UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File number:811-08894

JNL Series Trust

(Exact name of registrant as specified in charter)

1 Corporate Way, Lansing, Michigan 48951

(Address of principal executive offices)

225 West Wacker Drive, Suite 1200, Chicago, Illinois 60606

(Mailing address)

Daniel W. Koors

Jackson National Asset Management, LLC

225 West Wacker Drive, Suite 1200

Chicago, Illinois 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312)338-5800

Date of Fiscal Year End: December 31

Date of Reporting Period: December 31, 2018

FormN-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1). The Commission may use the information provided on FormN-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by FormN-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in FormN-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Report to Shareholders.

CHOOSE THE INBOX. NOT THE MAILBOX. Less waste. More convenience. Your choice. Three easy ways to go paperless: 1. Mail this postage-paid card 2. Call1-866-349-4564 3. Visit jackson.com I consent to receive by electronic delivery: ALL DOCUMENTS Periodic and immediate confirmation statements Annual and semi-annual reports Annual statements (Variable Products and Fixed Index Annuities only)(Variable Products only) (Fixed, Fixed Index and Target Select Annuities only)Other contract-related correspondence Prospectuses and prospectus supplements (Variable Products only) This consent will continue until revoked and will cover delivery to you in the form of ane-mail or by notice to you of a document’s availability on Jackson National Life Insurance Company®‘s (also referred to as Jackson®) website. For jointly owned contracts, all Joint Owners are consenting to electronic delivery and use of the singlee-mail address below. Please contact the appropriate Jackson Service Center or go to www.jackson.com to update youre-mail address, revoke your consent to electronic delivery, or request paper copies. Certain types of correspondence may continue to be delivered by the United States Postal Service for compliance reasons. Registration on Jackson’s website (www.jackson.com) is required for electronic delivery of contract-related correspondence Please write legibly. Fold Here Signature: Date: Signature: Date:E-mail address:I (We) will notify Jackson of any change to thise-mail address. Name: Address: City: State: ZIP: Policy Number Owner’s State of Residence Phone Number – – The computer hardware and software requirements that are necessary to receive, process and retain electronic communications that are subject to this consent are as follows: To view and download material electronically, you must have a computer with Internet access, an activee-mail account and Adobe Acrobat Reader. If you don’t already have Adobe Acrobat Reader, you can download it free from www.adobe.com. There is no charge for electronic delivery of electronic communications, although you may incur the costs of Internet access and of such computer and related hardware and software as may be necessary for you to receive, process and retain electronic communications from Jackson. Please make certain you have given Jackson a currente-mail address. Also let Jackson know if thate-mail address changes. We may need to notify you of a document’s availability throughe-mail. You may request paper copies, whether or not you consent or revoke your consent to electronic delivery, at any time and for no charge. Even if you have given us consent, we are not required to make electronic delivery and we have the right to deliver any communications in paper form. Tape Here VADV7339 01/19 ANNUAL REPORT December 31, 2018 JNL® Series Trust • Master Feeder Funds and Funds of Funds Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from Jackson. Instead, the reports will be made available on Jackson’s website (www.jackson.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from Jackson electronically by doing one of the following: • Mailing in the postage-paid card on the cover of this report; • Calling1-866-349-4564; or • Signing up on www.jackson.com Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. You can inform Jackson that you wish to continue receiving paper copies of your shareholder reports by contacting the appropriate Jackson Service Center. Your election to receive reports in paper will apply to all Funds held in each variable contract you purchased from Jackson. Please note that if you own more than one variable contract with Jackson, your delivery preferences must be set up for each variable contract separately. Issued by Jackson National Life Insurance Company 1 Corporate Way, Lansing, MI 48951

NO POSTAGE NECESSARY IF MAILED IN THE UNITED STATES BUSINESS REPLY MAIL FIR TS-CLA SS M IA L PERMIT NO. 600 L NA IS NG MI POSTAGE WILL BE PAID BY ADDRESSEE JACKSON PO BOX 24068 LANSING MI48909-4068 Fold Here This report is for the general information of qualified plan participants, as well as contract/policy owners of the Perspective SM, Perspective II®, Perspective Advisors SM, Perspective Advisory, Perspective Advisors IISM, Perspective Advisory IISM, Perspective L Series, Perspective Rewards®, Curiangard SM, Perspective Advantage SM, Perspective Focus®, Fifth Third Perspective, Jackson Private WealthSM, Retirement Latitudes®, Elite Access®, Elite Access Advisory SM, Elite Access Advisory II, Perspective (New York), Perspective II (New York), Perspective Advisors II (New York), Perspective L Series (New York), Curiangard (New York), Perspective Advisors (New York), Perspective Focus (New York), Perspective Rewards (New York) and Elite Access (New York). Not all the portfolios are available in all of the products. Jackson is the marketing name for Jackson National Life Insurance Company (Home Office: Lansing, Michigan) and Jackson National Life Insurance Company of New York® (Home Office: Purchase, New York).

1 Corporate Way

Lansing, MI 48951

Toll Free: 1-800-873-5654

IMPORTANT NOTICE REGARDING DELIVERY OF SHAREHOLDER DOCUMENTS

Dear Client:

If you are a current member of a household with multiple variable products, and have not instructed Jackson otherwise, you currently receive only one copy of the following general documents: Prospectus, Annual and Semi-Annual Report, and other documents as permitted under applicable federal laws relating to Jackson’s variable products and their underlying investment options.

We will continue to send one such copy of these general documents unless and until we receive contrary instructions from you. This delivery policy does not apply to account statements, confirmation statements, or other documents reflecting transaction activity, which you will continue to receive individually.

You may choose to receive a separate copy of these general documents at any time by contacting us toll-free at 1-800-873-5654. Once we receive your request, we will start sending you separate copies within 30 days of receipt of your request.

If you would rather receive your prospectus and other documents via e-mail, please register for Jackson’s Green Delivery Program by visiting the www.Jackson.com. Our Go Paperless process is quick and easy for policyholders – just have your policy number available when you register.

Jackson appreciates your cooperation as we do our part to aid the environment by reducing the amount of paper we distribute. While we’re committed to providing you with the information you need in the format you prefer, we are always looking for new ways to operate more efficiently.

