Exhibit 99.2

| March 31, 2008 Quarterly Results May 8, 2008 |

| 2 This presentation contains forward-looking statements based on current expectations that involve a number of risks and uncertainties. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. A discussion of these forward-looking statements and risk factors is set forth at the end of this presentation. The Company assumes no obligation to update any forward-looking statement in this presentation. Private Securities Litigation Reform Act of 1995 Safe Harbor For Forward-Looking Statements |

| 3 • Richard Launder, President, Global Operations • Mark Vipond, President, Global Product • Scott Behrens, Principal Financial Officer • Q&A: Phil Heasley, Richard Launder, Scott Behrens and Mark Vipond Agenda |

| 4 Richard Launder, President, Global Operations Business Operations Review |

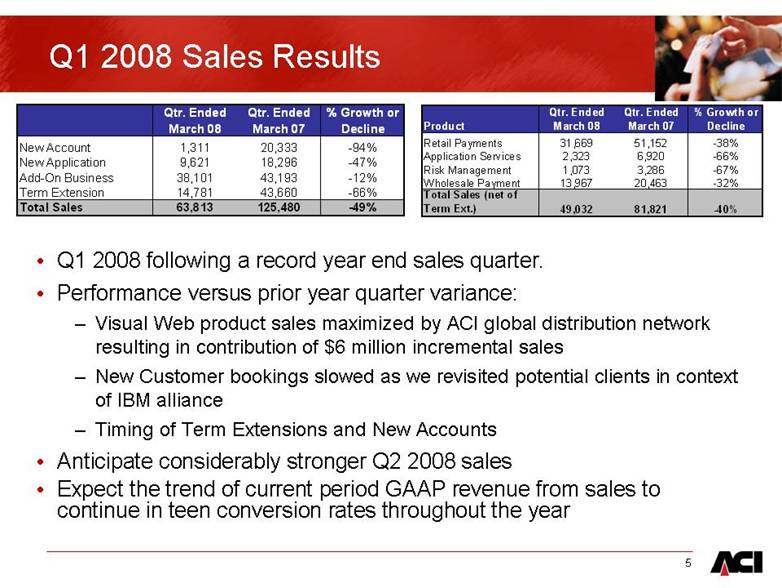

| 5 Q1 2008 Sales Results Qtr. Ended March 08 Qtr. Ended March 07 % Growth or Decline New Account 1,311 20,333 -94% New Application 9,621 18,296 -47% Add-On Business 38,101 43,193 -12% Term Extension 14,781 43,660 -66% Total Sales 63,813 125,480 -49% • Q1 2008 following a record year end sales quarter. • Performance versus prior year quarter variance: – Visual Web product sales maximized by ACI global distribution network resulting in contribution of $6 million incremental sales – New Customer bookings slowed as we revisited potential clients in context of IBM alliance – Timing of Term Extensions and New Accounts • Anticipate considerably stronger Q2 2008 sales • Expect the trend of current period GAAP revenue from sales to continue in teen conversion rates throughout the year Product Qtr. Ended March 08 Qtr. Ended March 07 % Growth or Decline Retail Payments 31,669 51,152 -38% Application Services 2,323 6,920 -66% Risk Management 1,073 3,286 -67% Wholesale Payment 13,967 20,463 -32% Total Sales (net of Term Ext.) 49,032 81,821 -40% |

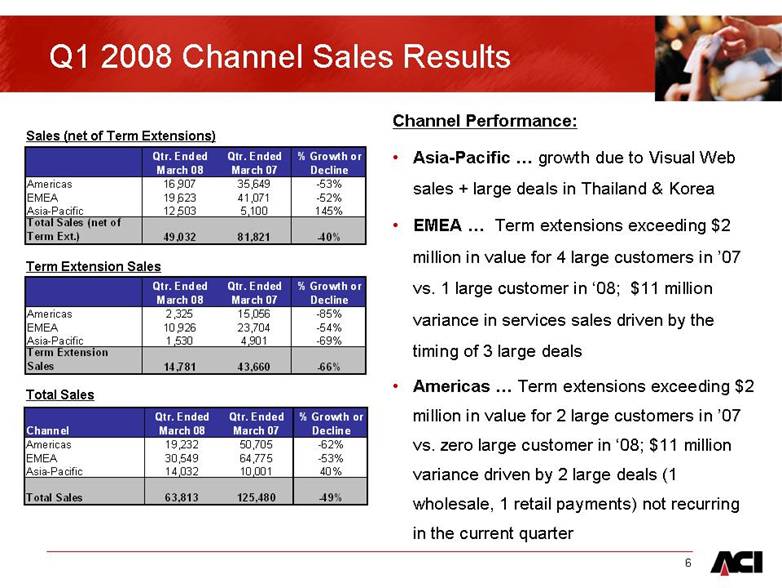

| 6 Q1 2008 Channel Sales Results Qtr. Ended March 08 Qtr. Ended March 07 % Growth or Decline Americas 16,907 35,649 -53% EMEA 19,623 41,071 -52% Asia-Pacific 12,503 5,100 145% Total Sales (net of Term Ext.) 49,032 81,821 -40% Channel Performance: • Asia-Pacific ... growth due to Visual Web sales + large deals in Thailand & Korea • EMEA ... Term extensions exceeding $2 million in value for 4 large customers in ’07 vs. 1 large customer in ‘08; $11 million variance in services sales driven by the timing of 3 large deals • Americas ... Term extensions exceeding $2 million in value for 2 large customers in ’07 vs. zero large customer in ‘08; $11 million variance driven by 2 large deals (1 wholesale, 1 retail payments) not recurring in the current quarter Qtr. Ended March 08 Qtr. Ended March 07 % Growth or Decline Americas 2,325 15,056 -85% EMEA 10,926 23,704 -54% Asia-Pacific 1,530 4,901 -69% Term Extension Sales 14,781 43,660 -66% Channel Qtr. Ended March 08 Qtr. Ended March 07 % Growth or Decline Americas 19,232 50,705 -62% EMEA 30,549 64,775 -53% Asia-Pacific 14,032 10,001 40% Total Sales 63,813 125,480 -49% Sales (net of Term Extensions) Term Extension Sales Total Sales |

