Class I | $88 | $274 | $477 | $1,061 |

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in Annual Fund Operating Expenses or in the Expense Examples, affect a Fund’s performance. For the fiscal year ended December 31, 2017, the portfolio turnover rates for the Real Assets Fund and the Real Return Fund were 127% and 162%, respectively, of the average value of each portfolio.

C

omparison of Investment Adviser and Sub-Adviser

The following table compares the investment adviser and sub-adviser of the Real Return Fund with that of the Real Assets Fund.

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

Investment Adviser Jackson National Asset Management, LLC Investment Sub-Adviser None | Investment Adviser Jackson National Asset Management, LLC Investment Sub-Adviser Pacific Investment Management Company LLC |

C

omparison of Investment Objectives and Principal Investment Strategies

The following table compares the investment objectives and principal investment strategies of the Real Assets Fund with those of the Real Return Fund. A Fund’s Board of Trustees may change the investment objective of a Fund without a vote of the Fund’s shareholders. For more detailed information about each Fund’s investment strategies and risks, see Appendix B.

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

Investment Objective The investment objective of the Fund is to seek long-term real return through an allocation in stocks and other asset classes and strategies through investment in other funds (the “Underlying Funds”). | Investment Objective The investment objective of the Fund is to seek maximum real return, consistent with preservation of real capital and prudent investment management. |

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

Principal Investment Strategies The Fund seeks to achieve its objective by investing, under normal circumstances, at least 80% of its assets (net assets plus the amount of any borrowings made for investment purposes) (“80% Policy”) in Class I shares of the Underlying Funds that focus on investments in one or more of inflation-linked instruments or the commodity, natural resource, or real estate sectors. The Fund allocates the majority of its assets to Underlying Funds that invest primarily in equity securities, inflation protected securities of issuers in the U.S. and foreign countries, including emerging markets and currencies. The Underlying Funds in which the Fund may invest each are a separate series of the Jackson Variable Series Trust, JNL Series Trust, JNL Variable Fund LLC, or JNL Investors Series Trust. Not all Funds of the Jackson Variable Series Trust, JNL Series Trust JNL Variable Fund LLC, or JNL Investors Series Trust are available as Underlying Funds. Please refer to “More Information on Strategies and Risk Factors – JNL Real Assets Fund” in Appendix B for a list of available Underlying Funds. | Principal Investment Strategies The Fund seeks its investment objective by investing under normal circumstances at least 80% of its assets (net assets plus the amount of any borrowings made for investment purposes) in inflation-indexed bonds of varying maturities issued by the U.S. and non-U.S. governments, their agencies or instrumentalities, and corporations, which may be represented by forwards or derivatives such as options, futures contracts, or swap agreements. Assets not invested in inflation-indexed bonds may be invested in other types of fixed-income instruments. “Fixed-income instruments” include bonds, debt securities and other similar instruments issued by various U.S. and non-U.S. public- or private-sector entities. Inflation-indexed bonds are fixed-income securities that are structured to provide protection against inflation. The value of the bond’s principal or the interest income paid on the bond is adjusted to track changes in an official inflation measure. The U.S. Treasury uses the Consumer Price Index for All Urban Consumers (“CPI-U”) as the inflation measure. Inflation-indexed bonds issued by a foreign government are generally adjusted to reflect a comparable inflation index, calculated by that government. “Real return” equals total return less the estimated rate of inflation, which is typically measured by the change in an official inflation measure, such as CPI-U. The average portfolio duration of this Fund normally varies within three years (plus or minus) of the duration of the Bloomberg Barclays U.S. TIPS Index, as calculated by Pacific Investment Management Company LLC (“PIMCO”). For these purposes, in calculating the Fund’s average portfolio duration, PIMCO includes the real duration of the inflation-indexed portfolio. |

| Consistent with its 80% Policy described above, the Fund typically allocates approximately 20% to 50% of its assets to Underlying Funds investing in fixed-income securities; 0% to 20% of its assets to Underlying Funds investing in equity securities; and 40% to 80% of its assets to Underlying Funds investing in alternative securities. | The Fund invests primarily in investment grade securities, but may invest up to 10% of its total assets in high yield securities (“junk bonds”) rated B or higher by Moody's or equivalently rated by S&P Global Ratings or Fitch Inc., or, if unrated, determined by PIMCO to be of comparable quality (except that within such 10% limitation, the Fund may invest in mortgage-related securities rated below B). The Fund also may invest up to 30% of its total assets in securities denominated in foreign currencies, and may invest beyond this limit in U.S. dollar denominated securities of foreign issuers. The Fund may invest up to 15% of its total assets in securities and instruments that are economically tied to emerging market countries. Foreign currency exposure (from non-U.S. dollar-denominated |