Variable Products issued by Jackson National Life Insurance Company® and distributed by Jackson National Life Distributors LLC, member FINRA. 800/873-5654

JNL Series Trust Master Feeder Funds and Funds of Funds

December 31, 2018

JNL Series Trust Master Feeder Funds and Funds of Funds including: JNL/American Funds® Balanced Fund, JNL/American Funds Blue Chip Income and Growth Fund, JNL/American Funds Capital Income Builder Fund, JNL/American Funds Global Bond Fund, JNL/American Funds Global Small Capitalization Fund, JNL/American Funds Growth-Income Fund, JNL/American Funds International Fund, JNL/American Funds New World Fund, JNL/Vanguard Capital Growth Fund, JNL/Vanguard Equity Income Fund, JNL/Vanguard International Fund, JNL/Vanguard Small Company Growth Fund, JNL Institutional Alt 25 Fund, JNL Institutional Alt 50 Fund, JNL/American Funds Moderate Growth Allocation Fund, JNL/American Funds Growth Allocation Fund, JNL Moderate Growth Allocation Fund, JNL Growth Allocation Fund, JNL Aggressive Growth Allocation Fund, JNL/Franklin Templeton Founding Strategy Fund, JNL/Mellon Capital 10 x 10 Fund, JNL/Mellon Capital Index 5 Fund, JNL/S&P 4 Fund, JNL/S&P Managed Conservative Fund, JNL/S&P Managed Moderate Fund, JNL/S&P Managed Moderate Growth Fund, JNL/S&P Managed Growth Fund, JNL/S&P Managed Aggressive Growth Fund, JNL/Vanguard US Stock Market Index Fund, JNL/Vanguard International Stock Market Index Fund, JNL/Vanguard Global Bond Market Index Fund

JNL Series Trust Approval of the Trust’s Investment Advisory and Sub-Advisory Agreements |

JNL Series Trust Supplements to Prospectus

Variable Products issued by Jackson National Life Insurance Company® and distributed by Jackson National Life Distributors LLC, member FINRA. 800/873-5654

JNL Series Trust Master Feeder Funds and Funds of Funds

December 31, 2018

Dear Investor,

Enclosed is the annual report for the JNL Series Trust Master Feeder Funds and Funds of Funds for the year ended December 31, 2018, together with Management’s Discussion of Fund Performance for each of the Funds.

Enclosed is the annual report for the JNL Series Trust Master Feeder Funds and Funds of Funds for the year ended December 31, 2018, together with Management’s Discussion of Fund Performance for each of the Funds.

Securities markets saw the abrupt return of volatility in 2018 after a placid and profitable 2017. The S&P 500 Index finished down more than -4% as it suffered several sharp and sudden downswings throughout the year, including a nearly 20% drop from its September highs through the last week of December. Small and mid-cap stocks fared worse. Foreign markets diverged from the U.S. by selling off before the summer in suffering the most. International developed equity markets fell double digits, with emerging markets dropping 14.6%. Global fixed income spent most of the year in negative territory before a flight to safety during the fourth quarter fueled by buying government and investment grade bonds that helped the Bloomberg Barclays U.S. Aggregate Bond Index to finish the year virtually flat (up 0.01%). Non-core fixed income segments, especially high yield bonds and emerging market debt, posted notable losses.

The return of volatility was not necessarily unwarranted. The initial bout in February was likely sparked by a steady uptick in long term bond yields that raised concerns of higher borrowing costs for companies and governments, exacerbated by a violent unwinding of low volatility trades that bet on the continuation of a docile market environment. That chain reaction served as a wake up call to investors and quickly passed, but concerns about the impact of higher interest rates on business profitability and stock valuations after a long period of extremely low rates persisted. Debt market turmoil in Italy, Turkey and Argentina, along with slowing economic growth, soured investors on markets overseas mid-year as U.S. equities regained their footing. That, however, only served as a prelude to further concerns about global growth that hit stocks during the fourth quarter as U.S. China trade tensions and continued U.S. Federal Reserve rate hikes added to negative expectations for future earnings.

While not entirely unexpected, the suddenness and magnitude of downward volatility always serves as a jolt to investors. In last year’s letter we noted that the calmness of the market in 2017 (an entire year without a 5% or more correction) was unusual and likely unsustainable. A history of market declines tells us that a 10% drop in equities is a roughly once a year experience, while 20% drops happen about once every three and a half years on average. By the end of 2017, the last broad based 20% drop in large cap U.S. equities had concluded in March 2009—more than eight and half years before the start of 2018! This is not to say that such volatility is predictable, merely to put things in perspective as a reminder that post financial crisis market activity has been unusually moderate on the heels of unprecedentedly easy monetary policy. Moderation may have lulled a new generation of investors into a false sense of confidence, though history has shown that there has yet to be a solution to the cyclicality of markets.

The best that we can do as investors is to build diversified portfolios to withstand downswings such that long term plans remain intact and investment goals are still achievable. Although there were few places to hide in the market that offered positive returns during 2018, studies have shown that investors do better mixing their investment choices among a wide variety of asset classes and strategies instead of trying to guess or time exposure into a select few. As sentiment waned and volatility increased in 2018, market leadership shifted between sectors, styles and asset classes. As mentioned earlier, domestic fixed income was under water for most of the year before recovering in the fourth quarter to become the best absolute performing asset class. Utilities, among the bottom performing areas of the S&P 500 in June, finished the year up 4.1% behind only health care among top performers. Indeed, the dispersion of returns between sectors within the S&P 500 Index ranged from -18.10% (energy) to 6.47% (health care).

At Jackson, we seek to offer investors the building blocks for creating well diversified portfolios, and the freedom to do so however they see fit. We offer a wide array of Funds across asset classes and investment styles that allows investors to build portfolios that suit their individual risk tolerance and goals. We seek best of breed Sub-Advisors that we think represent not only the finest organizations in the industry but also offer unique investment approaches able to persistently meet our expectations. We offer both passive and actively managed options as we recognize the strengths and weaknesses of each approach can complement the other. These many traits all support and benefit from diversification to allow for the creation of a portfolio suited to any kind of investor.

No one knows what markets have in store for investors in 2019. A number of economic and geopolitical risks remain in the forefront, including slowing global growth, trade tensions, Brexit, excessive government and company debt and rising interest rates. No one can predict when and how these forces will act on markets, what other unknown issues may be lurking, or what the long term consequences will be on markets and investors. Against this uncertainty it is best to have a steady asset allocation plan to provide constancy amid a sea of market ambiguity. That, we think, is how successful investors achieve their goals.

Thank you for choosing Jackson for your investment needs.

Mark D. Nerud

President and Chief Executive Officer

JNL Series Trust

1

| JNL Series Trust Master Feeder Funds and Funds of Funds Market Summary (Unaudited) |

Major Indices Returns for the Year Ended December 31, 2018

Domestic Equity | Developed International Equity | ||||||||||

S&P 500 Index | -4.38 | % | MSCI All Country World ex-USA Index (Net) | -9.42 | % | ||||||

S&P MidCap 400 Index | -11.08 | MSCI EAFE Index (Net) | -13.79 | ||||||||

MSCI USA Index | -4.50 | ||||||||||

MSCI USA Mid Cap Index | -9.37 | Emerging Markets | |||||||||

MSCI USA Small Cap Index | -13.35 | MSCI Emerging Markets Index (Net) | -14.58 | % | |||||||

Fixed Income | Alternative Assets | ||||||||||

Bloomberg Barclays Global Aggregate Bond Index | -1.20 | % | Bloomberg Commodity Index | -11.25 | % | ||||||

Bloomberg Barclays U.S. Aggregate Bond Index | 0.01 | FTSE EPRA/NAREIT Developed Index | -4.74 | ||||||||