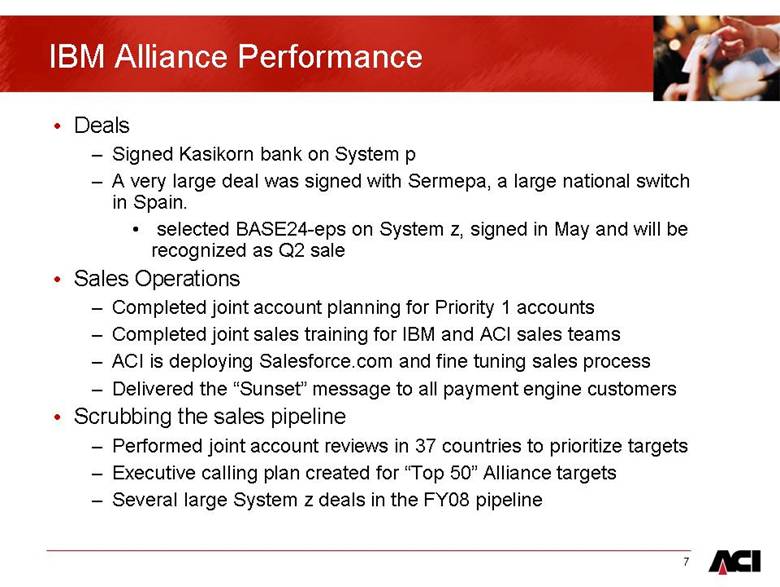

| 7 IBM Alliance Performance • Deals – Signed Kasikorn bank on System p – A very large deal was signed with Sermepa, a large national switch in Spain. • selected BASE24-eps on System z, signed in May and will be recognized as Q2 sale • Sales Operations – Completed joint account planning for Priority 1 accounts – Completed joint sales training for IBM and ACI sales teams – ACI is deploying Salesforce.com and fine tuning sales process – Delivered the “Sunset” message to all payment engine customers • Scrubbing the sales pipeline – Performed joint account reviews in 37 countries to prioritize targets – Executive calling plan created for “Top 50” Alliance targets – Several large System z deals in the FY08 pipeline |

| 8 Mark Vipond, President, Global Product Business Operations Review |

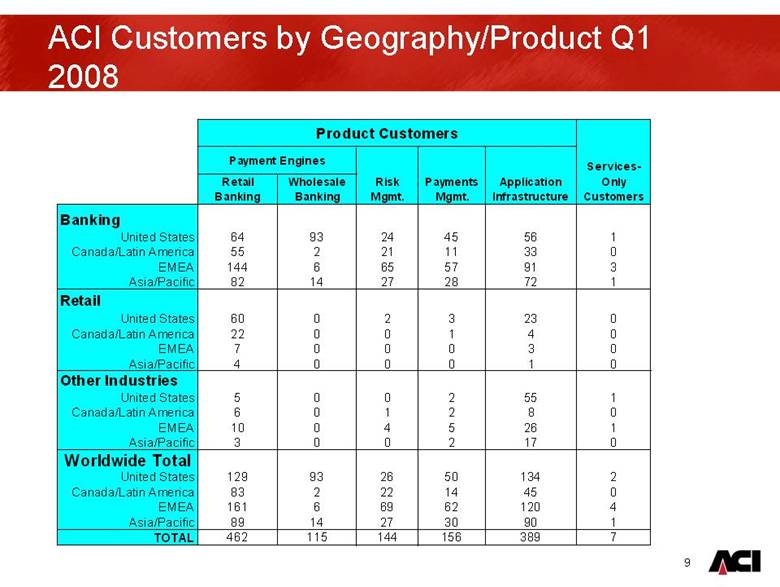

| 9 ACI Customers by Geography/Product Q1 2008 Product Customers Payment Engines Retail Banking Wholesale Banking Banking United States 64 93 24 45 56 1 Canada/Latin America 55 2 21 11 33 0 EMEA 144 6 65 57 91 3 Asia/Pacific 82 14 27 28 72 1 Retail United States 60 0 2 3 23 0 Canada/Latin America 22 0 0 1 4 0 EMEA 7 0 0 0 3 0 Asia/Pacific 4 0 0 0 1 0 Other Industries United States 5 0 0 2 55 1 Canada/Latin America 6 0 1 2 8 0 EMEA 10 0 4 5 26 1 Asia/Pacific 3 0 0 2 17 0 Worldwide Total United States 129 93 26 50 134 2 Canada/Latin America 83 2 22 14 45 0 EMEA 161 6 69 62 120 4 Asia/Pacific 89 14 27 30 90 1 TOTAL 462 115 144 156 389 7 Risk Mgmt. Payments Mgmt. Application Infrastructure Services- Only Customers |

| 10 ACI Customers by Region, Industry and Solution Set – March 31, 2008 • ACI customers use an average of 2.7 products. • 12 new customers added in March quarter. • 2 new countries added in the quarter – Romania (from a client perspective) and Kyrgyzstan. • Customers in 88 countries. • Total of 808 ACI customers. • Total of 2,189 products deployed. |

| 11 Solution Updates - Q1 2008 • Retail Payment Solutions – Maturity announcements of legacy Retail Payment Products on March 24, 2008. – BASE24-eps customer migration planning has begun. – System z enablement progress. • Wholesale Payment Solutions – Improving sales/market opportunities – in all regions. – “Hub” investments compliment existing payments function. – ACI On-demand leverage of IBM data center operations. • Risk Management Solutions – Enterprise Risk potential and investment. – New version of Automated Case Management solution. – Real-time rules and scoring of transactions. |

| 12 Focus Areas – Next 12 Months • IBM optimization, enablement and market success. • Continued progress with services revenue and margins. • Migration planning for Retail Payment customers. • Wholesale Payment Solution strategies and investment. • Customer satisfaction. • Enhancing the ACI brand. |