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

| | securities or currencies) normally will be limited to 20% of the Fund’s total assets. |

The Fund allocates its assets among Underlying Funds categorized by the Adviser into the following investment categories: · Alternative Assets · Alternative Strategies · Domestic/Global Equity · Domestic/Global Fixed-Income · International · International Fixed-Income · Risk Management · Sector · Specialty · Tactical Management The Fund considers the Underlying Funds in the Domestic/Global Fixed Income and International Fixed Income investment categories to be funds that invest primarily in fixed income securities, and the Underlying Funds in the Domestic/Global Equity, International, Sector, and Specialty investment categories to be funds that invest primarily in equity securities. The Underlying Funds in the Risk Management and Tactical Management investment categories include funds that can invest in a variety of asset classes in various proportions, may take measures to manage risk and/or adapt to prevailing market conditions and may have significant exposure to both fixed income and equity securities. To the extent the Fund invests in one of these Underlying Funds, the Fund’s exposure to fixed income securities and equity securities will be allocated according to the Underlying Fund’s relative exposure to these asset classes. The Fund considers the Underlying Funds in the Alternative Assets and Alternative Strategies investment categories to be funds that invest primarily in alternative assets and employ alternative strategies. | No corresponding strategy. |

| Each Underlying Fund has its own investment objective and invests in certain types of securities or other assets in order to implement its investment strategy and seek to achieve its investment objective. Those types of securities or other assets include, but are not limited to: equity securities (such as common stock, preferred stock, and convertible securities), equity futures, equity swaps, currency forwards, currency futures, commodity futures and swaps, bond futures, fixed income swaps, interest rate swaps, and inflation swaps; U.S. and foreign government bonds, including inflation protected bonds (such as Treasury Inflation Protected Securities); bank loans; cash and cash equivalents, including but not limited to money market fund shares. These holdings | The Fund may invest all of its assets in derivative instruments, such as futures, options, or swap agreements, or in mortgage or asset-backed securities. The Fund may purchase or sell securities on a when-issued basis, delayed delivery or forward commitment basis and may engage in short sales. The Fund may, without limitation, seek to obtain market exposure to the securities in which it primarily invests by entering into a series of purchase and sale contracts or by using other investment techniques (such as buybacks or dollar rolls). The Fund may also invest up to 10% of its total assets in preferred stocks. |

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

| can include investment exposure to both developed and emerging markets, and may be illiquid or thinly traded. Securities held by the Underlying Funds may be denominated in U.S. and/or non-U.S. currencies. | |

An Underlying Fund may be leveraged and therefore could be subject to a heightened risk of loss. The leverage involved in certain derivative transactions may result in an Underlying Fund’s net asset value being more sensitive to changes in the value of the related investment. In determining allocations to any particular Underlying Fund, the Adviser considers, among other things, long-term market and economic conditions, historical performance of each Underlying Fund, and expected long-term performance of each Underlying Fund, as well as diversification to control overall portfolio risk exposure. The Adviser may change the Underlying Funds in which the Fund invests from time to time at its discretion without notice or shareholder approval. Therefore, the Fund may invest in Underlying Funds that are not listed in the statutory prospectus. | No corresponding strategy. |

| The Fund is “non-diversified,” as defined in the Investment Company Act of 1940, as amended (the “1940 Act”), and may invest more of its assets in fewer issuers than “diversified” mutual funds. | The Fund is a “non-diversified” fund, as defined in the Investment Company Act of 1940, as amended (the “1940 Act”), and may invest more of its assets in fewer issuers than “diversified” mutual funds. |