Bloomberg Barclays U.S. Corporate High Yield Bond Index | -9.37 | ||||||||||

Alternative Strategy | |||||||||||

Wilshire Liquid Alternative Index | -4.26 | % | |||||||||

Domestic Equity: Volatility returned to the markets in 2018, after a calm and profitable 2017. All the major broad stock market indices lost ground during a turbulent year that saw a major selloff in stocks to finish the year. Steady gains midyear were bracketed by highly volatile trading during the first and fourth quarters that at times saw huge daily swings in prices that eventually led to losses. Volatility was even more severe among small- and mid-cap stocks, especially during the fourth quarter, resulting in even sharper losses by year end. While the heightened volatility favored value and traditionally defensive sectors of the market at times, growth stocks outperformed across the market cap spectrum overall, driven by information technology and ecommerce names. Still, it was health care and utilities that ultimately finished the year as the top performing sectors. Rising interest rates and a violent unwinding of low volatility trades following a docile 2017 market environment set the tone during the first quarter. The fourth quarter selloff was sparked by increased fears of slowing economic growth amid continued tightening of monetary policy by the U.S. Federal Reserve (“Fed”), which was also unwinding its massive balance sheet built up after the global financial crisis. Volatility is likely to continue in the first half of the year amid U.S. China trade negotiations and potential continued quantitative tightening on the part of the Fed.

Fixed Income: Concerns regarding a slowdown in growth and Fed monetary policy led to a rocky path for bonds. Bonds seemingly entered into a game of seesaw with the stock market in 2018. When bonds sold off to start the year, the resulting increase in interest rates sparked turmoil among stocks. As investors fled back to bonds, lower interest rates fueled a midyear rise in stocks, which ultimately ended in another reverse to end the year. All told, the investment grade U.S. bond market ended the year virtually flat, while global bonds posted modest losses. Government and investment grade bonds seesawed the most, but ultimately benefitted from lower rates by year end. High yield and credit sensitive bonds generally lost ground on valuation concerns, uncertainty about corporate credit ratings amid continued Fed rate hikes and slowing economic growth. Global bonds were hurt by a stronger U.S. Dollar for most of the year, with emerging markets (“EM”) debt hit especially hard by the Dollar and turmoil in select countries.

Developed International Equity: Slowing growth in Europe starting in the second quarter weighed heavily on foreign developed markets in 2018. Stock performance sharply diverged from the U.S. in the beginning of June, driven in part by a blowup in Italian politics that fueled fears of further Euro disruption. Weaker growth in Europe took the bloom off the global synchronized growth story, with U.S. economic strength and higher interest rates making it a more attractive option. Signals from the European Central Bank that it would be ending its quantitative easing program kept a lid on returns during the fourth quarter, though results were more in line with the U.S. Despite more encouraging economic news out of Japan, stocks were down double digits there as well.

Emerging Markets: After a standout 2017, EM bonds and equities were the laggards in their respective asset classes in 2018. EM equities finished the year down more than 14% despite holding up relatively better during the fourth quarter global sell off. A strong U.S. Dollar for most of the year, slowing economic growth in China and Europe and weaker commodity prices all contributed to a midyear downswing that diverged sharply from U.S. performance. EM debt followed equities lower midyear troubled by the stronger Dollar and debt market turmoil in Turkey and Argentina from which it didn’t really recover.

Alternative Assets: It was a mixed year for alternative assets as oil prices first soared then plummeted, throwing the commodities and natural resources categories into turmoil. Both segments posted double digit losses for the year in significantly lagging equities. Global infrastructure related assets also delivered losses, mostly in line with global equities. U.S. real estate was the relative bright spot in the category as it kept pace with U.S. equities, while global real estate investment trusts outperformed the lackluster global equity marketplace.

Alternative Strategies: Alternative investment strategies posted negative returns overall as measured by the Wilshire Liquid Alternative Index in slightly outperforming equities and trailing fixed income. Alternative strategies lagged stocks for most of the year but held up considerably better during the fourth quarter equity selloff. The event driven segment of the Index, which includes merger arbitrage strategies, stood out with positive returns for the year. The global macro and hedged equity segments underperformed the broader Index given their tilt towards equity and international exposure.

2

| JNL/American Funds Master Feeder Funds Capital Research and Management Company (Unaudited) |

JNL/American Funds Balanced Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Balanced Fund outperformed its primary benchmark by posting a return of -4.89% for Class A shares compared to -9.42% for the MSCI All Country World Index (Net). The Fund outperformed its secondary benchmark which posted a return of -6.42% for the 65% MSCI All Country World Index (Net), 35% Bloomberg Barclays Global Aggregate Bond Index.

The Fund seeks high total return (including income and capital gains) consistent with preservation of capital over the long term through exclusive investment in the Class 1 shares of the American Funds Insurance Series® - Asset Allocation FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/American Funds Blue Chip Income and Growth Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Blue Chip Income and Growth Fund underperformed its benchmark by posting a return of -9.00% for Class A shares compared to -4.38% for the S&P 500 Index.

The Fund seeks both income exceeding the average yield on U.S. stocks generally and to provide an opportunity for growth of principal consistent with sound common stock investing through exclusive investment in the Class 1 shares of the American Funds Insurance Series® - Blue Chip Income and Growth FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/American Funds Capital Income Builder Fund

Composition as of December 31, 2018: | ||

Global Balanced | 100.0 | % |

Total Investments | 100.0 | % |

Total Return |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

Since Inception | -5.90 | % | Since Inception | -5.70 | % | |

‡Inception date August 13, 2018 |

| |||||

†Inception date August 13, 2018 |

| |||||

For the period from August 13, 2018 to December 31, 2018, JNL/American Funds Capital Income Builder Fund outperformed its primary benchmark by posting a return of -5.90% for Class A shares compared to -11.04% for the MSCI All Country World Index (Net). The Fund outperformed its secondary benchmark which posted a return of -7.80% for the 70% MSCI All Country World Index NR USD, 30% Bloomberg Barclays US Aggregate Bond Index.

The Fund seeks both to provide a level of current income that exceeds the average yield on U.S. stocks generally and to provide a growing stream of income over the years by investing through exclusive investment in the Class 1 shares of the American Funds Insurance Series® - Capital Income Builder FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/American Funds Global Bond Fund

Composition as of December 31, 2018: | ||

Global Fixed Income | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Global Bond Fund underperformed its benchmark by posting a return of -1.62% for Class A shares compared to -1.20% for the Bloomberg Barclays Global Aggregate Index.