| Financials Review Scott Behrens, Principal Financial Officer |

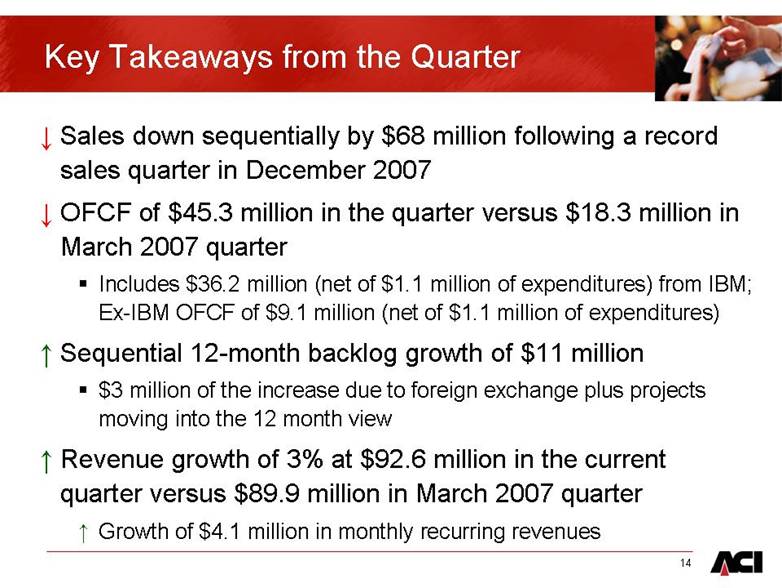

| 14 Key Takeaways from the Quarter . Sales down sequentially by $68 million following a record sales quarter in December 2007 . OFCF of $45.3 million in the quarter versus $18.3 million in March 2007 quarter Includes $36.2 million (net of $1.1 million of expenditures) from IBM; Ex-IBM OFCF of $9.1 million (net of $1.1 million of expenditures) . Sequential 12-month backlog growth of $11 million $3 million of the increase due to foreign exchange plus projects moving into the 12 month view . Revenue growth of 3% at $92.6 million in the current quarter versus $89.9 million in March 2007 quarter . Growth of $4.1 million in monthly recurring revenues |

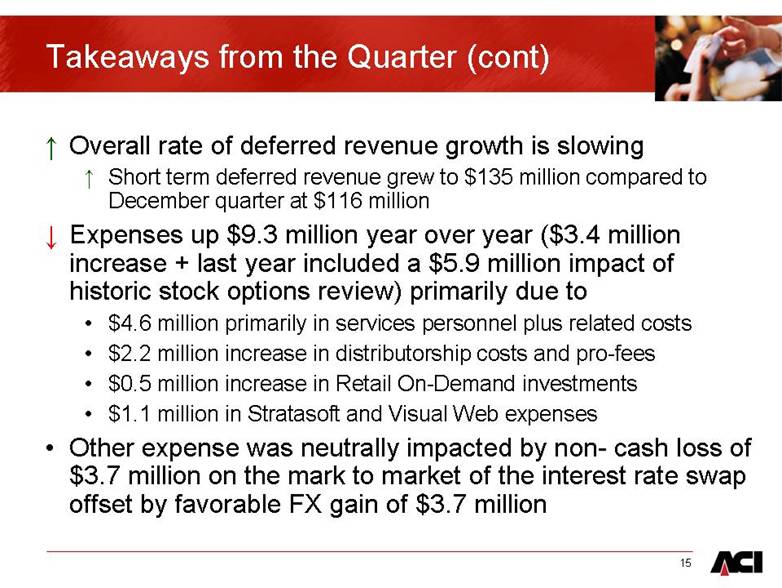

| 15 Takeaways from the Quarter (cont) . Overall rate of deferred revenue growth is slowing . Short term deferred revenue grew to $135 million compared to December quarter at $116 million . Expenses up $9.3 million year over year ($3.4 million increase + last year included a $5.9 million impact of historic stock options review) primarily due to • $4.6 million primarily in services personnel plus related costs • $2.2 million increase in distributorship costs and pro-fees • $0.5 million increase in Retail On-Demand investments • $1.1 million in Stratasoft and Visual Web expenses • Other expense was neutrally impacted by non- cash loss of $3.7 million on the mark to market of the interest rate swap offset by favorable FX gain of $3.7 million |

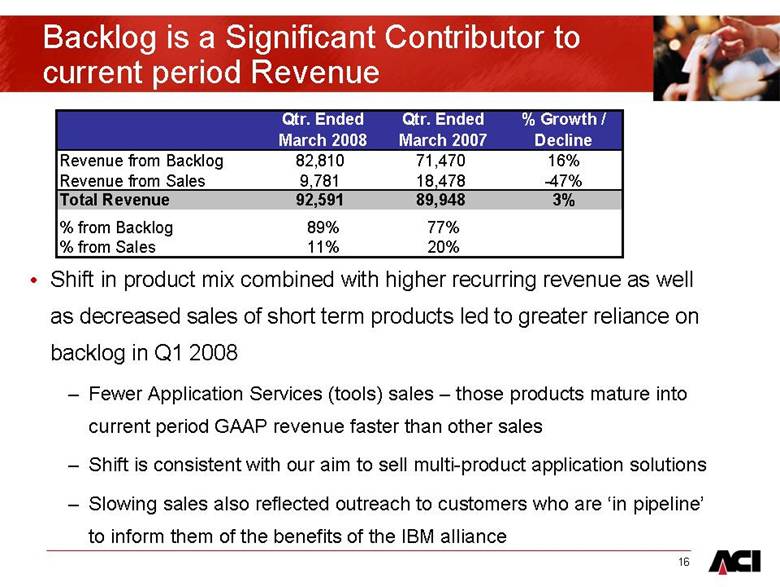

| 16 Backlog is a Significant Contributor to current period Revenue • Shift in product mix combined with higher recurring revenue as well as decreased sales of short term products led to greater reliance on backlog in Q1 2008 – Fewer Application Services (tools) sales – those products mature into current period GAAP revenue faster than other sales – Shift is consistent with our aim to sell multi-product application solutions – Slowing sales also reflected outreach to customers who are ‘in pipeline’ to inform them of the benefits of the IBM alliance Qtr. Ended March 2008 Qtr. Ended March 2007 % Growth / Decline Revenue from Backlog 82,810 71,470 16% Revenue from Sales 9,781 18,478 -47% Total Revenue 92,591 89,948 3% % from Backlog 89% 77% % from Sales 11% 20% |