C

omparison of Principal Risk Factors

While there are some similarities in the risk profiles of the Funds, there are also some differences of which you should be aware. Each Fund’s principal risks include credit risk, currency risk, derivatives risk, emerging markets and less developed countries risk, equity securities risk, fixed-income risk, foreign regulatory risk, foreign securities risk, inflation-indexed securities risk, interest rate risk, leverage risk, liquidity risk, managed portfolio risk, non-diversification risk, portfolio turnover risk, and short sales risk. The Real Assets Fund, however, also is subject to allocation risk, commodity risk, counterparty risk, market risk, natural resource related securities risk, real estate investment risk, sector risk, settlement risk, sovereign debt risk, TIPS and inflation-linked bonds risk, and underlying funds risk, while these generally are not principal risks for the Real Return Fund. In addition, the principal risks of investing in the Real Return Fund include call risk, debt securities ratings risk, extension risk, forward and futures contract risk, high yield bonds, lower-rated bonds, and unrated securities risk, investment strategy risk, issuer risk, mortgage-related and other asset-backed securities risk, options risk, prepayment risk, swaps risk, and U.S. Government securities risk, which are not principal risks of investing in the Real Assets Fund. For a detailed comparison of each Fund’s risks, see both “Comparison of Principal Risk Factors” below and Appendix B.

An investment in a Fund is not guaranteed. As with any mutual fund, the value of a Fund’s shares will change, and an investor could lose money by investing in a Fund. The following table compares the principal risks of an investment in each Fund. The Acquired Fund will incur the risks associated with each Underlying Fund in which it is invested. For additional information about each principal risk and other applicable risks, see Appendix B.

| | Acquired Fund | Acquiring Fund |

| Risks | Real Assets Fund | Real Return Fund |

| Allocation risk | X | |

| Call risk | | X |

| Commodity risk | X | |

| Counterparty risk | X | |

| Credit risk | X | X |

| Currency risk | X | X |

| Debt securities ratings risk | | X |

| Derivatives risk | X | X |

| Emerging markets and less developed countries risk | X | X |

| Equity securities risk | X | X |

| Extension Risk | | X |

| Fixed-income risk | X | X |

| Foreign regulatory risk | X | X |

| Foreign securities risk | X | X |

| Forward and futures contract risk | | X |

| High yield bonds, lower-rated bonds, and unrated securities risk | | X |

| Inflation-indexed securities risk | X | X |

| Interest rate risk | X | X |

| Investment strategy risk | | X |

| Issuer risk | | X |

| Leverage risk | X | X |

| Liquidity risk | X | X |

| Managed portfolio risk | X | X |

| | Acquired Fund | Acquiring Fund |

| Risks | Real Assets Fund | Real Return Fund |

| Market risk | X | |

| Mortgage-related and other asset-backed securities risk | | X |

| Natural resource related securities risk | X | |

| Non-diversification risk | X | X |

| Options risk | | X |

| Portfolio turnover risk | X | X |

| Prepayment risk | | X |

| Real estate investment risk | X | |

| Sector risk | X | |

| Settlement risk | X | |

| Short sales risk | X | X |

| Sovereign debt risk | X | |

| Swaps risk | | X |

| TIPS and inflation-linked bonds risk | X | |

| Underlying funds risk | X | |

| U.S. Government securities risk | | X |

C

omparison of Fundamental Policies

Each Fund is subject to certain fundamental policies and restrictions that may not be changed without shareholder approval. The following table compares the fundamental policies of the Real Assets Fund with those of the Real Return Fund.

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

| (1) The Fund is “non-diversified.” | Same. |

| Acquired Fund | Acquiring Fund |

| Real Assets Fund | Real Return Fund |

| (2) The Fund may not invest more than 25% of the value of its assets in any particular industry (other than U.S. Government securities and/or foreign sovereign debt securities). | Same. |

| (3) The Fund may not invest directly in real estate or interests in real estate; however, the Fund may own debt or equity securities issued by companies engaged in those businesses. | Same. |

| (4) The Fund may not purchase or sell physical commodities other than foreign currencies unless acquired as a result of ownership of securities (but this limitation shall not prevent the Fund from purchasing or selling options, futures, swaps and forward contracts or from investing in securities or other instruments backed by physical commodities). | Same. |

| (5) The Fund may not lend any security or make any other loan, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | The Fund may not lend any security or make any other loan if, as a result, more than 33 1/3% of the Fund’s total assets would be lent to other parties (but this limitation does not apply to purchases of commercial paper, debt securities or repurchase agreements). |

| (6) The Fund may not act as an underwriter of securities issued by others, except to the extent that the Fund may be deemed an underwriter in connection with the disposition of portfolio securities of the Fund. | Same. |