The Fund seeks, over the long term, a high level of total return consistent with prudent investment management through exclusive investment in the Class 1 shares of the American Funds Insurance Series® – Global Bond FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

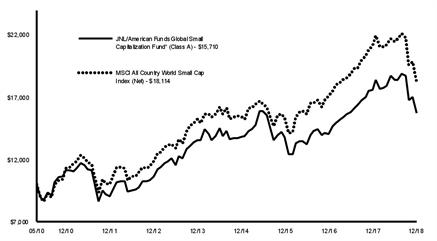

JNL/American Funds Global Small Capitalization Fund

Composition as of December 31, 2018: | ||

Global Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, the JNL/American Funds Global Small Capitalization Fund outperformed its benchmark by posting a return of -10.77% for Class A shares compared to -14.39% for the MSCI All Country World Small Cap Index (Net).

The Fund seeks growth of capital over time through exclusive investment in the Class 1 shares of the American Funds Insurance Series® – Global Small Capitalization FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/American Funds Growth-Income Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Growth-Income Fund outperformed its benchmark by posting a return of -2.16% for Class A shares compared to -4.38% for the S&P 500 Index.

The Fund seeks long term growth of capital and income through exclusive investment in the Class 1 shares of the American Funds Insurance Series® – Growth Income FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/American Funds International Fund

Composition as of December 31, 2018: | ||

International Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds International Fund outperformed its benchmark by posting a return of -13.53% for Class A shares compared to -14.20% for the MSCI All Country World ex USA Index (Net).

The Fund seeks long term growth of capital through exclusive investment in the Class 1 shares of the American Funds Insurance Series® – International FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the

3

| JNL/American Funds Master Feeder Funds Capital Research and Management Company (Unaudited) |

Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

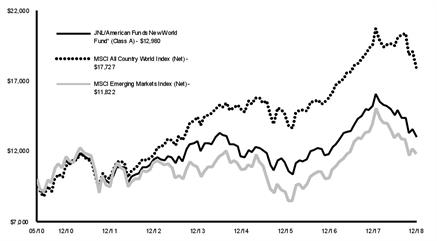

JNL/American Funds New World Fund

Composition as of December 31, 2018: | ||

Emerging Markets Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds New World Fund underperformed one of its benchmarks by posting a return of -14.41% for Class A shares compared to -9.42% for the MSCI All Country World Index and outperformed its other benchmark, the MSCI Emerging Markets Index (Net), which returned -14.58%.

The Fund seeks long term capital appreciation through exclusive investment in the Class 1 shares of the American Funds Insurance Series® – New World FundSM (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

4

| JNL/American Funds Master Feeder Funds Capital Research and Management Company (Unaudited) |

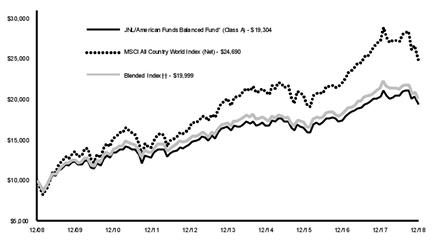

JNL/American Funds Balanced Fund

††65% MSCI All Country World Index (Net), 35% Bloomberg Barclays Global Aggregate Bond Index

Average Annual Total Returns* |

| |||||

Class A |

|

|

| Class I |

|

|

1 Year | -4.89 | % | 1 Year | -4.56 | % | |

5 Year | 3.05 |

|

| 5 Year | 3.29 |

|

10 Year | 6.80 |

|

| 10 Year | 7.04 |

|

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

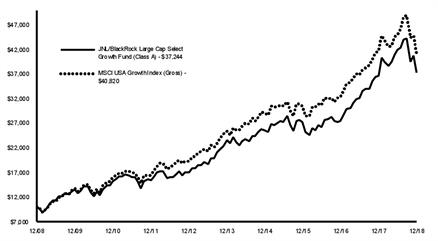

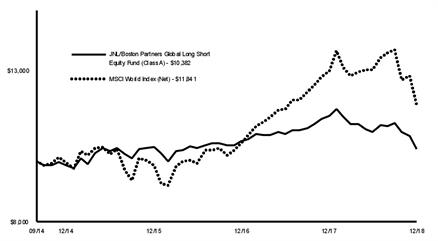

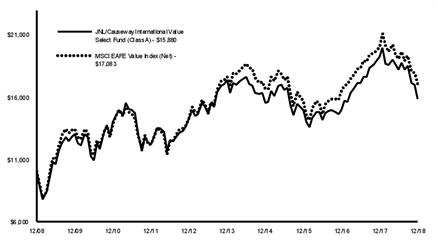

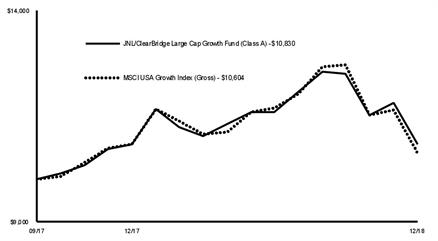

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/American Funds Blue Chip Income and Growth Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -9.00 | % | 1 Year | -8.72 | % | |

5 Year | 6.90 |

|

| 5 Year | 7.16 |

|

Since Inception | 9.25 |

|

| Since Inception | 9.49 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

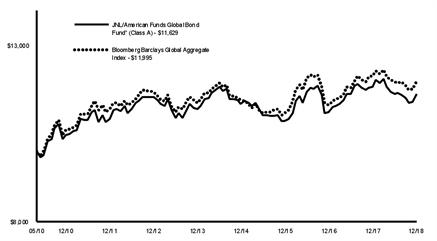

JNL/American Funds Global Bond Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -1.62 | % | 1 Year | -1.39 | % | |

5 Year | 0.77 |

|

| 5 Year | 0.99 |

|

Since Inception | 1.76 |

|

| Since Inception | 2.00 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

5

| JNL/American Funds Master Feeder Funds Capital Research and Management Company (Unaudited) |

JNL/American Funds Global Small Capitalization Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -10.77 | % | 1 Year | -10.48 | % | |

5 Year | 3.01 |

|

| 5 Year | 3.26 |

|

Since Inception | 5.35 |

|

| Since Inception | 5.59 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/American Funds Growth-Income Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -2.16 | % | 1 Year | -1.87 | % | |

5 Year | 8.07 |

|

| 5 Year | 8.33 |

|

Since Inception | 10.31 |

|

| Since Inception | 10.54 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/American Funds International Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -13.53 | % | 1 Year | -13.22 | % | |

5 Year | 1.60 |

|

| 5 Year | 1.84 |

|

Since Inception | 4.22 |

|

| Since Inception | 4.46 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

6

| JNL/American Funds Master Feeder Funds Capital Research and Management Company (Unaudited) |

JNL/American Funds New World Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -14.41 | % | 1 Year | -14.10 | % | |

5 Year | 0.48 |

|

| 5 Year | 0.74 |

|

Since Inception | 3.06 |

|

| Since Inception | 3.30 |

|

‡Inception date May 03, 2010 |

| |||||

†Inception date May 03, 2010 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

7

| JNL/Vanguard Master Feeder Funds Jackson National Asset Management, LLC (Unaudited) |

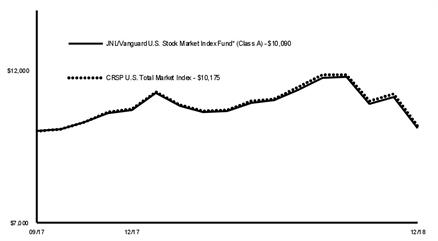

JNL/Vanguard Capital Growth Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/Vanguard Capital Growth Fund outperformed its primary benchmark by posting a return of -1.76% for Class A shares compared to -4.38% for the S&P 500 Index.