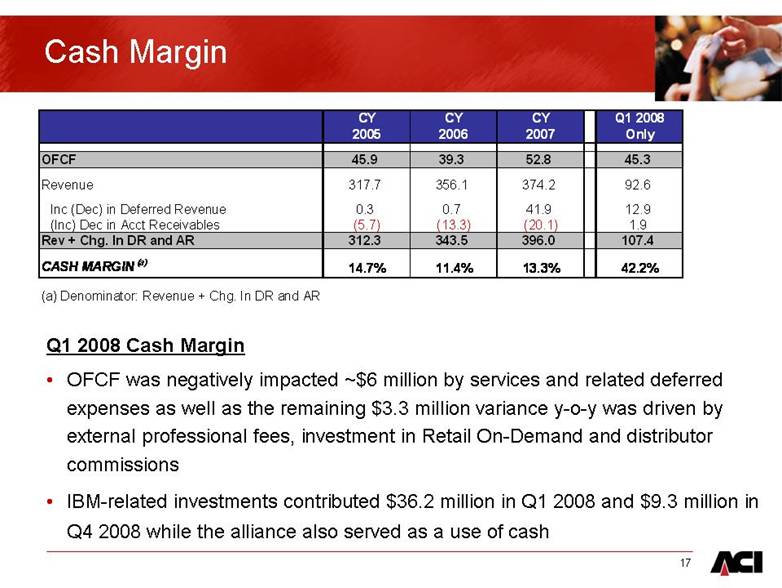

| 17 Cash Margin Q1 2008 Cash Margin • OFCF was negatively impacted ~$6 million by services and related deferred expenses as well as the remaining $3.3 million variance y-o-y was driven by external professional fees, investment in Retail On-Demand and distributor commissions • IBM-related investments contributed $36.2 million in Q1 2008 and $9.3 million in Q4 2008 while the alliance also served as a use of cash CY CY CY Q1 2008 2005 2006 2007 Only OFCF 45.9 39.3 52.8 45.3 Revenue 317.7 356.1 374.2 92.6 Inc (Dec) in Deferred Revenue 0.3 0.7 41.9 12.9 (Inc) Dec in Acct Receivables (5.7) (13.3) (20.1) 1.9 Rev + Chg. In DR and AR 312.3 343.5 396.0 107.4 CASH MARGIN(a) 14.7% 11.4% 13.3% 42.2% (a) Denominator: Revenue + Chg. In DR and AR |

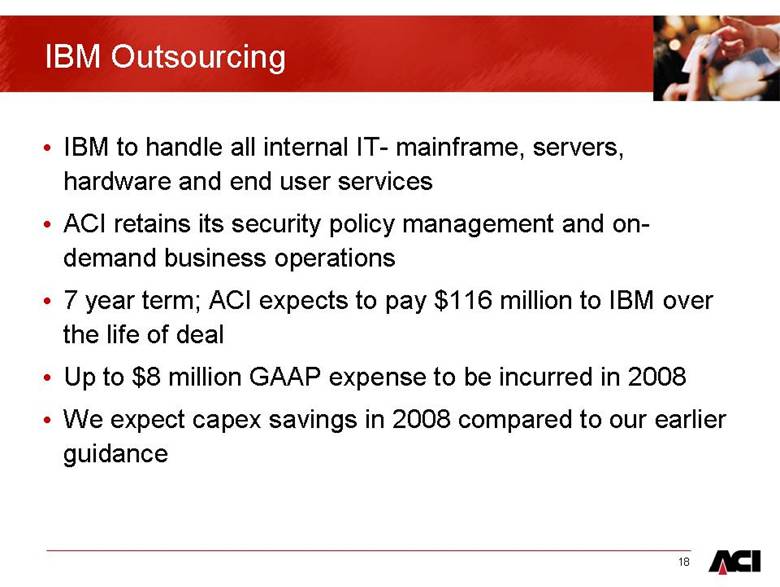

| 18 IBM Outsourcing • IBM to handle all internal IT- mainframe, servers, hardware and end user services • ACI retains its security policy management and ondemand business operations • 7 year term; ACI expects to pay $116 million to IBM over the life of deal • Up to $8 million GAAP expense to be incurred in 2008 • We expect capex savings in 2008 compared to our earlier guidance |

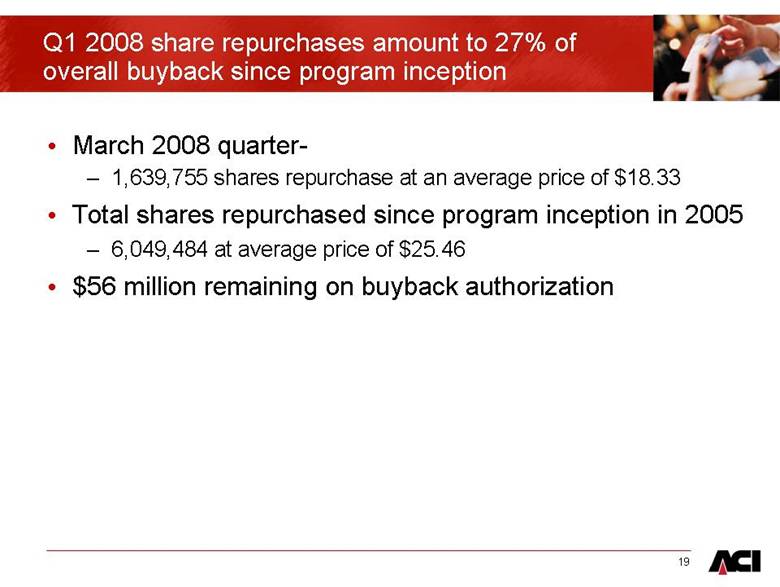

| 19 • March 2008 quarter- – 1,639,755 shares repurchase at an average price of $18.33 • Total shares repurchased since program inception in 2005 – 6,049,484 at average price of $25.46 • $56 million remaining on buyback authorization Q1 2008 share repurchases amount to 27% of overall buyback since program inception |