(7) The Fund may not issue senior securities, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | No corresponding fundamental restriction. |

(8) The Fund may not borrow money, except to the extent permitted by the 1940 Act, the rules and regulations thereunder, and any applicable exemptive relief. | Same. |

| (9) No corresponding fundamental restriction. | The Fund may not invest more than 15% of its net assets in illiquid securities. This limitation does not apply to securities eligible for resale pursuant to Rule 144A of the 1933 Act or commercial paper issued in reliance upon the exemption from registration contained in Section 4(a)(2) of that Act, which have been determined to be liquid in accord with guidelines established by the Board of Trustees. |

C

omparative Performance Information

The performance information shown below provides some indication of the risks of investing in each Fund by showing changes in each Fund’s performance from year to year and by showing how each Fund’s average annual returns compared with those of a broad-based securities market index that has investment characteristics similar to those of such Fund, and, for the Real Assets Fund, a composite index which has investment characteristics similar to those of the Fund. Past performance is not an indication of future performance.

Information for Real Assets Fund Class I shares is not shown because Class I shares commenced operations on September 25, 2017.

The returns shown in the bar chart and table do not include charges imposed under the Contracts. If these amounts were reflected, returns would be less than those shown.

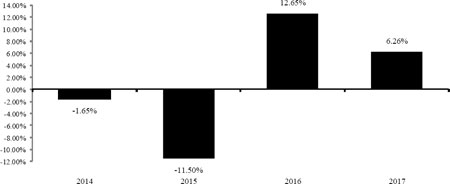

Real Assets Fund – Calendar Year Total Returns

(Acquired Fund)

Class A

Best Quarter (ended 6/30/2016): 8.69%; Worst Quarter (ended 9/30/2015): -8.66%

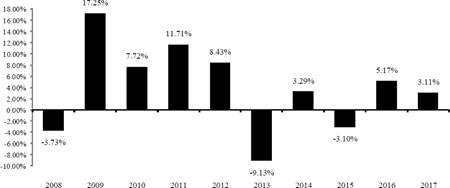

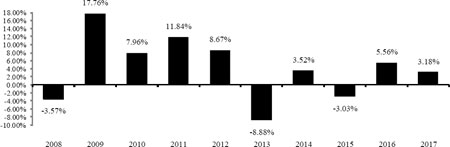

Real Return Fund – Calendar Year Total Returns

(Acquiring Fund)

Class A

Best Quarter (ended 3/31/2008): 5.77%; Worst Quarter (ended 6/30/2013): -8.29%

Class I

Best Quarter (ended 3/31/2008): 5.85%; Worst Quarter (ended 6/30/2013): -8.28%

Av

erage Annual Total Returns as of December 31, 2017

| Acquired Fund – Average Annual Total Returns as of December 31, 2017 | |

| | 1 year | Life of Fund (April 29, 2013) |

| Real Assets Fund (Class A) | 6.26% | 0.66% |

| Bloomberg Barclays U.S. Treasury Inflation Notes Index Value Unhedged (reflects no deduction for fees, expenses, or taxes) | 3.01% | 0.01% |

| 33% FTSE EPRA/NAREIT Developed Index, 33% Bloomberg Barclays Commodity Index, 34% Bloomberg Barclays U.S. TIPS Index (reflects no deduction for fees, expenses, or taxes) | 5.32% | -0.98% |

| FTSE EPRA/NAREIT Developed Real Estate Index (reflects no deduction for fees, expenses, or taxes) | 11.42% | 4.97% |

| Bloomberg Commodity Index (reflects no deduction for fees, expenses, or taxes) | 1.70 | -8.35% |

| Acquiring Fund – Average Annual Total Returns as of December 31, 2017 | |

| | 1 year | 5 year | 10 year |

| Real Return Fund (Class A) | 3.11% | -0.28% | 3.80% |

| Real Return Fund (Class I) | 3.18% | -0.08% | 4.03% |

| Bloomberg Barclays U.S. TIPS Index (reflects no deduction for fees, expenses or taxes) | 3.01% | 0.13%% | 3.53% |