The Fund seeks long-term capital appreciation through exclusive investment in the shares of the Vanguard Variable Insurance Fund - Capital Growth Portfolio (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

JNL/Vanguard Equity Income Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/Vanguard Equity Income Fund underperformed its primary benchmark by posting a return of -6.47% for Class A shares compared to -2.32% for the MSCI USA High Dividend Yield Index (Gross).

The Fund seeks to provide an above average level of current income and reasonable long term capital appreciation through exclusive investment in the shares of the Vanguard Variable Insurance Fund - Equity Income Portfolio (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

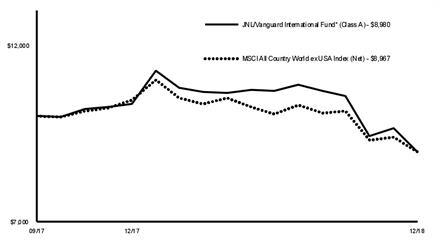

JNL/Vanguard International Fund

Composition as of December 31, 2018: | ||

International Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/Vanguard International Fund outperformed its primary benchmark by posting a return of -13.15% for Class A shares compared to -14.20% for the MSCI All Country World ex USA Index (Net).

The Fund seeks to provide long-term capital appreciation through exclusive investment in the shares of the Vanguard Variable Insurance Fund - International Portfolio (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

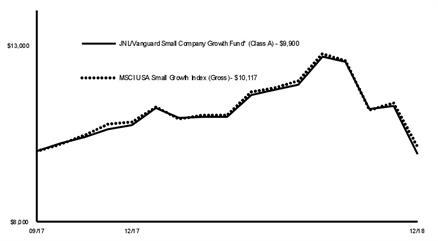

JNL/Vanguard Small Company Growth Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 100.0 | % |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/Vanguard Small Company Growth Fund underperformed its primary benchmark by posting a return of -7.82% for Class A shares compared to -6.58% for the MSCI USA Small Growth Index (Gross).

The Fund seeks to provide long-term capital appreciation through exclusive investment in the shares of the Vanguard Variable Insurance Fund - Small Company Growth Portfolio (“Master Fund”). The performance of the Fund is directly related to the performance of the Master Fund. The financial statements of the Master Fund, including the Schedule of Investments and portfolio manager commentary, are provided separately and should be read in conjunction with the Fund’s financial statements.

8

| JNL/Vanguard Master Feeder Funds Jackson National Asset Management, LLC (Unaudited) |

JNL/Vanguard Capital Growth Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -1.76 | % | 1 Year | -1.48 | % | |

Since Inception | 4.78 |

|

| Since Inception | 5.17 |

|

‡Inception date September 25, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/Vanguard Equity Income Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -6.47 | % | 1 Year | -6.17 | % | |

Since Inception | -0.16 |

|

| Since Inception | 0.24 |

|

‡Inception date September 25, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/Vanguard International Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -13.15 | % | 1 Year | -12.86 | % | |

Since Inception | -8.13 |

|

| Since Inception | -7.89 |

|

‡Inception date September 25, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

9

| JNL/Vanguard Master Feeder Funds Jackson National Asset Management, LLC (Unaudited) |

JNL/Vanguard Small Company Growth Fund

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -7.82 | % | 1 Year | -7.53 | % | |

Since Inception | -0.79 |

|

| Since Inception | -0.47 |

|

‡Inception date September 25, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

10

| JNL Alt Funds Jackson National Asset Management, LLC (Unaudited) |

The JNL Institutional Alt 25 Fund and JNL Institutional Alt 50 Fund (collectively “JNL Alt Funds”). Each Fund seeks to achieve its objective by investing in Class I shares of a diversified group of affiliated Underlying Funds (“Underlying Funds”). Each JNL Alt Fund has a target percentage allocation among the Underlying Funds that are categorized as investing in traditional asset classes and non-traditional asset classes. The Schedules of Investments and Financial Statements for the Underlying Funds are available at www.jackson.com or on the SEC’s website at www.sec.gov.

JNL Institutional Alt 25 Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 26.3 | % |

Alternative | 25.1 | |

Domestic Fixed Income | 17.9 | |

International Equity | 13.9 | |

Emerging Markets Equity | 5.6 | |

Global Equity | 5.6 | |

International Fixed Income | 3.1 | |

Global Fixed Income | 2.5 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL Institutional Alt 25 Fund underperformed its primary benchmark by posting a return of -6.97% for Class A shares compared to -5.21% for the Dow Jones Moderate Index. The Fund underperformed its blended benchmark return of -5.66% for the 25% Wilshire Liquid Alternative Index, 50% MSCI All Country World Index (Net) and 25% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is long term growth of capital and income through investment in other Funds.

The Fund allocates approximately 75% of its assets to the traditional investment categories creating a “core” component of its portfolio. The Fund then allocates approximately 25% of its assets to non-traditional investment categories creating an “alt” component of its portfolio. The Fund considers the Alternative Assets, Alternative Strategies and Risk Management investment categories to be non-traditional and all others to be traditional. Among the traditional investment categories, the Fund typically allocates approximately 5% to 45% of its assets in Underlying Funds investing in fixed income securities and 30% to 70% of its assets in Underlying Funds investing in equity securities.

The Fund underperformed its blended benchmark due to weak relative returns in the alternatives and equity sleeves plus a slight underweight allocation to fixed income. In the alternatives sleeve, strategies with higher equity net exposure, such as JNL/AQR Large Cap Relaxed Constraint Equity Fund (-13.10%) and JNL/Boston Partners Global Long Short Equity Fund (-9.22%) detracted significantly. Commodities failed to gain traction during the year due in part to a strong U.S. Dollar, leading to poor returns from JNL/Neuberger Berman Risk Balanced Commodity Strategy Fund (-10.22%). Allocations to infrastructure and real estate also failed to beat the alternatives benchmark.

JNL/Harris Oakmark Global Equity Fund (-20.97%) and JNL/Causeway International Value Select Fund (-17.26%), two value oriented managers, detracted most from results among international stocks. JNL/Oppenheimer Emerging Markets Innovator Fund (-22.25%) and JNL/Lazard Emerging Markets Fund (-18.13%) also lagged as emerging markets suffered in 2018. Underperformance by small and mid-cap strategies in the U.S. was partially offset by manager selection in those areas and JNL/T. Rowe Price Established Growth Fund (-1.13%). In the fixed income sleeve, positive manager selection helped offset some of the relative weakness from an underweight position and weakness from the credit and emerging markets sectors.