| Appendix |

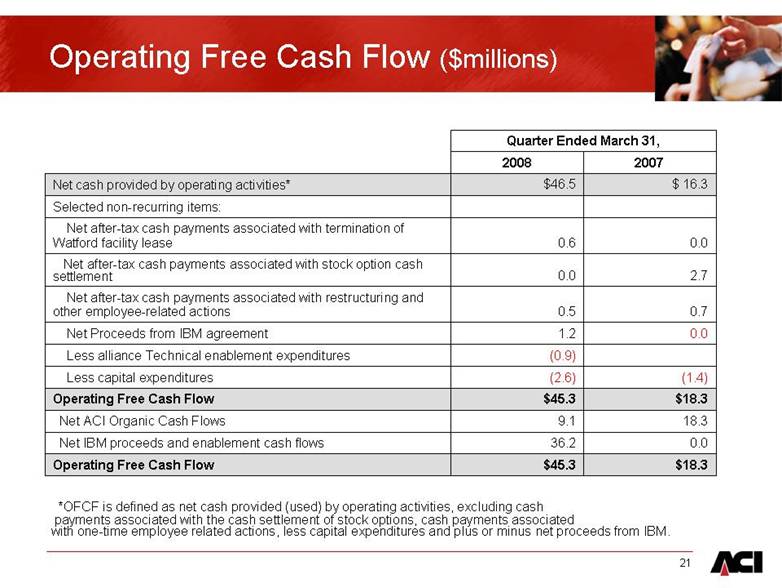

| 21 Operating Free Cash Flow ($millions) 18.3 9.1 Net ACI Organic Cash Flows $18.3 $45.3 Operating Free Cash Flow 0.0 36.2 Net IBM proceeds and enablement cash flows (0.9) Less alliance Technical enablement expenditures 2.7 0.0 Net after-tax cash payments associated with stock option cash settlement 0.0 1.2 Net Proceeds from IBM agreement 0.7 0.5 Net after-tax cash payments associated with restructuring and other employee-related actions $18.3 $45.3 Operating Free Cash Flow (1.4) (2.6) Less capital expenditures 0.0 0.6 Net after-tax cash payments associated with termination of Watford facility lease Selected non-recurring items: $ 16.3 $46.5 Net cash provided by operating activities* 2007 2008 Quarter Ended March 31, *OFCF is defined as net cash provided (used) by operating activities, excluding cash payments associated with the cash settlement of stock options, cash payments associated with one-time employee related actions, less capital expenditures and plus or minus net proceeds from IBM. |

| 22 60-Month Backlog ($ millions) $1,277 $1,380 $1,397 Backlog 60-Month 1,155 1,237 1,241 ACI Other 122 143 156 ACI Deferred Revenue $1,277 $1,380 $1,397 Backlog 60-Month 128 143 151 Asia/Pacific 457 504 522 EMEA $692 $733 $724 Americas 2007 2007 2008 March 31, December 31, March 31, Quarter Ended |

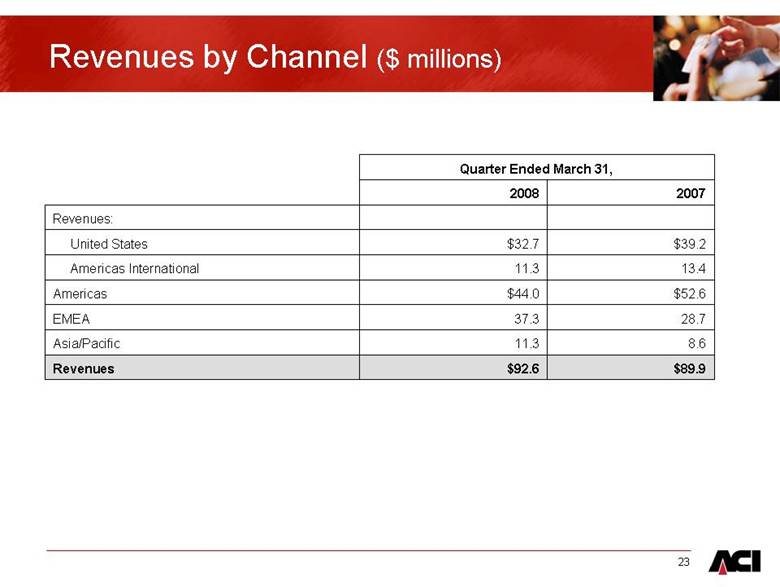

| 23 Revenues by Channel ($ millions) $89.9 $92.6 Revenues 8.6 11.3 Asia/Pacific 28.7 37.3 EMEA $52.6 $44.0 Americas 13.4 11.3 Americas International $39.2 $32.7 United States Revenues: 2007 2008 Quarter Ended March 31, |

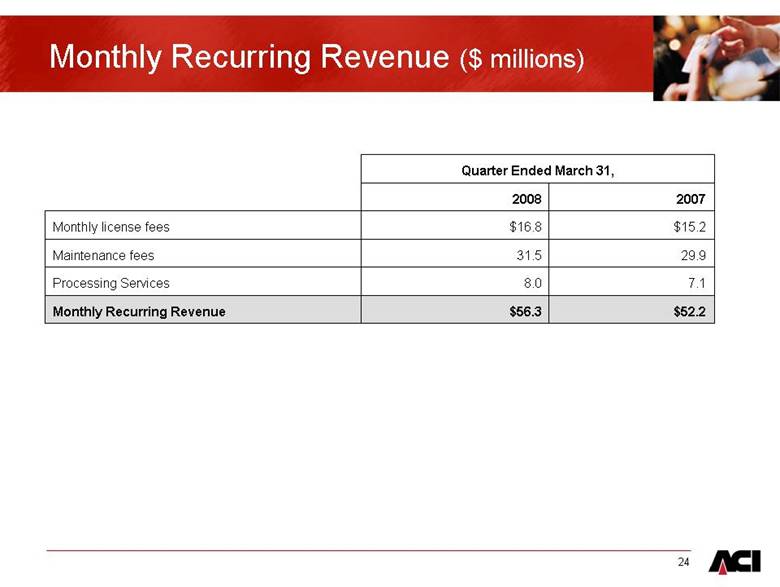

| 24 Monthly Recurring Revenue ($ millions) $52.2 $56.3 Monthly Recurring Revenue 7.1 8.0 Processing Services 29.9 31.5 Maintenance fees $15.2 $16.8 Monthly license fees 2007 2008 Quarter Ended March 31, |