The following table shows the capitalization of each Fund as of December 31, 2017, and of the Real Return Fund on a pro forma combined basis as of December 31, 2017 after giving effect to the proposed Reorganization. The actual net assets of the Real Assets Fund and the Real Return Fund on the Closing Date will differ due to fluctuations in net asset values, subsequent purchases, and redemptions of shares. No assurance can be given as to how many shares of the Real Return Fund will be received by shareholders of Real Assets Fund on the Closing Date, and the following table should not be relied upon to reflect the number of shares of the Real Return Fund that will actually be received.

| | Net Assets | Net Asset Value Per Share | Shares Outstanding |

| Real Assets Fund (Acquired Fund) – Class A | $12,153,258 | $9.84 | 1,234,603 |

| Real Return Fund (Acquiring Fund) – Class A | $1,195,715,417 | $9.95 | 120,139,964 |

| Adjustments | $0 | $0 | (13,170) (b) |

Pro forma Real Return Fund (assuming the Reorganization is approved) | $1,207,868,675 | $9.95 | 121,361,397 |

| Real Assets Fund (Acquired Fund) – Class I | $513 | $9.86 | 52 |

| Real Return Fund (Acquiring Fund) – Class I | $863,415,939 | $10.06 | 85,800,325 |

| Adjustments | $0 | $0 | (1) (b) |

Pro forma Real Return Fund (assuming the Reorganization is approved) | $863,416,452 | $10.06 | 85,800,376 |

| (a) | The costs and expenses associated with the Reorganization relating to the solicitation of proxies, including preparing, filing, printing, and mailing of the proxy statement and related disclosure documents, and the related legal fees, including the legal fees incurred in connection with the analysis under the Code of the tax treatment of this transaction as well as the costs associated with obtaining a consent of independent registered public accounting firm, will all be borne by JNAM, and no sales or other charges will be imposed on Contract Owners in connection with the Reorganization. There are no transaction expenses, such as trade commissions, related fees and taxes, or any foreign exchange spread costs (“Transaction Costs”), associated with the Reorganization. |

| (b) | The adjustment to the pro forma shares outstanding number represents a decrease in shares outstanding of the Acquiring Fund to reflect the exchange of shares of the Acquired Fund. |

The Reorganization provides for the acquisition of all the assets and all the liabilities of the Real Assets Fund by the Real Return Fund. If the Reorganization had taken place on December 31, 2017, shareholders of the Real Assets Fund would have received 1,221,433 and 51 Class A and Class I shares, respectively, of the Real Return Fund.

After careful consideration, the JVST Board unanimously approved the Plan of Reorganization with respect to the Real Assets Fund. Accordingly, the JVST Board has submitted the Plan of Reorganization for approval by the Real Assets Fund’s shareholders. The JVST Board recommends that you vote “FOR” this Proposal.

* ��* * * *

A

DDITIONAL INFORMATION ABOUT THE REORGANIZATION

T

erms of the Plan of Reorganization

The terms of the Plan of Reorganization are summarized below. For additional information, you should consult the Plan of Reorganization, a copy of which is attached as Appendix A.

If shareholders of the Acquired Fund approve the Plan of Reorganization, then the assets of the Acquired Fund will be acquired by, and in exchange for, Class A and Class I shares, respectively, of the Acquiring Fund and the liabilities of the Acquired Fund will be assumed by the Acquiring Fund. The Acquired Fund will then be terminated by JNLST, and the Class A and Class I shares of the Acquiring Fund distributed to the Class A and Class I shareholders, respectively, of the Acquired Fund in the redemption of the Class A and Class I Acquired Fund Shares. Immediately after completion of the Reorganization, the number of shares of the Acquiring Fund then held by former shareholders of the Acquired Fund may be different than the number of shares of the Acquired Fund that had been held immediately before completion of the Reorganization, but the total investment will remain the same (i.e., the total value of the Acquiring Fund shares held immediately after the completion of the Reorganization will be the same as the total value of the Acquired Fund shares formerly held immediately before completion of the Reorganization).