JNL Institutional Alt 50 Fund

Composition as of December 31, 2018: | ||

Alternative | 50.2 | % |

Domestic Equity | 15.8 | |

Domestic Fixed Income | 14.0 | |

International Equity | 8.7 | |

Emerging Markets Equity | 3.6 | |

Global Equity | 3.4 | |

International Fixed Income | 2.3 | |

Global Fixed Income | 2.0 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL Institutional Alt 50 Fund underperformed its primary benchmark by posting a return of -6.19% for Class A shares compared to -5.21% for the Dow Jones Moderate Index. The Fund underperformed its blended benchmark return of -4.86% for the 50% Wilshire Liquid Alternative Index, 30% MSCI All Country World Index (Net), 20% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is long term growth of capital and income through investment in other Funds.

The Fund allocates approximately 50% of its assets to the traditional investment categories creating a “core” component of its portfolio. The Fund then allocates approximately 50% of its assets to non-traditional investment categories creating an “alt” component of its portfolio. The Adviser considers the Alternative Assets, Alternative Strategies and Risk Management investment categories to be non-traditional and all others to be traditional. Among the traditional investment categories, the Fund typically allocates approximately 0% to 40% of its assets in Underlying Funds investing in fixed-income securities and 10% to 50% of its assets in Underlying Funds investing in equity securities.

The Fund underperformed its blended benchmark due to weak relative returns in the alternatives and equity sleeves plus a slight underweight allocation to fixed income. In the alternatives sleeve, strategies with higher equity net exposure, such as JNL/AQR Large Cap Relaxed Constraint Equity Fund (-13.10%) and JNL/Boston Partners Global Long Short Equity Fund (-9.22%) detracted significantly. Commodities failed to gain traction during the year due in part to a strong U.S. Dollar, leading to poor returns from JNL/Neuberger Berman Risk Balanced Commodity Strategy Fund (-10.22%). Allocations to infrastructure and real estate also failed to beat the alternatives benchmark.

JNL/Harris Oakmark Global Equity Fund (-20.97%) and JNL/Causeway International Value Select Fund (-17.26%), two value oriented managers, detracted most from results among international stocks. JNL/Oppenheimer Emerging Markets Innovator Fund (-22.25%) and JNL/Lazard Emerging Markets Fund (-18.13%) also lagged as emerging markets suffered in 2018. Underperformance by small and mid-cap strategies in the U.S. was partially offset by manager selection in those areas and JNL/T. Rowe Price Established Growth Fund (-1.13%). In the fixed income sleeve, positive manager selection helped offset some of the relative weakness from an underweight position and weakness from the credit and emerging markets sectors.

11

| JNL Alt Funds Jackson National Asset Management, LLC (Unaudited) |

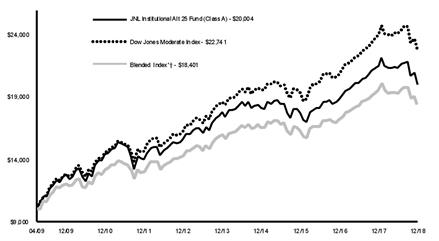

JNL Institutional Alt 25 Fund

†25% Wilshire Liquid Alternative Index, 50% MSCI All Country World Index (Net) and 25% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -6.97 | % | 1 Year | -6.62 | % | |

5 Year | 2.42 |

|

| 5 Year | N/A |

|

Since Inception | 7.38 |

|

| Since Inception | -2.54 |

|

‡Inception date April 06, 2009 |

| |||||

†Inception date September 25, 2017 |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

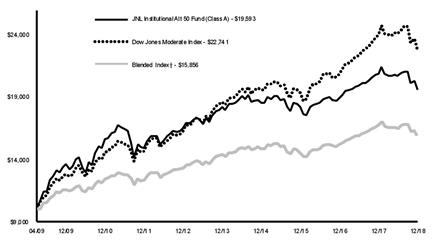

JNL Institutional Alt 50 Fund

†50% Wilshire Liquid Alternative Index, 30% MSCI All Country World Index (Net) and 20% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -6.19 | % | 1 Year | -5.95 | % | |

5 Year | 1.49 |

|

| 5 Year | N/A |

|

Since Inception | 7.15 |

|

| Since Inception | -2.38 |

|

‡Inception date April 06, 2009 |

| |||||

†Inception date September 25, 2017 |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

12

| JNL/American Funds Funds of Funds Jackson National Asset Management, LLC (Unaudited) |

Each Fund seeks to achieve its objective by investing in shares of a diversified group of other Underlying Funds (“Underlying Funds”). The Underlying Funds in which each Fund may invest are a separate series of American Funds Insurance Series® or the American Funds R6 mutual fund share class. The Schedules of Investments and Financial Statements for the Underlying Funds are available on the SEC’s website at www.sec.gov.

JNL/American Funds Moderate Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Fixed Income | 37.1 | % |

Domestic Equity | 29.9 | |

Global Equity | 19.1 | |

International Equity | 5.1 | |

International Fixed Income | 4.8 | |

Emerging Markets Equity | 4.0 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Moderate Growth Allocation Fund outperformed its primary benchmark by posting a return of -4.57% for Class A shares compared to -5.21% for the Dow Jones Moderate Index. The Fund outperformed its blended benchmark return of -5.52% for the 60% MSCI All Country World Index (Net) and 40% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek a balance between current income and growth of capital.

Under normal circumstances, the Fund allocates approximately 40% to 80% of its assets to Underlying Funds that invest primarily in equity securities and 20% to 60% of its assets to Underlying Funds that invest primarily fixed-income securities. The equity and fixed-income allocation may fall outside of the above limits in a volatile market environment where investment outcomes are expected to remain beyond normal range.

The Fund outperformed its blended benchmark in 2018 thanks to significant outperformance from the equity sleeve. Equity returns were driven by their growth bias, both in the U.S. and internationally, as more than a third of the Fund’s equity exposure came from American Funds Insurance Series Growth Fund (-0.01%) and American Funds Insurance Series Growth - Income Fund (-1.55%) which both bested global equities by a wide margin. Strategy outperformance helped offset some of the weakness from international equity exposure as American Funds Insurance Series International Fund (-12.94%) was the worst absolute performer but did outperform MSCI ACWI Ex-US Index.

The fixed income sleeve performed slightly behind the benchmark, mainly due to an allocation to emerging markets bonds through the American Funds Emerging Markets Bond Fund (-5.88%). A core position in American Funds Bond Fund of America (0.22%) helped offset the emerging markets weakness. A new position in American Funds Intermediate Bond Fund of America (1.96%) was a positive addition as well.

JNL/American Funds Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 38.3 | % |

Global Equity | 29.0 | |

Domestic Fixed Income | 18.2 | |

Emerging Markets Equity | 6.1 | |

International Equity | 6.0 | |

International Fixed Income | 2.4 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/American Funds Growth Allocation Fund outperformed its primary benchmark by posting a return of -5.39% for Class A shares compared to -7.33% for the Dow Jones Moderately Aggressive Index. The Fund outperformed its blended benchmark return of -7.45% for the 80% MSCI All Country World Index (Net) and 20% Bloomberg Barclays Capital U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek capital growth with secondary emphasis on current income.