|

|

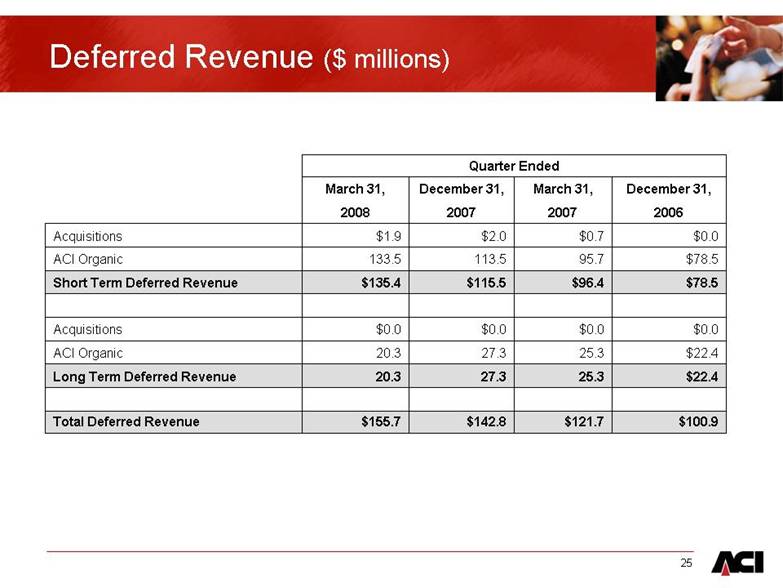

| 25 Deferred Revenue ($ millions) Quarter Ended March 31, December 31, March 31, December 31, 2008 2007 2007 2006 Acquisitions $1.9 $2.0 $0.7 $0.0 ACI Organic 133.5 113.5 95.7 $78.5 Short Term Deferred Revenue $135.4 $115.5 $96.4 $78.5 Acquisitions $0.0 $0.0 $0.0 $0.0 ACI Organic 20.3 27.3 25.3 $22.4 Long Term Deferred Revenue 20.3 27.3 25.3 $22.4 Total Deferred Revenue $155.7 $142.8 $121.7 $100.9 |

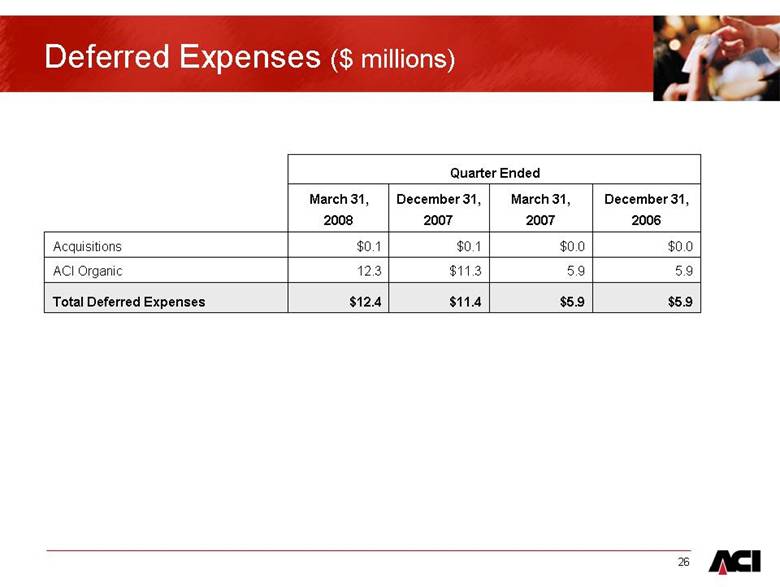

| 26 Deferred Expenses ($ millions) $5.9 $5.9 $11.4 $12.4 Total Deferred Expenses 5.9 5.9 $11.3 12.3 ACI Organic $0.0 $0.0 $0.1 $0.1 Acquisitions 2006 2007 2007 2008 December 31, March 31, December 31, March 31, Quarter Ended |

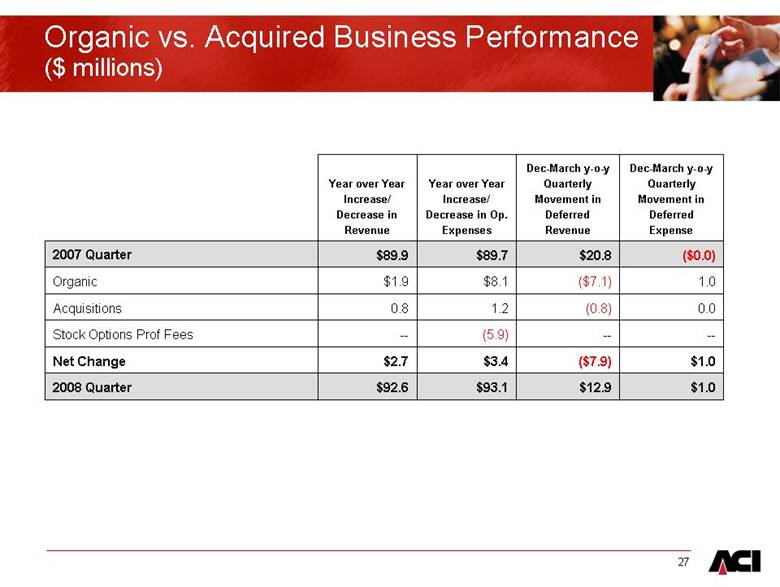

| 27 Organic vs. Acquired Business Performance ($ millions) -- -- (5.9) -- Stock Options Prof Fees $1.0 $12.9 $93.1 $92.6 2008 Quarter $1.0 ($7.9) $3.4 $2.7 Net Change 0.0 (0.8) 1.2 0.8 Acquisitions 1.0 ($7.1) $8.1 $1.9 Organic ($0.0) $20.8 $89.7 $89.9 2007 Quarter Dec-March y-o-y Quarterly Movement in Deferred Expense Dec-March y-o-y Quarterly Movement in Deferred Revenue Year over Year Increase/Decrease in Op. Expenses Year over Year Increase/Decrease in Revenue |