It is anticipated that the Reorganization will be consummated as of the close of business on August 10, 2018, or on such later date as may be deemed necessary in the judgment of the JVST Board or JNLST Board and in accordance with the Plan of Reorganization, subject to the satisfaction of all conditions precedent to the closing. It is not anticipated that the Acquired Fund will hold any investment that the Acquiring Fund would not be permitted to hold (“non-permitted investments”).

De

scription of the Securities to Be Issued

The Class A shareholders of the Acquired Fund will receive Class A shares of the Acquiring Fund, and the Class I shareholders of the Acquired Fund will receive Class I shares of the Acquiring Fund in accordance with the procedures provided for in the Plan of Reorganization. Each such share will be fully paid and non-assessable by JNLST when issued and will have no preemptive or conversion rights.

JNLST may issue an unlimited number of full and fractional shares of beneficial interest of the Acquiring Fund and divide or combine such shares into a greater or lesser number of shares without thereby changing the proportionate beneficial interests in JNLST. Each share of the Acquiring Fund represents an equal proportionate interest in that Fund with each other share. JNLST reserves the right to create and issue any number of Fund shares. In that case, the shares of the Acquiring Fund would participate equally in the earnings, dividends, and assets of the Fund. Upon liquidation of the Acquiring Fund, shareholders are entitled to share pro rata in the net assets of the Fund available for distribution to shareholders. The Acquiring Fund is a series of JNLST.

JNLST currently offers two classes of shares, Class A and Class I shares, for the Acquiring Fund. All of the JNLST Funds have adopted a distribution plan in accordance with the provisions of Rule 12b-1 under the 1940 Act. Pursuant to the distribution plan, Class A shares will be charged a Rule 12b-1 fee at the annual rate of 0.30% of the average daily net assets attributable to the Class A shares of the respective Fund. Because these distribution/service fees are paid out of the Funds’ assets on an ongoing basis, over time these fees will increase your cost of investing and may cost more than paying other types of charges. Class I shares are not charged a 12b-1 fee.

At a meeting of the JVST Board of Trustees (in this section, the “JVST Board”) held on February 28 – March 2, 2018, (the “Board Meeting”), the JVST Board, including all of the independent trustees, who are not interested persons of the funds (as defined in the Investment Company Act of 1940, as amended) (the “Independent Trustees”), considered information relating to the proposed reorganization of Acquired Funds, a series of the JVST, into the Acquiring Fund, a series of the JNLST. Prior to approving the Reorganization, the Independent Trustees reviewed the foregoing information with their independent legal counsel and with management, reviewed with independent legal counsel applicable law and their duties in considering such matters, and met with independent legal counsel in a private session without management present. The JVST Board considered a number of principal factors presented at the time of the JVST Board Meeting in reaching its determinations, including the following:

| · | Investment Objectives and Investment Strategies. The JVST Board considered that the Reorganization will permit the Contract Owners and others with beneficial interest in the Acquired Fund to continue to invest in a professionally managed fund with similar investment goals, noting that the Acquired Fund’s investment objective is to seek long-term real return through an allocation in stocks and other asset classes and strategies through investment in Underlying Funds, and the Acquiring Fund’s investment objective is to seek maximum real return, consistent with preservation of real capital and prudent investment management. The JVST Board also considered that the Acquired Fund is structured as a fund-of-funds, while the Acquiring Fund is a stand-alone fund that is managed by a sub-adviser. The JVST Board noted that both the Acquired and Acquiring Funds have an investment mandate that focuses on inflation-related securities and that the Acquiring Fund makes up approximately 36% of the Acquired Fund’s holdings, making it the Acquired Fund’s largest underlying holding. As described below, the JVST Board also considered how the Acquired Fund’s shareholders will benefit from the Reorganization. For a full description of the investment objectives and investment strategies of the Acquired Fund and Acquiring Fund, see “Comparison of Investment Objectives and Principal Investment Strategies.” |

| · | Operating Expenses. The JVST Board considered that, if approved by the Acquired Fund’s shareholders, the Reorganization will result in a Combined Fund with a total annual fund operating expense ratio that is lower than those of the Acquired Fund currently, though the Combined Fund will have higher management fees than the Acquired Fund does currently. The JVST Board noted that the lower total annual fund operating expense ratio after the Reorganization is primarily a result from having no acquired fund fees and expenses for the Combined Fund. The JVST Board further noted that the Acquiring Fund’s total annual expense ratio and management fees are not expected to change as a result of the Reorganization. See “Comparative Fee and Expense Tables.” |