Under normal circumstances, the Fund allocates approximately 60% to 100% of its assets to Underlying Funds that invest primarily in equity securities and 0% to 40% of its assets to Underlying Funds that invest primarily fixed-income securities, and 0% to 20% of its assets to Underlying Funds that invest primarily in money market securities. The equity and fixed-income allocation may fall outside of the above limits in a volatile market environment where investment outcomes are expected to remain beyond normal range.

The Fund outperformed its blended benchmark in 2018 thanks to significant outperformance from the equity sleeve. Equity returns were driven by its growth bias, both in the U.S. and internationally, as more than a third of the Fund’s equity exposure came from American Funds Insurance Series Growth Fund (-0.01%) and American Funds Insurance Series Growth – Income Fund (-1.55%) which both bested global equities by a wide margin. Strategy outperformance helped offset some of the weakness from international equity exposure as American Funds Insurance Series International Fund (-12.94%) was the worst absolute performer but did outperform MSCI ACWI Ex-US benchmark.

The fixed income sleeve slightly outperformed its benchmark as a new position in American Funds Intermediate Bond Fund of America (1.96%) helped to offset weakness in emerging market debt that weighed on returns through the addition of American Funds Emerging Markets Bond Fund (-5.88%). A core position in American Funds Bond Fund of America (0.22%) outperformed the broader bond market to aid relative returns as well.

13

| JNL/American Funds Funds of Funds Jackson National Asset Management, LLC (Unaudited) |

JNL/American Funds Moderate Growth Allocation Fund

†60% MSCI All Country World Index (Net), 40% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -4.57 | % | 1 Year | -4.29 | % | |

5 Year | 4.29 |

|

| 5 Year | N/A |

|

Since Inception | 6.07 |

|

| Since Inception | -0.77 |

|

‡Inception date April 30, 2012 |

| |||||

†Inception date September 25, 2017 |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

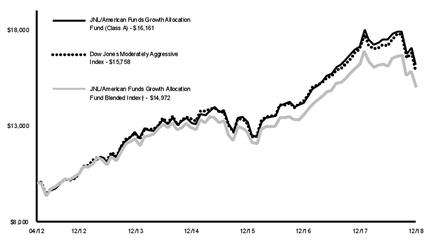

JNL/American Funds Growth Allocation Fund

†80% MSCI All Country World Index (Net), 20% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -5.39 | % | 1 Year | -5.08 | % | |

5 Year | 5.07 |

|

| 5 Year | N/A |

|

Since Inception | 7.46 |

|

| Since Inception | -0.56 |

|

‡Inception date April 30, 2012 |

| |||||

†Inception date September 25, 2017 |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

14

| JNL/DFA Funds Jackson National Asset Management, LLC (Unaudited) |

Each Fund seeks to achieve its objective by investing in shares of a diversified group of other Underlying Funds (“Underlying Funds”). The Underlying Funds in which each Fund may invest are a separate series of Dimensional Fund Advisors (“DFA”) Investment Dimensions Group Inc. and Dimensional Investment Group Inc. (collectively, “DFA Fund Groups”). The Schedules of Investments and Financial Statements for the Underlying Funds are available on the SEC’s website at www.sec.gov.

JNL/DFA Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 42.5 | % |

International Equity | 27.7 | |

Domestic Fixed Income | 17.8 | |

Emerging Markets Equity | 8.0 | |

Alternative | 4.0 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/DFA Growth Allocation Fund underperformed its primary benchmark by posting a return of -10.65% for Class A shares compared to -7.33% for the Dow Jones Moderately Aggressive Index. The Fund underperformed its blended benchmark of -7.45% for the 80% MSCI All Country World Index (Net), 20% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek total return consisting of capital appreciation and current income.

To achieve its investment objective, the Fund under normal market circumstances, allocates its assets to Underlying Funds that invest in equity and fixed income securities. Generally, the Fund invests its assets in domestic and international equity Underlying Funds and fixed income Underlying Funds to achieve an allocation of approximately 60% to 100% (with a target allocation of approximately 80%) of the Fund’s assets to domestic and international equity Underlying Funds and 0% to 40% (with a target allocation of approximately 20%) of its assets to fixed-income Underlying Funds. The equity and fixed-income allocation may fall outside of the above limits in a volatile market environment where investment outcomes are expected to remain beyond normal range.

The Fund underperformed its blended benchmark owing to its bias towards smaller companies and value within the equity sleeve, plus an underweight allocation to the fixed income. Within international equities, DFA International Small Cap Value Portfolio (-23.31%) and a large position in DFA International Core Equity Portfolio (-17.40%) were the top detractors, while a value bias served as a minor tailwind in emerging markets leading to the relative outperformance of DFA Emerging Markets Portfolio (-13.62%). In the U.S., a core position in DFA U.S. Large Company Portfolio (-4.43%) provided ballast but was offset by weakness from DFA U.S. Targeted Value Portfolio (-15.78%), DFA U.S. Large Cap Value Portfolio (-11.65%), and DFA U.S. Small Cap Fund (-13.37%).

A fixed income bias toward short term and higher quality bonds helped offset weakness elsewhere as the sleeve slightly outperformed the broader bond market. DFA Short-Term Extended Quality Portfolio (1.34%) and DFA Short-Duration Real Return Portfolio (0.11%) were the sleeve’s top performers.

JNL/DFA Moderate Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Fixed Income | 38.5 | % |

Domestic Equity | 33.0 | |

International Equity | 19.5 | |

Emerging Markets Equity | 6.1 | |

Alternative | 2.9 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL/DFA Moderate Growth Allocation Fund underperformed its primary benchmark by posting a return of -7.93% for Class A shares compared to -5.21% for the Dow Jones Moderate Index. The Fund underperformed its blended benchmark return of -5.52% for the 60% MSCI All Country World Index (Net), 40% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek total return consisting of capital appreciation and current income.

To achieve its investment objective, the Fund under normal market circumstances, allocates its assets to Underlying Funds that invest in equity and fixed-income securities. Generally, the Fund invests its assets in domestic and international equity Underlying Funds and fixed income Underlying Funds to achieve an allocation of approximately 40% to 80% (with a target allocation of approximately 60%) of the Fund’s assets to domestic and international equity Underlying Funds and 20% to 60% (with a target allocation of approximately 40%) of its assets to fixed income Underlying Funds. The equity and fixed income allocation may fall outside of the above limits in a volatile market environment where investment outcomes are expected to remain beyond normal range.