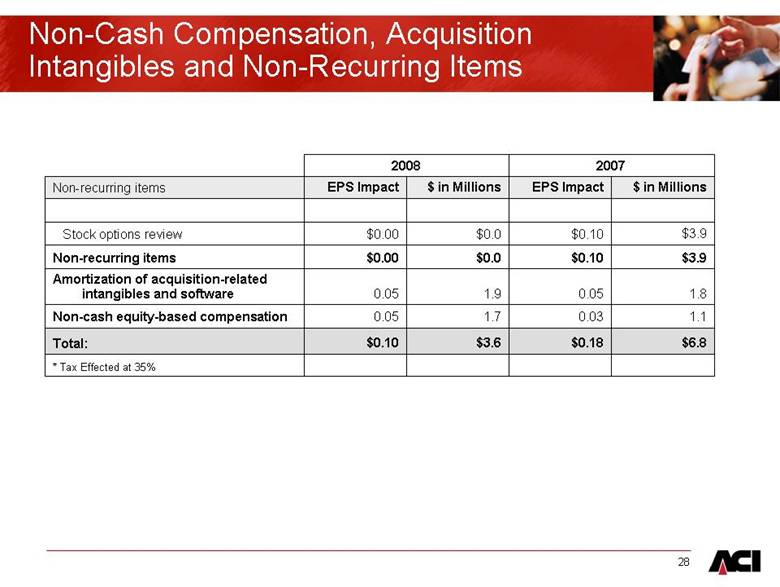

| 28 Non-Cash Compensation, Acquisition Intangibles and Non-Recurring Items * Tax Effected at 35% $6.8 $0.18 $3.6 $0.10 Total: 1.1 0.03 1.7 0.05 Non-cash equity-based compensation 1.8 0.05 1.9 0.05 Amortization of acquisition-related intangibles and software $3.9 $0.10 $0.0 $0.00 Non-recurring items $3.9 $0.10 $0.0 $0.00 Stock options review $ in Millions EPS Impact $ in Millions EPS Impact Non-recurring items 2007 2008 |

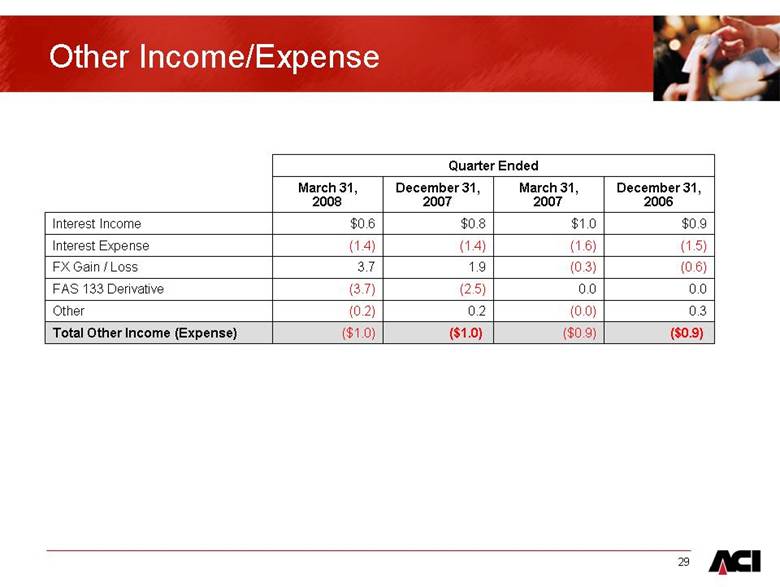

| 29 Other Income/Expense ($0.9) ($0.9) ($1.0) ($1.0) Total Other Income (Expense) 0.3 (0.0) 0.2 (0.2) Other 0.0 0.0 (2.5) (3.7) FAS 133 Derivative (0.6) (0.3) 1.9 3.7 FX Gain / Loss (1.5) (1.6) (1.4) (1.4) Interest Expense $0.9 $1.0 $0.8 $0.6 Interest Income December 31, 2006 March 31, 2007 December 31, 2007 March 31, 2008 Quarter Ended |

| 30 Non-GAAP Financial Measures • This presentation includes operating free cash flow and backlog estimates. ACI is presenting these non-GAAP guidance measures to provide more transparency to its earnings, focusing on operating free cash flow and backlog • ACI is presenting operating free cash flow, which is defined as net cash provided (used) by operating activities, excluding cash payments associated with the cash settlement of stock options, cash payments associated with one-time employee related actions, less capital expenditures, plus net proceeds from IBM. We utilize this non-GAAP financial measure, and believe it is useful to investors, as an indicator of cash flow available for debt repayment and other investing activities, such as capital investments and acquisitions. We utilize operating free cash flow as a further indicator of operating performance and for planning investing activities. Operating free cash flow is considered a non-GAAP financial measure as defined by SEC Regulation G. • Operating free cash flow should be considered in addition to, rather than as a substitute for, net cash provided (used) by operating activities. A limitation of operating free cash flow is that it does not represent the total increase or decrease in the cash balance for the period. This measure also does not exclude mandatory debt service obligations and, therefore, does not represent the residual cash flow available for discretionary expenditures. Management generally compensates for limitations in the use of non-GAAP financial measures by relying on comparable GAAP financial measures and providing investors with a reconciliation of non-GAAP financial measures only in addition to and in conjunction with results presented in accordance with GAAP. We believe that these non-GAAP financial measures reflect an additional way of viewing aspects of our operations that, when viewed with our GAAP results, provide a more complete understanding of factors and trends affecting our business. These non-GAAP measures should be considered as a supplement to, and not as a substitute for, or superior to, loss from operations and net loss per share calculated in accordance with GAAP. We believe that operating free cash flow is useful to investors to provide disclosures of our operating results on the same basis as that used by our management. We also believe that this measure can assist investors in comparing our performance to that of other companies on a consistent basis without regard to certain items, which do not directly affect our ongoing cash flow. |