| · | Larger Asset Base. The JVST Board considered that the Reorganization may benefit Contract Owners and others with beneficial interests in the Acquired Fund by allowing them to invest in the Combined Fund that has a larger |

asset base than that of the Acquired Fund currently. The JVST Board noted that as of December 31, 2017, the Acquired Fund had assets of $12.15 million as compared to assets of $2,059.13 million for the Acquiring Fund. The JVST Board considered that, according to management, the Acquired Fund does not have good prospects for growth, and thus increasing its size through a reorganization into the Acquiring Fund appears to be the best way to offer Contract Owners and other investors a comparable investment alternative with assets that may be operated more efficiently than the Acquired Fund. The JVST Board considered that reorganizing the Acquired Fund into the Acquiring Fund offers Contract Owners and other investors the ability to benefit from economies of scale.

| · | Performance. The JVST Board considered that the Acquiring Fund has had better performance than the Acquired Fund for the 3-year period ended December 31, 2017. The Board also noted that the Acquiring Fund outperformed the Acquired Fund during calendar years 2014 and 2015 and that the Acquiring Fund has outperformed the Funds’ primary benchmark, the Bloomberg Barclays U.S. TIPS Index, in the three-month, one-year, three-year, five-year and ten-year periods ended December 31, 2017. |

| · | Investment Adviser and Other Service Providers. The JVST Board considered that that the Funds currently have the same investment adviser and administrator, JNAM, and the same service providers, with the exception of sub-adviser. It considered that the Acquired Fund will have the same investment adviser and other service providers after the Reorganization as it has currently. Specifically, the JVST Board noted that the Acquired Fund does not have a sub-adviser whereas the Acquiring Fund is sub-advised by Pacific Investment Management Company LLC, and it considered that after the Reorganization, the Combined Fund will be sub-advised by Pacific Investment Management Company LLC. The JVST Board discussed how the addition of a sub-adviser may benefit the Acquired Fund’s shareholders. The JVST Board considered management’s high level of conviction in the Acquiring Fund, as well as management’s confidence in the Acquiring Fund’s sub-adviser. See “Comparison of Investment Adviser and Sub-Adviser.” |

| · | Federal Income Tax Consequences. The Board took into account that Contract Owners are not expected to have adverse tax consequences as a result of the Reorganization. Although the Acquired Fund will sell all of its portfolio securities prior to and in connection with the Reorganization, which will result in gain or loss that is allocated to the Acquired Fund’s shareholders, the Reorganization is not expected to result in any material adverse federal income tax consequences to shareholders of the Acquired Fund that are Separate Accounts, in light of their tax favored status, and Jackson National. |

| · | Costs of Reorganization. The JVST Board considered that the costs and expenses associated with the Reorganization relating to the solicitation of proxies, including preparing, filing, printing, and mailing of the proxy statement and related disclosure documents, and the related legal fees, including the legal fees incurred in connection with the analysis under the Code of the tax treatment of this transaction, as well as the costs associated with obtaining a consent of independent registered public accounting firm will all be borne by JNAM, and no sales or other charges will be imposed on Contract Owners in connection with the Reorganization. Please see “Additional Information about the Reorganization” above for more information. |

In summary, in determining whether to recommend approval of the Reorganization, the JVST Board considered factors including (1) the terms and conditions of the Reorganization and whether the Reorganization would result in dilution of the Acquired Fund’s shareholders’, Contract Owners’, and plan participants’ interests; (2) the compatibility of the Funds’ investment objectives, investment strategies and investment restrictions, as well as shareholder services offered by the Funds; (3) the expense ratios and information regarding the fees and expenses of the Funds; (4) the advantages and disadvantages to the Acquired Fund’s shareholders, Contract Owners, and plan participants of having a larger asset base in the Combined Fund; (5) the relative historical performance of the Funds; (6) the management of the Funds; (7) the federal income tax consequences of the Reorganization; and (8) the costs of the Reorganization. No one factor was determinative and each Trustee may have attributed different weights to the various factors.