The Fund underperformed its blended benchmark owing to its bias towards smaller companies and value within the equity sleeve, plus a slight underweight allocation to the fixed income. Within international equities, DFA International Small Cap Value Portfolio (-23.31%) and a large position in DFA International Core Equity Portfolio (-17.40%) were the top detractors, while a value bias served as a minor tailwind in emerging markets leading to the relative outperformance of DFA Emerging Markets Portfolio (-13.62%). In the U.S., a core position in DFA U.S. Large Company Portfolio (-4.43%) provided ballast but was offset by weakness from DFA U.S. Targeted Value Portfolio (-15.78%), DFA U.S. Large Cap Value Portfolio (-11.65%) and DFA U.S. Small Cap Fund (-13.37%).

A fixed income bias toward short term and higher quality bonds helped offset weakness elsewhere as the sleeve finished the year even with the broader market. DFA Short-Term Extended Quality Portfolio (1.34%) and DFA Short-Duration Real Return Portfolio (0.11%) were the sleeve’s top performers.

15

| JNL/DFA Funds Jackson National Asset Management, LLC (Unaudited) |

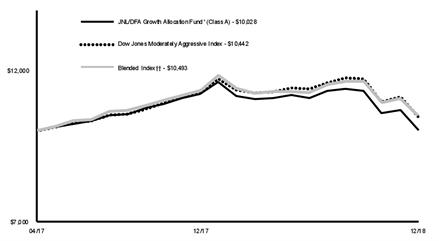

JNL/DFA Growth Allocation Fund

††80% MSCI All Country World Index (Net), 20% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -10.65 | % | 1 Year | -10.37 | % | |

Since Inception | 0.17 |

|

| Since Inception | -4.63 |

|

‡Inception date April 24, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

JNL/DFA Moderate Growth Allocation Fund

††60% MSCI All Country World Index (Net), 40% Bloomberg Barclays U.S. Aggregate Bond Index

Average Annual Total Returns* |

| |||||

Class A‡ |

|

|

| Class I† |

|

|

1 Year | -7.93 | % | 1 Year | -7.55 | % | |

Since Inception | 0.64 |

|

| Since Inception | -3.02 |

|

‡Inception date April 24, 2017 |

| |||||

†Inception date September 25, 2017 |

| |||||

*The Fund's investment adviser waived/reimbursed certain expenses of the Fund. Performance results shown reflect the waiver, without which performance results would have been lower. |

| |||||

The graph shows the change in value of an assumed $10,000 investment in the Fund's Class A shares over 10 years, or since inception if the inception is less than 10 years, as well as the Fund's benchmark(s) performance for the same period.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but do not reflect the deduction of insurance charges.

16

| JNL Allocation Funds Jackson National Asset Management, LLC (Unaudited) |

Each Fund seeks to achieve its investment objective by investing in shares of a diversified group of affiliated Underlying Funds (“Underlying Funds”). The Schedules of Investments and Financial Statements for the Underlying Funds are available at www.jackson.com or on the SEC’s website at www.sec.gov.

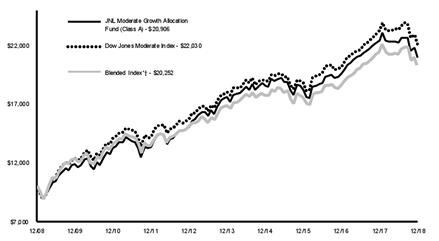

JNL Moderate Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Fixed Income | 26.7 | % |

Domestic Equity | 23.0 | |

International Equity | 15.6 | |

Domestic Balanced | 11.3 | |

Emerging Markets Equity | 6.6 | |

Alternative | 5.5 | |

Global Equity | 4.7 | |

International Fixed Income | 3.3 | |

Global Fixed Income | 3.3 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL Moderate Growth Allocation Fund underperformed its primary benchmark by posting a return of -6.64% for Class A shares compared to -5.21% for the Dow Jones Moderate Index. The Fund underperformed its blended benchmark of -5.52% for the 60% MSCI All Country World Index (Net), 40% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek capital growth and current income.

Under normal circumstances, the Fund allocates approximately 40% to 80% of its assets to Underlying Funds that invest primarily in equity securities, 20% to 60% to Underlying Funds that invest primarily in fixed-income securities and 0% to 20% of its assets to Underlying Funds that invest primarily in money market securities.

The Fund underperformed its blended benchmark mainly due to an underweight allocation to fixed income and underlying manager selection in the international equity sleeve. JNL/Harris Oakmark Global Equity Fund (-20.97%), and JNL/Causeway International Value Select Fund (-17.26%), two value oriented managers, detracted the most from relative results. Despite better relative performance in the fourth quarter, emerging market equity Funds also detracted for the year. JNL/Oppenheimer Emerging Markets Innovator Fund (-22.25%), JNL/Lazard Emerging Markets Fund (-18.13%), and JNL/GQG Emerging Markets Equity Fund (-14.64) all underperformed in 2018. Manager selection helped to offset some of the relative weakness from the underweight to fixed income as JNL/DoubleLine Total Return Fund (2.11%) and JNL/Franklin Templeton Global Multisector Bond Fund (0.93%) added positively to results.

In the U.S., underperformance from small cap and value oriented strategies was offset by positive relative results from growth strategies, particularly JNL/T. Rowe Price Established Growth Fund (-1.13%) and a sizeable allocation to JNL/T. Rowe Price Capital Appreciation Fund (0.67%).

The alternatives sleeve detracted relative to fixed income due to underlying strategy and manager selection, with the JNL/Neuberger Berman Risk Balanced Commodity Strategy Fund (-10.22%) and JNL/Boston Partners Global Long Short Equity Fund (-9.22%) weighing on returns.

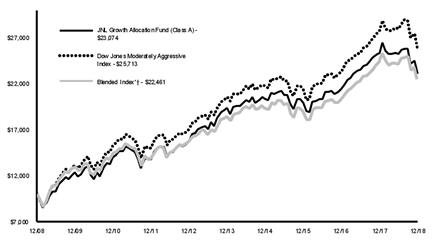

JNL Growth Allocation Fund

Composition as of December 31, 2018: | ||

Domestic Equity | 34.8 | % |

International Equity | 22.0 | |

Domestic Fixed Income | 13.4 | |

Emerging Markets Equity | 9.0 | |

Global Equity | 7.9 | |

Alternative | 5.2 | |

Domestic Balanced | 4.1 | |

International Fixed Income | 2.1 | |

Global Fixed Income | 1.5 | |

Total Investments | 100.0 | % |

For the year ended December 31, 2018, JNL Growth Allocation Fund underperformed its primary benchmark by posting a return of -9.07% for Class A shares compared to -7.33% for the Dow Jones Moderately Aggressive Index. The Fund underperformed its blended benchmark return of -7.45% for the 80% MSCI All Country World Index (Net), 20% Bloomberg Barclays U.S. Aggregate Bond Index.

The investment objective of the Fund is to seek capital growth and current income.

Under normal circumstances, the Fund allocates approximately 60% to 100% of its assets to Underlying Funds that invest primarily in equity securities, 0% to 40% to Underlying Funds that invest primarily in fixed income securities and 0% to 20% of its assets to Underlying Funds that invest primarily in money market securities.