| 31 Non-GAAP Financial Measures • ACI also includes backlog estimates which are all software license fees, maintenance fees and services specified in executed contracts, as well as revenues from assumed contract renewals to the extent that we believe recognition of the related revenue will occur within the corresponding backlog period. We have historically included assumed renewals in backlog estimates based upon automatic renewal provisions in the executed contract and our historic experience with customer renewal rates. • Backlog is considered a non-GAAP financial measure as defined by SEC Regulation G. Our 60-month backlog estimate represents expected revenues from existing customers using the following key assumptions: • Maintenance fees are assumed to exist for the duration of the license term for those contracts in which the committed maintenance term is less than the committed license term. • License and facilities management arrangements are assumed to renew at the end of their committed term at a rate consistent with our historical experiences. • Non-recurring license arrangements are assumed to renew as recurring revenue streams. • Foreign currency exchange rates are assumed to remain constant over the 60-month backlog period for those contracts stated in currencies other than the U.S. dollar. • Our pricing policies and practices are assumed to remain constant over the 60-month backlog period. • Estimates of future financial results are inherently unreliable. Our backlog estimates require substantial judgment and are based on a number of assumptions as described above. These assumptions may turn out to be inaccurate or wrong, including for reasons outside of management’s control. For example, our customers may attempt to renegotiate or terminate their contracts for a number of reasons, including mergers, changes in their financial condition, or general changes in economic conditions in the customer’s industry or geographic location, or we may experience delays in the development or delivery of products or services specified in customer contracts which may cause the actual renewal rates and amounts to differ from historical experiences. Changes in foreign currency exchange rates may also impact the amount of revenue actually recognized in future periods. Accordingly, there can be no assurance that contracts included in backlog estimates will actually generate the specified revenues or that the actual revenues will be generated within the corresponding 60-month period. • Backlog should be considered in addition to, rather than as a substitute for, reported revenue and deferred revenue. • The presentation of these non-GAAP financial measures should be considered in addition to our GAAP results and is not intended to be considered in isolation or as a substitute for the financial information prepared and presented in accordance with GAAP. |

| 32 Forward Looking Statements This presentation contains forward-looking statements based on current expectations that involve a number of risks and uncertainties. Generally, forward-looking statements do not relate strictly to historical or current facts and may include words or phrases such as “believes,” “ will,” “expects,” “anticipates”, “looks forward to,” and words and phrases of similar impact. The forward-looking statements are made pursuant to safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements in this presentation include, but are not limited to, statements regarding the: The strength of, or improvement in, future sales results including the anticipation of considerably stronger sales for the second quarter of 2008; Expectations relating to our ability to convert current period sales into GAAP revenue at the rates projected throughout 2008; Retention of customers; Sales and financial expectations, including the ability to increase sales and market opportunities for our Wholesale Payment Solutions in all regions and leverage our on demand products; Expected impacts and benefits of the IBM alliance, including our ability to achieve success related to the sales pipeline for IBM Alliance customer prospects and other joint marketing efforts; Expectations relating to the IBM outsourcing relationship, including the ability to achieve the expected operating cost savings and capital expenditure reductions and our ability to leverage the IBM data centers for our on demand products; Ability to successfully enable our products to operate on IBM’s System z series and to successfully market the enabled products to customers; Expectations relating to the impact, if any, of the maturity announcement for our legacy retail payment products and the ability to successfully migrate affected retail payment customers to BASE24-eps; Expectations relating to technical headcount investment, aggression in product life cycle management, wholesale payment hub opportunity, solutions and integration focus, implementation and services margin improvement, and harvesting backlog; Expectations related to the reduced rate of increase in our overall deferred revenue and our belief that this indicates that we are converting a greater amount of deferred revenue into current period GAAP earnings; and Expectations related to the timing of the GAAP expense associated with the IBM outsourcing agreement. Any or all of the forward-looking statements may turn out to be wrong. They can be affected by the judgments and estimates underlying such assumptions or by known or unknown risks and uncertainties. Many of these factors will be important in determining our actual future results. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially from those expressed or implied in any forward-looking statements. In addition, we disclaim any obligation to update any forward-looking statements after the date of this presentation. All of the foregoing forward-looking statements are expressly qualified by the risk factors discussed in our filings with the Securities and Exchange Commission. For a detailed discussion of these risk factors, parties that are relying on the forward-looking statements should review our filings with the Securities and Exchange Commission, including our Form 10-K filed on January 30, 2008 and our Form 10-Q filed on February 19, 2008, both as amended by our Form 10-K/A and Form 10-Q/A, respectively, filed on March 4, 2008, and specifically the sections entitled “Factors That May Affect Our Future Results or the Market Price of Our Common Stock.” |

|

|

| 33 Forward Looking Statements The risks identified in our filings with the Securities and Exchange Commission include: Risks associated with the restatement of our financial statements; Risks associated with our performance which could be materially adversely affected by a general economic downturn or lessening demand in the software sector; Risks associated with our ability to successfully and effectively compete in a highly competitive and rapidly changing industry; Risks inherent in making an estimate of our backlogs which may not be accurate and may not generate the predicted revenue; Risks associated with tax positions taken by us which require substantial judgment and with which taxing authorities may not agree; Risks associated with consolidation in the financial services industry which may adversely impact the number of customers and our revenues in the future; Risks associated with our stock price which may be volatile; Risks associated with conducting international operations; Risks regarding one of our most strategic products, BASE24-eps, which may prove to be unsuccessful in the marketplace; Risks associated with our future profitability which depends on demand for our products; lower demand in the future could adversely affect our business; Risks associated with the complexity of our software products and the risk that our software products may contain undetected errors or other defects which could damage our reputation with customers, decrease profitability, and expose us to liability; Risks associated with the IBM alliance, including our and/or IBM’s ability to perform under the terms of that alliance and customer receptiveness to the alliance Risks associated with future acquisitions and investments which could materially adversely affect us; Risks associated with our ability to protect our intellectual property and technology and that we may be subject to increasing litigation over our intellectual property rights; Risks associated with litigation that could materially adversely affect our business financial condition and/or results of operations; Risks associated with our offshore software development activities which may be unsuccessful and may put our intellectual property at risk; Risks associated with security breaches or computer viruses which could disrupt delivery of services and damage our reputation; Risks associated with our ability to comply with governmental regulations and industry standards to which are customers are subject which may result in a loss of customers or decreased revenue; Risks associated with our ability to comply with privacy regulations imposed on providers of services to financial institutions; Risks associated with system failures which could delay the provision of products and services and damage our reputation with our customers; Risks associated with our restructuring plan which may not achieve expected efficiencies; Risks associated with material weaknesses in our internal control over financial reporting; Risks associated with the impact of economic changes on our customers in the banking and financial services industries including the current mortgage crisis which could reduce the demand for our products and services; and Risks associated with the our recent outsourcing agreement with IBM which may not achieve the level of savings that we anticipate and involves many changes in systems and personnel which increases operational and control risk during transition, including, without limitation, the risks described in our Current report on Form 8-K filed March 19, 2008. Risks associated with our announcement of the maturity of certain legacy retail payment products may result in decreased customer investment in our products and our strategy to migrate customers to our next generation products may be unsuccessful which may adversely impact our business and financial condition. |

| [LOGO] |